Change-point inference on volatility in noisy Itô semimartingales

Abstract

This work is concerned with tests on structural breaks in the spot volatility process of a general Itô semimartingale based on discrete observations contaminated with i.i.d. microstructure noise. We construct a consistent test building up on infill asymptotic results for certain functionals of spectral spot volatility estimates. A weak limit theorem is established under the null hypothesis relying on extreme value theory. We prove consistency of the test and of an associated estimator for the change point. A simulation study illustrates the finite-sample performance of the method and efficiency gains compared to a skip-sampling approach.

keywords:

Change-point analysis, high-frequency data , market microstructure , volatility estimation , volatility jumpMSC:

[2010] 62M10 , 62G101 Introduction

Inference on structural breaks for discrete-time stochastic processes, particularly in time series analysis, is a very active research field within mathematical statistics. Whereas the latter is usually concerned with i.i.d. data, important contributions beyond that case are presented in Wu and Zhao (2007), proving limit theorems for nonparametric change-point analysis under weak dependence. These results serve as an important ingredient for the present work. So far inference on structural breaks for continuous-time stochastic processes has attracted less attention. Let us mention the very recent work by Bücher

et al. (2017), which also deals with questions of detecting structural breaks of certain continuous-time stochastic processes. Our target of inference is the volatility process. Understanding the structure and dynamics of stochastic volatility processes is a highly important issue in finance and econometrics. Due to the outstanding role of volatility for quantifying financial risk, there is a vast literature on these topics.

Motivated by fundamental results in financial mathematics, the process modeling the logarithmic price of an asset belongs to the class of semimartingales. Whereas statistics for general semimartingales is less developed, a lot of work has been done if is an Itô semimartingale, that is, a semimartingale with a characteristic triple being absolutely continuous with respect to the Lebesgue measure. An overview on existing theory is available by Jacod and

Protter (2012). More precisely, our continuous-time model is

| (1) |

with the continuous part,

| (2) |

with a standard Brownian motion , the volatility process and the drift process . We define the pure-jump process through the Grigelionis representation

| (3) |

with a Poisson random measure having a compensator of the form with a -finite measure .

In this paper we are going to work with discrete observations and within the framework of infill asymptotics. That is, our data is generated by discretizing a path of the continuous-time stochastic process on a regular, equidistant grid. Though the model (1) is quite flexible, empirical evidence suggests that the recorded financial high-frequency data in applications does not follow a ‘true’ semimartingale. Therefore, an extension of model (1) incorporating microstructure noise is necessary. Market microstructure noise is caused by various trading mechanisms as discreteness of prices and bid-ask spread bounce effects. The observed data is modeled through

| (4) |

as a discretization of a continuous-time stochastic process , given by a superposition

| (5) |

with being a centered white noise process modeling the microstructure noise. This prominent additive noise model has attained considerable attention in the econometrics and statistics literature, let us refer to the book by Aït-Sahalia and Jacod (2014) for an overview. Infill asymptotics implies or, equivalently, . Whereas the drift process is not identifiable in a high-frequency framework, also without noise, quantities as the spot volatility process and the integrated volatility process , respectively, are identifiable. Since they constitute key quantities for an econometric risk analysis, there exists a rich literature on estimation theory. We refer to Jacod and Protter (2012) for a comprehensive presentation of these topics. This work is aimed to increase the understanding of the structure of the spot volatility process and to complement existing literature. The recent work by Bibinger et al. (2017) presents results on change-point detection for the model (1) without noise. We focus on a test that distinguishes continuous volatility paths from paths with volatility jumps. Inference on volatility jumps is currently of great interest in the literature, see, for instance, Jacod and Todorov (2010) and Tauchen and Todorov (2011). Moreover, it provides a necessary ingredient to analyze possible discontinuous leverage effects, see Aït-Sahalia et al. (2017) for a recent approach to this question. Inference on the volatility poses a challenging statistical problem, the volatility being latent and not directly observable. In the model (5) with microstructure noise, this becomes even more involved. The only work we are aware of addressing inference on volatility jumps in this model is by Bibinger and Winkelmann (2018) who extend the test for contemporaneous price and volatility jumps by Jacod and Todorov (2010) to noisy observations. Restricting to finitely many price-jump times, their results do not render general inference on volatility jumps. In this work we will extend the methods and results presented in Bibinger et al. (2017) in order to construct a general test for volatility jumps based on the model (5). Our statistics are functionals of spectral spot volatility estimates building up on the local Fourier method of moments in Altmeyer and Bibinger (2015) extending the volatility estimation approach introduced by Reiß (2011). While several linear estimators for functionals of the volatility have by now been generalized to noise-robust approaches, the considered change-point test is based on maximum statistics and its extension to an efficient method under noise requires new techniques.

The key theorem for the test is a limit theorem under the null hypothesis with an extreme value limit distribution of Gumbel-type. In particular, a clever rescaling of differences of local spot volatility estimates, quite different from the statistics considered in Bibinger et al. (2017), yields an asymptotic distribution-free test. In a certain sense, our test for volatility jumps complements the prominent Gumbel-test for price jumps proposed by Lee and Mykland (2008) and further studied by Palmes and Woerner (2016a) and Palmes and Woerner (2016b). An extension of the Gumbel-test for price jumps to noisy observations is given in Lee and Mykland (2012). We prove that our Gumbel-test for volatility jumps is consistent. Similar to the price-jump test, it facilitates also detection of the jump times – the change points. One main difficulty to prove the limit theorem is to uniformly control the spot volatility estimation errors.

The paper is organized as follows. Section 2 introduces the testing problem and the assumptions. Section 3 constructs the test. We begin with the test for a continuous semimartingale which is then extended to the general case utilizing truncation techniques. Section 4 establishes the asymptotic theory including the limit theorem under the null hypothesis, consistency of the test and consistent estimation of the change point under the alternative hypothesis. In Section 5 we conduct a Monte Carlo simulation study. The main insight is that the new test considerably increases the power compared to (optimally) skip sampling the noisy data to lower frequencies and applying the not noise robust method by Bibinger et al. (2017) directly. Section 6 gathers the proofs.

2 Testing problem and theoretical setup

We will develop a test for volatility jumps. We aim to test for some càdlàg squared volatility process hypotheses of the form

| (6) | ||||

It is standard in the theory of statistics of high-frequency data to address such questions path-wise. This means that and are formulated for one particular path of the squared volatility and we strive to make a decision based on discrete observations of the given path of . The semimartingale is defined on a filtered probability space . We need further assumptions on the coefficient processes of .

Assumption 2.1.

The processes and are locally bounded. is almost surely strictly positive, that is, .

Our notation for jump processes follows Jacod and Protter (2012).

Assumption 2.2.

Suppose is locally bounded for some deterministic non-negative function which satisfies for some :

| (7) |

The smaller , the more restrictive Assumption 2.2. The case is tantamount to jumps of finite activity.

On the null hypothesis, we allow for very general and rough continuous stochastic volatility processes.

Hypothesis (-).

Under the null hypothesis, the modulus of continuity

is locally bounded in the sense that there exists and a sequence of stopping times , such that , for some and some (almost surely finite) random variables .

The regularity exponent is selected for the testing problem. The test can be repeated for different values also. The regularity exponent coincides with a usual Hölder exponent when is a fix constant. Integrating a sequence enables us to include stochastic volatility processes in our theory. Since stochastic processes as Brownian motion are not in some fix Hölder class, it is crucial to work with (slightly) more general smoothness classes determined by the exponent and by . Observe that if

then the Kolmogorov Čentsov Theorem implies that

if arbitrarily slowly. In particular, we can impose that for our derivation of upper bounds in the sections below. The null hypothesis is the same as in Assumption 3.1 of Bibinger et al. (2017). Our test distinguishes the null hypothesis from alternative hypotheses of the following type.

Alternative (-).

In particular, the alternative hypothesis does not restrict to only one jump. We establish a consistent test when at least one non-negligible jump is present. Multiple jumps and quite general jump components are possible. Consistency of our test only requires that in a small vicinity of , and are sufficiently regular such that the jump is detected. Bibinger et al. (2017) impose in their Theorem 4.3 the condition that all volatility jumps are positive. This condition is replaced here by the semimartingale assumption on . Both ensure that can not be compensated by opposite jumps in an asymptotically small vicinity. In order to incorporate microstructure noise, we have to extend the original probability space. We set . The data generating process is defined on the filtered probability space . The construction can be pursued such that the process remains a semimartingale on the extension with the same characteristic triplet and the same Grigelionis representation. For the details of the construction we refer to Chapter 16 in Jacod and Protter (2012). For the noise process, we impose further assumptions.

Assumption 2.3.

The stochastic process is defined on and fulfills the following conditions.

-

(1)

is a centered white noise process, , and with

-

(2)

The following moment condition holds.

(8)

It is well-known that can be estimated in this model with -rate by either a rescaled realized volatility or from the negative first-lag autocovariances of the noisy increments. Under Assumption 2.3, Zhang et al. (2005) provide a rate-optimal consistent estimator for :

| (9) |

Remark 2.4.

The moment condition (8) is standard in related literature, see, for instance, Assumption (WN) of (Aït-Sahalia and Jacod, 2014, page 221) or Assumption 16.1.1 of Jacod and Protter (2012), but in a certain sense purely technical. Let us stress that in our setting, we do impose as less assumptions as possible on the volatility process . More precisely, the regularity under (-), for arbitrarily small , requires the existence of all moments in (8). More precisely, the smaller , the larger has to be chosen. Nevertheless, we point out that the moment condition is not that restrictive for standard models of volatility. In the usual case, for instance, where itself is assumed to be an Itô semimartingale, when , only the existence of moments up to order has to be imposed.

Remark 2.5.

While Assumption 2.3 is in line with standard conditions on the additive noise component in the literature, possible generalizations with respect to the structure of the noise process in three directions are of interest: serial dependence, heterogeneity and endogeneity. Such generalizations are also motivated by stylized facts in econometrics, see Hansen and Lunde (2006) for a detailed discussion. For instance, Chapter 16 in Jacod and Protter (2012) includes conditional i.i.d. noise, endogenous as it may depend (in a certain way) on , in the theory of pre-average estimators. This allows to model phenomena as noise by price discreteness (rounding). Bibinger and Winkelmann (2018) provide some first extensions of spectral spot volatility estimation to serially correlated and heterogeneous noise. Though the possible extensions appear to be relevant for applications, we work in the framework formulated in Assumption 2.3, mainly due to the lack of groundwork sufficient for the present work. Since we exploit some ingredients from previous works on spectral volatility estimation, particularly the form of the efficient asymptotic variance based on Altmeyer and Bibinger (2015), a generalization of our results requires non-trivial generalizations of these ingredients first. Furthermore, more general noise processes ask for extensive work on the estimation of the local long-run variance replacing (9). This topic, however, is beyond the scope of this work. Let us remark that it is as well not obvious how to apply strong embedding principles in these cases to generalize our proofs. Since Wu and Zhao (2007) provide strong approximation results for weakly dependent time series, we nevertheless conjecture that certain generalizations in the three directions are possible.

3 The statistical methods

3.1 The continuous case

In this paragraph, we construct the test first for the model without jumps, that is, we assume that

The construction of the test is based on a combination of the techniques by Altmeyer and Bibinger (2015) and Bibinger et al. (2017). In order to do so, we pick a sequence with

| (10) |

and .

The observation interval is split into bins of length , such that each bin is given by

Furthermore, we consider the orthonormal systems, given by

with

We define, for any stochastic process , the increments by

and the spectral statistics

The squared volatility can be estimated locally by a parametric estimator through oracle versions of bias corrected linear combinations of the squared spectral statistics,

| (11) |

with variance minimizing oracle weights , given by

| (12) |

The empirical scalar products , for any functions and , are given by

The order in (10) ensures that the error by discretization of the signal part and the error due to noise are balanced.

In a second step we split the observation interval by some “big blocks” with length :

where is some -valued sequence fulfilling as :

| (13) |

for some and the regularity exponent under the null hypothesis (-). Using spectral estimators and averaging within each big block provides a consistent estimator for :

| (14) |

A feasible adaptive estimation is obtained by a two-stage method where from (9) and

| (15) |

are inserted in the oracle weights to derive feasible estimated weights . The result (15) has been established and used in previous works on spectral volatility estimation, see Bibinger and Winkelmann (2018). The pilot volatility estimator (15) is an average of squared bias corrected spectral statistics over Fourier frequencies and bins. For some fix and an optimal choice of , it renders a rate-optimal estimator for which the -term in (15) is . A sub-optimal choice of will not affect our results, however. Other weights than (12) do not yield an asymptotically efficient estimator with minimal asymptotic variance. With estimated versions of the optimal weights (12), Altmeyer and Bibinger (2015) show that a Riemann sum over the estimates (11) yields a quasi-efficient estimator for the integrated squared volatility. Hence, we use the statistics (11) with exactly these weights and the orthogonal sine basis motivated by the efficiency results of Reiß (2011). Finally, with adaptive versions of the local volatility estimators (14)

| (16) | ||||

our test statistic is given by

| (17) |

where , with from (9). We write the absolute value in the denominator, since due to the bias correction in (11) the statistics and are not guaranteed to be positive.

Remark 3.1.

-

1.

The construction of the test statistic (17) is based on the idea to compare the values of the spot volatility process on intervals and and to reject the null hypothesis of no jumps, if the test statistic fulfills for some accurate sequence .

-

2.

The statistic (17) significantly differs from the statistic given in Equation (13) of Bibinger et al. (2017) beyond replacing spot volatility estimates by noise-robust spot volatility estimates. Though both statistics are quotients, the underlying structure of them is different. Whereas in Bibinger et al. (2017) the simple structure of the (asymptotic) variance of spot volatility estimates allows to use statistics based on their quotients, (17) is based on differences rescaled with their estimated variances. The statistics which are used to wipe out the influence of the noise process imply that volatility does not simply “cancel out” in our case as in Proposition A.3 of Bibinger et al. (2017). The construction of (17) is particularly appropriate from an implementation point of view, since it scales to obtain an asymptotic distribution-free test and makes it possible to avoid pre-estimation of higher order moments.∎

In order to increase the performance of the statistic, we also include a statistic based on overlapping big blocks:

| (18) |

with given by

3.2 The discontinuous case

In this paragraph, we generalize the method to be robust in the presence of jumps in (1). When is our target of inference, the jumps are a nuisance quantity. In order to eliminate jumps of in the approach, we consider truncated spot volatility estimates

| (19) |

with a truncation exponent . Truncated volatility estimators have been introduced first for integrated volatility estimation by Mancini (2009) and Jacod (2008). We define the test statistics with the truncated spot volatility estimates (19)

| (20a) | ||||

| (20b) | ||||

4 Asymptotic theory

4.1 Limit theorem under the null hypothesis

The hypothesis test formulated in Section 2 is based on asymptotic results for the statistics and , constructed in Section 3.

Theorem 4.1.

Theorem 4.1 is a key tool tackling the testing problem which is based on non-overlapping big blocks. The following result covers the case of overlapping big blocks.

Corollary 4.2.

We extend this result to the setup with jumps in when using truncated functionals.

Proposition 4.3.

It is natural that we derive the same limit results as above, since the truncation aims to eliminate the nuisance jumps. Proposition 4.3 gives rather minimal conditions, in particular (23), under that we can guarantee that the truncation works in this sense.

Remark 4.4.

Condition (23) ensures that different error terms in the proof of Proposition 4.3 are asymptotically negligible. Though we state it in terms of upper bounds on the jump activity , it rather puts restrictions on the interplay between , and . Given from (-), we choose close to to attain the highest possible power of the test. This results in , where the case for appears the most relevant one including a test for jumps in a semimartingale volatility process. Rewritten in terms of bounds on , (23) gives:

For finite activity, , we only have mild lower bounds on the choice of . Usually, a choice of close to 1 is advocated in previous works on truncated volatility estimation. For , this requires . The different error terms under noise for the maximum obtained here actually suggest that is an even better choice when we require only . Overall, the conditions on the jumps are not much more restrictive than required for central limit theorems of linear volatility estimators, see Chapter 13 of Jacod and Protter (2012). Compared to Proposition 3.5 of Bibinger et al. (2017), we relax the conditions on by a more sophisticated strategy of our proof. In particular, we do not have to restrict to a Lévy-type process with independent increments, since we work with Doob’s submartingale maximal inequality instead of Kolmogorov’s maximal inequality. With this strategy it is also possible to generalize the result in Proposition 3.5 of Bibinger et al. (2017).

4.2 Key ideas of the proof of the limit results

Since the proofs of the results stated in Section 4.1 are quite long, we want to sketch the key ideas of the proof shortly. The details are worked out in Section 6.

Starting with the continuous case, for the results given in Theorem 4.1 and Corollary 4.2, the main ingredients are described as follows. In the first step we carry out the crucial approximation where we show that the error, replacing the true log-price increments of by Brownian increments multiplied with a locally constant approximated volatility, is negligible. More precisely, we show that the spectral statistics are adequately approximated through with the volatility approximated constant over the big blocks. The analogues of after the approximation are denoted , given in (32).

In the second step, we conduct a time shift with respect to the volatility in to approximate the volatility by the same constant in the differences .

The third step is to replace the estimated asymptotic standard deviation in the denominator in (17) by its stochastic limit. The latter step is essentially completed by a Taylor expansion. Finally, we establish in a fourth step that the difference between the statistics using (14) with oracle weights and the statistics using (16) with adaptive weights is sufficiently small to extend the results to the feasible statistics.

The approximation steps combine Fourier analysis for the spectral estimation with methods from stochastic calculus. Disentangling the approximation errors of maximum statistics requires a deeper study than for linear statistics. After an appropriate decomposition of the terms, we frequently use Burkholder, Jensen, Rosenthal and Minkowski inequalities to derive upper bounds.

The final step is to apply strong invariance principles by Komlós

et al. (1976) and to apply results from Sakhanenko (1996) to conclude with Lemma 1 and Lemma 2, respectively, in Wu and Zhao (2007). Concerning the non-overlapping statistics we need Lemma 1, whereas the overlapping case needs the more involved limit result presented in Lemma 2 of Wu and Zhao (2007).

In order to prove Proposition 4.3, we show that under the stated conditions the jump robust statistics provide the same limit as in the continuous case. That is, the jumps do not affect the limit at all. We decompose the additional error term by truncation in several terms of different structure which we prove to be asymptotically negligible under the mild conditions (23) on the jump activity and its interplay with the truncation and smoothing parameters. We use Doob’s maximal submartingale inequality to bound one crucial remainder without imposing a more restrictive Lévy structural assumption as has been used in Bibinger

et al. (2017).

4.3 Rejection rules and consistency

Based on the limit results presented in Section 4.1, we can summarize the following rejection rules. Thereto, let be the -quantile of the Gumbel-type limit law of in the limit theorems. Since the latter is absolutely continuous with respect to the Lebesgue measure, there is a unique solution, given by

Theorem 4.5.

Consistency of the test means that under the alternative hypothesis, if for some we have that for some fix , the power of the test, for instance by (25), tends to one as :

Theorem 4.1 ensures that (25) facilitates an asymptotic level--test that correctly controls the type 1 error, that is,

Thereby, even for small , the test can distinguish continuous volatility paths from paths with jumps.

Remark 4.6.

The rate in (21), (22), (24a) and (24b) determines how fast the power of the test increases in the sample size . The convergence rate, for close to the upper bound in (13), is close to . The latter coincides with the optimal convergence rate for spot volatility estimation under noise, see Munk and Schmidt-Hieber (2010). In light of the lower bound for the testing problem without noise established in Bibinger et al. (2017) and the relation of the models with and without noise studied in Gloter and Jacod (2001), we conjecture that the above test yields an asymptotic minimax-optimal decision rule. A formal generalization of the proof for the detection boundary from Theorem 4.1 of Bibinger et al. (2017) to our setting however appears not to be feasible, since it heavily exploits simple -approximations of squared increments.

4.4 Consistent estimation of the change point

In this subsection, we present an estimator for the change point , which is of importance, once we have decided to reject (-). Therefore, we suppose (-) and that there exists one with . The aim is to estimate , in general referred to as the change point or break date in change-point statistics, which here gives the time of the volatility jump. We suggest the estimator , given by

| (29) |

where

It is sufficient to use these modified non-rescaled versions of the statistics in (18). We prove the following consistency result for our estimator.

Proposition 4.7.

Remark 4.8.

Put another way, we can detect jump times associated with sequences of jump sizes as as long as in the sense of weak consistency. Choosing as small as possible, such that (13) is satisfied, yields the best possible rate, while for the testing problem in Theorem 4.1 we select as large as possible. In the optimal case, a jump with fix size can be detected with a convergence rate close to . This provides important information how precisely volatility jump times can be located under noisy observations. With jumps in , we conjecture that an analogous results holds true under the conditions of Proposition 4.3. A sequential application of our methods allows for testing and the estimation of multiple change points. The extension of the estimation from the one change to the multiple change-point alternative is accomplished similarly to Algorithm 4.9 from paragraph 4.2.2. in Bibinger et al. (2017).

5 Simulations and a bootstrap adjustment

In this section we investigate the finite-sample performance of the new method in a simulation study. We also analyze the efficiency gains of our noise-robust approach based on the spectral volatility estimation methodology in comparison to simply skip sampling the data and applying the non noise-robust method from Bibinger et al. (2017). Skip sampling the data, which means we only consider every 60th datapoint, reduces the dilution by the noise and is a standard way to deal with high-frequency data in practice. We consider observations of (5), a typical sample size of high-frequency returns over one trading day. The noise is centered and normally distributed with a realistic magnitude, , see, for instance, Bibinger et al. (2018). We implement the same volatility model as in Section 5 of Bibinger et al. (2017), where

| (30) |

is a semimartingale volatility process fluctuating around the seasonality function

| (31) |

where and , with a standard Brownian motion independent of . We set and the drift . We perform the simulations in R using an Euler-Maruyama discretization scheme.

5.1 Performance of the test, comparison to skip sampling, bootstrap adjustment and sensitivity analysis

Concerning the jumps of and under the alternative hypothesis, we implement two different model configurations. In order to grant a good comparison to Bibinger et al. (2017) in the evaluation of the efficiency gains by our method instead of a skip-sample approach, we adopt in Section 5.1 the setup from Section 5 of Bibinger et al. (2017). There, under the alternative hypothesis, the volatility admits one jump of size at time . The jump size equals the range of the expected continuous movement. Under the alternative hypothesis, admits a jump at the same time . Under the null hypothesis and the alternative hypothesis, also jumps at some uniformly drawn time. All price jumps are normally distributed with expected size and variance . More general jumps are considered in Section 5.2.

We consider the test statistic (20b) with overlapping blocks and truncation. Section 5.2 confirms that it outperforms the non-overlapping version (20a). We set and . Robustness with respect to different choices of and is discussed below. For the truncation, we set according to Remark 4.4. In all cases, we compute the adaptive feasible statistics and do not make use of the generated volatility paths to derive the weights (12). We rather rely on the two-stage method and insert (15) with and (9) in the statistics. The spectral estimates from (11) are computed as sums up to the spectral cut-off , smaller than , as the fast decay of the weights (12) in , compare also (48), renders higher frequencies completely negligible. The investigated test statistics will be identically feasible in data applications.

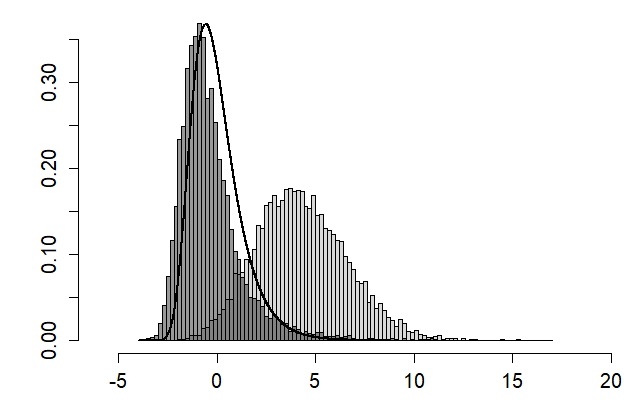

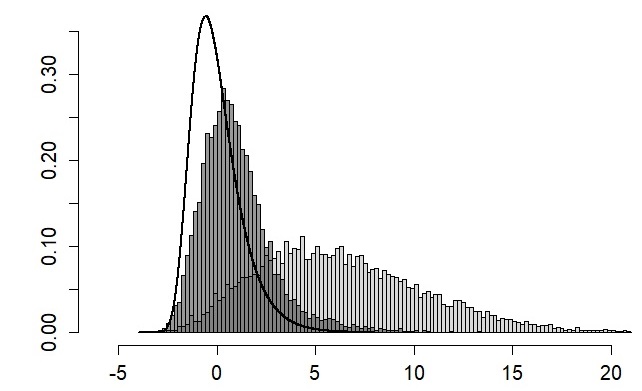

Figure 1 visualizes the empirical distribution from Monte Carlo iterations under the null hypothesis and the alternative hypothesis. The left plot shows our statistics while the right plot gives the results for the statistics from Bibinger

et al. (2017) applied to a skip sample of 500 observations. The skip-sampling frequency has been chosen to maximize the performance of these statistics. While they are reasonably robust to minor modifications, too large samples lead to an explosion of the statistics also under the null hypothesis and much smaller samples result in poor power. The length of the smoothing window for the statistics given in Equation (24) of Bibinger

et al. (2017) is set , adopted from the simulations in Bibinger

et al. (2017). In the optimal case, null and alternative hypothesis are reasonably well distinguished by the skip-sampling method – but the two plots confirm that our approach improves the finite-sample power considerably. For the spectral approach, of the outcomes under exceed the -decile of the empirical distribution under . For the optimized skip-sample approach this number reduces to . The approximation of the limit law appears somewhat imprecise. The relevant high quantiles, however, fit their empirical counterparts quite well.

Nevertheless, we propose a bootstrap procedure to fit the distribution of under with improved finite-sample accuracy. We start with an estimator for the spot volatility , from , using the same and as for the test. We also define and compute , averaging over the available number of blocks, smaller than , back in time. In order to smooth the random fluctuations of the spot volatility pre-estimates, we apply a filter to the estimates of length 30 with equal weights and denote , the resulting estimated volatility path. At the boundaries we interpolate linearly to and , respectively. Repeating each entry times, we obtain a (bin-wise constant) estimator . For two sequences of i.i.d. standard normals , and , denote with

a pseudo path generated with the estimated volatility path and estimated noise variance and the . We can iterate the procedure as a Monte Carlo simulation and produce different pseudo paths using independent generalizations of random variables . With

we derive the pseudo test statistic

In fact, the truncation with the indicator function is obsolete, since we do not have jumps in the pseudo samples. For a test, we can use the approximative (conditional) quantiles

and compute based on Monte Carlo approximation. We reject when

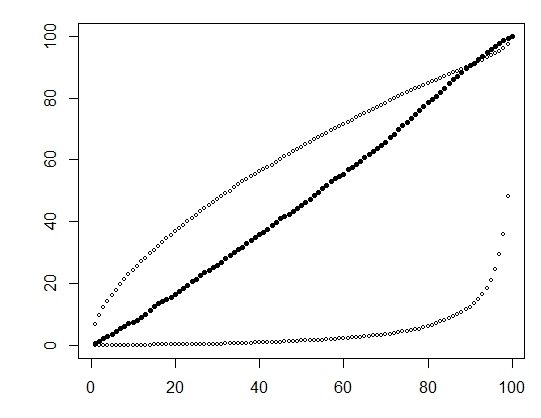

In the left plot of Figure 2 the black dots compare the empirical percentiles of the left-hand side in (24b), the standardized versions of , under to the ones of the bootstrap, i.e. . The finite-sample accuracy of the bootstrap for the distribution under is significantly better than the limit law (light points). Since the high percentiles of bootstrap and limit law are quite close, the power of both tests is comparable. For a level test, we obtain approx. power using the limit law and power using the bootstrap. For a level test, we obtain approx. and , respectively.

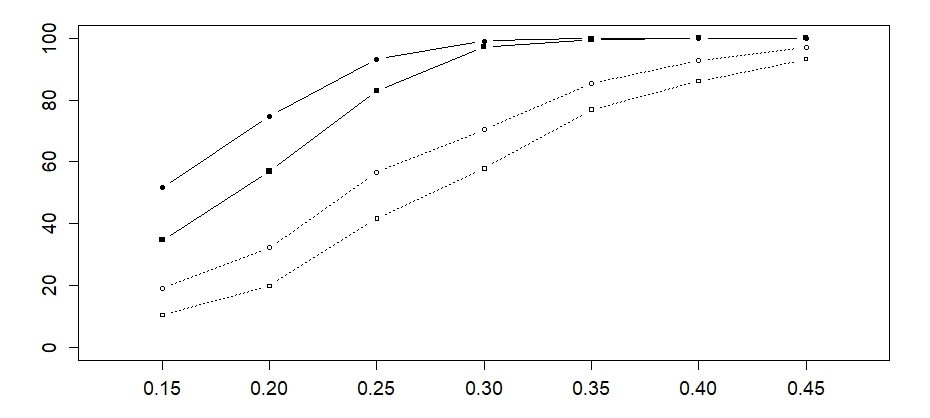

Finally, we consider different parameter configurations . Since we can exploit the bootstrap to ensure a good fit under , we concentrate on the ability of to distinguish hypothesis and alternative. To quantify the ability to separate and , we visualize the relative number of exceedances under of the empirical quantile under . We plot the percentage numbers in the right plot of Figure 2 over a grid of different values for . Additionally, we draw the marginal curve for at points (black line). Choosing a different (reasonable) quantile under does not change the shape of the surface with respect to the values of . Figure 2 confirms that the test is reasonably robust with respect to different values of the tuning parameters. For sufficiently large, setting between and yields the highest power. For , values between 60 and 180 grant a good performance. Hence, we choose and as suitable configuration for the simulation study.

5.2 Comparison of tests with overlapping and non-overlapping statistics

We illustrate the improvement in the power of the test based on (20b) compared to the non-overlapping version (20a). Here, we use a prominent general model for jumps of often considered in related literature, including Jacod and Todorov (2010), with a predictable compensator . Since jumps of very small absolute sizes are not generated, the truncation works well and we do not see a manipulation of the empirical distribution of the test statistics due to errors in the truncation step. We investigate the power of the tests for different volatility-jump sizes under the alternative, . The volatility-jump time is randomly generated in each run according to a uniform distribution on . Note that not excluding the boundary intervals would slightly reduce the power in all configurations, since the test is not able to detect jumps in these boundary blocks. In order to include common price and volatility jumps, we add an additional price jump at with uniformly distributed size as according to above. We keep to the parameters , and and compute the adaptive statistics as in Section 5.1 in iterations.

Figure 3 confirms that the test using (20b) with overlapping statistics has a significantly higher power than the test based on (20a) and non-overlapping statistics. The largest difference for is 17.8% at 10% testing level and for , 14.8% at 5% testing level. Thus, for volatility jumps with moderate absolute size in the range considered in Figure 3, the overlapping statistics attain relevant efficiency gains. The location of the volatility jump – when the boundaries are excluded – does not affect the power of the tests. Figure 3 illustrates increasing power of both tests as gets larger. It also reveals that volatility jumps with are difficult to detect in our setting where this corresponds only to approximately 20 times the average absolute increment . Due to the required smoothing over blocks we cannot expect to detect such small volatility jumps with good power. We can further report a better accuracy of the theoretical limit law under from Proposition 4.3 for the empirical distribution of the statistics with overlapping compared to non-overlapping blocks. The average amount of realizations of simulated statistics (20a) exceeding the theoretical 90%-percentile is 9.99% and exceeding the 95%-percentile 6.41%. For the statistics (20b) these values are 21.00% and 11.11%, respectively.

6 Proofs

6.1 Proof of Theorem 4.1

For notational convenience, we replace

and

respectively.

We also introduce the following notation, adapting the elements of the spectral statistics on each big block.

Set

and

Furthermore, we define the big block-wise spectral statistics

and the associated variance minimizing oracle weights

We further introduce the bias correction terms

We can strengthen the assumptions, presented in Assumption 2.1 and (-), as follows. We replace local boundedness of , , and the modulus of continuity under (-) by global boundedness. We refer to Section 4.4.1 of Jacod and Protter (2012) for a proof and the construction through localization. We set

with

| (32) |

Finally we fix some constants , such that almost surely

The first step described in Section 4.2 is accomplished in the next proposition.

Proof of Proposition 6.1.

Since we can proceed as follows.

The reverse triangle inequality and the decomposition

yield the following decomposition:

| (33) |

Starting with in (33) we proceed as follows.

For all and , such that , the following holds:

| (34) |

In (34) we dropped the dependence on the constants and for notational convenience. We start with the term . We split the term into various summands in the following way:

That yields

| (35) |

In order to handle , we rewrite the spectral statistics , for any stochastic process , using step functions , given by

which yield

for any semimartingale .

By virtue of the Itô process structure of , we obtain that

Itô’s formula yields

with

Similarly,

with

For notational brevity, we suppress the dependence of and , respectively, on . We bound via

where

and

Starting with we employ Markov’s inequality, applied to the function , and :

The identity

implies, together with Jensen’s inequality, that

Concerning the second inequality we have taken into account, that in order to apply Jensen’s inequality a second time.

We employ the generalized Minkowski inequality for double measure integrals, which implies

| (36) |

In order to bound the expectation in (36), we apply Burkolder’s inequality to the local martingale part. The general case can be handled via the elementary inequality and the standard bound for Lebesgue integrals

| (37) |

applied to the finite variation part. Taking into account, that the quadratic variation process, , is given by

yields

| (38) |

(38) is a consequence of (37),

| (39) |

and the global boundedness of . Consequently the above yields

Taking into account that

we can conclude, if , that

For the term , we start with

| (40) |

In (40) the triangle inequality and Jensen’s inequality are applied. Combining the regularity under (-) and (13) gives

Concerning we use further decompositions rewriting

| (41) |

in the following way:

| (42) | |||

| (43) | |||

| (44) |

Using this decomposition, we can bound via

We start with the probability involving the summand (42). We have to bound the probability

where we have applied Markov’s inequality with some exponent and . Set

In order to apply Itô isometry, we set , with some and . We derive that

where we have again used the Minkowski inequality for double measure integrals. Since and are disjoint if and is fixed, we get

We proceed with Jensen’s inequality, which yields

Using (39), global boundedness of the volatility and (38) we can conclude that

Consequently, we can conclude as follows using (38):

| (45) |

That yields the following bound for

for sufficiently large.

We proceed with the probability involving the term (43). We first get the standard bound by the Markov inequality with some exponent and :

We define

In order to apply Itô isometry, we set , with and . We obtain that

We have that

by the regularity under (-). Overall, we can deduce for that

if sufficiently large. Proceeding with , we have with and :

| (46) | |||

Analogously, we set

With , and we apply Itô isometry and Minkowski inequality.

Since and are disjoint if and is fixed, we get

where we applied Jensen’s inequality. Proceeding with Burkholder’s inequality and (37), we get

which gives the following bound concerning :

if is sufficiently large. We have completed the third term and so . Overall, the term has shown to be negligible. We proceed with from (35). Therefore, we take into account that

| (47) |

Using this identity, we bound by

where the probability is based on the local martingale part in (47) and is based on the finite variation part. The elementary inequality allows to split the discussion of . Starting with we proceed as follows using Markov’s inequality with an exponent and .

We define

such that with , and

In order to bound this expectation, we split the -sum using the elementary inequality and that the weights fulfill the following growth behaviour:

| (48) |

That yields

Since

it is sufficient to consider the first summand only.

The calculations pursued in Lemma 2 in Bibinger and

Winkelmann (2018) imply the following, using the fact, that is independent of .

such that

We can conclude that

Overall, we get

if is sufficiently large.

The term can be handled easier, using (37) instead of Burkholder’s inequality. Overall, it is shown that .

We can proceed with from (34). Note that

It is sufficient to bound the probability

Note that and , such that we can proceed with Markov’s inequality with an exponent and the elementary inequality :

by the classical central limit theorem. This implies

if sufficiently large. Thus, we have completed the term , and so the term (II).

We proceed with (I) from (33). It holds that

such that for every we have

| (49) | |||

| (50) |

We start with the second probability (50).

The second probability has already been considered, since

Concerning the first one, it holds that

Since

we can proceed with (49). For every and , it holds that

| (51) | |||

| (52) | |||

We start with (51).

| (53) | |||

| (54) |

Note that

holds. We proceed with the triangle inequality and using that uniformly in ,

Applying the Markov inequality, bounding the volatility from above, and concluding with a classical central limit theorem argument, yields the bound

such that

holds if the exponent is sufficiently large. This completes (53), since the first probability therein is included in .

We proceed with (54). The discussion of this term can be traced back to with a Taylor expansion. More precisely,

we set and expand around the point ,

Since , and since the remainder is negligible,

by the reverse triangle inequality and the estimates for . Therefore, only

is crucial. But, using the reverse triangle inequality again this has already been worked out in , too. So we have completed (54) and so (51). We proceed with (52). It holds that

Thus, this probability has already been considered within (53). Therefore, we also have completed (52), such that we are done with

The terms and in (33) are only shifted in . So we have finished the proof of Proposition 6.1.

∎

For the second step described in Section 4.2 we approximate the volatility locally constant over two consecutive blocks by shifting the index of in as follows: . We set

Proof of Proposition 6.2.

The decomposition

yields, via the triangle inequality, the three terms

We start with (III). For any it holds that

| (55) | |||

| (56) |

The probability (56) has already been done, since it only differs by a shift in with respect to the volatility from the term in Proposition 6.1. We continue with (55). It holds that

That yields

Concerning the first term it holds that

It remains to show that

We conclude with a classical central limit theorem argument, using Markov’s inequality with .

with sufficiently large. We have completed (55) and so (III).

We proceed with (I). For any it holds that

| (57) | |||

| (58) |

We start with (58).

Only the second probability has to be considered. But, since the involved statistic only differs by a shift in the volatility, we can bound the latter from below and argue with the central limit theorem. So we have completed (58) and continue with (57).

We handle (57) via a Taylor expansion. So, expanding the function around the point yields the desired result using the procedure for (III). We will omit the details for (II), since it only differs by a shift in . So Proposition 6.2 is proven.

∎

We do a further approximation step, replacing the denominator in Proposition 6.2 by its limit. This is the third step outlined in Section 4.2. Here, we use the estimator from (9).

Proof of Proposition 6.3.

We have to bound the term

We will employ a 2-dimensional Taylor expansion of order 1 with respect to the second term. We set and expand around the point . Therefore, we have to bound the term

| (59) |

Since can be bounded globally, we get the following uniform bounds in :

The first summand in (59) with can be handled easily, using

This implies

Proceeding with the second term in (59), we need a bound for the uniform error. It can be obtained in a similar (in fact easier) way as for the term in (34). Such a bound is already given in Bibinger and Reiß (2013) on page 10 for the estimators in (15) with , and readily extends to the case . Since is the rate-optimal choice, we get with the upper bound from Bibinger and Reiß (2013) that

Proceeding with the term

we conclude similarly with the triangle inequality,

the uniform bound applied to each summand and the regularity of under the null hypothesis (-). This implies

such that the convergence in Proposition 6.3 follows.

∎

In order to conclude the convergence for the adaptive statistics in Theorem 4.1, we have to show that replacing the oracle versions by the adaptive statistics does not affect the limit. It is sufficient to show the following for the fourth step to complete the proof of the approximation steps mentioned in Section 4.2.

Proof of Proposition 6.4.

As we have argued above, can be replaced by the -rate consistent estimator (9) without affecting the limit behaviour of the statistics. Therefore it is sufficient to consider the plug-in estimation of the spot volatility in the weights . First of all, taking into account that the asymptotic order of the weights (48) do not depend on , we may consider them as a function of the spot volatility. Calculating the first derivative, as pursued on page 40 in Altmeyer and

Bibinger (2015), we get the upper bound

| (60) |

In order to bound , take into account that for every . So, it is sufficient to consider the term

The only difference compared with Bibinger and Winkelmann (2018) and Altmeyer and Bibinger (2015), is to replace the point-wise bound for by the uniform bound from Proposition 6.3, with that the bound

follows, using the mean value theorem and (60).

∎

The key, proving the last conclusion is to apply strong invariance principles by Komlós

et al. (1976). First of all, we have to take into account, that the rescaling factors in provide only an asymptotically distribution-free limit. So it is more adequate for our purpose to rescale with the exact finite-sample standard deviation, that is

Using a Taylor approximation and the convergence of the above variances to , presented in Section 6.2. of Altmeyer and

Bibinger (2015), it is clear that the approximation holds.

Let and be the exact finite-sample variances and define and given by

The distributions of and do not depend on the volatility. Therefore, and due to the independence of Brownian increments, the latter are two independent families. Furthermore, the independence of Brownian increments also yields that each family itself forms an independent family in . Taking into account the remark in Komlós et al. (1976) below Theorem 4, we can proceed as follows. Since we want to ensure the existence of a properly approximating independent Gaussian family , according to Theorem 4 in Komlós et al. (1976), we have to pick a function such that

| (61) |

| (62) |

| (63) |

We pick a power function and set with some such that (61) and (62) are fulfilled. For the latter condition (63), by Jensen’s inequality and Rosenthal’s inequality, we require at this point (8) up to . In order to control the remainder term in the approximation, we take into account that

Furthermore, the triangle inequality and the Markov inequality yield

Applying (1.6) in Sakhanenko (1996), we get

where is the positive constant given in (1.6) in Sakhanenko (1996). We set

Since there are more bins than big blocks, the conditions of Theorem 4 in Komlós et al. (1976) are fulfilled. Furthermore, we can choose by (13) such that

So the remainder term fulfills

Let be the Brownian Motion in the invariance principle. This implies, that the family defined as

are i.i.d. standard normal variables. We set

The scaling properties of Brownian motion and the upper bound given for the remainder term give the desired result using Lemma 1 in Wu and Zhao (2007) applied to .

∎

6.2 Proof of Corollary 4.2

The proof of Corollary 4.2 works along the same lines as the one of Theorem 4.1. More precisely,

-

1.

in a first step, we have to show that the overlapping versions can be replaced by . In a second step, we

-

2.

have to do a shift in the volatility and proceed

-

3.

by showing that the estimated asymptotic standard deviations can be replaced by their limits and that

-

4.

the difference between oracle and adaptive versions is asymptotically negligible, where the final step is to

-

5.

use a limit theorem for extreme value statistics similar to Lemma 1 in Wu and Zhao (2007). The appropriate tool for the overlapping versions is given by Lemma 2 in Wu and Zhao (2007), which can be directly applied choosing as the rectangular kernel. The latter works, since even if the big blocks may intersect, it is crucial that the bins remain to be disjoint.

Starting with (a) we will argue that the estimates provided in the proof of Theorem 4.1 are sufficient to conclude the limit for the overlapping statistics. We have to show that

The triangle inequality, the decomposition (33) and a Taylor expansion yield that it is sufficient to prove

The key step proving this is to consider the term corresponding to in (34). It is basically sufficient to translate the terms and to the overlapping case. Starting with we have to take into account the fact, that in the overlapping case, the index set, is a factor times larger than the index set for the non-overlapping case. But, since we can adapt the exponent in the Markov inequality by (8), we get a similar upper bound for . Considering the corresponding part to the term we proceed as follows using Assumption (-) and (39):

Concerning (b) we have to show that

Again, after a proper decomposition of the terms and a Taylor expansion, it is sufficient to show that

The discussion of this term works very similar as in the non-overlapping case. Using (-) and the central limit theorem, as presented above, we can conclude the desired asymptotic behaviour by adapting the exponent in the Markov inequality. The third and fourth steps (c) and (d) are analogues of Propositions 6.3 and 6.4. Since the upper bound, which is presented in Bibinger and Reiß (2013), is not affected for overlapping big blocks, we omit the details. Concerning (e) let us only mention, that an additional tool which is necessary, is Lévy’s modulus of continuity theorem in order to control the discretization error. Then, the limit (21) in Corollary 4.2 is an immediate consequence of Lemma 2 in Wu and Zhao (2007).

6.3 Proof of Proposition 4.3

We decompose the process with the continuous semimartingale part

and write for the statistics (16) applied to observations of a process where the jump part is eliminated. We begin with some preliminaries for the proof. Throughout this proof, is a generic constant that may change from line to line. For a sequence of counting processes with , with from Assumption 2.2, we have by (13.1.14) from Jacod and Protter (2012) that

| (64) |

with from (7). We may restrict to the more difficult result for with overlapping statistics. With an analogous decomposition as in (33), the proof reduces to

| (65) |

We separate bins on that truncations occur from (most) other bins

and consider the two terms separately. For the second maximum the term with is the most involved one and we prove that

| (66) |

With some the relation

can be used to decompose the term in two addends. First, we prove that

| (67) |

Using the elementary estimate and that , we obtain the bound

| (68) |

We deduce the upper bound

We decompose this term as follows

where we use the triangle inequality, that if , and elementary inequalities for the maximum. We begin with . It holds for arbitrarily small that

with from (64). The additional indicator function in the last addend may be added, since when there is at most one jump on the bin. By (64) with and , we obtain for the Poisson process :

for all , and we infer that

We used that by (13), since , for the first term and that by Condition (23):

| (69) |

Define the sequence of random variables

We have that

From equation (54) of Aït-Sahalia and Jacod (2010), we obtain the bounds

| (70a) | ||||

| (70b) | ||||

Observe that

Since is a martingale, is a submartingale as the martingale increments are uncorrelated and a squared martingale is always a submartingale. We apply Doob’s submartingale maximal inequality which yields

| (71) |

such that for . Thus, is negligible as long as

| (72) |

From Condition (23) we have that and it follows that , what ensures the above relation. Under this condition, becomes negligible as well, since with (64) for and , we obtain that

We have proved (67). Finally, we show that

| (73) |

and discuss the similar remaining second term for (66). With some , we use the relation

With Markov’s inequality, we obtain that

| (74) | ||||

using moment bounds from Lemma 2 of Bibinger and Winkelmann (2018) under condition (8). We derive that

| (75) |

for arbitrary . In particular, for from (13)

With (68), we obtain the estimate

Since for , we have by (64) that

we may consider instead

It is thus sufficient to show that

for some where we have applied an inequality analogous to (64). This holds true, since

and by Condition (23). Using (68), (74) and that the squared jumps are summable, we obtain that for with

| (76) |

This is sufficient for

| (77) |

Equations (67) and (76) imply Equation (66). Maxima of the terms with cross terms and can be handled similarly (or with Cauchy-Schwarz) and are of smaller order. Equations (66) and (73) imply Equation (65) what finishes the proof of Proposition 4.3. ∎

6.4 Proof of Theorem 4.5

We have to show that (25), (26), (27) and (28) yield asymptotically tests with power 1. Concerning (25), that is, under (-),

| (78) |

We set

| (79) |

with

For , set . For , set . Since , for sufficiently large. By the reverse triangle inequality, we get:

First of all, we can conclude by Theorem 4.1 that for all :

Then we take into account that the sum over is convex and is already bias corrected with respect to the noise part. Furthermore, bounding the volatility from below, using the Itô isometry and

we obtain that with a constant :

with

Note that the denominator in (79) can be ‘absorbed’ by the constant . We give a lower bound on . Under the alternative hypothesis (-), we have for the continuous volatility part that

The jump component of the volatility is most difficult to handle for . If it satisfies (7) with some , we derive for some constant dependent on the bound

| (80) |

With and for , we thus obtain for that

and an analogous bound for . Thus, we obtain that

where we have applied the reverse triangle inequality. This implies (78). In the non-overlapping case, two neighboring differences incorporate the volatility jump. Our above definition of ensures that we consider the most affected one for the lower bound. A corresponding lower bound for in the overlapping case becomes simpler as we always include statistics over two neighboring blocks, such that is close to the end-point between the two blocks. Proving that

under (-), is an immediate consequence of Theorem 4.1. This completes the proof for (25). We omit further details concerning (26), (27) and (28), since the estimates we have presented above can be readily adapted. ∎

6.5 Proof of Proposition 4.7

We adopt the following elementary lemma, related to Lemma B.1 in Aue et al. (2009) and Lemma D.1. in Bibinger et al. (2017).

Lemma 1.

Let and be functions on such that is non-negative and increasing. As long as for some , we have that

An analogous result holds if and are functions on and is decreasing.

Proof.

Since

we derive that

such that . ∎

Let be the change point, that is, the jump time of the volatility. Without loss of generality . Define , the smallest integer such that holds. We use the following decomposition of for :

where

with the path of the volatility from that the jump is eliminated:

By definition, then fulfills the regularity properties on (-). This implies that

Under (-), we obtain uniformly in that almost surely

This is sufficient for

From the proof of Theorem 4.1, we can thus conclude the following bound:

Next, we consider a step-wise defined function given by

and being step-wise defined via

The function fulfills

-

1.

is monotonically increasing and

-

2.

is monotonically decreasing.

We get the following representation of :

The calculations above imply that

| (81) |

Furthermore, for , with any , it holds that

with a probability tending to one as . Therefore,

for those with a probability tending to one as . For a sequence , with , it holds that

and

When we set

we derive with (81) that almost surely for sufficiently large:

Therefore, satisfies the conditions of Lemma 1. This implies that

An analogous procedure applied to the function yields that

Overall, this yields

which completes the proof of Proposition 4.7. ∎

References

- Aït-Sahalia and Jacod (2010) Aït-Sahalia, Y. and J. Jacod (2010). Is Brownian motion necessary to model high-frequency data? The Annals of Statistics 38(5), 3093–3128.

- Aït-Sahalia and Jacod (2014) Aït-Sahalia, Y. and J. Jacod (2014). High-frequency financial econometrics. Princeton, NJ: Princeton University Press.

- Altmeyer and Bibinger (2015) Altmeyer, R. and M. Bibinger (2015). Functional stable limit theorems for quasi-efficient spectral covolatility estimators. Stochastic Processes and their Applications 125(12), 4556–4600.

- Aue et al. (2009) Aue, A., S. Hörmann, L. Horváth, and M. Reimherr (2009). Break detection in the covariance structure of multivariate time series models. The Annals of Statistics 37(6B), 4046–4087.

- Aït-Sahalia et al. (2017) Aït-Sahalia, Y., J. Fan, R. J. A. Laeven, C. D. Wang, and X. Yang (2017). Estimation of the continuous and discontinuous leverage effects. Journal of the American Statistical Association, forthcoming.

- Bibinger et al. (2018) Bibinger, M., N. Hautsch, P. Malec, and M. Reiß (2018). Estimating the spot covariation of asset prices – statistical theory and empirical evidence. Journal of Business and Economic Statistics, forthcoming.

- Bibinger et al. (2017) Bibinger, M., M. Jirak, and M. Vetter (2017). Nonparametric change-point analysis of volatility. The Annals of Statistics 45(4), 1542–1578.

- Bibinger and Reiß (2013) Bibinger, M. and M. Reiß (2013). Spectral estimation of covolatility from noisy observations using local weights. Scandinavian Journal of Statistics 41(1), 23–50.

- Bibinger and Winkelmann (2018) Bibinger, M. and L. Winkelmann (2018). Common price and volatility jumps in noisy high-frequency data. Electronic Journal of Statistics 12(1), 2018–2073.

- Bücher et al. (2017) Bücher, A., M. Hoffmann, M. Vetter, and H. Dette (2017, 05). Nonparametric tests for detecting breaks in the jump behaviour of a time-continuous process. Bernoulli 23(2), 1335–1364.

- Gloter and Jacod (2001) Gloter, A. and J. Jacod (2001). Diffusions with measurement errors 1 and 2. ESAIM Probability and Statistics 5, 225–242.

- Hansen and Lunde (2006) Hansen, P. R. and A. Lunde (2006). Realized variance and market microstructure noise. Journal of Business & Economic Statistics 24(2), 127–161.

- Jacod (2008) Jacod, J. (2008). Asymptotic properties of realized power variations and related functionals of semimartingales. Stochastic Processes and their Applications 118(4), 517–559.

- Jacod and Protter (2012) Jacod, J. and P. Protter (2012). Discretization of processes. Springer.

- Jacod and Todorov (2010) Jacod, J. and V. Todorov (2010). Do price and volatility jump together? The Annals of Applied Probability 20(4), 1425–1469.

- Komlós et al. (1976) Komlós, J., P. Major, and G. Tusnády (1976). An approximation of partial sums of independent RV’s, and the sample DF. II. Z. Wahrscheinlichkeitstheorie und Verw. Gebiete 34(1), 33–58.

- Lee and Mykland (2008) Lee, S. and P. A. Mykland (2008). Jumps in financial markets: A new nonparametric test and jump dynamics. Review of Financial Studies 21, 2535–2563.

- Lee and Mykland (2012) Lee, S. and P. A. Mykland (2012). Jumps in equilibrium prices and market microstructure noise. Journal of Econometrics 168, 396–406.

- Mancini (2009) Mancini, C. (2009). Non-parametric threshold estimation for models with stochastic diffusion coefficient and jumps. Scandinavian Journal of Statistics 36(4), 270–296.

- Munk and Schmidt-Hieber (2010) Munk, A. and J. Schmidt-Hieber (2010). Lower bounds for volatility estimation in microstructure noise models. In J. O. Berger, T. T. Cai, and I. M. Johnstone (Eds.), Borrowing Strength: Theory Powering Applications – A Festschrift for Lawrence D. Brown, Volume 6 of Collections, pp. 43–55. Beachwood, Ohio, USA: Institute of Mathematical Statistics.

- Palmes and Woerner (2016a) Palmes, C. and J. H. C. Woerner (2016a). The gumbel test and jumps in the volatility process. Statistical Inference for Stochastic Processes 19(2), 235–258.

- Palmes and Woerner (2016b) Palmes, C. and J. H. C. Woerner (2016b). A mathematical analysis of the gumbel test for jumps in stochastic volatility models. Stochastic Analysis and Applications 34(5), 852–881.

- Reiß (2011) Reiß, M. (2011). Asymptotic equivalence for inference on the volatility from noisy observations. The Annals of Statistics 39(2), 772–802.

- Sakhanenko (1996) Sakhanenko, A. I. (1996). Estimates for the accuracy of constructions on a probability space in the central limit theorem. Rossiĭskaya Akademiya Nauk. Sibirskoe Otdelenie. Institut Matematiki im. S. L. Soboleva. Sibirskiĭ Matematicheskiĭ Zhurnal 37(4), 919–931, iv.

- Tauchen and Todorov (2011) Tauchen, G. and V. Todorov (2011). Volatility jumps. Journal of Business and Economic Statistics 29, 356–371.

- Wu and Zhao (2007) Wu, W. B. and Z. Zhao (2007). Inference of trends in time series. Journal of the Royal Statistical Society. Series B. Statistical Methodology 69(3), 391–410.

- Zhang et al. (2005) Zhang, L., P. A. Mykland, and Y. Ait-Sahalia (2005). A tale of two time scales: Determining integrated volatility with noisy high-frequency data. Journal of the American Statistical Association 100(472), 1394–1411.