Checking Validity of Monotone Domain Mean Estimators

Cristian Oliva , Mary C. Meyer and Jean D. Opsomer Department of Statistics, Colorado State University, Fort Collins, Colorado, USA, 80523

coliva@colostate.edumeyer@stat.colostate.edujopsomer@stat.colostate.edu

( Updated version by )

Abstract

Estimates of population characteristics such as domain means are often expected to follow monotonicity assumptions. Recently, a method to adaptively pool neighboring domains was proposed, which ensures that the resulting domain mean estimates follow monotone constraints. The method leads to asymptotically valid estimation and inference, and can lead to substantial improvements in efficiency, in comparison with unconstrained domain estimators. However, assuming incorrect shape constraints could lead to biased estimators. Here, we develop the Cone Information Criterion for Survey Data (CICs) as a diagnostic method to measure monotonicity departures on population domain means. We show that the criterion leads to a consistent methodology that makes an asymptotically correct decision choosing between unconstrained and constrained domain mean estimators.

1 Introduction

Monotone population characteristics arise naturally in many survey problems. For example, average salary might be increasing in pay grade, average cholesterol level could be decreasing in physical activity time, etc. In large-scale surveys, there is often interest in estimating the characteristics of domains within the overall population, including those of domains with small sample sizes. One possibility to handle small domains is to apply small area estimation methods. However, that requires switching from the design-based to a model-based paradigm, which can be undesirable. An alternative approach is to remain within the design-based paradigm but take advantage of qualitative assumptions about the population structure, when such are available.

Isotonic regression has been widely studied outside of the survey context. Some remarkable works on this topic include Brunk, (1955), VanEeden, (1956), Brunk, (1958), Robertson et al., (1988), and Silvapulle and Sen, (2005). In contrast, merging isotonic regression techniques into survey estimation and inference has just been studied recently. Wu et al., (2016) considered the case when both sampling design and monotone restrictions are taking into account on the domain estimation. They proposed a design-weighted constrained estimator by combining domain estimation and the Pooled Adjacent Violators Algorithm (PAVA) (Robertson et al.,, 1988). Further, they showed that their proposed constrained estimator improved estimation and variability of domain means, under both linearization-based and replication-based variance estimation.

Although the constrained estimator proposed by Wu et al., (2016) improves the precision of the usual survey sampling estimators, it has to be used carefully since invalid population constraint assumptions could lead to biased domain mean estimators. The main objective of this work is to develop diagnostic methods to detect population departures from monotone assumptions. Particularly, we propose the Cone Information Criterion for Survey Data (CICs) as a data-driven method to determine whether or not it is better to use the constrained estimator to estimate the population domain means. The Cone Information Criterion (CIC) was originally developed for the i.i.d. case by Meyer, 2013a .

In Section 2, we describe the constrained estimator proposed by Wu et al., (2016) and explain some of its properties such as adaptive pooling domain and linearization-based variance estimation. Section 3 contains the proposed CICs along with some of its theoretical properties. In particular, we show that CICs is consistently choosing the correct estimator based on the underlying shape of the population domain means, in the sense that with probability going to 1 as the sample size increases, CICs will determine that pooling of domains that violate monotonicity constraints is unwarranted. Section 4 demonstrates the performance of the CICs under a broad variety of simulation scenarios. In Section 5 we apply our CICs methodology to the 2011-2012 National Health and Nutrition Examination Survey (NHANES) laboratory data. Lastly, Section 6 states some general conclusions of the work developed in this paper, and contains a brief discussion about future related areas of research.

2 Constrained Domain Mean Estimator for Survey Data

We begin by reviewing the survey setting and the constrained estimator proposed by Wu et al., (2016). Consider a finite population , and let denote a domain for . Assume that constitute a partition of the population . Denote as the population size of domain . Given a study variable , let be the population domain means,

Suppose we draw a sample using the probability sampling design . Let be the sample size of . We are going to consider the case where the sampling design is measurable, i.e., both first-order and second-order inclusion probabilities are strictly positive, where is the indicator variable of whether or not. Denote as the corresponding sample in domain obtained from . Further, let . For simplicity in our notation, we will omit the subscript from these and related quantities from now on.

Consider the problem of estimating the population domain means . When no qualitative information is assumed on the population domains, we can consider either the Horvitz-Thompson estimator (Horvitz and Thompson,, 1952) or the frequently preferred Hájek estimator (Hájek,, 1971), which are given by

(1)

respectively, where . We will refer to them as unconstrained estimators of . Note that both estimators in Equation 1 consider only the information contained in domain , leading to large standard errors on domains with small sample sizes.

Suppose now that we want to include monotonicity assumptions into the estimation stage of domain means. For instance, assume the population domain means are isotonic over the domains. That is, (analogously, , but which we will not further consider explicitly here). Wu et al., (2016) proposed a domain mean estimator that respect monotone constraints, given by the ordered vector which optimizes

(2)

The objective function in Equation 2 can be written in matrix terms as , where , , is a consistent estimator of , and .

Following Brunk, (1955), the general closed form solution for the constrained problem in Equation 2 can be expressed as the set of pooled weighted domain means given by

(3)

where for . Moreover, we can make use of the Pooled Adjacent Violator Algorithm PAVA (Robertson et al.,, 1988) along with and the weights to compute efficiently the constrained estimator . Observe that the constrained estimator in Equation 3 consists of adaptively collapsing neighboring domains. Furthermore, the above procedure can be simplified in the obvious way when applied to the Horvitz-Thompson estimator with weights , leading to the constrained estimator vector with entries of the form . We refer to Wu et al., (2016) for a discussion of the properties of these constrained estimators, including design consistency and asymptotic distribution.

We conclude this section by defining some of the quantities we will use in the development of the CICs. Note that the estimator has a random weighted projection matrix associated with it, which is defined by the pooling obtained from the PAVA and the weights . That is, is the matrix such that . For example, suppose and that PAVA chooses to pool domains 1 and 2, but not to pool domain 2 and 3. Hence, , and . Then,

Let be the unbiased estimator of the covariance matrix of , given by

where . Further, for any , let be the pooled population mean of domains through . That is,

and .

For any indexes such that and , let , be the Hájek estimators of and , respectively. By standard linearization arguments (Särndal et al.,, 1992, Chapter 5), the approximated covariance of and is given by

(4)

Moreover, given that for all , a design consistent estimator of the approximate covariance in Equation 4 is

(5)

where .

3 Main results

In this section, we present the Cone Information Criterion for Survey Data (CICs). The CICs is a tool that may be used to validate the monotone estimator in Equation 2 as an appropriate estimator of population domain means. In what follows, we define the CICs for the Horvitz-Thompson estimator and propose a natural extension that applies to the Hájek setting. Further, main properties of the CICs are shown along with their theoretical foundation.

3.1 Cone Information Criterion for Survey Data (CICs)

For the Horvitz-Thompson estimator, we define the CICs as

(6)

where is the projection matrix associated with .

The proposed CICs shares similar features with the Akaike Information Criterion (AIC) (Akaike,, 1973) and the Bayesian Information Criterion (BIC) (Schwarz,, 1978), which have been broadly used for model selection. The first term measures the deviation between the constrained estimator and the unconstrained estimator , while the second term can be seen as a penalty for the complexity of the constrained estimator. The penalty term is large when the number of different groups chosen by the constrained estimator is also large, meaning that the number of different parameters to estimate (or effective degrees of freedom) of the constrained estimator is high.

The development of proceeds similarly as for the Cone Information Criterion (CIC) proposed by Meyer, 2013a . Its motivation comes from properties of the Predictive Squared Error (PSE) under the Horvitz-Thompson setting, which is defined as

(7)

where is the vector of Horvitz-Thompson domain mean estimators obtained from a sample that is independent to , where is drawn using the same probability sampling design as . Furthermore, define the Sum of Squared Errors (SSE) as

We define CIC as an estimator of PSE that involves SSE. Proposition 1 establishes a relationship between PSE and SSE; its proof and all subsequent ones are included in the Appendix.

Proposition 1. .

Motivated by Proposition 1, an estimate of PSE can be derived by estimating both and . The first term has a straightforward unbiased estimator SSE, and an estimator for the covariance term can be obtained using the observed pooling on . As we will show later, the latter term can be estimated by the asymptotically unbiased estimator under certain assumptions. That produces the proposed CICs in Equation 6.

However, recall that the use of the Horvitz-Thompson estimator requires information about the population domain sizes , which is not frequently the case in many practical survey applications. Therefore, analogously to Equation 6, we extend the CICs to the Hájek setting by using the estimator instead of SSE, and instead of ; where denotes the estimator of the covariance matrix of and , which is based on the observed pooling of and is defined element-wise as

Hence, the proposed CICs for the Hájek estimator setting is

(8)

3.2 Assumptions

In order to state properly our theoretical results, we need to consider some required assumptions.

(A1)

The number of domains is a fixed known constant.

(A2)

The non-random sample size satisfies .

(A3)

.

(A4)

for . Also, for some constants and any integers such that , then with .

(A5)

For all , , , and .

(A6)

, where denotes the set of all distinct tuples from .

(A7)

.

(A8)

.

Assumption (A1) states that the number of domains will not change as the population size changes. Assumption (A2) declares that the sample size is asymptotically strictly less than the population size but greater than zero, which intuitively means that the sample and the population size are of the same order. The boundedness property of the finite population fourth moment in Assumption (A3) is used several times in our proofs to show that the approximated scaled covariances in Equation 4 are asymptotically bounded, and also, that their estimators are consistent for them. In addition, Assumption (A4) is used to assure that the population size and the subpopulation size are of the same order. Further, it establishes that the pooled population domain means converge to some constant limiting domain means with rate . The consistency result of CICs is based on whether the constants are strictly monotone or not. Assumption (A5) implies that both first and second-order inclusion probabilities can not tend to zero as increases. Moreover, this assumption states that the sampling design covariances () tend to zero, i.e., sampling designs that produces asymptotically highly correlated elements are not allowed. Lastly, Assumptions (A6)-(A8) are similar to the higher order assumptions considered by Breidt and Opsomer, (2000). These assumptions involve fourth moment conditions on the sampling design. These assumptions hold for simple random sampling without replacement and for stratified simple random sampling with fixed stratum boundaries (Breidt and Opsomer,, 2000).

3.3 Properties of CICs

Under above assumptions, CIC has the property of being an asymptotically unbiased estimator of PSE when the pooling obtained from applying the PAVA to the vector with weights is unique. To show that, we first prove that there are certain poolings which are chosen with probability tending to zero as tends to infinity. This is stated in Theorem 1, which makes use of the Greatest Convex Minorant (GCM).

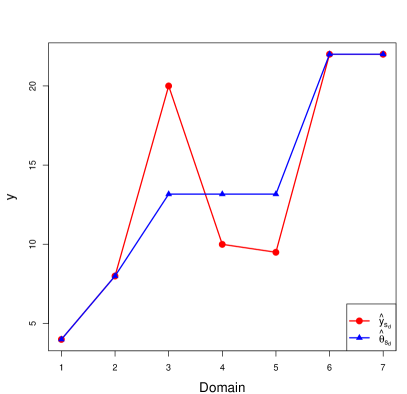

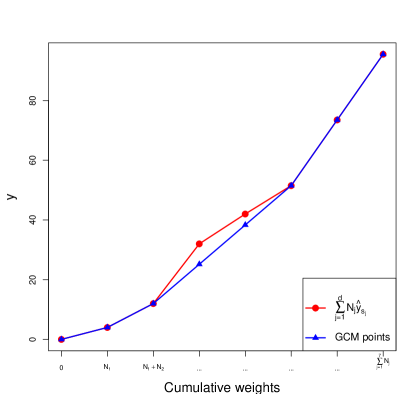

The GCM provides of an illustrative way to express monotone estimators. Figure 1 displays an example of sample domain means with their respective monotone estimates (Figure 1(a)), and a plot of their corresponding cumulative sum diagram and GCM (Figure 1(b)). The GCM is conformed by points, indexed from 0 to , and their left-hand slopes are the values. The points indexed by 0 and are the boundaries of the GCM, and the rest are its interior points. Three possible scenarios can be identified for each of the interior points: the slope of the GCM changes (corner points); the GCM slope does not change and the cumulative sum coincides with the minorant (flat spots); or the GCM slope does not change but the cumulative sum is strictly above the minorant (points above the GCM). The example displayed in Figure 1(b) shows that the indexes 1, 2, 5 correspond to corner points, the index 6 to a flat spot, and the indexes 3, 4 to points above the GCM. In particular, note that flat spots correspond to cases where consecutive domain means are equal ().

(a)Sample domain means and monotone estimates.

(b)Cumulative sum diagram and GCM.

Figure 1: GCM example.

Theorem 1. Let and , for , where , and . Also, let be the GCM points of the cumulative sum diagram with points . Define and to the indexes of points strictly above and indexes of its corner points, respectively. Based on the sample , define and , with , and let , , , and be the analogous sample quantities of , , , and . Denote and to be the events where and , respectively. Then, and .

To have a better understanding of Theorem 1, note that for every pair of mutually exclusive sets , , there are certain poolings (groupings) allowed by to obtain . In particular, if (i.e. no flat spots), then there is a unique pooling allowed by . Speaking somewhat loosely and referring to ‘bad poolings’ to those poolings of that are chosen with zero asymptotic probability, Theorem 1 states that bad poolings correspond to those pairs of disjoint sets , that do not satisfy and .

One case of particular interest is when there are no flat spots on the GCM corresponding to , i.e., . Such scenario is equivalent than saying that, asymptotically, there is a unique pooling allowed by . Moreover, under this scenario, it can be proved (Theorem 2) that the proposed CICs in Equation 6 is an asymptotic unbiased estimator of the PSE in Equation 7.

Theorem 2. If , then CICPSE+.

In practice, the proposed CICs can be used as a decision tool that validates the use of the constrained estimator as an estimate of the population domain means. The decision rule would be to choose the estimator, either the constrained or the unconstrained, that produces the smallest CICs value. As we mentioned, CICs is an overall measure that balances the deviation of the constrained estimator from the unconstrained, as well as the complexity of such estimator. The fact that CICs measures the estimator complexity would avoid the undesired situation of choosing always the unconstrained estimator above the constrained estimator.

Although we will focus on the Hájek version of the CICs (Equation 8) for the rest of this section, it is important to remark that the following properties are also valid under the Horvitz-Thompson setting.

Let CIC and CIC denote the CICs values for the unconstrained and constrained estimators, respectively. From Equation 8, that is,

where . Similarly as AIC and BIC, we might choose the estimator that produces the smallest CICs value. We show that this decision rule is asymptotically correct when choosing the shape based on the limiting domain means (Theorem 5), and also, that the decision made from CICs is consistent with the decision made from PSE (Theorem 6). Theorems 3 and 4 contain theoretical properties of that are required to establish Theorem 5.

Theorem 3. For any domains where , ,

Furthermore,

Theorem 4. Let be the weighted isotonic population domain mean vector of with weights . Then,

Theorem 5.

P

when .

Theorem 3 states that the scaled is asymptotically bounded and also, that is a consistent estimator of with a rate of . Hence, both the covariance between and , and its proposed estimate are well defined. Theorem 4 establishes that the constrained estimator gets closer to the weighted isotonic population domain mean with a rate of . This theorem generalizes the results in Wu et al., (2016), where it was only considered the case when the limiting domain means are monotone. Recall that if and only if the population domain means are monotone increasing. Theorem 5 shows that CICs consistently chooses the correct estimator based on the order of the limiting domain means .

Finally, Theorem 6 establishes that the chosen estimator driven by PSE in Equation 7 is analogous to the decision made by CICs.

Theorem 6.

Observe that neither Theorem 5 nor Theorem 6 deal with the case where the vector entries of are non-strictly monotone. Although in that case we would like both PSE and CICs to choose the constrained estimator, neither of them is able to choose it universally. Nevertheless, we show in the Simulations section that the constrained estimator is chosen with a high frequency under the non-strictly monotone scenario.

4 Simulations

We demonstrate the CICs performance through simulations under several settings. We consider the set-up in Wu et al., (2016) as a baseline to produce our simulation scenarios.

For the first set of simulations, we generate populations of size using limiting domain means . Each element in the population domain is independently generated from a normal distribution with mean and standard deviation . That is, for a given domain , for . Samples are generated using a stratified simple random sampling design without replacement in all strata. The strata constitutes a partition of the total population of size . We make use of an auxiliary random variable to define the stratum membership of the population elements, with created by adding random noise to , for . Stratum membership of is then determined by sorting the vector , creating blocks of elements based on their ranks, and assigning these blocks to the strata. Also, we set , , , and . The number of replications per simulation is 10000.

The vector of limiting domain means is created using the sigmoid function given by for . We consider three different scenarios for : the monotone scenario, where ’s are strictly increasing; the flat scenario, where ’s are non-strictly increasing; and the non-monotone scenario, where ’s are not monotone increasing. The limiting domain means on the monotone scenario are given by for . The flat scenario is formed by “pulling down” until it is equal to , that is, where . For the non-monotone scenario, we pull down until it gets below by using . Note that the only difference among these three scenarios relies on the right tail. For each of the above scenarios, the total population size varies from . Further, the total sample size is divided among the 4 strata as for , which makes the sampling design informative. Once the sample is generated, the Hájek domain mean estimators are computed along with the CICs in Equation 8.

We consider the design Mean Squared Error (MSE) of any estimator given by

For each scenario mentioned above, we compute both the MSE for the unconstrained estimator MSE and for the constrained estimator MSE through simulations. In addition, we compute the MSE for the CICs-adaptive estimator , given by

Although there are no other existing methods that aim to choose between the unconstrained and the constrained estimator for survey data, we compare the performance of CICs versus two conditional testing methods that are based on the following hypothesis test under the linear regression model setting,

The first test is a naive Wald test which depends on the sample-observed pooling. For this, we compute the test statistic

and then compare it to a , where is the number of different estimated values on .

The second test is the conditional test proposed by Wollan and Dykstra, (1986). Even though the latter test is established for independent data with known variances, we use instead the estimated design variances of the sample-observed pooling obtained from Equation 5. To perform this, we compute the test statistic -as in the Wald test- but then we compare it to a with point mass of at , where is the probability that under the hypothesis . Note that the conditional test might perform similar as the Wald test when the number of domains is large.

Since both Wald and conditional tests require the variance-covariance matrix of the domain mean estimators to be non-singular, these could be performed only when the variance-covariance matrix formed by the estimates in Equation 5 is in fact a valid covariance matrix. We set the significance level of these tests at .

Tables 1, 2 and 3 contain the proportion of times that the unconstrained estimator is chosen over the constrained estimator under the monotone, flat and non-monotone scenarios, respectively. In cases where the unconstrained and constrained estimators agree (i.e. the unconstrained estimator satisfies the constraint), this is counted as a constrained estimator in the calculation of this proportion. The last two rows of these tables show the MSE of the constrained estimator and the CICs-adaptive estimator, relative to the MSE of the unconstrained estimator. The former ratio can be viewed as a measure of how much better (or worse) naively applying the constrained estimator is under the different scenarios, while the latter ratio shows how well the adaptive estimator is in terms of balancing the MSE’s of the constrained and unconstrained estimators.

From Table 1, we can note that CICs tends not to choose the unconstrained estimator under the monotone scenario as increases. In contrast, the unconstrained estimator is chosen most of the times under the non-monotone simulation scenario (Table 3). Flat scenario results (Table 2) show that although the proportion of times the unconstrained estimator is chosen do not tend to zero as grows, it is fairly small, meaning that CICs is choosing the constrained estimator most of the times. From these three tables, we can observe that CICs tends to be more conservative when choosing the unconstrained estimator over the constrained, in comparison with both Wald and conditional tests.

Table 1: Monotone scenario. . generated from . Based on 10000 replications. Rows 1-3: Proportion of times that unconstrained estimator is chosen using CICs, Wald test, and conditional test. Rows 4-5: MSE ratios.

CICs

0.061

0.016

0.005

0.045

0.014

0.004

0.022

0

Wald

0.018

0.003

0.001

0.012

0.002

0.001

0.005

0

Conditional

0.020

0.004

0.001

0.013

0.003

0.001

0.005

0

MSE/MSE

0.721

0.896

0.962

0.774

0.938

0.968

0.875

0.994

1

MSE/MSE

0.796

0.917

0.970

0.831

0.953

0.972

0.902

0.994

1

Table 2: Flat scenario. . generated from . Based on 10000 replications. Rows 1-3: Proportion of times that unconstrained estimator is chosen using CICs, Wald test, and conditional test. Rows 4-5: MSE ratios.

CICs

0.098

0.045

0.121

0.102

0.081

0.079

0.073

0.134

0.015

Wald

0.033

0.011

0.044

0.036

0.026

0.024

0.023

0.048

0.003

Conditional

0.038

0.013

0.047

0.040

0.029

0.026

0.025

0.052

0.004

MSE/MSE

0.720

0.860

0.906

0.789

0.898

0.906

0.844

0.918

0.942

MSE/MSE

0.813

0.902

0.972

0.869

0.953

0.959

0.901

0.985

0.959

Table 3: Non-monotone scenario. . generated from . Based on 10000 replications. Rows 1-3: Proportion of times that unconstrained estimator is chosen using CICs, Wald test, and conditional test. Rows 4-5: MSE ratios.

CICs

0.118

0.126

0.602

0.126

0.497

0.513

0.172

0.623

0.963

Wald

0.042

0.045

0.386

0.051

0.299

0.302

0.070

0.420

0.894

Conditional

0.048

0.049

0.403

0.056

0.310

0.315

0.073

0.434

0.899

MSE/MSE

0.712

0.854

1.346

0.695

1.211

1.224

0.860

1.400

2.705

MSE/MSE

0.814

0.928

1.128

0.807

1.115

1.118

0.945

1.137

1.037

On a second set of simulations, we consider the case where the population elements are generated from a skewed distribution. For a given domain , is generated from a distribution with degrees of freedom, for and . As in the first set of simulations, we consider the same three scenarios for using the sigmoid function. For each of them, we consider the case where and . Table 4 contains the results of this skewed case. Again, we can observe that CICs behaves as expected despite the skewness of the population generating distribution.

Table 4: Skewed case. . generated from . Based on 10000 replications. Rows 1-3: Proportion of times that unconstrained estimator is chosen using CICs, Wald test, and conditional test. Rows 4-6: MSE ratios.

Monotone

Flat

Non-monotone

CICs

0.029

0.003

0

0.052

0.079

0.138

0.193

0.326

0.693

Wald

0.014

0.001

0

0.024

0.031

0.055

0.114

0.172

0.573

Conditional

0.014

0.001

0

0.025

0.033

0.057

0.117

0.177

0.579

MSE/MSE

0.808

0.958

1

0.806

0.853

0.886

0.817

1.034

1.890

MSE/MSE

0.855

0.966

1

0.872

0.936

0.982

0.927

1.086

1.230

A third set of simulations considers the case where the domain mean estimators are more correlated in comparison with the stratified simple random sample simulations. The setting for this simulation set is basically equal to the first set, except that we use the auxiliary variable to create 100 clusters. Then, we sample clusters with equal probability. We let . We only consider the case where and for each of the three scenarios. Table 5 contains the simulation results for this correlated case. Note that CICs is choosing the unconstrained estimator with a low proportion under the monotone scenario, which is desired. However, the proportion of times that the unconstrained estimator is chosen under the non-monotone scenario is almost half in comparison of its corresponding stratified simple random sample simulation (see Table 3). The stars () in Table 5 mean that results for the Wald and the conditional tests are not available since the estimated variance-covariance matrix of the Hájek domain means is in fact a singular matrix. Recall that both tests need such matrix to be a valid covariance matrix in order to be performed. Note that on those cases with stars, CICs continues to be a plausible option to choose between the two estimators.

Table 5: Correlated case. . generated from . Based on 10000 replications. Rows 1-3: Proportion of times that unconstrained estimator is chosen using CICs, Wald test, and conditional test. Rows 4-6: MSE ratios.

Monotone

Flat

Non-monotone

CICs

0.194

0.025

0.005

0.245

0.085

0.069

0.284

0.461

0.696

Wald

*

0.011

0.001

*

0.071

0.035

*

0.417

0.574

Conditional

*

0.019

0.002

*

0.072

0.037

*

0.422

0.582

MSE/MSE

0.717

0.901

0.958

0.690

0.838

0.842

0.694

1.263

1.911

MSE/MSE

0.862

0.937

0.966

0.836

0.930

0.929

0.856

1.178

1.233

Table 5 shows that although the CICs performs as expected for the correlated case, the unconstrained estimator is being chosen only 69.6% of the times under the non-monotone scenario when the sample size is 20% of the total population. One plausible reason could be the fact that the monotonicity violation on this scenario is weak. Therefore, we would like to analyze the efficacy of the CICs as the violation of monotonicity increases. To do that, we consider again the correlated case. To increase the violation on the limiting domain means, we create from pulling down by a quantity , where . That is, . The results of this simulation case (Table 6) shows that the MSE ratio between the unconstrained and the constrained estimators overpass 1 as the violation increases. Moreover, the proportion of times that the unconstrained estimator is chosen also increases and approaches to 1 as expected.

Table 6: Increasing Monotonicity Violation - Correlated case. . generated from . Based on 10000 replications. Rows 1-3: Proportion of times that unconstrained estimator is chosen using CICs, Wald test, and conditional test. Rows 4-6: MSE ratios.

CICs

0.388

0.708

0.934

0.450

0.881

0.936

0.507

0.963

1

Wald

*

0.658

0.882

*

0.852

0.835

*

0.952

1

Conditional

*

0.664

0.885

*

0.854

0.890

*

0.953

1

MSE/MSE

0.798

1.963

3.554

0.882

2.999

3.617

1.022

4.302

9.037

MSE/MSE

0.962

1.233

1.107

1.002

1.169

1.109

1.059

1.081

1.000

We also perform simulations to study the behavior of CICs when the number of domains is larger than 4. We consider the case where . The values of are obtained from the sigmoid function . The setting in this 8-domain case is basically the same as the first simulation set, but using instead of , , and . We choose these values for and in order to have a similar rough average sample size in each domain as it was in simulations where . As shown in Table 7, CICs follows a similar behavior as in the previous simulations.

Table 7: 8-domain case. . generated from . Based on 10000 replications. Rows 1-3: Proportion of times that unconstrained estimator is chosen using CICs, Wald test, and conditional test. Rows 4-5: MSE ratios.

Monotone

Flat

Non-monotone

CICs

0.054

0.042

0.003

0.075

0.127

0.060

0.084

0.287

0.631

Wald

0.021

0.010

0.031

0.048

0.017

0.037

0.158

0.439

Conditional

0.023

0.010

0.034

0.049

0.017

0.041

0.159

0.441

MSE/MSE

0.666

0.902

0.975

0.648

0.877

0.961

0.666

0.935

1.162

MSE/MSE

0.719

0.921

0.978

0.710

0.918

0.978

0.731

0.970

1.047

We end this section by showing simulation results obtained using the exact same set-up as in Wu et al., (2016). To get the values, we use the sigmoid function . We set the population size as and the domain size as . We simulate the values from a normal distribution with mean and standard deviation . As it was done before, samples are generated from a stratified sampling design with simple random sampling without replacement in each of four strata; and the stratum membership was assigned using the auxiliary random variable .

We study four cases obtained by varying the number of domains ; and the standard deviation . The sample size is set to when , splitted as 25, 50, 50, 75 samples in each stratum; and when , splitted as 100, 200, 200, 300 samples in each stratum. For each case, we create 7 different cases for . These cases are determined by setting for ; and for . Note that corresponds to the flat scenario, meanwhile define monotone scenarios and define non-monotone scenarios.

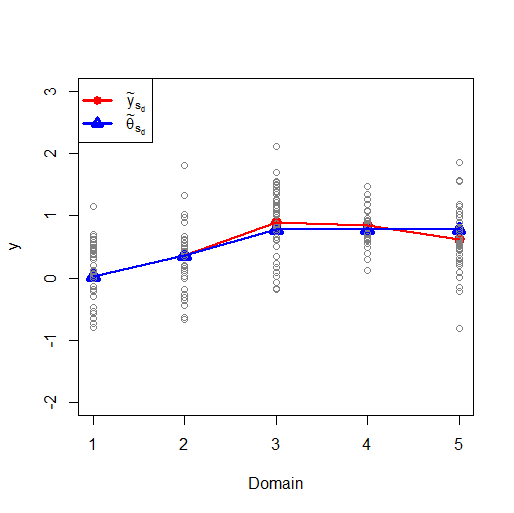

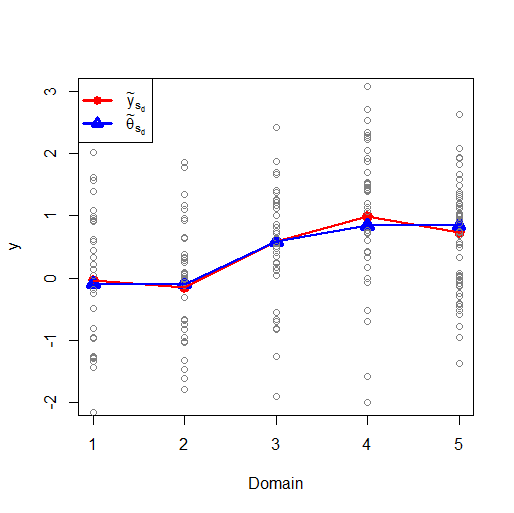

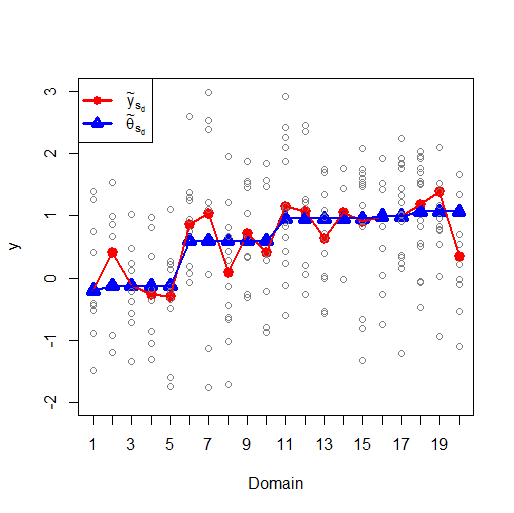

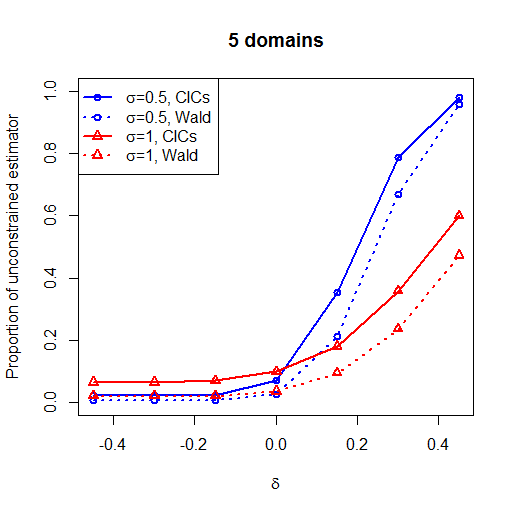

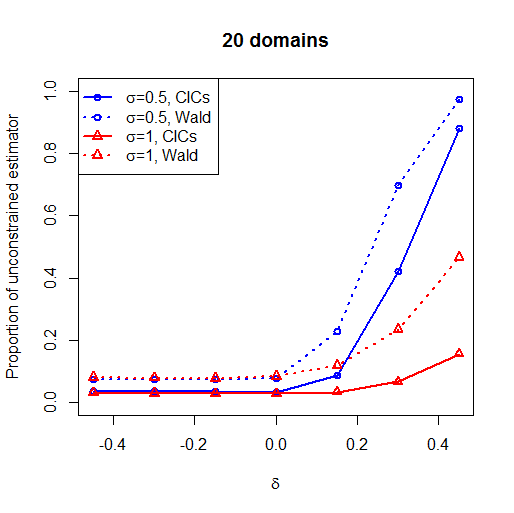

Figure 2 contains examples of one fitted samples for each of the four cases mentioned above. Note that the fact that the sigmoid function is considerably flat at its extremes makes especially complicated to decide whether the population domain means are isotonic or not, when . Tables 8-11 present the proportion of times that the unconstrained estimator is chosen in each case, along with MSE ratios. To visualize these results better, we create Figure 3 which contains plots of the proportion of times that the unconstrained estimator is chosen under CICs and Wald test, for the set values of . We ignore the results obtained by the conditional test since these are shown to be practically the same as lead by the Wald test (see Tables 8-11).

Plots in Figure 3 demonstrates that both CICs and Wald test perform better when the standard deviation is smaller. Figure 3(a) shows that CICs tends to choose more the unconstrained estimator than the Wald test, when . This fact provides evidence that the CICs does better than the Wald test under non-monotone scenarios. In contrast, Figure 3(b) shows an opposite behavior between CICs and Wald test. The worst performance for both CICs and Wald test is shown when and . In this case, CICs chooses the constrained estimator more than 80% of times, meanwhile Wald test choose it a little less than 60% of times, although is desirable to never choose it. However, it can be seen in Table 11 that the MSE ratio of the constrained estimator over the unconstrained estimator does not show neither a clear preference for the latter estimator.

(a), .

(b), .

(c), .

(d), .

Figure 2: One fitted samples for each of four cases obtained using . Dots correspond to unconstrained estimates, triangles to constrained estimates.

Table 8: . . Based on 10000 replications. Rows 1-3: Proportion of times that unconstrained estimator is chosen using CICs, Wald test, and conditional test. Rows 4-5: MSE ratios.

Monotone

Flat

Non-monotone

CICs

0.023

0.023

0.024

0.072

0.352

0.787

0.980

Wald

0.006

0.006

0.006

0.026

0.212

0.667

0.958

Conditional

0.006

0.006

0.006

0.026

0.213

0.668

0.959

MSE/MSE

0.882

0.880

0.857

0.781

0.957

1.822

3.479

MSE/MSE

0.911

0.909

0.887

0.849

1.013

1.153

1.036

Table 9: . . Based on 10000 replications. Rows 1-3: Proportion of times that unconstrained estimator is chosen using CICs, Wald test, and conditional test. Rows 4-5: MSE ratios.

Monotone

Flat

Non-monotone

CICs

0.065

0.065

0.070

0.099

0.181

0.358

0.600

Wald

0.021

0.021

0.021

0.036

0.095

0.236

0.473

Conditional

0.022

0.021

0.021

0.036

0.095

0.237

0.474

MSE/MSE

0.806

0.788

0.747

0.704

0.732

0.915

1.296

MSE/MSE

0.875

0.858

0.826

0.807

0.861

1.012

1.145

Table 10: . . Based on 10000 replications. Rows 1-3: Proportion of times that unconstrained estimator is chosen using CICs, Wald test, and conditional test. Rows 4-5: MSE ratios.

Monotone

Flat

Non-monotone

CICs

0.037

0.037

0.036

0.034

0.087

0.422

0.881

Wald

0.074

0.074

0.073

0.078

0.229

0.697

0.972

Conditional

0.074

0.074

0.073

0.078

0.229

0.697

0.972

MSE/MSE

0.503

0.503

0.495

0.468

0.556

0.905

1.533

MSE/MSE

0.539

0.539

0.530

0.503

0.625

0.994

1.075

Table 11: . . Based on 10000 replications. Rows 1-3: Proportion of times that unconstrained estimator is chosen using CICs, Wald test, and conditional test. Rows 4-5: MSE ratios.

Monotone

Flat

Non-monotone

CICs

0.031

0.030

0.028

0.028

0.034

0.067

0.156

Wald

0.081

0.079

0.078

0.084

0.119

0.235

0.466

Conditional

0.081

0.079

0.078

0.084

0.119

0.235

0.466

MSE/MSE

0.415

0.410

0.398

0.386

0.402

0.475

0.617

MSE/MSE

0.451

0.445

0.431

0.420

0.441

0.540

0.723

(a).

(b).

Figure 3: Proportion of times that the unconstrained estimator is chosen under the 4 scenarios of , for several values of . Solid lines: CICs, dotted lines: Wald test. Dots: , triangles: .

5 Real data application: NHANES data

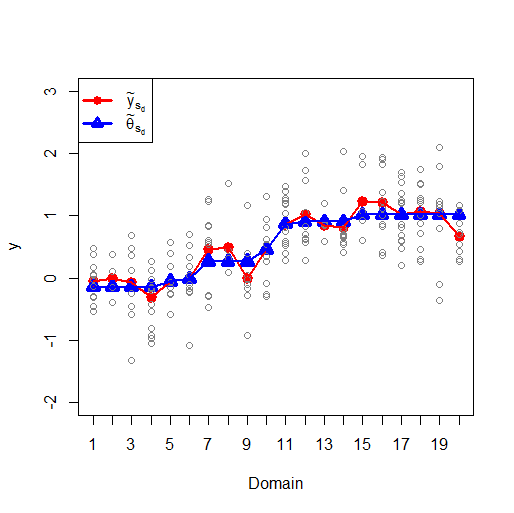

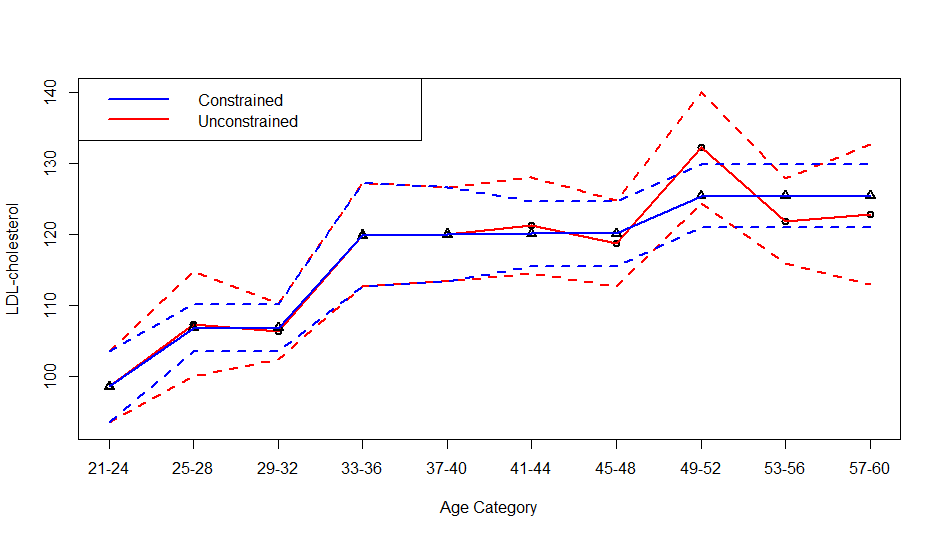

We apply the proposed CICs methodology to the 2011-2012 NHANES laboratory data obtained from the Center of Disease Control website. There are complete observations for variables age and LDL-cholesterol measures (mg/dL), where we only consider observations with age range between 21-60 years old. The LDL-cholesterol measure is the variable of interest . Under the consideration that LDL-cholesterol measures might increase with age, we intend to use that information on the construction of domain means estimates. We create 10 domains by partitioning the age variable in 10 categories of three years each, i.e., 21-24, 25-28, …, 57-60.

Since there is no information available regard the population domain sizes , we compute both unconstrained and constrained estimators of the population domain means using the Hájek estimator. The constrained estimator in Equation 3 is obtained by using the PAVA. The covariance term in CICs for both estimators is estimated using Equation 5.

Figure 4 contains both unconstrained and constrained estimators along with their pointwise 95% Wald confidence intervals. The variance estimates to construct these intervals are based on Equation 5, and the observed pooling is used to compute the estimated variance of the constrained estimator. Note that there are notable differences between them on the last three domains. Since and , then our proposed method chooses the constrained estimator above the unconstrained as an estimate of the population domain means. Moreover, notice that the confidence interval is tighter for the constrained estimator than for the unconstrained, which shows the fact that pooling domains decrease the uncertainty of the estimates.

We have proposed the Cone Information Criterion for Survey data (CICs) as a data-driven criterion for choosing between the constrained and the unconstrained domain mean estimators. We showed that the CICs is consistently selecting the correct estimator based on the shape of the limiting domain means . Moreover, the CICs shares similar characteristics with other information criteria like AIC and BIC. Mainly, it is a measure that balances the deviation of the constrained estimator from the unconstrained with a measure of the complexity of such estimator.

Some generalizations can be naturally derived from this work. Note the trace term in the CICs could be multiplied by any positive constant (instead of , as proposed) so that the consistency of the CICs remains true. The larger the value of would imply a larger penalization of the constrained estimator complexity. Since we are able to control the amount of such penalization by changing the value of , one question might be how to choose the optimum value . A generalization of a more practical interest might be to extend the CICs to other shape constraints beyond monotonicity, so that it can be used to choose among many other types of shapes on the survey context. In that case, the constrained estimator might be computed through the Cone Projection Algorithm proposed by Meyer, 2013b . Both of these extensions are currently being considered by the authors.

Acknowledgment

This material is based upon research work supported by the National Science Foundation under Grant MMS-1533804.

References

Akaike, (1973)

Akaike, H. (1973).

Information theory as an extension of the maximum likelihood

principle.

In Petrov, B. N. and Csaki, F., editors, Second International

Symposium on Information Theory, pages 267–281. Akademiai Kiado, Budapest.

Breidt and Opsomer, (2000)

Breidt, F. and Opsomer, J. (2000).

Local polynomial regression estimators in survey sampling.

The Annals of Statistics, 28(4):1026–1053.

Brunk, (1955)

Brunk, H. D. (1955).

Maximum likelihood estimates of monotone parameters.

The Annals of Mathematical Statistics, 28:1026–1053.

Brunk, (1958)

Brunk, H. D. (1958).

Maximum likelihood estimates of monotone parameters.

The Annals of Mathematical Statistics, 29(2):437–454.

Hájek, (1971)

Hájek, J. (1971).

Comment on a paper by D. Basu.

In Godambe, V. P. and Sprott, D. A., editors, Foundations of

Statistical Inference, page 236. Holt, Rinehart and Winston, Toronto.

Horvitz and Thompson, (1952)

Horvitz, D. G. and Thompson, D. J. (1952).

A generalization of sampling without replacement from a finite

universe.

Journal of the American Statistical Association, 47:663–685.

(7)

Meyer, M. C. (2013a).

Semi-parametric additive constrained regression.

Journal of Nonparametric Statistics, 25:715–730.

(8)

Meyer, M. C. (2013b).

A simple new algorithm for quadratic programming with applications in

statistics.

Communications in Statistics, 42:1126–1139.

Robertson et al., (1988)

Robertson, T., Wright, F. T., and Dykstra, R. L. (1988).

Order Restricted Statistical Inference.

John Wiley & Sons, New York.

Särndal et al., (1992)

Särndal, C.-E., Swensson, B., and Wretman, J. (1992).

Model Assisted Survey Sampling.

Springer, New York.

Schwarz, (1978)

Schwarz, G. (1978).

Estimating the dimension of a model.

Annals of Statistics, 6:461–464.

Silvapulle and Sen, (2005)

Silvapulle, M. J. and Sen, P. (2005).

Constrained Statistical Inference.

Wiley, Hoboken, New Jersey.

VanEeden, (1956)

VanEeden, C. (1956).

Maximum likelihood estimation of ordered probabilities.

Indigationes Mathematicae, 18:444–455.

Wollan and Dykstra, (1986)

Wollan, P. C. and Dykstra, R. L. (1986).

Conditional tests with an order restriction as a null hypothesis.

In Dykstra, R. L., Robertson, T., and Wright, F. T., editors, Advances in Order Restricted Statistical Inference, pages 279–295.

Springer-Verlag, New York.

Wu et al., (2016)

Wu, J., Meyer, M. C., and Opsomer, J. D. (2016).

Survey estimation of domain means that respect natural orderings.

Canadian Journal of Statistics, 44(4):431–444.

Appendix

The first part of this section contains all lemmas used to prove the theoretical results contained in Sections 2 and 3. Complete proofs of latter results are included at the end of this section.

Lemma 1. , for any , .

Proof of Lemma 1.

For simplicity of notation and without loss of generality, we will use instead of and instead of . Note that

We will now prove that converge to zero as goes to infinity. For , we have that

where the term to the right goes to zero from Assumptions (A2)-(A3). Further,

which converges to zero by Assumption (A7). Finally, note that

where the last term diminishes as by Assumptions (A7)-(A8). This concludes the proof.

∎

Lemma 2.

Let . Assume that for . Then,

where could be either or coordinate-wise function.

Proof of Lemma 2.

We are going to prove this proposition by induction in . The case is clear since . Assume the result is true for . That is,

We need to prove that the result is true for . Note that

which is also true for the sequence of ’s.

Denote and . By the induction assumption, For the rest of the proof we are going to consider only the case when . Later we will note that the proof for is analogous to what follows.

Note that we can write and . Hence,

Since both and , then for any there exist and such that

Therefore,

Setting , then we can conclude that . Thus, the result is true for . For the case when , we just need to use the fact that and then follow an analogous proof as above.

∎

Lemma 3. Let be the weighted isotonic vector of the limiting domain means with weights . Then,

Proof of Lemma 3.

Fix . Following the proof of Lemma 2, it can be proved that from Assumption (A4). By Theorem 4, . Therefore, we can conclude that .

∎

Lemma 4. , where .

Proof of Lemma 4.

From and , we get that . Further, by Lemma 3. Therefore, . In addition, for . Thus, . ∎

Lemma 5.

, for any .

Proof of Lemma 5.

Define to the set of representative elements , and as it was done in the proof of Theorem 2. In addition, let be the set of representative elements of those poolings that correspond to the disjoint sets and such that and . That is, if and only if the pooling represented by is allowed by to produce . Further, let .

Suppose that there exist indexes such that . First, note that both and converge to the vector . From Assumption (A4), and , which implies that .

Consider any index such that . Denote to the -element of . Fix . From the fact that the function is minimized by the constant , then we have

which implies that . Thus, by the Cauchy-Schwartz inequality, we conclude that for .

∎

Proof of Proposition 1.

Note that

By adding and subtracting in the expectation term of the above equality, we have that

Further,

Hence, .

∎

Proof of Theorem 1.

First, consider an index such that and assume that . Define . Consider the largest index that is less than , and the smallest index that is greater than . Then, the slope from point to is greater than the slope from point to . That is, . Now, since , then the slope from point to is at most equal to the slope from point to . That implies . Therefore, we have

where the last equality comes from Lemma 1 and Assumption (A4). Thus, .

Now, consider an index such that but . Let . Let be the largest index less than and the smallest index greater than , respectively. Since is not a corner point of , then is either on or above it, i.e. . Moreover, because is a corner point of . Hence,

which leads to the conclusion that . ∎

Proof of Theorem 2.

Let be representative elements for each of the possible poolings (groupings) for a vector of length . Also, define to the set of all of these representative elements. Since and without loss of generality, let be the representative element of the unique pooling allowed by . Denote to be the weighted projection matrix that corresponds to the pooling represented by with weights . Also, define to the probability that the pooling represented by is allowed by to obtain . By Theorem 1,

P

Also, since for , then for ,

which implies that . Hence,

Then, we obtain that

Analogously, , where is the matrix of ones. Therefore, we can conclude that

Now, note that

which implies that for . Moreover,

Then,

Thus, from Proposition 1,

∎

Proof of Theorem 3.

The term can be broken into two sums: one with the common and one with the uncommon elements of and . By doing that, we get

where the last inequality is obtained from Assumption (A5). Given that each of the terms in the above upper bound is asymptotically bounded by Assumptions (A2)-(A5), then the first result is true.

To show the second result, note that

where we used the identities , and .

To conclude the proof, we just need to show that converge in probability to zero as . The Markov inequality guarantees that converges in probability to zero if its second moment does. Such moment can be written as

Furthermore,

which converges to zero as by Assumptions (A2)-(A5). Also, after separating the double sum in into two sums where and , we get that

where the last term goes to zero by Assumptions (A2)-(A6). In addition, an application of the Cauchy-Schwarz inequality along with the fact that both tend to zero, shows that converges to zero. Therefore, the Markov-inequality let us conclude that .

Now, note that

Then, since and . Analogously, and . Thus,

Finally, we have that since and . Therefore,

which concludes the proof.

∎

Proof of Theorem 4.

Fix . First, recall that

By linearization arguments, it is true that .

Define and for . Hence, we have that

By Lemma 2, it is true that

Now, define and . Therefore,

Finally, applying again Lemma 2 let us conclude that

which concludes the proof.

∎

Proof of Theorem 5.

The CICs difference between the constrained and the unconstrained estimator can be expressed as

First, assume that . Define to the event where , that is, and . Then, from Theorem 1, we can conclude that . Moreover, note that the CICs difference is zero when holds. Hence,

Now, suppose that are not monotone. From Theorem 1 and Lemma 3, . Further, , since are not monotone. Thus,

which concludes the proof.

∎

Proof of Theorem 6.

We can write the PSE difference as

Assume first that . This implies that and i.e. all points of the GCM are corner points. Based on the proof of Theorem 2 (with ), we have that and . Therefore, and , which concludes the first part of the proof.

Assume now that are not monotone. Lemma 5 and a direct application of Chebyshev’s inequality imply that . Moreover, since , then . Hence, , where the quadratic form is strictly greater than zero by the non-monotone assumption on the ’s. On the other hand, since both and are of the order , then . This concludes the proof.

∎