Capacity Upper Bounds for Deletion-Type Channels††thanks: A preliminary version of this work appears in Proceedings of the 50th ACM Symposium on Theory of Computing (STOC 2018).

Abstract

We develop a systematic approach, based on convex programming and real analysis, for obtaining upper bounds on the capacity of the binary deletion channel and, more generally, channels with i.i.d. insertions and deletions. Other than the classical deletion channel, we give a special attention to the Poisson-repeat channel introduced by Mitzenmacher and Drinea (IEEE Transactions on Information Theory, 2006). Our framework can be applied to obtain capacity upper bounds for any repetition distribution (the deletion and Poisson-repeat channels corresponding to the special cases of Bernoulli and Poisson distributions). Our techniques essentially reduce the task of proving capacity upper bounds to maximizing a univariate, real-valued, and often concave function over a bounded interval. The corresponding univariate function is carefully designed according to the underlying distribution of repetitions and the choices vary depending on the desired strength of the upper bounds as well as the desired simplicity of the function (e.g., being only efficiently computable versus having an explicit closed-form expression in terms of elementary, or common special, functions). Among our results, we show the following:

-

1.

The capacity of the binary deletion channel with deletion probability is at most for , and, assuming the capacity function is convex, is at most for , where is the golden ratio. This is the first nontrivial capacity upper bound for any value of outside the limiting case that is fully explicit and proved without computer assistance.

-

2.

We derive the first set of capacity upper bounds for the Poisson-repeat channel. Our results uncover further striking connections between this channel and the deletion channel, and suggest, somewhat counter-intuitively, that the Poisson-repeat channel is actually analytically simpler than the deletion channel and may be of key importance to a complete understanding of the deletion channel.

-

3.

We derive several novel upper bounds on the capacity of the deletion channel. All upper bounds are maximums of efficiently computable, and concave, univariate real functions over a bounded domain. In turn, we upper bound these functions in terms of explicit elementary and standard special functions, whose maximums can be found even more efficiently (and sometimes, analytically, for example for ).

Along the way, we develop several new techniques of potentially independent interest.

For example, we develop systematic techniques to study channels with mean constraints

over the reals.

Furthermore, we motivate the study of novel probability distributions over non-negative

integers as well as novel special functions which could be of interest to mathematical analysis.

Keywords: Coding theory, Synchronization error-correcting codes, Channel coding.

1 Introduction

The binary deletion channel is generally regarded as the simplest model for communication in presence of synchronization errors. In this model, a transmitter encodes messages as a (potentially unbounded) stream of bits which is then sent to a receiver over a communications channel. The channel does not corrupt bits. However, each bit may be independently discarded by the channel with a deletion probability . The receiver receives the sequence of undiscarded bits, in their respective order, and has to reconstruct the sent message with vanishing failure probability. Despite the remarkable simplicity of this fundamental model of communication, the capacity of the deletion channel; i.e., the maximum achievable transmission rate, remains unknown. Apart from the obvious significance in information, coding, and communications theory, the problem has attracted significant attention from the theoretical computer science community (e.g., [ref:Mit09, ref:SZ99, ref:GNW12, ref:GW17, ref:BGZ16, ref:BGH17]). This is due to the problem’s rich combinatorial structure and its fundamental connection with the understanding of the distribution of long subsequences in bit-strings, which, in turn, is of significance to such theory problems as pattern matching, edit distance, longest common subsequence, communication complexity problems involving the edit distance, the document exchange problem (cf. [ref:BZ16]) or secure sketching in cryptography [ref:DORS08], to name a few. It is also closely related to the algorithmic trace reconstruction problem which, in turn, is of significance to real world applications ranging from sensor networks to computational biology [ref:Mit09].

1.1 Previous work

There is already a relatively vast literature on the deletion channel problem, and we are only able to touch upon some of the major results most relevant to this work. Qualitatively, it is known that i) the capacity curve for this channel is continuous, ii) the capacity is positive for all [ref:DG01, ref:DG06], iii) the capacity is (as in the binary symmetric channel) when [ref:KMS10, ref:KM13] and when (as in the binary erasure channel) [ref:DM07, ref:MD06, ref:Dal11]. Trivially, the capacity is at most the capacity of the binary erasure channel; i.e., . Nevertheless, the exact capacity of the channel remains elusive. A related problem is to identify the best achievable rate against adversarial, or oblivious, deletions; for which significant progress has been recently made [ref:BGH17, ref:GR18]. However, in this work we focus on the Shannon-type capacity over random deletions (and, more generally, repetitions). Much of the major known results on the subject as well as the significance to theoretical computer science are discussed in Mitzenmacher’s excellent survey [ref:Mit09].

On the achievability side, Diggavi and Grossglauser [ref:DG01, ref:DG06] were the first to show that the capacity of the deletion channel is nonzero for all . A more explicit capacity lower bound of (slightly better than) , for all , was proved by Drinea and Mitzenmacher [ref:DM07, ref:MD06], where in the latter work they also introduced and motivated the Poisson-repeat channel. This channel not only deletes bits but may also insert replicated bits in the stream. More precisely, the channel is defined by a parameter and, given a bit, replicates the bit by a number sampled from a Poisson distribution with mean (the bit is deleted if the number of repetitions is zero). In [ref:MD06], the authors establish a connection between the Poisson-repeat and the deletion channel. Namely, they show that any lower bound on the capacity of any Poisson-repeat channel translates into a capacity lower bound for any deletion channel. Using a first-order Markov chain for generating the input distribution, and numerical computations on the resulting capacity bound expressions for various choices of , they derive the claimed capacity lower bound of for the deletion channel.

For small deletion probability , several results show that the deletion capacity behaves similar to the symmetric channel. Combined with [ref:Gal61, ref:Zig69, ref:DG06], Kalai, Mitzenmacher, and Sudan [ref:KMS10] show that in this regime that capacity is , where is the binary entropy function. Independently of this work, and based on a parameter continuity argument, Kanoria and Montanari [ref:KM13] obtain a more refined asymptotic estimate in this regime that is correct up to the term111We remark that the constant behind the residual term is not specified or bounded in [ref:KM13]. Therefore, while this result sharply characterizes the limiting behavior of the capacity curve, it cannot be used to obtain concrete, numerical, bounds on the channel capacity for any nonzero value of . .

Diggavi, Mitzenmacher and Pfister [ref:MDP07] obtained capacity upper bounds for all , including the first nontrivial upper bound, of , for . To show the upper bounds, they consider a genie-aided decoder with access to side information about the deletion process, and then upper bound the capacity of the channel with side information (which is higher than the original capacity) using a combination of classical information theoretic tools and a computer-based distribution-optimization component. Different sets of numerical capacity upper bounds were obtained in [ref:FD10] (and for more general channels in [ref:FDE11]) based on several, carefully designed, genie-aided decoders. These constructions essentially reduce the problem to upper bounding the capacity of a finite variation of the deletion channel problem, whose capacity is in turn numerically computed using the Arimoto-Blahut algorithm (which runs in exponential time in the finite number of bits). Both [ref:MDP07] and [ref:FD10] thus cleverly identify a finite-domain capacity problem, that is solved numerically, and then upper bound the deletion capacity using the numerical results for the finite problem. Such techniques cannot be readily extended to such problems as the Poisson-repeat channel problem which are inherently infinite.

1.2 Our main contributions

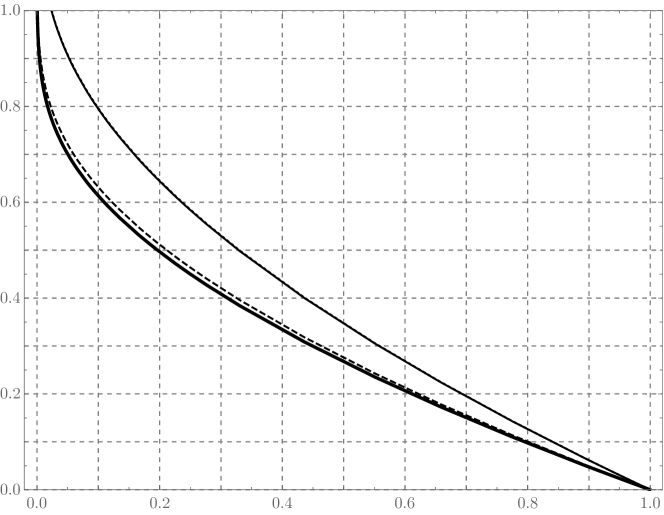

Roughly speaking, the techniques of [ref:MDP07] and [ref:FD10] pursue the following recipe: i) “enhance” the channel to one with a higher capacity by carefully considering a “genie-aided” decoder that receives auxiliary information from the channel; ii) Heuristically extract a finite optimization problem to upper bound the capacity of the enhanced (and thus the original) channel; iii) Numerically solve the finite optimization problem by a computer. While the above general method results in very strong capacity upper bounds, much of the mathematical structure of the problem is pushed into the computationally intensive numerical optimization problem in the third step. It is thus unclear to what extent can the methods be further developed towards a complete understanding of the channel capacity. In this work, rather than setting our goal to improving the best known numerical capacity upper bounds for the deletion channel, we focus on gaining deeper insights about the analytic structure of the problem (nevertheless, as a proof of concept, we are able to improve the best reported numerical upper bounds for small deletion probability; e.g., for ). We develop several tools that further the existing intuitions on the deletion channel problem and may potentially serve as key steps towards a full characterization of the capacity. As a result, we are able, for the first time, to develop a single and systematic method that results in a capacity upper bound curve for the deletion channel which is smooth, convex-shaped, non-trivial for all , and simultaneously exhibits the correct behavior of , for a constant , at and at (see Figure 16). The fact that our approach obtains the above features in a natural and organic way suggests that the true capacity of the deletion channel might have the same qualitative shape as what we obtain222In particular, we believe that this observation further supports a conjecture of Dalai [ref:Dal11] that the capacity curve is convex, towards which significant progress has already been made in [ref:RD15]. .

As discussed above, the best known reported capacity upper bounds for the deletion channel [ref:FD10, ref:MDP07, ref:RD15], are based on identifying a finite, but as large as possible, sub-problem (possibly by adding side information) and then searching for the optimum solution for the finite problem by a computer. In contrast, a key focus in our work is to avoid any computer-assisted components in the proofs as much as possible, so as to gain as much intuition about the mathematical structure of the problem as possible. Our results, including all the involved distributions in the proofs, are indeed fully analytical. Namely, we upper bound the capacity of the deletion channel as the maximum of a univariate real function, which is concave and smooth, over the interval (depicted in Figure 14). The function to be maximized is explicitly defined in terms of exponentially decaying sums, and is thus computable in polynomial time in the desired accuracy. If desired, computation of the involved sums can be avoided by using the sharp upper and lower bound estimates on the function that we provide in terms of both elementary and standard special functions (Figure 15). The only numerical computation would thus involve finding the maximum value of an explicitly defined concave function over . Even this can be avoided in some cases, leading us to the first fully explicit capacity upper bound for the deletion channel that is nontrivial for all deletion probabilities and proved without any numerical computation: The deletion capacity is at most for , and, under the plausible conjecture that the capacity function is convex [ref:Dal11], at most for , where is the golden ratio. We remark that this, itself, is better than the bounds reported in [ref:MDP07] for all , while our numerical bounds improve those of [ref:MDP07] for all .

In addition to the classical deletion channel, our methods are generally applicable to any channel with independent insertions and deletions defined by any given repetition rule. Namely, given an arbitrary (possibly infinite) distribution on non-negative integers, our methods can be applied to upper bound the capacity of a channel—what we call a -repeat channel, that replaces each input bit independently with a number of repetitions sampled from (where the outcome zero would cause deletion of the bit). For the deletion channel, would be a known Bernoulli distribution.

For such problems as the Poisson-repeat channel problem, introduced by Mitzenmacher and Drinea [ref:MD06], that are inherently infinite (even if only one bit is supplied at the input), the known methods [ref:FD10, ref:MDP07] cannot be readily used, since it is not clear how to identify a finite sub-problem that can be optimized by a computer-based search. In contrast, we show that our method easily applies to the Poisson-repeat channel (where is Poisson with a known mean ), and thus we obtain the first set of capacity upper bounds for this channel. Our methods demonstrate striking connections between the analytical structure of this channel and the deletion channel, and suggest that understanding the Poisson-repeat channel may be the key towards the ultimate characterization of the capacity of the deletion channel. Even though the Poisson-repeat channel may appear more complex than the deletion channel (since it not only deletes, but also inserts bits), our results suggest that the Poisson-repeat channel may be simpler to analyze. This is mainly due to the fact that an -fold convolution of with itself is a binomial distribution for the deletion channel, which is a more complex distribution than Poisson, and indeed, contains the latter as a limiting special case. In fact, we study the Poisson-repeat channel first, which then naturally guides us towards our results for the deletion channel. Our obtained bounds for both channels are plotted in Figures 9 and 16 and tabulated in Tables B.5 and B.5.

To obtain our results, we develop a number of techniques along the way that may be of independent interest. We motivate a systematic study of what we call general mean-limited channels, and their special case of convolution channels. These are channels, with input and output alphabets over the reals, defined by a known probability transition rule and a mean-constraint on their output distributions. Special cases include the mean-limited binomial and Poisson channels, that model how the deletion and Poisson-repeat channels shrink consecutive runs of bits. The notion and our techniques can be used to model physical channels studied outside the context of deletion-type channels as well, a notable example being the well-known Poisson channel that is of central importance to optical communications systems [ref:Sha90]. Indeed, a subsequent work by the author [ref:CR18] successfully applies the techniques developed in this work to obtain improved upper bounds on the capacity of the discrete-time Poisson channel. Furthermore, our contributions in probability theory include motivating novel distributions over non-negative integers and a first study of them, which may be of use in other contexts as well. This includes what we define as an “inverse binomial” distribution, as well as distributions obtained by multiplying the probability mass function of the Poisson distribution by or , where denotes harmonic numbers (see (43) and (52)). We introduce novel special functions to study such distributions (e.g., generalizations of the log-gamma function; see (112)) which may be of independent interest to mathematical analysis.

Organization

The rest of the article is organized as follows: Section 2 gives a high-level exposition of the entire work, explaining the developed techniques with a focus on intuitions and underlying insights rather than the technical details. In Section 3, we formally define the notion of general mean-limited channels, as well as the special case of convolution channels. We prove a duality-based necessary and sufficient condition for achieving the capacity of such channels, as well as the dual feasibility criteria that certify upper bounds on the capacity. Section 4 formally defines the general notion of -repeat channels, and proves a capacity upper bound for such channels based on the capacity of a mean-limited channel defined according to . We use the obtained tools in Section 5 to obtain our capacity upper bounds for the Poisson-repeat channel. Towards this end, we construct two dual-feasible solutions for the corresponding mean-limited channel and estimate their parameters in terms of elementary and standard special functions. In Section 6, guided by the result obtained for the Poisson-repeat channel, we prove our capacity upper bounds for the deletion channel. We first introduce the notion of inverse binomial distributions, and then show that it is dual feasible for the mean-limited binomial channel. We estimate the parameters of this distribution in terms of elementary and standard spacial functions. We then apply a truncation technique, that we first develop for Poisson-repeat channels, to refine the dual feasible solution and obtain improved capacity upper bounds.

Notation

Unless otherwise stated, all logarithms are taken to base , and the measure of information is converted from nats to bits only for the final numerical estimates. We denote the set of non-negative real numbers by and the set of non-negative integers by . As is standard in information theory, we generally use capital letters for random variables. When there is no risk of confusion, we may use the same symbol for a random variable and its underlying distribution. Support of a random variable , denoted by , is the set of the possible outcomes of . Calligraphic letters are used for several purposes; alphabets, distributions, and probability transition rules. The entropy of a random variable is denoted by , and denotes the binary entropy function:

The Kullback-Leibler (KL) divergence between the underlying distributions of random variables and , denoted by , is defined as

We use for the mutual information between jointly distributed random variables and , and for the conditional mutual information given a third variable . We use the asymptotic notation to mean . The binomial distribution with trials and success probability is denoted by , and the Bernoulli distribution with mean is denoted by . The capacity of a channel is denoted by . We may use the binomial coefficient over non-integers, in which case the definition should be used.

2 High-level exposition of the techniques and results

In this work, we formalize and study the notion of “general repeat channels”, which are binary input channels characterized by a given probability distribution over non-negative integers. A -repeat channel, given a bit, draws an independent sample from and outputs copies of the received bit. We define the deletion probability of the channel to be the probability that assigns to zero, and let be the retention probability. Thus, what we call the deletion channel corresponds to the case where is the Bernoulli distribution with mean . On the other hand, if is a Poisson distribution with mean , we get a Poisson-repeat channel with deletion probability . We note that, in general, need not be uniquely determined by its deletion parameter , albeit this is the case for the class of deletion and Poisson-repeat channels.

2.1 Reduction to mean-limited and convolution channels

Suppose the input to a -repeat channel is a bit-sequence with being the output bit-sequence. If , the expected output length would be . By Shannon’s theorem, it can be seen (as in [ref:Dob67]) that the capacity of the channel, that we denote below by , is the supremum of the normalized mutual information between and ; i.e., .

A common technique in analyzing the deletion channel is to consider how it acts on runs of bits, rather than the individual bits. Given a run of bits, the deletion channel outputs a run of bits; i.e., a sample from the binomial distribution with trials and success probability . For the Poisson-repeat channel, this would be a run of length given by a Poisson sample with mean . In general, the distribution of the output run-length would be the -fold convolution of with itself, that we denote by .

Since grows to infinity, without loss of generality, we can assume that the first input bit is zero. This allows us to unambiguously think of as its run-length encoding , where each is a positive integer. Similarly, we may also think of by its run-length encoding , where each is a positive integer. This will identify up to a negation of all bits. Since the channel has memory, the random variables (unconditionally) are not necessarily independent. However, this would be the case if the are independent and identically distributed, in which case the also become identically distributed. Note that, given , the bit-length of and the parameter are random variables determined by the channel, and indeed the randomness of causes technical difficulties that should be rigorously handled by a careful analysis. However, in the informal exposition below we pretend that is known and fixed a priori. One may now attempt to use the chain rule and write

A major difficulty in deriving the capacity of the deletion channel is the fact that, unlike channels with no synchronization errors, a certain does not only depend on the corresponding , but rather, potentially any part of . Given , we know that has a binomial distribution with mean depending on the summation , for some random variables and that are in general difficult to analyze. Furthermore, even given a fixed , the random variables do not become conditionally independent. Therefore, the above result of the chain rule cannot be upper bounded by a simpler, single-letter, expression. A natural idea, that has been pursued previously (e.g., [ref:MDP07, ref:FD10]), is to consider “genie-aided” decoders that receive enhanced side information by the channel. The side information is carefully designed so as to reduce the problem to an i.i.d. channel problem that can be analyzed more conveniently. However, this approach generally comes at the expense of effectively turning the channel into one with strictly higher capacity, and consequently, obtaining inherently sub-optimal capacity upper bounds.

The result of Diggavi, Mitzenmacher, and Pfister [ref:MDP07].

An elegant execution of the above idea, that in fact inspires the starting point of our work, has been done in [ref:MDP07] which we briefly explain here. This result is based on the simple idea that, if we imagine that the channel places a “comma” after each run of bits, such that the commas are never deleted by the channel, this can only increase the capacity333For the limiting case , the authors establish a different channel enhancement argument using carefully placed markers, that we do not discuss here. . Furthermore, the enhanced channel is equivalent to an i.i.d. channel that receives a stream of positive integers (i.e., the run-length encoding of ) and passes each integer independently over a “run-length” channel. The effect of the run-length channel, given an input , is to output a sample from ; i.e., the binomial distribution with trials and success probability . Now, the capacity of the deletion channel can be upper bounded by the capacity of the run-length channel, normalized by the number of input channel uses (i.e., the length of ). Since the run-length channel is i.i.d., its capacity is equivalent to the single-letter capacity. Thus, letting and denote the input and output of a single use of the run-length channel, capacity of the deletion channel is upper bounded by , where the supremum is over the distribution of over positive integers444It is important to note that is defined over non-zero integers. Without this consideration, the capacity upper bound would be infinite. This can be easily seen by considering a distribution that puts of the probability mass on the zero outcome, for some , and has mean . A straightforward calculation shows that, in this case, , and that the capacity upper bound becomes , which can be made arbitrarily large by choosing a sufficiently small . . At this point, a fundamental result of Abdel-Ghaffar [ref:AG93] on per-unit-cost capacity can be used to, in turn, upper bound the resulting expression.

In the per-unit-cost capacity problem, a cost function is defined over the input domain of a channel with transition rule and the capacity is defined as , where the supremum is over the distribution of . For the above application, the input domain is the positive integers and the cost function is identity: . As proved in [ref:AG93], a necessary and sufficient condition for a pair to be capacity achieving is the following: Letting

where is the output distribution corresponding to a fixed input and is the Kullback-Leibler (KL) divergence, the supremum is attained for all on the support of . In this case, is the per-unit-cost capacity. Furthermore, for any distribution on the output domain (whether or not it corresponds to an input distribution), the capacity is upper bounded by as defined above.

There are two drawbacks with the above approach taken by [ref:MDP07]. First, the side information in fact genuinely increases the channel’s capacity, and therefore, the upper bounds resulting from this method are inherently sub-optimal. One way to see this is to consider the case where is small. Consider the run-length channel and a choice of that assigns a of the probability mass to , and the rest to . In this case, one can see that , and thus, the per-unit-cost capacity is also at least . This is while, by the trivial erasure channel upper bound, the deletion capacity must be at most . Indeed, the numerical upper bounds reported by [ref:MDP07] exhibit this phenomenon at close to one (notice the distinctive concavity in this area in Figure 16). The second drawback is that, while the result of Abdel-Ghaffar is in principle powerful enough to characterize the true per-unit-cost capacity upper bound, it may be extremely difficult to work with this result analytically. A way around this issue, undertaken in [ref:MDP07], is to employ a computer-based search. In order to do so, first a finite-domain distribution (supported up to an integer ) for that maximizes the capacity is constructed by a computer-based search, and the corresponding KL divergence supremum, up to , is numerically computed. Then, the resulting is truncated and the tail is geometrically redistributed over the remaining (infinite) input domain. The KL divergence at large values of can be accurately approximated by a linear function of , at which point [ref:AG93] can be applied with the modified choice of , allowing the resulting capacity upper bound to be numerically computed. While this approach indeed achieves very strong numerical capacity upper bounds (especially for small to moderate values of ), much of the analytic structure of the problem is absorbed by the computer-based search, making further progress elusive. In this work, we develop a systematic, albeit technically demanding, approach to overcome the barriers encountered by [ref:MDP07].

Equivalent reformulation of the channel.

Consider any -repeat channel with deletion probability . Rather than introducing side information, which, as demonstrated above, may result in a channel with strictly larger capacity, we use a careful analysis to decompose the action of the channel into two steps, forming a Markov chain , such that the resulting from the two-step process has the exact distribution as the run-length encoding of the output of . Then, we upper bound the capacity by divided by the number of channel uses in . Assume, without loss of generality, that the first input bit in is zero and this bit is promised not to be deleted by the channel (in particular, the first bit ever output by the channel is also zero). Given the input , the channel considers the run-length encoding of . In order to produce the first run in the output, the channel starts deleting bits from the even runs until the first non-deletion event occurs, say at run . The odd runs are then combined as , and the process continues from the first survived bit in the even runs until the input is fully scanned. The resulting sequence is then passed component-wise through a channel , with integer input and output, defined according to , to produce the output sequence (for the case of the deletion channel, each is formed simply by passing through a binomial channel555A binomial channel, given a non-negative integer input , outputs a sample from the binomial distribution with trials and success probability ., much similar to [ref:MDP07]). We show that the resulting sequence has precisely the same distribution as the run-length encoding of the output of . By a delicate analysis of this process, which is depicted in Figure 1, we are able to show that the capacity of is upper bounded as

| (1) |

where and are the input and output distributions of . This constitutes the first technical building block in our capacity upper bound proofs. The bound (1) has a similar flavor in form, but is strictly stronger, than the upper bound expression in [ref:MDP07] (especially for larger ).

Mean-limited and convolution channels.

Once (1) is available, one may attempt to apply Abdel-Ghaffar’s result [ref:AG93] to obtain a capacity upper bound, by using the cost function . Indeed, any upper bound may in principle be obtained by this result as it provides necessary and sufficient conditions for characterizing the quantity on the right hand side of (1). However, as demonstrated by [ref:MDP07], an analytic approach for obtaining a distribution that minimizes the divergence fraction , or even gets sharply close to the minimum, may be extremely challenging. Instead, [ref:MDP07] uses a computer-assisted optimization subroutine to construct a satisfactory and numerically upper bound the capacity. While this exact numerical optimization subroutine applied on (1) will strictly improve the numerical capacity upper bounds reported in [ref:MDP07] (since the cost function resulting from (1) is strictly larger than the cost function that is used in [ref:MDP07]), our aim is to obtain an analytic improvement that avoids extensive numerical computations and provides deeper insights into the structure of the problem. To overcome this difficulty, we observe that it would be much more natural to break down the task of finding the best distribution for into two steps. First, we restrict the mean of to a fixed parameter and optimize only over those such that . This fixes the denominator of the divergence fraction to a constant and allows us to focus on optimizing the non-fractional quantity with respect to the fixed mean constraint. Then, we take the supremum of the resulting bounds over the choice of to upper bound (1). Note that the optimal for the two-step optimization must satisfy the (necessary and sufficient) conditions of [ref:AG93] as well, so the two methods for characterizing the capacity-achieving pair are technically equivalent. However, factoring out the mean allows for a much more natural and systematic derivation of the right distribution for , and is what allows us to achieve the desired analytic breakthroughs.

We thus obtain the abstraction of what we call a “mean-limited channel”. Such a channel is defined with respect to certain input and output domains over non-negative reals, and a transition rule for producing an output distribution over the output domain given an input distribution over the input domain. Furthermore, the channel is given a mean parameter and only accepts those input distributions for which the corresponding output distributions have mean . The capacity of the channel is determined in the standard sense of maximal mutual information between admissible input and output distributions.

The abstraction is of general and independent interest to the study of communications channels in presence of mean “power constraints”, such as the classical Poisson channel. However, for our applications, it suffices to consider discrete domains (in particular, non-negative integers) and the special case of transition rules that are defined by convolutions of distributions, resulting in a special case that we call a “convolution” channel. A convolution channel is defined with respect to a distribution over non-negative reals, and is denoted by , where is the output mean constraint. Given an input , the channel produces a sample from (i.e., the distribution defined by the th power of the characteristic function of ) in the output. One may extend the notion of mean-limited channels to allow for uses, and for a total mean constraint . Namely, the channel now accepts an -dimensional sequence at input and passes each through an independent, identical, mean-limited channel to generate the output sequence . The mean-constraint in this case would enforce the condition . It is straightforward to show that the capacity of this channel is achieved by a product distribution.

2.2 Upper bounding the capacity of general mean-limited channels

The appeal in reducing the capacity upper bound problems for -repeat channels to that of general mean-limited channels is that, for the latter, one may naturally use powerful tools from convex optimization to obtain strong capacity upper bounds in a systematic and completely analytic fashion. To this end, we prove an analogue of Abdel-Ghaffar’s result [ref:AG93] for general mean-limited channels. However, we use a different, direct, proof. Namely, in Section 3.1 we directly write the mutual information maximization problem as a convex program, form its dual and observe that strong duality holds. Hence, we may write down the Karush-Kuhn-Tucker (KKT) conditions that provide the necessary and sufficient conditions for optimality.

Characterization of channel capacity in terms of the optimum of a convex program and the use of duality is a standard technique in information theory (cf. [ref:CK11]). Variations of this technique has been used, for example, towards understanding the capacity of multiple-antenna systems [ref:LM03] and the discrete time Poisson channel [ref:Mar07, ref:LM09]. In this section, we derive a variation tailored to our applications for upper bounding the capacity of mean-limited channels666The variation developed in this section can be generally applied to any mean-limited discrete or continuous channel. In a subsequent work by the author [ref:CR18], the technique has been successfully applied to obtain simple and improved upper bounds on the capacity of the discrete-time Poisson channel. .

Consider a general mean-limited channel with transition rule , input domain , and mean-constraint . With a slight overload of the notation, in this section consider an input distribution for and let denote the corresponding output distribution. For any fixed input , denote by the output random variable when the input is fixed to . The KKT conditions imply that is capacity achieving if and only if, for some real parameters and , we have

| (2) |

with equality for all . In this case, the capacity is equal to . Furthermore, if there is a distribution over the output alphabet for which (2) holds (and we call the distribution “dual feasible”), then . These results are summarized in Theorem 1.

Perhaps the most technically demanding aspect of this work is to obtain fully analytical dual feasible solutions that provably provide sharp, and explicit, or at least efficiently computable, upper bound estimates on the capacity of the mean-limited Poisson and binomial channels. These, in turn, lead to capacity upper bounds for the Poisson-repeat and deletion channels. In both cases, we carefully construct dual feasible distributions parameterized by a parameter that controls the mean to any arbitrary positive value. Once the feasibility of these distributions are proved, we explicitly write down the corresponding real parameters , as well as the resulting capacity upper bound (which requires writing as a function of ), and plug in the resulting upper bound in (1). This, in turn, results in an upper bound expression for the capacity of the original -repeat problem (e.g., either the Poisson-repeat or deletion channel) as the maximum of a uni-variate real function in (which turns out to be concave in ). In all cases, this function is efficiently computable. In turn, we upper bound this function in terms of either explicit elementary functions, or more sharply, in terms of the standard special functions. Thus, in particular, we are able to reduce the problem of upper bounding the capacity of a Poisson-repeat or deletion channel to finding the maximum of an elementary, concave, function of . Numerical computation is then only applied, if necessary, at the very last stage for computing the maximizing value of for this function, and the corresponding capacity upper bound.

The Poisson-repeat channel.

In order to obtain a capacity upper bound for the Poisson-repeat channel, we use (1) combined with a capacity upper bound for the corresponding mean-limited Poisson channel using the KKT conditions described above. Suppose that the Poisson-repeat channel replaces each bit with a number of bits sampled from a Poisson distribution with mean . Therefore, the deletion probability of this channel (i.e., probability that a bit is replaced by zero copies) is . The corresponding mean-limited Poisson channel with mean constraint takes a non-negative integer at input and outputs a fresh sample from the Poisson distribution with mean . We use a convexity argument to show that the following distribution over the non-negative integers, parameterized by , satisfies (2) with and :

| (3) |

where is the normalizing constant, and . The values of and would in turn be functions of , and can numerically be computed in polynomial time in the desired accuracy, given the exponential decay of (3) (see Table B.5). This results in a capacity upper bound of for the mean-limited channel (Theorem 10). Furthermore, combined with (1), we get the first set of capacity upper bounds for the Poisson-repeat channel with deletion probability (Theorem 17):

| (4) |

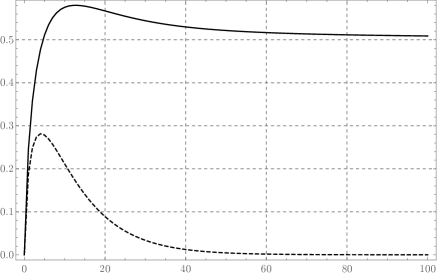

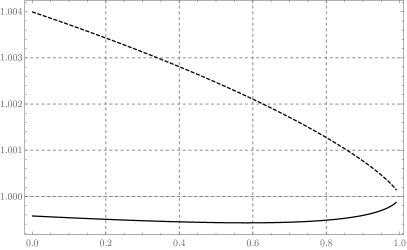

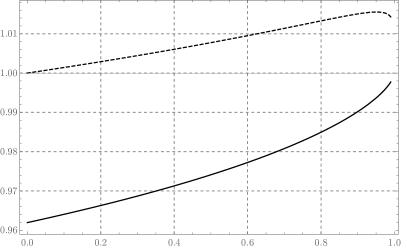

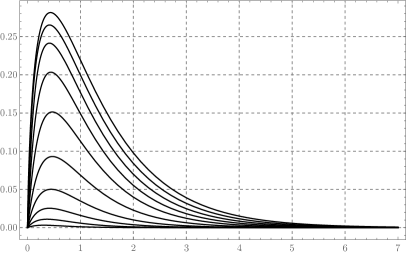

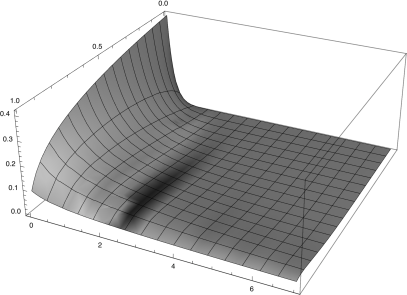

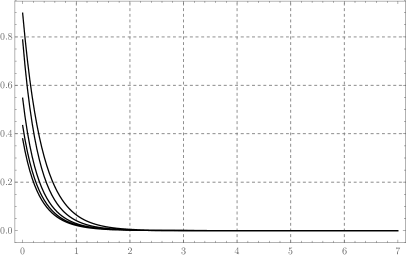

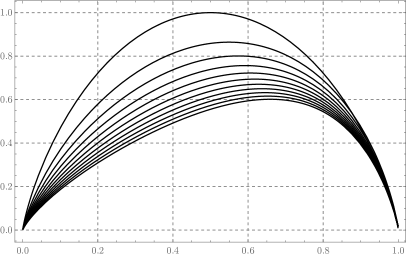

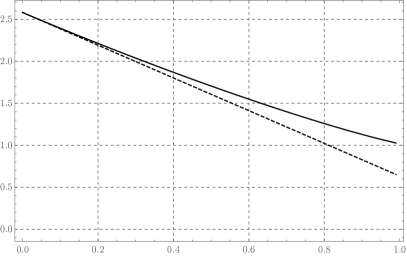

The function inside the supremum turns out to be concave, and the maximum can efficiently be found by a simple search (Figure 8). However, it is desirable to have sharp upper bound estimates on the function (in ) to be maximized. Note that, from Stirling’s approximation, the asymptotic behavior of (3) is . Therefore, intuitively, it should be possible to estimate and in terms of the summations and , which may be expressed by the polylogarithm function (148), a well studied special function (however, obtaining upper and lower bounds requires more work). This allows us to provide a remarkably sharp upper estimate on the function in (4) in terms of the standard special functions. This is made precise in Theorem 13 and the quality of the approximation is depicted in Figure 6.

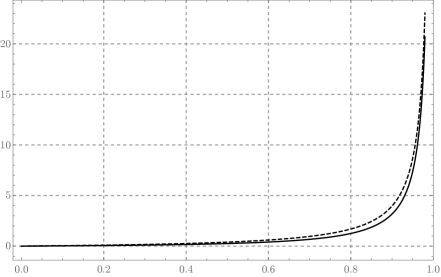

We observe that the gap in (2) achieved by (3) is zero at but converges to an absolute constant (namely, ) as . This results in sub-optimal capacity upper bounds. We rectify this issue by replacing the term in (3) with , where is the digamma function (essentially we are replacing the in the exponent with harmonic numbers, which have the same asymptotic behavior); namely, we now use what we call the digamma distribution

| (5) |

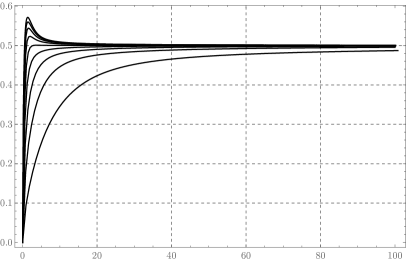

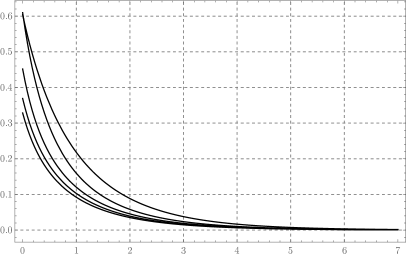

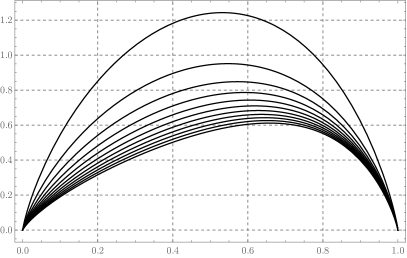

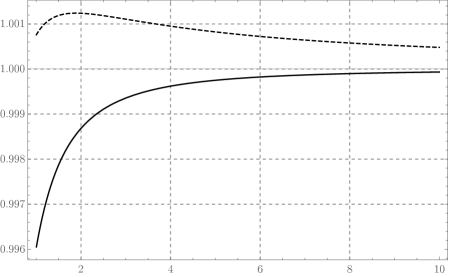

with . Using the Newton series expansion of harmonic numbers as well as the factorial moments of the Poisson distribution, we show that this alternative choice is also dual feasible, and in fact, the gap in (2) offered by this choice is precisely , where is the exponential integral function (49). Thus the gap is zero at and exponentially vanishes as grows (Figure 2). This leads to a significant improvement in the resulting capacity upper bounds (Figure 9). We note that the digamma distribution (5) still exhibits the same asymptotic behavior as (3), and thus its parameters can be similarly approximated. However, we show that the same asymptotic behavior is exhibited by the well-studied negative binomial distribution (65) of order . Since the parameters of a negative binomial distribution take remarkably simple forms, we are able to obtain excellent upper and lower bound estimates on the parameters and of the digamma distribution (5), and in turn the function inside the supremum in (4), in terms of elementary functions. This is made precise in Section 5.3.2 (Corollary 16). As a result, we obtain several upper bound estimates on the capacity of the Poisson-repeat channel (either using (3) or the digamma distribution (5) or their upper bound estimates), which are depicted in Figure 9 and listed in Table B.5.

The deletion channel.

At a first glance, it is natural to get the impression that understanding the capacity of a Poisson-repeat channel may be a more complex problem than that of a deletion channel. After all, a deletion channel only deletes bits whereas a Poisson-repeat channel may cause insertions (repetitions) in addition to deletions. However, our work indicates that, counter-intuitively, the deletion channel is analytically more complex than the Poisson-repeat channel. In fact, we use the above results for the Poisson-repeat channel as a guiding tool towards attacking the deletion channel problem (which is why the Poisson-repeat channel is discussed first). The mean-limited channel corresponding to a deletion channel is a binomial channel, which maps an input to the binomial distribution over trials. On the other hand, the Poisson-repeat channel corresponds to a mean-limited Poisson channel, which maps to a Poisson random variable with mean . A Poisson distribution, being a one-parameter distribution, is analytically simpler than a two-parameter binomial distribution. Indeed, the Poisson distribution is a limiting special case of the binomial distribution. We use this intuition to extend our results for the Poisson-repeat channel to the deletion channel. As in the Poisson case, we invoke (1) to reduce the capacity upper bound problem for the deletion channel to that of the mean-limited binomial channel with output mean constraint . Then, the task of finding a dual feasible distribution naturally leads us to a novel distribution that we call an “inverse binomial” distribution (discussed in Section 6.1), which is defined, for , by

| (6) |

where is the binary entropy function. The parameter uniquely determines the normalizing constant and the mean (and the mean can be adjusted to any desired positive value). We use a convexity argument to show (in Theorem 26) that the above distribution indeed satisfies (2) with and , thus resulting in a capacity upper bound of for the mean-limited binomial channel and a capacity upper bound of

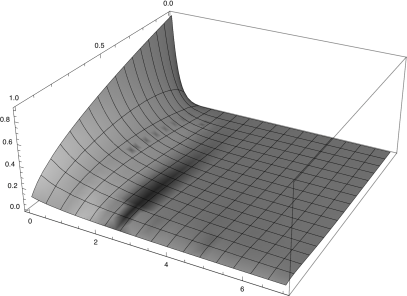

| (7) |

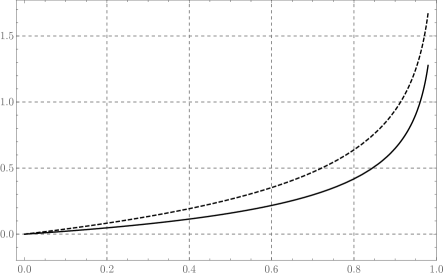

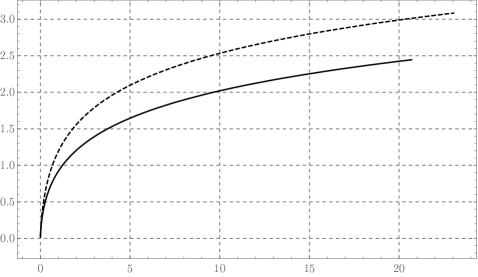

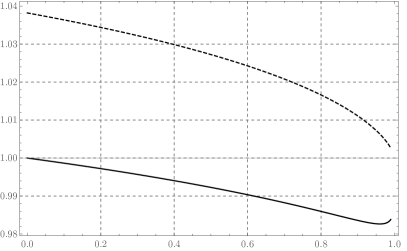

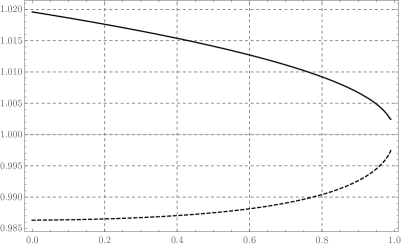

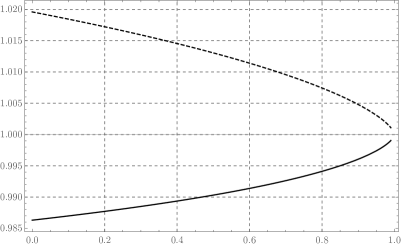

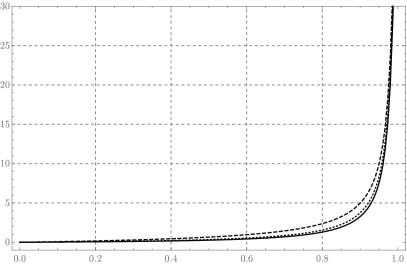

for the deletion channel. As in the Poisson case, it is desirable to obtain sharp upper bound estimates on the term inside the supremum in (7), which turns out to be a concave function of , in terms of elementary or common special functions. This is a technical task, and in Section 6.1.2 (in particular, Theorem 24), we obtain sandwiching bounds for the parameters of an inverse binomial distribution in terms of the Lerch transcendent (62), a well studied generalization of the Riemann zeta function. Furthermore, we observe that an inverse binomial distribution exhibits the same asymptotic growth as a negative binomial distribution of order . Using this, we are able to obtain upper and lower bound estimates on the parameters of an inverse binomial distribution in terms of elementary functions (Corollary 22 in Section 6.1.1). The estimates are excellent if the deletion probability is not too small (Figure 10).

Interestingly, we show that for , the inverse binomial distribution is exactly a negative binomial distribution. Thus, in this case, we can write down the exact parameters of the distribution in terms of elementary functions and show that the term inside the supremum in (7) is simply , which is maximized at , where is the golden ratio, which results in the fully explicit capacity upper bound of for the deletion channel with . We may then interpolate between this bound and the trivial values at using a convexity technique777For extending the bounds to , the results of [ref:RD15] are not tight, so in this regime we rely on the plausible conjecture that the capacity function is convex [ref:Dal11]. of [ref:RD15], thereby obtaining fully explicit capacity upper bounds for general that are proved without any need for numerical computation (Corollary 36).

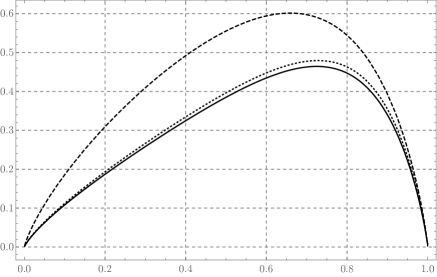

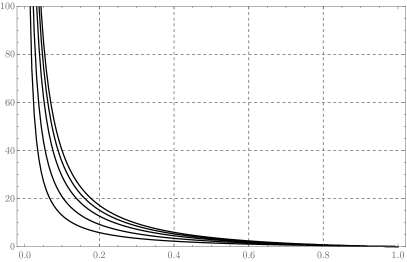

As in the Poisson case with (3), the inverse binomial distribution suffers from a constant asymptotic gap of in the KKT conditions (2) (Figure 11). By examining the connection between (3) and the digamma distribution (5), we develop a systematic “truncation technique” (made precise in Section 5.2) that allows us to refine (6) to sharply eliminate the gap for the binomial case as well. To begin with, we prove that enforcing the KKT conditions (2) with equality for all results in a unique class of solutions for the distribution of , which is exactly

| (8) |

Therefore, if such a distribution feasibly exists, it would necessarily be capacity achieving. However, we observe that the term inside the exponent (what we have labeled as in (8)) exponentially grows in , and therefore, there is no normalizing constant888Interestingly, using (2), this shows that while the optimal input distribution must have infinite support, it cannot have a full support. See Remark 30, and, similarly for the Poisson case, Remark 12. that would make (8) a valid distribution for any . Our proposed truncation technique adjusts the exponent of this alleged optimal solution so as to make its growth rate manageable, while still satisfying the KKT conditions (2) with a potentially nonzero gap that exponentially decays in . In order to do so, we first prove the following integral expression for in (8):

| (9) |

We show that exponentially grows in when , and grows as when (Claim 27). The truncation technique would involve the truncation of the upper bound of the integral that defines (when ) to . The resulting function, that we call , may be written, after a change of variables, as

We remark that . When , the growth rate of is

where is the logarithmic integral (116). Using the factorial moments of the binomial distribution, we show that (Proposition 29), and furthermore, that

From the above results, it follows that, letting

and replacing the in (8) with (except for the special case ) results in a refined distribution for that sharply satisfies (2). Despite the complex-looking expression defining the above distribution, as we see in Section 6.2.2, the distribution converges pointwise to the dual-feasible solution (5) (the digamma distribution) for the Poisson case as ; therefore, it is indeed a generalization of (5) to arbitrary values of . The gap to equality in the KKT conditions can be explicitly computed in integral form (using the above results for the expectations of and ), which we show to be

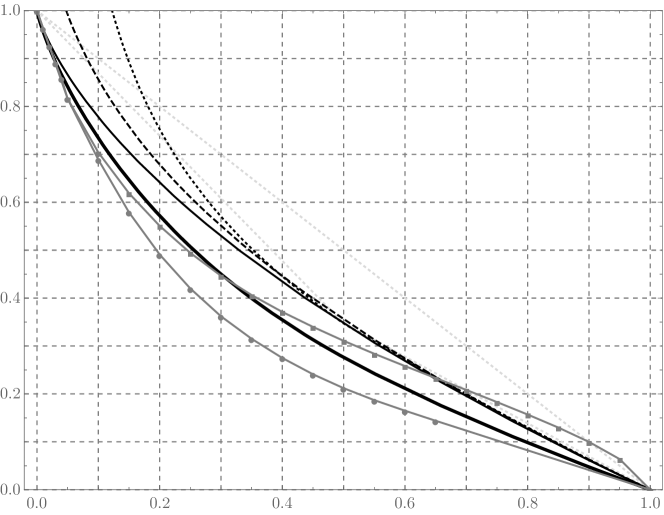

with the second integral understood to be zero for . This gap is zero at , exponentially decays as grows, and converges to (as in the Poisson case) for (see Figure 11). Hence, we obtain several capacity upper bounds, of varying complexities, for the deletion channel. This depends on the chosen dual feasible distribution for , that is, either the truncated variation of (8) or the inverse binomial distribution (6), or in the latter case, whether the function in (7) is numerically computed or upper bounded by either elementary or standard special functions (Figures 14 and 15). The resulting bounds are depicted in Figure 16 and are listed in Table B.5. For the limiting case , we see that our best upper bound estimate is which comes quite close to the computer-assisted upper bound reported in [ref:RD15], and substantially improves the in [ref:MDP07] (which is also computer-assisted). Our fully explicit upper bound of is also better than what reported in [ref:MDP07]. Since our methods for the Poisson-repeat channel converge to what we obtain for the deletion channel in the limit , we obtain the same upper bound estimate of for the capacity of the Poisson-repeat channel with deletion probability as well. Finally, we analyze our results for the limiting case (Section 6.3.4). We prove that, in this regime, our upper bounds exhibit the asymptotic behavior of which is known to be the case for the true capacity of the deletion channel [ref:KMS10, ref:KM13].

3 General mean-limited and convolution channels

In this section, we consider general classes of channels that we call “general mean-limited” and “convolution channels”. The input and output alphabet for these channels is the set of non-negative reals. In general, any such channel can be described by a probability transition rule over the non-negative reals, where . The channel takes an input and outputs the output random variable according to the rule . Since the capacity of this channel may in general be infinite, we restrict the set of possible input distributions by defining a mean constraint , for a parameter , and use the notation and the terminology general mean-limited channel for the channel defined with respect to the transition rule and mean constraint . The rate achieved by an input distribution for this channel is defined as , and naturally, the capacity is the supremum of the achievable rates subject to the given mean constraint.

A natural choice for the transition rule , that results in what we call a convolution channel, is via a multiplicative noise distribution over non-negative reals. For an , let denote the distribution attained by raising the characteristic function of to the power . When is a positive integer, this would correspond to adding together independent samples from , or equivalently, the -fold convolution of the distribution with itself (hence the terminology “convolution channel”). The convolution channel defined with respect to , that we use the overloaded notation for, takes an input and outputs a sample from .

Let . Note that, since , the rate achieved by an input distribution would be , and the capacity is simply , where the supremum is over the input distributions satisfying .

A convolution channel, or more generally any channel , can be defined over continuous or discrete distributions. In this work, for the sake of concreteness and a unified notation, we focus on the discrete case (and in fact, the integer case). However, the results can be readily extended to continuous distributions if differential entropy and mutual information are used (rather than the discrete Shannon entropy) to measure information, and summations are replaced by the the analogous integrals.

3.1 Capacity of general mean-limited channels

In this section, we characterize the capacity of a general mean-limited channel , defined with respect to a probability transition rule and output mean constraint , as the optimum solution of a convex program. This particularly provides the technical tool for analyzing the capacity of convolution channels, and subsequently, general repeat channels.

Recall that the capacity of is the supremum mutual information between the input and output of the channel, where the supremum is taken with respect to all input distributions whose corresponding output distribution satisfies the given mean constraint . Although our methods are general and apply to any (continuous or discrete) transition rule , in this section we focus on discrete distributions. In particular, we assume that the input alphabet is a discrete set and so is the output alphabet (for the purpose of this work, we may think of both and as the set of non-negative integers).

For each fixed , let denote the random variable conditioned on (i.e., is the output of the channel when a fixed input is given). The problem of maximizing the mutual information

where denotes the Kullback-Leibler (KL) divergence, can naturally be written as a convex minimization program as follows:

| (10) | ||||

| subject to | (11) | |||

| (12) | ||||

| (13) | ||||

| (14) |

where we have used the following notation: (resp., ) in (10) and (13) denotes the probability assigned by the distribution of (resp., the distribution of ) to the outcome (resp., ). Moreover, with a slight abuse of notation, we may think of and as vectors of probabilities assigned to the possible outcomes by the distributions that define the underlying random variables, so that for example in (12), where is the all-ones vector, is a shorthand for the summation of probabilities that define (which should be equal to one). Note that for each fixed , the entropy in (10) is a constant value defined by the transition rule . In (14), denotes the (infinite dimensional) transition matrix from to whose entry at row and column is equal to .

Following the standard approach in convex optimization, we define slack variables , , for each constraint in (14), , , for each non-negativity constraint in (11), for (12) and for (13). Now, the Lagrangian for the program (10) may be written as

| (15) |

From (15), the derivatives of with respect to each variable and can be written as

| (16) | ||||

where denotes the column of indexed by .

Observe that one can trivially construct a strictly feasible solution for (10). Therefore, Slater’s condition holds and the duality gap for this program is zero. The dual objective function

can now be written by analytically optimizing with respect to and . Setting implies that

| (17) |

where expectation is taken over the random variable . This can be deduced from (16) by observing that the product is precisely the average of the values defined by , , with respect to the measure defined by the th column of ; i.e., the distribution of .In other words,

Setting , on the other hand, gives us

| (18) |

and thus,

| (19) |

Since linearly depends on variables and a linear function has bounded infimum only when the function is zero, is only finite when (17) holds for all , which we will assume in the sequel. In this case, we deduce

| (20) |

The dual program to (10) can now be written, recalling the constraints (17), as

| subject to | |||

which we rewrite, using (20), as a convex minimization problem

| (21) | ||||

| subject to | (22) |

Now, the objective value achieved by any feasible solution to the above dual formulation gives an upper bound on the maximum attainable mutual information and thus a capacity upper bound. Furthermore, since (10) is convex and satisfies strong duality, Karush-Kuhn-Tucker (KKT) conditions imply that a primal feasible solution for (10) is optimal if and only if there is a dual feasible solution such that, recalling (18),

| (23) |

for all , and moreover, (22) holds with equality for all such that . In this case, using (23), the dual objective function simplifies to

On the other hand, we can write

where we define , so that (22) can be rewritten as

We have thus proven the following result (written with a trivial change of the variable ):

Theorem 1.

Consider a general mean-limited channel with output alphabet , and let be any distribution over . Denote by the random variable the output of the channel given as the input, and let and be any real parameters such that999It is worthwhile to note that having the term on the right hand side of (25), as opposed to , is quite useful for finding natural dual feasible distributions, and causes a mean-adjusting term of the form in the distribution of to be naturally absorbed in the constant . However, this would not necessarily be the case if, on the right hand side, we had (as would be the case if the techniques of [ref:AG93] were applied). For the special case of the convolution channels, is a linear function of and the distinction disappears. However, our best upper bounds (Theorem 4) consider non-convolution channels as well.

| (24) |

Then, capacity of is at most . Furthermore, the capacity is exactly if and only if there is a distribution over the input alphabet such that the corresponding output distribution is and moreover,

| (25) |

3.2 Extension to multiple uses

We now extend the notion of general mean-limited channels to multiple uses and observe that the capacity is achieved by a product input distribution.

Let be the -fold concatenation of the channel ; i.e., the channel takes an -dimensional input vector and applies the transition rule on each independently, resulting in an output vector . In this case, the input distribution is allowed to be arbitrary subject to a total mean constraint . Naturally, the achieved rate by an input distribution is and the capacity of the -fold channel is the supremum of the achievable rates.

It is straightforward to argue that the capacity of is achieved by an independent input distribution. To see this, consider any input distribution satisfying the total mean constraint. Let denote a distribution of independent real numbers such that the marginal distribution of is identical to that of for all . Clearly, this would mean that the output distribution corresponding to consists of independent entries, where each has the same marginal distribution as . Therefore, and thus, also satisfies the total mean constraint. However, we may show that the rate achieved by is no less than that of , as follows:

Therefore, we have proved the following:

Lemma 2.

Let be an -use general mean-limited channel. Then, there is a capacity achieving input distribution which is a product distribution.

4 General repeat channels

A natural model to generalize both deletion and Poisson-repeat channels is the following: Let be a distribution on non-negative integers. The -repeat channel is defined to receive a (possibly infinite) stream of bits and replaces each bit independently with a number of copies of the bit distributed according to . We call such a channel a general repeat channel with respect to the repetition rule . The binary deletion channel and Poisson-repeat channels are repeat channels with respect to the Bernoulli and Poisson repetition rules, respectively.

To characterize the capacity of a -repeat channel, without loss of generality, one may assume that the first-ever bit given to the channel is not deleted by the channel (i.e., it will be replicated at least once). The effect of this assumption on the capacity is amortized down to zero as the number of channel uses tends to infinity, and thus we shall make this assumption in the sequel. Similarly, we may assume that the first input bit ever given to the channel is a , as this assumption will also have no effect on the capacity of the channel.

Consider any input distribution on -bit sequences , where we think of as growing to infinity. If we know the first bit of , we may equivalently think of it as its run-length encoding which we denote by a sequence of positive integers , where we also think of (where ) as growing to infinity. Let the “deletion probability” denote the probability assigned to the zero outcome by , and .

We now aim to model the behavior of the -repeat in a way that can be analyzed more conveniently. Towards this goal, consider the following pre-processor procedure on a bit sequence :

-

1.

Let . Given the input sequence , draw a geometrically distributed random variable with mean .

-

2.

Let the bit sequence be the sequence of “even runs” in ; i.e., the bits of corresponding to the runs . Let be so that , the th bit of , corresponds to the th bit in (if , output and terminate). Suppose that the bit corresponds to the run in .

-

3.

Output the integer . Repeat the procedure with .

Note that, since each iteration of the above procedure eliminates at least one of the , the number of integers output by the procedure (which are all positive) must necessarily satisfy .

Denote by the distribution conditioned on the outcome being nonzero. We now define an auxiliary, run-processor channel as follows: The channel receives, at input, a sequence of positive integers . For each , the channel independently computes as will be described next and then outputs the sequence . To compute , the channel outputs a sample from , where denotes convolution of distributions (i.e., the distribution of independent random samples from each component added together). A schematic diagram of the above pre-processor and run-processor procedures appears in Figure 1. We now show that the combination of the pre-processor and the run-processor is statistically equivalent to action of the -repeat channel.

Lemma 3.

Let be a bit-sequence and be the output of the pre-processor on with respect to a distribution . Let be the output of the run-processor channel on (with respect to ). Then, the distribution of is identical to the run-length encoding of the output of the -repeat channel on .

Proof.

Recall the convention that the first bit of the input sequence is assumed to be zero, and that this bit is not deleted by the channel. Given , the -repeat channel replaces each independently with copies sampled from (except for , which is sampled from the conditional distribution ). Since the decision is made independently for each , the can be sampled in any order without a change in the resulting output distribution. Suppose, therefore, that the channel first decides on the even runs corresponding to . Namely, the channel can be thought of as performing the following procedure to produce the output distribution:

-

1.

For each bit in the input sequence represented by the even runs , decide, in order, whether the bit is deleted (i.e., replaced by zero copies), until the first non-deletion is found. Suppose the first non-deletion occurs at some located in block .

-

2.

Consider now the odd runs , up to the non-deletion position. Replace (which ought not be deleted) by one or more copies as determined by a fresh sample from . Furthermore, independently replace each remaining bit in the odd runs with a number of copies determined by a fresh sample from .

-

3.

Restart the process on the remaining bits , until the input sequence is exhausted.

Note that, by the end of each execution of the above procedure, we have revealed that is a non-deletion position. In the subsequent round, will be the first bit in the remaining input sequence, and this is consistent with the assumption that the first input bit in each round is replaced by a number of copies sampled from (i.e., conditioned on the nonzero outcomes), as opposed to .

We see that the number of zeros output by the first iteration of the above process determines the distribution of the first run-length of the output of the -repeat channel given , which is . Moreover, conditioned on the outcome of the first iteration, the second iteration determines the distribution of the second run of the output of the -repeat channel, i.e., , given and . Inductively, we see that the th iteration of the above procedure, conditioned on the outcome of the first iterations, produces a number of bits distributed according to the conditional distribution given . Therefore, the entire procedure samples according to the exact run-length encoding distribution of the output of the -repeat channel, given the input .

We now observe that the first step of the above procedure corresponds to the first step of the pre-processor; i.e., the geometric random variable determines the position of the first non-deletion within the even runs (recall that is the deletion probability of a bit). Furthermore, observe that the combined length of the odd runs is exactly the random variable output by each iteration of the pre-processor.

Now, the run-processor takes each produced by the th execution of the pre-processor and replaces it with , which is an independent sample from . Observe that a sample from the above convolution corresponds to the number of bits generated by taking a run of bits of length , replacing the first bit with a non-zero number of copies sampled from and replacing each remaining bit by a number of copies independently sampled from . This is precisely what the above procedure does with the combined bits from the odd runs in each round. That is, the integer output by the run-processor (conditioned on ) has the same distribution as the number of bits output by the above procedure in round (conditioned on the transcript of the execution the procedure for the first rounds).

We conclude that the pre-processor followed by the run-processor generate an integer sequence that has the same distribution as the run-length encoding of the above procedure, which in turn has the same distribution as the run-length encoding of the output of the -repeat channel given input . ∎

In light of Lemma 3, characterizing the capacity of a -repeat channel (that we denote by ) is equivalent to characterizing capacity of the cascade of the pre-processor and the run-processor. Let this cascade channel be denoted by the Markov chain . We are interested in

where the supremum is taken over all input distributions . Unlike channels with no synchronization errors (e.g., binary symmetric or erasure channels), it is not trivial to show that the above limit exists, and is equal to the capacity. However, the identity follows from [ref:Dob67]. Note that

| (26) |

so that

| (27) |

where the supremum is still over the distribution of . A major technical tool that we introduce is the following theorem, which reduces the task of upper bounding the capacity of a -repeat channel to a capacity upper bound problem for a related mean-limited channel. A proof of this result appears in Section 4.1.

Theorem 4.

Consider a -repeat channel and let be the general mean-limited channel with respect to the transition rule over positive integer inputs that, given an integer , outputs a sample from the convolution , where is the distribution conditioned on the outcome being nonzero. Let , , and be the probability assigned to the outcome zero by . Then,

| (28) |

A slightly simpler result to apply is the following corollary of Theorem 4:

Corollary 5.

Consider a -repeat channel and let be a convolution channel corresponding to and restricted to non-negative integer inputs. Let be the probability assigned to the outcome zero by , and . Then, the capacity of the -repeat channel can be upper bounded as

| (29) |

Proof.

Let be the channel defined in the statement of Theorem 4. The mean-limited channel corresponding to the transition rule receives a positive integer , and outputs a summation of independent random variables where is sampled from (i.e., conditioned on the outcome being nonzero) and the rest are sampled from . Let be a modification of with side information, in which the receiver also receives the exact value of . This side information can only increase the capacity of the channel for the corresponding parameter . Let . Since the input to is a positive integer, the modified channel is equivalent to, and has the same capacity as, the convolution channel (with the input restricted to non-negative integers). This is due to the fact that the receiver may simply subtract the given value of , which is independent of the input and thus bears no information about the input, from and thereby simulate a convolution channel with the matching mean constraint, which is . This means that .

Remark 6.

Compared with Theorem 4, Corollary 5 is in general more convenient to work with. This is due to the fact that the normalizing constant in the probability mass function of the conditional distribution in Theorem 4 incurs an additive factor in the entropy expression for that, in general, may be of little effect but nevertheless cause significant technical difficulties. However, this convenience comes at cost of potentially obtaining worse capacity upper bounds than what Theorem 4 would give. For the case of the deletion channel, is a Bernoulli distribution and becomes a trivial, singleton, distribution. Therefore, in this case, Corollary 5 can obtain the same result as Theorem 4. However, for channels for which contains substantial entropy; e.g., the Poisson-repeat channel where has a large mean, the loss incurred by applying Corollary 5 rather than Theorem 4 may be noticeable and even potentially trivialize the resulting upper bounds.

4.1 Proof of Theorem 4

In order to prove Theorem 4, we first recall (27); i.e.,

where the supremum is over the distribution of the -bit input sequence (and and being the corresponding distributions of the outputs of the pre-processor and run-processor, respectively). Assume that the capacity is not zero (otherwise, the claimed upper bound would be trivial). In order to avoid introducing excessive notation for the various error terms involved, in the sequel we use asymptotic notation as grows to infinity (with hidden constants possibly depending on ); so that a term can be made arbitrarily small as grows; an term grows with , and so forth. Consider a large enough (that we will tend to infinity in the end) and a choice for that approaches the corresponding supremum, so that, for the and defined by , we have

The minimum possible would depend on the desired magnitude of the added term. We note that the length of and is itself a random variable jointly correlated with , and . This causes technical difficulties that we first handle by showing below that we may essentially assume that the length is large, but fixed and known. In order to do so rigorously, first recall that, denoting and , we may write (since the knowledge of either or uniquely reveals as well),

where for the last inequality we are using the fact that is always an integer between and . Therefore, conditioning on has no asymptotic effect on the capacity upper bound and we may write

Without loss of generality, in the sequel we assume that is entirely supported on -bit sequences that consist of runs (much lower estimates would also suffice). The contribution of all other sequences to the entropy of would be , which would have no asymptotic effect on the achieved rate. For any such input sequence (and consequently, for the distribution defined by ), it is straightforward to show (e.g., using Azuma-Hoeffding inequality) that with overwhelming probability , the resulting choice of will also be large; particularly, that for some . Let us now write

| (30) |

where in the second inequality, we have used the fact that with probability , and have used the trivial upper bound of for when (recall that is always the run-length encoding of a bit-string of length at most , and thus its entropy is at most ).

Consider an alternative, but equivalent, realization of the pre-processor that, given the input , first draws an infinite sequence of i.i.d., geometrically distributed random variables (each with mean ), and sets in the first step of the th iteration (thus the variables are never looked at).

Note that the total bit-length of consists of the summation of the produced values of by the pre-processor plus the corresponding (which represent the deleted bits by the pre-processor; i.e., hatched part in Figure 1), except for the final which may extend beyond the length of . More formally, it is always the case that

or, in other words,

| (31) |

where .

We recall that, for all , we simultaneously have . Furthermore, by a Chernoff-Hoeffding inequality, the summation highly concentrates around its expectation due to the being independent; namely we may observe that with probability , it is the case that for all we have . Furthermore, the value of is with probability by Markov’s inequality. Overall, combined with (31), it follows that with probability , we have

| (32) |

Note also that, the left hand side of (32) is (treating as a constant) with probability . For an integer , denote by the random variable conditioned on the event . Given the input , if we condition the output of the pre-processor on the event , the joint distribution of obviously changes, to possibly even a non-product distribution. However, we may still apply an averaging argument on (32) to show that101010Some care is needed for the averaging argument. Particularly, we may take advantage of the fact that, with high probability, the concentration bound holds simultaneously for all . Therefore, it just suffices to construct so that, for all , the random variable conditioned on the event is upper bounded by , which in turn follows by a simple averaging using Markov’s inequality. , for some set such that , the following holds: For all , we have

with probability over the distribution of . This, in turn, implies that, for all ,

| (33) |

Similar to , define , where is the random variable conditioned on the event . In other words, is the output of the run-processor when given at input. We may now rewrite (30) as

| (34) |

Consider any fixed . Note that the effect of the run-processor on is precisely the same as an -use mean-limited channel, as defined in Section 3.2 (albeit without the mean constraint), where the transition rule is given by the conditional distribution . That is, given an integer input , the transition rule outputs a sample from . Therefore, as in the proof of Lemma 2, since each only depends on the corresponding random variable , we may write

| (35) |

Furthermore, recall and , and observe that, for all ,

| (36) |

Using (35) and (36), we may now rewrite (34) as

| (37) |

where the second inequality is due to the following simple result:

Proposition 7.

For positive real numbers and , we have

Proof.

Without loss of generality suppose the right hand side is . Then, the inequality is equivalent to

which is true since for each , we have assumed . ∎

Now, observe that for any and , we have

since, assuming that , the random variable is sampled by transmitting over a mean-limited channel with transition rule and mean constraint . Therefore, the mutual information would be no more than the capacity of this channel. Using this, (37) further simplifies to

where the last equality is attained from the fact that, by taking the limit , the terms vanish. This completes the proof of Theorem 4.

5 Upper bounds on the capacity of the Poisson-repeat channel

5.1 Upper bounds on the capacity of a mean-limited Poisson channel

Let be a Poisson distribution with mean , and be the convolution channel defined with respect to the distribution111111We note that, in the context of optical communications, this channel was also considered in [ref:AW12]. A related channel is the standard, additive, discrete-time Poisson channel [ref:Sha90] that has been extensively studied in information theory. and mean constraint . Let be the probability transition rule corresponding to when seen as a general mean-limited channel. Recall that the input and output alphabets for this channel are both the set of non-negative integers. By Theorem 1, in order to upper bound the capacity of , it suffices to exhibit a distribution over non-negative integers and real parameters and , so that the corresponding random variable drawn from this distribution satisfies (24).

Let be the output of the channel when the input is fixed to . Explicitly, has a Poisson distribution with mean , so that (24) can be rewritten as

| (38) |

By the conclusion of Theorem 1, exhibiting any such distribution and parameters and would imply

| (39) |

We consider the following general form for the distribution of :

| (40) |

for some function , real parameter , and normalizing constant

assuming that the summation is convergent. Given any function that grows linearly in or slower, it is always possible to choose small enough so that the distribution is well defined. Moreover, by varying the choice of it is possible to set the expectation of to match the chosen parameter121212By varying , the mean may be adjusted to any arbitrary positive value so long as, for some fixed , the summation defining diverges to infinity with but, on the other hand, converges for all . . It turns out to be more convenient to set , for some function , and our goal would be to obtain an appropriate choice for .

Recall that, for any choice of positive integers and ,

The KL divergence can now be written as

| (41) |

Note that the only nonlinear term (in ) in the above is , so achieving (38) is equivalent to having real coefficients such that

| (42) |

At this point, the following feasible choice is immediate:

which results in

| (43) |

where is to be understood as . Numerical estimates on the mean and normalizing constants of this distribution for various choices of are listed in Table B.5. To see that this choice satisfies (42), it suffices to note that the function defined above is convex, and thus, by Jensen’s inequality,

so (42) is satisfied for . One can, however, observe that the inequality is strict by a constant gap as grows (as we show in Section 5.2).

Using Stirling’s approximation , we may write the asymptotic behavior of (43) as

| (44) |

so we see that (43) can be normalized to a valid distribution if and only if .