Efficient data augmentation techniques for some classes of state space models

Supplement to “Efficient data augmentation techniques for some classes of state space models”

Abstract

Data augmentation improves the convergence of iterative algorithms, such as the EM algorithm and Gibbs sampler by introducing carefully designed latent variables. In this article, we first propose a data augmentation scheme for the first-order autoregression plus noise model, where optimal values of working parameters introduced for recentering and rescaling of the latent states, can be derived analytically by minimizing the fraction of missing information in the EM algorithm. The proposed data augmentation scheme is then utilized to design efficient Markov chain Monte Carlo (MCMC) algorithms for Bayesian inference of some non-Gaussian and nonlinear state space models, via a mixture of normals approximation coupled with a block-specific reparametrization strategy. Applications on simulated and benchmark real datasets indicate that the proposed MCMC sampler can yield improvements in simulation efficiency compared with centering, noncentering and even the ancillarity-sufficiency interweaving strategy.

keywords:

Data augmentation, State space model, Stochastic volatility model, EM algorithm, Reparametrization, Markov chain Monte Carlo, Ancillarity-sufficiency interweaving strategy1 Introduction

Data augmentation is a powerful approach for improving the efficiency of iterative algorithms such as the EM algorithm (Dempster, Laird and Rubin, 1977) and Markov chain Monte Carlo (MCMC) methods like the Gibbs sampler (Geman and Geman, 1984), via the introduction of carefully designed latent variables. Let be the density of observed data conditional on unknown parameter . A data augmentation scheme constructs unobserved or missing data, , such that

where is the augmented data.

An important development is the working parameter approach proposed by Meng and van Dyk (1997, 1998) to improve the convergence rate of the EM algorithm for the multivariate , Poisson and mixed effects models. In conditional augmentation, optimal working parameters are found by minimizing the fraction of missing information governing the EM algorithm convergence rate. Tan et al. (2007) applied this approach to quadratic optimization problems. Efficient MCMC algorithms for posterior sampling can also be constructed using marginal augmentation (van Dyk and Meng, 2001), where working parameters are assigned prior distributions and then marginalized out in the sampling scheme. Goplerud (2021) extends marginal augmentation to variational Bayes (Blei, Kucukelbir and McAuliffe, 2017) to improve posterior approximation of non-nested binomial hierarchical models. Alternatively, PX-EM (Liu, Rubin and Wu, 1998) accelerates EM by expanding the set of model parameters to adjust the covariance among parameters in the M-step. Recently, Tak et al. (2020) proposed a data transforming augmentation scheme that reduces heteroscedastic models into homoscedastic ones.

In Bayesian inference, data augmentation is also known as reparametrization, and two well-known parametrizations are (hierarchical) centering and noncentering. Convergence rates of MCMC algorithms (Roberts and Sahu, 1997) for these schemes have been studied for random effect models (Gelfand, Sahu and Carlin, 1995, 1996), Gaussian state space models (Pitt and Shephard, 1999a; Frühwirth-Schnatter, 2004), hierarchical models (Papaspiliopoulos, Roberts and Sköld, 2003, 2007) and Gaussian process based models (Bass and Sahu, 2017). Zanella and Roberts (2021) investigate convergence of the Gibbs sampler for Gaussian multilevel models of depth more than two, lending insight on the choice of parametrization, that is also applicable beyond Gaussian models.

Centering and noncentering play complementary roles as the Gibbs sampler often converges much faster under one parametrization than the other. Yu and Meng (2011) developed ASIS (ancillarity-sufficiency interweaving strategy) to exploit this contrasting feature. Kastner and Frühwirth-Schnatter (2014) evaluate the performance of ASIS on stochastic volatility (SV) models (Taylor, 1982), while Kastner, Frühwirth-Schnatter and Lopes (2017) proposed shallow and deep interweaving strategies for multivariate factor SV models, which can boost efficiency by several orders of magnitude. Simpson, Niemi and Roy (2017) apply ASIS to dynamic linear models using data augmentations based on (wrongly) scaled errors and disturbances. ASIS was also used to achieve shrinkage for time-varying parameter models (Bitto and Frühwirth-Schnatter, 2019), perform model selection for factor SV models incorporating leverage, asymmetry and heavy tails (Li and Scharth, 2020), and combined with elliptical slice sampling for posterior estimation in nonlinear state space models with univariate autoregressive state equation (Kreuzer and Czado, 2020).

Another alternative is partial noncentering, which lies on the continuum between centering and noncentering, and is capable of utilizing the information in the data to determine an almost optimal parametrization. Partial noncentering has been shown to yield better convergence in MCMC methods than both centering and noncentering for random effect models (Papaspiliopoulos, Roberts and Sköld, 2003) and spatial generalized linear mixed models (Christensen, Roberts and Sköld, 2006). It can also increase efficiency and provide more accurate posterior approximations in variational Bayes for generalized linear mixed models (Tan and Nott, 2013; Tan, 2021).

1.1 Proposed data augmentation scheme

We propose a data augmentation scheme for state space models with univariate observations and latent states , where is generated from independently and is a stationary AR(1) (first order autoregressive) process given by

| (1) | ||||||

, , persistence and . Many influential models fall inside this framework, such as the SV model with leverage (Omori et al., 2007), skewness or heavy tails (Abanto-Valle and Dey, 2014), stochastic conditional duration model (Bauwens and Veredas, 2004) and stochastic copula autoregressive model (Almeida and Czado, 2012). Our scheme introduces working parameters, and , to rescale and recenter so that the transformed latent state is

| (2) |

1.2 Maximum likelihood parameter estimation

First, we consider maximum likelihood estimation of the parameters of the AR(1) plus noise model using the EM algorithm. The observation equation is

, and and are independent for all and , and of . In this Gaussian context, optimal working parameters in different settings can be derived analytically by minimizing the fraction of missing information. Studies of their large sample properties reveal features distinct from random effect models. To incorporate the optimal schemes for inferring each parameter, an alternating expectation-conditional maximization algorithm (Meng and van Dyk, 1997) is designed and shown to be more attractive than centering and noncentering.

The EM algorithm is a natural approach for maximum likelihood estimation of parameters in linear Gaussian state space models (Shumway and Stoffer, 1982) as the latent states can be treated as missing data and the E-step can be performed using smoothed estimates from the Kalman filter (Kalman, 1960). Compared with gradient-ascent (scoring) methods, EM is simple to implement, numerically stable (likelihood increases monotonically) and guaranteed to converge to a local maximum (Wu, 1983). It is preferred when the M-step is tractable or parameters are high-dimensional as computational costs tend to be lower. While Newton and quasi-Newton algorithms converge quadratically or superlinearly, the EM algorithm converges linearly or sublinearly. Slow convergence often occurs in later stages, especially in high signal-to-noise ratio settings (Olsson and Hansen, 2006). Besides data augmentation, techniques proposed to accelerate EM include quasi-Newton (Jamshidian and Jennrich, 1997; Zhou, Alexander and Lange, 2011), extrapolation (Saâdaoui, 2010), parabolic (Berlinet and Roland, 2009) and Anderson acceleration (Henderson and Varadhan, 2019) and linearly preconditioned nonlinear conjugate gradient (Zhou and Tang, 2021). Both EM and scoring can also be combined with particle methods in an online or offline manner to obtain maximum likelihood parameter estimates of general state space models (Kantas et al., 2015).

1.3 Bayesian parameter estimation and smoothing

As the rate of convergence of EM algorithms and Gibbs samplers are closely linked (Sahu and Roberts, 1999), data augmentation schemes optimized for the EM algorithm can potentially be utilized to design efficient MCMC algorithms. Here we focus on parameter estimation and smoothing in a Bayesian framework but do not address online filtering. We consider two non-Gaussian and nonlinear state space models; the SV model for financial returns and the stochastic conditional duration model for time intervals between transactions, whose observation equations can be linked to the AR(1) plus noise model via mixture of normals approximations (Kim, Shephard and Chib, 1998). A block-specific reparametrization (BSR) strategy, which allows the parametrization of latent states to vary across blocks in a MCMC sampler, is proposed to incorporate the optimal schemes derived previously. Experiments on simulated data and real applications indicate that BSR always performs better than the worse of centering and noncentering, and often surpasses both and even ASIS.

Sequential Monte Carlo or particle filters (Doucet, de Freitas and Gordon, 2012) are widely used for online state estimation, and have also become popular for smoothing and parameter estimation. The particle learning and smoothing algorithm (Carvalho et al., 2010) incorporates parameter estimation via a fully adapted filter and smoothing via recursive backward sampling. Yang, Stroud and Huerta (2018) propose a modification of this algorithm to capture dependence between states and parameters, and a new smoothing algorithm called refiltering which can be parallelized easily.

For nonlinear and non-Gaussian state space models, it is difficult to design efficient proposal densities for sampling from the (conditional) posterior of high-dimensional latent states. Particle MCMC (Andrieu, Doucet and Holenstein, 2010) overcome this by using sequential Monte Carlo to build efficient proposals. Particle marginal Metropolis-Hastings, for instance, uses the marginal likelihood estimated from a particle filter run at each iterate to compute acceptance probabilities. For good mixing, the number of particles should scale linearly with the number of observations. Fearnhead and Meligkotsidou (2016) suggest using data augmentation to reduce Monte Carlo error in the particle filter. In contrast, gradient-based sampling methods such as Hamiltonian Monte Carlo (Neal, 2011) and Metropolis adjusted Langevin (Girolami and Calderhead, 2011) construct proposal densities adaptively based on the local geometry of the target, and gradients must be computed or approximated numerically at each iteration. Compared to standard MCMC, particle MCMC and gradient-based methods have higher computational cost, but are more generally applicable as they require little design effort. The efficient tuning of parameters in Hamiltonian Monte Carlo is a challenging task, and the No-U-Turn Sampler (Hoffman and Gelman, 2014) in Stan (Stan Development Team, 2019) employs automatic tuning based on the leapfrog method. Kleppe (2019) introduce dynamically rescaled Hamiltonian Monte Carlo where the target distribution is reparametrized to have constant scaling, while Osmundsen, Kleppe and Liesenfeld (2021) modify the target to be close to Gaussian using transport map. We provide some comparisons of BSR with particle marginal Metropolis-Hastings and Hamiltonian Monte Carlo implemented in the R package nimble (de Valpine et al., 2017) and Stan respectively in one of the real applications.

1.4 Extensions

The general linear Gaussian state space model (dynamic linear model) can be written as

with . Here is the observation vector, is the state vector and the error sequences , and are assumed to be independent. The proposed scheme in (2) is not applicable generally to the dynamic linear model as the idea of partial rescaling and recentering using fixed means and variances is usually relevant when is a stationary process. However, it is still useful in some special cases where , and do not vary with time, and is known.

If , , , and , then reduces to the stationary AR(1) process and the proposed scheme in (2) can be applied. Optimal values of working parameters for multivariate Gaussian observations can be derived similarly as for univariate and details are given in the Supplement (Tan, 2022).

Suppose . Let scalar functions on vectors be defined elementwise, and . If where each , and , then each element in is an AR(1) process (see, e.g. multivariate factor SV models in Li and Scharth, 2020). In this case, a data augmentation scheme similar to (2), where

may be used. More generally, if , and are defined such that is a stationary process with mean and covariance matrix , where is a unit lower triangular matrix and , a scheme such as

may be useful. Optimal values of the working parameters can be found similarly by optimizing the convergence rate of the EM algorithm, albeit with higher complexity.

2 EM algorithm for partially noncentered AR(1) plus noise model

The AR(1) plus noise model can be expressed in terms of as

where . Now and appear in both the observation and state equations. Suppose we have observations . Let be the latent states, , and , where and denote the vectors of all ones and zeros respectively (dimension inferred from context). When and , we recover the fully centered parametrization (CP) in (1), so called as is centered around the a priori expected value , and the parameters and appear only in the state equation. The fully noncentered parametrization (NCP) is obtained when and . Let be the model parameters, and the signal-to-noise ratio be defined as . In matrix notation, the AR(1) plus noise model can be expressed as

| (3) |

where is a symmetric tridiagonal matrix with off-diagonal elements equal to and diagonal given by . For , is invertible. Regardless of the parametrization, the marginal distribution of is where .

Suppose we wish to find that maximizes the observed data log-likelihood using an EM algorithm. We consider as missing data and as augmented data. Given an initial estimate , the algorithm performs an E-step and M-step at each iteration , where the E-step computes , and the M-step maximizes with respect to . The conditional distribution is , where

| (4) |

The subscripts of and represent their dependence on the values of and in the scheme. For instance, when and ,

It can be derived that

where , and and are evaluated at . At each iteration, the EM algorithm updates and given and sets . The expectation-conditional maximization algorithm (Meng and Rubin, 1993) reduces the complexity of the M-step by replacing it with a sequence of conditional maximization steps. If we maximize with respect to each element of with the remaining elements held fixed at current values, then the update of can be obtained by setting . This yields the following closed form updates for and :

| (5) |

Setting , we obtain closed form updates for the CP and NCP,

However, there are no closed form updates for and for arbitrary values of . For , closed form updates do not exist for the CP and NCP as well. We use the optimize function from the Optim package (Mogensen and Riseth, 2018) in Julia to maximize with respect to these parameters. Brent’s method is used to find while the unconstrained L-BFGS method is used to find .

We are interested in finding values of that optimize the rate of convergence of the EM algorithm. Define the information matrices as ,

and , where . In a neighborhood of ,

where , the matrix rate of convergence of the EM algorithm, is given by

The actual observed (global) rate of convergence is

where is any norm on . Under some regularity conditions, is given by the largest eigenvalue of , and a larger value indicates slower convergence. If is positive semidefinite, then . The EM algorithm converges rapidly ( is close to 0) if the observed information is close to the augmented information. Since depends only on the observed data and is independent of the parametrization, the rate of convergence can be optimized by minimizing with respect to in the sense of a positive semidefinite ordering (see Theorem 1 of Meng and van Dyk, 1997). Let denote the element in . We first consider cases where only or is unknown (matrix and actual observed rate of convergence are identical), followed by the case where all parameters are unknown. The proofs of all results in Sections 2.1, 2.2 and 2.3 are given in the Supplement (Tan, 2022).

2.1 Unknown location parameter

Suppose , and are known and only is unknown. The EM algorithm for this case (Algorithm 1) alternately updates and as in (4) and (5).

Theorem 1.

Rate of convergence of Algorithm 1 is

where and . This rate is minimized to zero at

From Theorem 1, the rate of convergence of Algorithm 1 for the CP and NCP are and respectively, which are strictly positive. However, when , Algorithm 1 converges instantly to

This can be seen by plugging into the update in (5). Moreover, it is possible to compute in advance for Algorithm 1 as does not depend on , and the rate of convergence is also independent of , so that can be set to any convenient value.

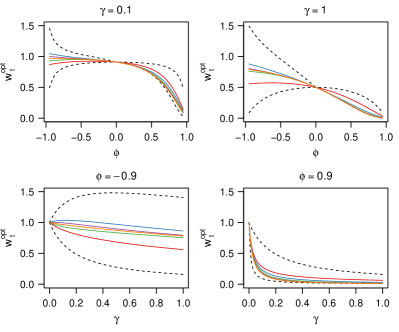

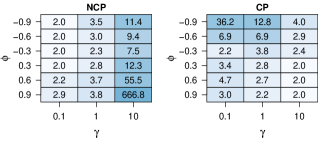

We investigate the range of elements in and their dependence on , and by deriving an explicit expression for using results on the inverse of tridiagonal matrices in Tan (2019). From the expression of in Theorem S1 (see Supplement (Tan, 2022)), depends on , and on and only through the signal-to-noise ratio . Corollary 1 presents bounds for which are tight when , showing that if and if . This is unlike normal hierarchical models, where always lies in (Papaspiliopoulos, Roberts and Sköld, 2003). From Corollary 2, the location centered parametrization () is increasingly preferred as the persistence and signal-to-noise ratio increase when . However, if , may not be strictly decreasing with either or . Figure 1 shows the values of elements in when for different values of and .

Corollary 1.

For ,

where and .

Corollary 2.

If , each element of decreases strictly as and the signal-to-noise ratio increase. As approaches 1, approaches .

From Theorem 1, instant convergence is achievable only if the portion of subtracted from in (2) is allowed to vary with . However, Theorem 2 shows that for large , the convergence rate of Algorithm 1 goes to zero even if is common for all , that is, if we restrict . The optimal value of in Theorem 2 is easy to compute and store, and can be used in place of that in Theorem 1 when is large.

Theorem 2.

If , the rate of convergence of Algorithm 1 is optimized at , where . As , where and the optimal rate of convergence of Algorithm 1 goes to zero.

2.2 Unknown scale parameter

Next, suppose , and are known and only is unknown. We assume as this is the case of interest. The EM algorithm for this case (Algorithm 2), alternately updates and at the E-step as in (4) and at the M-step.

Theorem 3.

If , the rate of convergence of Algorithm 2 is jointly minimized at

| (6) |

where .

From Theorem 3, depend on the unknown , while also depends on observed data . Thus, even if the true is known, will still vary across datasets generated from the AR(1) plus noise model due to sampling variability. We recommend updating based on the latest estimate of . In Corollary 3, we show that . However, the same does not apply to , which has been observed to be negative or exceed 1 in simulations.

Corollary 3.

depends on , and on and only through the signal-to-noise ratio . In addition, and decreases strictly as increases.

Corollary 4.

For in (6), and , where .

Theorem 4.

As , converges to

| (7) |

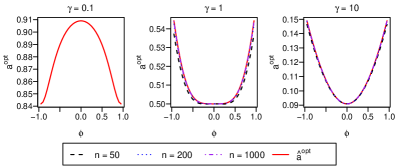

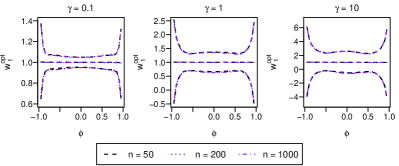

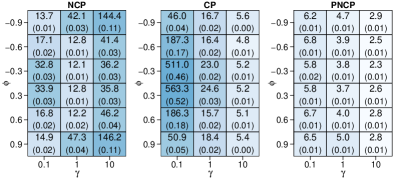

Theorem 4 derives a large-sample estimate of , which lends insight on how varies with and . From (7), is symmetric about and decreases strictly with as , but the relationship of with is not monotone. Figure 2 shows the values of and in different parameter settings, and is indistinguishable from for . In addition, decreases as increases, is symmetric about , and varies with in the form of a (sometimes inverted) U-shape. We can compute efficiently using a Kalman filter and smoother using time steps, but is even easier to compute and can be used in place of for large .

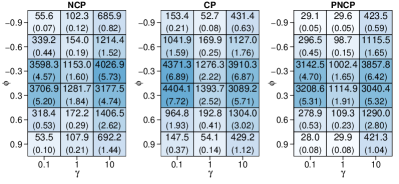

To investigate the dependence of on and signal-to-noise ratio , we compute for 1000 data sets simulated under different parameter settings. We set , , , and . Figure 3 shows the mean, 5th and 95th quantiles of the first element of evaluated across 1000 simulated data sets. Plots of other elements look similar and are not shown. The mean is approximately 1 as is consistent with Corollary 4, but the variance increases with and as . The behavior of does not appear to vary with and thus we cannot find an asymptotic estimate of that is valid for large as we have done for in Theorem 4.

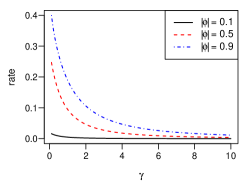

Theorem 5 gives the approximate rate of convergence of Algorithm 2 for large and Figure 4 shows how this rate varies for different combinations of and . The asymptotic rate of convergence is always less than 0.5 and symmetric about . Algorithm 2 converges faster for smaller and larger signal-to-noise ratio . It converges most slowly when is close to 1 and is close to 0.

Theorem 5.

The asymptotic rate of convergence of Algorithm 2 as is approximately , where and . This rate decreases as increases and decreases.

2.3 All parameters are unknown

When all four parameters are unknown, the augmented information matrix is given by

Each element is dependent only on the working parameters stated in brackets and explicit expressions are given in the Supplement (Tan, 2022). For instance, is independent of while depends on both and . Note that , and , are both independent of . We also prove that , , and converge to 0 almost surely as . Hence these elements do not change substantially with for large , and it suffices to focus on

when optimizing the EM algorithm convergence rate.

From Sections 2.1 and 2.2, the parametrization optimal for inferring and are different, and it is impossible to find that jointly minimizes and . Hence when all parameters are unknown, we employ the alternating expectation-conditional maximization algorithm, which inserts an E-step before each conditional update, thus allowing the data augmentation scheme to vary across parameters. This enables us to use the optimal augmentation scheme for each parameter while conditioning on the rest, at the cost of more computation per iteration. To minimize the number of additional E-steps, we group with and perform only one E-step based on the optimal parametrization for before the conditional updates of . This is feasible as any convenient parametrization can be used for . The updates of is a joint update as and are independent in . After that, we update using its optimal parametrization. Instead of performing the E-step and M-step separately, we note that the update for in (5) for simplifies to , and . Hence we can compute followed by the update directly without computing . This choice of corresponds to having no missing data since the update is that obtained by maximizing directly with respect to . Algorithm 3 (for inferring all the parameters) is outlined below, and each iteration has two cycles. Algorithm 1 (for inferring only) omits step 2 while Algorithm 2 (for inferring only) omits step 3 and updates of in step 2(c). We say that Algorithms 1, 2 and 3 are using the partially noncentered parametrization (PNCP) as both the mean and scale are partially noncentered.

Initialize , and . While and ,

-

1.

.

-

2.

-

(a)

Set and .

-

(b)

Update and as in (4).

-

(c)

Update , and .

-

(a)

-

3.

-

(a)

Set .

-

(b)

Update .

-

(a)

-

4.

Compute .

If , compute .

2.4 Initialization and diagnosing convergence

The EM algorithm can be sensitive to initialization and there is also a risk of getting stuck in local modes. To aid convergence, we initialize using the strategy below. Recall that , where . Let and denote the autocovariance and sample autocovariance respectively at lag . Then

We initialize as the sample mean . Since , Shumway and Stoffer (2017) suggest initializing as . This strategy works well if is close to 1 but can be poor if is close to 0. Let and . As , we consider values of taking the sign of , such that and . If this set is empty (e.g. if ), we consider . For each plausible value of , we compute and . Then we evaluate the log-likelihood at each and choose the one that maximizes the likelihood as initial values. For diagnosing convergence, we consider the relative increment in the log-likelihood (defined in Algorithm 3), and terminate the algorithm when is less than a tolerance or if the maximum number of iterations is reached. We set and in all experiments unless stated otherwise. Efficient computation of the log-likelihood and optimal values of using the Kalman filter are discussed in the Supplement (Tan, 2022). The cost per iteration of Algorithm 3 is , where is the number of observations as the cost of computing the working parameters, log likelihood and parameter updates all scale linearly in .

3 Experimental results for EM algorithm

We compare Algorithms 1–3 with the expectation-conditional maximization algorithms using the CP or NCP. For the expectation-conditional maximization algorithms, only one E-step is used at the beginning of each iteration followed by the CM-steps. In contrast, Algorithm 3 requires more computation in each iteration to update working parameters and find numerically the value of that maximizes . To make Algorithms 2 and 3 more competitive, the updates in steps 2a and 3 are performed only in the first five iterations and thereafter only at . After convergence, we perform a final update of and the log-likelihood. These modifications do not affect the convergence rate of Algorithms 2 and 3 but are helpful in reducing the computation cost.

3.1 Simulations

First, we simulate data from the AR(1) plus noise model by setting , , , and . Twenty datasets are generated in each setting.

Algorithm 1 considers as the only unknown. When , it is difficult to differentiate among different parametrizations as all algorithms converge on average in less than five iterations and the averaged estimates of are almost identical. To magnify the differences, we reduce to . The average number of iterations NCP and CP take to converge are shown in Figure 5, whereas Algorithm 1 converges instantly. With this lower tolerance, NCP achieves the same averaged estimates of as CP and PNCP, but becomes increasingly inefficient as increases and as approaches 1. On the other hand, CP is least efficient when is small and , and improves as increases and . Hence the performance of NCP and CP are complementary. These observations can also be explained using Theorem 2, which states that as . From this expression, as and . Hence the CP is strongly preferred in these conditions.

For Algorithm 2 where is the only unknown parameter, the average number of iterations required for each algorithm to converge are shown in Figure 6. The average runtime in seconds is also given in brackets. The rate of convergence appears to be symmetric about for each parametrization. As is consistent with Theorem 5, PNCP becomes more efficient as increases and decreases. The efficiency of CP worsens as decreases and , while NCP performs best when is close to 1 and worsens as increases. The estimates of obtained using different parametrizations are virtually identical except and . In these cases, NCP converges slowly and yields slightly different estimates from CP and PNCP.

Algorithm 3 treats all parameters as unknown. The average number of iterations required and runtime of each algorithm are shown in Figure 7.

Again, there is symmetry about . In each setting, PNCP converges using the least number of iterations and achieves a higher log-likelihood on average. Its average runtime is always close to, if not faster than the better of NCP and CP. Table 1 shows that PNCP is able to provide speedup over CP and NCP in most cases, of up to 4.9 times.

| 0.9 | 0.6 | 0.3 | 0.3 | 0.6 | 0.9 | |||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 0.1 | 1 | 10 | 0.1 | 1 | 10 | 0.1 | 1 | 10 | 0.1 | 1 | 10 | 0.1 | 1 | 10 | 0.1 | 1 | 10 | |

| NCP | 1.3 | 2.3 | 1.4 | 1.0 | 1.3 | 0.9 | 1.0 | 1.0 | 0.9 | 1.0 | 1.0 | 0.9 | 1.0 | 1.3 | 0.9 | 1.4 | 2.6 | 1.4 |

| CP | 4.2 | 1.6 | 1.1 | 3.5 | 1.7 | 1.1 | 1.5 | 1.3 | 1.1 | 1.5 | 1.3 | 1.1 | 3.6 | 1.8 | 1.1 | 4.9 | 1.6 | 1.1 |

These properties make PNCP a great option as it is always faster than the worst of CP and NCP, often able to provide speedup and achieves a higher log likelihood on average. In most cases, the estimates obtained using different parametrizations are practically identical (more details are given in the Supplement (Tan, 2022)).

3.2 Real data

The first dataset contains IBM stock prices from 1962 to 1965 () studied in Pal and Prakash (2017), and it is available in the code bundle for the book on GitHub. The second dataset involves an industrial robot making a sequence of movements and the time series () records the distance in inches from a final target. It is available in the R package TSA (Cryer and Chan, 2008) as data(robot). We scale up all measurements in robot up by 1000 as the magnitude of the original measurements are very small with a maximum of 0.0083.

Tables 2 and 3 show the results for the IBM data and robot data respectively. Iterations refers to the number of iterations required for the EM algorithm to converge, where convergence is determined using the criteria described in Section 2.4. The runtime reported is in seconds and the log-likelihood is the maximum value of attained at convergence. Maximum likelihood estimates of at convergence are also given.

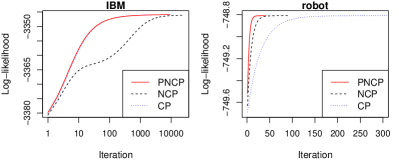

For the IBM data, is very close to 1, while is large. From Figure 7, we expect CP to perform better than NCP which is indeed the case. PNCP automatically leans towards CP and provides a speedup of about 2.2 compared to NCP. The maximum log-likelihood attained by NCP is lower than CP and PNCP, and the estimates of , and also differ noticeably. This is likely because the NCP is stuck at a poorer local mode, or it is converging so slowly and the relative increment in the log-likelihood per iteration is so small that the algorithm was terminated before full convergence is reached.

| NCP | CP | PNCP | |

|---|---|---|---|

| Iterations | 23504 | 9036 | 9030 |

| Runtime (s) | 4.86 | 2.30 | 2.25 |

| Max. log-likelihood | 3346.113 | 3345.929 | 3345.929 |

| 463.125 | 482.043 | 482.043 | |

| 43.946 | 44.275 | 44.275 | |

| 0.995 | 0.995 | 0.995 | |

| 0.153 | 0.135 | 0.135 |

For the robot data, is also close to 1, but is small, and NCP is expected to perform better based on Figure 7. Indeed, NCP converges faster than CP, while PNCP reduces the number of iterations of NCP further by about half. The estimates returned by NCP and PNCP are identical while CP differs slightly.

| NCP | CP | PNCP | |

|---|---|---|---|

| Iterations | 93 | 326 | 42 |

| Runtime (s) | 0.00 | 0.03 | 0.00 |

| Max. log-likelihood | 748.809 | 748.809 | 748.809 |

| 1.486 | 1.486 | 1.486 | |

| 0.209 | 0.210 | 0.209, | |

| 0.947 | 0.947 | 0.947 | |

| 5.062 | 5.061 | 5.062 |

Figure 8 tracks the log-likelihood at each iteration, and optimization of the working parameters has provided PNCP with a good headstart. Overall, PNCP provides an attractive alternative to NCP and CP as it automatically gravitates towards the better parametrization and is often able to outperform both in terms of speed and accuracy.

4 Extensions

We have proposed a data augmentation scheme for the AR(1) plus noise model in which working parameters are introduced for rescaling and recentering. Optimal values of that optimize the convergence of the EM algorithm in maximum likelihood estimation have been derived. However, the EM algorithm can also be used in the Bayesian framework to find the mode of a posterior distribution. Will the optimal values of vary depending on the prior specified on ? It is known that the rate of convergence of the Gibbs sampler is closely linked to the EM algorithm. Will the proposed data augmentation scheme also improve convergence for the Gibbs sampler? We seek to address these issues in this section and also touch briefly on the connection to variational Bayes.

4.1 EM Algorithm for finding posterior mode

Suppose a prior is placed on , and we wish to use the EM algorithm to find the posterior mode . That is, we wish to find maximizing . As before, let denote the latent states dependent on . In this case,

has an additional term . Hence the E-step is unchanged but the M-step must be modified. As , taking the logarithm, differentiating twice with respect to and taking expectation with respect to leads to

This yields the Bayesian analogue of the missing information principle,

where and

To optimize the rate of convergence of the EM algorithm, we seek values of that minimizes . Since is independent of , it suffices to minimize with respect to . Hence the only difference is that is evaluated at the posterior mode instead of maximum likelihood estimate . As is independent of , the optimal value of derived in Section 2.1 remains valid. As for , it is shown in the Supplement (Tan, 2022) that the optimal values of derived in Section 2.2 miraculously remain valid for any prior distribution . Thus we can still use the optimal values of derived in Sections 2.1 and 2.2 to optimize the rate of convergence of the EM algorithm when finding the posterior mode of the AR(1) plus noise model.

4.2 Gibbs sampler and variational Bayes

It is well known that the convergence rates of the EM algorithm and Gibbs sampler are closely related. When the target distribution is Gaussian, Sahu and Roberts (1999) showed that the rate of convergence of the Gibbs sampler that alternately updates and is equal to that of the corresponding EM algorithm. Specifically, if the precision matrix of is

where and are blocks corresponding to and respectively, then the common rate of convergence is .

As illustration, suppose is the only unknown parameter and a flat prior is used. We show that the strategy of partially noncentering and results in Section 2.1 can be transferred to the Gibbs sampler corresponding to Algorithm 1 given below.

| Initialize . For , |

| Step 1. Sample from . |

| Step 2. Sample from . |

The conditional distribution is given in (4) and

The joint posterior density is Gaussian with precision matrix , where , and . By Sahu and Roberts (1999), the rate of convergence of the Gibbs sampler is , the same as that stated in Theorem 1. Hence the Gibbs sampler converges instantly and produces independent draws when . Alternatively, if we combine the updates in steps 1 and 2, the update of at the th iteration is

where . The rate of convergence can be optimized by minimizing the autocorrelation at lag 1, , and the result in Theorem 1 follows.

Next, we demonstrate that variational Bayes can also benefit from partial noncentering. Consider a variational Bayes approximation to of the form . Subjected to this product density restriction, the optimal and , obtained by minimizing the Kullback-Leibler divergence from to , are and respectively (see, e.g. Ormerod and Wand, 2010), where

The variational Bayes algorithm thus iterates between updating and . Combining the two updates, we have at the th iteration,

Hence the rate of convergence is also given by , which is minimized to zero when . Moreover, . Hence and is able to capture the true marginal distribution of .

In summary, when is the only unknown parameter, the rate of convergence of the EM algorithm, Gibbs sampler and variational Bayes are all equal to , which is optimized at . This outcome is in line with the result of Tan and Nott (2014), who showed the equivalence of the rates of convergence between the EM algorithm, Gibbs sampler and variational Bayes, when the target density is Gaussian. Intuitively, minimizes the fraction of missing information for the EM algorithm, and the autocorrelation at lag 1 for the Gibbs sampler. For variational Bayes, , besides optimizing the rate of convergence, also produces a more accurate posterior approximation. This is because is zero when , and is then an accurate reflection of the dependence structure between and .

5 Non-Gaussian state space models

Next, we consider MCMC algorithms for Bayesian inference of some nonlinear and non-Gaussian state space models and demonstrate how the optimal augmentation schemes derived for the AR(1) plus noise model can be utilized to improve the mixing and convergence of the MCMC sampler. We focus on the stochastic volatility (SV) and stochastic conditional duration models.

5.1 Stochastic volatility model

The returns of financial time series often have variances that vary with time, and the SV model seeks to capture this behavior by modeling the log of the squared volatility as a hidden AR(1) process. The observation equation is

where represents the volatility, while is defined in (1). The and are independent sequences and the unknown parameter . We can transform the SV model into a linear model by writing

where follows a log distribution with mean, , and variance, . Harvey, Ruiz and Shephard (1994) approximate the distribution of using , thereby recovering the AR(1) plus noise model with replaced by and . They then estimated by maximizing the quasi-likelihood using Kalman filtering. However, Kim, Shephard and Chib (1998) showed that the distribution of is highly skewed and poorly approximated by a normal distribution, and they approximate it using a 7-component mixture of normal densities instead. Here we consider the improved mixture approximation with components by Omori et al. (2007). Let be mixture component indicators such that and for . Conditional on the mixture indicator ,

and the AR(1) plus noise model is recovered with replaced by and replaced by .

5.2 Stochastic conditional duration model

The timing of transactions is central to the study of the microstructure of financial markets. As time intervals between transactions are highly irregular, Engle and Russell (1998) formulated the autoregressive conditional duration model to analyze such data, treating arrival times as a point process and allowing the conditional intensity to be dependent on past durations. As an extension, Bauwens and Veredas (2004) propose the stochastic conditional duration model, which treats the log of the conditional mean of durations as a latent AR(1) process. The duration has positive support, and the observation equation is

where follows the exponential distribution with mean 1, while is defined as in (1). Other possible choices for the distribution of include Weibull and Gamma (Strickland, Forbes and Martin, 2006). We similarly transform this model into a linear one by writing

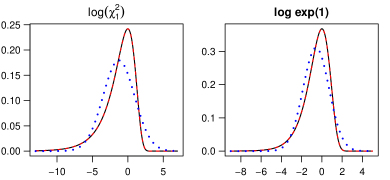

where has mean, , and variance, . The distribution of is also poorly approximated by and we approximate it using a mixture of normal densities. The 5-component mixture approximation for provided by Carter and Kohn (1997) is rather imprecise and we consider instead the 10-component mixture approximation for the standard Gumbel (type I extreme value) distribution found by Frühwirth-Schnatter and Frühwirth (2007), which is fitted by minimizing the Kullback-Leibler distance and shown to improve the accuracy of auxiliary mixture sampling when used in a Metropolis-Hastings algorithm. Frühwirth-Schnatter and Wagner (2010) further illustrates the use of auxiliary mixture sampling for variable selection in non-Gaussian state space models. The distribution of is a standard Gumbel and hence it suffices to add a negative sign to the means in Table 1 of Frühwirth-Schnatter and Frühwirth (2007). The parameters of the mixture approximation for the SV and stochastic conditional duration models are given in the Supplement (Tan, 2022). Figure 9 shows the true densities of and log exp(1), Gaussian approximation based on the mean and variance of the original variables and 10-component mixture approximations.

Using the mixture of normals approximation, we can construct MCMC algorithms for the SV and stochastic conditional duration models similarly, the only difference being for the SV model, while for the stochastic conditional duration model. Let , , and . In matrix notation,

where . As before, we introduce . Then the model can be written as

Following Kastner and Frühwirth-Schnatter (2014), we specify independent priors for the components of ; , such that , and for (Kim, Shephard and Chib, 1998). The joint posterior is

Choice of a gamma prior for instead of the conventional inverse-gamma prior reduces sensitivity to prior hyperparameters (Frühwirth-Schnatter and Wagner, 2010).

6 MCMC Algorithms

Kastner and Frühwirth-Schnatter (2014) have designed MCMC samplers for the SV model based on the mixture of normals approximation approach described in Section 5.1, using the CP or NCP. However, the performance of these algorithms vary across datasets with the CP or NCP preferred at times, depending on the level of volatility and persistence. On the other hand, the ancillarity-sufficiency interweaving strategy (ASIS, Yu and Meng, 2011) was shown to improve the sampling efficiency of all parameters across different settings. In this section, we first introduce a baseline MCMC algorithm for the SV and stochastic conditional duration models that is similar to Kastner and Frühwirth-Schnatter (2014) in some aspects, but may be used with arbitrary values of . Then we describe the ASIS algorithm followed by the proposed block-specific reparametrization strategy (BSR) that makes use of the optimal data augmentation schemes derived in Section 2.

Initialize and . For ,

-

1.

Sample from ,

-

2.

Sample from ,

-

3.

Sample from .

Return the draws .

The MCMC algorithm above may be used with arbitrary values of , and updates for the CP and NCP can be obtained simply by substituting appropriate values of . In steps 1 and 3, the sampling of and from their conditional posterior distributions are performed using Gibbs. To sample in step 2, Kastner and Frühwirth-Schnatter (2014) investigated 1-block, 2-block and 3-block samplers, all requiring Metropolis-Hastings updates. Conditional on the parametrization, the simulation efficiency was similar across different blocking strategies, but the 3-block sampler has lower simulation efficiency for compared to the 1-block and 2-block samplers under the CP. Here we only consider the 3-block sampler for . The updates in each step are derived below.

For the latent states, , where

As is a symmetric tridiagonal matrix, we first compute the decomposition of , where is a diagonal matrix and is a unit lower triangular matrix with only the first lower diagonal nonzero. is then computed using backward substitution. To generate , a random vector is first simulated from so that .

For the indicators ,

Thus, the are conditionally independent a posteriori. For , ,

where . Hence we can sample each according to the conditional posterior probabilities (normalized to sum to one) across .

We have , where

For , let for . Then

| (8) |

where is given by

We perform a Metropolis-Hastings step (Kim, Shephard and Chib, 1998), where a proposal is generated from

based on a normal approximation to the last term in (8). If , then is accepted with probability equal to .

For , we first discuss updates for the CP and NCP before proposing an update for arbitrary . For the CP, , where

and . Kastner and Frühwirth-Schnatter (2014) propose a Metropolis-Hastings step, where a proposal is generated from the inverse gamma distribution, , and is accepted with a probability of

For the NCP,

where and . Thus we can generate a proposal from , which is accepted if . For arbitrary , we consider a transformation so that is unconstrained. We have , where and its first and second order derivatives are given in the Supplement (Tan, 2022). Let denote the posterior mode found using the L-BFGS algorithm. Then since , and a normal approximation to the conditional posterior is . A proposal generated from this normal density is accepted with probability , where

6.1 Ancillarity-sufficiency interweaving strategy

The mixing and convergence of the baseline MCMC sampler depends heavily on the parametrization chosen for the data. For any parametrization, the simulation efficiency may also differ across parameters. As the behavior of the CP and NCP are often complementary (one converges quickly if the other is slow), Yu and Meng (2011) proposed an ancillarity-sufficiency interweaving strategy (ASIS), that interweaves a sufficient augmentation scheme where the missing data is a sufficient statistic for (usually the CP), and an ancillary augmentation scheme where the missing data is an ancillary statistic independent of (usually the NCP). It is proven that ASIS is at least better than the worse of the two schemes. ASIS can be implemented using the CP or NCP as baseline, but Kastner and Frühwirth-Schnatter (2014) report that choice of the baseline is immaterial. Hence, we only consider ASIS with CP as baseline, the steps of which are outlined below.

Initialize and . For ,

-

1.

Under the CP (set , ):

-

(a)

Sample from .

-

(b)

Sample from .

-

(a)

-

2.

Move to the NCP (set , ):

-

(a)

Compute .

-

(b)

Sample from .

-

(a)

-

3.

Move back to the CP (set , ):

-

(a)

Compute .

-

(b)

Sample from .

-

(a)

Return the draws .

6.2 Block-specific reparametrization strategy

To optimize the convergence rate of the EM algorithm for the AR(1) plus noise model, we employed Algorithm 3 so that the optimal parametrization for each parameter can be used while conditioning on the rest. As the convergence rate of the Gibbs sampler is equal to the corresponding EM algorithm when the target density is well approximated by a Gaussian (Sahu and Roberts, 1999), tailoring the data augmentation scheme to each block in a Gibbs sampler may yield similar improvements in convergence rates as in the EM algorithm. This is important as the simulation efficiency of a parametrization may be good for certain parameters but poor for others. Hence we propose a block-specific reparametrization (BSR) strategy that allows one to adopt a different parametrization for sampling from each block in a multi-block MCMC sampler. This yields flexibility in choosing a parametrization optimal for sampling from each block.

First, we outline the steps of an MCMC sampler adopting the BSR strategy and verify that the sampler will converge to the target density, before discussing the reparametrizations for each block. For simplicity, we limit the discussion to two blocks although BSR can be applied to multiple blocks. Suppose the parameters are split into two blocks, , and consider two augmentation schemes with missing data and such that their joint distribution is well defined. This distribution may be degenerate, e.g. if is a deterministic function of . Consider an MCMC algorithm that initializes and then performs the following steps at the th iteration for (explicit conditioning on has been omitted for simplicity):

-

1.

Sample from .

-

2.

Sample from .

-

3.

Sample from .

-

4.

Sample from .

The draws are retained. The transition density of the above chain is

Let denote the stationary density. We have

Hence the stationary density is preserved by BSR. Moreover, if is a deterministic function () of given , then we can compute without sampling in step 3. This feature is important in models where is high-dimensional (e.g. state space models) and sampling of is time-consuming.

Next, we discuss how BSR can be applied. Conditional on , and , . Comparing this distribution with (3), the differences are, is replaced by , and is replaced by . In Section 4.1, we have shown that when using the EM algorithm to find the posterior mode, the optimal parametrizations for and remain unchanged and are independent of the priors. It can also be verified that for the AR(1) plus noise model, if is not constant across time, then it suffices to replace in the expressions of and by a diagonal matrix filled with the variances at different time points (see Supplement (Tan, 2022)). Applying these results to the SV and stochastic conditional duration models using a mixture of normals approximation, we divide the parameters into two blocks, and , and use the optimal schemes for and respectively in these two blocks. Based on the EM algorithm, is independent of . Hence it is not possible to choose to optimize the convergence of , and we just sample it along with in the second scheme. For convenience, is sampled in the second scheme as well. Conditional on , the values of in the first scheme are

| (9) |

where and we have chosen for simplicity. For the second scheme,

| (10) |

where . Since for , we can set when switching from the first to second scheme. The steps in the MCMC sampler using BSR are outlined below.

Initialize and . For ,

-

1.

First scheme (set , ):

-

(a)

Sample .

-

(b)

Sample .

-

(a)

-

2.

Switch to second scheme (set , ):

-

(a)

Compute .

-

(b)

Sample .

-

(c)

Sample .

-

(d)

Sample .

-

(a)

Return the draws .

The values of in (9) and (10) depend on the true values of and , which are unknown. Hence we propose the following procedure to overcome this difficulty. To initialize , , and , we run Algorithm 3 on transformed responses , by approximating the distribution of in the SV model by a single Gaussian , and in the stochastic conditional duration model by . The maximum likelihood estimate is used as initial estimate , while is simulated randomly from its prior distribution. This initialization is also used for the baseline MCMC algorithm and ASIS. We use to compute , , by assuming is constant across (equal to 4.93 and 1.64 for the SV and stochastic conditional duration models respectively). These values of , , are held fixed for the first two-thirds of the burn-in period. We estimate the posterior means of and using draws after the first one-third till the first two-thirds of burn-in, and these are used to update the values of , , after the first two-thirds of burn-in. For the remainder of the sampling period, , , are held fixed at these values. Our experiments indicate that BSR works well even with these rather crude estimates of , , .

For the SV model, it may be of interest to estimate the volatility at time , . Since , we can draw by sampling from , which is under the CP, for each draw of from . The MCMC samplers presented are based on a mixture of normals approximation of the and log exp(1) distributions, and hence the samples are not strictly drawn from the true posterior. This minor approximation error can be corrected by reweighting the draws (see Kim, Shephard and Chib, 1998). As the mixture approximation used is very accurate, Kim, Shephard and Chib (1998) and Omori et al. (2007) report that the effect of reweighting is small and estimates of posterior means are not significantly different statistically. There is however, some improvement in the Monte Carlo standard errors. We focus on comparison of different MCMC samplers, and do not perform reweighting in our experiments. Hosszejni and Kastner (2021) present two R packages, stochvol and factorstochvol for Bayesian estimation of univariate SV models (with linear means, leverage or heavy tails) and multivariate factor SV models. In stochvol, sampling of the latent states also relies on a Gaussian mixture approximation and correction of the approximation error, while not implemented by default, can be enabled simply through an argument.

7 Experimental results

We compare BSR with the baseline MCMC algorithm using the CP or NCP and ASIS, using simulated data and several benchmark real datasets. Following Kastner and Frühwirth-Schnatter (2014), we use the inefficiency factor to assess simulation efficiency, which is estimated as the ratio of the variance of the sample mean from the MCMC sampler, to the variance of the sample mean based on independent draws. It can be computed using the R package coda (Plummer et al., 2006) as number of draws/effective sample size. Smaller inefficiency factors indicate better mixing and lower autocorrelation among draws. Each MCMC sampler is run for 30,000 iterations, of which the first 10,000 are discarded as burn-in. All code is written in Julia 1.6.1 (Bezanson et al., 2017) and R (R Core Team, 2020). The experiment on consumer price index is run on an Intel Xeon Gold 5222 CPU @3.80GHz while all other experiments are run on an Intel Core i9-9900K CPU @3.60 GHz.

7.1 Simulations

First, we present results on data simulated from the SV and stochastic conditional duration models. For each model, we consider , and , which yields nine parameter settings. In each setting, observations are generated and each experiment is repeated ten times. For the priors, following Kastner and Frühwirth-Schnatter (2014), we set , , , and (this represents a prior on with mean equal to ).

| NCP | CP | ASIS | BSR | NCP | CP | ASIS | BSR | NCP | CP | ASIS | BSR | ||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 0.4 | 0.05 | 18 | 79 | 17 | 20 | 63 | 710 | 63 | 66 | 109 | 111 | 116 | 112 |

| 0.5 | 17 | 16 | 9 | 9 | 42 | 68 | 32 | 31 | 51 | 54 | 52 | 48 | |

| 5 | 67 | 4 | 4 | 4 | 40 | 17 | 15 | 13 | 16 | 13 | 13 | 12 | |

| 0.7 | 0.05 | 14 | 26 | 11 | 13 | 72 | 471 | 73 | 68 | 110 | 128 | 114 | 112 |

| 0.5 | 32 | 7 | 5 | 5 | 54 | 64 | 37 | 31 | 43 | 43 | 34 | 28 | |

| 5 | 226 | 2 | 2 | 2 | 70 | 17 | 16 | 13 | 19 | 9 | 9 | 8 | |

| 0.95 | 0.05 | 99 | 2 | 2 | 2 | 69 | 136 | 51 | 30 | 48 | 75 | 36 | 21 |

| 0.5 | 823 | 1 | 1 | 1 | 114 | 28 | 24 | 13 | 33 | 9 | 8 | 5 | |

| 5 | 5994 | 1 | 1 | 1 | 330 | 12 | 12 | 9 | 13 | 3 | 2 | 2 | |

The inefficiency factors averaged over ten repetitions for each parameter setting are shown in Tables 4 and 5 for the SV and stochastic conditional duration models respectively. The BSR strategy worked very well for both models, and the inefficiency factors are (almost) always better than the worst of NCP and CP. It is even able to yield improvements over ASIS in many cases. We also observe that in a given setting, neither the CP or NCP may be superior to the other in terms of simulation efficiency across all parameters. Hence BSR can yield benefits beyond the CP and NCP by tailoring the parametrization to each block. We have also performed experiments for negative values of and the results (not shown) are similar to positive values of (much like a reflection about ).

| NCP | CP | ASIS | BSR | NCP | CP | ASIS | BSR | NCP | CP | ASIS | BSR | ||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 0.4 | 0.05 | 20 | 35 | 19 | 18 | 94 | 402 | 87 | 87 | 112 | 110 | 113 | 112 |

| 0.5 | 34 | 10 | 8 | 8 | 51 | 49 | 34 | 33 | 42 | 36 | 36 | 33 | |

| 5 | 197 | 2 | 2 | 2 | 70 | 9 | 8 | 7 | 8 | 6 | 6 | 6 | |

| 0.7 | 0.05 | 21 | 16 | 11 | 11 | 111 | 302 | 92 | 96 | 110 | 127 | 106 | 105 |

| 0.5 | 92 | 4 | 4 | 3 | 76 | 43 | 34 | 29 | 44 | 27 | 25 | 21 | |

| 5 | 700 | 1 | 1 | 1 | 130 | 10 | 10 | 8 | 11 | 5 | 5 | 4 | |

| 0.95 | 0.05 | 322 | 2 | 1 | 1 | 124 | 85 | 54 | 32 | 62 | 39 | 30 | 18 |

| 0.5 | 2427 | 1 | 1 | 1 | 239 | 23 | 21 | 16 | 36 | 6 | 6 | 5 | |

| 5 | 9765 | 1 | 1 | 1 | 731 | 9 | 9 | 7 | 7 | 2 | 2 | 2 | |

The average runtime of each MCMC sampler is given in Table 6. The amount of computation required by NCP and CP are about the same, while BSR requires slightly more computation (for updating the working parameters and switching to the second scheme in each iteration). ASIS requires the most computation due to switching of schemes and multiple simulation of certain parameters at each iteration, but the increase in runtime of BSR and ASIS compared to CP and NCP are not significant.

| NCP | CP | ASIS | BSR | |

|---|---|---|---|---|

| SV | 238 | 238 | 245 | 241 |

| Stochastic conditional duration | 202 | 202 | 210 | 206 |

7.2 Real data

We consider three datasets on exchange rates, US consumer price index and IBM transactions. We set the priors as , (following Kim, Shephard and Chib, 1998), and . For the exchange rates, , while for the consumer price index and IBM transactions, .

The exchange rate data is downloaded from the European Central Bank’s Statistical Data Warehouse. Kastner and Frühwirth-Schnatter (2014) analyzed observations of the daily Euro exchange rates of 23 currencies from 3 Jan 2000 to 4 Apr 2012 using the SV model. Of these, we select the Danish krone, New Zealand dollar and US dollar, which are representative of currencies with the lowest, moderate and highest persistence respectively. Let be the exchange rate at time . The response is the mean-corrected differenced log return. Using MCMC samplers to fit the SV model to the exchange rates, we obtain the inefficiency factors in Table 7. The simulation efficiency of CP is higher than NCP for but lower than NCP for . Hence, neither is a good option. ASIS achieves much better results but BSR is the clear winner, with the lowest inefficiency factors across all currencies and parameters.

| NCP | CP | ASIS | BSR | NCP | CP | ASIS | BSR | NCP | CP | ASIS | BSR | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Danish | 91 | 3 | 3 | 3 | 97 | 143 | 64 | 43 | 71 | 87 | 52 | 32 |

| NZ | 110 | 3 | 2 | 2 | 189 | 461 | 129 | 72 | 147 | 345 | 113 | 58 |

| US | 455 | 1 | 1 | 1 | 123 | 354 | 78 | 28 | 84 | 114 | 39 | 14 |

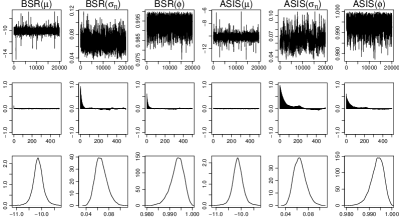

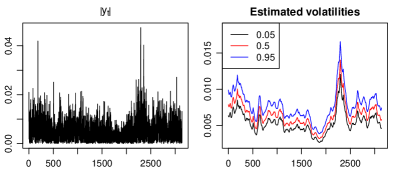

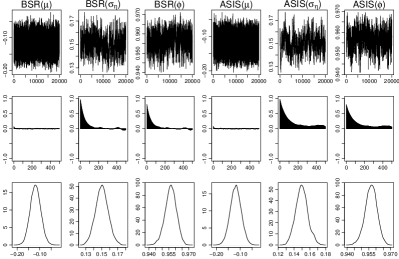

The parameter estimates and runtime of each sampler are given in the Supplement (Tan, 2022). NCP is the fastest, followed by CP, BSR and ASIS, but the runtime of all samplers are practically the same. Figure 10 shows the trace plots, sample autocorrelation function and marginal posterior densities of for the US dollar. There is better mixing in BSR’s chain than ASIS’s, and the sample autocorrelation for also decay faster. These observations are consistent with the inefficiency factors. Figure 11 shows the 0.05, 0.5 and 0.95 quantiles of volatilities estimated using 20000 samples from BSR, and a similar pattern with can be detected.

The US consumer price index inflation rate from the 2nd quarter of 1947 to the 3rd quarter of 2011 (Kroese and Chan, 2014) comprises of observations and a SV model is fitted to the mean-corrected rates. Besides the baseline MCMC samplers, ASIS and BSR, we also provide comparisons with NUTS (Hamiltonian Monte Carlo No U-turn sampler in Stan) and PMMH (particle marginal Metropolis-Hastings algorithm in R package nimble). No tuning is required for NUTS. Following Michaud et al. (2020), PMMH is run using the auxiliary particle filter (Pitt and Shephard, 1999b) and a block random walk sampler with a normal proposal. It is rather sensitive to initialization, the number of particles and the scale of proposal, which must be set by the user. We set the starting values as the posterior means, and standard deviations of the proposal as times the posterior standard deviations computed using BSR. We consider and . For this dataset, PMMH tends to get stuck for many iterations and mixing is poor. We report results for and , which has the best inefficiency factors. The parameter estimates, inefficiency factors and runtimes are given in Table 8.

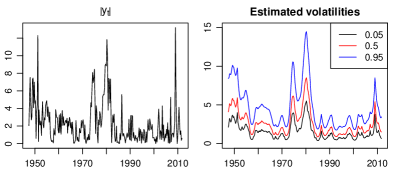

The simulation efficiency of CP is better than NCP, and ASIS improves upon CP, while BSR improves upon ASIS. NUTS also provided improvements compared to the respective baseline samplers. NUTS and PMMH are generally more computationally intensive than standard MCMC samplers. NUTS uses automatic differentiation to compute gradients of the Hamiltonian at each iteration, which enables it to explore the posterior distribution of highly correlated parameters more thoroughly. On the other hand, a particle filter has to be run at each iteration for PMMH and computation costs scale linearly with the number of particles. While PMMH is valid even for small number of particles, it has a risk of getting stuck due to the variance in the likelihood approximation. The consumer price index inflation exhibits high persistence, and the volatilities estimated using 20000 samples from BSR in Figure 12 captures the high inflation in the late 1970s to early 1980s. After that, inflation remains low and stable until the 2008 financial crisis.

| NCP | CP | ASIS | BSR | NUTS (NCP) | NUTS (CP) | PMMH | ||

| Parameter estimates | 1.56 0.48 | 1.61 0.48 | 1.62 0.47 | 1.61 0.47 | 1.61 0.45 | 1.61 0.55 | 1.66 0.42 | |

| 0.60 0.10 | 0.60 0.11 | 0.59 0.10 | 0.60 0.10 | 0.61 0.11 | 0.60 0.11 | 0.56 0.09 | ||

| 0.90 0.04 | 0.90 0.04 | 0.90 0.04 | 0.90 0.04 | 0.90 0.04 | 0.90 0.04 | 0.91 0.03 | ||

| Inefficiency factor | 260 | 2 | 1 | 1 | 24 | 1 | 72 | |

| 50 | 37 | 26 | 19 | 8 | 24 | 118 | ||

| 37 | 15 | 13 | 8 | 7 | 10 | 92 | ||

| Runtime | 14 | 14 | 15 | 16 | 113 | 138 | 749 |

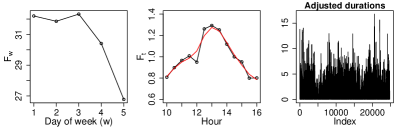

The benchmark IBM transactions data is extracted from the TORQ data built by Joel Hasbrouck and NYSE (Tsay, 2010). It has the time of occurrence (measured in seconds from midnight) of each transaction from 1 Nov 1990 to 31 Jan 1991, and we analyze the duration between consecutive transactions, , using the stochastic conditional duration model. Only transactions within normal trading hours (9.30 a.m to 4 p.m.) from 1 Nov to 21 Dec are considered to avoid holiday effects, and 23 Nov is excluded due to a halt in trading. Due to the unusually high concentration of short durations immediately after opening, Engle and Russell (1998) recommend removing transactions before 10 a.m. and taking the first duration as the average duration of transactions from 9.50 a.m. to 10 a.m. After this procedure and the removal of zero durations, we have observations. Following Feng, Jiang and Song (2004), we remove seasonality due to day-of-week effect (trading increases in frequency towards end of week) and time-of-day effect (trading is more frequent at the start and end, than in middle of the day) before analysis. To remove day-of-week effect, we compute the average duration for each weekday and set if falls in the weekday . For time-of-week effect, we construct 13 knots at 30 minutes interval from 10 a.m. to 4 p.m., . The value at knot is the average of durations whose transaction time falls in . The smoothed value is computed using piecewise cubic splines via the smooth.spline function in R, and the adjusted duration is if transaction time of falls in . See Figure 13 for illustration.

Fitting the stochastic conditional duration model to the adjusted durations, the parameter estimates and inefficiency factors are shown in Table 9. The simulation efficiency of the CP is better than NCP for and , but worse for . ASIS improves the simulation efficiency for and significantly but BSR produces even better results. The trace plots in Figure 14 also indicate that there is better mixing in the MCMC chains of and for BSR than ASIS (sample autocorrelations also decay faster).

| NCP | CP | ASIS | BSR | ||

|---|---|---|---|---|---|

| Parameter estimates | 0.022 | 0.023 | 0.023 | 0.023 | |

| 0.149 0.008 | 0.150 0.008 | 0.150 0.008 | 0.150 0.008 | ||

| 0.957 0.004 | 0.956 0.004 | 0.957 0.004 | 0.956 0.004 | ||

| Inefficiency factor | 132 | 3 | 2 | 2 | |

| 259 | 311 | 135 | 88 | ||

| 207 | 186 | 107 | 68 |

8 Conclusion

This article investigates efficient data augmentation techniques for some classes of state space models by introducing working parameters for rescaling and recentering of the latent states. First, we focus on maximum likelihood estimation of the AR(1) plus noise model via the EM algorithm and derived optimal values of by minimizing the fraction of missing information. An alternating expectation-conditional maximization algorithm that allows the optimal parametrization for each parameter to be used while conditioning on others is then designed. Experiments indicate that this algorithm is often able to outperform the CP and NCP in rate of convergence and maximized likelihood. The proposed data augmentation scheme is then utilized to design efficient MCMC algorithms for Bayesian inference of the SV and stochastic conditional duration models through a mixture of normals approximation. A BSR strategy which allows the data augmentation scheme to be tailored to each block is proposed for a MCMC sampler. Experimental results indicate that BSR works well, surpassing ASIS in all real applications.

These encouraging results motivate the application of BSR to other classes of state space models where the parametrization greatly affects the convergence of the MCMC sampler. Consider the multivariate factor SV model of Pitt and Shephard (1999c), where each of the factor terms and idiosyncratic error terms follow independent SV processes. As the standard full conditional sampler converges slowly, Kastner, Frühwirth-Schnatter and Lopes (2017) employ ASIS to improve convergence. We can also apply BSR to sample the parameters of each SV process via the mixture of normals approximation, by allowing each SV process to have its own set of working parameters. Optimal values of the working parameters for each SV process can likely be deduced from this article by conditioning on other variables. For parsimony, one may also restrict to be constant across time points which is feasible when the number of observations is large (Theorem 2). Li and Scharth (2020) further apply ASIS to factor SV models with leverage, asymmetry and heavy tails, and the BSR strategy is likely to be useful here as well although it is challenging to derive optimal values of the working parameters analytically. It is worth exploring if plugging in values based on Gaussian approximations of such models will yield improvements compared to the NCP and CP.

Another application is to the time-varying parameter models investigated by Bitto and Frühwirth-Schnatter (2019), which resemble regression models with time-varying coefficients following a random walk. To prevent overfitting, the double gamma shrinkage prior was placed on process variances to reduce time-varying coefficients to statics ones. The parametrization is important here as the CP is preferred for time-varying coefficients while the NCP is preferred for static ones, and Bitto and Frühwirth-Schnatter (2019) use ASIS to “combine the best of both worlds”. In this case, it is possible to partially rescale and recenter the time-varying coefficients using fixed mean and standard deviation parameters. If each coefficient is allowed to have its own set of working parameters, then BSR offers the flexibility of using the optimal parametrization for each coefficient and hence it can potentially perform as well as or even better than ASIS. However, the random walk is a non-stationary process and the optimal working parameters will have to be re-derived using say the EM algorithm as a starting point (as in this article), or some other criteria such as minimization of the posterior correlation between blocks.

Kreuzer and Czado (2020) consider nonlinear state space models where the latent states follow an AR(1) process and apply ASIS to improve the efficiency of the proposed elliptical slice sampler. They consider an NCP of the form instead of , and it is worthwhile to contemplate the construction of an associated PNCP which directly impacts the convergence rate of . Finally, it is also interesting to explore how the proposed data augmentation scheme can be applied to construct efficient variational approximation algorithms for state space models whose rate of convergence is also strongly dependent on the choice of parametrization.

[Acknowledgments] The author would like to thank the Editor, Associate Editor and three referees for their comments and helpful suggestions which have improved this manuscript greatly. The author also wish to thank Dion Kwan and Robert Kohn for comments and discussion on this work. {funding} The author was supported by the start-up grant (R-155-000-190-133).

Zip file \sdescriptionJulia code and a pdf file containing derivations, proofs and additional details.

References

- Abanto-Valle and Dey (2014) {barticle}[author] \bauthor\bsnmAbanto-Valle, \bfnmCarlos A.\binitsC. A. and \bauthor\bsnmDey, \bfnmDipak K.\binitsD. K. (\byear2014). \btitleState space mixed models for binary responses with scale mixture of normal distributions links. \bjournalComput. Statist. Data Anal. \bvolume71 \bpages274–287. \bdoihttps://doi.org/10.1016/j.csda.2013.01.009 \endbibitem

- Almeida and Czado (2012) {barticle}[author] \bauthor\bsnmAlmeida, \bfnmCarlos\binitsC. and \bauthor\bsnmCzado, \bfnmClaudia\binitsC. (\byear2012). \btitleEfficient Bayesian inference for stochastic time-varying copula models. \bjournalComput. Statist. Data Anal. \bvolume56 \bpages1511–1527. \bdoihttps://doi.org/10.1016/j.csda.2011.08.015 \endbibitem

- Andrieu, Doucet and Holenstein (2010) {barticle}[author] \bauthor\bsnmAndrieu, \bfnmChristophe\binitsC., \bauthor\bsnmDoucet, \bfnmArnaud\binitsA. and \bauthor\bsnmHolenstein, \bfnmRoman\binitsR. (\byear2010). \btitleParticle Markov chain Monte Carlo methods. \bjournalJ. R. Stat. Soc. Ser. B. Stat. Methodol. \bvolume72 \bpages269–342. \bdoihttps://doi.org/10.1111/j.1467-9868.2009.00736.x \endbibitem

- Bass and Sahu (2017) {barticle}[author] \bauthor\bsnmBass, \bfnmMark R.\binitsM. R. and \bauthor\bsnmSahu, \bfnmSujit K.\binitsS. K. (\byear2017). \btitleA comparison of centring parameterisations of Gaussian process-based models for Bayesian computation using MCMC. \bjournalStat. Comput. \bvolume27 \bpages1491–1512. \endbibitem

- Bauwens and Veredas (2004) {barticle}[author] \bauthor\bsnmBauwens, \bfnmLuc\binitsL. and \bauthor\bsnmVeredas, \bfnmDavid\binitsD. (\byear2004). \btitleThe stochastic conditional duration model: a latent variable model for the analysis of financial durations. \bjournalJ. Econom. \bvolume119 \bpages381–412. \bdoihttps://doi.org/10.1016/S0304-4076(03)00201-X \endbibitem

- Berlinet and Roland (2009) {barticle}[author] \bauthor\bsnmBerlinet, \bfnmA.\binitsA. and \bauthor\bsnmRoland, \bfnmC.\binitsC. (\byear2009). \btitleParabolic acceleration of the EM algorithm. \bjournalStat. Comput. \bvolume19 \bpages35–47. \endbibitem

- Bezanson et al. (2017) {barticle}[author] \bauthor\bsnmBezanson, \bfnmJeff\binitsJ., \bauthor\bsnmEdelman, \bfnmAlan\binitsA., \bauthor\bsnmKarpinski, \bfnmStefan\binitsS. and \bauthor\bsnmShah, \bfnmViral B\binitsV. B. (\byear2017). \btitleJulia: A fresh approach to numerical computing. \bjournalSIAM review \bvolume59 \bpages65–98. \endbibitem

- Bitto and Frühwirth-Schnatter (2019) {barticle}[author] \bauthor\bsnmBitto, \bfnmAngela\binitsA. and \bauthor\bsnmFrühwirth-Schnatter, \bfnmSylvia\binitsS. (\byear2019). \btitleAchieving shrinkage in a time-varying parameter model framework. \bjournalJ. Econom. \bvolume210 \bpages75–97. \bdoihttps://doi.org/10.1016/j.jeconom.2018.11.006 \endbibitem

- Blei, Kucukelbir and McAuliffe (2017) {barticle}[author] \bauthor\bsnmBlei, \bfnmDavid M.\binitsD. M., \bauthor\bsnmKucukelbir, \bfnmAlp\binitsA. and \bauthor\bsnmMcAuliffe, \bfnmJon D.\binitsJ. D. (\byear2017). \btitleVariational inference: A review for statisticians. \bjournalJ. Am. Stat. Assoc. \bvolume112 \bpages859–877. \endbibitem

- Carter and Kohn (1997) {barticle}[author] \bauthor\bsnmCarter, \bfnmC. K.\binitsC. K. and \bauthor\bsnmKohn, \bfnmR.\binitsR. (\byear1997). \btitleSemiparametric Bayesian inference for time series with mixed spectra. \bjournalJ. R. Stat. Soc. Ser. B. Stat. Methodol. \bvolume59 \bpages255–268. \bdoihttps://doi.org/10.1111/1467-9868.00067 \endbibitem

- Carvalho et al. (2010) {barticle}[author] \bauthor\bsnmCarvalho, \bfnmCarlos M.\binitsC. M., \bauthor\bsnmJohannes, \bfnmMichael S.\binitsM. S., \bauthor\bsnmLopes, \bfnmHedibert F.\binitsH. F. and \bauthor\bsnmPolson, \bfnmNicholas G.\binitsN. G. (\byear2010). \btitleParticle learning and smoothing. \bjournalStatist. Sci. \bvolume25 \bpages88–106. \bdoi10.1214/10-STS325 \endbibitem

- Christensen, Roberts and Sköld (2006) {barticle}[author] \bauthor\bsnmChristensen, \bfnmOle F\binitsO. F., \bauthor\bsnmRoberts, \bfnmGareth O\binitsG. O. and \bauthor\bsnmSköld, \bfnmMartin\binitsM. (\byear2006). \btitleRobust Markov chain Monte Carlo methods for spatial generalized linear mixed models. \bjournalJ. Comput. Graph. Statist. \bvolume15 \bpages1–17. \bdoi10.1198/106186006X100470 \endbibitem

- Cryer and Chan (2008) {binbook}[author] \bauthor\bsnmCryer, \bfnmJ. D.\binitsJ. D. and \bauthor\bsnmChan, \bfnmK. S.\binitsK. S. (\byear2008). \btitleTime series analysis with applications in R. \bpublisherSpringer, \baddressNew York, USA. \endbibitem

- de Valpine et al. (2017) {barticle}[author] \bauthor\bsnmde Valpine, \bfnmPerry\binitsP., \bauthor\bsnmTurek, \bfnmDaniel\binitsD., \bauthor\bsnmPaciorek, \bfnmChristopher\binitsC., \bauthor\bsnmAnderson-Bergman, \bfnmCliff\binitsC., \bauthor\bsnmTemple Lang, \bfnmDuncan\binitsD. and \bauthor\bsnmBodik, \bfnmRas\binitsR. (\byear2017). \btitleProgramming with models: writing statistical algorithms for general model structures with NIMBLE. \bjournalJournal of Computational and Graphical Statistics \bvolume26 \bpages403–413. \endbibitem

- Dempster, Laird and Rubin (1977) {barticle}[author] \bauthor\bsnmDempster, \bfnmA. P.\binitsA. P., \bauthor\bsnmLaird, \bfnmN. M.\binitsN. M. and \bauthor\bsnmRubin, \bfnmD. B.\binitsD. B. (\byear1977). \btitleMaximum likelihood from incomplete data via the EM algorithm. \bjournalJ. R. Stat. Soc. Ser. B. Stat. Methodol. \bvolume39 \bpages1–38. \endbibitem

- Doucet, de Freitas and Gordon (2012) {binbook}[author] \bauthor\bsnmDoucet, \bfnmArnaud\binitsA., \bauthor\bparticlede \bsnmFreitas, \bfnmNando\binitsN. and \bauthor\bsnmGordon, \bfnmNeil\binitsN. (\byear2012). \btitleSequential Monte Carlo methods in practice. \bpublisherSpringer, \baddressNew York. \endbibitem

- Engle and Russell (1998) {barticle}[author] \bauthor\bsnmEngle, \bfnmRobert F.\binitsR. F. and \bauthor\bsnmRussell, \bfnmJeffrey R.\binitsJ. R. (\byear1998). \btitleAutoregressive conditional duration: A new model for irregularly spaced transaction data. \bjournalEconometrica \bvolume66 \bpages1127–1162. \endbibitem

- Fearnhead and Meligkotsidou (2016) {barticle}[author] \bauthor\bsnmFearnhead, \bfnmP.\binitsP. and \bauthor\bsnmMeligkotsidou, \bfnmL.\binitsL. (\byear2016). \btitleAugmentation schemes for particle MCMC. \bjournalStat. Comput. \bvolume26 \bpages1293–1306. \endbibitem

- Feng, Jiang and Song (2004) {barticle}[author] \bauthor\bsnmFeng, \bfnmDingan\binitsD., \bauthor\bsnmJiang, \bfnmGeorge J.\binitsG. J. and \bauthor\bsnmSong, \bfnmPeter X. K.\binitsP. X. K. (\byear2004). \btitleStochastic conditional duration models with “leverage effect” for financial transaction data. \bjournalJ. Financial Econ. \bvolume2 \bpages390–421. \bdoi10.1093/jjfinec/nbh016 \endbibitem

- Frühwirth-Schnatter (2004) {bincollection}[author] \bauthor\bsnmFrühwirth-Schnatter, \bfnmSylvia\binitsS. (\byear2004). \btitleEfficient Bayesian parameter estimation. In \bbooktitleState Space and Unobserved Component Models: Theory and Applications (\beditor\bfnmAndrew\binitsA. \bsnmHarvey, \beditor\bfnmSiem Jan\binitsS. J. \bsnmKoopman and \beditor\bfnmNeilEditors\binitsN. \bsnmShephard, eds.) \bpages123–151. \bpublisherCambridge University Press. \endbibitem

- Frühwirth-Schnatter and Frühwirth (2007) {barticle}[author] \bauthor\bsnmFrühwirth-Schnatter, \bfnmSylvia\binitsS. and \bauthor\bsnmFrühwirth, \bfnmRudolf\binitsR. (\byear2007). \btitleAuxiliary mixture sampling with applications to logistic models. \bjournalComput. Statist. Data Anal. \bvolume51 \bpages3509–3528. \endbibitem

- Frühwirth-Schnatter and Wagner (2010) {barticle}[author] \bauthor\bsnmFrühwirth-Schnatter, \bfnmSylvia\binitsS. and \bauthor\bsnmWagner, \bfnmHelga\binitsH. (\byear2010). \btitleStochastic model specification search for Gaussian and partial non-Gaussian state space models. \bjournalJ. Econom. \bvolume154 \bpages85–100. \endbibitem

- Gelfand, Sahu and Carlin (1995) {barticle}[author] \bauthor\bsnmGelfand, \bfnmAlan E.\binitsA. E., \bauthor\bsnmSahu, \bfnmSujit K.\binitsS. K. and \bauthor\bsnmCarlin, \bfnmBradley P.\binitsB. P. (\byear1995). \btitleEfficient parametrisations for normal linear mixed models. \bjournalBiometrika \bvolume82 \bpages479–488. \endbibitem

- Gelfand, Sahu and Carlin (1996) {binproceedings}[author] \bauthor\bsnmGelfand, \bfnmAlan E.\binitsA. E., \bauthor\bsnmSahu, \bfnmSujit K.\binitsS. K. and \bauthor\bsnmCarlin, \bfnmBradley P.\binitsB. P. (\byear1996). \btitleEfficient parametrisations for generalized linear mixed models. In \bbooktitleBayesian Statistics 5 (\beditor\bfnmJ. M.\binitsJ. M. \bsnmBernardo, \beditor\bfnmJ. O.\binitsJ. O. \bsnmBerger, \beditor\bfnmA. P.\binitsA. P. \bsnmDawid and \beditor\bfnmA. F. M.\binitsA. F. M. \bsnmSmith, eds.) \bpages165–180. \bpublisherOxford University Press, \baddressNew York. \endbibitem

- Geman and Geman (1984) {barticle}[author] \bauthor\bsnmGeman, \bfnmStuart\binitsS. and \bauthor\bsnmGeman, \bfnmDonald\binitsD. (\byear1984). \btitleStochastic relaxation, Gibbs distributions, and the Bayesian restoration of Images. \bjournalIEEE Trans. Pattern Anal. Mach. Intell. \bvolumePAMI-6 \bpages721–741. \bdoi10.1109/TPAMI.1984.4767596 \endbibitem