Empirical regression quantile process with possible application to risk analysis

Abstract.

The processes of the averaged regression quantiles and of their modifications provide useful tools in the regression models when the covariates are not fully under our control. As an application we mention the probabilistic risk assessment in the situation when the return depends on some exogenous variables. The processes enable to evaluate the expected -shortfall () and other measures of the risk, recently generally accepted in the financial literature, but also help to measure the risk in environment analysis and elsewhere.

Key words and phrases:

Averaged regression quantile, one-step regression quantile, R-estimator, risk measurement1991 Mathematics Subject Classification:

Primary 62J02 , 62G30; Secondary 90C05, 65K05, 49M29, 91B301. Introduction

In everyday life and practice we encounter various risks, depending on various contributors. The risk contributors may be partially under our control, and information on them is important, because it helps to make good decisions about system design. This problem appears not only in the financial market, insurance and social statistics, but also in environment analysis dealing with exposures to toxic chemicals (coming from power plants, road vehicles, agriculture), and elsewhere; see [30] for an excellent review of such problems. Our aim is to analyze the risks with the aid of probabilistic risk assessment. In the literature were recently defined various coherent risk measures, some satisfying suitable axioms. We refer to [5], [6], [31], [41], [43], [36], [1], [42], [9], [37], [38], and to other papers cited in, for discussions and some projects. For possible applications in the insurance we refer to [10].

A generally accepted measure of the risk is the expected shortfall, based on quantiles of a portfolio return. Its properties were recently intensively studied. Acerbi and Tasche in [1] speak on ”expected loss in the 100% worst cases”, or shortly on ”expected -shortfall”, which is defined as

| (1.1) |

where is the distribution function of the asset The quantity can be estimated by means of approximations of the quantile function by the sample quantiles.

The quantile regression is an important method for investigation of the risk of an assett in the situation that it depends on some exogenous variables. An averaged regression quantile, introduced in [22], or some of its modifications, serve as a convenient tool for the global risk measurement in such a situation, when the amount of covariates is not under our control. The typical model for the relation of the loss to the covariates is the regression model

| (1.2) |

where are observed responses, are independent model errors, possibly non-identically distributed with unknown distribution functions The covariates are random or nonrandom, and is an unknown parameter. For the sake of brevity, we also use the notation

An important tool in the risk analysis is the regression -quantile

It is a -dimensional vector defined as a minimizer

| (1.3) |

The solution minimizes the convex combination of residuals over where the choice of depends on the balance between underestimating and overestimating the respective losses The increasing reflects a greater concern about underestimating losses Y, comparing to overestimating.

The methodology is based on the averaged regression -quantile, what is the following weighted mean of components of :

| (1.4) |

In [22] it was shown that is asymptotically equivalent to the -quantile of the model errors, if they are identically distributed. Hence, can help to make an inference on the expected -shortfall (1.1) even under the nuisance regression.

Besides , its various modifications can also be used, sometimes better comprehensible. The methods are nonparametric, thus applicable also to heavy-tailed and skewed distribution; notice that [8] speak about considerable improvement over normality, trying to use different distributions. An extension to autoregressive models is possible and will be a subject of the further study; there the main tool will be the autoregression quantiles, introduced in [29], and their averaged versions. The autoregression quantile will reflect the value-at-risk, based on the past assets, while its averaged version will try to mask the past history.

The behavior of with has been illustrated in [4] and [27], and summarized in [25]; here it is showed that is nondecreasing step function of The extreme with was studied in [19]. Notice that the upper bound of the number of breakpoints of and also of is However, Portnoy in [34] showed that, under some condition on the design matrix the number of breakpoints is of order as and thus much smaller.

An alternative to the regression quantile is the two-step regression -quantile, introduced in [21]. Here the slope components are estimated by a specific rank-estimate which is invariant to the shift in location. The intercept component is then estimated by the -quantile of residuals of ’s from The averaged two-step regression quantile is asymptotically equivalent to under a wide choice of the R-estimators of the slopes. However, finite-sample behavior of generally differs from that of is affected by the choice of R-estimator, but the main difference is that the number of breakpoints of exactly equals to .

Being aware of various important applications of the problem, we shall study this situation in more detail. The averaged regression quantile is monotone in while the two-step averaged regression quantile can be made motonone by a suitable choice of R-estimate Hence, we can consider their inversions, which in turn estimate the parent distribution of the model errors. As such they both provide a tool for an inference. The behavior of these processes and of their approximations is analyzed and numerically illustrated.

2. Behavior of over

Let us first describe one possible form of the averaged regression quantile as a weighted mean of the basic components of vector Consider again the minimization (1), fixed fixed. This was treated in [26] as a special linear programming problem, and later on various modifications of this algorithm were developed. Its dual program is a parametric linear program, which can be written simply as

| maximize | ||||

| under | ||||

where

| (2.2) |

The components of the optimal solution of (2), called regression rank scores, were studied in[12], who showed that is a continuous, piecewise linear function of and Moreover, is invariant in the sense that it does not change if is replaced with (see [12] for detail).

Let be the optimal base in (2) and let be the corresponding responses in model (1.2). Then equals to a weighted mean of , with the weights based on the regressors. Indeed, we have a theorem

Theorem 1.

Assume that the regression matrix (2.2) has full rank and that the distribution functions of model errors are continuous and increasing in Then with probability 1

| (2.3) | |||||

| (2.4) |

where the vector corresponds to the optimal base of the linear program (2).

The vector of coefficients equals to

| (2.5) |

where is the submatrix of with the rows

Proof.

The regression quantile is a step function of If is a continuity point of the regression quantile trajectory, then we have the following identity, proven in [22]:

| (2.6) |

where Moreover, (2) implies

| (2.7) | |||

Notice that iff is the point of continuity of and To every fixed continuity point correspond exactly such components, such that the corresponding belongs to the optimal base of program (2). Hence there exist coefficients such that

Let us now consider as a process in Assume that all model errors are independent and equally distributed according to joint continuous increasing distribution function We are interested in the the average regression quantile process

where is the population counterpart of the regression quantile. As proven in [20], the process converges to a Gaussian process in the Skorokhod topology as under mild conditions on and More precisely,

| (2.8) |

where is the Brownian bridge on (0,1).

However, we are rather interested in behavior of the process under a finite number of observations. The trajectories of are step functions, nondecreasing in and they have finite numbers of discontinuities for each . As shown in [7], if for then with probability 1, then the length of interval, on which is constant, tends to 0 for and fixed Let be the breakpoints of and be the corresponding values of between the breakpoints. Then we can consider the inversion of namely

It is a bounded nondecreasing step function and, given satisfying (1.2), is a distribution function of a random variable attaining values with probabilities equal to the spacings of The tightness of the empirical process and its convergence to was studied in [33] under some specific conditions; is recommended as an estimate of which would enable e.g. goodness-of-fit testing about in the presence of a nuisance regression.

3. Properties of the averaged two-step regression quantile

While the advantage of is in its monotonicity, the inference based on the process can be more comprehensible. Hence, we can consider the empirical process based on two-step regression quantiles as an alternative to Both processes are asymptotically equivalent as

The two-step regression -quantile treats the slope components and the intercept separately. The slope component part is an R-estimate of Its advantage is that it is invariant to the shift in location, hence independent of It starts with selection of a nondecreasing function , square-integrable on (0,1). Then we can consider two types of rank scores, generated by

-

(1)

(3.1) where is the ordered random sample of size from the uniform (0,1) distribution.

-

(2)

(3.2)

The test criteria and estimates based on either of these scores are asymptotically equivalent as but the rank tests based on the exact scores are locally most powerful against pertinent alternatives under finite . The R-estimator of the slopes is a minimizer of the [14] measure of rank dispersion

| (3.3) | |||||

| where |

and where can be replaced with Here is the rank of the -th residual, The intercept component pertaining to the two-step regression -quantile is defined as the -order statistic of the residuals The two-step -regression quantile is then the vector

| (3.4) |

The typical choice of is the following:

| (3.5) |

combined with the approximate scores (ii) in (3.2). These scores were originated in [15]; he used the following scores [now known as Hájek’s rank scores]:

| (3.6) |

The solutions of (3.3) are generally not uniquely determined. We can e.g. take the center of gravity of the set of all solutions; however, the asymptotic representations and distributions apply to any solution.

Define the averaged two-step regression -quantile as

| (3.7) |

By (3.3),

| (3.8) |

hence it is equal to the -th order statistic of the residuals Then is obviously scale equivariant and regression equivariant. [21] originally considered the two-step regression -quantile with in (3.5) for each in the R-estimator of the slopes. The averaged two-step version corresponding to this choice is very close to but for finite it is generally not monotone in However, it suffices to consider fixed, independent of this makes monotone in thus invertible and simpler. is asymptotic equivalent to under general conditions, hence also asymptotically equivalent to Hence is a convenient tool for an inference under a nuisance regression. The asymptotic equivalence of and will be proven under the following mild conditions on and on

- (A1):

-

Smoothness of : The errors are independent and identically distributed. Their distribution function has an absolutely continuous density and positive and finite Fisher’s information:

- (A2):

-

Noether’s condition on regressors:

- (A3):

-

Rate of regressors:

We shall prove the asymptotic equivalence for R-estimators based on score function because of its simplicity. However, an analogous proof applies to an R-estimator generated by any nondecreasing and square-integrable function

Theorem 2.

Proof.

Let us write

| (3.11) | |||

We shall study the -quantile of variables

Recall the Bahadur representation of sample -quantile of

| (3.12) |

a.s. as Under conditions (A1)–(A3), the R-estimator admits the following asymptotic representation:

| (3.13) | |||

hence The details for (3) and (3.13) can be found in [23].

The quantile of is a solution of the minimization

where Denote as the right-hand derivative of i.e. Using Lemma A.2 in [39], we can show that

| (3.14) | |||

almost surely as Notice that hence we conclude from [23], Lemma 5.5, that it holds

| (3.15) |

for every Inserting into (3), we obtain

| (3.16) |

Combining (3), (3.14)–(3), we conclude that as hence

| (3.17) |

what gives (3.9). This together with Theorem 2 in [22] implies (3.10). ∎

Remark 1.

can be replaced by any -consistent R-estimator of However, the score function of type is more convenient for computation and hence more convenient for applications. Various choices of R-estimators are numerically compared in Section 4.

4. Computation and numerical illustrations

The simulation study describes the methods for computation of the proposed estimates and illustrates their properties. For the computation of the averaged regression quantile the R package quantreg and its function rq() is used; it makes use of a variant of the simplex algorithm.

Concerning the two-step averaged regression quantile , the most difficult is the first step - the computation of the R-estimator of the slopes. In the numerical illustration below the score function from (3.5) and the approximate scores (i) from (3.2) are applied. In this case the function rfit() from the R package Rfit could be directly used. For the rfit() function the score function corresponding to (3.5) and (i) of (3.2) has to be defined, i.e. at point attaining the value . The function rfit() uses the minimization routine optim() which is a quasi-Newton optimizer. This method works well for simple linear regression model but is less precise in case of multiple regression. So, it is better to use the fact that when employing the score function (3.5) with and the approximate scores (i) from (3.2) the slope components of the regression -quantile and the two-step regression -quantile coincide, for every fixed , see [20]. Therefore, the rq() function from the quantreg package is then used to find the exact solution .

The averaged regression quantile and the two-step averaged regression quantile (and their inversions) can be used as the estimates of the quantile function (and of the distribution function, respectively) of the model errors. The behavior of the proposed estimates is illustrated in the following simulation study.

The regression model

| (4.1) |

is simulated with the following parameters:

-

•

sample size ,

-

•

,

-

•

.

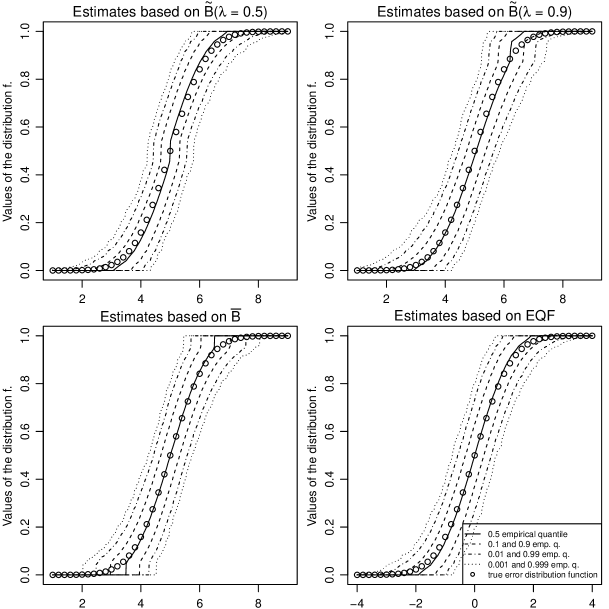

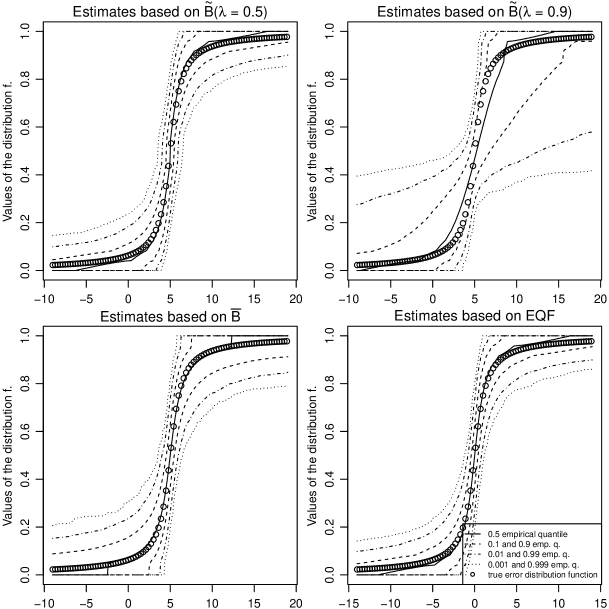

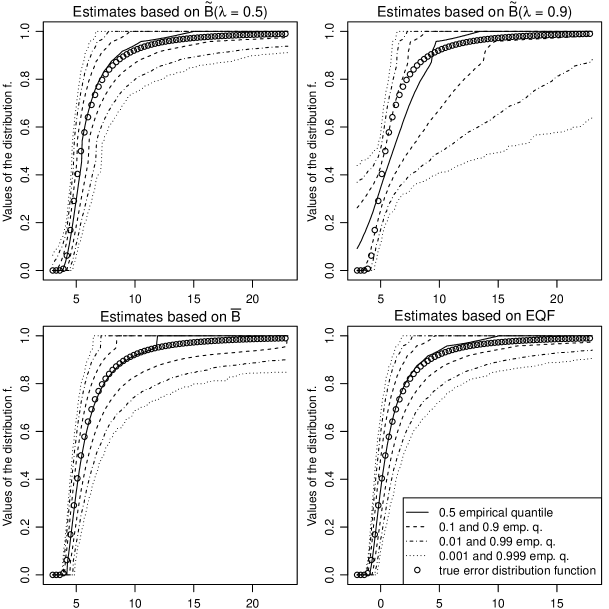

The columns of the regression matrix and are generated as two independent samples from the uniform distributions and , respectively, and are standardized so that . The errors are generated from the standard normal, the standard Cauchy or the generalized extreme value (GEV) distribution with the shape parameter . For each case replications of the model were simulated and and and their inversions were computed. For the two-step version the score-generating function (3.5) with fixed or was used. For a comparison, the empirical quantile function of the errors and its inversion were calculated as well. Empirical quantile estimates based on and on were then calculated and plotted. Since the figures showing estimates of the true quantile functions and of the true distribution functions look very similar, up to the inversion, only the figures for the distribution functions are presented. The statistical software R was used for all calculations.

The Figures 1 - 3 show the empirical quantile estimates of the normal, Cauchy and GEV distribution functions. The approximation of the distribution functions appears to be very good. We notice that in the case of two-step regression quantile with fixed, the quality of the estimate is sensitive to the choice of , especially for skewed or heavy-tailed distributions. The choice around is generally recommended.

5. Conclusion

The averaged regression quantile and its two-step modification appear to be very convenient tools in the analysis of various functionals of the risk in the situation that the this depends on some exogenous variables, in the intensity that is not fully under our control. The choice of provides a balance between the concerns about underestimating and overestimating the losses in the situation. The increasing reflects a greater concern about underestimating the loss, comparing to overestimating. Both and can be advantageously used in estimating the expected shortfall (1.1) and other modern measures of the risk, as well as estimating and testing other characteristics of the market or the everyday practice, based on the functionals of the quantiles.

References

- [1] Acerbi, C. and Dirk Tasche, D.: Expected shortfall: A natural coherent alternative to value at risk, Economic Notes, 31, (2002), 379–388.

- [2] Angrist, J., Chernozhukov, V. and Fernández-Val, I.: Quantile regression under misspecification, with an application to the U.S. wage structure, Econometrica, 74, (2006), 539–563.

- [3] Arias, O., Hallock, K. F. and Sosa-Escudero, W.: Individual heterogeneity in the returns to schooling: Instrumental variables quantile regression using twins data, Empirical Economics, 26, (2001), 7–40.

- [4] Bassett, G.W. Jr., A property of the observations fit by the extreme regression quantiles, Comp. Stat. Data Anal., 6, (1988), 353–359.

- [5] Artzner, P., Delbaen, F., Eber, J.-M. and Heath, D.: Thinking coherently, RISK, 10/11, (1997).

- [6] Artzner, P., Delbaen, F., Eber, J.-M. and Heath, D.: Coherent measures of risk, Math. Fin., 9, (1999), 203–228.

- [7] Bassett, G. W. and Koenker, R. W.: An empirical quantile function for linear models with iid errors, J. Amer. Statist. Assoc., 77, (1982), 405–415.

- [8] Braione, M. and Scholtes, N. K.: Forecasting value-at-risk under different distributional assumptions, Econometrics, 4, (2016), 2–27.

- [9] Cai, Z. and Wang, X.: Nonparametric estimation of conditional VaR and expected shortfall, Journal of Econometrics, 147, (2008), 120–130.

- [10] Chan, J. S .K., Predicting loss reserves using quantile regression, Journal of Data Science, 13, (2015), 127–156.

- [11] Carroll, R. J., Maca, J. D. and Ruppert, D.: Nonparametric regression in the presence of mesurement error, Biometrika, 86, (1999), 541–554.

- [12] Gutenbrunner,C. and Jurečková, J.: Regression rank scores and regression quantiles, Ann. Statist., 20, (1992), 305–330.

- [13] Gutenbrunner,C., Jurečková, J., Koenker, R. and Portnoy, S.: Tests of linear hypotheses based on regression rank scores, Nonpar. Statist., 2, (1993), 307–331.

- [14] Jaeckel, L. A.: Estimating regression coefficients by minimizing the dispersion of the residuals, Ann. Math. Statist., 43, (1972), 1449–1459.

- [15] Hájek, J., Extension of the Kolmogorov-Smirnov test to regression alternatives, In: Proceedings of the International Research Seminar, LeCam, L., Editor, Univ. of California Press, Berkeley, (1965), 45–60.

- [16] Jurečková, J.: Asymptotic relation ofM-estimates and R-estimates in the linear regression model, Ann. Statist., 5, (1977), 464–472.

- [17] Jurečková, J.: Remark on extreme regression quantile, Sankhy, 69, (2007), 87–100.

- [18] Jurečková, J.: Remark on extreme regression quantile II, In: Proceedings of the 56th Session, Section CPM026, (2007).

- [19] Jurečková, J.: Finite sample behavior of averaged extreme regression quantile, Extremes, 19, (2016), 41–49.

- [20] Jurečková, J.: Regression Quantile and Averaged Regression Quantile Processes, In: Analytical Methods in Statistics, J. Antoch et al. (Eds.), Springer Proceedings in Mathematics and Statistics, (2017), 53–62.

- [21] Jurečková, J. and Picek, J.: Two-step regression quantiles, Sankhy, 67, (2005), 227–252.

- [22] Jurečková, J. and Picek, J.: Averaged regression quantiles, In: Contemporary Developments in Statistical Theory, Lahiri, S. et al. (Eds.), Springer Proceedings in Mathematics and Statistics, 68, (2014), 203–216.

- [23] Jurečková, Sen, P.K., Picek, J.: Methodology in Robust and Nonparametric Statistics, (2013), CRC Press.

- [24] Knight, K.: Limiting distributions for linear programming estimators, Extremes, 4, (2001), 87–103.

- [25] Koenker, R.: Quantile Regression, (2005), Cambridge University Press, Cambridge, UK.

- [26] Koenker, R. and Bassett, G.: Regression quantiles, Econometrica, 46, (1978), 33–50.

- [27] Koenker, R. and Bassett, G.: An empirical quantile function for linear models with iid errors, J. of the American Statist. Assoc., 77, (1982), 407–415.

- [28] Koul, H. L.: Weighted empirical processes in dynamic nonlinear models, Lecture Notes in Statistics, 166, (2000), Springer-Verlag.

- [29] Koul, H. L. and Saleh, A. K. Md. E.: Autoregression quantiles and related rank-scores processes, Ann. Statist., 23, (1995), 670–689.

- [30] Molak, V. (ed.): Fundamentals of risk analysis and risk management, (1997), CRC Press.

- [31] Pflug, G.: Some remarks on the value-at-risk and the conditional value-at-risk, In: Probabilistic Constrained Optimization: Methodology and Applications (Uryasev, S., ed.), (2000), Kluwer Academic Publishers.

- [32] Pollard, D.: Asymptotics for least absolute deviation regression estimators, Econometric Theory, 7, (1991), 186–199.

- [33] Portnoy, S.: Tightness of the sequence of empiric c.d.f. processes defined from regression fractiles, In: Robust and Nonlinear Time Series Analysis, Franke, J. et al. eds., Lecture Notes in Statistics, 26, (1984), 231–245.

- [34] Portnoy, S.: Asymptotic behavior of the number of regression quantile breakpoints, SIAM J. Sci. Statistical Computing, 12, (1991), 867–883.

- [35] Portnoy, S. and Jurečková, J.: On extreme regression quantiles, Extremes, 2, (1999), 227–243.

- [36] Rockafellar, R.T. and Uryasev, S.: Conditional Value-at-Risk for general loss distributions, Research report 2001-5, ISE Depart., University of Florida, (2001).

- [37] Rockafellar, R.T. and Uryasev, S.: Rockafellar, R. T. and Uryasev, S., The Fundamental Risk Quadrangle in Risk Management, Optimization and Statistical Estimation, Surveys in Operations Research and Management Science, 18, (2013), 33–53.

- [38] Rockafellar, R. T., Royset, J. O. and Miranda, S. I.: Superquantile regression with applications to buffered reliability, uncertainty quantification, and conditional value-at-risk, European Journal of Operational Research, 234, (2014), 140–154.

- [39] Ruppert, D. and R. J. Carroll: Trimmed least squares estimation in the linear model, J. Amer. Statist. Assoc., 75, (1980), 828–838.

- [40] Smith, R.: Nonregular regression, Biometrika, 81, (1994), 173–183.

- [41] Tasche, D.: Conditional expectation as quantile derivative, Working paper, TU München, (2000).

- [42] Trindade, A. A. , Uryasev, S., Shapiro, A. and Zrazhevsky, G: Financial prediction with constrained tail risk, Journal of Banking & Finance, 31, (2007), 3524–3538.

- [43] Uryasev, S.: Conditional Value-at-Risk: Optimization Algorithms and Applications, Financial Engineering News, 2/3, (2000).