From Distance Correlation to Multiscale Graph Correlation

Abstract

Understanding and developing a correlation measure that can detect general dependencies is not only imperative to statistics and machine learning, but also crucial to general scientific discovery in the big data age. In this paper, we establish a new framework that generalizes distance correlation — a correlation measure that was recently proposed and shown to be universally consistent for dependence testing against all joint distributions of finite moments — to the Multiscale Graph Correlation (MGC). By utilizing the characteristic functions and incorporating the nearest neighbor machinery, we formalize the population version of local distance correlations, define the optimal scale in a given dependency, and name the optimal local correlation as MGC. The new theoretical framework motivates a theoretically sound Sample MGC and allows a number of desirable properties to be proved, including the universal consistency, convergence and almost unbiasedness of the sample version. The advantages of MGC are illustrated via a comprehensive set of simulations with linear, nonlinear, univariate, multivariate, and noisy dependencies, where it loses almost no power in monotone dependencies while achieving better performance in general dependencies, compared to distance correlation and other popular methods.

Keywords: testing independence, generalized distance correlation, nearest neighbor graph

1 Introduction

Given pairs of observations for , assume they are generated by independently identically distributed (iid) . A fundamental statistical question prior to the pursuit of any meaningful joint inference is the independence testing problem: the two random variables are independent if and only if , i.e., the joint distribution equals the product of the marginals. The statistical hypothesis is formulated as:

For any test statistic, the testing power at a given type error level equals the probability of correctly rejecting the null hypothesis when the random variables are dependent. A test is consistent if and only if the testing power converges to as the sample size increases to infinity, and a valid test must properly control the type error level. Modern datasets are often nonlinear, high-dimensional, and noisy, where density estimation and traditional statistical methods fail to be applicable. As multi-modal data are prevalent in much data-intensive research, a powerful, intuitive, and easy-to-use method for detecting general relationships is pivotal.

The classical Pearson’s correlation [1] is still extensively employed in statistics, machine learning, and real-world applications. It is an intuitive statistic that quantifies the linear association, a special but extremely important relationship. A recent surge of interests has been placed on using distance metrics and kernel transformations to achieve consistent independence testing against all dependencies. A notable example is the distance correlation (Dcorr) [2, 3, 4, 5]: the population Dcorr is defined via the characteristic functions of the underlying random variables, while the sample Dcorr can be conveniently computed via the pairwise Euclidean distances of given observations. Dcorr enjoys universal consistency against any joint distribution of finite second moments, and is applicable to any metric space of strong negative type [6]. Notably, the idea of distance-based correlation measure can be traced back to the Mantel coefficient [7, 8]: the sample version differs from sample Dcorr only in centering, garnered popularity in ecology and biology applications, but does not have the consistency property of Dcorr.

Developed almost in parallel from the machine learning community, the kernel-based method (Hsic) [9, 10] has a striking similarity with Dcorr: it is formulated by kernels instead of distances, can be estimated on sample data via the sample kernel matrix, and is universally consistent when using any characteristic kernel. Indeed, it is shown in [11] that there exists a mapping from kernel to metric (and vice versa) such that Hsic equals Dcorr. Another competitive method is the Heller-Heller-Gorfine method (Hhg) [12, 13]: it is also universally consistent by utilizing the rank information and the Pearson’s chi-square test, but has better finite-sample testing powers over Dcorr in a collection of common nonlinear dependencies. There are other consistent methods available, such as the Copula method that tests independence based on the empirical copula process [14, 15, 16], entropy-based methods [17], and methods tailored for univariate data [18].

As the number of observations in many real world problems (e.g., genetics and biology) are often limited and very costly to increase, finite-sample testing power is crucial for certain data exploration tasks: Dcorr has been shown to perform well in monotone relationships, but not so well in nonlinear dependencies such as circles and parabolas; the performance of Hsic and Hhg are often the opposite of Dcorr, which perform slightly inferior to Dcorr in monotone relationships but excel in various nonlinear dependencies.

From another point of view, unraveling the nonlinear structure has been intensively studied in the manifold learning literature [19, 20, 21]: by approximating a linear manifold locally via the k-nearest neighbors at each point, these nonlinear techniques can produce better embedding results than linear methods (like PCA) in nonlinear data. The main downside of manifold learning often lies in the parameter choice, i.e., the number of neighbor or the correct embedding dimension is often hard to estimate and requires cross-validation. Therefore, assuming a satisfactory neighborhood size can be efficiently determined in a given nonlinear relationship, the local correlation measure shall work better than the global correlation measure; and if the parameter selection is sufficiently adaptive, the optimal local correlation shall equal the global correlation in linear relationships.

In this manuscript we formalize the notion of population local distance correlations and MGC, explore their theoretical properties both asymptotically and in finite-sample, and propose an improved Sample MGC algorithm. By combing distance correlation with the locality principle, MGC inherits the universal consistency in testing, is able to efficiently search over all local scales and determine the optimal correlation, and enjoys the best testing powers throughout the simulations. A number of real data applications via MGC are pursued in [22], e.g., testing brain images versus personality and disease, identify potential protein biomarkers for cancer, etc. And MGC are employed for vertex dependence testing and screening in [23, 24].

The paper is organized as follows: In Section 2, we define the population local distance correlation and population MGC via the characteristic functions of the underlying random variables and the nearest neighbor graphs, and show how the local variants are related to the distance correlation. In Section 3, we consider the sample local correlation on finite-samples, prove its convergence to the population version, and discuss the centering and ranking scheme. In Section 4, we present a thresholding-based algorithm for Sample MGC, prove its convergence property, propose a theoretically sound threshold choice, manifest that MGC is valid and consistent under the permutation test, and finish the section with a number of fundamental properties for the local correlations and MGC. The comprehensive simulations in Section 5 exhibits the empirical advantage of MGC, and the paper is concluded in Section 6. All proofs are in Appendix A, the simulation functions are presented in Appendix B, and the code are available on Github 111https://github.com/neurodata/mgc-matlab and CRAN 222https://CRAN.R-project.org/package=mgc.

2 Multiscale Graph Correlation for Random Variables

2.1 Distance Correlation Review

We first review the original distance correlation in [2]. A non-negative weight function on is defined as:

where is a non-negative constant tied to the dimensionality , and is the complete Gamma function. Then the population distance covariance, variance and correlation are defined by

where is the complex modulus, denotes the exponential transformation within the expectation of the characteristic function, i.e., (i represents the imaginary unit) and is the characteristic function. Note that distance variance equals if and only if the random variable is a constant, in which case distance correlation shall be set to . The main property of population Dcorr is the following.

Theorem.

For any two random variables with finite first moments, if and only if and are independent.

To estimate the population version on sample data, the sample distance covariance is computed by double centering the pairwise Euclidean distance matrix of each data, followed by summing over the entry-wise product of the two centered distance matrices. When the underlying random variables have finite second moments, the sample Dcorr is shown to converge to the population Dcorr , and is thus universally consistent for testing independence against all joint distributions of finite second moments.

2.2 Population Local Correlations

Next we formally define the population local distance covariance, variance, correlation by combining the k-nearest neighbor graphs with the distance covariance. For simplicity, they are named the local covariance, local variance, and local correlation from now on, and we always assume the following regularity conditions:

The finite second moments assumption is required by Dcorr, and also required by the local version to establish convergence and consistency. The non-constant condition is to avoid the trivial case and make sure population local correlations behave well. The continuous assumption is for ease of presentation, so the definition and related properties can be presented in a more elegant manner. Indeed, for any discrete random variable one can always apply jittering (i.e., add trivial white noise) to make it continuous without altering the independence testing.

Definition.

Suppose are iid as . Let be the indicator function, define two random variables

with respect to the closed balls and centered at and respectively. Then let denote the complex conjugate, define

as functions of and respectively,

The population local covariance, variance, correlation at any are defined as

| (1) | ||||

| (2) |

where we limit the domain of population local correlation to

for a small positive that is no larger than .

The domain of local correlation needs to be limited so the population version is well-behaved. For example, when is a constant or , equals and the corresponding local correlation is not well-defined. All subsequent analysis for the population local correlations is based on the domain , which is non-empty and compact as shown in Theorem 3. In practice, it suffices to set as any small positive number, see the sample version in Section 3. Also note that in either indicator function, the two random variables and the distribution are independent, e.g., at any realization of , the first indicator equals , and its expectation is taken with respect to .

The above definition makes use of the characteristic functions, which is akin to the original definition of Dcorr and easier to show consistency. Alternatively, the local covariance can be equivalently defined via the pairwise Euclidean distances. The alternative definition better motivates the sample version in Section 3, is often handy for understanding and proving theoretical properties, and suggests that local covariance is always a real number, which is not directly obvious from Equation 1.

Theorem 1.

Suppose are iid as , and define

The local covariance in Equation 1 can be equally defined as

| (3) |

which shows that local covariance, variance, correlation are always real numbers.

Each local covariance is essentially a local version of distance covariance that truncates large distances at each point in the support, where the neighborhood size is determined by . In particular, distance correlation equals the local correlation at the maximal scale, which will ensure the consistency of MGC.

Theorem 2.

At any , when and are independent. Moreover, at , . They also hold for the correlations by replacing all the by .

2.3 Population MGC and Optimal Scale

The population MGC can be naturally defined as the maximum local correlation within the domain, i.e.,

| (4) |

and the scale that attains the maximum is named the optimal scale

| (5) |

The next theorem states the continuity of the local covariance, variance, correlation, and thus the existence of population MGC.

Theorem 3.

Given two continuous random variables ,

- (a)

-

The local covariance is a continuous function with respect to , so is local variance in and local correlation in .

- (b)

-

The set is always non-empty unless either random variable is a constant.

- (c)

-

Excluding the trivial case in (b), the set is always non-empty and compact, so an optimal scale and exist.

Therefore, population MGC and the optimal scale exist, are distribution dependent, and may not be unique. Without loss of generality, the optimal scale is assumed unique for presentation purpose. The population MGC is always no smaller than Dcorr in magnitude, and equals if and only if independence, a property inherited from Dcorr.

Theorem 4.

When and are independent, ; when and are not independent, .

3 Sample Local Correlations

Sample Dcorr can be easily calculated via properly centering the Euclidean distance matrices, and is shown to converge to the population Dcorr [2, 4, 5]. Similarly, we show that the sample local correlation can be calculated via the Euclidean distance matrices upon truncating large distances for each sample observation, and the sample version converges to the respective population local correlation.

3.1 Definition

Given pairs of observations for , denote as the data matrix with each column representing one sample observation, and similarly . Let and be the Euclidean distance matrices of and respectively, i.e., . Then we compute two column-centered matrices and with the diagonals excluded, i.e., and are centered within each column such that

| (6) |

Next we define as the “rank” of relative to , that is, if is the closest point (or “neighbor”) to , as determined by ranking the set by ascending order. Similarly define for the ’s. As we assumed are continuous, with probability there is no repeating observation and the ranks always take value in . In practice ties may occur, and we recommend either using minimal rank to keep the ties or jittering to break the ties, which is discussed at the end of this section.

For any , we define the rank truncated matrices and as

Let denote the entry-wise product, denote the diagonal-excluded sample mean of a square matrix, then the sample local covariance, variance, and correlation are defined as:

If either local variance is smaller than a preset (e.g., the smallest positive local variance among all), then we set the corresponding instead. Note that once the rank is known, sample local correlations can be iteratively computed in rather than a naive implementation of . A detailed running time comparison is presented in Section 5.

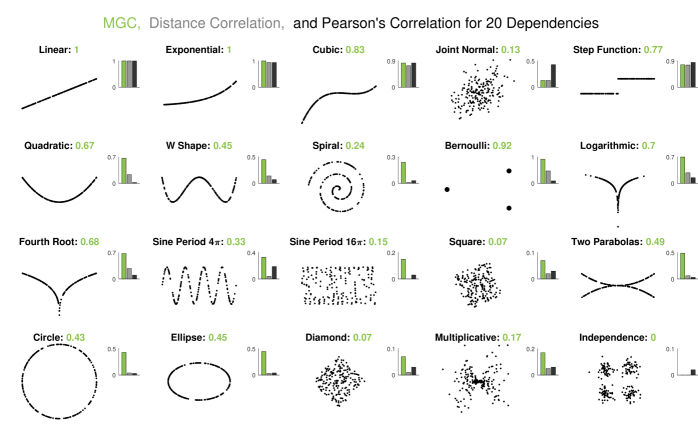

In case of ties, minimal rank offers a consecutive indexing of sample local correlations, e.g., if only takes two values, takes value in under minimal rank, but maximal rank yields . The sample local correlations are not affected by the tie scheme, but minimal rank is more convenient to work with for implementation purposes. Alternatively, one can break ties deterministically or randomly, e.g., apply jittering to break all ties. For example, in the Bernoulli relationship of Figure 1, there are only three points for computing sample local correlations and the Sample MGC equals . If white noise of variance were added to the data, we break all ties and obtain a much larger number of sample local correlations. The resulting Sample MGC is , which is slightly smaller but still much larger than and implies a strong dependency.

Whether the random variable is continuous or discrete, and whether the ties in sample data are broken or not, does not affect the theoretical results except in certain theorem statements. For example, in Theorem 5, the convergence still holds for discrete random variables, but the index pair does not necessarily correspond to the population version at , e.g., when is Bernoulli with probability and minimal rank is used, corresponds to instead of . Nevertheless, Theorem 5 and all results in the paper hold regardless of continuous or discrete random variables, but the presentation is more elegant for the continuous case.

3.2 Convergence Property

The sample local covariance, variance, correlation are designed to converge to the respective population versions. Moreover, the expectation of sample local covariance equals the population counterpart up to a difference of , and the variance diminishes at the rate of .

Theorem 5.

Suppose each column of and are generated iid from . The sample local covariance satisfies

where and . In particular, the convergence is uniform and also holds for the local correlation, i.e., for any there exists such that for all ,

for any pair of .

The convergence property ensures that Theorem 2 holds asymptotically for the sample version.

Corollary 1.

For any , when and are independent. In particular, .

3.3 Centering and Ranking

To combine distance testing with the locality principle, other than the procedure proposed in Equation 3, there are a number of alternative options to center and rank the distance matrices. For example, letting

still guarantees the resulting local correlation at maximal scale equals the distance correlation; and letting

makes the resulting local correlation at maximal scale equal the Mantel coefficient, the earliest distance-based correlation coefficient.

Nevertheless, the centering and ranking strategy proposed in Equation 3 is more faithful to k-nearest neighbor graph: the indicator equals if and only if , which happens with probability . Viewed another way, when conditioned on , the indicator equals if and only if , thus matching the column ranking scheme in Equation 6. Indeed, the locality principle used in [19, 20, 21] considers the k-nearest neighbors of each sample point in local computation, an essential step to yield better nonlinear embeddings.

On the centering side, the Mantel test appears to be an attractive option due to its simplicity in centering. All the Dcorr, Hhg, Hsic have their theoretical consistency, while the Mantel coefficient does not, despite it being merely a different centering of Dcorr. An investigation of the population form of Mantel yields some additional insights:

Definition.

Given and , the Mantel coefficient on sample data is computed as

where and are the pairwise Euclidean distance, and is the diagonal-excluded sample mean of a square matrix.

Corollary 2.

Suppose each column of and are iid as , and are also iid as . Then

where

Corollary 2 suggests that Mantel is actually a two-sided test based on the absolute difference of characteristic functions: under certain dependency structure, the Mantel coefficient can be negative and still imply dependency (i.e., ); whereas population Dcorr and MGC are always no smaller than , and any negativity of the sample version does not imply dependency. Therefore, Mantel is only appropriate as a two-sided test, which is evaluated in Section 5.

Another insight is that Mantel, unlike Dcorr, is not universally consistent: due to the integral , one can construct a joint distribution such that the population Mantel equals under dependence (see Remark 3.13 in [6] for an example of dependent random variables with uncorrelated distances). However, empirically, simple centering is still effective in a number of common dependencies (like two parabolas and diamond in Figure 3).

4 Sample MGC and Estimated Optimal Scale

A naive sample version of MGC can be defined as the maximum of all sample local correlations

Although the convergence to population MGC can be guaranteed, the sample maximum is a biased estimator of the population MGC in Equation 4. For example, under independence, population MGC equals , while the maximum sample local correlation has expectation larger than , which may negate the advantage of searching locally and hurt the testing power.

This motivates us to compute Sample MGC as a smoothed maximum within the largest connected region of thresholded local correlations. The purpose is to mitigate the bias of a direct maximum, while maintaining its advantage over Dcorr in the test statistic. The idea is that in case of dependence, local correlations on the grid near the optimal scale shall all have large correlations; while in case of independence, a few local correlations may happen to be large, but most nearby local correlations shall still be small. The idea can be similarly adapted whenever there are multiple correlated test statistics or multiple models available, for which taking a direct maximum may yield too much bias [23]. From another perspective, Sample MGC is like taking a regularized maximum.

4.1 Sample MGC

The procedure is as follows:

- Input:

-

A pair of datasets .

- Compute the Local Correlation Map:

-

Compute all local correlations:

. - Thresholding:

-

Pick a threshold , denote as the operation of taking the largest connected component, and compute the largest region of thresholded local correlations:

(7) Within the region , set

(8) (9) as the Sample MGC and the estimated optimal scale. If the number of elements in is less than , or the above thresholded maximum is no more than , we instead set and .

- Output:

-

Sample MGC and the estimated optimal scale .

If there are multiple largest regions, e.g., and where their number of elements are more than and coincide with each other, then it suffices to let and locate the MGC statistic within the union. The selection of at least elements for is an empirical choice, which balances the bias-variance trade-off well in practice. The parameter can be any positive integer without affecting the validity and consistency of the test. But if the parameter is too large, MGC tends to be more conservative and is unable to detect signals in strongly nonlinear relationships (e.g., trigonometric functions), and performs closer and closer to Dcorr; if the parameter is set to a very small fixed number, the bias is inflated so MGC tends to perform similarly as directly maximizing all local correlations.

4.2 Convergence and Consistency

The proposed Sample MGC is algorithmically enforced to be no less than the local correlation at the maximal scale, and also no more than the maximum local correlation. It also ensures in Theorem 4 to hold for the sample version.

Theorem 6.

Regardless of the threshold , the Sample MGC statistic satisfies

- (a)

-

It always holds that

- (b)

-

When and are independent, ; when and are not independent, a positive constant.

The next theorem states that if the threshold converges to , then whenever population MGC is larger than population Dcorr, Sample MGC is also larger than sample Dcorr asymptotically; otherwise if the threshold does not converge to , Sample MGC may equal sample Dcorr despite of the first moment advantage in population. Moreover, Sample MGC indeed converges to population MGC when the optimal scale is in the largest thresholded region . The empirical advantage of Sample MGC is illustrated in Figure 1.

Theorem 7.

Suppose each column of and are iid as continuous , and the threshold choice as .

- (a)

-

Assume that under the joint distribution. Then for sufficiently large.

- (b)

-

Assume there exists an element within the the largest connected area of with , such that the the local correlation of that element equals . Then .

Alternatively, Theorem 7(b) can be stated that the Sample MGC always converges to the maximal population local correlation within the largest connected area of thresholded local correlations. Therefore, Sample MGC converges either to Dcorr (when the area is empty) or something larger, thus improving over Dcorr statistic in first moment.

4.3 Choice of Threshold

The choice of threshold is imperative for Sample MGC to enjoy a good finite-sample performance, especially at small sample size. According to Theorem 7, the threshold shall converge to for Sample MGC to prevail sample Dcorr.

A model-free threshold was previously used in [22]: for the following set

let be the sum of all its elements squared, and set as the threshold; if there is no negative local correlation and the set is empty, use .

Although the previous threshold is a data-adaptive choice that works pretty well empirically and does not affect the consistency of Sample MGC in Theorem 8, it does not converge to . The following finite-sample theorem from [4] motivates an improved threshold choice here:

Theorem.

Under independence of , assume the dimensions of are exchangeable with finite variance, and so are the dimensions of . Then for any and , as increase the limiting distribution of equals the symmetric Beta distribution with shape parameter .

The above theorem leads to the new threshold choice:

Corollary 3.

Denote , , as the inverse cumulative distribution function. The threshold choice

converges to as .

The limiting null distribution of Dcorr is still a good approximation even when are not large, thus provides a reliable bound for eliminating local correlations that are larger than Dcorr by chance or by noise. The intuition is that Sample MGC is mostly useful when it is much larger than Dcorr in magnitude, which is often the case in non-monotone relationships as shown in Section 5 Figure 1. Alternatively, directly setting also guarantees the theoretical properties and works equally well when the sample size is moderately large.

4.4 Permutation Test

To test independence on a pair of sample data , the random permutation test has been the popular choice [25] for almost all methods introduced, as the null distribution of the test statistic can be easily approximated by randomly permuting one data set. We discuss the computation procedure, prove the testing consistency of MGC, and analyze the running time.

To compute the p-value of MGC from the permutation test, first compute the Sample MGC statistic on the observed data pair. Then the MGC statistic is repeatedly computed on the permuted data pair, e.g. is permuted into for a random permutation of size , and compute . The permutation procedure is repeated for times to estimate the probability , and the estimated probability is taken as the p-value of MGC. The independence hypothesis is rejected if the p-value is smaller than a pre-set critical level, say or . The following theorem states that MGC via the permutation test is consistent and valid.

Theorem 8.

Suppose each column of and are generated iid from . At any type error level , Sample MGC is a valid test statistic that is consistent against all possible alternatives under the permutation test.

4.5 Miscellaneous Properties

In this subsection, we first show a useful lemma expressing sample local covariance in Section 3.1 by matrix trace and eigenvalues, then list a number of fundamental and desirable properties for the local variance, local correlation, and MGC, akin to these of Pearson’s correlation and distance correlation as shown in [2, 3].

Lemma 1.

Denote as the matrix trace, as the th eigenvalue of a matrix, and as the matrix of ones of size . Then the sample covariance equals

Theorem 9 (Local Variances).

For any random variable , and any with each column iid as ,

- (a)

-

Population and sample local variances are always non-negative, i.e.,

at any and any .

- (b)

-

if and only if either or is a degenerate distribution;

if and only if either or is a degenerate distribution.

- (c)

-

For two constants , and an orthonormal matrix ,

Therefore, the local variances end up having properties similar to the distance variance in [2], except the distance variance definition there takes a square root.

Theorem 10 (Local Correlations and MGC).

For any pair of random variable , and any with each column iid as ,

- (a)

-

Symmetric and Boundedness:

at any and any .

- (b)

-

Assume is non-degenerate. Then at any , if and only if are dependent via an isometry for some non-zero constant .

Assume is non-degenerate. Then at any , if and only if are dependent via an isometry for some non-zero constant .

- (c)

-

Both population and Sample MGC are symmetric and bounded:

- (d)

-

Assume is non-degenerate. Then if and only if are dependent via an isometry for some non-zero constant .

Assume is non-degenerate. Then if and only if are dependent via an isometry for some non-zero constant .

The proof of Theorem 10(b)(d) also shows that the local correlations and MGC cannot be .

5 Experiments

In the experiments, we compare Sample MGC with Dcorr, Pearson, Mantel, Hsic, Hhg, and Copula test on different simulation settings based on a combination of simulations used in previous works [2, 26, 27]. Among the settings, the first are monotonic relationships (and several of them are linear or nearly so), the last simulation is an independent relationship, and the remaining settings consist of common non-monotonic and strongly nonlinear relationships. The exact distributions are shown in Appendix.

The Sample Statistics

Figure 1 shows the sample statistics of MGC, Dcorr, and Pearson for each of the simulations in a univariate setting. For each simulation, we generate sample data at and without any noise, then compute the sample statistics. From type , the test statistics for both MGC and Dcorr are remarkably greater than and almost identical to each other. For the nonlinear relationships (type ), MGC benefits from searching locally and achieves a larger test statistic than Dcorr’s, which can be very small in these nonlinear relationships. For type , the test statistics for both MGC and Dcorr are almost as expected. On the other hand, Pearson’s test statistic is large whenever there exists certain linear association, and almost otherwise. The comparison of sample statistics indicate that Dcorr may have inferior finite-sample testing power in nonlinear relationships, but a strong dependency signal is actually hidden in a local structure that MGC may recover.

Finite-Sample Testing Power

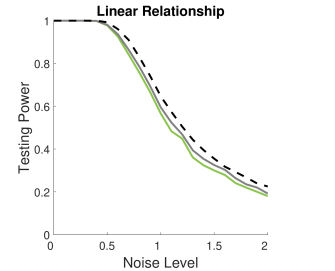

Figure 2 shows the finite-sample testing power of MGC, Dcorr, and Pearson for a linear and a quadratic relationship at and with white noise (controlled by a constant). The testing power of MGC is estimated as follows: we first generate dependent sample data for replicates, compute Sample MGC for each replicate to estimate the alternative distribution of MGC. Then we generate independent sample data using the same marginal distributions for replicates, compute Sample MGC to estimate the null distribution, and estimate the testing power at type error level . The testing power of Dcorr is estimated in the same manner, while the testing power of Pearson is directly computed via the t-test. MGC has the best power in the quadratic relationship, while being almost identical to Dcorr and Pearson in the linear relationship.

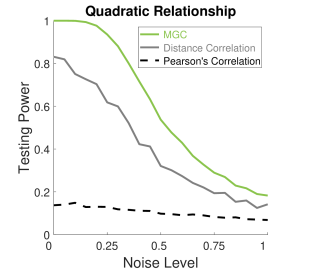

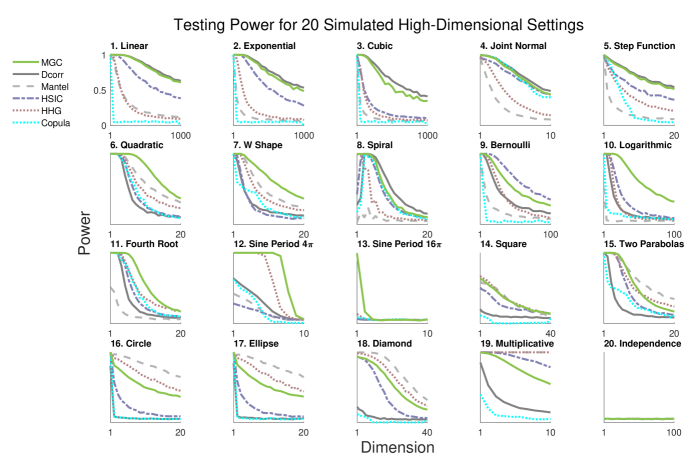

The same phenomenon holds throughout all the simulations we considered, i.e., MGC achieves almost the same power as Dcorr in monotonic relationships, while being able to improve the power in monotonic and strongly nonlinear relationships. The testing power of MGC versus all other methods are shown in Figure 3 for the univariate settings, and we plot the power versus the sample size from to for each simulation. Note that the noise level is tuned for each dependency for illustration purposes.

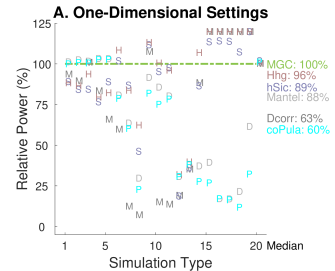

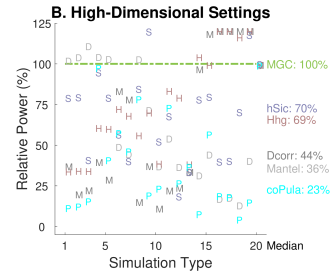

Figure 4 compares the testing performance for the same simulations with a fixed sample size and increasing dimensionality. The relative powers in the univariate and multivariate settings are then summarized in Figure 5. MGC is overall the most powerful method, followed by Hhg and Hsic. Since non-monotone relationships are prevalent among the settings, it is not a surprise that Dcorr is overall worse than Hhg and Hsic, both of which also excel at nonlinear relationships.

Note that the same simulations were also used in [22] for evaluation purposes. The main difference is that the Sample MGC algorithm is now based on the improved threshold with theoretical guarantee. Comparing to the previous algorithm, the new threshold slightly improves the testing power in monotonic relationships (the first simulations).

Running Time

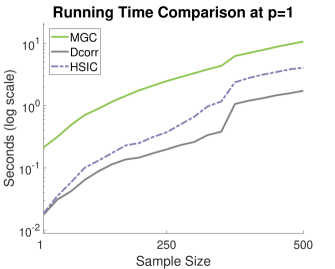

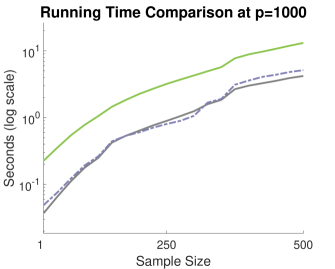

Sample MGC can be computed and tested in the same running time complexity as distance correlation: Assume is the maximum feature dimension of the two datasets, distance computation and centering takes , the ranking process takes , all local covariances and correlations can be incrementally computed in (the pseudo-code is shown in [22]), the thresholding step of Sample MGC takes as well. Overall, Sample MGC can be computed in . In comparison, the Hhg statistic requires the same complexity as MGC, while distance correlation saves on the term.

As the only part of MGC that has the additional term is the column-wise ranking process, a multi-core architecture can reduce the running time to . By making ( is no more than at billion samples), MGC effectively runs in and is of the same complexity as Dcorr. The permutation test multiplies another to all terms except the distance computation, so overall the MGC testing procedure requires , which is the same as Dcorr, Hhg, and Hsic. Figure 6 shows that MGC has approximately the same complexity as Dcorr, and is slower by a constant in the actual running time.

6 Conclusion

In this paper, we formalize the population version of local correlation and MGC, connect them to the sample counterparts, prove the convergence and almost unbiasedness from the sample version to the population version, as well as a number of desirable properties for a well-defined correlation measure. In particular, population MGC equals and the sample version converges to if and only if independence, making Sample MGC valid and consistent under the permutation test. Moreover, Sample MGC is designed in a computationally efficient manner, and the new threshold choice achieves both theoretical and empirical improvements. The numerical experiments confirm the empirical advantages of MGC in a wide range of linear, nonlinear, high-dimensional dependencies.

There are many potential future avenues to pursue. Theoretically, proving when and how one method dominates another in testing power is highly desirable. As the methods in comparison have distinct formulations and different properties, it is often difficult to compare them directly. However, a relative efficiency analysis may be viable when limited to methods of similar properties, such as Dcorr and Hsic, or local statistic and global statistic. In terms of the locality principle, the geometric meaning of the local scale in MGC is intriguing — for example, does the family of local correlations fully characterize the joint distribution, and what is the relationship between the optimal local scale and the dependency geometry — answering these questions may lead to further improvement of MGC, and potentially make the family of local correlations a valuable tool beyond testing.

Method-wise, there are a number of alternative implementations that may be pursued. For example, the sample local correlations can be defined via ball instead of nearest neighbor graphs, i.e., truncate large distances based on absolute magnitude instead of the nearest neighbor graph. The maximization and thresholding mechanism may be further improved, e.g., thresholding based on the covariance instead of correlation, or design a better regularization scheme. There are many alternative approaches that can maintain consistency in this framework, and it will be interesting to investigate a better algorithm. In particular, we name our method as “multiscale graph correlation” because the local correlations are computed via the k-nearest neighbor graphs, which is one way to generalize the distance correlation.

Application-wise, the MGC method can directly facilitate new discoveries in many kinds of scientific fields, especially data of limited sample size and high-dimensionality such as in neuroscience and omics [22]. Within the domain of statistics and machine learning, MGC can be a very competitive candidate in any methodology that requires a well-defined dependency measure, e.g., variable selection [28], time series [29], etc. Moreover, the very idea of locality may improve other types of distance-based tests, such as the energy distance for K-sample testing [30].

References

- [1] K. Pearson, “Notes on regression and inheritance in the case of two parents,” Proceedings of the Royal Society of London, vol. 58, pp. 240–242, 1895.

- [2] G. Szekely, M. Rizzo, and N. Bakirov, “Measuring and testing independence by correlation of distances,” Annals of Statistics, vol. 35, no. 6, pp. 2769–2794, 2007.

- [3] G. Szekely and M. Rizzo, “Brownian distance covariance,” Annals of Applied Statistics, vol. 3, no. 4, pp. 1233–1303, 2009.

- [4] G. Szekely and M. Rizzo, “The distance correlation t-test of independence in high dimension,” Journal of Multivariate Analysis, vol. 117, pp. 193–213, 2013.

- [5] G. Szekely and M. Rizzo, “Partial distance correlation with methods for dissimilarities,” Annals of Statistics, vol. 42, no. 6, pp. 2382–2412, 2014.

- [6] R. Lyons, “Distance covariance in metric spaces,” Annals of Probability, vol. 41, no. 5, pp. 3284–3305, 2013.

- [7] N. Mantel, “The detection of disease clustering and a generalized regression approach,” Cancer Research, vol. 27, no. 2, pp. 209–220, 1967.

- [8] J. Josse and S. Holmes, “Measures of dependence between random vectors and tests of independence,” arXiv, 2013.

- [9] A. Gretton, R. Herbrich, A. Smola, O. Bousquet, and B. Scholkopf, “Kernel methods for measuring independence,” Journal of Machine Learning Research, vol. 6, pp. 2075–2129, 2005.

- [10] A. Gretton and L. Gyorfi, “Consistent nonparametric tests of independence,” Journal of Machine Learning Research, vol. 11, pp. 1391–1423, 2010.

- [11] D. Sejdinovic, B. Sriperumbudur, A. Gretton, and K. Fukumizu, “Equivalence of distance-based and rkhs-based statistics in hypothesis testing,” Annals of Statistics, vol. 41, no. 5, pp. 2263–2291, 2013.

- [12] R. Heller, Y. Heller, and M. Gorfine, “A consistent multivariate test of association based on ranks of distances,” Biometrika, vol. 100, no. 2, pp. 503–510, 2013.

- [13] R. Heller, Y. Heller, S. Kaufman, B. Brill, and M. Gorfine, “Consistent distribution-free -sample and independence tests for univariate random variables,” Journal of Machine Learning Research, vol. 17, no. 29, pp. 1–54, 2016.

- [14] C. Genest, J.-F. Quessy, and B. Rémillard, “Local efficiency of a cramer-von mises test of independence,” Journal of Multivariate Analysis, vol. 97, pp. 274–294, 2006.

- [15] C. Genest, J.-F. Quessy, and B. Rémillard, “Asymptotic local efficiency of cramer-von mises tests for multivariate independence,” The Annals of Statistics, vol. 35, pp. 166–191, 2007.

- [16] I. Kojadinovic and M. Holmes, “Tests of independence among continuous random vectors based on cramér-von mises functionals of the empirical copula process,” Journal of Multivariate Analysis, vol. 100, pp. 1137–1154, 2009.

- [17] A. Dionísio, R. Menezes, and D. A. Mendes, “Entropy-based independence test,” Nonlinear Dynamics, vol. 44, p. 351–357, 2006.

- [18] D. Reshef, Y. Reshef, H. Finucane, S. Grossman, G. McVean, P. Turnbaugh, E. Lander, M. Mitzenmacher, and P. Sabeti, “Detecting novel associations in large data sets,” Science, vol. 334, no. 6062, pp. 1518–1524, 2011.

- [19] J. B. Tenenbaum, V. de Silva, and J. C. Langford, “A global geometric framework for nonlinear dimension reduction,” Science, vol. 290, pp. 2319–2323, 2000.

- [20] L. K. Saul and S. T. Roweis, “Nonlinear dimensionality reduction by locally linear embedding,” Science, vol. 290, pp. 2323–2326, 2000.

- [21] M. Belkin and P. Niyogi, “Laplacian eigenmaps for dimensionality reduction and data representation,” Neural Computation, vol. 15, no. 6, pp. 1373–1396, 2003.

- [22] C. Shen, E. Bridgeford, Q. Wang, C. E. Priebe, M. Maggioni, and J. T. Vogelstein, “Discovering and deciphering relationships across disparate data modalities,” https://arxiv.org/abs/1609.05148, 2018.

- [23] Y. Lee, C. Shen, C. E. Priebe, and J. T. Vogelstein, “Network dependence testing via diffusion maps and distance-based correlations,” https://arxiv.org/abs/1703.10136, 2018.

- [24] S. Wang, C. Shen, A. Badea, C. E. Priebe, and J. T. Vogelstein, “Signal subgraph estimation via vertex screening,” https://arxiv.org/abs/1801.07683, 2018.

- [25] P. Good, Permutation, Parametric, and Bootstrap Tests of Hypotheses. Springer, 2005.

- [26] N. Simon and R. Tibshirani, “Comment on “detecting novel associations in large data sets”,” arXiv, 2012.

- [27] M. Gorfine, R. Heller, and Y. Heller, “Comment on “detecting novel associations in large data sets”,” Technical Report, 2012.

- [28] R. Li, W. Zhong, and L. Zhu, “Feature screening via distance correlation learning,” Journal of American Statistical Association, vol. 107, pp. 1129–1139, 2012.

- [29] Z. Zhou, “Measuring nonlinear dependence in time‐series, a distance correlation approach,” Journal of Time Series Analysis, vol. 33, no. 3, pp. 438–457, 2012.

- [30] G. Szekely and M. Rizzo, “Energy statistics: A class of statistics based on distances,” Journal of Statistical Planning and Inference, vol. 143, no. 8, pp. 1249–1272, 2013.

- [31] V. Koroljuk and Y. Borovskich, Theory of U-Statistics. Springer, 1994.

Acknowledgment

This work was partially supported by the National Science Foundation award DMS-1712947, and the Defense Advanced Research Projects Agency’s (DARPA) SIMPLEX program through SPAWAR contract N66001-15-C-4041. The authors are grateful to the anonymous reviewers for the invaluable feedback leading to significant improvement of the manuscript, and thank Dr. Minh Tang and Dr. Shangsi Wang for useful discussions and suggestions.

APPENDIX

Appendix A Proofs

Theorem 1

Proof.

Equation 1 defines the local covariance as

Expanding the first integral term yields

Every other step being routine, the third equality transforms the integral to Euclidean distances via the same technique employed in Remark 1 and the proof of Theorem 8 in [3]. Also note that all four expectations are finite. For example, the first expectation in the third equality is finite, because is always non-negative, and is non-negative and finite by the finite second moments assumption on and , such that

which can be similarly established for the other three expectations.

The second integral term can be decomposed into

because the first expectation only has and the second expectation only has , and is a product of and . Then

where the two expectations involved are also finite. Similarly . Thus

Theorem 2

Proof.

When and are independent,

thus at any . So is the local correlation at any .

To show the local covariance at the maximal scale equals the distance covariance, we proceed via the alternative definition in Theorem 1:

where the first equality follows by noting that at , the second equality holds by switching the random variable notations within each expectation, and the last equality is the alternative definition of distance covariance in Theorem 8 of [3]. It follows that , , and .

∎

Theorem 3

Proof.

Given two continuous random variables , we first illustrate the continuity of local covariance with respect to at fixed : For any with the understanding that , we have

where the expectation is taken with respect to all random variables inside, and

Then Cauchy-Schwarz and finite second moment of yield that

Moreover, the finite second moment of guarantees finiteness of and

which leads to the continuity of local covariance with respect to :

The same holds for fixed such that

Applying the above yields that

So the local covariance is continuous with respect to . The continuity of the local variance can be shown similarly, and it follows that the local correlation is continuous in .

At , with equality if and only if is a constant, and is empty in the trivial case. Otherwise by the continuity of local variance, for any there exists such that for all , . Same for , thus is non-empty except when either random variable is a constant. It follows that the local correlation is continuous within the non-empty and compact domain , and extreme value theorem ensures the existence of population MGC and the optimal scale. ∎

Theorem 4

Proof.

Theorem 5

Proof.

We prove this theorem by three steps: (i), the expectation of the sample local covariance is shown to equal the population local covariance; (ii), the variance of the sample statistic is of ; (iii), sample local covariance is shown to convergence to the population counterpart uniformly. Then the convergence trivially extends to the sample local variance and correlation.

(i): Expanding the first and second term of population local covariance in Equation 3, we have with

and with

All the ’s are bounded due to the finite first moment assumption on . Note that for distance covariance, one can go through the same proof with only three terms – – while the local version involves eight terms, due to the additional random variables for local scales.

For the sample local covariance, the expectation of the first term can be expanded as

The expectation of the second term can be similarly expanded as

Combining the results yields that .

(ii): The variance of sample local covariance is computed as

The last equality follows because: there are covariance terms in the numerator of , because are only related via the column centering when does not equal ; and there remains covariance terms of at most . Note that the finite second moment assumption of is required for the big notation to have a bounding constant. Therefore, the variance of sample local covariance is of .

(iii): converges to the population local covariance by applying the strong law of large numbers on U-statistics [31]. Namely, the first term of sample local covariance satisfies

where the second line applies law of large numbers at each by conditioning on for each ’s, and the last line follows by applying law of large numbers to the independently distributed conditioned ’s. Similarly, the second term of sample local covariance can be shown to converge to the second term in population local covariance. The convergence is also uniform: each local covariance are dependent with each other, and actually repeats the summands with each other. Thus there exists a scale such that has the largest deviation from the mean than all other local covariances, and one can find a suitable to bound the maximum deviation for all .

Alternatively, convergence in probability can be directly established from (i) and (ii) by applying the Chebyshev’s inequality; the almost sure convergence can also be proved via the integral definition using almost the same steps as in Theorems 1 and 2 from [2], i.e., first define the empirical characteristic function via the integral for the sample local covariance, and show it converges to the population local covariance in Equation 1 by the law of large numbers on U-statistics. ∎

Corollary 1

Corollary 2

Proof.

The population Mantel and its equivalence to expectation of Euclidean distances can be established via the same steps as in Theorem 1. The convergence of sample Mantel to its population version can be derived based on either the same procedure in Theorem 5, or Theorems 1 and 2 from [2] with minimal notational changes. ∎

Theorem 6

Proof.

(a): Regardless of the threshold choice, the algorithm enforces Sample MGC to be always no less than , and no more than .

Theorem 7

Proof.

(a): Given , by the continuity of local correlations with respect to , there always exists a non-empty connected area such that for all . Among all possible areas we take the one with largest area.

As increases to infinity, the set is a dense subset of , and is also a dense subset of . Thus for sufficiently large, the area can always be approximated via the largest connected component by the Sample MGC algorithm. As all sample local correlations within the region are larger than the sample distance correlation, so is the smoothed maximum. Note that if the threshold does not converge to , e.g., if is a positive constant like , Sample MGC will fail to identify a region when .

(b): Following (a), if optimal scale of MGC is in the largest area , the sample maximum within converges to the true maximum within , i.e., Sample MGC converges to the population MGC. ∎

Corollary 3

Proof.

For , , the convergence of can be shown as follows: by computing the variance of the Beta distribution and using Chebyschev’s inequality, it follows that

The equation also implies that the percentile choice can be either fixed or anything no larger than for some constant , beyond which the convergence of to will be broken. ∎

Theorem 8

Proof.

To prove consistency under the permutation test, it suffices to show that at any type error level , the p-value of MGC is asymptotically less than . The p-value can be expressed by:

by conditioning on the permutation being a partial derangement of size , e.g., means is a derangement, while means does not permute any position.

As , we always have

Thus it suffices to show that for any ,

| (10) |

Then we decompose the above summations into two different cases. The first case is when is a fixed size, and are asymptotically independent (due to the iid assumption), thus converges to . The other case is the remaining partial derangements of size , but these partial derangements occur with probability converging to , i.e., for any , there exists such that

as is bounded above and converges to . Then back to the first case, there further exists such that for any and all

It follows that for all ,

Thus the convergence in Equation 10 holds.

Therefore, at any type error level , the p-value of Sample MGC under the permutation test will eventually be less than as increases, such that Sample MGC always successfully detects any dependency. Thus Sample MGC is consistent against all dependencies with finite second moments.

When and are independent, each column of and the corresponding column of are independent for any permutation. Therefore, distributes the same as for any random permutation , and is uniformly distributed in . Thus Sample MGC is valid. ∎

Lemma 1

Proof.

where the first line is the definition, the second line follows by noting that and for any two matrices and , and the last two lines follow from basic properties of matrix trace. ∎

Theorem 9

Proof.

For all these properties, it suffices to prove them on the sample local variance first. Then the population version follows by the convergence property in Theorem 5.

(a): Based on Lemma 1 it holds that

(b): Following part (a), we have

where the last line follows by observing that by Equation 6. Therefore, distance variance equals if and only if is the zero matrix.

A trivial case is , which corresponds to asymptotically. Otherwise is a zero matrix if and only if for all satisfying ,

Namely, for each point , its smallest distance entries all equal the mean distances with respect to , which can only happen when is a constant for all at a fixed . Due to the symmetry of the distance matrix, all the off-diagonal entries of are the same, i.e., for some constant .

When , all observations are the same, so is a constant. Otherwise all observations are equally distanced from each other by a distance of , which occurs with probability under the iid assumption. This is because when and are independent, one cannot have almost surely unless they are degenerate.

From another point of view, for given sample data that happens to be equally distanced, e.g., points in dimensions, sample variances can still be . But this scenario occurs with probability when each observation is assumed iid.

(c): This follows trivially from the definition, because upon the transformation the distance matrix is unchanged up-to a factor of . ∎

Theorem 10

Proof.

Similar as in Theorem 9, it suffices to prove (a) and (b) for the sample local correlation, then they automatically hold for the population version by convergence.

(a): The symmetric part is trivial: for any , by Lemma 1

Then by the Cauchy-Schwarz inequality on the trace,

Thus .

(b): The if direction is clear: under isometry, , both share the same k-nearest-neighbor graph, so that . Thus , and . For the only if direction: by part (a), the local correlation can be if and only if is a scalar multiple of , say some constant .

First we argue that the non-zero entries in must match the non-zero entries in . Namely, the k-nearest neighbor graph is the same between and . As , must be a scalar multiple of . Then if there exists such that while , must be the same scalar multiple of , which is not possible unless . Thus and for all .

Next we show the scalar multiple must be positive, i.e., the local correlation cannot be . Assuming it can be , then

where the second to last line follows because the diagonal entries of are by definition, and the last line follows by observing that and are both negative unless (e.g., is always centered to have zero matrix mean, while keeps the smallest entries per column so its matrix mean is negative til ). However, if the last line is true, then the original distance correlation shall be , which cannot happen under the iid assumption as shown in [2]. Note that the derivation also shows that the local correlations can be for general dissimilarity matrices without the iid assumption, i.e., when for some constant .

Therefore, the scalar multiple must be positive, and . As the diagonals satisfy , it holds that and . Thus for each satisfying :

We argue that if for each satisfying , it also holds for all . Suppose there exists with and for some . Without loss of generality, there must exist one more index such that and to maintain the mean (or multiple indices in a similar manner). This requires , so and are related by when conditioning on . Thus it imposes a dependency structure and violates the iid assumption.

Therefore . When , is equivalent to that ) are related by an isometry. When , it requires each distance entries to be added by the same constant, which occurs with probability under the iid assumption. Namely, if almost surely, then and are related by when conditioning on , in which case these two pairs become dependent and the iid assumption is violated.

(c): As each local correlation is symmetric and bounded for either population or sample case, MGC is symmetric and within by part (a).

(d): If and are related by an isometry, the distance correlation (or the local correlation at the largest scale) equals . For population, MGC takes the maximum local correlation; for sample, MGC cannot be smaller than the local correlation at the largest scale. In both cases population and Sample MGC equal .

When population or Sample MGC equal , there exists at least one local correlation that equals , i.e., . From the inequality in part (a), must equal for the equality to hold. Otherwise the number of non-zero entries does not match between and , and cannot be a scalar multiple of . Thus there exists such that , and the conclusion follows from part (b). ∎

Appendix B Simulation Dependence Functions

This section presents the simulations used in the experiment section, which is mostly based on a combination of simulations from previous works [2, 26, 27]. We only made changes to add noise and a weight vector for higher dimensions, thereby making them more difficult and easier to compare all methods throughout different dimensions and sample sizes.

For the random variable , we denote as the dimension of . For the purpose of high-dimensional simulations, is a decaying vector with for each , such that is a weighted summation of all dimensions of . Furthermore, denotes the uniform distribution on the interval , denotes the Bernoulli distribution with probability , denotes the normal distribution with mean and covariance , and represent some auxiliary random variables, is a scalar constant to control the noise level (which equals for one-dimensional simulations and otherwise), and is sampled from an independent standard normal distribution unless mentioned otherwise.

-

1.

Linear :

-

2.

Exponential :

-

3.

Cubic :

-

4.

Joint normal : Let , be the identity matrix of size , be the matrix of ones of size , and . Then

-

5.

Step Function :

where is the indicator function, that is is unity whenever true, and zero otherwise.

-

6.

Quadratic :

-

7.

W Shape : ,

-

8.

Spiral : , ,

-

9.

Uncorrelated Bernoulli : , , ,

-

10.

Logarithmic :

-

11.

Fourth Root :

-

12.

Sine Period : , , ,

-

13.

Sine Period : Same as above except and the noise on is changed to .

-

14.

Square : Let , , , . Then

for .

-

15.

Two Parabolas : , ,

-

16.

Circle : , , ,

-

17.

Ellipse : Same as above except .

-

18.

Diamond : Same as “Square” except .

-

19.

Multiplicative Noise : ,

-

20.

Multimodal Independence : Let , , , . Then

For the increasing dimension simulations in the main paper, we always set and , with increasing. For types , such that increases as well; otherwise . The decaying vector is utilized for to make the high-dimensional relationships more difficult (otherwise, additional dimensions only add more signal). For the one-dimensional simulations, we always set , and .