Nonparametric Testing for Differences in Electricity Prices: The Case of the Fukushima Nuclear Accident

Abstract

This work is motivated by the problem of testing for differences in the mean electricity prices before and after Germany’s abrupt nuclear phaseout after the nuclear disaster in Fukushima Daiichi, Japan, in mid-March 2011. Taking into account the nature of the data and the auction design of the electricity market, we approach this problem using a Local Linear Kernel (LLK) estimator for the nonparametric mean function of sparse covariate-adjusted functional data. We build upon recent theoretical work on the LLK estimator and propose a two-sample test statistics using a finite sample correction to avoid size distortions. Our nonparametric test results on the price differences point to a Simpson’s paradox explaining an unexpected result recently reported in the literature.

keywords:

appendixReferences\arxivarXiv:1711.03367 \startlocaldefs \endlocaldefs

1 Introduction

On March 15, 2011, Germany showed an abrupt reaction to the nuclear disaster in Fukushima Daiichi, Japan, and shut down of its nuclear power plants—permanently. This substantial loss of cheap (in terms of marginal costs) nuclear power raised concerns about increases in electricity prices and subsequent problems for industry and households. So far, however, empirical studies are scarce and based on restrictive model assumptions. In this work we add a nonparametric functional data perspective and compare our test results with the existing benchmark results. Our results point to a Simpson’s paradox explaining the unexpected result recently reported by Grossi, Heim and Waterson (2017).

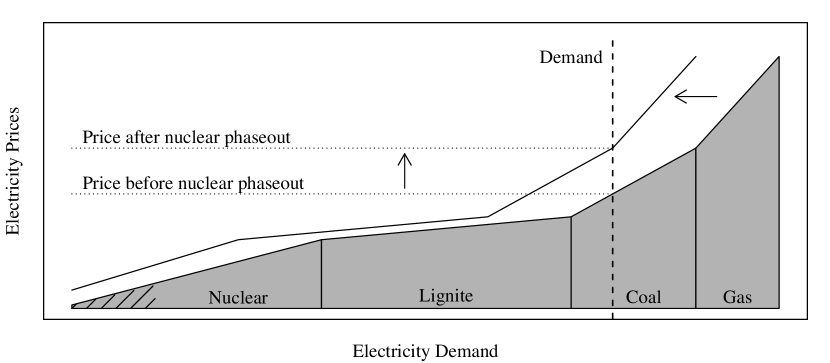

Pricing at electricity exchanges is explained well by the merit-order model. This model assumes that spot prices are based on the merit-order curve—a monotonically increasing curve reflecting the increasingly ordered generation costs of the installed power plants. The merit-order model is a fundamental market model (see, for instance, Burger, Graeber and Schindlmayr, 2008, Ch. 4) and is most important for the explanation of electricity spot prices in the literature on energy economics (see Burger et al., 2004; Sensfuß, Ragwitz and Genoese, 2008; Hirth, 2013; Liebl, 2013; Cludius et al., 2014; Bublitz, Keles and Fichtner, 2017; Grossi, Heim and Waterson, 2017).

The plot in Figure 1 sketches the merit-order curve of the German electricity market and is in line with Cludius et al. (2014). The interplay of the demand curve (dashed line) with the merit-order curve determines the electricity prices, where electricity demand is assumed to be price-inelastic in the short-term perspective of a spot market. The latter assumption is regularly found in the literature (see, e.g., Sensfuß, Ragwitz and Genoese, 2008) and confirmed in empirical studies (see, e.g., Lijesen, 2007).

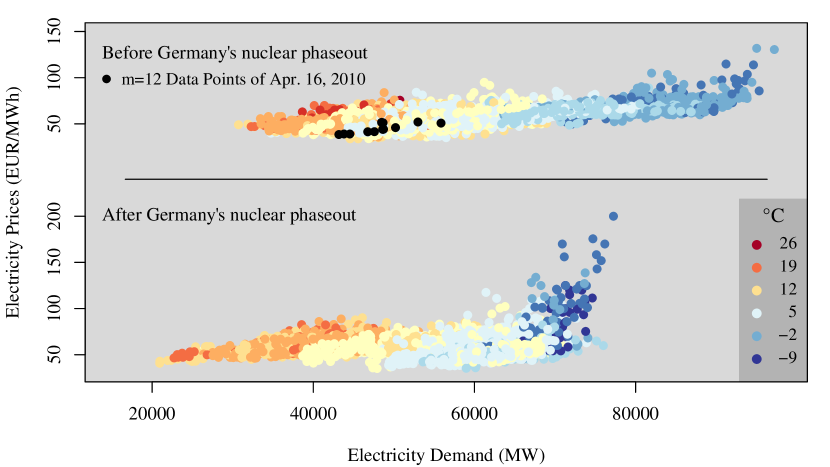

We consider electricity spot prices from the European Power Exchange (EPEX), where the hourly electricity spot prices of day are settled simultaneously at am the day before (see, for instance, Benth, Kholodnyi and Laurence, 2013, Ch. 6). Following the literature, we differentiate between “peak-hours” (from 9am to 8pm) and “off-peak-hours” (all other hours) and focus on the peak-hours, since these show the largest variations in electricity prices and electricity demand.

The daily simultaneous pricing scheme at the EPEX results in a daily varying merit-order curve (or simply “price curve”) . However, we do not directly observe the price functions , but only their noisy discretization points , with (see black points in Figure 2). This data situation with only a few, i.e., , irregularly spaced evaluation points, , per function is referred to as sparse functional data (see, e.g., Yao, Müller and Wang, 2005). The smoothness of the underlying price curve induces a high correlation between electricity prices and with similar values of electricity demand . Ignoring these correlations when doing inference can result in serious size distortions and invalid test decisions (see Liebl, 2019a).

Therefore, we model the electricity spot price of day and peak-hour as a discretization point of the underlying (unobserved) daily merit-order curve evaluated at the corresponding value of electricity demand ,

| (1.1) |

where denotes the daily mean air temperature—a covariate of fundamental importance for the shape and the location of the random function . The statistical error term is assumed to be independently and identically distributed (iid) with mean zero and finite variance and assumed to be independent from , , and .

The shape of and its location, i.e., , with , are both allowed to be functions of the covariate temperature . The scatter plot of the data triplets is shown in Figure 2. Note that electricity demand is observed within temperature-specific subintervals, i.e., and that the discretization points suggest steeper functions for cold days than for warm days. These observations motivate our modeling assumption that ; see Horváth and Kokoszka (2012), Ch. 2, for fundamental properties of random functions in the space .

Germany’s (partial) nuclear phaseout means a shift of the mean merit-order curve resulting in higher electricity spot prices—particularly at hours with large values of electricity demand (see Figure 1). This effect is obvious in the data for very cold days (see Figure 2), though not obvious on other days. Therefore, the objective of this article is a two-sample test of the pointwise null hypothesis of equal means against the alternative of larger mean values after Germany’s nuclear phaseout, i.e.,

where and are the mean functions of the random price functions fter, , and efore, , Germany’s nuclear phaseout.

We estimate the mean functions and separately for each period from the observed data points using the Local Linear Kernel (LLK) estimator for sparse functional data suggested by Jiang and Wang (2010). Recently, it has been demonstrated that the asymptotic results of Jiang and Wang (2010) neglect an additional functional-data-specific variance term which is asymptotically negligible, but typically not negligible in practice. Neglecting this additional variance term leads to a too small variance component resulting in size distortions of the test statistic and in invalid test decisions (Liebl, 2019a). Therefore, we take into account the small sample correction proposed by Liebl (2019a) and propose a two-sample test statistic, which guarantees valid test decisions in practical finite samples as well (see also the in-depth simulation study in Liebl (2019a)).

In order to control for the effects of the remaining fundamental market factors, i.e., the price of natural gas, CO2 emission allowances, and coal (see, e.g., Maciejowska and Weron, 2016) we use what is called an event study approach. Event studies are essentially two-sample test problems comparing a “control” sample, from the period just before the event, with a “treatment” sample, from the period just after the event. The time period before the event is called “estimation window” and the time period after the event is called “event window”. The idea is to choose small enough time windows for which the non-controlled, but less important, market factors do not have confounding effects (McWilliams and Siegel, 1997). The event study method used today was introduced by Ball and Brown (1968) and Fama et al. (1969). A well-known introductory survey article is written by MacKinlay (1997). We are not the first to use the event study approach for analyzing effects that are due to Germany’s unexpected nuclear phaseout after the Fukushima Daiichi nuclear disaster. Ferstl, Utz and Wimmer (2012) analyze the stock prices of energy companies using an event study. Betzer, Doumet and Rinne (2013) use an event study to test for differences in the shareholder wealth of German nuclear energy companies. Thoenes (2014) considers the effect on futures prices.

In terms of the research question, our paper is closely related to the recent work of Grossi, Heim and Waterson (2017), who consider differences in the electricity spot prices before and after Germany’s nuclear phaseout. Therefore, we use the approach of Grossi, Heim and Waterson (2017) as a benchmark for comparing our nonparametric test approach. While Grossi, Heim and Waterson (2017) estimate the price differences conditionally on demand, we additionally allow for an interaction effect with temperature. This way our nonparametric test result demonstrates that a Simpson’s paradox (Wagner, 1982) can explain the unexpected structure of the parametric price differences reported by Grossi, Heim and Waterson (2017).

The literature on covariate-adjusted functional data is fairly scarce. Cardot (2007) considers functional principal component analysis for covariate-adjusted random functions, though he focuses on the case of dense functional data and does not derive inferential results for his mean estimate. Jiang and Wang (2010) show many theoretical results of fundamental importance for sparse covariate-adjusted functional data and we use their pointwise asymptotic normality result for the mean function as a benchmark. Li, Staicu and Bondell (2015) consider a copula-based model and Zhang and Wei (2015) propose an iterative algorithm for computing functional principal components, though neither contributes inferential results for the covariate-adjusted mean function. For the case without covariate adjustments there are several papers considering inference for the mean function (see, for instance, Zhang and Chen, 2007; Hall and Van Keilegom, 2007; Benko, Härdle and Kneip, 2009; Cao, Yang and Todem, 2012; Gromenko and Kokoszka, 2012; Horváth, Kokoszka and Reeder, 2013; Fogarty and Small, 2014; Vsevolozhskaya, Greenwood and Holodov, 2014; Zhang and Wang, 2016). We emphasize, however, that the existing results for functional data without covariate adjustments cannot easily be generalized to account for additional covariate adjustments. Related to our work is also that of Serban (2011) and Gromenko, Kokoszka and Sojka (2017), who consider covariate-adjusted, namely, spatio-temporal functional data; however, they do not focus on a sparse functional data context. Two recent works on modeling and forecasting electricity data using methods from functional data analysis are Shah and Lisi (2018) and Lisi and Shah (2018). Readers with a general interest in functional data analysis are referred to the textbooks of Ramsay and Silverman (2005), Ferraty and Vieu (2006), Horváth and Kokoszka (2012), and Hsing and Eubank (2015).

The rest of the paper is organized as follows. The next section introduces the LLK estimator and our two-sample test statistic. Section 3 introduces approximations to the unknown bias, variance and bandwidth components. Section 4 contains the real data study. The paper concludes with a discussion in Section 5. The proofs of our theoretical results are based on standard arguments in nonparametric statistics and can be found in the online supplement supporting this article (Liebl, 2019b).

2 Nonparametric two-sample inference

In the following, we use a common notation for both samples ( and ) unless a differentiation is required by the context. Without loss of generality, we consider a standardized domain where such that . The standardization can be achieved as and . The functional interval borders and are unobserved, but can be estimated from the data points using the LLK estimators of Martins-Filho and Yao (2007).

Let denote the centered function . Model (1.1) can then be rewritten as a nonparametric regression model with the conditional mean function , given and , i.e.,

| (2.1) |

where , , and are assumed to be a stationary weakly-dependent functional and univariate time series. The error term is a classical iid error term with mean zero, finite variance , and assumed to be independent from , , and for all and .

Note that Model (2.1) has a rather unusual composed error term consisting of a functional and a scalar component . The functional error component introduces very strong local correlations, since

which leads to the above mentioned functional-data-specific variance term that makes it necessary to use the finite sample correction proposed by (Liebl, 2019a).

We estimate the mean function using the same LLK estimator as considered in Jiang and Wang (2010). In the following we define the estimator based on a matrix notion:

| (2.2) | |||

where the vector selects the estimated intercept parameter and is a dimensional data matrix with typical rows . The dimensional diagonal weighting matrix holds the bivariate multiplicative kernel weights where is a usual second-order kernel such as, e.g., the Epanechnikov or the Gaussian kernel, denotes the bandwidth in direction, and the bandwidth in direction. The kernel constants are denoted by , with , and , with . All vectors and matrices are filled in correspondence with the dimensional vector .

The following theorem is an adjusted version of Corollary 3.1, part (b) in Liebl (2019a) and takes into account the finite sample correction for the variance component:

Theorem 2.1 (Asymptotic normality).

Theorem 2.1 generalizes the corresponding result in Liebl (2019a) by additionally allowing for a time series context with weakly dependent auto-correlation structure; a proof can be found in the supplement supporting this article (Liebl, 2019b). The theorem implies the standard optimal convergence rate () for bivariate LLK estimators. The finite sample correction is accomplished by the additional second variance term which could be dropped from a pure asymptotic view. However, this second variance term is typically not negligible in practice and serves as a very effective finite sample correction (Liebl, 2019a). Note that the variance effects due to the autocorrelations from our time series context are not first-order relevant. The reason for this is that we localize with respect to the variables and and not with respect to time . The resulting decorrelation effect is referred to as the “whitening window” property (see, for instance, Fan and Yao, 2003, Ch. 5.3).

Theorem 2.1 without the variance term , i.e., without finite sample correction, is essentially equivalent to Theorem 3.2 in Jiang and Wang (2010), who, however, consider the case where is bounded, i.e., for some small (e.g., or ), as typically assumed in the literature on sparse functional data analysis (cf. Yao, Müller and Wang, 2005; Zhang and Wang, 2016, and many others). In contrast, our asymptotic normality result allows for bounded as well as non-bounded , such that . This explains the empirical finding in Liebl (2019a) that our asymptotic normality result with finite sample correction provides very good finite sample approximations for practical small- (e.g., ) as well as moderate- cases (e.g., )—by contrast to the corresponding results in Jiang and Wang (2010).

The following corollary follows directly from Theorem 2.1 and contains the asymptotic normality result for our two-sample test statistic:

Corollary 2.1 (Two-sample test statistic).

Under the same conditions as in Theorem 2.1 and under the null hypothesis : , the following two two-sample test statistic is asymptotically normal:

where the dependencies on the bandwidth parameters and are suppressed for readability reasons.

The test statistic is infeasible as it depends on the unknown bias, variance, and bandwidth expressions, , , , and . In our application, we use the practical rule-of-thumb bandwidth, bias and variance approximations as described in the following section.

Remark

A common number (: number of discretization points per function ) may be unrealistic for some applications. However, our estimators can be directly applied to data-scenarios with function-specific numbers of discretization points with . To adjust our asymptotic analysis for this situation, one can consider the case where with for all (cf. Zhang and Chen, 2007). As Hall, Müller and Wang (2006), Zhang and Chen (2007) and Zhang and Wang (2016) we do not consider random numbers , but if are random, our theory can be considered as conditional on .

3 Practical approximations

We approximate the unknown bias term by

| (3.1) |

where the estimates of the second-order partial derivatives and are local polynomial (order ) kernel estimators. That is,

with , , , and diagonal matrix with weights on its diagonal, where and are the bandwidths in and direction. The estimator is defined correspondingly, but with replaced by . For estimating the bandwidths and we use bivariate GCV based on second-order differences. We follow the procedure of Charnigo and Srinivasan (2015), but use a GCV-penalty instead of the (asymptotically equivalent) -penalty proposed there.

We estimate the unknown first variance term by

| (3.2) |

The Noisy Diagonal (ND) LLK estimator of is defined as follows:

| (3.3) |

with and denoting the bandwidths in and direction and with consisting only of the noisy diagonal raw-covariances for which . Note that is equivalent to the LLK estimator “” in Jiang and Wang (2010). The estimate is computed using the bivariate kernel density estimation function kde2d() of the R-package MASS (Venables and Ripley, 2002), where the involved bandwidths are selected using the R-function width.SJ() of the R-package MASS containing an implementation of the method of Sheather and Jones (1991).

The unknown second variance term is estimated by

| (3.4) |

The estimate is computed using the R-function density() for univariate kernel density estimation, where the involved bandwidth is selected using the R-function width.SJ() of the R-package MASS. The LLK estimator of is defined as follows:

| (3.5) |

Here, and is a dimensional data matrix with typical rows and . (The latter explains the requirement of Assumption A1 that .) The dimensional diagonal weighting matrix holds the trivariate multiplicative kernel weights . All vectors and matrices are filled in correspondence with the dimensional vector consisting only of the off-diagonal raw-covariances

with for which . We use bivariate GCV in order to estimate the bandwidth parameters , , and .

4 Application

On March 15, 2011, just after the nuclear meltdown in Fukushima Daiichi, Japan, Germany decided to switch to a renewable energy economy and initiated this by an immediate and permanent shutdown of about of its nuclear power plants. This substantial loss of nuclear power with its low marginal production costs raised concerns about increases in electricity prices and subsequent problems for industry and households. Energy economists typically use Monte Carlo simulations in order to approximate the price effect of Germany’s nuclear phaseout (see, for instance, Bruninx et al., 2013). Empirical data-based evidence, however, is scarce. Thoenes (2014) uses an event study approach to estimate the effect of Germany’s nuclear phaseout on electricity futures prices. The work of Grossi, Heim and Waterson (2017) considers the less speculative electricity spot prices and can be seen as a parametric counterpart to our work. Therefore, we use the approach of Grossi, Heim and Waterson (2017) as a benchmark for our nonparametric approach.

In Section 4.1 we introduce the benchmark models. In Section 4.2 we compare the benchmark results with the results of our nonparametric two-sample test statistic and demonstrate that a Simpson’s paradox can explain the unexpected finding in Grossi, Heim and Waterson (2017).

Data

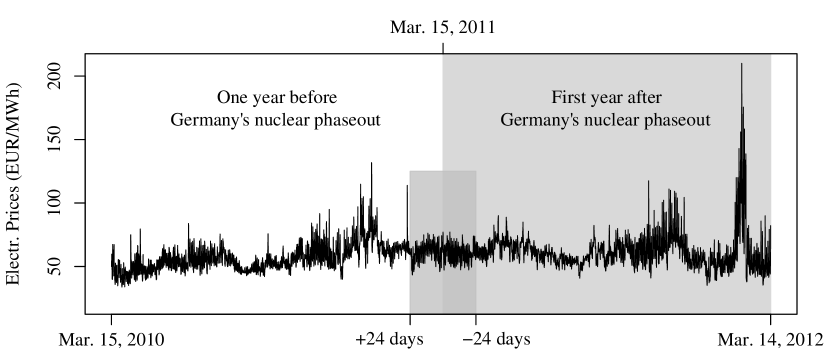

The data for our analysis come from different sources that are described in detail in the online supplement supporting this article (Liebl, 2019b). The German electricity market, like many others, provides purchase guarantees for renewable energy sources. Therefore, the relevant variable for pricing is electricity demand (or “load”) minus electricity infeeds from RES and an additional correction for the net imports of electricity from neighboring countries (see, e.g., Paraschiv, Erni and Pietsch, 2014). Correspondingly, in our application refers to residual electricity demand defined as , with and , where denotes electricity demand, denotes infeeds from renewable energy sources, denotes wind-power, denotes solar-power, denotes net-imports, denotes electricity imports, and denotes electricity exports. The effect of further renewable energy sources such as biomass is still negligible for the German electricity market. Very few () of the data tuples with prices EUR/MWh are considered as outliers and set to EUR/MWh. Such extreme prices are often referred to as “price spikes”; they are caused by market speculations involving potential capacity scarcities and need to be modeled using different approaches (see, for instance, Burger et al., 2004, Ch. 4). Our data set consists of the peak-hour prices (; from am to pm) of the working days from one year before () and one year after () Germany’s partial nuclear phaseout on March 15, 2011. We consider only working days, since for weekends there are different compositions of the power plant portfolio. The same reasoning applies to holidays and so-called Brückentage, which are extra days off that bridge single working days between a bank holiday and the weekend. Therefore, we remove also all holidays and Brückentage from the data. The temporal gaps in the data due to weekend days, holidays and Brückentage do not violate our theoretical assumptions on the auto-covariance structure, since such gaps do not increase the auto-correlations. The main fundamental market factors (i.e., temperature, gas, CO2 allowance, and coal prices) are available at a daily sampling scheme. Legal issues do not allow us to publish the original data sets, however, simulated data sets that closely resemble the original data can be found in the online supplement supporting this article (Liebl, 2019b).

4.1 Parametric benchmark models

As a benchmark case study for our nonparametric approach, we use the following two increasingly complex parametric regression models:

| (4.1) | ||||

| (4.2) |

where denotes the daily mean (peak-hours) electricity spot price, denotes the daily mean (peak-hours) Residual Demand (RD), is a dummy variable which equals zero for all time points before Germany’s nuclear phaseout and equals one for all other time points, denotes air temperature, contains further control variables, and is a classical Gaussian statistical error term. As control variables we use the same fundamental market factors as in the fundamental electricity market model of Maciejowska and Weron (2016), i.e., temperature, CO2 emission allowance prices, coal prices, and natural gas prices. For lignite and nuclear energy resources there are no relevant market prices (Grossi, Heim and Waterson, 2017).

Model (4.1) estimates a possible price effect using a simple dummy variable approach. Model (4.2) corresponds to the regression model of Grossi, Heim and Waterson (2017), who estimate the price effect of Germany’s nuclear phaseout using the quadratic dummy-interaction function ; see Table 4 in Grossi, Heim and Waterson, 2017. We cannot consider most all of the control variables proposed by Grossi, Heim and Waterson (2017), since we do not have access to the data used in their case study (missing variables: export congestion index, residual supply index (i.e., a market power index), and low/high river level). In order to rectify this shortcoming, we use the event study approach with short estimation and event windows each containing 24 days (see Figure 3). Our window size is one day smaller than the window size in the related event study of Thoenes (2014), since we want to exclude the strong price jump one day before our estimation window. Our estimation results are robust to smaller window sizes.

| Model (4.1) | Model (4.2) | ||||||||

| I | II | III | IV | I | II | III | IV | ||

| RD | |||||||||

| RD2 | |||||||||

| Dummy | |||||||||

| DummyRD | |||||||||

| DummyRD2 | |||||||||

| Temperature | |||||||||

| Temperature2 | |||||||||

| CO2 price | |||||||||

| Coal price | |||||||||

| Gas price | |||||||||

| R2 | |||||||||

| Adj. R2 | |||||||||

| F Statistics | |||||||||

| I vs II | 1.6 | 1.0 | |||||||

| II vs III | 8.8∗ | 4.1∗ | |||||||

| III vs IV | 0.9 | 1.1 | |||||||

| Note: ∗p0.05 | |||||||||

The F statistics in the lower panel of Table 1 show that the simple benchmark Model (4.1) is insufficient for describing the price effect of Germany’s nuclear phaseout, expect if the temperature-component is added to the control variables (III and IV). In contrast to this, Model (4.2), which contains the quadratic dummy-interaction function, describes the price effect with a significantly strong explanatory power in all model-specifications I-IV. Comparing the different model-specifications reveals that the resource prices (CO2, coal, and gas) are jointly insignificant control variables: neither adding them to the smallest model-specification (I vs II), nor removing them from the larges model-specification (III vs IV) has a significant impact on the fit of the models. That is, our event study approach successfully minimizes the confounding effects of the control variables CO2, coal, and gas, which are known to be less important in the short run. Furthermore, it demonstrates the importance of including the temperature-component.

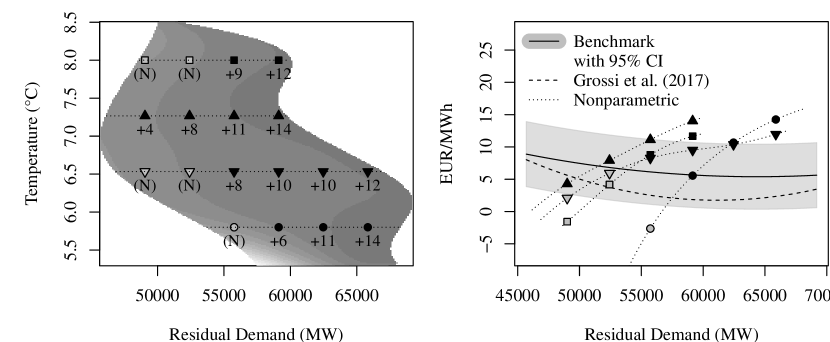

The graph of the estimated quadratic dummy-interaction function of benchmark Model (4.2-IV) together with its 95% confidence interval is shown in Figure 4. The confidence interval covers the dummy-interaction function reported111The data for this graph are extracted from Figure 6 in Grossi, Heim and Waterson (2017) using the WebPlotDigitizer of Rohatgi (2018). by Grossi, Heim and Waterson (2017). The dummy-interaction function of our benchmark Model shows slightly larger values than reported by Grossi, Heim and Waterson (2017), since the market reactions to Germany’s unexpected nuclear phaseout are less moderated in the short time frame of our event study than in the long time frame ( years) considered by Grossi, Heim and Waterson (2017).

4.2 Nonparametric testing

In contrast to the parametric benchmark models, we do not assume any specific functional form for the price effect of Germany’s nuclear phaseout. Additionally, we allow for interactions between residual demand and temperature. As for any nonparametric model, however, we need to deal with the curse of dimensionality which prevents us from considering all control variables of potential relevance. Therefore, we focus on the two most important control variables (residual demand and temperature) and use the event study approach in order to minimize the confounding effects of the remaining less important control variables as in our benchmark study.

Residual demand and temperature are the two most important market fundamental control variables within the short term of an event study. First, because the interplay of residual demand with the merit-order curve determines electricity spot prices (see Figure 1). Second, because the merit-order curve itself depends on temperature. For the latter dependency, there are multiple reasons, both fundamental and speculative. The most important fundamental reason is that the merit-order curve is determined by the generation costs of the conventional (i.e., nuclear, lignite, coal, and gas) power plants. These conventional power plants are thermal-based electricity generators using river water as their primary cooling resource. The resulting thermal pollution is substantial and environmentally hazardous and, therefore, strictly regulated by public institutions. This regulation affects the cost structure, i.e., the merit-order curve (McDermott and Nilsen, 2014). For given values of electricity demand, the merit-order curve is higher (lower) on warm (cold) days, when the river water has a smaller (larger) cooling capacity222McDermott and Nilsen (2014) propose to use river temperature as a control variable. However, we do not have access to their data and therefore use air temperature as a proxy which is known to correlate strongly with river temperature (see Rabi, Hadzima-Nyarko and Šperac, 2015) (see Figure 2, for middle to high temperatures). However, there is also a reverse interaction effect between residual demand and temperature which can revert the fundamental price component described above. Due to the use of heating and cooling devices, cold and hot days are associated with the large amounts of electricity demand resulting in market situations where the electricity production capacities become scarce.333The use of air conditioning systems is, however, less extensive in Germany than, for instance, in the US. In these situations of market stress, one observes the high electricity prices (see Figure 2, for cold temperatures), since the electricity producers demand additional scarcity premiums (see Burger, Graeber and Schindlmayr, 2008, Ch. 4).

To conclude, the effects of residual demand and temperature and their interaction effects are quite complex and it is easy to end up with a misspecified model, particularly when using a parametric approach. Despite these complexities, the parametric benchmark Model (4.2), proposed by Grossi, Heim and Waterson (2017), does not consider interaction effects between electricity demand and temperature. In the following, we compare our nonparametric test results with our parametric benchmarks and demonstrate the importance of this interaction effect.

The left plot in Figure 4 shows a contour plot of the price difference surface of the mean estimates before and after Germany’s nuclear phaseout. The support of the difference surface equals the intersection of the supports of the mean functions and ,

where the empirical boundary functions and , , are computed using the LLK boundary estimator of Martins-Filho and Yao (2007).

In order to test the pointwise null hypothesis : against the alternative : , we use our finite sample corrected two-sample test statistic described in Section 2 with plugged-in empirical bias and variance expressions and GCV-optimal bandwidths as described in Section 3. The test statistic is evaluated at regular grid-points , , within the intersection . These test-points are shown by the points in the plots of Figure 4, where the different point shapes correspond to different temperature values. In order to account for the multiple testing we use a Bonferroni-adjusted significance level where we set . Significant differences at the chosen test-points are depicted by the numerical values in the left plot of Figure 4; non-significant differences are marked by “(N)”. We are interested in pointwise hypotheses as we would like to identify significant and non-significant test-points. The Bonferroni-adjustment is known to be conservative, but works well for our application. Practitioners seeking for an alternative to the Bonferroni-adjustment are referred, for instance, to the work of Cox and Lee (2008).

The plots in Figure 4 show that the price differences are large (moderate) for large (moderate) values of electricity demand. This is in line with our expectations, since the merit-order curve is known to be steep (relatively flat) for large (moderate) values of electricity demand resulting in large (moderate) price differences (see Figure 1). Furthermore, there is a clear interaction effect in the price differences. If temperature increases, the thermal power plans loose cooling capacities which increases the production costs—particularly for the less efficient power plants. The latter results in a stepper merit-order curve and, therefore, larger price differences.

5 Discussion

On March 15, 2011, the German government showed a drastic reaction to the nuclear disaster in Fukushima Daiichi, Japan, and permanently shut down of its nuclear power plants. This political decision raised concerns about increases in electricity prices and subsequent problems for industry and households. Empirical studies on possible price effects, however, are scarce and existing studies are based on restrictive parametric model assumptions.

In this work we add a functional data perspective based on the merit-order model, the most important model for explaining electricity spot prices (see Burger et al., 2004; Sensfuß, Ragwitz and Genoese, 2008; Hirth, 2013; Liebl, 2013; Cludius et al., 2014; Bublitz, Keles and Fichtner, 2017; Grossi, Heim and Waterson, 2017). We extend the work of Liebl (2013) and additionally control for non-functional covariate adjustments.

In order to test for a possible price effect, we compare the multivariate nonparametric local linear kernel estimates of the mean price functions before and after Germany’s nuclear phase out on March 15, 2011, using a pointwise test statistic. Nonparametric smoothing of the pooled data is used, since the underlying daily price functions are only observed at noisy discretization points (“sparse functional data”). The existing asymptotic results on this nonstandard smoothing problem only consider the leading variance term and neglect an additional functional data specific variance term, which is asymptotically negligible, but typically not practically negligible. Ignoring this additional variance term can result in serious size distortions and invalid test decisions (see Liebl, 2019a). Therefore, we propose a finite sample correction that considers also the second functional data specific variance term (see Theorem 2.1 and Corollary 2.1). Theorem 2.1 generalizes the main result in Liebl (2019a) by allowing for a time series context with weak dependency structure.

We compare our nonparametric test results with parametric benchmark results replicating the results recently reported by Grossi, Heim and Waterson (2017). Our results confirm the existence of a price effect due to Germany’s abrupt nuclear phase out, but our price effect is structured quite differently to the results in Grossi, Heim and Waterson (2017). While our nonparametric price differences are highest for large values of residual demand, the parametric benchmark models estimate the highest price differences for small values of residual demand (see right panel in Figure 4). One of the fundamental differences between our approach and the approach of Grossi, Heim and Waterson (2017) is that we take into account interactions with the important temperature factor, while Grossi, Heim and Waterson (2017) do not allow for this kind of interaction effect. Such a reversal of effects that is due to introducing an additional conditioning variable is known as Simpson’s paradox (see, for instance, Wagner, 1982). Grossi, Heim and Waterson (2017) concede that their result is “unexpected” and present different market explanations for their unexpected result; however, a possible model-misspecification is not taken into account. Our nonparametric case study points at such a possible model-misspecification and demonstrates that a Simpson’s paradox can explain their unexpected finding.

Acknowledgements

I would like to thank my colleague Alois Kneip (University of Bonn) for many stimulating and fruitful discussions on this project. Furthermore, I am grateful to the referees and the editors for their constructive feedback which helped to improve this research work.

Supplement A\stitleR-Codes and Data \slink[doi]COMPLETED BY THE TYPESETTER \sdatatypezip file \sdescriptionThis supplementary material contains the R codes of the real data application and simulated data which closely resembles the original data set. {supplement} \snameSupplement B\stitleSupplementary Paper \slink[doi]COMPLETED BY THE TYPESETTER \sdatatypepdf file \sdescriptionThis supplementary paper contains the proofs of our theoretical results and a detailed description of the data sources.

References

- Ball and Brown (1968) {barticle}[author] \bauthor\bsnmBall, \bfnmRay\binitsR. and \bauthor\bsnmBrown, \bfnmPhilip\binitsP. (\byear1968). \btitleAn empirical evaluation of accounting income numbers. \bjournalJournal of Accounting Research \bpages159–178. \endbibitem

- Benko, Härdle and Kneip (2009) {barticle}[author] \bauthor\bsnmBenko, \bfnmM\binitsM., \bauthor\bsnmHärdle, \bfnmW\binitsW. and \bauthor\bsnmKneip, \bfnmA\binitsA. (\byear2009). \btitleCommon functional principal components. \bjournalThe Annals of Statistics \bvolume37 \bpages1–34. \endbibitem

- Benth, Kholodnyi and Laurence (2013) {bbook}[author] \bauthor\bsnmBenth, \bfnmFred Espen\binitsF. E., \bauthor\bsnmKholodnyi, \bfnmValery A\binitsV. A. and \bauthor\bsnmLaurence, \bfnmPeter\binitsP. (\byear2013). \btitleQuantitative Energy Finance: Modeling, Pricing, and Hedging in Energy and Commodity Markets, \bedition1. ed. \bpublisherSpringer Science & Business Media. \endbibitem

- Betzer, Doumet and Rinne (2013) {barticle}[author] \bauthor\bsnmBetzer, \bfnmAndré\binitsA., \bauthor\bsnmDoumet, \bfnmMarkus\binitsM. and \bauthor\bsnmRinne, \bfnmUlf\binitsU. (\byear2013). \btitleHow policy changes affect shareholder wealth: The case of the Fukushima Daiichi nuclear disaster. \bjournalApplied Economics Letters \bvolume20 \bpages799–803. \endbibitem

- Bruninx et al. (2013) {barticle}[author] \bauthor\bsnmBruninx, \bfnmKenneth\binitsK., \bauthor\bsnmMadzharov, \bfnmDarin\binitsD., \bauthor\bsnmDelarue, \bfnmErik\binitsE. and \bauthor\bsnmD’haeseleer, \bfnmWilliam\binitsW. (\byear2013). \btitleImpact of the German nuclear phase-out on Europe’s electricity generation—A comprehensive study. \bjournalEnergy Policy \bvolume60 \bpages251–261. \endbibitem

- Bublitz, Keles and Fichtner (2017) {barticle}[author] \bauthor\bsnmBublitz, \bfnmAndreas\binitsA., \bauthor\bsnmKeles, \bfnmDogan\binitsD. and \bauthor\bsnmFichtner, \bfnmWolf\binitsW. (\byear2017). \btitleAn analysis of the decline of electricity spot prices in Europe: Who is to blame? \bjournalEnergy Policy \bvolume107 \bpages323–336. \endbibitem

- Burger, Graeber and Schindlmayr (2008) {bbook}[author] \bauthor\bsnmBurger, \bfnmMarkus\binitsM., \bauthor\bsnmGraeber, \bfnmBernhard\binitsB. and \bauthor\bsnmSchindlmayr, \bfnmGero\binitsG. (\byear2008). \btitleManaging Energy Risk: An Integrated View on Power and Other Energy Markets, \bedition1. ed. \bpublisherWiley. \endbibitem

- Burger et al. (2004) {barticle}[author] \bauthor\bsnmBurger, \bfnmMarkus\binitsM., \bauthor\bsnmKlar, \bfnmBernhard\binitsB., \bauthor\bsnmMüller, \bfnmAlfred\binitsA. and \bauthor\bsnmSchindlmayr, \bfnmGero\binitsG. (\byear2004). \btitleA spot market model for pricing derivatives in electricity markets. \bjournalQuantitative Finance \bvolume4 \bpages109–122. \endbibitem

- Cao, Yang and Todem (2012) {barticle}[author] \bauthor\bsnmCao, \bfnmGuanqun\binitsG., \bauthor\bsnmYang, \bfnmLijian\binitsL. and \bauthor\bsnmTodem, \bfnmDavid\binitsD. (\byear2012). \btitleSimultaneous inference for the mean function based on dense functional data. \bjournalJournal of Nonparametric Statistics \bvolume24 \bpages359–377. \endbibitem

- Cardot (2007) {barticle}[author] \bauthor\bsnmCardot, \bfnmHervé\binitsH. (\byear2007). \btitleConditional functional principal components analysis. \bjournalScandinavian Journal of Statistics \bvolume34 \bpages317–335. \endbibitem

- Charnigo and Srinivasan (2015) {barticle}[author] \bauthor\bsnmCharnigo, \bfnmRichard\binitsR. and \bauthor\bsnmSrinivasan, \bfnmCidambi\binitsC. (\byear2015). \btitleA multivariate generalized Cp and surface estimation. \bjournalBiostatistics \bvolume16 \bpages311–325. \endbibitem

- Cludius et al. (2014) {barticle}[author] \bauthor\bsnmCludius, \bfnmJohanna\binitsJ., \bauthor\bsnmHermann, \bfnmHauke\binitsH., \bauthor\bsnmMatthes, \bfnmFelix Chr\binitsF. C. and \bauthor\bsnmGraichen, \bfnmVerena\binitsV. (\byear2014). \btitleThe merit order effect of wind and photovoltaic electricity generation in Germany 2008–2016: Estimation and distributional implications. \bjournalEnergy Economics \bvolume44 \bpages302–313. \endbibitem

- Cox and Lee (2008) {barticle}[author] \bauthor\bsnmCox, \bfnmDennis D.\binitsD. D. and \bauthor\bsnmLee, \bfnmJong Soo\binitsJ. S. (\byear2008). \btitlePointwise testing with functional data using the Westfall-Young randomization method. \bjournalBiometrika \bvolume95 \bpages621-634. \endbibitem

- Fama et al. (1969) {barticle}[author] \bauthor\bsnmFama, \bfnmEugene F\binitsE. F., \bauthor\bsnmFisher, \bfnmLawrence\binitsL., \bauthor\bsnmJensen, \bfnmMichael C\binitsM. C. and \bauthor\bsnmRoll, \bfnmRichard\binitsR. (\byear1969). \btitleThe adjustment of stock prices to new information. \bjournalInternational Economic Review \bvolume10 \bpages1–21. \endbibitem

- Fan and Yao (2003) {bbook}[author] \bauthor\bsnmFan, \bfnmJ\binitsJ. and \bauthor\bsnmYao, \bfnmQ\binitsQ. (\byear2003). \btitleNonlinear Time Series, \bedition1. ed. \bseriesSpringer Series in Statistics. \bpublisherSpringer. \endbibitem

- Ferraty and Vieu (2006) {bbook}[author] \bauthor\bsnmFerraty, \bfnmF\binitsF. and \bauthor\bsnmVieu, \bfnmP\binitsP. (\byear2006). \btitleNonparametric Functional Data Analysis: Theory and Practice, \bedition1. ed. \bseriesSpringer Series in Statistics. \bpublisherSpringer. \endbibitem

- Ferstl, Utz and Wimmer (2012) {barticle}[author] \bauthor\bsnmFerstl, \bfnmRobert\binitsR., \bauthor\bsnmUtz, \bfnmSebastian\binitsS. and \bauthor\bsnmWimmer, \bfnmMaximilian\binitsM. (\byear2012). \btitleThe effect of the Japan 2011 disaster on nuclear and alternative energy stocks worldwide: An event study. \bjournalBusiness Research \bvolume5 \bpages25–41. \endbibitem

- Fogarty and Small (2014) {barticle}[author] \bauthor\bsnmFogarty, \bfnmColin B\binitsC. B. and \bauthor\bsnmSmall, \bfnmDylan S\binitsD. S. (\byear2014). \btitleEquivalence testing for functional data with an application to comparing pulmonary function devices. \bjournalThe Annals of Applied Statistics \bvolume8 \bpages2002–2026. \endbibitem

- Gromenko and Kokoszka (2012) {barticle}[author] \bauthor\bsnmGromenko, \bfnmOleksandr\binitsO. and \bauthor\bsnmKokoszka, \bfnmPiotr\binitsP. (\byear2012). \btitleTesting the equality of mean functions of ionospheric critical frequency curves. \bjournalJournal of the Royal Statistical Society: Series C (Applied Statistics) \bvolume61 \bpages715–731. \endbibitem

- Gromenko, Kokoszka and Sojka (2017) {barticle}[author] \bauthor\bsnmGromenko, \bfnmOleksandr\binitsO., \bauthor\bsnmKokoszka, \bfnmPiotr\binitsP. and \bauthor\bsnmSojka, \bfnmJan\binitsJ. (\byear2017). \btitleEvaluation of the cooling trend in the ionosphere using functional regression with incomplete curves. \bjournalThe Annals of Applied Statistics \bvolume11 \bpages898–918. \endbibitem

- Grossi, Heim and Waterson (2017) {barticle}[author] \bauthor\bsnmGrossi, \bfnmLuigi\binitsL., \bauthor\bsnmHeim, \bfnmSven\binitsS. and \bauthor\bsnmWaterson, \bfnmMichael\binitsM. (\byear2017). \btitleThe impact of the German response to the Fukushima earthquake. \bjournalEnergy Economics \bvolume66 \bpages450–465. \endbibitem

- Hall, Müller and Wang (2006) {barticle}[author] \bauthor\bsnmHall, \bfnmP\binitsP., \bauthor\bsnmMüller, \bfnmH G\binitsH. G. and \bauthor\bsnmWang, \bfnmJ L\binitsJ. L. (\byear2006). \btitleProperties of principal component methods for functional and longitudinal data analysis. \bjournalThe Annals of Statistics \bvolume34 \bpages1493–1517. \endbibitem

- Hall and Van Keilegom (2007) {barticle}[author] \bauthor\bsnmHall, \bfnmPeter\binitsP. and \bauthor\bsnmVan Keilegom, \bfnmIngrid\binitsI. (\byear2007). \btitleTwo-sample tests in functional data analysis starting from discrete data. \bjournalStatistica Sinica \bvolume17 \bpages1511–1531. \endbibitem

- Hirth (2013) {barticle}[author] \bauthor\bsnmHirth, \bfnmLion\binitsL. (\byear2013). \btitleThe market value of variable renewables: The effect of solar wind power variability on their relative price. \bjournalEnergy Economics \bvolume38 \bpages218–236. \endbibitem

- Horváth and Kokoszka (2012) {bbook}[author] \bauthor\bsnmHorváth, \bfnmLajos\binitsL. and \bauthor\bsnmKokoszka, \bfnmPiotr\binitsP. (\byear2012). \btitleInference for Functional Data with Applications, \bedition1. ed. \bseriesSpringer Series in Statistics \bvolume200. \bpublisherSpringer. \endbibitem

- Horváth, Kokoszka and Reeder (2013) {barticle}[author] \bauthor\bsnmHorváth, \bfnmLajos\binitsL., \bauthor\bsnmKokoszka, \bfnmPiotr\binitsP. and \bauthor\bsnmReeder, \bfnmRon\binitsR. (\byear2013). \btitleEstimation of the mean of functional time series and a two-sample problem. \bjournalJournal of the Royal Statistical Society: Series B (Statistical Methodology) \bvolume75 \bpages103–122. \endbibitem

- Hsing and Eubank (2015) {bbook}[author] \bauthor\bsnmHsing, \bfnmTailen\binitsT. and \bauthor\bsnmEubank, \bfnmRandall\binitsR. (\byear2015). \btitleTheoretical Foundations of Functional Data Analysis, with an Introduction to Linear Operators. \bpublisherJohn Wiley & Sons. \endbibitem

- Jiang and Wang (2010) {barticle}[author] \bauthor\bsnmJiang, \bfnmCi-Ren\binitsC.-R. and \bauthor\bsnmWang, \bfnmJane-Ling\binitsJ.-L. (\byear2010). \btitleCovariate adjusted functional principal components analysis for longitudinal data. \bjournalThe Annals of Statistics \bvolume38 \bpages1194–1226. \endbibitem

- Li, Staicu and Bondell (2015) {barticle}[author] \bauthor\bsnmLi, \bfnmMeng\binitsM., \bauthor\bsnmStaicu, \bfnmAna-Maria\binitsA.-M. and \bauthor\bsnmBondell, \bfnmHoward D.\binitsH. D. (\byear2015). \btitleIncorporating covariates in skewed functional data models. \bjournalBiostatistics \bvolume16 \bpages413–426. \endbibitem

- Liebl (2013) {barticle}[author] \bauthor\bsnmLiebl, \bfnmD.\binitsD. (\byear2013). \btitleModeling and forecasting electricity spot prices: a functional data perspective. \bjournalThe Annals of Applied Statistics \bvolume7 \bpages1562–1592. \endbibitem

- Liebl (2019a) {barticle}[author] \bauthor\bsnmLiebl, \bfnmDominik\binitsD. (\byear2019a). \btitleInference for sparse and dense functional data with covariate adjustments. \bjournalJournal of Multivariate Analysis (forthcoming). \endbibitem

- Liebl (2019b) {barticle}[author] \bauthor\bsnmLiebl, \bfnmDominik\binitsD. (\byear2019b). \btitleSupplement to “Nonparametric Testing for Differences in Electricity Prices: The Case of the Fukushima Nuclear Accident”. \endbibitem

- Lijesen (2007) {barticle}[author] \bauthor\bsnmLijesen, \bfnmMark G.\binitsM. G. (\byear2007). \btitleThe real-time price elasticity of electricity. \bjournalEnergy Economics \bvolume29 \bpages249–258. \endbibitem

- Lisi and Shah (2018) {barticle}[author] \bauthor\bsnmLisi, \bfnmFrancesco\binitsF. and \bauthor\bsnmShah, \bfnmIsmail\binitsI. (\byear2018). \btitleForecasting next-day electricity demand and prices based on functional models. \bjournal(working paper). \endbibitem

- Maciejowska and Weron (2016) {barticle}[author] \bauthor\bsnmMaciejowska, \bfnmKatarzyna\binitsK. and \bauthor\bsnmWeron, \bfnmRafał\binitsR. (\byear2016). \btitleShort-and mid-term forecasting of baseload electricity prices in the UK: The impact of intra-day price relationships and market fundamentals. \bjournalIEEE Transactions on Power Systems \bvolume31 \bpages994–1005. \endbibitem

- MacKinlay (1997) {barticle}[author] \bauthor\bsnmMacKinlay, \bfnmA Craig\binitsA. C. (\byear1997). \btitleEvent studies in economics and finance. \bjournalJournal of Economic Literature \bvolume35 \bpages13–39. \endbibitem

- Martins-Filho and Yao (2007) {barticle}[author] \bauthor\bsnmMartins-Filho, \bfnmCarlos\binitsC. and \bauthor\bsnmYao, \bfnmFeng\binitsF. (\byear2007). \btitleNonparametric frontier estimation via local linear regression. \bjournalJournal of Econometrics \bvolume141 \bpages283–319. \endbibitem

- McDermott and Nilsen (2014) {barticle}[author] \bauthor\bsnmMcDermott, \bfnmGrant R\binitsG. R. and \bauthor\bsnmNilsen, \bfnmØivind A\binitsØ. A. (\byear2014). \btitleElectricity prices, river temperatures, and cooling water scarcity. \bjournalLand Economics \bvolume90 \bpages131–148. \endbibitem

- McWilliams and Siegel (1997) {barticle}[author] \bauthor\bsnmMcWilliams, \bfnmAbagail\binitsA. and \bauthor\bsnmSiegel, \bfnmDonald\binitsD. (\byear1997). \btitleEvent studies in management research: Theoretical and empirical issues. \bjournalAcademy of Management Journal \bvolume40 \bpages626–657. \endbibitem

- Paraschiv, Erni and Pietsch (2014) {barticle}[author] \bauthor\bsnmParaschiv, \bfnmFlorentina\binitsF., \bauthor\bsnmErni, \bfnmDavid\binitsD. and \bauthor\bsnmPietsch, \bfnmRalf\binitsR. (\byear2014). \btitleThe impact of renewable energies on EEX day-ahead electricity prices. \bjournalEnergy Policy \bvolume73 \bpages196–210. \endbibitem

- Rabi, Hadzima-Nyarko and Šperac (2015) {barticle}[author] \bauthor\bsnmRabi, \bfnmAnamarija\binitsA., \bauthor\bsnmHadzima-Nyarko, \bfnmMarijana\binitsM. and \bauthor\bsnmŠperac, \bfnmMarija\binitsM. (\byear2015). \btitleModelling river temperature from air temperature: Case of the river Drava (Croatia). \bjournalHydrological Sciences Journal \bvolume60 \bpages1490-1507. \endbibitem

- Ramsay and Silverman (2005) {bbook}[author] \bauthor\bsnmRamsay, \bfnmJ O\binitsJ. O. and \bauthor\bsnmSilverman, \bfnmB W\binitsB. W. (\byear2005). \btitleFunctional Data Analysis, \bedition2. ed. \bseriesSpringer Series in Statistics. \bpublisherSpringer. \endbibitem

- Rohatgi (2018) {bmanual}[author] \bauthor\bsnmRohatgi, \bfnmAnkit\binitsA. (\byear2018). \btitleWebPlotDigitizer, Version: 4.1, \baddressAustin, Texas, USA. \endbibitem

- Ruppert and Wand (1994) {barticle}[author] \bauthor\bsnmRuppert, \bfnmD.\binitsD. and \bauthor\bsnmWand, \bfnmM. P.\binitsM. P. (\byear1994). \btitleMultivariate locally weighted least squares regression. \bjournalThe Annals of Statistics \bvolume22 \bpages1346–1370. \endbibitem

- Sensfuß, Ragwitz and Genoese (2008) {barticle}[author] \bauthor\bsnmSensfuß, \bfnmFrank\binitsF., \bauthor\bsnmRagwitz, \bfnmMario\binitsM. and \bauthor\bsnmGenoese, \bfnmMassimo\binitsM. (\byear2008). \btitleThe merit-order effect: A detailed analysis of the price effect of renewable electricity generation on spot market prices in Germany. \bjournalEnergy Policy \bvolume36 \bpages3086–3094. \endbibitem

- Serban (2011) {barticle}[author] \bauthor\bsnmSerban, \bfnmNicoleta\binitsN. (\byear2011). \btitleA space-time varying coefficient model: The equity of service accessibility. \bjournalThe Annals of Applied Statistics \bvolume5 \bpages2024–2051. \endbibitem

- Shah and Lisi (2018) {barticle}[author] \bauthor\bsnmShah, \bfnmIsmail\binitsI. and \bauthor\bsnmLisi, \bfnmFrancesco\binitsF. (\byear2018). \btitleForecasting of electricity price through a functional prediction of supply and demand curves. \bjournal(working paper). \endbibitem

- Sheather and Jones (1991) {barticle}[author] \bauthor\bsnmSheather, \bfnmSimon J\binitsS. J. and \bauthor\bsnmJones, \bfnmMichael C\binitsM. C. (\byear1991). \btitleA reliable data-based bandwidth selection method for kernel density estimation. \bjournalJournal of the Royal Statistical Society. Series B (Methodological) \bvolume53 \bpages683–690. \endbibitem

- Thoenes (2014) {barticle}[author] \bauthor\bsnmThoenes, \bfnmStefan\binitsS. (\byear2014). \btitleUnderstanding the determinants of electricity prices and the impact of the German nuclear moratorium in 2011. \bjournalThe Energy Journal \bvolume35 \bpages61–78. \endbibitem

- Venables and Ripley (2002) {bbook}[author] \bauthor\bsnmVenables, \bfnmW. N.\binitsW. N. and \bauthor\bsnmRipley, \bfnmB. D.\binitsB. D. (\byear2002). \btitleModern Applied Statistics with S, \beditionFourth ed. \bpublisherSpringer, \baddressNew York. \endbibitem

- Vsevolozhskaya, Greenwood and Holodov (2014) {barticle}[author] \bauthor\bsnmVsevolozhskaya, \bfnmOlga\binitsO., \bauthor\bsnmGreenwood, \bfnmMark\binitsM. and \bauthor\bsnmHolodov, \bfnmDmitri\binitsD. (\byear2014). \btitlePairwise comparison of treatment levels in functional analysis of variance with application to erythrocyte hemolysis. \bjournalThe Annals of Applied Statistics \bvolume8 \bpages905–925. \endbibitem

- Wagner (1982) {barticle}[author] \bauthor\bsnmWagner, \bfnmClifford H\binitsC. H. (\byear1982). \btitleSimpson’s paradox in real life. \bjournalThe American Statistician \bvolume36 \bpages46–48. \endbibitem

- Yao, Müller and Wang (2005) {barticle}[author] \bauthor\bsnmYao, \bfnmF\binitsF., \bauthor\bsnmMüller, \bfnmH G\binitsH. G. and \bauthor\bsnmWang, \bfnmJ L\binitsJ. L. (\byear2005). \btitleFunctional data analysis for sparse longitudinal data. \bjournalJournal of the American Statistical Association \bvolume100 \bpages577–590. \endbibitem

- Zhang and Chen (2007) {barticle}[author] \bauthor\bsnmZhang, \bfnmJin-Ting\binitsJ.-T. and \bauthor\bsnmChen, \bfnmJianwei\binitsJ. (\byear2007). \btitleStatistical inferences for functional data. \bjournalThe Annals of Statistics \bvolume35 \bpages1052–1079. \endbibitem

- Zhang and Wang (2016) {barticle}[author] \bauthor\bsnmZhang, \bfnmXiaoke\binitsX. and \bauthor\bsnmWang, \bfnmJane-Ling\binitsJ.-L. (\byear2016). \btitleFrom sparse to dense functional data and beyond. \bjournalThe Annals of Statistics \bvolume44 \bpages2281–2321. \endbibitem

- Zhang and Wei (2015) {barticle}[author] \bauthor\bsnmZhang, \bfnmWenfei\binitsW. and \bauthor\bsnmWei, \bfnmYing\binitsY. (\byear2015). \btitleRegression based principal component analysis for sparse functional data with applications to screening growth paths. \bjournalThe Annals of Applied Statistics \bvolume9 \bpages597–620. \endbibitem

1

Supplementary Paper for:

Nonparametric Testing for Differences in Electricity Prices: The Case of the Fukushima Nuclear Accident

By Dominik Liebl

Our basic assumptions, are essentially equivalent to those in Ruppert and Wand (1994) with some straightforward adjustments to our functional data and time series context.

-

A1 (Asymptotic Scenario) , where such that with . Hereby, “” denotes that the two sequences and are asymptotically equivalent, i.e., that with constant .

-

A2 (Random Design) The triple ) has the same distribution as with pdf where for all and zero else. The error term is iid and independent from , , and for all and .

-

A3 (Smoothness & Kernel) The pdf and its marginals are continuously differentiable. All second-order derivatives of the function are continuous. The (auto-)covariance functions , , are continuously differentiable for all points within their supports. The multiplicative kernel functions and are products of second-order kernel functions .

-

A4 (Moments & Dependency) , , and are strictly stationary, ergodic, and weakly dependent time series with auto-covariances that converge uniformly to zero at a geometrical rate. It is assumed that , , for all , , and .

-

A5 (Bandwidths) and as . and as .

Remark

Assumption A1 is a simplified version of the asymptotic setup of Zhang and Wang (2016). The case implies that is bounded which corresponds to a simplified version of the finite- asymptotic considered by Jiang and Wang (2010). For we can consider all further scenarios from sparse to dense functional data. In line with our real data application, we consider a deterministic as also done, for instance, by Hall, Müller and Wang (2006). However, our results are generalizable to a random using some minor modifications.

Appendix A Proofs

The following Lemma A.1 builds the basis of our theoretical results.

Lemma A.1 (Bias and Variance of ).

Let be an interior point of . Under Assumptions A1-A5 the conditional asymptotic bias and variance of the LLK estimator in Eq. (2.2) are then given by

Proof of Lemma A.1. Our proof of Lemma A.1 generally follows that of \citeappendixRW94, and differs only from the latter reference as we consider additionally a conditioning variable , a function-valued error term, and a time series context.

Proof of Lemma A.1, part (i): For simplicity, consider a second-order kernel function with compact support such as the Epanechnikov kernel; this is, of course, without loss of generality. Let be a interior point of and define , , and . Using a Taylor-expansion of around , the conditional bias of the estimator can be written as

| (A.1) | |||

where is a vector with typical elements

with being the Hessian matrix of the regression function . The vector holds the remainder terms as in \citeappendixRW94.

Next we derive asymptotic approximations for the matrix

and the matrix

of the right hand side of Eq. (A.1). Using standard arguments from nonparametric statistics it is easy to derive that

where and is the vector of first order partial derivatives (i.e., the gradient) of the pdf at . Inversion of the above block matrix yields

| (A.2) |

The matrix can be partitioned as following:

where the dimensional upper element can be approximated by

| (A.3) | ||||

and the dimensional lower bloc is equal to

| (A.4) | |||

Plugging the approximations of Eqs. (A.2)-(A.4) into the first summand of the conditional bias expression in Eq. (A.1) leads to the following expression

Furthermore, it is easily seen that the second summand of the conditional bias expression in Eq. (A.1), which holds the remainder term, is given by

Summation of the two latter expressions yields the asymptotic approximation of the conditional bias

Proof of Lemma A.1, part (ii): In the following we derive the conditional variance of the local linear estimator

where is a matrix with typical elements

with being the indicator function.

Lemma A.2.

The upper-left scalar (block) of the matrix

is given by

where . Under Assumption A4 there exists a constant , , such that .

Lemma A.3.

The dimensional upper-right block of the matrix

is given by

where . Under Assumption A4 there exists a constant , , such that .

Remark

The dimensional lower-left block of the matrix

is simply the transposed version of the result in Lemma A.3.

Lemma A.4.

The lower-right block of the matrix

is given by

where . Under Assumption A4 there exists a constant , , such that .

Using the approximations for the bloc-elements of the matrix

, given by the Lemmas A.2-A.4, and the approximation for the matrix

, given in (A.2), we can approximate the conditional variance of the bivariate local linear estimator, given in (LABEL:Varexpr). Some straightforward matrix algebra leads to

which is asymptotically equivalent to our variance statement of Lemma A.1 part (ii).

Proof of Lemma A.2. (The proofs of Lemmas A.3 and A.4 can be done correspondingly.) To show Lemma A.2 it will be convenient to split the sum such that . Using standard procedures from kernel density estimation leads to

| (A.6) | ||||

| (A.7) | ||||

| (A.8) | ||||

where . Summing up (A.6)-(A.7) leads to the result in Lemma A.2. Lemmas A.3 and A.4 differ from Lemma A.2 only with respect to the additional factors and . These come in due to the usual substitution step for the additional data parts .

Appendix B Data Sources

Hourly spot prices of the German electricity market are provided by the European Energy Power Exchange (EPEX) (www.epexspot.com), hourly values of Germany’s gross electricity demand and electricity exchanges with other countries are provided by the European Network of Transmission System Operators for Electricity (www.entsoe.eu). German wind and solar power infeed data are provided by the transparency platform of the European Energy Exchange (www.eex-transparency.com). German air temperature data are available from the German Weather Service (www.dwd.de). The daily prices for natural gas are provided via the trading platform PEGAS, which is part of the European Energy Exchange (EEX) Group operated by Powernext (www.powernext.com). Daily prices for European CO2 Emission Allowances (EUA) and for the Amsterdam-Rotterdam-Antwerp (ARA) coal futures are provided via the websites of the EEX (www.eex.com)

imsart-nameyear \bibliographyappendixbibfile_ARCHIV.bib