In search of a new economic model determined by logistic growth

Abstract

In this paper333Preliminary report, published in arXiv: https://arxiv.org/abs/1711.02625. we extend the work by Ryuzo Sato devoted to the development of economic growth models within the framework of the Lie group theory. We propose a new growth model based on the assumption of logistic growth in factors. It is employed to derive new production functions and introduce a new notion of wage share. In the process it is shown that the new functions compare reasonably well against relevant economic data. The corresponding problem of maximization of profit under conditions of perfect competition is solved with the aid of one of these functions. In addition, it is explained in reasonably rigorous mathematical terms why Bowley’s law no longer holds true in post-1960 data.

1 Introduction

As is well known, a production function is an essential feature of an economics growth model. Such a function can either be fixed, so that it is used to estimate the dynamics of other quantities, or it is the essential output of the model, obtained by studying the dynamics of the input factors.

An example of the former application of a production function is the celebrated Solow-Swan economic growth model [70, 73, 33] introduced in the 1950s to explain long-run economic growth, at which point it also generalized and extended the Harrod-Domar model [22, 38] tasked with this undertaking prior. The model in turn was later used as a starting point for the development of other economic growth models that emerged as its generalizations (see, for example, Ferrara and Guerrini [31] and the relevant references therein).

At the core of the Solow-Swan model and its generalizations is a production function , normally of the Cobb-Douglas type [19], where the factors and represent capital and labor respectively. The function is required to satisfy the so-called Inada conditions [41]. From a mathematical standpoint, the Solow-Swan economic growth model and its generalizations, for example, the Ramsey-Cass-Koopmans model [16, 49, 59], are governed by a single nonlinear differential equation or a system of such equations that describe the evolution of per capita capital stock, consumption, etc.

The theory of technical change and economic invariance developed by Ruzyo Sato [65] is an example of the latter approach, in which a production function is an output obtained within the framework of a model. In particular, the author and his collaborators have derived the Cobb-Douglas production function as a consequence of the exponential growth in factors (capital and labor).

In this article we continue the development of Sato’s theory by changing the assumptions about the Lie group theoretical properties of the technical progress representing the growth in factors.

Recall that in 1928 Charles Cobb and Paul Douglas published a paper [19] devoted to the study of the growth of the American economy during the period 1899-1922. To model the production output they used the following function, introduced earlier by Knut Wicksell:

| (1.1) |

where and are as before (i.e., in economic terms they are the factors of production), while denotes the total production, is total factor productivity, and are the output elasticities of capital and labor respectively. Sometimes the Cobb-Douglas function displays constant return to scale, which holds if

| (1.2) |

The Cobb-Douglas function (1.1) can be easily derived under the assumptions that there is no production if either capital or labor vanishes, the marginal productivity of capital is proportional to the amount of production per unit of capital (i.e., ), and the marginal productivity of labor is proportional to the amount of production per unit of labor (i.e., ).

More recently, Ryuzo Sato [64, 65] (see also Sato and Ramachardan [61]), while resolving the so-called Solow-Stigler controversy [71, 72], developed a Lie group theoretical framework to study technical progress and production functions. It can be viewed as an analogue of the Felix Klein approach to geometry formulated in his celebrated Erlangen Program [47] in which Lie transformation groups play a central role. For instance, within this framework the Cobb-Douglas production function (1.1) can be recovered as an invariant of the one-parameter Lie group action [21] that afford exponential growth in both and in the first quadrant of the two-dimensional Euclidean space . The key idea employed by Sato [64, 65], as well as Sato and Ramachadran [61] was to identify the corresponding exogeneous technical progress with the action of a one-parameter Lie group that acts in . More specifically, a Klein geometry can be described as a pair where is a Lie group and is a closed Lie subgroup of such that the (left) coset space is connected. The group is called the principal group of the geometry and is called the space of the geometry, which is a homogeneous space for . For instance, in this view the pair describes the Euclidean geometry of and its objects, say, surfaces can be classified modulo the action of the continuous isometry group (see, for example, Horwood et al [40], as well as Cochran et al [20] for more details). By analogy, a neoclassical growth model in the sense of Sato can be viewed as a pair , where the one-parameter Lie group of transformations acting in represents the technical progress in question. So far in the literature has been considered to be either of a uniform (neutral) factor-augmenting type, that is , , for some , or representing a non-uniform, biased type, that is , for some , . Therefore it is assumed in both cases that the economy grows exponentially (as per the corresponding growths in capital and labor), which was a reasonable assumption in the past based on the existing data at the time. It might no longer be the case, however, which may be attested to the fact, for example, that the Cobb-Douglas function can no longer be used to describe adequatly the growth of the American economy over a long run, including the recent decades — in the same way as it was done by Cobb and Douglas for the period 1899-1922 [19] (see Section 7 for more details).

The main goal of this paper is to use the existing model to develop a new mathematical paradigm that can be used to study the current state of economy. Accordingly, in what follows we will modify the economic growth models described by Sato within the framework of the Lie group theory according to the present economic realities [7]. More specifically, we will replace in a neoclassical growth model in the sense of Sato a group representing an exponential growth with another one-parameter Lie group that describes a logistic growth:

This idea is currently being exploited and developed from different angles and in different directions quite extensively in the literature by economists and mathematicians alike (see, for example, [1, 2, 12, 13, 14, 34, 35, 36, 26, 27, 28, 29, 30]), which is quite natural, given that the resources on our planet are limited.

Therefore our first task is to modify a basic growth model as described above and then, following Sato’s approach, derive a new production function that may replace the Cobb-Douglas function (1.1) in any models considered within the new paradigm of logistic growth, which is a reasonable further development, given that, for example, “… the US economy is not well described by a Cobb-Douglas aggregate production function …” (see Antràs [7] for more details).

Next, we will test the new production function derived purely by mathematical methods against a more up-to-date data to verify its suitability for being part of any new mathematical models. Finally, we will reconsider several classical examples utilizing the properties of the Cobb-Douglas production funciton by replacing it with our new production function derived via the Lie group theoretical approach developed by Sato and discuss the new results obtained under the assumption of logistic growth.

This paper is organized as follows. In Section 2 we lay the groundwork for the introduction of a new growth model and derivation of new production functions. Specifically, we review the Lie group approach introduced in [65] and employ it to rederive the Cobb-Douglas function (1.1). In Section 3 we depart from the growth model described by Sato based on exponential growth and introduce instead a new one — based on the assumption that factors grow logistically. In Section 4 we derive a new production function (4.5) within the framework of the growth model (3.1) introduced in Section 3. Section 5 is devoted to solving the problem of maximization of profit under condition of perfect competition, using the new production function (4.5). In Section 6 we explain, using mathematical reasonings and the results obtained in preceeding sections, why Bowley’s law [9, 10] no longer holds true in post-1960 data. In the process we also derive another production function (6.22) and a new modified wage sare (6.21). In Section 7 we use statistical analysis to investigate how estimations of the new production function (4.5) compare to economic data. In Section 8 we make concluding remarks and summarize our findings.

2 A Lie group approach to the study of holothetic production functions

In this section we will briefly review the Lie group theoretical approach developed by Sato to study holothetic production functions and employ it to derive the Cobb-Douglas production function (1.1). Consider a growth model , where is a continuous one-parameter group of transformations (see [61, 64, 65] for more details). In order to show that the increases in efficiency of inputs due to technical progress can be explained by economies of scale, Sato interpreted technical progress as the action of a one-parameter Lie group of transformations, for which the production function was an invariant. Under this arrangement the resulting transformation representing technical progress and generated by , indeed, preserves the isoquant map, i.e., maps one isoquant (or, in mathematical terms, a level curve of ) to another, that is, technical progress has the same effect as economies of scale.

More specifically, let capital and labour affected by technical progress and measured in the efficiency units, and , be given by

| (2.1) |

where and represent the effect of the exogenous technical progress. Following Sato and Ramachardan [61], let us remark that if the change generated by technical progress is Hicks-neutral. If technical progress is factor augmenting and biased, then . The functions , may depend on only, or they may be functions of , which would imply that the rate of technical progress on different rays are different, but the rate is constant on each of them. They functions , can also be functions of , and , which would entail that the rate of technical progress will also vary along a ray. In what follows, we will also require that the technical progress functions , represent the action of a one-parameter Lie group.

Consider now the case when both , , moreover, , , . Note, if the change generated by such technical progress is Hick-neutral. Clearly, the corresponding transformations

| (2.2) |

form a continuous one-parameter Lie group, which follows from the fact, for example, that transformation (2.2) determines the flow

| (2.3) |

generated by the following vector field

| (2.4) |

which generates the Lie algebra of the one-parameter Lie group , where is determined by (2.3) for each fixed .

More generally, suppose a technical progress is defined by the functions and such that

| (2.5) |

where is the technical progress parameter and the functions , are analytic and functionally independent. Moreover, let us also suppose the family of transformations (2.5) forms a one-parameter Lie group . Recall, that Sato observed in [65] that in this case a production function is holothetic under a continuous one-parameter Lie group transformatoin (2.5) iff

| (2.6) |

where , . The condition of holotheticity is crucial from the economic standpoint, because it assures that the isoquant map (i.e., the family of level curves of ) is invariant under the transformation (2.5) representing the technical change, which means that under isoquants are mapped onto isoquants and the techinical change in this case is transformed into a scale effect.

For example, if and in (2.6), , , which means , in (2.1), , it is a straigforward calculation, using the method of characteristic, that the general solution to the partial differential equation (2.6) is given by [65] (see also [63])

| (2.7) |

where is an arbitrary function.

The converse problem was also considered by Sato. Specifically, he established necessary and sufficient conditions for the existence of a technical progress that affords holotheticity of a given production function (see Lemma 4 in [65] on p. 34).

Now let us derive the Cobb-Douglas function (1.1) within the framework of the model , where the one-parameter Lie group of transformations determines the exponential growth (2.2). Consider the partial differential equation (2.6) with the coefficients and determined by (2.2) for , , . Clearly, we can determine a particular production function (2.7) by specifynig the function in (2.2). Since in this case defines an exponential growth, it is natural to impose the corresponing condition on — so that it is also subject to an exponential growth. Indeed, let , . Therefore we have

| (2.8) |

or, alternatively, we can solve instead the following partial differential equation

| (2.9) |

where , is a solution to (2.9), while is a solution to (2.8) and an invariant. Solving the corresponding sysetm of ordinary differential equations

| (2.10) |

using the method of characteristics, yields the function (1.1), where . Unfortunately, the elasticity elements in this case do not attain economically meaningful values like (1.2). To overcome this problem Sato in [65] adjusted the model accodingly. Specifically, he introduces the notion of the simultaneous holothenticity, which implies that a production function is holothetic under more than one type of technical change simultaneously. Mathematically, it means that a production function is an invariant of an integrable distribution of vector fields [3] on , each representing a technical change as per the formula (2.8) (or, (2.9)). More specifically, let us consider the following two vector fields, for which a function is an invariant:

| (2.11) |

Clearly, the vector fields , form a two-dimensional integrable distribution on : , where . The corresponding total differential equation is given by (see Chapter VII, Sato [65] for more details)

or,

| (2.12) |

Integrating (2.12), we arrive at a Cobb-Douglas function of the form (1.1), where the elasticity coefficients

satisfy the condition of constant return to scale (1.2).

Remark 2.1.

Note that, in principle, we could have used only one vector field generating a partial differential equation of the type (2.8). However, the resulting Cobb-Douglas function would have had the parameters satisfying the condition (see (1.1)). The latter constraint on the parameters and in (1.1) is incompatible with the economic growth theory main postulates. We suppose that exactly for this reason Sato [65] introduced the concept of simultaneous holotheticity. This arrangement, in particular, allows us to generate two-input Cobb-Douglas functions of the type (1.1) depending on a wide range of parameters and , which we can, for instance, make to satify the condition , so that the function (1.1) displays constant returns to scale as in the example above.

These considerations lead to a very important conclusion, namely the Cobb-Douglas function, derived within the framework of the growth model , where the Lie group is determined by the exponential growth (2.2), is precisely a manifestation of this exponential growth, or, more succinctly, we have

which means that the Cobb-Douglas function (1.1) is a consequence of exponential growth representing technical change.

3 From exponential to logistic growth models

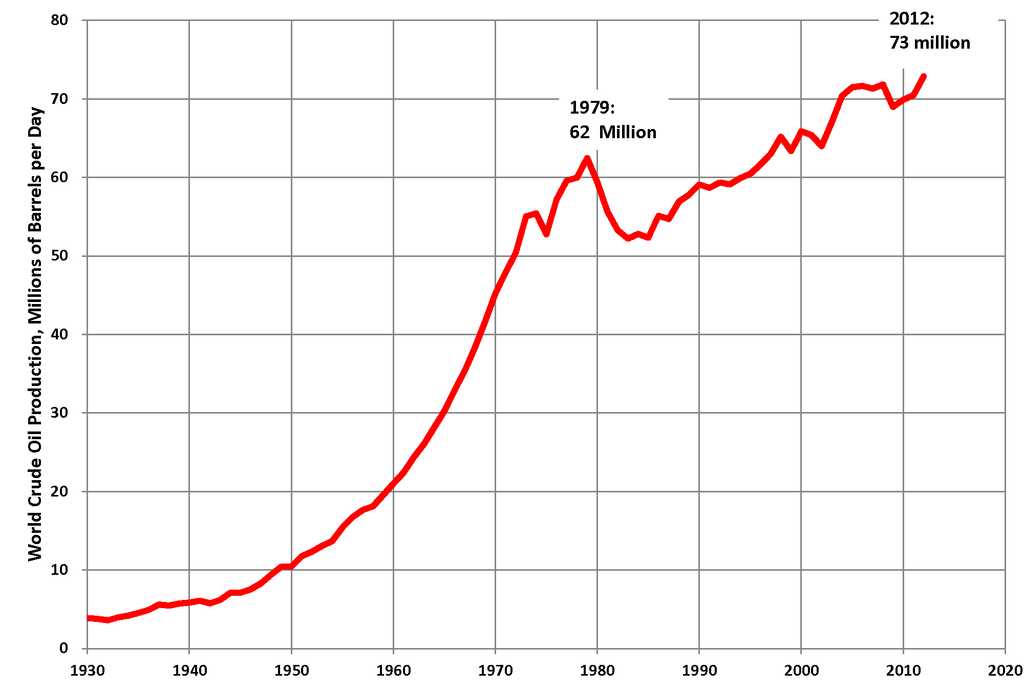

In this section we depart from the assumption that the input factors (i.e., capital and labor) grow exponentially in order to extend Sato’s growth model . In what follows we assume that labor and capital grow logistically. There is already a substantial literature, starting with the pioneering paper by Verhulst [76], in which the authors have already based their considerations on this rather natural assumption, while studying various growth models with the aid of methods and techniques developed in economics, mathematics and statistics (see, for example, Brass [11], Ferrara and Guerrini [26, 27, 28, 29, 30, 31], Leach [52], Oliver [54], Tinter [75]). The same assumption can be made about the growth in capital, if, for example, we look at such natural resources as oil and gold as proxies for energy and money respectively, it is quite evident that globally, given the fact that all resources are limited, both the accumulation of gold reserves and oil production are subject to logistic rather than exponential growth, as can be illustrated by Figure 1.

We note that from the mathematical viewpoint it is also evident that there cannot be unbounded, continuous exponential growth, whether in terms of production, capital, or population, on a planet with limited resources as per the following well-known theorem [60]:

Theorem 3.1 (Extreme value theorem).

If is a compact set and is a continuous function, then is bounded and there exist such that and .

In view of the above, we propose the following growth model based on the assumption that both capital and labor are affected by logistic growth, namely

| (3.1) |

where and , are the respective carrying capacities. Clearly, is a one-parameter Lie group, acting in , whose flow is generated by the vector field

| (3.2) |

Remark 3.2.

It is also natural to consider the growth models and determined by the assumption that only one of the two variables grow logistically, while the other is affected by exponential growth, that is

| (3.3) |

or,

| (3.4) |

Following the approach developed by Sato in [65], we can now determine the corresponding family of production functions by solving the partial differential equation determined by the vector field (3.2):

| (3.5) |

where is an arbitrary function of . Employing the method of characteristics, we arrive at the following family of functions:

| (3.6) |

where is an arbitrary function. We note that for and the family of functions given by (3.6) , where is given by (2.7). Therefore we arrive at the following

Proposition 3.3.

Remark 3.4.

Our next goal is to derive a new production function under the assumption of logistic growth in both capital and labor . Since the Cobb-Douglas function (1.1) has been shown above to be a member of the family of production functions (2.7) determined within the neoclassical growth model , where the Lie group is given by (2.2), it is natural to seek a new production function compatible with the logistic growth determined by the action of the Lie group (3.1) within the growth model . This is the subject of the considerations that follow.

4 From logistic growth to a new production function

In Section 2 we saw how the Cobb-Douglas production function could be derived as an element of the family of production functions (2.7) within the framework of the growth model , where the Lie group was defined by (2.2). Now let us consider the new growth model , where the Lie group was given by (3.1). Before we formally derive the corresponding production function as an element of the family of production functions (3.6), following the procedure outlined above, let us first give a reasonable justification for the calculations that we shall present below.

Recall that a necoclassical growth model of the Solow type may be defined as follows (see, for example, Jones and Scrimgeour [42], a model with decay in produced capital was studied in Cheviakov and Hartwick [17]):

| (4.1) | |||||

where and represent consumption and investment (savings) respectively, while denotes depreciation of capital. It is also assumed that the production function satisfies the Inada conditions [41]:

-

1.

, this condition accounts for growth in both and ,

-

2.

, that implies diminishing marginal returns also in both and ,

-

3.

has constant returns to scale, that is for all ,

-

4.

satisfies the following properties:

For example, the Cobb-Douglas function (1.1) satisfies the above assumptions, provided the condition (1.2) holds. Such a model and its generalizations ensure steady long-run growth, ignoring short-run fluctuations. Since the pioneering paper by Solow [70] was published in 1956 the model (4) and its many generalizations have played the most prominent role in the development of the endogenous growth theory. Clearly, the production function is the cornerstone of the model and if it satisfies the Inada conditions the growth is driven by decreasing marginal returns from the very beginning for all . Many important examples of endogenous growth support this assumption (see, for example, Cobb and Douglas [19]). Nevertheless, there are situations when growth cannot be described by a strictly concave production function. For instance, at a microeconomic level a company may develop a product based on an original idea, such a product initially can be sold unrestricted in the absence of competition, generating increasing marginal returns. After a while, a competition may become a factor (e.g., other companies may introduce similar products) affecting the sales of the original product, whose market share may shrink. In turn, this situation in a long-run will manifest itself in decreasing marginal returns. Mathematically, the corresponding production function will no longer be strictly concave. Capasso et al [15] gave a different motivation for the introduction of a (globally) nonconcave production function based on the idea of “poverty traps”. The authors also pointed out two examples of models based on nonconcave production functions: Skiba [69] (economics) and Clark [18] (mathematical biology). A macroeconomic example of such a scenario of growth can be found in Tainter [74] (see Figure 16, p. 109).

To address the issue Capasso et al [15] (see also Engbers et al [25], La Torre et al [51], Anita et al [4, 5, 6]) employed a purely heuristic approch to introduce a new general family of production functions of the form

| (4.2) |

reducible to the Cobb-Douglas function (1.1) and enjoying an “-shaped” (concave-convex) behavior for . Clearly, the functions of the class (4.2) have a horizontal asymptote as when and are compatible with logistic growth. These functions were used by the authors as a cornerstone for building a new, highly non-trivial generalization of the Solow model with spacial component in which they did not make assumptions about logistic growth for . It is worth mentioning at this point that Ferrara and Guerrini [26, 27, 28, 29, 30, 31], while generalizing the Ramsey and Solow models of economic growth, assumed logistic growth in , but kept the Cobb-Douglas function (1.1) intact.

The introduction of the family of production functions (4.2) is certainly a big step in the right direction, nevertheless these functions cannot account for all possible examples of growth (and decay). For example, a production function can exhibit growth, followed by a period of stabilization and then decay (see, for example, [JBC1973]). Another option is growth, followed by a period of stabilization, which is followed by growth again. In this view our next goal is to derive a more general production function that can be used to describe a wider range of economic growth models, including the situations outlined above. We shall employ the Lie group theoretical method developed by Sato [65] and briefly described in Section 2.

Indeed, consider the growth model given by (3.1). Next, we are going to identify a member of the family (3.6) compatible with logistic growth given by (3.1) by imposing the corresponding constraints on the RHS of the equation (3.5). By analogy with the case of the Cobb-Douglas function derived by Sato [65] within the framework of the growth model , where the action of the Lie group is determined by (2.2), let us consider the following partial differential equation determined by the vector field given by (3.2):

| (4.3) |

or, in other words, let us specify the function in (3.5) to be that implies logistic growth in the production function as well. Compare (4.3) with the equation (2.8).

Remark 4.1.

We note that the choice for the RHS of (4.3) is not arbitrary. It turns out that in order to obtain a meaningful solution one needs to assure that the properties of the function in (3.2) are compatible with the logistic growth determined by (3.1). For example, if we set in (3.2), which would imply that the growth in both and is logistic, while grows exponentially, the resulting production function would have singularities (see the equation (8.1)). Therefore the above equation reflects the fact that the growth determined by (4.3) is consistent for all quantities involved, that is for , and .

Next, we employ the same reasoning that Sato in [65] based his derivation of the Cobb-Douglas function (1.1) upon (see also Section 2). Let us assume that the production functions in two sectors of an economy (or, two countries) are identical, so that the aggregate production function sought is of the same form. However, it does not necessarily mean that the technical changes in both sectors are also the same. That is in what follows we shall give conditions under which the aggregate production function in question is holothetic under two types of technical changes simultaneously and solve (again) the corresponding simultaneous holotheticity problem. In mathematical terms, let us consider the following two vector fields acting on a function :

Clearly, the vector fields and form an integrable distribution on , because , where . Then the corresponding total differential equation which has for a solution assumes the following form:

or,

| (4.4) |

Integrating the differential equation (4.4) (compare it with (2.12)), we arrive at a solution of the form defined in the open domain

and satisfying the condition . Solving for by the impilcit function theorem, we arrive at the following hypersurface in :

| (4.5) |

where is the constant of integration, , . Note . Note that in view of the symmetry of the differential equation (4.4), we could have solved the equation for and as well. The function given by (4.5) whose range is coinsides with the function on .

Furthermore, we note that in the subset of the domain of the function its growth is governed by the logistic growth in the factors and . Note that in this region the growth of the production function is “-shaped”, which agrees with the assumptions that led to the introduction of the production function (4.2). However, the production function (4.5) is also defined outside of the region , which impies in turn that its shape in the subset is determined by the growth in and that goes beyond the respective carrying capacities and . We will elaborate on this matter without loss of generality while dealing with the corresponding one-input analog of the new two-input production function (4.5) below.

We conclude, therefore, that by analogy with the algorithm based on the Lie group theory methods devised by Sato and applied in [65] to generate the Cobb-Douglas function (1.1), we have used it, after some modifications, to generate a new production function (4.5). More succinctly, we have

Remark 4.2.

Remark 4.3.

See Remark 2.1.

Remark 4.4.

Remark 4.5.

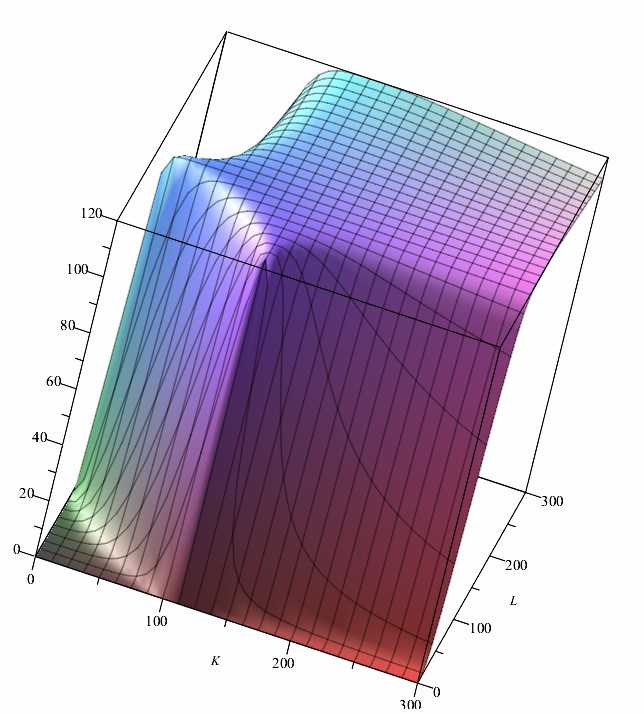

Figure 2 presents the surface of a two-input production function of the type (4.5) for , , , , without singularities (see Remark 4.6).

Remark 4.6.

Employing the same procedure, we can determine now in a fairly straightforward manner the corresponding one-input analogue of the new two-input production function (4.5). Thus, let us derive a new production function whose growth is governed the growth in which we assume to be logistic. Hence, we can formulate the following problem within the framework of the growth model :

| (4.10) |

| (4.11) |

where the vector field represents the infinitesimal action defined by the Lie group (4.10). Separating the variables and integrating the differential equation (4.11) yields the follwoing solution (production function):

| (4.12) |

where is the constant of integration and with the corresponding steady state given by

| (4.13) |

Note that in this case as well the new production function (4.12) exhibits first an “-shaped” growth in the region , followed by a decline for . Let us investigate this case from the economics point of view in more detail.

Let us recover the corresponding group action that affects the input , so that this action could be viewed as growth which entails the condition . Indeed, consider the infinitesimal action given by so that Solving the last equation, we obtain the following solutions:

| (4.14) |

and

| (4.15) |

In view of the fact that , , it follows from (4.14) and (4.15) that

| (4.16) |

and

| (4.17) |

so that both and represent growth. Solving the above equations, we obtain

| (4.18) |

where and are constants of integration. Next, we determine the time interval corresponding to growth in . It follows (4.18) that for and for . Substituting the equation (4.18) into (4.12), we arrive at the following function:

| (4.19) |

where is the time at which the function shifts from the logistic to a different growth type. Let us assume to be a positive integer. Furthermore, we note that increases or decreases depending on whether is odd or even respectively. To assure that (4.19) is compatible with (4.12) we assume that is an even integer (see below). Next, rewrite the production function given by (4.19) as follows:

| (4.20) |

where is the Heaviside (unit) step function,

In this view the function (4.20) may interpreted as an impulse response function. Indeed, a sudden change in the input at causes a jump in the output from to . From the economics viewpoint we can identify this phenomenon as a “shock” [68], which means that a sudden change in exogenous factors yields the corresponding sudden change in production (see [48, 57, 39] for more details and referenses). The gap between and caused by a sudden change in at is given by

| (4.21) |

where denotes the distance between the two curves at . Next, we note that

| (4.22) |

Note that if is an even number, the RHS of (4.22) is precisely the steady state (4.13).

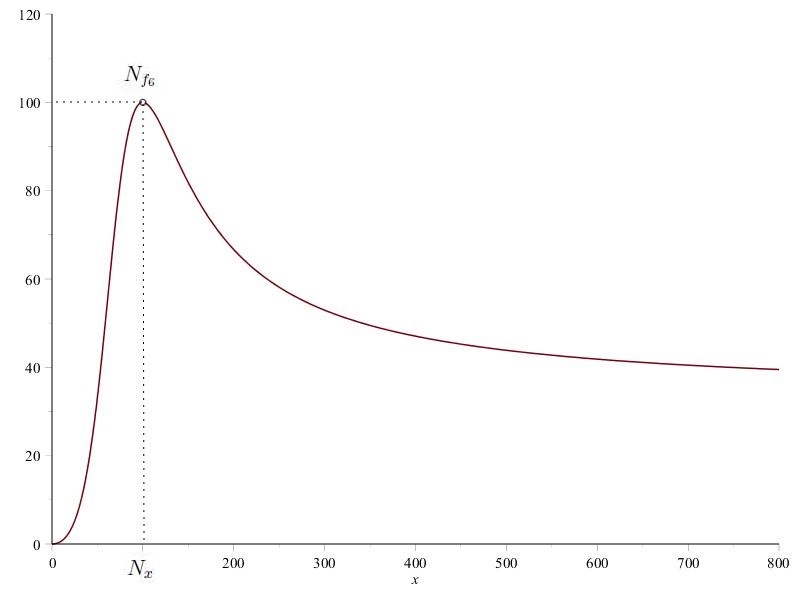

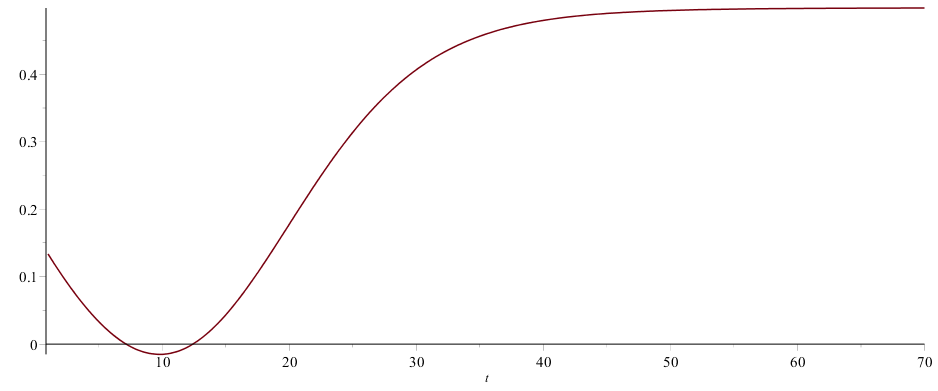

Figure 3 presents the graph of a one-input production function of the type (4.12) generated for , and . Note the function given by (4.12) defines an invariant of the infinitesimal action determined by vector field (3.2) for (or, ) and (or, ), namely , where

5 The problem of maximization of profit under conditions of perfect competition

In 1947 Paul Duglas gave his presidential address to the American Economics Association in which he referred to a coherent assembly of the statistical evidence accumulated in the course of the previous 20 years while he and other people were studying various economic data that confirmed the validity of the Cobb-Douglas production function. It is safe to assume that this event marked the beginning of its universal acceptance by the mainstream economic science. He wrote in [23]: “… the Cobb-Douglas function was being widely used, and that a host of younger scholars led by my former student, Paul Samuelson, his colleague Solow and Marc Nerlove, the son of my friend and former colleague, Samuel Nerlove, were all pushing forward into new and more sophisticated fields.” In fact, Marc Nerlove gave a series of lectures at the Econometric Workshop held at the University of Minnesota in 1957, which were subsequently published a few years later in a book [53]. One of the problem considered by the author was the problem of maximization of profit of a firm under conditions of perfect competition in both factors and product markets under the assumption that the revenue of the firm from sales was determined by the Cobb-Douglas production function. In what follows we shall solve the problem using the same arguments mutatis mutandis as in [53] by assuming that the revenue of the firm from sales is now determined by the new production function (4.5).

Consider an individual firm functioning under conditions of perfect competition in both factors and product markets. It attempts to maximize its profits by employing optimal quantities of inputs and producing an optimal quantity of output. At the same time its purchases of factors and supply of output do not affect the prices of the factors involved and the final product. Therefore the said prices are assumed to be given, while the profits are to be maximized. Let , , , be the profit, the price of the final product, the cost of using one unit of capital, and the wage of labor respectively. Hence, we have

| (5.1) |

Traditionally, in problems like this the output is assumed to be related to the inputs (capital) and (labor) by the Cobb-Douglas production function (1.1). Instead, suppose now is related to and via the new production function (4.5). Next, let us solve the problem of maximization of the profit given by (5.1) subject to the constraint implied by (4.5). The corresponding Lagrangian function is readily found to be

| (5.2) |

where is a Lagrange multiplier. For profit to be a maximum, the total differential

| (5.3) |

where

| (5.4) |

The condition (5.3) yields

| (5.5) |

The equations (5.5) give us necessary conditions for maximum profit. Solving (5.5) with the aid of the computer algebra system Maple, we get

| (5.6) |

The resulting equations (5.6) are sufficient to determine the variables , and . The corresponding sufficient conditions for maximum profit are provided by the necessary conditions established above supplemented by the following second-order condition:

or, given the fact that in (5.2) is linear in , and (see (5.1)) and by (5.5), we have

| (5.7) |

where

Solving (5.7), using Maple, we arrive at the following set of inequalities:

| (5.8) |

The first two inequalities entail that . The second two inequalities imply that and . Hence, we arrive at the following conditions that assure maximum profit:

| (5.9) |

Next, we observe that since and , the last inequality in (5.9) implies that

| (5.10) |

which in turn implies that the assumption of perfect competition and maximization of profit are inconsistent in the case when

Finally, we conclude that the equations and inequalities (5.6), (5.9) and (5.10) constitute sufficient conditions for maximum profit of a firm in the environment of perfect competition. The equations (5.6) determine the output a firm will deliver and the inputs of factors it will employ once the prices of the product and factors are established. Therefore the conclusions are pretty much the same as in the case when the revenue is determined by the Cobb-Douglas production function (1.1) considered in Nerlove [53]. The case of imperfect competition in both factor and production markets will be considered in a forthcoming paper.

Note that all of the calculations above have been carried out under the assumption that . If the condition (5.10) changes to .

6 The wage share and logistic growth

The labor share is the fraction of national income, or the income of a particular economic sector, defined as the share which is payed out to employees. Therefore it is often also called the wage share. As is well-known, the wage share in the economic growth models governed by the Cobb-Douglas production function (1.1) is a constant. More specifically, its constant value can be derived directly from the Cobb-Douglas function and expressed in terms of the output elasticity of capital in a simple and elegant way when the Cobb-Douglas function, say, enjoys constant return to scale (see, for example, Rabbani [58]). The invariance of the wage share is subject to Bowley’s law [9, 10] or the law of the constant wage share, which states that the share of national income that is paid out to the employees as compensation for their work (normally, in the form of wages), remains unchanged (invariant) over time [45, 50, 67]. Economic data collected in different countries till about 1980 gave rise to and most strongly supported this law, which was widely accepted by the economics community at the time. However, this is no longer the case on both counts (see, for example, Schneider [67] for more details and references).

In view of the mathematics presented above, it should not be viewed as a surprise. Indeed, the ivariance of wage share is linked to the Cobb-Douglas production function, which in turn is a consequence of exponential growth, as shown by Sato [65]. Next, since one of the the main points of this research project is the idea that we must depart from the exponential growth model and accept the logistic one, let us ivestigate how this transition affects the wage share.

In what follows we shall propose a new formula for the wage share compatible with logistic growth and support our claim by a rigorous mathematical analysis.

First, let us recover the formula for the wage share as an invariant of a prolonged infinitesimal group action given in terms of the corresponding projective coordinates defined as the output-capital ration and the labor-capital output . The terminology and notations that we will use are compatible with those adopted by Olver [55, 56] and Saunders [66]. Consider a general production function

| (6.1) |

under the assumption that the dependent and independent variables , and grow exponentially:

| (6.2) |

In view of the material presented in Section 2 we know that the production function (6.1) is bound to be of the Cobb-Douglas type (1.1), in terms of the projective coordinates it assumes the following form:

| (6.3) |

Clearly, the one-parameter Lie group of transformations (6.2) induces the corresponding action on the projective coordinates, which is also exponential:

| (6.4) |

with the corresponding infinitesimal action given by the vector field (compare it with (2.4)) given by

| (6.5) |

Following Saunders [66], let us suppose that is a trivial bundle so that and are adapted coordinates. Then the corresponding jet bundles are and as per the commutative diagram (6.7), where the first-jet manifold of is given by

| (6.6) |

with adapted coordinates

| (6.7) |

Here

Next, the first prolongation of on is the following vector field , which has to be a symmetry of the Cartan distribution on (see Saunders [66] for more details), that is the vector field

| (6.8) |

is required to be a symmetry of the Cartan distribution on . Indeed, consider a basic contact form Next, in view of the above, we require that the one-form is a contact form, where denotes the Lie derivative. Thus, we compute

| (6.9) |

The last line of (6.9) implies that the expression in the parentheses above vanishes, which entails that . Therefore the first prolongation of is found to be

| (6.10) |

The vector field (6.10) represents an infinitesimal action of a one-parameter Lie group of transformations in a three-dimensional (prolonged) space. Hence, we expect to obtain fundamental differential invariants. Indeed, solving the corresponding partial differential equation by the method of characteristics, we arrive at the following set of two fundamenal differential invariants:

| (6.11) |

as expected, which means that any other differential invariant of the prolonged infinitesimal group action defined by (6.10) if a function of and . Now, combining the fundamental differential invariants (6.11) in such a way that the parameters and disappear, we arrive at the following differential invariant:

| (6.12) |

which we immediately recognize to be precisely the wage share (see, for example, Rabbani [58] and Schneider [67] for more details).

Therefore we conclude that not only the Cobb-Douglas production function (1.1), but also the wage share given by (6.12) is a consequence of the exponential growth in and as a differential invariant obtained within the framework of the growth model , where the action of the Lie group is given by (2.2), that is

Now let us redo the above calculations for the growth model , where the action of is given by (3.1) and thus give a solution to the seemingly unresolved problem of the determination of why Bowley’s law [9, 10] does not hold true anymore in post-1960s data [8, 24, 37, 44].

First, we observe in the example considered above the exponential growth in and induced the corresponding exponential growth in the projective coordinates and . However, the logistic growth in and given by (3.1) does not translate into the same type of transformations for the projective coordinates and . Therefore, let us assume that the growth in is suppressed by, say, excessive debt and so it does not affect logistic growth in and . Hence, both projective coordinates and grow logistically, that is we have

| (6.13) |

where we assumed without loss of generality that both carrying capacities were equal to one. The corresponding infinitesimal action of the Lie group is given by the vector field

| (6.14) |

To determine its first prolongation we proceed as above within the same framework as in the previous case (see the commutative diagram (6.7)). We note first that the vector field on is projectable, since the bundle is endowed with a vector structure (see Saunders [66], Chapter 2 for more details). Next, define

| (6.15) |

and require that the vector field (6.15) is a symmetry of the Cartan distribution, which will assure that (6.15) is the first prolongation of (6.14). Indeed, consider again a basic contact form . Then again, is a contact form iff is a symmetry of the Cartan distribution on , which in turn assures that (6.15) is indeed the first prolongation of (6.14), where as before denotes the Lie derivative. Thus, we compute

| (6.16) |

In view of the above, is again a contact form, provided the expression in the parenthesis that appears in the last line of (6.16) vanishes. Hence, we have

or,

| (6.17) |

We conclude therefore that the first prolongation of the vector field given by (6.14) is the following fector field:

| (6.18) |

whose infinitesimal action brings about the following two fundamental differential invariants:

| (6.19) |

In order to eliminate the parameters and let us consider the following combination:

| (6.20) |

Definition 6.1.

Remark 6.2.

The modified wage share given by (6.21) is a differential invariant of the growth model , where the action of the Lie group is given by (3.1), while the classical wage share given by (6.12) is not. That is a reason why has been in decline: it may be attributed to the fact that post-1960 economic data has been generated within the framework of the growth model , rather than . More specifically, it follows that the decline in is due to the relation (see (6.21)). Indeed, if the output-to-capital ratio grows logistically faster than the labor-to-capital ratio under the condition of supressed capital (e.g., by excessive debt), that is if the ratio in (6.21) clearly contributes to decline in , since is a constant. Simply put, more wealth (real or perceived) distributed among fewer people implies a marked decrease in the classical wage share and so Bowley’s law [9, 10] no longer holds in the economic environment of the logistic growth model .

Remark 6.3.

The corresponding production function compatible with the infinitesimal action generated by the vector field (6.14) is readily found to be

| (6.22) |

which we derived by integrating the equation , where is given by (6.20) and rewriting the solution in terms of and .

Now, let us analyse the second new production function (6.22). The partial derivatives of the production function (6.22), called in economic literature marginal productivities, are found to be

| (6.23) |

| (6.24) |

Next, the slope of an isoquant is the marginal rate of technical substitution (MRTS), or technical rate of substitution (TRS). Thus, so that in our case

| (6.25) |

which decreases when grows and declines. We conclude, therefore, that (6.25) has concave up isoquants when increases and decreases, that is if the labour-capital ratio is less than approximately , in which case increases, while otherwise the isoquants are concave down, since decreases.

Recall that the new productoin function (4.5) does not enjoy constant return to scale. Now let us examine the function (6.22) from this viewpoint. Indeed, for a factor the substitution in (6.22) yields

| (6.26) |

which means that the new production function (6.22) has constant returns to scale, since it is a homogeneous function of degree one. Therefore we conclude that it satisfies the law of diminishing marginal returns and has constant return to scale, which means it has a great potential for playing a pivotal role in various economic growth models.

Finally, let us investigate the behavior of the new production function (6.22) as and under the assumption that both and grow logistically according to the one-parameter Lie group transformations defined by (3.1). To understand its behaviour when and are small, we employ economic reasoning. Thus, at the beginning of a production cycle a company, say, invests much of its resources into fixed assets (e.g., infrastructure, materials, land, etc) and so when is small it is safe to assume that , which implies that

| (6.27) |

that is the production function enjoys a similar behaviour to that of the Cobb-Douglas production function (1.1) that has constant returns to scale. When both and grow logistically and so we have by (6.22)

7 The new production function vis-à-vis economic data

In this section we present a similar analysis to the one conducted by Cobb and Doublas [19], namely we l compare the new production function with some available US economic data from 1947-2016. We make use of the data from the period 1947-2016 that is provided by the Federal Reserve Bank of St. Louis (https://fred.stlouisfed.org), employing the FRED tool. The variables are as follows: — capital services of nonfarm business sector [79], — compensations of employees of nonfarm business sector [80], — real output of nonfarm business sector [81]. The values of all variables are dimensionless, they are index values with the values at 2009 taken as 100. To estimate the new production function (4.5), we have used R Programming [43], employing the method of least squares, and assuming the corresponding carrying capacities to be of the following values: , . We have also assumed that .

The elasticity of substitution (see Sato [62]) of the new production function (4.5) in this case assumes the following form:

| (7.2) |

where , , while and are constants. The vairable , giving the best estimate when and , ranges approximately from to .

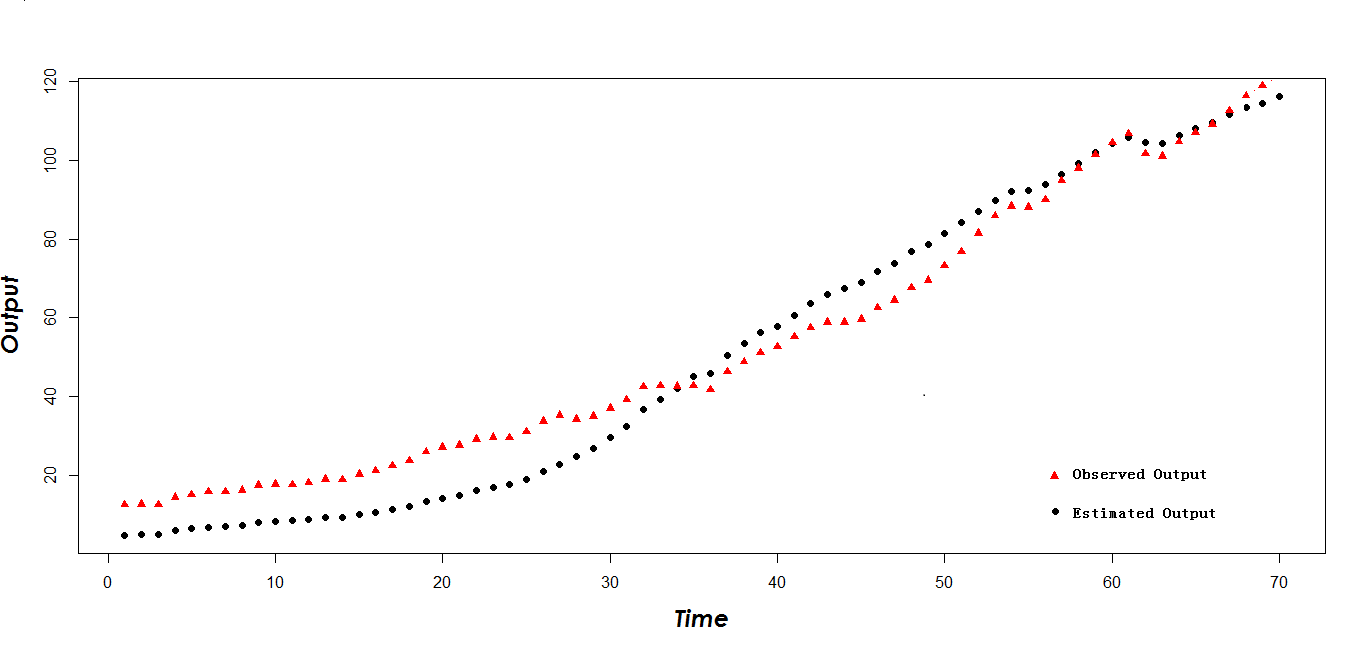

Whether the function , derived using the Lie group theoretical methods, can accurately predict the future still remains to be seen, but it looks like the function can “predict” the past. More specifically, while running our simulations, we have noticed that the negative value of occurs in the year of 1958 - excatly the year of a sharp economic downturn [32], see Figure 5.

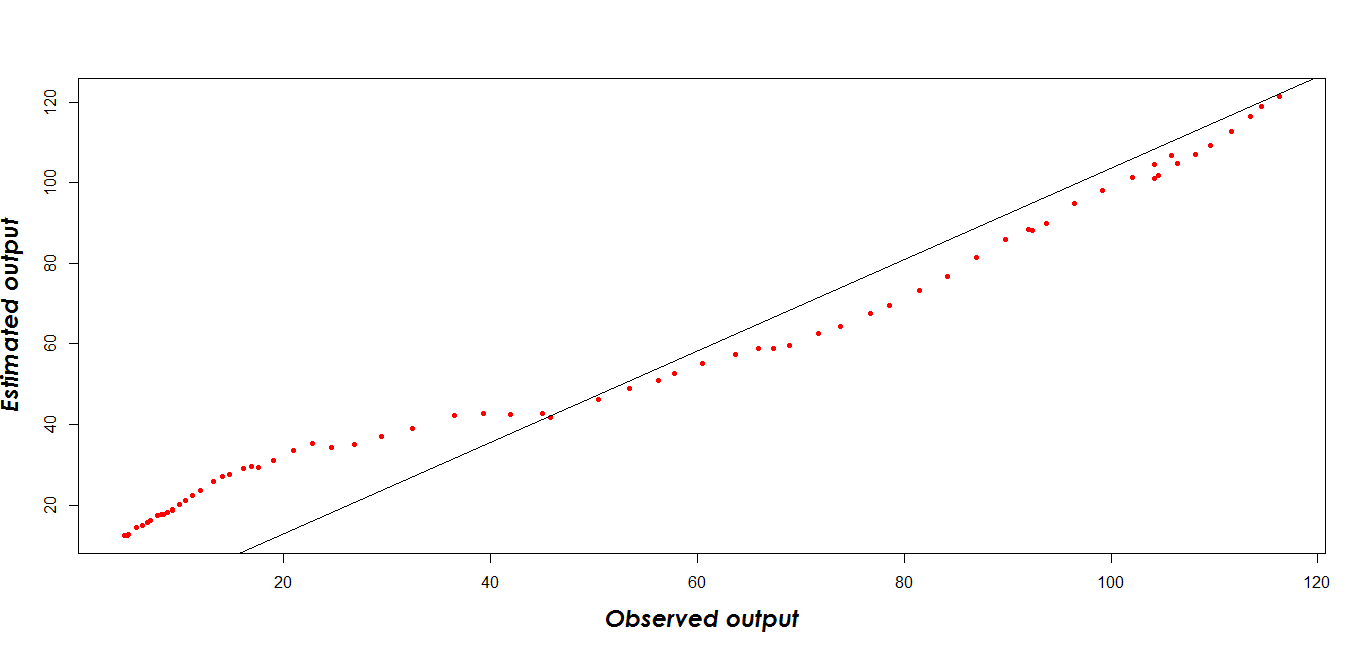

We conclude from the above that the time series from the period 1947-2016 that compares the observed and estimated outputs (see Figure 6) reveals that our model fits quite well the data with the the adjusted R-squared value of 97.65. On the other hand, the Cobb-Douglas function (1.1) with a constant elasticity of substitutions, i.e., , does not provide satisfactory results in terms of the values of parameters and . The best estimation of the Cobb-Douglas function that we managed to have obtained, using the same method, is as follows:

| (7.3) |

where and . We see that this (negative!) value of the parameter is not compatible with the definition of the Cobb-Douglas production function given by the formula (1.1).

8 Summary and discussion

In this paper we have introduced a new (logistic) growth model given by (3.1) as an extension and natural continuation of the preceeding studies in the area of economic growth done by Ryuzo Sato [62, 63, 64, 65], as well as a new framework for the development of more general production functions that we believe fit better current economic data. The resulting new production functions (4.5) and (6.22) are consequences of the logistic growth in factors (capital and labor). The former function has shown to provide an adequate estimate for economic data, as for the latter — there are indications that it will perform even better, the work in this direction is underway. Furthermore, we have presented a purely mathematical justification of why Bowley’s law [9, 10] no longer holds true in post-1960 economic data by introducing a new notion of modified wage share (6.21).

Our research has also demonstrated that there can not be exponential growth of production while factors grow logistically. We are inclined to believe that this is the most important consequence of our studies. Indeed, if one “forces” the production function to grow exponentially (i.e., by setting in (4.3)), while the factors and grow logistically as in (3.1), the resulting production function will be of the form

| (8.1) |

where we assumed without loss of generality that . The production function (8.1) blows up very quickly near the singularities at and . Similarly unsatisfactory result can by obtained by enforcing logistic growth in the production function, while the factors and grow exponentially, that is by setting in (2.8): the resulting production function will not even grow.

When we were starting this project, our original goal was to only extend the theoretical framework based on the Lie group theory developed by Sato, we did not excpect that the resulting production functions would perfom so well. Therefore the results obtained in this paper have exceeded our expectations.

We see many applicatoins in both economic theory of growth and applied mathematics where the new production functions (4.5) and (6.22), as well as the new modified wage share (6.21) can be used essentially mutatis mutandis by simply replacing the Cobb-Douglas function or its generalizations (like the CES function, for example) and wage share with them as appropriate.

As we have already mentioned in Introduction, the idea that exponential growth ought to be replaced with the logistic one is slowly but surely becoming more and more accepted by the scientists developing various growth models (see Capasso et al [15], Engbers et al [25], Brass [11], Ferrara and Guerrini [26, 27, 28, 29, 30, 31], Leach [52], Oliver [54], Tinter [75]) fore more details and references).

In light of the results that we have obtained so far, some of the projects that we have learned from and appreciated so much, we belive could be modified accordingly, which in turn may lead to more accurate mathematical models. For example, in Ferrara and Guerrini [30] the authors generalized the Ramsey model by introducing the logistic growth in , which was a very adequate assumption. However, they still used the Cobb-Douglas function which, we believe, is not entirely accurate, because the logistic growth in suggests that the growth model given by (3.4) is underpinning the dynamics of the variables involved and so one has to use the corresponding production function compatible with (3.4) that is the function (3.8) instead of the Cobb-Douglas production funciton (1.1). Similarly, Capasso et al [15] did introduce a modified production function (4.2) instead of the usual Cobb-Douglas production function (1.1), however it was done heuristically and a more natural choice for a production function in the model developed by the authors is either the production function (4.5) or (6.22), both of which were derived here in a systematic way. More specifically, the partial differential equation

governing the dynamics of should use either (4.5) or (6.22) in place of , which we believe will lead to more accurate results.

Acknowledgement

The authors wish to thank Ryuzo Sato for valuable comments, constructive critique and suggestions. The second author (KW) wishes to thank Chaoyue Liu for his invaluable help with R Programming and statistical analysis he used while working on the material presented in Section 7.

References

- [1] E. Accinelli and J. G. Brida, Re-formulation of the Ramsey model of optimal growth with the Richards population growth law, WSEAS Transactions on Mathematics, 5, 2006, pp. 473–478.

- [2] E. Accinelli and J. G. Brida, The Ramsey model with logistic population growth, Economics Bulletin, 3, 2007, pp. 1–8.

- [3] I. Agricola and T. Friedrich, Global Analysis: Differential Forms in Analysis, Geometry and Physics, AMS Graduate Studies in Mathematics, Vol. 52, 2002.

- [4] S. Anita, V. Capasso, H. Kunze, D. La Torre, Optimal control and long-run dynamics for spatial economic growth model with physical capital accumulation and pollution diffusion, Appl. Math. Letters, 26, 2013, pp. 908–912.

- [5] S. Anita, V. Capasso, H. Kunze, D. La Torre, Dynamics and optimal control in a spatially structured economic growth model with pollution diffusion and environmental taxation, Appl. Math. Letters, 42, 2015, pp. 36–40.

- [6] S. Anita, V. Capasso, H. Kunze, D. La Torre, Optimizing environmental taxation on physical capital for a spacially structured economic growth model including pollution diffusion, Vietnam J. Math., 45, 2017, pp. 199–206.

- [7] P. Antràs, Is the US aggregate production function Cobb-Douglas? New estimates of the elastisity of substitution, Contributions to Macroeconomics, 4(1), 2004, pp. 1–34.

- [8] S. Bentolila and G. Saint-Paul, Explaining movements in the labor share, Contributions to Macroeconomics, 3(1), 2003, pp. 1–31.

- [9] A. L. Bowley, Wages in the United Kingdom in the Nineteenth Century: Notes for the Use of Students of Social and Economic Questions, Cambridge, UK: Cambridge University Press, 1900.

- [10] A. L. Bowley, Wages and Income in the United Kingdom Since 1860, Cambridge: Cambridge University Press, 1937.

- [11] W. Brass, Perspectives in population prediction: illustrated by the statistics of England and Wales, J. R. Statist. Soc. A, 137, 1974, pp. 532-570.

- [12] J. G. Brida and G. Cayssials, Population dynamics and the Mankiw-Romer-Weil model, Int. J. Math. Model. Num. Opt., 7 (3-4), 2016, pp. 363–375.

- [13] J. G. Brida, G. Cayssials, and J. S. Pereyra, The discrete-time Ramsey model with a decreasing population growth rate: stability and speed of convergence, J. Dyn. Systems and Diff.l Equations, 6(3), 2016, pp. 219–233.

- [14] D. Cai, An economic growth model with endogenous carrying capacity and demographic transition, Math. and Comp. Model., 55 (3-4), 2012, pp. 432–441.

- [15] V. Capasso, R. Engbers, and D. La Torre, Population dynamics in a spatial Solow model with a convex-concave production function, in C. Perna, M. Sibillo (Editors), Mathematical and Statistical Methods for Actuarial Sciences and Finance. Springer, Milano, 2012, pp. 61–68.

- [16] D. Cass, Optimum growth in an aggregative model of capital accumulation, Review of Economic Studies, 32 (3), 1965, pp. 233–240.

- [17] A. F. Cheviakov and J. Hartwick, Constant per capita consumption paths with exhaustible resources and decaying produced capital, Ecological Economics, 68, 2009, pp. 2969–2973.

- [18] C. W. Clark, Economically optimal policies for the utilization of biologically renewable resources, Math. Biosci., 12, 1971, pp. 245–260.

- [19] C. W. Cobb and P. H. Douglas, A theory of production, American Economic Review, 18 (Supplement), 1928, pp. 139–165.

- [20] C. M. Cochran, R. G. McLenaghan and R. G. Smirnov, Equivalence problem for the orthogonal separable webs in 3-dimensional hyperbolic space, J. Math. Phys. 58, 2017, 063513.

- [21] A. Cohen, An Introduction to the Lie Theory of One-Parameter Groups, DC Health Company, 1911.

- [22] E. D. Domar, Capital expansion, rate of growth, and employment, Econometrica, 14, 1946, pp. 137–147.

- [23] P. H. Douglas, The Cobb-Douglas production function once again: Its history, its testing, and some new empirical values, J. Polit. Economy, 84(5), 1976, pp. 903–916.

- [24] M. W. L. Elsby, B. Hobijn and A. Sahin, The decline of the U.S. labor share, Brookings Papers on Economic Activity, 47(2), 2013, pp. 1–63.

- [25] R. Engbers, M. Burger and V. Capasso, Inverse problems in geographical economics: parameter identification in the spacial Solow model, Phil Trans. R. Soc. A, 372, 2014, 20130402.

- [26] M. Ferrara and L. Guerrini, Economic development and sustainability in a two-sector model with variable population growth rate, Journal of Mathematical Sciences: Advances and Applications, 1, 2008, pp. 232–339.

- [27] M. Ferrara and L. Guerrini, Economic development and sustainability in a Solow model with natural capital and logistic population change, International Journal of Pure and Applied Mathematics, 48, 2008, pp. 435–450.

- [28] M. Ferrara and L. Guerrini, The neoclassical model of Solow and Swan with logistic population growth, Proceedings of the 2nd International Conference of IMBIC on “Mathematical Sciences for Advancement of Science and Technology (MSAST), Kolkata, India, 2008, pp. 119–127.

- [29] M. Ferrara and L. Guerrini, The Green Solow model with logistic population change, Proceedings of the 10th WSEAS International Conference on Mathematics and Computers in Business and Economics, Prague, Czech Republic, March 23–25, 2009, pp. 17–20.

- [30] M. Ferrara and L. Guerrini, The Ramsey model with logistic population growth and Benthamite felicity function, Proceedings of the 10th WSEAS International Conference on Mathematics and Computers in Business and Economics, Prague, Czech Republic, March 23–25, 2009, pp. 231–234.

- [31] M. Ferrara and L. Guerrini, The Ramsey model with logistic population growth and Benthamite felicity function revisited, WSEAS Transactions on Mathematics, 8(3), 2009, pp. 97–106.

- [32] R. W. Gable, The politics and economics of the 1957-1958 recession,Western Political Quarterly, 12(2), 1959, pp.557–559.

- [33] C. García-Peãlosa and S. J. Turnovsky, The dynamics of wealth inequality in a simple Ramsey model: A note on the role of production flexibility, Macroeconomic Dynamics 13, 2009, pp. 250–262.

- [34] L. Guerrini, A closed-form solution to the Ramsey model with the von Bertalanffy population law, Appl. Math. Sciences, 4 (65), 2010, pp. 3239–3244.

- [35] L. Guerrini, The Ramsey model with a bounded population growth rate, J. Macroeconomics, 32, 2010, pp. 872–878.

- [36] L. Guerrini, A closed-form solution to the Ramsey model with logistic population growth, Econ. Modelling, 27, 2010, pp. 1178–1182.

- [37] A. Guscina, Effects of globalization on labor’s share in national income, IMF Working Paper No. 06/294, 2007.

- [38] R. F. Harrod, An essey in dynamics theory, Economic Journal, 49, 1939, pp. 14–33.

- [39] A. Hatemi-J, Asymmetric generalized impulse responses with an application in finance, Econ. Modelling, 36, 2014, pp. 18–22.

- [40] J. T. Horwood, R. G. McLenaghan, and R. G. Smirnov, Invariant classification of orthogonally separable Hamiltonian systems in Euclidean Space, Comm. Math. Phys., 259(3), 2005, pp. 679–709.

- [41] K. Inada, On a two-sector model of economic growth: comments and a generalization, The Review of Economic Studies, 30 (2), 1963, pp. 119–127.

- [42] C. I. Jones and D. Scrimgeour, A new proof of Uzawa’s steady-state growth theorem, Rev. Econ. Stat., 90(1), 2008, pp. 180–182.

- [43] R. I. Kabacoff, R in Action, Manning, 2010.

- [44] L. Karabournis and B. Neiman, The global decline of the labor share, Quarterly Journal of Economics, 129(1), 2014, pp. 61–103.

- [45] J. M. Keynes, Relative movements of real wages and output, The Economic J., 49(193), 1939, pp. 34–51.

- [46] D. R. Klein, The introduction, increase, and crash of reindeer on St. Matthew island, The Journal of Wildlife Management, 32(2), 1968, pp. 350–367.

- [47] F. Klein, Vergleichende Betrachtungen über Neuere Geometrische Forschungen, Verlag von Andreas Deichert, Erlangen, 1872.

- [48] G. Koop, M. H. Pesaran, and S. M. Potter, Impulse response analysis in nonlinear multivariate models, J. Econometrics, 74(1), 1996, pp. 119–147.

- [49] T. C. Koopmans, On the concept of optimal economic growth, The Economic Approach to Development Planning, Chicago: Rand McNally, 1965, pp. 22–287.

- [50] H. M. Krämer, Bowley’s Law: the diffusion of an empirical supposition into economic theory, Cahiers d’économie politique/Papers in Political Economy, 61, 2011, pp. 19–49.

- [51] D. La Torre, D. Liuzzi, and S. Marsiglio, Pollution diffusion and abatement activities across space and over time, Math. Social Sci. 78, 2015, pp. 48–63.

- [52] D. Leach, Re-evaluation of the logistic curve for human populations, J. R. Statist. Soc. A (General) 144, 1981, pp. 94–103.

- [53] M. Nerlove, Estimation and Identification of Cobb-Douglas Production Functions, Rand McNally: Chicago, 1965.

- [54] E. R. Oliver, Notes on the logistic curve for human populations, J. R. Statist. Soc. A (General), 145, 1982, pp. 359–363.

- [55] P. J. Olver, Applications of Lie Groups to Differential Equations, Springer, 2nd Edition, 1993.

- [56] P. J. Olver, Equivalence, Invariants, and Symmetry, Cambridge University Press, 1995.

- [57] H. H. Pesaran and Y. Shin, Generalized impulse response analysis in linear multivariate models, Econ. Lett. 58(1), 1998, pp. 17–29.

- [58] S. Rabbani, Derivation of constant labor and capital share from the Cobb-Douglas production function, http://srabbani.com.

- [59] F. P. Ramsey, A Mathematical theory of saving, Economic Journal, 38 (152), 1928, pp. 543–559.

- [60] W. Rudin, Principles of Mathematical Analysis, New York: McGraw Hill, 1976.

- [61] R. Sato and R. V. Ramachandran, Symmetry and Economic Invariance, 2nd Enhanced Edition, Springer, 2014.

- [62] R. Sato, The estimation of biased technical progress and the production function, International Economic Review, 11(2), 1970, pp.179–208.

- [63] R. Sato, Homothetic and non-homothetic CES production functions, American Econ. Rev., 67(4), 1977, pp. 559–569.

- [64] R. Sato, The impact of technical change on holotheticity of production functions, Review of Economic Studies, 47, 1980, pp. 767–776.

- [65] R. Sato, Theory of Technical Change and Economic Invariance, Academic Press, 1981.

- [66] D. J. Saunders, The Geometry of Jet Bundles, London Mathematical Society Lecture Notes Series, 142, Cambridge University Press, 1989.

- [67] D. Schneider, The labor share: A rewview of theory and evidence, SFB649 Economic Risk, Discussion Paper, 2011.

- [68] C. A. Sims, Macroeconomics and reality, Econometrica: J. Econ. Society, 48, 1980, pp. 1–48.

- [69] A. K. Skiba, Optimal growth with convex-concave production function, Econom. 46(3), 1978, pp. 527–539.

- [70] R. M. Solow, A contribution to the theory of economic growth, Quarterly Journal of Economics, 70, 1956, pp. 65–94.

- [71] R. M. Solow, Technological change and aggregate production function, Review of Economics and Statistics, 39(3), 1957, pp. 312–320.

- [72] G. Stigler, Economic problems in measuring changes in productivity, in Output, Input and Productivity, Princeton: Income and Wealth Series, 1961, pp. 47–63.

- [73] T. W. Swan, Economic growth and capital accumulation, Economic Record, 32, 1956, pp. 334–361.

- [74] J. A. Tainter, The Collapse of Complex Societies, New York Cambridge, UK: Cambridge University Press, 1988.

- [75] G. Tinter, Econometrics, New York: Wiley, 1952.

- [76] P. F. Verhurst, Recherches mathématiques sur la loi d’accroissement de la population, Nouveaux Mémoires de l’Académie Royale des Sciences et Belles Lettres de Bruxelles, 18, 1845, 1–38.

- [77] This article uses material from the Wikipedia article Gold reserve, which is released under the Creative Commons Attribution-Share-Alike License 3.0.

- [78] This article uses material from the Wikipedia article Petroleum industry, which is released under the Creative Commons Attribution-Share-Alike License 3.0.

- [79] This article uses material from U.S. Bureau of Labor Statistics, Nonfarm Business Sector: Non-Labor Payments [PRS85006083], retrieved from FRED, Federal Reserve Bank of St. Louis; https://fred.stlouisfed.org/series/PRS85006083, October 30, 2017.

- [80] This article uses material from U.S. Bureau of Labor Statistics, Nonfarm Business Sector: Compensation [PRS85006063], retrieved from FRED, Federal Reserve Bank of St. Louis; https://fred.stlouisfed.org/series/PRS85006063, October 31, 2017.

- [81] This article uses material from U.S. Bureau of Labor Statistics, Nonfarm Business Sector: Real Output [OUTNFB], retrieved from FRED, Federal Reserve Bank of St. Louis; https://fred.stlouisfed.org/series/OUTNFB, October 31, 2017.