Numerical approximation of general Lipschitz BSDEs with branching processes

Abstract

We extend the branching process based numerical algorithm of Bouchard et al. [3], that is dedicated to semilinear PDEs (or BSDEs) with Lipschitz nonlinearity, to the case where the nonlinearity involves the gradient of the solution. As in [3], this requires a localization procedure that uses a priori estimates on the true solution, so as to ensure the well-posedness of the involved Picard iteration scheme, and the global convergence of the algorithm. When, the nonlinearity depends on the gradient, the later needs to be controlled as well. This is done by using a face-lifting procedure. Convergence of our algorithm is proved without any limitation on the time horizon. We also provide numerical simulations to illustrate the performance of the algorithm.

Keywords: BSDE, Monte-Carlo methods, branching process.

MSC2010: Primary 65C05, 60J60; Secondary 60J85, 60H35.

1 Introduction

The aim of this paper is to extend the branching process based numerical algorithm proposed in Bouchard et al. [3] to general BSDEs in form:

| (1.1) |

where is a standard -dimensional Brownian motion, is the driver function, is the terminal condition, and is the solution of

| (1.2) |

with constant initial condition and coefficients , that are assumed to be Lipschitz333As usual, we could add a time dependency in the coefficients , and without any additional difficulty. . From the PDE point of view, this amounts to solving the parabolic equation

The main idea of [3] was to approximate the driver function by local polynomials and use a Picard iteration argument so as to reduce the problem to solving BSDE’s with (stochastic) global polynomial drivers, see Section 2, to which the branching process based pure forward Monte-Carlo algorithm of [12, 13, 14] can be applied. See for instance [16, 17, 18] for the related Feynman-Kac representation of the KPP (Kolmogorov-Petrovskii-Piskunov) equation.

This algorithm seems to be very adapted to situations where the original driver can be well approximated by polynomials with rather small coefficients on quite large domains. The reason is that, in such a situation, it is basically a pure forward Monte-Carlo method, see in particular [3, Remark 2.10(ii)], which can be expected to be less costly than the classical schemes, see e.g. [1, 4, 5, 11, 21] and the references therein. However, the numerical scheme of [3] only works when the driver function is independent of , i.e. the nonlinearity in the above equation does not depend on the gradient of the solution.

Importantly, the algorithm proposed in [3] requires the truncation of the approximation of the -component at some given time steps. The reason is that BSDEs with polynomial drivers may only be defined up to an explosion time. This truncation is based on a priori estimates of the true solution. It ensures the well-posedness of the algorithm on an arbitrary time horizon, its stability, and global convergence.

In the case where the driver also depends on the component of the BSDE, a similar truncation has to be performed on the gradient itself. It can however not be done by simply projecting on a suitable compact set at certain time steps, since only maters up to an equivalent class of . Alternatively, we propose to use a face-lift procedure at certain time steps, see

(2.10). Again this time steps depend on the explosion times of the corresponding BSDEs with polynomial drivers. Note that a similar face-lift procedure is used in Chassagneux, Elie and Kharroubi [6]444We are grateful to the authors for several discussions on this subject. in the context of the discrete time approximation of BSDEs with contraint on the -component.

We prove the convergence of the scheme. The very good performance of this approach is illustrated in Section 4 by a numerical test case.

Notations: All over this paper, we view elements of , , as column vectors. Transposition is denoted by the superscript ⊤. We consider a complete filtered probability space supporting a -dimensional Brownian motion . We simply write for , . We use the standard notations (resp. ) for the class of progressively measurable processes such that (resp. ) is finite. The dimension of the process is given by the context. For a map , we denote by is derivative with respect to its first variable and by and its Jacobian and Hessian matrix with respect to its second component.

2 Approximation of BSDE using local polynomial drivers and the Picard iteration

For the rest of this paper, let us consider the (decoupled) forward-backward system (1.1)-(1.2) in which and are both bounded and Lipschitz continuous, and is non-degenerate such that there is a constant satisfying

| (2.1) |

We also assume that , , and are all bounded and continuous. In particular, (1.1)-(1.2) has a unique solution . The above conditions indeed imply that , for some .

Remark 2.1.

The above assumptions can be relaxed by using standard localization or mollification arguments. For instance, one could simply assume that has polynomial growth and is locally Lipschitz. In this case, it can be truncated outside a compacted set so as to reduce to the above. Then, standard estimates and stability results for SDEs and BSDEs can be used to estimate the additional error in a very standard way. See e.g. [7].

2.1 Local polynomial approximation of the generator

As in [3], our first step is to approximate the driver by a driver that has a local polynomial structure. The difference is that it now depends on both components of the solution of the BSDE. Namely, let

| (2.2) |

in which , (with ), the functions and (with ) are continuous and satisfy

| (2.3) |

for all , and , for some constants .

For a good choice of the local polynomial , we can assume that

is globally bounded and Lipschitz. Then, the BSDE

| (2.4) |

has a unique solution , and standard estimates imply that provides a good approximation of whenever is a good approximation of :

| (2.5) |

for some that depends on the global Lipschitz constant of (but not on the precise expression of ), see e.g. [7].

One can think at the as the coefficients of a polynomial approximation of in terms of on a subset , the ’s forming a partition of . Then, the ’s have to be considered as smoothing kernels that allow one to pass in a Lipschitz way from one part of the partition to another one.

The choice of the basis functions as well as will obviously depend on the application, but it should in practice typically be constructed such that the sets

| (2.6) |

are large and the intersection between the supports of the ’s are small. See [3, Remark 2.10(ii)] and below. Finally, since the function is chosen to be globally bounded and Lipschitz, by possibly adjusting the constant , we can assume without loss of generality that

| (2.7) |

For later use, let us recall that is related to the unique bounded and continuous viscosity solution of

though

| (2.8) |

Moreover,

| is bounded by and -Lipschitz. |

2.2 Picard iteration with truncation and face-lifting

Our next step is to introduce a Picard iteration scheme to approximate the solution of (2.4) so as to be able to apply the branching process based forward Monte-Carlo approach of [12, 13, 14] to each iteration: given , use the representation of the BSDE with driver .

However, although the map is globally Lipschitz, the map is a polynomial, given fixed , and hence only locally Lipschitz in general. In order to reduce to a Lipschitz driver, we need to truncate the solution at certain time steps, that are smaller than the natural explosion time of the corresponding BSDE with (stochastic) polynomial driver. As in [3], it can be performed by a simple truncation at the level of the first component of the solution. As for the second component, that should be interpreted as a gradient, a simple truncation does not make sense, the gradient needs to be modified by modifying the function itself. Moreover, from the BSDE viewpoint, is only defined up to an equivalent class on , so that changing its value at a finite number of given times does not change the corresponding BSDE. We instead use a face-lifting procedure, as in [6].

More precisely, let us define the operator on the space of bounded functions by

where

The operation maps into the smallest -Lipschitz function above . This is the so-called face-lifting procedure, which has to be understood as a (form of) projection on the family of -Lipschitz functions, see e.g. [2, Exercise 5.2], see also Remark 2.2 below. The outer operations in the definition of are just a natural projection on .

Let now be such that (A.3) and (A.4) in the Appendix hold. The constant is a lower bound for the explosion time of the BSDE with driver for any fixed . Let us then fix such that , and define

Our algorithm consists in using a Picard iteration scheme to solve (2.4), which re-localize the solution at each time step of the grid by applying operator .

Namely, using the notation to denote the solution of (1.2) on such that , we initialize our Picard scheme by setting

in which is a continuous function, -Lipschitz in space, continuously differentiable in space on and such that and . Then, given , for , we define as follows:

-

1.

For , set

-

2.

For , given :

-

(a)

Let be the unique solution on of

(2.9) -

(b)

Let , and set

(2.10) -

(c)

Set on , , and on , for .

-

(a)

-

3.

We finally define and

(2.11)

In above, the existence and uniqueness of the solution to (2.9) is ensured by Proposition A.1. The projection operation in (2.10) is consistent with the behavior of the solution of (2.4), recall (2.7), and it is crucial to control the explosion of and therefore to ensure both the stability and the convergence of the scheme. This procedure is non-expansive, as explained in the following Remark, and therefore can not alter the convergence of the scheme.

Remark 2.2.

Let be two measurable and bounded maps on . Then, , and therefore . In particular, since defined through (2.8) is -Lipschitz in its space variable and bounded by , we have for and therefore

for all and all measurable and bounded map .

Also note that, if we had if and only if , for all , then we would have , recall (2.6) and the definition of in terms of . This means that we do not need to be very precise on the original prior, whenever the sets can be chosen to be large.

From the theoretical viewpoint, the error due to the above Picard iteration scheme can be deduced from classical arguments. Recall that is such that (A.3) and (A.4) in the Appendix hold.

Theorem 2.1.

For each , the algorithm defined in 1.-2.-3. above provides the unique solution . Moreover, it satisfies , and there exists a measurable map , that is continuous on , such that is continuous on for all , and

| (2.12) | ||||

Moreover, for any constant , there is some constant such that

Proof. Recall from Remark 2.2 that maps bounded functions into -Lipschitz functions that are bounded by . Then, by Proposition A.1 in the Appendix, the solutions as well as are uniquely defined in and below (2.9). Moreover, one has , for all , and . As a consequence, is also uniquely defined and satisfies . Using again Proposition A.1, one has the existence of satisfying the condition in the statement.

We next prove the convergence of the sequence to . Since is uniformly bounded, the generator in (2.9) can be considered to be uniformly Lipschitz in and . Assume that the corresponding Lipschitz constants are and .

Let us set and define where denotes the solution of

on each , recall (2.8). In the following, we fix and use the notation

Fix . By applying Itô’s formula to and then taking expectation, we obtain

Using the Lipschitz property of and the inequality for all , it follows that, for all ,

| (2.13) | ||||

Let us now choose such that

| (2.14) |

For , we have for all . Choosing and in (2.13) such that

it follows from (2.13) that, for , for , where

and then, by (2.13) again,

Recalling Remark 2.2, this shows that

| (2.15) |

in which

Assume now that (2.15) holds true for and some given . Recall that . Applying (2.13) with the above choice of and , we obtain

which, by (2.14) and the fact that , induces that

| (2.16) |

where

Let us further choose such that , and recall that . Then, using again (2.13), (2.14), (2.15) applied to , we obtain, for ,

so that it follows from Remark 2.2 that

| (2.17) |

where

Since and on each , this concludes the proof. ∎

3 A branching diffusion representation for

We now explain how the solution of (2.9) on can be represented by means of a branching diffusion system. We slightly adapt the arguments of [13].

Let us consider an element such that , set for , and . Let be a sequence of independent -dimensional Brownian motions, and be two sequences of independent random variables, such that

and

for some continuous strictly positive map . We assume that

| , , and are independent. |

Given the above, we construct particles that have the dynamics (1.2) up to a killing time at which they split in different (conditionally) independent particles with dynamics (1.2) up to their own killing time. The construction is done as follows. First, we set , and, given with , we let in which . We can then define the Brownian particles by using the following induction: we first set

then, given and , we let

in which we use the notation

and

Now observe that the solution of (1.2) on with initial condition can be identified in law on the canonical space as a process of the form in which the deterministic map is -measurable, where is the predictable -filed on . We then define the corresponding particles by . Moreover, we define the -dimensional matrix valued tangent process defined on by

| (3.1) | ||||

where denotes the -dimensional identity matrix, and denotes the -th column of matrix .

Finally, we give a mark to the initial particle , and, for every particle , knowing , we consider its offspring particles and give the first particles the mark , the next particles the mark , the next particles the mark , etc. Thus, every particles carries a mark taking values in to .

Given the above construction, we can now provide the branching process based representation of . We assume here that defined in (2.12) are given for some , recall that by construction. We set . Then, for , we define on each interval recursively by

| (3.2) |

for , in which

where

Compare with [13, (3.4) and (3.10)].

The next proposition shows that actually coincides with in (2.12), a result that follows essentially from [13]. Nevertheless, to be more precise on the square integrability of and , one will fix a special density function as well as probability weights . Recall again that are defined in Theorem 2.1 and satisfy (2.12), and that are chosen such that (A.3)-(A.4) in the Appendix hold.

Proposition 3.1.

The proof of the above mimics the arguments of [13, Theorem 3.12] and is postponed to the Appendix A.2.

Remark 3.1.

The integrability and representation results in Proposition 3.1 hold true for a large class of parameters , and (see e.g. [13, Section 3.2] for more details). We restrict to a special choice of parameters in Proposition 3.1 in order to compute explicitly the lower bound for the explosion time as well as the upper bound for the variance of the estimators.

Remark 3.2.

a. The above scheme requires the computation of conditional expectations that involve the all path on each , for all , and therefore the use of an additional time space grid on which and are estimated by Monte-Carlo. For , the precision does not need to be important because the corresponding values are only used for the localization procedure, see the discussion just after Remark 2.2, and the grid does not need to be fine. The space grid should be finer at the times in because each is used per se as a terminal condition on , and not only for the localization of the polynomial. This corresponds to the Method B in [3, Section 3]. One can also consider a very fine time grid and avoid the use of a sub-grid. This is Method A in [3, Section 3]. The numerical tests performed in [3] suggest that Method A is more efficient.

b. From a numerical viewpoint, can also be estimated by using a finite difference scheme based on the estimation of . It seems to be indeed more stable.

c. Obviously, one can also adapt the algorithm to make profit of the ghost particle or of the normalization techniques described in [20], which seem to reduce efficiently the variance of the estimations, even when is the exponential distribution.

4 Numerical example

This section is dedicated to a simple example in dimension one showing the efficiency of the proposed methodology. We use the Method A of [3, Section 3] together with the normalization technique described in [20] and a finite difference scheme to compute . In particular, this normalization technique allows us to take as an exponential density rather than that in Proposition 3.1. See Remark 3.2.

We consider the SDE with coefficients

The maturity is and the non linearity in (1.1) is taken as

where

| (4.1) |

It is complemented by the choice of the terminal condition , so that an analytic solution is available :

We use the algorithm to compute an estimation of on .

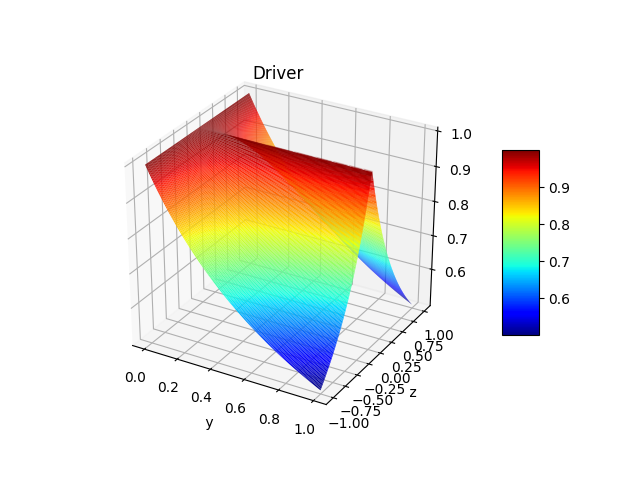

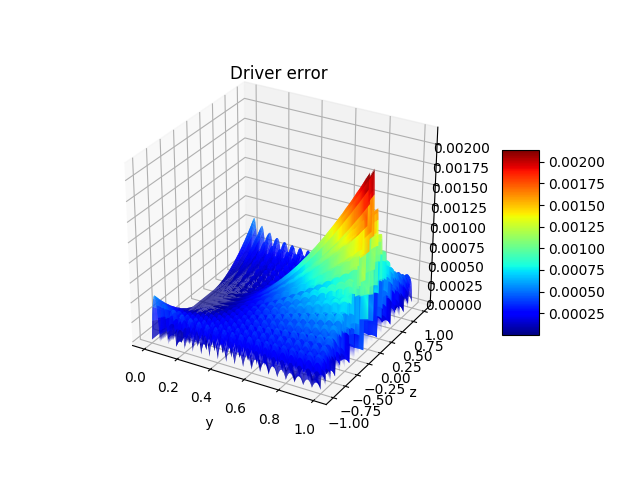

To construct our local polynomials approximation of , we use a linear spline interpolation in each direction, obtained by tensorization, and leading to a local approximation on the basis , , , on each mesh of a domain . Figure 1 displays the function and the error obtained by a discretization of meshes.

The parameters affecting the convergence of the algorithm are:

-

•

The couple of meshes used in the spline representation of (4.1), where (resp. ) is the number of linear spline meshes for the (resp. ) discretization.

-

•

The number of time steps .

-

•

The grid and the interpolation used on at and for all dates , . Note that the size of the grid has to be adapted to the value of , because of the diffusive feature of (1.2). All interpolations are achieved with the StOpt library (see [9, 10]) using a modified quadratic interpolator as in [19]. In the following, denotes the mesh of the space discretization.

-

•

The time step is set to and we use an Euler scheme to approximate (1.2).

-

•

The accuracy of the estimation of the expectations appearing in our algorithm. We compute the empirical standard deviation associated to each Monte Carlo estimation of the expectation in (3.2). We try to fix the number of samples such that does not exceed a certain level, fixed at , at each point of our grid. We cap this number of simulations at .

-

•

The intensity, set to , of the exponential distribution used to define the random variables .

Finally, we take in the definition of .

We only perform one Picard iteration with initial prior .

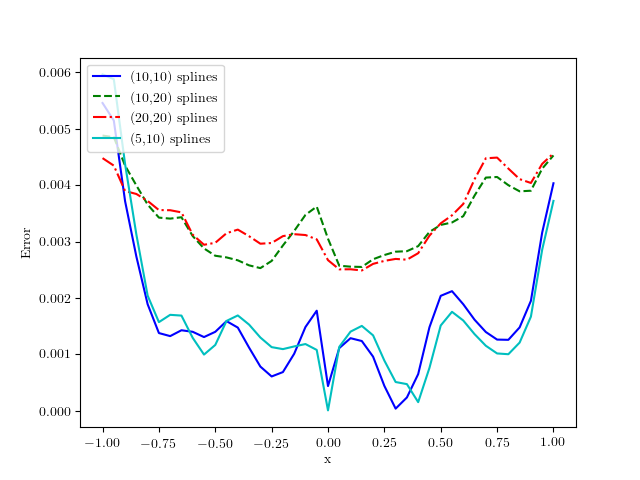

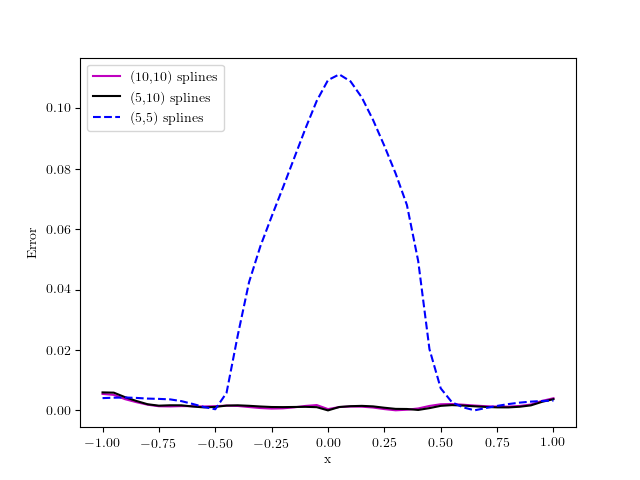

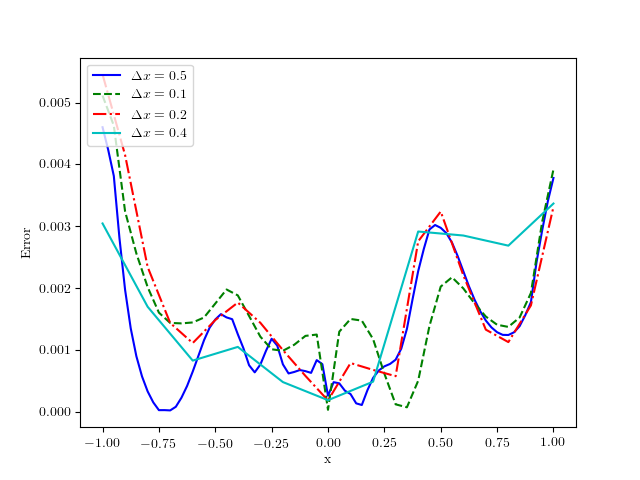

On the different figures below, we plot the errors obtained on for different values of , and . We first use time steps and an interpolation step of In figure 2, we display the error as a function of the number of spline meshes. We provide two plots:

-

•

On the left-hand side, varies above 5 and varies above 10,

-

•

On the right-hand side, we add . It leads to a maximal error of , showing that a quite good accuracy in the spline representation in is necessary.

In figure 3, we plot the error obtained with and a number of time steps equal to , for different values of : the results are remarkably stable with the interpolation space discretization.

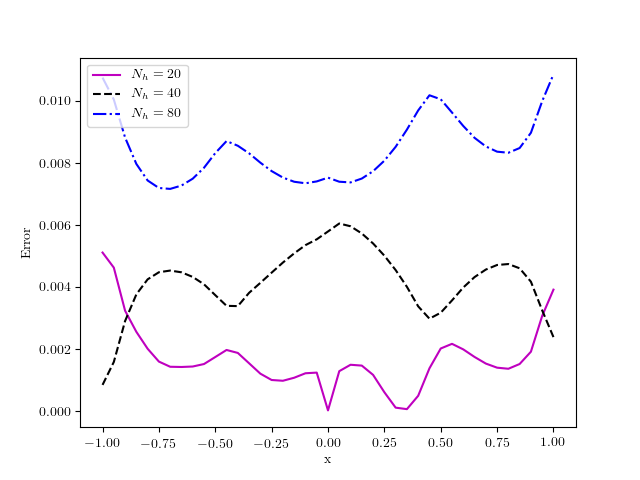

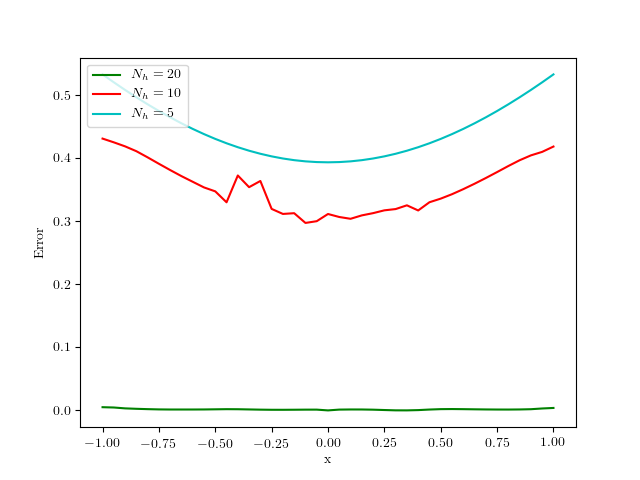

In Figure 4, we finally let the number of time steps vary. Once again we give two plots:

-

•

one with above or equal to ,

-

•

one with small values of .

The results clearly show that the algorithm produces bad results when is too small: the time steps are too large for the branching method. In this case, it exhibits a large variance. When is too large, then interpolation errors propagate leading also to a deterioration of our estimations.

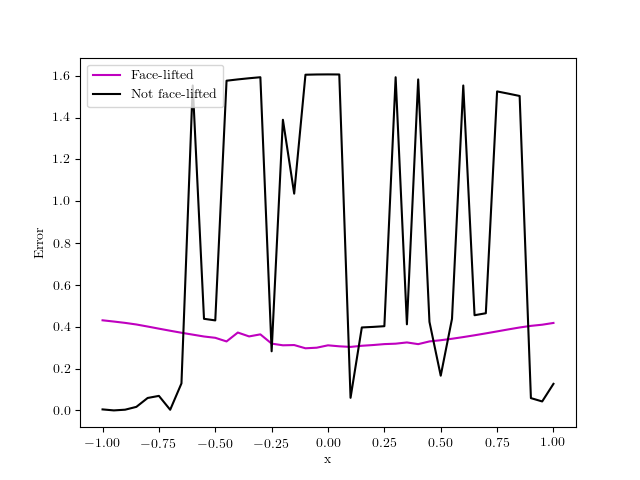

Numerically, it can be checked that the face-lifting procedure is in most of the cases useless when only one Picard iteration is used:

-

•

When the variance of the branching scheme is small, the face-lifting and truncation procedure has no effect,

-

•

When the variance becomes too large, the face-lifting procedure is regularizing the solution and this permits to reduce the error due to our interpolations.

In figure 5, we provide the estimation with and without face-lifting, obtained with , and a space discretization .

For the computational time is equal to seconds on a year old laptop.

Appendix A Appendix

A.1 A priori estimates for the Picard iteration scheme

In this section, we let be the tangent process associated to on by

and we define

for . Standard estimates lead to

| (A.1) |

for some that only depends on , , , , in (2.1) and . In particular, it does not depend on . Up to changing this constant, we may assume that

| (A.2) |

Set

and let and be such that

| (A.3) |

and

| (A.4) |

The existence of and follows from (2.2) and (2.3). Note that they do not depend on .

Proposition A.1.

Let be bounded by and -Lipschitz. Fix . Let be measurable such that . Then, there exists a unique bounded solution on to

| (A.5) |

It satisfies

| (A.6) |

Moreover, there exists a bounded continuous map such that on -a.s. and -a.e. on . It satisfies on .

Proof. We construct the required solution by using Picard iterations. We set , and define recursively on the couple as the unique solution of

whenever it is well-defined. It is the case for . We now assume that is well-defined and such that on for some . Then,

in which we used (A.3) for the second inequality. On the other hand, up to using a mollifying argument, one can assume that is and that is Lipschitz. Then, it follows from the same arguments as in [15, Theorem 3.1, Theorem 4.2] that admits the representation

By combining the above together with (A.1) and (A.2), we obtain that

in which we used (A.4) for the second inequality. The above proves that the sequence is uniformly bounded on . Therefore, we can consider as a Lipschitz generator, and hence is in fact a Picard iteration that converges to a solution of (A.5) with the same bound.

The existence of the maps and such that follows from [15, Theorem 3.1] applied to (A.5) when is , uniformly in . The representation result of [15, Theorem 4.2] combined with a simple approximation argument, see e.g. [8, (ii) of the proof of Proposition 3.2], then shows that the same holds on under our conditions.

A.2 Proof of the representation formula

We adapt the proof of [13, Theorem 3.12] to our context. We proceed by induction. In all this section, we fix

and assume that the result of Proposition 3.1 holds up to rank on (with the convention , ), and up to rank on . In particular, we assume that .

We fix and define

where

in which is the tangent process of with initial condition at . We then set

Since is non-increasing and is bounded by and -Lipschitz, direct computations imply that

| (A.7) |

We first estimate the right-hand side, see (A.10) below.

Let us denote by the constant in the Burkholder-Davis-Gundy inequality such that for any continuous martingale with . Denote further

where the largest eigenvalue of the matrix , the largest eigenvalue of the matrix , , and . Define also as the largest eigenvalue of matrix .

Lemma A.1.

Proof. Let be a fixed vector. Set . Then, it follows from direct computations that

Further, remember that each is assumed to be bounded by , so that is uniformly bounded by . Then, direct computations lead to

and

It remains to use our specific choice of and in Proposition 3.1 to conclude. ∎

Let us now choose and such that

| (A.8) |

and

| (A.9) |

Lemma A.2.

Let the conditions of Proposition 3.1 hold. Then, the ordinary differential equation with initial condition has a unique solution on , and it is bounded by . Moreover,

| (A.10) |

for all .

Proof. The result follows from exactly the same arguments as in [3, Lemma A.1]. ∎

We can now conclude the proof of Proposition 3.1.

Proof of Proposition 3.1. In view of (A.7), Lemma A.2 implies that is uniformly integrable (with a bound that does not depend on for ). Then, arguing exactly as in [3, Proposition A.2] leads to on . Combined with [13, Proposition 3.7], the uniform integrability also implies that on , and one can conclude from Theorem 2.1 that on . By the induction hypothesis of the beginning of this section, this proves that the statements of Proposition 3.1 hold. ∎

Remark A.1.

The constants and (and hence and ) are clearly not optimal for applications. For instance, if , for some non-degenerate constant matrix, the constants and can be significantly simplified as shown in [13, Remark 3.9].

Acknowledgements

This work has benefited from the financial support of the Initiative de Recherche “Méthodes non-linéaires pour la gestion des risques financiers” sponsored by AXA Research Fund.

Bruno Bouchard and Xavier Warin acknowledge the financial support of ANR project CAESARS (ANR-15-CE05-0024)..

Xiaolu Tan acknowledges the financial support of the ERC 321111 Rofirm, the ANR Isotace (ANR-12-MONU-0013), and the Chairs Financial Risks (Risk Foundation, sponsored by Société Générale) and Finance and Sustainable Development (IEF sponsored by EDF and CA).

References

- [1] V. Bally and P. Pages, Error analysis of the quantization algorithm for obstacle problems, Stochastic Processes & Their Applications, 106(1), 1-40, 2003.

- [2] B. Bouchard, J.F. Chassagneux. Fundamentals and advanced techniques in derivatives hedging. Springer Universitext, 2016.

- [3] B. Bouchard, X. Tan , X. Warin and Y. Zou, Numerical approximation of BSDEs using local polynomial drivers and branching processes, Monte Carlo Methods and Applications, to appear.

- [4] B. Bouchard and N. Touzi, Discrete-time approximation and Monte-Carlo simulation of backward stochastic differential equations, Stochastic Process. Appl., 111(2), 175-206, 2004.

- [5] B. Bouchard, X. Warin, Monte-Carlo valuation of American options: facts and new algorithms to improve existing methods. In Numerical methods in finance (pp. 215-255). Springer Berlin Heidelberg, 2012.

- [6] J.F. Chassagneux, R. Elie and I. Kharroubi, A numerical probabilistic scheme for super-replication with Delta constraints, arXiv, forthcoming.

- [7] N. El Karoui, S. Peng, M.C. Quenez, Backward stochastic differential equations in finance, Mathematical finance 7(1), 1-71, 1997.

- [8] E. Fournié, J.M. Lasry, , J. Lebuchoux, P.L. Lions, N. Touzi, Applications of Malliavin calculus to Monte Carlo methods in finance. Finance and Stochastics, 3(4), 391–412, 1999.

- [9] H. Gevret, J. Lelong, X. Warin , The StOpt library, https://gitlab.com/stochastic-control/StOpt

- [10] H. Gevret, J. Lelong, X. Warin , STochastic OPTimization library in C++, EDF Lab, 2016.

- [11] E. Gobet, J.P. Lemor, X. Warin, A regression-based Monte Carlo method to solve backward stochastic differential equations. The Annals of Applied Probability, 15(3), 2172-202, 2005.

- [12] P. Henry-Labordère, Cutting CVA’s Complexity, Risk, 25(7), 67, 2012.

- [13] P. Henry-Labordere, N. Oudjane, X. Tan, N. Touzi, X. Warin, Branching diffusion representation of semilinear PDEs and Monte Carlo approximation. arXiv preprint, 2016.

- [14] P. Henry-Labordere, X. Tan, N. Touzi, A numerical algorithm for a class of BSDEs via the branching process. Stochastic Processes and their Applications, 28, 124(2), 1112-1140, 2014.

- [15] J. Ma and J. Zhang, Representation theorems for backward stochastic differential equations. The annals of applied probability, 12(4), 1390–1418, 2002.

- [16] H.P. McKean, Application of Brownian motion to the equation of Kolmogorov-Petrovskii-Piskunov, Comm. Pure Appl. Math., 28, 323-331, 1975.

- [17] A.V. Skorokhod Branching diffusion processes, Theory of Probability & Its Applications, 9(3), 445-449, 1964.

- [18] S. Watanabe, On the branching process for Brownian particles with an absorbing boundary, J. Math. Kyoto Univ. 4(2), 385-398, 1964.

- [19] X. Warin, Some Non-monotone Schemes for Time Dependent Hamilton-Jacobi-Bellman Equations in Stochastic Control, Journal of Scientific Computing, 66(3), 1122-1147, 2016.

- [20] X. Warin, Variations on branching methods for non linear PDEs, arXiv preprint arXiv:1701.07660, 2017

- [21] J. Zhang, A numerical scheme for backward stochastic differential equations, Annals of Applied Probability, 14(1), 459-488, 2004.