Generalized High-Dimensional Trace Regression via Nuclear Norm Regularization***This paper is supported by NSF grants DMS-1406266, DMS-1662139, and DMS-1712591

Abstract

We study the generalized trace regression with a near low-rank regression coefficient matrix, which extends notion of sparsity for regression coefficient vectors. Specifically, given a matrix covariate , the probability density function , where . This model accommodates various types of responses and embraces many important problem setups such as reduced-rank regression, matrix regression that accommodates a panel of regressors, matrix completion, among others. We estimate through minimizing empirical negative log-likelihood plus nuclear norm penalty. We first establish a general theory and then for each specific problem, we derive explicitly the statistical rate of the proposed estimator. They all match the minimax rates in the linear trace regression up to logarithmic factors. Numerical studies confirm the rates we established and demonstrate the advantage of generalized trace regression over linear trace regression when the response is dichotomous. We also show the benefit of incorporating nuclear norm regularization in dynamic stock return prediction and in image classification.

1 Introduction

In modern data analytics, the parameters of interest often exhibit high ambient dimensions but low intrinsic dimensions that can be exploited to circumvent the curse of dimensionality. One of the most illustrating examples is the sparse signal recovery through incorporating sparsity regularization into empirical risk minimization (Tibshirani (1996); Chen et al. (2001); Fan and Li (2001)). As shown in the profound works (Candes and Tao (2007); Fan and Lv (2008, 2011); Zou and Li (2008); Zhang et al. (2010), among others), the statistical rate of the appropriately regularized M-estimator has mere logarithmic dependence on the ambient dimension . This implies that consistent signal recovery is feasible even when grows exponentially with respect to the sample size . In econometrics, sparse models and methods have also been intensively studied and are proven to be powerful. For example, Belloni et al. (2012) studied estimation of optimal instruments under sparse high-dimensional models and showed that the instrumental variable (IV) estimator based on Lasso and post-Lasso methods enjoys root-n consistency and asymptotic normality. Hansen and Kozbur (2014) and Caner and Fan (2015) investigated instrument selection using high-dimensional regularization methods. Kock and Callot (2015) established oracle inequalities for high dimensional vector autoregressions and Chan et al. (2015) applied group Lasso in threshold autoregressive models and established near-optimal rates in the estimation of threshold parameters. Belloni et al. (2017) employed high-dimensional techniques for program evaluation and causal inference.

When the parameter of interest arises in the matrix form, elementwise sparsity is not the sole way of constraining model complexity; another structure that is exclusive to matrices comes into play: the rank. Low-rank matrices have much fewer degrees of freedom than its ambient dimensions . To determine a rank- matrix , we only need left and right singular vectors and singular values, which correspond to degrees of freedom, without accounting the orthogonality. As a novel regularization approach, low-rankness motivates matrix representations of the parameters of interest in various statistical and econometric models. If we rearrange the coefficient in the traditional linear model as a matrix, we obtain the so-called trace regression model:

| (1.1) |

where denotes the trace, is a matrix of explanatory variables, is the matrix of regression coefficients, is the response and is the noise. In predictive econometric applications, can be a large panel of time series data such as stock returns or macroeconomic variables (Stock and Watson, 2002; Ludvigson and Ng, 2009), whereas in statistical machine learning can be images. The rank of a matrix is controlled by the -norm for of its singular values:

| (1.2) |

where is the th largest singular value of , and is a positive constant that can grow to infinity. Note that when , it controls the rank of at . Trace regression is a natural model for matrix-type covariates, such as the panel data, images, genomics microarrays, etc. In addition, particular forms of can reduce trace regression to several well-known problem setups. For example, when contains only a column and the response is multivariate, (1.1) becomes reduced-rank regression model (Anderson (1951), Izenman (1975b)). When is a singleton in the sense that all entries of are zeros except for one entry that equals one, (1.1) characterizes the matrix completion problem in item response problems and online recommendation systems. We will specify these problems later.

To explore the low rank structure of in (1.1), a natural approach is the penalized least-squares with the nuclear norm penalty. Specifically, consider the following optimization problem.

| (1.3) |

where is the nuclear norm of . As -norm regularization yields sparse estimators, nuclear norm regularization enforces the solution to have sparse singular values, in other words, to be low-rank. Recent literatures have rigorously studied the statistical properties of . Negahban and Wainwright (2011) and Koltchinskii et al. (2011) derived the statistical error rate of when is sub-Gaussian. Fan et al. (2016) introduced a shrinkage principle to handle heavy-tailed noise and achieved the same statistical error rate as Negahban and Wainwright (2011) when the noise has merely bounded second moments.

However, (1.1) does not accomodate categorical responses, which is ubiquitous in pragmatic settings. For example, in P2P microfinance, platforms like Kiva seek potential pairs of lenders and borrowers to create loans. The analysis is based on a large binary matrix with the rows correspondent to the lenders and columns correspondent to the borrowers. Entry of the matrix is either checked, meaning that lender endorses an loan to borrower , or missing, meaning that lender is not interested in borrower or has not seen the request of borrower . The specific amount of the loan is inaccessible due to privacy concern, thus leading to the binary nature of the response (Lee et al. (2014)). Another example is the famous Netflix Challenge. There, people are given a large rating matrix with the rows representing the customers and the columns representing the movies. Most of its entries are missing and the aim is to infer these missing ratings based on the observed ones. Since the Netflix adopts a five-star movie rating system, the response is categorical with only five levels. This kind of matrix completion problems for item response arise also frequently in other economic surveys, similar to the aforementioned P2P microfinance. These problem setups with categorical responses motivate us to consider the generalized trace regression model.

Suppose that the response follows a distribution from the following exponential family:

| (1.4) |

where is the linear predictor, is a constant and and are known functions. The negative log-likelihood corresponding to (1.4) is given, up to an affine transformation, by

| (1.5) |

and the gradient and Hessian of are respectively

| (1.6) |

To estimate , we recruit the following M-estimator that minimizes the negative log-likelihood plus nuclear norm penalty.

| (1.7) |

This is a high-dimensional convex optimization problem. We will discuss the algorithms for computing (1.7) in the simulation section.

Related to our work is the matrix completion problem with binary entry, i.e., 1-bit matrix completion, which is a specific example of our generalized trace regression and has direct application in predicting aforementioned P2P microfinance. Therein entry of the matrix is modeled as a response from a logistic regression or probit regression with parameter and information of each responded items is related through the low-rank assumption of . Previous works studied the estimation of by minimizing the negative log-likelihood function under the constraint of max-norm (Cai and Zhou (2013)), nuclear norm (Davenport et al. (2014)) and rank (Bhaskar and Javanmard (2015)). There are also some works in 1-bit compressed sensing to recover sparse signal vectors (Gupta et al., 2010; Plan and Vershynin, 2013a, b). Nevertheless, we did not find any work in the generality that we are dealing with, which fits matrix-type explanatory variables and various types of dependent variables.

In this paper, we establish a unified framework for statistical analysis of in (1.7) under the generalized trace regression model. As showcases of the applications of our general theory, we focus on three problem setups: generalized matrix regression, reduced-rank regression and one-bit matrix completion. We explicitly derive statistical rate of under these three problem setups respectively. It is worth noting that for one-bit matrix completion, our statistical rate is sharper than that in Davenport et al. (2014). We also conduct numerical experiments on both simulated and real data to verify the established rate and illustrate the advantage of using the generalized trace regression over the vanilla trace regression when categorical responses occur.

The paper is organized as follows. In Section 2, we specify the problem setups and present the statistical rates of under generalized matrix regression, reduced-rank regression and one-bit matrix completion respectively. In Section 3, we present simulation results to back up our theoretical results from Section 2 and to demonstrate superiority of generalized trace regression over the standard one. In Section 4, we use real data to display the improvement brought by nuclear norm regularization in return prediction and image classification.

2 Main Results

2.1 Notation

We use regular letters for random variables, bold lower case letters for random vectors and bold upper case letter for matrices. For a function , we use , and to denote its first, second and third order derivative. For sequences and , we say if there exists a constant such that for , and we say if there exists a constant such that for . For a random variable , we denote its sub-Gaussian norm as and its sub-exponential norm as . For a random vector , we denote its sub-Gaussian norm as and its sub-exponential norm as . We use to denote a vector whose elements are all 0 except that the th one is 1. For a matrix , we use to represent the vector that consists of all the elements from column by column. We use , , , to denote the rank, elementwise max norm, operator norm and nuclear norm of respectively. We call a -ball centered at with radius r for . Define and . For matrices and , let . For any subspace , define its orthogonal space .

2.2 General Theory

In this section, we provide a general theorem on the statistical rate of in (1.7). As we shall see, the statistical consistency of essentially requires two conditions: i) sufficient penalization ; ii) localized restricted strong convexity of around . In high-dimensional statistics, it is well known that the restricted strong convexity (RSC) of the loss function underpins the statistical rate of the M-estimator (Negahban et al., 2011; Raskutti et al., 2010). In generalized trace regression, however, the fact that the Hessian matrix depends on creates technical difficulty for verifying RSC for the loss function. To address this issue, we apply the localized analysis due to Fan et al. (2015), where they only require local RSC (LRSC) of around to derive statistical rates of . Below we formulate the concept of LRSC. For simplicity, from now on we assume that is a -by- square matrix. We can easily extend our analysis to the case of rectangular ; the only change in the result is a replacement of with in the statistical rate.

Definition 1.

Given a constraint set , a local neighborhood of , a positive constants and a tolerance term , we say that the loss function satisfies LRSC if for all and ,

| (2.1) |

Note that is a tolerance term that will be specified in the main theorem. Now we introduce the constraint set in our context. Let be the SVD of , where the diagonals of are in the decreasing order. Denote the first columns of and by and respectively, and define

| (2.2) | ||||

where and denote the column space and row space respectively. For any and Hilbert space , let be the projection of onto . We first clarify here what , and are. Write as

then the following equalities hold:

| (2.3) |

According to Negahban et al. (2012), when , regardless of what is, falls in the following cone:

Now we present the main theorem that serves as a roadmap to establish the statistical rate of convergence for .

Theorem 1.

Suppose and

| (2.4) |

Define for some constant and let for some constant . Suppose satisfies LRSC, where and are constructed as per (2.2) and is a positive constant. Then it holds that

| (2.5) |

where are constants.

Theorem 1 points out two conditions that lead to the statistical rate of . First, we need to be sufficiently large, which has an adverse impact on the rates. Therefore, the optimal choice of is the lower bound given in (2.4). The second requirement is LRSC of around . In the sequel, for each problem setup we will first derive the rate of the lower bound of as shown in (2.4) and then verify LRSC of so that we can establish the statistical rate.

For notational convenience, later on when we refer to certain quantities as constants, we mean they are independent of . In the next subsections, we will apply the general theorem to analyze various specific problem setups and derive the explicit rates of convergence.

2.3 Generalized Matrix Regression

Generalized matrix regression can be regarded as a generalized linear model (GLM) with matrix covariates. Here we assume that , the vectorized version of , is a sub-Gaussian random vector with bounded -norm. Consider as defined in (1.7). To derive statistical rate of , we first establish the rate of the lower bound of as characterized in (2.4).

Lemma 1.

Consider the following conditions:

-

(C1)

are i.i.d. sub-Gaussian vectors with ;

-

(C2)

for any ;

Then for any , there exists a constant such that as long as , it holds that

| (2.6) |

where and are constants.

Next we verify the LRSC of .

Lemma 2.

Remark 1.

Condition (C4) is mild and is satisfied if there are at least elements of that are . Condition (C5) requires that the third order derivative of decays sufficiently fast. In fact, except for Poisson regression, most members in the family of generalized linear models satisfy this condition, e.g., linear model, logistic regression, log-linear model, etc.

Based on the above two lemmas, we apply Theorem 1 and establish the explicit statistical rate of as follows.

Theorem 2.

When , becomes the rank of and there are free parameters. Each of these parameters can be estimated at rate . Therefore, the sum of squared errors should at least be . This is indeed the bound of given by (2.7), which depends on the effective dimension rather than the ambient dimension . The second result of (2.7) confirms this in the spectral “-norm”, the nuclear norm.

2.4 Generalized Reduced-Rank Regression

Consider the conventional reduced-rank regression model (RRR)

where is the covariate, is the response, is a near low-rank coefficient matrix and is the noise. Again, we set the number of covariates to be the same as the number of responses purely for simplicity of the presentation. Note that in each sample there are responses correspondent to the same covariate vector. RRR aims to reduce the number of regression parameters in multivariate analysis. It was first studied in detail by Anderson (1951), where the author considered multi-response regression with linear constraints on the coefficient matrix and applied this model to obtain points estimation and confidence regions in “shock models” in econometrics (Marshak (1950)). Since then, there has been great amount of literature on RRR in econometrics (Ahn and Reinsel (1994), Geweke (1996), Kleibergen and Paap (2006)) and statistics (Izenman (1975a), Velu and Reinsel (2013), Chen et al. (2013)).

Now we generalize the above reduced-rank regression to accommodate various types of dependent variables. For any and , is generated from the following density function.

| (2.8) |

where is the th row of , , and are known functions. We further assume that for any , . Note that we can recast this model as a generalized trace regression with samples: . We emphasize here that throughout this paper we will use and to denote the vector and matrix forms of the th sample in RRR.

According to model (2.8), we solve for the nuclear norm regularized M-estimator as follows.

| (2.9) | |||||

Under the sub-Gaussian design, we are able to derive the covergence rate of in RRR with the same tool as what we used in matrix regression. Again, we explicitly derive the rate of the lower bound of in the following lemma.

Lemma 3.

Suppose the following conditions hold:

-

(C1)

are i.i.d sub-Gaussian vectors with ;

-

(C2)

, .

Then for any , there exists a constant such that as long as , it holds that

| (2.10) |

where is the same as in (2.8) and is a constant.

The following lemma establishes the LRSC of the loss function.

Lemma 4.

Combining to the above lemmas with Theorem 1, we can derive the statistical rate of as defined in (2.9).

Theorem 3.

Again, as remarked at the end of Section 2.3, the error depends on the effective dimension rather than the ambient dimension for the case .

2.5 One-Bit Matrix Completion

Another important example of the generalized trace regression is the one-bit matrix completion problem, which appears frequently in the online item response questionnaire and recommendation system. The showcase example is the aforementioned Kiva platform in P2P microfinance, in which we only observe sparse binary entries of lenders and borrowers. Suppose that we have users that answer a small fraction of binary questions. For simplicity of presentation, we again assume that . Specifically, consider the following logistic regression model with . Namely, the th data records the th user answers the binary question . The problem is also very similar to the aforementioned Netflix problem, except that only dichotomous responses are recorded here.

The logistic regression model assumes that

| (2.12) |

Note that this model can be derived from generalized trace regression (1.4) with . (2.12) says that given , is a Bernoulli random variable with . We assume that are randomly and uniformly distributed over . We further require to be non-spiky in the sense that and thus . This condition ensures consistent estimation as elucidated in Negahban and Wainwright (2012). For ease of theoretical reasoning, from now on we will rescale the design matrix and the signal such that and . Based on such setting, we estimate through minimizing negative log-likelihood plus nuclear norm penalty under a elementwise max-norm constraint:

| (2.13) |

where and are tuning parameters.

Again, we first derive the rate of the lower bound for as shown in Theorem 1. For this specific model, simple calculation shows that the lower bound (2.4) reduces to

Lemma 5.

Under the following conditions:

-

(C1)

, where ;

-

(C2)

are uniformly sampled from ;

For any , there exists such that as long as , the following inequality holds for some constant :

| (2.14) |

Next we study the LRSC of the loss function. Following Negahban and Wainwright (2012), besides , we define another constraint set

| (2.15) |

Here and are measures of spikiness and low-rankness of . Let . Note that is not the same as in Theorem 1 any more. As we shall see later, instead of directly applying Theorem 1, we need to adapt the proof of Theorem 1 to the matrix completion setting to derive statistical rate of . The following lemma establishes LRSC of for some .

Lemma 6.

There exist constants such that as long as and , it holds with probability greater than that for all and ,

| (2.16) |

Now we are ready to establish the statistical rate of in (2.13).

Theorem 4.

Remark 2.

In Davenport et al. (2014), they derived that when is exactly low-rank. This is slower than our rate . Moreover, we provide an extra bound on the nuclear norm of the error.

3 Simulation Study

3.1 Generalized Matrix Regression

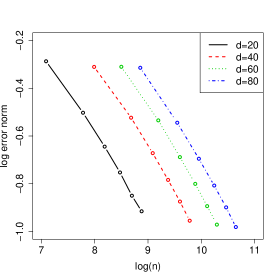

In this section, we verify the statistical rates derived in (2.7) through simulations. We let and . For each dimension, we take to be and . We set with and all the nonzero singular values of equal to . Each design matrix has i.i.d. entries from and , where . We choose and tune the constant before the rate for optimal performance.

Our simulation is based on independent replications, where we record the estimation error in terms of the logarithmic Frobenius norm . The averaged statistical error is plotted against the logarithmic sample size in Figure 1.

As we can observe from the plot, the slope of curve is almost , which is consistent with the order of in the statistical rate we derived for . The intercept also matches the order of in our theory. For example, in the plot, the difference between the green and red lines predicted by the theory is , which is in line with the empirical plot. Similarly, the difference between the red and black lines should be around , which is also consistent with the plot.

To solve the optimization problem (1.7), we exploit an iterative Peaceman-Rachford splitting method. We start from . In the th step, we take the local quadratic approximation of at :

| (3.1) | ||||

and then solve the following optimization problem to obtain :

| (3.2) |

We borrow the algorithm from Fan et al. (2016) to solve the optimization problem (3.2). In Section 5.1 of Fan et al. (2016), they applied a contractive Peaceman-Rachford splitting method to solve a nuclear norm penalized least square problem:

| (3.3) |

Construct

and

Some algebra shows that the following nuclear norm penalized least square problem is equivalent to (3.2)

| (3.4) |

We can further write (3.4) as an optimization problem of minimizing the sum of two convex functions:

| subject to |

It has been explicitly explained in Fan et al. (2016) on how to solve the above optimization problem using the Peaceman-Rachford splitting method. We provide the algorithm that is specific to our problem here. Here we first define the singular value soft thresholding operator . For any , let be its SVD, where and are two orthonormal matrices and with . Then , where . Let be an matrix whose rows are and be the response vector . For ,

| (3.5) |

where we choose and . for and we can initialize them by . When and converge, we reshape as a matrix and return it as . We iterate this procedure until is smaller than and return as the final estimator of .

3.2 Generalized Reduced-Rank Regression

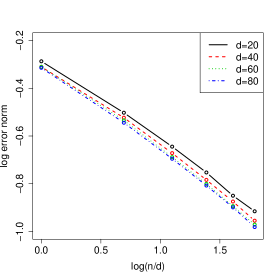

In this section, we let and . For each dimension, we consider 6 different values for such that and . We set the rank of to be and let . For and , we let the covariate have i.i.d. entries from and let follow where . We choose and tune the constant before the rate for optimal performance. The experiment is repeated for 100 times and the logarithmic Frobenius norm of the estimation error is recorded in each repetition. We plot the averaged statistical error in Figure 2.

We can see from the left panel that the logarithmic error decays as logarithmic sample size grows and the slope is almost . The right panel illustrates that when we standardize the sample size by , the statistical error curves are well-aligned, which is consistent with the statistical error rate in our theorem.

As for the implementation, we again use the iterative Peaceman-Rachford splitting method to solve for the estimator. We start from . In the th step , let

We iterate the following algorithm to solve for . Here and .

| (3.6) |

Here, is the singular value soft thresholding function we introduced in Section 3.1. Note that for all and they are irrelevant to though they share similar notations. We start from and iterate this procedure until they converge. We return the last to be .

We repeat the above algorithm until is smaller than and take as the final estimator of .

3.3 1-Bit Matrix Completion

3.3.1 Statistical consistency

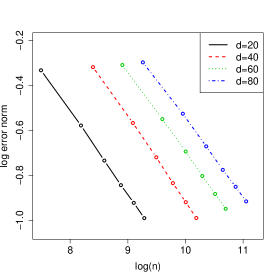

We consider with dimension and . For each dimension, we consider 6 different values for such that and . We let , and . The design matrix is a singleton and it is uniformly sampled from . We choose and tune the constant before the rate for optimal performance. The experiment is repeated for 100 times and the logarithmic Frobenius norm of the estimation error is recorded in each repetition. We plot the averaged statistical error against the logarithmic sample size in Figure 3.

We can see from the left panel in Figure 3 that decays as grows and the slope is almost . Meanwhile, Theorem 4 says that should be proportional to . The right panel of Figure 3 verifies this rate: it shows that the statistical error curves for different dimensions are well-aligned if we adjust the sample size to be .

To solve the optimization problem in (2.13), we exploit the ADMM method used in Section 5.2 in Fan et al. (2016). In Fan et al. (2016), they minimized a quadratic loss function with a nuclear norm penalty under elementwise max norm constraint. Our goal is to replace the quadratic loss therein with negative log-likelihood and solve the optimization problem. Here we iteratively call the ADMM method in Fan et al. (2016) to solve a series of optimization problems whose loss function is local quadratic approximation of the negative log-likelihood. We initialize with and introduce the algorithm below.

In the th step, we take the local quadratic approximation of at :

| (3.7) | ||||

and solve the following optimization problem to obtain :

| (3.8) |

To solve the above optimization problem, we borrow the algorithm proposed in Fang et al. (2015). Let be the variables in our algorithm and let . Define

We introduce the algorithms of the variables in our problem and interested readers can refer to Fang et al. (2015) for the technical details in the derivation and stopping criteria of the algorithm. For ,

| (3.9) |

In the algorithm, represents the projection operator onto the space of positive semidefinite matrices , is taken to be 0.1 and is the step length which is set to be 1.618. When the algorithm converges and stops, we elementwise truncate at the level of and return the truncated as . Specifically, for .

When is smaller than , we return as our final estimator of .

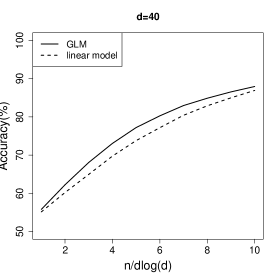

3.3.2 Comparison between GLM and linear model

As we mentioned in the introduction, the motivation of generalizing trace regression is to accommodate the dichotomous response in recommending systems such as Netflix Challenge, Kiva, etc. In this section, we compare the performance of generalized trace regression and standard trace regression in predicting discrete ratings.

The setting is very similar to the last section. We set to be a square matrix with dimension and . We let and its top five eigenspace be the top five eigenspace of the sample covariance matrix of random vectors following . For each dimension, we consider 10 different values for such that . and generate the true rating matrix in the following way:

We will show that generalized trace regression outperforms the linear trace regression in prediction.

We predict the ratings in two different ways. We first estimate the underlying with nuclear norm regularized logistic regression model. We set and derive the estimator according to (2.13). We estimate the rating matrix by as defined below:

The second method is to estimate with nuclear norm regularized linear model. Again, we take the tuning parameter and derive the estimator as follows:

| (3.10) |

To estimate the rating matrix , we use

The experiment is repeated for 100 times. In each repetition, we record the prediction accuracy as for and , which is the proportion of correct predictions. We plot the average prediction accuracy in Figure 4.

We use solid lines to denote the prediction accuracy achieved by regularized GLM and we use dotted lines to denote the accuracy achieved by regularized linear model. We can see from Figure 4 that no matter how the dimension changes, the solid lines are always above the dotted lines, showing that the generalized model always outperforms the linear model with categorical response. This validates our motivation to use the generalized model in matrix recovery problems with categorical outcomes.

4 Real Data Analysis

In this section, we apply generalized trace regression with nuclear norm regularization to stock return prediction and image classification. The former can be regarded as a reduced rank regression and the latter can be seen as the categorical responses with matrix inputs. The results demonstrate the advantage of recruiting nuclear norm penalty compared with no penalty or using -norm regularization.

4.1 Stock Return Prediction

In this subsection we aim to predict the sign of the one-day forward stock return, i.e., whether the price of the stock will rise or fall in the next day. We pick individual stocks as our objects of study: AAPL, BAC, BRK-B, C, COP, CVX, DIS, GE, GOOGL, GS, HON, JNJ, JPM, MRK, PFE, UNH, V, WFC and XOM. These are the largest holdings of Vanguard ETF in technology, health care, finance, energy, industrials and consumer. We also include S&P500 in our pool of stocks since it represents the market portfolio and should help the prediction. Therefore, we have stocks in total. We collect the daily returns of these stocks from 01/01/13 to 8/31/2017 and divide them into the training set (2013-2014), the evaluation set (2015) and the testing set (2016-2017). The sample sizes of the training, evaluation and testing sets are and respectively.

We fit a generalized reduced-rank regression model (2.8) based on the moving average (MA) of returns of each stock in the past 1 day, 3 days, 5 days, 10 days and 20 days. Hence, the dimension of is . Let be the sign of returns of the selected stocks on the th day. We assume that is a near low-rank matrix, considering high correlations across the returns of the selected stocks. We tune for the best performance on the evaluation data. When we predict on the test set, we will update on a monthly basis, i.e., for each month in the testing set, we refit (2.8) based on the data in the most recent three years. Given an estimator , our prediction are the signs of .

We have two baseline models in our analysis. The first one is the deterministic bet (DB): if a stock has more positive returns than negative ones in the training set, we always predict positive returns; otherwise, we always predict negative returns. The second one is the generalized RRR without any nuclear norm regularization. We use this baseline to demonstrate the advantage of incorporating nuclear norm regularization.

| Stock | DB |

|

|

||||

|---|---|---|---|---|---|---|---|

| AAPL | 55.13 | 51.07 | 51.07 | ||||

| BAC | 47.26 | 49.88 | 49.64 | ||||

| BRK-B | 54.18 | 59.90 | 59.90 | ||||

| C | 52.98 | 51.55 | 51.07 | ||||

| COP | 47.49 | 54.18 | 54.18 | ||||

| CVX | 48.69 | 55.37 | 54.18 | ||||

| DIS | 49.40 | 56.80 | 56.80 | ||||

| GE | 48.45 | 55.61 | 56.09 | ||||

| GOOGL | 53.94 | 52.74 | 52.74 | ||||

| GS | 52.74 | 53.22 | 47.49 | ||||

| HON | 56.09 | 51.55 | 51.31 | ||||

| JNJ | 51.79 | 54.65 | 53.70 | ||||

| JPM | 52.27 | 53.94 | 47.02 | ||||

| MRK | 51.55 | 51.31 | 51.31 | ||||

| PFE | 49.40 | 52.27 | 49.40 | ||||

| UNH | 52.74 | 53.70 | 52.74 | ||||

| V | 56.09 | 58.00 | 58.23 | ||||

| WFC | 49.16 | 52.74 | 50.12 | ||||

| XOM | 48.21 | 54.42 | 53.46 | ||||

| SPY | 54.89 | 54.89 | 54.42 | ||||

| Average | 51.62 | 53.89 | 52.74 |

From Table 1, we can see that the nuclear norm penalized model yields an average accuracy of 53.89% while the accuracy of the unpenalized model and DB are 52.74% and 51.62%. Note that the penalized model performs the same as or better than the unpenalized model in 18 out of 20 stocks. When compared with the DB, the penalized model performs better in 15 out of the 20 stocks. The improvement in the overall performance illustrates the advantage of using generalized RRR with nuclear norm regularization.

4.2 CIFAR10 Dataset

Besides the application in finance, we also apply our model to the well-known CIFAR10 dataset in image classification. The CIFAR10 dataset has 60,000 colored images in 10 classes: the airplane, automobile, bird, cat, dog, deer, dog, frog, horse, ship and truck. There are 3 channels (red, green and blue) in each figure, hence each image is stored as a matrix. We represent the 10 classes with the numbers 0,1, …, 9. The training data contains 50,000 figures and the testing data contains 10,000 figures. In our work, we only use 10,000 samples to train the model.

We construct and train a convolutional neural networks (CNN) with norm and nuclear norm regularizations on respectively to learn the pattern of the figures. The structure of the CNN follows the online tutorial from TensorFlow†††The code can be downloaded from https://github.com/tensorflow/models/tree/master/tutorials/image/cifar10. The tutorial can be found at https://www.tensorflow.org/tutorials/deep_cnn. It extracts a -dimensional feature vector from each image and maps it to 10 categories through logistic regression with a coefficient matrix. Here to exploit potential matrix structure of the features, we reshape this 384-dimensional feature vector into a matrix and map it to one of the ten categories through generalized trace regression with ten coefficient matrices. We impose nuclear norm and -norm regularizations on on coefficient matrices respectively and we summarize our results in Table 2 below.

| 0 | 0.02 | 0.05 | 0.1 | 0.2 | 0.3 | |

|---|---|---|---|---|---|---|

| nuclear penalty | 74.30% | 76.04% | 76.17% | 75.29% | 74.45% | 73.46% |

| 0 | 0.001 | 0.002 | 0.005 | 0.008 | 0.01 | |

| penalty | 74.30% | 75.70% | 75.90% | 75.53% | 75.37% | 75.22% |

The results show that both regularization methods promote the prediction accuracy while nuclear norm regularization again outperforms norm. The main reason might be that there is low-rankness instead of sparsity lying in the deep features extracted by neural network.

References

- Ahn and Reinsel (1994) Sung K Ahn and Gregory C Reinsel. Estimation of partially nonstationary vector autoregressive models with seasonal behavior. Journal of Econometrics, 62(2):317–350, 1994.

- Anderson (1951) Theodore Wilbur Anderson. Estimating linear restrictions on regression coefficients for multivariate normal distributions. The Annals of Mathematical Statistics, pages 327–351, 1951.

- Belloni et al. (2012) Alexandre Belloni, Daniel Chen, Victor Chernozhukov, and Christian Hansen. Sparse models and methods for optimal instruments with an application to eminent domain. Econometrica, 80(6):2369–2429, 2012.

- Belloni et al. (2017) Alexandre Belloni, Victor Chernozhukov, Ivan Fernández-Val, and Christian Hansen. Program evaluation and causal inference with high-dimensional data. Econometrica, 85(1):233–298, 2017.

- Bhaskar and Javanmard (2015) Sonia A Bhaskar and Adel Javanmard. 1-bit matrix completion under exact low-rank constraint. In Information Sciences and Systems (CISS), 2015 49th Annual Conference on, pages 1–6. IEEE, 2015.

- Cai and Zhou (2013) Tony Cai and Wen-Xin Zhou. A max-norm constrained minimization approach to 1-bit matrix completion. Journal of Machine Learning Research, 14(1):3619–3647, 2013.

- Candes and Tao (2007) Emmanuel Candes and Terence Tao. The dantzig selector: Statistical estimation when p is much larger than n. The Annals of Statistics, pages 2313–2351, 2007.

- Caner and Fan (2015) Mehmet Caner and Qingliang Fan. Hybrid generalized empirical likelihood estimators: Instrument selection with adaptive lasso. Journal of Econometrics, 187(1):256–274, 2015.

- Chan et al. (2015) Ngai Hang Chan, Chun Yip Yau, and Rong-Mao Zhang. Lasso estimation of threshold autoregressive models. Journal of Econometrics, 189(2):285–296, 2015.

- Chen et al. (2013) Kun Chen, Hongbo Dong, and Kung-Sik Chan. Reduced rank regression via adaptive nuclear norm penalization. Biometrika, 100(4):901–920, 2013.

- Chen et al. (2001) Scott Shaobing Chen, David L Donoho, and Michael A Saunders. Atomic decomposition by basis pursuit. SIAM review, 43(1):129–159, 2001.

- Davenport et al. (2014) Mark A Davenport, Yaniv Plan, Ewout van den Berg, and Mary Wootters. 1-bit matrix completion. Information and Inference, 3(3):189–223, 2014.

- Fan et al. (2016) J. Fan, W. Wang, and Z. Zhu. A Shrinkage Principle for Heavy-Tailed Data: High-Dimensional Robust Low-Rank Matrix Recovery. ArXiv e-prints, March 2016.

- Fan and Li (2001) Jianqing Fan and Runze Li. Variable selection via nonconcave penalized likelihood and its oracle properties. Journal of the American statistical Association, 96(456):1348–1360, 2001.

- Fan and Lv (2008) Jianqing Fan and Jinchi Lv. Sure independence screening for ultrahigh dimensional feature space. Journal of the Royal Statistical Society: Series B (Statistical Methodology), 70(5):849–911, 2008.

- Fan and Lv (2011) Jianqing Fan and Jinchi Lv. Nonconcave penalized likelihood with np-dimensionality. IEEE Transactions on Information Theory, 57(8):5467–5484, 2011.

- Fan et al. (2015) Jianqing Fan, Han Liu, Qiang Sun, and Tong Zhang. Tac for sparse learning: Simultaneous control of algorithmic complexity and statistical error. arXiv preprint arXiv:1507.01037, 2015.

- Fang et al. (2015) Ethan X Fang, Han Liu, Kim-Chuan Toh, and Wen-Xin Zhou. Max-norm optimization for robust matrix recovery. Mathematical Programming, pages 1–31, 2015.

- Geweke (1996) John Geweke. Bayesian reduced rank regression in econometrics. Journal of econometrics, 75(1):121–146, 1996.

- Gupta et al. (2010) Ankit Gupta, Robert Nowak, and Benjamin Recht. Sample complexity for 1-bit compressed sensing and sparse classification. In Information Theory Proceedings (ISIT), 2010 IEEE International Symposium on, pages 1553–1557. IEEE, 2010.

- Hansen and Kozbur (2014) Christian Hansen and Damian Kozbur. Instrumental variables estimation with many weak instruments using regularized jive. Journal of Econometrics, 182(2):290–308, 2014.

- Izenman (1975a) Alan Julian Izenman. Reduced-rank regression for the multivariate linear model. Journal of multivariate analysis, 5(2):248–264, 1975a.

- Izenman (1975b) Alan Julian Izenman. Reduced-rank regression for the multivariate linear model. Journal of multivariate analysis, 5(2):248–264, 1975b.

- Kleibergen and Paap (2006) Frank Kleibergen and Richard Paap. Generalized reduced rank tests using the singular value decomposition. Journal of econometrics, 133(1):97–126, 2006.

- Kock and Callot (2015) Anders Bredahl Kock and Laurent Callot. Oracle inequalities for high dimensional vector autoregressions. Journal of Econometrics, 186(2):325–344, 2015.

- Koltchinskii et al. (2011) Vladimir Koltchinskii, Karim Lounici, and Alexandre B Tsybakov. Nuclear-norm penalization and optimal rates for noisy low-rank matrix completion. The Annals of Statistics, pages 2302–2329, 2011.

- Lee et al. (2014) Eric L Lee, Jing-Kai Lou, Wei-Ming Chen, Yen-Chi Chen, Shou-De Lin, Yen-Sheng Chiang, and Kuan-Ta Chen. Fairness-aware loan recommendation for microfinance services. In Proceedings of the 2014 International Conference on Social Computing, page 3. ACM, 2014.

- Ludvigson and Ng (2009) Sydney C Ludvigson and Serena Ng. Macro factors in bond risk premia. The Review of Financial Studies, 22(12):5027–5067, 2009.

- Marshak (1950) Jacob Marshak. Statistical inference in economics: an introduction. John Wiley Sons, 1950.

- Negahban and Wainwright (2011) Sahand Negahban and Martin J Wainwright. Estimation of (near) low-rank matrices with noise and high-dimensional scaling. The Annals of Statistics, pages 1069–1097, 2011.

- Negahban and Wainwright (2012) Sahand Negahban and Martin J Wainwright. Restricted strong convexity and weighted matrix completion: Optimal bounds with noise. Journal of Machine Learning Research, 13(1):1665–1697, 2012.

- Negahban et al. (2011) Sahand Negahban, Pradeep Ravikumar, Martin J Wainwright, and Bin Yu. A unified framework for high-dimensional analysis of m-estimators with decomposable regularizers. In Adv. Neural Inf. Proc. Sys.(NIPS). Citeseer, 2011.

- Plan and Vershynin (2013a) Yaniv Plan and Roman Vershynin. One-bit compressed sensing by linear programming. Communications on Pure and Applied Mathematics, 66(8):1275–1297, 2013a.

- Plan and Vershynin (2013b) Yaniv Plan and Roman Vershynin. Robust 1-bit compressed sensing and sparse logistic regression: A convex programming approach. IEEE Transactions on Information Theory, 59(1):482–494, 2013b.

- Raskutti et al. (2010) Garvesh Raskutti, Martin J Wainwright, and Bin Yu. Restricted eigenvalue properties for correlated gaussian designs. Journal of Machine Learning Research, 11(Aug):2241–2259, 2010.

- Stock and Watson (2002) James H Stock and Mark W Watson. Forecasting using principal components from a large number of predictors. Journal of the American statistical association, 97(460):1167–1179, 2002.

- Tibshirani (1996) Robert Tibshirani. Regression shrinkage and selection via the lasso. Journal of the Royal Statistical Society. Series B (Methodological), pages 267–288, 1996.

- Velu and Reinsel (2013) Raja Velu and Gregory C Reinsel. Multivariate reduced-rank regression: theory and applications, volume 136. Springer Science & Business Media, 2013.

- Vershynin (2010) Roman Vershynin. Introduction to the non-asymptotic analysis of random matrices. arXiv preprint arXiv:1011.3027, 2010.

- Zhang et al. (2010) Cun-Hui Zhang et al. Nearly unbiased variable selection under minimax concave penalty. The Annals of statistics, 38(2):894–942, 2010.

- Zou and Li (2008) Hui Zou and Runze Li. One-step sparse estimates in nonconcave penalized likelihood models. Annals of statistics, 36(4):1509, 2008.

5 Proofs and Technical Lemmas

5.1 Proof for Theorem 1

We follow the proof scheme of Lemma B.4 in Fan et al. (2015). We first construct a middle point such that we choose when and when . Here, will be determined later. We denote the Frobenius ball . For simplicity, we let and in the remainder of the proof.

According to Negahban et al. (2012), when , falls in the following cone:

Since is parallel to , also falls in this cone. Given and LRSC() of , we have

| (5.1) |

where and . By Lemma F.4 in Fan et al. (2015), We thus have

| (5.2) |

Since is the minimizer of the loss, we shall have the optimality condition for some subgradient of the at . Therefore, (5.2) simplifies to

| (5.3) |

For a threshold , we choose . Then it follows that

| (5.4) |

On the other hand, , so . Choose . Given (5.3), (5.4) and yields that for some constant , . If we choose in advance, we have . Note that ; we thus have

| (5.5) | ||||

5.2 Proof for Lemma 1

Let and . Since due to independency, we have

| (5.6) |

We use the covering argument to bound the above operator norm.

Let , be the covering on and for .

We claim that

| (5.7) |

To establish the above inequality, we shall notice that since is a covering, for any given , there is a and such that and . Therefore,

Take the supremum over all possible , we have

and this leads to (5.7).

In the remaining of this proof, for fixed and , denote by and by for convenience. According to the definition of sub-gaussian norm and sub-exponential norm, given the independence between the two terms, we have . Here, the reason why is shown in the proof of Lemma 3. By Proposition 5.16 (Bernstein-type inequality) in Vershynin (2010), it follows that for sufficiently small ,

| (5.8) |

where is a positive constant.

Then the combination of the union bound over all points on and (5.7) delivers

| (5.9) |

In conclusion, if we choose , we can find a constant such that as long as , it holds that

| (5.10) |

where and are constants.

5.3 Proof for Lemma 2

In this proof, we will first show the RSC of at over the cone

for some . Then, we will prove the LRSC of in a Frobenius norm neighborhood of with respect to the same cone.

-

1.

An important inequality that leads to RSC of at .

We first prove that the following inequality holds for all with probability greater than :

(5.11) Let be the SVD of . Then and . It follows that

(5.12) Here, , and .

To derive a lower bound for (5.12), we bound the first term from below and bound the second one from above.

(5.13) Hence,

(5.14) Meanwhile, for some appropriate constants and , we establish the following inequality, which serves as the key step to bound .

(5.15) We apply the covering argument to prove the claim above. Denote the net of by . For any , define

and

Note that for any , there exist such that and for . Then it follows that

(5.16) So we have . For any and , we know from Lemma 5.14 in Vershynin (2010) that

(5.17) Applying Bernstein Inequality yields

Finally, by the union bound over , we have

(5.18) -

2.

RSC at over

For all where , we have

(5.19) Let . As we did in the proof for Theorem 1, we take and let . Then,

(5.20) On the other hand, so that . Plugging these results into (5.19), we have

(5.21) Since , there exist constants and such that as long as , combining (5.14) and (5.21) we have

(5.22) with high probability.

In the first two parts of this proof, we not only verify the RSC of , but also provide the complete procedure of how to verify the RSC of the empirical loss given the RSC of the population loss. This is very important in Part 3 of this proof.

-

3.

LRSC of around

In the remaining proof, we verify the LRSC by showing that there exists a positive constant such that

(5.23) holds for all and such that for some positive constant . Note that given , by (5.21) we have for some constant .

Define functions and for constants and to be determined. Recall that

The only difference between and is the indicator function so that .

We will finish the proof of LRSC in two steps. Firstly, we show that is positive definite over the restricted cone. Then by following the procedure of showing (5.22), we can prove that is positive definite over the cone with high probability. Secondly, we bound the difference between and and show that is locally positive definite around . This naturally lead to the LRSC of around .

We establish the following lemma before proceeding.

Lemma 7.

When and are sub-Gaussian, there exist a universal constant such that where is a positive constant.

We select an appropriate to make positive definite. Follow the same procedure in Part 1 and Part 2 of this proof, we derive that

(5.24) for a positive with high probability.

Meanwhile,

(5.25) Here is a middle point between and , thus it is also in the nuclear ball centered at with radius . We know that when the indicator function equals to 1. If , according to Condition (C5),

(5.26) Otherwise, is bounded by and where is the upper bound of for . In summary,

(5.27) where . Denote and . Suppose the eigenvalues of is upper bounded by , as a similar result to (5.11) and (5.21), as long as , we shall have

(5.28) with high probability. As long as the constant is sufficiently small such that , holds with . This delivers that is locally positive definite around with hight probability. Recall that , we have verified that is also locally positive definite around . In summary, there exist some constant such that for any ,

(5.29) for all with high probability. This finalized our proof of the LRSC of around .

Below we provide the proof of Lemma 7.

Proof for Lemma 7

We first show that for any , there exist constants and such that .

We would show that and for some positive constants and . Then

(5.30) On one hand, is a sub-Gaussian variable since it is a linear transformation of a sub-Gaussian vector. Its mean is 0 and its sub-Gaussian norm is bounded by . Since , take to be sufficiently small, we have

(5.31) where is a sub-Gaussian variable and .

On the other hand,

(5.32) Recall the covering argument in the proof of Lemma 1. Denote as a -net on , then

(5.33) For any , , given , we have . According to Bernstein-type inequality in Vershynin (2010), it follows that for sufficiently small and some positive constant ,

(5.34) Therefore, the overall union bound follows:

(5.35) Let for some positive constant , the above probability decays. This means that with high probability (which is greater than ) is less than . This finalize our proof of (5.30).

Now we look at . Denote as an event with probability sufficiently close to 1. For any ,

(5.36) Here, is an global upper bound of and is the largest eigenvalue of the fourth moment of . Since is sub-Gaussian, the fourth moment is bounded. We let be sufficiently small so that , then we proved that and thus is positive definite.

5.4 Proof of Lemma 3

where satisfies that . Note that given , . To see why, let . We have

Besides, for given . Therefore, . Since , by the standard covering argument used in the proof of 1, for any , there exists such that when , it holds for some constant ,

5.5 Proof of Lemma 4

| (5.37) | ||||

Note that for any , . By Theorem 5.39 in Vershynin (2010), there exists some such that if , we have for some universal constant ,

| (5.38) |

By the union bound, it holds that

In addition, for any such that , holds for all . Given that ,

Substituting into the inequality above, we have

Denote the above event by . Therefore, under ,

| (5.39) | ||||

Again by Theorem 5.39 in Vershynin (2010), when is sufficiently large,

Therefore, when is sufficiently large, . Denote this event by . Combining this with (5.38) and (5.39), we have under ,

Finally, for sufficiently large , it holds with probability at least for all such that ,

By a union bound across , we can deduce that for any , it holds with probability at least that for all and all ,

Since , as long as is sufficiently small, LRSC holds.

5.6 Proof for Lemma 5

Here, we take advantage of the singleton design of and apply the Matrix Bernstein inequality (Theorem 6.1.1 in Tropp(2015)) to bound the operator norm of the gradient of the loss function.

Denote . ,

Thus . Meanwhile,

| (5.40) |

Similarly, we have . Therefore, .

According to Matrix Bernstein inequality,

| (5.41) |

Let , then

| (5.42) |

for some constant as long as for some constant .

5.7 Proof for Lemma 6

We aim to show that the loss function has LRSC property in a -ball centered at with radius .

For all satisfying , let us denote . Then

| (5.43) |

Here is a middle point between and . Due to the singleton design of , . Given that the derivative of is bounded by 0.1, we have

| (5.44) |

It is proved in the proof of Theorem 1 in Negahban and Wainwright (2012) that as long as ,

| (5.45) |

for all with probability at most . Therefore, since and , we shall have

| (5.47) |

for sufficiently small . The following inequality thus holds for all satisfying :

| (5.48) |

5.8 Proof for Theorem 4

In this proof, we define an operator such that for all .

Denote . If , according to Case 1 in the proof for Theorem 2 in Negahban and Wainwright (2012), we shall have

| (5.49) |

for any . Following the same strategy we used in the proof for Theorem 1, we will have

for some constant .

| (5.50) |

As what we did in the proof for Theorem 1, we take and we have

| (5.51) |

for some constant .

On the other hand, if , we have

| (5.52) |

In summary, as long as is sufficiently large, we shall have

| (5.53) |

with probability greater than , where and are constants.