Nonparametric MANOVA in Mann-Whitney effects1

Abstract

Multivariate analysis of variance (MANOVA) is a powerful and versatile method to infer and quantify main and interaction effects in metric multivariate multi-factor data. It is, however, neither robust against change in units nor a meaningful tool for ordinal data. Thus, we propose a novel nonparametric MANOVA. Contrary to existing rank-based procedures we infer hypotheses formulated in terms of meaningful Mann-Whitney-type effects in lieu of distribution functions. The tests are based on a quadratic form in multivariate rank effect estimators and critical values are obtained by the bootstrap. This newly developed procedure provides asymptotically exact and consistent inference for general models such as the nonparametric Behrens-Fisher problem as well as multivariate one-, two-, and higher-way crossed layouts. Computer simulations in small samples confirm the reliability of the developed method for ordinal as well as metric data with covariance heterogeneity. Finally, an analysis of a real data example illustrates the applicability and correct interpretation of the results.

Keywords: Covariance Heteroscedasticity; Multivariate Data; Multivariate Ordinal Data; Multiple Samples; Rank-based Methods; Wild Bootstrap.

∗ Vrije Universiteit Amsterdam, Department of Mathematics, Netherlands

email: d.dobler@vu.nl

† Ulm University, Institute of Statistics, Germany

email: sarah.friedrich@uni-ulm.de

email: markus.pauly@uni-ulm.de

1 Authors are in alphabetical order.

1 Motivation and Introduction

In many experiments, e.g., in the life sciences or in econometrics, observations are obtained in elaborate factorial designs with multiple endpoints. Such data are usually analyzed using MANOVA methods such as Wilk’s . These procedures, however, rely on the assumptions of multivariate normality and covariance homogeneity and usually break down if these prerequisites are not fulfilled. In particular, if the observations are not even metric, such applications are no longer possible since means no longer provide adequate effect measures. To this end, several rank-based methods have been proposed for nonparametric MANOVA and repeated measures designs which are usually based on Mann-Whitney-type effects: In the context of a nonparametric univariate two-sample problem with independent and continuous observations , Mann and Whitney, (1947) introduced the effect also known as ordinal effect size measure (Acion et al., , 2006). An estimator of is easily obtained by replacing the distribution functions with their empirical counterparts. While this effect has several desirable properties and is widely accepted in practice (Brumback et al., , 2006; Kieser et al., , 2013), generalizations to more than one dimension or higher-way factorial designs are not straightforward.

Concerning the latter, there basically exist two possibilities in the literature to cope with sample groups with independent univariate observations : First, considering only the pairwise effects (as proposed by Rust and Filgner, , 1984) can lead to paradox results in the sense of Efron’s Dice; see also Thas et al., (2012) and the contributed discussions by M. P. Fay and W. Bergsma and colleagues for pros and cons of the possibly induced intransitivity by certain probabilistic index models. We refer to Brown and Hettmansperger, (2002); Thangavelu and Brunner, (2007) or Brunner et al., (2017) and the references cited therein for further considerations on this issue. Second, in order to circumvent the problem of intransitive effects, the group-wise distribution functions may be compared to the same reference distribution. Usually, this is the pooled distribution function (Kruskal, , 1952; Kruskal and Wallis, , 1952), resulting in so-called (e.g., Brunner et al., , 2017) relative effects . Multivariate generalizations of this approach can be found in Puri and Sen, (1971), Munzel and Brunner, (2000) or Brunner et al., (2002); see also De Neve and Thas, (2015) for a related approach. Since these quantities depend on the sample sizes , however, they are no fixed model constants and changing the sample sizes might dramatically alter the results; see again Brunner et al., (2017) for an example in the univariate case. For this reason, Brunner and Puri, (2001) proposed a different nonparametric effect for univariate factorial designs, where denotes the unweighted mean of all distribution functions. The same approach has also been extended to other settings by Gao and Alvo, (2005), Gao and Alvo, (2008), Gao et al., (2008) and Umlauft et al., (2017). Nevertheless, none of them considered null hypotheses formulated in terms of fixed and meaningful model parameters. For a more intuitive interpretation of the results, however, it is sensible to formulate and test hypotheses in more vivid effect sizes. In particular, it is widely accepted in quantitative research that “effect sizes are the most important outcome of empirical studies” (Lakens, , 2013). Brunner et al., (2017) therefore infer null hypotheses stated in terms of the unweighted nonparametric effects via for a suitable hypothesis matrix H and the pooled vector p of the effects , see also Konietschke et al., (2012) for the special case of one group repeated measures.

In the present paper, we strive to generalize their models and methods in several directions:

-

1.

We examine generalizations to the more involved context of multivariate data where dependencies between observations from the same unit need to be taken into account. This multivariate case allows for testing hypotheses on the influence of several factors on single or several outcome measurements.

-

2.

More general as in Repeated Measures designs the outcomes in different components may be measured on different units (such as grams and meters). In particular, they actually need not even be elements of metric spaces; totally ordered sets serve equally well as spaces of outcomes because we develop rank-based methods for our analyses. Query scores are an example of such ordered data without having a unit in general. Differences will be tested with the help of a quadratic form in the rank-based effect estimates.

-

3.

This test statistic is analyzed by means of modern empirical process theory (instead of the more classical and sometimes cumbersome projection-based approaches for rank statistics). Since it is asymptotically non-pivotal, appropriate bootstrap methods for asymptotically reproducing its correct limit null distribution are proposed. As bootstrapping entails several good properties when applied to empirical distribution functions and our rank-based estimates offer a representation as a functional of multiple empirical distribution functions, we expect to obtain reliable inference methods using bootstrap techniques. This conjecture will be supported by simulation results which indicate a good control of the type-I error rate even for small sample set-ups with ordinal or heteroscedastic metric data.

Our model formulation thereby comprises novel procedures for general multivariate factorial designs with crossed or nested factors and even contains the so-called nonparametric multivariate Behrens-Fisher problem as a special case. Moreover, the methodology also allows for subsequent post-hoc tests.

The paper is organized as follows: In Section 2 we describe the statistical model and the null hypotheses of interest. Section 3 presents the asymptotic properties of our estimator and, subsequently, states the asymptotic validity of its bootstrap versions. Deduced statistical inference procedures are discussed in Section 4 and their small sample behavior is analyzed in extensive simulation studies in Section 5. Section 6 contains the real data analysis of the gender influence on education and annual household income of shopping mall customers in the San Francisco Bay Area. We conclude with some final remarks in Section 7. The proofs of all theoretic results and the derivation of the asymptotic covariance matrices are given in the Appendices A and B, respectively. Proof of all large sample properties of the classical bootstrap applied in the present framework, further simulation results regarding the power of all proposed methods, and additional analyses of the shopping mall customers data example are provided in Appendices C, D, and E, respectively.

2 Statistical Model

Throughout, let be a probability space on which all random variables will be defined. We assume a general factorial design with multivariate data, that is, we consider independent random vectors

| (1) |

of dimension , where denotes the -th measurement of individual in group . Thus, the total sample size is . The distribution of is assumed to be the same within each group with marginals denoted by

Throughout, we understand all as the so-called normalized distribution functions, i.e. the means of their left- and right-continuous versions (Ruymgaart, , 1980; Akritas et al., , 1997; Munzel, , 1999). This allows for a unified treatment of metric and ordinal data and will later on lead to statistics formulated in terms of mid-ranks. For convenience, we combine the observations in larger vectors

| (2) |

containing all the information of group and the pooled sample, respectively. Different to the special case of repeated measurements (Konietschke et al., , 2012; Brunner et al., , 2017) the components are in general not commensurate. Therefore, comparisons between the different groups are performed component-wise. To this end, let denote the unweighted mean distribution function for the -th component. We consider as a benchmark distribution for comparisons in the -th component. In particular, denote by a random variable that is independent of X and define unweighted nonparametric effects for group and component by

| (3) |

where quantifies the Mann-Whitney effect for groups and in component .

Note that in case of .

This definition naturally extends the univariate effect measure given in Brunner et al., (2017) to our general multivariate set-up.

Note that, in contrast to their suggestion for an extension to repeated measures designs,

comparisons with respect to the overall mean distribution are not appropriate here

since we study a more general model that allows for components measured on different units.

However, the advantages of an unweighted effect measure as discussed in Brunner et al., (2017) still apply:

The ’s in (3) are fixed model quantities that do not depend on the sample sizes ,

thus allowing for a transitive ordering.

Moreover, interpretation of these effects is rather simple: An effect smaller than 1/2 means that observations from the distribution (i.e.

from component in group ) tend to smaller values than those from the corresponding benchmark distribution .

In this set-up, we formulate null hypotheses as

where denotes the vector of the relative effects , and H is a suitable hypothesis matrix with columns. Instead of H we may equivalently use the unique projection matrix

which is idempotent and symmetric and fulfills ; see e.g., Brunner et al., (1997); Brunner and Puri, (2001) and Brunner et al., (2017).

Henceforth, let and denote the -dimensional unit matrix and the matrix of 1’s, respectively, and define by the so-called -dimensional centering matrix.

In particlar, in case of our approach includes the nonparametric multivariate Behrens-Fisher problem

with and , . Similarly, one-way layouts are covered by choosing , leading to the null hypothesis . Moreover, more complex factorial designs can be treated as well by splitting up the group index into sub-indices according to the number of factors considered. For example, consider a two-way layout with crossed factors and with levels and , respectively. In this case, the random vectors in (1) become . We thus obtain the effect vector , where all vectors are -variate and there are subjects observed at each factor level combination. Hypotheses of interest in this context are the hypotheses of no main effects as well as the hypothesis of no interaction effect between the factors. The hypothesis of no main effect of factor can be written as , where denotes the Kronecker product. Similarly, the hypothesis of no effect of factor is formulated as and the hypothesis of no interaction effect as . For other covered factorial designs and corresponding contrast matrices we refer to Section 4 in Konietschke et al., (2015). Equivalent formulations of the above null hypotheses in terms of the illustrative but notationally more elaborate decomposition into all factor influences are given in the Supplementary Material of Brunner et al., (2017) for the univariate case, but directly carry over to the present context. We note that in the general multivariate case, null hypotheses like have only been considered in the special case of the nonparametric Behrens-Fisher problem (Brunner et al., , 2002). Up to now, multivariate testing procedures for one-, two-, or even higher-way layouts focus on null hypotheses formulated in terms of distribution functions; see, e.g., Bathke et al., (2008), Harrar and Bathke, (2008), Harrar and Bathke, (2012) and the references given in Section 1.

To estimate the vector of effects, we consider the empirical (normalized) distribution functions where . Thus, we obtain estimators for the nonparametric effects by replacing the distribution functions with their empirical counterparts

where and

Here, denotes the (mid-)rank of observation in dimension among the observations in the pooled sample and are the corresponding rank means. We combine all estimated effect sizes into the -dimensional vector . To detect deviations from null hypotheses of the form we propose the application of the following ANOVA-type test statistic (ATS)

| (4) |

where again denotes the total sample size in the experiment.

3 Asymptotic Properties and Resampling Methods

In this section, we discuss asymptotic properties of the vector of estimated effect sizes and propose bootstrap methods to approximate its unknown limit distribution. For a lucid presentation of the results we thereby assume the following sample size condition:

Condition 1.

for all groups as .

In other words, no group shall constitute a vanishing fraction of the combined sample. Due to the Glivenko-Cantelli theorem in combination with the continuous mapping theorem, the consistency of for p follows already under the weaker assumption . Asymptotic normality is established in our main theorem below:

Theorem 1.

Note that this theorem immediately implies the asymptotic normality of under . Thus, the continuous mapping theorem yields the corresponding convergence in distribution for the quadratic form defined in (4):

Corollary 1.

Suppose Condition 1 holds. As , we have under

| (6) |

where are independent and standard normally distributed and are the eigenvalues of .

The limit theorem (5) raises the question how to calculate adequate critical values for tests in . A first naive idea might be to approximate the right hand side of (5) by using its representation as a weighted sum of independent -variables together with (consistent) estimators for the involved eigenvalues or the covariance matrix . However, these choices usually result in too liberal inference methods as already observed by Brunner et al., (2017) for the univariate case. Another idea would be to generalize the -approximation proposed in Brunner et al., (2017) to the present situation. But since this will in general not lead to asymptotic correct level tests (even in the most simple univariate two sample setting with and , see Brunner et al., 2017), we instead focus on resampling the test statistic . In particular, we study two bootstrap approaches for recovering the unknown limit distribution of under : A sample-specific as well as a wild bootstrap.

Here, a wild bootstrap approach is implemented in the following fashion: first, we notice that has an asymptotically linear representation in . Indeed, if we denote for functions such that the integral is well-defined, then

| (7) | ||||

The second equality follows from the functional delta-method applied to the integral functionals ; cf. Dobler and Pauly, (2017) for the two-sample case. In this asymptotic expansion, the now proposed wild bootstrap tries to estimate each involved residual by another centered quantity with approximately the same conditional variance given X:

where are i.i.d. zero-mean, unit variance random variables with . This condition is implied by for any , and it is thus a weak assumption on the heaviness of tails; cf. p. 177 in van der Vaart and Wellner, (1996). Note that, for each , our wild bootstrap implementation uses the same multiplier for every component in order to ensure an appropriate dependence structure.

Additionally, apart from estimating the residuals by , the unknown distribution functions in the integrators in (7) need to be estimated by their empirical counterparts. Denote by and the wild bootstrap versions of and , respectively. Finally, we obtain the following wild bootstrap counterpart of :

| (8) |

Combined into an -vector , we have the following conditional central limit theorems which hold under both the null hypothesis and the alternative hypothesis :

Theorem 2.

Corollary 2.

The corollary again follows from the continuous mapping theorem applied to Theorem 2. The conditional central limit theorem (10) is sufficient for providing random quantiles which converge in outer probability to the quantiles of the asymptotic distribution of the ATS under , i.e. : repeated realizations of are derived and their empirical quantiles serve as critical values for the hypothesis tests.

Similarly, instead of a wild bootstrap, a variant of the classical bootstrap (Efron, , 1979) may be applied to obtain a similar convergence result. The procedure is as follows: for each group , we randomly draw -dimensional data vectors from with replacement to obtain bootstrap samples . Denote their marginal empirical distribution functions as . Then, is the bootstrap counterpart of and the respective bootstrap versions and of and are derived analogously to the wild bootstrap. Conditional central limit theorems analogous to (9) and (10) hold too; see Appendix C for details. We compare the performances of both proposed resampling procedures, i.e. the wild bootstrap and the classical bootstrap, in Section 5 below.

4 Deduced Inference Procedures

The previous considerations directly imply that consistent and asymptotic level tests for are given by

where and denote the quantile of the classical bootstrap and wild bootstrap versions of given X, i.e. of in case of the wild bootstrap. Their finite sample performance will be studied in Section 5 below. As described in Section 2, these tests can be used to infer various global null hypotheses of interest about (nonparametric) main and interaction effects of interest which can straightforwardly be inverted to construct confidence regions for these nonparametric effects.

Moreover, the results derived in Section 3 also allow post-hoc analyses, i.e. subsequent multiple comparisons. To exemplify the typical paths of action we consider the one-way situation with independent groups and nonparametric effect size vectors in group . If the global null hypothesis

of equal effect size vectors is rejected, one is usually interested in inferring

-

(i)

the (univariate) endpoints that caused the rejection, as well as

-

(ii)

the groups showing significant differences (all pairs comparisons).

The above questions directly translate to testing the univariate hypotheses

| (11) |

in case of (i) and to an all pairs comparison given by multivariate hypotheses

| (12) |

in case of (ii). Note that our derived methodology allows for testing these hypotheses in a unified way by performing tests on all univariate endpoints for (11) and by selecting pairwise comparison contrast matrices for (12). Therefore, a first naive approach would be to adjust the individual tests accordingly (e.g. by Bonferroni or Holm corrections) to ensure control of the family-wise error rate. However, note that the effect size vectors are defined via component-wise comparisons. This implies that the intersection of all as well as the intersection of all is exactly given by the global null hypothesis . Moreover, we can even test all subset intersections of (or ) by choosing adequate contrast matrices and performing the corresponding bootstrap procedures. Thus, both questions can even be treated (separately) by applying the closed testing principle of Marcus et al., (1976). This is a major advantage over existing inference procedures that are developed for testing null hypotheses formulated in terms of distribution functions (Ellis et al., , 2017). In particular, since equality of marginals does not imply equality of multivariate distributions, the closed testing principle cannot be applied to the latter to answer question (i).

To ensure a reasonable computation time, the above approach is only applicable for small or moderate and . However, some computation time can be saved by formulating a hierarchy on the questions (either for study-specific reasons or by weighing up the sizes of and ). For example, assume that (i) is more important than (ii). In this case we may start by applying the closed testing algorithm to test hypotheses and subsequently only infer pair-wise comparisons on the significant univariate endpoints (instead of testing all multivariate ). Contrary, assume that is much larger than . Then it may be reasonable to first infer (ii) and subsequently consider (i) for the significant pairs.

5 Simulations

5.1 Continuous Data

For the one-way layout, data was generated similarly to the simulation study in Konietschke et al., (2015). We considered treatment groups and endpoints as well as the following covariance settings:

| Setting 1: | ||||

| Setting 2: |

Setting 1 represents a compound symmetry structure, while Setting 2 is an autoregressive covariance structure. Data was generated as

where denotes a square root of the matrix , i.e., . The i.i.d. random errors with mean and were generated by simulating independent standardized components for various distributions of . In particular, we simulated standard normal and standard lognormal distributed random variables. We investigated balanced as well as unbalanced designs with sample size vectors , , and , and increased sample sizes by adding to each element of the respective vector . In this setting, we tested the null hypothesis of no treatment effect , where , and . All simulations were conducted using the R-computing environment (R Core Team, , 2016), version 3.2.3, each with 5,000 simulation runs and 5,000 bootstrap iterations.

The results for the normal and lognormal distribution are displayed in Table 1. The wild bootstrap approach shows a very good type-I error control for normally distributed data and dimensions, even for sample sizes as small as . For the other scenarios considered, particularly for lognormal data, we need slightly larger sample sizes to achieve good type-I error control. An exception is the scenario with dimensions and covariance setting S2 with lognormal data, where the wild bootstrap approach maintains the pre-assigned level of 5% already for sample sizes as small as 10. However, sample sizes of about 40 are enough to ensure very good type-I error rates across all scenarios considered here. The classical, group-wise bootstrap, in contrast, leads to slightly larger type-I error rates as compared to the wild bootstrap and only maintains the 5% level for sample sizes of about 60.

| wild bootstrap | group-wise bootstrap | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|

| distr | Cov | 0 | 10 | 30 | 50 | 0 | 10 | 30 | 50 | ||

| normal | S1 | (10, 10) | 5.2 | 5.5 | 5.5 | 5.5 | 8 | 5.8 | 5.8 | 5.5 | |

| (10, 20) | 5.1 | 5.1 | 5.4 | 5.2 | 7.7 | 6.5 | 5.4 | 4.9 | |||

| (20, 10) | 5.5 | 5.3 | 4.9 | 5.3 | 7.1 | 6.4 | 5.2 | 5 | |||

| S2 | (10, 10) | 4.8 | 5.2 | 5.2 | 5.3 | 7.8 | 5.8 | 5.9 | 5.2 | ||

| (10, 20) | 5 | 4.9 | 5.6 | 4.9 | 7.7 | 6 | 5.7 | 5.1 | |||

| (20, 10) | 5 | 5.3 | 5 | 5.1 | 6.9 | 6.3 | 5.2 | 4.9 | |||

| lognormal | S1 | (10, 10) | 6 | 5.8 | 5.7 | 5.2 | 8.4 | 6.3 | 5.8 | 5.6 | |

| (10, 20) | 5.9 | 5.8 | 5.7 | 5.3 | 8.2 | 6.7 | 5.7 | 5.6 | |||

| (20, 10) | 6.5 | 6.2 | 5.3 | 5.5 | 7.9 | 6.2 | 5.8 | 5.3 | |||

| S2 | (10, 10) | 5.8 | 6 | 5.7 | 5.1 | 8.2 | 6.6 | 5.9 | 5.3 | ||

| (10, 20) | 5.5 | 5.7 | 5.5 | 5.3 | 8.2 | 6.4 | 5.6 | 5.2 | |||

| (20, 10) | 6.2 | 6.1 | 4.9 | 5.3 | 7.8 | 6.4 | 5.9 | 5.3 | |||

| normal | S1 | (10, 10) | 6 | 5.3 | 5.2 | 5.1 | 8.1 | 6.3 | 5.7 | 6.1 | |

| (10, 20) | 5.7 | 5.9 | 5.2 | 4.7 | 7.7 | 5.6 | 5.4 | 5.6 | |||

| (20, 10) | 5.9 | 5.3 | 4.8 | 4.8 | 7.5 | 5.7 | 5.8 | 5.7 | |||

| S2 | (10, 10) | 3.5 | 4.3 | 4.1 | 4.7 | 6.6 | 6.4 | 5.1 | 5.6 | ||

| (10, 20) | 3.7 | 4.9 | 5 | 4.4 | 7 | 5.7 | 5.5 | 5.2 | |||

| (20, 10) | 4.3 | 4.5 | 4.4 | 4.4 | 6.1 | 5.8 | 5.2 | 5.7 | |||

| lognormal | S1 | (10, 10) | 6.9 | 5.9 | 5.3 | 5.7 | 8.6 | 6.5 | 6 | 5.6 | |

| (10, 20) | 6.4 | 6.7 | 5.7 | 4.6 | 8.4 | 6 | 6 | 5.5 | |||

| (20, 10) | 6.5 | 6.2 | 5.1 | 4.7 | 8.3 | 6.1 | 5.9 | 5.4 | |||

| S2 | (10, 10) | 4.9 | 4.4 | 4.5 | 5.1 | 7.6 | 6.3 | 5.6 | 5.7 | ||

| (10, 20) | 5.1 | 5.2 | 4.8 | 4.7 | 7.7 | 6.3 | 6 | 5.6 | |||

| (20, 10) | 4.7 | 5 | 4.9 | 4.4 | 7.3 | 6.1 | 5.5 | 5.7 | |||

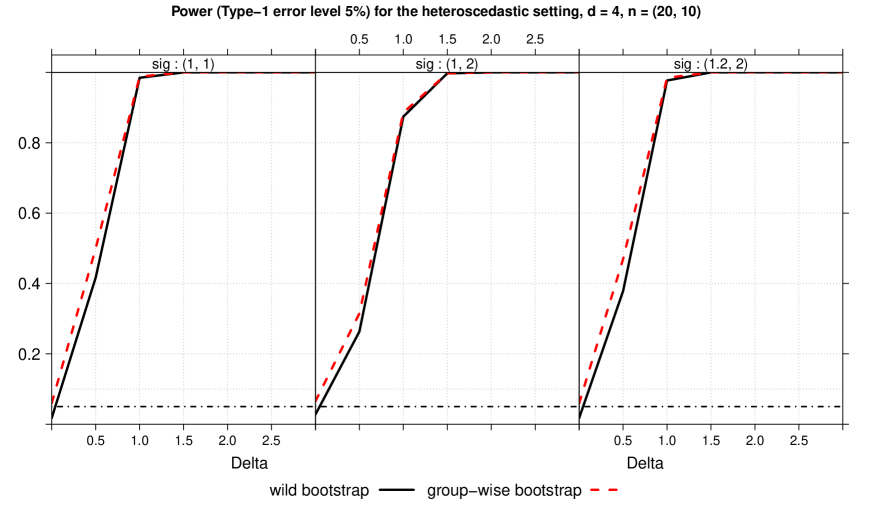

5.1.1 A heteroscedastic setting

We simulated a heteroscedastic setting, where is satisfied. To this end, we took

for different choices of as well as sample sizes . Sample sizes were again increased as described above. The results are displayed in Table 2. In this case, we observe a rather conservative behavior across all scenarios, which improves with growing sample sizes, but is still slightly conservative in case of dimensions, even for sample sizes of 60 and 70. In this heteroscedastic setting, the classical, group-specific bootstrap yields better results in many scenarios, especially for growing dimension. We note that this was the only studied setting where the group-specific bootstrap was better than the wild. Apart from this exception, it was the other way around.

| wild bootstrap | group-wise bootstrap | |||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| 0 | 10 | 30 | 50 | 0 | 10 | 30 | 50 | |||

| (1, 2) | (10, 10) | 1.3 | 2.4 | 3.5 | 4.4 | 6.2 | 5.2 | 5.3 | 5.6 | |

| (10, 20) | 1.4 | 2.5 | 3.5 | 3.6 | 5.6 | 5.8 | 5.2 | 4.9 | ||

| (20, 10) | 2.2 | 3.9 | 3.9 | 4.5 | 6.6 | 6.1 | 6 | 5.2 | ||

| (1, 1) | (10, 10) | 0.9 | 2.2 | 3.2 | 4.3 | 6.1 | 5.4 | 5.2 | 5.1 | |

| (10, 20) | 1.8 | 2.9 | 3.8 | 3.9 | 5.9 | 5.4 | 5.1 | 5.1 | ||

| (20, 10) | 1.4 | 3.1 | 3.5 | 4 | 6 | 5.5 | 5.6 | 5.1 | ||

| (1.2, 1) | (10, 10) | 1 | 2.3 | 3.2 | 4.2 | 6.1 | 5.3 | 5.4 | 4.9 | |

| (10, 20) | 1.9 | 3.1 | 4 | 4 | 6.1 | 5.6 | 5.1 | 5 | ||

| (20, 10) | 1.2 | 2.9 | 3.6 | 4 | 6 | 5.4 | 5.4 | 5.1 | ||

| (1, 2) | (10, 10) | 0.3 | 1.5 | 2.8 | 3.7 | 4.7 | 4.7 | 4.6 | 4.8 | |

| (10, 20) | 0.3 | 1.7 | 3 | 3.7 | 4.2 | 4.8 | 4.9 | 5.2 | ||

| (20, 10) | 1.3 | 2.8 | 4 | 4.4 | 4.4 | 4.9 | 4.8 | 4.8 | ||

| (1, 1) | (10, 10) | 0.3 | 1.6 | 2.6 | 3.6 | 5 | 4.9 | 4.6 | 5.2 | |

| (10, 20) | 0.6 | 2.1 | 3.2 | 3.6 | 4.7 | 4.5 | 4.8 | 5.1 | ||

| (20, 10) | 0.9 | 2.1 | 3.4 | 3.7 | 4.4 | 4.6 | 4.5 | 5 | ||

| (1.2, 1) | (10, 10) | 0.2 | 1.5 | 2.8 | 3.5 | 4.8 | 4.9 | 4.8 | 5.3 | |

| (10, 20) | 0.8 | 2.2 | 3.3 | 3.8 | 4.8 | 4.3 | 4.7 | 5.1 | ||

| (20, 10) | 0.8 | 2.1 | 3.3 | 3.6 | 4.4 | 4.6 | 4.5 | 4.9 | ||

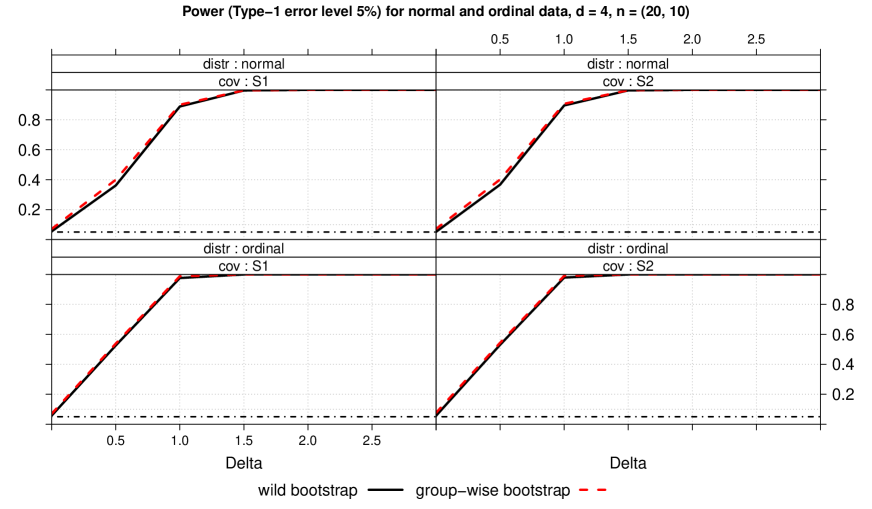

5.2 Ordinal Data

We simulated ordinal data using the function ordsample from the R package GenOrd (Barbiero and Ferrari, , 2015; Ferrari and Barbiero, , 2012). The package GenOrd allows for simulation of discrete random variables with a given correlation structure and given marginal distributions. The latter are linked together via a Gaussian copula in order to achieve the desired correlation structure on the discrete components. We simulated uniform marginal distributions, such that the outcomes in the -th dimension are uniformly distributed on categories, . For the correlation structure, we used the same underlying covariance matrices as in the continuous setting above. Again, we considered dimensions and the same sample sizes as above. The results are displayed in Table 3, showing a rather good type-I error control in the settings considered. The results here are similar to the ones obtained above for continuous data, with slightly larger type-I errors for the small sample scenarios. In this scenario, the group-wise bootstrap again shows a rather liberal behavior for small sample sizes. Although the behavior improves with growing sample size, the wild bootstrap is again superior here.

| wild bootstrap | group-wise bootstrap | |||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| Cov. setting | 0 | 10 | 30 | 50 | 0 | 10 | 30 | 50 | ||

| S1 | (10, 10) | 6.9 | 5.2 | 5.1 | 5.3 | 8.1 | 6.5 | 6.0 | 5.8 | |

| (10, 20) | 6.5 | 5.7 | 4.9 | 5.3 | 8.1 | 6.6 | 5.5 | 5.5 | ||

| (20, 10) | 6.4 | 5.5 | 6.1 | 5.3 | 8.4 | 6.7 | 5.6 | 5.3 | ||

| S2 | (10, 10) | 6.3 | 4.7 | 5.2 | 5.4 | 8.2 | 6.1 | 6.1 | 5.3 | |

| (10, 20) | 5.9 | 5.7 | 5.0 | 5.3 | 7.8 | 6.9 | 5.7 | 5.3 | ||

| (20, 10) | 6.3 | 5.3 | 5.8 | 5.6 | 8.1 | 6.8 | 5.5 | 5.5 | ||

| S1 | (10, 10) | 6.4 | 5.8 | 5.1 | 4.8 | 8.7 | 6.7 | 5.9 | 5.6 | |

| (10, 20) | 6.4 | 5.7 | 5.5 | 5.6 | 7.5 | 7.0 | 6.2 | 6.0 | ||

| (20, 10) | 6.4 | 5.5 | 5.2 | 5.0 | 8.0 | 6.5 | 5.3 | 6.0 | ||

| S2 | (10, 10) | 4.3 | 4.6 | 4.5 | 4.3 | 8.0 | 6.3 | 5.7 | 5.4 | |

| (10, 20) | 4.5 | 4.8 | 4.7 | 4.8 | 6.8 | 6.5 | 6.0 | 5.6 | ||

| (20, 10) | 4.5 | 4.5 | 4.7 | 4.8 | 7.4 | 6.3 | 5.9 | 5.9 | ||

In addition to type-I error rates, we have also compared the two bootstrap approaches with respect to their power behavior. The results can be found in Appendix D.

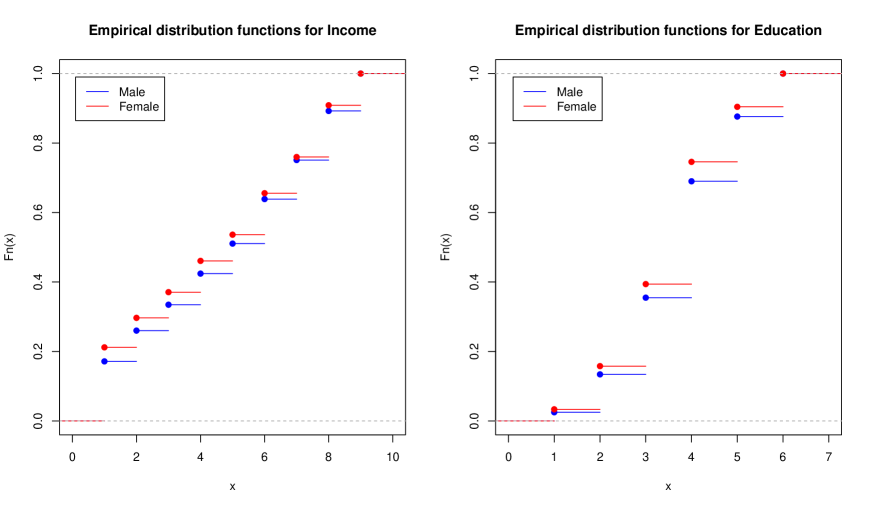

6 Data Example

As a data example, we consider the data set ‘marketing’ in the R-package ElemStatLearn (Halvorsen, , 2015). This data set contains information on the annual household income along with 13 other demographic factors of shopping mall customers in the San Francisco Bay Area. Most of the variables in this data set are measured on an ordinal scale, rendering mean-based approaches unfeasible. For our example, we consider the influence of sex on annual household income and educational status. The annual household income is categorized in 9 categories ranging from ‘less than $10,000’ to ‘$75,000 and more’, while education ranges from ‘Grade 8 or less’ to ‘Grad Study’ (6 categories). This two-dimensional outcome is to be analyzed with respect to the influence factor sex (Male vs. Female) .

The original data set consists of 8993 observations. After removing those observations with missing values in one of the variables considered here, 8907 observations remain (4041 male and 4866 female participants).

The estimated unweighted treatment effects are displayed in Table 4, while Figure 1 shows the empirical distribution functions for the two dimensions for male and female participants, respectively. The effects can be interpreted in the following way: For both income and education, male participants tend to have higher values than female participants, i.e., males tend to have higher annual incomes and a higher level of education than females.

A statistical analysis of the data example based on our wild bootstrap approach reveals a highly significant effects (-value ) of sex on the two-dimensional outcome data, i.e., household income and educational status differ significantly between male and female participants.

As a sensitivity analysis, we imputed the missing values using the R package missForest (Stekhoven, , 2013; Stekhoven and Buehlmann, , 2012). Performing the analysis as above with the imputed data leads to the same results.

| Sex | Income | Education |

|---|---|---|

| Male | 0.511 | 0.517 |

| Female | 0.489 | 0.483 |

7 Conclusions and Discussion

We have considered an extension of the unweighted treatment effects recently proposed by Brunner et al., (2017) to multivariate data. These effects do not depend on the sample sizes and allow for transitive ordering. We have rigorously proven the asymptotic behavior of the vector of unweighted treatment effects and proposed two bootstrap approaches to derive data-driven critical values for global and multiple test decisions. We proved the asymptotic validity of the bootstrap using empirical process arguments and analyzed its behavior in a large simulation study, where we considered continuous and ordinal distributions with different covariance settings and sample sizes. The wild bootstrap method performed very well in most scenarios for small to moderate sample sizes. Only in heteroscedastic settings, it turned out to be rather conservative for small sample sizes. In this scenario, the sample-specific bootstrap provided better results.

In order to make them easily available for users, the proposed methods have been implemented by Sarah Friedrich in an R package rankMANOVA, which is available from GitHub (https://github.com/smn74/rankMANOVA).

In future work we will consider extensions of the present set-up to censored multivariate data as well as address the question “Which resampling method remains valid and performs preferably?”. Here, a challenge will be the correct treatment of ties: The wild bootstrap ceases to reproduce the correct limit distribution in case of right-censored and tied data if it is not adjusted accordingly (Dobler, , 2017). On the other hand, Akritas, (1986) has verified that Efron’s bootstrap for right-censored data (Efron, , 1981) still works in the presence of ties. The planned future paper may also be considered an extension of the article by Dobler and Pauly, (2017) to the multi-sample and multivariate case.

Acknowledgment

This work was supported by the German Research Foundation.

Appendix A Proofs

Throughout, let be the empirical processes based on the samples , respectively, which are indexed by the class of functions , where

and is the class of all canonical coordinate projections . Using this indexation, it is easily possible to derive the normalized empirical distribution functions from . We also see that every group-specific empirical process can be considered as an element of which contains all bounded sequences with indices in .

Proof of Theorem 1.

Clearly, can be written as the image of all group- and component-specific, normalized empirical distribution functions

, , , under a Hadamard-differentiable mapping .

This can be seen following the lines in the proof of Theorem 2.1 in Dobler and Pauly, (2017)

where the case is discussed; in their proof, needs to be chosen.

Hence, asymptotic normality follows from an application of the functional delta-method; cf. Theorem 3.9.4 in van der Vaart and Wellner, (1996).

The asymptotic covariance structure of the resulting multivariate normal distribution is derived in detail in Appendix B, where the asymptotic linear expansion of in all empirical distribution functions is utilized.

Proof of Theorem 2.

First note that, given X, we have conditional convergence in distribution of to a multivariate Brownian bridge process in outer probability: this follows from an application of the conditional Donsker Theorem 3.6.13 in van der Vaart and Wellner, (1996) in combination with Example 3.6.12 dedicated to the wild bootstrap and the choice of the Vapnik-C̆ervonenkis subgraph class concatenated with the class of all canonical coordinate projections . This conserves the Vapnik-C̆ervonenkis subgraph property as argued in Lemmata 2.6.17(iii) and 2.6.18(vii) of van der Vaart and Wellner, (1996).

Next, recall the asymptotic linear representation (7) of which followed from the functional delta-method and which motivated the wild bootstrap version (8). This presentation involves Hadamard-derivatives that depend on estimated quantities:

Here each is a distribution on , which may hence be considered as an element of , with marginal normalized distribution functions .

We apply the extended continuous mapping theorem (Theorem 1.11.1 in van der Vaart and Wellner, , 1996) to the (random) functional . The extended continuous mapping theorem is applied for almost every realization of X thanks to the subsequence principle (Lemma 1.9.2 in van der Vaart and Wellner, , 1996): convergence in outer probability is equivalent to outer almost sure convergence along subsequences. The actual requirement for an application of the extended continuous mapping theorem is satisfied as well: note that basically consists of integral mappings of the form

where is the space of right- (or left-)continuous functions on with existing left- (or right-)sided limits

and is the subspace of functions with total variation bounded by 1.

Lemma 3.9.17 in van der Vaart and Wellner, (1996) states that is Hadamard-differentiable, hence continuous.

We conclude that for all sequences of functions and , which converge to in and to in , respectively, the sequence of functionals satisfies as .

All in all, the extended continuous mapping theorem, combined with the conditional central limit theorem for the wild bootstrapped empirical distribution functions as stated at the beginning of this proof,

concludes the proof of the conditional convergence in distribution of .

Appendix B Covariances

In this appendix we derive the covariance matrix of the multivariate limit normal distribution in Theorem 1. The exact representation may not be strictly necessary for the practical purposes in this paper because a covariance estimator is not required due to the wild bootstrap asymptotics as described in Theorem 2. But the covariances below will give some insights into the asymptotically independent components of and what kind of studentization may be applied if one wishes to test sub-hypotheses. Furthermore, it is important to see that the limit distribution is not degenerate. Therefore, let be the vector consisting of all

This estimator is consistent for the vector, say, w consisting of the different . As an intermediate result, we are interested in the asymptotic covariance matrix of the vector, i.e. in the limits of

To this end, we consider an asymptotically linear development which is due to the functional delta-method: Let again denote the Wilcoxon functional; cf. Section 3.9.4.1 in van der Vaart and Wellner, (1996). As and , (according to Condition 1),

Thus, we know that is the limit of

where is Kronecker’s delta.

We continue by calculating any of the above covariances, but we need to distinguish between two cases:

Equal coordinates :

Unequal coordinates : Denote by the joint normalized distribution function of and .

Recall that . To sum up, we have the following asymptotic covariances (symmetric cases not listed):

In order to present the above covariances in a more compact matrix notation, we introduce the following matrices: Denote by the -matrix of zeros, by the -dimensional column vector of zeros, by the -diagonal matrices of ’s, by

the -matrices of ’s with zeros along the diagonal entries, and the vector of treatment effects between groups and by . Recall that, in the whole -vector, we first first the -value, then the -value, so that we first go through the component index . With the above notation, we thus obtain the following first block of the covariance matrix in which which, for general indices and , we denote by :

Note that the other -matrices have a similar structure but with the -matrices in the th block row and block column and with all ’s replaced by ’s. In the same way,

The representation of the general block matrix with is similarly obtained, where the zero-rows have to shifted to the row block number and the zero-column to the column block number . Furthermore, the repeating ’s and ’s in the above representation need to be replaced with ’s and ’s, respectively.

Since each is the mean of , we conclude that the limit covariance matrix of is given by

Appendix C Theory for the classical, group-wise bootstrap

In this section, we present the results of the classical, group-wise bootstrap as a competitor of the wild bootstrap. The bootstrap is implemented in the following fashion: For each group , we draw independent selections randomly with replacement from the vectors . These are used to build the bootstrapped empirical distribution functions as described in Section 2, i.e., . The bootstrapped treatment effects are then obtained via

The asymptotics of Theorem 1 and Corollary 1 for these bootstrapped treatment effects hold under both the null hypothesis and the alternative hypothesis which is shown by using similar arguments as in the proofs for the wild bootstrap:

Theorem 3.

The continuous mapping theorem immediately implies the corresponding conditional convergence in distribution for the bootstrapped ATS:

Corollary 3.

Proof of Theorem 3.

Similarly, as argued in the proof of Theorem 1, is obtained as a Hadamard-differentiable functional of all bootstrapped (normalized) empirical distribution functions , , . As the conditional central limit theorem holds in outer probability for each bootstrapped empirical distribution function, i.e. for each

cf. Theorem 3.6.1 in van der Vaart and Wellner, (1996),

the convergence is transferred to by means of the functional delta-method for the bootstrap; cf. Theorem 3.9.11 in van der Vaart and Wellner, (1996).

Note that the pooled bootstrap, corresponding to drawing with replacement from the combined sample, is not available in this context: this method involves asymptotic eigenvalues other than those in Corollary 2. Hence, the limiting distribution of the pooled bootstrapped ATS would only be correct in special cases.

Appendix D Additional simulation results: Power

In order to in compare the power behavior of the two bootstrap methods, we have considered a shift alternative, i.e., we simulated data as

where and for and corresponds to the respective random vectors simulated in Section 5 of the paper. The simulation results for some scenarios are exemplarily shown in Figures 2 and 3. We find that the power results for both bootstrap approaches are almost identical in the chosen situations.

Appendix E Additional analyses of the data example

In order to demonstrate the proposed methods in a more complex context, we consider another analysis of the ’marketing’ data example. Additionally to the variables described in Section 6 we now also include the factor ’language’, which describes the language spoken most often at home with the three levels ’English’, ’Spanish’ and ’Other’. After removing the observations with missing values in these variables, 8423 observations remain. We thus want to conduct some exploratory analyses of the two-dimensional outcome in a two-way layout with factors ’sex’ and ’language’. The estimated nonparametric effects are displayed in Table 5 and the wild bootstrap approach results in highly significant -values for the two main as well as the interaction effect, see Table 6.

Since the interaction hypothesis is significant, we continue by analyzing male and female participants separately. In order to further interpret the results, we also apply the post hoc comparisons described in Section 4. In particular, since the global null hypothesis is significant in both groups, we continue with the pairwise comparisons of the languages. Since again all results are significant at 5 % level, we finally consider the univariate outcomes. The results are displayed in Table 7. This reveals some interesting aspects of the data. For example, the significant difference between ‘English’ and ‘Other’ in the male group is driven by education, while there is no significant effect on the income. A similar result is obtained for ‘Spanish’ vs. ‘Other’ in the female group.

| Sex | Language | Income | Education |

|---|---|---|---|

| Male | English | 0.586 | 0.605 |

| Spanish | 0.560 | 0.568 | |

| Other | 0.464 | 0.407 | |

| Female | English | 0.401 | 0.367 |

| Spanish | 0.529 | 0.554 | |

| Other | 0.460 | 0.499 |

| Effect | -value | ||

|---|---|---|---|

| multivariate | Income | Education | |

| Sex | |||

| Language | |||

| Sex:Language | |||

| Sex | Language | -value | ||

|---|---|---|---|---|

| multivariate | Income | Education | ||

| Male | global null hypothesis | |||

| English vs. Spanish | ||||

| English vs. Other | 0.028 | 0.067 | 0.029 | |

| Spanish vs. Other | 0.042 | |||

| Female | global null hypothesis | |||

| English vs. Spanish | ||||

| English vs. Other | 0.018 | |||

| Spanish vs. Other | 0.069 | |||

All these analyses can be conducted with the R package rankMANOVA by splitting the data accordingly. The implementation of a routine for these calculations is part of future research.

References

- Acion et al., (2006) Acion, L., Peterson, J. J., Temple, S., and Arndt, S. (2006). Probabilistic index: An intuitive non-parametric approach to measuring the size of treatment effects. Statistics in Medicine, 25(4):591–602.

- Akritas, (1986) Akritas, M. G. (1986). Bootstrapping the Kaplan–Meier Estimator. Journal of the American Statistical Association, 81(396):1032–1038.

- Akritas et al., (1997) Akritas, M. G., Arnold, S. F., and Brunner, E. (1997). Nonparametric hypotheses and rank statistics for unbalanced factorial designs. Journal of the American Statistical Association, 92(437):258–265.

- Barbiero and Ferrari, (2015) Barbiero, A. and Ferrari, P. A. (2015). GenOrd: Simulation of Discrete Random Variables with Given Correlation Matrix and Marginal Distributions. R package version 1.4.0.

- Bathke et al., (2008) Bathke, A. C., Harrar, S. W., and Madden, L. V. (2008). How to compare small multivariate samples using nonparametric tests. Computational Statistics & Data Analysis, 52(11):4951–4965.

- Brown and Hettmansperger, (2002) Brown, B. M. and Hettmansperger, T. P. (2002). Kruskal–Wallis, multiple comparisons and Efron dice. Australian & New Zealand Journal of Statistics, 44(4):427–438.

- Brumback et al., (2006) Brumback, L. C., Pepe, M. S., and Alonzo, T. A. (2006). Using the ROC curve for gauging treatment effect in clinical trials. Statistics in Medicine, 25(4):575–590.

- Brunner et al., (1997) Brunner, E., Dette, H., and Munk, A. (1997). Box-type approximations in nonparametric factorial designs. Journal of the American Statistical Association, 92(440):1494–1502.

- Brunner et al., (2017) Brunner, E., Konietschke, F., Pauly, M., and Puri, M. L. (2017). Rank-based procedures in factorial designs: hypotheses about non-parametric treatment effects. Journal of the Royal Statistical Society: Series B (Statistical Methodology), 79(5):1463–1485.

- Brunner et al., (2002) Brunner, E., Munzel, U., and Puri, M. L. (2002). The multivariate nonparametric Behrens–Fisher problem. Journal of Statistical Planning and Inference, 108(1):37–53.

- Brunner and Puri, (2001) Brunner, E. and Puri, M. L. (2001). Nonparametric methods in factorial designs. Statistical papers, 42(1):1–52.

- De Neve and Thas, (2015) De Neve, J. and Thas, O. (2015). A regression framework for rank tests based on the probabilistic index model. Journal of the American Statistical Association, 110(511):1276–1283.

- Dobler, (2017) Dobler, D. (2017). A Discontinuity Adjustment for Subdistribution Function Confidence Bands Applied to Right-Censored Competing Risks Data. Electronic Journal of Statistics, 11(2):3673–3702.

- Dobler and Pauly, (2017) Dobler, D. and Pauly, M. (2017). Inference for the Mann-Whitney Effect for Right-Censored and Tied Data. TEST. To appear.

- Efron, (1979) Efron, B. (1979). Bootstrap methods: another look at the jackknife. The Annals of Statistics, 7(1):1–26.

- Efron, (1981) Efron, B. (1981). Censored Data and the Bootstrap. Journal of the American Statistical Association, 76(374):312–319.

- Ellis et al., (2017) Ellis, A. R., Burchett, W. W., Harrar, S. W., and Bathke, A. C. (2017). Nonparametric inference for multivariate data: the r package npmv. Journal of Statistical Software, 76(4):1–18.

- Ferrari and Barbiero, (2012) Ferrari, P. A. and Barbiero, A. (2012). Simulating ordinal data. Multivariate Behavioral Research, 47(4):566–589.

- Gao and Alvo, (2005) Gao, X. and Alvo, M. (2005). A unified nonparametric approach for unbalanced factorial designs. Journal of the American Statistical Association, 100(471):926–941.

- Gao and Alvo, (2008) Gao, X. and Alvo, M. (2008). Nonparametric multiple comparison procedures for unbalanced two-way layouts. Journal of Statistical Planning and Inference, 138(12):3674–3686.

- Gao et al., (2008) Gao, X., Alvo, M., Chen, J., and Li, G. (2008). Nonparametric multiple comparison procedures for unbalanced one-way factorial designs. Journal of Statistical Planning and Inference, 138(8):2574–2591.

- Halvorsen, (2015) Halvorsen, K. B. (2015). ElemStatLearn: Data Sets, Functions and Examples from the Book: ”The Elements of Statistical Learning, Data Mining, Inference, and Prediction” by Trevor Hastie, Robert Tibshirani and Jerome Friedman. R package version 2015.6.26.

- Harrar and Bathke, (2008) Harrar, S. W. and Bathke, A. C. (2008). Nonparametric methods for unbalanced multivariate data and many factor levels. Journal of Multivariate Analysis, 99(8):1635–1664.

- Harrar and Bathke, (2012) Harrar, S. W. and Bathke, A. C. (2012). A modified two-factor multivariate analysis of variance: asymptotics and small sample approximations (and erratum). Annals of the Institute of Statistical Mathematics, 64(1):135–165.

- Kieser et al., (2013) Kieser, M., Friede, T., and Gondan, M. (2013). Assessment of statistical significance and clinical relevance. Statistics in Medicine, 32(10):1707–1719.

- Konietschke et al., (2015) Konietschke, F., Bathke, A. C., Harrar, S. W., and Pauly, M. (2015). Parametric and nonparametric bootstrap methods for general MANOVA. Journal of Multivariate Analysis, 140:291–301.

- Konietschke et al., (2012) Konietschke, F., Hothorn, L. A., and Brunner, E. (2012). Rank-based multiple test procedures and simultaneous confidence intervals. Electronic Journal of Statistics, 6:738–759.

- Kruskal, (1952) Kruskal, W. H. (1952). A nonparametric test for the several sample problem. The Annals of Mathematical Statistics, 23(4):525–540.

- Kruskal and Wallis, (1952) Kruskal, W. H. and Wallis, W. A. (1952). Use of ranks in one-criterion variance analysis. Journal of the American Statistical Association, 47(260):583–621.

- Lakens, (2013) Lakens, D. (2013). Calculating and reporting effect sizes to facilitate cumulative science: a practical primer for t-tests and anovas. Frontiers in Psychology, 4.

- Mann and Whitney, (1947) Mann, H. B. and Whitney, D. R. (1947). On a test of whether one of two random variables is stochastically larger than the other. The Annals of Mathematical Statistics, 18(1):50–60.

- Marcus et al., (1976) Marcus, R., Eric, P., and Gabriel, K. R. (1976). On closed testing procedures with special reference to ordered analysis of variance. Biometrika, 63(3):655–660.

- Munzel, (1999) Munzel, U. (1999). Linear rank score statistics when ties are present. Statistics & Probability Letters, 41(4):389–395.

- Munzel and Brunner, (2000) Munzel, U. and Brunner, E. (2000). Nonparametric methods in multivariate factorial designs. Journal of Statistical Planning and Inference, 88(1):117–132.

- Puri and Sen, (1971) Puri, M. L. and Sen, P. K. (1971). Nonparametric methods in multivariate analysis. Technical report.

- R Core Team, (2016) R Core Team (2016). R: A Language and Environment for Statistical Computing. R Foundation for Statistical Computing, Vienna, Austria.

- Rust and Filgner, (1984) Rust, S. W. and Filgner, M. A. (1984). A modification of the Kruskal-Wallis statistic for the generalized Behrens-Fisher problem. Communications in Statistics-Theory and Methods, 13(16):2013–2027.

- Ruymgaart, (1980) Ruymgaart, F. H. (1980). A unified approach to the asymptotic distribution theory of certain midrank statistics. In Statistique non Parametrique Asymptotique, pages 1–18. Springer.

- Stekhoven, (2013) Stekhoven, D. J. (2013). missForest: Nonparametric Missing Value Imputation using Random Forest. R package version 1.4.

- Stekhoven and Buehlmann, (2012) Stekhoven, D. J. and Buehlmann, P. (2012). Missforest - non-parametric missing value imputation for mixed-type data. Bioinformatics, 28(1):112–118.

- Thangavelu and Brunner, (2007) Thangavelu, K. and Brunner, E. (2007). Wilcoxon-Mann-Whitney test for stratified samples and Efron’s paradox dice. Journal of Statistical Planning and Inference, 137(3):720 – 737. Special Issue on Nonparametric Statistics and Related Topics: In honor of M.L. Puri.

- Thas et al., (2012) Thas, O., De Neve, J., Clement, L., and Ottoy, J.-P. (2012). Probabilistic index models. Journal of the Royal Statistical Society: Series B (Statistical Methodology), 74(4):623–671.

- Umlauft et al., (2017) Umlauft, M., Konietschke, F., and Pauly, M. (2017). Rank-based permutation approaches for nonparametric factorial designs. British Journal of Mathematical and Statistical Psychology, 70:368–390.

- van der Vaart and Wellner, (1996) van der Vaart, A. W. and Wellner, J. A. (1996). Weak Convergence and Empirical Processes. Springer, New York.