Quantum Bounds for Option Prices

Abstract

Option pricing is the most elemental challenge of mathematical finance. Knowledge of the prices of options at every strike is equivalent to knowing the entire pricing distribution for a security, as derivatives contingent on the security can be replicated using options. The available data may be insufficient to determine this distribution precisely, however, and the question arises: What are the bounds for the option price at a specified strike, given the market-implied constraints?

Positivity of the price map imposed by the principle of no-arbitrage is here utilised, via the Gelfand-Naimark-Segal construction, to transform the problem into the domain of operator algebras. Optimisation in this larger context is essentially geometric, and the outcome is simultaneously super-optimal for all commutative subalgebras.

This generates an upper bound for the price of a basket option. With

innovative decomposition of the assets in the basket, the result is used to

create converging families of price bounds for vanilla options, interpolate

the volatility smile, price options on cross FX rates, and analyse the

relationships between swaption and caplet prices.

Keywords: Option pricing; volatility smile; FX options; swaptions and caplets; no-arbitrage principle; quantum probability; operator algebras; Gelfand-Naimark-Segal construction.

††Author email: p.mccloud@ucl.ac.uk††Available on arXiv: arxiv.org/abs/1712.01385††Available on SSRN: ssrn.com/abstract=30825611 Introduction

The incomplete market provides prices for a subset of the full universe of securities, which constrains, but does not determine, the prices of securities outside the mark-to-market subspace. In some cases, the available data imposes model-independent limits on the possible prices for a security that are sufficiently constrained as to provide useful guidelines for pricing. These limits are the extremal valuations from the set of arbitrage-free pricing models that satisfy the market constraints.

In this article, families of bounds for option prices are constructed from finite-dimensional covariance matrices extracted from the price distribution of the underlying assets. The approach allows for the arbitrary decomposition of assets into sub-assets contingent on market events, a property that is exploited to refine the bounds as more market information is incorporated. The option price bound is then used to analyse problems such as options on portfolios, interpolation of the Black-Scholes [2] implied volatility smile, the pricing of options on cross rates in the foreign exchange market, and the relationships between swaption and caplet prices.

Options on a security are a rich source of information regarding the pricing measure, as the marginal distribution for the security is fully determined from the prices of vanilla options. For the underlying security , integration by parts generates an expansion for the derived security in terms of the vanilla put options and call options :

| (1) | ||||

Setting to be the price of the underlying security and taking the expectation in the pricing measure leads to the Carr-Madan replication formula [6] for the price of the derived security:

| (2) | ||||

If the price of the derived security is observed in the market, this formula constrains the prices of vanilla options on the underlying security. The challenge is to derive the bound for the price of the vanilla option subject to the constraints imposed by the market prices of a finite collection of derived securities. This bound should converge to a unique price for the vanilla option as more market information is included.

The general problem considered here is the determination of bounds for the price of a basket option:

| (3) |

for the assets , defined to be positive securities, and the quantities , which may be positive or negative. The main theoretical result of this article derives bounds for these options from the matrix of moments:

| (4) |

extracted from the price distribution. The diagonal elements of this matrix are the prices of the assets, and the remaining elements are parametrised by the volatilities and correlations of the square-roots of the assets. This furnishes the bound with a convenient and intuitive parametrisation.

The method exploits the Gelfand-Naimark-Segal (GNS) construction [9, 22] to transform the problem into one involving operator algebras, mirroring techniques applied in the study of quantum systems. This foundational result from the theory of operator algebras is used to generate an inner product on the securities and :

| (5) |

thereby defining a Hilbert space structure on the securities. Aside from technical details, the only properties required to validate this construction are linearity and positivity of the price map, properties that translate to the concepts of replicability and absence of arbitrage in the finance application. The securities are represented as operators on the Hilbert space – the security is represented as the operator whose action on the securities is defined by:

| (6) |

Acting via pointwise multiplication, this representation identifies the securities with the diagonal operators on the Hilbert space.

Optimisation within the wider context of all operators is essentially geometric, allowing for the simple derivation of bounds for option prices. The digital functions that indicate exercise in classical probability are generalised as projections in quantum probability, and the central theoretical result is the following observation for projections on a Hilbert space.

Theorem 1

For the vectors and the scalars , the supremum of the valuation:

| (7) |

over all projections is given by the sum of the positive eigenvalues of a finite-dimensional self-adjoint matrix constructed from the inner products and the scalars .

From a practical perspective, the important element of this theorem is the construction of the matrix , which turns out to be a simple application of standard matrix methods. The GNS construction translates this theorem to the following result for options in arbitrage-free pricing models.

Theorem 2

For the assets and the quantities , the option valuation:

| (8) |

is bounded above by the sum of the positive eigenvalues of a finite-dimensional self-adjoint matrix constructed from the valuations and the quantities .

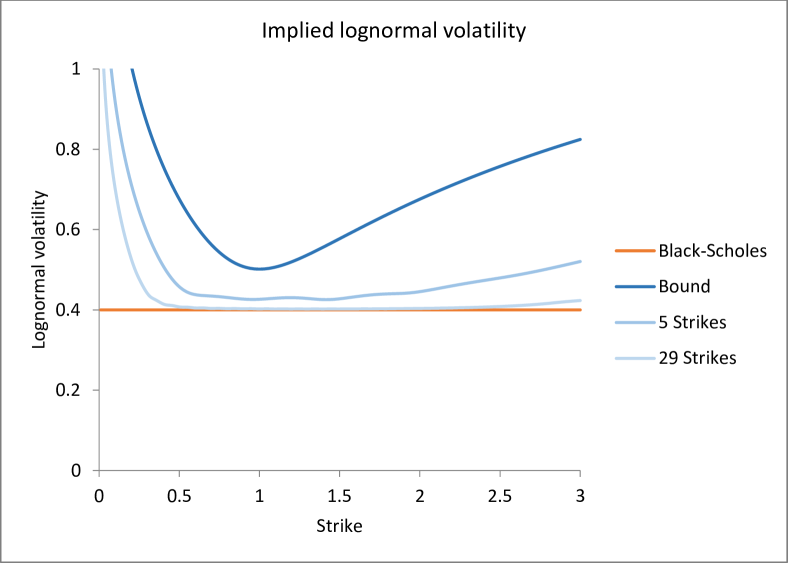

Using creative decompositions of the assets, the bound in this theorem is arbitrarily refined by extracting more information from the market, generating families of volatility smiles that converge monotonically to the market-implied smile.

By relying only on linearity and positivity of the map from security to price, this approach is perfectly adapted to the economic principles of replicability and the absence of arbitrage, so much so that the original works by Gelfand and Naimark [9] and Segal [22] could be considered as early results in the development of mathematical finance. These results themselves emerged from the matrix approach to quantum mechanics pioneered by Born, Jordan and Heisenberg [4, 3, 10], through its formalisation in the work of von Neumann [17, 18] and others, and are now a staple in the study of operator algebras (see the standard texts [8, 12, 13]).

The precise correspondence with the principle of no-arbitrage encapsulated in the GNS construction makes operator algebras the natural platform for mathematical finance. The development is more commonly framed in the familiar language of classical probability by taking the Arrow-Debreu securities [1] as a basis for the market. While this approach is largely unquestioned in the domain of mathematical finance, its validity in the modelling of uncertainty has been the subject of debate in wider economics circles, as this quote from Keynes [14] suggests.

By “uncertain” knowledge, let me explain, I do not mean merely to distinguish what is known for certain from what is only probable. … About these matters there is no scientific basis on which to form any calculable probability whatever. We simply do not know. Nevertheless, the necessity for action and for decision compels us as practical men to do our best to overlook this awkward fact and to behave exactly as we should if we had behind us a good Benthamite calculation of a series of prospective advantages and disadvantages, each multiplied by its appropriate probability, waiting to be summed.

John M. Keynes, 1937

As has been observed by economists such as Shackle [23], the translation to classical probability is problematic as it assumes that the range of outcomes indicated by the Arrow-Debreu securities is known a priori, a requirement strangely at odds with the aims of probabilistic modelling.

We think of uncertainty as more than the existence in the decision-maker’s mind of plural and rival (mutually exclusive) hypotheses amongst which he has insufficient epistemic grounds of choice. Decision, as we mean the word, is creative and is able to be so through the freedom which uncertainty gives for the creation of unpredictable hypotheses. Decision is not choice amongst the delimited and prescribed moves in a game with fixed rules and a known list of possible outcomes of any move or sequence of moves. There is no assurance that any one can in advance say what set of hypotheses a decision maker will entertain concerning any specified act available to him. Decision is thought and not merely determinate response.

George L. S. Shackle, 1969

Shackle rightly observes that ‘this language however is not merely a vessel but a mould’ [24] that excludes the possibility of surprise outcomes, though Shackle’s attempts to remedy the mathematics of classical probability are inadequate.

The solution is quantum probability. In the construction of Gelfand, Naimark and Segal, the Arrow-Debreu securities manifest as commuting projections. A fundamental result from the theory of operator algebras states that the commutative algebra generated by these projections is unitarily isomorphic to the bounded measurable functions on a measure space [19, 8, 12]. In this perspective, the state space is an emergent property of the market, naturally evolving as more potential outcomes are uncovered. More important, though, is the corollary that the algebra of all operators contains commutative subalgebras associated with every possible configuration of the economy. Optimisations within the full operator algebra are simultaneously super-optimal for all markets represented as commutative subalgebras, and the analysis proceeds without the need to make further assumptions on the nature of the economy.

While the resulting bounds for option prices could be determined using purely classical methods, the ease with which they are derived using quantum methods is noteworthy, and suggests further interesting applications. The approach is liberated from the requirement that the securities form a commutative algebra, leading to a framework for mathematical finance that can be applied in noncommutative geometries [15, 16] with novel features not available to the classical variant.

2 Bounds for option prices

In this article, securities are identified with real-valued functions and pricing models are identified with real-valued measures on the state space of the economy. These identifications are based on the following core assumptions:

-

•

The security is completely determined by specifying its payoffs for each state .

-

•

The pricing model is completely determined by specifying its prices of the Arrow-Debreu securities for each subset of states .

Appealing to the principle of replicability, the price of the security in the pricing model is given by the integral:

| (9) |

Prohibiting arbitrage then requires that the pricing measure is positive, so that a security whose payoff is positive in all states of the economy has positive price.

2.1 The Gelfand-Naimark-Segal construction

Positivity of the pricing model associated with a finite positive measure enables the Gelfand-Naimark-Segal, or GNS, construction on the space of securities. The content of the GNS construction is captured in the statement that, for an arbitrage-free pricing model, the definition:

| (10) |

provides an inner product on the securities . The security is then represented as a diagonal operator via pointwise-multiplication:

| (11) |

The apparent simplicity of this definition belies the technical challenges of the construction, which needs to exclude securities with infinite prices and factor out the degeneracy arising from securities whose payoffs are zero almost everywhere. Standard results from the theory of operator algebras are outlined here for completeness. The detail is not required for an understanding of the finance applications that follow.

The foundational result is the Cauchy-Schwarz inequality [7, 5, 21] that positivity implies for pricing.

Theorem 3 (Cauchy-Schwarz inequality)

The arbitrage-free pricing model satisfies the inequality:

| (12) |

for the securities .

Define the following subspaces of securities:

| (13) | ||||

where:

| (14) |

for the security . The first subspace includes the securities that are zero almost everywhere, and the second subspace includes the securities that are square-integrable, relative to the measure. The pricing model is used to construct an inner product on the quotient space . Denote by the coset containing the security . The inner product of the two cosets is defined by:

| (15) |

Repeated application of the Cauchy-Schwarz inequality demonstrates that this is a well-defined inner product on the quotient space.

The topological completion of the quotient space is the Hilbert space:

| (16) |

Define the following subspace of securities:

| (17) |

where:

| (18) |

for the security . This subspace is closed under the product, forming a subalgebra of the securities, and the GNS construction represents the subalgebra as an algebra of bounded operators on the Hilbert space.

Theorem 4 (Gelfand-Naimark-Segal construction)

For the arbitrage-free pricing model , there is a representation:

| (19) |

of the securities as bounded operators on the Hilbert space , such that the pricing model is a pure state of the representation:

| (20) |

for the security .

The representation in this construction is first defined on the dense subspace via left-multiplication:

| (21) |

for the securities and , and extended to by continuity, where finiteness of the norm ensures that this extension is possible.

Heuristically, the left-multiplication operators are the diagonal operators with respect to the basis of Dirac delta functions. This identification is strictly valid only when the state space is discrete, but the analogy can be a useful aid to understanding. The security is thus identified with a diagonal operator on a Hilbert space, with the price of the security given by the vacuum expectation of the operator.

By considering optimisation problems within the expanded domain of all operators on the Hilbert space, it is possible to determine solutions that are super-optimal for the restricted application. This can be used to derive bounds for option prices.

2.2 Super-optimal exercise strategies

For the assets , defined to be positive securities, and the quantities , which may be positive or negative scalars, consider the option to receive the portfolio . Exercise of the option is indicated by the Arrow-Debreu security , restricted so that it only takes the values zero or one, . The price of the option is then:

| (22) |

Optimal exercise happens when the option price is maximised over all possible exercise strategies. In this case, optimal exercise corresponds to the indicator , with option price:

| (23) |

The option price is obtained as the supremum price over a range of securities, each identified by its exercise strategy. Without additional information regarding the measure, it is not possible to refine this statement. It is possible, however, to obtain a super-optimal price for the option that requires only partial information from the pricing model.

Using the GNS construction associated with the pricing model, the option price is expressed as:

| (24) |

The optimal option price is the supremum of this expression over projections in the subalgebra of left-multiplication operators. This is bounded above by the supremum of the expression:

| (25) |

over projections in the algebra of all operators. The beauty of this observation is that the evaluation of the supremum over all projections is essentially geometric, requiring optimisation only over the projections on the finite-dimensional subspace spanned by the cosets associated with the square-roots of the assets.

2.3 Eigenvalue solution for the supremum

Motivated by the preceding argument, consider the following problem on a Hilbert space : Given the vectors and the scalars , determine the supremum of the valuations over all projections . This supremum is determined in the following theorem.

Theorem 5

Let be a Hilbert space. For the vectors and the scalars , define the finite-dimensional matrices and with matrix elements:

| (26) | ||||

For a decomposition of the positive semi-definite matrix in terms of a matrix , define the self-adjoint matrix . Then the supremum of the valuation:

| (27) |

over all projections is given by the sum of the positive eigenvalues of the matrix .

Proof. The aim is to determine the supremum:

| (28) | ||||

The problem is simplified by decomposing the Hilbert space, , where is the finite-dimensional Hilbert space spanned by the vectors and is its orthogonal complement in . The valuation depends only on the restriction of the projection to the subspace:

| (29) |

where the projection is decomposed relative to the decomposition of the Hilbert space:

| (30) |

for the operators , and . The upper-left operator is self-adjoint, but it is not necessarily a projection. Instead, the projection condition translates to the property:

| (31) |

Interference from the off-diagonal operator prevents from being a projection. The operator is positive semi-definite, so the projection property implies that with interference creating the possibility of eigenvalues between zero and one.

The restricted projection is diagonalised as:

| (32) |

where are diagonalising orthonormal basis eigenvectors and the eigenvalues satisfy . Using this diagonalisation, the valuation becomes:

| (33) |

where the self-adjoint operator is defined by:

| (34) |

Among the restricted projections that share the eigenvectors , the maximum valuation is obtained by using the projection onto the subspace of spanned by the eigenvectors for which the diagonal element is positive. The expression for the supremum is then:

| (35) | ||||

The valuation is the sum of the positive diagonal elements of the operator . A straightforward appeal to the Schur-Horn theorem [20, 11] demonstrates that this is bounded above by the sum of the positive eigenvalues of . To see this, first assume without loss of generality that the diagonal elements and the eigenvalues of are arranged in non-increasing order. The Schur-Horn theorem states that:

| (36) |

for all . Taking the maximum over , first on the right and then on the left, shows that:

| (37) |

The required result then follows from the observation that the maxima in this expression are given by the sum of the positive elements in their respective sequences, so that:

| (38) |

The sum of the positive eigenvalues of bounds the sum of the positive diagonal elements of , and so provides an upper bound for the supremum. This bound is attained by using the projection onto the subspace of spanned by the eigenvectors of with positive eigenvalues. The supremum of the valuations is then finally identified with the sum of the positive eigenvalues of :

| (39) |

The supremum is thus related to the solution of a finite-dimensional eigenvalue problem, and is obtained as the sum of the positive roots of a polynomial of order matching the dimension of the subspace spanned by the vectors.

The computation of the eigenvalues is enabled by expressing the problem in terms of an orthonormal basis for the subspace. The algorithm seeks to construct the matrix from the input matrix , where the matrix elements are:

| (40) | ||||

The solution requires the matrices and with matrix elements:

| (41) | ||||

The essential relationships among these matrices are:

| (42) | ||||

The program for solving the eigenvalue problem is now clear: First decompose the positive semi-definite matrix in the form , then solve for the eigenvalues of the self-adjoint matrix . Any such decomposition for the matrix generates the same result, as the eigenvalue problem is unaffected by unitary transformations. The solution thus depends only on the scalars and the inner products , and the dimension of the eigenvalue problem is the rank of the matrix with elements given by these inner products.

3 Applications of the option price bound

The GNS construction determines an inner product on the securities, and this relates the result of the previous section to the prices of options.

Theorem 6

For the arbitrage-free pricing model , the assets and the quantities , define the finite-dimensional matrices and with matrix elements:

| (43) | ||||

For a decomposition of the positive semi-definite matrix in terms of a matrix , define the self-adjoint matrix . Then the option valuation:

| (44) |

is bounded above by the sum of the positive eigenvalues of the matrix .

Proof. The GNS construction translates this statement into the language of the previous theorem. The proof is then completed by observing that the option valuation takes the form:

| (45) |

where the projection is the left-multiplication operator associated with the digital security indicating the exercise strategy for the option. The option valuation is thus bounded above by the supremum of this expression over all projections which, by the previous theorem, is the sum of the positive eigenvalues of the matrix .

The matrix is constructed from the diagonal matrix , whose diagonal elements are the quantities of the portfolio, and the symmetric matrix , whose elements are the moments of the measure. The diagonal elements of are the prices of the assets, typically sourced from available market data. The off-diagonal elements introduce additional volatility and correlation dependencies, providing the model parametrisation for the bound.

The theorem generates a bound on the price of the basket option. In this application, the matrices and are given by:

| (46) | ||||

Here, is the price of the th asset and is the normalised cross-term for the th and th assets:

| (47) | ||||

The cross-term is driven by the volatilities of the assets and the correlation between them, and can be expressed as:

| (48) |

where is the normalised variance of the square-root of the th asset and is the correlation between the square-roots of the th and th assets:

| (49) | ||||

The price is positive, , the root-variance lies in the range , and the correlation lies in the range . This completes the parametrisation of the model.

This result stands alone as an interesting application, providing an intuitive parametrisation for the price of the basket option. There is an ingenious interpretation of the result that extends its applicability beyond basket options, leading to a significant family of upper bounds that converges to the exact price as more information is absorbed. The key is to recognise that the decomposition of the portfolio into constituent assets can be arbitrarily refined, with each such decomposition yielding a new upper bound.

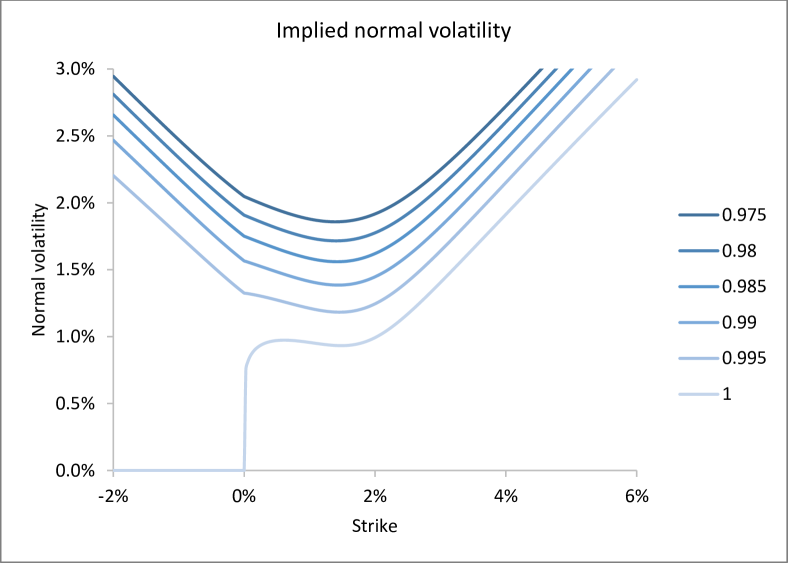

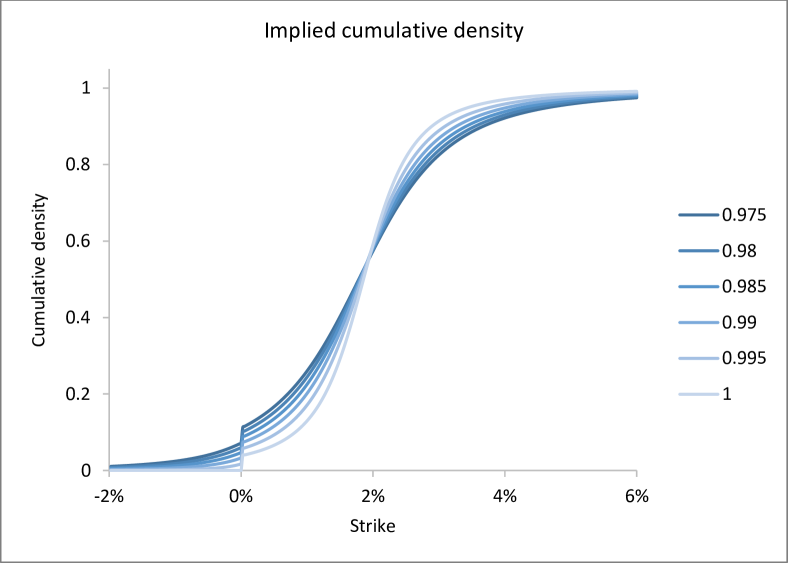

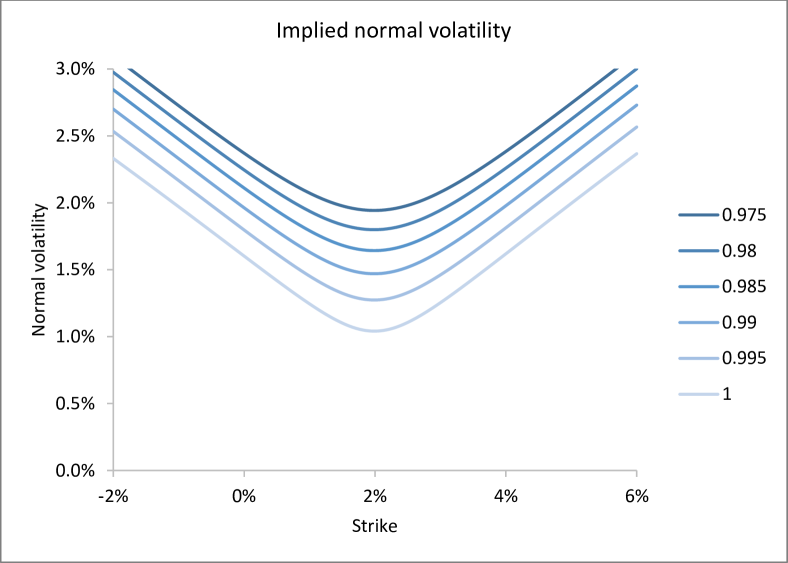

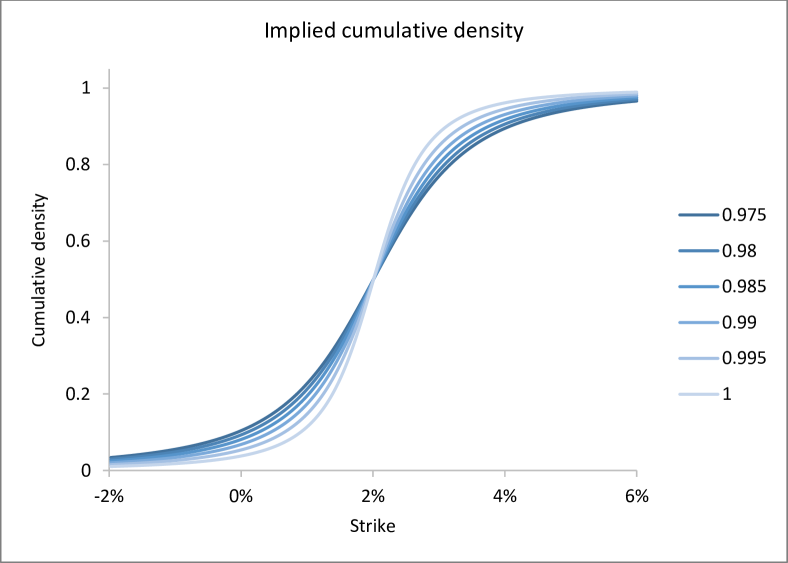

The range of results obtained in this manner is limited only by the creativity applied in the deconstruction of the portfolio. Taking a partition of unity constructed from vanilla call and put options generates a convergent family of upper bounds for the volatility smile. Another application for interest rate products derives from the decomposition of the swap rate in terms of its constituent forward rates, creating links between the prices of swaptions and caplets. These applications are explored below.

3.1 Vanilla options

|

|

The eigenvalue problem as formulated above is solved using standard matrix methods. In the case of two assets, this reduces to a quadratic equation with an explicit solution. For the asset and positive strike , the price of the option to receive the portfolio is bounded above by:

| (50) |

where and are the eigenvalues of the matrix constructed from the diagonal matrix , whose diagonal elements depend on the strike, and the symmetric matrix , whose elements are generated from the moments and of the measure. The diagonal element of the matrix is the price of the asset, which is marked to market. The off-diagonal element introduces an additional volatility dependency in the bound, controlled by a single model parameter.

The result is applied to generate a bound on the price of the vanilla option. In this application, the matrices and are given by:

| (51) | ||||

Here, is the price of the asset and is the normalised variance of the square-root of the asset:

| (52) | ||||

The price is positive, , and the root-variance lies in the range .

Represent the matrix as , where is the lower-triangular matrix generated using the Cholesky decomposition:

| (53) |

The eigenvalue solution for the supremum is derived from the matrix defined as the combination of the diagonal matrix with the lower-triangular matrix :

| (54) |

The eigenvalues of the matrix are the solutions of the quadratic equation derived from the determinant condition :

| (55) |

There are two solutions to this quadratic equation, but only one of them is positive. This eigenvalue provides the bound for the option price:

| (56) |

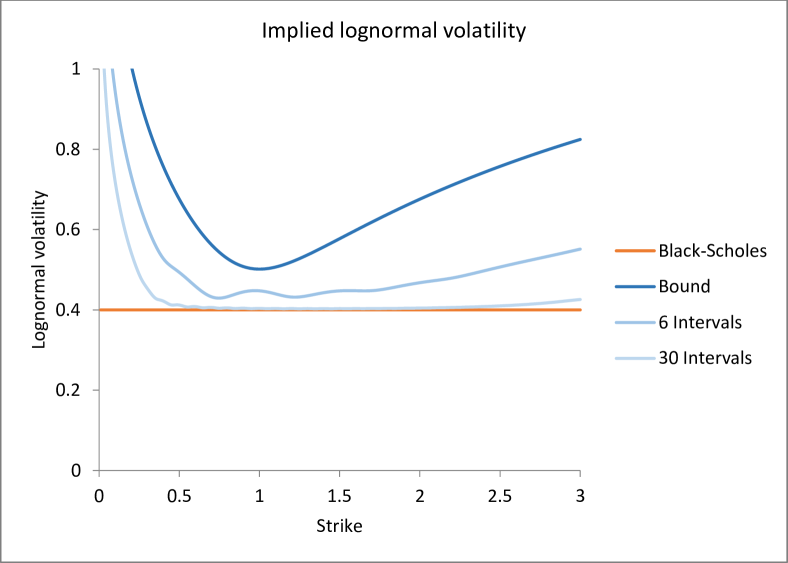

The bound extracts only two moments, the price and root-variance, from the measure, and applies to all pricing models calibrated to these moments.

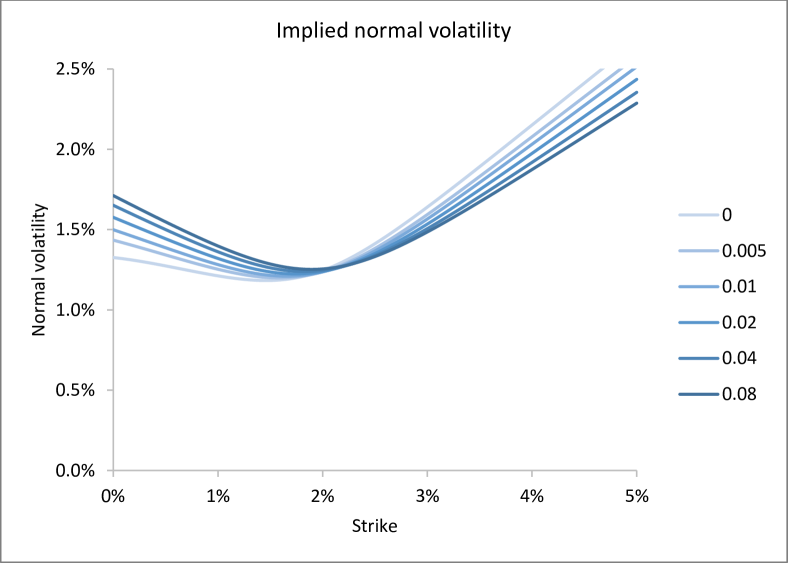

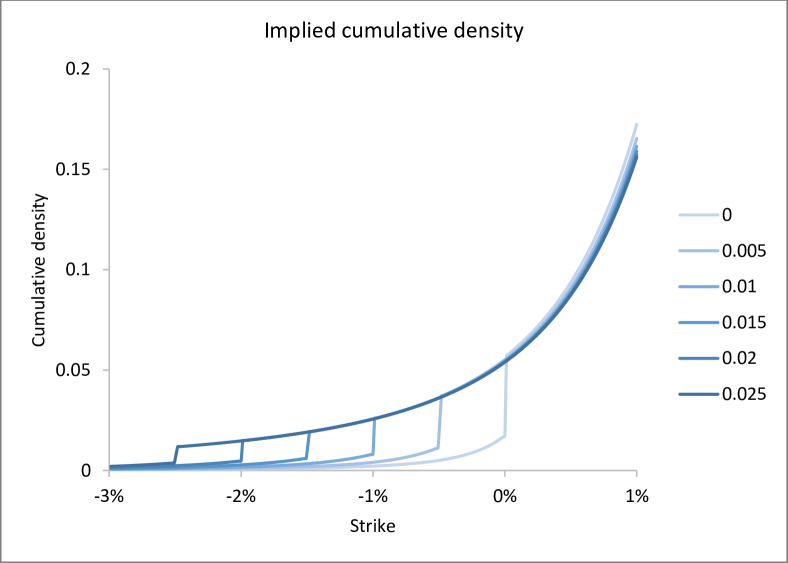

3.2 Refining the option price bound

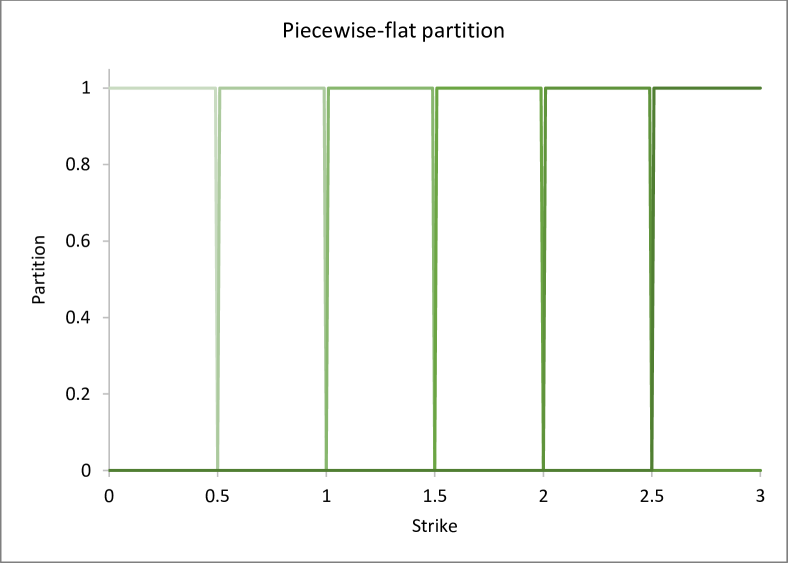

The bound for the option price is refined by using a partition of unity to decompose the option payoff, resulting in a bound that is constrained by the prices of options at a finite set of strikes. Consider the partition assets , satisfying the properties and . Using this partition, the spread between the asset and strike is expressed as the portfolio:

| (57) |

This decomposition generates a bound for the option price from a matrix whose diagonal elements are the prices of the partition assets scaled by the asset and the strike. The utility of the bound then depends on whether an intuitive parametrisation can be found for the off-diagonal moments implied by the partition.

|

|

|

A simple example constructs the partition from a decomposition of the upper half-line into subsets satisfying and for . The partition comprises the digital options on the asset indicated by the subsets:

| (58) |

with prices given by:

| (59) |

The matrices and both divide into four quadrants, with each quadrant containing a diagonal matrix:

| (62) | ||||

| (65) |

where is the price of the asset and is the normalised variance of the square-root of the asset conditional on the asset being in the subset :

| (66) | ||||

In these definitions, the measure is the measure conditional on , defined by:

| (67) |

for the security . The digital prices satisfy , while the conditional price is positive, , and the conditional root-variance lies in the range . These conditional moments are normalised by:

| (68) | ||||

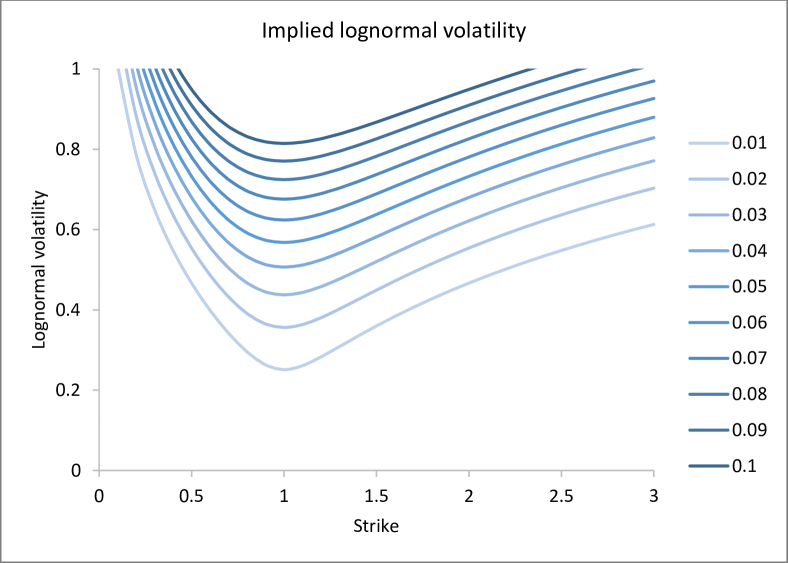

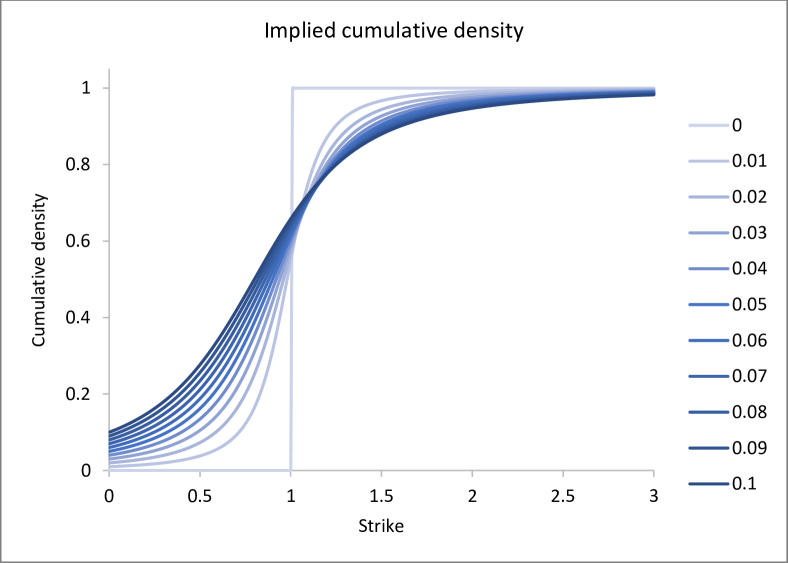

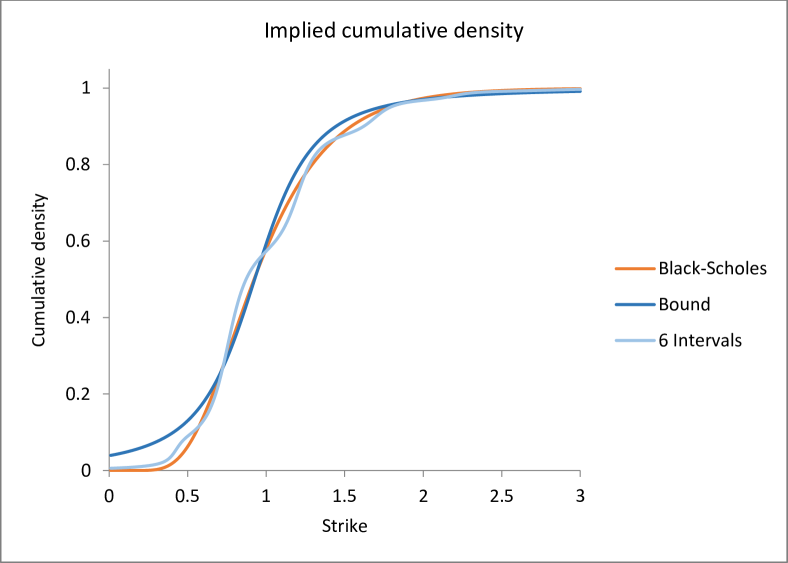

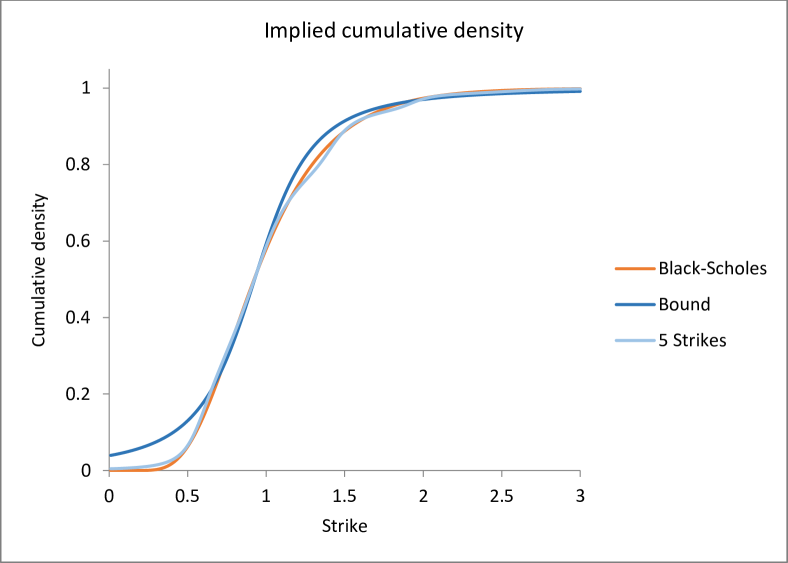

The decomposition of the upper half-line refines the bound for the option price, using a breakdown of the asset price and root-variance conditional on the asset being localised in nominated subsets. As the decomposition is further refined, more information from the pricing measure is incorporated into the bound, which converges to the price of the option in the limit of pointwise localisation.

3.3 Refinements based on option payoffs

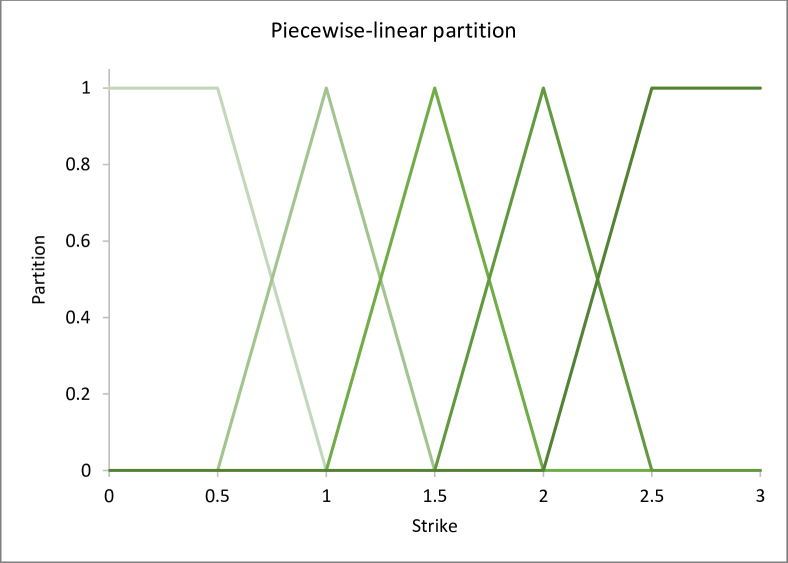

An alternative approach determines the bound for the option price from the prices of options at a finite set of strikes. For the positive strikes , the partition comprises the functions:

| (69) | ||||

These functions are positive and sum to one, supported on the domains:

| (70) | ||||

Aside from the diagonal products, only consecutive functions have nonzero products:

| (71) |

|

|

|

The four quadrants of the -dimensional matrix are tridiagonal. The upper-left quadrant has nonzero elements:

| (72) | ||||

The upper-right and lower-left quadrants have nonzero elements:

| (73) | ||||

The lower-right quadrant has nonzero elements:

| (74) | ||||

These elements are driven by correlations between the options that are parametrised similarly to the basket option case. In practice, a simple parametric model, such as the Black-Scholes model, can be used to imply sensible values for the correlations dependent on a smaller set of model parameters. By using continuous basis functions, this partition generates a smoother bound than that implied by the digital partition of the previous example.

3.4 Foreign exchange options

The previous examples show how families of bounds for the option price can be obtained by subdividing the assets into localised components. An alternative strategy decomposes the asset into more fundamental economic units, using an understanding of the financial structure of the asset. The next example applies this approach to generate bounds for the price of an option on a cross FX rate.

The option on the FX rate is a vanilla option in the form considered previously, and the option price is subject to the same bound:

| (75) |

where is the price of the FX rate and is the normalised variance of the square-root of the FX rate:

| (76) | ||||

In these expressions, the pricing measure is associated with the base currency of the FX rate.

Options on an illiquid FX rate are more commonly written on the cross FX rate , where and are the FX rates for the two currencies versus a fixed domestic currency. In this situation, the bound for the vanilla option continues to apply, but the volatility can be further decomposed in terms of the volatilities and correlation of the two contributing FX rates:

| (77) |

where and are the normalised variances of the square-roots of the liquid FX rates and is the correlation between the square-roots of the liquid FX rates:

| (78) | ||||

In these expressions, the pricing measure is associated with the domestic currency, related to the pricing measure by:

| (79) |

If the two contributing FX rates have liquid option markets, the volatilities and can be replicated from the prices of options, leaving the correlation to parametrise the bound for the price of the option on the cross FX rate.

3.5 Swaptions and caplets

Another example, taken from the interest rate market, considers the decomposition of the swap rate into its constituent forward rates. Inverting the relationship between swap and forward rates leads to bounds on the prices of forward-starting caplets expressed in terms of the distributions of the swap rates.

The -period swap rate is decomposed as the weighted average of the forward rates for :

| (80) |

In this expression, is the discount factor to the th payment date and is the daycount fraction for the th accrual period, where for simplicity the daycount conventions on the fixed and float legs are assumed to be the same. The weights in this weighted average are positive and sum to one. In the following discussion these weights are assumed to be deterministic, an approximation that not only allows the swap rate to be expressed as a linear combination of the forward rates, but also avoids complications with differences in the pricing measures associated with the annuities. These considerations, while significant, are beyond the scope of the present article.

Inverting the above relationship, the forward rate is decomposed in terms of the swap rates and :

| (81) |

with weight given by:

| (82) |

The general result for the bound on the price of a basket option can be applied to this decomposition. Consider the forward-starting caplet with strike on the th forward rate . The payoff for the caplet decomposes in terms of the swap rates and :

| (83) |

In this application, the matrices and are the three-dimensional matrices given by:

| (84) | ||||

Here, is the price of the th swap rate and is the normalised variance of the square-root of the th swap rate:

| (85) | ||||

and the cross-term is defined from the correlation between the square-roots of the th and th swap rates:

| (86) |

by:

| (87) |

The price is positive, , the root-variance lies in the range , and the correlation lies in the range . The price and root-variance are determined from the market for swaps and swaptions, leaving the correlation as the model parameter for the price of the forward-starting caplet.

|

|

|

|

|

|

There is an implicit assumption that the swap rates are positive in this application, which cannot be guaranteed. The economic floor for the forward rate is , so the economic floor for the swap rate is where the daycount fraction is the weighted average of the daycount fractions for :

| (88) |

Positivity can be restored to the terms in the decomposition of the forward rate by shifting the swap rates and strike by a proportion of the economic floor:

| (89) | ||||

Applying these substitutions in the expressions above for the matrices and generates an upper bound based on swap rates with negative floors. The additional model parameter in this construction is the shift, which takes values in the range .

4 Attaining the option price bound

Application of the GNS construction to the pricing measure generates upper bounds for the option price, and with the creative decomposition of the option portfolio this leads to a diverse range of bounds depending on partial information extracted from the measure. There is, however, no guarantee that the bound derived from this construction is useful, though the examples of the previous section suggest this is the case.

One question to ask is whether there is a measure satisfying the constraints that attains the bound for the option price, and in this statement there are two variations: local and global attainment. For options on portfolios generated from the assets , the bound is derived from the matrix with elements . The portfolio quantities are provided by the scalars , and the GNS construction generates an option price bound as a function of these quantities. For this configuration, the local and global attainment of the bound is expressed in the following definitions.

- Local attainment:

-

For each portfolio there is an arbitrage-free pricing model that satisfies the constraints:

(90) and has option price given by:

(91) - Global attainment:

-

There is an arbitrage-free pricing model that satisfies the constraints:

(92) and for each portfolio has option price given by:

(93)

The remainder of this article investigates local and global attainment in the simple case of two assets. Consider the option to exchange the asset for units of the asset . The GNS construction provides an upper bound for the option price across all pricing models constrained to match the price and root-variance :

| (94) |

where:

| (95) | ||||

This bound is attained by the binomial model, albeit with a configuration that depends on the strike, and this demonstrates local attainment. The Carr-Madan replication formula shows that the measure implied by the bound does not match the required moments – there is no single measure that generates the bound for all strikes – so the bound is not globally attained.

4.1 Local attainment

In the binomial model, the asset with binomial spectrum has price:

| (96) |

where the angle in the range generates positive weights that sum to one. The calibration problem is transformed into trigonometry by assigning for the angle in the range . Calibration to the price and root-variance then leads to the constraints:

| (97) | ||||

|

|

For a given angle , assumed not to be equal to the edge cases or , these relations can be inverted to identify the asset with the specified moments. The constraint imposed by calibration to the price is solved by:

| (98) | ||||

for an angle in the range . The constraint imposed by calibration to the root-variance is then solved for the angle :

| (99) |

There are two solutions to this equation. The first solution is valid for angle in the range , leading to the following spectrum for the asset:

| (100) | ||||

This solution satisfies . The second solution is valid for angle in the range , leading to the following spectrum for the asset:

| (101) | ||||

This solution satisfies . The two solutions transform into each other under the transformation that switches the underlying states.

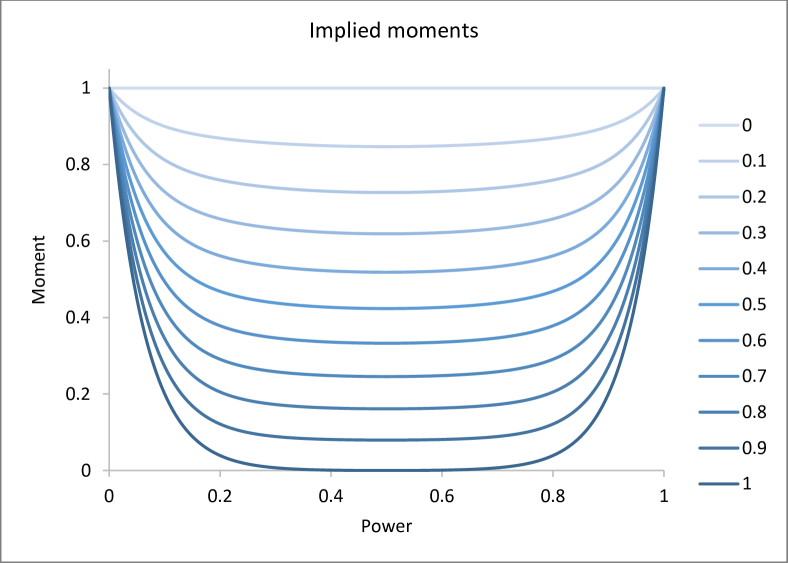

Focussing, without loss of generality, on the second solution, the option price is maximised at the angle satisfying:

| (102) |

At this angle, the price of the option is given by the supremum price:

| (103) |

The binomial model at this angle generates the supremum option price for pricing models that calibrate to the asset price and root-variance. This is not entirely surprising, as the supremum problem is essentially a linear programming problem, and with two constraints the solution reduces to a domain comprised of just two states. Note, however, that the angle that specifies the optimal binomial model depends on the strike. There is no single binomial model that achieves the bound for all strikes.

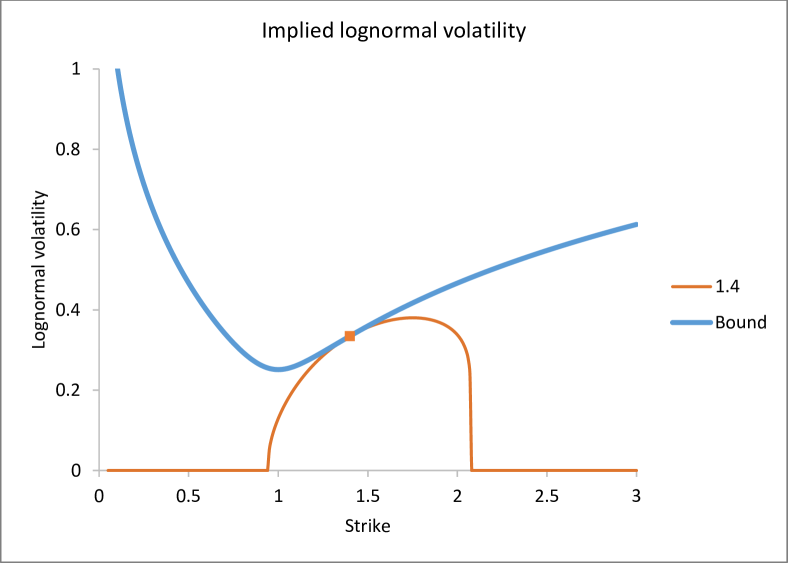

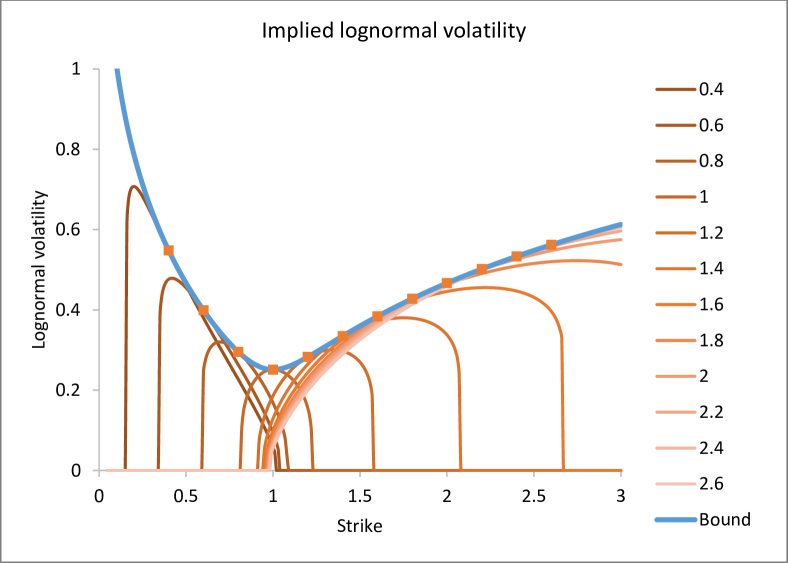

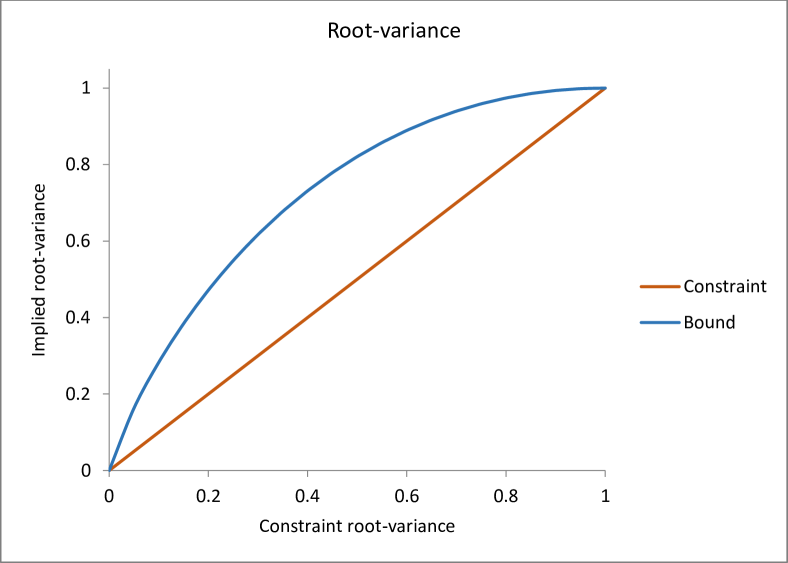

4.2 Global attainment

The bound for the option price is decreasing and convex as a function of the strike, and so represents a pricing measure that is free of arbitrage. For any individual strike, the bound provides the maximum possible option price from pricing models matching the asset price and root-variance. This does not imply that the bound itself defines a pricing model that matches the asset price and root-variance. Application of the Carr-Madan replication formula demonstrates that the implied measure has root-variance that exceeds the calibration constraint.

|

|

Consider the pricing model with call and put option prices given by:

| (104) | ||||

Subtracting these expressions, it immediately follows that the measure is calibrated to the price :

| (105) |

The Carr-Madan replication formula determines the price of the payoff to be:

| (106) | ||||

The first integral is simplified with the change of variables and the second integral is simplified with the change of variables , leading to:

| (107) | ||||

The moment is finite only for . The integer moments are and , and for the moment is given by:

| (108) | ||||

The moment is symmetric under the transformation . The case corresponds to the fixed point of this transformation:

| (109) |

This expression is numerically integrated to generate the root-variance implied by the option price bounds. The implied root-variance exceeds the constraint everywhere except at the edge cases, demonstrating that the bound is not globally attained.

5 Conclusion

By exploring the exercise strategies that are available in the larger algebra of all operators on the Hilbert space in the GNS construction, the approach developed here generates bounds for option pricing contingent only on partial information from the pricing measure. In some cases this is a tight bound for the option price, being attained by the multinomial model calibrated to the same target moments, and can be arbitrarily refined by extracting more information. The family of bounds generated by this approach depends on the partition of the option portfolio, and with ingenuity leads to methods for interpolating the volatility smile, linking swaption and caplet prices, and many other financial applications. Intriguingly, the volatility smiles implied by these bounds are similar to smiles observed in the market.

These results accommodate an extension to the classical theory of mathematical finance that, by admitting noncommuting assets, is amenable to the methods of quantum analysis. At opposing extremes in this picture are the classical algebra of left-multiplication operators and the quantum algebra of all operators on the Hilbert space. There are many layers of algebra between these extremes, each of which determines a domain for the exercise strategies, thereby creating a hierarchy of option pricing bounds. This suggests a relationship between the theory of von Neumann algebras and the pricing of options that is worthy of further investigation.

References

- [1] K. J. Arrow and G. Debreu. Existence of an equilibrium for a competitive economy. Econometrica, 22:265–290, 1954.

- [2] F. Black and M. Scholes. The pricing of options and corporate liabilities. Journal of Political Economy, 81(3):637–654, 1973.

- [3] M. Born, W. Heisenberg, and P. Jordan. Zur Quantenmechanik II. Zeitschrift fur Physik, 35:557–615, 1926.

- [4] M. Born and P. Jordan. Zur Quantenmechanik. Zeitschrift fur Physik, 34:858–888, 1925.

- [5] V. Y. Bouniakowsky. Sur quelques inegalités concernant les intégrales aux différences finies, Mem. Acad. Sci. St. Petersbourg I, (9):1–18, 1859.

- [6] P. Carr and D. Madan. Towards a theory of volatility trading. 1998.

- [7] A. L. Cauchy. Cours d’analyse de l’École Royale Polytechnique: Analyse algébrique. Pte. 1. Imprimerie Royale, 1821.

- [8] J. B. Conway. A Course in Functional Analysis. Springer-Verlag, second edition, 1990.

- [9] I. M. Gelfand and M. A. Naimark. On the imbedding of normed rings into the ring of operators in Hilbert space. Matematiceskij sbornik, 54(2):197–217, 1943.

- [10] W. Heisenberg. Über quantentheoretische Umdeutung kinematischer und mechanischer Beziehungen. Zeitschrift fur Physik, 33:879–893, 1925.

- [11] A. Horn. Doubly stochastic matrices and the diagonal of a rotation matrix. American Journal of Mathematics, 76(3):620–630, 1954.

- [12] R. V. Kadison and J. R. Ringrose. Fundamentals of the Theory of Operator Algebras Volume I: Elementary Theory. American Mathematical Society, 1997.

- [13] R. V. Kadison and J. R. Ringrose. Fundamentals of the Theory of Operator Algebras Volume II: Advanced Theory. American Mathematical Society, 1997.

- [14] J. M. Keynes. The General Theory of Employment. Quarterly Journal of Economics, 51:209–223, 1937.

- [15] P. McCloud. In Search of Schrödinger’s Cap: Pricing Derivatives with Quantum Probability. SSRN e-prints, 2014, ssrn.2341301.

- [16] P. McCloud. Quantum Duality in Mathematical Finance. ArXiv e-prints, 2017, q-fin.MF/1711.07279.

- [17] J. von Neumann. Mathematische Begründung der Quantenmechanik. Nachrichten von der Gesellschaft der Wissenschaften zu Göttingen, Mathematisch-Physikalische Klasse, 1927:1–57, 1927.

- [18] J. von Neumann. Allgemeine Eigenwerttheorie Hermitescher Funktionaloperatoren. Mathematische Annalen, 102:49–131, 1930.

- [19] J. von Neumann. On Rings of Operators. Reduction Theory. Annals of Mathematics, 50(2):401–485, 1949.

- [20] I. Schur. Uber eine Klasse von Mittelbildungen mit Anwendungen auf die Determinantentheorie. Sitzungsberichte der Berliner Mathematischen Gesellschaft, 22:9–20, 1923.

- [21] H. A. Schwarz. Über ein die flächen kleinsten flächeninhalts betreffendes problem der variationsrechnung. In Gesammelte Mathematische Abhandlungen, pages 223–269. Springer, 1890.

- [22] I. E. Segal. Irreducible representations of operator algebras. Bull. Amer. Math. Soc., 53(2):73–88, 1947.

- [23] G. L. S. Shackle. Decision, Order and Time in Human Affairs. Cambridge University Press, second edition, 1969.

- [24] G. L. S. Shackle. Epistemics and Economics. Cambridge University Press, 1972.