Stochastic Volatily Models using Hamiltonian Monte Carlo Methods and Stan

Abstract

This paper presents a study using the Bayesian approach in stochastic volatility models for modeling financial time series, using Hamiltonian Monte Carlo methods (HMC). We propose the use of other distributions for the errors in the observation equation of stochastic volatiliy models, besides the Gaussian distribution, to address problems as heavy tails and asymmetry in the returns. Moreover, we use recently developed information criteria WAIC and LOO that approximate the cross-validation methodology, to perform the selection of models. Throughout this work, we study the quality of the HMC methods through examples, simulation studies and applications to real datasets.

Key words: Bayesian methods, Stochastic Volatility Models, Hamiltonian Monte Carlo, WAIC.

1 Introduction

Stochastic volatility (SV) models have been around for decades now and succesfully applied to study the volatility which is characteristic in financial markets. A number of estimation methods have been proposed to estimate these models, but Markov Chain Monte Carlo (MCMC) are usually considered one of the most efficient methods. Great advances have been made recently with the Hamiltonian Monte Carlo algorithms (HMC, see for example Neal (2011)) for the estimation of latent variable models. The practitioner, usually interested in fast answers, has benefited from these recent methodological developements and most importantly from availability of computational programs.

The computations in this paper were implemented using open-source statistical software. In particular, we used the R environment (R Development Core Team (2015)) and recently released R packages which can efficiently estimate stochastic volatility (SV) models. The rstan package is an interface to the open-source Bayesian software Stan (Stan Development Team (2014)) and the stochvol package was proposed by Kastner (2016) which jointly samples all instantaneous volatilities “all without a loop” (AWOL), a technique discussed in more detail in McCausland et al. (2011) and Kastner and Frühwirth-Schnatter (2014). The stochvol package was designed to reduce serial correlations of the MCMC draws significantly and uses the auxiliary finite mixture approximation of the errors as described in Kim et al. (1998) and Omori et al. (2007). As such, it is crafted to provide efficient estimation of SV models with normal errors.

Stan on the other hand is actually a language designed for Bayesian analysis with continuous parameter spaces and can be run from R. Also, Stan uses Hamiltonian Monte Carlo (HMC) methods coupled with the no-U-turn sampler (NUTS) which are designed to improve speed, stability and scalability compared to standard MCMC as Metropolis-Hastings and the Gibbs sampler. In particular, HMC methods are also designed to reduce serial correlations of the MCMC draws and usually the chains reach the stationary distribution with fewer iterations.

In this paper, we first compare the rstan and stochvol packages to estimate SV model with normal errors. Being more flexible than stochvol in terms of likelihood and prior specifications checking whether Stan is at least as efficient provides a useful information for the applied researcher. We then move to explore Stan facilities to specify more flexible SV models with heavy tailed distributions for the errors. These models are subsequently compared in terms of recently proposed information criteria, namely the Watanabe information criterion (WAIC, Watanabe (2010)) and the Approximate Leave-One-Out Cross-Validation (LOO, Vehtari et al. (2015)).

The rest of the paper is structured as follows. In Section 2 SV models are briefly reviewed and the prior distributions are described. The methodology for estimating and comparing models is also described here. These methods are assessed through a simulation study in Section 3 and through the statistical analysis of real time series in section 4. Some final comments are given in Section 5.

2 Model Description and Methods

The canonical form of the SV model as given in Kim et al. (1998) is defined as,

| (1) | ||||

| (2) | ||||

where is a stationary process describing the log-volatility at time , is a sequence of independent and identicaly distributed random variables with mean zero and variance one is a sequence such that , with and uncorrelated for all . Then is the level of log-volatilities and is the persistence parameter. The parameter is playing the role of a scale factor.

In its original formulation introduced by Taylor (1982), is assumed to follow a standard normal distribution. However, several other error distributions have been proposed as many empirical studies indicate that the canonical model does not account for the amount of kurtosis usually observed in most financial time series returns. Therefore, we also consider other (heavy tailed) distributions for the error term in the observation equation (1) which are described below.

The Exponential Power distribution (or generalized error distribution, GED) with mean zero and variance one whose density function is given by,

| (3) |

In this formulation, and is the shape parameter. It is not difficult to see that the double exponential or Laplace distribution is obtained for and the standard normal distribution for . Also, the kurtosis is given by and then leads to heavy tail distributions.

The -Student distribution with degrees of feedom and density function given by,

| (4) |

when this approaches the density of a standard normal distribution.

Additionaly, we consider a standardized Skew-Normal distribution with shape parameter and density function given by,

| (5) |

where . This distribution is skewed to the left for and right skewed for thus taking into account another empirical evidence that many returns present a slight skewness. The standard normal is a particular case for .

To complete the model specification under the Bayesian paradigm we define independent prior distributions for the parameters and . As in Kim et al. (1998) the prior for is specified by setting where so that,

| (6) |

where is the Beta function. The support of under this distribution is the interval and stationarity of the log-volatility process is then guaranteed. Kim et al. (1998) recommended using and which implies a prior expectation of equal to 0.86 with a prior standard deviation of 0.11 thus asigning very little probability mass for values . Many authors have chosen to work with this prior (e.g. Girolami and Calderhead (2011), Kastner and Frühwirth-Schnatter (2014), Zevallos et al. (2016)) as in practice the parameter is commonly estimated close to 1. Also, for identifiability the model should be configured with either or . We chose to work with in which case we asign the prior distribution .

Finally, the prior distribution for the parameters was chosen as in Kastner (2016) for comparison purposes, i.e.

| (7) |

also noting that this prior is less influent when the true volatility of log-volatility is small as it does not bound away from zero a priori.

We now turn to the prior distributions on the parameter which depends on the distribution adopted for the error terms and is assumed independent of and . For GED errors we follow Zevallos et al. (2016) and propose the prior for Inv-(10,0.05) while for Student- errors, following Watanabe and Asai (2001), we consider the truncated exponential density,

and zero otherwise, as the prior for . However, differently from Watanabe and Asai (2001) we specified . For the Skew-Normal distribution we used .

2.1 Model Comparison

Choosing a model that best represents the data dynamics from a set of candidate models is challenging in any statistical research. Despite recent advances in computing the marginal likelihood and the associated Bayes factor (e.g. Friel and Pettit (2008) and Bauwens and Rombouts (2012)), this remains a difficult and computationaly expensive task in practice. This motivates us to base model comparison on information criteria which implementation usually leads to a small extra computational cost.

A popular choice since the seminal work of Spiegelhalter et al. (2002) is the Deviance Information Criterion (DIC). This criterion has been previously used for comparing a number of SV models (e.g. Berg et al. (2004), Abanto-Valle et al. (2010)) and is defined as,

where is the vector of parameters in the model, and is a penalizing term given by,

Then, given simulations from the posterior distribution of , can be approximated as,

| (8) |

Recent studies however have cautioned against indiscriminate use of DIC as a comparison device for latent variable models (e.g. Celeux et al. (2006), Miller (2009)). So, in this paper we propose to compare SV models by looking at the accuracy of competing models in predicting out-of-sample observations. This is the idea behind the so called Watanabe information criterion (WAIC, Watanabe (2013), Vehtari et al. (2015)). WAIC does not depend on Fisher asymtotic theory and consequently does not assume that the posterior distribution converges to a single point, thus providing an attractive alternative to compare hierarchical models. It can be interpreted as a computationally convenient approximation to cross-validation and is defined as,

| (9) |

where penalizes for the effective number of parameters and is the log pointwise predictive density as defined in Vehtari et al. (2015) with each term in the sum given by,

In practice, given simulated values of from its posterior distribution, the two terms in (9) are estimated as,

and

where denotes the sample variances of , . The WAIC is then defined as,

or equivalently as to be on the deviance scale. Watanabe (2010) showed that under certain regularity conditions, the WAIC is asymptotically equivalent to leave-one-out cross-validation (see also, Gelman et al. (2014)).

The log pointwise predictive density can also be estimated via approximate leave-one-out cross-validation (LOO) as,

where denotes the data vector with the th observation deleted. Vehtari et al. (2017) introduced an efficient approach to compute LOO using Pareto-smoothed importance sampling (PSIS) for regularizing importance weights. The computations are implemented in the R packaged loo which we use here together with Stan to perform model comparison. An interesting byproduct of this approach is that approximate standard errors for estimated predictive errors are also obtained.

3 Simulations

In this section, a simulation study is carried out to compare the two sampling approaches in stochvol and Stan to estimate SV models with normal errors. We generated replications of time series with , and observations from the model described in (1)-(2) with for identifiability. The model parameters were fixed as follows, , and .

The prior distributions assumed were as described in (6) for the parameter , and the prior in (7) was asigned for with . These were the prior distributions used in Kastner (2016) to describe the stochvol package and are adopted here in both sampling methods for comparison purposes. Then, for each series we simulated 10,000 MCMC samples with the first 5,000 discarded as burn-in. The estimation performance was evaluated considering two criteria, the bias and the square root of the mean square error (smse), defined as,

where is the point estimate of parameter in the -th replication, .

The results for and combinations of and are shown in Tables 1, 2, 3 and 4. The first two tables refer to a very high degree of persistence in the log-volatility process (). In Table 1 for , we obtained good results in terms of bias and smse for all parameters with HMC doing better for larger sample sizes. For series with smaller sizes () the results are close for both methods (slightly better for stochvol) except for the parameter which shows a much smaller bias when using stochvol. In Table 2 (), we notice much smaller values for bias and smse for both methods, but with HMC doing better overall.

[ Table 1 around here ]

[ Table 2 around here ]

Tables 3 and 4 refer to a log-volatility process with a smaller persistence (). From the results in these tables we first notice that both methods provide better estimates compared to the case with higher persistence and this is in general expected. However, for all sample sizes and parameters the HMC method using Stan is doing even better compared to stochvol. Also, the resulting Markov chains using HMC (not shown to save space) in general present lower autocorrelations thus mixing better.

[ Table 3 around here ]

[ Table 4 around here ]

4 Applications

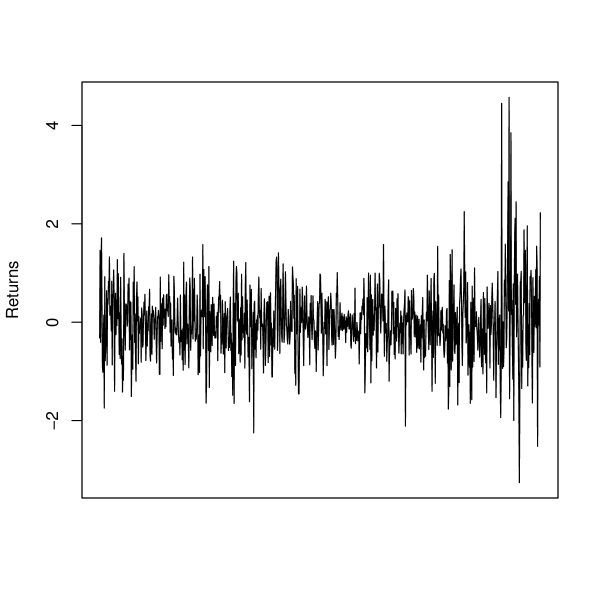

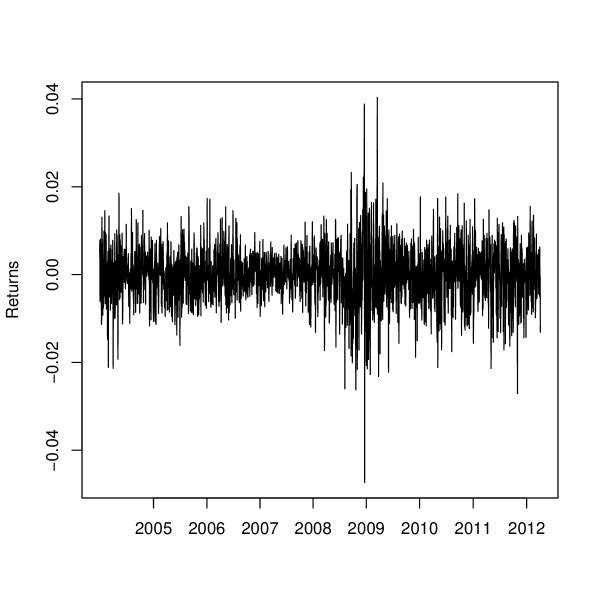

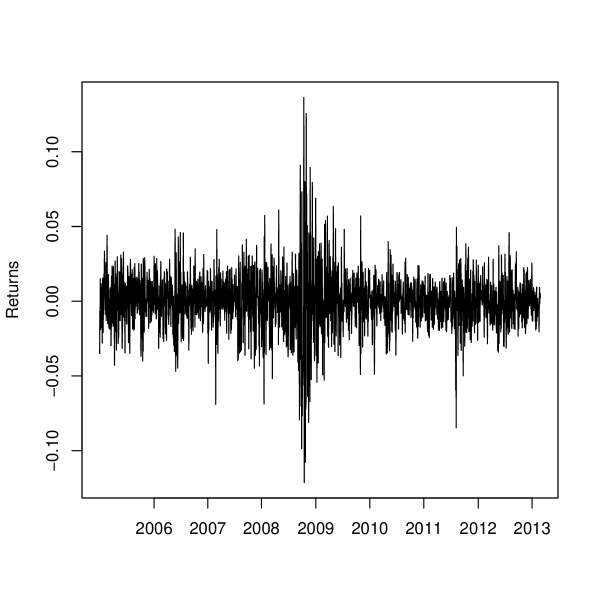

In this section we illustrate the use of HMC methods via Stan for the Bayesian estimation of SV models with different distributions for the observation error . The illustration uses two exchange rate time series data: the Pound/Dollar (£/USD) and the Euro/Dollar (EUR/USD), plus the stock index in São Paulo (IBOVESPA). The time series are the daily continuously compounded returns in percentage, defined as where is the price at time . The £/USD series of daily returns in percentage covers the period from 1/10/81 to 28/6/85 and was studied before by for example Harvey et al. (1994) and Zevallos et al. (2016). The series EUR/USD covers the period from 03/01/2004 to 04/04/2012 and is available in the stochvol package. Finally, the series IBOVESPA covers the period from 03/01/2005 to 28/02/2013.

The £/USD, EUR/USD and IBOVESPA time series have 945, 2120 and 2016 observations respectively. The series are depicted in Figures 1, 2 and 3 and Table 5 consigns some descriptive statistics for these series. From this table we notice high kurtosis for all series and a little skewness for the two exchange rate series. Finally, the autocorrelation function (not shown) indicated no serial correlation in the three series.

[ Table 5 around here ]

[ Figure 1 around here ]

[ Figure 2 around here ]

[ Figure 3 around here ]

For each time series, the SV model was estimated using demeaned returns and considering the four different distributions for the errors: the Gaussian, the GED distribution with parameter , the Student’s distribution with degrees of freedom and the Skew-Normal distribution. We considered prior distributions as described in (6) for the parameter , and the Gamma prior (7) was asigned for with hyperparameter . For the parameter in the GED, -Student and Skew-Normal the prior distributions are Inv-(10,0.05), truncated exponential and respectively as described in the end of Section 2.

Then, for each time series we drew 10,000 MCMC samples for the parameters and volatilities using Stan and NUTS where the first 5,000 were discarded as burn-in. To compare models with different error distributions we used the information criteria described in Section (LABEL:CritSel). The results are reported in Tables 6 and 7.

According to Table 6, we can see that for the £/USD series the information criteria have similar values for the Gaussian and Skew-Normal distributions. DIC and LOO show slightly lower values for the Gaussian model although our descriptive analysis has shown high kurtosis and slight skewness for this series. For the EUR/USD returns the SV model with -Student and GED errors show better results in terms of all criteria with DIC selecting the -Student while WAIC and LOO have lower values for the GED. Finally, for the IBOVESPA series all criteria indicate Gaussian and Skew-Normal errors as most appropriate SV models.

[ Table 6 around here ]

[ Table 7 around here ]

The parameter estimates (posterior mean and standard deviation) obtained for the three series are shown in 7. We notice that the standard deviation of the parameter for the EUR/USD and IBOVESPA are quite smaller than for the £/USD series and the persistence is quite high for all series indicating that the volatility in the previous day tends to have an impact on the current exchange rates prices. We also notice that estimates for the parameter in the Skew-Normal distribution were close to zero for the three series with 0.95 credible intervals given by , and . However, for the £/USD and IBOVESPA series this models presented good results in terms of information criteria.

4.1 Sensitivity to the Choice of Prior

In this section we investigate whether the prior choice for the parameter can influence the results for model comparison. We estimated the SV model for the £/USD series considering the prior distributions described in (10), (11) and (12) below,

| (10) | ||||

| (11) | ||||

| (12) |

The sensitivity was evaluated considering the information criteria for model comparison and checking if the model rankings changed with the choice of prior. In this estimation we simulated 5,000 samples from the posterior distribution using Stan from which 50% were discarded as burn-in resulting in a final sample of 2500 values. The four distributions for the error term in the SV model were considered and we repeated this procedure twice.

The results appear in Table 8 where we notice that the choice of the prior distribution for does not seem to influence model selection for this series. So, according to these criteria the Gaussian and Skew-Normal models are still prefered. It is worth noting that even with only 2500 samples used in the computations the HMC method converged rather quickly and the values of the criteria were similar to the ones obtained with 5000 effective samples (after burn-in).

[ Table 8 around here ]

5 Conclusions

In this paper we discuss and compare the Bayesian estimation approach in stochastic volatility models with heavy tailed and possibly asymmetric distributions for the error term. We employed both traditional Markov chain Monte Carlo and Hamiltonian Monte Carlo methods to obtain approximations to the posterior marginal distributions of interest.

In particular we compared very fast algorithms which implementation is freely available in R packages, namely the stochvol package and the rstan package (an interface with the Stan package). These methods were assessed through a simulation study and the Stan package was also tested with real time series of returns. Overall, we found evidence that Stan is slightly more efficient for estimation with the advantage of being able to deal with different model structures and distributions. We hope that our findings are useful to the practitioners.

Acknowledgments

Ricardo Ehlers received support from São Paulo Research Foundation (FAPESP) - Brazil, under grant number 2016/21137-2.

References

- Abanto-Valle et al. (2010) C. A. Abanto-Valle, D. Bandyopadhyay, V. H. Lachos, and I. Enriquez. Robust Bayesian analysis of heavy-tailed stochastic volatility models using scale mixtures of normal distributions. Computational Statistics and Data Analysis, 54(12):2883–2898, 2010.

- Bauwens and Rombouts (2012) L. Bauwens and J. V. K. Rombouts. On marginal likelihood computation in change-point models. Computational Statististics and Data Analysis, 56(11):3415–3429, 2012.

- Berg et al. (2004) A. Berg, R. Meyer, and J. Yu. Deviance information criterion for comparing stochastic volatility models. Journal of Business and Economics Statistics, 22(1):107–120, January 2004.

- Celeux et al. (2006) G. Celeux, F. Forbes, C. P. Robert, and D. M. Titterington. Deviance information criteria for missing data models. Bayesian Analysis, 1:651–674, 2006.

- Friel and Pettit (2008) N. Friel and A. N. Pettit. Marginal likelihood estimation via power posteriors. Journal of the Royal Statistical Society, B, 70:589–607, 2008.

- Gelman et al. (2014) A. Gelman, J. Hwang, and A. Vehtari. Understanding predictive information criteria for bayesian models. Statistics and Computing, 24(6):997–1016, 2014.

- Girolami and Calderhead (2011) M. Girolami and B. Calderhead. Riemann manifold Langevin and Hamiltonian Monte Carlo methods. Journal of the Royal Statistical Society B, 73:123–214, 2011.

- Harvey et al. (1994) A. C. Harvey, E. Ruiz, and N Shephard. Multivariate stochastic variance models. Reviews of Economic Studies, 61:247–264, 1994.

- Kastner (2016) Gregor Kastner. Dealing with stochastic volatility in time series using the R package stochvol. Journal of Statistical Software, 69(5):1–30, 2016.

- Kastner and Frühwirth-Schnatter (2014) Gregor Kastner and Sylvia Frühwirth-Schnatter. Ancillarity-sufficiency interweaving strategy (asis) for boosting mcmc estimation of stochastic volatility models. Computational Statistics & Data Analysis, 76:408–423, 2014.

- Kim et al. (1998) S. Kim, N. Shepard, and S. Chib. Stochastic volatility: likelihood inference comparison with ARCH models. Review of Economic Studies, 65:361–393, 1998.

- McCausland et al. (2011) William J McCausland, Shirley Miller, and Denis Pelletier. Simulation smoothing for state–space models: A computational efficiency analysis. Computational Statistics & Data Analysis, 55(1):199–212, 2011.

- Miller (2009) R. G. Miller. Comparison of hierarchical Bayesian models for overdispersed count data using DIC and Bayes factors. Biometrics, 65(3):962–969, 2009.

- Neal (2011) R. M. Neal. MCMC using Hamiltonian dynamics. In Handbook of Markov chain Monte Carlo, pages 113–162. Boca Raton: Chapman and Hall-CRC Press, 2011.

- Omori et al. (2007) Y. Omori, S. Chib, N. Shephard, and J. Nakajima. Stochastic volatility with leverage: Fast and efficient likelihood inference. Journal of Econometrics, 140(2):425–449, 2007.

- R Development Core Team (2015) R Development Core Team. R: A language and environment for statistical computing. R Foundation for Statistical Computing, Vienna, Austria, 2015.

- Spiegelhalter et al. (2002) David J. Spiegelhalter, Nicola G. Best, Bradley P. Carlin, and Angelika Van Der Linde. Bayesian measures of model complexity and fit. Journal of the Royal Statistical Society: Series B (Statistical Methodology), 64(4):583–639, 2002.

- Stan Development Team (2014) Stan Development Team. Rstan: the r interface to stan, version 2.10.1, 2014. URL http://mc-stan.org/rstan.html.

- Taylor (1982) S. Taylor. Financial returns modelled by the product of two stochastic processes-a study of the daily sugar prices 1961-75. In O. Anderson, editor, Time Series Analysis: Theory and Practice, volume 1, pages 203–226. 1982.

- Vehtari et al. (2015) A. Vehtari, A. Gelman, and J. Gabry. Practical Bayesian model evaluation using leave-one-out cross-validation and WAIC. ArXiv e-prints, July 2015.

- Vehtari et al. (2017) Aki Vehtari, Andrew Gelman, and Jonah Gabry. Practical bayesian model evaluation using leave-one-out cross-validation and waic. Statistics and Computing, 27(5):1413–1432, 2017.

- Watanabe (2013) S. Watanabe. A widely applicable Bayesian information criterion. Journal of Machine Learning Research, 14:867–897, 2013.

- Watanabe (2010) Sumio Watanabe. Asymptotic equivalence of Bayes cross validation and widely applicable information criterion in singular learning theory. Journal of Machine Learning Research, 11:3571–3594, 2010.

- Watanabe and Asai (2001) T. Watanabe and M. Asai. Stochastic volatility models with heavy-tailed distributions: A Bayesian analysis. Technical report, Discussion paper 2001-E-17, Institute for Monetary and Economic Studies, Bank of Japan, 2001.

- Zevallos et al. (2016) M. Zevallos, L. Gasco, and R. S. Ehlers. Riemann manifold Langevin methods on stochastic volatility estimation. Communications in Statistics: Simulation and Computation, 2016. To appear.

| T | Method | ||||||

|---|---|---|---|---|---|---|---|

| Bias | smse | Bias | smse | Bias | smse | ||

| 500 | Stochvol | 0.213 | 0.474 | 0.020 | 0.030 | -0.137 | 0.121 |

| HMC | 0.491 | 0.491 | 0.068 | 0.066 | -0.117 | 0.118 | |

| 1000 | Stochvol | 0.223 | 0.415 | 0.007 | 0.011 | -0.019 | 0.031 |

| HMC | 0.055 | 0.056 | 0.002 | 0.002 | -0.006 | 0.007 | |

| 1500 | Stochvol | 0.129 | 0.366 | 0.004 | 0.007 | -0.012 | 0.024 |

| HMC | 0.120 | 0.267 | 0.003 | 0.007 | -0.007 | 0.021 | |

| T | Method | ||||||

|---|---|---|---|---|---|---|---|

| Bias | smse | Bias | smse | Bias | smse | ||

| 500 | Stochvol | 0.063 | 0.218 | 0.106 | 0.121 | -0.071 | 0.082 |

| HMC | 0.090 | 0.093 | 0.132 | 0.133 | 0.023 | 0.029 | |

| 1000 | Stochvol | 0.041 | 0.146 | 0.042 | 0.064 | -0.039 | 0.049 |

| HMC | 0.018 | 0.134 | -0.001 | 0.002 | -0.010 | 0.012 | |

| 1500 | Stochvol | 0.017 | 0.122 | 0.027 | 0.047 | -0.027 | 0.037 |

| HMC | 0.017 | 0.123 | 0.018 | 0.034 | -0.015 | 0.026 | |

| T | Method | ||||||

|---|---|---|---|---|---|---|---|

| Bias | smse | Bias | smse | Bias | smse | ||

| 500 | Stochvol | 0.049 | 0.151 | 0.050 | 0.066 | -0.042 | 0.059 |

| HMC | 0.042 | 0.150 | 0.030 | 0.049 | 0.000 | 0.051 | |

| 1000 | Stochvol | 0.022 | 0.107 | 0.025 | 0.045 | -0.022 | 0.044 |

| HMC | 0.019 | 0.106 | 0.014 | 0.035 | -0.003 | 0.038 | |

| 1500 | Stochvol | 0.027 | 0.083 | 0.018 | 0.030 | -0.023 | 0.042 |

| HMC | 0.024 | 0.082 | 0.011 | 0.024 | -0.011 | 0.035 | |

| T | Method | ||||||

|---|---|---|---|---|---|---|---|

| Bias | smse | Bias | smse | Bias | smse | ||

| 500 | Stochvol | 0.025 | 0.079 | 0.119 | 0.124 | -0.050 | 0.060 |

| HMC | 0.011 | 0.076 | 0.086 | 0.091 | 0.009 | 0.037 | |

| 1000 | Stochvol | 0.008 | 0.059 | 0.118 | 0.123 | -0.046 | 0.060 |

| HMC | -0.001 | 0.057 | 0.087 | 0.092 | 0.001 | 0.043 | |

| 1500 | Stochvol | 0.005 | 0.042 | 0.116 | 0.122 | -0.037 | 0.049 |

| HMC | -0.001 | 0.044 | 0.087 | 0.097 | -0.006 | 0.037 | |

| Series | Mean | Std Dev | Skewness | Kurtosis | |

|---|---|---|---|---|---|

| £/USD | 945 | -0.03530 | 0.7111 | 0.60 | 7.85 |

| EUR/USD | 2120 | 0.00001 | 0.0066 | -0.15 | 6.18 |

| IBOVESPA | 2016 | 0.00041 | 0.0188 | -0.04 | 8.89 |

| Series | Dist. | DIC | WAIC | SEwaic | LOO | SEloo |

|---|---|---|---|---|---|---|

| £/USD | Gaussian | 1802.7 | 1807.4 | 53.5 | 1811.8 | 54.3 |

| t-Student | 1805.3 | 1812.8 | 52.8 | 1813.5 | 52.9 | |

| Skew-Normal | 1803.1 | 1807.4 | 53.3 | 1812.2 | 54.2 | |

| GED | 1810.6 | 1811.3 | 53.2 | 1814.0 | 53.7 | |

| EUR/USD | Gaussian | -15647.9 | -15640.2 | 77.0 | -15638.2 | 77.3 |

| t-Student | -15664.9 | -15647.8 | 76.4 | -15647.4 | 76.4 | |

| Skew-Normal | -15646.7 | -15638.9 | 77.2 | -15636.6 | 77.5 | |

| GED | -15651.2 | -15650.9 | 76.6 | -15650.2 | 76.7 | |

| IBOVESPA | Gaussian | -10986.7 | -10983.7 | 74.9 | -10975.9 | 75.6 |

| t-Student | -10974.6 | -10970.3 | 75.7 | -10968.0 | 75.9 | |

| Skew-Normal | -10984.3 | -10981.0 | 75.1 | -10973.7 | 75.8 | |

| GED | -10977.3 | -10979.1 | 75.4 | -10974.4 | 75.8 |

. Series Dist. £/USD Gaussian - 9.580 (1.014) 0.999 (0.000) 0.137 (0.024) t-Student - 9.591 (1.046) 0.999 (0.000) 0.113 (0.024) 12.143 (3.581) Skew-Normal - 9.606 (1.026) 0.999 (0.000) 0.141 (0.026) -0.038 (0.042) GED - 9.592 (1.043) 0.999 (0.000) 0.123 (0.025) 1.763 (0.141) EUR/USD Gaussian -10.197 (0.288) 0.994 (0.002) 0.065 (0.010) t-Student -10.321 (0.289) 0.994 (0.002) 0.059 (0.010) 14.090 (3.393) Skew-Normal -10.199 (0.290) 0.994 (0.002) 0.065 (0.010) 0.016 (0.027) GED -10.175 (0.312) 0.995 (0.002) 0.055 (0.010) 1.681 (0.082) IBOVESPA Gaussian - 8.416 (0.199) 0.980 (0.006) 0.148 (0.019) t-Student - 8.546 (0.236) 0.984 (0.005) 0.128 (0.017) 16.202 (4.229) Skew-Normal - 8.416 (0.211) 0.981 (0.006) 0.145 (0.020) 0.020 (0.028) GED - 8.417 (0.216) 0.983 (0.005) 0.132 (0.018) 1.801 (0.107)

| Prior for | Dist. | DIC | WAIC | EPwaic | LOO | EPloo |

|---|---|---|---|---|---|---|

| Gaussian | 1805.0 | 1810.3 | 53.8 | 1811.0 | 54.5 | |

| 1801.4 | 1805.8 | 53.4 | 1809.6 | 54.0 | ||

| -Student | 1804.5 | 1811.5 | 52.8 | 1812.3 | 52.9 | |

| 1805.7 | 1813.4 | 52.8 | 1814.2 | 52.9 | ||

| Skew-Normal | 1803.7 | 1808.3 | 53.4 | 1812.0 | 54.0 | |

| 1803.4 | 1807.7 | 53.3 | 1811.4 | 53.9 | ||

| GED | 1809.7 | 1810.4 | 53.2 | 1813.2 | 53.0 | |

| 1812.6 | 1813.3 | 53.2 | 1815.5 | 53.6 | ||

| Gaussian | 1800.9 | 1805.0 | 53.1 | 1809.3 | 53.8 | |

| 1801.7 | 1806.8 | 53.4 | 1811.1 | 54.1 | ||

| -Student | 1805.3 | 1812.8 | 52.8 | 1813.4 | 52.9 | |

| 1804.0 | 1810.7 | 52.9 | 1811.5 | 52.9 | ||

| Skew-Normal | 1804.0 | 1808.8 | 53.5 | 1812.7 | 54.2 | |

| 1803.9 | 1808.2 | 53.3 | 1812.1 | 54.0 | ||

| GED | 1809.0 | 1809.5 | 53.0 | 1812.0 | 53.4 | |

| 1811.4 | 1812.2 | 53.2 | 1815.0 | 53.7 | ||

| Gaussian | 1803.4 | 1808.0 | 53.4 | 1811.7 | 54.0 | |

| 1804.2 | 1809.0 | 53.5 | 1813.0 | 54.3 | ||

| -Student | 1805.8 | 1813.5 | 52.8 | 1814.1 | 52.9 | |

| 1807.3 | 1815.1 | 52.9 | 1815.7 | 53.0 | ||

| Skew-Normal | 1804.2 | 1808.5 | 53.4 | 1811.6 | 53.9 | |

| 1802.9 | 1807.6 | 53.3 | 1811.2 | 54.0 | ||

| GED | 1811.3 | 1812.0 | 53.2 | 1813.9 | 53.5 | |

| 1814.8 | 1815.5 | 53.3 | 1817.0 | 53.6 |