Double continuation regions for American and Swing options with negative discount rate in Lévy models

Abstract.

In this paper we study perpetual American call and put options in an exponential Lévy model. We consider a negative effective discount rate which arises in a number of financial applications including stock loans and real options, where the strike price can potentially grow at a higher rate than the original discount factor. We show that in this case a double continuation region arises and we identify the two critical prices. We also generalize this result to multiple stopping problems of Swing type, that is, when successive exercise opportunities are separated by i.i.d. random refraction times. We conduct an extensive numerical analysis for the Black-Scholes model and the jump-diffusion model with exponentially distributed jumps.

Keywords. American option negative rate optimal stopping Lévy process

1. Introduction

In this paper, we study the optimal stopping problem

| (1.1) |

for the asset price

where is an asymmetric Lévy process, or , is a family of stopping times with respect to the right-continuous augmentation of the natural filtration of satisfying usual conditions, but, in contrast to the standard assumption, we take . When , corresponding to the case where early stopping is suboptimal, we use the convention that . In a financial market context, the solution of this problem is the price of a perpetual American option, in a Lévy market with a negative interest rate. Our analysis is then extended to a more general type of American options, called Swing options, which allow for multiple exercise opportunities separated by i.i.d. random refraction times.

The non-standard assumption of negative discount rate has received some attention in the last few years because several decision-making problems in finance fall under that umbrella.

One of the main example concerns gold loans. After the financial crisis, collateralized borrowing has increased. Treasury bonds and stocks are the collateral usually accepted by financial institutions, but gold is increasingly being used around the world; see [Cui and Hoyle (2011)]. Major Indian non-banking financial companies, like Muthoot Finance and Manappuram Finance, have been quite active in lending against gold collateral. As [Churiwal and Shreni (2012)] report in their survey of the Indian gold loan market, gold loans tend to have short maturities and rather high spreads (borrowing rate minus risk-free rate), even if significantly lower than without collateral. The prepayment option is common, permitting the redemption of the gold at any time before maturity. In a gold loan, a borrower receives at time (the date of contract inception) a loan amount using one mass unit (one troy ounce, say) of gold as collateral, which must be physically delivered to a lender. This amount grows at the constant borrowing rate , stipulated in the contract (and usually higher than the risk-free rate ). The cost of reimbursing the loan at time is thus given by . When paying back the loan, the borrower redeems the gold and the contract is terminated. In our model, we assume that the costs of storing and insuring gold holdings are per unit of time, where is the gold spot price, which dynamics is governed by an exponential Lévy process; specifically,

where is a Lévy process, that is a càdlàg process whose increments in non–overlapping time intervals are independent and stationary. The dynamics of under the risk-neutral measure is such that the discounted price is a martingale, that is ; see e.g. [Hull (2011)]. If, as a first step in the analysis, we assume that redemption can be done at any time (perpetual contract), the value of the contract, with infinite maturity date, at time is

for ,

and being a Lévy process satisfying

| (1.2) |

Thus this price equals the initial value of a perpetual American call option, that is (1.1) with , calculated with respect to the martingale measure, hence satisfying (1.2). Data from the [Gold World Council] show that the daily log change in the gold spot price, expressed in Indian rupees, has registered an annualized historical volatility of % over the period from the 3rd of January 1979 to the 5th of May 2013. Average storage/insurance costs are about % and other parameters can be chosen as follows %, % and %. Then, in this case, we have

namely, a negative discounting rate.

There are many other financial products where a negative rate appears. For example, [Xia and Zhou (2007)] consider a stock loan, which is similar to the above gold loan, but here a stock is used as collateral and can be redeemed at any time if it is convenient for the borrower. Such a contract can be reduced to a perpetual American put option with a possibly negative interest rate, given by the difference between the market interest rate and the loan rate. Indeed, if an investor lends at time an amount with interest rate and he/she gets as collateral some stock with the price , then the value of stock loan is given by

| (1.3) |

where is a risk-free interest rate. The essential difference between the above instrument and a classical American put option is the time-dependent strike price. We can still rewrite problem (1.3) into an American put option form as follows:

| (1.4) |

where for and may appear to be negative.

In the context of real options, [Battauz et al. (2012), Battauz et al. (2014)] consider an optimal investment problem: a firm must decide when to invest in a single project and both the value of the project and the cost of entering it are stochastic. This problem is reduced to the valuation of an American put option where the underlying is the ratio between the stochastic cost and the present value of the project (cost-to-value ratio) and the strike price is equal to 1. The interest rate is negative if the growth rate of the project’s present value dominates the discount rate. When the cost of the investment is constant it is always convenient for the firm to wait and early exercise never occurs (see, for instance, [Dixit et al.(1993)]), thus this case is usually neglected. On the other hand, it turns out that the presence of a stochastic cost makes the problem relevant, because it may imply the existence of a well-defined exercise region. As a last example where a negative interest rate may appear, we recall the presence nowadays of markets with a domestic non-positive short rate (as the Euro or the Yen denominated market): in [Battauz et al. (2017)], American quanto options (put or call options written on a foreign security) are analyzed in such markets.

In [Xia and Zhou (2007)] and [Battauz et al. (2012), Battauz et al. (2014), Battauz et al. (2017)], the question of the pricing and the identification of the exercise region for American options with negative interest rate has been extensively studied under the assumption that the price of the underlying evolves according to a geometric Brownian motion. In particular, [Battauz et al. (2012), Battauz et al. (2014), Battauz et al. (2017)] show that when the coefficients satisfy some special conditions, a nonstandard double continuation region appears: exercise is optimally postponed not only when the option is not sufficiently in the money but also when the option is too deep in the money. They explicitly characterize the value function and the two critical prices which delimit the exercise region in the perpetual case, and study the properties of the time-dependent boundaries in the finite-maturity case. A double continuation region can also appear with positive interest rate in the case of capped options. See [Broadie and Detemple (1995)] for the case of a capped option with growing cap, and [Detemple and Kitapbayev (2018)] for the case of a capped option with two-level cap.

Our aim is to extend this analysis to a Lévy market. It is well-known that the dynamics of securities in a financial market is described more accurately by processes with jumps. Indeed, several empirical studies show that the log-prices of stocks have a heavier left tail than the normal distribution, on which the seminal Black-Scholes model is founded. The introduction of jumps in a financial market dates back to [Merton (1976)], who added a compound Poisson process to the standard Brownian motion to better describe the dynamics of the logarithm of an asset. Since then, many papers have been written about the use of general Lévy processes in the modeling of financial markets and in the pricing of derivatives (see for instance [Cont and Tankov (2003), Schoutens (2003)]). Among the most recent examples of Lévy processes used in modeling the evolution of the stock price process we refer to the normal inverse Gaussian model of [Nielssen (1998)], the hyperbolic model of [Eberlein and Keller (1995)], the variance gamma model of [Madan and Seneta (1990)], the CGMY model of [Carr et al. (2002)], and the tempered stable process first introduced by [Koponen (1995)] and extended by [Boyarchenko and Levendorskii (2002)].

American options in Lévy markets have been studied in many papers. [Aase (2010)] studies perpetual put options and characterizes the continuation region in a jump-diffusion model. In a general Lévy market, [Mordecki (2002)] obtains closed formulas for the price of the perpetual call and put options and their critical prices, in terms of the law of the supremum and the infimum of a Lévy process. [Boyarchenko and Levendorskii (2002)] exploit the Wiener-Hopf factorization and analytical methods to derive closed formulas for a large class of Lévy processes and find explicit expressions in some special cases. [Asmussen et al. (2004)] also use the Wiener-Hopf factorization to compute the price of American put options but concentrate on Lévy processes with two-sided phase-type jumps. [Baurdoux and Kyprianou (2008)] use fluctuation theory to give an alternative proof of Mordecki’s result; see also [Baurdoux (2007)], and [Alili and Kyprianou (2005)], and references therein.

A major technique that has been widely used in the theory of optimal stopping

problems driven by diffusion processes is the free boundary formulation for the value

function and the optimal boundary. The free boundary formulation consists primarily of a partial differential equation and (among other boundary conditions) the continuous

and smooth pasting conditions used to determine the unknown boundary and

specify the value function; see [Peskir and Shiryaev (2006)].

In the context of the Lévy market,

[Surya (2007)] gives sufficient and

necessary conditions for the continuous and smooth pasting conditions (see also [Lamberton and Mikou (2012)]): in particular, the assumption of non zero volatility turns out to be fundamental.

A special case when the diffusion of the underlying process is degenerate has been also considered e.g. in [Alvarez and Tourin (1996), Boyarchenko and Levendorskii (2002), Cont and Tankov (2003), Kyprianou and Surya (2007)],

[Lamberton and Mikou (2012)].

Another particular case of Lévy market with nonzero volatility is the jump-diffusion market.

For this scenario, both the methods of variational inequalities and viscosity solutions of the boundary value problem have been used to study American options; see

e.g. [Lamberton and Mikou (2012), Pham (1997), Pham (1998)]. We also refer to section 7 in [Detemple (2014)], for a general survey on American option in the jump-diffusion model and other references.

In this paper we propose a new approach to the pricing of American options. To illustrate it, let us focus on the put option. The price of the perpetual option is a convex function of the initial value of the underlying , and, when tends to 0, the price goes to if the interest rate is non-negative, otherwise goes to infinity. Moreover it always dominates the payoff function and coincides with it on the exercise region. Therefore, if it is optimal to early exercise, we can derive either a single continuation region (when the interest rate is non-negative, the stopping region is a half-line) or a double continuation region (when the interest rate is negative, hence the stopping region is an interval). Our approach consists in considering all possible pairs of critical prices which may delimit the exercise region and maximize the value function over them: so doing, we derive necessary and sufficient conditions for the existence of a double continuation region.

To compute the two critical prices which delimit the stopping region, we need to calculate the Laplace transform of the entrance time of a closed interval. This is a non-standard problem in the context of Lévy processes because they may jump over the interval without entering it. Still, we manage to solve this problem for one-sided Lévy processes, that is, for Lévy processes either without positive jumps (so-called spectrally negative Lévy processes) or without negative jumps (so-called spectrally positive Lévy processes).

The assumption of one-sided jumps in a Lévy market is quite common in financial modeling. It appears, for example, in [Baurdoux and Kyprianou (2008)], [Baurdoux (2007)], [Surya (2007)], [Alili and Kyprianou (2005)], [Avram et al. (2004)], and [Chan (2005)]. Moreover, it can be also found in [Gerber and Shiu (1998)], who exploit it to compute prices and optimal exercise strategies for the perpetual American put option in a jump-diffusion model, and in [Chesney and Jeanblanc (2004)], who evaluate currency American options. Similarly, [Barrieu and Bellamy (2005)] analyze an investment problem in a jump-diffusion framework through a real option approach: they formulate it as an American call option problem on the ratio between the project value and the cost, which is assumed to jump only downwards, to represent a market crisis.

A core instrument in the fluctuation theory of completely asymmetric Lévy processes are the so-called scale functions, which are usually exploited in the study of exit problems. For our entrance problem, we derive equations determining both ends of the stopping interval and the price of the American option in terms of these functions. Later, we analyze in details two cases, the Black-Scholes market and the jump-diffusion market with exponential jumps, where explicit solution and an extensive numerical analysis can be conducted.

We underline that the new method presented in this paper does not require the smooth-fit condition. Still, we prove that it holds in our case. The most general conditions for smooth fit follow from the arguments given in [Lamberton and Mikou (2012), Thms. 4.1, 5.1 and 5.2] which are based on the variational inequality approach. Under the more restrictive assumption that volatility is strictly positive () we give a new proof of this fact based on the extended version of Itô’s formula for Lévy processes that involves a local time on a curve separating two regions to account for possible jumps over it; see [Eisenbaum (2006)], [Eisenbaum and Kyprianou (2008)], [Peskir (2005)], [Surya (2007)]. Note that this approach is different from the one used in most of the papers, where this condition is used to determine the unknown boundary and is also used as a ’rule of thumb’; see [Peskir and Shiryaev (2006), p. 49]. It appears that the assumption of regularity of for is crucial here; indeed [Surya (2007)] and [Lamberton and Mikou (2012)] show that without this assumption the smooth-fit condition is not valid in an asymmetric Lévy market for .

The above results for American put options can be transformed into results for American call options using the so-called put-call symmetry formula. Another contribution of this paper is to show that indeed the put-call symmetry formula holds in our, Lévy framework with negative discount rate, case, and a dual relation between the two free boundaries of the call and the put options can be derived. Our finding supplements [Fajardo and Mordecki (2006)] and, independently, [Eberlein and Papantaleon (2005)] who extend to the Lévy market the findings by [Carr and Chesney (1996)], under the assumption of a non-negative interest rate. An analogous result for the negative discounting rate case is obtained in [Battauz et al. (2014)] in the Black and Scholes market. An interesting remark is due here: the symmetry formula shows that for some set of parameters one can observe the double continuation region also for the American call option. However, there are also some cases when a single continuation region appears, in spite of the assumption of a negative interest rate . This occurs when the dividend rate is strictly positive, which is the case considered for instance by [Xia and Zhou (2007)]. In Section 6, Tables 1 and 2, we collect all the possible cases for the put and call option in the Black and Scholes market to give a complete picture.

A further result of this paper is the generalization of the above results to multiple stopping problems of Swing type, that is when successive exercise opportunities are possible and are separated by i.i.d. random refraction times. These multiple stopping rules might appear when the same option can be exercised repeatedly in the future, meaning that an investor can acquire a series of stock loans, or a firm can make an investment sequentially over time. The features of refraction periods and multiple exercises also arise in the pricing of Swing options commonly used for energy delivery. For instance, [Carmona and Touzi (2008)] formulate the valuation of a Swing put option as an optimal multiple stopping problem, with constant refraction periods, under the geometric Brownian motion model. In a related study, [Zeghal and Mnif (2006)] value a perpetual American Swing put when the underlying Lévy price process has no negative jumps. [Leung et al. (2015)] consider call Swing options, under the assumption of a negative effective discount rate, and, as in the case of [Xia and Zhou (2007)], they derive single continuation regions. Again this is a consequence of Assumption 2.1 made in [Leung et al. (2015)] that corresponds to the case when and in Table 2 given in Section 6. Therefore, in contrast to [Leung et al. (2015)], we describe a complementary case of double continuation regions.

The paper is organized as follows. In Section 2 we introduce basic facts concerning asymmetric, and in particular, spectrally negative, Lévy markets. In Section 3 we compute the price of the American put option for completely asymmetric log Lévy prices and identify possibly double continuation region in this case. Section 4 deals with the Swing put options. Section 5 presents a put-call symmetry formula for a Lévy market with a negative discounting rate, which allows for the extension of the previous results to call options and Swing call options. Finally, in Section 6 we give an extensive numerical analysis and in Section 7 we summarize our results and propose possible generalizations.

2. Lévy-type financial market

We model the logarithm of the underlying asset price by a completely asymmetric Lévy process, that is a stationary stochastic process with independent increments, right-continuous paths, with left limits for which all jumps have the same sign. Throughout the paper, we will use the following notation: because we mainly consider a spectrally negative Lévy process, that is a process with only downward jumps, we denote it simply with ; a spectrally positive process will be denoted by (note that where is spectrally negative); lastly, we denote by a generic asymmetric Lévy process. More generally, when using the basic notation we refer to spectrally negative processes; a ”hat” means that we are dealing with spectrally positive processes and a ”tilde” with general asymmetric processes. So, for instance, the process

is the geometric Lévy process, which describes the price of the underlying with spectrally negative. The asset price process corresponding to the spectrally positive case is , whereas equals or depending on the scenario of the support of jumps.

We start from defining the Laplace exponent of a completely asymmetric Lévy process

which is well defined for for the spectrally negative case due to the non-positive jumps and for for the spectrally positive case due to the non-negative jumps. By the Lévy-Khintchine theorem, for , and a Lévy measure defined on such that

we have

| (2.1) |

It is easily shown that is zero at the origin, tends to infinity at infinity and it is strictly convex. We denote

where is the last (going from the left hand side) asymptote of .

We will choose for which is well-defined. An important tool in the theory of spectrally negative Lévy processes, which we will exploit to express our results, is the so-called scale function. For a spectrally negative process , with Laplace exponent , we define the first scale function as the unique continuous and strictly increasing function on with the following Laplace transform:

where is a Laplace exponent of . The classical definition for scale function is given for . Note that this definition may be extended to (see [Kyprianou (2006), Lemma 8.3]). In particular, we can consider the case of . The function has left and right derivatives on . Throughout the paper we assume that X has unbounded variation or the jump measure is absolutely continuous with respect to the Lebesgue measure. In that case,

| (2.2) |

see [Kyprianou et al. (2013), Lem. 2.4, p. 117].

From now on, we further assume that the underlying process is calculated under the martingale measure (see [Cont and Tankov (2003), Prop. 9.9]). Under this measure the discounted price process is a martingale and by definition of the Laplace exponent the process is also a martingale. Thus, under , we have

| (2.3) |

for given in (2.1), being a discounting rate and being a dividend payment intensity or, if negative, borrowing rate or just the costs of storing depending on applications.

Lastly, because we will use identities related to the first passage times above and below some level, we give the following definitions:

| (2.4) |

We will denote by the family of all stopping times with respect to the right-continuous augmentation of the natural filtration of (or depending on the analyzed case) satisfying the usual conditions.

We conclude this preliminary section introducing the following notational convention:

, , are the corresponding expectations to the above measures.

3. American put option

We start from the evaluation of the perpetual American put option with negative discounting rate for both the spectrally negative and spectrally positive cases. The problem for the spectrally negative case is defined in (1.4); for the spectrally positive case, according to our notation, we will write

To make the problem of pricing well-defined we assume throughout this paper that

| (3.1) |

The next lemma gives a sufficient condition for (3.1) to hold true.

Lemma 1.

Proof.

We prove only the spectrally negative case. The proof of the spectrally positive case is very similar. According to [Kyprianou (2006), Theorem 7.2], if , then

As is geometric Lévy process, then the above limit implies that also tends to infinity as goes to infinity. Thus, the payoff at equals 0 and it is not optimal to stop there anymore. Now, as for the discounting factor is finite. Indeed, by [Kyprianou (2006)] we have

Now, by [Baurdoux (2009), Thm 2] we know that is finite as long as is well-defined which we assumed in Section 2. This observation together with the boundness of the payoff function give the condition (3.1). ∎

Following [Battauz et al. (2012)] which deals with the Black-Scholes model, that is when is an arithmetic Brownian motion, we will show that in the completely asymmetric Lévy market the optimal stopping rule has the following interval-type form:

| (3.2) |

for some , and , namely it is an entrance time. This means that an investor should exercise the option whenever the price process enters the interval . One can give heuristic arguments for the above choice of the optimal stopping time. It is never optimal to exercise early if because the payoff function is then equal to 0. Thus one would wait until the process falls below some level . On the other side, if then for the value of the American put option dominates the payoff function, because, when , . This means that the price of the underlying asset cannot be too small. Thus, if it is optimal to exercise early, then the stopping region is for some optimal levels and .

Formally, the structure (3.2) of the stopping region follows from the following fact which can be of own interest.

Lemma 2.

The value function is non-increasing, convex (and hence continuous) on the open set and the optimal stopping rule has the form (3.2).

Proof.

Because the payoff function of the put option is continuous, by [Peskir and Shiryaev (2006), Thm. 2.2, p. 29, Cor. 2.9, p. 46, Rem. 2.10, p. 48 and (2.2.80), p. 49] the optimal stopping rule is given by

| (3.3) |

To identify its special form, observe that the European option price is strictly convex in the underlying asset . Indeed, first observe that from its definition this price is continuous. Then from classical mollifying arguments without loss of generality we can assume that this price is also differentiable. In the last step we follow [Bergman et al. (1996)] heavily using fact that log price in our case depends linearly on the initial position of the process . Now, following the proof of [Ekström (2004), Cor. 2.6] (taking the maturity tending to infinity at the last step), we can conclude that is also convex. By definition is also non-increasing. Besides it, can not smoothly paste to zero for . Indeed, by our assumptions we have for any because

This implies that the function and the payoff function can cross each other at most two times. In other words, the stopping region has to be an interval or a half-line. ∎

Remark 1.

In this paper we decided to deal only with the infinite time horizon case but part of the results hold true for the finite maturity case as well. For example, defining

for maturity , where is the set of stopping times satisfying , following [Ekström (2004)] one can show that is non increasing and convex with respect to (see also [Lamberton and Mikou (2012), Prop. 2.2]. As and for negative , if the infinite maturity option has an exercise region of the form , then has an exercise region (depending on ) of the form with .

If, as in our case, , then the function is strictly greater than when is close to 0, therefore the stopping region is necessarily an interval. To identify the optimal levels and , we have to calculate the value function for the stopping rule (3.2). Note that these arguments hold for any Lévy process. The additional assumption of one-sided jumps allows for explicitly computing the value function. Let

for

In the following lemma we express the function and in terms of the scale function of the process for the spectrally negative case and of the process for the spectrally positive case.

Lemma 3.

Let be a spectrally negative Lévy process. Assume that is well-defined and .

(i) Then the function is given by

| (3.4) | ||||

where

is a resolvent density of the process killed on exiting .

(ii) Then for the spectrally positive Lévy process we have

Proof.

To prove the first case (i) note that we can consider only . Indeed, if , then the payoff is zero because . This cannot produce the optimal value since waiting longer gives a nonzero payoff. With this assumption we may rewrite the value function as follows

As the process is spectrally negative, when it starts below , it enters the interval in a continuous way and hence . Thus for we get

The first expectation given above is the solution to the so-called one-sided exit problem and is a well known identity for Lévy processes (see [Kyprianou (2006), Theorem 8.1]).

If , then there are two cases: either the underlying process enters the interval going downward or the process jumps from to and after that enters , that is, it enters creeping upward. Note that it is impossible that jumps from to and after that goes back to because it has only downward jumps. We may separate this two cases in the function as follows

| (3.5) |

The first term in the right-hand side equation corresponds to the case when the process enters the interval through jump or by creeping downwards to level . This last case is possible when (see [Kyprianou (2006), Exercise 7.6]). Thus

The joint law for the first passage below and the position at this time are given in [Kyprianou (2006), Chapter 8.4]

| (3.6) | |||

The second formula above is well-defined because by (2.2) the derivative of the scale function exists.

The second term in the right-hand side of equation (3.5) refers to the case where the process firstly jumps from to and, after that, enters . Note that when the process jumps below level , it creeps upward starting from . Hence

Applying the joint law for given earlier in (3.6) we get the assertion for .

Obviously, when then the first moment when process enters happens immediately, i.e. and the value is . This completes the proof of the part (i). The proof of the case (ii) is similar. ∎

We sum up our findings in the following theorem.

Theorem 1.

Assume that the value functions and calculated in Lemma 3 for spectrally negative and spectrally positive log asset Lévy price process respectively admits unique maximizers and . Then the stopping set for the American put option with negative interest rate in a completely asymmetric Lévy market is not empty and the optimal stopping rule, which is finite, is given in (3.2) for and . The prices of the perpetual American option in the two cases are respectively

Traditionally, the optimal stopping regions are identified using the continuous and smooth fit conditions. Though we do not need them to prove our results, we show in the following proposition that in fact under mild assumptions the optimal levels and satisfy these conditions.

Proposition 1.

Assume that the optimal stopping rule is finite, that is, the stopping region is non-empty. Consider the following smooth and continuous fit conditions:

(i) The optimal value function of the perpetual American put option for a completely asymmetric Lévy process always satisfies continuous fit conditions.

(ii) If is regular for , then the smooth-fit principle is satisfied for .

(iii) If is regular for , then the smooth-fit principle is satisfied for .

(iv) If is of bounded variation and then the smooth-fit principle at is not satisfied.

(v) If is of bounded variation and then the smooth-fit principle at is not satisfied.

Remark 2.

The equivalent conditions of the regularity of for negative half-line in terms of the volatility and the jump measure are given, e.g,. in [Alili and Kyprianou (2005), Prop. 7] and [Lamberton and Mikou (2012), Prop. 4.1].

Remark 3.

We do not give any specific procedure for computing the optimal thresholds . The main reason is that for a wild class of spectrally negative Lévy process the scale function is in the form of liner combination of some exponential functions. This is the case for example when jumps have phase-type distribution. In this case the value functions and could be calculated explicitly. Thus identifying optimal and is equivalent to finding the values and maximizing these functions. That could be done explicitly or by any numerical procedure finding the maximum of the function. For instance, in our Examples in Section 6, first-order conditions can be invoked instead of the smooth-fit condition, to compute and .

Proof.

The first statement follows from the continuity of the value function proved in Lemma 2. Statement (ii) follows from very similar arguments like the ones given in the proof of [Lamberton and Mikou (2012), Thms. 4.1 and 5.1]. The only explanation requires inequality appearing in the proof of [Lamberton and Mikou (2012), Thms. 4.1]

for

| (3.7) |

and for . This inequality is straightforward from definition of the value function because is a stopping time since, by Lemma 2, we have . The case of the lower critical point could be resolved in the same way by taking instead of . Finally the two last statements follow from the proof of [Lamberton and Mikou (2012), Thm. 5.2]. In particular, the inequality [Lamberton and Mikou (2012), (5.13)] is obvious in this case (by taking the negative interest rate instead there).

If we assume a more stronger condition than the regularity of for negative or positive half-line, namely that

| (3.8) |

then we can give a different and new proof of the smooth fit conditions at and . We also assume that the density of jump measure satisfies

| (3.9) |

in a neighborhood of the origin, for some and .

We assume that is spectrally negative, hence . The proof for the spectrally positive case is the same. Under condition (3.8) (recall also the global assumption (3.9)), we have

| (3.10) |

see [Kyprianou et al. (2013), Thm. 3.11, p. 140] and hence by Lemmas 2 and 3 we can conclude that for and because the optimal thresholds and do not depend on initial asset prices . Indeed, in this case

| (3.11) | ||||

for

and

| (3.12) | ||||

for

Hence we can apply the change of variable formula.

From Theorem 1 it follows that is the value function of the American put option and from the general optimal stopping theory we know that dominates the payoff function and is a supermartingale (see [Peskir and Shiryaev (2006)]).

Let us focus on the boundary . As the value function dominates the payoff function and both are non-increasing and convex, we have that

| (3.13) |

To prove the inequality in the opposite direction we

use the change of variable formula presented in

[Eisenbaum and Kyprianou (2008), p. 208] together with Dynkin formula

where is a local martingale, is a local time of at , is an infinitesimal generator of and and . Note that by Lemma 3 and by (3.10), the functions and are in the domain of the infinitesimal generator (see [Eisenbaum and Kyprianou (2008), Thm. 2]). Now, from the general theory of optimal stopping (see [Peskir and Shiryaev (2006)] for details) we know that is a supermartingale. Thus,

| (3.14) |

for any . From [Eisenbaum and Kyprianou (2008), Thm. 3] it follows that the process

is of unbounded variation on any finite interval similarly as is by assumption (3.8). On the other hand, the processes and are of bounded variation. Thus, taking in (3.14) we can conclude that

| (3.15) |

for all sufficiently small and . Indeed, assume a contrario that for some , we have . As the local time is nondecreasing and it increases only when process enters the half-line leaving the set , then, by taking , from (3.13) we have that is equal to its variation which is . Then

which is a contradiction to (3.14).

From (3.15) the following inequality must hold true

This inequality together with the already proved converse inequality completes the proof of the smooth fit property at . The smooth fit property at follows by similar arguments or by direct calculation. ∎

4. Swing put option

A multiple stopping option, the so-called Swing option, is a derivative with exercise opportunities with some refraction period between them. Let be the refraction periods between consecutive exercise times. We assume that are positive random variables and that has no atoms. The value of the perpetual Swing put option is defined as follows

| (4.1) |

for some strike price , where

| (4.2) |

where is a shift operator associated with the transition probability of . Note that is the value of the American put option analyzed in the previous section and that condition (3.1) implies that . To solve the optimal stopping problem (4.1) of the Swing option we follow the approach of [Leung et al. (2015)] and define recursively following single optimal stopping problems:

| (4.3) |

with

| (4.4) |

for given in (3.7), and .

Lemma 4.

For every and all the function is a non-increasing and convex function of .

Proof.

We prove the result by induction. For and the payoff function (3.7) the result follows immediately from the fact that the value of the American put option is a non-increasing and convex function of (see e.g. [Ekström (2004), Cor. 2.6]). Now, suppose that the results holds for for some . Thus

is also non-increasing and convex with respect to as the functions and are of the same type. We can use the same arguments as the ones given in the proof of [Ekström (2004), Cor. 2.6] to prove that is a non-increasing and convex function of . Then, the claim is proved.∎

From the previous considerations given in Section 3 we know that there exist and such that for any . We now extend this result for adapting the idea of the proof of Lemma 2.3 of [Carmona and Touzi (2008)].

Lemma 5.

Let . Then for all and all , we have .

Proof.

It is sufficient to show that on as the reverse inequality is trivial. From the definition of we can write

From the general theory of optimal stopping we know that is a supermartingale. Thus, we have that

As for , we get on

This completes the proof. ∎

Let us define a set of stopping times for the recursive single stopping problems (4.3)-(4.4) as follows

| (4.5) | |||

| (4.6) |

We prove below the equivalence between (4.3) and the Swing problem (4.1). Thus, by the general optimal stopping theory, we will prove that the set of stopping times

| (4.7) |

solves the Swing optimal stopping problem (4.1).

Theorem 2.

Proof.

Firstly, note that , Indeed, by repeating below calculation -times we have

On the other hand, we know that the set of stopping times defined in (4.6) is optimal for the single recursion problem (4.3). Therefore, we can write

where the above inequality follows from the supermartingale property of . Summarizing, we get

From the definition of as a supremum over all stopping times separated by the sequence it follows that

This completes the proof. ∎

We now give a characterization of the set of optimal stopping rules for the Swing put option.

Theorem 3.

The -th optimal stopping rule is a first moment of entering some interval , i.e.

| (4.8) |

where and satisfies the smooth fit property. Moreover, the sequence is nested, i.e. .

Proof.

From Lemma 4 we can conclude that for any the functions and are non-increasing and convex. Hence the optimal stopping times are of the form (4.8) for some sets being possibly sum of intervals (or half-lines). To prove that are true intervals it is sufficient to prove that exercise regions are connected. To do so assume to the contrary that the th exercise region is not connected. That is, we assume that there exists such that

| (4.9) |

Let . Now from the classical Wald-Bellman equation (see e.g. [Peskir and Shiryaev (2006), (2.1.6)-(2.1.7), p. 28]) or straightforward from the th optimization problem (4.3)

| (4.10) |

that holds true for any stopping time . Denote by the stopping region that is on the left from (jointly with ). We choose . Now, as is non-increasing, observe that

| (4.11) |

This produces a contradiction with the fact is continuous and hence .

In order to show that is nested we use inductive arguments. Let us define an auxiliary process

for with . For we have and the function for is equal to the value of the single American put option (1.4). Therefore, for , by the general theory of stopping problems, the process is a supermartingale. Moreover, from Lemma 5 we know that . Now, assume that for some the sequence is nested and the supermartingale property of is satisfied for all , i.e.

and

Firstly, by induction we show that is also a supermartingale. We define

From the general theory of optimal stopping we know that the stopped process is a martingale because are martingales for all . Furthermore, the process

is a stopped supermartingale less a stopped martingale, hence a supermartingale. Finally, is a supermartingale from the definition of and independence of and

All these cases together with the smooth fit property at all and give us the supermartingale property of the process . The smooth fit is satisfied by the same arguments as the ones presented in Proposition 1 for the single American put option.

Now, using proved supermartingale property of we show that . Indeed, for we have:

This proves that and hence . ∎

5. The put-call symmetry

Let be a completely asymmetric Lévy process. We recall that has the Laplace exponent (2.1)

where by (2.3). We recall that by we denote a dividend rate. The process can be identified via its triplet .

In this section we will find a relationship between the values and the exercise regions of perpetual American call and put options, the so-called put-call symmetry. We denote by

the value of the perpetual American put option and by

the value of the perpetual American call option.

If the discounting rate , the arguments given in Section 3 (see also [Battauz et al. (2012)]), show that the perpetual American put option either is never exercised or admits a double continuation region identified by the two critical prices

Lemma 6.

For all we have

| (5.1) |

Proof.

We prove the result for being spectrally negative. The proof for the spectrally positive case is similar. When is spectrally negative, similar arguments to those employed in Lemma 3 show that for we have

Denote

and . Note that is the spectrally positive process starting from and defined by the triplet , with . As shown in the proof of Lemma 2.1 in [Fajardo and Mordecki (2006)], its characteristic exponent is related to by the following identity . The process is spectrally negative with the Laplace exponent , which right continuous inverse function is given by

Indeed, note that

Finally, Lemma 8.4 of [Kyprianou (2006)] gives us that the first scale function of satisfies

and its resolvent density satisfies

Using the above relations and Lemma 3 we can straightforward derive equation (5.1). Thus the assertion of this lemma holds true. ∎

Lemma 6 immediately produces the following put-call symmetry for perpetual American options.

Theorem 4.

Assume that the stopping region of the perpetual put option is not empty, with optimal stopping boundaries and . Then,

Moreover, the American call option admits a double continuation region with optimal stopping boundaries , such that

or equivalently

Remark 4.

A similar result for the Black-Scholes model is derived in [Battauz et al. (2014)]. For the standard case , Theorem 4 is proved by [Carr and Chesney (1996)] in a diffusive market and by [Schroder (1999)] in a general semimartingale model. A precise description of the duality in the Lévy market for can be found in [Fajardo and Mordecki (2006), Cor. 2.2]. A comprehensive review of the put-call duality for American options is given in [Detemple (2001)].

Proof.

Using similar arguments like in the proof of Lemma 2 one can conclude that for the call American option the stopping region has to be also an interval or a half-line. Now, Lemma 6 implies that

All above derivatives are equal zero (hence maximizing appropriate option values) if and only if , This completes the proof. ∎

A put-call symmetry result can be derived also for Swing options as a consequence of the previous theorem. Let

be put and call American options, respectively, where is defined in (4.2) and

are the corresponding optimal stopping rules. From Theorems 2 and 3 it follows that

where for and defined in Theorem 3.

Corollary 1.

The following put-call symmetry holds

and

| (5.2) |

with

Proof.

To prove that stopping regions for the call Swing option are of the form of (5.2) one can use similar idea like the one given in (4.11) but in this case one has to exchange roles of and as payoff functions are all non-decreasing. Now, the result follows immediately from Lemma 6 as symmetry holds for all such that , given also that the Swing option is a sum of single options. ∎

6. Numerical analysis

6.1. Black-Scholes model

Let

be a linear Brownian motion where is a Brownian motion, is a drift under a martingale measure (see (2.3)), is a volatility and is the starting position of . As the linear Brownian motion do not have any jumps, it is the only Lévy process which is at the same time spectrally negative and spectrally positive. This model corresponds the seminal Black-Scholes market model.

For the linear Brownian motion the Laplace exponent and the scale functions are given by

and

where

Using Lemma 3, we now give the value of the American put option with the negative discounting factor . Firstly, we calculate the right inverse Laplace transform

It is well-defined when and for it takes negative value. Thus, the American put option with the negative rate admits the double continuation region and its value for the Brownian motion reduces to:

where the optimal levels and could be identified using either first-order condition or the smooth fit principle given in Proposition 1, and they are given by

Remark 5.

The optimal level solves

because it maximizes the value function of the American put option. The above equation is equivalent to

which does not have solution when . This means that for we always have a single continuation region; see Table 1. In fact, [Alili and Kyprianou (2005)] (see also [Kyprianou (2006), Th. 9.2]) proved that this stopping region is , hence the continuation region equals in this case.

In Table 1 we give a summary for all possible continuation regions with respect to parameters for the American put option in the Brownian motion case. The put-call symmetry yields an analogous result for the American call option, which we describe in Table 2. Note that in the case of the American call option one can derive only single stopping region when and . This case corresponds to the conditions considered by [Xia and Zhou (2007)].

| discounting rate | continuation region | ||

|---|---|---|---|

| single continuation region; | |||

| single continuation region; | |||

| no early exercise; | |||

| double continuation region; | |||

| no early exercise; | |||

| double continuation region; ; | |||

| no early exercise; | |||

| no early exercise; | |||

| discounting rate | continuation region | |||

|---|---|---|---|---|

| single continuation region; | ||||

| no early exercise; | ||||

| single continuation region; | ||||

| no early exercise; | ||||

| double continuation region; | ||||

| no early exercise; | ||||

| double continuation region; ; | ||||

| no early exercise; | ||||

| no early exercise; | ||||

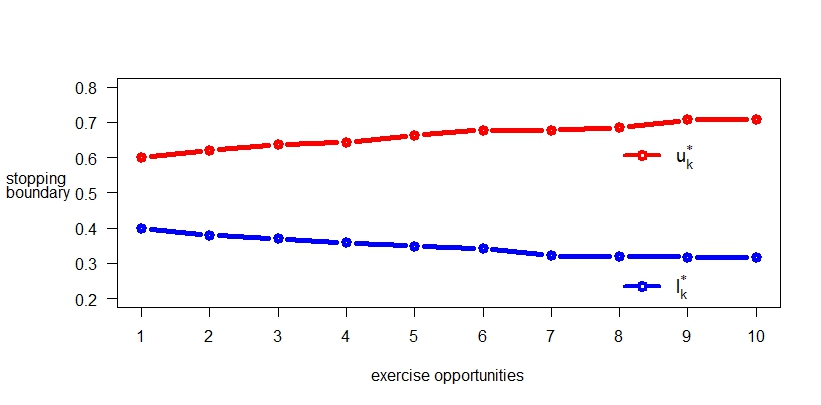

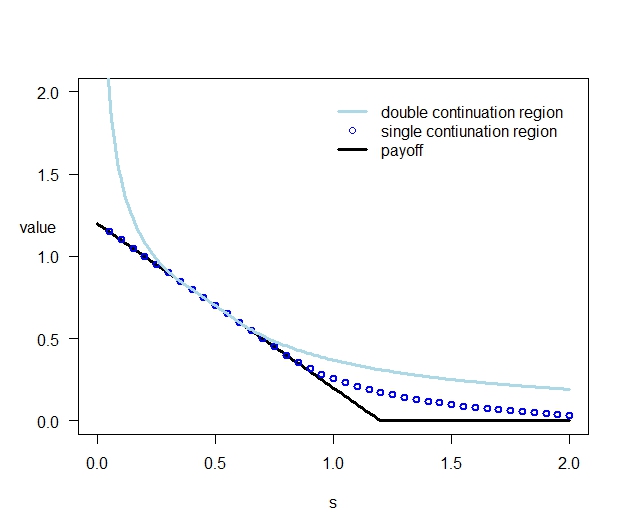

By numerical methods, we also find the optimal stopping regions for the Swing option in the Black-Scholes model. In Figure 2 we present the sequence of the optimal levels and calculated by Monte Carlo methods with iterations in each recursive step.

6.2. Jump-diffusion model

For comparison purpose we extend the numerical calculation of the Black-Scholes model given above by adding the possibility of downward jumps for the log prices. We model this jumps by an exponential distribution with parameter and we assume that they occur in the market with fixed intensity . Formally, we model the logarithm of the risky underlying asset price by

| (6.2) |

where, and , is a Poisson process with intensity and is an sequence of i.i.d. exponential jumps with parameter . It is well-known that jump-diffusion models better reproduces a wide variety of implied volatility skews and smiles, and market fluctuation (see the discussion and references in the introduction).

Note that the process given in (6.2) is a spectrally negative Lévy process with Laplace exponent

In order for the American put option stopping problem to be well-defined, following Lemma 1 we assume that

The scale function is given by:

where (possibly complex) valued for satisfy

| (6.3) |

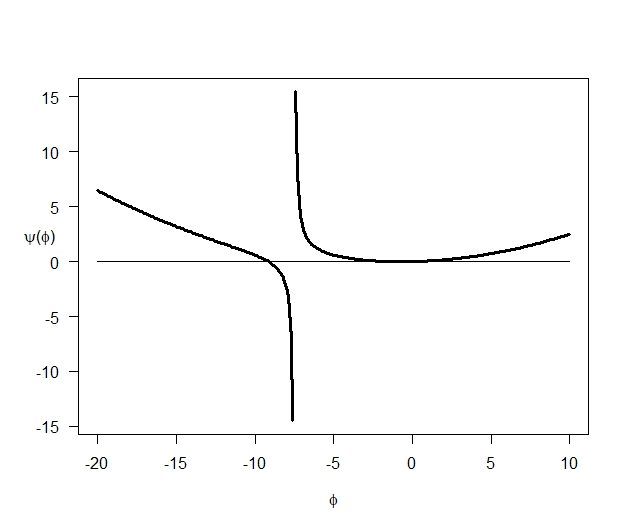

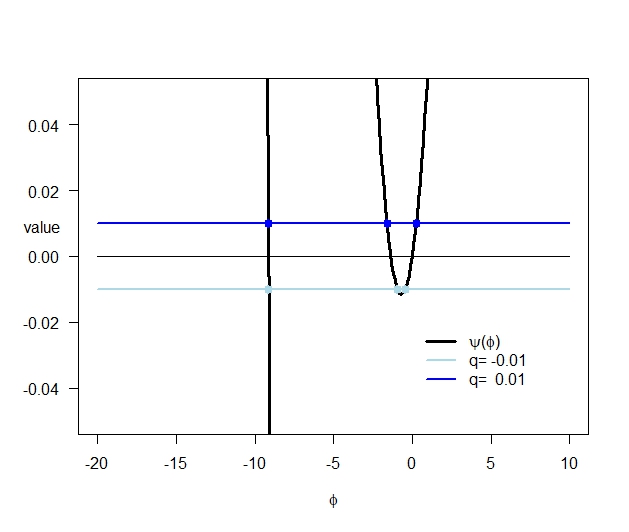

One can observe that the above equation is equivalent to a cubic equation and it can be solved using Cardano roots. This type of equation either have all three roots real or one real root and two non-real complex conjugate roots. The problem of the American put option with the negative rate is well-defined when exists. This is equivalent to having three real solutions of (6.3). The roots of for the negative discounting rate are presented in the Figure 3. Note that has also to satisfy the following inequality

| (6.4) |

Indeed, as , we can write

Now, the integral in the second expectation is finite if and only if (6.4) holds true.

We can find the value of the American put option using (3.12). To do so, it remains only to to calculate the double integral appearing in the formula. As the jumps have exponential distribution, it can be computed as a product of two integrals as follows:

and

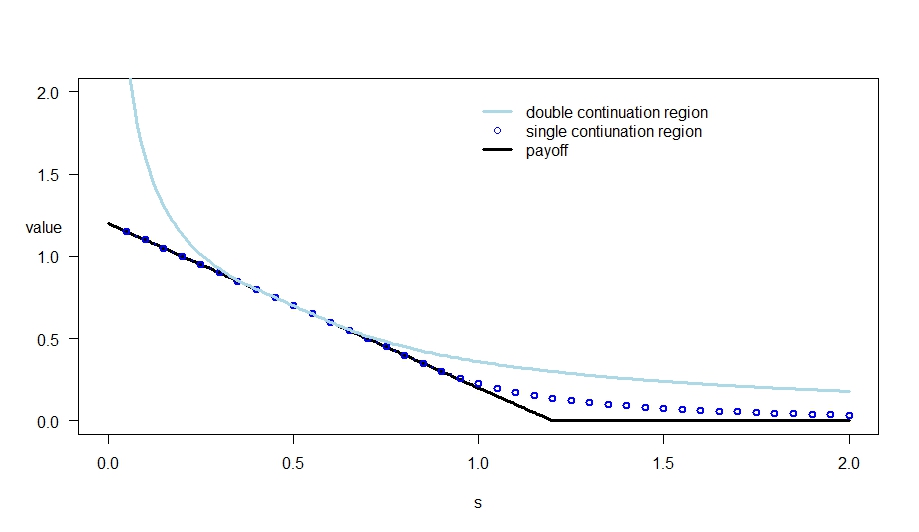

The optimal boundaries can then be derived by using the smooth fit principle or first-order conditions. The value functions of the American put option and the optimal stopping regions for some negative discounting factor (double continuation region) and for some positive discounting factor (single continuation region) are presented in Figure 4.

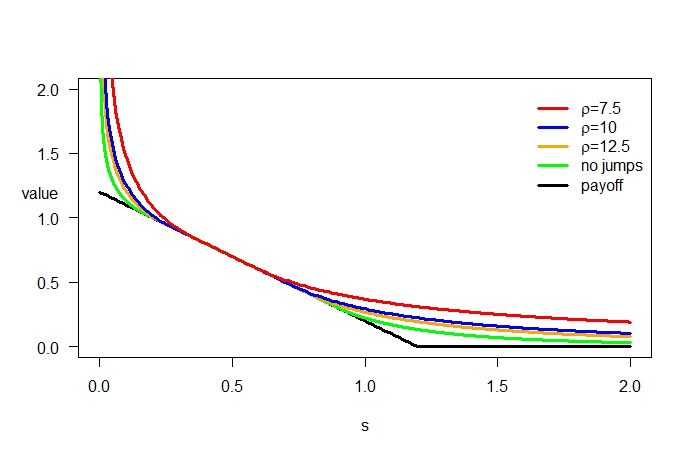

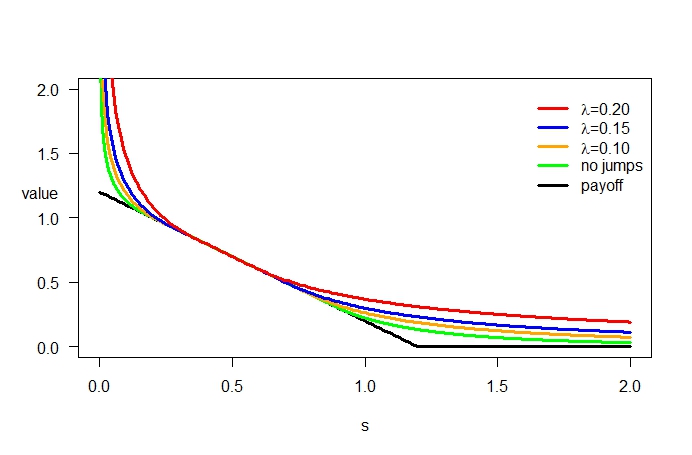

To understand the impact of jumps on the value function and on the stopping region we compare various intensities of exponential distribution and various intensities of arrival rate , leaving fixed the other parameters, in Figure 5 and Figure 6, respectively. Note that the increase in corresponds to a decrease in the average sizes of the jumps, which, we recall, are downward jumps. On the other hand, the increase in impacts in increase of average number of observed jumps in one time unit.

Note that the value function gets lower and the stopping region gets larger as the parameter of the exponential distribution increases. The same behaviour is observed when the arrival intensity decreases. As for an American put option the jump reduces the asset price a higher or more frequent downward jumps increase the likelihood of a higher gain, hence the price of the option. As for the critical prices, we recall that when the interest rate is negative, it is not convenient to exercise the option if it is either too deep or not enough in the money. If the option is in the money, a higher or more frequent downward jumps could drastically reduce the asset price, making the exercise no longer convenient, therefore a safer (namely higher) lower level for the stopping region is required. The behaviour of the upper critical value, which for the put option is the ”standard” one, agrees with the literature for the case . For instance [Amin (1993)] shows that jumps may reduce the value of the asset, early exercise is postponed and the option is exercised if the asset is deeper in the money.

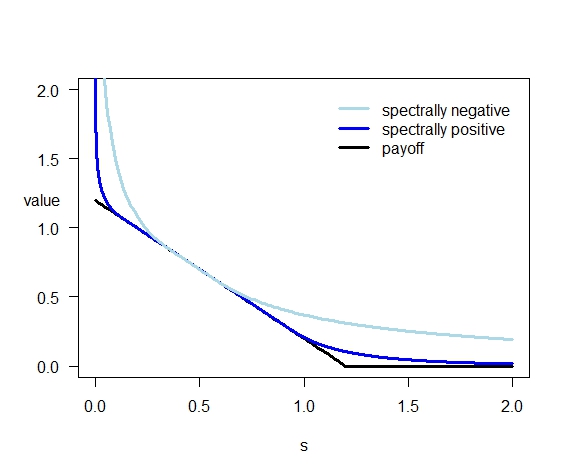

Finally, we also compare the cases of spectrally negative and spectrally positive processes. When we set just opposite sign of the jumps comparing to spectrally negative case and all other parameters constant, we observe larger stopping region and lower value function in case of positive jumps. This behaviour is consistent with previous analysis of jump’s parameters and . When the jumps for spectrally negative process get smaller, i.e. the jump intensity increases, the stopping region expands. If we allow opposite sign of jump’s size, we get a spectrally positive process and further dilation. This result can be observed in Figure 7.

7. Conclusions and future work

In this paper we have studied perpetual American options in a completely asymmetric Lévy market, when the discounting rate is negative. We have explicitly calculated the price of the American options and identified the critical prices, hence the double continuation region, in terms of the scale function of an appropriate spectrally negative Lévy process. We have also extended our approach to the analysis of Swing options. We have also conducted an extensive numerical analysis for the Black-Scholes model and the jump-diffusion model with exponential jumps. The main vehicle for deriving all results was based on fluctuation theory of Lévy processes and general theory of stopping problems. This kind of study is still at its first step and several further extensions can be done. First of all, the characterization of the price and critical prices of the perpetual American options is the starting point for the analysis of finite-maturity American options and Canadized options. Moreover, one can think of more general settings involving Markov regime switching to model the underlying price. These type of results could be achieved using the work of [Ivanovs and Palmowski (2012)] where some exit identities related to the first passage times (2.4) are given. It would also be interesting to consider multi-dimensional exponential Lévy process (see [Klimsiak and Rozkosz (2018)]). Finally, the analysis of a market in the presence of a negative discounting rate should address also other types of options, e.g. the -options described by [Guo and Zervos (2010)]. All of these problems are quite complex and left for future research.

Acknowledgments

This paper was conceived while the first author was visiting the Hugo Steinhaus Center at Wrocław University of Science and Technology. A special thank is due to prof. A. Weron and his group for their kind hospitality.

References

- [Gold World Council] http://www.gold.org/investment/statistics/.

- [Aase (2010)] K.K. Aase (2010). The perpetual american put option for jump-diffusions. In Endre Bjørndal, M. Bjørndal, P. M. Pardalos, and M. Rönnqvist, editors, Energy, Natural Resources and Environmental Economics, 493–507. Springer Berlin Heidelberg.

- [Alili and Kyprianou (2005)] L. Alili and A.E. Kyprianou (2005). Some remarks on first passage of Lévy process, the American put and pasting principles. Annals of Applied Probability, 15, 2062–2080.

- [Alvarez and Tourin (1996)] O. Alvarez and A. Tourin (1996). Viscosity solutions of nonlinear integro-differential equations. Ann. Inst. H. Poincaré Anal. Non Linéaire, 13(3), 293–317.

- [Amin (1993)] K.I. Amin (1993). Jump diffusion option valuation in discrete time. The Journal of Finance, 48(5), 1833–1863.

- [Asmussen et al. (2004)] S. Asmussen, F. Avram, and M.R. Pistorius (2004). Russian and American put options under exponential phase-type Lévy models. Stochastic Processes and their Applications, 109, 79–111.

- [Avram et al. (2004)] F. Avram, A.E. Kyprianou, and M.R. Pistorius (2004). Exit problems for spectrally negative Lévy processes and applications to Russian, American and Canadized options. Ann. Appl. Probab., 14(1), 215–238.

- [Nielssen (1998)] O. B. Nielssen (1998). The McKean stochastic game driven by a spectrally negative Lévy process. Finance Stoch., 1, 41–68.

- [Barrieu and Bellamy (2005)] P. Barrieu and N. Bellamy (2005). Impact of a market crisis on real options. In Wilmott Kyprianou, Schoutens, editor, Exotic Option Pricing and Advanced Lévy Models. Wiley Finance.

- [Battauz et al. (2012)] A. Battauz, M. De Donno, and A. Sbuelz (2012). Real options with a double continuation region. Quantitative Finance, 12(3), 465–475.

- [Battauz et al. (2014)] A. Battauz, M. De Donno, and A. Sbuelz (2014). Real options and American derivatives: the double continuation region. Management Science, 61(5), 1094–1107.

- [Battauz et al. (2017)] A. Battauz, M. De Donno, and A. Sbuelz (2017). On the exercise of American quanto options. Preprint.

- [Baurdoux (2007)] E. Baurdoux (2007). Fluctuation Theory and Stochastic Games for Spectrally Negative Lévy Processes. Phd Thesis, Utrecht University, see http://stats.lse.ac.uk/baurdoux/thesis.pdf.

- [Baurdoux (2009)] E. Baurdoux (2009). Last exit before an exponential time for spectrally negative Lévy processes. Journal of Applied Probability, 46(2), 542–558.

- [Baurdoux and Kyprianou (2008)] E. Baurdoux and A. Kyprianou (2008). The McKean stochastic game driven by a spectrally negative Lévy process. Electronic Journal of Probability, 8, 173–197.

- [Bergman et al. (1996)] Y. Bergman, B. Grundy, Z. Wiener (1996). General properties of option prices. J. Finance , 51, 1573–1610.

- [Boyarchenko and Levendorskii (2002)] S.I. Boyarchenko and S.Z. Levendorskii (2002). Perpetual American options under Lévy processes. SIAM Journal of Control and Optimization, 40, 1663–1696.

- [Broadie and Detemple (1995)] M. Broadie and J. Detemple (1995). American Capped Call Options on Dividend-Paying Assets The Review of Financial Studies, 8(1), 161–191.

- [Carmona and Touzi (2008)] R. Carmona and N. Touzi (2008). Optimal multiple stopping and valuation of swing options. Mathematical Finance, 18(2), 446–460.

- [Carr et al. (2002)] P. Carr, D. Madan, H. Geman, and M. Yor (2002). The fine structure of asset returns, an empirical investigation. J. Business, 75(2), 305–332.

- [Carr and Chesney (1996)] P. Carr and M. Chesney (1996). American put call symmetry. Preprint.

- [Chan (2005)] T. Chan (2005). Pricing perpetual American options driven by spectrally one-sided Lévy processes. In Wilmott Kyprianou, Schoutens, editor, Exotic Option Pricing and Advanced Lévy Models. Wiley Finance.

- [Chesney and Jeanblanc (2004)] M. Chesney and M. Jeanblanc (2004). Pricing American currency options in an exponential Lévy model. Applied Mathematical Finance, 11, 207–225.

- [Churiwal and Shreni (2012)] A. Churiwal and A. Shreni (2012). Surveying the Indian gold loan market. Cognizant 20-20 Insights.

- [Cont and Tankov (2003)] R. Cont and P. Tankov (2003). Financial modelling with jump processes. Chapman and Hall, CRC Press.

- [Cui and Hoyle (2011)] C. Cui and R. Hoyle (2011). J.P. Morgan will accept gold as type of collateral. Wall Street Journal, Commodities, 8.

- [Detemple (2001)] J. Detemple (2001). American options: symmetry properties. In Musiela Jouini, Cvitanić, editor, Option pricing, interest rates and risk management, 67–104. Cambridge University Press.

- [Detemple (2014)] J. Detemple (2014). Optimal exercise for derivative securities. Annual Review of Financial Economics, 6, 459–487.

- [Detemple and Kitapbayev (2018)] J. Detemple and Y. Kitapbayev (2018) American Options with Discontinuous Two-Level Caps. SIAM J. of Financial Mathematics, 9(1), 219–250.

- [Dixit et al.(1993)] A.K. Dixit and R.S. Pindyck (1993). Investment under Uncertainty. Princeton University Press.

- [Eberlein and Keller (1995)] E. Eberlein and U. Keller (1995). Hyperbolic distributions in finance. Bernoulli, 1, 281–299.

- [Eberlein and Papantaleon (2005)] E. Eberlein and A. Papantaleon (2005). Symmetries and pricing of exotic options in Lévy models. In Wilmott Kyprianou, Schoutens, editor, Exotic Option Pricing and Advanced Lévy Models. Wiley Finance.

- [Eisenbaum (2006)] N. Eisenbaum (2006). Local time–space stochastic calculus for Lévy processes. Stochastic Processes and their Applications, 116, 757–778.

- [Eisenbaum and Kyprianou (2008)] N. Eisenbaum and A.E. Kyprianou (2008). On the parabolic generator of a general one-dimensional Lévy process. Electronic Communications in Probability, 13, 198–208.

- [Ekström (2004)] E. Ekström (2004). Properties of American option prices. Stochastic Processes and their Applications, 114, 265–278.

- [Fajardo and Mordecki (2006)] J. Fajardo and E. Mordecki (2006). Symmetry and duality in Lévy markets. Quantitative Finance, 6, 210–227.

- [Gerber and Shiu (1998)] H. Gerber and E. Shiu (1998). Pricing perpetual options for jump processes. North American Actuarial Journal, 2, 101–112.

- [Guo and Zervos (2010)] X. Guo and M. Zervos (2010). options. Stochastic Processes and their Applications, 120, 1033–1059.

- [Hull (2011)] J.C. Hull (2011). Options, Futures and Other Derivatives. Prentice Hall.

- [Ivanovs and Palmowski (2012)] J. Ivanovs and Z. Palmowski (2012). Occupation densities in solving exit problems for Markov additive processes and their reflections. Stochastic Processes and their Applications, 122(9), 3342–3360.

- [Klimsiak and Rozkosz (2018)] T. Klimsiak and A. Rozkosz (2018). The valuation of American options in a multidimensional exponential Lévy model. Financial Mathematics, http://onlinelibrary.wiley.com/doi/10.1111.

- [Koponen (1995)] I. Koponen (1995). Analytic approach to the problem of convergence of truncated Lévy flights towards the Gaussian stochastic process. Phys. Rev. E., 52, 1197–1199.

- [Kyprianou and Surya (2007)] A. E. Kyprianou and B. A. Surya (2007). Principles of smooth and continuous fit in the determination of endogenous bankruptcy levels. Finance and Stochastics, 11(1), 131–152.

- [Kyprianou (2006)] A.E. Kyprianou (2006). Introductory Lectures on Fluctuations of Lévy Processes with Applications. Springer.

- [Kyprianou et al. (2013)] A.E. Kyprianou, A. Kuznetsov, and V. Rivero (2013). The theory of scale functions for spectrally negative Lévy processes. Lévy Matters II, Springer Lecture Notes in Mathematics.

- [Lamberton and Mikou (2012)] D. Lamberton and M. Mikou (2012). The smooth-fit property in an exponential Lévy model. Journal of Applied Probability, 49 (1), 137–149.

- [Leung et al. (2015)] T. Leung, K. Yamazaki, and H. Zhang (2015). Optimal multiple stopping with negative discount rate and random refraction times under Lévy models. SIAM Journal on Control and Optimization, 53(4), 2373–2405.

- [Madan and Seneta (1990)] D. B. Madan and E. Seneta (1990). The variance gamma model for share market returns. J. Business, 63, 511–524.

- [Merton (1976)] R. Merton (1976). Option pricing when the underlying stock returns are discontinuous. Journal of Financial Economics, 3, 125–144.

- [Mordecki (2002)] E. Mordecki (2002). Optimal stopping and perpetual options for Lévy processes. Finance and Stochastics, 6(4), 473–493.

- [Peskir (2005)] G. Peskir (2005). A change-of-variable formula with local time on curves. Journal of Theoretical Probability, 18(3), 499–535.

- [Peskir and Shiryaev (2006)] G. Peskir and A. Shiryaev (2006). Optimal Stopping and Free-Boundary Problems. Birhäuser.

- [Pham (1997)] H. Pham (1997). Optimal stopping, free boundary, and American option in a jump-diffusion model. Applied mathematics and optimization, 35(2), 145–164.

- [Pham (1998)] H. Pham (1998). Optimal stopping of controlled jump diffusion processes: a viscosity solution approach. Journal of Mathematical Systems, Estimation and Control, 8, 1–27.

- [Schoutens (2003)] W. Schoutens (2003). Lévy Processes in Finance: Pricing Financial Derivatives. Wiley.

- [Schroder (1999)] M. Schroder (1999). Changes of numeraire for pricing futures, forwards, and options. Review of Financial Studies, 12 (5), 1143–1163.

- [Surya (2007)] B. Surya (2007). Optimal stopping problems driven by Lévy processes and pasting principles. Phd Thesis, Utrecht University.

- [Xia and Zhou (2007)] J. Xia and X. Zhou (2007). Stock loans. Mathematical Finance, 17(2), 307–317.

- [Zeghal and Mnif (2006)] A. B. Zeghal and M. Mnif (2006). Optimal multiple stopping and valuation of swing options in Lévy models. International Journal of Theoretical and Applied Finance, 9(8), 1267–1297.