Dynamic Portfolio Optimization with Looping Contagion Risk

Abstract

In this paper we consider a utility maximization problem with defaultable stocks and looping contagion risk. We assume that the default intensity of one company depends on the stock prices of itself and other companies, and the default of the company induces immediate drops in the stock prices of the surviving companies. We prove that the value function is the unique viscosity solution of the HJB equation. We also perform some numerical tests to compare and analyse the statistical distributions of the terminal wealth of log utility and power utility based on two strategies, one using the full information of intensity process and the other a proxy constant intensity process.

Keywords: dynamic portfolio optimization, looping contagion risk, HJB equation, viscosity solution, robust tests, statistical comparisons.

AMS MSC2010: 93E20, 90C39

1 Introduction

There has been extensive research in dynamic portfolio optimization and credit risk modelling, both in theory and applications (see Pham (2009), Brigo and Morini (2013), and references therein). Utility maximization with credit risk is one of the important research areas, which is to find the optimal value and optimal control in the presence of possible defaults of underlying securities or names. The early work includes Korn and Kraft (2003) using the firm value structural approach and Hou and Jin (2002) using the reduced form intensity approach. Defaults are caused by exogenous risk factors such as correlated Brownian motions, Ornstein-Uhlenbeck or CIR intensity processes. Bo et al. (2010) consider an infinite horizon portfolio optimization problem with a log utility and assume that both the default risk premium and the default intensity dependant on an external factor following a diffusion process and show the pre-default value function can be reduced to a solution of a quasilinear parabolic PDE (partial differential equation). Capponi and Figueroa-Lopez (2011) assume a Markov regime switching model and derive the dynamics of the defaultable bond and prove a verification theorem with applications to log and power utilities. Callegaro et al. (2012) consider a wealth allocation problem with several defaultable assets whose dynamics depend on a partially observed external factor process.

Contagion risk or endogenous risk has grown into a major topic of interest as it is clear that the conventional dependence modelling of assets using covariance matrix cannot capture the sudden market co-movements. The failure of one company will have direct impacts on the performance of other related companies. For example, during the global financial crisis of 2007-2008, the default of Lehman Brothers led to sharp falls in stock prices of other investment banks and stock indices such as Dow Jones US Financial Index. Since defaults are rare events, one may have to rely on the market information of other companies or indices to infer the default probability of one specific company. For example, one can often observe in the financial market data that the stock price of one company has negative correlation with the CDS (credit default swap) spread (a proxy of default probability) of another company. A commonly used contagion risk model is the interacting intensity model (see Jarrow and Yu (2001)) in which the default intensity of one name jumps whenever there are defaults of other names in a portfolio. Contagion risk has great impact on pricing and hedging portfolio credit derivatives (see Gu et al. (2013)).

There is limited research in the literature on dynamic portfolio optimization with contagion risk. Jiao and Pham (2011) consider a financial market with one stock which jumps downward at the default time of a counterparty which is not traded and not affected by the stock and, for power utility, solve the post-default problem by the convex duality method and show the process defined by the pre-default value function satisfies a BSDE (backward stochastic differential equations). Jiao and Pham (2013) discuss multiple defaults of a portfolio with exponential utility and prove a verification theorem for the value function characterized by a system of BSDEs. Bo and Capponi (2016) consider a market consisting of a risk-free bank account, a stock index, and a set of CDSs. The default of one name may trigger a jump in default intensities of other names in the portfolio, which in turn leads to jumps in the market valuation of CDSs referencing the surviving names and affects the optimal trading strategies. They solve the problem with the DPP (dynamic programming principle) and, for power utility, find the optimal trading strategy on the stock index is Merton’s strategy, and those on the CDSs can be determined by a system of recursive ODEs (ordinary differential equations). Capponi and Frei (2017) introduce an equity-credit portfolio with a market consisting of a risk-free bank account, defaultable stocks, and CDSs referencing these stocks. The default intensities of companies are functions of stock prices and some external factors, which provides a genuine looping contagion default structure. For a log utility investor, there exists an explicit optimal strategy which crucially depends on the existence of CDSs in the portfolio, see Remark 3.2 for details.

In this paper we analyse the interaction of market and credit risks and its impact on dynamic portfolio optimization. The market is assumed to have one risk-free savings account, and multiple defaultable stocks in which the underlying companies may default and the value of defaulted stock price becomes zero. The default time of any stock is the first jump time of a pure jump process driven by an intensity process that depends on all the surviving stock prices, and the surviving stock prices jump at time of default. This setup characterizes an investment with multiple stocks that are closely dependent on each other, both endogenously and exogenously. Compared with exogenous factor models in the literature, which strongly depend on the historical calibration of factor parameters, the looping contagion model has the ability to adjust trading strategies automatically based on current stock prices in the portfolio. We study a terminal wealth utility maximization problem with general utility functions under this looping contagion framework.

The aforementioned papers by Bo and Capponi (2016) and Capponi and Frei (2017) characterize the value function as a solution of the HJB (Hamilton-Jacobi-Bellman) equation and, for power and log utility respectively, find the optimal trading strategies with some implicit unknown functions. For general utilities, it is essentially impossible one may guess a solution form of the HJB equation nor can one apply the verification theorem. In that case, a standard approach to studying the value function is the viscosity solution method. We prove, in addition to the verification theorem, that the value function is the unique viscosity solution of the HJB equation. The result is important as it lays a solid theoretical foundation for numerical schemes to find the value function, in contrast to the verification theorem that requires priori the existence of a classical solution to the HJB equation, which is in general difficult to prove. To the best of our knowledge, this is the first time the viscosity solution properties of the value function are studied and established in the literature of utility maximization with looping contagion risk. This is one of the main contributions of the paper.

We perform some numerical and robust tests to compare the statistical distributions of terminal wealth of log utility and power utility based on two trading strategies, one uses the full information of intensity process, the other a proxy constant intensity process. These two strategies may be considered respectively the active and passive portfolio investment. The numerical examples show that, statistically, they have similar terminal wealth distributions, but active portfolio investment is more volatile in general. Furthermore, we illustrate the financial insight of the looping contagion model via a similar numerical test, but with different initial stock prices. The numerical test assumes that the constant intensity is estimated from historical calibration window, but there are big falls of stock prices at the start of the investment. The numerical example shows that the terminal wealth based on strategies using stock dependent intensity would have much higher expected return and standard deviation than the one using a constant intensity. Therefore, one may greatly improve the performance of investment if one uses the information of stock dependant default intensity in a financial crisis period.

The rest of the paper is organized as follows. In Section 2 we introduce the market model and state the main results, including the continuity of the value function for one-sided contagion case (Theorem 2.5), the verification theorem (Theorem 2.7), and the unique viscosity solution property of the value function (Theorems 2.10 and 2.14). In Section 3 we perform numerical and robust tests with statistical distribution analysis for log and power utility. In Section 4 we prove Theorems 2.5, 2.7, 2.10 and 2.14. Section 5 concludes the paper.

2 Model Setting and Main Results

Let be a complete probability space satisfying the usual conditions and a filtration to be specified below. Let the market consist of one risk-free bank account with value process and interest rate and defaultable stocks with price process , where is the transpose of a vector . Let be the filtration generated by correlated Brownian motions , which represents the market information. Let be a vector of nonnegative random variables representing the default time of each defaultable stock, defined by

where is an intensity rate process and is a standard exponential variable on the probability space and is independent of the filtration , which means that is a totally inaccessible stopping time. We make the further assumption that is independent of for . Under this assumption, the default of each stock is independent.

Let be the filtration generated by the default indicator process where each of the default process is associated with the intensity process and defined by , the indicator function that equals 0 if and 1 otherwise. Denote the value of indicator process by , thus . The indicator process can only jump from to its neighbor state with rate for . We denote the number of surviving stocks when and the set of surviving stock numbers.

Finally, let be an enlarged filtration, defined by , which contains both the market information and the default information. The stopping time defined in above way satisfies the so-called -hypothesis, which means any -square integrable martingale is also a -square integrable martingale (see Bielecki and Rutkowski (2003)), a property we will use later in the proofs. The market model is driven by the following stochastic differential equations (SDEs):

for integer where is the growth rates of , respectively, is the volatility rate. The vector represents the default impact of each stock to the th stock, thus .

All coefficients are positive constants to simplify discussions. We assume that the defaults of stocks do not occur at the same time. At default time the defaultable stock price falls to zero and the other stock price is reduced by a percentage of for . We require that and for . ensures the other stock price does not fall to zero at default time of . We denote by a generic constant which may have different values at different places.

Assumption 2.1.

The intensity process of the default indicator process can be represented by , a function of surviving stock prices and the state of default indicator process . For simplicity, we denote by . We further assume that is bounded and continuous in for and .

To classify the looping contagion model setting, we give two examples which contain only two stocks in the market, denoted by and .

Example 2.1.

(One-sided contagion) In this case, denotes the price of ETF (exchange-traded-fund) on DJ US Financial Index and denotes the price of a US investment bank. We may treat the ETF as default-free and its stock price reflects the whole US banking industry and thus has impact on the performance of the individual bank. Then the model is given by

where and are the growth rates of and , respectively, and are the volatility rates, and is the percentage loss of the stock upon the default of stock . At default time the defaultable stock price falls to zero and the stock price is reduced by a percentage of . The intensity process of the default indicator process can be represented by .

Example 2.2.

(Looping contagion) In this case, both and denote the prices of single stocks. Then the model is given by

At default time of (resp. ), the stock price (resp. ) falls to zero and the stock price (resp. ) is reduced by a percentage of (resp. ). The intensity process (resp. ) of the default indicator process (resp. ) can be represented by (resp. ). After the default of (resp. ), the intensity process (resp. ) of the default indicator process (resp. ) can be represented by (resp. ).

An investor dynamically allocates proportions of the total wealth into the stocks and the bank account. The admissible control set is the set of control processes that are progressively measurable with respect to the filtration and for all . The set is defined by

where is a bounded set in and is a positive constant. The dynamics of the wealth process is given by

| (2.1) |

where

The matrix-valued process is adapted to the filtration and plays the role of removing the defaulted stocks. Even though the admissible control set is still after default time , and is not a variable but a constant. The requirement for ensures that when th stock defaults, the maximum percentage loss of the wealth does not exceed , in other words, if is the pre-default wealth, then the post-default wealth is at least .

Remark 2.2.

For a given control process , equation (2.1) admits a unique strong solution that satisfies

| (2.2) |

for any . This can be easily verified as , where

Note that is the correlation between Brownian motion and . Since is a bounded set and for , we have , independent of , and is an exponential martingale, thus , which gives (2.2).

Our objective is to maximize the expected utility of the terminal wealth, that is,

where is a utility function defined on and satisfies the following assumption.

Assumption 2.3.

The utility function is continuous, non-decreasing, concave, and satisfies and for all , where and are constants.

Depending on the default scenarios, the value function is defined by

for and . Note that if is independent of , then the value function is a function of only.

For the one-sided contagion model defined in Example 2.1, the problem can be naturally split into pre-default case and post-default case. The latter is a standard utility maximization problem as stock disappears and the post-default value function is a function of time and wealth only, see Pham (2009). We have the following continuity result for the pre-default value function .

Theorem 2.5.

For the one-sided contagion model (Example 2.1), assume further that is non-increasing in , monotone in and Lipschitz continuous in , and satisfies for all . Then the pre-default value function is continuous in .

Remark 2.6.

We assume is non-increasing in as intuitively the default probability of one company is non-increasing with its own stock price. We also assume that is monotone in as we consider and are strongly correlated in the sense that the default probability of stock is either positively or negatively affected by the stock . The continuity of pre-default value function for the one-sided contagion model relies on the special structure that there is only one default process in the place. For general looping contagion models, the continuity of the value function is difficult to obtain as the order of multiple jumps is random.

Applying the DPP, one can show that the value function satisfies the following HJB equation:

| (2.3) |

for and with terminal condition , where is the infinitesimal generator of processes , and with control , given by

| (2.4) | |||||

where for and for . Note that the dimension of is which is equal to as we have removed the th defaulted stock.

We next give a verification theorem for the value function.

Theorem 2.7.

Assume that the function tuple where for any solves (2.3) with the terminal condition , that satisfies a growth condition for , that the maximum of the Hamiltonian in (2.3) is achieved at in , and that SDE (2.1) admits a unique strong solution with control . Then coincides with the value function and is the optimal control process.

Remark 2.8.

For log utility , the assumption is not satisfied. However, one may postulate that the value function has a form , where is a solution of a linear PDE, see (3.1). If we assume and is bounded, then one can show that is indeed the value function with the same proof as that of Theorem 2.7 except one change: instead of using , which does not hold for log utility, one uses . Since

for , we have , which provides the required uniform integrability property in the proof.

The verification theorem assumes the existence of a classical solution of the HJB equation (2.3), which may not be true for the value function . Next we show that the value functions is the unique viscosity solution to the PDE system characterized by (2.3) based on the following definition.

To facilitate discussions of viscosity solution, we define function by

where is the gradient vector of with respect to , and is the Hessian matrix of with respect to . and its derivatives are evaluated at . The HJB equation (2.3) is the same as

for .

Definition 2.9.

(i) is a viscosity subsolution of the PDE system (2.3) on if

for all , and testing functions such that and for on , where is the upper-semicontinuous envelope of , defined by .

(ii) is a viscosity supersolution of the PDE system (2.3) on if

for all , and testing functions such that and for on , , where is the lower-semicontinuous envelope of , defined by .

Based on the above definition, we have the following viscosity solution property for the value function.

Theorem 2.10.

The value function is a viscosity solution of the PDE system (2.3) on , satisfying the growth condition for some constant .

To prove the uniqueness of the viscosity solution, we need to introduce a structure condition on the model.

Assumption 2.11.

The following inequality holds:

where

and matrices and satisfy

Remark 2.12.

The dimension of matrices and in Theorem 2.14 is . We use to represent the right index of matrices which corresponds to where . The introduction of is to resolve the gap between index and matrix index. We use a simple example to illustrate the definition of . For example, . In this case, there are three surviving stocks in the market, namely . The dimension of matrices and is 4 (including 3 surviving stocks and the wealth process ). Then .

Remark 2.13.

For the simplest case where there are only two defaultable stocks in the market, e.g. Example 2.1 and Example 2.2, Assumption 2.11 holds for , as can be written as

where , , and . Using the matrix inequality and simple algebraic calculation, one can show that

By the boundedness of control set , Assumption 2.11 holds for all .

The next result states the uniqueness of the viscosity solution.

Theorem 2.14.

Remark 2.15.

The condition for on the boundary is equivalent to the existence of the limit of the value function at boundary points. This condition is needed as the domain of variables is , not , in which case one may impose some polynomial growth conditions on , see Pham (2009), Remark 4.4.8, for further discussions on this point.

3 Numerical Tests

In this section, we perform some statistical and robust tests for log and power utilities. We assume that there are two defaultable stocks and one risk-free bank account in the market (Example 2.2).

3.1 Optimal strategies for log utility

For , the post-default case is investing into the risk-free bank account, thus and . We conjecture that the pre-default value function takes the form

| (3.1) |

and the value function respectively take the forms

| (3.2) |

Substituting (3.1) and (3.2) into (2.3), we get a linear PDE for depending on the value of and :

| (3.3) |

with the terminal condition , where is defined by

and the other notations are given by

By the same argument, we get a linear PDE for :

with the terminal condition , where is defined by

The PDE associated with can be obtained similarly.

Assume the control constraint set is given by

where are chosen such that for . We need to solve a constrained optimization problem:

Since is compact and is continuous, there exists an optimal solution which satisfies the Kuhn-Tucker optimality condition

| (3.4) |

and the complementary slackness condition

| (3.5) |

where , , are Lagrange multipliers. Since can only take value either in the interior of interval or one of two endpoints, the same applies to , we have nine possible combinations.

If both and are interior points, then for from (3.5). Assuming that there exists a unique solution of (3.4) such that and , then is the optimal control. We can discuss other cases one by one. For example, if and , then from (3.5) and and are solutions of equation (3.4). If solutions do not satisfy and , then this case is impossible.

Remark 3.1.

Applying Kuhn-Tucker optimality condition to , we get the explicit optimal control for as

provided , otherwise, equals or .

Remark 3.2.

Capponi and Frei (2017) derive explicit optimal trading strategies for log utility investors when there are stocks and CDSs for these stocks. Applying Ito’s formula to log wealth process and taking expectation, they get

| (3.6) |

where and is a vector of dimension such that each component is a linear combination of controls into stocks and controls into CDSs, and , , are similarly defined. To maximize over controls and , Capponi and Frei (2017) use a clever trick of maximizing and separately and derive a linear equation system with equations and variables in and . The explicit optimal controls come from solving the equation system, see equation (B.3) in the E-companion paper of Capponi and Frei (2017).

The success of finding the explicit optimal control in Capponi and Frei (2017) crucially relies on the existence of equal number of CDSs in the model. When there is no CDS in the portfolio as in our case, maximizing and separately would result in an incompatible system of equations with variables. It is therefore impossible to get the closed-form optimal control for log utility investors in our looping contagion model by applying Capponi and Frei’s technique. In fact, applying Ito’s formula to log wealth process and taking expectation in our model, we get

where . Taking derivatives of with respect to would lead to the same equation system as that in (3.4).

3.2 Performance comparison of state-dependent and constant intensities

We now do some statistical analysis. The data used are the same as the benchmark case and:

Assume the intensity function is given by

| (3.7) |

with minimum intensity , maximum intensity , and parameter . The default intensity functions with respect to each stock and default state are given by

Note that controls the initial intensity and weights control the sensitivity of intensity to stock prices and . We set such that the initial intensity is 0.1 and which means the default intensity of one stock is slightly more sensitive to its own stock price. Moreover, the intensity of one stock jumps up when the other stock defaults, which captures the virtue of interacting default intensity model, see Bo and Capponi (2013).

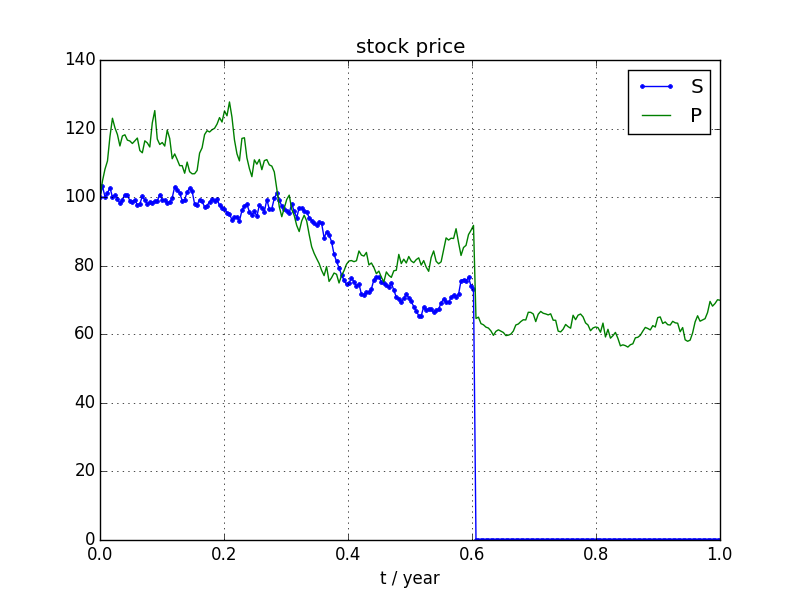

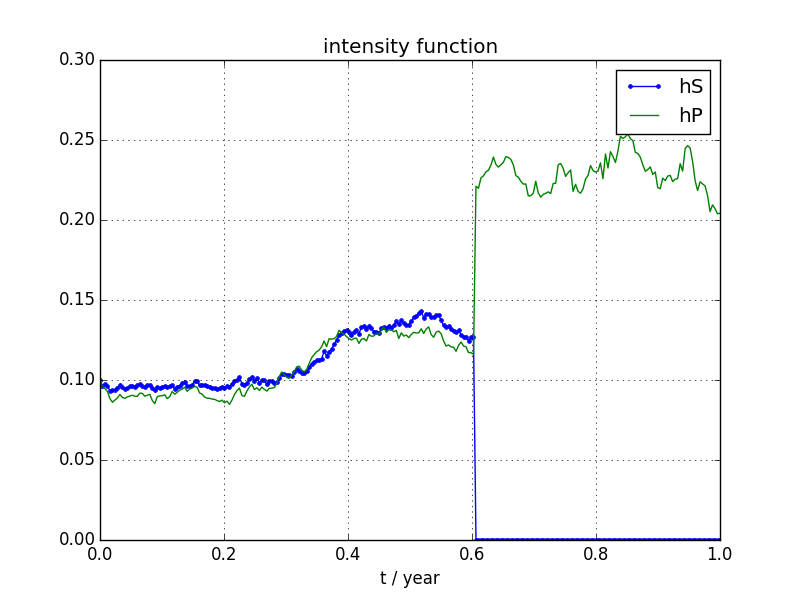

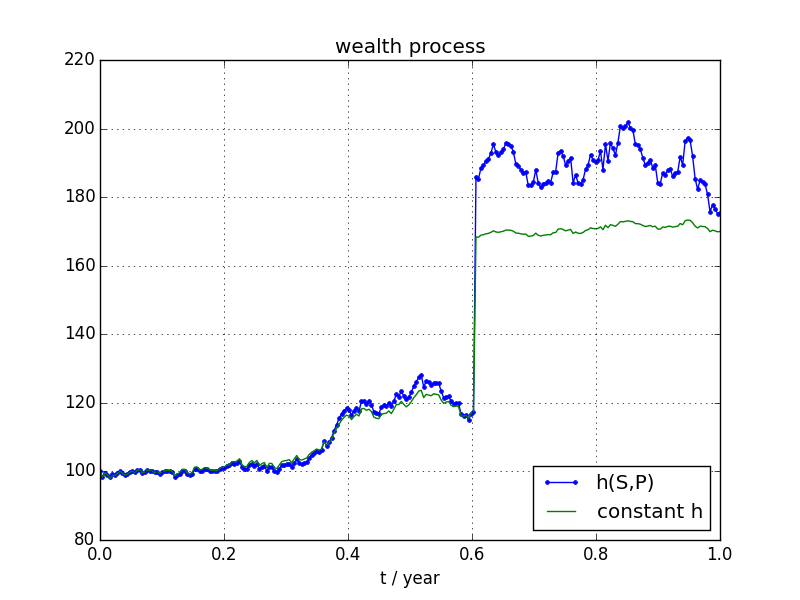

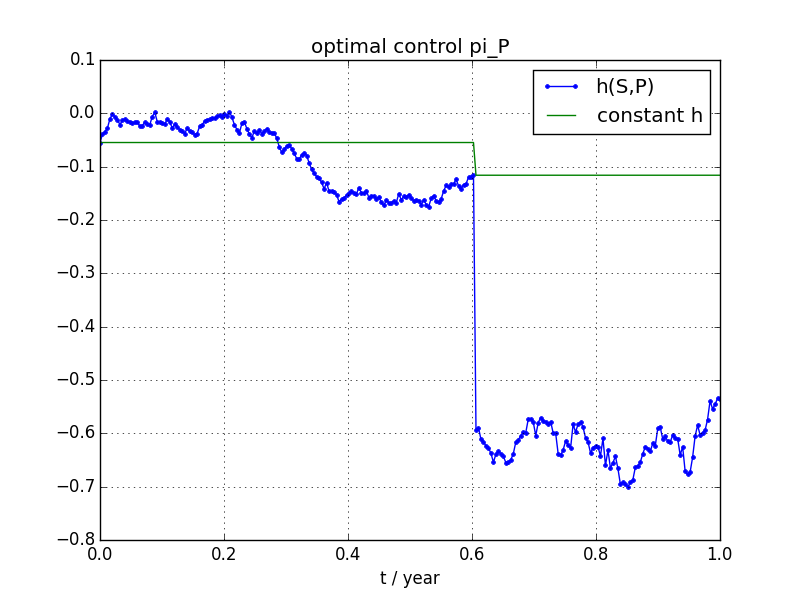

Figure 1 shows sample paths of stock prices, default intensities, and optimal wealth with two different trading strategies. The left panel shows stock price paths of and . In this scenario, only stock defaults. At time of default, stock price drops to zero and stock price jumps down then continues. The middle panel shows the default intensity processes and , which are functions of stock prices . The intensity of stock becomes zero after default, while the default intensity jumps up to . The right panel shows the sample wealth paths when optimal control strategies used are based on -dependant intensities and constant intensities (value equal to ). Both the wealth paths with -dependant intensities and constant intensities jump up when default occurs and then two wealth paths move in the same pattern. Compared with the constant intensities, the -dependant wealth path jumps more. This is not surprising as at time of default, strategies with intensity short sells more stocks and than strategies with constant intensity, which means gain is more, see Figure 2. Of course, this is due to the fact that at time of default the default intensities of and are both above 0.1. The opposite phenomenon happens when the intensity at time of default is larger than constant intensity 0.1.

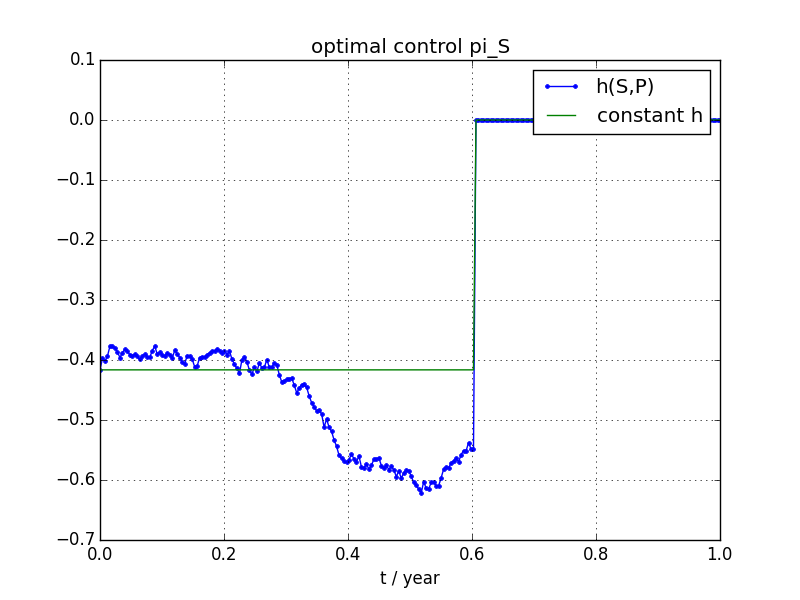

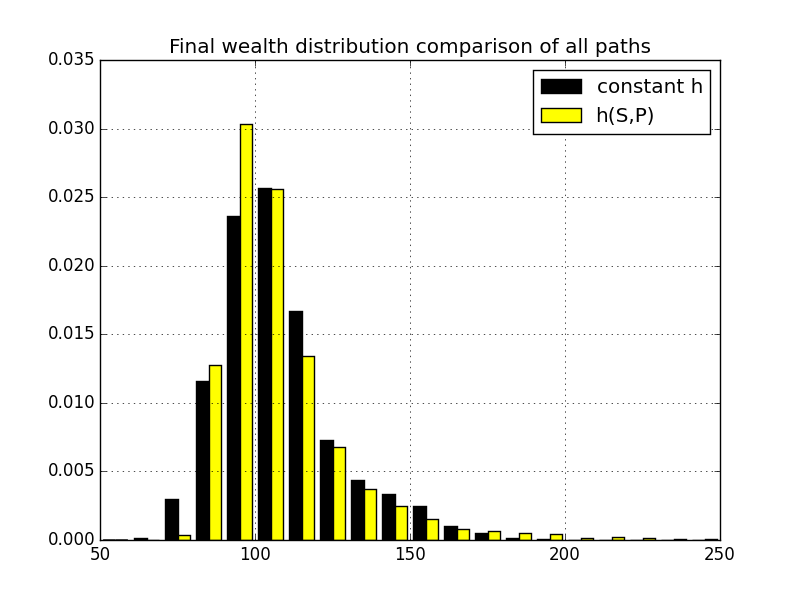

Figure 2 shows optimal controls and associated with the stock paths in Figure 1 and the statistical distributions of the wealth at time . The left panel and mid panel are proportions of wealth invested in stocks and , respectively. It is clear that as default intensity increases, investments in stocks and both decrease and investment in savings account increases, which is intuitively expected as if the default probability of one stock increases, then one would reduce the holdings of both stocks and to reduce the risk of loss in case the default of system indeed occurs. In this scenario, both the optimal investment strategies to stock and are short-selling, which is a combination effect of parameters chosen and default in the place. We simulate 10000 paths of both stock prices and , using -dependent default intensity . Among all these paths, about 1/5 (precisely 1752 paths) contain defaults of either or . The terminal wealth is generated by two strategies: one is optimal strategy based on the full information of , the other is optimal strategy based on constant intensity 0.1. The right panel shows the histograms of terminal wealth of these two strategies. It is clear that their distributions are similar but with some slight differences at tail parts, that is, probability of over-performance is higher and probability of under-performance is lower with -dependant intensities. These histograms seem to indicate, for log utility, the overall performance of -dependent optimal strategies and constant strategies are similar, while the -dependent optimal strategies perform better in extreme scenarios.

| mean | std dev | 2.3% quantile | 97.7% quantile | |

| All samples | 107.78 | 22.60 | 84.08 | 171.82 |

| All samples constant | 107.59 | 19.27 | 78.60 | 157.80 |

| Default | 134.81 | 36.04 | 83.80 | 225.20 |

| Default constant | 134.68 | 21.50 | 95.29 | 178.04 |

| No-default | 102.17 | 12.82 | 84.11 | 134.68 |

| No-default constant | 101.96 | 12.99 | 78.13 | 130.48 |

Table 1 contains sample means, sample standard deviations, and quantile values at low end (2.3%) and high end (97.7%) for both -dependant intensity and constant intensity . It is clear that the overall sample mean with -dependent optimal strategies is (slightly) higher than constant intensity optimal strategies, which is expected as the former is the genuine optimal control, however, the sample standard deviation with -dependent optimal strategies is also higher, which implies the -dependent optimal strategies can be volatile and risky, while the constant optimal strategies are more conservative. However, if we check the quantiles of the distribution (which is a different risk measure), we find that the -dependent optimal strategies overall generate both higher 2.3% quantile (less loss) and higher 97.7% quantile (more gain), which implies the -dependent optimal strategies outperform the constant strategies in the extreme scenarios. Note that the outperformance in upper quantile comes from more short selling (anticipating the default when stock price is very low).

Remark 3.3.

By far the conclusion drawn relies on the benchmark parameter values, in which case the optimal controls for both stocks are short selling in most scenarios. We repeat the same comparison tests on two other parameter sets (if not specified, the parameter value is the same as benchmark case).

-

•

Parameter set 1.

-

•

Parameter set 2.

In most scenarios, the strategies of parameter set 1 is short selling stock and longing stock and the strategies of parameter set 2 are longing both stocks . The overall performance with -dependent optimal strategies is very similar to that with constant intensity optimal strategies. The overall sample mean with -dependent optimal strategies is (slightly) higher than constant intensity optimal strategies, and the sample standard deviation with -dependent optimal strategies is also higher, which implies the difference in the tail distribution and that -dependant optimal strategies can be more volatile.

3.3 Robust tests of model parameters

Assume intensity function is given by (3.7) and stock prices and are generated based on that. It may be difficult to calibrate parameters accurately even one knows the exact form of the intensity function. We do some robust tests for parameters , that is, we compare the optimal performances of two investors, one uses benchmark parameter values and the other incorrect estimated values. We change one parameter only in each test while keep all other parameters fixed at benchmark values.

| mean | std dev | 2.3% quantile | 97.7% quantile | |

| benchmark | 107.78 | 22.60 | 84.08 | 171.82 |

| 107.69 (-0.09%) | 22.85 (1.10%) | 83.00 (-1.29%) | 173.82 (1.16%) | |

| 107.69 (-0.09%) | 23.15 (2.44%) | 80.95 (-3.73%) | 174.67(1.66%) | |

| 111.59 (3.53%) | 53.15 (135.20%) | 53.18 (-36.75%) | 262.58 (52.82%) | |

| 105.17 (-2.42%) | 9.43 (-58.26%) | 84.52 (0.53%) | 122.93 (-28.45%) | |

| 107.77 (-0.01%) | 22.60 (0.01%) | 84.08 (0.00%) | 171.82 (0.00%) | |

| 107.76 (-0.02%) | 22.62 (0.07%) | 83.91 (-0.20%) | 171.82 (0.00%) | |

| 105.36 (-2.25%) | 9.52 (-57.86%) | 85.24 (1.39%) | 124.36 (-27.62%) | |

| 109.76 (1.84%) | 37.64 (66.55%) | 70.59 (-16.04%) | 221.49 (28.91%) |

Table 2 shows that sample means are essentially the same over a broad range of model parameters. The main difference is sample standard deviations. Percentage changes over the benchmark values are listed in parentheses. The performance of state-dependent intensity strategies is robust for some parameters, including weight , minimum intensity level and maximum intensity level . Changes of these parameters do not greatly change sample standard deviations and quantile values at low and high ends. On the other hand, it seems important to have correct estimations of parameters and to avoid large changes of the standard deviation. Those parameters have strong impact on the estimated intensity levels. For example, if one overestimates the initial default intensity ( instead of correct value ) then the sample standard deviation is greatly increased with large loss at low end quantile value.

Next we do some robust tests to see the impact of changes of model parameters on the distribution of optimal terminal wealth, including drift , volatility , correlation , and percentage loss . We change drift and volatility parameters by 20% of their benchmark values and correlation and percentage loss parameters by some big deviations.

| mean | std dev | 2.3% quantile | 97.7% quantile | |

| benchmark | 107.78 | 22.60 | 84.08 | 171.82 |

| 107.05 (-0.68%) | 17.54 (-22.39%) | 91.98 (9.39%) | 158.13 (-7.97%) | |

| 108.55 (0.71%) | 28.35 (25.44%) | 75.99 (-9.62%) | 187.88 (9.35%) | |

| 107.53 (-0.23%) | 21.78 (-3.61%) | 80.93 (-3.75%) | 165.05 (-3.94%) | |

| 108.08 (0.28%) | 25.58 (13.17%) | 83.68 (-0.48%) | 182.54 (6.24%) | |

| 107.28 (-0.46%) | 18.87 (-16.49%) | 88.04 (4.71%) | 161.89 (-5.78%) | |

| 108.47 (0.64%) | 27.88 (23.37%) | 78.37 (-6.79%) | 188.35 (9.62%) | |

| 107.74 (-0.04%) | 21.94 (-2.92%) | 84.12 (0.04%) | 169.01 (-1.63%) | |

| 107.86 (0.07%) | 23.56 (4.24%) | 83.84 (-0.29%) | 175.82 (2.33%) | |

| 108.21 (0.40%) | 25.50 (12.83%) | 83.45 (-0.75%) | 183.56 (6.83%) | |

| 107.57 (-0.20%) | 21.83 (-3.39%) | 82.74 (-1.59%) | 167.26 (-2.65%) | |

| 107.49 (-0.26%) | 20.49 (-9.33%) | 87.32 (3.85%) | 166.49 (-3.10%) | |

| 108.24 (0.43%) | 26.45 (17.05%) | 77.52 (-7.80%) | 181.95 (5.90%) | |

| 107.70 (-0.07%) | 21.94 (-2.91%) | 83.26 (-0.97%) | 169.43 (-1.39%) | |

| 107.88 (-0.10%) | 23.90 (5.74%) | 84.69 (0.73%) | 177.53 (3.32%) |

Table 3 lists statistical results of distributional sensitivity to changes of parameters. It is clear that sample means are essentially the same for all parameters, but sample standard deviations are sensitive to changes of drift, volatility, correlation and percentage loss, which would significantly affect overall distributions of optimal terminal wealth. This requires one to have good estimations of these parameters to have correct distributions. It is well known that it is easy to estimate volatility but difficult to estimate drift (see Rogers (2013)) and information of percentage loss is rarely available. Since optimal trading strategies and optimal wealth distributions are greatly influenced by these parameters which are difficult to be correctly estimated, one needs to be cautious in using state-dependent intensity to model and solve optimal investment problems. Using sub-optimal but conservative and robust trading strategies, instead of optimal ones based on unobservable parameters and intensities, might be more sensible and less risky.

3.4 Performance comparison of different initial stock prices

Table 1 shows the overall distributions of the terminal wealth are similar whether one uses the intensity or constant intensity 0.1 as approximation. This is possibly due to the fact that the initial price of and are both 100, which results in the inital intensity being equal to the constant intensity. The value 0.1 comes from the calibration which relies only on the historical data, while is a forward-looking function which depends on the future stock prices. Table 1 represents the normal situation where the default probability in calibration window is close to that in investment window. However, if the initial intensity is vastly different from which comes from the estimation of calibration window (one example is that the calibration window is just before the financial crisis, while the investment starts from the financial crisis period), the distributions of terminal wealth can be significantly different. We use a numerical example to illustrate this.

For simplicity, let the intensity function be given by . This means the default intensity of jumps from to after defaults. So is the situation when defaults. Assume that the initial prices of and are respectively, then the initial intensity is , which makes the stocks ten times more likely to default than the constant intensity would have suggested (from the calibration window). This would cause one to take different control strategies (more shortselling when ) and would have large impact on the distributions of the terminal wealth as shown in the table below.

| mean | std dev | 2.3% quantile | 97.7% quantile | |

|---|---|---|---|---|

| All samples | 179.74 | 63.21 | 58.63 | 316.08 |

| All samples | 66.26 | 22.87 | 44.62 | 138.28 |

| Default | 195.90 | 52.78 | 99.20 | 318.65 |

| Default | 57.70 | 7.16 | 44.23 | 73.82 |

| No-default | 88.18 | 31.46 | 50.36 | 172.72 |

| No-default | 114.78 | 20.69 | 78.99 | 157.11 |

Table 4 shows the statistics of the terminal wealth with 10000 simulation scenarios which produces 8542 default scenarios, a reflection of the high initial default intensity . When stock prices are small, defaultable stocks are very likely to default. With dependent intensity, the optimal controls are to short sell more stocks, which results in a much larger mean (195.90) than the mean (57.70) with constant intensity if stock or indeed defaults (anticipated). However, if stock does not default (non-anticipated), then the opposite outcomes appear. This numerical test shows -dependant control strategies may outperform or under-perform independent control strategies, depending on the anticipated market event (default of stock) occurring or not.

3.5 Numerical method for power utility

For power utility , , the post-default case is well known with the optimal control (and ) and the post-default value function , where

We conjecture that the pre-default value function takes the form

| (3.8) |

Substituting (3.8) into (2.3), we get a semilinear PDE for :

| (3.9) |

with terminal condition , where

and

Equation (3.9) is a nonlinear PDE with two state variables and it is highly unlikely, if not impossible, to find a closed form solution . However, by Pham (2009) (Remark 3.4.2), equation (3.9) is the HJB equation for the value function of the following optimal control problem:

| (3.10) |

where , , is a controlled Markov state process satisfying the following SDE:

| (3.11) |

with the initial condition , is a 2-dimensional standard Brownian motion and is a discount factor.

By our theoretical result, we claim that the value function is the unique viscosity solution of the HJB equation (3.9). Moreover, if the HJB equation (3.9) has a classical solution, then it is the value function . In other words, we may find the solution of equation (3.9) by solving a stochastic optimal control problem (3.10). Since the diffusion coefficient of SDE (3.11) does not contain control variable , we may use the numerical method of Kushner and Dupuis (2001) to find the optimal value function in (3.10), which would give us a numerical approximation to the solution of equation (3.9). Next we give some details.

According to Kushner and Dupius (2001), the process can be approximated by a Markov chain process, which transits a point at time to one of nine points may take at time , that is, , with the following transition probabilities:

where is the step size of space, is the step size of time with an integer, , and , .

The numerical scheme is based on the following discretized dynamic programming principle:

for , where is the piece-wise constant control and the expectaton is computed with the help of the above Markov chain transition probabilities. The terminal condition is given by .

We compare the passive investment and active investment under the power utility setting. Most parameter values used in power utility case are the same as log utility benchmark case, except the step size of space , the step size of time , and the set of control parameters are . Table 5 lists the numerical results with mean, variance, and quantile values at lower and upper ends. It is clear the performance is similar to that of the log utility as one would expect. We have also done other tests defined in log utility scope and drawn the similar conclusions for the power utility investors.

| mean | std dev | 2.3% quantile | 97.7% quantile | |

| All samples | 106.38 | 17.45 | 77.30 | 148.20 |

| All samples constant | 105.99 | 14.90 | 79.92 | 139.08 |

| Default | 106.70 | 21.00 | 71.67 | 158.63 |

| Default constant | 106.18 | 15.78 | 78.50 | 140.40 |

| No-default | 106.35 | 17.06 | 77.83 | 146.52 |

| No-default constant | 105.97 | 14.80 | 80.03 | 138.94 |

There is a backward stochastic differential equation (BSDE) representation of the solution of equation (3.9). So in theory one may find if one can solve a highly nonlinear BSDE, which is not pursued in this paper, see Cheridito et al. (2007) for details.

4 Proofs

4.1 Proof of Theorem 2.5

Proof.

We prove the theorem in four steps: 1) is continuous in , uniformly in , 2) is continuous in , uniformly in , 3) is continuous in , uniformly in and 4) is continuous in . Combining these four steps gives the continuity of in .

Step 1. For any , and , using Assumption 2.3, we have

by virtue of (2.2). Therefore, is continuous in , uniformly in .

Step 2. Fix and . Denote by the stock price that starts from , , and and the corresponding default intensity and default time of stock , respectively. By our model setting, can be represented by

where is a standard exponential random variable on the probability space and is independent of the filtration , which means are totally inaccessible stopping times.

Define . It is clear that before , the stock price dynamic is a standard geometric Brownian motion. We have

and

| (4.1) |

for any .

If there is no jump on interval , then and , where is the jump process associated with default time . If there is at least one jump on interval , then as and do not jump at the same time. We have the relation

Since equals 0 or 1, we have for any . Using for and and the Cauchy-Schwarz inequality, also noting Remark 2.2, we have

We therefore have

We can decompose as , where is a martingale and is a bounded variation process, see Bielecki and Rutkowski (2003). Applying Doob’s sub-martingale inequality, we have

Since is a monotone function of by Assumption 2.1, without loss of generality, we assume is non-increasing in , then before the first default occurs. By the definition of , we have and . Then

for any . Therefore,

Note that is non-decreasing before and non-increasing after , we conclude that

By inequality (4.1), we have

| (4.2) |

Since equals 0 or 1, we have

Since is martingale, also note that , we have

| (4.3) |

Combining (4.3) and (4.2), we conclude that , which gives

Therefore, is continuous in , uniformly in .

Step 3. Fix and , by same technique as in Step 2, we can show

Therefore, is continuous in , uniformly in .

Step 4. For any and , by the definition of and the dynamic programming principle, , such that

Rearranging the order, we have

Using the Cauchy-Schwartz inequality, we have

which tends to 0 since as .

Next we prove the first term goes to zero as .

As shown in Step 1, , and by (2.2),

Therefore, is uniformly integrable, and we can exchange the order of expectation and limit to get

The same argument can be applied to the term based on Step 2 and based on Step 3, and we conclude that

and

The last term , which tends to zero when . Therefore

as and we finally have

Since is arbitrary, we conclude that is continuous in . Combining Steps 1,2,3,4, we conclude that is continuous in . ∎

4.2 Proof of Theorem 2.7

Proof.

For , define a new process where denotes the wealth process starting with associated with control process , and denotes the prices of surviving stocks at time starting with .

As is smooth in for , we can apply Ito’s formula to and get for any time

where is defined in (2.4), and is a local martingale defined by

Since satisfies the HJB equation (2.3), we have . Define stopping times

then is a martingale due to the boundedness of control set and values and derivatives of . Letting and taking expectation on both sides, we have

with equality if . Next we show that

| (4.4) |

for . Since , also noting (2.2), we have

for any . Since is uniformly integrable, we can take the limit under the expectation to get (4.4). This shows that with equality if . Furthermore, SDE (2.1) admits a unique strong solution by the assumption, therefore, coincides with the value function and is the optimal control process. ∎

4.3 Proof of Theorem 2.10

Lemma 4.1.

Denote by the following function

where for . Then is continuous in .

Proof.

Let and the point and be the ball with center and radius . By the definition of supremum function, for any , there exists a control such that

| (4.5) | |||||

For any point , we have

| (4.6) | |||||

Combining Lemma 4.1 and the smoothness of , we conclude that given in Definition 2.9 is continuous in . Based on this result, we prove the value function is a viscosity solution to the PDE system (2.3).

Proposition 4.2.

The value function is a viscosity supersolution to equation (2.3) on .

Proof.

Let , and be tuple of test functions such that

| (4.9) |

and for on .

By definition of , there exists a sequence in such that

when goes to infinity. By the continuity of and by (4.9) we also have that

when goes to infinity.

Let be a constant control process and be the ball with center and radius . Note that when is large enough, , thus , we have . We denote by the associated controlled wealth process. Let be the stopping time given by

Let be a strictly positive sequence such that

when goes to infinity. Then we can define a stopping time give by where is the first default time of the surviving stocks, starting from .

Next we use the weak dynamic programming principle (weak-DPP) proved in Bouchard and Touzi (2011), that is,

for any -measurable stopping time such that and are -bounded.

Since under stopping time , the processes and are both bounded, we can apply above weak dynamic programming principle (weak-DPP) for to and get

Equation (4.9) implies for , thus

Applying Ito’s formula to the whole term in bracket, we obtain

| (4.10) |

after noting that the stochastic integral term cancels out by taking expectations since the integrand is bounded. Note that is defined the same as (2.4).

Next we investigate the stopping time when is large enough. Firstly, for the stopping time , denoting , we have

By Pham (2009), Page 67, each term in the bracket converges to zero as , which gives

By definition of conversion time , we have

due to the boundedness of intensity function . Thus

Finally for the stopping time , we have

| (4.11) | |||||

Combining above results, we get

We now estimate

By the mean value theorem and dominated convergence theorem, taking limit on both sides of the inequality, we have

which implies

due to the arbitrariness of . ∎

Proposition 4.3.

The value function is a viscosity subsolution to equation (2.3) on .

Proof.

Let , and be tuple of test functions such that

| (4.12) |

and for on .

We prove the result by contradiction. Assume on the contrary that

Then by the continuity of , there exists and such that

for . By definition of , there exists a sequence taking values in such that

when goes to infinity. By the continuity of and by (4.12) we also have that

when goes to infinity.

We denote by the controlled wealth process associated with control process . Let be the stopping time given by

Let be a strictly positive sequence such that

when goes to infinity. Then we can define a stopping time give by where is the first default time of surviving stocks starting from .

Next we use the weak dynamic programming principle (weak-DPP) proved in Bouchard and Touzi (2011), that is, for any , there exists a control process such that

for any –stopping time .

We apply above weak dynamic programming principle (weak-DPP) for to and get for , there exists such that

Equation (4.12) implies for , thus

Applying Ito’s formula to the whole term in bracket, we obtain

| (4.13) |

after noting that the stochastic integral term cancels out by taking expectations since the integrand is bounded. By the similar technique as the supersolution proof, we can show that as .

Since in if , we have

in . Thus

Then we obtain

which implies . We thus get the desired contradiction with . ∎

4.4 Proof of Theorem 2.14

To prove the comparison principle, we need an alternative definition of viscosity solution in terms of the notions of semijets defined as below.

Definition 4.4.

For , given a function on , the superjet of at is defined by:

where , , and the bracket is the inner product of two vectors. We define its closure as the set of elements for which there exists a sequence satisfying . We also define the subjets

By standard arguments, one has an equivalent definition of viscosity solutions in terms of semijets: is a viscosity subsolution (resp. supersolution) to (2.3) at if and only if for all and (resp. ).

We can now state and prove the following comparison principle which gives rise to the uniqueness of viscosity solution.

Proposition 4.5.

Let (resp. ) be a u.s.c. viscosity subsolution (resp. l.s.c. viscosity supersolution) of (2.3) on and satisfy the growth condition , the terminal relation , and the boundary relations on the boundary of for . Then we have for on .

Proof.

We prove the result in several steps.

Step 1. Let and for constant , then a straightforward calculation shows that (resp. ) is a subsolution (resp. supersolution) of

for , where is given by

| (4.14) | |||||

We will show that for on in the next few steps, thus we conclude . We further define function by

Step 2. Define , where . We claim that is a viscosity supersolution to (4.14). Note that

where , for and

We have that for all ,

Since is a viscosity supersolution to (4.14), we have

for by the equivalent definition of viscosity supersolution. Using the inequality and the boundedness of controls and coefficients, we have

for a constant . Therefore, for a large enough , which implies that is a viscosity supersolution of (4.14).

Step 3. We show that for all , it is for on , and thus conclude that . Fix and define

and

where . We next show that . Suppose on the contrary that , by the growth condition on and we have

for any . By the terminal and boundary conditions, we also have

Note that here denotes for any .

Since is upper-semicontinuous and , there exists some open bounded set such that

We now use the doubling variable technique. For any fixed , define

where . Note that is upper-semicontinuous and hence achieves its maximum on the compact set at . We may write that, for all ,

The sequence converges, up to a subsequence, to some . Moreover, since is upper bounded due to the upper-semicontinuity of and , we know is bounded, which implies . Let tend to 0 and take the , we get . Therefore, and .

Step 4. Since converges to with , we may assume that for small enough, lies in . We may write and . Then we have

Applying Crandall-Ishii’s lemma (see Crandall et al. (1992)), we have that there exist and in such that

and the following matrix inequality holds in the non-negative definite sense:

By the viscosity subsolution (resp. supersolution) property of (resp. ), we have

| (4.15) |

and

| (4.16) |

Subtracting (4.15) from (4.16), using the fact that the difference of the supreme is less than the supreme of the difference, we obtain

where

and

Since , we can derive for any . By the definition of , we have for any . By the structure condition and Crandall Ishii’s inequality, we have

Thus we can derive that for any . Therefore

Since , we have , which is a contradiction to the assumption that . We conclude that , which implies for on . ∎

5 Conclusions

In this paper we consider a utility maximization problem with looping contagion risk. We assume that the default intensity of one company depends on the stock prices of other companies and the default of one company induces immediate drops in the stock prices of the other surviving companies. In addition to the verification theorem, we prove the value function is the unique viscosity solution of the HJB equation system. We also compare and analyse the statistical distributions of terminal wealth of log utility based on two optimal strategies, one using the full information of intensity process, the other a proxy constant intensity process. Our numerical tests show that, statistically, using trading strategies based on stock price dependant intensities would achieve higher return on average, especially when the difference of the stock dependent intensity and the proxy constant intensity is big, but could also be more volatile in extreme scenarios. There remain many open questions in utility maximization with contagion risk, for example, the BSDE simulation method for power utility. We leave these and other questions to future research.

Acknowledgements. The authors are very grateful to anonymous reviewers whose constructive comments and suggestions have helped to improve the paper of the previous version.

References

- [1] Bielecki, T. R. and M. Rutkowski (2003), Credit Risk: Modeling, Valuation and Hedging, Springer.

- [2] Bo, L. and A. Capponi (2016), Optimal investment in credit derivatives portfolio under contagion risk, Mathematical Finance, 26(4), 785-834.

- [3] Bouchard, B. and N. Touzi (2011), Weak dynamic programming principle for viscosity solutions, SIAM Journal on Control and Optimization, 49 (3), 948-962.

- [4] Bo, L., Y. Wang and X. Yang (2010), An optimal portfolio problem in a defaultable market, Advances in Applied Probability 42, 689-705.

- [5] Brigo, D. and M. Morini (2013), Counterparty Credit Risk, Collateral and Funding, Wiley.

- [6] Callegaro, G., Jeanblanc, M., and Runggaldier, W. Portfolio optimization in a defaultable market under incomplete information, forthcoming in Decisions in Economics and Finance.

- [7] Capponi, A. and J. E. Figueroa-Lopez (2011), Dynamic portfolio optimization with a defaultable security and regime switching, Mathematical Finance 24, 207-249.

- [8] Capponi, A. and C. Frei (2017), Systemic influences on optimal equity-credit investment, Management Science 63, 2756-2771.

- [9] Cheridito, P. , H. M. Soner , N. Touzi and N. Victoir (2007), Second order backward stochastic differential equations and fully non-linear parabolic PDEs, Communications on Pure and Applied Mathematics 60, 1081-1110.

- [10] Crandall, M., H. Ishii and P.L. Lions (1992), User’s guide to viscosity solutions of second order partial differential equations, Bulletin of the American Mathematical Society 27, 1-67.

- [11] Gu, J.W., W.K. Ching, T.K. Siu, and H. Zheng (2013), On pricing basket credit default swaps, Quantitative Finance 13, 1845-1854.

- [12] Hou, Y. and X. Jin (2002), Optimal investment with default risk, FAME Research Paper No. 46, Switzerland.

- [13] Jarrow, R. and F. Yu (2001), Counterparty risk and the pricing of defaultable securities, Journal of Finance 56, 1765-1799.

- [14] Jiao, Y. and H. Pham (2011), Optimal investment with counterparty risk: a default-density modeling approach, Finance and Stochastics 15, 725-753.

- [15] Jiao, Y. and H. Pham (2013), Optimal investment under multiple defaults risk: a BSDE-decomposition approach, Annals of Applied Probability 23, 455-491.

- [16] Korn, R. and H. Kraft (2003), Optimal portfolios with defaultable securities: a firm value approach, International Journal of Theoretical and Applied Finance 6, 793-819.

- [17] Kushner, H.J. and P. Dupuis (2001), Numerical methods for stochastic control problems in continuous time, Springer.

- [18] Pham, H. (2009), Continuous-Time Stochastic Control and Optimization with Financial Applications, Springer.

- [19] Rogers, L.C.G. (2013), Optimal Investment, Springer.