Abstract

We consider a general class of dynamic resource allocation problems within a stochastic optimal control framework. This class of problems arises in a wide variety of applications, each of which intrinsically involves resources of different types and demand with uncertainty and/or variability. The goal involves dynamically allocating capacity for every resource type in order to serve the uncertain/variable demand, modeled as Brownian motion, and maximize the discounted expected net-benefit over an infinite time horizon based on the rewards and costs associated with the different resource types, subject to flexibility constraints on the rate of change of each type of resource capacity. We derive the optimal control policy within a bounded-velocity stochastic control setting, which includes efficient and easily implementable algorithms for governing the dynamic adjustments to resource allocation capacities over time. Computational experiments investigate various issues of both theoretical and practical interest, quantifying the benefits of our approach over recent alternative optimization approaches.

Bounded-Velocity Stochastic Control for Dynamic Resource Allocation***An abbreviated preliminary form of this paper has appeared in a conference proceedings (without copyright transfer) [17].

Xuefeng Gao †††Department of Systems Engineering and Engineering Management, The Chinese University of Hong Kong, Shatin, Hong Kong; (xfgao@se.cuhk.edu.hk).,Yingdong Lu ‡‡‡Mathematical Sciences Department, IBM Research AI -– Science, Yorktown Heights, NY 10598, USA; (yingdong@us.ibm.com)., Mayank Sharma §§§AI and Blockchain Solutions Department, IBM Research, Yorktown Heights, NY 10598, USA; (mxsharma@us.ibm.com)., Mark S. Squillante ¶¶¶Mathematical Sciences Department, IBM Research AI -– Science, Yorktown Heights, NY 10598, USA; (mss@us.ibm.com)., Joost W. Bosman ∥∥∥Centrum Wiskunde & Informatica, 1098 XG Amsterdam, The Netherlands; (J.W.Bosman@cwi.nl)

1 Introduction

A general class of canonical forms of dynamic resource allocation problems arises naturally across a broad spectrum of computer systems, communication networks and business applications. As their complexities continue to grow, together with ubiquitous advances in technology, new approaches and methods are required to effectively and efficiently solve canonical forms of general dynamic resource allocation problems in such complex system, network and application environments. These environments often consist of different types of resources that are allocated in combination to serve demand whose behavior over time includes diverse types of uncertainty and variability. Each type of resource has a different reward and cost structure that ranges from the best of a set of primary resource allocation options – having the highest reward, highest cost and highest net-benefit – to the next best primary resource allocation option – having the next highest reward, next highest cost and next highest net-benefit – and so on down to a secondary resource allocation option – having the lowest reward, lowest cost and lowest net-benefit. Each type of resource also has different degrees of flexibility and different cost structures with respect to making changes to the allocation capacity. The resource allocation optimization problem we consider consists of adaptively determining the vector of primary resource capacities and the secondary resource capacity that serve the uncertain/variable demand and that maximize the expected net-benefit over a time horizon of interest based on the foregoing structural properties of the different types of resources.

Motivated by this general class of dynamic resource allocation problems, we take a stochastic control approach that manages future risks associated with resource allocation decisions and uncertain demand, including the reward, cost and flexibility structures of the primary and secondary resource allocation options. Specifically, we consider the underlying fundamental stochastic optimal control problem where the dynamic control policy that allocates the set of primary resource capacities to serve uncertain/variable demand, modeled as Brownian motion, is a vector of absolutely continuous stochastic processes with constraints on its element-wise rates of change with respect to time (“bounded-velocity”), which in turn determines the secondary resource allocation capacity. The ultimate objective is to maximize the expected discounted net-benefit over an infinite horizon based on the structural properties of the different resources types, with the desired outcome rendering an explicit characterization of the optimal dynamic control policy that includes efficient and easily implementable algorithms for governing the dynamic adjustments to resource allocation capacities over time.

1.1 Motivating applications

The wide variety of system, network and application domains in which arise the general class of canonical forms of dynamic resource allocation problems of interest in this study include cloud computing and data center environments, computer and communication networks, energy-aware computing and smart power grid environments, and business analytics and optimization, among many others. For example, large-scale cloud computing and data center environments often involve resource allocation over different server options (ranging from the fastest performance and most expensive to the slowest performance and least expensive) and different network bandwidth options (ranging from the highest guaranteed performance at the highest cost to opportunistic options at no cost, such as the Internet); e.g., refer to [2, 9, 13, 22, 32].

In related energy-aware computing environments, the dynamic resource allocation problem concerns the effective and efficient management of the consumption of energy by resources in the face of time-varying uncertain system demand and (especially in large-scale environments) energy prices; e.g., see [19, 27]. In particular, the system control policy dynamically adjusts the allocation of very high-performance, very high-power servers (best primary resource option), the next highest performance, next highest power servers (next primary resource option), and so on to satisfy the uncertain/variable system demand where any remaining demand is satisfied by low-performance, low-power servers (secondary resource), with the objective of maximizing expected (discounted) net-benefit over time. Here, the rewards (costs) are based on the performance (energy) properties of the type of servers allocated to satisfy demand over time, together with the additional per-unit costs incurred for respectively increasing or decreasing the allocation of the primary resource capacities over time. The resulting optimal dynamic control policy determines the adaptive control of the primary resource capacities at every time, subject to certain constraints and to the demand process.

Another motivating application is based on strategic business provisioning and workforce sourcing in human capital supply chains; refer to, e.g., [8]. The demand for product and services offerings is satisfied through resource allocation from among a diversity of available supply options. These sourcing options include internal resources with the highest reward, highest cost and highest net-benefit, business-partner resources with the next highest reward, next highest cost and next highest net-benefit, and so forth down to contractor or crowdsourcing resources with the lowest reward, lowest cost and lowest net-benefit. For each supply option, examples of the rewards can be revenue and quality of service and examples of the costs can be salary and other compensation. The goal of the strategic human capital sourcing problem is to determine the portfolio of various supply options to meet the time-varying and uncertain demand in the sense of maximizing expected (discounted) net-benefit over time, including the costs incurred in hiring, reskilling, promoting and incentivizing to reduce attrition for the primary human capital resources over time. This also involves constraints on the rates of change in the capacities of primary options to accommodate the non-instantaneous adjustment of human capital resources and the limited availability of such resources in the labor market (see, e.g., [14]).

1.2 Related work

The research literature contains a great diversity of studies of resource allocation problems, with differing objective functions, control policies, and reward, cost and flexibility structures. A wide variety of approaches and methods have been developed and applied to (approximately) solve this diversity of resource allocation problems including, for example, online algorithms and dynamic programming. It is therefore important to compare and contrast our problem formulation and solution approach with some prominent and closely related alternatives. One classical instance of a dynamic resource allocation problem is the multi-armed bandit problem [28] where the rewards are associated with tasks and the goal is to determine under uncertainty which tasks the resource should work on, rather than the other way around. Another widely studied problem is the ski-rental or lease-or-buy problem [39] where there is demand for a resource, but it is initially not known as to how long the resource would be required. In each decision epoch, the choice is between two options: either lease the resource for a fee, or purchase the resource for a price much higher than the leasing fee. Our resource allocation problem differs from this situation in that there are multiple types of resources each with an associated reward and cost per unit time of allocation, since the resources cannot be purchased outright.

From a methodological perspective, the general resource allocation problem we consider in this paper is closely related to the vast literature on stochastic control; refer to, e.g., [33, 40]. Of particular relevance is the so-called bounded velocity follower problem [4, 23] where the control is an absolutely continuous process with bounded derivative. For example, Beneš et al. [4] consider this bounded velocity follower problem with a quadratic running cost objective function, where the authors propose a smooth-fit principle to characterize the optimal policy. In comparison with our study, the paper only considers a single resource, does not consider any costs associated with the actions taken by the control policy, and deals with a smoother objective function. Karatzas and Ocone [23] study an alternative bounded velocity follower problem where discretionary stopping is allowed and the objective is to choose a control law and a stopping time that minimizes the expected sum of a running cost and a termination cost. Davis et al. [14] consider a control problem where a decision maker determines the rate of investment in capacity expansion to satisfy a Poisson demand process, showing that the optimal control is “bang-bang” type (either carry out construction at the maximal speed or take no action) and using computational methods to compute the value function. In contrast, we derive the optimal solution to a stochastic optimal control problem that does not allow discretionary stopping and that seeks to maximize the expected discounted net-benefit over an infinite horizon under a Brownian motion demand process, where we analytically characterize the corresponding value function and explicitly characterize the optimal dynamic control policy. Our work is also related to, but different from, the problem of drift control for Brownian motion (see, e.g., [3, 29, 30]) where the controller can, at some cost, shift the drift among a finite set of alternatives, and the problem of bounded variation control for diffusion processes (see, e.g., [38]) where the available control is an added bounded variation process (but without bounded velocity constraints). Additional related studies include reversible/irreversible investment and capacity planning using a stochastic control approach, for which we refer the interested reader to [1, 5, 16, 20, 21, 31, 34] as well as [36] for a survey and a list of references.

From an applications perspective, there is a growing interest and vast literature in the computer system, communication network and operations research communities to address allocation problems involving various types of resources associated with computation, memory, bandwidth and/or energy; refer to, e.g., [12, 15, 22, 25, 27, 35] and the references therein. We limit our discussions here to the works of Lin et al. [27] and Ciocan and Farias [12] since we will compare our dynamic control policy through computational experiments with the optimization algorithms from both of these studies that are cast within discrete time-interval models. Lin et al. [27] study the problem of dynamically adjusting the number of active servers in a data center as a function of demand to minimize operating costs. They consider average demand over small intervals of time, subject to system constraints, and propose an optimal offline algorithm together with an online algorithm that is shown to be within a constant factor worse than the proposed optimal offline policy. Ciocan and Farias [12] study model predictive control for a large class of dynamic resource allocation problems with stochastic demand rate processes. They develop an online algorithm for demand allocation within appropriately selected time intervals that relies on frequent reoptimization using suitably updated demand forecasts. Our work differs from these two and the aforementioned studies in that we take a stochastic control approach for the dynamic resource allocation optimization problem where the control has bounded velocity constraints and associated costs.

1.3 Our contributions

The goal of our study is to determine the optimal dynamic risk hedging strategy for managing the portfolio of primary resource allocation options and secondary resource allocation option in order to maximize the expected discounted net-benefit over an infinite time horizon based on the structural properties of the different primary and secondary resources, which we show to be equivalent to a minimization problem involving a piecewise-linear running cost and a proportional cost for making adjustments to the control policy process. Our solution approach is based on explicitly constructing a twice continuously differentiable (with the exception of at most three points) solution to the corresponding Hamilton-Jacobi-Bellman equation. Our theoretical results also include an explicit characterization of the dynamic control policy, which is of threshold type, and then we verify that this control policy is optimal through a martingale argument. In contrast to an optimal static allocation strategy, in which a single primary allocation vector capacity is determined to maximize expected net-benefit over the entire time horizon, our theoretical results establish that the optimal dynamic control policy adjusts its allocation decisions in primary and secondary resources to hedge against the risks of under-allocating primary resource capacities (resulting in lost reward opportunities) and over-allocating primary resource capacities (resulting in incurred cost penalties).

Our study provides important methodological contributions and new theoretical results by deriving the solution of a fundamental stochastic optimal control problem. This stochastic optimal control solution approach highlights the importance of timely and adaptive decision making in the allocation of a mixture of different resource options with distinct features in optimal proportions to satisfy time-varying and uncertain demand. Our study also provides important algorithmic contributions through a new class of online policies for dynamic resource allocation problems arising across a wide variety of application domains. Computational experiments quantify the effectiveness of our optimal online dynamic control algorithm over recent work in the area, including comparisons demonstrating how our optimal online algorithm significantly outperforms the type of optimal offline algorithm within a discrete-time framework recently proposed in [27], which appears to be related to the optimal online model predictive control algorithm proposed in [12] within a different discrete-time stochastic optimization framework. This includes relative improvements up to and in comparison with the optimal offline algorithm considered in [27], and even larger relative improvements of more than and in comparison with the optimal online algorithm in [12].

An abbreviated preliminary form of this paper has appeared in a conference proceedings (without copyright transfer) [17] in which we presented a subset of our results on the optimal control policy for resource allocation problems with only a single primary resource option and a secondary resource option, together with limited computational experiments demonstrating some of the benefits of our optimal dynamic control policy over the optimal offline algorithm proposed in [27]. The current paper significantly extends the preliminary conference paper in four important aspects: First, we present herein our complete derivation of the optimal control policy for resource allocation problems with single primary and secondary resource options; Second, we present herein a more thorough set of computational experiments that demonstrate the significant benefits of our optimal dynamic control policy over both the optimal offline algorithm in [27] and the optimal online algorithm proposed in [12]; Third, we extend herein our theoretical results beyond the case of a single primary resource allocation option to a general case with multiple primary resource allocation options and provide computational experiments that compare the single and multiple primary resource allocation models; Finally, we provide herein rigorous proofs of all our main results for both resource allocation models under all possible conditions on the model parameters.

The remainder of this paper is organized as follows. Section 2 defines our mathematical models of the stochastic resource allocation optimization problem, first for the case of a single primary resource and then for a version of the multiple primary resources case. Our mathematical formulations and main results for the corresponding stochastic control problems are presented in Sections 3 and 4, respectively. A representative sample of numerous computational experiments are discussed in Section 5. Concluding remarks are provided in Section 6, including a discussion of the use of model predictive control and learning to determine the parameters of our optimal dynamic control policy over time. All of our technical proofs are provided in the appendices.

2 Mathematical Models

We investigate a general class of fundamental resource allocation problems in which a set of primary resource allocation options and a secondary resource allocation option are available to satisfy demand whose behavior over time includes uncertainty and/or variability. There is an important reward and cost ordering among these resource options where the first primary resource allocation option has the highest net-benefit, followed by the second primary resource allocation option having the next highest net-benefit, and so on, with the (single) secondary resource allocation option having the lowest net-benefit. In addition, the set of primary resource capacities are somewhat less flexible in the sense that their rates of change at any instant of time are bounded, whereas the secondary resource capacity is more flexible in this regard (as made more precise below). Beyond these differences, the set of primary resources and the secondary resource are capable of serving the demand and all of this demand needs to be served, i.e., there is no loss of demand.

To elucidate the exposition of our analysis, we first consider the single primary and secondary instance of our general resource allocation model. This instance captures the key aspects of the fundamental trade-offs among the net-benefits of the various resource allocation options together with their associated risks. We then consider our general resource allocation model comprising multiple primary resources and a secondary resource together with an important relationship maintained among the primary resources.

2.1 System model: Single primary resource

We consider the stochastic optimal control problems underlying our resource allocation model in which uncertain and/or variable demand needs to be served by the primary resource allocation capacity and the secondary resource allocation capacity. A control policy defines at every time the level of capacity allocation for the primary resource, denoted by , and the level of secondary resource capacity allocation, denoted by , that are used in combination to satisfy the uncertain/variable demand, denoted by .

The demand process is modeled by

| (2.1) |

where is the demand growth/decline rate (which can be extended to a deterministic function of time), is the demand volatility, and is a one-dimensional standard Brownian motion, whose sample paths are continuous but nondifferentiable almost everywhere [24]. This model is natural when the demand forecast involves Gaussian noises; see, e.g., [11, 10] for similar Brownian demand models. The demand process is served by the combination of primary and secondary resource allocation capacities . Given the higher net-benefit structure of the primary resource option, the optimal dynamic control policy seeks to determine an absolutely continuous stochastic process describing the primary resource allocation capacity to serve the demand such that any remaining demand is served by the secondary resource allocation capacity .

Let and respectively denote the reward and cost associated with the primary resource allocation capacity at time . The rewards are linear functions of the primary resource capacity and the demand, whereas the costs are linear functions of the primary resource capacity. We therefore have

| (2.2) |

where , captures all per-unit rewards for serving demand with the primary resource capacity, captures all per-unit costs for the primary resource capacity, and . Observe that the rewards for the primary resource are linear in as long as , otherwise any primary resource capacity exceeding the demand will solely incur costs without rendering rewards. Hence, from a risk hedging perspective, the risks associated with the primary resource allocation position at time , , concern lost reward opportunities whenever on the one hand and concern incurred cost penalties whenever on the other hand.

In addition, any adjustments to the primary resource allocation capacities have associated costs, where we write and to denote the per-unit costs of increasing and decreasing the decision process , respectively. Namely, represents the per-unit cost whenever the allocation of the primary resource capacity is being increased while represents the per-unit cost whenever the allocation of the primary resource capacity is being decreased.

Since all the remaining demand is served by the secondary resource allocation capacity, we therefore have

| (2.3) |

The corresponding reward function and cost function are then given by

| (2.4) |

where , captures all per-unit rewards for serving demand with the secondary resource capacity, captures all per-unit costs for the secondary resource capacity, and . Hence, from a risk hedging perspective, the secondary resource allocation position at time , , is riskless in the sense that rewards and costs are both linear in the resource capacity actually used.

2.2 System model: Multiple primary resources

We next consider the stochastic optimal control problems underlying our resource allocation models in which uncertain and/or variable demand needs to be served by the set of primary resource allocation capacities and the secondary resource allocation capacity. Let denote the number of primary resource options. A control policy then defines at every time the level of capacity allocation for all primary resources, respectively denoted by , and the level of secondary resource capacity allocation, denoted by , that are used in combination to satisfy the uncertain/variable demand, denoted by .

The demand process continues to be modeled as in (2.1). This demand process is served by the combination of primary and secondary resource allocation capacities , where has absolutely continuous paths for each . Given the higher net-benefit structures of the primary resource options, the optimal dynamic control policy seeks to determine at every time the primary resource allocation capacity vector to serve the demand such that any remaining demand is served by the secondary resource allocation capacity .

The corresponding stochastic control problem becomes high-dimensional in the presence of multiple primary resources, and thus it is inherently prohibitive to solve analytically or computationally in general. We therefore introduce in our system model definition the notion of coordination through a contractual agreement among the multiple primary resources, namely the model definition includes a contract that fixes the ratio of capacities among the primary resources. From a mathematical perspective, this contract-based system model definition makes it possible to derive explicit solutions for the corresponding stochastic control problem. In particular, by introducing such a contractual agreement among the multiple primary resource options, the dimensionality of the stochastic control problem is relaxed and our mathematical derivations exploit and build on the results we obtain for the single primary resource model. From an applications perspective, our contract-based model definition is consistent with coordinated contractual agreements that have been adopted in various resource allocation problems in practice, such as strategic sourcing in human capital supply chains (see, e.g., [7] and the strategic sourcing example in the introduction) because they capture important business relationships and are easy to implement.

More formally, we introduce a nonnegative vector , with , to represent the contract-based fixed distribution of capacities among the multiple primary resources. Then, for each , we set

| (2.5) |

where (with a slight abuse of notation) represents the aggregate capacity of primary resources and is set to maintain the initial (agreed upon) percentage . In other words, for a given contract vector , all primary resource allocations must maintain the relationship (2.5) at all time .

For each primary resource type , let and respectively denote the reward and cost associated with the th primary resource allocation capacity at time . When the collection of primary resource allocations exceeds the demand, the rewards are linear functions of the fraction of the demand served by the th primary resource allocation capacity, namely , from (2.5). However, when the demand exceeds the collection of primary resource allocations, then the rewards are linear functions of the th primary resource allocation capacity, which is less than due to (2.5). The costs are linear functions of the th primary resource allocation capacity. We therefore have

| and | (2.6) |

where , captures all per-unit rewards for serving demand with the th primary resource capacity, captures all per-unit costs for the th primary resource capacity, and . The per-unit reward and the per-unit cost for the aggregate primary resource capacity , under a given contract vector , are then respectively given by

| (2.7) |

Observe that the rewards for the th primary resource allocation are linear in as long as , or equivalently ; otherwise the fraction of the th primary resource capacity exceeding will solely incur costs without rendering rewards. Hence, from a risk hedging perspective, the risks associated with the collection of primary resource allocations at time concern lost reward opportunities whenever on the one hand and concern incurred cost penalties whenever on the other hand.

Similarly to (2.7), as any adjustments to the primary resource allocation capacities have associated costs, let and respectively denote the per-unit cost associated with increasing and decreasing the allocation of the th primary resource capacity. The per-unit costs of increasing and decreasing the allocation of the aggregate primary resource capacity are then respectively given by

| (2.8) |

Since the optimal dynamic control policy serves all remaining demand with secondary resource allocation capacity, we therefore have

| (2.9) |

The corresponding reward function and cost function are then given by

| and | (2.10) |

where , captures all per-unit rewards for serving demand with secondary resource capacity, captures all per-unit costs for secondary resource capacity, and . Hence, from a risk hedging perspective, the secondary resource allocation position at time , , is riskless in the sense that rewards and costs are both linear in the resource capacity actually used.

3 Main Results: Single Primary Resource

In this section we consider our main results on the optimal dynamic control policy for the stochastic optimal control problem when there is a single primary resource. After providing a formulation of the stochastic control problem and some technical preliminaries, we present our main results under different conditions for the values of and , including the special case in which both are zero.

3.1 Problem formulation

The stochastic optimal control problem associated with the system model of Section 2.1 allows the dynamic control policy to adjust its allocation positions in primary and secondary resource capacities based on the demand realization observed up to the current time, which we call the risk-hedging position of the dynamic control policy. More formally, in the single primary resource case, the decision process , is adapted to the filtration generated by . Then the objective of the optimal dynamic control policy is to maximize the expected discounted net-benefit over an infinite horizon, where net-benefit at time consists of the difference between the rewards and costs from the primary resource allocation capacity and the secondary resource allocation capacity minus the additional costs for adjustments to .

In formulating the corresponding stochastic optimization problem, we impose a pair of additional conditions on the decision process based on practical aspects of the diverse application domains motivating our study. The control policy cannot make unbounded adjustments in the primary resource allocation capacity at any instant in time; i.e., the amount of change in at time is restricted (even if only to a very small extent) by various factors. We therefore assume that the rate of change in the primary resource allocation capacity by the control policy is bounded. More precisely, for an absolutely continuous process , there is a pair of finite constants and such that for each

| (3.1) |

where denotes the derivative of the decision variable (absolutely continuous process) with respect to time. On the other hand, the ability of the control policy to make adjustments to the secondary resource capacity in response to changes in the primary resource capacity tends to be more flexible such that (2.3) holds at all time .

Now we can present the mathematical formulation of our stochastic optimization problem for the case of a single primary resource. Defining

| and |

we seek to determine the optimal dynamic control policy that solves the problem (SC-OPT:S)

| (3.2) | |||||

| s.t. | (3.4) | ||||

where is the discount factor and denotes the indicator function returning if is true and otherwise. The control variable is the rate of change in the primary resource capacity by the control policy at every time subject to the lower and upper bound constraints on in (3.4). Note that the second (third) expectation in (3.2) causes a decrease with rate () in the value of the objective function whenever the control policy increases (decreases) .

3.2 Preliminaries

For notational convenience, we define the constants

| (3.5) | |||||

| (3.6) | |||||

| (3.7) |

These quantities are the roots of the quadratic equation

when takes on the values of , or .

Next, we turn to consider the first expectation in the objective function (3.2) of the stochastic optimization problem (SC-OPT:S), which can be simplified as follows. Define

and . Upon substituting (2.2) and (2.4) into the first expectation in (3.2), and making use of the fact that

we obtain

| (3.8) |

Note that the second expectation in (3.8) represents the expected discounted cumulative demand over the infinite horizon. Since this second summand in (3.8) does not depend on the control variable , this term plays no role in determining the optimal dynamic control policy. Together with the above results, we derive the following stochastic optimization problem which is equivalent to the original problem formulation (SC-OPT:S):

| (3.9) | |||||

| s.t. | (3.12) | ||||

where denotes expectation with respect to the initial state distribution (i.e., state at time ) being with probability one.

We use to represent the optimal value of the objective function (3.9); namely, is the value function of the corresponding stochastic dynamic program. Given its equivalence with the original optimization problem (SC-OPT:S), the remainder of this section will focus on the stochastic dynamic program formulation in (3.9) – (3.12).

3.3 Case 1: and

Let us first briefly explain the conditions of this subsection, which are likely to be the most relevant case in practice. Observe from the objective function (3.9) that reflects the discounted overage cost associated with the primary resource capacity and reflects the corresponding discounted shortage cost, recalling that is the discount rate. In comparison, represents the cost incurred for decreasing when in an overage position while represents the cost incurred for increasing when in a shortage position.

To elucidate the exposition, we denote

Condition (1a): , .

Condition (1b): , and .

Condition (1c): , and .

Condition (2a): , .

Condition (2b): , and .

We are now ready to state our main result for Case 1.

Theorem 1

Suppose the adjustment costs satisfy and . Then there are two threshold values and with such that the optimal dynamic control policy is given by: For each ,

Moreover, the values of and can be characterized by the following three cases.

-

I.

If either Condition (1a), (1b) or (1c) hold, we have where and are uniquely determined by

(3.13) (3.14) -

II.

If either Condition (2a) or (2b) hold, we have where and are uniquely determined by

(3.15) (3.16) -

III.

If none of the above conditions hold, we then have where and are uniquely determined by

(3.17) (3.18)

Theorem 1 can be interpreted as follows. The optimal dynamic control policy seeks to maintain within the risk-hedging interval at all time , taking no action (i.e., making no change to ) as long as . Whenever falls below , the optimal dynamic control policy pushes toward the risk-hedging interval as fast as possible, namely at rate , thus increasing the primary resource capacity allocation. Similarly, whenever exceeds , the optimal dynamic control policy pushes toward the risk-hedging interval as fast as possible, namely at rate , thus decreasing the primary resource capacity allocation. In each of the cases I, II and III, the optimal threshold values and are uniquely determined by two nonlinear equations.

3.3.1 Special Case

In the special case where the dynamic control policy incurs no costs for making adjustments, which may be of particular interest in some application domains, Theorem 1 has the following reduced form.

Corollary 2

Suppose there are no adjustment costs, namely . Then there exists a constant such that the optimal dynamic control policy is given by

Moreover, can be given explicitly by

| (3.19) |

The interpretation of this corollary is the same as that for Theorem 1 where the risk-hedging interval collapses to a single point . Hence, the optimal dynamic control policy seeks to maintain at the position at all time , pushing toward this point as fast as possible with rate when below and with rate when above.

3.4 Case 2: and

We next consider the case in which the per-unit cost for decreasing the decision variable is at least as large as the discounted overage cost associated with this decision variable. Our main result for this case can be expressed as follows.

Theorem 3

Suppose the adjustment costs satisfy and . Then there exists a threshold such that the optimal policy is given by

Moreover, the value of can be characterized by

| (3.22) |

This result is closely related with Theorem 1. One readily checks that in Theorem 3 when , satisfies

which has a similar structure as (3.14). When , solves

which is the same as Equation (3.17) if we regard . Therefore, given the relatively larger cost for decreasing , this theorem essentially provides a one-sided version of Theorem 1 in which the optimal dynamic control policy seeks to maintain at or above the threshold at all time . Whenever falls below , the optimal dynamic control policy pushes toward the risk-hedging threshold as fast as possible, namely at rate . Otherwise, the optimal dynamic control policy takes no action, because taking action to decrease an overage position costs more than the benefits from such an action.

3.5 Case 3: and

We now consider the case in which the per-unit cost for increasing the decision variable is at least as large as the discounted shortage cost associated with this decision variable. Our main result for this case can be expressed as follows.

Theorem 4

Suppose the adjustment costs satisfy and . Then there exists a threshold such that the optimal policy is given by

Moreover, the value of can be characterized by

| (3.25) |

We also observe the connection of this result with Theorem 1. It can be readily verified from Theorem 4 that when , satisfies

and thus is equivalent to (3.18) if we regard . When , we have solving

which is closely related to (3.15) and (3.16). Hence, given the relatively larger cost for increasing , this theorem essentially provides a one-sided version of Theorem 1 in which the optimal dynamic control policy seeks to maintain at or below the threshold at all time . Whenever exceeds , the optimal dynamic control policy pushes toward the risk-hedging threshold as fast as possible, namely at rate . Otherwise, the optimal dynamic control policy takes no action, because taking action to increase a shortage position costs more than the benefits from such an action.

3.6 Case 4: and

Lastly, we consider the case in which the per-unit costs for adjusting the decision variable are at least as large as the corresponding discounted overage and shortage costs associated with this decision variable. We now state our main result for this case.

Theorem 5

Suppose the adjustment costs satisfy and . Then the optimal policy consists of taking no action. Specifically,

Given the relatively larger costs for adjusting , this theorem essentially consists of the inaction sides of both Theorems 3 and 4. Intuitively, the theorem characterizes the conditions under which the costs of any control policy action exceeds the resulting benefit, namely taking an action to decrease an overage position or increase a shortage position costs more than the benefits from such an action.

4 Main Results: Multiple Primary Resources with Contract

In this section we consider our main results on the optimal dynamic control policy for the stochastic optimal control problem when there are multiple primary resources under a contract-based relationship. After providing a formulation of the stochastic optimal control problem and some technical preliminaries, we present our main results analogous to those in Section 3.

4.1 Problem formulation

The stochastic optimal control problem associated with the system model of Section 2.2 allows the dynamic control policy to adjust its allocation positions in primary and secondary resource capacities, while maintaining the contract-based relationship , based on the demand realization observed up to the current time. More formally, the decision processes , are adapted to the filtration generated by . Then the objective of the optimal dynamic control policy is to maximize the expected discounted net-benefit over an infinite horizon, subject to the contract-based constraints (2.5), where net-benefit at time consists of the difference between rewards and costs from both the set of primary resource allocation capacities and the secondary resource allocation capacity and the additional costs for adjustments to .

Similar to the single primary resource formulation, the control policy cannot make unbounded adjustments in the th primary resource allocation capacity at any instant in time; i.e., the amount of change in at time is restricted (even if only to a very small extent) by various factors. We therefore assume that the rate of change in the th primary resource allocation capacity by the control policy is bounded. More precisely, there are pairs of finite constants and such that for each

| (4.1) |

where denotes the derivative of the decision variable with respect to time, for all . On the other hand, the ability of the control policy to make adjustments to the secondary resource capacity, in response to changes in the primary resource capacities, tends to be more flexible such that (2.9) holds at all time .

Now we can present the mathematical formulation of our stochastic optimization problem for the case of multiple primary resources with a contract-based relationship among these resources. Let us fix a given contract vector . Defining

| and |

we seek to determine the optimal dynamic control policy for the contract vector that solves the problem (SC-OPT:M)

| (4.2) | |||||

| s.t. | (4.6) | ||||

where is the discount factor and again denotes the indicator function associated with event . The control variables are the rates of change in the primary resource capacities by the control policy at every time subject to the lower and upper bounds on each in (4.6) and the contract-based relationship among the primary resources in (4.6) and (4.6). Note that the second (third) expectation in (4.2) causes a decrease with rate () in the value of the objective function whenever the control policy increases (decreases) .

4.2 Preliminaries

Consider the first expectation in the objective function (4.2) of the stochastic optimization problem (SC-OPT:P). From (2.5), (2.7) and (2.6), we can rewrite this expectation in terms of the aggregate primary resource capacity for a given contract vector . Upon analogously applying the derivations of Section 3.2, we then can simplify and reduce this expectation to the single primary resource setting as follows:

where , , , , and . Similarly, the second and third expectations in (4.2) can be rewritten with respect to (2.8) in terms of the aggregate primary resource capacity for the given contract vector . Define , for .

Next, we deduce from (2.5), (4.1) and the system model definition of Section 2.2 that the aggregate control process satisfies the constraint

| (4.7) |

where

| (4.8) |

Then, for a given contract vector , we have the following stochastic optimization problem in terms of the aggregate control process that is equivalent to the original problem formulation (SC-OPT:M):

| (4.9) | ||||

| s.t. | ||||

where again denotes expectation with respect to the initial state distribution (i.e., state at time ) being with probability one.

Once again, we use to represent the optimal value of the objective function in (4.9) for a given contract vector ; namely, is the value function of the corresponding stochastic dynamic program. Given its equivalence with the original optimization problem (SC-OPT:M), the remainder of this section will focus on the stochastic dynamic program formulation in (4.9).

For notational convenience, we define the following constants which represent modifications of some of the constants in Section 3.2 due to the differences in the parameters and the problem setting:

and

4.3 Case 1: and

Let us first briefly explain the conditions of this subsection, for a given contract vector where

The conditions of this subsection are likely to be the most relevant case in practice. Observe that, if and for each primary resource type , then the conditions and hold for any . Further observe from the objective function in (4.9) that reflects the discounted overage cost associated with the aggregate primary resource capacity and reflects the discounted shortage cost associated with the aggregate primary resource capacity, recalling that is the discount rate. In comparison, represents the cost incurred for decreasing when in an overage position while represents the cost incurred for increasing when in a shortage position.

The conditions of this subsection represent counterparts of the conditions (1a), (1b), (1c), (2a) and (2b) of Section 3.3. To elucidate the exposition, we denote

Condition (1a’): , .

Condition (1b’): , and .

Condition (1c’): , and .

Condition (2a’): , .

Condition (2b’): , and .

We are now ready to state our main result for Case 1 under this setting. Recall that and are defined in (4.8).

Theorem 6

Fix . Suppose the adjustment costs satisfy and . Then there are two threshold values and with such that the optimal dynamic control policy is given by

Moreover, the values of and can be characterized by the following three cases.

-

I.

If either Condition (1a’), (1b’) or (1c’) hold, we have where and are uniquely determined by

(4.10) (4.11) -

II.

If either Condition (2a’) or (2b’) hold, we have where and are uniquely determined by

(4.12) (4.13) -

III.

If none of the above conditions hold, we then have where and are uniquely determined by

(4.14) (4.15)

Theorem 6 can be interpreted similar to Theorem 1. Given a fixed contract among primary resource options, the optimal dynamic control policy seeks to maintain within the risk-hedging interval at all time . When outside this risk-hedging interval , the optimal dynamic control policy pushes toward this interval as fast as possible in a synchronized way such that the contract condition (2.5) is always maintained among the primary resource allocations ; namely, for each . The optimal threshold values and are uniquely determined by two nonlinear equations for each of the cases , and .

We now explore the dependence of the value function on the contract . For a fixed contract , and , we write for the optimal value of the objective function (4.2), i.e., the maximal expected discounted net-benefit over an infinite time horizon when one optimally adjusts the aggregate primary resource option under the fixed contract among these primary options together with the secondary resource option in order to meet the Brownian demand. Then it is easily seen from Section 3.2 (refer to (3.8)) that

| (4.16) |

where is the value function of the stochastic dynamic program (4.9) with parameters given in (2.5) – (2.10) and in (2.7) are linear in . A closer examination of the expression we obtained for Theorem 1 and its proof imply that the value function continuously depends on . Such continuity is the consequence of the continuity of the solution of the corresponding ordinary differential equation with respect to the initial condition and parameters, as well as the “smooth-fit” principle.

Theorem 7

Given any fixed , the optimal threshold values and in Theorem 6 are continuous functions of . As a consequence, and are continuous with respect to .

This result also suggests a simple possible scheme for our dynamic resource allocation problem in the presence of multiple primary resource options. Given the initial imbalance between the aggregate primary resource capacity and the demand, i.e., , one can first solve offline an optimal contract given the characteristics of the demand, the reward and the cost associated with each sourcing option. Such an optimal contract exists due to the continuity result in Theorem 7. Next, in order to meet the uncertain and volatile demand over time, one fixes this optimal contract among primary resource options throughout the time horizon and then dynamically adjusts the primary sourcing capacities according to the threshold policy given in Theorem 6. Note that the capacity of each individual primary resource is aligned according to the contract vector, i.e., the ratio is fixed for all . Any remaining demand will be served by the secondary resource option.

4.4 Remaining Cases

It is easy to see that similar results can be obtained for all remaining possible conditions on the adjustment costs and . In particular, a corollary to Theorem 6 can be expressed and established analogous to Corollary 2 applied to the aggregate control process . Similarly, the theorems corresponding to Theorems 3 – 5 can be expressed and established analogous to these theorems applied to the aggregate control process .

5 Computational Experiments

The foregoing sections establish the explicit optimal dynamic control policy among all admissible nonanticipatory control processes within a stochastic optimal control setting that maximizes the stochastic dynamic programs (SC-OPT:S) and (SC-OPT:M). These optimal dynamic control policies render a new class of online algorithms for general dynamic resource allocation problems that arise across a wide variety of application domains. The resulting online algorithms are easily implementable in computer systems and communication networks (among others) at runtime and consists of maintaining respectively within the risk-hedging intervals and at all time , where , , and are easily obtained from application parameters. In this section, we present a representative sample of computational experiments conducted across a broad spectrum of application environments to investigate various issues of both theoretical and practical interest by comparing our online optimal dynamic control algorithm against alternative optimization approaches from recent work in the research literature.

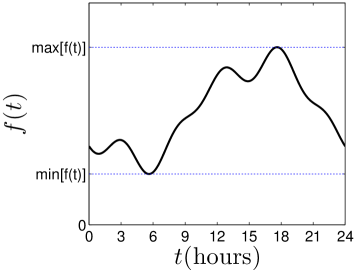

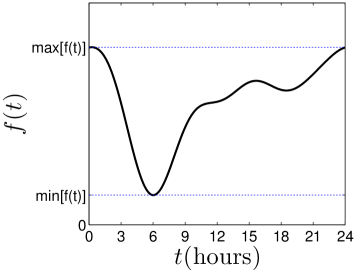

Through a detailed analysis of real-world trace data [17], we fitted average daily demand processes for different environments by smooth functions and , depicted in Figure 1. In addition, our detailed analysis of real-world data revealed a wide range of volatility in the demand process over time, as well as from one environment to another. We therefore focus in the remainder of this section on the average daily demand patterns and for the drift parameter of the demand process while varying its volatility parameter (as made more precise below), thus representing a broad spectrum of application environments.

5.1 Single Primary Resource

For comparison with our optimal online dynamic control algorithm, we consider two alternative optimization approaches that have recently appeared in the research literature. First, Lin et al. [27] propose an optimal offline algorithm that consists of making optimal provisioning decisions in a clairvoyant anticipatory manner based on the known average demand within each slot of a discrete-time model where the slot length is chosen to match the timescale at which a data center can adjust its resource capacity and so that demand activity within a slot is sufficiently nonnegligible in a statistical sense. Applying this particular optimal offline algorithm within our mathematical framework, we partition the daily time horizon into slots of length such that , , , , and we compute the average demand within each slot yielding the average demand vector . Define , where denotes the primary resource allocation capacity for slot . The optimal solution under this offline algorithm is then obtained by solving the following linear program (LP) for each sample path:

| (5.1) | |||||

| s.t. | (5.2) |

where the constraints on the control variables in (5.2) correspond to (3.12). We refer to this solution as the offline LP algorithm.

Second, we consider a related optimal online algorithm proposed by Ciocan and Farias [12]. Although they focus on dynamic resource allocations with stochastic demand rate, their allocation scheme based on re-optimization heuristics (Section 3.1 in [12]) is quite general and can be applied to our setting with stochastic demand process and deterministic demand rate. The main idea of their algorithm is that at each discrete point in time, one uses demand information realized up to that point and assumes the demand rate over the remaining time horizon is unchanged, and then employs the allocation rule that is optimal for such a scenario over the interval of time until the next re-solve. We refer to this as the online CF algorithm.

The sample paths of demand for our computational experiments are generated from a linear diffusion process for the entire time horizon such that the drift of the demand process is obtained as the derivative of (i.e., ) and the corresponding volatility term is set to match . Since the volatility pattern tended to be fairly consistent with respect to time within each daily real-world trace for a specific environment and since the volatility pattern tended to vary considerably from one daily real-world trace to another, our linear diffusion demand process is assumed to be governed by the following model

where we vary the volatility term to investigate different application environments. Each workload then consists of a set of sample paths generated from the Brownian demand process defined in this manner.

Given such a demand process, we calibrate our optimal online dynamic control algorithm by first partitioning the average daily demand function into piecewise linear segments, then correspondingly setting the drift function of the demand process , and finally computing the threshold values and for each per-segment drift and according to Theorem 1. This (fixed) version of our optimal online dynamic control algorithm is applied to every daily sample path of the Brownian demand process and the time-average value of net-benefit is computed over this set of daily sample paths. For comparison under the same set of Brownian demand process sample paths, we compute the average demand vector and the corresponding solution under the offline LP algorithm for each daily sample path by solving the linear program (5.1),(5.2) with respect to , and then we calculate the time-average value of net-benefit over the set of daily sample paths. The corresponding computational experiments for the CF algorithm are performed within this discrete-time framework and the corresponding time-average net-benefit is computed in a similar manner. All of our computational experiments were implemented in Matlab using, among other functionality, the econometrics toolbox.

For our first set of results based on the average daily demand pattern illustrated in the leftmost plot of Figure 1, the base parameter settings are given by , , , , , , , , , , and , where , and . In addition to these base settings, we vary the parameter values one at a time for , , , and , in order to investigate the impact and sensitivity of these parameters on the performance of the various optimization algorithms. For each computational experiment under a given set of parameters, we generate daily sample paths using a timescale of a couple of seconds and a setting of five minutes, noting that a wide variety of experiments with different timescale and settings provided the same performance trends as those presented herein. We then apply our optimal dynamic control policy and the two alternative optimization approaches to this set of daily sample paths as described above.

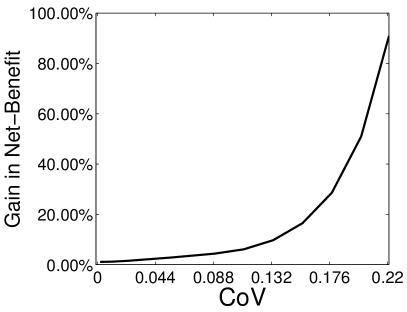

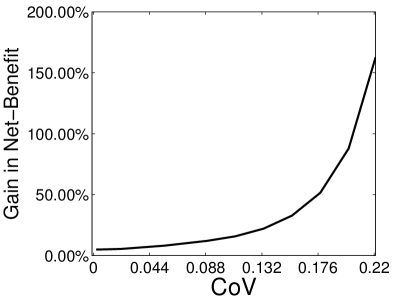

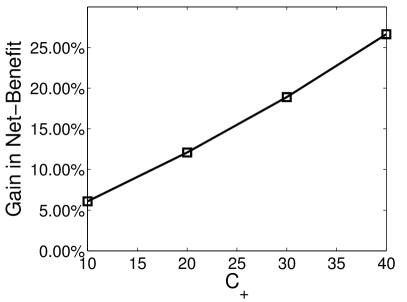

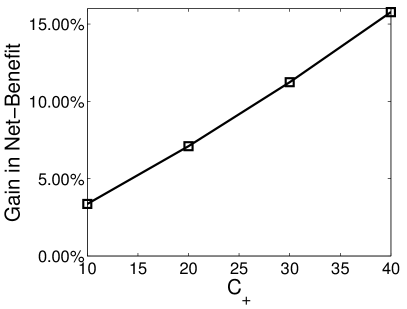

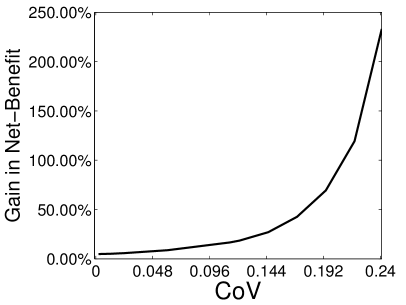

Figure 2 presents a representative sample of our computational results for the first demand process based on . The two leftmost graphs provide performance comparisons of our optimal online dynamic control algorithm against the alternative offline LP and online CF algorithms, respectively, where both comparisons are based on the relative improvements in expected net-benefit under our optimal control policy as a function of ; the relative improvement is defined as the difference in expected net-benefit under our optimal dynamic control policy and under the alternative optimization approach, divided by the expected net-benefit of the alternative approach. For the purpose of comparison across sets of workloads with very different values, we plot both of these graphs as a function of the coefficient of variation . The two rightmost graphs provide similar comparisons of relative improvement in expected net-benefit between our optimal dynamic control policy and the two alternative optimization approaches as a function of , both with fixed to be .

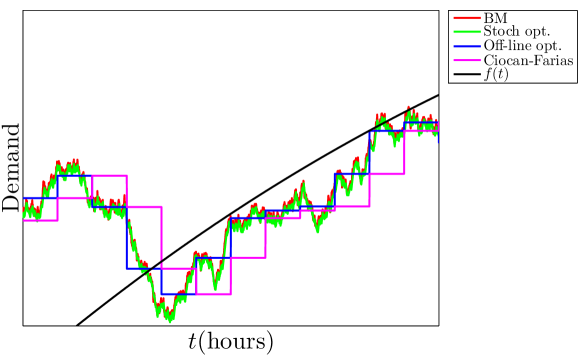

We first observe from the two leftmost graphs in Figure 2 that our optimal online dynamic control algorithm outperforms the two alternative optimization approaches for all . The relative improvements in expected net-benefit grow in an exponential manner with respect to increasing values of over the range of CoV values considered, with relative improvements up to in comparison with the offline LP algorithm and more than in comparison with the CF algorithm. Our results illustrate and quantify the fact that, even in discrete-time models with small time slot lengths , nonnegligible volatility plays a critical role in the expected net-benefit of any given resource allocation policy. The significant relative improvements under the optimal online dynamic control algorithm then follow from our stochastic optimal control approach that directly addresses the volatility of the demand process in all primary and secondary resource allocation decisions. This can be clearly seen in the results of Figure 3 that illustrate the performance of the three algorithms relative to demand over a representative interval of an individual sample path. Figure 3 represents a zoomed-in view of the results over a small segment of the time horizon (60 minutes of the 24 hour time horizon). Although the offline LP algorithm based on (5.1),(5.2) would eventually outperform our optimal online dynamic control algorithm as the time slot length decreases toward , we note that the choice for in our computational experiments is considerably smaller than the -minute intervals suggested in [27]. Moreover, as discussed in [12], the optimal choice of is a complex issue in and of itself and it may need to vary over time depending upon the statistical properties of the demand process . A key advantage of our optimal online dynamic control algorithm is that such parameters are not needed.

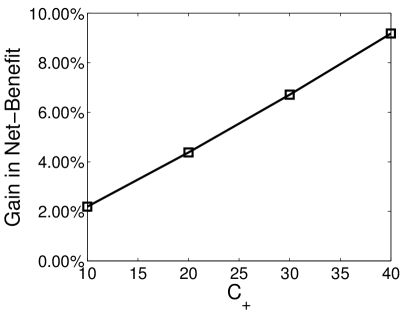

We next observe from the two rightmost graphs in Figure 2 that the relative improvements in expected net-benefit under our optimal online dynamic control algorithm similarly increases with respect to increasing values of , though in a more linear fashion. We also note that very similar trends were observed with respect to varying the value of , though the magnitude of the relative improvement in expected net-benefit is smaller. Within the limited range of parameter values considered, our computational experiments suggest that the relative improvements in net-benefit under our optimal dynamic control policy can be more sensitive to than to . Recall that is the cost for the primary resource allocation capacity, whereas is the difference in net-benefit between the primary and secondary resource allocation capacities. We also note that similar trends were observed for changes in the values of and when the relative improvement results are considered as a function of CoV.

Now let us turn to our second set of results based on the average daily demand pattern illustrated in the rightmost plot of Figure 1, where the base parameter settings are given by , , , , , , , , , , , . In addition to these base settings, we vary the parameter values one at a time for , , , and . Once again, for each experiment comprising a specific workload, we generate sample paths using a timescale of a couple of seconds and a setting of five minutes, noting that a wide variety of experiments with different timescale and settings provided performance trends that are identical to those presented herein. We then apply our optimal dynamic control policy and the two alternative optimization approaches to this set of sample paths as described above. Our performance evaluation comparisons are based on the expectation of net-benefit realized under each of the three algorithms, also as described above.

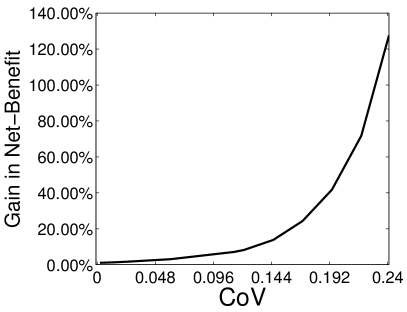

Figure 4 presents a representative sample of our computational results for the demand process based on , providing the analogous results that correspond to those in Figure 2. We note that the larger range exhibited in the second average daily demand pattern as well as a higher value of lead to both a higher relative net-benefit for fixed and a higher sensitivity to changes in , thus improving the gains of our optimal online dynamic control algorithm over the alternative offline LP and online CF algorithms. This relative improvement in expected net-benefit as compared to the set of experiments for the average daily demand pattern can be understood to be caused in part by the sharp drop in average demand from the maximum value of to a minimum of within a fairly short time span, thus contributing to an increased effective volatility over and above that represented by . Hence, the fact that the relative improvement exhibited by our optimal online dynamic control algorithm is larger under the average daily demand pattern , up to in comparison with the offline LP algorithm and over in comparison with the CF algorithm, can be viewed in a sense to be very much an extension of the finding that the relative improvement provided by our optimal online algorithm increases with an increase in CoV. A similar gain in performance improvement can be seen in the rightmost two plots when we vary with a fixed value of .

5.2 Multiple Primary Resources

We now turn to investigate the relationship between the single primary resource formulation (SC-OPT:S) and the multiple primary resource formulation (SC-OPT:M). One can envision, under appropriate circumstances and contractual agreements among the multiple primary resource options, that the multiple primary resource allocation model can potentially render greater performance benefits to an organization than the corresponding performance benefits from the single primary resource allocation model. In this section we consider the performance trade-offs between both primary resource allocation models.

To this end, we present a comparison between the single primary resource formulation (SC-OPT:S) and the multiple primary resource formulation (SC-OPT:M) under a two-dimensional contract vector . The particular representative set of results presented here is based on the average daily demand pattern illustrated in the rightmost plot of Figure 1, with the base parameter settings given by , , , , , , , , , , , , , , , , , and , where , and . In addition to these base settings, we vary the parameter values one at a time for , , , , , and , in order to investigate the impact and sensitivity of these parameters on the performance trade-offs between the two formulations. Within this experimental setting, as a representative example, we consider the corresponding single primary resource allocation model with and consider a corresponding instance of the multiple primary resource allocation model with . The values of and are separately obtained for each of the two primary resource formulations. For every computational experiment under a given set of parameters, we generate daily sample paths using a timescale of a couple of seconds and a setting of five minutes. We note that a wide variety of experiments with different parameter, timescale and settings were evaluated and shown to exhibit similar performance trends as those presented herein. We then apply our optimal dynamic control policy for each formulation to this set of daily sample paths as described in Section 5.1.

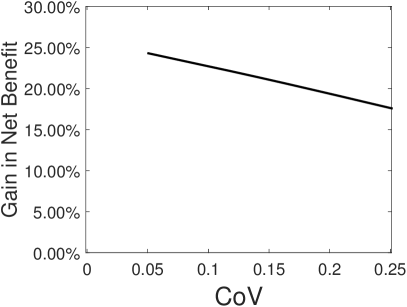

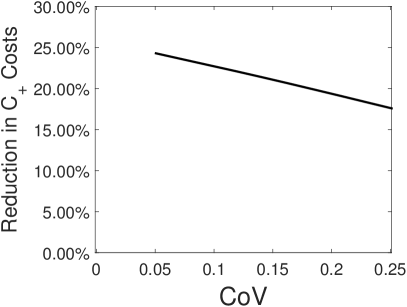

Figure 5 presents a representative sample of our computational results in which the leftmost graph provides comparisons based on the relative improvements in expected net-benefit under our optimal control policy for the two primary resource formulations as a function of the coefficient of variation ; analogous to the leftmost graphs in Figures 2 and 4, the relative improvement is defined here as the difference between the expected net-benefit for the multiple primary resource model and the single primary resource model, divided by the expected net-benefit for the single primary resource model. The rightmost graph provides comparisons based on the relative improvements in expected cumulative discounted costs associated with under our optimal control policy for the two primary resource formulations as a function of CoV; the relative improvement is defined here as the difference between the expected cumulative discounted contributions of over the infinite horizon for the single primary resource model (i.e., in (3.9)) and the multiple primary resource model (i.e., in (4.9)), divided by the expected net-benefit for the single primary resource model. From these results we observe that the gain in expected net-benefit is significant, demonstrating the potential performance benefits to an organization under the multiple primary resource allocation model for such problem instances. These expected net-benefit improvements in the leftmost graph tend to decrease as the coefficient of variation increases, while still remaining significant over the range of CoV values. This decrease in the expected net-benefit gain is primarily due to a similar decreasing trend in the relative difference in the expected cumulative discounted contributions of over the infinite horizon as CoV increases. To help explain this, we note that the values of the second summand in (3.8) and the expected cumulative discounted contributions of over the infinite horizon are of the same order of magnitude in these experiments, whereas the values of the remaining terms in (3.9) and (4.9) are orders of magnitude smaller; the similarity of the two graphs are due to the facts that the two higher order magnitude terms dominate the objective function value (expected net-benefit) and the value of the second summand in (3.8) is the same under both primary resource models. Hence, the trends in the relative expected net-benefit improvements as a function of CoV are directly related to the very similar trends in the relative expected discounted cumulative cost improvements as a function of CoV. These trends in turn are primarily due to the role of the risk-hedging interval that widens under each model as a function of the increasing CoV in order to have the optimal dynamic control policy reduce the expected discounted cumulative costs associated with the primary resource(s) over the infinite horizon. In other words, the optimal dynamic control policy under both models becomes somewhat more conservative due to the greater risks associated with having a primary resource allocation position that is too large and that would otherwise result in larger expected discounted cumulative costs associated with . These factors have a somewhat stronger impact on the multiple primary resource model as CoV increases.

Lastly, it can also be important to consider the role of the margin of rewards and costs when investigating the relationship between the single primary resource formulation (SC-OPT:S) and the multiple primary resource formulation (SC-OPT:M). In many practical applications, the overall rewards and costs are of similar magnitude with reasonably balanced margins, and thus the relationship between the two formulations includes key trade-offs among the net-benefits from both the second summand in (3.8) and the term involving and in (3.9) and (4.9) on the one hand, and the relative costs from the terms involving , and in (3.9) and involving , and in (4.9) on the other hand. These trade-offs are indeed reflected in the representative results illustrated in Figure 5. However, in situations where the net-benefits are considerably larger than the relative costs in (3.9) and (4.9), then the relationship between the single primary resource formulation and the multiple primary resource formulation can depend in large part on the magnitude and ordering between and ; in this case with dominating , the single primary resource model can outperform the multiple primary resource model . Analogously, when the relative costs are considerably larger than the net-benefits in (3.8), (3.9) and (4.9), then the relationship between the two formulations can depend in large part on the magnitude and ordering among , , , , and ; in this case with, e.g., dominating , the multiple primary resource model can outperform the single primary resource model.

6 Conclusions

In this paper we investigated a general class of dynamic resource allocation problems arising across a broad spectrum of application domains that intrinsically involve different types of resources and uncertain/variable demand. With a goal of maximizing expected net-benefit based on rewards and costs from the different resources, we derived the provably optimal dynamic control policy within a stochastic optimal control setting. Our mathematical analysis includes obtaining simple expressions that govern the dynamic adjustments to resource allocation capacities over time under the optimal control policy. A wide variety of extensive computational experiments demonstrates and quantifies the significant benefits of our optimal dynamic control policy over recently proposed alternative optimization approaches in addressing a general class of resource allocation problems across a diverse range of application domains, including cloud computing and data center environments, computer and communication networks, and human capital supply chains. Moreover, our results strongly suggest that the stochastic optimal control approach taken in this paper can provide an effective means to develop easily-implementable online algorithms for solving stochastic optimization problems. Both single primary resource allocation and multiple primary resource allocation models can be exploited, with the best option depending upon the system environment and model parameters.

Following along the lines of our computational experiments, our algorithm can exploit any consistent seasonal patterns for and observed from historical traces in order to predetermine the threshold values and or and . In addition, various approaches such as statistical learning and/or model predictive control (e.g., [12]) can be used to adjust these threshold values in real-time based on identifying and learning any nonnegligible changes in the realized values for and . Furthermore, this latter approach can be used directly for system/network environments whose demand processes do not exhibit consistent seasonal patterns.

Acknowledgments.

Xuefeng Gao acknowledges support from Hong Kong RGC ECS Grant 2191081 and CUHK Direct Grants for Research with project codes 4055035 and 4055054. A portion of Mark Squillante’s research was sponsored by the US Army Research Laboratory and the UK Ministry of Defence and was accomplished under Agreement Number W911NF-06-3-0001. The views and conclusions contained in this document are those of the authors and should not be interpreted as representing the official policies, either expressed or implied, of the US Army Research Laboratory, the US Government, the UK Ministry of Defense, or the UK Government. The US and UK Governments are authorized to reproduce and distribute reprints for Government purposes notwithstanding any copyright notation hereon.

Appendix A Proofs of Results in Section 3

In this appendix we collect the proofs of our main results in Section 3. We start with a rigorous proof of Theorem 1 and Corollary 2, which proceeds in three main steps. First, we express the optimality conditions for the stochastic dynamic program, i.e., the Bellman equation corresponding to (3.9) – (3.12). We then derive a solution of the Bellman equation and determine the corresponding candidate value function and dynamic control policy, establishing smoothness and convexity of the candidate value function and uniqueness of the threshold values. Finally, we verify that this dynamic control policy is indeed optimal through a martingale argument. Each of these main steps is presented in turn. Then we present the proofs of our other main results.

A.1 Proof of Theorem 1 and Corollary 2: Step 1

From the Bellman principle of optimality, we deduce that the value function satisfies for each

| (A.1) |

refer to [40, Chapter 4]. Suppose the value function is smooth, belonging to the set (i.e., the set of twice continuously differentiable functions) except for a finite number of points, and is bounded for any . Then, based on a standard application of Ito’s formula as in [26, Chapter 1], we derive that the desired Bellman equation for the value function has the form

| (A.2) |

where

| (A.3) |

A.2 Proof of Theorem 1 and Corollary 2: Step 2

Our next goal is to construct a convex function that satisfies the Bellman equation (A.2) and show that the threshold values and are uniquely determined by the corresponding pair of nonlinear equations in Theorem 1. Suppose a candidate value function satisfies (A.2). Given (A.3), we expect a “bang-bang” type solution based on the signs of and . In particular, we seek to find and such that

| (A.4) |

Moreover, we require that meets smoothly at the points , and to order one, and as (i.e., for some ) so that is bounded.

For each of the three cases in Theorem 1, we first solve the Bellman Equation (A.2) to derive the corresponding pair of equations that and satisfy. Then we discuss conditions on model parameters under which the points and are located in comparison with . Finally, we show that the function we construct has the property (A.4).

A.2.1 Case I:

We proceed to solve the Bellman equation (A.2) depending on the value of in relation to , and . There are four subcases to consider as follows.

(i). If , we obtain from (A.4) that

Then the Bellman equation (A.2) yields

or equivalently

Solving this second order linear nonhomogeneous differential equation, we obtain

where are given in (3.7) and are two constants to be determined. Since when goes to , one finds Thus we derive for

| (A.5) |

(ii). If , we have

and thus we obtain

This implies for

| (A.6) |

where are given by (3.5), and are two generic constants to be determined.

(iii). If , we find from (A.4) that

Then (A.2) becomes

and thus

| (A.7) |

where are given by (3.6), and are two generic constants to be determined.

(iv). If , we have

and we similarly derive that

Since as , we deduce that the solution is then given by

| (A.8) |

where is given by (3.6), and is a generic constant to be determined.

Now we determine and as well as the other six unknown constants . We do so by matching the value and the first-order derivative of at the points , and . This leads to eight nonlinear equations in total as illustrated below. In addition, using such a construction, the function will be twice continuously differentiable with the exception of at most three points. Let us first consider such matchings at the point . From (A.4), (A.5) and (A.6), we obtain three equations:

Upon simplifying, we can express in terms of and the model parameters as follows:

| (A.9) | |||||

| (A.10) | |||||

| (A.11) |

Similarly, matching at the point , we obtain another three equations:

Upon plugging the expressions for and into , we obtain (3.13). On the other hand, it follows from that

| (A.12) |

Combining this with , we cancel and derive

| (A.13) |

Lastly, solving by matching at the point 0 to order one, we obtain two equations:

Solving these two equations renders

| (A.14) |

Upon substituting the expressions for , and into (A.13) and simplifying the resulting expression, we conclude that and satisfy (3.14). Once we determine and from (3.13) and (3.14), the other unknown constants can be derived from (A.9)-(A.14) accordingly.

Next, we provide conditions under which (3.13) and (3.14) have a unique solution and that are both non-negative. Define for ,

| (A.15) |

We first consider the case In this case, one can readily verify that

| (A.16) |

In addition, is strictly convex and . Thus has a unique solution in . Since (3.13) is equivalent to , we deduce that is negative and it is uniquely determined by (3.13). On the other hand, observe that holds if and only if holds since . Using (3.14), this condition is equivalent to

which, upon canceling using (3.13), becomes

Therefore, guaranteeing that (3.13) and (3.14) has a unique solution with is equivalent to showing that has a unique solution in the interval

This is true if either of the following two set of conditions hold:

Note that We then find that these conditions are exactly condition (1a) and (1b) in Theorem 1 after applying simple algebraic manipulations. We next consider the case where . It is clear from (A.16) that , and . This implies the unique solution to (3.13) is . Now we deduce from Equation (3.14) that

and if and only if . This condition is equivalent to , which corresponds to condition (1c) in Theorem 1. Note that if and only if . Thus, as a byproduct, we have obtained the explicit form of in Corollary 2 when .

Finally, we verify that the candidate value function satisfies the required first-order properties in (A.4). Since we have constructed the function with and , then to establish (A.4) it suffices to verify the convexity of the function . To this end, we first consider . One readily confirms from (A.5) and (A.9) that

Given that and that in (3.7), we can conclude

Similarly, when , we have

Hence, to show , it suffices to show that . From (A.14), it is equivalent to show

| (A.17) |

Using the relationship between and in and substituting given in (A.14), we infer from (A.17) that we simply need to establish

Given , it suffices to show

| (A.18) |