Convergence Rates of Variational Posterior Distributions

Abstract

We study convergence rates of variational posterior distributions for nonparametric and high-dimensional inference. We formulate general conditions on prior, likelihood, and variational class that characterize the convergence rates. Under similar “prior mass and testing” conditions considered in the literature, the rate is found to be the sum of two terms. The first term stands for the convergence rate of the true posterior distribution, and the second term is contributed by the variational approximation error. For a class of priors that admit the structure of a mixture of product measures, we propose a novel prior mass condition, under which the variational approximation error of the mean-field class is dominated by convergence rate of the true posterior. We demonstrate the applicability of our general results for various models, prior distributions and variational classes by deriving convergence rates of the corresponding variational posteriors.

Keywords. posterior contraction, mean-field variational inference, density estimation, Gaussian sequence model, piecewise constant model, empirical Bayes

1 Introduction

Variational Bayes inference is a popular technique to approximate difficult-to-compute probability posterior distributions. Given a posterior distribution , and a variational family , variational Bayes inference seeks a that best approximates under the Kullback-Leibler divergence. Though it is not exact Bayes inference, the variational class often gives computational advantage and leads to algorithms such as coordinate ascent that can be efficiently implemented on large-scale data sets. Researchers in many fields have used variational Bayes inference to solve real problems. Successful examples include statistical genetics [8, 31], natural language processing [6, 23], computer vision [36], and network analysis [4, 43], to name a few. We refer the readers to an excellent recent review [7] on this topic.

The goal of this paper is to study the variational posterior distribution from a theoretic perspective. We propose general conditions on the prior, the likelihood and the variational class to characterize the convergence rate of the variational posterior to the true data generating process.

Before discussing our results, we give a brief review on the theory of convergence rates of the posterior distributions in the literature. In order that the posterior distribution concentrates around the true parameter with some rate, the “prior mass and testing” framework requires three conditions on the prior and the likelihood: a) The prior is required to put a minimal amount of mass in a neighborhood of the true parameter; b) Restricted to a subset of the parameter space, there exists a testing function that can distinguish the truth from the complement of its neighborhood; c) The prior is essentially supported on the subset described above. Rigorous statements of these three conditions can be found in seminal papers [19, 35, 18]. Earlier versions of these conditions go back to [34, 24, 3, 2]. We also mention another line of work [44, 40, 10, 20] that established posterior rates of convergence using other approaches.

In this paper, we show that under almost the same three conditions, the variational posterior also converges to the true parameter, and the rate of convergence is given by

| (1) |

The first term is the rate of convergence of the posterior distribution . The second term is the variational approximation error with respect to the class under the data generating process . Since we are able to generalize the “prior mass and testing” theory with the same old conditions, many well-studied problems in the literature can now be revisited under our framework of variational Bayes inference with very similar proof techniques. This will be illustrated with several examples considered in the paper.

Remarkably, for a special class of prior distributions and a corresponding variational class, the second term of (1) will be automatically dominated by under a modified “prior mass” condition. We illustrate this result by a prior distribution of product measure

and a mean-field variational class

As long as there exists a subset , such that the prior mass condition

| (2) |

holds together with the testing conditions, then the variational posterior distribution converges to the true parameter with the rate . In other words, the variational approximation error term in (1) is dominated under this stronger prior mass condition (2). This is the result of Theorem 2.4. Here, stands for a Rényi divergence with some . The implication of the condition (2) is important. It says that as long as the prior satisfies a “prior mass” condition that is coherent with the structure of the variational class, the resulted variational approximation error will always be small compared with the statistical error from the true posterior. Therefore, the condition (2) offers a practical guidance on how to choose a good prior for variational Bayes inference. In addition, as a condition only on the prior mass, (2) is usually very easy to check. This mathematical simplicity is not just for independent priors and the mean-field class. In Section 4, a more general condition is proposed that includes the setting of (2) as a special case.

Besides the general formulation of conditions to ensure convergence of the variational posteriors, several interesting aspects of variational Bayes inference are also discussed in the paper. We show that for a general likelihood with a sieve prior, its mean-field variational approximation of the posterior distribution has an interesting relation to an empirical Bayes procedure. We also show that the empirical Bayes procedure is exactly a variational Bayes procedure using a specially designed variational class. This connection between empirical Bayes and variational Bayes is interesting, and may suggest similar theoretical properties of the two.

Finally, we would like to remark that the general rate (1) for variational posteriors is only an upper bound. It is not always true that the variational posterior has a slower convergence rate than the true posterior. Sometimes the variational posterior may not be a good approximation to the true posterior, but it can still contract faster to the true parameter if additional regularity is imposed by the variational class . We construct examples in Section 5.2 to illustrate this point.

Related Work

Statistical properties of variational posterior distributions have also been studied in the literature. A recent work by [41] established Bernstein-von Mises type of results for parametric models. We refer the readers to [7, 41] for other related references on theories for parametric variational Bayes inference. For nonparametric and high-dimensional models, recent work by [1, 42] studied variational approximation to tempered posteriors, where the likelihood is replaced by for some . Just as the convergence of tempered posteriors [39], the convergence of the variational approximation can also be established under generalizations of the prior mass condition. In addition, the paper [1] also studied convergence rates under model misspecification, and the paper [42] considered a more general setting that can handle latent variables, which is quite useful to analyze mixture models. We would like to point out that these results do not apply to the usual posterior distributions with . After the first version of our paper was posted, similar results on have also been obtained independently by [29]111Some extensions of the results of [29] were later added in the revised version of [42] by the same authors.. An early related work on this topic is by [44], where the results cover both posterior distributions and their variational approximations. However, the conditions in [44] are rather abstract and are not easy to check in applications.

Organization

The rest of the paper is organized as follows. In Section 2, we formulate the problem and introduce the general conditions that characterize convergence rates of variational posteriors. This section also includes results for the mean-field variational class, where the variational approximation error can be explicitly analyzed. In Section 3, we apply our general theory to three examples that use three different variational classes. Then, in Section 4, for a general class of prior distributions and a mean-field class under a model selection setting, we propose a new prior mass condition that leads to an automatic control of the variational approximation error. In Section 5, we discuss the relation between variational Bayes and empirical Bayes. We also discuss possible situations where the variational posterior outperforms the true posterior in this section. An extension of the main results under model misspecification is also discussed in Section 5. All the proofs will be given in the Appendix.

Notation

We close this section by introducing notations that will be used later. For , let and . For a positive real number , is the smallest integer no smaller than and is the largest integer no larger than . For two positive sequences and , we write or if for all with some constant that does not depend on . The relation holds if both and hold. For an integer , denotes the set . Given a set , denotes its cardinality, and is the associated indicator function. The norm of a vector with is defined as for and . Moreover, we use to denote the norm by convention. For any function , the norm is defined in a similar way, i.e. . Specifically, . We use and to denote generic probability and expectation whose distribution is determined from the context. The notation also means expectation of under so that . Throughout the paper, , and their variants denote generic constants that do not depend on . Their values may change from line to line.

2 Main Results

2.1 Definitions and Settings

We start this section by introducing a class of divergence functions.

Definition 2.1 (Rényi divergence).

Let and . The -Rényi divergence between two probability measures and is defined as

The relations between the Rényi divergence and other divergence functions are summarized below.

-

1.

When , the Rényi divergence converges to the Kullback-Leibler divergence, defined as

From now on, we use without the subscript to denote .

-

2.

When , the Rényi divergence is related to the Hellinger distance by

and the Hellinger distance is defined as

-

3.

When , the Rényi divergence is related to the -divergence by

and the -divergence is defined as

Definition 2.2 (total variation).

The total variation distance between two probability measures and is defined as

The relation among the divergence functions defined above is given by the following proposition (see [38]).

Proposition 2.1.

With the above definitions, the following inequalities hold,

Moreover, the Rényi divergence is a non-decreasing function of .

Now we are ready to introduce the variational posterior distribution. Given a statistical model parametrized by , and a prior distribution , the posterior distribution is defined by

To address possible computational difficulty of the posterior distribution, variational approximation is a way to find the closest object in a class of probability measures to . The class is usually required to be computationally or analytically tractable. The most popular mathematical definition of variational approximation is given through the KL-divergence.

Definition 2.3 (variational posterior).

Let be a family of distributions. The variational approximation of the posterior is defined as

| (3) |

Just like the posterior distribution , the variational posterior is a data-dependent measure that summarizes information from both the prior and the data. For a variational set , the corresponding variational posterior can be regarded as the projection of the true posterior onto under KL-divergence. When is the set of all distributions, turns out to be the true posterior . The choice of the class usually determines the difficulty of the optimization (3). In this paper, our main goal is to study the statistical property of the data-dependent measure for a general .

2.2 Results for General Variational Posteriors

Assume the observation is generated from a probability measure , and is the variational posterior distribution driven by . The goal of this paper is to analyze from a frequentist perspective. In other words, we study statistical properties of under . The first theorem gives conditions that guarantee convergence of the variational posterior .

Theorem 2.1.

Suppose is a sequence that satisfies . Consider a loss function , such that for any two probability measures and , . Let be constants such that . We assume

-

•

For any , there exists a set and a testing function , such that

(C1) -

•

For any , the set above satisfies

(C2) -

•

For some constant ,

(C3)

Then for the variational posterior defined in (3), we have

| (4) |

for some constant only depending on and , where the quantity is defined as

Conditions (C1)-(C3) resemble the three conditions of “prior mass and testing” in [19]. Interestingly, Theorem 2.1 shows that with a slight modification, these three conditions also lead to the convergence of the variational posterior. The testing conditions (C1) and (C2) are required to hold for all . In the prior mass condition (C3), the neighborhood of is defined through a Rényi divergence with a , compared with the KL-divergence used in [19]. According to Proposition 2.1, for , so the condition (C3) in our paper is slightly stronger than that in [19]. This stronger “prior mass” condition ensures that the loss is exponentially integrable under the true posterior , which is a key step in the proof of Theorem 2.1. In all the examples considered in this paper, we will check (C3) with , which turns out to be a very convenient choice.

The convergence rate is the sum of two terms, and . The first term is the convergence rate of the true posterior . The second term characterizes the approximation error given by the variational set . A larger means more expressive power given by the variational approximation, and thus the rate of is smaller.

It is worth mentioning that we characterize the convergence of the variational posterior through the expected loss . Bounds for this quantity are also obtained by [29] independently with a stronger testing condition on the entire space. We remark that convergence in automatically implies that the entire variational posterior distribution concentrates in a neighborhood of the true distribution with a radius of the same rate. When the loss function is convex, it also implies the existence of a point estimator that enjoys the same convergence rate. We summarize these results in the next corollary.

Corollary 2.1.

Proof.

The first result is an application of Markov’s inequality

The second result is directly implied by Jensen’s inequality that

∎

To apply Theorem 2.1 to specific problems, we need to analyze the variational approximation error in each individual setting. However, this task may not be trivial for many problems. Now we borrow a technique in [44] to get a useful upper bound for . For any , we have

where . Then, we obtain the upper bound

where

| (5) |

Now, it is easy to see that a sufficient condition for the variational posterior to converge at the same rate as the true posterior is

| (C4) |

We incorporate this condition into the next theorem.

Theorem 2.2.

We would like to remark that the quantity is easier to analyze compared with the original definition of . According to its definition given by (5), it is sufficient to find a distribution , such that

| (7) |

These are exactly the two conditions formulated by [1] as a natural extension of the prior mass condition. The relation between the prior mass condition and (7) has also been discussed in [42].

One way to construct such a distribution that satisfies the above two inequalities is to focus on those whose supports are within the set for some constant . We summarize this method into the following theorem.

Theorem 2.3.

Suppose there exist constants , such that

| (C4*) |

where with . Then, we have

2.3 Results for Mean-Field Variational Posteriors

A special choice of is the mean-field class of distributions. Not only does this class leads to computationally efficient algorithms such as coordinate ascent, but in this section, we will also show that the structure of this class leads to a convenient convergence analysis. We begin with its definition.

Definition 2.4 (mean-field class).

For parameters in a product space that can be written as with some , the mean-field variational family is defined as

The following theorem can be viewed as an application of Theorem 2.3 to the mean-field class.

Theorem 2.4.

Suppose there exists a and a subset , such that

| (8) |

and

| (9) |

for some constants . Then, we have

Note that the condition (9) can also be written as

In other words, Theorem 2.4 gives an interesting “distribution mass” type of characterization for . Checking (9) is very similar to checking the “prior mass” condition (C3), and is usually not hard in many examples. We only need to make sure that is not too far away from the prior in the sense of (8). In fact, if the prior belongs to the class , then one can take , and the conditions of Theorem 2.4 simply become a “prior mass” condition , with the choice of being a subset of the KL-neighborhood . A more general characterization of the variational approximation error under model selection setting through a prior mass condition will be studied in Section 4.

3 Applications

In this section, we consider several examples to illustrate the theory developed in Section 2.

3.1 Gaussian Sequence Model

Consider observations generated by a Gaussian sequence model,

| (10) |

We use the notation for the distribution above. Our goal is to use variational Bayes methods to estimate the true parameter that belongs to the following Sobolev ball,

| (11) |

Here, the smoothness and the radius are considered as constants throughout the paper. The loss function for this problem is , which is a natural choice for the Gaussian sequence model.

The prior distribution is described through the following sampling process.

-

1.

Sample ;

-

2.

Conditioning on , sample for all , and set for all .

In other words, the prior on is a mixture of product measures,

| (12) |

Priors of similar forms are also considered in [32, 14, 15, 33]. Direct calculation implies that the posterior is also in the form of a mixture of product measures.

Consider the variational posterior defined by (3) with . That is, we seek a data-dependent measure in a more tractable form of a product measure. In most cases, the variational posterior does not have a closed form and needs to be solved by coordinate ascent algorithms [7]. However, for the Gaussian sequence model (10) with the prior distribution (12), one can write down the exact form of the mean-field variational posterior distribution.

Theorem 3.1.

Consider the variational posterior induced by the likelihood (10), the prior (12) and the mean-field variational set . The distribution is a product measure with the density of each coordinate specified by

| (13) |

where

and

| (14) |

The number is the posterior probability of the model dimension, and according to Bayes formula, it is

In other words, the mean-field variational posterior is nearly equivalent to a thresholding rule. It estimates all by after and applies the usual posterior distribution for each coordinate before . A mixed strategy is applied to the th coordinate. The effective model dimension is found in a data-driven way through (14).

Next, we will show that even though the posterior itself is not a product measure, using from the mean-field class still gives us a rate-optimal contraction result. The conditions on the prior distributions are summarized below.

-

•

There exist some constants such that

(15) -

•

There exist some constants such that for ,

(16) -

•

For the defined above, there exist some constants and such that

(17)

These three conditions on include a large class of prior distributions. We remark that even though (17) involves , it does not mean that one needs to know when defining the prior . For example, the choice that and being for some constants easily satisfies all the three conditions (15)-(17).

Conditions (15)-(17) will be used to derive the four conditions in Theorem 2.2. To be specific, (C1) and (C2) are consequences of (15) (see Lemma B.7 in the appendix), and (C3) and (C4) can be derived from (16) and (17) (see Lemma B.8 in the appendix). Then, by Theorem 2.2, we obtain the following result.

Theorem 3.2.

It is well known that the minimax rate of estimating in is [21]. Using a mean-field variational posterior, we achieve the minimax rate up to a logarithmic factor. In fact, the following proposition demonstrates that this rate cannot be improved for a very general class of priors.

Proposition 3.1.

On the other hand, the extra logarithmic factor can actually be removed by a rescaling of the prior. Details of this improvement are given in Appendix A.1.

3.2 Infinite Dimensional Exponential Families

In this section, we study another interesting variational family. The Gaussian mean-field family is defined as

| (18) |

This class offers better interpretability of the results because every distribution in is fully determined by a sequence of mean and variance parameters. Note that we allow to be zero and is understood as the delta measure on .

The application of is illustrated by an infinite dimensional exponential family model. We define the probability measure by

| (19) |

where denotes the Lebesgue measure on , is the th Fourier basis function of , and is given by

Since and can take arbitrary values without changing , we simply set . In other words, is fully parameterized by . Given i.i.d. observations from , our goal is to estimate , where is assumed to belong to the Sobolev ball defined in (11). The loss function is chosen as times the squared Hellinger distance .

We consider a prior distribution that is similar to the one used in Section 3.1. Its sampling process is described as follows.

-

1.

Sample ;

-

2.

Conditioning on , sample for all , and set for all .

We impose the following conditions on the prior .

-

•

There exist some constants such that

(20) -

•

There exist some constants such that for

(21) -

•

There exist some constants and such that

(22) for all and with defined above.

-

•

For the defined above, there exist some constants and such that

(23)

The conditions (20)-(23) are satisfied by a large class of prior distributions. For example, one can choose and being the density of for some constants , and then the four conditions are easily satisfied.

Theorem 3.3.

The theorem shows that the Gaussian mean-field variational posterior is able to achieve the minimax rate up to a logarithmic factor. We remark that the same result also holds for the mean-field variational posterior defined with . This is because , and thus . Compared with the class , the objective function using the parametric family can be optimized by algorithms such as stochastic gradient descent over the parameters . The objective function can be greatly simplified according to the general mean-field solution given in Theorem 5.1.

3.3 Piecewise Constant Model

The previous two sections consider examples of the mean-field variational set and its variant. In this section, we use another example to illustrate a situation where the mean-field variational set only gives a trivial rate. On the other hand, we show that alternative variational classes with appropriate dependence structures are able to achieve the optimal rate.

We consider the following piecewise constant model,

| (24) |

where independently for all . We assume throughout the section. The true parameter is assumed to belong to the class , where for a general ,

| (25) | |||||

Here for any two integers , we use to denote all integers from to . We assume both and are constants throughout this section. A vector is a piecewise constant signal with at most pieces. We use to denote the probability distribution of in this section.

The piecewise constant model is widely studied in the literature of change-point analysis. Recently, the minimax rate of the class is derived by [16]. When for some constant , the minimax rate is . With an extra constraint on the infinity norm, the minimax rate for is still , with a slight modification of the proof in [16]. Since in this case, it is natural to choose the loss function as .

We put a prior distribution on the parameter . Consider that has the following sampling process.

-

1.

Sample ;

-

2.

Conditioning on , sample for ;

-

3.

Conditioning on , sample , and then for , sample according to if and if .

We first consider variational inference via the mean-field class, defined as

We also define on the joint distribution of by

The variational posteriors and are given by (3) with variational classes defined above respectively222To be rigorous, the posterior distribution used in are the marginal posterior of and the joint posterior of , respectively.. Interestingly, for the piecewise constant model, both and give a trivial rate.

Theorem 3.4.

For the prior specified above with any absolutely continuous with respect to the Lebesgue measure, we have

for any , where and are the variational posteriors defined by (3) with and , respectively.

The result of Theorem 3.4 shows that the mean-field variational posteriors and are unable to achieve a better rate than simply estimating by the naive estimator . The proof, given in Appendix B.5, reveals the reason of this phenomenon. Since the independence structure of the two classes fails to capture the underlying dependence structure of the parameter space , the variational posterior distributions are equivalent to the posterior distribution induced by the prior , and therefore the condition (C4) is violated. Note that this is the first negative result in the literature on the statistical convergence of the mean-field approximation.

In order to achieve the minimax rate of the space , it is necessary to introduce some dependence structure in the variational class. One of the simplest classes of dependent distributions is the class of first-order Markov chains, defined by

The class introduces a natural dependence structure for the piecewise constant model, and it is compatible with the prior distribution , because conditioning on the change point pattern , the prior distribution of belongs to the class . We also introduce a similar variational class on the joint distribution of , defined by

Besides the distribution of restricted to , the distributions of and are both in the mean-field classes.

In order to derive the rates for the variational posterior distributions induced by and , we impose the following conditions on the prior distribution .

-

•

There exist some constants such that

(26) -

•

There exists a constant such that

(27)

According to Theorem 2.2, we get the following result.

Theorem 3.5.

Theorem 3.5 shows that both and are able to achieve the minimax rate of the problem. This example illustrates the importance of the choice of the variational class. According to Theorem 2.1, the rate of a variational posterior is upper bounded by , the rate of the true posterior, plus , the variational approximation error. The choice of for the piecewise constant model leads to a very large , and thus a trivial rate in Theorem 3.4. On the other hand, the variational approximation errors given by the classes and are small, which are dominated by the minimax rate.

Though the statistical properties of the two classes and are both satisfactory, the class enjoys a computational advantage, and the solution can be computed exactly via dynamic programming. In order to characterize the solution , we consider the following discrete optimization problem:

| (28) |

The solution of (28) is denoted as the sequence . We remark that under the condition (26), the penalty term of (28) comes from the fact that

which coincides with the minimax rate.

Theorem 3.6.

Let the maximizer of (28) be . For

the distributions , and are specified as follows.

-

1.

Under , for , and elsewhere with probability .

-

2.

We have .

-

3.

We have , where

By Theorem 3.6, in order to get , it is sufficient to solve (28). This can be done through a dynamic programming given in Algorithm 1. To simplify the notation, we define

| (29) |

for any integers .

4 Variational Bayes with Model Selection

4.1 General Settings

In this section, we consider a general form of probability models

Here, the probability is determined by an index and a parameter . We assume that the set is either countable or finite. For a given , the probability is parametrized by a in a parameter space that is indexed by this . Without loss of generality, we assume that the parameter can be written in a blockwise structure

Note that the dimension of may vary with .

The model is very natural for many applications. One can think of as a model dimension index, which determines the complexity of the parameter space . A leading example is the mixture density model, where stands for the number of components.

To model the hierarchical structure of , one naturally uses a hierarchical prior distribution, which is specified through the following sampling process:

-

1.

Firstly, sample from ;

-

2.

Conditioning on , sample from the probability measure , and has a product structure

(30)

For variational inference, we consider a mean-field class that naturally takes advantage of the structure of the prior distribution. For a given , the corresponding mean-field class is defined as

| (31) |

In order to select the best model from the data, we consider optimizing the evidence lower bound (ELBO). With the notation standing for the joint likelihood function, the marginal likelihood given a model is defined by

| (32) |

Then, a straightforward model selection procedure is to maximize over . In order to overcome the intractability of the integral (32), we instead optimize a lower bound, which is given by

| (33) | |||||

which can be derived by a direct application of Jensen’s inequality. Denote the right hand side of (33) by , and we will solve the following optimization problem,

| (34) |

Finally, the solution to (34) leads to the variational posterior distribution that we use in a model selection context. A similar variational approximation to the tempered posterior in the model selection setting was studied by [12].

4.2 Convergence Rates

Assume the observation is generated from a probability measure , and is the variational posterior that is a solution to (34). For the general settings described above, we show that the variational approximation error can be automatically controlled by a prior mass condition. Let be the prior distribution on induced by the sampling process of .

Theorem 4.1.

Suppose is a sequence that satisfies . Let be a constant and be constants. We assume that there exists a and a subset , such that

| (C3*) |

where and are defined in the prior sampling procedure. Moreover, assume that the conditions (C1) and (C2) hold for all with respect to prior procedure and some constant . Then for the variational posterior defined as the solution of (34), we have

| (35) |

Theorem 4.1 characterizes the convergence rate of mean-field variational posterior with model selection using the conditions (C1), (C2) and (C3*). Given the structure of the prior distribution, an equivalent way of writing (C3*) is

for the factorized structure of . Therefore, our three conditions (C1), (C2) and (C3*) still fall into the “prior mass and testing” framework, and directly correspond to the three conditions in [19] for convergence rates of the true posterior.

4.3 Density Estimation via Location-Scale Mixtures

In this section, we consider the location-scale mixture model as an application of the theory. The location-scale mixture density is defined as

| (36) |

where , with , , and

| (37) |

for some positive even integer . The kernel has a pre-specified form, for example, Gaussian density when , while the parameters and are to be learned from the data.

The location-scale mixture model (36) can be written as a special example of the general probability models introduced in Section 4.1. In this case, the countable set is the positive integer set . The parameter space indexed by is defined as

Given i.i.d. observations sampled from some density function , our goal is to estimate the density through the location-scale mixture model (36). We denote the probability distribution of the mixture density as and a probability distribution with a general density as . In the paper [22], a Bayesian procedure is proposed and a nearly minimax optimal convergence rate is derived for the true posterior distribution. We will follow the same setting in [22], but analyze the variational posterior.

We first specify the prior distribution through the following sampling process:

-

1.

Sample the number of mixtures ;

-

2.

Conditioning on , sample the location parameters independently from , sample the weights from , and then sample the precision parameter from .

In order to optimize (34) in the variational Bayes framework, we specify the blockwise structure (31) in this case as

| (39) |

Note that we do not factorize because of the constraint . The variational posterior distribution is defined as that solves (34). The loss function here is chosen as times squared Hellinger distance, i.e., .

In order that enjoys a good convergence rate, we need conditions on the prior distribution and the true density function . We first list the conditions on the prior.

-

1.

There exist constants , such that

(40) for all . There exist constants , such that

(41) for all .

-

2.

There exist constants , such that

(42) for all and constants , such that

(43) for all .

-

3.

There exist constants , such that

(44) for all and , where .

-

4.

There exist constants , such that

(45) for all . There exist constants and a constant that satisfy

(46) for all .

The conditions on the prior distribution are quite general. For example, one can choose , , and for some positive constants . Then, the conditions above are all satisfied.

Next, we list the conditions on the true density function :

-

B1

(Smoothness) The logarithmic density function is assumed to be locally -Hölder smooth. In other words, for the derivative , there exists a polynomial and a constant such that,

(47) for all that satisfies . Here, the degree and the coefficients of the polynomial are all assumed to be constants. Moreover, the derivative satisfies the bound for all with some constants .

-

B2

(Tail) There exist positive constants , , , such that

(48) for all .

-

B3

(Monotonicity) There exist constants such that is nondecreasing on and is nonincreasing on . Without loss of generality, we assume and for all with some constant .

These conditions are exactly the same as in [22] and similar conditions are also considered in [26]. The conditions allow a well-behaved approximation to the true density by a location-scale mixture. There are many density functions that satisfy the conditions (B1)-(B3), for which we refer to [22].

The convergence rate of the variational posterior is given by the following theorem.

Theorem 4.2.

The proof of Theorem 4.2 largely follows the arguments in [22] that are used to establish the corresponding result for the true posterior distribution, thanks to the fact that Theorem 4.1 requires three very similar “prior mass and testing” conditions to that of [19]. The only difference is that function approximations via location-scale mixtures need to be analyzed under a stronger divergence for some . For this reason, the proof of Theorem 4.2 relies on the construction of a surrogate density function . We first apply Theorem 4.1 and establish a convergence rate under . Then, the conclusion is transferred to with a change-of-measure argument. Details of the proof are given in Appendix B.6.

4.4 Dealing with Latent Variables

For the mixture model considered in Section 4.3, we discuss a variation of the variational Bayes approach (34) by including latent variables. This facilitates computation and leads to a simple coordinate ascent algorithm that has closed-form updates. In the setting of mixture model, our approach is adaptive to the unknown number of components, and can be regarded as an extension of [42, 29] for variational inference with latent variables.

Since with , we can write

where , and the probability of is under . We use the notation for the joint distribution of , and then the marginal likelihood (32) can be written as

Similar to (33), the evidence lower bound with the latent variables is given by

| (49) | |||||

The right hand side of (49) is shorthanded by . Define

Then, we solve the following optimization problem,

| (50) |

The solution to (50) leads to the variational posterior distribution . It is worth noting that even though is a joint distribution of , the posterior inference only relies on the marginal of , since the parametrization of the density in (36) does not depend on the latent variables. The existence of the latent variables only facilitates computation.

Theorem 4.3.

Theorem 4.3 shows that the variational posterior with latent variables achieves the same contraction rate as in Theorem 4.2. In fact, the two variational lower bounds (33) and (49) satisfy the following relation,

which implies that the introduction of latent variables makes the variational approximation looser. On the other hand, Theorem 4.3 shows that the worse variational approximation does not compromise the statistical convergence rate. Moreover, with the help of latent variables, can be computed via standard variational inference algorithms. Details of the computational issues are given in Appendix A.2.

5 Discussion

5.1 Variational Bayes and Empirical Bayes

In this section, we discuss an intriguing relation between variational Bayes and empirical Bayes in the context of sieve priors. We consider a nonparametric model with an infinite dimensional parameter . This includes the Gaussian sequence model and the infinite dimensional exponential family discussed in Section 3, as well as nonparametric regression and spectral density estimation. For each dimension, we assume and . Then, a sieve prior is specified by the following sampling process.

-

1.

Sample ;

-

2.

Conditioning on , sample for all , and sample for all .

We assume that the densities and satisfy and . A leading example of the sieve prior is case of and , as is used in Section 3.1 and Section 3.2.

An empirical Bayes procedure maximizes 333The canonical form of empirical Bayes has a flat prior on ., where

is the logarithm of marginal likelihood. With the maximizer , the empirical Bayes posterior is defined as

| (51) |

Compared with a hierarchical Bayes approach, the empirical Bayes procedure does not need to evaluate the posterior distribution of , and thus in many cases is easier to implement.

We also study mean-field approximation of the posterior distribution. In order to characterize its form, we need a few definitions. For any , define

By Jensen’s inequality, we observe that

| (52) |

for any . We also define the density classes and . The next theorem gives the exact form of the mean-field variational posterior.

Theorem 5.1.

Consider the variational posterior induced by the sieve prior and the mean-field variational set . The distribution is a product measure with the density of each coordinate specified by

where for each given , and maximize the following objective function,

| (53) |

under the constraints that and for all , maximizes

| (54) |

and finally,

The result of Theorem 5.1 also applies to the class discussed in Section 3.2 with replaced by the Gaussian class. We note that Theorem 5.1 can be viewed as an extension of Theorem 3.1. In fact, if the likelihood function can be factorized over each coordinate of , the form of can be greatly simplified.

Corollary 5.1.

In light of Theorem 5.1, we can compare the variational Bayes approach and the empirical Bayes approach, especially the definitions of and . The empirical Bayes chooses the best model by maximizing , or equivalently , while the variational Bayes maximizes (54). There are two major differences. The first difference is that empirical Bayes uses the exact marginal likelihood function and variational Bayes uses a mean-field approximation of . We remark that in the case of likelihood that can be factorized, the mean-field approximation is exact, which leads to (55). The second difference is that empirical Bayes maximizes the posterior probability of the th model, but the variational Bayes maximizes the sum of the posterior probabilities (or their mean-field approximations) of the th and the th models.

Despite the two differences, the empirical Bayes approach and the variational Bayes approach have a lot in common. Both are random probability distributions that summarize the information in data and prior. Both select a sub-model according to very similar criteria. To close this section, we show that with a special variational class, the induced variational posterior is exactly the empirical Bayes posterior.

Theorem 5.2.

Define the following set

Then, the empirical Bayes posterior defined by (51) is the variational posterior induced by the sieve prior and the variational class .

5.2 Variational Approximation as Regularization

According to Theorem 2.1, the convergence rate of the posterior is determined by the sum of , the rate of the true posterior, and , the variational approximation error. Since , it seems that the convergence rate of variational posterior is always no faster than that of the true posterior. However, Theorem 2.1 just gives an upper bound. In this section, we give two examples, and we show that it is possible for a variational posterior to have a faster convergence rate than that of the true posterior.

Example 1

We consider the setting of Gaussian sequence model (10). The true signal that generates the data is assumed to belong to the Sobolev ball . The prior distribution is specified as

Note that a similar Gaussian process prior is well studied in the literature [37, 9]. We force all the coordinates after to be zero, so that the variational approximation through Kullback-Leibler divergence will not explode. For the specified prior, the posterior contraction rate is , and when , the optimal minimax rate is achieved.

Consider the following variational class

for a given integer . It is easy to see that the variational posterior defined by (3) with can be written as

In other words, the class does not put any constraint on the first coordinates and shrink all the coordinates after to zero. Ideally, one would like to use for the coordinates after . However, that would lead to for all given that the support of is a singleton. That is why we use instead. The rate of for each is given by the following theorem.

Theorem 5.3.

Note that Theorem 5.3 gives both upper and lower bounds for . This makes the comparison between variational posterior and true posterior possible. Observe that when , we have , and the result is reduced to the posterior contraction rate in [9].

Depending on the values of and , the rate for can be better than that of the true posterior. For example, when , the choice leads to the minimax rate , which is always faster than . This is because for a , the true posterior distribution undersmooths the data, but the variational class with helps to reduce the extra variance resulted from undersmoothing by thresholding all the coordinates after . On the other hand, when , an improvement through the variational class is not possible. In this case, the true posterior has already overly smoothed the data, and the information loss cannot be recovered by the variational class.

Example 2

Consider the problem of sparse linear regression , where is a design matrix of size and belongs to the sparse set for some . The prior distribution on is specified by the Laplace density

Though the posterior distribution has a close connection to LASSO, it is proved in [11] that the posterior distribution cannot adapt to the sparsity of . In particular, the common choice of in the theoretical analysis of LASSO only leads to a dense posterior.

In fact, it is known in the literature (e.g. [5]) that the LASSO, which is the posterior mode, achieves a nearly optimal rate over the class . We show that the posterior mode can be well approximated by applying a simple variational class. Consider the variational class

Define to be the minimizer of .

Theorem 5.4.

For any and , we have , where

| (56) |

The function is defined by with and .

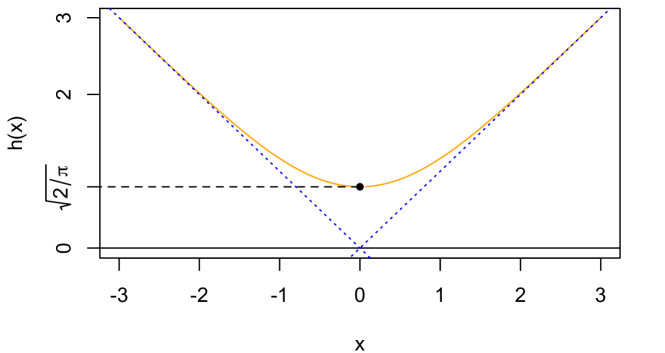

Theorem 5.4 shows that the variational approximation is characterized by the penalized least-squares estimator (56). Observe that is a convex function, and it satisfies (see Figure 1), and thus will get arbitrarily close to the LASSO estimator as . Therefore, even though the posterior does not have a good frequentist property, its variational approximation can recover a sparse signal.

By the fact that , we have

| (57) |

Hence, a risk bound for the penalized least-squares estimator (56) directly leads to the convergence of the variational posterior. To present a bound for , we need to introduce some new notation. Let be the support of . Define the restricted eigenvalue by

| (58) |

where and is defined similarly. The same quantity (58) also appears in the risk bound of LASSO [5].

Theorem 5.5.

We note that is the same rate of convergence of LASSO [5]. With chosen as small as , the statistical property of the variational posterior is very similar to that of the LASSO, and thus improves the original dense posterior distribution that is not suitable for sparse recovery.

5.3 Model Misspecification

In this section, we present an extension of Theorem 2.1 in the context of model misspecification. We consider a data generating process that may not satisfies the conditions (C1)-(C3). The following theorem shows that the convergence rate of the variational posterior will then have an extra term that characterizes the deviation of to the model specified by the likelihood.

Theorem 5.6.

We note that here is defined with respect to instead of in Theorem 2.1. Theorem 2.1 can be viewed as a special case of Theorem 5.6 with . The extra term in the convergence rate that characterizes model misspecification is given by . In fact, it can be replaced by any -Rényi divergence with .

Convergence rates of variational approximation to tempered posterior distributions under model misspecification have been studied by [1] (See their Theorem 2.7). Our results complement theirs by considering variational approximation to the ordinary posterior.

The next theorem gives sufficient conditions so that the variational approximation error is dominated by the sum of the other two terms in (59). It can be viewed as an extension of Theorem 2.3.

Theorem 5.7.

Suppose there are constants , such that

| (C4**) |

where with

Then, we have

Acknowledgements

The authors are grateful to an associate editor and two referees who give very insightful feedbacks that lead to the improvement of the paper.

Appendix A Additional Results

A.1 Sharp Convergence Rates for Gaussian Sequence Model

In this section, we consider a prior so that the logarithmic term in the convergence rate of Theorem 3.2 can be removed. The sampling process of the prior is specified as follows.

-

1.

Sample ;

-

2.

Conditioning on , sample for all , and set for all .

Obviously, this prior is the same as the previous one when . However, the -scaling allows us to formulate conditions that help remove the logarithmic factor in Theorem 3.2. The same rescaling is also used in [14, 15] to achieve sharp minimax rates. The following two conditions will be used to replace (16) and (17).

-

•

There exist some constants such that for ,

(60) -

•

For the defined above, there exist constants and , such that

(61)

The condition (60) is similar to (16), while (61) is stronger compared with (17). In general, one can choose to be a density with a heavy tail. As an example, one can easily check that and with constants satisfy the two conditions. Conditions (C3) and (C4) can be derived from (60) and (61) (see Lemma B.9). This leads to the following result.

A.2 An Algorithm for (50)

In this section, we discuss how to optimize (50). We first consider the problem for a fixed . To solve this problem, a traditional method is to apply the coordinate ascent variational inference (CAVI). In order to obtain closed-form updates, we restrict ourselves to conjugate priors. In particular, we choose the kernel to be , and priors to be

where . By conjugacy, we can assume the variational posterior density for as with

and

where . Then, we only need to iteratively update the parameters as below.

-

1.

Update by

-

2.

Update by

-

3.

Update by

-

4.

Update by

The above iterations will approximately solve for a fixed . The solution is parametrized by . To select the best , we then need to evaluate the objective function (50), which is equivalent to plugging the values of into the right hand side of (49). This leads to the objective function

| (62) |

which can be calculated with a closed form by conjugacy. Finally, we choose that maximize (62).

Note for each fixed , computing (62) is straightforward and efficient by CAVI. The bottleneck of the algorithm is that one needs to evaluate (62) for every . However, in terms of achieving the same statistical convergence rate given by Theorem 4.3, this is not necessary. Even if the variational posterior selects the best from a much smaller set according to (50), the same rate in Theorem 4.3 can still be achieved with a slight modification of the proof. Therefore, one only needs to compute (62) for all .

A.3 Beyond the Kullback-Leibler Approximation

Modern variational approximation methods are not limited to the approximation by Kullback-Leibler divergence. For example, [25] proposed a generalized variational inference method using Rényi divergence and derived a corresponding evidence lower bound. Though alternative divergences may be hard to optimize, they may give better approximations [27, 28].

It is possible to generalize our results to variational approximation using other criterions. We first introduce a -variational posterior.

Definition A.1 (-variational posterior).

Let be a family of distributions. The -variational posterior is defined as

| (63) |

Then we state a result that extends Theorem 2.1 to the -variational posterior distribution.

Theorem A.2.

Theorem A.2 is a generalization of Theorem 2.1 for a divergence that is not smaller than the Kullback-Leibler divergence. Examples of applications include all Rényi divergence with and the -divergence. Divergence functions that are not necessarily larger than the Kullback-Leibler require new techniques to analyze, and will be considered as an interesting future project.

Appendix B Proofs

B.1 Proof of Theorem 2.1

This section gives the proof of Theorem 2.1, which is divided into several lemmas. We first give an inequality that uses the basic property of the KL-divergence.

Lemma B.1.

For any function and two probability measure and , we have

Proof.

By the definition of KL-divergence, we have

where is a probability measure given by

∎

Then, we can use the inequality in Lemma B.1 to derive a useful bound for .

Lemma B.2.

For the defined in (3), we have

Proof.

By Lemma B.1, we have

for all . By the definition of , we have

for all . Taking expectation on both sides, we have

Using Jensen’s inequality, we get

Therefore,

The proof is complete by taking minimum over and . ∎

In order to bound , we need the following lemma on the posterior tail probability. Its proof is similar to the one used in [19].

Proof.

We first define the sets

We also define the event

where the probability measure is defined as . Let and be the set and the testing function in (C1). Then, we bound by

We will give bounds for the three terms above respectively. By (C1),

| (65) |

Using the definitions of , we have

| (66) | |||||

Now we analyze the third term. On the event , we have

where the last inequality is by (C3). Then, it follows that

where the last inequality is by (C1) and (C2). Since , we obtain the bound

| (67) |

Combining the bounds (65), (66) and (67), we have

∎

Next, we derive a moment generating function bound for a sub-exponential random variable.

Lemma B.4.

Suppose the random variable satisfies

for all . Then, for any ,

Proof.

Set for some . Then, for any .

Choose , and then since , we have

∎

Now we are ready to prove Theorem 2.1.

B.2 Proofs of Theorem 2.3, Theorem 2.4 and Theorem 4.1

Proof of Theorem 2.3.

For any , we have , and thus . By (C4*), we have . Therefore, , and the proof is complete. ∎

Proof of Theorem 2.4.

Lemma B.5.

For defined as the solution of (34),

where is the prior distribution on induced by the sampling process of .

Proof.

We use , to denote the densities of , . A lower bound can be directly derived from the right hand side minus the left hand side. For any , any , and any , we have

where is the probability measure with the density with

and

The proof is complete. ∎

Proof of Theorem 4.1.

By Lemma B.5, we have

Now we analyze each term on the right hand side. By Jensen’s Inequality together with Lemma B.3 and Lemma B.4, we have

with some small constant . This is because the conditions (C1) and (C2) with respect to prior hold by assumption, and (C3) is implied by (C3*) with the argument

For the remaining terms, we choose and . According to prior structure, , and

We also have

Hence, we obtain the desired result. ∎

B.3 Proofs of Theorem 3.1, Proposition 3.1, Theorem 3.2 and Theorem A.1

Proof of Theorem 3.1.

To show Proposition 3.1, the following lemma is needed.

Lemma B.6.

For the prior distribution defined in (12), we assume that and is nonincreasing over . Then, we have

for any , where .

Proof.

We use the notation

By the condition , we have . Define the objective function

It is easy to check that

To give a bound for , we first study the difference for any . We use the inequalities

and

Then, we have

where . Now we bound by

| (68) |

where , and is some large constant. For each ,

where the last inequality is by the fact that is of a smaller order than . Finally, a standard chi-squared tail bound gives

Using (68) and summing over , we get , and the proof is complete. ∎

Proof of Proposition 3.1.

According to Theorem 3.1, the variational posterior is a product measure, and for any coordinate after a , the component is . By Theorem B.6, we know that . Use the notation . Then, we have by Markov inequality. Consider a with every entry zero except that . It is easy to check that . For this , we have

Thus, the proof is complete. ∎

The proofs of Theorem 3.2 and Theorem A.1 will be split into the following three lemmas. Recall that we use the loss for this model.

Proof.

Given any and any , we define

Then, by (15), we have

This proves (C2). To show (C1), we consider the following testing problem,

Define as the -covering number of a set under a metric . Then, according to Lemma 5 in [18] and Theorem 7.1 in [19], it is sufficient to establish the bound

This is obviously true given a standard volume ratio calculation in a Euclidean space of dimension . Then, by Theorem 7.1 in [19], there exists a testing procedure such that (C1) holds. Note that the testing error can be arbitrarily small given a sufficiently large . ∎

Lemma B.8.

Proof.

We first show (C4). We will apply Theorem 2.4 by constructing a and that satisfy the conditions (8) and (9). Define for all and for all , where is the same as defined in 16. We also define the measure by

It is easy to see that . For any , we have

| (69) |

and

| (70) |

Therefore, the condition (8) holds. To check the condition (9), we use the bound

where we have used Jensen’s inequality above. We are going to bound each of the integral above using (17). For any , we have

Hence, we get

| (71) |

which implies that (9) holds. The condition (C4) is thus proved by applying Theorem 2.4.

Lemma B.9.

Proof.

The proof is essentially the same as that of Lemma B.8. We define and in the same way except that . Then, by the same calculation, we have for any ,

Therefore, the condition (8) holds. For any ,

By Hölder’s inequality,

Therefore,

Using Hölder’s inequality again, we get

Set . As , we have . Then

Thus,

This leads to the desired bound in (9). The condition (C4) is thus proved by applying Theorem 2.4.

B.4 Proof of Theorem 3.3

For Theorem 3.3, the loss function is . We split the proof of Theorem 3.3 into following two lemmas.

Lemma B.10.

Lemma B.11.

Before proving these two lemmas, we need the following two results that establish relations between different divergence functions for the exponential family model.

Lemma B.12.

If , then

Proof.

We first give some uniform bounds that are well known for exponential family density functions (see [32]). For any , we have

| (72) |

We start from the left hand side of the inequality:

where we have applied the property that is monotonically increasing for all . Then it follows that . ∎

Lemma B.13.

For any and any with , we have

where the constant only depends on and .

Proof.

For any , we have . Since

| (73) |

where for . This gives

| (74) |

Proof of Lemma B.10.

Given any , we define the set

where and . We bound by

where we have used the conditions (20) and (22). Therefore, for any , we can choose a sufficiently large , such that , which proves (C2).

To prove (C1), we consider the following testing problem,

By Theorem 7.1 in [19], it is sufficient to establish the bound

Note that for any , we have . Therefore, by Lemma B.12,

when . This means as long as , we have . Thus, there exists a constant , such that

where we have used the condition in the last two steps above.

It implies the existence of a testing function that satisfies (C1). The testing error can be made arbitrarily small by choosing a sufficiently large . Hence, the proof is complete. ∎

Proof of Lemma B.11.

In the first part of the proof, we derive (C3). We take . Define , where for all and for all . Then, by Lemma B.12, for all ,

where we have use the condition .

Therefore, it is sufficient to lower bound , which has been done in the proof of Lemma B.8.

Now we will derive (C4). Rather than using the results of Theorem 2.3 or Theorem 2.4, we will construct a and bound directly. Note that in the current setting, we have

For , define , where for and for . Then, it is easy to see that .

We first give a bound for . Let denote the probability distribution with density function . Then, we have

where the first term on the right hand side above can be bounded as

according to the condition (21). For any , we use to denote the density function of . Then, by (23), we have

Since , we have

Therefore, we have obtained .

B.5 Proofs of Theorem 3.4, Theorem 3.5 and Theorem 3.6

Proof of Theorem 3.4.

Recall that is the space of piecewise constant vectors with at most pieces. Then, we have the partition

First of all, we consider . Suppose the measure and , then the support of must be a subset of the support of . Note that the distributions ’s are all absolutely continuous. That is, for any singleton , , which indicates that for any singleton . Thus, is continuous in each coordinate and for any , . Therefore,

because otherwise the independent structure of would imply a delta measure for some coordinate, which leads to . This implies that is supported on . Therefore,

where . Then, by the definition of and the independent structure of , we have

This gives

In other words, the mean-field variational posterior is a product measure, and on each coordinate, it equals the posterior distribution induced by the prior . Now we give a lower bound for . Since , we have

where we use to stand for the posterior expectation of with the prior . By Jensen’s inequality,

Therefore,

Next, we consider . As , we can assume

For the same reason, is supported on . The joint distribution of prior is written as

Thus, conditioning on , for all . In other words, for all . Plug it in the definition of , we have

This gives and . It implies that

The proof is complete. ∎

Proof of Theorem 3.5.

Proof of Theorem 3.6.

If , we will have . For , as , we can conclude that and . In other words, the conclusion leads to , or , .

Thus, we can define a set , such that for , and , whereas for , and , a continuous density function. Then we can write

Plug it into , and we get

where

Then

For a given set with , we first solve the minimization over and . The solutions without constraint that are given by

and

As obtained above is still in the variational set , this is a valid solution to (B.5) for a specific set , which implies that

and

Now the only thing is to show that and are the solution of (3.3). Plug and into (B.5), and then

| (79) | |||||

and

Plug (79) and (B.5) into (B.5), and the optimization problem becomes (3.3). The proof is complete. ∎

B.6 Proofs of Theorem 4.2 and 4.3

To prove Theorem 4.2, we first establish an upper bound of by applying Theorem 4.1 for a that is constructed to be close to . Then, with a change-of-measure argument, we derive a bound for . The construction of the surrogate density function is given by the following lemma.

Lemma B.14.

With the definition of and its property given by Lemma B.14, we can bound by checking the conditions (C1), (C2) and (C3*) in Theorem 4.1. This argument is split into the next two lemmas.

Lemma B.15.

Lemma B.16.

We first prove Lemma B.14, and then prove Lemma B.15 and Lemma B.16. To facilitate the proof of Lemma B.14, we introduce the following lemma, which is analogous to Theorem 1 in in [22].

Lemma B.17.

Proof.

We set and

This is the same definition that appears in Lemma 1 of [22]. Note that , and we only need to derive an upper bound for this integral. We first have the following decomposition

The first and third terms can be bounded by according to the same argument in the proof of Theorem 1 in [22] when is chosen to be large enough. For the second term, according to Remark 1 in [22], we have with some constant for all . Then Lemma 2 in [22] implies

The last term can be upper bounded by . Summing up all the terms, we obtain the desired conclusion. ∎

Proof of Lemma B.14.

The proof uses a slightly modified argument in the proof of Lemma 4 in [22]. First of all, according to Lemma B.17, there exists a density such that . Define , where is chosen to be large enough. Set . Define the number , with and some constant . We choose with to be the finite mixture given by Lemma 12 in [22] that satisfies

for , where is the density of . We will show that this mixture density satisfies (81). We write

The four ratios will be bounded separately.

- 1.

-

2.

For the second term, we have

Since for a constant uniformly over ,

Combining with Lemma B.17, we conclude that

for a constant .

- 3.

-

4.

According to the proof of Lemma 4 in [22], we have for some constant . Because , . This leads to the inequality . Note that for any , we have uniformly over . Thus, for a sufficiently large ,

where we have used the condition . Then we have

for all with some constant .

Combining the bounds of all terms above, we get

which indicates that (81) holds. When , and , according to Lemma 3 in [22], we have

Then the four points listed above also hold, which means that (81) is also satisfied for these . The proof is complete. ∎

Proof of Lemma B.15.

We consider the set

| (82) |

where

with , , and . It’s easy to see that

where . Thus

Now we derive an upper bound for each term.

- 1.

-

2.

By the condition (40), we have

- 3.

Summing up the three bounds above, we have for some constant . In order that the constant can be arbitrarily large, one can replace by for a sufficiently large and use the same argument above. We therefore obtain (C2).

Now we start to show (C1). By Theorem 7.1 in [19], it is sufficient to bound the metric entropy

Since , we have . According to (82),

and thus it is sufficient to bound for each .

We use to denote with in short. According to Lemma 3 in [22], for any with and with such that , we have

Based on the fact that , we have

Then, we use Lemma 5 in [22], and obtain

where , and

for some constants . Note that we have used the condition for some constant to derive the above bounds. Finally, we have

which leads to

The proof is complete. ∎

Proof of Lemma B.16.

According to Lemma B.14, there exist , such that (81) holds. Then we set in Theorem 4.1 and , where . To be specific, let be any fixed constant such that , and then we define

and

The conclusion of Lemma B.14 implies

| (83) |

for a constant . Choose , then for any as . Then the condition (41) implies

| (84) |

We also have

According to the condition (43) and Lemma B.14, we have with as in Lemma B.14. Then,

By (44), we have

Finally, the condition (46) leads to

With the choice and , we have

where . Plug in ,we obtain (C3*) with respect to . ∎

Finally we prove Theorem 4.2.

Proof of Theorem 4.2.

Now we prove Theorem 4.3. We also use change of measure argument and show the concentration around at first.

Proof of Theorem 4.3.

We first present a latent variable version of Lemma B.5,

| (85) | |||||

where is defined in the Lemma B.15. The proof of this inequality follows the same argument as in the proof of Lemma B.5 and thus we omit it. Note that the parametrization of the density in (36) does not rely on the latent variables. Therefore, when the conditions of Theorem 4.2 are satisfied, for some small constant , we have

Now we need to choose some and to bound the remaining terms of (85). We consider and , where . We sometimes shorthand by when the context is clear. Write , and we have

Thus, the optimal choice of is that

and we fix this choice as our . We then have

We now specify the choice of and in (B.6). According to Lemma B.14, for , when such that

we have

| (87) |

Suppose , then and when . Then consider . Obviously, and for all . Set

where with and to be determined later. Choose and in (B.6), where

Now, we build an upper bound for

| (88) |

or equivalently, construct lower bounds for for all and . Set and , and then for any , , , we have

and

Now we build the upper bounds of in two cases:

-

•

If , then

-

•

If , then

Therefore,

and then

where the last step we apply the fact that . Thus, we have

so

where .

We plug the above upper bound into (B.6), and then

Now we build the upper bound for each term in the right hand side above. For the first term, when , , we have

Choose and . When and , we have

Next, for the second term, as , by (87), we have

Finally, for the last term,

Then, by the same arguments as in the proof of Lemma B.16, when , we can further obtain that

Therefore, with the choice of , we have

where is the same defined in Theorem 4.2. Combining all the bounds above, we have

Finally, we have

With the same change of measure argument in the proof of Theorem 4.2, the proof is complete. ∎

B.7 Proofs of Theorem 5.1, Corollary 5.1 and Theorem 5.2

We first show the following lemma to assist the proof of Theorem 5.1

Lemma B.18.

The variational posterior with respect to the set is a product measure, with the density for each coordinate in the form of

| (89) |

where and for all j, is some integer, and .

Proof.

In order that , we must have

In other words, for any set such that , we must have . For each coordinate, we can assume that , where and . For each , define

Obverse that for , . Then, we can define the set . According to the sampling process of , , which implies that . Note that for each ,

and then

| (90) |

For any ,

Therefore, for all , and there are three possible cases:

-

•

for all .

-

•

for all .

-

•

for , for , and for some .

However, the first two cases do not satisfy the constraint (90). Thus, the variational posterior is limited to the form (89), which completes the proof. ∎

Proof of Theorem 5.1.

By Lemma B.18, the variational posterior has the form

Now we need to determine , , for and for . We denote the above distribution by . Then, it is easy to see that . This implies

where . Minimizing over leads to

Plugging into (B.7), we have

Therefore, , , are the solution to maximizxing the objective function

under the constraints that and for all . The proof is complete. ∎

Proof of Corollary 5.1.

If , then

and

The equalities above hold when for and for . Plug these choices into the objective function, and then the objective function becomes

This implies that maximizes , where

Therefore, is given by

The proof is complete. ∎

Proof of Theorem 5.2.

Assume , according to the definition, there exists a such that

where . Then

where .

Therefore, for a specific , is chosen as

to minimize under the constraint that . Plug this form into the right hand side of (B.7), we can get selected as

And therefore, is the variational posterior with the variational class . ∎

B.8 Proof of Theorem 5.3

Proof of Theorem 5.3.

Recall that

Then, we can decompose the risk into

For the upper bound, we have

Now we discuss in the two cases:

-

•

When , we have

and

Therefore,

-

•

When , we have

and

Thus, we have

Now we prove the lower bound. According to the risk decomposition, we have

-

•

When , we consider a with every coordinate except that . It is easy to check that . Then, we have and . Therefore,

-

•

When , we consider a with every coordinate except that , and it is easy to check that . Then, we have

and

This leads to the lower bound

Now the proof is complete. ∎

B.9 Proofs of Theorem 5.4 and Theorem 5.5

Proof of Theorem 5.4.

Define , and then

which is a constant with respect to . Thus,

where . With , we have ’s independently drawn from , and therefore,

where

The proof is complete. ∎

Lemma B.19.

Proof of Lemma B.19.

It is not hard to see that . Thus, we only need to show the inequality for . For , set , and then

Thus, is monotonically decreasing when and . For the left part of inequality, notice that for all in [30], and then we can directly obtain that . ∎

Proof of Theorem 5.5.

We use the notation . By Lemma B.19, we have . By rearranging the basic inequality , we have

For the terms on the right hand side of the above inequality, we have and . Therefore, with the notation , we have

| (93) |

as long as . Note that the choice implies that the condition holds with probability at least by a union bound argument in [5]. With the decompositions , and , the inequality (93) becomes

| (94) |

The inequality (94) immediately implies what is known as the generalized cone condition defined in [17],

| (95) |

Another consequence of (94) is the error bound

| (96) |

For the that satisfies (95), we define

It is easy to see that . Since

we have by the definition of in (58). We also bound by

where the last inequality is by (95). Therefore,

Since , we have

Combining the above inequality and (96), we have

which further leads to

With and , we have , which completes the proof. ∎

B.10 Proofs of Theorem 5.6, Theorem 5.7 and Theorem 5.8

To show Theorem 5.6, we need the following three lemmas.

Lemma B.20.

Lemma B.21.

Lemma B.22.

Proof of Lemma B.20.

According to Lemma B.3

with for any . Then by Markov inequality,

Denote and . Then,

When and , it is easy to check that

Under the event ,

where we have used the condition that . The conclusion of the lemma directly follows the result above. ∎

Proof of Lemma B.21.

Proof of Lemma B.22.

By Hölder’s inequality,

where . Replace by , and we have

where , and are the same constants in Lemma B.21. ∎

Now we can show Theorem 5.6.

Proof of Theorem 5.6.

Define

Then Lemma B.22 implies that

for all . Note that

For the first term on the right hand side of the above equality, we have

The term can be bounded by

The proof is complete by choosing . ∎

Proof of Theorem 5.7.

In the end of this part, we will show Theorem 5.8, which directly implies Theorem 3.5. We want to check conditions (C1)-(C3) for . For this aim, we establish the following lemmas.

Lemma B.23.

The marginal sampling process of in the prior for piecewise constant model can be regarded as following procedure:

-

•

Sample with

(97) -

•

Conditioning on , sample change points uniformly from . In the other words, we uniformly sample a subset of size with probability ;

-

•

Conditioning on , sample according to for all and for all .

Moreover, when (26) is satisfied,

Proof.

First of all, the density of marginal prior on can be written as

where above is the set of label such that and is defined in (97), which implies the marginal sampling process of can be written as the procedure above.

Then the condition (26) indicates that

which implies that

When , , it is easy to see that as is decreasing with respect to . Hence, we have

∎

Lemma B.24.

Suppose . For some integer , define

| (98) |

Then for any with , we have

Proof.

According to the definition,

Using the identity , we get

Since , we have

where . Then,

where , . Then a standard chi-squared bound gives

The proof is complete. ∎

We want check conditions (C1)-(C3) with respect to . This step can be split into the following two lemmas.

Lemma B.26.

Proof of Lemma B.25.

Proof of Lemma B.26.

We first verify condition (C3). Note that for any ,

Consider the set , then for ,

and

where and is given in (26). Therefore, condition (C3) is satisfied.

Now we check condition (C4**) for both and . When , assume and with . Since , we must have . Define

Then we define

Then choose . As

we have . For any ,

Moreover,

Thus, condition (C4**) is satisfied for .

When . Choose , where

Obviously, we have and for any , we have shown that

On the other hand, suppose and , we have

Thus, condition (C4**) is satisfied for . The proof is complete.

∎

B.11 Proof of Theorem A.2

References

- Alquier and Ridgway [2017] Pierre Alquier and James Ridgway. Concentration of tempered posteriors and of their variational approximations. arXiv preprint arXiv:1706.09293, 2017.

- Barron et al. [1999] Andrew Barron, Mark J Schervish, and Larry Wasserman. The consistency of posterior distributions in nonparametric problems. The Annals of Statistics, 27(2):536–561, 1999.

- Barron [1988] Andrew R Barron. The exponential convergence of posterior probabilities with implications for Bayes estimators of density functions. Department of Statistics, University of Illinois, 1988.

- Bickel et al. [2013] Peter Bickel, David Choi, Xiangyu Chang, and Hai Zhang. Asymptotic normality of maximum likelihood and its variational approximation for stochastic blockmodels. The Annals of Statistics, 41(4):1922–1943, 2013.