Transition probability of Brownian motion in the octant and its application to default modeling

Abstract

We derive a semi-analytical formula for the transition probability of three-dimensional Brownian motion in the positive octant with absorption at the boundaries. Separation of variables in spherical coordinates leads to an eigenvalue problem for the resulting boundary value problem in the two angular components. The main theoretical result is a solution to the original problem expressed as an expansion into special functions and an eigenvalue which has to be chosen to allow a matching of the boundary condition. We discuss and test several computational methods to solve a finite-dimensional approximation to this nonlinear eigenvalue problem. Finally, we apply our results to the computation of default probabilities and credit valuation adjustments in a structural credit model with mutual liabilities.

Keywords: three-dimensional Brownian motion; transition probability; nonlinear eigenvalue problem; structural default model; mutual liabilities.

1 Introduction

The transition probability of multi-dimensional Brownian motion in with absorption at the boundary, occurs in different areas of applied mathematics. We are particularly motivated by mathematical finance. For example, it appears in counterparty credit risk modeling (Lipton and Savescu, (2014), Lipton and Sepp, (2009), Itkin and Lipton, (2016), Zhou, (2001)), market microstructure (Cont and De Larrard, (2012), Lipton et al., (2014)), and exotic option pricing (Escobar et al., (2014) for barrier options on three assets with special correlation structure; He et al., (1998) for lookback options whose payoff depends on the minima, maxima, and endpoint of the asset price process; Lipton, (2001)).

The one-dimensional case is classical and is solved analytically by the reflection principle, or, in PDE terms, by the method of images. The two-dimensional problem can be solved analytically by the method of images or separation of variables; see Lipton and Sepp, (2009) for details. The three-dimensional problem is much more difficult than the one- and two-dimensional ones. For several particular cases of the correlation matrix, Escobar et al., (2013) offered solutions to the three-dimensional problem by the method of images. Unfortunately, it cannot be extended to general correlation matrices. A semi-analytical solution was proposed in Lipton and Savescu, (2014), where a separation of variables technique is used and the problem is split into radial and angular PDEs. The radial PDE is solved analytically, while the angular PDE is solved by finite elements.

In this paper, we use the separation of variables technique and solve the angular PDE semi-analytically, and thus provide a ‘‘fully semi-analytical’’ representation of the Green’s function. By this we mean that the solution is expressed as a (double) infinite series of terms involving special functions (hypergeometric and Bessel). We also require the solution of a countably infinite-dimensional non-linear eigenvalue problem. In practice, the sums can be truncated to a relatively small number of terms (low tens) without significant loss of accuracy, as evidenced by our numerical tests, and similarly for the dimension of the non-linear eigenvalue problem.

There are a number of published methods available for solving (finite-dimensional) non-linear eigenvalue problems. A detailed review can be found in Mehrmann and Voss, (2004). Most methods use a linearization and solution of a corresponding linear eigenvalue problem. As an example of this type of methods, we consider a method based on Chebyshev interpolation (Trefethen, (2013)). We also study another recently developed approach based on computing contour integrals (Beyn, (2012)). Both methods are easy to implement and have good properties for our specific problem.

By this semi-analytical approach, we can compute the transition density and its derivatives to high accuracy much more quickly than by numerical solution of the original three-dimensional parabolic PDE. We demonstrate this by comparison with a finite difference approximation obtained with the Hundsdorfer-Verwer scheme (Hundsdorfer and Verwer, (2013)).

To our knowledge, this is the first published expression for the transition probability of general correlated Brownian motion with absorbing boundaries on the octant. Moreover, we consider a slightly more general formulation compared to other published special cases which allows a constant drift.

In the context of credit risk applications, we show how to compute the joint survival probability of firms in a Black-Cox setting semi-analytically using Gegenbauer polynomial expansion, and give expressions for credit- and debt-valuation adjustments in terms of integrals over (analytically available) derivatives of the transition probability.

The rest of the paper is organized as follows. In Section 2, we formulate the problem as PDE, show how to eliminate the drift and correlation terms, and transform the equation to spherical coordinates. In Section 3, we use separation of variables to obtain radial and angular PDEs, solve both equations, and write the final expression for the Green’s function in terms of unknown non-linear eigenvalues and eigenvectors. In Section 4, we discuss various methods to solve the nonlinear eigenvalue problem. In Section 5, we perform numerical tests. In Section 6, we study applications of the three-dimensional transition probability to a default model with mutual liabilities. In Section 7, we conclude.

2 Problem formulation and preliminaries

We consider a three-dimensional standard Brownian motion with constant drift ,

with infinitesimal generator

where is a symmetric positive definite matrix with , , the correlation matrix of the three-dimensional standard Brownian motion .

Now consider the stopped process , with the exit time of the positive octant. Then the distribution of has a singular component at the boundary where one of the coordinates is 0, corresponding to the absorbed mass, and a continuous density in the interior, which goes to zero at the boundaries. Let denote this continuous component of the distribution evaluated at at time . For a fixed pair , it satisfies the forward Kolmogorov equation

| (1) |

with initial condition , boundary condition for , , and where is the adjoint operator of ,

In PDE theory, the transition probability can be interpreted as Green’s function, that is the fundamental solution to a suitable initial(-boundary) value problem which we will specify later. Thus, by time homogeneity, we use the notation . For convenience, we will denote the state variables occasionally by .

To eliminate the cross-derivative terms, we use the change of variables as in Lipton et al., (2014) and Lipton and Savescu, (2014); see also Appendix A. To eliminate the drift term, we further use the transformation

| (2) | |||||

(see also Appendix A). We omit tilde in the following for simplicity of notation.

Finally, we rewrite the equation in spherical coordinates to take advantage of the wedge-shape of the domain, where , with , and , where can be implicitly defined as

| (3) | |||||

| (4) |

where for .

The final initial-boundary value problem for the Green’s function has the form

| (5) |

3 Semi-analytical solution by expansion

In this section, we show how the solution to (5) can be given via an eigenvalue expansion. First, we apply separation of variables

then (5) decomposes into two separate (initial-)boundary value problems

| (6) |

and

| (7) |

where is an eigenvalue. The eigenvalue is real and positive because the differential operator on the left-hand side of (7) is symmetric and positive definite with respect to a certain weighted inner product, as is seen from the variational formulation given in equation (40) in Lipton and Savescu, (2014).

We note an asymmetry between (6), which contains the time variable and hence an initial condition is imposed, and (7), which is stationary and hence does not match any initial condition. The initial condition of the solution in (5) will eventually be ensured by superposition in Section 3.2. Since (7) does not depend on here (due to the ignorance of the initial condition), we further write for simplicity.

The PDE (6) can be solved analytically, with solution

where is the modified Bessel function of the second kind.

The eigenvalue problem for the angular PDE (7) was solved numerically in Lipton and Savescu, (2014) by a finite element method. In the following, we consider an alternative, semi-analytical approach.

3.1 Semi-analytical method for angular PDE

We begin by further simplifying the problem by the extra transformation (as in Lipton et al., (2014) for the stationary case)

| (8) |

which changes the domain to the semi-infinite strip and the eigenvalue problem to

| (9) |

Denote . Then, (9) becomes

We shall find solutions in the form . Thereby, we can split (9) into the system

| (10) | ||||

| (11) |

where is an eigenvalue and with boundary conditions

| (12) |

Equation (10) with the first and second boundary conditions in (12) can be solved as

where , while (11) is the Schrödinger equation with Pöschl–Teller potential. Solving it with the third boundary condition in (12), we get (see Appendix B)

where is the Gaussian hypergeometric function. Thus, we find in the form

| (13) |

As an aside, we note that for , which gives

and coincides with the expression in Lipton et al., (2014) for the stationary problem.

3.2 Final expression for Green’s function

Now we can write the expression for the Green’s function using the eigenvalue expansion

| (17) | |||||

where the (countably many) eigenvalues and coefficients can be determined as the solution of the nonlinear eigenvalue problem (16) and .

The coefficients can be determined by imposing the initial condition

We have already ensured the initial condition for the radial part, thus we need

| (18) |

From the weak formulation of the angular PDE it is easy to see that the eigenvectors are orthogonal in the scalar product weighted by (Lipton and Savescu, (2014)). Multiplying (18) by and integrating over the whole domain,

Substituting the expression for from the last equation into (17), expanding the expression for and , we get

Returning to the variable , we have

| (19) |

4 Solution of the nonlinear eigenvalue problem

In this section, we first give properties of the eigenvalue problem (16). Then, we describe several methods to solve nonlinear eigenvalue problems and outline how the methods are applied in the tests.

4.1 Truncation and the smallest (linear) eigenvalue of

If we truncate the sum (16) after terms, the resulting equation can be rewritten in matrix form

| (20) |

where .

Equation (20) is a nonlinear eigenvalue problem for a symmetric positive semi-definite matrix (as the matrix is a Gram matrix). Eigenvalues of this truncated problem have to satisfy the equation

| (21) |

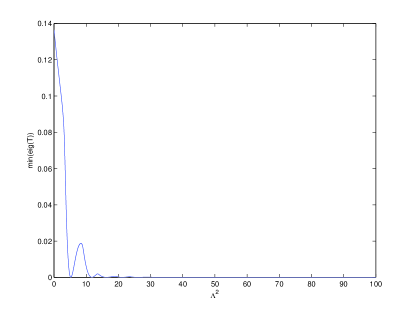

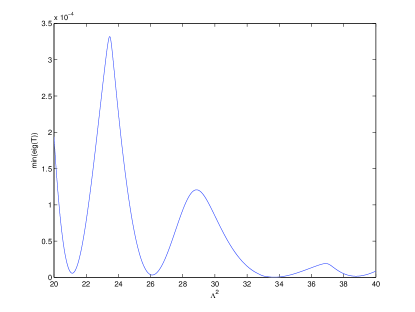

where is the minimum eigenvalue of the positive semi-definite matrix . Due to the truncation, however, the problem (20) generally does not have real-valued solutions for . Indeed, numerical tests suggest that is typically strictly positive definite for all and then a non-zero solution for does not exist. Figure 1 illustrates the dependence of the smallest eigenvalue of on .

In order to find an approximation to the original problem, we need to ‘‘regularize’’ it in the sense that there exists a solution of the truncated problem that is close to the solution of the infinite problem when the number of terms increases.

4.2 Chebyshev polynomial interpolation of

In this approach, we approximate for complex using Chebyshev polynomials,

| (22) |

where is a (scalar) Chebyshev polynomial basis of degree and are the corresponding coefficients.

The following result is a modification of Theorem 18.1 in Trefethen, (2013) (see, for example, Nakatsukasa et al., (2015), Section 7.2).

Theorem 1.

The solutions of the polynomial eigenvalue problem for in (22) are the eigenvalues of the linear matrix pencil (of dimension )

| (23) |

(i.e., all such that the above matrix is singular), where entries not displayed are zero.

Thus, by finding the eigenvalues of the linear matrix pencil we obtain the solution of a polynomial eigenvalue problem, which is an approximation to the nonlinear eigenvalue problem (20).

4.3 Contour integral method

The following method due to Beyn, (2012) finds nonlinear complex eigenvalues within a given contour . We give the main steps in Algorithm 1 and subsequently discuss the choice of contour.

A few further specifications and comments:

-

1.

In line 2, we choose with the identity matrix and an matrix of zeros.

-

2.

The integrands in line 3 are found by solution of linear systems for .

-

3.

For the linear systems, SVDs and linear eigenvalue problems we use the Matlab default functions.

-

4.

We choose as contours circles with the center and radius . Then, for , and can be approximated by quadrature with nodes,

-

5.

As can be large, for computational stability it is better to shift the coordinates to .

5 Numerical tests

In this section, we discuss the application of the methods in Sections 3 and 4 for solving (20) and give numerical tests.

5.1 Matrix assembly

To compute the elements of , we have to evaluate the integral in (15). We notice that

is analytic on and , where . Then, according to Javed and Trefethen, (2014), the trapezoidal quadrature rule with nodes converges with order with small constant.

An advantage of using the standard trapezoidal rule compared to other, adaptive quadrature rules is that on a fixed grid we can precompute the functions

Therefore, we use only instead of computations of hypergeometric functions, which is an expensive operation.

The elements of grow fast in and due to the term , and for large can become highly inaccurate. We will use the following straightforward result to improve the condition of .

Proposition 1.

Consider non-singular square matrices and . Define . Then, is a nonlinear eigenvalue of if and only if it is a nonlinear eigenvalue of .

Define the matrices as with

Then, the elements of are

| (24) |

Transformation (24) helps to decrease the elements proportionally to the growth rate, where is chosen in the tests as maximum or average value of .

The standard Matlab hypergeometric function is very slow. Therefore, we implemented our own function in C and inserted it into Matlab as mex function.

5.2 Computation of eigenvalues

Now we consider the application of the numerical methods from Section 4 to the truncated problem (20).

Chebyshev approximation of smallest eigenvalue of (Section 4.1).

For this method the application is straightforward, using Cholesky factorisation and chebfun (Driscoll et al., (2014)) to find the local minima.

Chebyshev polynomial interpolation (Section 4.2).

Here, we consider complex eigenvalues and Chebyshev interpolation of is implemented using chebfun (Driscoll et al., (2014)). The resulting generalised linear eigenvalue problem is solved by the default method in Matlab.

Contour integral method (Section 4.3).

To find all (complex) eigenvalues, we have to pick suitable centres and radii to apply Algorithm 1. Based on the empirical observation that the distribution of the eigenvalues is roughly uniform (see Table 1 below), we can choose a fixed radius and increase the centre by slightly under twice that amount to find the next eigenvalue. We discard any eigenvalues found previously due to the overlap of contours. This is summarised in Algorithm 2.

In Tables 1 and 2, we compare the approximate nonlinear eigenvalues and the computational time for different methods (from Section 4) in the semi-analytical approach with those from the finite element method in Lipton and Savescu, (2014). Consider parameters . For the semi-analytical method we take for the approximation of the infinite sum in (16), and quadrature nodes.

| EV | Finite elements | Chebyshev approximation | Contour integrals / |

|---|---|---|---|

| of smallest eigenvalue of | Chebyshev interpolation | ||

| 5.232 | 5.228 | 5.229 (0.028) | |

| 11.805 | 11.787 | 11.787 (0.076) | |

| 16.313 | 16.285 | 16.284 (0.068) | |

| 21.204 | 21.149 | 21.147 (0.151) | |

| 26.184 | 26.112 | 26.109 (0.188) | |

| 33.392 | 33.230 | 33.261 (0.215) | |

| 72.911 | 72.841 | 72.708 (0.731) | |

| 138.087 | 139.421 | 139.391 (1.331) |

| Chebyshev approximation | Chebyshev interpolation of | Contour integrals |

| of smallest eigenvalue of | ||

| 561.17 s | 60.27 s | 220.79 s |

We also compare the numerically computed nonlinear eigenvalues to the analytic expressions in the case (see Appendix B.4), in Table 3. We can see that the semi-analytical method is vastly superior to the finite element method. The semi-analytical method has the advantage in this case that there exists a finite basis and the truncation for the nonlinear eigenvalue problem after sufficiently many, say terms does not change the solution (see Appendix B.4). Here, is chosen large enough so that the remaining errors come predominantly from the approximate solution of the linear eigenvalue problem in the case of the Chebyshev method and the singular value decomposition in the contour integral method.

| EV | Value | Finite elements | Chebyshev approx. | Chebyshev | Contour integrals |

|---|---|---|---|---|---|

| of sm. eig of | interpolation | ||||

| 12.0 | 0.018 | ||||

| 30.0 | 0.097 | ||||

| 30.0 | 0.105 | ||||

| 56.0 | 0.309 | ||||

| 56.0 | 0.353 | ||||

| 90.0 | 0.767 | ||||

| 132.0 | 2.311 | ||||

| 306.0 | 8.896 |

From the numerical experiments we can conclude that the method based on the smallest linear eigenvalue is slow. The methods based on contour integrals and Chebyshev interpolation show the best results. From a computational point of view, Chebyshev interpolation is faster than the contour integral method, because for the latter we have to run the computations several times on different circles, as well as compute numerical integrals along contours.

The complexity of the Chebyshev interpolation method consists of two steps. The first step is the interpolation of in using Chebyshev polynomials as in (22) to obtain a polynomial eigenvalue problem. This can be performed in , where is the number of terms in the eigenvalue expansion and is the dimension of the Chebyshev basis. The second step is to solve the polynomial eigenvalue problem, for which the complexity equals that of the linear eigenvalue decomposition of a matrix of size . Thus, the complexity of the second step is proportional to that of matrix multiplication, i.e., in practice.555Theoretically, algorithms with for are available (see Demmel et al., (2007)), but the constant is found to be too large to be competitive for the matrix size relevant here.

We give an empirical analysis of the CPU time in Table 4. Since the first step has a higher constant factor, it dominates for small , while for large the second step dominates.

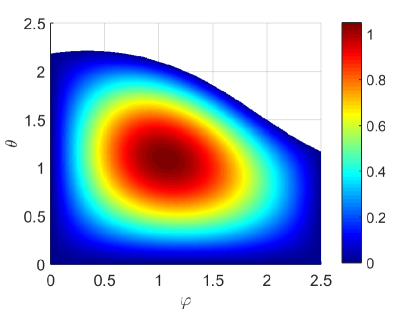

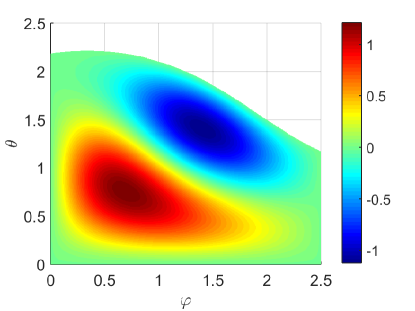

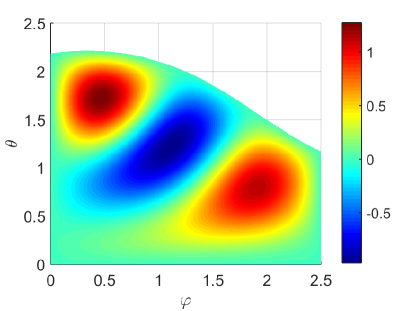

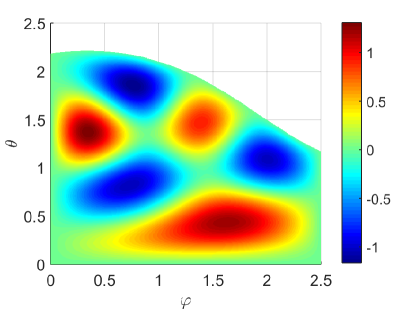

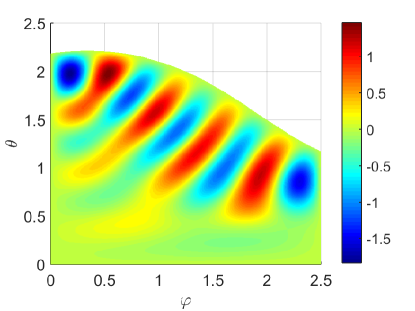

Once we have computed the eigenvalues and the corresponding eigenvectors, we can compute using expression (13). An example of eigenvectors is given in Figure 2, shown in the -plane.

5.3 Convergence of expansion and computational speed

We now focus on the most efficient method, the Chebyshev interpolation method from Section 4.2. To explore the convergence numerically, we compare our results for the Green’s function with the analytical solution available for the special correlation case using a method of images (Escobar et al., (2013)).

It is worth pointing out that we should not expect uniform convergence in , especially as , because the initial condition is a Dirac delta. In applications, the quantity of interest is usually an integral in the space variables of the Green’s function for . It is well-known that for the Green’s function is smoothed. In our experiments, we consider the spatial norm (for fixed ) for comparison.

Our truncated Green’s function approximation has the form

We have several numerical parameters:

- (i)

- (ii)

-

(iii)

, the dimension of the Chebyshev basis in (22) to approximate the nonlinear eigenvalue problem by a polynomial one;

- (iv)

We expect convergence of the approximation as those four parameters go to infinity. This involves in particular that , combined with the terms they are multiplied by, go to zero sufficiently fast as . Moreover, one needs that for fixed the and , which implicitly depend on through the truncation of the infinite-dimensional eigenvalue problem and on and by the approximations made to the finite-dimensional eigenvalue problems, converge as .

In absence of theoretical error estimates, we test this empirically. In our experiments, we choose nodes for the trapezoidal rule for (15); very good tolerance is already achieved with much fewer nodes, however, even for the computational time for these integrals is not very significant (about 10-15% of the total eigenvalue computation procedure).

We now provide three experiments: in each, we fix two of the remaining parameters (, , ) to be large enough and vary the third parameter to compare the Green’s function with the analytical solution. For , in our experiments, further increase of either parameter does not affect the Green’s function’s value beyond the accuracy required here.

The results and computational times are given in Table 4 below666 In order to approximate the error, we compute the Green’s function on a grid covering some and then approximate the error by numerical quadrature by , where is the semi-analytical or numerical solution and the analytical solution from Escobar et al., (2013). . Recall that the infinite-dimensional nonlinear eigenvalue problem (16) is ultimately approximated by the -dimensional generalized linear eigenvalue problem for (23). To investigate the convergence in the number of terms in the expansion, , we choose the smallest out of the resulting eigenvalues and corresponding eigenvectors. As the main computational cost comes from the solution of the eigenvalue problem, which is here identical for all , we do not report computational times for different .

In comparison, using the finite element method from Lipton and Savescu, (2014) with a 1500 point mesh, we get the precision with CPU time 621s. This accuracy is comparable with that of the semi-analytical solution for around 15 and around 7, which is computable within a fraction of a second. Note that the approach of Lipton and Savescu, (2014) requires the solution of a 1500-dimensional (determined by the number of finite elements) generalized linear eigenvalue problem. In our tests, however, the cost was dominated by the construction of the locally refined finite element mesh.

| 10 | 20 | 50 | 80 | 100 | |

| Error | |||||

| CPU time (s) | |||||

| 5 | 10 | 20 | 25 | 30 | |

| Error | |||||

| CPU time (s) | |||||

| 5 | 10 | 20 | 40 | 50 | |

| Error |

As a further benchmark, we present the results for a second order ADI finite-difference method (the Hundsdorfer-Verwer scheme; see Hundsdorfer and Verwer, (2013)) in Table 5 below††footnotemark: . We use up to points in each spatial direction and points in time.

The numerical initial condition is chosen as

in order to approximate the Dirac delta, with the mesh constructed in such a way that coincides with a mesh point. This is a special case of the approximations to non-smooth initial conditions analysed numerically in Pooley et al., (2003) and by means of Fourier methods in Reisinger and Whitley, (2014).

The data in Table 5 show second order convergence in both and .

| 25 | 50 | 100 | |

| Error | |||

| CPU time (s) | |||

| 50 | 100 | 200 | |

| Error | |||

| CPU time (s) |

This test demonstrates the superior accuracy of the semi-analytical solution for relatively few terms in comparison to the ones obtained for the ADI scheme on the highest computationally feasible levels.

It is worth pointing out though that the semi-analytical expression gives the density in a single point, while the finite difference solution is simultaneously obtained on a whole mesh. This is useful, for example, to compute survival probabilities, where one needs to integrate the density (see next section).

6 Applications to default model with mutual liabilities

Diffusions with absorption play a central role in structural credit models. In particular, we investigate in this section such a model of an interconnected banking network with mutual liabilities as in Lipton, (2016). Several papers have considered specific cases of this model. For example, Itkin and Lipton, (2016) considered the special case of two banks without jumps, Kaushansky et al., (2017) considered the case of two banks with negative exponential jumps, and Itkin and Lipton, (2015) considered the cases of two and three banks with a fairly general correlated Lévy process in the jump component.

Here, we study the case of three banks without jumps. The case of three counterparties is of practical importance as it allows us to compute bilateral Credit and Debt Value Adjustments. In the following, we briefly introduce the framework and show how to compute the joint survival probability, as well as CVA and DVA for a CDS.

6.1 Extended default model with mutual liabilities for three banks

We assume that assets are driven by geometric Brownian motion with drift

where is the growth rate, is the corresponding volatility, are correlated standard Brownian motions with correlation . The liabilities are assumed to be deterministic with the same growth rate,

where are the external liabilities of the -th bank, and are interbank liabilities between bank and bank .

If the -th bank defaults at intermediate time , the surviving banks suffer losses due to any of the -th bank’s unpaid net obligations to them and we have to consider a two-dimensional problem with modified boundary conditions. We then change the indexation of the surviving banks by applying the function

We also introduce the inverse function

The corresponding default boundaries are modified to

It is clear that

Thus, and the corresponding default boundaries move to the right.

We need to specify the settlement process at time . We shall do this in the spirit of Eisenberg and Noe, (2001). Since at time full settlement is expected, we assume that bank will pay the fraction of its total liabilities to creditors. This implies that if the bank pays all liabilities (both external and interbank) and survives. On the other hand, if , bank defaults, and pays only a fraction of its liabilities. Thus, we can describe the terminal condition as a system of equations

| (25) |

There is a unique vector such that the condition (25) is satisfied. See Lipton, (2016) for details.

For convenience, we introduce normalized dimensionless variables

where Denote also for . Applying Itô’s formula to , we find its dynamics

In the following, we omit bars for brevity and denote the state variable by . The default boundaries change to

The problems we will consider can all be written in the form

| (26) | ||||

| (27) | ||||

| (28) | ||||

| (29) | ||||

| (30) |

with suitably defined terminal conditions , boundary conditions and right-hand sides , and where the Kolmogorov backward operator is

Once the Green’s function has been constructed numerically for a set of model parameters, prices of different derivatives and hedge parameters can be found as the solution of (26)–(30) by simple convolution of the Green’s function with the appropriate inhomogeneous right-hand sides and boundary data. It is the strength of the Green’s function concept that no further numerical solution of PDEs is required. We illustrate this in the following sections.

6.2 Joint survival probability

The corresponding Kolmogorov backward equation for the joint survival probability is

where is the subset of where all banks survive.

Due to various regulation requirements, assets of large banks cannot drop below their liabilities, which means that their recovery rates should be close to 1. This implies that the domain becomes the positive octant .

The analytical solution for the survival probability in the positive quadrant (i.e., two dimensions) with non-zero drift was recently found by Itkin and Lipton, (2016). Here, we extend this result to three dimensions using the expression for the Green’s function from Section 3 and an expansion in Gegenbauer polynomials.

In this section alone, we use instead of , and instead of , to shorten the notation in the integrals, and similarly for . The solution can then be written as

| (31) |

where , and

Next, we use the idea of exponent representation via ultra-spherical polynomials from Itkin and Lipton, (2016),

where are Gegenbauer polynomials and the parameter can be chosen arbitrarily.

Substituting this representation with into (31), we get

| (32) |

For simplicity we choose and then use the identity (Gradštejn et al., (2007)) for the second integral

| (33) | |||

where is a generalized hypergeometric function.

Moreover, with the Gegenbauer polynomials become the Chebyshev polynomials of the second kind, which admit the representation (Abramowitz and Stegun, (1964))

where is the floor function. Thus, the integral in (32) over can be represented as

| (34) |

As a result, we get the expression for the integral

| (35) |

where the expression for is given in (34) and the expression for in (33).

From a computational point of view, this semi-analytical representation has an advantage in comparison to a direct integration of the Green’s function. Consider parameters and , the limits in the summation (35), and the number of terms in the eigenvalue expansion of . The integrals over can be computed numerically. Since is smooth, we can transform the domain to a rectangle by a smooth change of variables and use a high order integration method such as Gaussian quadrature. We denote by the number of two-dimensional integration nodes. First, we precompute for all on the grid; it can be done with operations. Then, we precompute the integrals in (34), the complexity of which is is . Then, we precompute , with complexity . Finally, we compute (35), using our precomputations, with operations. As a result, overall complexity is . In comparison, the direct integration of the Green’s function with pre-computations of for all gives operations, where is the number of quadrature nodes for the variable , and which requires a truncation at some in order to deal with the improper integral over . Note that (19) is for the de-drifted Green’s function, so that after multiplication by the factor in (2) each term in the sum is a non-trivial function of and no separation structure can be exploited. Usually, the values of and can be chosen relatively small in comparison to for comparable accuracy.

| 1 | 1 | 1 | 0.8 | 0.2 | 0.5 | 0.4 | 0.45 | 0.4 | 1 |

| 60 | 70 | 65 | 10 | 15 | 10 | 10 | 5 | 10 |

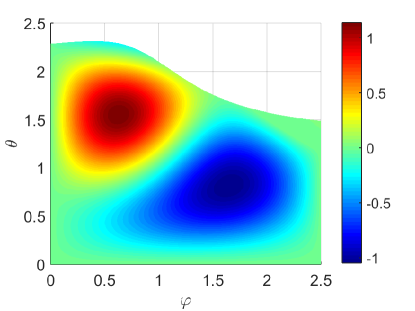

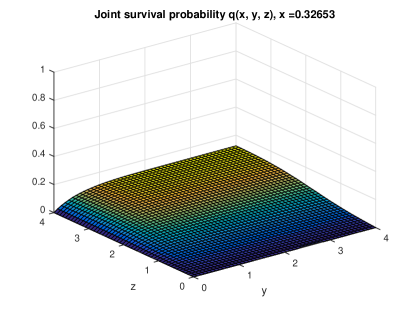

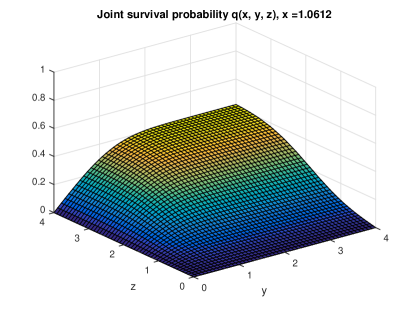

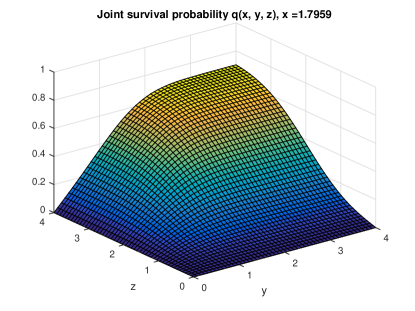

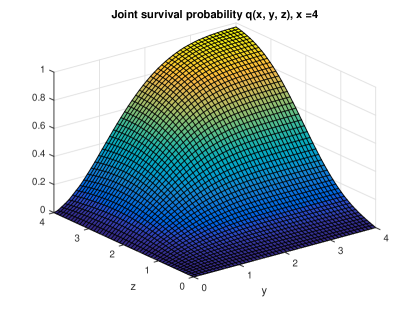

In Figure 3 we show the computed joint survival probabilities as a projection onto the - plane for different values of .

6.3 Computation of Credit and Debt Value Adjustments

In this section, we compute valuation adjustments for credit default swaps (CDS). We associate with the protection seller (PS), with the protection buyer (PB), and with the reference name (RN).

The Credit Value Adjustment (CVA) is the additional cost due to the possibility of the protection seller’s default and can be written as (see Lipton and Savescu, (2014))

where , and are the default times of the protection seller, protection buyer and reference name, respectively, and is the price of a CDS contract on the reference name with non-risky counterparties.

Using Feynman-Kac, we can write the initial-boundary value problem for CVA as

Then, by an application of Green’s formula as in Lipton and Savescu, (2014),

| (36) |

where can be found analytically (Itkin and Lipton, (2016)).

Similarly, the Debt Value Adjustment (DVA) represents the additional benefit associated with the default and is given by

Then, using again the Feynman-Kac formula

Thus,

| (37) |

A distinct advantage of our semi-analytical method is that we can compute the derivative in (36) and (37) analytically as

Therefore, all terms in (36) and (37) can be computed analytically, and CVA can be computed by integration. As the functions are smooth, this can be done with a higher order integration method, such as Gaussian quadrature.

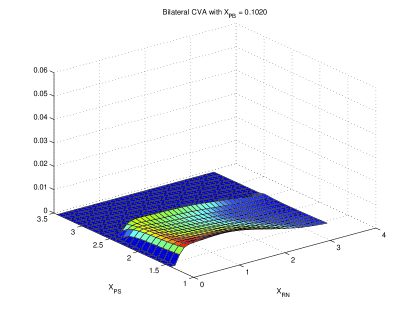

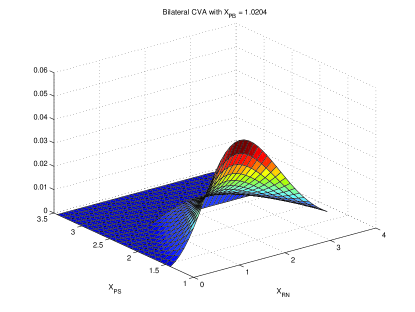

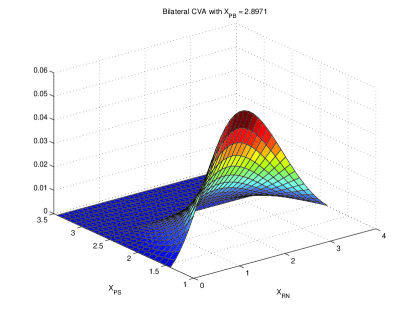

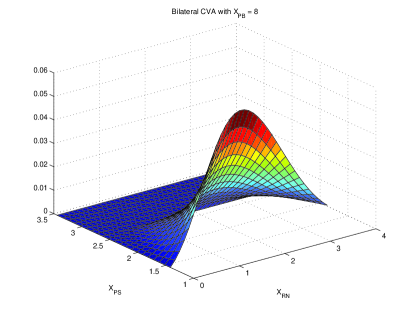

In our computations we use the parameters from Tables 6 and 7. In Figure 4, we then show the computed CVA as a projection on the - plane for different values of .

The CVA decreases with the distance (or ) from the default boundary of the protection seller: the less likely the protection seller is to default, the lower the CVA. In terms of the distance to default (or ) of the reference name, the CVA is highest for intermediate values: if the RN is close to default, it is unlikely that the PS defaults before their CDS liability and the CVA is small; if the RN is far from default, it is unlikely that the protection is payable and again the CVA is small. The CVA mostly increases with the value of the protection buyer (or ) as their default, which is more likely for small , voids the protection payment.

For all three firms, the marginal default probability decreases with the (rescaled, logarithmic) firm value. It increases with the firm’s volatility. The dependence of the CVA on the marginal default probabilities and volatilities is therefore implicitly given by the plots in Figure 4 and we do not show them explicitly for brevity.

The impact of CVA and DVA on CDS prices in this model and its sensitivity to input parameters, specifically and importantly the correlations between the firms, is discussed in more detail in Section 7 of Lipton and Savescu, (2014) (using the finite element approach). The complexity of the integration remains the same in the finite-element method, but, using our semi-analytical method, we compute derivatives in (36) and (37) analytically.

6.4 Comparison with Merton model

In this section, we compare various important characteristics of the model with a simple Merton-style model as in Merton, (1974), where at the terminal time the settlement process is defined in the spirit of Eisenberg and Noe, (2001). The main difference to the above set-up is that there is no continuous default monitoring as in Black and Cox, (1976). As a result, the Green’s function satisfies the following equation

with the boundary and initial conditions

| (39) |

for given .

We compare the results of both models for different sets of correlations. We calibrate the volatilities for the Lipton, (2016) model to individual CDS spreads, while for the Merton model we use individual bond spreads, because they can be easily evaluated as in the original paper Merton, (1974).777For CDSs, one needs to take into account the intermediate payments up to default, but in Merton’s model the default can occur only at the terminal time . For simplicity, we ignore the dependence (through liabilities) between banks for the calibration step, and calibrate them individually.

We choose Unicredit, Santander, and Société Générale as the first, second, and third bank, respectively. The data for external liabilities can be found in banks’ balance sheets, which are publicly available. Usually, mutual liabilities data are not public information, thus we make the assumption as in Kaushansky et al., (2017) that they are a fixed proportion of the total liabilities, namely 5% here. An asset’s value is the sum of liabilities and equity price.

In Table 8, we provide all assets and liabilities . We take 5-year CDS/bond spread data from Bloomberg. The results of the calibration are given in Table 9. As expected, a higher volatility is needed in the Merton model than for continuous default monitoring to give the same default probabilities and hence credit spreads.

| 346.58 | 362.96 | 89.67 | 96.37 | 1607.21 | 1654.38 |

| Model | |||

|---|---|---|---|

| Lipton, (2016) | 0.0179 | 0.0231 | 0.0105 |

| Merton | 0.0194 | 0.0245 | 0.0118 |

Now we consider several sets of parameters for the correlations along with the calibrated volatilities and present the resulting joint survival probabilities in Table 10. The most striking observation is that while volatilities have been calibrated to give the same marginal survival probabilities, the Merton model now consistently underestimates the joint survival probabilities relative to the continuously monitored model. Had we used the same volatilities for both models, it is clear that the Merton model would have overestimates the joint survival probabilities.

| Set | Lipton, (2016) | Merton | |||

|---|---|---|---|---|---|

| 1 | 0.0 | 0.0 | 0.0 | 0.6776 | 0.6316 |

| 2 | 0.8 | 0.2 | 0.5 | 0.7542 | 0.7165 |

| 3 | 0.2 | -0.1 | -0.6 | 0.6739 | 0.6226 |

| 4 | 0.5 | 0.5 | 0.5 | 0.7428 | 0.7060 |

| 5 | 0.1 | -0.1 | -0.2 | 0.6726 | 0.6249 |

7 Conclusion

We have found a semi-analytical formula for the three-dimensional transition probability of Brownian motion in the positive octant with absorbing boundaries. The density is hereby represented as a series of special functions containing unknown parameters, which can be found as the solution of a nonlinear eigenvalue problem.

Applying the results to an extended default model of Lipton, (2016) for three banks, we obtained expressions for joint survival probability, CVA and DVA for a CDS.

This study of the three-dimensional case raised a number of open questions: (i) Establishing the speed of convergence of the solution as the truncation index increases, and finding computable error estimates, would be valuable. (ii) Numerical tests suggest that the nonlinear eigenvalues of are also nonlinear eigenvalues of , the derivative of with respect to the parameter . It would be interesting to investigate this analytically. (iii) In the uncorrelated case, the -th eigenvalue has multiplicity (see the last example in Appendix B), while in the tests with non-zero correlations the eigenvalues are fairly evenly spaced with multiplicity 1 (see Table 1). The transition from one case to the other merits further investigation.

A similar approach may in principle be possible in more than three dimensions. For an -dimensional transition probability, separation into spherical coordinates, i.e. the radius and angles, can be applied as in the three-dimensional case. In the four-dimensional case specifically, preliminary computations suggest that a similar representation by special functions can be found. This involves finding two nested sequences of nonlinear eigenvalues, i.e. for each nonlinear eigenvalue as in (16) a further infinite-dimensional eigenvalue problem has to be solved, in order to match the zero boundary conditions. The main question here is the complexity and accuracy of the method. We leave this question and the -dimensional problem for future research.

Appendix A Elimination of the cross-derivatives and drift terms

The correlation matrix of the Brownian motion is positive definite and has the form

Then equation (1) can be rewritten as

| (41) |

with the boundary and initial conditions

for given .

To eliminate the cross-derivatives, we introduce the following change of variables (Lipton et al., (2014), Lipton and Savescu, (2014))

where and . It transforms the equation (41) to

| (42) |

with zero boundary conditions on the new domain

where

and where

Now we can eliminate the drift term by considering from (2), which satisfies the following PDE

with zero boundary conditions on .

We omit tilde for convenience in the following. In order to take advantage of the wedge-shape of the domain, we change the variables to spherical coordinates

where varies from 0 to . In order to determine the range of values of , we project and onto the plane and get normalized vectors

Appendix B Schrödinger equation with Pöschl–Teller potential

Consider the Schrödinger equation with Pöschl–Teller potential on a half-line,

| (43) |

and boundary condition

| (44) |

B.1 Fundamental solution

We follow Flügge, (2012) for the solution of (43). Consider the change of variables . Then, (43) can be rewritten as

Then, if we consider , we get the hypergeometric equation

The solution of this equation is

where

As a fundamental system we consider standard odd and even real solutions:

where is the Gaussian hypergeometric function.

Any solution can be represented as a linear combination of the fundamental system,

| (45) |

Now consider an asymptotic expansion for large . Unlike Flügge, (2012), who consider the asymptotics at (see the case below), if is bounded above, we only consider the asymptotics at .

B.2 General boundary conditions

From the known expansion of the hypergeometric function we get

and

Assume . First, consider the case . Thus, is singular and satisfies the condition (44). Similar, if , then is singular and satisfies the condition (44).

Hence, in order to satisfy the condition (44) we can choose

B.3 Special case , , i.e.

Consider first the case when is unbounded. Now we have to take into account also the asymptotics at . We note that and . The first term in and goes to infinity unless and are singular, respectively. The gamma function is singular if the argument is a negative integer. Thus,

and

B.4 Special case , i.e.

In this case . We can easily see that and for any and . Thus, . Now we want to find the corresponding eigenvalues. Applying boundary condition (44), we get

and the corresponding eigenvectors are

where .

References

- Abramowitz and Stegun, (1964) Abramowitz, M. and Stegun, I. A. (1964). Handbook of mathematical functions: with formulas, graphs, and mathematical tables, volume 55. Courier Corporation.

- Beyn, (2012) Beyn, W.-J. (2012). An integral method for solving nonlinear eigenvalue problems. Linear Algebra and its Applications, 436(10):3839–3863.

- Black and Cox, (1976) Black, F. and Cox, J. C. (1976). Valuing corporate securities: Some effects of bond indenture provisions. The Journal of Finance, 31(2):351–367.

- Cont and De Larrard, (2012) Cont, R. and De Larrard, A. (2012). Order book dynamics in liquid markets: limit theorems and diffusion approximations. Preprint, arXiv:1202.6412 [q-fin.TR].

- Demmel et al., (2007) Demmel, J., Dumitriu, I., and Holtz, O. (2007). Fast linear algebra is stable. Numerische Mathematik, 108(1):59–91.

- Driscoll et al., (2014) Driscoll, T. A., Hale, N., and Trefethen, L. N. (2014). Chebfun guide. Pafnuty Publ.

- Eisenberg and Noe, (2001) Eisenberg, L. and Noe, T. H. (2001). Systemic risk in financial systems. Management Science, 47(2):236–249.

- Escobar et al., (2013) Escobar, M., Ferrando, S., and Wen, X. (2013). Three dimensional distribution of Brownian motion extrema. Stochastics: An International Journal of Probability and Stochastic Processes, 85(5):807–832.

- Escobar et al., (2014) Escobar, M., Ferrando, S., and Wen, X. (2014). Barrier options in three dimensions. International Journal of Financial Markets and Derivatives, 3(3):260–292.

- Flügge, (2012) Flügge, S. (2012). Practical quantum mechanics. Springer Science & Business Media.

- Gradštejn et al., (2007) Gradštejn, I. S., Ryžik, I. M., Jeffrey, A., and Zwillinger, D. (2007). Table of integrals, series, and products. Elsevier/Academic Press.

- He et al., (1998) He, H., Keirstead, W. P., and Rebholz, J. (1998). Double lookbacks. Mathematical Finance, 8(3):201–228.

- Hundsdorfer and Verwer, (2013) Hundsdorfer, W. and Verwer, J. G. (2013). Numerical solution of time-dependent advection-diffusion-reaction equations, volume 33. Springer Science & Business Media.

- Itkin and Lipton, (2015) Itkin, A. and Lipton, A. (2015). Efficient solution of structural default models with correlated jumps and mutual obligations. International Journal of Computer Mathematics, 92(12):2380–2405.

- Itkin and Lipton, (2016) Itkin, A. and Lipton, A. (2016). Structural default model with mutual obligations. Review of Derivatives Research. doi: 10.1007/s11147-016-9123-1.

- Javed and Trefethen, (2014) Javed, M. and Trefethen, L. N. (2014). A trapezoidal rule error bound unifying the Euler–Maclaurin formula and geometric convergence for periodic functions. Proceedings of the Royal Society A, 470(2161):20130571.

- Kaushansky et al., (2017) Kaushansky, V., Lipton, A., and Reisinger, C. (2017). Numerical analysis of an extended structural default model with mutual liabilities and jump risk. Journal of Computational Science.

- Lipton, (2001) Lipton, A. (2001). Mathematical Methods For Foreign Exchange: A Financial Engineer’s Approach. World Scientific.

- Lipton, (2016) Lipton, A. (2016). Modern monetary circuit theory, stability of interconnected banking network, and balance sheet optimization for individual banks. International Journal of Theoretical and Applied Finance, 19(06). doi: 10.1142/S0219024916500345.

- Lipton et al., (2014) Lipton, A., Pesavento, U., and Sotiropoulos, M. (2014). Trading strategies via book imbalance. Risk, pages 70–75.

- Lipton and Savescu, (2014) Lipton, A. and Savescu, I. (2014). Pricing credit default swaps with bilateral value adjustments. Quantitative Finance, 14(1):171–188.

- Lipton and Sepp, (2009) Lipton, A. and Sepp, A. (2009). Credit value adjustment for credit default swaps via the structural default model. The Journal of Credit Risk, 5(2):123–146.

- Lipton and Sepp, (2013) Lipton, A. and Sepp, A. (2013). Credit value adjustment in the extended structural default model. In Lipton, A. and Rennie, A., editors, The Oxford Handbook of Credit Derivatives, chapter 12, pages 406–463. Oxford University Press.

- Mehrmann and Voss, (2004) Mehrmann, V. and Voss, H. (2004). Nonlinear eigenvalue problems: A challenge for modern eigenvalue methods. GAMM-Mitteilungen, 27(2):121–152.

- Merton, (1974) Merton, R. C. (1974). On the pricing of corporate debt: The risk structure of interest rates. The Journal of Finance, 29(2):449–470.

- Nakatsukasa et al., (2015) Nakatsukasa, Y., Noferini, V., and Townsend, A. (2015). Computing the common zeros of two bivariate functions via bézout resultants. Numerische Mathematik, 129(1):181–209.

- Pooley et al., (2003) Pooley, D. M., Vetzal, K. R., and Forsyth, P. A. (2003). Convergence remedies for non-smooth payoffs in option pricing. Journal of Computational Finance, 6(4):25–40.

- Reisinger and Whitley, (2014) Reisinger, C. and Whitley, A. (2014). The impact of a natural time change on the convergence of the Crank–Nicolson scheme. IMA Journal of Numerical Analysis, 34(3):1156–1192.

- Trefethen, (2013) Trefethen, L. N. (2013). Approximation Theory and Approximation Practice. SIAM, Philadelphia.

- Zhou, (2001) Zhou, C. (2001). The term structure of credit spreads with jump risk. Journal of Banking & Finance, 25(11):2015–2040.