On Integrated Convergence Rate of an Isotonic Regression Estimator for Multivariate Observations

Konstantinos Fokianos

University of Cyprus

Department of Mathematics and Statistics

P.O. Box 20537

CY – 1678 Nicosia

Cyprus

E-mail: fokianos@ucy.ac.cy

Anne Leucht

Technische Universität Braunschweig

Institut für Mathematische Stochastik

Universitätsplatz 2

D – 38106 Braunschweig

Germany

E-mail: a.leucht@tu-bs.de

Michael H. Neumann

Friedrich-Schiller-Universität Jena

Institut für Mathematik

Ernst-Abbe-Platz 2

D – 07743 Jena

Germany

E-mail: michael.neumann@uni-jena.de

Abstract

We consider a general monotone regression estimation where we allow for independent and dependent regressors. We propose a modification of the classical isotonic least squares estimator and establish its rate of convergence for the integrated -loss function. The methodology captures the shape of the data without assuming additivity or a parametric form for the regression function. Furthermore, the degree of smoothing is chosen automatically and no auxiliary tuning is required for the theoretical analysis. Some simulations and two real data illustrations complement the study of the proposed estimator.

Keywords: Isotonic least squares estimation, multivariate isotonic regression,

nonparametric estimation, rate of convergence, shape constraints, strong mixing.

1. Introduction

We consider the classical mean regression model

| (1.1) |

where we assume that the regression function , , is unknown and allow for both independent and dependent observations (here and in the sequel, denotes the transpose of a vector ).

Notably, the problem of estimating a regression function subject to shape constraints, in the context of time series, has not been addressed adequately in the literature, to the best of our knowledge. There exist a large body of literature on estimation and testing for situations where the class of admissible functions can be parametrized by a finite-dimensional parameter; see e.g. Escanciano (2006), Francq and Zakoian (2010) and Shumway and Stoffer (2011) among others. There are also many results on nonparametric kernel estimators for relying on the assumption that the covariate vector has a Lebesgue density. For an overview, we refer the reader to the monographs by Härdle (1990) and Fan and Gijbels (1996). On the other hand, there are numerous applications that the covariates do not possess a density with respect to the Lebesgue measure; a case in point is various count time series models which have been employed for the analysis of financial data (e.g. modeling the number of transactions) or biomedical data (e.g. modeling infectious diseases); see Fokianos et al. (2009) for instance and Sec. 4.2.

The primary aim of this work is to provide integrated -loss convergence rate of a nonparametric estimator of subject to shape constraints without assuming additivity; in particular we assume throughout this work that the function in (1.1) is isotonic. The assumption of isotonicity seems to be appropriate in the context of many applications and, in fact, some popular parametric models share this property, for example, autoregressive and GARCH type models with nonnegative coefficients. Application of standard nonparametric methods such as kernel estimators of the function , as proposed e.g. by Mukarjee and Stern (1994), Dette et al. (2006), Chernozhukov et al. (2009), Daouia and Park (2013) or generalized additive modeling Chen and Samworth (2016) among other references, depends on a data-driven choice of smoothing parameters, such as a bandwidth. While the simple leave-one-out cross-validation may fail, the method of leave--out cross-validation involves a choice of , which in turn requires a difficult subjective decision.

Another popular shape-constrained estimator of the function is the isotonic least squares estimator (LSE) which is given by

In sharp contrast to usual kernel estimators, the isotonic least squares estimator does not require the choice of any smoothing parameter since an appropriate tuning of the degree of smoothing is done automatically. This estimator seems to be less sensitive to irregularities in the design and if the target function is indeed isotonic then this estimator is consistent; see e.g. Christopeit and Tosstorff (1987) and references therein.

Denote by the indicator function. Then, it is well known that satisfies at all observation points the following equations:

| (1.2a) | |||||

| (1.2b) | |||||

where

and and denote upper and lower sets, respectively; see e.g. Theorem 1 in Brunk (1955) and Theorem 1.4.4 in Robertson et al. (1988, p. 23). (A set is called an upper set if and imply that . Analogously, is called a lower set if and imply that . Here, the notation (, respectively) denotes that (, respectively), for all .) While is uniquely defined at the observation points, there is some arbitrariness of choosing between these points; only the postulated isotonicity has to be satisfied.

For the univariate case, i.e. , there are already several results reported in the literature concerning the asymptotic behavior (usually assuming a deterministic regressor) of the classical isotonic least squares estimator . Pointwise asymptotic distributions of isotonic least squares estimators assuming short and long range dependence of the error sequence have been derived recently by Anevski and Hössjer (2006) and Dedecker et al. (2011). In particular, it is known that this estimator converges at the optimal rate to . Zhang (2002, Theorem 2.3) studies the case of independent but not necessarily identically distributed errors and shows that , where are values of a deterministic covariate and ; see also Chatterjee et al. (2015) for a refinement in the case that but under the assumption of independent and identically distributed errors. Furthermore, Durot (2002, Theorem 1) proves that .

However, much less is known about the asymptotic behavior of in the case of multivariate regression models. The only results concerning the estimator that we are aware are the following. Hanson et al. (1973, Theorem 5) prove uniform consistency of in the case under the assumptions of deterministic regressors and a continuous target function . Additionally, these authors provide intuition for the convergence of large deviation probabilities between the estimator and the true regression function towards zero; see Hanson et al. (1973, Eq. (26)). Robertson and Wright (1975, Theorems 2.1 and 2.2) state pointwise consistency for in the context of a general partial order for the regressors. Finally, Christopeit and Tosstorff (1987, Theorem 1) prove a consistency result in the -dimensional case. The authors assume that the errors form a martingale difference sequence and the covariates are continuous and stochastic.

To the best of our knowledge, there are no any available results concerning the integrated convergence rate of isotonic LSE in the case of multivariate regression models. We conjecture that a serious obstacle for deriving such rates of convergence for when is the enormous amount of possible lower and upper set involved in computing (1.2a) and (1.2b); see e.g. Gao and Wellner (2007) as well as the discussion in Section 3 in Wu et al. (2005).

Our goal is to fill this gap by proposing a suitable modification of isotonic LSE as described in Section 2. For the case of univariate regression we let intact the isotonic LSE . However, in the multivariate case we propose a slightly simpler estimator by restricting attention to lower and upper sets of (hyper-)rectangular type. As we will show, for both cases of independent regressors (see Theorem 2.1) and dependent data (see Theorem 3.1), such modification avoids the entropy problem and allows derivation of the desired convergence rate. In sharp contrast to usual nonparametric estimators and in accordance with the classical isotonic LSE, this estimator does not require the choice of an appropriate bandwidth which could cause problems in our general setting with a possibly irregular distribution of the explanatory variables and with dependent observations. This general framework we consider allows inclusion of a trend component. Such a covariate accommodates the case of gradual changes over time in contrast to change-point models with stationarity between these points of (abrupt) changes.

The paper is structured as follows. We introduce the proposed estimators and present results on their rate of convergence in Sections 2 (independence case without trend component) and 3 (dependence case allowing for a deterministic trend). Numerical examples are discussed in Section 4. All proofs as well as technical auxiliary results are deferred to Section 5.

2. Multivariate isotonic regression under independence

Recall (1.1) where we now assume that and are independent and identically distributed random variables on a probability space . We assume that the conditional mean function is isotonic, that is, monotonically non-decreasing in each argument. Following the discussion of Section 1, consider the estimators defined by

and

where, for , . It follows from the construction of both and that they are isotonic and that holds for all . We define the isotonic estimator of as any isotonic function that satisfies

| (2.1) |

For example, choose . In the univariate case any choice of which is between and is equal to at the observation points. The proposed estimator deviates from in the multivariate case though. The proofs of Theorems 2.1 and 3.1 below show that replacing lower and upper sets by hyperrectangles in (1.2a) and (1.2b) simplifies the derivation of the desired rate of convergence and its computation.

Firstly, we study the case of independent and identically distributed variables . We impose the following condition.

-

(A1)

-

(i)

The information variables possess a density on , such that

where .

-

(ii)

The error sequence satisfies

where .

-

(i)

Define

| (2.2) |

Note that corresponds to an asymptotically mean square error-optimal bandwidth of a kernel estimator when the function to be estimated has a degree of smoothness 1. Here, and in the following, the notation denotes the –dimensional vector consisting of ones. The estimator is based on means over hyperrectangles. For multi-indexes , we define grid points by

and subsets of by

where . The estimator is based on means over hyperrectangles. We expect therefore a regular behavior of if there are sufficiently many observations in each box . Recall that is the lower bound on the density of the information variables which is assumed to exist by (A1)(i). Then, regularity of is guaranteed to hold, provided that the event

| (2.3) |

occurs with probability tending to one. This is stated in the following lemma.

Lemma 2.1.

Suppose that Assumption (A1) holds true. Then

It is well known that the traditional isotonic estimator is problematic when is close to the boundary of the support of the distribution of the ; see e.g. the discussion in Sampson et al. (2003). The same is true for at points near the boundary of the domain. To fix the bias problem at extreme small and large design points, Wu et al. (2005) proposed an adequate modification by pulling up and down the isotonic LSE at these particular locations. We do not implement a boundary correction since this would involve some sort of tuning parameter whose appropriate choice is somewhat subjective. In fact, we neglect the behavior of near the boundary and focus on estimating on the box

Under minimal assumptions and assuming existence of second moments for the error terms we prove the following theorem.

Theorem 2.1.

Suppose that Assumption (A1) holds true. Then, with denoting the Lebesgue measure on ,

First, we notice that Theorem 2.1 and Lemma 2.1 imply that

Furthermore, consider the special case of a partially differentiable function . Then the assumption of isotonicity implies that

Hence, the degree of smoothness, say , measured in the -norm, is equal to 1. It is well known that, under appropriate conditions, the optimal rate of convergence for the -loss is which reduces to , when ; see Stone (1982). Hence, Theorem 2.1 indicates that achieves the optimal rate of convergence in the class of isotonic functions. Recall that in contrast to the classical isotonic estimator which is obtained by using all possible lower and upper sets in (1.2a) and (1.2b) our estimator is based on averages over hyperrectangles only. This reduced complexity allows us to derive the desired rate of convergence.

3. Multivariate isotonic regression under dependence

Recall again (1.1) where we now allow the random variables to be dependent. We assume the information variables to be of the form , where is a -dimensional vector consisting of components with values in , and is a -dimensional covariate consisting of variables with continuous marginal distribution functions and possibly a trend component . Here, we allow for with . Note that by setting or , it is possible that is just equal to or , respectively. More specifically, we distinguish between two cases: either the covariate vector includes a trend component of the form , i.e. , where denotes the rest of the covariates, or the covariate vector is free of a trend. In this section, we consider again the isotonic estimator defined by (2.1). We show that the results of Lemma 2.1 and Theorem 2.1 can be generalized to the case of strong mixing random variables provided that we impose some additional assumptions. We suppose that:

-

(A2)

-

(i)

The error sequence satisfies

where .

-

(ii)

The process is strong (-) mixing with corresponding mixing coefficients satisfying

-

(iii)

The function is bounded.

-

(i)

Having in mind that contains components

with a discrete distribution and components having either a continuous distribution or being nonrandom

such as we impose the following condition:

-

(A3)

For and , the random vectors consist of components with continuous marginal distribution functions and/or a trend component .

-

(i)

There exist continuous distribution functions on and, for all , constants such that

-

(ii)

There exists some constant such that, for all -dimensional hyperrectangles ,

-

(i)

Before we proceed some comments on assumption (A3) are in order. Condition (A3)(i) means that the “average distribution” of the continuous random variables behaves as a -dimensional product distribution which has, after an appropriate rescaling with , a density bounded away from zero on . The terms are needed to accommodate the possible case of a trend variable . Also note that assumption (A1)(i) implies the validity of assumption (A3)(ii). We impose a condition on rather than in order to accommodate the case where .

To simplify the notation, we suppress the index in , and from here on, just keeping in mind that also a triangular scheme is allowed, e.g., when a trend variable is included. We define

and, for multi-indexes ( , ), subsets of the domain of as

Since the estimator is based on means over hyperrectangles, a “regular” behavior of it can be expected if there are sufficiently many observations in each box . It turns out that regularity can be assured if the following event occurs:

| (3.1) |

where is some positive constant and .

Using a Fuk-Nagaev-type inequality for dependent random variables we can prove the following analogous result to Lemma 2.1.

Lemma 3.1.

Suppose that Assumptions (A2) and (A3) hold true. Then, for sufficiently small in (3.1),

Recall again that the traditional isotonic estimator is problematic when is close to the boundary of the support of the distribution of the . We neglect the behavior of near the boundary and focus on estimating on

Denote by the probability measures corresponding to the distribution functions , respectively. With being the counting measure on , define .

Theorem 3.1.

Suppose that Assumptions (A2) and (A3) hold true. Then,

Here, in the definition of the event , the constant is chosen such that the assertion of Lemma 3.1 holds true.

Some remarks are in order. First, it follows again from this theorem and Lemma 3.1 that

Furthermore, we point out that the obtained rate of convergence does not depend on the number of discrete explanatory random variables. This is explained by the fact that, for any , the cardinality of the set is proportional to the sample size . Therefore, there is no need to smooth over the first directions and there is no loss due to a trade-off between bias and variance that would appear with nonparametric smoothing techniques.

Properties of the noise process can be taken into account, provided that we have some prior knowledge. Indeed, if we knew the conditional variance , e.g. in the case of a known distributional family for the errors, then we could replace the means by the weighted means , where the weights are proportional to . This corresponds to a weighted least squares estimator in linear regression. However, our main intention was to produce a general, fully nonparametric method. Since prior knowledge of is rarely available, we pursue the approach based on unweighted means.

Example 3.1.

Suppose that integer-valued random variables are observed, where

and is a covariate with values in which is independent of , . Assume that the function is isotonic and bounded by . The information variable at time is . We have that

where

It can be shown that Assumption (A2)(i) is also fulfilled. Indeed, let . Since for all values of and ,

that is, Doeblin’s condition is fulfilled. It follows from Theorem 2.4.1 on page 88 in Doukhan (1994) that the Markov chain is uniformly (-) mixing and, therefore, absolutely regular with coefficients satisfying

for some and . Since the process is also a Markov chain, we obtain that

(The first and the last but one equalities follows from the Markovian structure; see also the note after Theorem 7.3 in Bradley (2007). The last one follows from independence of and ; see also Theorem 6.2 in Bradley (2007).) Hence, the coefficients of absolute regularity of the process satisfy

4. Applications

4.1. Simulations

We illustrate the theoretical results by a limited simulation study comparing the performance of and the isotonic LSE in terms of their error. More specifically, consider the following Poisson count time series model, as described in Example 3.1, where we have assumed that is a deterministic trend, i.e. for

where

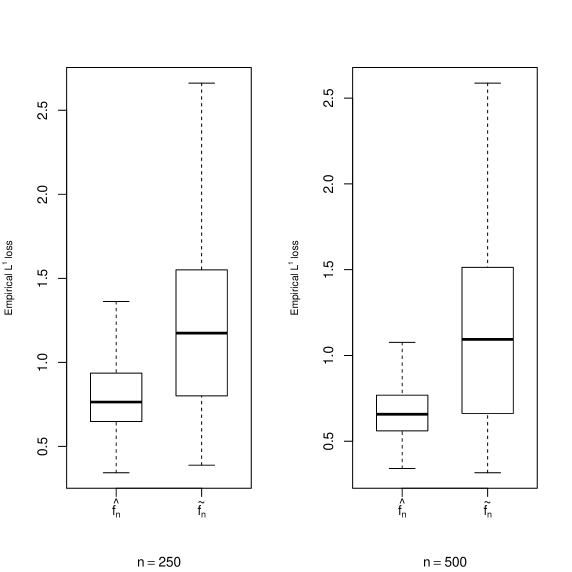

We compute the isotonic least squares estimator by using the R package isotonic.pen which returns the values of the estimated function on an equidistant grid; see Wu et al. (2005) for details. Note that can be computed (exactly) on any grid. We use the grid employed by isotonic.pen discarding some points so that we can avoid any boundary issues. To this end, we choose the lower left / upper right corner of the grid such that, on the one hand, the number of observed information variables within the corresponding rectangle is maximized and on the other hand, for every grid point all upper and lower rectangles contain at least one data point. To compare the empirical performance of the estimators, we compute the integrated error over the grid values. This process is repeated 500 times. Figure 1 shows box plots of the values of integrated error for two different sample sizes and illustrates that achieves smaller error than the isotonic LSE.

4.2. Data Examples

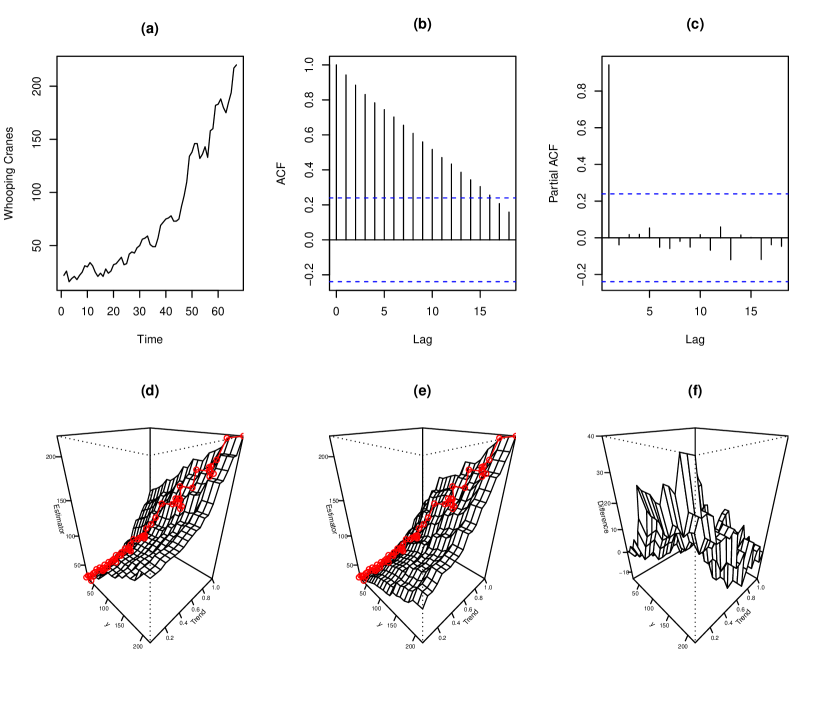

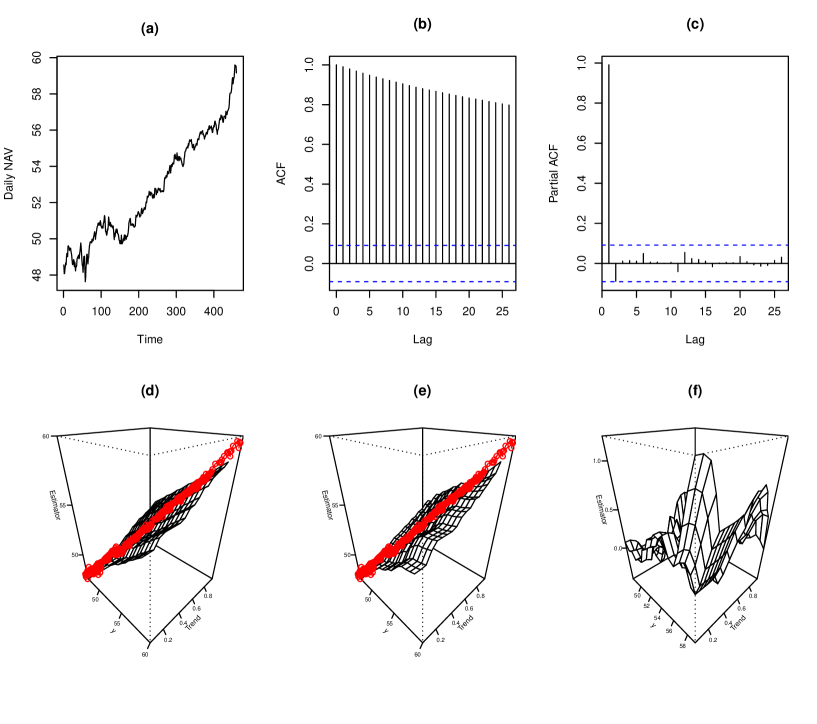

We apply the methodology to biological and financial time series which exhibit some form of non-stationarity. First, we investigate the population growth of whooping cranes that became nearly extinct during the period 1938-1955. Whooping cranes are one of the largest birds in North America but also one of the rarest that can be found in the continent. For some time their population has been constantly decreasing and reached to about 20 individual birds in the world. With the employment of various conservation measures the population grew over the last years. The data we have are depicted in Figure 2 which shows the growth of population of whooping cranes between 1938 to 2005; see Int. Recovery Plan (2007). Note that this is a case of an integer valued time series. The second example refers to daily net asset value (NAV) of the BlackRock Global Allocation Fund during the period 1/4/2016 to 30/1/2018. Here we note that series takes values on real numbers.

For both of these data examples, a simple time series plot reveals increasing trend and strong autocorrelation which decays slowly. The partial autocorrelation functions shows a strong autocorrelation at lag 1; see the upper panel of Figures 2 and 3. We fit a non-parametric time series model to these data by using isotonic estimation methods. We include the covariate vector , where is number of effective observations (e.g. for the population growth of whooping cranes the number of observation is equal to 68 but because of the inclusion of ). We consider again the estimator and the isotonic LSE and work the same way as it was explained in Subsection 4.1 . The lower panels of Figures 2 and 3 show that both estimators are quite close near the observation points, but differ significantly at some grid points that are located far from the bulk of data. We examine the performance of both methods for estimating the two models. This task is accomplished by studying the in sample predictive power using the mean absolute prediction error (MAPE), that is . Here, is obtained by evaluating and , respectively, on a grid point close to . The results are shown in Table 1. Clearly, the new estimator outperforms the isotonic LSE in terms of MAPE for both data examples.

| Example 1 (Whooping cranes) | Example 2 (BlackRock Global Allocation Fund) | |

|---|---|---|

| 5.916453 | 0.3108097 | |

| 6.002488 | 0.3118416 |

5. Proofs and Auxiliary Results

We prove our main results in Section 5.1. Some auxiliary lemmas are stated and proved in Section 5.2.

5.1. Proofs of the main results

Proof of Lemma 2.1.

Since it suffices to show that

| (5.1) |

by recalling that denotes the indicator function. We obtain from Bernstein’s inequality, for all and , that

for some , which proves (5.1). ∎

Proof of Theorem 2.1.

We analyze the contribution of the stochastic part and the bias of the estimator separately. For the latter, we exploit the assumed isotonicity in conjunction with boundedness of in order to construct an estimate of the integrated bias from above and below. To this end, denote for an arbitrary function its positive (respectively negative) part by (respectively ). Then, it suffices to show that

| (5.2a) | ||||

| and | ||||

| (5.2b) | ||||

We have, for all ,

| (5.3) | |||||

By Lemma 5.1 and since we obtain for the bias that

| (5.4) | |||||

For the stochastic part, we estimate . For this purpose, we define a dyadic scheme of nested hyperrectangles: For ,

(We have in particular and .) Since and since implies that we obtain, for all ,

Recall that if the event occurs, then for all , which implies that

Furthermore, it follows from Lemma 5.2 that for some

| (5.5) |

Therefore, we obtain that

This yields, in conjunction with (5.3) and (5.4), that (5.2a) holds. The proof of (5.2b) is completely analogous and therefore it is omitted. ∎

Proof of Lemma 3.1.

Analogously to the proof of Lemma 2.1, we will show that

| (5.6) |

Let and, for arbitrary , . It follows from the Fuk-Nagaev-type inequality (I.6) of Rio (2000, page 4) that, for all ,

| (5.7) |

where

Note that (A2)(ii) implies that

| (5.8) |

To see the first relationship of (5.8), note that, for ,

which implies that . Since the sequence is monotonically non-increasing, we obtain that . Note that the second relationship of (5.8) follows from .

Since we obtain that

that is, the second term on the right-hand side of (5.7) is of the required order. It remains to estimate . To this end, we distinguish between the two cases of covariates without and with a trend component. In the first case, we obtain from the upper bound in (A3)(i) that, for all with ,

On the other hand, we obtain from a covariance inequality for strong mixing processes (see e.g. Bradley (2007, Corollary 10.16)) that

Therefore, with ,

| (5.10) | |||||

In the case with trend, we get from (A3)(i) that

On the other hand, we see that , and therefore if . Hence, here with ,

| (5.12) | |||||

We see from (5.10) and (5.12) that in the two cases without and with trend the term is of order , for some . Choosing we see that (5.6) follows from (5.7), which completes the proof. ∎

Proof of Theorem 3.1.

The proof of this theorem is largely the same as that of Theorem 2.1. We show that

| (5.13a) | |||

| and | |||

| (5.13b) | |||

We define grid points

We have, for all ,

| (5.14) | |||||

We apply Lemma 5.1 to , with . Since we obtain for the bias that

| (5.15) | |||||

We define again a dyadic scheme of nested hyperrectangles: For ,

and

Since and since implies that we obtain, for all ,

Recall that if the event occurs, then for all , which implies that

Furthermore, it follows from Lemma 5.3 that for some

| (5.16) |

Therefore, we obtain that

This yields, in conjunction with (5.14) and (5.15), that (5.13a) holds. The proof of (5.13b) is completely analogous and therefore it is omitted. ∎

5.2. Some auxiliary results

Lemma 5.1.

Suppose that is isotonic and let, for and , . Then

Proof of Lemma 5.1.

Let . We estimate the sum by considering the main and minor diagonals as follows:

The assertion of the lemma follows because . ∎

Lemma 5.2.

Suppose that the assumptions of Theorem 2.1 hold true. Then, for arbitrary with and some ,

| (5.17a) | |||

| and | |||

| (5.17b) | |||

Proof of Lemma 5.2.

We prove only (5.17a) since the proof of (5.17b) is completely analogous. One of the main tools which is used is given by Bickel and Wichura (1971, Thm. 1). For this purpose, we adopt some notation from there. A block in is a subset of of the form . For , the th face of is . Disjoint blocks and are -neighbors if they are abut and have the same th face; they are neighbors if they are -neighbors for some . (For example, and are -neighbors if .) For each block , let

In what follows we show that condition (2) in Bickel and Wichura (1971, Thm. 1) is fulfilled. To this end, let and be arbitrary neighboring blocks in . We will estimate the expected value of the term

Since and are disjoint sets it follows that

if . Therefore, and by independence of ,

Furthermore, again by independence of , and since

if , we obtain that

| (5.18) | |||||

Let . From (5.18) we obtain by Markov’s inequality that

for all and the measure . Hence, condition (2) of Bickel and Wichura (1971, Thm. 1) is fulfilled and it follows that

for all and some . This, however, implies that

which proves the assertion of the lemma. ∎

Lemma 5.3.

Suppose that the assumptions of Theorem 3.1 hold true. Define . Then, for arbitrary with and some ,

| (5.19a) | |||

| and | |||

| (5.19b) | |||

Proof of Lemma 5.3.

The proof is pretty much the same as that of Lemma 5.2. Since we impose condition (A3)(ii), we have only a bound for the conditional probability but not for at our disposal. In view of this, we consider first the -thinned partial sums

for , instead of the full partial sums. In analogy to (5.18) in the proof of Lemma 5.2 we show that, for any neighboring blocks and in and any ,

| (5.20) |

for some .

As in the independent regressors case, we consider again, for arbitrary neighbored blocks and and arbitrary , the terms . Since and are disjoint sets it follows as before that provided that . This implies that the above expectation is equal to 0. Moreover, if the largest index appears only once, then the expectation also vanishes since, by (A2)(i), . Therefore, we have to examine in more detail two cases: and . Hence we obtain that

as required. Using (5.20) to estimate (5.18), similar to the proof of Lemma 5.2, we obtain in the same manner that

Finally, summing up over we obtain (5.19a). The proof of (5.19b) is analogous and therefore it is omitted. ∎

Acknowledgment .

This research was partly funded by the German Research Foundation DFG, project NE 606/2-2 and by the Volkswagen Foundation (Professorinnen für Niedersachsen des Niedersächsischen Vorab). Part of this work was completed while K. Fokianos was visiting the Department of Statistics at TU Dortmund.

References

- (1)

- Anevski and Hössjer (2006) Anevski, D. and Hössjer, O. (2006). A general asymptotic scheme for inference under order restrictions. Ann. Statist. 34, 1874–1930.

- Bickel and Wichura (1971) Bickel, P. J. and Wichura, M. J. (1971). Convergence criteria for multiparameter stochastic processes and some applications. Ann. Math. Statist. 42, 1656–1670.

- Bradley (2007) Bradley, R. C. (2007). Introduction to Strong Mixing Conditions, Volume I. Kendrick Press.

- Brunk (1955) Brunk, H. D. (1955). Maximum likelihood estimates of monotone parameters. Ann. Math. Statist. 26, 607–616.

- Chatterjee et al. (2015) Chatterjee, S., Guntuboyina, A., and Sen, B. (2015). On risk bounds in isotonic regression and other shape restricted regression problems. Ann. Statist. 43, 1774–1800.

- Chen and Samworth (2016) Chen, Y. and Samworth, R. J. (2016). Generalized additive and index models with shape constraints. J. R. Statist. Soc. B. 78, 729–754.

- Chernozhukov et al. (2009) Chernozhukov, V. and Fernández-Val, I., and Galichon, A. (2009). Improving point and interval estimators of monotone functions by rearrangement. Biometrika 96, 559–575.

- Christopeit and Tosstorff (1987) Christopeit, N. and Tosstorff, G. (1987). Strong consistency of least-squares estimators in the monotone regression model with stochastic regressors. Ann. Statist. 15, 568–586.

- Daouia and Park (2013) Daouia, A. and Park, B. U. (2013). On projection-type estimators of multivariate isotonic unctions. Scand. J. Stat., 40, 363–386.

- Dedecker et al. (2011) Dedecker, J., Merlevède, F., and Peligrad, M. (2011). Invariance principles for linear processes with application to isotonic regression. Bernoulli 17, 88–113.

- Dette et al. (2006) Dette, H., Neumeyer, N., and Pilz, K. F. (2006). A simple nonparametric estimator of a strictly monotone regression function. Bernoulli 12, 469–490.

- Doukhan (1994) Doukhan, P. (1994). Mixing: Properties and Examples. Lecture Notes in Statistics 85. Springer-Verlag, Berlin, Heidelberg.

- Durot (2002) Durot, C. (2002). Sharp asymptotics for isotonic regression. Probab. Theory Relat. Fields 122, 222–240.

- Escanciano (2006) Escanciano, J. C. (2006). Goodness-of-fit tests for linear and nonlinear time series models. J. Amer. Statist. Assoc. 101, 531–541.

- Fan and Gijbels (1996) Fan, J. and Gijbels, I. (1996). Local Polynomial Modelling and its Applications. London: Chapman & Hall.

- Fokianos et al. (2009) Fokianos, K., Rahbek, A., and Tjøstheim, D. (2009). Poisson autoregression, J. Amer. Statist. Assoc. 104, 1430–1439.

- Francq and Zakoian (2010) Francq, C. and Zakoïan, J.-M. (2010). GARCH models: Structure, Statistical Inference and Financial Applications. UK: Wiley.

- Gao and Wellner (2007) Gao, F. and Wellner, J. A. (2007). Entropy estimate for high-dimensional monotonic functions. J. Mult. Anal. 98, 1751–1764.

- Hanson et al. (1973) Hanson, D. L., Pledger, G., and Wright, F. T. (1973). On consistency in monotonic regression. Ann. Statist. 1, 401–421.

- Härdle (1990) Härdle, W. (1990). Applied Nonparametric Regression. Cambridge; New York; New Rochelle: Cambridge University Press.

- Int. Recovery Plan (2007) International Recovery Plan for the Whooping Crane (Grus Americana), Third Revision (2007). Endangered Species Bulletins and Technical Reports (US Fish and Wildlife Service). Paper 45.

- Mukarjee and Stern (1994) Mukarjee, H. and Stern, S. (1994). Feasible nonparametric estimation of multiargument monotone functions. J. Amer. Stat. Assoc., 89, 77–80.

- Rio (2000) Rio, E. (2000). Théorie asymptotique des processus aléatoires faiblement dépendants. Mathématiques & Applications 31, Springer.

- Robertson and Wright (1975) Robertson, T. and Wright, F. T. (1975). Consistency in generalized isotonic regression. Ann. Statist. 3, 350–362.

- Robertson et al. (1988) Robertson, T., Wright, F. T., and Dykstra, R. L. (1988). Order Restricted Statistical Inference. Wiley, New York.

- Sampson et al. (2003) Sampson, A. R., Singh, H., and Whitaker, L. R. (2003). Order restricted estimators: some bias results. Statist. Probab. Lett. 61, 299–308.

- Shumway and Stoffer (2011) Shumway, R. H. and Stoffer, D. S. (2011) Time Series Analysis and its Applications. Third ed. Springer, New York.

- Stone (1982) Stone, C. J. (1982). Optimal global rates of convergence for nonparametric regression. Ann. Statist. 10, 1040–1053.

- Wu et al. (2005) Wu, J., Meyer, M. C., and Opsomer, J. D. (2015). Penalized isotonic regression. J. Statist. Plann. Inference 161, 12–24.

- Zhang (2002) Zhang, C.-H. (2002). Risk bounds in isotonic regression. Ann. Statist. 30, 528–555.