Asymptotic Expansion as Prior Knowledge in

Deep Learning Method for high dimensional BSDEs

This version: March 5, 2019)

Abstract

We demonstrate that the use of asymptotic expansion as prior knowledge in the “deep BSDE solver”, which is a deep learning method for high dimensional BSDEs proposed by Weinan E, Han & Jentzen (2017), drastically reduces the loss function and accelerates the speed of convergence. We illustrate the technique and its implications by using Bergman’s model with different lending and borrowing rates as a typical model for FVA as well as a class of solvable BSDEs with quadratic growth drivers. We also present an extension of the deep BSDE solver for reflected BSDEs representing American option prices.

1 Introduction

This work presents a simple acceleration technique for deep learning methods for high-dimensional backward stochastic differential equations (BSDEs). Since its invention, BSDEs have attracted many mathematicians by their deep connections to non-linear partial differential equations and stochastic control problems. The relevance of BSDEs for financial problems has also increased recently, particularly since the financial crisis. Early attempts such as Fujii & Takahashi (2012, 2013) [18, 19] and Crepey (2015) [10] have shown that BSDEs are indispensable tools to describe the non-linear effects in various valuation adjustments stemming from collateralization, credit risks, funding and regulatory costs. See Brigo, Morini & Pallavicini (2013) [7] and Crepey & Bielecki (2014) [9] as reviews on the financial problems closely related to BSDEs. Due to their direct connection to the stochastic control problems, BSDEs are also actively studied to obtain probabilistic representation of optimal liquidation, switching and portfolio selection problems.

The progress in numerical computation schemes for BSDEs has also been significant. The famous -regularity established by Zhang (2001, 2004) [34, 33] was soon followed by now standard regression-based Monte-Carlo simulation scheme developed, among others, by Bouchard & Touzi (2004) [6], Gobet, Lemor & Warin (2005) [25]. There now exist many extensions of these fundamental works to various types of BSDEs. Unfortunately, however, applications to high dimensional problems required in the practical setups have been almost infeasible due to their heavy numerical burden. This is the biggest obstacle that has been hindering BSDE from becoming a standard mathematical tool in the financial industry. As a result, many of the XVAs are usually implemented as linear approximations by neglecting sometimes crucial non-linear feedback effects.

A potential breakthrough may come from the recent boom as well as explosive progress of reinforcement machine learning, which makes use of deep neutral networks mimicking the cognitive mechanism of human brains. In fact, Weinan E, Han & Jentzen (2017) [17] motivated by the work of Weinan E & Han (2016) [14] have just demonstrated astonishing power of “deep BSDE solver” for high dimensional problems, which is based on the deep neural networks constructed by the free package Tensorflow.444See also Beck, E & Jentzen (2017) [5], where the method is applied to different types of BSDEs, and [15, 16] as different approaches to high-dimensional problems. Their main idea is to interpret a Markovian BSDE

as a control problem minimizing the square difference . Here, is the terminal condition and the terminal value of forwardly simulated process based on the estimated initial value as well as the coefficients of Brownian motions , which are treated as the control variables in the minimization problem. This is nothing but concrete implementation of Method of Optimal Control as a solution technique for FBSDEs given in Chapter 3 of Ma & Yong (2000) [27]. Although the mathematical understanding for the deep learning algorithm is still in its infancy, the deep BSDE solver seems to be capable of handling high dimensional problems very efficiently in a quite straightforward way.555As interesting applications of machine learning to various investment strategies, see Nakano et.al. (2017) [28, 29, 30].

Despite its remarkable success for high dimensional problems, it is not free from some important issues. By closely studying the deep BSDE solver given in [17], we find that its direct application to the Bergman (1995) [4] equation, as a typical model for funding value adjustment (FVA) with different lending and borrowing rates, yields persistently high loss function even when the estimated , which corresponds to the price of the contingent claim, is quite accurate. The slow convergence and large loss function seem to arise from non-smooth terminal condition as well as driver of the BSDE, which are ubiquitous in financial applications.

Let us denote by the value of the solution at time under the -initialized setup with the input . Due to the strong Markov property of Brownian motions and Blumenthal’s - law, is almost surely deterministic and hence is given by some Borel-measurable function as . When is smooth, it is well-known that where is the diffusion coefficient of the SDE specifying the dynamics of the forward component . This observation shows that the deep BSDE solver is actually looking for the optimal delta-hedging strategy under given time partition. It is thus natural to have slower convergence when the relevant coefficient functions are not smooth. Similarly, from the financial viewpoint, the loss function is the square of “replication error” from the associated delta-hedging strategy. Therefore, even when is known to be accurate, the resultant strategy is not useful when the loss function remains high. Worse, we do not know the accurate value of in general. Only available criterion at hand is the famous stability result of BSDEs to guarantee the uniqueness of their solutions, which thus requires the convergence of the loss function to a sufficiently small value. Since many of the financial problems related to the valuation adjustments i.e. XVAs have quite similar form to the Bergman’s model, this is not an exceptional problem. The speed of learning process is found to be strongly affected by the correlation among the underlying security processes, too.

It has been widely known that the prior knowledge to prepare the starting point of the learning process significantly affects the performance of deep learning methods. In this work, we demonstrate that a simple approximation formula based on an asymptotic expansion (AE) of BSDEs serves as very efficient prior knowledge for the deep BSDE solver. Using the method proposed in the works Fujii & Takahashi (2012, 2019) [20, 24], one obtains an analytic expression of approximate . We write and apply the reinforcement learning only to the residual term . We shall show that the use of drastically reduces the loss function and accelerates the speed of convergence. We have also presented an extension of the deep BSDE solver for reflected backward stochastic differential equations (RBSDEs), which become relevant when studying optimal stopping/switching problems. Using an American basket option as an example, we have shown that the effectiveness of AE as prior knowledge still holds for RBSDEs. Numerical examples for a class of quadratic growth BSDEs (qg-BSDEs) are also given. Despite the notorious difficulty to obtain stable numerical results for qg-BSDEs, the deep BSDE solver with AE is shown to handle the problem quite efficiently.

2 An application to Bergman’s model

2.1 Model

Let us consider the filtered probability space generated by a -dimensional Brownian motion , which is assumed to satisfy the usual conditions. We suppose that the risky assets follow the dynamics

| (2.1) |

where is the initial value, are constants and is the square root of the (instantaneous) correlation matrix among , normalized as . is assumed to be invertible. There are two interest rates, one is for lending and the other for borrowing. The dynamics of portfolio value under the least-borrowing self-financing strategy for replicating the terminal payoff , where is a Lipschitz continuous function, is given by the following BSDE:

| (2.2) | |||||

See, for example, Example 1.1 in [12] as a simple derivation of the above form. The existence of unique solution is guaranteed by the standard results for the Lipschitz BSDEs. Note that the cash amount invested to the ith risky asset at time is given by .

Remark 2.1.

When one applies the method to a BSDE, the coefficient of the Brownian motion is estimated for each scenario at each time step. By defining the deterministic map by , where denotes the initial data of the underlying security price process , the representation theorem of the BSDE implies (when has appropriate regularity) that . In other words, one obtains not only the price but also the path-wise delta sensitives through the learning process of the deep BSDE solver. This is quite valuable information, for example, to estimate the necessary independent amount based on the standard initial margin method (SIMM).

2.2 Asymptotic expansion based on driver’s linearization

We adopt an asymptotic expansion method proposed in [20] which is based on perturbative expansion of the non-linear driver of the BSDE around a linear term. Mathematical justification of the expansion is available in Takahashi & Yamada (2015) [32]. Its implementation with a particle method Fujii & Takahashi (2015) [21] has been successfully applied to large scale numerical simulations in many works using up to the second order expansions. See, for example, Crepey & Nguyen (2016) [11] and references therein.

In this work, we only use the leading term of the asymptotic expansion. For higher order corrections, see discussions and examples available in [20, 32]. According to [20], we consider (2.2) as the perturbed model around the linear driver:

The idea of the approximation is to expand around . The leading order terms are determined by

This immediately gives with the probability measure defined by

where is Doléans-Dade exponential. Since is equal to the price process in Black-Scholes model with the risk-free rate , is obtained as deltas with respect to multiplied by the diffusion coefficient . For example, if and , one has where is the distribution function of the standard normal and .

Remark 2.2.

We should emphasize that an analytical expression can be obtained even when and the process have more general forms. This is a well-known application of asymptotic expansion technique to European contingent claims. See Takahashi (2015) [31] and references therein for details on this topic. It is also important to notice that the leading order asymptotic expansion keeps linearity. Since it is derived from a linearized BSDE, the resultant approximation is also linear with respect to the cash flow. Thus, in particular, the approximation for a derivatives portfolio is given by a sum of for its individual contract.

In the following, in order to focus on the implications of AE as prior knowledge in the deep BSDE solver instead of deriving AE formulas for general setups, we only deal with the terminal conditions consisting of call/put options and the log-normal process for in (2.1).

2.3 Numerical examples

2.3.1 Purely call terminals

Suppose that the terminal condition is given by

In this case, the one who tries to replicate the terminal payoff must always hold a long position for every risky asset. Since this implies that she must always borrow cash to finance her hedging position, the BSDE (2.2) is equivalent to

Notice that this holds true irrespective of the correlation among ’s. After a simple measure change, one sees that the exact solution of is given by the corresponding Black-Scholes formula with replaced by .

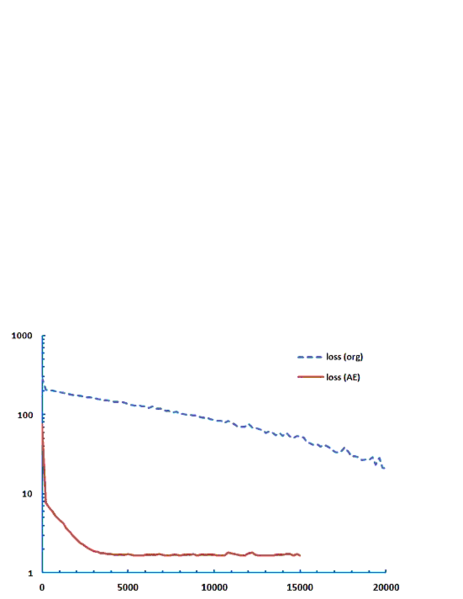

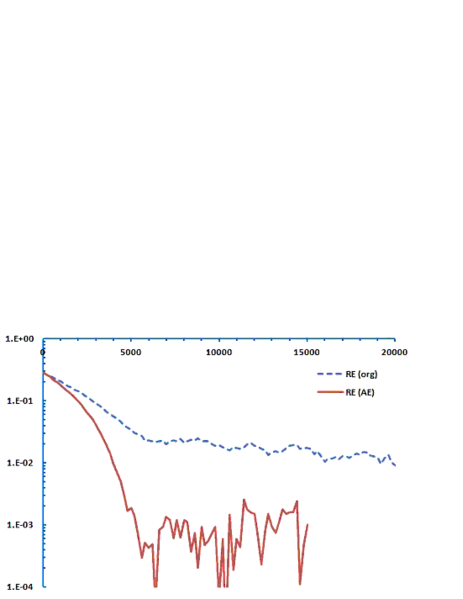

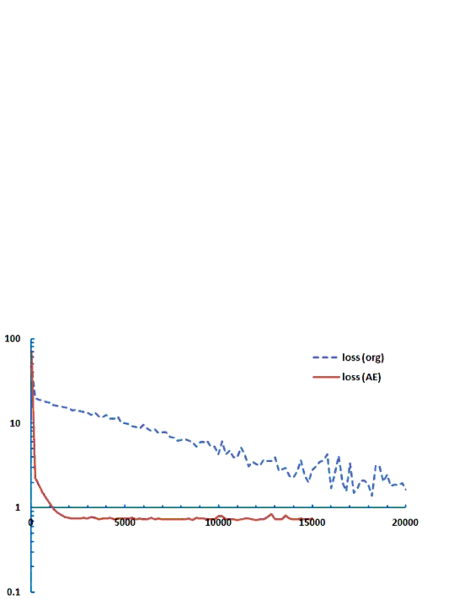

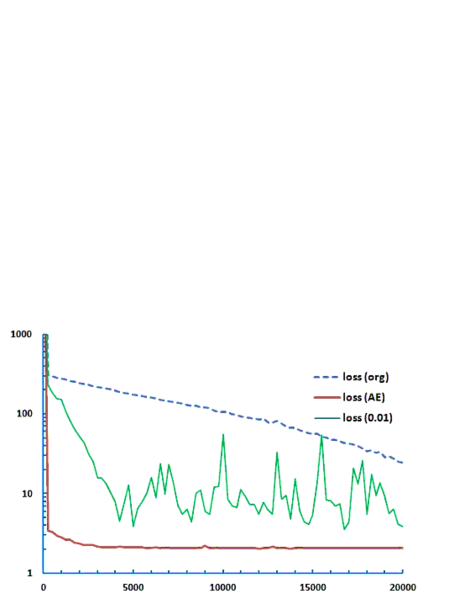

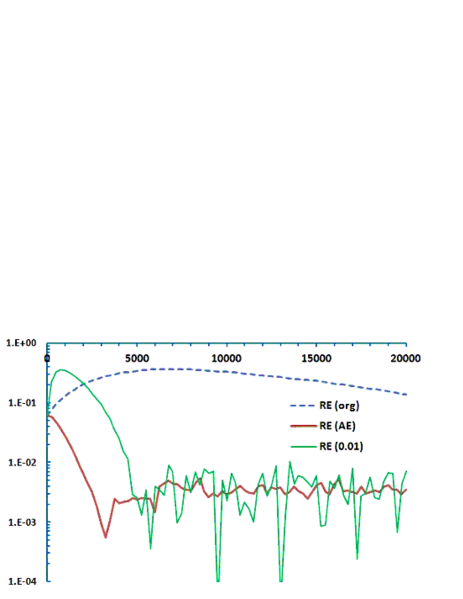

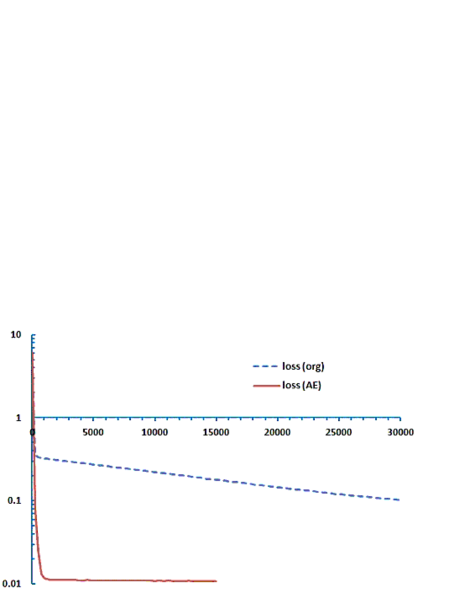

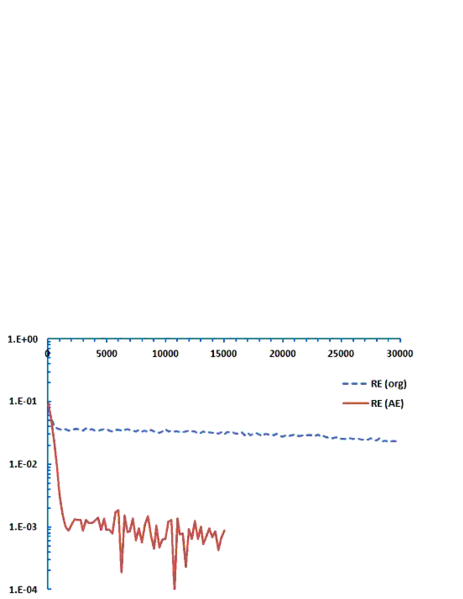

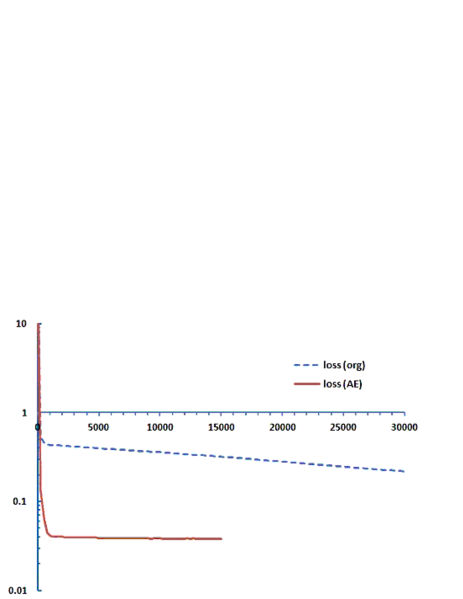

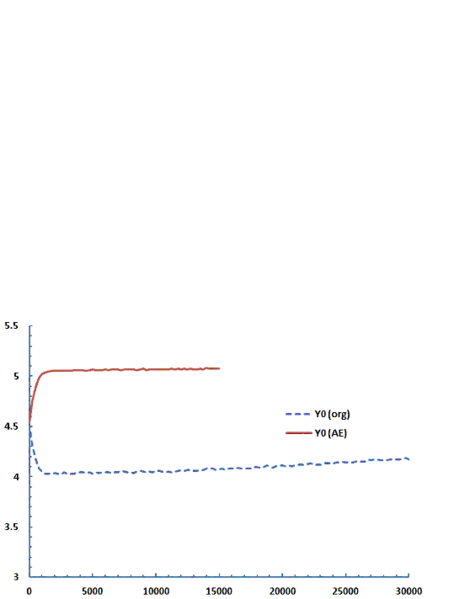

Let us start from the simplest one-dimensional example with . In this case, the above discussion gives as the exact solution. We have used (time discretization), , , in the deep BSDE solver [17] in Figure 1. The loss function is estimated with 1024 paths. As explained before, we have used only the leading order approximation as and put in the deep BSDE solver, where only the residual term and are used as the targets of the training process. In Figure 1, we have compared the performance of the deep BSDE solver with and without AE as prior knowledge. It is observed that one achieves much quicker convergence and roughly by one order of magnitude smaller relative error when one uses AE as prior knowledge. After roughly 5,000 iterations, its loss function reaches 1.7. Since the option is around at-the-money, the gamma at the last stage is huge in many paths. If the delta-hedging at the last period completely fails, its contribution to the loss function is estimated roughly by . This estimate implies that the deep BSDE solver with AE reaches its limit performance already at 5,000 iterations. When AE is not used, one sees that the loss function (and hence the replication error) remains rather big and slow to converge.

Notice that the deep BSDE solver uses tf.train.AdamOptimizer available in the TensorFlow package for optimizing the coefficient matrices usually denoted by w. This is the algorithm proposed in [2], in which the learning_rate is recommended as a default value. Although one can speed up the learning process by increasing the learning rate, this is not always appropriate. Let us study the effects of the learning rate using the next 30-dimensional example.

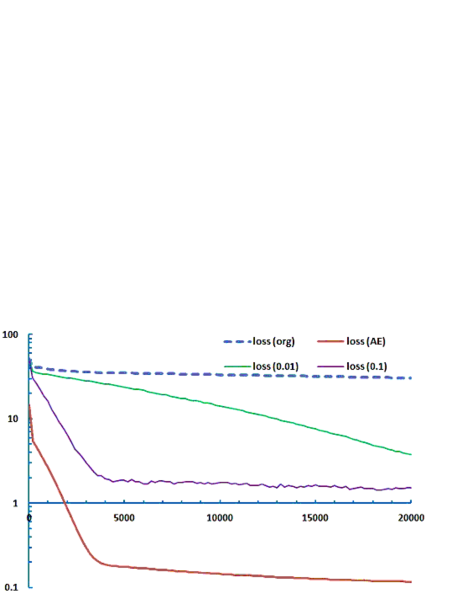

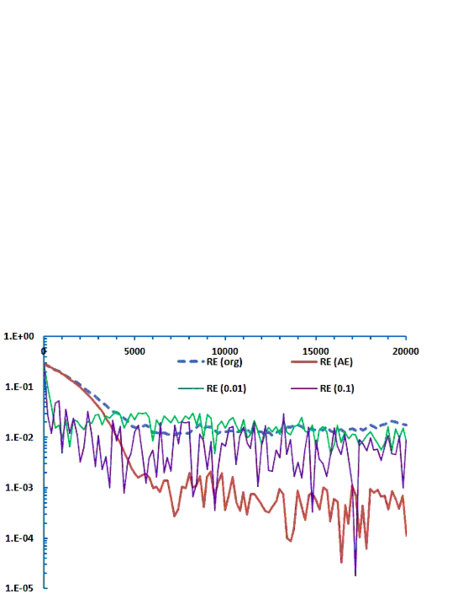

We study the case with where the set A is replaced by and are common and the same with those in set A i.e., is given by the average of the call options. The matrix is assumed to have the form

| (2.3) |

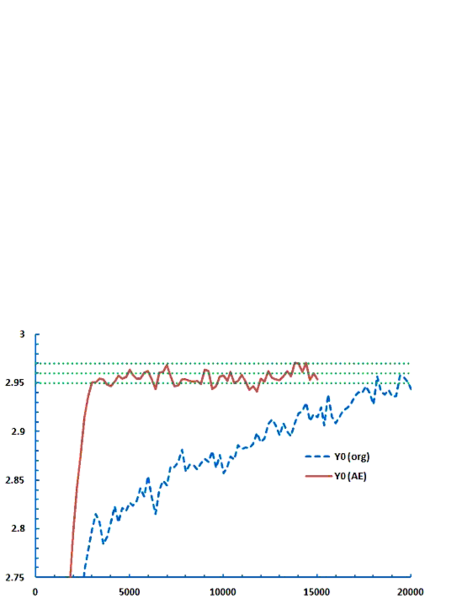

with . This implies that the correlation for every pair is about 20%. The exact value of must be the same . In Figure 2, we have provided the numerical results for this case. In addition to those with the default learning_rate , we have added two cases with learning_rate and without AE as prior knowledge. One sees, for example, learning_rate yields a fast decline of the loss function in the first 5,000 steps comparable to the case with AE, but it stops at the level 10 times higher than the case with AE. Moreover, the estimated (and hence the relative error) exhibits strong instability. The use of asymptotic expansion with the default learning rate yields a more stable and accurate estimate. Notice that the instability associated with a higher learning rate is more prominent for lower dimensional problems. The 30-dimensional example we have just considered, the instability is somewhat mitigated by the diversification effects from the imperfectly correlated 30 assets.

Remark 2.3.

Dynamically choosing the optimal learning rate is an important issue and, in fact, is a popular topic for researchers on computation algorithms. At the moment, however, there exists no established rule and it looks to depend on a specific problem under consideration. As we have seen above, the optimal choice depends on the dimension of the forward process as well as their correlation even if the form of the BSDE is the same. In the reminder of the paper, we shall fix the learning rate to the default value for the tf.train.AdamOptimizer unless explicitly stated otherwise.

Remark 2.4.

We have no intention to deny the possibility that the convergence speed can be improved by implementing some hyper-parameter optimization, for example, tuning the learning rate, batch size, and the number of layers etc. However, this is not usually an easy task requiring trial and error. Note that one may even use our acceleration technique together with the hyper-parameter optimization.

2.3.2 Call spread

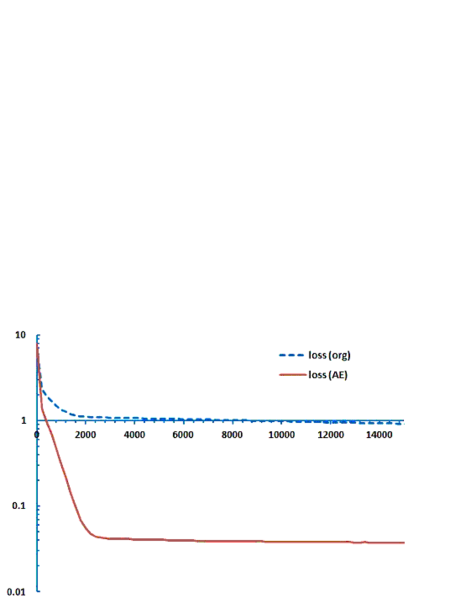

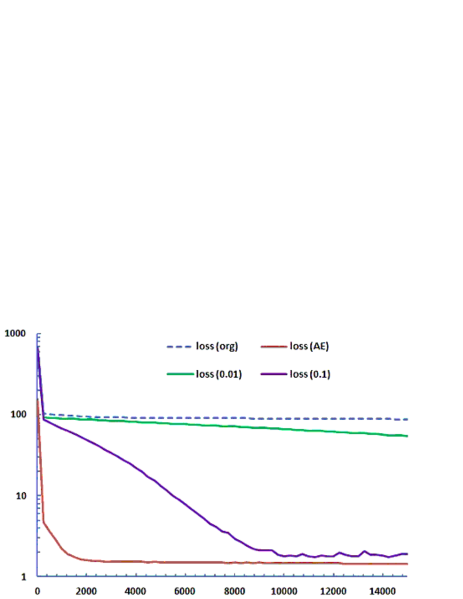

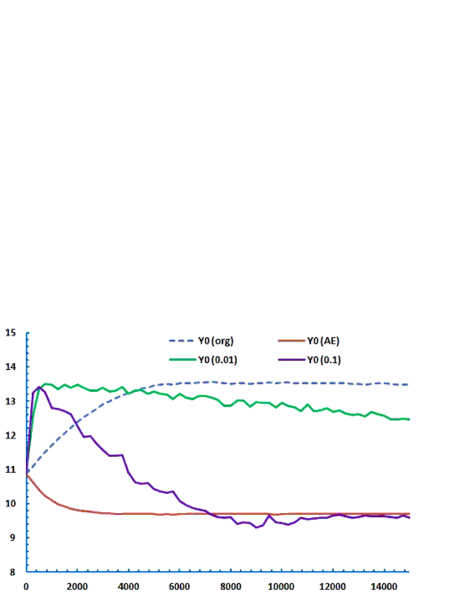

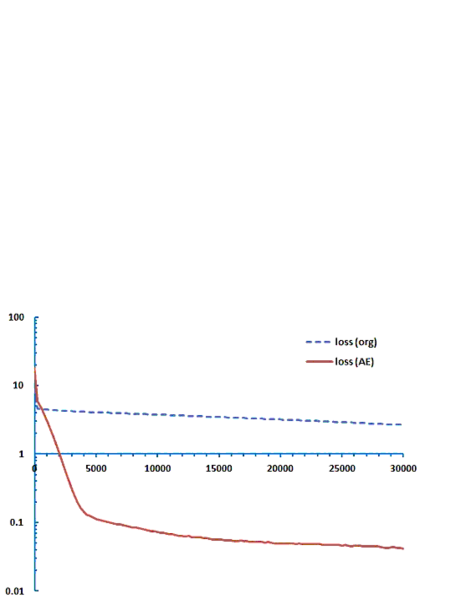

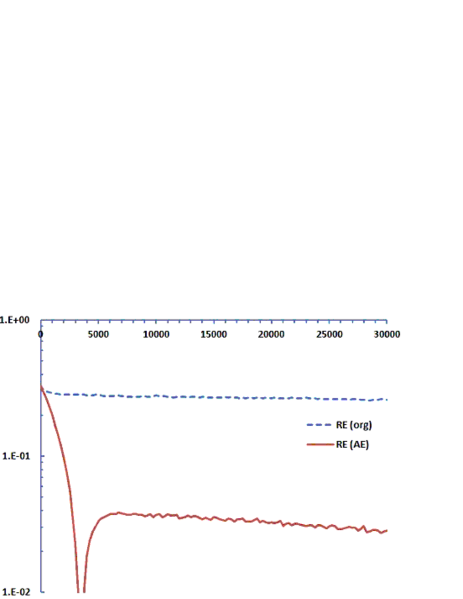

We next study the terminal function with . For this 1-dimensional example of call spread, there is no closed-form solution anymore. However, it is estimated as in Bender & Steiner (2012) [3] using the regression based Monte Carlo scheme improved by the martingale basis functions. The numerical results are given in Figure 3. A much quicker convergence and smaller loss function are observed as before.

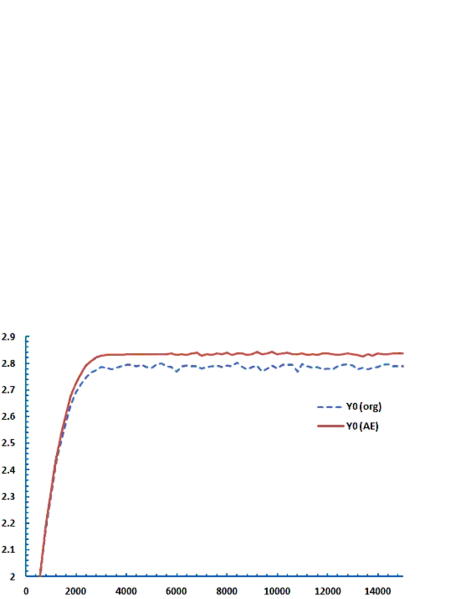

Finally, we provide the numerical results for a high dimensional setup with

and the same matrix with given in the last subsection. The numerical comparison is given in Figure 4. Probably due to the diversification effects, one observes the quicker convergence of the estimated for both cases. However, the original deep BSDE solver without AE effectively ceases improvement where the loss function is more than one magnitude larger than the case with AE. It is likely that this is a cause of small gap in the estimated given in the right-hand figure.

3 An example of a reflected BSDE

3.1 Model

We now study a reflected BSDE corresponding to the pricing problem of an American option. The relevant BSDE where corresponds to the option price is given by

| (3.1) |

where is a dividend yield of the ith security , is the reflecting process that keeps the solution from going below the barrier for every . The other assumptions made in Section 2.1 are in force, in particular, the dynamics of is still given by (2.1). The detailed derivation of the above BSDE is available, for example, in Chapter 6 of [35].

Instead of using the penalization method [13], we extend the deep BSDE solver so that it learns the process directly in addition to and . We adopt the loss function

where the weight is used to take a balance between the terminal and the lateral conditions. Remember that is the forwardly simulated process based on the estimated and . We apply to update the process only when so that we can avoid the explicit inclusion of the second condition of (3.1) into the loss function.

Remark 3.1.

Since it is impossible to make the loss function exactly zero, the weight factor slightly affects the estimated (as well as the size of the loss function). For the two examples we shall see below, halving the weight factor to lowers the American option prices by roughly 1.0%.

3.2 Numerical examples

In the following, we adopt corresponding to an American basket call option. The leading order asymptotic expansion is still given by and as its deltas multiplied by . Although one cannot get the exact solution, it is not difficult to expand the solution in terms of to obtain

| (3.2) |

where

The above approximation is based on the well-known small-diffusion expansion technique [31]. We perturb the forward process as

Notice the fact that the expansion of as a power series of is equivalent to that of after setting .

One sees that the 0th order expansion corresponds to the deterministic forward process and that the next order expansion is defined by and . Using the expansion up to the first order, it is easy to derive the result (3.2) since the process is now Gaussian. Although one can continue the expansion to an arbitrary higher order, it is expected to give only marginal effects when used in the deep BSDE solver. As we can easily see from the above analysis, the leading order term of the small-diffusion expansion always yield a Gaussian process regardless of the underlying process for . Therefore deriving up to the first order of volatility can be performed easily in most cases.

3.2.1 American call option

Let us first check the general performance by studying one-dimensional example. We use . Note that the choice of should not affect . The benchmark price based on a binomial tree model with 10,000 time steps available in the literature is , while the corresponding European option price is . The comparison of the loss function and the relative error is given in Figure 5. In order to achieve an accurate estimate, fine discretization (n_time) is used. Since the direct use of the deep BSDE solver with the default learning rate yields very slow convergence, we have also provided the case with the learning rate . The associated instability in the loss function as well as suggests that one needs to fine-tune the learning rate dynamically in the deep BSDE solver for achieving the comparable performance to the case with AE.

3.2.2 American 50-dimensional basket call option

We now study a 50-dimensional American basket call option. Let us use , and in (2.3), which implies around 30% correlation for every pair of ’s. We have used (n_time) time partition as before. The price of the corresponding European option is estimated as by a simulation with 500,000 paths.

As one can see from Figure 6, the convergence is very quick when AE is used as prior knowledge. After 2,000 iterations, is settled around 9.7. When AE is not used, the convergence is very slow. Even if we use an extremely large learning_rate, it takes more than 10,000 iterations to give a comparable size of loss function. The stability of estimated with AE clearly stands out from the others. In the deep BSDE solver, we estimate at each time step using neural networks with multiple layers. Therefore quick convergence brought by a simple AE approximation is a great advantage, in particular, for the problems that require many time-steps for accurate estimates. Comparing to the previous one-dimensional example, one clearly sees that the optimal choice of the learning rate depends on the details of the settings (such as, the number of assets and the correlation among them) even for the BSDE with the same form.

Remark 3.2.

Changing the code for the penalization method [13] is very simple. The solution of the penalized BSDE, which is obtained by replacing with

is known to converge to that of (3.1) in the limit of . Although there is no need to estimate the process , we have found that the numerical results depend quite sensitively on the size of . Moreover small slows down the learning process significantly and hence not useful in many cases. It helps, however, double checking the correct implementation by comparing the numerical results.

4 An example of a Quadratic BSDE

4.1 Model

We now consider the following qg-BSDE

| (4.1) |

where is a constant, a -dimensional Brownian motion, is a bounded Lipschitz continuous function. For simplicity, we assume that the associated forward process is given by

with a common initial value , and a volatility . is a square root of correlation matrix among and assumed to be invertible.

Thanks to this special form, it is easy to derive a closed form solution

| (4.2) |

by applying Itô formula to . The existence of a closed-form solution allows us to test the performance of the deep BSDE solver. Note however that the numerical evaluation of qg-BSDE is known to be very difficult. See discussions in Imkeller & Reis (2010) [26], Chassagneux & Richou (2015) [8] and Fujii & Takahashi (2018) [22].

A formal application of the method [20] to the current case gives as the leading order asymptotic expansion, and hence can be derived as deltas in exactly the same manner as in the last section. Although the asymptotic expansion methods in [20, 32] are only proved for the Lipschitz BSDEs, using Malliavin’s differentiability and the associated representation theorem for given in Ankirchner, Imkeller & Dos Reis (2007) [1], one can justify the method also for the quadratic case in a similar way. The asymptotic expansion for the Lipschitz BSDEs with jumps in [24] can also be extendable to a quadratic-exponential growth BSDEs by using the results of Fujii & Takahashi (2018) [23]. The details may be given in different opportunities.

4.2 Numerical examples

We suppose a bounded terminal condition defined by

| (4.3) |

with two constants . As a first example, we have tested a 50-dimensional model with zero correlation: . The solution (4.2) is estimated as by a simulation with one million paths. We use as discretization. In Figure 7, we have compared the performance of the deep BSDE solver with and without AE as prior knowledge. When the asymptotic expansion is used, the convergence is achieved just after a few thousands iterations and the relative error becomes 0.1%. On the other hand, the learning process proceeds very slowly when the deep BSDE solver is directly applied without using AE. Even after 30,000 iterations, both of the loss function and the relative error are still larger than the former by more than an order of magnitude. It seems that clever dynamic tuning of the learning rate is necessary for achieving comparable speed of convergence and stability to those for the case with asymptotic expansion.

Next, we have studied the impact of correlation among ’s. Since the regressors have non-zero correlation, one can expect that the learning process becomes more time consuming. We have used the same parameters in except that the matrix is now defined by (2.3) with , which implies about 30% correlation among ’s. In this case, the solution (4.2) estimated by one million paths is . The comparison of the performance is given in Figure 8. Although the accuracy is deteriorated in the both cases, the deep BSDE solver with the asymptotic expansion still achieves the relative error after 5,000 iterations. When AE is not used, the relative error remains more than even after 30,000 iteration steps. Similarly to the previous examples, one sees that the use of AE as prior knowledge effectively ameliorates the problem of correlated inputs also for this case.

Finally, let us study a bit extreme situation with a large quadratic coefficient as well as volatility. We set and increase the number of time partition to n_time. The solution (4.2) estimated by a million paths of Monte Carlo simulation with the same step size is given by . We have provided the numerical results in Figure 9. Although the loss function becomes larger by a factor of few, the deep BSDE solver with AE quickly reaches its equilibrium after a few thousands steps and the relative error is around . As is clearly seen from the graph, the estimated obtained without using AE is quite far from the target after 30,000 iterations steps.

5 Concluding remarks

In this work, we have demonstrated that one can greatly accelerate the learning process by using a simple approximation formula as “prior knowledge”. This overcomes the issue of slow progress of the learning process in the presence of the non-smooth functions as well as correlated security processes for the deep BSDE solver, and may pave the way for the practical use of BSDEs with more realistic description of non-linearity in the financial markets. As a nature of machine-learning technique, accelerated convergence is expected to be a generic phenomenon regardless of the exact form of algorithm when appropriate prior knowledge is given.

Although appropriately chosen hyper-parameters may achieve quicker convergence, their optimization is usually a difficult task requiring trial and error. For example, TensorFlow provides a simple tool to make the learning rate decay at a certain rate, but choosing an appropriate decay rate becomes another trouble because we do not know, a priori, the “limit” of the loss function, which is determined by the size of the delta-hedging error unavoidable for given discretization. If the speed of decay is too fast, then there remains large loss function at the time when the learning rate becomes very small. This results in slow convergence. On the other hand, if the speed of decay is too slow, one has to wait unnecessary long time for the learning rate becoming small enough to yield a stable estimate. A simple AE formula nicely solves these issues. Moreover, it may be combined with the hyper-parameter optimization to enhance its performance.

Application of the deep learning methods to the BSDEs with jumps remains as an important challenge. Relatively small intensity of the jumps (such as those in credit models) is expected to make the learning process very hard to proceed. An analytic approximation of the jump coefficients available by the asymptotic expansion in [24] may mitigate the difficulty.

Acknowledgement

The research is partially supported by Center for Advanced Research in Finance (CARF).

References

- [1] Ankirchner, S., Imkeller, P. and Dos Reis, G., Classical and Variational Differentiability of BSDEs with Quadratic Growth, Electronic Journal of Probability, Vol. 12, 1418-1453.

- [2] Kingma, D. P. and Ba, J.L., 2015, ADAM: A method for stochastic optimization, arXiv:1412.6980.

- [3] Bender, C. and Steiner, J., 2012, Least-squares Monte Carlo for Backward SDEs, Numerical Methods in Finance (edited by Carmona et al.), 257-289, Springer, Berlin.

- [4] Bergman, Y. Z., 1995, Option pricing with different interest rates, Review of Financial Studies, Vol. 8, 2, 475-500.

- [5] Beck, C., E, W. and Jentzen, A., 2017, Machine learning approximation algorithm for high-dimensional fully nonlinear partial differential equations and second-order backward stochastic differential equations, arXiv:1709.05963.

- [6] Bouchard, B. and Touzi, N., 2004, Discrete-time approximation and Monte-Carlo simulation of backward stochastic differential equations, Stochastic Processes and their Applications, 111, 175-206.

- [7] Brigo, D, M Morini and A Pallavicini (2013), Counterparty Credit Risk, Collateral and Funding, Wiley, West Sussex.

- [8] Chassagneux, J.F. and Richou, A., 2016, Numerical Simulation of Quadratic BSDEs, Annals of Applied Probabilities, Vol. 26, No. 1, 262-304.

- [9] Crepey, S, T Bielecki with an introductory dialogue by D Brigo (2014), Counterparty Risk and Funding, CRC press, NY.

- [10] Crepey, S., 2015, Bilateral Counterparty Risk under Funding Constraints Part I: Pricing, Part II: CVA Mathematical Finance, Vol. 25, No. 1, 1-22, 23-50.

- [11] Crepey S., Nguyen T.M., 2016, Nonlinear Monte Carlo Schemes for Counterparty Risk on Credit Derivatives. In: Glau K., Grbac Z., Scherer M., Zagst R. (eds) Innovations in Derivatives Markets. Springer Proceedings in Mathematics & Statistics, vol 165. Springer, Cham.

- [12] El Karoui, N., Peng, S. and Quenez, M.C., 1997, Backward stochastic differential equations in finance, Mathematical Finance, Vol. 7, No. 1, 1-71.

- [13] El Karoui, N., Kapoudjian, C., Pardoux, E., Peng, S. and Quenez, M.C., 1997, Reflected solutions of backward SDE’s and related obstacle problems for PDE’s, Annals of Probability, Vol. 25, 2, 702-737.

- [14] E, W. and Han, J., 2016, Deep learning approximation for stochastic control problems, arXiv:1611.07422.

- [15] E, W., Hutzenthaler, M., Jentzen, A. and Kruse, T., 2016, Linear scaling algorithm for solving high-dimensional nonlinear parabolic differential equations, arXiv:1607.03295.

- [16] E, W., Hutzenthaler, M., Jentzen, A. and Kruse, T., 2017, On multilevel Picard numerical approximations for high-dimensional nonlinear parabolic partial differential equations and high-dimensional nonlinear backward stochastic differential equations, arXiv:1708.03223.

- [17] E, W., Han, J. and Jentzen, A., 2017, Deep learning-based numerical methods for high-dimensional parabolic partial differential equations and backward stochastic differential equations, arXiv:1706.04702.

- [18] Fujii, M. and Takahashi, A., 2012, Collateralized Credit Default Swaps and Default Dependence, The Journal of Credit Risk, Vol. 8, No. 3, 97-113.

- [19] Fujii, M. and Takahashi, A., 2013, Derivative pricing under asymmetric and imperfect collateralization and CVA, Quantitative Finance, Vol. 13, Issue 5, 749-768.

- [20] Fujii, M. and Takahashi, A., 2012, Analytical approximation for non-linear FBSDEs with perturbation scheme, International Journal of Theoretical and Applied Finance, 15, 5, 1250034 (24).

- [21] Fujii, M. and Takahashi, A., 2015, Perturbative expansion technique for non-linear FBSDEs with interacting particle method, Asia-Pacific Financial Markets, Vol. 22, 3, 283-304.

- [22] Fujii, M. and Takahashi, A., 2018, Solving backward stochastic differential equations with quadratic-growth drivers by connecting the short-term expansions, Stochastic Processes and their Applications, in press.

- [23] Fujii, M. and Takahashi, A., 2018, Quadratic-exponential growth BSDEs with jumps and their Malliavin’s differentiability, Stochastic Processes and their Applications, Vol. 128, Issue 6, 2083-2130.

- [24] Fujii, M. and Takahashi, A., 2019, Asymptotic Expansion for Forward-Backward SDEs with Jumps, Stochastics, Vol. 91, No. 2, 175-214.

- [25] Gobet, E., Lemor, J-P. and Warin, X., 2005, A regression-based Monte Carlo method to solve backward stochastic differential equations, The Annals of Applied Probability, Vol. 15, No. 3, 2172-2202.

- [26] Imkeller, P. and Dos Reis, G., 2010, Path regularity and explicit convergence rate for BSDEs with truncated quadratic growth, Stochastic Processes and their Applications, 120, 348-379. Corrigendum for Theorem 5.5, 2010, 120, 2286-2288.

- [27] Ma, J. and Yong, J., 2000, Forward-backward stochastic differential equations and their applications,Springer, Berlin.

- [28] Nakano, M., Takahashi, A. and Takahashi, S., 2017, Fuzzy logic-based portfolio selection with particle filtering and anomaly detection, Knowledge-Based Systems, Vol 131, 113-124.

- [29] Nakano, M., Takahashi, A. and Takahashi, S., 2017, Robust technical trading with fuzzy knowledge-based systems, forthcoming in Frontiers in Artificial Intelligence and Applications.

- [30] Nakano, M., Takahashi, A. and Takahashi, S., 2017, Creating investment scheme with state space modeling, Expert Systems with Applications, Vol. 81, 53-66.

- [31] Takahashi, A., 2015, Asymptotic Expansion Approach in Finance in Large Deviations and Asymptotic Methods in Finance, edited by Friz, P., Gatheral, J., Gulisashvili, A., Jacquier, A. and Teichman, J. Springer Proceedings in Mathematics and Statistics, Springer, N.Y.

- [32] Takahashi, A. and Yamada, T., 2015, An asymptotic expansion of forward-backward SDEs with a perturbed driver, International Journal of Financial Engineering, Vol. 02, Issue 02, 1550020 (29).

- [33] Zhang, J., 2004, A numerical scheme for BSDEs, The Annals of Applied Probability, Vol 14, No. 1, 459-488.

- [34] Zhang, J., 2001, Some fine properties of backward stochastic differential equations, Ph.D Thesis, Purdue University.

- [35] Zhang, J., 2017, Backward Stochastic Differential Equations, Probability Theory and Stochastic Modelling 86, Springer, N.Y.