Long-Term Online Smoothing Prediction

Using Expert Advice

Abstract

For the prediction with experts’ advice setting we construct forecasting algorithms that suffer loss not much more than any expert in the pool. In contrast to the standard approach, we investigate the case of long-term forecasting of time series and consider two scenarios. In the first one, at each step the learner has to combine the point forecasts of the experts issued for the time interval ahead. Our approach implies that at each time step experts issue point forecasts for arbitrary many steps ahead and then the learner (algorithm) combines these forecasts and the forecasts made earlier into one vector forecast for steps . By combining past and the current long-term forecasts we obtain a smoothing mechanism that protects our algorithm from temporary trend changes, noise and outliers. In the second scenario, at each step experts issue a prediction function, and the learner has to combine these functions into the single one, which will be used for long-term time-series prediction. For each scenario we develop an algorithm for combining experts forecasts and prove adversarial regret upper bound for both algorithms.

keywords:

long-term online smoothing forecasting , prediction with expert advice , online smoothing regression1 Introduction

The problem of long-term forecasting of time series is of high practical importance. For example, nowadays nearly everybody uses long-term weather forecasts [1, 2] (24 hour, 7 days, etc.) provided by local weather forecasting platforms. Road traffic and jams forecasts [3, 4, 5] are being actively used in many modern navigating systems. Forecasts of energy consumption and costs [6], web traffic [7] and stock prices [8, 9] are also widely used in practice.

Many state-of-the-art (e.g. ARIMA [10]) and modern (e.g. Facebook Prophet111https://github.com/facebook/prophet [11]) time series forecasting approaches produce a model that is capable of predicting arbitrarily many steps ahead. The advantage of such models is that when building the final forecast at each step for interval ahead, one may use forecasts made earlier at the steps . Forecasts of each step are made using less of the observed data. Nevertheless, they can be more robust to noise, outliers and novelty of the time interval . Thus, the usage of such outdated forecasts may prove useful, especially if time series is stationary.

In general, we consider the game-theoretic on-line learning model in which a master (aggregating) algorithm has to combine predictions from a set of experts. The problem setting we investigate can be considered as the part of Decision-Theoretic Online Learning (DTOL) or Prediction with Expert Advice (PEA) framework (see e.g. [12, 13, 14, 15, 16, 17] among others). In this framework the learner is usually called the aggregating algorithm. The aggregating algorithm combines the predictions from a set of experts in the online mode during time steps .

In practice for time series prediction the square loss function is widely used. The square loss function is mixable [15]. For mixable loss functions Vovk’s aggregating algorithm (AA) [15, 18] is the most appropriate, since it has theoretically best performance among all known algorithms. We use the aggregating algorithm as the base and modify it for the long-term forecasting.

The long-term forecasting considered in this paper is a case of the forecasting with a delayed feedback. As far as we know, the problem of the delayed feedback forecasting was first considered by [19].

In this paper we consider the two scenarios of the long-term forecasting. In the first one, at each step the learner has to combine the point forecasts of the experts issued for the time interval ahead. In the second scenario, at each step experts issue prediction functions, and the learner has to combine these functions into the single one, that will be used for long-term time-series prediction.

The first theoretical problem we investigate in the paper is the effective usage of the outdated forecasts. Formally, the learner is given basic forecasting models. Each model at every step produces infinite forecast for the steps ahead. The goal of the learner at each step is to combine the current models’ forecasts and the forecasts made earlier into one aggregated long-term forecast for the time interval ahead. We develop an algorithm to efficiently combine these forecasts.

Our main idea is to replicate any expert in an infinite sequence of auxiliary experts , where . Each expert issues at time moment an infinite sequence of forecasts for time moments . Only a finite number of the experts are available at any time moment. The setting presented in this paper is valid also in case where only one expert () is given. At any time moment the AA uses predictions of each expert for the time interval (made by expert at time ). In our case, the performance of the AA on the step is measured by the regret which is the difference between the average loss of the aggregating algorithm suffered on time interval and the average loss of the best auxiliary expert suffered on the same time interval. Note that the recent related work is [20] where an algorithm with tight upper bound for predicting vector valued outcomes was presented.

In the second part of our paper we consider the online supervised learning scenario. The data is represented by pairs of predictor-response variables. Instead of point or interval predictions, the experts and the learner present predictions in the form of functions from signals . Signals appear gradually over time and allow to calculate forecasts as the values of these functions. For this problem we present method for smoothing regression using expert advice.

2 Preliminaries

In this section we recall the main ideas of prediction with expert advice theory. Let a pool of experts be given. Suppose that elements of a time series are revealed online – step by step. Learning proceeds in trials . At each time moment experts present their predictions and the aggregating algorithm presents its own forecast . When the corresponding outcome(s) are revealed, all the experts suffer their losses using a loss function: , . Let be the loss of the aggregating algorithm. The cumulative loss suffered by any expert and by AA during steps are defined as

The performance of the algorithm w.r.t. an expert can be measured by the regret .

The goal of the aggregating algorithm is to minimize the regret with respect to each expert. In order to achieve this goal, at each time moment , the aggregating algorithm evaluates performance of the experts in the form of a vector of experts’ weights , where and for all . The weight of an expert is an estimate of the quality of the expert’s predictions at step . In classical setting (see [13], [14] among others), the process of expert weights updating is based on the method of exponential weighting with a learning rate :

| (1) |

where is some weight vector, for example, . In classical setting, we prepare weights for using at the next step or, in a more general case of the -th outcome ahead prediction, we define , where .

The Vovk’s aggregating algorithm (AA) ([14], [15]) is the base algorithm in our study. Let us explain the main ideas of learning with AA.

We consider the learning with a mixable loss function . Here is an element of some set of outcomes , and is an element of some set of forecasts . The experts present the forecasts .

In this case the main tool is a superprediction function

where is a probability distribution on the set of all experts and is a vector of the experts predictions.

The loss function is mixable if for any probability distribution on the set of experts and for any set of experts predictions a value of exists such that

| (2) |

for all .

We fix some rule for computing a forecast satisfying (2). is called a substitution function.

It will be proved in Section A that using the rules (1) and (2) for defining weights and the forecasts in the online mode we obtain

for all .

A loss function is -exponential concave if for any the function is concave w.r.t. . By definition any -exponential concave function is -mixable.

The square loss function is -mixable for any such that , where and are a real numbers and for some , see [14, 15].

3 Algorithm for Combining Long-term Forecasts of Experts.

In this section we consider an extended setting. At each time moment each expert presents an infinite sequence of forecasts for the time moments . A sequence of the corresponding confidence levels also can be presented at time moment . Each element of this sequence is a number between 0 and 1. If , then it means that we use the forecast only partially (e.g. it may become obsolete with time). If then the corresponding forecast is not taken into account at all.222For example, in applications, it is convenient for some to set for all , since too far predictions become obsolete. Confidence levels can be set by the expert itself or by the learner.333 The setting of prediction with experts that report their confidences as a number in the interval was first studied by [22] and further developed by [23].

At each time moment we observe sequences , issued by the experts at the time moments . To aggregate the forecasts of all experts, we convert any “real” expert into the infinite sequence of the auxiliary experts , where .

At each time moment expert presents his forecast which is the segment of the sequence of length starting at its th element. More precisely, the forecast of the auxiliary expert is a vector

where for we set .

We also denote the corresponding segments of confidence levels by

where for and for .

Using the losses suffered by the experts (for ) on the time interval , the aggregating algorithm updates the weights of all the experts by the rule (1). We denote these weights by and use them for computing the aggregated interval forecast for time moments ahead

We use the fixed point method by [24]. Define the virtual forecasts of the experts :

where and .

We consider any confidence level as a probability distribution on a two element set.

First, we provide a justification of the algorithm presented below. Our goal is to define the forecast such that for

| (5) |

for each outcome . Here is the mathematical expectation with respect to the probability distribution . Also, is the weight of the auxiliary expert accumulated at the end of step .

We rewrite inequality (5) in a more detailed form: for any ,

| (6) | |||

| (7) |

for all . Therefore, the inequality (5) is equivalent to the inequality

| (8) |

where

| (9) |

According to the aggregating algorithm rule we can define for such that (8) and its equivalent (5) are valid. Here is the substitution function and

The outcomes will be fully revealed only at the time moment . The inequality (5) holds for and for the forecasts for all . By convexity of the exponent the inequality (5) implies that

| (10) |

holds for all . We use the generalized Hölder inequality and obtain

| (11) |

For more details of the Hölder inequality see A. The inequality (11) can be rewritten as

| (12) |

where

is the (averaged) loss of the aggregating algorithm suffered on the time interval and

is the (averaged) mean loss of the expert .

The protocol of algorithm for aggregating forecasts of experts is shown below.

Algorithm 1

Set , where , , .

FOR

IF THEN put for all and .

ELSE

-

1.

Observe the outcomes and predictions of the learner issued at the time moment .

-

2.

Compute the loss of the learner on the time segment , where .

-

3.

Compute the losses of the experts for , where for we set if and if .

ENDIF

-

4.

Update weights:

(13) for , .444These weights can be computed efficiently, since the divisor in (13) can be represented (14)

-

5.

Prepare the weights: for and .

-

6.

Receive predictions issued by the experts at the time moments and their confidence levels .

-

7.

Extract the segments of forecasts of the the auxiliary experts , where for , and the segments of the corresponding confidences , where .555Here is a forecast of the real expert for the time moment issued at the time moment and .

- 8.

ENDFOR

Denote for

We put these quantities to be 0 for . Also, for . Since by definition

we have

Recall that be the algorithm (average) loss and be the (average) loss of the auxiliary expert .

Define the discounted (average) excess loss with respect to an expert at a time moment by

| (16) |

By definition of we can represent the discounted excess loss (16) as

We measure the performance of our algorithm by the cumulative discounted (average) excess loss with respect to any expert .

Theorem 1.

For any and , the following upper bound for the cumulative excess loss holds true:

| (17) |

4 Online Smoothing Regression

In this section we consider the online learning scenario within the supervised setting (that is, data are pairs of predictor-response variables). A forecaster presents a regression function defined on a set of objects, which are called signals. After a pair be revealed the forecaster suffers a loss , where is some loss function. We assume that and that the loss function is -mixable for some .

An example is a linear regression, where is a set of -dimensional vectors and a regression function is a linear function , where is a weight vector and is the square loss.

In the online mode, at any step , to define the forecast for step – a regression function , we use the prediction with expert advice approach. A feature of this approach is that we aggregate the regression functions for , each of which depends on the segment of the sample. At the end of step we define (initialize) the next regression function by the sample .

Since the forecast can potentially be applied to any future input value , we consider this method as a kind of long-term forecasting.

We briefly describe below the changes made in Algorithm 1. We introduce signals in the protocol from Section 3.

Algorithm 2

Set initial weights as in Algorithm 1.

FOR

-

1.

Observe the pair and compute the losses suffered by the learner and by the expert regression functions: if and otherwise.

- 2.

- 3.

ENDFOR

For the square loss , where , by (3) the regression function (20) can be defined in the closed form:

| (21) |

for each or by the rule (4).888The most appropriate choices of are for the rule (3) and for (4). The more straightforward definition (4) results in four times more regret but easier for computation.

Let us analyze the performance of Algorithm 2 as a forecaster on steps ahead.

For any time moment a sequence is revealed. Denote by the average loss of the learner on time interval and by the average loss of any auxiliary expert .

The regret bound of Algorithm 2 does not depend on :

Theorem 2.

For any ,

| (22) |

Proof. The analysis of the performance of Algorithm 2 for the case of prediction on steps ahead is similar to that of Algorithm 1 for . Let and be given. Using the technics of Section A, we obtain for any ,

Summing this inequality by and dividing by , we obtain (22).

In particular, Theorem 2 implies that the total loss of Algorithm 2 at any time interval is no more (up to logarithmic regret) than the loss of the best regression algorithm constructed in the past.

Online regression with a sliding window. Some time series show a strong dependence on the latest information instead of all the data. In this case, it is useful to apply regression with a sliding window. In this regard, we consider the application of Algorithm 2 for the case of online regression with a sliding window. The corresponding expert represents some type of dependence between input and output data. If this relationship is relatively regular the corresponding experts based on past data can successfully compete with experts based on the latest data. Therefore, it may be useful to aggregate the predictions of all the auxiliary experts based on past data.

Let be the ridge regression function, where for , . Here is the matrix in which rows are formed by vectors ( is the transposed matrix ), is a unit matrix, is a parameter, and . For we set equal to some fixed value.

We use the square loss function and assume that for all . For each we define the aggregating regression function (the learner forecast) by (21) using the regression functions (the expert strategies) for , where each such a function is defined using a learning sample (a window) .999 The computationally efficient algorithm for recalculating matrices during the transition from to for some special type of online regression with a sliding window was presented by [25]. Similar effective options for regression using Algorithm 2 can also be developed.

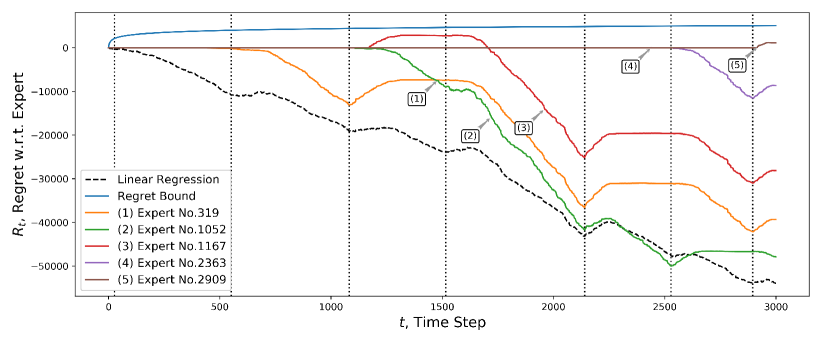

Experiments. Let us present the results of experiments which were performed on synthetic data. The initial data was obtained as a result of sampling from a data generative model.

We start from a sequence of -dimensional signals sampled i.i.d from the multidimensional normal distribution. The signals are revealed online and .

The target variable is generated as follows. First, three random linear dependencies are generated, i.e. three weights vectors are generated (so for on the corresponding time intervals). The time scale is divided into random consecutive parts. On each interval data is generated based on one of these three random regressions , where or and is a low noise. That is, the dependence of on is switched times.

Each expert corresponds to a linear regression trained in a sliding data window of length . There are a total of experts.

Figure 1 shows the results of the random experiment, where the graphs of present the regret of Algorithm 2 with respect to the experts starting at several time moments .

The regret with respect to the simple linear regression performed on all data interval is also presented. We see that Algorithm 2 efficiently adapts to data and also outperforms linear regression on the entire dataset. The theoretical upper bound for the regret is also plotted (it is clear that all lines are below it).

5 Conclusion

In the paper we have developed the aggregating algorithm for long-term interval forecasting which is capable of combining current predictions of the experts with the outdated ones (made earlier). Combining past and current long-term forecasts allows to protects the algorithm from temporary changes in the trend of the time series, noise and outliers. Our mechanism can be applied to the time series forecasting models that are capable of predicting for the infinitely many time moments ahead, e.g. widespread ARMA-like models. For the developed algorithm we proved the sublinear regret bound.

We have applied PEA approach for the case of online supervised learning, where instead of point predictions, the experts and the learner present predictions in the form of regression functions. The method for smoothing regression using expert advice was presented. We consider this method of regression as a kind of long-term forecasting. Experiments conducted on synthetic data show the effectiveness of the proposed method.

Acknowledgments

The research was partially supported by the Russian Foundation for Basic Research grant 16-29-09649 ofi m.

References

- Richardson [2007] L. F. Richardson, Weather prediction by numerical process, Cambridge University Press, 2007.

- Lorenc [1986] A. C. Lorenc, Analysis methods for numerical weather prediction, Quarterly Journal of the Royal Meteorological Society 112 (474) (1986) 1177–1194.

- De Wit et al. [2015] C. C. De Wit, F. Morbidi, L. L. Ojeda, A. Y. Kibangou, I. Bellicot, P. Bellemain, Grenoble traffic lab: An experimental platform for advanced traffic monitoring and forecasting [applications of control], IEEE Control Systems 35 (3) (2015) 23–39.

- Herrera et al. [2010] J. C. Herrera, D. B. Work, R. Herring, X. J. Ban, Q. Jacobson, A. M. Bayen, Evaluation of traffic data obtained via GPS-enabled mobile phones: The Mobile Century field experiment, Transportation Research Part C: Emerging Technologies 18 (4) (2010) 568–583.

- Myr [2002] D. Myr, Real time vehicle guidance and forecasting system under traffic jam conditions, uS Patent 6,480,783, 2002.

- Gaillard and Goude [2015] P. Gaillard, Y. Goude, Forecasting electricity consumption by aggregating experts; how to design a good set of experts, in: Modeling and stochastic learning for forecasting in high dimensions, Springer, 95–115, 2015.

- Oliveira et al. [2016] T. P. Oliveira, J. S. Barbar, A. S. Soares, Computer network traffic prediction: a comparison between traditional and deep learning neural networks, International Journal of Big Data Intelligence 3 (1) (2016) 28–37.

- Ding et al. [2015] X. Ding, Y. Zhang, T. Liu, J. Duan, Deep learning for event-driven stock prediction., in: Ijcai, 2327–2333, 2015.

- Pai and Lin [2005] P.-F. Pai, C.-S. Lin, A hybrid ARIMA and support vector machines model in stock price forecasting, Omega 33 (6) (2005) 497–505.

- Box et al. [2015] G. E. Box, G. M. Jenkins, G. C. Reinsel, G. M. Ljung, Time series analysis: forecasting and control, John Wiley & Sons, 2015.

- Taylor and Letham [2018] S. J. Taylor, B. Letham, Forecasting at scale, The American Statistician 72 (1) (2018) 37–45.

- Littlestone and Warmuth [1994] N. Littlestone, M. K. Warmuth, The Weighted Majority Algorithm, Inf. Comput. 108 (2) (1994) 212–261, ISSN 0890-5401, URL http://dx.doi.org/10.1006/inco.1994.1009.

- Freund and Schapire [1997] Y. Freund, R. E. Schapire, A Decision-Theoretic Generalization of On-Line Learning and an Application to Boosting, Journal of Computer and System Sciences 55 (1) (1997) 119 – 139, ISSN 0022-0000, URL http://www.sciencedirect.com/science/article/pii/S002200009791504X.

- Vovk [1990] V. G. Vovk, Aggregating Strategies, in: Proceedings of the Third Annual Workshop on Computational Learning Theory, COLT ’90, Morgan Kaufmann Publishers Inc., San Francisco, CA, USA, ISBN 1-55860-146-5, 371–386, URL http://dl.acm.org/citation.cfm?id=92571.92672, 1990.

- Vovk [1998] V. Vovk, A Game of Prediction with Expert Advice, J. Comput. Syst. Sci. 56 (2) (1998) 153–173, ISSN 0022-0000, URL http://dx.doi.org/10.1006/jcss.1997.1556.

- Cesa-Bianchi and Lugosi [2006] N. Cesa-Bianchi, G. Lugosi, Prediction, Learning, and Games, Cambridge University Press, New York, NY, USA, ISBN 0521841089, 2006.

- Korotin et al. [2018] A. Korotin, V. V’yugin, E. Burnaev, Aggregating Strategies for Long-term Forecasting, arXiv preprint arXiv:1803.06727 .

- Vovk [2001] V. Vovk, Competitive on-line statistics, INTERNATIONAL STATISTICAL REVIEW 69 (2) (2001) 213–248, ISSN 0306-7734.

- Weinberger and Ordentlich [2002] M. J. Weinberger, E. Ordentlich, On delayed prediction of individual sequences, IEEE Transactions on Information Theory 48 (7) (2002) 1959–1976, ISSN 0018-9448.

- Adamskiy et al. [2017] D. Adamskiy, T. Bellotti, R. Dzhamtyrova, Y. Kalnishkan, Aggregating Algorithm for Prediction of Packs, CoRR abs/1710.08114, URL http://arxiv.org/abs/1710.08114.

- Kivinen and Warmuth [1999] J. Kivinen, M. K. Warmuth, Averaging Expert Predictions, in: P. Fischer, H. U. Simon (Eds.), Computational Learning Theory, Springer Berlin Heidelberg, Berlin, Heidelberg, ISBN 978-3-540-49097-5, 153–167, 1999.

- Blum and Mansour [2007] A. Blum, Y. Mansour, From External to Internal Regret, J. Mach. Learn. Res. 8 (2007) 1307–1324, ISSN 1532-4435, URL http://dl.acm.org/citation.cfm?id=1314498.1314543.

- Cesa-Bianchi et al. [2007] N. Cesa-Bianchi, Y. Mansour, G. Stoltz, Improved Second-order Bounds for Prediction with Expert Advice, Mach. Learn. 66 (2-3) (2007) 321–352, ISSN 0885-6125, URL http://dx.doi.org/10.1007/s10994-006-5001-7.

- Chernov and Vovk [2009] A. V. Chernov, V. Vovk, Prediction with Expert Evaluators’ Advice, in: LNCS, vol. 5809, Springer, 8–22, 2009.

- Arce and Salinas [2012] P. Arce, L. Salinas, Online ridge regression method using sliding windows, in: Chilean Computer Science Society (SCCC), 2012 31st International Conference of the, IEEE, 87–90, 2012.

- Bousquet and Warmuth [2003] O. Bousquet, M. K. Warmuth, Tracking a Small Set of Experts by Mixing Past Posteriors, J. Mach. Learn. Res. 3 (2003) 363–396, ISSN 1532-4435, URL http://dl.acm.org/citation.cfm?id=944919.944940.

Appendix A Auxiliary results

Vector-valued forecasts. In this paper we aggregate the vector forecasts. To do this, following [20], we apply the aggregation rule to each coordinate separately. Since the loss function is -mixable, for any time moment for each a prediction exists such that the inequality (6) is valid.

Let be a sequence of outcomes. Multiplying the inequalities (10) for we obtain

| (23) |

The generalized Hölder inequality says that

where , and for . Let for all , then . Let

for and , where

Then by Hölder inequality we obtain (11).

Regret analysis. We use relative entropy as the basic tool for the regret analysis. Let be the relative entropy, where and are probability vectors.101010That is, , for all and and . We also define .

Let be the losses of the experts at step , where and for . Let also, the evolution of the weights of the experts be defined by the rule (1) and . Denote the dot product of two vectors by . Let also, for .

Lemma 1.

(see [26]) For any , and for a comparison probability vector ,

| (24) |

Corollary 1.

Let be a forecasting horizon and be a number of the experts. Consider the case of -steps ahead prediction for . Then for any comparison vector ,

| (25) |

Proof. Summing (24) for , we obtain

| (26) | |||

| (27) | |||

| (28) |

In transition from (26) to (27) we use equality for . In transition from (27) to (28) the positive and corresponding negative terms telescope and only first positive terms remain. Also, we have used the inequality

for all probability vectors and .

Since for all and , (25) follows.