Estimation and Inference of Treatment Effects with L2-Boosting in High-Dimensional Settings

Abstract. Empirical researchers are increasingly faced with rich data sets containing many controls or instrumental variables, making it essential to choose an appropriate approach to variable selection. In this paper, we provide results for valid inference after post- or orthogonal -Boosting is used for variable selection. We consider treatment effects after selecting among many control variables and instrumental variable models with potentially many instruments. To achieve this, we establish new results for the rate of convergence of iterated post--Boosting and orthogonal -Boosting in a high-dimensional setting similar to Lasso, i.e., under approximate sparsity without assuming the beta-min condition. These results are extended to the 2SLS framework and valid inference is provided for treatment effect analysis. We give extensive simulation results for the proposed methods and compare them with Lasso. In an empirical application, we construct efficient IVs with our proposed methods to estimate the effect of pre-merger overlap of bank branch networks in the US on the post-merger stock returns of the acquirer bank.

Key words: -Boosting, inference, treatment effects, instrumental variables, post-selection inference, high-dimensional data.

1. Introduction

Boosting algorithms are popular in machine learning and have proven to be useful for prediction and variable selection (Bühlmann and Hothorn (2007)). Nevertheless, in many applications, researchers are interested in inference on pre-specified variables, and this requires a different approach. Often these variables are so-called treatment or policy variables that researchers would like to learn and make inferences about, particularly in high-dimensional settings.

It is well-known that inference after model selection may lead to invalid results when the selection step is not taken into account or safeguarded against. For an overview of the pitfalls and challenges of post-selection inference in general, we refer to Leeb and Pötscher (2005). In this paper, we describe our approach to address this issue. First, we substantially extend the techniques in Luo and Spindler (2016) to provide a set of novel convergence results on iterated post--Boosting and orthogonal -Boosting. These results are derived under approximate sparsity and without assuming the beta-min condition. Second, we provide results for valid inference in high-dimensional settings in which post- or orthogonal -Boosting is applied for variable selection and estimation. For this, we combine the convergence results with the techniques of orthogonalized moment conditions as described in Chernozhukov et al. (2016).

Boosting has proven very valuable for prediction. We show in this paper that it can also be applied to (causal) inference. In particular, we consider the case of the estimation of a treatment effect with many control variables, and the case of instrumental variable (IV) estimation such as two stage least squares procedure with many potential instruments. The first case can also be interpreted as estimation and inference on a prespecified variable in a high-dimensional linear regression model estimated with -Boosting, where all other variables are considered as nuisance variables. As the first ingredient of our estimation method, it relies on the so-called orthogonalized or Neyman moment conditions. This theory was developed by Belloni, Chernozhukov, Hansen, and coauthors in a series of papers. The case of instrumental variables is analyzed in Belloni et al. (2012), and the treatment effect case in Belloni, Chernozhukov and Hansen (2014). Papers with extensions of the general idea are Chernozhukov et al. (2016) and Chernozhukov, Hansen and Spindler (2015). The second ingredient is rates of convergence that are fast enough to estimate the nuisance part of the orthogonal moment condition. Our results only rely on the standard assumptions in the high-dimensional literature, and nearly-Lasso convergence rates are derived for the iterated post--Boosting (-) and orthogonal -Boosting () algorithms. In addition, a data-driven early stopping criterion is proposed and we show that such stopping criterion achieves nearly-Lasso convergence rate under our assumptions. These results might be of independent interest since Boosting is widely used and the results for Boosting in the high-dimensional case under such weak assumptions have been missing in the literature to date.

Additionally, we conduct extensive simulation studies and compare the Boosting algorithm with Lasso in various high-dimensional settings. These results might give guidance to empirical researchers to decide when to choose which algorithm. We conclude that -Boosting with a theoretical-grounded stopping criterion is the more efficient method with respect to computation time and also provides the best estimation accuracy in our simulation study. We also show the computational advantage of -Boosting over Lasso by comparing the CPU time in a high-dimensional (causal) inference framework. Finally, we conduct an empirical analysis of how the pre-merger overlap of bank branch networks in the United States can affect the post-merger stock returns of acquirer banks. In this setting, many potential instrumental variables are available. We show how -Boosting can be used to select these in a data-driven, principled way and to estimate the treatment effect of interest.

Boosting algorithms are one of the major recent advances in machine learning and statistics. One of the earliest examples is Freund and Schapire’s AdaBoost algorithm for classification (Freund and Schapire (1997)), which has led to numerous variants that have proven to be competitive in terms of their prediction accuracy in a variety of applications and their strong resistance to overfitting as shown in Bühlmann and Hothorn (2007). Boosting methods were originally proposed as ensemble methods, which rely on the principle of generating multiple predictions and majority voting (averaging) of the individual classifiers. An important development in the analysis of Boosting algorithms was Breiman’s interpretation of Boosting as a gradient descent algorithm in a function space (Breiman (1996), Breiman (1998)), inspired by numerical optimization and statistical estimation. Building on this insight, Friedman, Hastie and Tibshirani (2000) and Friedman (2001) embedded Boosting algorithms into the framework of statistical estimation and additive basis expansion. This also enabled Boosting to be applied to regression analysis. Boosting for regression was proposed by Friedman (2001), and then Bühlmann and Yu (2003) defined and introduced -Boosting. Zhang and Yu (2005) show the consistency of -Boosting and derive the rate of convergence in low-dimensional settings, and Bühlmann et al. (2006) show the consistency of -Boosting in high-dimensional settings without stating the rate. Luo and Spindler (2016) derive rates for boosting and variants in high dimensions under a beta-min condition and exact sparsity assumption. An extensive overview of the development of Boosting and its manifold applications is given in Bühlmann and Hothorn (2007).

The paper is structured as follows: In Section 2, we discuss the problem of estimating treatment effects in high-dimensional settings. In Section 3, we introduce -Boosting and two variants. In Section 4, we present the formal results for the predictive performance of Boosting and for valid inference on (low-dimensional) treatment effects in a possibly high-dimensional setting. In Sections 5 and 6, we provide a simulation study and an empirical application. Finally, we conclude in Section 7. Proofs and additional results of the simulation study are available in Appendices A and B.

2. Estimation of Treatment Effects in High Dimensions

The goal is to estimate the treatment effect of a treatment variable on an outcome variable in a high-dimensional regression model, namely

| (1) |

where denotes the intercept and a statistical error term. The coefficient of treatment variable is the treatment effect of interest. There are two reasons for including covariates in model (1) for the estimation of the treatment effect. First, in randomized control trials the treatment variable is assigned randomly, and additional covariates improve the precision of the estimate of the average treatment effect. This argument has already been made in Cox (1958) and, more recently, Lin (2013). Second, in observational studies, covariates might be need to be included to establish unconfoundedness, in order to ensure that . This means that given the variables , the treatment can be regarded as if it had been randomly assigned and there are no unobserved confounders, as described in Imbens and Rubin (2015).

A related question is that of which variables to include in model (1) from a set of potential covariates. In high-dimensional settings, when the number of covariates is larger than the sample size , variable selection is inevitable because the least squares estimate is not well defined. Even when is smaller than but the ratio for some positive constant , ordinary least squares estimates are unreliable and, again, variable selection is needed because including too many (noisy) covariates might overfit and disguise the true treatment effect. In the empirical study in Section 6, we analyze how the pre-merger overlap of bank branch networks in the US affects the post-merger stock returns of acquirer banks. The data set contains 442 observations and 153 potential instrumental variables, comprising a high-dimensional setting in which variable selection is needed in the first-stage regression.

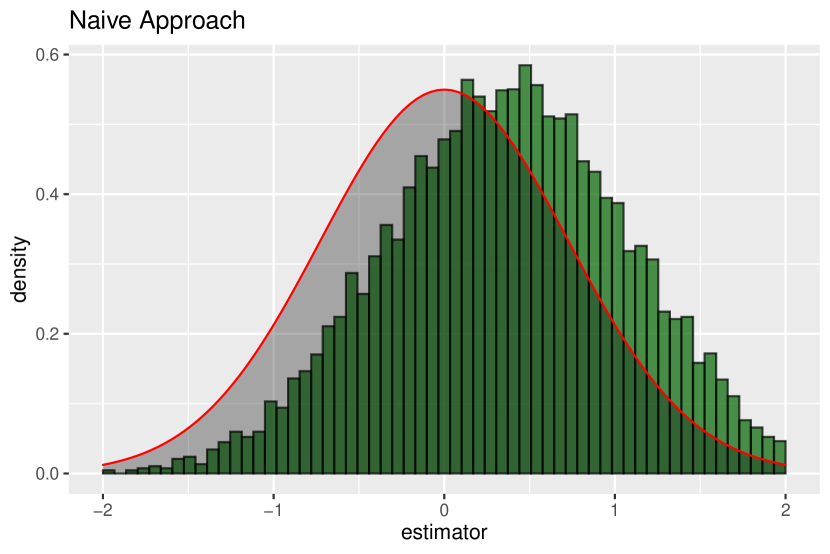

In a naive approach to estimating the treatment effect in model (1), one might first select the relevant covariates by using classical -tests or modern machine learning methods, such as Lasso or -Boosting, and then estimate the treatment effect by including only the selected variables and continue with standard inference methods. However, this procedure, while often used in applied work, might fail to provide valid post-selection inference. This is because many modern methods like Lasso or Boosting yield consistent model selection only under very strong assumptions that are often unrealistic, particularly in applications in economics.

In general, machine learning methods may miss key variables that are moderately correlated with the outcome but highly correlated with the treatment variable. Although this does not hurt predictive performance, it introduces an omitted variable bias that leads to invalid post-selection inference.

We demonstrate this by a simple simulation study with a binary treatment variable and covariates. The data generating process is given by

with for . The high-dimensional coefficient vectors and are sparse with and , respectively. The noise is normally distributed with and following a standard logistic distribution. For the high-dimensional vector , we set

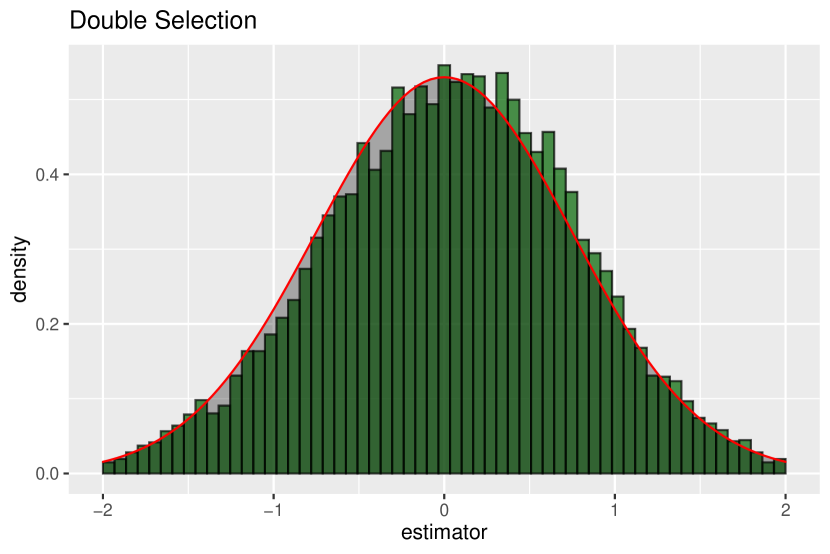

The results for repetitions of the estimate are displayed in Figure 1. The resulting distribution using the naive approach is highly biased, shows heavy tails and is not in line with a standard normal distribution (see Figure 1(b)).

To deal with such a problem and provide valid post-selection inference, we apply the double selection approach, which is described in detail in Section 4.2.1 and implicitly creates an orthogonal moment condition. Figure 1(a) shows the empirical distribution of the estimates when employing the double selection methods introduced in Belloni, Chernozhukov and Hansen (2014) and reviewed and extended in Chernozhukov et al. (2016). The estimates are nearly unbiased and can be approximated by a normal distribution. The intuition of the double selection method is that it cures the omitted variable bias seen with machine learning methods by running an auxiliary regression/step. This is equivalent to using an orthogonal moment function. This property means that estimating the nuisance parameters with machine learning methods and plugging it into the moment function has no first order effect on the estimation of the target parameter, as long as the machine learning estimator does not converge too slowly.

3. L2-Boosting

In this section, we describe the -Boosting algorithm, namely the original Boosting algorithm for regression defined in Bühlmann and Yu (2003) and two variants thereof (iterated post--Boosting and orthogonal -Boosting).

3.1. L2-Boosting

To define the Boosting algorithm for linear models, we consider the following regression setting:

| (2) |

where is a vector that consists of predictor variables. is a -dimensional coefficient vector and is a random, zero-mean error term with . We allow the dimension of the predictors to grow with the sample size . Also, the case is allowed. In this setting, a so-called sparsity condition is unavoidable. This means that there is a large set of potential variables, but the number of variables that have non-zero coefficients, denoted by , is small compared to the sample size, i.e., . In our theoretical analysis, we weaken this assumption to approximate sparsity. In the rest of this paper, we drop the dependence of on the sample size and denote it by so no confusion will arise. Let denote the design matrix where the single observations form the rows of . Let denote the th column of the design matrix, and is the th component of the vector . For a set , we define as the submatrix of with respect to column indices in . We assume a fixed design with for all and for absolute constants . Without loss of generality, we consider standardized regressors, i.e., and for . Further assumptions will be imposed in the next sections.

The basic principle of -Boosting is as follows: The criterion function that we want to minimize is the sum of squared residuals, as is the case with ordinary least squares (OLS). We initialize the estimator to zero (strictly speaking, a -dimensional vector consisting of zeros) and subsequently calculate the residuals, which in this case are equivalent to the observations in this first step. Then, we conduct univariate regressions by regressing the residuals (in the first round, the observations) on each of the regressors separately, resulting in univariate regressions. After this, we select the variable that explains most of the residuals and update the coordinate of our estimated coefficient vector in this direction. The above procedure is repeated until some stopping criterion is reached. The algorithm for -Boosting with componentwise least squares is given below.

-

(1)

Start/ initialization: (-dimensional vector), , set maximum number of iterations and set iteration index to .

-

(2)

At the step, calculate the residuals .

-

(3)

For each predictor variable , calculate the correlation with the residuals:

Select the variable that is most correlated with the residuals, i.e.,

-

(4)

Update the estimator: , where is the th index vector, , and .

-

(5)

Increase by one. If , continue with (2); otherwise stop.

The version above and the orthogonal version, introduced later, are also known in deterministic settings as the pure greedy algorithm (PGA) and the orthogonal greedy algorithm (OGA), respectively. Boosting is a gradient descent method. In the -case, the gradient of squared loss equals the residuals, and the residuals are iteratively fitted by a so-called base learner – here, componentwise univariate regressions. Hence the gradient is approximated in each step by a simple parametric model, namely a univariate linear model. In the low-dimensional case, the estimator converges to the OLS solution. In the high-dimensional case, overfitting can occur in the absence of the stopping criteria because the algorithms will ultimately build a model that explains all the variances in .

The act of stopping is crucial for Boosting algorithms because stopping too late or never stopping leads to overfitting, and therefore some kind of penalization is required. A suitable solution is to stop early, i.e., before overfitting takes place. Early stopping can be considered an unusual penalization/regularization scheme. Similar to Lasso, early stopping might induce a bias through shrinkage. A potential way to decrease the bias is to perform the post--Boosting approach defined in the next section.

3.2. Post- and Orthogonal L2-Boosting

Post--Boosting () is a post-model selection estimator that applies ordinary least squares (OLS) to the model selected by -Boosting in the first step. To formally define this estimator, we make the following definitions: and , which are the support of the true model and the support of the model estimated by -Boosting as described in Algorithm 1 stopping at . Further, denotes the complement of a set with regard to .

In the context of Lasso, OLS after model selection was analyzed in Belloni and Chernozhukov (2013). Given the above definitions, the post-model selection estimator or post--Boosting estimator takes the form

| (3) |

where denotes the squared sum of residuals defined as .

In our theoretical analysis, we consider a modified version of post--Boosting called iterated post--Boosting (-), which is given in Algorithm 2 below. Instead of one final projection, a projection is conducted regularly, described by a sequence ,

-

(1)

Given a sequence , . Start/ initialization: (-dimensional vector), , set maximum number of iterations and set iteration index to .

-

(2)

At the step, calculate the residuals , for .

-

(3)

For each predictor variable , calculate the correlation with the residuals:

Select the variable that is the most correlated with the residuals, i.e.,

-

(4)

If , update the estimator according to gradient descent: , where is the th index vector and .

-

(5)

If , perform post--Boosting: Define with .

-

(6)

Increase by one. If , continue with (2); otherwise stop.

Another variant of the Boosting algorithm is orthogonal Boosting (), described in Algorithm 3, or the OGA in its deterministic version. Only the updating step is changed in comparison to Algorithm 1. In every step, an orthogonal projection of the response variable is carried out on all the variables that have been selected up to that point. The advantage of this method is that any variable is selected at the most once in this procedure, whereas in the previous version the same variable might be selected at different steps making the analysis much more complicated. More formally, the method is described in Algorithm 3 by modifying step (4) in Algorithm 1.

-

(1)

Start/ initialization: (-dimensional vector), , set maximum number of iterations and set iteration index to .

-

(2)

At the step, calculate the residuals , for .

-

(3)

For each predictor variable , calculate the correlation with the residuals:

Select the variable that is most correlated with the residuals, i.e.,

-

(4)

Update the estimator: , with and .

-

(5)

Increase by one. If , continue with (2); otherwise stop.

As mentioned, early stopping is crucial for Boosting to avoid overfitting. Therefore, in the last step of Algorithms 1, 2 or 3, an early stopping criteria is needed. The standard approaches for determining the “optimal” stopping time are cross-validation and a corrected Akaike information criterion (Bühlmann (2006)). Although both lack a theoretical foundation in a high-dimensional setting, they are applied by practitioners and often give competitive results. We provide a data-driven early stopping criterion later in Section 4, first developed in Luo and Spindler (2016), with beta-min condition and exact sparsity needed for guaranteeing theoretical performance. In this paper, we prove the nearly-Lasso convergence rate of such early stopping criterion without the strong beta-min and exact sparsity conditions. We demonstrate the good performance of such early stopping criterion in our simulation study.

3.3. Computational Perspective and Comparison to Lasso

Friedman, Hastie and Tibshirani (2001) were the first to point out a strong relationship between -Boosting with componentwise linear least squares and Lasso. Although these methods are generally not equivalent, Efron et al. (2004) proved an approximate equivalence between -Boosting and Lasso and confirmed that -Boosting and Lasso are closely related. Compared to Lasso, Boosting uses an unusual “penalization scheme” by early stopping. -Boosting can therefore be interpreted as an approximate and implicit regularized optimization, whereas Lasso directly solves a complex penalized optimization problem.

In this paper, we show that iterated post--Boosting and orthogonal -Boosting achieve nearly the same rate of convergence as Lasso in a high-dimensional linear regression model. This aligns with the work of Bühlmann and Hothorn (2007) who did not find Lasso to be superior overall to -Boosting (or vice versa) in terms of empirical performance for prediction. More recently, Hepp et al. (2016) also performed an extensive simulation study comparing -Boosting and Lasso. Their results suggest that in high-dimensional settings when , Boosting has a slight advantage in terms of prediction accuracy, whereas Lasso leads, on average, to sparser models. They also point out that the amount of regularization imposed on the models clearly determines the quality of the estimation methods.

Next, we extend these results and perform simulation studies that compare -Boosting and Lasso within advanced inferential procedures in high-dimensional linear regression models. A simulation of this nature is lacking in the literature and in general little is known about the empirical performance and computation time of machine learning methods in causal/inferential settings (see, for example, Knaus (2020)). As discussed, -Boosting solves univariate regressions and is therefore computationally efficient and feasible in high dimensions, having a linear complexity in the number of predictor variables (cf. Bühlmann et al. (2006), Mayr et al. (2014)). The computational complexity of -Boosting, including - and , is , where denotes the number of steps. Lasso has a computational complexity of , where (cf. Efron et al. (2004)). This leads to a computational superiority of -Boosting over Lasso in high-dimensional settings if . This phenomenon has been observed in Bühlmann and Hothorn (2007) who compare the computing time of -Boosting to that of Lasso in high-dimensional regressions. Boosting is employed in practice in cases where explicitly solving regularized optimization problems is not practical. This usually happens in very high-dimensional settings when , see, e.g., Efron et al. (2004). In our simulation studies in Section 5, we confirm the computational advantage of Boosting over Lasso by comparing the CPU time in high-dimensional (causal) inference settings. Such advantage can be substantial when and become large.

Moreover, in settings where the number of observations is very large (“big data”), an advantage of -Boosting is that the estimation can be easily parallelized and distributed to different cores (e.g. CPUs) or machines. It is a gradient based method. In each step, univariate regressions are calculated and are independent of each other and hence can be computed in a distributed fashion. This allows for efficient implementation and the application to big data.

4. Main Results

In this section, we provide the theoretical results of our paper, including novel results on the convergence rate of iterated post--Boosting (-) and orthogonal -Boosting () in subsection 4.1. Note that, compared to existing literature, the results rely only on approximate sparsity, and no beta-min condition is required. Based on these results, we present, in subsection 4.2, inference results for treatment effects in a setting with high-dimensional controls and in an instrumental variable model.

4.1. New Results on Boosting

Consider the following high-dimensional approximate sparse linear regression model

where denotes the approximation error of the sparse model and is i.i.d. across with variance .111In this subsection we consider homoscedastic error terms. Our proofs can be easily generalized to heteroscedastic errors. We assume the following conditions to establish new rates of convergence for -Boosting:

Assumption 1 (Approximate Sparsity).

-

(i)

;

-

(ii)

for some generic constant and defined in Assumption 3;

-

(iii)

There exists a constant such that .

For the next assumption, we first define the smallest and largest restricted eigenvalues of a matrix:

Definition 1.

The smallest and largest restricted eigenvalues of matrix with size is defined as:

where and denote the smallest and largest eigenvalues of matrix and is the set of all -dimensional square diagonal-submatrices of .

Assumption 2 (SE).

Consider the Gram matrix . Assume that all the elements on the diagonal of are equal to one. We assume that there exist positive constants and such that

holds for , where is a sequence such that slowly along with and , where is a large enough generic constant.

Comment 2.

This condition is standard for Lasso and other machine learning methods in a high-dimensional setting. It allows for a more general behavior requiring only that the sparse eigenvalues of the Gram matrix are bounded from above and away from zero. A standard assumption in traditional econometric research is to assume that the (population) Gram matrix has eigenvalues bounded from above and away from zero. The condition is fulfilled for many relevant designs. For various examples, we refer to Belloni and Chernozhukov (2013). An extensive overview of different conditions on matrices and how they are related is given in Van De Geer and Bühlmann (2009).

Next, we require the following assumption on the tails of and :

Assumption 3 (Tails).

For any small enough, with probability , we have:

where denotes the empirical inner product of two vectors with size . In addition, we require that satisfies that

for some small enough fixed constant .

Comment 3.

Assumption 3 holds, for example, if the error terms are i.i.d. normally distributed random variables. This in turn can be generalized/weakened to cases of non-normality by self-normalized random vector theory (de la Peña, Lai and Shao, 2009) or the approach introduced in Chernozhukov, Chetverikov and Kato (2014).

For the theoretical analysis, first, we consider the (iterated) Post--Boosting algorithm that is defined in Algorithm 2.

Theorem 1 (Convergence of iterated-pBA (-)).

Consider Algorithm 2. Suppose that the sequence satisfies the condition that if and only if for a positive integer and , where is a fixed positive constant. Suppose the Assumptions 1-3 hold with for some large enough constant . Let be a constant such that with such that

Suppose that the growth condition holds. Then, for large enough, with probability , the iterated post--Boosting algorithm satisfies:

| (4) |

and

| (5) |

Comment 4.

Theorem 1 shows that the iterated post--Boosting algorithm nearly achieves the Lasso rate of convergence . This algorithm implements post--Boosting iteratively and therefore, it shares the computational advance of the standard . The additional factor in the convergence rate result is inevitable due the nature of iterative algorithms like - in the absence of beta-min conditions: in the best case, the - algorithm and others alike will have convergence on at step for some fixed constant . To accommodate that can grow with and there can exist small coefficients in , the number of iterations must be at least of order in order to have either (1) the variables with small coefficients are already selected, or (2) the unselected variables’ corresponding coefficients must be small enough. The additional term can be removed if certain beta-min conditions are imposed. It’s not clear to us and in the literature if the standard algorithm achieves the same rate of convergence under these mild assumptions and therefore, more restrictive growth conditions are required for unless strong conditions such as the beta-min condition are employed.

Corollary 1 (- Stopping Criterion).

Assume that all assumptions in Theorem 1 hold. Consider the stopping criteria such that the Algorithm 2 stops at the first such that:

where is a fixed positive constant. Denote such as . Suppose is large enough such that , where is a generic constant defined in (77) in the Appendix. Then, with probability , we have that: . In addition, (4) and (5) hold when replacing with .

Comment 5.

Corollary 1 is a natural extension of Theorem 1. It provides a practical stopping criteria that achieves the same rate as stopping at . In practice, could be much smaller than . is a tuning parameter that is similar to the penalty of Lasso. When becomes larger, the algorithm stops earlier, leading to smaller number of iterations in the algorithm. In practice, we recommend to pick as a rule of thumb, which is used in the simulation.

The next theorem provides the same rates of convergence for the orthogonal -Boosting () algorithm that has also been defined in Section 3.

Theorem 2 (Convergence of orthogonal -Boosting ()).

Comment 6.

Again, it is worth noting that neither exact sparsity nor the beta-min condition are required to show the results in Theorem 2. Therefore, this theorem is a strong generalization of previous results in the literature.

Corollary 2 ( Stopping Criterion).

Assume that all assumptions in Theorem 2 hold. Consider the stopping criteria such that the Algorithm 3 stops at the first such that:

where is a fixed positive constant. Denote such as . Suppose is large enough such that , where is a constant defined in (77). Then, with probability , we have that: . In addition, (6) and (7) hold when replacing with .

4.2. Inference for Treatment Effects

In this section, we present inference results for treatment effects using -Boosting. We first consider the case in which a researcher is interested in estimating the treatment effect of a treatment variable after selecting among many control variables as discussed in Section 2. Then, we provide new results for inference in an instrumental variable model with potentially many instruments when post- or orthogonal -Boosting is used for the variable selection. Essential ingredients for valid inference in these settings are the rates of convergence of -Boosting that have been provided in the previous subsection.

4.2.1. Inference Results after Selecting among Many Controls

We consider the model

| (8) | |||||

| (9) |

where and are approximation errors, . The estimation method consists of the following three steps, the first two of which involve model selection with -Boosting:

-

(1)

Run an iterated post- or orthogonal -Boosting regression of on . The set of variables that is selected will be denoted by .

-

(2)

Run an iterated post- or orthogonal -Boosting regression of on . The set of variables that is selected will be denoted by .

-

(3)

Run an OLS regression of on the treatment variable and the set of variables selected in the first two steps. This set can be augmented by additional variables.

The estimated regression coefficient of the treatment variable in step (3) above is the double selection estimator . To analyze this estimator based on -Boosting, we impose the following assumptions:

A. 1.

A. 2.

We assume that for any , where is a sequence such that slowly along with , and , for some large enough constant .

A. 3.

With probability greater or equal , we have

for and with and for fixed .

A. 4.

There exists an absolute constant such that

. Further, it holds that a.s. and for all , where and are some generic positive constants.

It holds that

-

(a)

, and

-

(b)

.

Assumptions A.1–A.3 allow us to apply Theorem 1 and Theorem 2 to ensure sufficiently fast estimation rates for -Boosting in models (8) and (9). Assumption A.4 (i) imposes weak technical conditions on the moments of the error terms to allow for valid inference. Assumption A.4 (ii) restricts the growth of the number of parameters. Moreover, we assume that, in the -Boosting algorithms, early stopping takes place. This ensures that the conditions for the stopping time in Theorem 1 and Theorem 2 are satisfied. With these assumptions, we can now formulate our first main theorem regarding inference.

Theorem 3.

The proof of Theorem 3 is given in Appendix A. This result can be used to conduct valid inference on the regression coefficient . The construction of uniformly valid confidence intervals is given in the following corollary.

Corollary 3.

Let the collection of all data generating processes for which the assumptions of Theorem 3 hold for given . Further, let be the collection of data-generating processes for which the conditions above hold for all , and define . The confidence regions based upon and are uniformly valid in :

4.2.2. Inference on Treatment Effects in an Instrumental Variable Model

In this section, we consider the following instrumental variable model with potentially very many instruments

with instrument function . Again, we allow for approximate sparsity in the second equation. For simplicity, in our technical analysis, we consider the model above without controls in the first equation and a regular fix design with observations :

| (11) | |||||

| (12) |

To estimate the coefficient of the endogenous treatment variable, we employ the following two-stage least squares (2SLS) procedure: In the first step, we estimate and predict the instrument by iterated post- or orthogonal -Boosting. Finally, we estimate by regressing the outcome variable on the predicted instrument . To analyze this estimator based on -Boosting, we impose the following assumptions:

B. 1.

B. 2.

We assume that for any , where is a sequence such that slowly along with , and for some large enough positive constant .

B. 3.

With probability greater or equal , it holds for and for .

B. 4.

There exists an absolute constant such that

. Furthermore, it holds that for all , where and are absolute positive constants.

It holds that

-

(a)

.

Assumptions B.1-B.4 are essentially the same as Assumptions A.1-A.4 except for some small modifications in B.4 related to the different underlying setting in subsection 4.2.1. It is worth noting that the growth condition B.4(ii) is slightly weaker than the growth condition A.4(ii) because Assumption A.4(ii) implies Assumption B.4(ii). Assumption A.1(ii)(b) is needed to ensure consistency of the respective variance estimators. With these assumptions, we can show that the instrumental variable estimator following the two-stage least squares (2SLS) procedure is asymptotically normally distributed. This result is provided by the following theorem.

Theorem 4.

5. Simulation Study

In this section, we present simulation results for both settings.

5.1. Setting with High-Dimensional Controls

First, we consider the following i.i.d. data generating process:

| (13) | ||||

| (14) |

where . The second auxiliary equation captures the confounders. We consider two different covariance structures : First, an i.i.d. structure with being the identity matrix and secondly a structure with correlated covariates, for which we generate a Toeplitz design but then perform a random covariate rotation. The parameter of interest, , is equal to . We consider both a sparse setting (Control-1) and an approximately sparse setting (Control-2). In the sparse setting, the first coefficients are set to one and all other parameters are equal to zero. In the approximately sparse setting, the first coefficients are set to one and the remaining coefficients are declining:

The residuals and are generated independently with

to control the empirical signal-to-noise ratio (),

We vary the sample size , the number of covariates and the . The number of repetitions is . For estimation of the treatment effect we use the double selection procedure presented in Section 4.2.1. Because we use different approaches for variable selection, we are able to compare -Boosting and Lasso in terms of how capable they are in treatment effect estimation. The results are provided in subsection 5.3.

5.2. IV Estimation with Many Instruments

In the setting with many instrumental variables, we consider the following i.i.d. data generating process, which is similar to that used in the simulation experiment in Belloni et al. (2012):

| (15) | ||||

| (16) |

with

The parameter of interest is set to . The regressors are drawn from a normal distribution for the same covariance structures as in subsection 5.1. Further, we set and . Let such that the unconditional variance of the endogenous variable equals one. The first-stage coefficients are set according to . For the high-dimensional regression coefficient , we use a sparse design, i.e., with coordinates equal to one and all other equal to zero. The constant is set in such a way that we generate data with an SNR of and . This leads to the concentration parameter of size or , which determines the behavior of the instrumental variable estimators as described in Hansen, Hausman and Newey (2008). As in subsection 5.1, we also vary the sample size and the number of covariates . The number of repetitions in the simulations study is again . We subsequently employ two-stage least squares with -Boosting and Lasso to compare the performance in estimating the treatment effect in a high-dimensional setting with many instrumental variables.

5.3. Simulation Results

The results of both simulation settings described in subsection 5.1 and 5.2 are summarized in Tables 4 – 9 in Appendix B. We present the mean absolute error (MAE) of ,

the standard deviation of the estimators and the empirical rejection rates at a significance level . In our analysis, pBA refers to post--Boosting, I-pBA to the iterated version, and oBA to the orthogonal variant as in Section 3.2. Each of these uses the theoretically justified stopping criterion from Corollary 1 and Corollary 2. The Lasso method refers to the Post-Lasso estimator with theoretically justified selection of the shrinkage parameter . For comparison, we also use an implementation of Post--Boosting with cross-validated stopping (CV-pBA) as well as a Lasso implementation with cross-validated . The estimators based on -Boosting yield a low MAE throughout all these settings. On average, the methods based on -Boosting also provide empirical rejection rates that are close to the nominal level of . Compared to Lasso, the MAE provided by -Boosting is slightly lower and, on average, the empirical rejection rates are slightly closer to the nominal level of . Nevertheless, the differences in MAE between -Boosting and Lasso are all within one standard error of each other. In summary, both -Boosting and Lasso provide empirical rejection rates that are close to the nominal level of . This is in line with the theory that both -Boosting and Lasso can be used for valid estimation of treatment effects in high-dimensional settings. Further, the cross-validated methods yield a higher MAE and higher standard deviations than the methods with a theoretically justified tuning parameter. Table 1 below summarizes the results for the setting with and .

| iid covariates | correlated covariates | ||||||||||||

| Lasso | pBA | I-pBA | oBA | CV-pBA | CV-Lasso | Lasso | pBA | I-pBA | oBA | CV-pBA | CV-Lasso | ||

| p | Mean Absolute Error | ||||||||||||

| 200 | 0.033 | 0.033 | 0.035 | 0.034 | 0.037 | 0.038 | 0.035 | 0.036 | 0.035 | 0.036 | 0.038 | 0.037 | Control-1 |

| 600 | 0.033 | 0.034 | 0.037 | 0.034 | 0.042 | 0.050 | 0.035 | 0.036 | 0.035 | 0.036 | 0.041 | 0.044 | |

| 1000 | 0.037 | 0.036 | 0.036 | 0.036 | 0.049 | 0.059 | 0.036 | 0.036 | 0.036 | 0.037 | 0.044 | 0.052 | |

| 1400 | 0.038 | 0.037 | 0.038 | 0.038 | 0.050 | 0.066 | 0.038 | 0.035 | 0.035 | 0.037 | 0.048 | 0.061 | |

| 1800 | 0.042 | 0.037 | 0.039 | 0.038 | 0.053 | 0.073 | 0.041 | 0.037 | 0.037 | 0.038 | 0.050 | 0.066 | |

| 200 | 0.036 | 0.036 | 0.033 | 0.036 | 0.039 | 0.039 | 0.035 | 0.035 | 0.033 | 0.035 | 0.038 | 0.035 | Control-2 |

| 600 | 0.036 | 0.034 | 0.035 | 0.034 | 0.043 | 0.048 | 0.036 | 0.035 | 0.036 | 0.035 | 0.044 | 0.044 | |

| 1000 | 0.035 | 0.034 | 0.034 | 0.034 | 0.048 | 0.051 | 0.035 | 0.035 | 0.035 | 0.035 | 0.045 | 0.047 | |

| 1400 | 0.038 | 0.037 | 0.035 | 0.038 | 0.052 | 0.056 | 0.037 | 0.037 | 0.035 | 0.038 | 0.047 | 0.053 | |

| 1800 | 0.036 | 0.035 | 0.036 | 0.035 | 0.052 | 0.059 | 0.036 | 0.035 | 0.034 | 0.035 | 0.050 | 0.054 | |

| 200 | 0.045 | 0.044 | 0.044 | 0.044 | 0.043 | 0.044 | 0.079 | 0.079 | 0.079 | 0.078 | 0.070 | 0.077 | IV |

| 600 | 0.046 | 0.045 | 0.045 | 0.046 | 0.045 | 0.047 | 0.091 | 0.086 | 0.087 | 0.086 | 0.073 | 0.098 | |

| 1000 | 0.043 | 0.042 | 0.042 | 0.042 | 0.044 | 0.044 | 0.093 | 0.090 | 0.091 | 0.090 | 0.073 | 0.208 | |

| 1400 | 0.046 | 0.046 | 0.045 | 0.046 | 0.047 | 0.047 | 0.096 | 0.095 | 0.095 | 0.094 | 0.078 | 0.380 | |

| 1800 | 0.046 | 0.046 | 0.044 | 0.046 | 0.048 | 0.047 | 0.098 | 0.102 | 0.096 | 0.100 | 0.080 | 0.895 | |

| p | Standard Deviation | ||||||||||||

| 200 | 0.042 | 0.041 | 0.043 | 0.041 | 0.047 | 0.044 | 0.044 | 0.045 | 0.043 | 0.045 | 0.048 | 0.046 | Control-1 |

| 600 | 0.040 | 0.040 | 0.045 | 0.040 | 0.052 | 0.046 | 0.043 | 0.043 | 0.044 | 0.043 | 0.051 | 0.046 | |

| 1000 | 0.045 | 0.044 | 0.044 | 0.044 | 0.061 | 0.056 | 0.044 | 0.044 | 0.042 | 0.044 | 0.056 | 0.050 | |

| 1400 | 0.045 | 0.044 | 0.045 | 0.045 | 0.064 | 0.053 | 0.044 | 0.042 | 0.041 | 0.043 | 0.061 | 0.055 | |

| 1800 | 0.047 | 0.044 | 0.044 | 0.045 | 0.068 | 0.059 | 0.044 | 0.043 | 0.044 | 0.044 | 0.063 | 0.053 | |

| 200 | 0.043 | 0.043 | 0.043 | 0.043 | 0.048 | 0.045 | 0.044 | 0.044 | 0.043 | 0.044 | 0.049 | 0.045 | Control-2 |

| 600 | 0.044 | 0.044 | 0.044 | 0.044 | 0.054 | 0.054 | 0.044 | 0.044 | 0.044 | 0.044 | 0.055 | 0.050 | |

| 1000 | 0.044 | 0.043 | 0.043 | 0.043 | 0.059 | 0.054 | 0.044 | 0.043 | 0.043 | 0.044 | 0.057 | 0.051 | |

| 1400 | 0.048 | 0.046 | 0.044 | 0.047 | 0.065 | 0.060 | 0.046 | 0.046 | 0.044 | 0.047 | 0.060 | 0.054 | |

| 1800 | 0.045 | 0.043 | 0.044 | 0.043 | 0.063 | 0.058 | 0.046 | 0.045 | 0.043 | 0.045 | 0.062 | 0.054 | |

| 200 | 0.056 | 0.054 | 0.054 | 0.055 | 0.052 | 0.055 | 0.097 | 0.095 | 0.094 | 0.093 | 0.080 | 0.093 | IV |

| 600 | 0.057 | 0.057 | 0.057 | 0.057 | 0.053 | 0.056 | 0.112 | 0.105 | 0.106 | 0.105 | 0.076 | 0.195 | |

| 1000 | 0.053 | 0.053 | 0.052 | 0.053 | 0.048 | 0.052 | 0.114 | 0.106 | 0.107 | 0.106 | 0.072 | 0.782 | |

| 1400 | 0.057 | 0.058 | 0.057 | 0.057 | 0.051 | 0.057 | 0.119 | 0.115 | 0.111 | 0.114 | 0.079 | 2.407 | |

| 1800 | 0.057 | 0.058 | 0.056 | 0.058 | 0.052 | 0.057 | 0.117 | 0.119 | 0.113 | 0.117 | 0.077 | 5.709 | |

| p | Rejection Rate | ||||||||||||

| 200 | 0.056 | 0.058 | 0.064 | 0.056 | 0.048 | 0.070 | 0.064 | 0.072 | 0.066 | 0.072 | 0.064 | 0.072 | Control-1 |

| 600 | 0.052 | 0.050 | 0.088 | 0.052 | 0.032 | 0.184 | 0.062 | 0.072 | 0.060 | 0.074 | 0.046 | 0.126 | |

| 1000 | 0.082 | 0.076 | 0.072 | 0.072 | 0.062 | 0.268 | 0.064 | 0.074 | 0.058 | 0.072 | 0.056 | 0.186 | |

| 1400 | 0.080 | 0.076 | 0.086 | 0.084 | 0.052 | 0.314 | 0.074 | 0.064 | 0.062 | 0.068 | 0.060 | 0.248 | |

| 1800 | 0.110 | 0.078 | 0.072 | 0.086 | 0.060 | 0.358 | 0.104 | 0.082 | 0.070 | 0.098 | 0.044 | 0.312 | |

| 200 | 0.066 | 0.056 | 0.060 | 0.050 | 0.048 | 0.076 | 0.070 | 0.074 | 0.060 | 0.068 | 0.074 | 0.068 | Control-2 |

| 600 | 0.062 | 0.064 | 0.060 | 0.064 | 0.062 | 0.176 | 0.074 | 0.068 | 0.054 | 0.060 | 0.054 | 0.124 | |

| 1000 | 0.080 | 0.064 | 0.056 | 0.066 | 0.058 | 0.210 | 0.062 | 0.058 | 0.052 | 0.058 | 0.070 | 0.148 | |

| 1400 | 0.088 | 0.068 | 0.076 | 0.084 | 0.084 | 0.206 | 0.088 | 0.074 | 0.058 | 0.086 | 0.064 | 0.224 | |

| 1800 | 0.072 | 0.044 | 0.066 | 0.056 | 0.052 | 0.238 | 0.082 | 0.066 | 0.054 | 0.074 | 0.058 | 0.226 | |

| 200 | 0.046 | 0.042 | 0.042 | 0.044 | 0.052 | 0.048 | 0.070 | 0.070 | 0.062 | 0.072 | 0.088 | 0.074 | IV |

| 600 | 0.066 | 0.066 | 0.046 | 0.072 | 0.110 | 0.068 | 0.072 | 0.074 | 0.056 | 0.082 | 0.122 | 0.084 | |

| 1000 | 0.044 | 0.052 | 0.048 | 0.052 | 0.062 | 0.046 | 0.068 | 0.054 | 0.072 | 0.054 | 0.116 | 0.052 | |

| 1400 | 0.066 | 0.072 | 0.064 | 0.068 | 0.090 | 0.072 | 0.070 | 0.074 | 0.076 | 0.078 | 0.126 | 0.066 | |

| 1800 | 0.066 | 0.066 | 0.052 | 0.078 | 0.106 | 0.078 | 0.062 | 0.066 | 0.078 | 0.064 | 0.142 | 0.060 | |

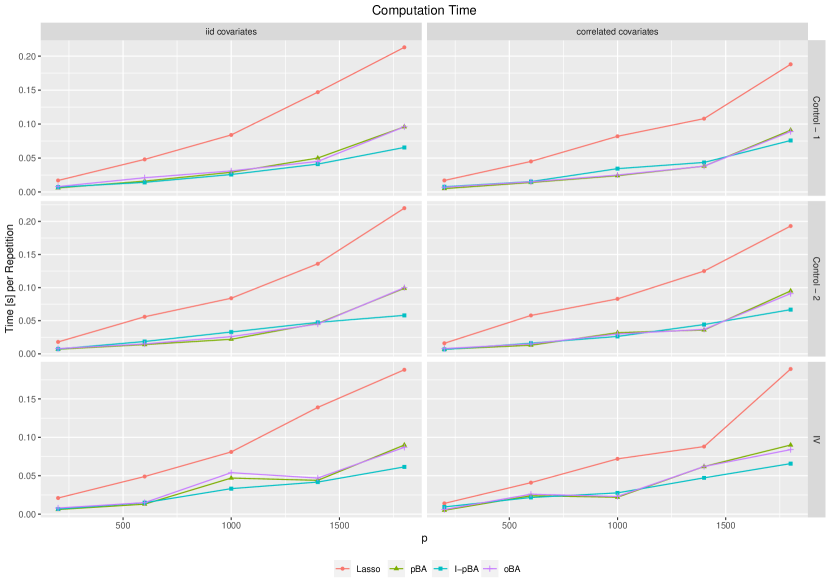

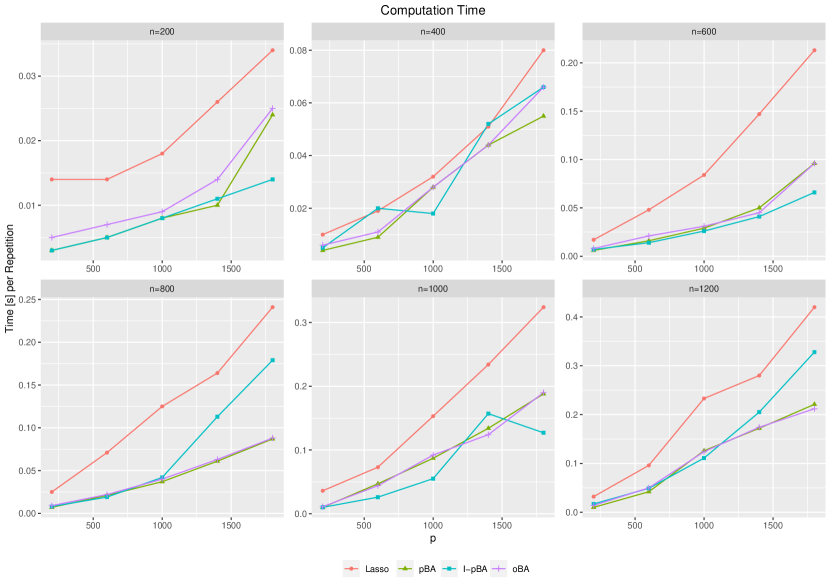

In addition, we provide the average CPU time of the proposed methods for a single iteration in Tables 4 – 9 in the Appendix B. These results refer to an implementation of all methods in Python to make the different computation times of the applied methods comparable. 222We are using the Python version 3.6.5. The operating system is Linux/Ubuntu. The hardware is Intel(R) Xeon (R) CPU E5-2650 v3 @2.30GHz. We provide the results for the setting with and again in Figure 2 below. It is clearly visible that -Boosting has a computational advantage over Lasso. For example, in the sparse setting (Control-1) for i.i.d. covariates with , post-Lasso requires a CPU time of seconds per iteration, whereas post--Boosting (pBA) takes only seconds. On average, the CPU time for Lasso is more than twice that for post-L2-Boosting. For an overview of how the computation time increases with sample size , we refer to Figure 3 in the appendix. Obviously, the methods with cross-validated penalty are significantly slower than those with a theoretically justified tuning parameter, cf. Appendix B. In summary, we conclude that -Boosting with a theoretically justified stopping criterion is the most efficient method with respect to computation time, and it also provides the best estimation accuracy in our simulation study.

6. Application: Empirical Analysis of Bank Mergers

In this section, we apply -Boosting for instrumental variable estimation in a setting with many instruments. We build on the empirical study in Levine, Lin and Wang (2020) and show how our methodology can improve IV estimation in high-dimensional settings.

6.1. Brief Introduction

We use a data set from Levine, Lin and Wang (2020), who study how the pre-merger overlap of bank branch networks in the US can affect the post-merger stock returns of acquirer banks over the period 1984 to 1995. The target variable of interest is the cumulative abnormal returns (CAR) of the acquirer bank within a window of five days around the announcement of the acquisition, denoted CAR(-2,2).333Acquirer CAR(-2, 2) is the 5-day CAR (cumulative abnormal returns) during the window (-2, +2), where day 0 is the announcement date of the acquisition. Abnormal returns are defined by using the difference between actual and projected returns. For a definition of the projected returns we refer to Levine, Lin and Wang (2020).

We are interested in estimating the causal effect of the overlap of bank branch networks on the outcome of the acquisition, i.e., CAR(-2,2). This overlap is measured by three variables, namely the Overlap, Correlation, and Cosine Distance. The Overlap variable is measured as the quotient of the number of states in which both banks are present and the total number of states in which at least one bank is present. Correlation and Cosine Distance are derived from the vector for each bank, which denotes if they are present in each state. For details on the construction of the three measurements of bank branch network overlap, we refer to Levine, Lin and Wang (2020). Additionally, 13 variables are available as controls.444The covariates are: Acquirer run-up (-200, -11), Acquirer Net Income, Acquirer Tobin’s Q, Deal size adjusted by Acquirer Assets, Cash deal dummy, Stock Deal dummy, Attitude dummy, Target public dummy, Percentage of shares acquired, Acquirer Total Assets, Acquirer/Target Assets Ratio, a dummy for whether the acquiring banks acquired another target during the last three years, and number of offers that the target received. The regressions also contain Year fixed effects and Acquirer Bank State*Target Bank State fixed effects.

The endogeneity problem arises because measures of the overlap of bank branch networks and bank merger decisions and outcomes may be affected by unobservable hidden factors. In many states in the US, banks were not allowed to set up branches in other states. In the 1980s and 1990s, states gradually relaxed this restriction, which was largely exogenous to the individual banks (Jayaratne and Strahan (1996)). Therefore, a connection forms when a state allows another state’s banks to open branches, and these connections generate a directed spatial state network between the 50 states in the United States and Washington D.C.. As a result, interstate deregulation events generate exogenous changes of the state network, which allows information from such state network to serve as instruments to the endogenous bank network, e.g., the three overlap measures mentioned above.

It is common to utilize neighborhood structure of nodes in a network to serve as instruments to deal with endogeneity in the literature, e.g., Chandrasekhar (2016). Specifically, for any pairs of nodes , we can define as the minimum number of edges that link to . For any , we can define the order neighbor of a node , denoted as a set , as the collection of those nodes such that .

Note that the state network has a spatial structure. Consider the case that a bank (the acquirer) in acquires a bank in . Consider measuring “overlap” in the state network for two states subjective to the target bank’s state, . We can construct order (geographical) distance-weighted overlap between two states and , subject to , denoted as , as follows:

| (17) |

where is a function that measures “geographic distance ratio”, and is the collection of all states and Washington D.C., which has a cardinality of . In Levine, Lin and Wang (2020), the authors define three different ways to construct geographic distance ratio (GDR) and -. For details, see Appendix C.

Specifically, in (17), we call as FNN, and as SNN, referring to “first” and “second order neighbor’s distance weighted network overlap”, respectively. Note that for each acquisition, given , there exists possible and three ways to measure FNN, leading to FNN instruments.

Using the state network, Levine, Lin and Wang (2020) construct three IVs based on SNNs, namely weighted Overlap, Correlation Coefficient, and Cosine Distance of states that allowed market entry.555Details on the construction can be found in the online appendix of Levine, Lin and Wang (2020). We instead use the FNN variables as potential IVs. Because we have observations, this leads to a high ratio, only a small set of which, however, might be relevant.666Note that the number of observations differ slightly to the original study because we corrected a minor data mistake in the sample. This mistake is confirmed after communication with one of the authors. In fact, our later analysis shows that there are only four to six FNNs with non-zero coefficients after applying iterated post- or orthogonal -Boosting, meaning that most FNNs are filtered out during the selection step.777Note that in our estimation with -Boosting, we do not include the original, constructed IVs that Levine, Lin and Wang (2020) use. However, if we include them in the selection process, the results do not change – indeed, these are still better than those obtained using the combination of simple instrumental variables.

The FNNs appear to be much weaker than SNNs because none of the FNNs are found to be significantly correlated to the explanatory variable in the first stage. For this reason, Levine, Lin and Wang (2020) use SNNs instead of FNNs. However, discarding the FNNs leads to a loss of efficiency. The advantage of -Boosting algorithm is that it utilizes the useful information of FNNs and selects a combination of FNNs to form IVs that may be even better than SNNs.

6.2. Results

We apply iterated post--Boosting and orthogonal -Boosting on the bank merger data, conduct inference as described in Section 4.2.2, and present the estimates in Table 2. We control for all firm-year characteristics, year fixed effects, and acquirer-state times target-state fixed effects as was done in the original study. The numbers in parentheses are standard errors.

Columns 1-3 in Table 2 give the estimated coefficients and standard errors using original IVs (SNNs) of Levine, Lin and Wang (2020).888Note that the estimates differ slightly to the original study since we corrected a minor data mistake in the sample. Columns 4-6 give the estimates of the coefficients and standard errors using iterated post--Boosting (I-pBA). Rows 4-6 in Table 3 give the FNNs that are ultimately selected for use. For example, as shown in Row 4, six FNNs (, , , , , ) are selected to jointly instrument for Overlap in our estimation procedure. These six instruments provide a smaller standard error (3.53) than the original IVs of Levine, Lin and Wang (2020) (5.27) – indicating the selection of more efficient IVs. The standard errors using the IVs selected from I-pBA for Correlation Coefficient and Cosine Distance are also smaller than those obtained using the original IVs. This shows that the estimation is more efficient when using our selection procedure. Moreover, all estimated coefficients using I-pBA are also statistically significant.

Orthogonal -Boosting also works well on this sample. Columns 7-9 present the estimates of the coefficients and standard errors using orthogonal -Boosting. Rows 7-9 in Table 3 present the FNNs that are selected. For example, as shown in Row 7, six IVs (, , , , , ) are selected to jointly instrument for Overlap and produce a smaller standard error (3.52) than that produced by the SNNs (5.27). The standard errors using the combined FNNs selected from orthogonal -Boosting for Correlation Coefficient and Cosine Distance are also smaller than the SNNs in Levine, Lin and Wang (2020).

In the last three Columns 10-12 in Table 2, we present the estimates using post-Lasso for a comparison. As shown in the bottom row of the table, the computing time for post-Lasso is higher than that for post--Boosting.

| (1) | (2) | (3) | (4) | (5) | (6) | (7) | (8) | (9) | (10) | (11) | (12) | |

| Dependent Variable: Acquirer CAR (-2, +2) | ||||||||||||

| Original IV | iterated post--Boosting | orthogonal -Boosting | post-Lasso | |||||||||

| Overlap | 17.18*** | 8.827** | 8.753** | 3.575 | ||||||||

| (5.27) | (3.53) | (3.52) | (4.39) | |||||||||

| Correlation Coefficient | 12.93*** | 11.50*** | 12.34*** | 5.102 | ||||||||

| (4.86) | (4.44) | (4.68) | (4.73) | |||||||||

| Cosine Distance | -17.66*** | -13.64*** | -8.386 | -5.364 | ||||||||

| (5.63) | (5.28) | (5.12) | (4.84) | |||||||||

| Firm-year Controls | Yes | Yes | Yes | Yes | Yes | Yes | Yes | Yes | Yes | Yes | Yes | Yes |

| Year Fixed Effects | Yes | Yes | Yes | Yes | Yes | Yes | Yes | Yes | Yes | Yes | Yes | Yes |

| Acquirer-State Target-State Fixed Effects | Yes | Yes | Yes | Yes | Yes | Yes | Yes | Yes | Yes | Yes | Yes | Yes |

| Observations | 442 | 442 | 442 | 442 | 442 | 442 | 442 | 442 | 442 | 442 | 442 | 442 |

| R-squared | 0.088 | 0.298 | 0.144 | 0.404 | 0.338 | 0.288 | 0.406 | 0.315 | 0.410 | 0.466 | 0.446 | 0.446 |

| Algorithm Execution Time (ms) | 3.313 | 2.381 | 2.426 | 3.658 | 3.866 | 4.227 | 19.928 | 5.260 | 5.298 | |||

| Column | Instrumental Variables |

|---|---|

| (1) | Original SNN IV for Overlap |

| (2) | Original SNN IV for Correlation Coefficient |

| (3) | Original SNN IV for Cosine Distance |

| (4) | |

| (5) | |

| (6) | |

| (7) | |

| (8) | |

| (9) | |

| (10) | |

| (11) | |

| (12) |

7. Conclusion

In this paper, we apply -Boosting, namely the iterated post- and orthogonal versions, for estimation and inference of treatment effects in the setting of many controls and many instruments. We derive uniformly valid results for the asymptotic distribution of estimated treatment effects. We use the framework of orthogonalized moment conditions introduced by Belloni, Chernozhukov, Hansen, and coauthors in a series of papers to derive these results. We also provide new results on the rate of convergence of iterated post- and orthogonal -Boosting, which are needed as an ingredient of our approach, but might also be of independent interest.

To derive these rates, we do not require the beta-min condition, and we rely only on approximate sparsity, which is a substantial improvement on earlier work. In an extensive simulation study, we show that our proposed method works well and has a computational advantage over Lasso. Finally, we analyze how the pre-merger overlap of bank branch networks in the US can affect the post-merger stock returns of acquirer banks. Our results show that IV selection with our procedure gives more efficient estimates than standard approaches and is capable of selecting the relevant instruments from among a large set of potential instruments.

Appendix A Proofs of Theoretical Results.

Throughout this section, we assume that Assumptions 1 - 3 hold. Define

as the set of selected variables at the beginning of the iteration. We require the following lemma for proving our main results. For any set , define as the projection operator

Proof.

From now on, denote as the vector of errors between the true model and the estimated model at period . By definition, it is easy to see that for all , we have that:

Proof of Theorem 1.

If the number of selected variables is less than , it is easy to see that statement (4) implies statement (5) due to Assumption 2. Therefore, it suffices to prove that (a) statement (4) is true and (b) the number of variables selected in is less than or equal to , which is implied by our assumption that . WLOG., we can assume that is an integer so that . As a result, .

By assumption, define the value of such that . Further, define and the epoch as the periods of , for . At the beginning of the epoch, the corresponding vector of residuals is

| (23) |

Recall that is the support of the true parameter .

Define for any . Assume that .

If , then all the variables in are already selected by the algorithm at . As a result, must also be . Consequently, by Lemma 1, we have that:

| (24) |

which concludes the result.

Now, suppose that . By construction of Algorithm 2, we have that:

| (25) |

Define , which differs from by

Note that is decreasing in as for all . If

| (26) |

holds for some generic constant and , by Lemma 1, we have that:

| (27) |

which concludes our result.

From now on, we assume that

| (28) |

for all such that . Our strategy is to show that this is impossible if is large enough and is properly chosen. By construction of the algorithm, we know that for any , we have that 999 The inequality (29) holds as equality for by definition of steps.:

| (29) |

Define as the change of the parameter , and define . For , denote

with

| (30) |

and

| (31) |

Next, we divide our discussion into two cases, Case () and Case ().

Case ()

For a fixed such that

| (32) |

assume that with .

Then, by (29), we have that:

| (33) |

Case ()

Assume . Consequently, for any , we have that:

| (34) |

Then, we have:

| (35) | |||

| (36) |

where (35) follows from Assumption 2 and (36) follows from (34) and (32).

Therefore by definition of , for , we have:

| (37) | ||||

| (38) | ||||

| (39) | ||||

| (40) | ||||

| (41) |

with

| (42) |

where (37) holds by Cauchy-Schwarz inequality, (38) holds by Lemma 1 and (27), (39) holds by (27), (40) holds by Assumption 2, Assumption 3 and , and (41) holds by (27).

For fixed and large enough, we have that . Therefore,

| (43) | ||||

| (44) | ||||

| (45) |

where the last inequality follows from Assumption 2. Therefore, we have that:

| (46) |

Consequently, we have

| (47) |

Combining Case () and Case (), based on (33) and (47), we have that:

| (48) |

where . By assumption that , we have that:

| (49) |

where is a generic positive constant.

Define as the smallest integer . WLOG., we can assume that for simplicity, i.e., is an integer. By applying (48) to , we have that:

| (50) |

Note that is a decreasing sequence in .

We divide our analysis into two Cases: Case and Case .

Case

| (51) |

Then, (51) and (50) implies that:

| (52) |

Recall that for any positive integer ,

Consequently, we have:

| (53) |

Plugging in (53) with and in (52), we have that:

| (54) |

Next, we establish bounds on and . Note that and only differ by the indices and . It is sufficient to bound , then will obey the same bound.

Note that . By Assumption 2, we have:

| (55) |

Therefore,

| (56) |

where the third last inequality follows from statement (ii) of Assumption 1, the second last inequality follows from Lemma 1, and the last inequality follows from (55), and

| (57) |

is a constant bounded by for large enough.

Note that we assume . Hence, (57) implies that

| (58) |

Similarly, we have

| (59) |

Note the , so we have that

| (60) |

Plugging in (58), (59) and (60) in (54), we have that:

| (61) |

given that is chosen such that .

Case

| (62) |

Therefore, combining Case and Case , we have that:

| (63) |

where is a generic constant. Following (63), for all such that , we have that:

| (64) |

Since , let , i.e.,

we have that . Replace with in (64), by statement (iii) of Assumption 1, we have that for large enough:

which contradicts with the assumption stated in (28). It implies that either (24) or (27) must hold. Therefore, we have the conclusion.

Proof of Corollary 1.

By construction of Algorithm 2, we have that

for all non-negative integers . Therefore,

| (65) |

It implies that the algorithm will not stop if

| (66) |

Suppose the algorithm does not stop before for some but . By Theorem 1, we know that at some , we have that

| (67) |

Since is decreasing in , (67) holds for all when is replaced by . For any such that , we have that:

| (68) | |||

| (69) | |||

| (70) |

where the second last inequality follows from Assumption 1, Assumption 3, and Lemma 1, the last inequality follows from Assumption 2 and (67), and

| (71) |

is a constant bounded by

| (72) |

for large enough. Hence, given the growth condition that , for large enough, we have that

where is a small positive constant defined in Assumption 3 and the second last inequality follows from Assumption 3. Therefore, for any , and for large enough, we have that:

Consequently, (66) implies that:

| (73) |

As a result, assume that such that . WLOG., assume that is an integer so that . On the one hand, we have that:

| (74) |

On the other hand, for large enough, (70) suggests that:

| (75) |

or equivalently,

| (76) |

This implies that

| (77) |

Therefore, if , for large enough, the algorithm must stop before , i.e., , by assumption that .

Now, we show that . A similar bound will hold for , due to Assumption 2.

When the algorithm stops, then it must hold that

| (78) |

For large enough, we know that from analysis in the above. Therefore, there exists such that . In the following, we use the notation from the proof of Theorem 1. For any , for large enough, we have that:

| (79) |

where the last inequality follows from Assumption 3 and . Therefore, (78) and (79) implies that:

| (80) |

Assume that for some fixed constant . Otherwise we already have that , which provides the result.

For large enough, by Theorem 1, we know that . Recall that

| (81) |

Note that can be rewritten as:

| (82) | |||

| (83) | |||

| (84) |

where is a vector of dimension with that has cardinality

As a result, by optimality of , we have that:

| (85) |

where the second last inequality follows from Assumption 3, the last inequality follows from Assumption 2, statement (ii) of Assumption 1, and Lemma 1, and

| (86) |

is bounded from below by a fixed positive constant

| (87) |

for arbitrarily small and large enough, given that . As a result, (85) yields that

| (88) |

where the last inequality follows from Assumption 2. Plugging in (88) in (80), we have:

| (89) |

which yields that:

| (90) | |||

| (91) |

Given the growth condition that , for large enough such that , we have that:

which yields the conclusion.

Proof of Theorem 2.

Proof of Corollary 2.

Proof of Theorem 3.

According to Theorem 1 and 2, the condition on the prediction rates in HLMS(P) in Belloni, Chernozhukov and Hansen (2014) are satisfied by Assumption A.3 (i):

Although we have and , the slightly stronger growth conditions in Assumption A.3 allow us to apply the proof of Theorem 2 in Belloni, Chernozhukov and Hansen (2014). It is worth to notice that the growth rate is needed for consistent variance estimation (see Step 5 in the proof of Theorem 2 in Belloni, Chernozhukov and Hansen (2014)). Condition ASTE(P) and Condition SE(P) hold due to Assumptions A.1-A.3. Hence, Theorem 2 in Belloni, Chernozhukov and Hansen (2014) yields the result.

Proof of Theorem 4.

Assumptions B.1-B.3 ensure sufficiently fast convergence rates of the fitted optimal instruments via I-pBA or oBA in the first step, i.e.,

with probability by Theorem 1 and Theorem 2, respectively. Since the maximal sparse eigenvalues are uniformly bounded from above due to Assumption B.2, we conclude

with probability which implies

Assuming in Assumption B.4, it implies equation (F.2) in Belloni et al. (2012):

This allows us to apply the proof of Theorem 4 in Belloni et al. (2012). It is also worth to notice that the growth rate ensures consistency of the variance estimation (see Step 5 in the proof of Theorem 4 in Belloni et al. (2012)). This concludes the proof.

Appendix B Additional Results of the Simulation Study

| iid covariates | correlated covariates | ||||||||||||

| Lasso | pBA | I-pBA | oBA | CV-pBA | CV-Lasso | Lasso | pBA | I-pBA | oBA | CV-pBA | CV-Lasso | ||

| p | Mean Absolute Error | ||||||||||||

| 200 | 0.042 | 0.042 | 0.045 | 0.042 | 0.051 | 0.051 | 0.045 | 0.046 | 0.046 | 0.045 | 0.049 | 0.047 | Control-1 |

| 600 | 0.046 | 0.044 | 0.045 | 0.045 | 0.063 | 0.070 | 0.048 | 0.047 | 0.044 | 0.049 | 0.062 | 0.064 | |

| 1000 | 0.055 | 0.050 | 0.048 | 0.052 | 0.077 | 0.091 | 0.049 | 0.044 | 0.049 | 0.046 | 0.068 | 0.075 | |

| 1400 | 0.062 | 0.047 | 0.049 | 0.050 | 0.080 | 0.099 | 0.059 | 0.047 | 0.049 | 0.050 | 0.074 | 0.089 | |

| 1800 | 0.076 | 0.049 | 0.049 | 0.052 | 0.089 | 0.112 | 0.068 | 0.050 | 0.047 | 0.054 | 0.082 | 0.098 | |

| 200 | 0.044 | 0.042 | 0.040 | 0.042 | 0.049 | 0.049 | 0.040 | 0.040 | 0.042 | 0.040 | 0.045 | 0.043 | Control-2 |

| 600 | 0.045 | 0.042 | 0.045 | 0.043 | 0.061 | 0.059 | 0.046 | 0.045 | 0.044 | 0.045 | 0.057 | 0.056 | |

| 1000 | 0.048 | 0.046 | 0.044 | 0.045 | 0.074 | 0.078 | 0.045 | 0.044 | 0.043 | 0.044 | 0.063 | 0.064 | |

| 1400 | 0.051 | 0.045 | 0.044 | 0.046 | 0.075 | 0.073 | 0.049 | 0.044 | 0.045 | 0.046 | 0.072 | 0.076 | |

| 1800 | 0.056 | 0.046 | 0.046 | 0.046 | 0.083 | 0.082 | 0.052 | 0.044 | 0.041 | 0.045 | 0.072 | 0.074 | |

| 200 | 0.059 | 0.057 | 0.059 | 0.056 | 0.055 | 0.056 | 0.100 | 0.097 | 0.096 | 0.097 | 0.082 | 0.120 | IV |

| 600 | 0.058 | 0.057 | 0.057 | 0.056 | 0.055 | 0.056 | 0.140 | 0.118 | 0.117 | 0.115 | 0.133 | 1.075 | |

| 1000 | 0.062 | 0.063 | 0.063 | 0.061 | 0.060 | 0.061 | 0.145 | 0.123 | 0.130 | 0.123 | 0.113 | 2.180 | |

| 1400 | 0.061 | 0.065 | 0.063 | 0.064 | 0.059 | 0.061 | 0.417 | 0.124 | 0.133 | 0.125 | 0.256 | 3.089 | |

| 1800 | 0.062 | 0.064 | 0.063 | 0.062 | 0.060 | 0.176 | 0.229 | 0.133 | 0.135 | 0.131 | 0.207 | 2.318 | |

| p | Standard Deviation | ||||||||||||

| 200 | 0.053 | 0.053 | 0.054 | 0.053 | 0.065 | 0.058 | 0.055 | 0.057 | 0.056 | 0.055 | 0.061 | 0.055 | Control-1 |

| 600 | 0.057 | 0.054 | 0.054 | 0.053 | 0.078 | 0.065 | 0.060 | 0.060 | 0.054 | 0.060 | 0.079 | 0.067 | |

| 1000 | 0.062 | 0.057 | 0.055 | 0.057 | 0.097 | 0.072 | 0.058 | 0.055 | 0.058 | 0.054 | 0.086 | 0.068 | |

| 1400 | 0.062 | 0.054 | 0.055 | 0.055 | 0.100 | 0.075 | 0.064 | 0.058 | 0.057 | 0.058 | 0.093 | 0.071 | |

| 1800 | 0.071 | 0.057 | 0.056 | 0.058 | 0.115 | 0.081 | 0.065 | 0.062 | 0.056 | 0.059 | 0.106 | 0.072 | |

| 200 | 0.053 | 0.052 | 0.050 | 0.053 | 0.062 | 0.058 | 0.050 | 0.049 | 0.052 | 0.050 | 0.057 | 0.053 | Control-2 |

| 600 | 0.055 | 0.052 | 0.056 | 0.053 | 0.073 | 0.066 | 0.057 | 0.056 | 0.055 | 0.056 | 0.072 | 0.063 | |

| 1000 | 0.060 | 0.057 | 0.054 | 0.057 | 0.092 | 0.076 | 0.055 | 0.053 | 0.053 | 0.054 | 0.080 | 0.066 | |

| 1400 | 0.062 | 0.056 | 0.055 | 0.057 | 0.093 | 0.074 | 0.061 | 0.055 | 0.056 | 0.056 | 0.090 | 0.078 | |

| 1800 | 0.068 | 0.058 | 0.057 | 0.058 | 0.104 | 0.083 | 0.060 | 0.055 | 0.053 | 0.055 | 0.089 | 0.072 | |

| 200 | 0.073 | 0.070 | 0.074 | 0.069 | 0.063 | 0.068 | 0.122 | 0.119 | 0.119 | 0.118 | 0.094 | 0.322 | IV |

| 600 | 0.072 | 0.069 | 0.072 | 0.068 | 0.059 | 0.067 | 0.296 | 0.140 | 0.136 | 0.136 | 0.724 | 3.754 | |

| 1000 | 0.074 | 0.077 | 0.076 | 0.075 | 0.065 | 0.073 | 0.314 | 0.145 | 0.152 | 0.145 | 0.283 | 10.787 | |

| 1400 | 0.072 | 0.079 | 0.077 | 0.077 | 0.061 | 0.072 | 4.993 | 0.142 | 0.156 | 0.144 | 1.424 | 9.670 | |

| 1800 | 0.071 | 0.077 | 0.076 | 0.074 | 0.061 | 2.551 | 1.443 | 0.153 | 0.153 | 0.150 | 1.541 | 7.232 | |

| p | Rejection Rate | ||||||||||||

| 200 | 0.070 | 0.076 | 0.074 | 0.062 | 0.058 | 0.082 | 0.064 | 0.070 | 0.090 | 0.066 | 0.050 | 0.080 | Control-1 |

| 600 | 0.080 | 0.080 | 0.074 | 0.088 | 0.038 | 0.230 | 0.090 | 0.102 | 0.066 | 0.096 | 0.058 | 0.178 | |

| 1000 | 0.150 | 0.098 | 0.100 | 0.114 | 0.062 | 0.362 | 0.096 | 0.072 | 0.098 | 0.076 | 0.046 | 0.256 | |

| 1400 | 0.188 | 0.076 | 0.076 | 0.098 | 0.056 | 0.432 | 0.172 | 0.100 | 0.106 | 0.108 | 0.042 | 0.340 | |

| 1800 | 0.276 | 0.084 | 0.096 | 0.126 | 0.068 | 0.500 | 0.224 | 0.114 | 0.080 | 0.134 | 0.066 | 0.420 | |

| 200 | 0.058 | 0.058 | 0.034 | 0.050 | 0.038 | 0.090 | 0.054 | 0.032 | 0.050 | 0.044 | 0.038 | 0.058 | Control-2 |

| 600 | 0.078 | 0.058 | 0.064 | 0.046 | 0.048 | 0.180 | 0.070 | 0.076 | 0.074 | 0.074 | 0.052 | 0.146 | |

| 1000 | 0.094 | 0.074 | 0.064 | 0.082 | 0.080 | 0.264 | 0.058 | 0.058 | 0.048 | 0.062 | 0.068 | 0.194 | |

| 1400 | 0.118 | 0.072 | 0.060 | 0.084 | 0.068 | 0.242 | 0.102 | 0.066 | 0.060 | 0.066 | 0.062 | 0.274 | |

| 1800 | 0.154 | 0.078 | 0.070 | 0.084 | 0.064 | 0.296 | 0.118 | 0.060 | 0.074 | 0.066 | 0.046 | 0.278 | |

| 200 | 0.054 | 0.048 | 0.072 | 0.048 | 0.064 | 0.056 | 0.070 | 0.060 | 0.062 | 0.062 | 0.092 | 0.074 | IV |

| 600 | 0.068 | 0.056 | 0.062 | 0.064 | 0.104 | 0.070 | 0.066 | 0.062 | 0.052 | 0.052 | 0.118 | 0.042 | |

| 1000 | 0.072 | 0.072 | 0.080 | 0.074 | 0.106 | 0.072 | 0.078 | 0.068 | 0.080 | 0.070 | 0.140 | 0.050 | |

| 1400 | 0.054 | 0.056 | 0.076 | 0.064 | 0.098 | 0.062 | 0.070 | 0.048 | 0.074 | 0.054 | 0.126 | 0.040 | |

| 1800 | 0.076 | 0.062 | 0.058 | 0.060 | 0.138 | 0.064 | 0.070 | 0.068 | 0.074 | 0.066 | 0.140 | 0.040 | |

| p | Computation Time | ||||||||||||

| 200 | 0.010 | 0.004 | 0.005 | 0.006 | 1.511 | 9.360 | 0.010 | 0.004 | 0.005 | 0.006 | 1.498 | 9.553 | Control-1 |

| 600 | 0.019 | 0.009 | 0.020 | 0.011 | 3.956 | 22.451 | 0.018 | 0.009 | 0.019 | 0.012 | 4.077 | 23.140 | |

| 1000 | 0.032 | 0.028 | 0.018 | 0.028 | 10.032 | 63.795 | 0.029 | 0.027 | 0.015 | 0.028 | 10.313 | 65.936 | |

| 1400 | 0.051 | 0.044 | 0.052 | 0.044 | 14.901 | 100.427 | 0.050 | 0.041 | 0.049 | 0.040 | 15.121 | 97.662 | |

| 1800 | 0.080 | 0.055 | 0.066 | 0.066 | 19.741 | 131.798 | 0.066 | 0.052 | 0.078 | 0.052 | 19.832 | 131.833 | |

| 200 | 0.009 | 0.004 | 0.005 | 0.006 | 1.470 | 9.446 | 0.009 | 0.004 | 0.005 | 0.005 | 1.512 | 9.482 | Control-2 |

| 600 | 0.020 | 0.009 | 0.018 | 0.011 | 3.987 | 22.574 | 0.019 | 0.008 | 0.019 | 0.010 | 4.131 | 22.891 | |

| 1000 | 0.032 | 0.027 | 0.017 | 0.027 | 10.141 | 64.102 | 0.028 | 0.026 | 0.016 | 0.028 | 10.824 | 64.826 | |

| 1400 | 0.050 | 0.043 | 0.048 | 0.044 | 14.911 | 96.500 | 0.047 | 0.042 | 0.058 | 0.041 | 15.006 | 98.096 | |

| 1800 | 0.076 | 0.053 | 0.094 | 0.054 | 19.096 | 127.115 | 0.067 | 0.056 | 0.065 | 0.053 | 19.709 | 136.821 | |

| 200 | 0.009 | 0.005 | 0.005 | 0.009 | 1.504 | 9.935 | 0.009 | 0.004 | 0.005 | 0.006 | 1.484 | 9.857 | IV |

| 600 | 0.019 | 0.017 | 0.015 | 0.020 | 6.459 | 44.573 | 0.016 | 0.008 | 0.021 | 0.010 | 4.197 | 22.947 | |

| 1000 | 0.035 | 0.028 | 0.015 | 0.033 | 6.756 | 42.428 | 0.028 | 0.029 | 0.021 | 0.028 | 10.607 | 68.366 | |

| 1400 | 0.047 | 0.020 | 0.057 | 0.030 | 10.642 | 91.119 | 0.052 | 0.041 | 0.061 | 0.042 | 15.744 | 100.891 | |

| 1800 | 0.092 | 0.065 | 0.097 | 0.072 | 25.276 | 143.655 | 0.055 | 0.061 | 0.082 | 0.065 | 19.885 | 143.689 | |

| iid covariates | correlated covariates | ||||||||||||

| Lasso | pBA | I-pBA | oBA | CV-pBA | CV-Lasso | Lasso | pBA | I-pBA | oBA | CV-pBA | CV-Lasso | ||

| p | Mean Absolute Error | ||||||||||||

| 200 | 0.044 | 0.044 | 0.042 | 0.045 | 0.051 | 0.051 | 0.042 | 0.043 | 0.043 | 0.044 | 0.051 | 0.046 | Control-1 |

| 600 | 0.044 | 0.043 | 0.046 | 0.044 | 0.062 | 0.069 | 0.047 | 0.046 | 0.048 | 0.048 | 0.060 | 0.064 | |

| 1000 | 0.051 | 0.045 | 0.047 | 0.049 | 0.073 | 0.088 | 0.051 | 0.048 | 0.046 | 0.049 | 0.071 | 0.076 | |

| 1400 | 0.060 | 0.048 | 0.045 | 0.051 | 0.077 | 0.099 | 0.055 | 0.044 | 0.049 | 0.049 | 0.077 | 0.086 | |

| 1800 | 0.072 | 0.051 | 0.048 | 0.055 | 0.083 | 0.112 | 0.065 | 0.049 | 0.049 | 0.054 | 0.079 | 0.097 | |

| 200 | 0.045 | 0.042 | 0.042 | 0.043 | 0.050 | 0.051 | 0.043 | 0.042 | 0.043 | 0.043 | 0.048 | 0.046 | Control-2 |

| 600 | 0.045 | 0.044 | 0.044 | 0.044 | 0.063 | 0.064 | 0.042 | 0.041 | 0.042 | 0.041 | 0.059 | 0.059 | |

| 1000 | 0.046 | 0.045 | 0.047 | 0.046 | 0.073 | 0.072 | 0.045 | 0.042 | 0.044 | 0.043 | 0.067 | 0.070 | |

| 1400 | 0.050 | 0.046 | 0.048 | 0.046 | 0.078 | 0.079 | 0.048 | 0.045 | 0.044 | 0.046 | 0.073 | 0.077 | |

| 1800 | 0.052 | 0.044 | 0.044 | 0.045 | 0.082 | 0.092 | 0.051 | 0.043 | 0.049 | 0.043 | 0.081 | 0.082 | |

| 200 | 0.045 | 0.045 | 0.044 | 0.045 | 0.044 | 0.045 | 0.071 | 0.073 | 0.075 | 0.072 | 0.069 | 0.072 | IV |

| 600 | 0.048 | 0.048 | 0.045 | 0.048 | 0.048 | 0.048 | 0.080 | 0.082 | 0.076 | 0.080 | 0.079 | 0.080 | |

| 1000 | 0.043 | 0.043 | 0.045 | 0.042 | 0.044 | 0.043 | 0.078 | 0.080 | 0.080 | 0.079 | 0.076 | 0.076 | |

| 1400 | 0.045 | 0.045 | 0.046 | 0.045 | 0.045 | 0.045 | 0.079 | 0.081 | 0.088 | 0.080 | 0.078 | 0.078 | |

| 1800 | 0.047 | 0.047 | 0.048 | 0.047 | 0.047 | 0.047 | 0.080 | 0.084 | 0.081 | 0.081 | 0.079 | 0.080 | |

| p | Standard Deviation | ||||||||||||

| 200 | 0.054 | 0.054 | 0.053 | 0.055 | 0.062 | 0.059 | 0.053 | 0.053 | 0.053 | 0.053 | 0.064 | 0.056 | Control-1 |

| 600 | 0.053 | 0.052 | 0.054 | 0.052 | 0.076 | 0.063 | 0.057 | 0.055 | 0.057 | 0.056 | 0.076 | 0.068 | |

| 1000 | 0.056 | 0.054 | 0.055 | 0.055 | 0.092 | 0.072 | 0.060 | 0.058 | 0.053 | 0.058 | 0.090 | 0.074 | |

| 1400 | 0.060 | 0.054 | 0.054 | 0.055 | 0.098 | 0.073 | 0.059 | 0.051 | 0.055 | 0.055 | 0.100 | 0.074 | |

| 1800 | 0.067 | 0.057 | 0.054 | 0.060 | 0.109 | 0.082 | 0.062 | 0.055 | 0.056 | 0.057 | 0.100 | 0.076 | |

| 200 | 0.053 | 0.053 | 0.052 | 0.054 | 0.063 | 0.059 | 0.053 | 0.051 | 0.055 | 0.051 | 0.059 | 0.054 | Control-2 |

| 600 | 0.055 | 0.055 | 0.056 | 0.055 | 0.079 | 0.065 | 0.053 | 0.051 | 0.053 | 0.052 | 0.075 | 0.064 | |

| 1000 | 0.058 | 0.057 | 0.059 | 0.057 | 0.090 | 0.069 | 0.057 | 0.053 | 0.056 | 0.054 | 0.084 | 0.072 | |

| 1400 | 0.061 | 0.056 | 0.060 | 0.057 | 0.096 | 0.075 | 0.060 | 0.057 | 0.055 | 0.057 | 0.092 | 0.075 | |

| 1800 | 0.061 | 0.055 | 0.055 | 0.055 | 0.103 | 0.079 | 0.062 | 0.054 | 0.061 | 0.054 | 0.103 | 0.077 | |

| 200 | 0.056 | 0.056 | 0.054 | 0.056 | 0.054 | 0.056 | 0.088 | 0.089 | 0.095 | 0.088 | 0.082 | 0.087 | IV |

| 600 | 0.059 | 0.059 | 0.055 | 0.059 | 0.057 | 0.059 | 0.098 | 0.101 | 0.094 | 0.099 | 0.089 | 0.096 | |

| 1000 | 0.053 | 0.053 | 0.056 | 0.053 | 0.051 | 0.053 | 0.092 | 0.096 | 0.099 | 0.094 | 0.078 | 0.089 | |

| 1400 | 0.056 | 0.057 | 0.057 | 0.057 | 0.053 | 0.055 | 0.090 | 0.096 | 0.103 | 0.095 | 0.079 | 0.090 | |

| 1800 | 0.057 | 0.059 | 0.058 | 0.058 | 0.055 | 0.057 | 0.096 | 0.104 | 0.100 | 0.100 | 0.083 | 0.096 | |

| p | Rejection Rate | ||||||||||||

| 200 | 0.040 | 0.048 | 0.054 | 0.054 | 0.040 | 0.090 | 0.064 | 0.060 | 0.054 | 0.064 | 0.066 | 0.076 | Control-1 |

| 600 | 0.064 | 0.056 | 0.086 | 0.072 | 0.032 | 0.210 | 0.078 | 0.076 | 0.084 | 0.080 | 0.058 | 0.160 | |

| 1000 | 0.104 | 0.090 | 0.078 | 0.096 | 0.060 | 0.334 | 0.110 | 0.094 | 0.072 | 0.106 | 0.078 | 0.244 | |

| 1400 | 0.170 | 0.068 | 0.074 | 0.098 | 0.056 | 0.410 | 0.134 | 0.076 | 0.076 | 0.092 | 0.050 | 0.288 | |

| 1800 | 0.220 | 0.100 | 0.102 | 0.146 | 0.048 | 0.454 | 0.172 | 0.072 | 0.104 | 0.114 | 0.052 | 0.364 | |

| 200 | 0.070 | 0.062 | 0.052 | 0.066 | 0.052 | 0.126 | 0.054 | 0.042 | 0.066 | 0.042 | 0.046 | 0.048 | Control-2 |