Central limit theorem for the variable bandwidth kernel density estimators

Janet Nakarmia and Hailin Sangb111footnotetext: Corresponding author

a Department of Mathematics, University of Central Arkansas, Conway, AR 72035, USA. E-mail address: janetn@uca.edu

b Department of Mathematics, The University of Mississippi, University, MS 38677, USA. E-mail address: sang@olemiss.edu

Abstract

In this paper we study the ideal variable bandwidth kernel density estimator introduced by McKay [9, 10] and Jones et al. [7] and the plug-in practical version of the variable bandwidth kernel estimator with two sequences of bandwidths as in Gin\a’e and Sang [4]. Based on the bias and variance analysis of the ideal and true variable bandwidth kernel density estimators, we study the central limit theorems for each of them.

MSC 2010 subject classification: 62G07, 62E20, 62H12, 60F05

Key words and phrases: central limit theorem, variable bandwidth kernel density estimation.

1 Introduction

Suppose that , are independent identically distributed (i.i.d.) observations with density function , . Let to be a symmetric probability kernel satisfying some differentiability properties. The classical kernel density estimator

| (1) |

where is the bandwidth sequence with , and its properties have been well studied in the literature. The variance of (1) has order and the bias has order if has bounded second order partial derivatives. See Silverman [12] and Wand and Jones [14] for the literature on kernel density estimation. For , set , one may obtain bias with order for the estimator (1) if the fourth order kernel function is allowed: and for . Nevertheless, in (1) may take negative values and therefore not a true density function in this case since may take negative values. For example, see Marron [8]. In this paper we study the following multidimensional version of the variable bandwidth kernel density estimator proposed by McKay [9, 10]:

| (2) |

where is a smooth function of the form

| (3) |

The function has at least fourth order derivative and satisfies for all and for all for some , and a fixed number , where . The equation (2) is a variable bandwidth kernel density estimator since the bandwidth has form if we rewrite (2) in the form of the classical one, (1).

The study of variable bandwidth kernel density estimation goes back to Abramson [1]. Abramson proposed the following estimator

| (4) |

where . The bandwidth at each observation is inversely proportional to if . Notice that (2) also has the square root law since if by the definition of the function . The estimator (2) or (4) has clipping procedure in (3) or since they make the true bandwidth or . The clipping procedures prevent too much contribution to the density estimation at if the observation is too far away from . Abramson showed that this square root law and the clipping procedure improve the bias from the order of to the order of for the estimator (4) while at the same time keep the variance at the order of if and has fourth order continuous derivatives at . So, one has a non-negative estimator of the density that performs asymptotically as a kernel estimator based on a fourth order (hence, partly negative) kernel. However, this variable bandwidth estimator (4) is not a density function of a true probability measure since the integral of over is not .

Terrell and Scott [13] and McKay [10] showed that the following modification of the Abramson estimator without the ‘clipping filter’ on studied in Hall and Marron [5],

| (5) |

which has integral and thus is a true probability density, may have bias of order much larger than . Therefore, the clipping is necessary for such bias reduction. In the case , Hall, Hu and Marron [6] proposed the estimator

| (6) |

where is a fixed constant; see also Novak [11] for a similar estimator. This estimator is non-negative and achieves the desired bias reduction but, like Abramson’s, it does not integrate to 1.

In conclusion, it seems that the estimator (2) has all the advantages: it is a true density function with square root law and smooth clipping procedure. However, notice that this estimator and all the other variable bandwidth kernel density estimators are not applicable in practice since they all include the studied density function . Therefore, we call them ideal estimators in the literature. Hall and Marron [5] studied a true density estimator

by plugging in a pilot estimator, the classical estimator (1), into the estimator (5). Here the bandwidth sequence is the as in (5) and the bandwidth sequence is applied in the classical kernel density estimator (1), i.e.,

They took the Taylor expansion of at and then proved that the discrepancy between the true estimator and the ideal version (5) has asymptotic convergence rate pointwise. By applying this Taylor decomposition, McKay [10] studied convergence of plug-in true estimator of (2) in probability and pointwise. Giné and Sang [3, 4] studied plug-in true estimators of (6) and (2) for one and d-dimensional observations. They proved that the discrepancy between the true estimator and the true value converges uniformly over a data adaptive region at a rate of by applying empirical process techniques. The true estimator in Giné and Sang [4] has the following form

| (7) |

In this paper, we concentrate on the study of central limit theorem of the true estimator (7).

The paper has the following structure. Section 2 introduces the decompositions which will be applied throughout the paper. Section 3 gives the exact bias formula. In Section 4, we obtain an exact formula for the variance of the ideal estimator. Based on the study in Sections 3 and 4, we provide a central limit theorem for the true estimator in Section 5. The simulation study in Section 6 demonstrates the advantage of the variable bandwidth kernel estimation.

2 Preliminary decomposition

For convenience, we adopt the notations as in Giné and Sang [4] for the Taylor series expansion of at . We also give statements without detailed explanation. For details, readers are referred to Giné and Sang [4]. will denote the set of densities on for which they and their partial derivatives of order or lower are bounded by and are uniformly continuous. We say that a function is in if it and its first derivatives are bounded and uniformly continuous on .

Define by the equation

Then,

| (8) |

and

| (9) |

for a constant that depends only on the function . Here the constant and the function are applied in the definition of in (3). Although we study the asymptotics of the true estimator pointwise, the uniform asymptotic behavior of the quantity is needed in the latter analysis. Define

Note that for , , and by Giné and Guillou [2],

for . Denote

| (10) |

Then we have,

and

| (11) |

for . By the definition of , we also have,

| (12) |

where is between and . Notice that for some constant which depends only on the clipping function . It is also convenient to record the following expansion of implied by (8) and (11):

| (13) |

with

Set

| (14) |

where denotes the partial derivative of in the direction of the -th coordinate, and denotes the -th coordinate of . By symmetry and integration by parts, we notice that is a second order kernel.

We then have the following Taylor series expansion

| (15) |

where

being a (random) number between and . By the analysis in Giné and Sang [4],

| (16) |

if . Therefore using equation , Taylor series expansion of in , and expansion of in , we have

| (17) | |||

| (18) | |||

| (19) | |||

| (20) |

3 Bias

The following notations are necessary for the rest of the paper: for and vector , set

| (21) | ||||

where means that we take partial order derivatives on the first coordinate, partial order derivatives on the second coordinate, until we take partial order derivatives on the -th coordinate.

We also define

Here, and are the constants that appear in the definition of the clipping function in (3).

Proposition 3.1

Let be a density function in , let be a clipping function in , set for some , and define as in (7). Suppose that the kernel on has the form for some real function with uniformly bounded second order derivative and with support contained in , . is non-negative and integrates to 1. For the quantity defined in (10), assume that . Then as , for ,

Proof. By McKay [9, 10] or Corollary 1 of Gin\a’e and Sang [4], the ideal estimator (2) satisfies

| (22) |

Hence by the expansion of in (17)-(20) and equation (22), the expectation of is

| (23) | ||||

| (24) | ||||

| (25) | ||||

| (26) | ||||

| (27) |

By (3.20) of Gin\a’e and Sang [4] and the boundedness of , and , we have

| (28) |

| (29) |

and

| (30) |

where the is defined in (10). We further decompose (24) using the decomposition (12) of first, and then the decomposition of into the random part and the bias :

| (31) | |||

| (32) | |||

| (33) |

By (16) or (3.24) of Gin\a’e and Sang [4] and the boundedness of and , we obtain,

| (34) |

By (3.26) of Gin\a’e and Sang [4], we have

| (35) |

In the following we give the estimation of (31) to finish the proof of the proposition.

Let be an integrable function of two i.i.d. random variables and . Then the -statistic is

where the variables are i.i.d. copies of . The second order Hoeffding projection of is If we set

then we can decompose the following quantity into a diagonal term and a -statistic term,

| (36) | |||

| (37) | |||

| (38) | |||

| (39) |

Obviously, (38) and (39) have mean zero since

In the empirical process (37), set and observe that,

for some finite constant . By combining the above analysis and by the analysis of Giné and Sang [4] on page 144, we have

| (40) |

By the analysis in (23)-(35) and (40), the bias

4 Variance of the ideal estimator

We develop the second moment expansion uniformly to deal with the variance of the ideal estimator. Here we denote and for convenience. Then, the ideal estimator (2) has the form

Denote , then we have the second moment of the ideal estimator as follows:

Recall that

if . Since , we have

| (41) | |||||

In the next proposition, we study the quantity . The idea is similar to the uniform bias expansion as in McKay [10], Jones, McKay and Hu [7], and particularly Gin\a’e and Sang [4].

Proposition 4.1

Suppose that the kernel on has the form for some real function with uniformly bounded second order derivative and with support contained in , . is non-negative and integrate to 1. Assume the density function is in . Suppose that for some and all , and that the function is in . Then we have,

| (42) |

as , uniformly in . The set of functions , which are uniformly bounded and equicontinuous, are defined as

| (43) |

uufor , in particular, . Here and are defined in (3).

Proof. Note that there exists such that , , are bounded away from zero, , , are small enough for all and for functions that are bounded away from zero and their derivatives that are bounded. Hence the matrix is invertible. Thus the vector function is invertible on the neighborhood of for each . By differentiation, it is easy to see that the inverse function, say , is times differentiable with continuous partial derivatives. Unless , . Hence, the change of variables

in the following integral is valid for all small enough

where is the partial derivative matrix of the vector function with respect to and is the determinant of . If we develop the function into powers of and then integrate it, noting the compactness of the domain of integration and the differentiability properties of and , we have .

Suppose is infinitely differentiable and has bounded support. Then, changing variables () from to in (4), developing , changing variables once more ()) and integrating by parts, we obtain

Here is defined in (3). Notice that for . Then, (43) follows by comparing the coefficients of in both expansions (42) and (4).

5 Central limit theorem

5.1 Central limit theorem for ideal estimator

The ideal estimator in (2) can be written as a sample mean of triangular array of i.i.d. random variables, i.e., , where

| (46) |

Notice that . By (41) and Proposition 4.1,

Hence, by the Lindeberg’s central limit theorem for triangular array of random variables, we have the following central limit theorem for the ideal estimator for all ,

Since for by McKay ([9], [10]) or Corollary 1 in Giné and Sang [4],

if we take for some constant . Note that,

Thus, by Slutsky’s theorem, for ,

5.2 Central limit theorem for the true estimator

Based on the above central limit theorems for the ideal estimator, we have the following central limit theorems for the true variable bandwidth kernel density estimator.

Theorem 5.1

Let be a random sample of size n with density function , , and defined as in is an estimator of . Assume to be in . Suppose the kernel on has the form for some real function with uniformly bounded second order derivative and with support contained in , . is non-negative and integrates to 1. The function in the estimator is defined in (3) for a nondecreasing clipping function for all and for all with five bounded and uniformly continuous derivatives, and constant . Let for some constants and assume that . Then for ,

| (47) |

and

| (48) |

Here, , , and .

Proof. The true estimator in (7) has decomposition

| (49) | ||||

| (50) | ||||

| (51) |

| (52) |

Since

by the analysis in Section 3, the term (51) is negligible in the central limit theorems (47) and (48). The term (49) has decomposition as in (17) - (20). We know that , and by (3.20) of Giné and Sang [4]. Hence they are also negligible in the central limit theorems (47) and (48).

We can further decompose into the random variation part and the bias by the decomposition (12):

| (53) | ||||

| (54) | ||||

| (55) |

By (3.24) of Giné and Sang [4], we have that and by the analysis for (3.27) of the same paper, we have . Also, the term multiplied by can be further decomposed into (37), (38) and (39) from Section 2, and by the proof of (3.33) of Giné and Sang [4], . Next we show that =.

It is easy to see that and are bounded by , for some constant . Thus,

Let be given. Then, by Markov’s inequality, we have

Hence, =.

By the above analysis, only the term (50) and the remaining term from (49), i.e., (39) divided by , have contribution in the central limit theorems (47) and (48). The other terms are all negligible. Now let , . Define , and where is defined as in (46). To prove the central limit theorem (47), it suffices to derive a central limit theorem for where is the sample mean of i.i.d. random variables , .

We have

by Corollary 1 of Giné and Sang [4] and since . Also, by Proposition 4.1 in Section 4. Since

we need to calculate the limit of terms and .

Let and be the change of variables. Then,

and

since . By the change of variables, it is easy to see that is bounded by for some and then as . Hence,

and

Thus,

Hence, by central limit theorem for i.i.d. random variables, we have

and by Slustsky’s theorem,

Since the term by Proposition 3.1,

Thus,

With the central limit theorem in Theorem 5.1, one can have better statistical inference on the density function value at a fixed point . For example, with some fixed confidence level, the confidence interval for the true density function at the fixed point using the variable bandwidth kernel estimation is better (the length of the confidence interval is shorter) than the classical case since the bandwidth here has order of instead of .

6 Simulation

In this section we evaluate the performance of the variable bandwidth kernel density estimator (VKDE), (7), in one dimensional case. Instead of the true estimator (7), Jones, McKay and Hu [7] did simulation study for the ideal estimator (2) in one dimensional case. First of all, we provide a result on the integrated mean squared error (IMSE) of the VKDE and therefore a formula of optimal bandwidth.

Theorem 6.1

Proof. From the analysis of Theorem 5.1, it is clear that for . Together with Proposition 3.1, we have (56). The optimal bandwidth (57), which minimize the IMSE, is obvious from the IMSE formula (56).

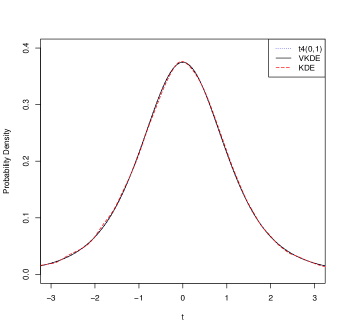

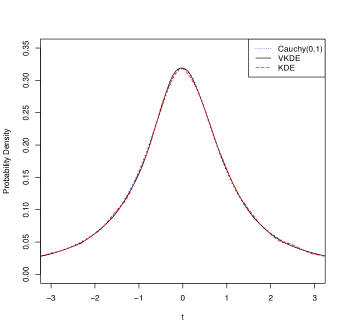

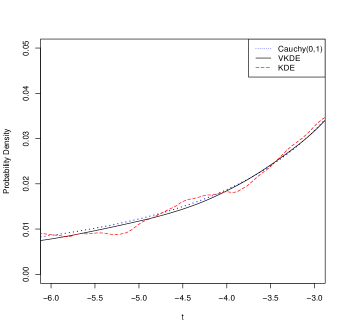

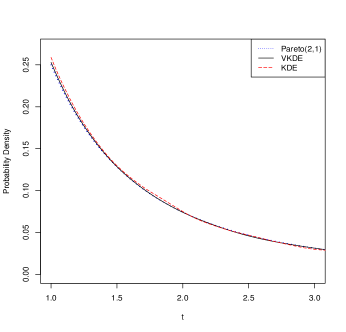

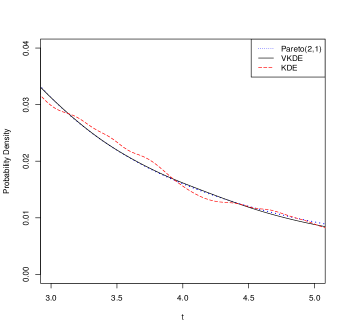

We compare the performance of VKDE and KDE by conducting one dimensional simulation study of t-distribution (), Cauchy(0,1) and Pareto(0,1). The sample size is for each simulation study. For all the simulations, we use KDE as in with the normal kernel function. We use the code density() in the programming software R and the default bandwidth chosen by R in the estimation for . For Cauchy(0,1) or Pareto(0,1), the code density() in R can not provide a classical kernel density estimate. Instead, we make new code and select the bandwidth which optimizes the performance among a variety of bandwidths. For VKDE, we assume that , , and use the Tricube kernel:

in either the pilot kernel density estimator or the true estimator (7). The following five time differentiable clipping function with (Giné and Sang [4]) is applied:

The simulation study in Figure 1 shows that, for each of these three distributions, VKDE has better performance than KDE, especially in the tail area.

Acknowledgement The authors thank the referee and the Editor for their careful reading of the manuscript and for their insightful comments, which have helped to improve the quality of this paper.

References

- [1] I. Abramson. On bandwidth variation in kernel estimates - a square-root law, Ann. Statist. 10 (1982) 1217-1223.

- [2] E. Giné and A. Guillou. Rates of strong uniform consistency for multivariate kernel density estimators. Ann. Inst. Henri. Poincaré Probab. Stat. 38 (2002) 907-921.

- [3] E. Giné and H. Sang. Uniform asymptotics for kernel density estimators with variable bandwidths. J. Nonparametr. Stat. 22 (2010) 773-795.

- [4] E. Giné and H. Sang. On the estimation of smooth densities by strict probability densities at optimal rates in sup-norm. IMS Collections, From Probability to Statistics and Back: High-Dimensional Models and Processes 9 (2013) 128-149.

- [5] P. Hall and J. S. Marron. Variable Window Width Kernel Estimates of Probability Densities. Probab. Theory Related Fields 80 (1988) 37-49. Erratum: Probab. Theory Related Fields 91 133.

- [6] P. Hall, T. Hu and J. S. Marron. Improved Variable Window Kernel Estimates of Probability Densities. Ann. Statist. 23 (1995) 1-10.

- [7] M. C. Jones, I. J. McKay and T.-C. Hu. Variable location and scale kernel density estimation. Ann. Inst. Statist. Math. 46 (1994) 521-535.

- [8] J. S. Marron. Visual understanding of higher order kernels. Journal of Computational and Graphical Statistics, 3 (1994) 447-458.

- [9] I. J. McKay. A note on bias reduction in variable kernel density estimates. Canad. J. Statist. 21 (1993a) 367-375.

- [10] I. J. McKay. Variable kernel methods in density estimation. Ph.D Dissertation, Queen’s University, (1993b).

- [11] S. Yu. Novak. A generalized kernel density estimator. (Russian) Teor. Veroyatnost. i Primenen. 44 (1999) 634–645; translation in Theory Probab. Appl. 44 (2000) 570–583.

- [12] B. W. Silverman. Density Estimation for Statistics and Data Analysis (1986). Chapman and Hall, London.

- [13] G. R. Terrell and D. Scott. Variable kernel density estimation. Ann. Statist. 20 (1992) 1236-1265.

- [14] M. Wand and M. C. Jones. Kernel Smoothing (1995). Chapman and Hall, London.