Expansion formulas for European quanto options

in a local volatility FX-LIBOR model

Abstract.

We develop an expansion approach for the pricing of European quanto options written on LIBOR rates (of a foreign currency). We derive the dynamics of the system of foreign LIBOR rates under the domestic forward measure and then consider the price of the quanto option. In order to take the skew/smile effect observed in fixed income and FX markets into account, we consider local volatility models for both the LIBOR and the FX rate. Because of the structure of the local volatility function, a closed form solution for quanto option prices does not exist. Using expansions around a proxy related to log-normal dynamics, we derive approximation formulas of Black–Scholes type for the price, that have the benefit of giving very rapid numerical procedures. Our expansion formulas have the major advantage that they allow for an accurate estimation of the error, using Malliavin calculus, which is directly related to the maturity of the option, the payoff, and the level and curvature of the local volatility function. These expansions also illustrate the impact of the quanto drift adjustment, while the numerical experiments show an excellent accuracy.

Key words and phrases:

European quanto derivatives, convexity adjustment, volatility skew/smile, local volatility FX-LIBOR model, expansion formula, analytical approximations, Malliavin calculus.1. Introduction

We are interested in the pricing of European quanto options on LIBOR rates. These correspond to a type of derivative in which the underlying rate is denominated in one currency (foreign currency) but the payment is made in another currency (domestic currency). Such products are attractive for speculators and investors who wish to have exposure to a foreign asset, but without the corresponding exchange rate risk. Think, for instance, of a Euro-based investor who is seeking exposure on the GBP LIBOR rate, but does not want to be exposed to changes of the GBP/EUR foreign exchange rate. A European quanto option on the GBP LIBOR rate is a very suitable financial product for her, as it has the payoff of a standard non-quanto option on the GBP LIBOR rate and converts the payout with a guaranteed rate of 1 from GBP into Euro at maturity.

In an arbitrage-free framework, the pricing of quanto options can be performed under the domestic forward measure. In order to express the dynamics of the underlying LIBOR rate under this pricing measure, one has to apply Girsanov’s theorem, leading to a drift term which depends on the volatility of the LIBOR rate, on the volatility of the FX rate, and on the correlation between the LIBOR and the FX rate. This drift term leads to an adjustment in the pricing that is referred to as quanto adjustment and falls into the more general category of what is called in mathematical finance convexity adjustment.

This class of contracts, termed exotic European options by Pellser (2000), are widely traded over the counter (OTC). The correct pricing and risk management of European quanto options constitutes an important issue in the financial industry. The consideration of the market skew/smile for interest rates and FX rates is fundamental for a correct valuation of European quanto derivatives as discussed in Romo (2012). In reference textbooks and articles, see e.g. Musiela and Rutkowski (2005), Brigo and Mercurio (2006) or Reiner (1992), a simplified Black–Scholes model is considered in order to obtain analytical formulas. A similar practical approach is commonly used in the financial industry; see Section 5.2 or e.g. Romo (2012) and Christoffersen and Jacobs (2004) for more details. However, it does not take into account properly the skew/smile effects of the underlying assets in the quanto drift adjustment. These issues with the commonly used approach and the importance of incorporating the skew/smile properly in the valuation of European quanto options are studied and discussed in e.g. Romo (2012), Jäckel (2016), Giese (2012) or Vong and Rojas-Carulla (2014).

Local volatility models, either parametric or non-parametric, see e.g. Dupire (1994); Derman and Kani (1998); Rubinstein (1994); Jäckel (2008) or Cox (1975), usually capture the surface of implied volatilities more precisely than other approaches, such as stochastic volatility models; see e.g. Ren et al. (2007) or Romo (2012) for discussions. Moreover, the findings in Romo (2012) or Hull and Suo (2002) indicate that the local volatility model can be a correct approach to price European quanto derivatives in the presence of volatility skew/smile.

Motivated by the discussions above, we propose to evaluate European quanto options in a general local volatility framework. Because of its generality, it is often difficult to get analytical formulas for pricing, especially in a high-dimensional case. In general, the effective pricing requires the use of a numerical method, based either on PDE (partial differential equation) techniques or Monte Carlo simulations, which can be prohibitively time-consuming for real-time applications. Only in very few cases does one have closed-form formulas; cf. Albanese et al. (2001). In the case of homogeneous volatility, singular perturbation techniques (Hagan and Woodward (1999)) have been used to obtain asymptotic expressions for the price of vanilla options (call, put). Implied volatility formulas are derived using asymptotic expansion methods for short maturities, as in Berestycki et al. (2002), Henry-Labordère (2005) and Albanese et al. (2001). In a more general diffusion setting, approximations of the density function and option prices are derived based on the small disturbance asymptotics, see e.g. Kunitomo and Takahashi (2004); Yoshida (1992) or Takahashi (1995, 1999) or Takahashi (2015) for a review. By adapting the singular perturbation method used in Hagan and Woodward (1999), several authors have developed expansion formulas for the density function of the underlying process and option prices in a general local volatility model; see e.g. Pagliarani and Pascucci (2012) and Foschi et al. (2013).

The purpose of the present article is to provide simple and accurate approximation formulas for quanto options in a general local volatility model. Towards this end, we apply the perturbation method using a proxy introduced in Benhamou et al. (2009). This method has been applied and extended in many directions, see e.g. Benhamou et al. (2010b, 2012), Gobet and Miri (2014), Gobet and Hok (2014) and Gobet and Bompis (2014). We derive expansion formulas, which are of Black–Scholes type, and develop the analysis using Malliavin calculus, to provide accurate estimations of the errors. We believe that rigorous error estimates are of prime importance because the accuracy of our expansion formulas depends on the regularity of the payoff function. Once done, this brings confidence in the derived expansions and sheds light on the needed assumptions; see our main results in Theorems 3.6 and 3.7.

A major advantage of our expansion formulas is that they clearly illustrate the impact of the quanto drift adjustment and provide very rapid numerical procedures for its implementation. The numerical tests, see Section 5, show that our formulas constitute a very accurate approximation. Our interest in such problems was motivated by specific applications to European quanto derivatives on LIBOR rates, hence we specialize our study to that setting. However, the approximation methodology and results could be applied to other financial assets as well. Moreover, we focus on single-curve LIBOR models as they constitute the basis for multi-curve models. The extension to multiple curves is straightforward given the analysis and results of the present paper, however it is also very tedious.

This article is structured as follows: Section 2 introduces local volatility models for simultaneously modeling FX and LIBOR rates, as well as quanto options. Section 3 outlines the approach to quanto pricing via expansions around a proxy model and states the main results, which are second and third order expansions for the prices of quanto options. Section 4 provides an error analysis and the derivation of the second order expansion formula, while Section 5 provides numerical results. Finally, the Appendices contains some auxiliary results and the derivation of the third order expansion formula.

2. FX-LIBOR models and European quanto options

2.1. A local volatility FX-LIBOR framework

Let denote a filtered probability space where the filtration satisfies the usual conditions and denotes a finite time horizon. Let also denote a discrete tenor structure where is the accrual fraction for the period , and define . The dates correspond to maturity dates of traded instruments.

We assume the existence of an arbitrage-free system of domestic and foreign zero coupon bonds, denoted respectively and . We further consider domestic and foreign forward martingale measures, denoted by and , where the corresponding zero coupon bond acts as the numeraire for each forward measure. Let and denote standard -dimensional Brownian motions relative to the domestic and foreign terminal forward measures and respectively.

Let and denote the domestic and foreign forward LIBOR rates, i.e. the discretely compounded forward rates for investing in the time period in the domestic and foreign market. Their relation to zero coupon bonds is classically given by

| (2.1) |

The dynamics of the system of foreign LIBOR rates is provided by a local volatility model of the form

| (2.2) |

where the -Brownian motion is related to the terminal Brownian motion via

| (2.3) |

for all . The functions , , are continuous, deterministic and satisfy a suitable linear growth condition, cf. Brigo and Mercurio (2006, §10.3). They represent the local volatility of the foreign forward LIBOR rate .

Let denote the foreign exchange (FX) rate expressed in terms of units of domestic currency per unit of foreign currency. The FX forward rate for settlement at time , denoted by , is defined by no-arbitrage arguments and provided by

| (2.4) |

for all . The FX forward rate is, per definition, a -martingale, and we assume it follows again a local volatility model of the form

| (2.5) |

where is the -Brownian motion and , , is a continuous, deterministic function satisfying a suitable linear growth condition, and represents the local volatility of the FX forward rate.

The domestic and foreign forward Brownian motions are related via

| (2.6) |

for all , and this equation together with (2.3) determines also the relations between the domestic forward Brownian motions; see Schlögl (2002) for the details (in particular Fig. 2). Therefore, the dynamics of the foreign LIBOR rate under the domestic forward measure are provided by

| (2.7) |

2.2. European quanto options and a local volatility model

A quanto cap is a series of quanto caplets, where each quanto caplet is a call option on the foreign LIBOR rate struck at the domestic currency. In other words, a quanto caplet with strike price and expiry date pays at time the amount

| (2.8) |

in units of domestic currency. Therefore, the price of a quanto caplet is provided by

| (2.9) |

where denotes the expectation with respect to the domestic forward measure .

In the sequel we will consider a local volatility model where each LIBOR rate and each FX forward rate are driven by ‘their own’ one-dimensional, correlated Brownian motions, resulting in the following system of SDEs:

| (2.10) |

with initial values , where and are -valued volatility functions and .

Assuming that all the coefficients in (2.10) are deterministic, is log-normally distributed and the price of a quanto caplet in (2.9) is given by a Black–Scholes type formula; see e.g. Brigo and Mercurio (2006) or Musiela and Rutkowski (2005). In order to take into account the skew and smile effects observed in the fixed income and foreign exchange markets, we will consider a local volatility model and suppose that and are functions of and respectively. In that case, a closed form solution does not exist anymore and computing (2.9) numerically by Monte Carlo simulations or PDE methods is time consuming. Our objective therefore is to provide an approximation formula for (2.9) which is accurate enough and allows for an efficient implementation.

Remark 2.1.

We assume throughout that the correlation between the forward LIBOR and the forward FX rate is deterministic and maturity-dependent. The extension to a time- and maturity-dependent correlation is straightforward.

3. An expansion approach to quanto pricing

The main idea of expansion approaches to option pricing is to derive an asymptotic expansion of the option price in terms of quantities that are known and can be computed quickly, such as prices in a Black–Scholes model and Greeks. This leads to a numerical scheme for the option price that is faster to compute than the corresponding PDE or Monte Carlo methods, while its accuracy can be improved by including additional terms in the expansion. This section performs an analogous expansion for the price of a (generic) quanto option, and provides formulas for this option price in terms of a Black–Scholes model and Greeks, while the correlation between FX and LIBOR plays a crucial role.

In order to simplify notation, we will suppress the sub- and super-scripts related to the tenor and currency, and make use of the following notation:

| (3.1) |

Considering the logarithms of the LIBOR and the FX rate, denoted by and , the system of SDEs (2.10) takes the form

| (3.2) |

where

| (3.3) |

Moreover, the price of a quanto option with generic payoff function is provided by

| (3.4) |

3.1. Closed-form formula under log-normal dynamics

Assume that the local volatility coefficients are deterministic, time-dependent functions, in particular and , for all . Then, follows a normal distribution and we can derive a closed-form formula for the price of the quanto caplet defined in (2.8).

Indeed, using standard results from stochastic calculus, we have that

| (3.5) |

where

| (3.6) |

Thus, exactly as in Brigo and Mercurio (2006), the price of the quanto caplet is given by the following, Black–Scholes type, formula:

| (3.7) |

with

| (3.8) |

where denotes the cdf of the standard normal distribution, , and

| (3.9) |

3.2. Expansion formulas under general dynamics

The aim of this subsection is to provide expansion formulas that approximate the price of a quanto option when we consider general local volatility dynamics for the LIBOR and the FX rate. Let us first introduce some notation, and some assumptions that allow us to derive these formulas.

Assumption ().

The volatility functions and are of class in and respectively, for some . In addition, these functions and their derivatives are uniformly bounded.

Let us introduce the following constants

| (3.10) | ||||

| (3.11) |

and also

| (3.12) |

Let us denote by the space of functions with growth being at most exponential. In other words, a function belongs to if , for any , for two positive constants and . Moreover, let denote the -th derivative of the function .

We will separate our analysis according to the smoothness of the payoff function, and distinguish between two cases:

Assumption ().

The payoff function belongs to , the space of real-valued infinitely differentiable functions with compact support.

Assumption ().

The payoff function is almost everywhere differentiable. In addition and belong to .

Remark 3.1.

The first assumption corresponds to (idealized) smooth payoff functions, while the second one corresponds to call and put options.

In real markets, the correlation between the forward LIBOR rate and the forward FX rate is typically not very large. As an example, the empirical study in Boenkost and Schmidt (2003) found its value in the range . Therefore, the following assumption is consistent with real market data.

Assumption ().

The correlation between the forward LIBOR rate and the forward FX rate is not perfect, i.e.

| (3.13) |

In order to perform the infinitesimal analysis in the error estimates, we rely on smoothness properties which are not provided by the payoff functions, but rather by the law of the underlying stochastic models; this is related to Malliavin calculus. The following ellipticity assumption on the volatility of the forward LIBOR combined with Assumption —i.e. Assumption with —guarantees that sufficient smoothness is available.

Assumption ().

The volatility of the forward LIBOR rate does not vanish and for a positive constant , one has

| (3.14) |

where and .

We consider now the following ‘proxy’ or ‘Black–Scholes’ processes:

| (3.18) |

and introduce a family of parametrized processes , for , via the system of SDEs:

| (3.24) |

Setting , we recover the dynamics of the local volatility model in (3.2) since and , while for we recover the Black–Scholes proxy in (3.18).

Assumption yields that, almost surely for any , is with respect to ; see e.g. Bell (2006) or Kunita (1997). Setting and by a direct differentiation of the SDEs (3.24), we get that

| (3.28) |

with , and

| (3.35) |

with , and

| (3.48) |

with Here, we have used the following shorthand notation for the first order derivatives of the coefficients of the SDEs

| (3.53) |

and analogously for higher order derivatives.

Let us now introduce the main tools of this method, which are expansions of the random variable and the payoff function of the quanto option around known values. In order to keep the notation simple, we set , . Then, by performing a Taylor expansion of around zero, we get that

| (3.54) |

The dynamics of the proxy model in (3.18) yield that is a Gaussian random variable with mean and variance , where

| (3.55) |

Performing now a Taylor expansion of the payoff in (3.4) around , we arrive at a formula of the following form:

| (3.56) |

The first term constitutes the leading order contribution, it is explicitly known (via an analytical formula analogous to (3.1) for the payoff function ), but as an approximation alone is not accurate enough. Therefore, in the sequel we will derive correction terms in order to achieve better accuracy. These correction terms are represented as a combination of Greeks of the option price formula (3.1). Hence, the numerical evaluation of all these terms is straightforward, with a computational cost equivalent to the analytical formula (3.1).

3.3. Definitions and notation

Before providing the main results, let us introduce some definitions and notation that will be used in the sequel.

Definition 3.2 (Integral Operator).

The integral operator is defined as follows: for any integrable function , set

| (3.57) |

for . Similarly, for integrable functions and set

| (3.58) |

This can be easily iterated to define .

Definition 3.3 (Greeks).

Let be an appropriate payoff function (such that the expression below makes sense). We set, for

| (3.59) |

Remark 3.4 (Generic constants).

We use the notation to assert that , where is a positive constant depending on the model parameters, on , , , and on other universal constants. The constant may change from line to line, but remains bounded when the model parameters go to .

Remark 3.5 (Notation for the coefficients).

The coefficients and their derivatives will be evaluated from now on at the initial values , i.e. when we write we mean , and the same holds for their derivatives. We will sometimes also use the subscript when we want to stress their dependence on time.

3.4. Main results

We are now ready to state the main results of this work, that provide second and third order expansions of an option price around the proxy model, thus making precise the formula in (3.56). The proofs are deferred to Section 4.

Theorem 3.6 (2nd order expansion in price).

Assume that conditions , , and are in force. Then, the second order expansion of the option price takes the form:

| (3.64) |

Additionally, the error estimate is provided by

| (3.65) |

Theorem 3.7 (3rd order expansion in price).

Assume that conditions , , and are in force. Then, the third order expansion of the option price takes the form:

| (3.66) |

where

| (3.73) |

with

| (3.77) |

The expressions for the coefficients , , are provided respectively by (C.16), (C.22), (C.28) and (C.33) in Appendix C. Additionally, the error estimate is given by

| (3.78) |

Remark 3.8 (Sanity check).

Consider a call option with payoff , then the theorems above provide an approximation formula for its price in log variables. In that case, corresponds to the Black–Scholes price given by (3.1). In order to compute the correction terms, we need to calculate the derivatives of w.r.t. . Below is a useful lemma allowing to calculate them in a systematic way using Hermitte polynomials.

Lemma 3.9.

Let , then we have

| (3.79) |

where , , denotes the Hermitte polynomials defined as

| (3.80) |

The proof is provided in Appendix A.

4. Analysis and proofs

This section provides the derivation of the expansion formulas for quanto pricing presented in Theorems 3.6 and 3.7, as well as an analysis of the corresponding error terms. After some preliminary results, the expansion formulas and the corresponding error estimates for the second and third order expansions are presented in Section 4.2. The derivation of the Greeks for the second order expansion is presented in Section 4.3, while the details for the Greeks of the third order expansion are deferred to the appendix for the sake of brevity.

4.1. Auxiliary results

We start with some results that are useful for the subsequent error analysis. The -estimates follow from the work of Benhamou et al. (2010a, Theorem 5.1), thus their proof is omitted. As usual, the -norm of a real random variable is provided by .

Lemma 4.1 (-estimates).

Assume that condition is in force. Then, for all and , we have

| (4.1) |

| (4.2) |

The following lemmata are used repeatedly in order to derive the analytical formulas in Theorems 3.6 and 3.7. An application of Itô’s lemma to yields the following result.

Lemma 4.2.

Let be a continuous (or piecewise continuous) function and be a continuous semimartingale with . Then

| (4.3) |

The lemma below follows directly from the duality relationship in the Malliavin calculus (see e.g. Nualart (2005, Lemma 1.2.1, p.25)) and by identifying Itô’s integral and the Skorohod operator for adapted integrands.

Lemma 4.3.

Let be a square integrable, progressively measurable process and assume satisfies . Then, for any , it holds:

| (4.4) |

with and . Moreover, if and are deterministic, then

| (4.5) |

where .

4.2. Price expansions and error estimates

We are now ready to provide the details in the derivation of the expansion formulas and the corresponding error estimates. We start with the analysis of the second order approximation, and divide the proof of Theorem 3.6 in several steps. First, we assume that the payoff is smooth and establish error estimates that depend only on , the first derivative of . To this end, we use Malliavin calculus and provide tight estimates on the Malliavin derivatives of the parametrized process. Then, we can approximate under by a sequence of smooth payoffs using a density argument. This last step is standard by now, hence we omit it for the sake of brevity.

4.2.1. Second order error analysis

As outlined in the previous section, we perform first a Taylor expansion of around , that yields

| (4.6) |

then another Taylor expansion for the smooth payoff , and then take expectations. Thus we obtain

| (4.7) |

Using (4.6), (4.2.1) can be written as

| (4.8) |

where

| (4.9) |

with

| (4.10) |

Using (4.2) with in Lemma 4.1 and the Cauchy–Schwarz inequality, the first term in (4.9) is estimated as

| (4.11) |

The second term in (4.9) requires some additional work because of . We use the integration-by-parts formula in the Malliavin calculus to write it using only. For this, we rely on Lemma B.2 and refer to Appendix 5.3.3 for notation related to the Malliavin calculus. Let us apply this result to , such that we can write

| (4.12) |

Using now the estimates in Lemmata 4.1 and B.1, we can show easily that

| (4.13) |

and get

| (4.14) |

Therefore, we can deduce that

| (4.15) |

Because and , we finally obtain

| (4.16) |

Thus far, we have bounded the error using only for a smooth function . In order to obtain a similar error bound under the assumption that satisfies (), we can use a density or regularization argument to approximate by a sequence of smooth functions as in Benhamou et al. (2009, Section 5.2, Step 4).

4.2.2. Third order error analysis

We follow again the same strategy as for the second order case. By a Taylor expansion of around , we have

| (4.17) |

and by performing again a Taylor expansion for a smooth payoff and taking expectations we obtain

| (4.18) |

Using (4.17), the latter becomes

| (4.19) |

where

| (4.20) | ||||

| (4.21) | ||||

| (4.22) |

Let us bound each term in the error separately. The first term (4.20), using (4.2) with in Lemma 4.1 and the Cauchy–Schwarz inequality, is estimated by

| (4.23) |

The second term (4.21) is handled as in the previous section. We recall that and apply Lemma B.2 with to such that we can write

| (4.24) |

Using the estimates in Lemmata 4.1 and B.1, we show easily that

| (4.25) |

hence

| (4.26) |

Therefore, we can deduce that

| (4.27) |

As for the third term (4.22), let us first provide a more explicit representation of . We define

| (4.28) |

and perform a second order Taylor expansion around to get

| (4.29) |

where

| (4.33) |

Setting in (4.29), we obtain

| (4.34) |

Replacing (4.34) into (4.22) and using Fubini’s theorem, we get

| (4.35) |

where for the last equality we have applied the integration-by-parts formula of Lemma B.2 with for . Applying now the Cauchy–Schwartz inequality, we get the following error estimate

| (4.36) |

while the estimates in Lemmata 4.1 and B.1 yield, for , that

| (4.37) |

and

| (4.38) |

Therefore, the third error term (4.36) is estimated by

| (4.39) |

4.3. Computation of the Greek coefficients

This subsection is devoted to the computation of the correction terms in the second order expansion of Theorem 3.6. The analogous derivation for the third order expansion is postponed to Appendix C. The correction terms are expressed in terms of Greeks of the payoff function around the proxy model, recall Definition 3.3, and we provide below a useful lemma for their computation.

Lemma 4.4.

Proof.

4.3.1. Greek coefficients for the second order approximation

The correction term for the second order expansion is provided by in (4.8) and our target now is to make this explicit. Let us recall equations (3.18)–(3.48), that and and Remark 3.5, which together yield that

| (4.48) | |||||

| (4.49) | |||||

| (4.50) | |||||

| (4.51) |

Let us also introduce the shifted payoff function

| (4.52) |

Then we have that

| (4.53) |

By applying Lemmata 4.3 and 4.4, we obtain

| (4.54) | ||||

| (4.55) | ||||

| (4.56) |

More specifically, the first equality follows directly by (4.41) and the second one by (4.42). For the third equality, we apply first Lemma 4.3 and then (4.41).

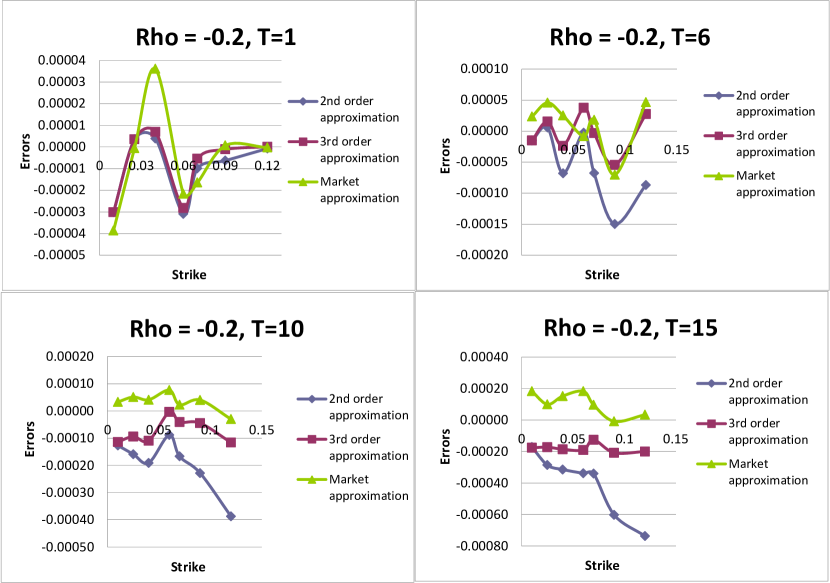

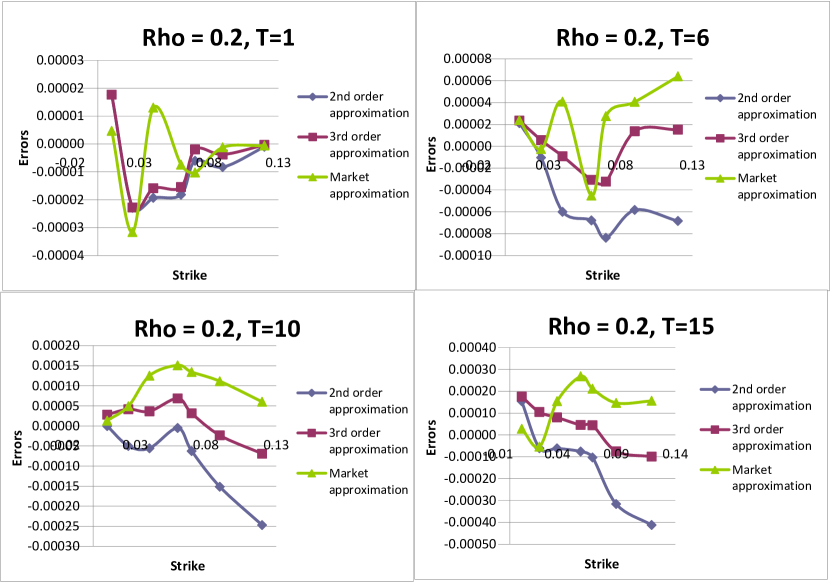

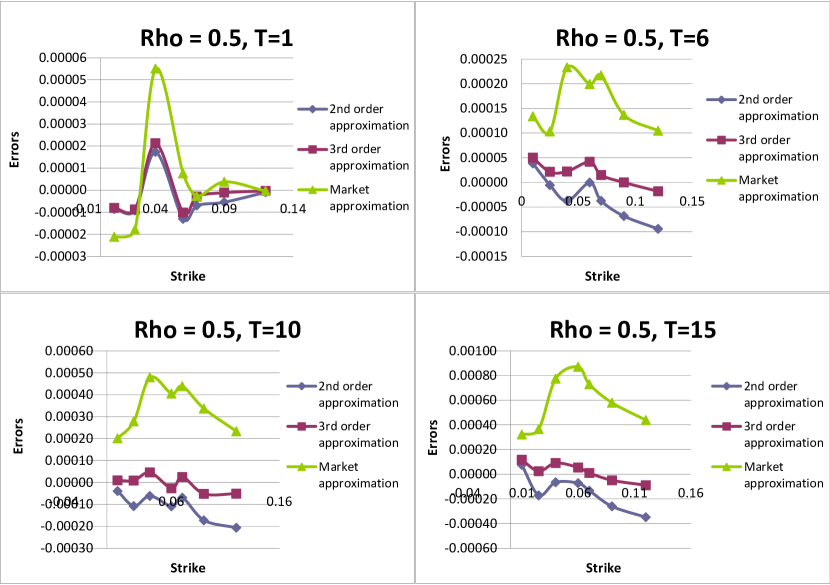

5. Numerical experiments

This section is dedicated to numerical experiments and a comparison of the second and third order expansions with the “market” approximation for quanto options.

5.1. Time-homogeneous hyperbolic local volatility model

We consider the time-homogeneous hyperbolic local volatility model where the SDEs for the forward LIBOR and the forward FX rate are provided by (2.2) and (2.5), while the coefficients and are homogeneous in time and take the form:

| (5.1) | ||||

| (5.2) |

where and , both strictly positive, represent the levels of volatility, while and , both valued in , represent the skew parameters. This model corresponds to the Black–Scholes model for and exhibits a skew for the implied volatility surface when . It was introduced by Jäckel (2008), behaves similarly to the CEV (Constant Elasticity of Variance) model, and has been used for numerical experiments also in Bompis and Hok (2014). The advantage of this model is that zero is not an attainable boundary, and that allows to avoid some numerical instabilities present in the CEV model when the underlying LIBOR or FX rate are close to zero; see e.g. Andreasen and Andersen (2000). Although the assumptions of boundedness and ellipticity are not fulfilled, we reasonably expect that our approximation formulas remain valid for this model, and apply Theorems 3.6 and 3.7. The payoff of a call option on the other hand does satisfy the smoothness assumption , as the payoff is everywhere differentiable apart from the kink at the strike level and grows exponentially. The numerical experiments that follow show that the derived approximations perform well in this setting, even though some theoretical assumptions are not satisfied.

5.2. Market approximation for pricing of European quanto option

The common market practice is to evaluate European quanto call/put options analytically using a Black–Scholes type formula with a quanto drift correction. More precisely, for a caplet with maturity date , strike and payment date , the market approximation is provided by

| (5.3) |

where , , is the cdf of the standard normal distribution, and

| (5.4) |

| (5.5) |

where , are respectively the ATM implied volatility for the forward LIBOR rate and the FX forward rate with expiry , while is implied volatility for the forward LIBOR rate with strike . This approach is similar to the “practitioner” Black–Scholes model considered in Christoffersen and Jacobs (2004) or Romo (2012). Observe that the approximation formula (5.3) becomes exact by construction when .

5.3. Comparison results for the second and third order expansions and the market approximation

5.3.1. Set of parameters

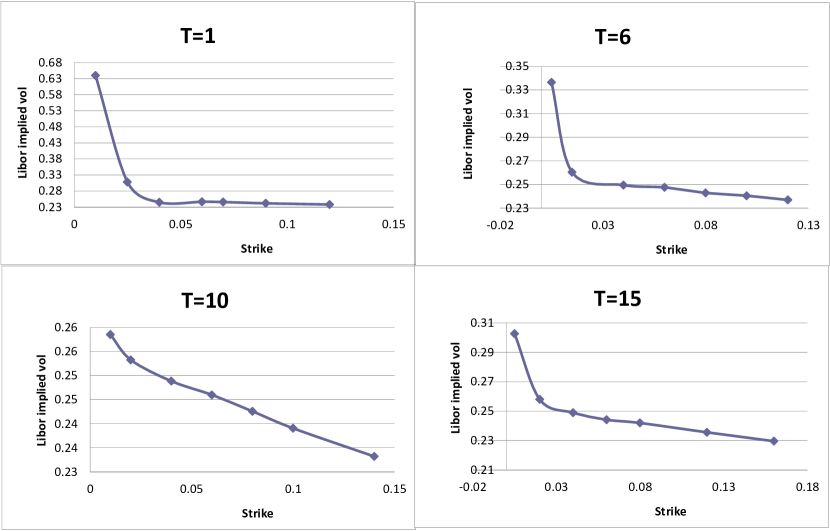

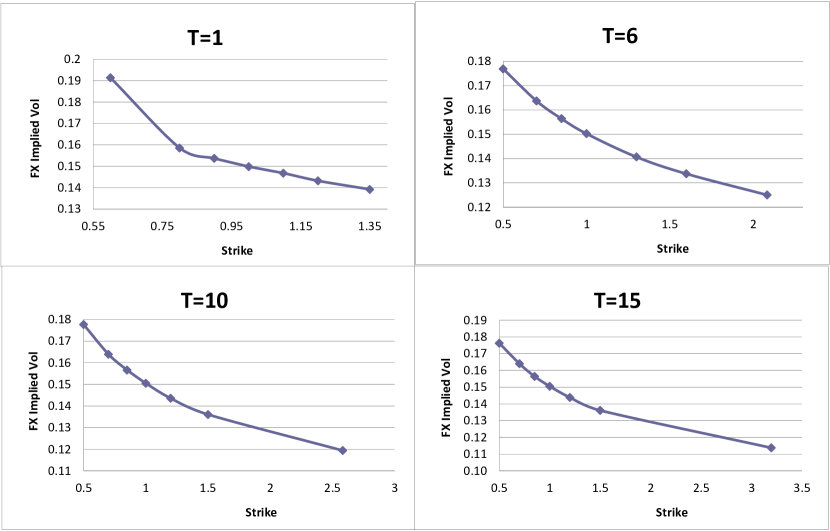

The numerical experiments are conducted using the following values for the parameters: , , , , and . They are chosen to be comparable to market values, see e.g. Hull and White (2000) and Ng and Sun (2008). In order to illustrate this, Figures 5.1 and 5.2 show, respectively, the implied volatilities for the forward LIBOR and the forward FX rates generated with these parameters for various maturities. They represent the skew typically observed in interest rates and FX markets.

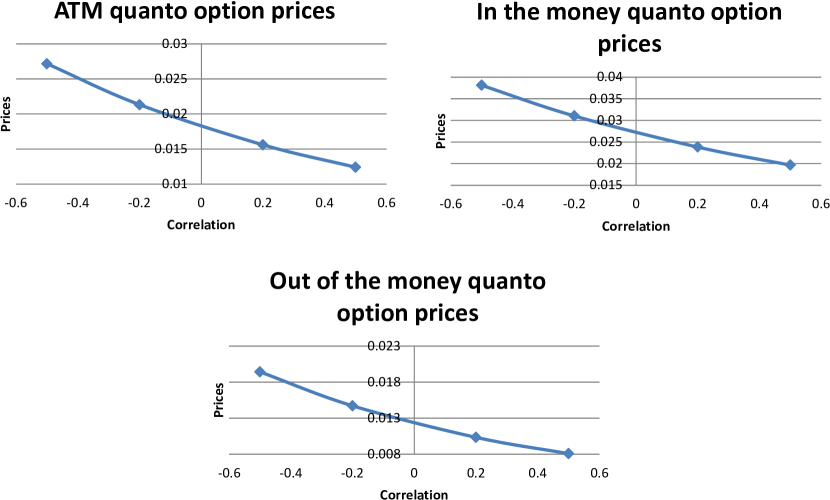

The challenging part for the pricing comes from the choice of the correlation parameter between the forward LIBOR rate and the foreign exchange rate, because its level is not directly observable in the market and has a significant impact in the pricing as showed in Figure 5.3. In practice, its level is either chosen by the trader or estimated using historical data. The empirical analysis in Boenkost and Schmidt (2003) shows that the estimated correlations depend on the underlying interest rates and the pair of currencies considered. In general, is not too large and belongs to the region . A trader who sells this product, may choose its level in a conservative way (higher selling price) by taking a lower or negative correlation level, as the option price is decreasing with . For these reasons and for the purpose of testing our formulas, we consider correlation levels .

In order for the tests to be comprehensive, we consider various relevant maturities (1, 6, 10 and 15 years) and strikes (with a range increasing with the maturity). This roughly covers very out-of-the-money options and very in-the-money options.

5.3.2. Benchmarks

Benchmarks for model prices are computed using the Monte Carlo method by discretizing the diffusion process using the Euler scheme. The number of Monte Carlo (MC) paths and the number of steps in the discretization are chosen such that the confidence intervals are within basis points.

5.3.3. Accuracy

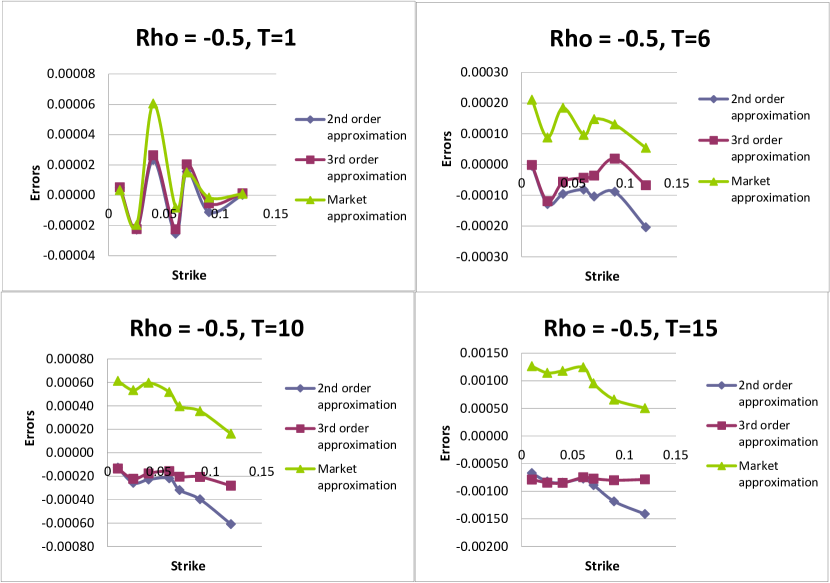

The results for the tests are illustrated in Figures 5.4, 5.5, 5.6 and 5.7. The following observations stem from these tests and their illustrations:

In general, the test results up to 15 years show that the second and third order approximation formulas provide very good accuracy.

Table 5.1 gives some statistics (average and maximum for the absolute discrepancy) for various correlation values considered.

The maximum average error for the second (third) order approximation formulas is () bps with correlation value equal to .

The maximum error for the second (third) order approximation is about () bps.

Third order approximation formulas produce better accuracy in comparison to the second order approximation formulas, which is expected.

The market approximation formulas provide good accuracy as well; see the statistics in Table 5.2.

This is due to the fact that this formula is exact for , which results in good accuracy when the correlation parameter is fairly small.

Indeed, the largest average error for the market approximation formulas is bps with correlation value equal to .

The maximum error for the market approximation is about bps.

In order to compare the different methods, let us mention that when the impact of the quanto effect becomes important (i.e. ), the accuracy of the third order approximation is better than the one given by the market approximation (see Figures 5.4 and 5.7), whereas the precision given by the second order and the market approximations is comparable. For a reduced quanto effect (i.e. ), the accuracy from the third order and the market approximation is similar. Indeed, in the limiting case of , the market approximation becomes exact by construction. The main advantage of our expansion formulas is to provide an accurate estimation of the error which is directly related to the maturity of the option (), the level and curvature of the local volatility functions ( and ) and the quanto impact ().

| Correlation | Average (2nd order) | MAX (2nd order) | Average (3rd order) | MAX(3rd order) |

|---|---|---|---|---|

| -0.5 | 0.00028 | 0.00141 | 0.00022 | 0.00084 |

| -0.2 | 0.00014 | 0.00074 | 0.00006 | 0.0002 |

| 0.2 | 0.00007 | 0.00041 | 0.00004 | 0.00017 |

| 0.5 | 0.00007 | 0.00035 | 0.00003 | 0.00011 |

| Correlation | Average (market approximation) | MAX (market approximation) |

|---|---|---|

| -0.5 | 0.00033 | 0.00126 |

| -0.2 | 0.00005 | 0.00018 |

| 0.2 | 0.00006 | 0.00027 |

| 0.5 | 0.00023 | 0.00087 |

Appendix A Proof of Lemma 3.9

Proof.

Let us write

| (A.1) |

where

| (A.2) |

with

| (A.3) |

For , we get . For , we apply the Leibniz formula for the product . ∎

Appendix B Malliavin calculus

We start by introducing some definitions and notation for the Malliavin calculus — see e.g. Bally et al. (2010) or Nualart (2005) more for details — before providing two lemmas for the estimates of Malliavin derivatives and the integration-by-parts formulas.

Let us write , where is a Brownian motion independent of , and consider the Malliavin calculus for the 2-dimensional Brownian motion . Let denote the Malliavin derivative of the random variable wrt to the Brownian motion at time , and similarly for the higher order derivatives, where for example .

Under the regularity assumption , using Nualart (2005), we know that for any , any and any , we have and . The existence of any moment is easy to establish, see e.g. Priouret (2005) or Nualart (2005). We focus on the Malliavin differentiability of the system of SDEs and their estimates.

Let , then . Now take , then solves the following system of SDEs

| (B.1) |

For the second order Malliavin derivatives, where for instance , we have

| (B.9) |

The process is independent from , hence its Malliavin derivatives wrt to it are zero. Similarly, for , while for , solves

| (B.10) |

For the second order Malliavin derivatives, take for instance , we have

| (B.11) |

Similarly, we provide the Malliavin derivatives for . because is independent of . for . For we have

| (B.12) |

Furthermore, for , while for , we get

| (B.22) |

Other Malliavin derivatives for this system of SDEs can be derived similarly, without particular difficulties. Following Benhamou et al. (2009, Theorem 5.2, Step 2), we provide in the following lemma tight estimates for this system of Malliavin derivatives, which are useful for the error analysis.

Lemma B.1 (Estimates of Malliavin derivatives).

The following hold, for any and :

| (B.30) |

uniformly in and .

In the following lemma, we state a key result of the integration-by-parts formula allowing to represent the error term (4.9) using only and providing some moments’ control useful in the error analysis.

Lemma B.2.

Let Assumptions and be in force. Let belong to . Then, for any , for , there exists a random variable in any such that for any function , one has

| (B.31) |

Moreover, one has , uniformly in .

Proof.

We prove the lemma for , since for the proof is similar.

-

Step 1: is a non-degenerate random variable (in the Malliavin sense).

Under , we know that is in . One has to prove that the Malliavin covariance matrix associated to , which is a scalar in this case, is defined as

(B.32) is almost surely positive and its inverse is in any .

By linearity, we have

(B.33) From (B.1) and by setting to and successively, we get for

(B.34) By solving (B.34) for , we obtain

(B.35) Hence, we can write

(B.36) The second inequality shows that is almost surely positive. With the last inequality and the control of the moments for the solution of an SDE (see Priouret (2005, Section 6.2.1)), we get for

(B.37) -

Step 2: Integration-by-parts formula.

Using Propositions 2.1.4 and 1.5.6 in Nualart (2005), one gets the existence of in with

(B.38) -

Step 3: Upper bound for , , for .

We recall that

(B.39) We bound each term above separately using the linearity of the Malliavin derivative operator to , the Holder inequality and the Malliavin derivatives’ estimates in Lemma B.1, to obtain

(B.40) For which is given by

(B.41) we use Lemma 2.1.6 in Nualart (2005) to write .

Similarly, we bound each term above separately using the linearity of the Malliavin derivative operator to (see (B.32)), the Hölder inequality, the Malliavin derivatives’ estimates in Lemma B.1 and the moments estimates in (B.37) to obtain

(B.42) Finally, using (Assumption ()) combined with inequalities (B.40) and (B.42), we get

(B.43) This completes our proof. ∎

Appendix C Derivation of the third order approximation formula

The additional correction terms for the third order expansion formula in (4.2.2) are provided by and . The first term, setting in (3.35), yields

| (C.1) |

Using Lemma 4.4, we compute each of the sub-correction terms separately:

| (C.2) |

| (C.3) |

| (C.4) |

| (C.5) |

| (C.6) |

| (C.7) |

| (C.8) |

As for the second corrective term, by applying Itô’s formula to (, we obtain

| (C.9) | |||||

We get directionsly for , by applying (4.45) with , that

| (C.10) |

Moreover, by applying Lemma 4.3 to , we get

| (C.11) |

hence and can be computed similarly. Indeed, with Itô’s formula and successive applications of Lemmata 4.2 and 4.3, we obtain for

| (C.12) |

Each term is computed explicitly using Lemma 4.4. Furthermore, with

| (C.13) |

we deduce directly the following expression for :

| (C.14) |

Each term above can be deduced from . Finally, the expression for is given by

| (C.15) |

By gathering all these terms, passing to the initial parameters and writing them as a polynomial function of (order 4), we obtain the third order expansion formulas in (3.66). We omit the details of these computations for the sake of brevity and provide directly the results. The constant coefficient is as in Theorem 3.7. The other coefficients are provided below.

We have that

| (C.16) | ||||

| (C.17) | ||||

| (C.18) | ||||

| (C.19) | ||||

| (C.20) | ||||

| (C.21) |

and

| (C.22) | ||||

| (C.23) | ||||

| (C.24) |

| (C.25) | ||||

| (C.26) | ||||

| (C.27) |

and

| (C.28) | ||||

| (C.29) | ||||

| (C.30) | ||||

| (C.31) | ||||

| (C.32) |

and finally

| (C.33) | ||||

| (C.34) | ||||

| (C.35) | ||||

| (C.36) |

All the expressions for the coefficients , and are gathered in Tables C.1, C.2 and C.3 below.

Acknowledgements

Philip Ngare gratefully acknowledges the financial support from an IMU Berlin Einstein Foundation Fellowship. The authors also thank the seminar participants at Global Derivatives for their fruitful comments.

References

- Albanese et al. (2001) C. Albanese, G. Campolieti, P. Carr, and A. Lipton. Black–Scholes goes hypergeometric. Risk, 14(12):99–103, 2001.

- Andreasen and Andersen (2000) J. Andreasen and L. Andersen. Volatility skews and extensions of the LIBOR market model. Applied Mathematical Finance, 7:1–32, 2000.

- Bally et al. (2010) V. Bally, L. Caramellino, and L. Lombardi. An introduction to Malliavin calculus and its applications to finance. Lecture notes, 2010.

- Bell (2006) D. Bell. The Malliavin Calculus. Dover Publications, 2006.

- Benhamou et al. (2009) E. Benhamou, E. Gobet, and M. Miri. Smart expansion and fast calibration for jump diffusion. Finance and Stochastics, 13:563–589, 2009.

- Benhamou et al. (2010a) E. Benhamou, E. Gobet, and M. Miri. Expansion formulas for European options in a local volatility model. International Journal of Theoretical and Applied Finance, 13:602–634, 2010a.

- Benhamou et al. (2010b) E. Benhamou, E. Gobet, and M. Miri. Time dependent Heston model. SIAM Journal on Financial Mathematics, 1:289–325, 2010b.

- Benhamou et al. (2012) E. Benhamou, E. Gobet, and M. Miri. Analytical formulas for local volatility model with stochastic rates. Quantitative Finance, 12(2):185–198, 2012.

- Berestycki et al. (2002) H. Berestycki, J. Busca, and I. Florent. Asymptotics and calibration of local volatility models. Quantitative Finance, 2:61–69, 2002.

- Boenkost and Schmidt (2003) W. Boenkost and W. M. Schmidt. Notes on convexity and quanto adjustments for interest rates and related options. Preprint No. 47, Frankfurt School of Finance and Management, 2003.

- Bompis and Hok (2014) R. Bompis and J. Hok. Forward implied volatility expansion in time-dependent local volatility models. ESAIM: Proceedings and Surveys, 45:88–97, 2014.

- Brigo and Mercurio (2006) D. Brigo and F. Mercurio. Interest Rate Models – Theory and Practice. Springer, 2nd edition, 2006.

- Christoffersen and Jacobs (2004) P. Christoffersen and K. Jacobs. The importance of the loss function in option valuation. Journal of Financial Economics, 72:291–318, 2004.

- Cox (1975) J. Cox. Notes on option pricing I: Constant elasticity of diffusions. Working paper, 1975.

- Derman and Kani (1998) E. Derman and I. Kani. Stochastic implied trees: Arbitrage pricing with stochastic term and strike structure of volatility. International Journal of Theoretical and Applied Finance, 1(1):61–110, 1998.

- Dupire (1994) B. Dupire. Pricing with a smile. Riks, 7(1):18–20, 1994.

- Foschi et al. (2013) P. Foschi, S. Pagliarani, and A. Pascucci. Black–Scholes formulae for Asian options in local volatility models. Journal of Computational and Applied Mathematics, 237:442–459, 2013.

- Giese (2012) A. Giese. Quanto adjustments in the presence of stochastic volatility. Risk, pages 67–71, May 2012.

- Gobet and Bompis (2014) E. Gobet and R. Bompis. Stochastic approximation finite element method for analytical approximation of multidimensional diffusion process. SIAM Journal on Numerical Analysis, 52:3140–3164, 2014.

- Gobet and Hok (2014) E. Gobet and J. Hok. Expansion formulas for bivariate payoffs with application to best-of options on equity and inflation. International Journal of Theoretical and Applied Finance, 17(2):1450010, 2014.

- Gobet and Miri (2014) E. Gobet and M. Miri. Weak approximation of averaged diffusion processes. Stochastic Processes and their Applications, 124:475–504, 2014.

- Hagan and Woodward (1999) P. Hagan and D. Woodward. Equivalent Black volatilities. Applied Mathematical Finance, 6:147–157, 1999.

- Henry-Labordère (2005) P. Henry-Labordère. A general asymptotic implied volatility for stochastic volatility models. Preprint, arXiv:0504317, 2005.

- Hull and Suo (2002) J. Hull and E. Suo. A methodology for assessing model risk and its application to the implied volatility function model. Journal of Financial and Quantitative Analysis, 37:297–318, 2002.

- Hull and White (2000) J. Hull and A. White. Forward rate volatilities, swap rate volatilities, and the implementation of the LIBOR market model. The Journal of Fixed Income, 10(2):46–62, 2000.

- Jäckel (2008) P. Jäckel. Hyperbolic local volatility. Preprint, www.jaeckel.org, 2008.

- Jäckel (2016) P. Jäckel. Quanto skew. Preprint, www.jaeckel.org, 2016.

- Kunita (1997) H. Kunita. Stochastic Flows and Stochastic Differential Equations. Cambridge University Press, 1997.

- Kunitomo and Takahashi (2004) N. Kunitomo and A. Takahashi. Applications of the asymptotic expansion approach based on Malliavin-Watanabe calculus in financial problems. In S. Watanabe, editor, Stochastic Processes and Applications to Mathematical Finance, pages 195–232. World Scientific, 2004.

- Musiela and Rutkowski (2005) M. Musiela and M. Rutkowski. Martingale Methods in Financial Modelling. Springer, 2nd edition, 2005.

- Ng and Sun (2008) K. H. Ng and Y. Sun. Risk management with the CEV LIBOR market model. Preprint, SSRN:497462, 2008.

- Nualart (2005) D. Nualart. The Malliavin Calculus and Related Topics. Springer, 2005.

- Pagliarani and Pascucci (2012) S. Pagliarani and A. Pascucci. Analytical approximation of the transition density in a local volatility model. Cent. Eur. J. Math., 10(1):250–270, 2012.

- Pellser (2000) A. Pellser. Efficient Methods for Valuing Interest Rate Derivatives. Springer, 2000.

- Priouret (2005) P. Priouret. Introduction aux processus de diffusion. Course for Master de Sciences et Technologies, 2005.

- Reiner (1992) E. Reiner. Quanto mechanics. Risk, 5(3):59–63, 1992.

- Ren et al. (2007) Y. Ren, D. Madan, and M. Qian. Calibrating and pricing with embedded local volatility models. Risk, pages 138–143, September 2007.

- Romo (2012) J. M. Romo. The quanto adjustment and the smile. Journal of Futures Markets, 32:877–908, 2012.

- Rubinstein (1994) M. Rubinstein. Implied binomial trees. Journal of Finance, 49:771–818, 1994.

- Schlögl (2002) E. Schlögl. A multicurrency extension of the lognormal interest rate market models. Finance and Stochastics, 6:173–196, 2002.

- Takahashi (1995) A. Takahashi. Essays on the Valuation Problems of Contingent Claims. PhD thesis, University of California, Berkeley, 1995.

- Takahashi (1999) A. Takahashi. An asymptotic expansion approach to pricing financial contingent claims. Asia-Pacific Financial Markets, 6(2):115–151, 1999.

- Takahashi (2015) A. Takahashi. Asymptotic expansion approach in finance. In P. K. Friz, J. Gatheral, A. Gulisashvili, A. Jacquier, and J. Teichmann, editors, Large Deviations and Asymptotic Methods in Finance, pages 345–411. Springer, 2015.

- Vong and Rojas-Carulla (2014) G. Vong and M. Rojas-Carulla. Quanto derivatives in local volatility models. Presentation at Global Derivatives, SSRN:2512510, 2014.

- Yoshida (1992) N. Yoshida. Asymptotic expansions for statistics related to small diffusions. Journal of the Japan Statistical Society, 22:139–159, 1992.