On the Hardness of Inventory Management with Censored Demand Data

Abstract

We consider a repeated newsvendor problem where the inventory manager has no prior information about the demand, and can access only censored/sales data. In analogy to multi-armed bandit problems, the manager needs to simultaneously “explore” and “exploit” with her inventory decisions, in order to minimize the cumulative cost. We make no probabilistic assumptions—importantly, independence or time stationarity—regarding the mechanism that creates the demand sequence. Our goal is to shed light on the hardness of the problem, and to develop policies that perform well with respect to the regret criterion, that is, the difference between the cumulative cost of a policy and that of the best fixed action/static inventory decision in hindsight, uniformly over all feasible demand sequences. We show that a simple randomized policy, termed the Exponentially Weighted Forecaster, combined with a carefully designed cost estimator, achieves optimal scaling of the expected regret (up to logarithmic factors) with respect to all three key primitives: the number of time periods, the number of inventory decisions available, and the demand support. Through this result, we derive an important insight: the benefit from “information stalking” as well as the cost of censoring are both negligible in this dynamic learning problem, at least with respect to the regret criterion. Furthermore, we modify the proposed policy in order to perform well in terms of the tracking regret, that is, using as benchmark the best sequence of inventory decisions that switches a limited number of times. Numerical experiments suggest that the proposed approach outperforms existing ones (that are tailored to, or facilitated by, time stationarity) on nonstationary demand models. Finally, we consider the “combinatorial” version of the repeated newsvendor problem, that is, single-warehouse multi-retailer inventory management of a perishable product. We extend the proposed approach so that, again, it achieves near-optimal performance in terms of the regret.

Keywords: repeated newsvendor problem, demand learning, censored observations, regret minimization, Exponentially Weighted Forecaster.

1 Introduction

We consider the multi-period inventory management problem of a perishable product, like newspapers, fresh food, or certain pharmaceutical products, where no prior information is available about the demand for the product over the different periods. This may be the case when a new product is introduced to the market, or when the market conditions for an existing product change drastically, e.g., due to a major competitor entering/exiting the market, due to a major economic downturn etc. An additional complication comes from the fact that, often times, the inventory manager cannot observe the actual demand for the product due to censoring: the firm is unable to measure or estimate accurately lost sales, so the manager has access only to sales data. However, the sales depend on the manager’s prior inventory decisions, making inferences about the underlying demand much harder. In such scenarios, the inventory manager is faced with a dynamic learning problem, having to simultaneously “explore” with her inventory decisions in order to learn the underlying demand, as well as “exploit,” that is, focus mostly on decisions that are likely to incur low cost. Due to its practical importance and intellectual challenge, the problem of inventory management with demand learning through censored data has attracted significant attention from the academic community, leading to valuable insights as we detail below.

Our main motivation, and point of departure from the existing literature, stems from the fact that the demand for a product may very well be nonstationary: trends and seasonalities are very common in a demand time series; competition in the market that a firm operates may change over time, in terms of both the assortments and the prices offered; consumers may time their decisions strategically. Our goal is to develop a framework that incorporates, in a tractable way, the potentially nonstationary nature of the demand, to explore the fundamental limits of performance in this setting and propose suitable inventory management policies, and to shed light on the performance loss compared to the case where the demand is time-stationary. Accordingly, we adopt a “nonstochastic” viewpoint: we formulate the problem of inventory management under censored demand as a repeated game between the inventory manager and the market, without making any probabilistic assumptions on the mechanism via which the market generates the demand. We evaluate the performance of different policies with respect to the regret criterion, that is, the difference between the cumulative cost of a policy and the cumulative cost of the best fixed action/inventory decision in hindsight, for a given demand sequence, and provide performance guarantees that hold uniformly over all demand sequences.

The above viewpoint is also referred to in the literature as the “adversarial” approach, although this term is somewhat unfortunate: in our setting, the market chooses a sequence of demands for the different time periods arbitrarily, as far as the inventory manager is concerned. Importantly though, the market does not adapt its strategy according to the actions of the inventory manager. Indeed, it seems far-fetched to assume that an entire market adapts, and acts adversarially, to the inventory decisions of a firm. So, while our modeling framework can capture demand correlations and nonstationarities to a significant extent, it is certainly not a game-theoretic model.

In the remainder of the introduction we provide a detailed account of the existing literature on the repeated newsvendor problem with demand learning, we give some background on the nonstochastic approach to dynamic learning problems, and we highlight the main contributions of the present paper.

1.1 Related Literature

Stochastic inventory theory is a field with a long history and rich literature. A detailed account of this literature is beyond the scope of our paper, so we refer the interested reader to Porteus (2002). It could be argued that one of the most influential contributions in this field is the development and analysis of the newsvendor model, where a manager has to make an inventory decision in anticipation of uncertain demand over a single selling period, aiming at minimizing the total expected overage and underage cost. Elementary arguments can show that the optimal inventory decision is a critical quantile of the demand distribution. Equally important is the mathematical model of multi-period inventory management of a nonperishable product with uncertain demand, whose dynamic programming formulation gives rise to the optimality of inventory replenishment policies. To some extent both models are related to our work, as we consider a multi-period inventory management problem of a perishable product, that is, a repeated newsvendor problem. However, a common (and critical) assumption in both models, and in “classical” stochastic inventory theory overall, is that even though the inventory manager does not know the realization of future demand, she does have access to an accurate probabilistic description of it, for example, via historical data. We do not make this assumption in our work.

Throughout the years, there have been several attempts to relax the assumption that the correct distribution of future demand is available. The most followed approach is to assume that the demand belongs to a particular family of probability distributions, but one or more parameters are unknown. This parametric approach is usually cast in a Bayesian learning framework: a prior on the parameters is also assumed, and the belief about the true parameter values is updated with observed demand samples through Bayes rule. Early works in that direction include Scarf (1959), Karlin (1960), and Iglehart (1964), which focus on exponential families of demand distributions. Murray and Silver (1966) and Azoury (1985) consider variants of the problem and incorporate Bayesian learning into a dynamic programming framework, while Chang and Fyffe (1971) uses the Kalman filtering approach to achieve efficient learning/forecasting. Finally, Lovejoy (1990) shows the near-optimality of simple myopic inventory management policies, when combined with adaptive tuning of the parameters via Bayes rule or exponential smoothing.

A common characteristic of the above works is that the inventory manager has access to the realized demand, in order to update her beliefs. During stock-outs, however, it is often the case that excess demand is lost, making it very hard to measure or estimate the realized demand. In other words, on many occasions it may be more realistic to assume that the inventory manager has access only to the sales, that is, censored demand data. The main insight here is that a dynamic analysis is required even in the case of a perishable product, and that the optimal inventory decision is higher than that of a Bayesian myopic policy, a phenomenon that is referred to in the literature as “information stalking.” The intuition behind it is that this additional inventory gives, occasionally, some extra uncensored demand samples, which contribute towards learning the true parameter values and are, thus, useful in the future. Consequently, some level of “experimentation/exploration” is necessary when dealing with censored demand. This result was first proved in Harpaz et al. (1982) in the context of a perfectly competitive firm making output decisions in the presence of demand uncertainty, and later cast in an inventory management setting and strengthened in Ding et al. (2002) and Lu et al. (2008).111Interestingly, a similar insight has been derived in a dynamic pricing context in Braden and Oren (1994). Lariviere and Porteus (1999) derives a closed-form expression for the Bayesian optimal inventory level if the demand belongs to the class of “newsvendor distributions” developed in Braden and Freimer (1991), and confirms that it is optimal to enhance learning through stocking higher. Recently, Besbes et al. (2015a), building on the framework of Lariviere and Porteus (1999), provides both analytical and numerical evidence to the fact that, while there is cost in being myopic (instead of far-sighted, in the Dynamic Programming sense), this cost is actually quite small. Hence, a Bayesian myopic policy is near-optimal, apart from being easy to implement. Moreover, the cost of censoring, despite being not too large either, is about an order of magnitude greater than the cost of myopia, so the inventory manager should direct her efforts in measuring/estimating lost sales.

The picture becomes more complicated in the case of nonperishable products: the inventory carried over from previous periods may force the inventory manager to stock higher or lower compared to the Bayesian myopic benchmark; see Chen and Plambeck (2008), where the effect of substitutable products is also studied. In a follow-up work, Chen (2010) develops improved bounds and heuristics for the problem.

A fundamental limitation, and the standard criticism against the parametric approach, is that if the parametric family adopted is not broad/flexible enough to capture the underlying demand process, estimating the best parameter values is of little help in really learning the demand, and then managing the inventory in a cost-effective way. Hence, in parallel to the aforementioned parametric approach to stochastic inventory theory with uncertainty regarding the demand distribution, a literature following a nonparametric approach has also been developing. The setting here is one where the inventory manager has no prior information on the demand, other than the fact that it is mutually independent (and in some cases, also identically distributed) over different time periods, and she has access to censored demand data. Burnetas and Smith (2000) and Kunnumkal and Topaloglu (2008) propose stochastic approximation algorithms for ordering and pricing, and prove their asymptotic optimality, without providing any rates of convergence though. Adaptive value-estimation methods that take advantage of the convexity of the newsvendor cost function are presented in Godfrey and Powell (2001) and Powell et al. (2004). Again, the convergence of these algorithms to the optimal solution is established, but the rate of convergence is explored only numerically. Huh et al. (2011) proves the asymptotic optimality of a myopic inventory control policy based on the Kaplan-Meier estimator, and compares the performance that it achieves to previously proposed policies through extensive computational experiments and for various classes of distributions. Finally, in the related setting of a repeated stochastic capacity control problem, van Ryzin and McGill (2000) proposes a stochastic approximation algorithm, whereas Maglaras and Eren (2015) introduces a methodology based on maximum entropy distributions. Similarly to all the works in this thread, the asymptotic convergence of these algorithms is established but the rates of convergence are not addressed.

The papers that come closest to our work are Huh and Rusmevichientong (2009) and Besbes and Muharremoglu (2013). Both consider the inventory management of a perishable product, in other words, a repeated newsvendor problem over time periods, and follow the nonparametric approach: the manager has no prior information on the demand - assumed to be independent and identically distributed over different time periods, drawn from an unknown distribution - and has access only to censored demand data. The objective is to minimize the expected regret, that is, the difference between the expected incurred cost and the optimal expected cost, had the demand distribution been known a priori. Huh and Rusmevichientong (2009) proposes an adaptive inventory management algorithm based on the methodology of online convex optimization (OCO); see Zinkevich (2003). This algorithm has expected regret that scales as , which is the minimax optimal scaling. This can be improved to if the demand has a continuous density, uniformly bounded away from zero. We note that the stationarity of the underlying demand is not crucial for OCO,222In fact, Zinkevich (2003) does not make this assumption. but the fact that demand and inventory are continuous quantities is important: this is a gradient descent-type algorithm, and the continuity of state and action spaces implies that a direction of cost improvement is available almost surely, irrespective of censoring. Consequently, in the case of discrete demand, their methodology requires the existence of a lost-sales indicator to recover the scaling of the expected regret. As we illustrate in our numerical experiments, in the absence of such an indicator, this approach cannot guarantee sublinear regret.

On the other hand, the objective in Besbes and Muharremoglu (2013) is to understand the impact of the available information/feedback structure (fully observable/censored/partially censored demand) on the optimal scaling of the expected regret.333Relatedly, following the parametric approach, Bensoussan and Guo (2015) and Jain et al. (2015) compare the optimal inventory management policies under different information levels (observable lost sales/unobservable lost sales but observable stock-out times/unobservable lost sales and stock-out times), and conclude that through additional information, improved performance can be achieved. In a different direction but still in a parametric setting, Mersereau (2015) studies the impact of inventory record inaccuracy when combined with censored demand samples. In the case of discrete demand and censored observations, which is most relevant to our work and often the case in practice, the authors develop an algorithm based on alternating exploration and exploitation intervals whose expected regret scales as , which is the minimax optimal scaling.444The discrepancy between the results in Huh and Rusmevichientong (2009) and Besbes and Muharremoglu (2013) in the case of discrete demand stems from the fact that the latter study makes somewhat stronger assumptions regarding the families of distributions allowed. In particular, it is assumed that the expected cost function is not “too flat” around the optimal ordering quantity, that is, the separation between the optimal and the best suboptimal ordering quantity is bounded from below by some , and the upper bound on the expected regret of their algorithm also scales as . Overall, the proposed algorithm is well equipped to deal with the discreteness of the demand, and the issues it may create when combined with censoring, but the stationarity of the underlying demand process seems to be crucial here: the exploration intervals could lead to very poor inferences, and hence performance during the subsequent exploitation intervals, if the demand is nonstationary.

Finally, in a related setting and with the same motivation as our work, is the recent contribution Besbes et al. (2015b). The authors develop a modeling and algorithmic framework for non-stationary stochastic optimization, an adaptation of the OCO setting where: (i) the actions of the nature/adversary are constrained by a variational budget; (ii) the comparator sequence is not static (i.e., a fixed action) but rather a dynamic oracle, a feature that bodes well with their focus on non-stationary environments. One of the main insights of the paper is to show that algorithms that perform well for OCO, can be successfully adapted for non-stationary stochastic optimization. On the other hand, the theory is developed in a quite abstract setting, so it does not take advantage of the special structure of the inventory management problem at hand. Moreover, and quite importantly, extending their approach to settings with limited feedback, such as censored data, is a challenging task, e.g., Besbes et al. (2014) explores the case of bandit feedback. As discussed earlier in the approach of Huh and Rusmevichientong (2009), OCO-based algorithms may not have guaranteed performance if a direction of cost improvement is not always available, e.g., through a lost-sales indicator.

Our goal is to fill the conceptual gap that exists between these influential works, that is, to devise an inventory management policy that learns from censored data without making any parametric assumptions, and which has guaranteed performance under discrete and nonstationary555It may be worthwhile to mention a thread in the literature that develops online approximation algorithms for inventory management problems, which are based on marginal cost accounting and cost balancing, and have guaranteed worst-case performance; see Levi et al. (2007), Levi et al. (2008), and several follow-up works. While their framework allows for correlated and nonstationary demand processes, which is a big part of our motivation, there is no learning, and hence no censoring problem in their case: given a realization of past demand and possibly additional information, a conditional joint distribution of future demand is assumed to be available. demand; in fact, near-optimal performance in terms of the regret criterion. Both features are quite important in practice, and as we elaborate below, jointly, they require a different methodological approach than the ones existing in the literature on stochastic inventory theory. Moreover, in existing works, action space (orders) and outcome space (demand) coincide. In practice, however, there may be only few, predetermined ordering levels, for example, due to fixed ordering cost. Accordingly, we disentangle the two, and provide more refined results that highlight the scaling of the expected regret not only with respect to the number of time periods, but also with respect to the number of ordering decisions available and the size of the demand support. We note that our approach has guaranteed performance not only with respect to the standard notion of regret, which is based on the best fixed action, in hindsight, but also with respect to the tracking regret, a much stronger benchmark. Furthermore, we discuss the possibility of extending our approach to even stronger benchmarks, such as the dynamic regret of Besbes et al. (2015b).

1.2 A Nonstochastic Approach to Dynamic Learning Problems

To understand why, and how, our methodological approach deviates from previous literature on stochastic inventory theory, let us put the repeated newsvendor problem with demand learning in a broader context, that of sequential prediction: a forecaster observes one after the other the elements of a sequence of outcomes Before the element of the sequence is revealed, the forecaster predicts its value on the basis of the previous observations. In the “classical” statistical theory of sequential prediction, the sequence of outcomes is assumed to be a realization of a stationary stochastic process. Under this hypothesis, statistical properties of that process may be estimated on the basis of the sequence of past observations, and effective prediction rules/policies can be derived from these estimates.666For instance, in the context of the repeated newsvendor model with time-stationary demand whose underlying distribution is unknown, one would use past observations to estimate the critical quantile of the demand distribution, which is the optimal solution when that distribution is known. In such a setting, the performance of a policy is captured through the expected value (with respect to the probability distribution governing the process) of some loss function measuring the discrepancy between predicted values and true outcomes.

On certain occasions though, an underlying probabilistic structure (in particular, time stationarity) may be hard to justify or estimate. Then, an alternative approach is to view the sequence as the product of some unknown and unspecified mechanism. In lack of any probabilistic assumptions on the sequence, the goal is to come up with prediction rules/policies that perform reasonably well for every possible outcome sequence, that is, to predict individual sequences uniformly well. The lack of probabilistic assumptions also raises the question of how to quantify the forecaster’s performance. To provide a baseline for measuring performance in this setting, one may introduce a class of reference forecasters or “experts.” These experts make their predictions available to the forecaster before each outcome is revealed, and the forecaster makes her own prediction based on the advice of the different experts. The goal of the forecaster is to keep her cumulative loss close to that of the best expert in hindsight (i.e., with full knowledge of the entire sequence of outcomes), or in other words to minimize her regret, uniformly over all outcome sequences.

The literature on prediction of individual sequences originates from repeated games: several of the basic ideas are introduced in the early influential works Blackwell (1956) and Hannan (1957), such as the use of randomization as a powerful tool to achieve low regret when it would be impossible otherwise. In a different strand of literature, Cover (1965), Lempel and Ziv (1976), and Ziv and Lempel (1977) give the information-theoretic foundations of sequential prediction of individual sequences, motivated by the problems of data compression and “universal” coding. More recently, the prediction of individual sequences has become a topic of intense research activity in the subfield of machine learning termed online learning. The pioneering papers De Santis et al. (1988), Littlestone and Warmuth (1989), and Vovk (1990) illustrate how the framework of prediction with expert advice can be transformed into a model of online learning, and a plethora of subsequent works builds on and extends their results; for a comprehensive treatment of the topic the reader is referred to Cesa-Bianchi and Lugosi (2006). Let us note that in this setting, typically, each expert is associated with a different action (e.g., predicted outcome), so the regret of the learner (e.g., the forecaster) is measured against the best fixed action in hindsight.

Of particular interest to us is the literature on partial monitoring, a special case of the online learning paradigm where the information available to the learner is limited in some way. A notable member of this class is the (nonstochastic) multi-armed bandit problem studied in Auer et al. (2002), where the actual outcome is not revealed to the learner after each round. What the learner knows with certainty is the loss of the actions that she takes, but she has no information on the losses of other actions she could have chosen instead. Hence, she has to “explore” in order to learn the losses associated with different actions, and to “exploit” by converging sooner rather than later to the ones she believes have the smallest loss. The main result is that a simple randomized policy, termed the Exponentially Weighted Forecaster (EWF), achieves expected regret777We note that when one refers to expected regret in the context of prediction of individual sequences, the expectation is taken with respect to the randomization induced by the forecasting policy; in essence, with respect to the beliefs of the forecaster. This is because in a nonstochastic setting there is no ground-truth or benchmark distribution to compare against. that scales as , which is also the optimal scaling for the particular problem. Piccolboni and Schindelhauer (2001) extends this setting significantly, to a repeated game between a learner and an opponent, making sequential decisions in a finite action and outcome space, respectively, with the loss and the feedback that the learner receives at the end of each round being arbitrary (but time invariant) functions of the action and outcome chosen during that round. The authors prove that under a relatively mild technical assumption, an adaptation of the EWF achieves expected regret that scales as . Cesa-Bianchi et al. (2006) improves this bound to , and also provides a lower bound of the same order for a specific feedback/loss structure. The question of the exact dependence of the minimax regret on the problem structure was first tackled in Bartók et al. (2011); see also Antos et al. (2013) for the case of stochastic outcomes. This series of research efforts culminated in Bartók et al. (2014), where a complete classification of finite partial monitoring games is provided: “trivial” games where the expected regret does not scale with ; “easy” games where the scaling is ; “hard” games where the scaling is ; and “hopeless” games with scaling . Importantly, there can be no other scaling apart from the aforementioned four, despite the fact that the structure of the game, in terms of both the loss and the feedback functions, can be chosen arbitrarily. A geometric condition, termed local observability, is shown to distinguish “easy” from “hard” games, and generic algorithms are developed for each case, albeit significantly more complicated than the EWF.

It is worthwhile to mention the sole paper on the repeated newsvendor problem with demand learning that adopts the nonstochastic framework, Levina et al. (2010). In their setting, however, there is no censoring, while demand and orders are continuous quantities; both crucial features as explained earlier.

1.3 Main Contributions

As already mentioned above, we focus on the multi-period inventory management problem of a perishable product, that is, a repeated newsvendor problem, where no information on the demand is available a priori, and learning occurs via sales/censored data. Importantly, demand and orders are discrete quantities, and no probabilistic assumptions (in particular, independence or time stationarity assumptions) are made regarding the demand. Our main contributions can be summarized as follows.

-

(1)

We show that the simple EWF policy has expected regret that scales as , which is optimal up to the logarithmic term. Note that even in the case where the demand over different time periods is i.i.d., no better scaling than can be achieved, unless further assumptions are made on the demand; see Section 2.5 in Huh and Rusmevichientong (2009) and Section 2.3 in Besbes and Muharremoglu (2013).

-

(2)

We disentangle the impact of the cardinality of the action space (orders) from that of the outcome space (demand). In particular, we assume that there are ordering points that the inventory manager can choose from at every period, arbitrarily placed within the demand support. We show that the expected regret of the EWF policy scales as , that is, near-optimally. Notably, the general theory developed in Bartók (2013) and Bartók et al. (2014) guarantees only polynomial scaling with respect to . Crucial to the performance of the EWF policy is a carefully designed cost estimator, which leverages the special structure of the problem.

-

(3)

The previous results allow us to reach an important conclusion about the dynamic learning problem at hand: the benefit from “information stalking” as well as the cost of censoring are both negligible, at least with respect to the regret criterion. Intuitively speaking, this seems to extend and solidify the insights in Besbes et al. (2015a), where in a time-stationary setting and for the class of “newsvendor” distributions, the benefit from “information stalking” has been shown to be very small, and the cost of censoring not significant either.

-

(4)

We modify the proposed policy so that it has guaranteed performance with respect to the tracking regret, that is, using as benchmark the best sequence of inventory decisions that switches a limited number of times. The tracking regret is a much stronger benchmark, particularly suitable for nonstationary demand models as our numerical experiments suggest. The tradeoff is a somewhat looser bound: while the scaling of the expected tracking regret with respect to and remains optimal up to logarithmic terms, the upper bound now includes a multiplicative term that relates to the number of times that the reference sequence is allowed to switch actions.

-

(5)

We consider the “combinatorial” version of the repeated newsvendor problem, that is, single-warehouse multi-retailer inventory management of a perishable product, with facility-dependent fixed ordering costs and overage/underage cost rates. We extend our approach so that, again, it achieves expected regret that scales as and , respectively, that is, near-optimally in both cases.

1.4 Outline of the Paper

The remainder of the paper is organized as follows. Section 2 provides a detailed description of our benchmark model, a repeated newsvendor model with demand learning via censored data, gives some necessary background on online learning, and presents the proposed inventory management policy accompanied by a regret analysis. Section 3 introduces the notion of tracking regret, and shows that a modification of the proposed policy has guaranteed performance with respect to the latter criterion. This is followed by extensive numerical experiments in Section 4. Section 5 presents the “combinatorial” version of the repeated newsvendor problem, that is, single-warehouse multi-retailer inventory management of a perishable product, again incorporating demand learning through censored observations from a nonparametric viewpoint. We conclude the paper with a brief commentary in Section 6. All major proofs are relegated to an appendix, at the end of the paper.

2 Inventory Management with Censored Demand Data

2.1 Problem Formulation

Fix , and define the sets and . Also, fix , with , and let be an arbitrary subset of with cardinality . We denote by the indicator variable of event , and by the maximum of scalar and 0.

Consider a firm that sells a single perishable product to the market. The following “game” between the firm’s inventory manager and the market is repeated over time periods: at the beginning of period , the inventory manager chooses an inventory level to have in stock. (So, implicitly, we assume that there is zero lead time between placing and receiving an order.) Simultaneously, the market chooses the demand that the firm experiences during that period, , which is covered up to the extent that the available inventory allows. At the end of the period any remaining inventory perishes, and the firm incurs a cost

| (1) |

where represent the overage and underage cost rates, respectively, which are known to the manager and fixed for all time periods.

An important characteristic of our model is that the inventory manager has no information about the demand prior to the beginning of the game. Moreover, she has to “learn” the demand via censored data: at the end of period , the inventory manager can only observe the sales during that period, . In particular, if the inventory turns out to be less than or equal to the demand, then the inventory manager does not know with certainty the exact demand that the firm experienced, , nor the exact cost that it incurred, .

Fix a sequence of demand realizations . We define the regret of the inventory manager, for any sequence of inventory decisions , to be the difference between the cumulative cost that is actually incurred and the cost that would have been incurred under the best fixed inventory decision, in hindsight:

where is defined similarly to Eq. (1). We denote by the minimizer in the equation above, omitting its dependence on the sequence for convenience.

An important point of our work is that when no probabilistic assumptions are made about the demand, that is, if one adopts the so-called nonstochastic viewpoint, then in many cases randomization is the only way to achieve low regret. Of course, under a randomized inventory management policy the regret is a random variable, so our goal is to design policies that have low expected regret:

| (2) |

where denotes the probability of selecting inventory level at the beginning of time period , conditional on all previous decisions made, that is, .

2.2 Feedback Structure and Local Observability

Before we proceed to the presentation and performance analysis the proposed inventory management policy, we delve into the feedback structure of the problem and make a connection to the notion of local observability, as first defined by Bartók et al. (2011). Understanding and exploiting this structure is precisely what allows for good (near-optimal) scaling of the expected regret with respect to .

Consider an arbitrary pair of inventory decisions , and a demand realization . We wish to compute the difference between the cost of the two actions. Without loss of generality, assume that . (If then, obviously, the difference in cost is zero.) We have that:

-

(i)

, if ;

-

(ii)

, if ;

-

(iii)

, if .

On the other hand, let , with , and denote by the identity matrix, and by the matrix, where if , and 0 otherwise. Finally, let be the -dimensional column vector, with if , and 0 otherwise.

The signal matrix of inventory decision , denoted by , is a matrix, where element if the sales of the firm are equal to , assuming that the demand is equal to and the inventory is equal to , and 0 otherwise. It can be verified that is equal to the concatenated matrix:

The essence of local observability is that the difference in cost between any two inventory decisions, for any demand realization, can be expressed in terms of their signal matrices, that is, the information that the inventory manager receives in the respective cases via the firm’s sales.

Lemma 1.

(Local Observability) Let be arbitrary inventory decisions. There exist vectors and such that

Proof.

Consider the -dimensional column vector , where

Define similarly the vector . The result follows through straightforward calculations. ∎

Lemma 1 implies that the game between the inventory manager and the market is locally observable, in the sense of Definition 6 in Bartók et al. (2014). This classifies the repeated newsvendor problem with demand learning via censored data as an “easy” partial monitoring problem - see Section 1.2 - which implies that the correct scaling of the expected regret is . Below, we introduce a simple policy that is near-optimal with respect to this criterion.

2.3 The Exponentially Weighted Forecaster

The Exponentially Weighted Forecasting (EWF) is a well-studied online learning methodology that simultaneously “explores” and “exploits,” in a randomized way. The main idea behind it is to keep track of not only the cost of actions that are actually taken, but also of the estimated cost of all other actions that could have been taken instead. Of course, the specifics of cost estimation are context-specific, as they are closely tied to the type of feedback that the learner receives. Based on the cumulative estimated cost of the different actions, the learner forms beliefs about the chances each of them has being the best one, in hindsight, and prioritizes future actions accordingly.

More concretely, let be the estimated cost that inventory decision would have incurred at period under demand . Note that, implicitly, may also be a function of the actual inventory decision that was made at period . In fact, that is the case in the cost estimator that we propose below. Similarly, we define as the cumulative estimated cost of (fixed) inventory decision at period , with . The cumulative estimated cost can be computed through the recursion:

For convenience, let us also define and , where is a positive constant whose exact value depends on the primitives of the problem in a way that is specified later on. Using this notation, we have that

| (3) |

The EWF policy chooses inventory with probability

| (4) |

where is another parameter, in the interval, whose precise value will be determined later.

Note that the EWF policy simultaneously “explores” the available action space by making every inventory decision with probability at least , and “exploits” by assigning higher probability to decisions that have low cumulative estimated cost. The precise way that the inventory manager prioritizes between exploration and exploitation depends on the exact values of the and parameters.

While the EWF is a generic and well-studied policy, what takes advantage of the special structure of the problem at hand is the design of the proper cost estimator . To get some insight into what type of estimator may be suitable, let us assume that at period the inventory manager decides to hold inventory . At the end of period , the firm gets (potentially censored) feedback about the demand, that is, the sales . Importantly, this feedback also gives information about the sales that the firm would have had during the particular period, had the inventory manager chosen any :

-

(i)

if the feedback was censored, that is, , then , for all ;

-

(ii)

if the feedback was not censored, that is, , then the demand is known with certainty and the sales can be computed, for all .

We use this insight to define the estimated cost of action under demand as follows:

| (5) |

where and are taken from Lemma 1, , and according to Eq. (4).

Next, we provide some properties regarding the bias and variance of the above estimator, which are critical in the performance analysis that follows.

Lemma 2.

(Bias and Variance of the Estimator) The cost estimator in Eq. (5) satisfies:

so that , and

where and respectively denote the probability and the expectation conditioned on the history of interaction up until the beginning of round .

Proof.

The first part of the lemma follows directly by noting that

The fact that is a direct consequence of being an upper bound on the absolute value of , for every and . Hence, regarding the second part of the lemma, we have that

∎

Note that the proposed estimator is biased, as . In particular, the estimator is pessimistic in the sense that it always overestimates the actual cost incurred. A direct corollary of Lemmas 1 and 2 is the following result.

Lemma 3.

The cost estimator in Eq. (5) is unbiased when inferring the difference in cost between two actions:

The significance of Lemma 3 lies in the fact that the regret, by definition, is a metric that is based on cost differences. This facilitates the analysis in our main result, which characterizes the performance of the proposed inventory management policy with respect to the regret criterion.

Theorem 1.

Consider the repeated newsvendor problem described above. The expected regret of the EWF policy with the cost estimator in Eq. (5) and parameters

is bounded from above as follows:

Proof.

See Appendix 1. ∎

Theorem 1 implies that the expected regret of the EWF policy scales as . On the other hand, the expected regret of any policy in the particular setting scales as , even if the demand over different time periods is i.i.d.; see Section 2.5 in Huh and Rusmevichientong (2009) and Section 2.3 in Besbes and Muharremoglu (2013).

Moreover, the expected regret of the EWF policy scales as . While the correct scaling with respect to is not known, the EWF policy cannot be further than a logarithmic factor off the optimal. We note that the best known scaling of the expected regret for locally observable, partial monitoring problems is , achieved by the algorithm introduced in Bartók (2013), a scaling that we improve considerably upon by taking advantage of the special structure of the problem when designing the cost estimator.

Note that since , the expected regret of the EWF policy scales as . It can be easily verified that the expected regret of any policy scales as so, again, the performance achieved by the EWF policy is near-optimal.

Finally, observe that the suggested choice of the parameters and involves the total number of time periods . Thus, in order to implement the suggested policy, the inventory manager needs to know –or at least an estimate of it–in advance. On the other hand, there are standard ways of getting rid of this assumption in the literature of online learning. In order to avoid tedious but straightforward technicalities, we assume that the inventory manager knows in advance and refer the reader to Section 2.3 of Cesa-Bianchi and Lugosi (2006).

2.4 Benefit from “Information Stalking” and Cost of Censoring

“Information stalking,” that is, the additional exploration that an optimal policy performs in a dynamic learning setting compared to reasonable myopic policies, can be measured in our scenario by the right-most term in Eq. (4), which captures the frequency of purely exploratory decisions made by the EWF policy.888The other term on the right-hand side of Eq. (4) captures the beliefs of the forecaster about each fixed action being the best one, in hindsight. So, the randomization that it induces is not equivalent to exploration. It is, rather, due to the absence of an underlying probabilistic structure. Note that with the optimal selection of the parameter, this term scales like . So, roughly speaking, across all periods and inventory decisions, the proposed policy is expected to explore only a constant number on times, differing little in that sense from a myopic policy. Moreover, the amount of exploration can be reduced arbitrarily: by choosing , for any , the number of expected exploratory decisions is decreasing in , at the cost of a constant term (so, not affecting the scaling) in the upper bound on the expected regret.

Let us also remark on the cost of censoring, that is, the additional cost incurred by having censored observations instead of pure demand samples, as captured by the regret criterion. If there is no censoring in the demand, then one can still use the EWF policy, simply replacing the estimator in Eq. 5 with , the actual cost that would have been incurred if the manager had held inventory at period . By following similar arguments to the proof of Theorem 1, it can be verified that the expected regret of the EWF policy in that case scales as , , and , respectively, in terms of the three key primitives of our problem. We note that this setting falls into the class of online learning problems with full information, and matching lower bounds are known: for a cost function that is defined as the absolute value of the difference between action and outcome, so essentially the newsvendor cost function in Eq. (1), no policy can achieve scaling of the expected regret that is better than the scaling achieved by the EWF policy, for all three key primitives of the problem; see Theorem 3.7 in Cesa-Bianchi and Lugosi (2006). Comparing these to Theorem 1, we have that censoring does not cost more than a root-log factor off the optimal scaling, for all three primitives. In that sense, the cost of censoring is negligible with respect to the regret criterion.

3 Tracking Regret and the Fixed-Share Forecaster

In this section, we consider a stronger notion of regret that compares the total cost incurred by a given policy to that of an arbitrary sequence of inventory decisions. Of course, establishing non-trivial performance guarantees is only possible under some restrictions on either the sequence of demands, or the reference sequence of decisions. Following the work of Herbster and Warmuth (1998), we consider reference sequences that switch between decisions at most times. Clearly, we cannot expect strong guarantees for values of comparable to , so we focus on the case where , which is also the more relevant in practice. Achieving low regret against such comparators intuitively translates to good performance in nonstationary environments, where the demand distribution may change abruptly several times, but otherwise remains roughly stationary for long periods of time.

More formally, let be a sequence of inventory decisions, and let

be the complexity of that sequence, that is, the number of times that switches between two actions. We denote the class of sequences of complexity at most by

Then, we can define the tracking regret against class as

We propose a simple variant of the EWF policy that aims to minimize the tracking regret. This variant is based on the Fixed-Share Forecaster (FSF) introduced in Herbster and Warmuth (1998); see also Auer et al. (2002), Bousquet and Warmuth (2002), and Cesa-Bianchi et al. (2012). The key difference compared to the standard EWF is that instead of using Equation (3) for updating the weights, the FSF policy uses the update rule:

| (6) |

for all in , where is an suitably chosen constant. Otherwise, the probabilities and the cost estimates are computed as described in the previous section. The following result summarizes the performance guarantee that we can prove for the FSF policy.

Theorem 2.

Consider the repeated newsvendor problem. The expected tracking regret of the FSF policy with the cost estimator in Eq. (5) and parameters

is bounded from above, for any , as follows:

Furthermore, for fixed , choosing parameters

leads to an improved bound:

Proof.

See Appendix 1. ∎

4 Numerical Experiments

In this section, we perform a numerical study of the EWF and FSF policies, comparing them to the most relevant existing methods in the literature. The goal of our experiments is to illustrate the robustness of the proposed approach to nonstationary demand sequences, and thus to show the benefits of designing policies that do away with time-stationarity assumptions. We particularly focus on making comparisons to an inventory management policy based on Alternating Exploration and Exploitation phases (AEE), introduced in Besbes and Muharremoglu (2013), which is designed for the same learning problem, albeit tailored to time-stationary demand settings. Our numerical investigation suggests that this assumption is crucial for the AEE policy to perform well: although it has excellent performance in time-stationary settings, by construction, it is unable to adapt to nonstationary demands, and consequently performs very poorly in the latter settings. The online gradient descent-based Adaptive Inventory Management policy (AIM), introduced in Huh and Rusmevichientong (2009), is also closely related to our work. This policy is shown to perform quite well in our numerical experiments. The caveat is that, unlike other policies, it requires a lost-sales indicator to work properly in the case of discrete demand. As we detail in Appendix 2, without such an indicator this policy has linear regret, and may perform poorly even in settings where the demand is constant.

In our numerical experiments, we tune the parameters as follows. Regarding the policies proposed in this paper, we set and , as suggested by Theorems 1 and 2, and , with for the EWF policy and some suitable for the FSF policy. Regarding the AEE policy, we use the parametrization provided in Section 5 of Besbes and Muharremoglu (2013), without resorting to the data aggregation technique described in their Section 5.1. We note that, in our setting, this choice actually works in favor of the AEE policy, as aggregating estimates from early periods is clearly harmful when the demand sequence is nonstationary.

In each experiment, we choose and . Each reported curve is an average of 100 runs, with shaded areas representing the standard deviations.

Finally, to gain some insight into the cost of censoring in practice, we study both the uncensored and the censored versions of each of the policies described above. Note that in the full information case, the policy proposed in Besbes and Muharremoglu (2013) has no reason to explore. Rather, it exploits in a greedy fashion by ordering the empirical critical quantile. We term the resulting policy “greedy-full.”

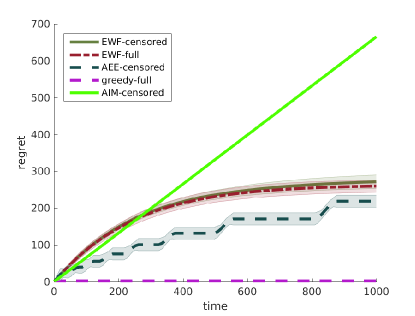

We start by reproducing the first numerical experiment in Section 5 of Besbes and Muharremoglu (2013), where the sequence of demands is i.i.d., with each generated independently from a binomial distribution representing independent trials with a success probability of . The regret of each policy is plotted on Figure 1. In this setting, the AEE policy outperforms the others by a wide margin. In particular, in both the censored and the uncensored cases, the regret of the EWF policy is about 10 times greater than that of the AEE policy. This observation is not surprising: EWF is decidedly more conservative, since it aims to perform reasonably even when the demand is nonstationary.999The inferior performance of general no-regret algorithms, like the EWF, in time-stationary environments has been widely acknowledged in the online learning literature, with some remedies offered by the works of Van Erven et al. (2014); Sani et al. (2014). Nevertheless, the empirical regret of the EWF policy grows in a square-root fashion, in line with our theoretical guarantees.

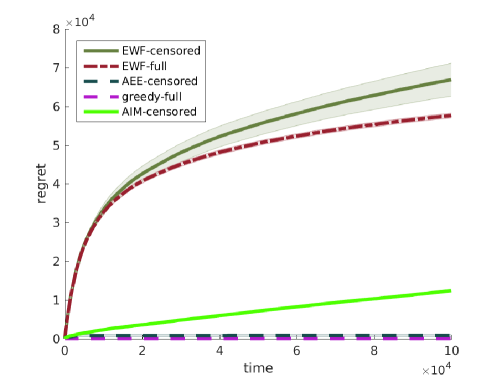

Our second batch of numerical experiments considers a simple nonstationary demand sequence. As before, the demands are generated independently from a binomial distribution with 30 trials, albeit with a time-dependent success probability . Similarly to the previous experiment, we set for most values of , however, this probability drops to for . The performance of each policy is shown on Figure 2; for clarity, we show the cumulative cost incurred by each policy instead of their respective regrets.

The first lesson from this experiment is that the AEE policy fails to cope with the shifting demand distribution, incurring a linearly increasing regret. The intuition behind this is simple: since the policy, effectively, collects data in deterministically (and scarcely) scheduled exploration periods, it is easily thrown off its tracks by a shifting demand distribution. In the particular experiment, the AEE policy bases all its decisions during the interval on data that has nothing to do with the actual demand distribution. The policy has no mechanism to recover from such mistakes, and introducing such a mechanism while maintaining strong performance guarantees, is far from trivial.

In contrast, the EWF policy is robust to this nonstationary behavior. Notably, its cumulative cost in the censored case, using our carefully designed cost estimator, is remarkably close to that in the full-feedback case. This confirms our main insight, that censoring has minimal impact on the performance of well-designed learning policies in this setting. We also highlight the excellent performance of the FSF policy: ran with , that is, correctly anticipating shifts in the comparator sequence, this policy is seen to react much quicker to the distributional shifts compared to the standard EWF variant, thus achieving superior performance.

As a concluding remark, let us note that the performance of the AIM policy is quite good in both experiments; in fact, superior to that of the EWF/FSF policies. This suggests that on some occasions, it may constitute a viable option. The main disadvantage is that in the absence of performance guarantees (i.e., when a lost-sales indicator is not available), it is hard to know in advance how well will this policy perform. We refer the reader to Appendix 2 for further discussion. It is reasonable, of course, to conjecture that as the demand becomes more fine-grained, the value of the lost-sales indicator decreases and, thus, the AIM policy performs better; see also Section 5.2 in Besbes and Muharremoglu (2013). However, apart from few numerical experiments, little else is known in terms of quantifying the rate at which the discrete setting “converges” to a continuous one, and the corresponding effect on the performance of online gradient descent-based policies. This simply reiterates the point about the lack of performance guarantees.

5 The Single-Warehouse Multi-Retailer Problem

In this section we extend our benchmark model to include the inventory management problem of a perishable product, for a vertically integrated supply chain with a single warehouse and retailers. Again, the demand in each of the retailers needs to be learned from censored/sales data, and a nonstochastic view of the problem is adopted. As this setting has many commonalities with the model of Section 2, for brevity, we only present the points at which they differ.

Let us denote by the set of retailers . At the beginning of period , the inventory manager allocates units of inventory from the warehouse to retailer . If is not zero, then the retailer incurs a fixed ordering cost of . We assume zero lead times, so the inventory is delivered to the retailer instantaneously. The retailer experiences demand during the particular period. At the end of the period, and depending on the initial inventory and the demand, the retailer incurs overage or underage cost at rates and , respectively, and any remaining inventory perishes. Thus, at the end of time period , retailer incurs a total cost of

We assume that the supply chain operates in a “push” manner, from upstream to downstream. More specifically, the upstream supplier replenishes the inventory of the warehouse with units at the beginning of every time period. The inventory manager allocates different parts of this inventory to the different retailers, but may also have an incentive to keep a part of it at the warehouse, if she believes that the total demand at the retailer level is low. (The overage cost rate usually increases as one moves downstream.) Hence, the cost that the warehouse incurs over time period is equal to

The allocation that the inventory manager can make must belong to the set

The goal of the inventory manager is to minimize the total cost incurred by the warehouse and the retailers throughout the periods. More concretely, the demand sequences and the inventory replenishment level are exogenously determined by the market and the upstream supplier, respectively, and the manager wishes to minimize her expected regret, , over the best fixed (-dimensional) inventory decision, in hindsight.

We refer to this setting as the “combinatorial” version of the repeated newsvendor problem, due to the fact that the manager’s inventory decisions have a combinatorial nature, taking values in . To the best of our knowledge, this setting has not been studied before from the angle of demand learning via censored data, and from a nonstochastic viewpoint. It may be worthwhile to mention, however, some high-level similarity to Shi et al. (2016), where the results in Huh and Rusmevichientong (2009) are extended to the capacitated multi-product case. The model analyzed in Shi et al. (2016) is also a repeated newsvendor model with a combinatorial action space, but the approach is quite different: in order to obtain results for the (arguably harder) case of nonperishable products, strong probabilistic assumptions are made about the demand for the different products.

For convenience, let us define the quantities

and

In what follows, we mimic the approach of Section 2, to construct an inventory management policy that performs well with respect to the regret criterion. At a high level, the proposed policy follows the EWF scheme, but unlike the versions discussed in previous sections, it draws actions in a non-uniform way during the exploration rounds.

Specifically, in each round the policy explores with probability . The exploration procedure generates a random allocation by selecting a retailer index uniformly at random from , and by choosing the order level uniformly at random from . The rest of the allocations can be completed arbitrarily; for simplicity, we choose an order level of for the remaining retailer. The probability of choosing the allocation is denoted by .

Now let us describe the main component of the policy, which is computing the weights of the assignments. Let be the estimated cost that inventory decision would have incurred at period . We compute, recursively, the quantities

where , with . We also use the shorthand notation

In this setting, the EWF policy chooses inventory with probability

Similarly to Section 2, the proper values for parameters and are specified during the analysis stage.

The special structure of the problem is exploited by designing a suitable cost estimator. For every , let

where and are the same as in Lemma 1, and

Through this, we define the estimated cost of inventory decision as

| (7) |

Note that the proposed estimator is designed in order to be unbiased in terms of inferring the difference in expected cost between two decisions:

| (8) | ||||

for every ; a consequence of the local observability property of the feedback structure in the single-retailer setting. Furthermore, it is easy to show that the mean of the estimator satisfies

| (9) |

The following lemma provides a bound on the second moment:

Lemma 4.

The second moment of the estimator defined in Equation (7) satisfies

Proof.

See Appendix 1. ∎

The following theorem establishes a performance guarantee of the proposed allocation policy.

Theorem 3.

Consider the “combinatorial” version of the repeated newsvendor problem described above. The expected regret of the EWF policy with the cost estimator in Eq. (7) and parameters

is bounded from above as

Proof.

See Appendix 1. ∎

As in the single-warehouse setting, the scaling of the expected regret of the EWF policy is near-optimal with respect to both and , similarly to the single-retailer setting in Section 2. Again, we highlight the fact that the logarithmic scaling with respect to is made possible by our carefully designed estimator that assigns non-zero entries to all inventory levels below the realized inventory decision. On the other hand, the scaling with respect to the number of retailers is unlikely to be optimal. To see this, we note that the combinatorial version of the repeated newsvendor problem falls into the broader class of online combinatorial optimization, for which the limitations of the EWF policy are now clearly understood. In particular, Audibert et al. (2014) shows that the EWF policy has, in general, suboptimal performance guarantees in terms of the size of the decision set, essentially translating to a suboptimal scaling with respect to in our case. We conjecture that the optimal scaling with respect to is linear, and it can be achieved by a suitable adaptation of the Component Hedge algorithm in Koolen et al. (2010) (also called Online Stochastic Mirror Descent in Audibert et al. (2014)). We omit a detailed treatment of that direction in order to maintain the clarity of our presentation. We also remark that a similar combination of feedback graphs and combinatorial decision sets is studied in Kocák et al. (2014). An adaptation of their algorithm, termed FPL-IX, combined with our cost estimates, can be shown to satisfy a regret bound identical to our Theorem 3. Details are again omitted for brevity.

Note that from a mathematical standpoint, the role of the cost that the warehouse incurs at every time period is to couple the inventory management problems of the different retailers. However, the exact functional form of is never used. Thus, the approach presented above extends in a straightforward way to the case where the supply chain operates in a “pull” manner, from downstream to upstream. In that case, the inventory manager has no incentive to keep any inventory at the warehouse, since the product is perishable. The only cost that the warehouse incurs is a fixed ordering cost of for procuring the required inventory from upstream:

With this minor modification, the rest of the analysis follows verbatim.

6 Concluding Remarks

We conclude the paper by drawing connections between our setting and two related problems which have attracted the attention of academic research recently, and discussing some directions for future research.

6.1 Two Related Problems

The first problem is bidding in repeated second-price auctions with valuation learning: a bidder participates in second-price auctions for different products, with her valuations of these products being unknown a priori. The bidder learns her true valuation of a given product only if she wins the respective auction, that is, if she submits the highest bid, and her reward in that case is equal to the difference between that valuation and the second highest bid; otherwise, the bidder learns nothing about her valuation and earns no reward. The goal of the bidder is to maximize her expected reward, which translates naturally into an exploration-exploitation tradeoff in her bidding strategy. Weed et al. (2016) studies this problem from a nonstochastic viewpoint, and proposes a bidding policy whose expected regret scales optimally with respect to the number of auctions. There is an intriguing similarity to our problem, in that the learner receives feedback only when her action is greater than the opponent’s, in which case the problem reduces to a full-information one. The cost structure, however, is quite different: in a newsvendor setting the amount of cost incurred depends on the inventory decision of the manager, whereas in a second-price auction the size of the reward is independent of the bid, conditional on winning/not winning the auction. The authors take advantage of this property by introducing a variation of the EWF policy that is based on interval splitting. Their approach does not seem applicable to our setting, and our cost estimator is, not surprisingly, quite different.

The second problem is sequential stock allocation to dark pools: a trader receives amounts of stocks to liquidate at different periods, and allocates these amounts among different dark pools, whose demand for the particular stocks is unknown a priori. The trader learns the demand at a certain dark pool only if the amount of stocks allocated there exceeds it. This problem is formulated as a dynamic learning problem with limited feedback in Ganchev et al. (2010), and analyzed from a nonstochastic viewpoint with regret guarantees in Agarwal et al. (2010). It is not hard to see that this is almost identical to the “combinatorial” newsvendor problem in Section 5, with the main difference being that the amount of inventory that the warehouse receives is constant, whereas the amount of stocks that the trader tries to liquidate may vary. (Relatedly, the notion of regret that the authors adopt is somewhat different than ours.) Hence, one can argue that we analyze a special case of the problem in Agarwal et al. (2010). On the other hand, the expected regret of the policy proposed in the latter paper, for the case of integral allocations, scales as , a result which we improve considerably upon by taking advantage of the local observability property.

6.2 Open Questions

A limitation of our results, as well as of most results on partial monitoring problems, is that they only hold in expectation, and assuming “oblivious” adversaries. While the latter restriction can be easily relaxed by standard techniques (see the discussion in Arora et al., 2012), extending the results to hold with high probability seems like a significant challenge. Indeed, all known algorithms that have such guarantees, such as the Exp3.P policy of Auer et al. (2002) or the Exp3-IX policy of Neu (2015), use optimistically biased estimates of the costs, whereas our proofs crucially rely on using unbiased estimators of cost differences for arbitrary pairs of actions. It is unclear how one can construct estimators that would provide a suitable optimistic bias, simultaneously for all pairs of actions.

Regarding the single-warehouse multi-retailer variant of our setting, we note that the policy proposed in Section 5 is not computationally efficient in its current form. However, it is already unclear how to compute an optimal solution in an efficient way even in the offline variant of this problem (i.e., computing an optimal allocation in perfect knowledge of the demands). If such an efficient way exists, a natural extension of the FPL-IX policy in Kocák et al. (2014) would also admit a computationally efficient implementation, thus settling this question. On the other hand, if the offline problem turns out to be hard, it is unreasonable to expect that there is an efficient algorithm for the online variant that we consider. We leave the study of this offline optimization problem as future work.

In Section 3, we provide an extension to the EWF that guarantees bounds on the tracking regret. While this performance measure is already much more expressive than regret against the best fixed action, we note that there are several, even stronger baselines that can be considered. Two particular performance notions are the strongly adaptive regret, which compares the performance of the learner to the best action within every subinterval of , see Zinkevich (2003); Hazan and Seshadhri (2009); Daniely et al. (2015); Adamskiy et al. (2016); and the dynamic regret, which uses the best sequence of actions as a comparator, see Hall and Willett (2013); Besbes et al. (2014, 2015b); Jadbabaie et al. (2015); Karnin and Anava (2016). The FSF scheme, proposed in Section 3, can be already shown to guarantee non-trivial bounds on its adaptive regret, as revealed by an inspection of the proof of Theorem 2, yet it is unclear whether non-trivial bounds can be achieved on the strongly adaptive regret or the dynamic regret in our setting. Regarding the dynamic regret, we find it likely that the techniques of Besbes et al. (2015b) can be adapted to our setting to achieve meaningful bounds, although one may need additional tools from Besbes et al. (2014) and Karnin and Anava (2016) to deal with partial feedback. The case of strong adaptivity seems to be significantly more complicated: as shown by Daniely et al. (2015), it is impossible to achieve non-trivial strongly adaptive regret guarantees in the multi-armed bandit setting. Since, feedback-wise, our setting is situated between the multi-armed bandit and full information, this negative result does not rule out the possibility to devise strongly adaptive algorithms. We leave this investigation, again, for future work.

Acknowledgements

G. Lugosi was supported by the Spanish Ministry of Economy, Industry and Competitiveness through the grant Grant MTM2015-67304-P (AEI/FEDER, UE). M.G. Markakis was supported by the Spanish Ministry of Economy, Industry and Competitiveness through a Juan de la Cierva fellowship, and the grant ECO2016-75905-R (AEI/FEDER, UE). G. Neu was supported by the UPFellows Fellowship (Marie Curie COFUND program n∘ 600387).

References

- Adamskiy et al. (2016) Adamskiy, Dmitry, Wouter M. Koolen, Alexey Chernov, Vladimir Vovk. 2016. A closer look at adaptive regret. Journal of Machine Learning Research 17(23) 1–21.

- Agarwal et al. (2010) Agarwal, Alekh, Peter Bartlett, Max Dama. 2010. Optimal allocation strategies for the dark pool problem. Proceedings of the International Conference on Artificial Intelligence and Statistics 9–16.

- Alon et al. (2014) Alon, Noga, Nicolò Cesa-Bianchi, Claudio Gentile, Shie Mannor, Yishay Mansour, Ohad Shamir. 2014. Nonstochastic multi-armed bandits with graph-structured feedback. URL https://arxiv.org/abs/1409.8428.

- Antos et al. (2013) Antos, András, Gábor Bartók, Dávid Pál, Csaba Szepesvári. 2013. Toward a classification of finite partial-monitoring games. Theoretical Computer Science 473 77–99.

- Arora et al. (2012) Arora, Raman, Ofer Dekel, Ambuj Tewari. 2012. Online bandit learning against an adaptive adversary: from regret to policy regret. In Proceedings of the 29th International Conference on Machine Learning.

- Audibert et al. (2014) Audibert, Jean-Yves, Sébastien Bubeck, Gábor Lugosi. 2014. Regret in online combinatorial optimization. Mathematics of Operations Research 39(1) 31–45.

- Auer et al. (2002) Auer, Peter, Nicolò Cesa-Bianchi, Yoav Freund, Robert E. Schapire. 2002. The nonstochastic multi-armed bandit problem. SIAM Journal on Computing 32(1) 48–77.

- Azoury (1985) Azoury, Katy S. 1985. Bayes solution to dynamic inventory models under unknown demand distribution. Management Science 31(9) 1150–1160.

- Bartók (2013) Bartók, Gábor. 2013. A near-optimal algorithm for finite partial-monitoring games against adversarial opponents. Proceedings of the Annual Conference on Learning Theory 30 1–15.

- Bartók et al. (2014) Bartók, Gábor, Dean P. Foster, Dávid Pál, Alexander Rakhlin, Csaba Szepesvári. 2014. Partial monitoring – classification, regret bounds, and algorithms. Mathematics of Operations Research 39(4) 967–997.

- Bartók et al. (2011) Bartók, Gábor, Dávid Pál, Csaba Szepesvári. 2011. Minimax regret of finite partial-monitoring games in stochastic environments. S. Kakade, U. von Luxburg, eds., Proceedings of the 24th Annual Conference on Learning Theory.

- Bensoussan and Guo (2015) Bensoussan, Alain, Pengfei Guo. 2015. Technical note–managing nonperishable inventories with learning about demand arrival rate through stockout times. Operations Research 63(3) 602–609.

- Besbes et al. (2015a) Besbes, Omar, Juan Chaneton, Ciamac C. Moallemi. 2015a. The exploration-exploitation trade-off in the newsvendor problem. URL https://papers.ssrn.com/sol3/papers.cfm?abstract_id=2530653.

- Besbes et al. (2014) Besbes, Omar, Yonatan Gur, Assaf Zeevi. 2014. Stochastic multi-armed-bandit problem with non-stationary rewards. Z. Ghahramani, M. Welling, C. Cortes, N.D. Lawrence, K.Q. Weinberger, eds., Advances in Neural Information Processing Systems 27. 199–207.

- Besbes et al. (2015b) Besbes, Omar, Yonatan Gur, Assaf Zeevi. 2015b. Non-stationary stochastic optimization. Operations Research 63(5) 1227–1244.

- Besbes and Muharremoglu (2013) Besbes, Omar, Alp Muharremoglu. 2013. On implications of demand censoring in the newsvendor problem. Management Science 59(6) 1407–1424.

- Blackwell (1956) Blackwell, David. 1956. An analog of the minimax theorem for vector payoffs. Pacific Journal of Mathematics 6(1) 1–8.

- Bousquet and Warmuth (2002) Bousquet, Olivier, Manfred K Warmuth. 2002. Tracking a small set of experts by mixing past posteriors. Journal of Machine Learning Research 3(Nov) 363–396.

- Braden and Freimer (1991) Braden, David J., Marshall Freimer. 1991. Informational dynamics of censored observations. Management Science 37(11) 1390–1404.

- Braden and Oren (1994) Braden, David J., Shmuel S. Oren. 1994. Nonlinear pricing to produce information. Marketing Science 13(3) 310–326.

- Burnetas and Smith (2000) Burnetas, Apostolos N., Craig E. Smith. 2000. Adaptive ordering and pricing for perishable products. Operations Research 48(3) 436–443.

- Cesa-Bianchi et al. (2012) Cesa-Bianchi, Nicolò, Pierre Gaillard, Gábor Lugosi, Gilles Stoltz. 2012. Mirror descent meets fixed share (and feels no regret). P. L. Bartlett, F. C. N. Pereira, C. J. C. Burges, L. Bottou, K. Q. Weinberger, eds., Advances in Neural Information Processing Systems 25. 989–997.

- Cesa-Bianchi and Lugosi (2006) Cesa-Bianchi, Nicolò, Gábor Lugosi. 2006. Prediction, learning, and games. Cambridge University Press.

- Cesa-Bianchi et al. (2006) Cesa-Bianchi, Nicolò, Gábor Lugosi, Gilles Stoltz. 2006. Regret minimization under partial monitoring. Mathematics of Operations Research 31(3) 562–580.

- Chang and Fyffe (1971) Chang, Sang Hoon, David E. Fyffe. 1971. Estimation of forecast errors for seasonal-style-goods sales. Management Science 18(2) B89–B96.

- Chen (2010) Chen, Li. 2010. Bounds and heuristics for optimal bayesian inventory control with unobserved lost sales. Operations Research 58(2) 396–413.

- Chen and Plambeck (2008) Chen, Li, Erica L. Plambeck. 2008. Dynamic inventory management with learning about the demand distribution and substitution probability. Manufacturing & Service Operations Management 10(2) 236–256.

- Cover (1965) Cover, Thomas M. 1965. Behavior of sequential predictors of binary sequences. Transactions of the Prague Conference on Information Theory, Statistical Decision Functions, and Random Processes 263–272.

- Daniely et al. (2015) Daniely, Amit, Alon Gonen, Shai Shalev-Shwartz. 2015. Strongly adaptive online learning. Francis Bach, David Blei, eds., Proceedings of the 32nd International Conference on Machine Learning, Proceedings of Machine Learning Research, vol. 37. PMLR, Lille, France, 1405–1411.

- De Santis et al. (1988) De Santis, Alfredo, George Markowski, Mark N. Wegman. 1988. Learning probabilistic prediction functions. Proceedings of the Annual Workshop on Computational Learning Theory 312–328.

- Ding et al. (2002) Ding, Xiaomei, Martin L. Puterman, Arnab Bisi. 2002. The censored newsvendor and the optimal acquisition of information. Operations Research 50(3) 517–527.

- Ganchev et al. (2010) Ganchev, Kuzman, Yuriy Nevmyvaka, Michael Kearns, Jennifer Wortman Vaughan. 2010. Censored exploration and the dark pool problem. Communications of the ACM 53(5) 99–107.

- Godfrey and Powell (2001) Godfrey, Gregory A., Warren B. Powell. 2001. An adaptive, distribution-free algorithm for the newsvendor problem with censored demands, with applications to inventory and distribution. Management Science 47(8) 1101–1112.

- Hall and Willett (2013) Hall, Eric, Rebecca Willett. 2013. Dynamical models and tracking regret in online convex programming. International Conference on Machine Learning. 579–587.

- Hannan (1957) Hannan, James. 1957. Approximation to bayes risk in repeated play. Contributions to the Theory of Games 3 97–139.

- Harpaz et al. (1982) Harpaz, Giora, Wayne Y. Lee, Robert L. Winkler. 1982. Learning, experimentation, and the optimal output decisions of a competitive firm. Management Science 28(6) 589–603.

- Hazan and Seshadhri (2009) Hazan, E., C. Seshadhri. 2009. Efficient learning algorithms for changing environments. A.P. Danyluk, L. Bottou, M.L. Littman, eds., Proceedings of the 26th Annual International Conference on Machine Learning (ICML 2009), ACM International Conference Proceeding Series, vol. 382. ACM, New York, NY, USA, 393–400.

- Herbster and Warmuth (1998) Herbster, M., M. Warmuth. 1998. Tracking the best expert. Machine Learning 32 151–178.

- Huh et al. (2011) Huh, Woonghee Tim, Retsef Levi, Paat Rusmevichientong, James B. Orlin. 2011. Adaptive data-driven inventory control with censored demand based on kaplan-meier estimator. Operations Research 59(4) 929–941.

- Huh and Rusmevichientong (2009) Huh, Woonghee Tim, Paat Rusmevichientong. 2009. A nonparametric asymptotic analysis of inventory planning with censored demand. Mathematics of Operations Research 34(1) 103–123.

- Iglehart (1964) Iglehart, Donald L. 1964. The dynamic inventory problem with unknown demand distribution. Management Science 10(3) 429–440.

- Jadbabaie et al. (2015) Jadbabaie, Ali, Alexander Rakhlin, Shahin Shahrampour, Karthik Sridharan. 2015. Online optimization: competing with dynamic comparators. Proceedings of the International Conference on Artificial Intelligence and Statistics 398–406.

- Jain et al. (2015) Jain, Aditya, Nils Rudi, Tong Wang. 2015. Demand estimation and ordering under censoring: stock- out timing is (almost) all you need. Operations Research 63(1) 134–150.

- Karlin (1960) Karlin, Samuel. 1960. Dynamic inventory policy with varying stochastic demands. Management Science 6(3) 231–258.

- Karnin and Anava (2016) Karnin, Zohar S, Oren Anava. 2016. Multi-armed bandits: Competing with optimal sequences. Advances in Neural Information Processing Systems. 199–207.

- Kocák et al. (2014) Kocák, Tomás, Gergely Neu, Michal Valko, Rémi Munos. 2014. Efficient learning by implicit exploration in bandit problems with side observations. Z. Ghahramani, M. Welling, C. Cortes, N.D. Lawrence, K.Q. Weinberger, eds., Advances in Neural Information Processing Systems 27. 613–621.

- Koolen et al. (2010) Koolen, Wouter, Manfred K. Warmuth, Jyrki Kivinen. 2010. Hedging structured concepts. Proceedings of the 23rd Annual Conference on Learning Theory (COLT). 93–105.

- Kunnumkal and Topaloglu (2008) Kunnumkal, Sumit, Huseyin Topaloglu. 2008. Using stochastic approximation methods to compute optimal base-stock levels in inventory control problems. Operations Research 56(3) 646–664.

- Lariviere and Porteus (1999) Lariviere, Martin A., Evan L. Porteus. 1999. Stalking information: bayesian inventory management with unobserved lost sales. Management Science 45(3) 346–363.

- Lempel and Ziv (1976) Lempel, Abraham, Jacob Ziv. 1976. On the complexity of finite sequences. IEEE Transactions on Information Theory 22(1) 75–81.