On the Runtime-Efficacy Trade-off of Anomaly Detection

Techniques for Real-Time Streaming Data

Abstract.

Ever growing volume and velocity of data coupled with decreasing attention span of end users underscore the critical need for real-time analytics. In this regard, anomaly detection plays a key role as an application as well as a means to verify data fidelity. Although the subject of anomaly detection has been researched for over 100 years in a multitude of disciplines such as, but not limited to, astronomy, statistics, manufacturing, econometrics, marketing, most of the existing techniques cannot be used as is on real-time data streams. Further, the lack of characterization of performance – both with respect to real-timeliness and accuracy – on production data sets makes model selection very challenging.

To this end, we present an in-depth analysis, geared towards real-time streaming data, of anomaly detection techniques. Given the requirements with respect to real-timeliness and accuracy, the analysis presented in this paper should serve as a guide for selection of the “best” anomaly detection technique. To the best of our knowledge, this is the first characterization of anomaly detection techniques proposed in very diverse set of fields, using production data sets corresponding to a wide set of application domains.

1. Introduction

Advances in technology – such as, but not limited to, decreasing form factor, network improvements and the growth of applications, such as location-based services, virtual reality (VR) and augmented reality (AR) – combined with fashion to match personal styles has fueled the growth of Internet of Things (IoT). Example IoT devices include smart watches, smart glasses, heads-up displays (HUDs), health and fitness trackers, health monitors, wearable scanners and navigation devices, connected vehicles, drones et cetera. In a recent report (Cisco, 2016), Cisco projected that, by 2021, there will be 929 M wearable devices globally, growing nearly from 325 M in 2016 at a CAGR of 23%.

The continuous and exponential increase of volume and velocity of the data streaming from such devices limit the use of existing Big Data platforms. To this end, recently, platforms such as Satori (Sat, 2017) have been launched to facilitate low-latency reactions on continuously evolving data. The other challenge in this regard pertains to analysis of real-time streaming data. The notion of real-time, though not new, is not well defined and is highly contextual (Kejariwal and Orsini, 2016). The following lists the various classes of latency requirements (Lat, 2010) and example applications.

-

❚

Nano seconds: High Frequency Trading (HFT).

-

❚

Micro seconds: Data center applications, cloud networks.

-

❚

Milli seconds: Text messaging, Publish Subscribe systems, cloud gaming.

-

❚

1-3 seconds: Ad targeting.

| Domain | Technique | Summary | P/N-P | <Pt,Pa > | Inc. | Robust | Recency | TG | CFAR |

| Statistics | |||||||||

| Mu-Sigma (Shewhart, 1926a, b; Wade and Woodall, 1993; Lowry and Montgomery, 1995; Wu and Spedding, 2000; Roberts, 1959; Jensen et al., 2006) | Thresholds based on mean and standard deviation | P | <✓, ✗> | ✓ | ✓ | 1sec | |||

| Med-Mad (Leys et al., 2013) | Thresholds based on median and median absolute deviation | P | <✓, ✗> | ✓ | 1msec | ||||

| GeneralisedESD (Grubbs, 1950, 1969; Tietjen and Moore, 1972; Rosner, 1983; Vallis et al., 2014a) | Uses Student t-distribution to calculate a max number of outliers | P | <✓, ✗> | ✓ | 100msec | ✓ | |||

| -Estimator (Yohai and Zamar, 1988; Rousseeuw and Croux, 1993; Maechler et al., 2016; Nunkesser et al., 2008) | Measure of Spread with better Gaussian efficiency than MAD | P | <✓, ✗> | ✓ | 1msec | ||||

| Huber M-Estimator (Huber, 1964; Venables and Ripley, 2002) | Huber’s M-estimator | P | <✓, ✓> | ✓ | 10msec | ||||

| t-digest (Dunning and Ertl, 2015; Cohen and Strauss, 2006; Plessis et al., 2016) | Streaming percentile based detection | N-P | <✓, ✗> | ✓ | ✓ | ✓ | 10sec | ✓ | |

| AdjBox Plots (Vandervieren and Huber, 2004; Hubert and Vandervieren, 2008) | Adjusted whiskers for box plots | N-P | <✓, ✗> | ✓ | 10msec | ||||

| Time Series Analysis | |||||||||

| STL (Cleveland et al., 1990; Vallis et al., 2014a; R Core Team, 2016; Hafen, 2016) | Seasonality Decomposition | N-P | <✓, ✗> | ✓ | 100msec | ||||

| SARMA (Box and Jenkins, 1990; Akaike, 1969, 1986; Durbin and Koopman, 2001; Hyndman and Athanasopoulos, 2014) | Seasonal Auto Regressive Moving Average (ARMA) | P | <✓, ✗> | 1sec | |||||

| STL-ARMA-KF (Kalman, 1960; Soule et al., 2005; Bera et al., 2016; Chen, 2012; Simon, 2010) | STL, ARMA on residuals | P | <✓, ✗> | 100msec | |||||

| STL-RobustKF (Ting et al., 2007; Agamennoni et al., 2011) | ARMA with Robust Kalman | P | <✓, ✗> | ✓ | ✓ | 100msec | |||

| SDAR (Yamanishi and Takeuchi, 2002; Yamanishi et al., 2004; Urabe et al., 2011) | Sequential Discounting AR | P | <✓, ✗> | ✓ | ✓ | 100msec | |||

| RobustOutlers (Fox, 1972; Muirhead, 1986; Kaiser and Maravall, 2001; de Lacalle, 2016) | Intervention Analysis with ARMA | P | <✓, ✗> | ✓ | 10min | ||||

| TBATS (Livera et al., 2011; Holt, 2004; Lucas and Saccucci, 1990; Hyndman, 2016; G. Grmanova, 2016) | Exponential Smoothing with Fourier Terms for Seasonality | P | <✓, ✗> | 10sec | |||||

| Pattern Mining | |||||||||

| HOTSAX (Keogh et al., 2005; Mueen et al., 2009) | Pattern Distance based on SAX | N-P | <✗, ✓> | ✓ | 1sec | ||||

| RRA (Senin et al., 2015, 2014) | Rare Rule Anomaly based on Grammar Induction | N-P | <✗, ✓> | ✓ | 1sec | ||||

| DenStream (Cao et al., [n. d.]) | Online Density Micro-Clustering | N-P | <✓, ✓> | ✓ | ✓ | ✓ | 20msec | ||

| CluStree (Kranen et al., 2011) | Hierarchical Micro-Clustering | N-P | <✓, ✓> | ✓ | 100msec | ||||

| DBStream (Hahsler and Bolanos, 2016; Tasoulis et al., 2007; Ester et al., 1998; Yan and Zhang, 2013) | Incremental Shared Density Based clustering | N-P | <✓, ✓> | ✓ | ✓ | ✓ | 10msec | ||

| Machine Learning | |||||||||

| MB-means (Amoualian et al., 2016; Zhai and Boyd-Graber, 2013) | Mini-batch clustering with -means | N-P | <✓, ✓> | 10msec | |||||

| PCA (Pearson, 1901; Hotelling, 1933a, b; Jolliffe, 1986) | Principal Components Analysis | P | <✓, ✗> | 1msec | |||||

| RobustPCA (Candès et al., 2011; Udell et al., 2014) | Low Rank Approximation | P | <✓, ✗> | ✓ | 1sec | ||||

| IForest (Liu et al., 2012; Tan et al., 2011; Guha et al., 2016) | Isolation Forests | N-P | <✓, ✓> | 100msec | |||||

| OneSVM (Schölkopf et al., 2001; Amer et al., 2013) | One Label SVM | P | <✗, ✓> | 1sec | |||||

In the realm of analytics on real-time streaming data, anomaly detection plays a key role as an application as well as a means to verify data fidelity. For example, finding anomalies in one’s vitals (see Figure 1 as an illustration) can potentially help doctors to take appropriate action in a timely fashion, thereby potentially obviating complications. Likewise, finding anomalies in physiological signals such as electrocardiogram, electromyogram, skin conductance and respiration of a driver can help gauge the stress level and thereby manage non-critical in-vehicle information systems (Healey and Picard, 2005a).

Although the subject of anomaly detection has been researched for over 100 years (AD_, 2017), most of the existing techniques cannot be used as is on real-time data streams. This stems from a multitude of reasons – a small set of these are mentioned below.

-

➣

Non-conformity between the assumptions behind a given technique and the underlying distribution and/or structure of data streams

-

➣

The need for labels; in other words, many existing techniques are supervised in nature. Note that obtaining labels in a production environment is not feasible

-

➣

Being multi-pass and non-incremental

-

➣

Lack of support for recency

-

➣

Lack of robustness

-

➣

Lack of low latency computation

-

➣

Lack of support for constant false alarm rate

-

➣

Lack of scalability

Further, other characteristics of IoT devices such as, but not limited to, small storage, small power budgets consumption et cetera limit the use of off-the-shelf anomaly detection techniques. Last but not least, constantly evolving nature of data streams in the wild call for support for continuous learning.

As overviewed in (AD_, 2017), anomaly detection has been researched in a wide variety of disciplines, for example, but not limited to, operations, computer vision, networking, marketing, and social media. Unfortunately, there does not exist a characterization of the performance of anomaly detection techniques – both with respect to real-timeliness and accuracy – on production data sets. This in turn makes model selection very challenging. To this end, in this paper, we present an in-depth analysis, geared towards real-time streaming data, of a large suite of anomaly detection techniques. In particular, the main contributions of the paper are as follows:

-

❏

We present a classification of over 20 (!) anomaly detection techniques across seven dimensions (refer to Table 1).

-

❏

As a first, using over 25 (!) real-world data sets and real hardware, we present a detailed evaluation of the real-timeliness of the anomaly detection techniques listed in Table 1. It is important to note that the evaluation was carried out in an unsupervised setting. In other words, irrespective of the availability of labels, a model was not trained a priori.

-

❏

We present detailed insights into the performance – as measured by precision, recall and score – of the anomaly detection techniques listed in Table 1. Specifically, we also present a deep dive view into the behavior subject to the following:

-

❚

Trend and level shifts

-

❚

Change in variance

-

❚

Change in seasonal level

-

❚

Change in seasonality period

-

❚

-

❏

We present a map of the accuracy-runtime trade-off for the anomaly detection techniques.

-

❏

Given an application domain and latency requirement, based on empirical evaluation, we make recommendations for the “best” technique for anomaly detection.

Given the requirements with respect to real-timeliness and accuracy, we believe that the analysis presented in this paper should serve as a guide for selection of the “best” anomaly detection technique. To the best of our knowledge, this is the first characterization of anomaly detection techniques proposed in a very diverse set of fields (refer to Table 1) using production data sets corresponding to a wide set of applications.

The rest of the paper is organized as follows: In Section 2, we define the terms in the subsequent sections. Section 3 present a brief overview of the techniques listed in Table 1. Section 4 details the experimental set up and Section 5 walks the reader through a deep dive of the analysis and insights learned from the experiments. Finally, in Section 6 we conclude with directions for future work.

2. Preliminaries

In this section we define the terms used in the rest of paper.

Definition 2.1.

Point Anomalies: are data points which deviate so much from other data points so as to arouse suspicions that it was generated by a different mechanism (Hawkins, 1980).

Definition 2.2.

Pattern Anomalies: Continuous set of data points that are collectively anomalous even though the individual points may or may not be point anomalies.

Definition 2.3.

Change Detection: This corresponds to a permanent change in the structure of a time series, e.g., change in the mean level (Level Shift), change in the amplitude of seasonality (Seasonal Level Shift) or change in the noise amplitude (Variance Change).

Definition 2.4.

Concept Drift: This corresponds to the change in statistical properties, for example, the underlying distribution, of a time series over time.

Next, we define the desirable properites for anomaly detection techniques geared towards real-time data streams.

Property 2.1.

Incremental: A property via which a technique can analyze a new data point without re-training a model.

Property 2.2.

Recency: Under this, a technique assigns weights to data points which decays with their age. In other words, recent data points play a dominant role during model training.

Property 2.3.

Constant False Alarm Rate (CFAR): A property under which the upper limit on the false alarm rate (FAR) – defined as the ratio of falsely tagged anomalies and the total number of non-anomalous points – is constant.

3. Background

As mentioned earlier in Section 1, the subject of anomaly detection has been researched for over 100 years (AD_, 2017). A detailed walkthrough of prior work is beyond the scope of this paper (the reader is referred to the books (Hawkins, 1980; Barnett and Lewis, 1994; Rousseeuw and Leroy, 2003; Aggarwal, 2013) or surveys (Chin et al., 2005; Chandola et al., 2009; Zhang et al., 2010; Gogoi et al., 2011; Ndong and Salamatian, 2011; Bhuyan et al., 2012; Gupta et al., 2014) written on the subject). In the section, we present a brief overview of the techniques listed in Table 1.

3.1. Statistics

In this subsection we briefly overview the common statistical techniques used for anomaly detection.

3.1.1. Parametric Approaches

One of the most commonly used rule to detect anomalies – popularly referred to as the rule – whereby, observations that lie 3 or more deviations () away from the mean () are classified as anomalies. The rule is based on the following two assumptions: (a) the underlying data distribution is normal and (b) the time series is stationary. In practice, production time series often do not satisfy the above, which results in false positives. Further, both and are not robust against the presence of anomalies. To this end, several robust estimators have been proposed. Specifically, Huber M-estimator (Huber, 1964) is commonly used as a robust estimate of location, whereas median, estimator (Yohai and Zamar, 1988) and Median Absolute Deviation (MAD) are commonly used as robust estimates of scatter.

In the presence of heavy tails in the data, -distribution (Zabell, 2008) is often used as an alternative to the normal distribution. The Generalized Extreme Studentized Deviate (ESD) test (Rosner, 1983) uses the -distribution to detect outliers in a sample, by carrying out hypothesis tests iteratively. GESD requires an upper bound on the number of anomalies, which helps to contain the false alarm rate (FAR).

3.1.2. Non-parametric Approaches

It is routine to observe production data to exhibit, for example but not limited to, skewed and multi-modal distribution. For finding anomalies in such cases, several non-parametric approaches have been proposed over the years. For instance, -digest (Dunning and Ertl, 2015) builds an empirical cumulative density function (CDF), using adaptive bin sizes, in a streaming fashion. Maximum bin size is determined based on the quantile of the value , where is the quantile and is a compression factor that controls the space requirements. In a similar vein, adjusted Boxplots (Vandervieren and Huber, 2004) have been proposed to identify anomalies in skewed distributions. For this, it uses a robust measure of the skew called medcouple(Brys et al., 2003).

3.2. Time Series Analysis

Observations in a data streams exhibit autocorrelation. Thus, prior to applying any anomaly detection technique, it is critical to weed out the autocorrelation. Auto Regressive Moving Average (ARMA) (Box and Jenkins, 1990) models have been commonly used for analysis of stationary time series. ARMA models are formulated as State Space Models (SSM) (Durbin and Koopman, 2001), where one can employ Kalman Filters for model estimation and inference. Kalman filters (KF) (Kalman, 1960) are first order Gaussian Markov Processes that provide fast and optimal inference for SSMs. KFs assume that the hidden and observed states are Gaussian processes. When that assumption fails, the estimates obtained via KFs can potentially be biased. Robust Kalman Filters (RobustKF) (Ting et al., 2007) treat the residual error as a statistical property of the process and down weight the impact of anomalies on the observed and hidden states.

Sequential Discounting AutoRegressive (SDAR) filters assign more weight to recent observations in order to adapt to non-stationary time series or change in dynamics of a system (Yamanishi and Takeuchi, 2002). Further, a key feature of SDAR filters is that they update incrementally. A discount rate is specified to guide the rate of adaptation to changing dynamics.

3.3. Pattern Mining

Time series with irregular but self-similar patterns are difficult to model with parametric methods. Non-parametric data mining approaches that find anomalous patterns and/or subsequences have been proposed for such time series. SAX is a discretization technique that transforms a series from real valued domain to a string defined over a finite alphabet of size (Keogh et al., 2005). It divides the real number scale into equal probabilistic bins based on the normal model and assigns a unique letter from to every bin. Before discretization, SAX z-normalizes the time series to map it to a probabilistic scale. It then forms words from consecutive observations that fall into a sliding window. The time series can now be represented as a document of words. SAX employs a dimensionality reduction technique called Piecewise Aggregate Approximation (PAA) which chunks the time series into equal parts and computes the average for each part. The reduced series is then discretized for further processing.

The key advantage of SAX over other discretization heuristics (Bu et al., [n. d.]; Fu et al., 2006) is that the distance between two subsequences in SAX lower bounds the distance measure on the original series. This allows SAX to be used in distance based anomaly detection techniques. For example, HOTSAX (Keogh et al., 2005) uses SAX to find the top- discords.

Another method that leverages SAX is the Rare Rule Anomaly (RRA) technique (Senin et al., 2015). RRA induces a context free grammar from the data. The grammar induction process compresses the input sequence by learning hierarchical grammar rules. The inability of compressing a subsequence is indicative of the Kolmogorov randomness of the sequence and hence, can be treated as being an anomaly. RRA uses the distance to the closest non-self match subsequence as the anomaly score.

3.4. Machine Learning

Machine Learning approaches such as clustering, random forests, and deep learning are very effective in modeling complex time series patterns. Having said that, the training time is usually very high and many of these techniques are not incremental in nature. Thus, most of these techniques work in batch mode where training is performed periodically.

Isolation forests (Liu et al., 2012) is a tree based technique that randomly splits the data recursively in an attempt to isolate all observations into separate leafs. The number of splits needed to reach a data point from the root node is called the path length. Many such random split forests are constructed and the average path length to reach a point is used to compute the anomaly score. Anomalous observations are closer to the root node and hence have lower average path lengths.

One Label Support Vector Machines (SVMs) (Schölkopf et al., 2001) are often used to construct a non-linear decision boundary around the normal instances, thereby isolating anomalous observation that lie away form the dense regions of the support vectors. A key advantage of this technique is that it can be used even with small number of data points, but are potentially slow to train.

Clustering

There are two main approaches to handle the stream clustering problem:

Micro-Clustering () and

Mini-Batching ().

Micro-Clustering

A large number of techniques follow a 2-phase Micro-clustering approach (Aggarwal et al., 2003) which has both an online as well as an offline component.

The online component is a dimensionality reduction step that computes the summary

statistics for observations very close to each other (called micro-clusters).

The offline phase is a traditional clustering technique that ingests a set of

s to output the final clustering, which can be used to identify anomalous

s.

DenStream is a density-based streaming technique which uses the paradigm (Cao et al., [n. d.]). In the online phase, it creates two kinds of s: potential micro-clusters () and anomalous micro-clusters(). Each cluster maintains a weight which is an exponential function of the age of the observations in the cluster. is updated periodically for all clusters to reflect the aging of the observations. If is above a threshold (), it is deemed as a core micro-cluster. If is more than (where <<), the cluster is deemed as a , otherwise it is deemed a . When a new observation arrives, the technique looks for a that can absorb it. If no is found, it looks for an that can absorb the observation. If no is found, a new is instantiated. Older clusters are periodically removed as their become smaller.

DBStream is an incremental clustering technique that decays s, akin to DenStream. It also keeps track of the shared density between s. During the offline phase, it leverages this shared density for a DBSCAN-style clustering to identify anomalous s.

Hierarchical clustering techniques such as Clustree use the paradigm to construct a hierarchical height balanced tree of s (Kranen et al., 2011). corresponding to an inner node is an aggregation of the clusters of all its children. A key advantage of these techniques is their being incremental; having said that, the data structures can grow balloon in size. For anomaly detection, the distance of a new observation from the closest leaf is used as the anomaly score.

Mini-Batching

The second approach for a data stream clustering entails batch clustering of a

sample generated from the data stream. These samples are significantly larger

than the micro-clusters and hence the name mini-batch. An example technique

of this kind is the mini-batch -means which uses cluster centroids from the

previous clustering step to reduce the convergence time significantly

(Feizollah et al., 2014) .

3.5. Potpourri

Seasonality in time series is commonly observed in production data. Filtering of the seasonal component is critical for effective anomaly detection. In this regard, a key challenge is how to determine the the seasonal period. For this, a widely used approach is to detect strong peaks in the auto-correlation function coupled with statistical tests for the strength of the seasonality.

Seasonal-Trend-Loess (STL) (Cleveland et al., 1990) is one the most commonly used techniques for removing the seasonal and trend components. STL uses LOESS (Cleveland, 1979) to smooth the seasonal and trend components. Presence of anomalies can potentially induce distortions in trend which in turn can result in false positives. To alleviate this, Robust STL iteratively estimates the weights of the residual – the number of robustness iterations is an input manual parameter. The downside of this is that the robustness iterations slow down the run time performance. Vallis et al. (Vallis et al., 2014b) proposed the use of piecewise medians of the trend or quantile regression – this is significantly faster than using the robustness iterations. Although STL is effective when seasonality is fixed over time, moderate changes to seasonality can be handled by choosing a lower value for the “s.window” parameter in the STL implementation of R.

Seasonal ARMA (SARMA) models handle seasonality via the use of seasonal lag terms (Durbin and Koopman, 2001). A key advantage with the use of SARMA models is the support for change in seasonality parameters over time. However, SARMA is not robust to anomalies. This can be addressed via the use of robust filters (Chakhchoukh et al., 2009). Note that the estimation of extra parameters increases the relative model estimation time considerably. SARMA models can also handle multiple seasonalities at the expense of complexity and runtime. Akin to SARMA, TBATS is an exponential smoothing model which handles seasonality using Fourier impulse terms (Livera et al., 2011).

Principal Components Analysis (PCA) is another common method used to extract seasonality. However, the use of PCA requires the data to be represented as a matrix. One way to achieve this is to fold a time series along its seasonal boundaries so as to build a rectangular matrix () where each row is a complete season. Note that PCA is not robust to anomalies as it uses the covariance matrix which is non-robust measure of scatter. To alleviate this, Candes et al. proposed Robust PCA (RPCA) (Candès et al., 2011), by decomposing the matrix into a low rank component() and a sparse component() by minimizing the nuclear-norm of .

4. Experimental Setup

In this section, we detail the data sets used for evaluation, the underlying methodology and walk through any transformation and/or tuning needed to ensure a fair comparative analysis.

4.1. Data Sets

| Domain | Description | Acronym | Len | WinSize | PL | Cnt | TG | Labels | SP | SJ | LS | VC | SLD | SLS | |

| NAB (Lavin and Ahmad, 2015) | |||||||||||||||

| NAB Advertising Click Rates | nab-ctr | 1600 | 240 | 20 | 4 | 1 hr | ✓ | 24 | ✓ | ✓ | ✓ | ||||

| NAB Tweet Volumes | nab-twt | 15800 | 2880 | 20 | 4 | 1 hr | ✓ | 288 | |||||||

| NAB Ambient Temperature | nab-iot | 7268, 22696 | 5000 | 20 | 1 | 1 hr | ✓ | 24 | ✓ | ✓ | ✓ | ✓ | |||

| YAD (Laptev et al., 2015) | |||||||||||||||

| Real operations series | yahoo-a1 | 1440 | 720 | 10 | 67 | 1hr | ✓ | 24,168 | ✓ | ✓ | ✓ | ||||

| Synthetic operations series | yahoo-a2 | 1440 | 720 | 10 | 100 | 1hr | ✓ | 100-300 | ✓ | ✓ | ✓ | ||||

| Synthetic operations series | yahoo-a3 | 1680 | 720 | 10 | 100 | 1hr | ✓ | 24,168 | ✓ | ✓ | ✓ | ||||

| HFT (qua, 2017) | |||||||||||||||

| Facebook Trades Dec. 2016 | fin-fb | 334783 | 10000 | 60 | 1 | 1 sec | Manual | ✓ | ✓ | ||||||

| Google Trades Dec. 2016 | fin-goog | 127848 | 10000 | 60 | 1 | 1 sec | Manual | ✓ | ✓ | ||||||

| Netflix Trades Dec. 2016 | fin-nflx | 177018 | 10000 | 60 | 1 | 1 sec | Manual | ✓ | ✓ | ||||||

| SPY Trades Dec. 2016 | fin-spy | 392974 | 10000 | 60 | 1 | 1 sec | Manual | ✓ | ✓ | ||||||

| Ops. | |||||||||||||||

| Minutely Operations Data | ops-* | 120000 | 14400 | 60 | 44 | 1 min | 1440,60 | ✓ | ✓ | ✓ | ✓ | ||||

| IoT (Beckel et al., 2014) | |||||||||||||||

| Power Usage of Freezer | iot-freezer01 | 432000 | 23820 | 1800 | 1 | 1 sec | 2382 | 2370-2390 | ✓ | ✓ | |||||

| Power Usage of Fridge | iot-fridge01 | 432000 | 81900 | 1800 | 1 | 1 sec | 8190 | 7900-8200 | ✓ | ✓ | |||||

| Power Usage of Dishwasher | iot-dishwasher01 | 432000 | 20000 | 1800 | 1 | 1 sec | ✓ | ✓ | |||||||

| Power Usage of Freezer | iot-freezer02 | 432000 | 20000 | 1800 | 1 | 1 sec | ✓ | ✓ | |||||||

| Power Usage of Fridge | iot-fridge02 | 432000 | 30360 | 1800 | 1 | 1 sec | 3036 | 3030-3080 | ✓ | ✓ | |||||

| Power Usage of Lamp | iot-lamp02 | 432001 | 20000 | 1800 | 1 | 1 sec | 2370-2390 | ✓ | ✓ | ||||||

| Power Usage of Freezer | iot-freezer04 | 432000 | 41500 | 1800 | 1 | 1 sec | 4150 | 4100-4200 | ✓ | ✓ | |||||

| Power Usage of Fountain | iot-fountain05 | 432000 | 432000 | 1800 | 1 | 1 sec | 86400 | ✓ | ✓ | ||||||

| Power Usage of Fridge | iot-fridge05 | 432000 | 47500 | 1800 | 1 | 1 sec | 4750 | 4720-5000 | ✓ | ✓ | |||||

| Health (Goldberger et al., e 13) | |||||||||||||||

| ECG Sleep Apnea (Penzel et al., 2000) | health-apnea-ecg/a02 | 15000 | 2000 | 40 | 1 | 10 msec | ✓ | 100 | 90-110 | ✓ | |||||

| ECG Seizure Epilepsy (Al-Aweel IC, 1999) | health-szdb/sz04 | 10000 | 2000 | 40 | 1 | 5 msec | ✓ | 200 | 190-230 | ✓ | |||||

| ECG Smart Health Monitoring (Melillo et al., 2015) | health-shareedb/02019 | 15000 | 2000 | 40 | 1 | 8 msec | ✓ | 110 | 95-105 | ✓ | |||||

| Skin Resistance Under Driving Stress (Healey and Picard, 2005b) | health-drivedb/driver02 | 22000 | 2000 | 40 | 1 | 60 msec | ✓ | ✓ | |||||||

| Skin Resistance Under Driving Stress (Healey and Picard, 2005b) | health-drivedb/driver09/foot | 20000 | 2000 | 40 | 1 | 60 msec | ✓ | ✓ | |||||||

| Respiration Under Driving Stress (Healey and Picard, 2005b) | health-drivedb/driver09/resp | 20000 | 2000 | 40 | 1 | 60 msec | ✓ | ✓ | |||||||

| ECG Premature Ventricular Contraction (Laguna et al., 1997) | health-qtdb/0606 | 10000 | 2000 | 40 | 1 | 4 msec | ✓ | 176 | 170-180 | ✓ | |||||

Table 2 details the data sets used for evaluation. Note that the data sets belong to a diverse set of domains. The diversity of the data sets is reflected based on the following attributes:

-

❚

Seasonality Period (SP): Most of these time series exhibit seasonal behavior and the SP increases with TG. For instance, the minutely time series of operations data experience daily seasonality (period=). In contrast, secondly time series of IoT workloads experience very long seasonalities (period= - ) depending on the operation cycles of the appliances. Health series have coarse TG but the seasonal periodicity are usually small(period= - ).

-

❚

Seasonal Jitter: It refers to the presence of jitter in seasonal periods, and is an artifact of coarse TG. IoT and Health time series exhibit this property.

-

❚

Non-stationarity: Time series exhibit one or more types of nonstationarities with respect to their level (amplitude) and variance.

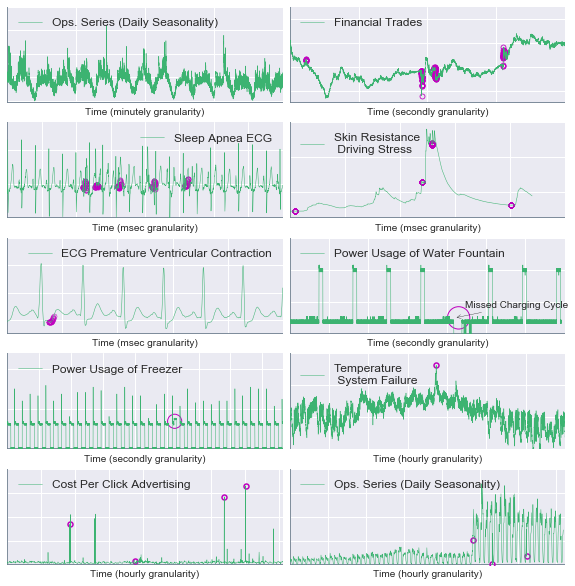

Figure 2 illustrates characteristics of these time series. From the figure we note that most of the series are non-stationary and exhibit one of these types of nonstationarities:

The Numenta Anomaly Benchmark (NAB) (Lavin and Ahmad, 2015) and the Yahoo Anomaly Dataset (YAD) (Laptev et al., 2015) – which are considered industry standard – provide labels. NAB itself is a collection of time series from multiple domains like Advertising Click Through Rates (nab-ctr), volume of tweets per hour (nab-twt), sensor data for temperature (nab-iot). The NAB series used herein have hourly granularity. YAD is composed of three distinct data sets: yahoo-a1 comprises of a set of operations time series with hourly granularity, whereas yahoo-a2 and yahoo-a3 are synthetic time series.

Anomalies detection in the context of high frequency trading (HFT) surfaces arbitrage opportunities and hence can have potentially large impact to the bottom line. In light of this, we included a month long time series of trades for the tickers FB, GOOG, NFLX and SPY. The time series, purchased from QuantQuote (qua, 2017), are of secondly granularity.

We collected 44 minutely time series of operations data from our production environment. The ECO dataset (Beckel et al., 2014) comprises of secondly time series of power usage. Given the increasing emphasis on healthcare apps owing to the use IoT devices in Healthcare domain, we included seven data sets from Physiobank (Goldberger et al., e 13).

4.2. Methodology

To emulate unbounded evolutionary data streams, we chose long time series and applied anomaly detection techniques for every new data point in a streaming fashion. Further, we limit the number of data points a technique can use to determine whether the most recent observation is anomalous. A common way of doing this is to define a maximum Window Size that can be used for training or modeling.

Window size is an important hyper-parameter which has a direct correlation with runtime and accuracy. Longer windows require more processing time, while shorter windows result in drop in accuracy. For a fair comparative analysis, we set an upper limit on the values of window size for different data sets, as listed in Table 2. The values were set based on the data set, e.g., for the minutely operations time series (seasonal period=1440), one would need at least periods (Lawhern et al., 2007) to capture the variance in the seasonal patterns, giving a seasonal period of . This is the maximum allowed valuer; techniques may choose a shorter seasonal period depending on their requirements. For instance, TBATS needs fewer number of periods to learn and hence, we used only periods (WinSize=) in the experiments. Data sets such as YAD have fixed seasonal periods due to hourly TG, and hence, require much smaller window sizes to achieve maximum accuracy. IoT data sets have the longest window sizes due to the long seasonal periods.

Pattern Length (PL) is a hyper-parameter of all pattern mining techniques. The value of PL is dependent on the application and the type of anomalies. For example, IoT workloads require a PL of minutes, whereas Health time series usually require a PL of only . A moving window equal to the PL is used to extract subsequences from the time series. Although pattern anomalies are typically not of fixed length in production data, most techniques require a fixed length to transform the series into subsequences. To alleviate this, post-processing can be used to string together multiple length anomalies (Senin et al., 2015).

In order to characterize the runtime performance of the technique listed in Table 1, we measured the runtime needed to process every new point in a time series. For every new data point in a time series, each technique was run times and the median runtime was recorded. Across a single time series, the run-times for all the data points in the time series were averaged. Across multiple time series in a group, geometric mean of the run-times111This approach is an industry standard as evidenced by its use by SPEC (SPE, 2006) for over 20 years. of the individual series is used to represent the runtime for the group. Given that some of the data sets listed in Table 2 have short time series (e.g., NAB and YAD), we replicate these series times to increase their length. All run-times are reported in milliseconds (msec).

4.2.1. Metrics

Accuracy for labeled data sets is calculated in terms of the correctly identified anomalies called True Positives (TP), falsely detected anomalies called False Positives (FP) and missed anomalies called False Negatives (FN). To measure accuracy of a single time series, we use the following three metrics:

-

❏

Precision: defined as the ratio of true positives (TP) to the total detected anomalies:

-

❏

Recall: defined as the ratio of true positives (TP) to the total labeled anomalies:

-

❏

-score: defined as the weighted harmonic mean of Precision and Recall: , where is a constant that weights precision vs recall based on the application

In most applications, it is common to set =1, giving equal weight-age to precision and recall. But for healthcare, recall is sometimes more important than precision and hence =2 is often used (Lawhern et al., 2013). This is because false negatives can be catastrophic. To calculate accuracy across a group of time series, we report the micro-average -score (Forman and Scholz, 2010), which calculates precision and recall across the whole group. The use of this is subject to time series in a group being similar to each other.

Most of our data sets are labeled with point anomalies. In light of this, we propose the following methodology to compute accuracy for detected patterns against labeled point anomalies. Let denote a time series and the pattern - be detected as a pattern anomaly. Let be a true anomaly. A naive way to compute a is to have a pattern anomaly end at the true anomaly. In this case, - would be considered a . In contrast, can correspond to an instance where a true anomaly occurs anywhere inside the boundary of an anomalous pattern. Pattern anomalies are very often closely spaced due to the property of neighborhood similarity as described by Handschin and Mayne (Keogh et al., 2005). Given this, it is important to count each true anomaly only once even if multiple overlapping pattern anomalies are detected. A post-processing pass can help weed out such overlapping subsequences.

Given that the methodology of calculating accuracy is so different for pattern techniques, we advise the reader to only compare accuracies of pattern techniques with other pattern techniques.

4.2.2. System Configuration

Table 3 details the hardware and software system configuration. Table 4 details the and packages used. For HOTSAX and RRA, we modified the implementation so as to make them amenable to a streaming data context.

| Architecture | Intel(R) Xeon(R) | Frequency | 2.40GHz |

|---|---|---|---|

| Num Cores | 24 | Memory | 128GB |

| L1d cache | 32K | L1i cache | 32K |

| L2 cache | 256K | L3 cache | 15360K |

| OS Version | CentOS Linux release 7.1.1503 | R, Python | 3.2.4, 2.7 |

| R | |||

| stream, streamMOA | MASS | rrcov | jmotif |

| robustbase | forecast | tsoutliers | rpca |

| Python | |||

| pykalman | scikit-learn | tdigest | statsmodels |

4.3. Hyper-parameters

In the interest of reproducibility, we detail the hyper-parameters used for the techniques listed in Table 1. In addition, we detail any transformation and/or tuning needed to ensure a fair comparative analysis.

4.3.1. Statistical techniques

For parametric statistical techniques such as mu-sigma, med-mad et cetera, we set the threshold to or its equivalent robust estimate of scale.

A constant false alarm rate can be set for techniques such as t-digest and GESD. In case of the former, we set the threshold at percentile which is equivalent to . In case of the latter, one can set an upper limit on the number of anomalies. Based on our experiments, we set this parameter to for all, but the Health data sets. The parameter was set to for the the Health data sets to improve recall at the expense of precision.

Model parameter estimates are computed at each new time step over the moving window. As these techniques do not handle seasonality or trend, we removed seasonality and trend using STL and evaluate these techniques on the residual of the STL. In light of this, i.e., statistical techniques are not applicable to the raw time series in the presence of seasonality or trend, the accuracy of these techniques should not be compared with ML and Pattern Mining based techniques.

4.3.2. Time series analysis techniques

Parametric time series analysis techniques such as TBATS, SARMA, STL-ARMA estimate model parameters and evaluate incoming data against the model. Retraining at every time step is often unnecessary as the temporal dynamics do not change at every point. In practice, it is common to retrain the model periodically and this retraining period is another hyper-parameter. This period depends on the application, but it should not be greater than the window size. We set the retraining period to be the same as the window size. We include the training runtime as part of the total runtime of a techniques so as to assess the total detection time for anomalies.

STL with default parameters assumes periodic series. To allow gradual seasonal level drift, we set the stl-periodic parameter equal to . For RobustSTL, we use robust iterations. SDAR is an incremental technique that requires a learning rate parameter (). Based on our experiments, we set . RobustKF is the robust kalman filter by Ting et al.(Ting et al., 2007) which requires parameters and for the prior on the robustness weights. We set .

We also evaluate techniques based on Intervention Analysis of time series implemented in the tsoutliers package of R. These techniques are significantly slower than most other techniques we evaluate in this work, e.g., for a series with data points, it took over 5 minutes (!) for parameter estimation. Clearly, these techniques are non-viable for real-time streaming data.

4.3.3. Pattern mining and machine learning techniques

Most pattern techniques require pattern length (PL) as an input parameter. Table 5 lists the specific parameters and their respective values for each technique. HOTSAX and RRA are robust to presence of trend in a time series as they use symbolic approximation, but they do require the series to be studentized. All the other pattern techniques are not robust to presence of trend as they use the underlying real valued series directly. Thus, all the subsequences need to be mean adjusted (i.e., subtract the mean from all the data points) to avoid spurious anomalies due to changing trend. Scale normalization is not carried as change in scale is an anomaly itself.

Keogh et al. proposed a noise reduction technique wherein a subsequence is rejected if its variance lies below a threshold, (Keogh et al., 2005). Our experiments show that this preprocessing step is critical, from an accuracy standpoint, for all pattern mining techniques considerably. Therefore, we use it by default, with =.

| Technique | Parameters | Description |

|---|---|---|

| HOTSAX | paa-size=, a-size= | PAA Size, Alphabet Size |

| RRA | paa-size=, a-size= | PAA Size, Alphabet Size |

| DenStream | epsilon= lambda= | MC radius, Decay Constant |

| DBStream | r=, Cm=, shared-density=True | MC radius, minimum weight for MC |

| ClustTree | max-height=, lambda= | Tree Height, Decay Constant |

| DBScan | eps= | Threshold used to re-cluster ClusTree |

| IForest | n-estimators=, contamin.= | Number of Trees, Number of Outliers |

| OneSVM | nu=, gamma= | support vectors, kernel coeff. |

| MB-means | n-clusters=, batch-size= | Number of Clusters, Batch Size |

DenStream is the only technique that works without an explicit re-clustering step. The technique can classify outlier micro-clusters () as anomalous, but this leads to a higher false positive rate. Alternatively, one can take the distance of the points to the nearest as the strength of the anomaly. This makes DenStream less sensitive to the radius as well. DenStream and DBStream are incremental techniques. Hence, they do not need an explicit window size parameter; having said that, they use a decay constant to discount older samples. IForest and OneSVM are not incremental techniques and hence, need to be retrained for each time step. MBKmeans is also not incremental, however, it uses cluster centroids from previous run to calculate the new clusters, which allows the clustering to converge faster.

5. Analysis

In this section we present a deep dive analysis of the techniques listed in Table 1, using the data sets detailed in Table 2.

5.1. Handling Non-stationarity

In this subsection we walk the reader through how the different techniques handle the different sources of non-stationarity exhibited by the data. Most techniques assume that the underlying process is stationary or evolving gradually. However, in practice, this assumption does not hold true thereby resulting in a larger number of false positives immediately after a process change. Though detecting the change is itself important, the false positives adversely impact the efficacy in a material fashion.

-

❐

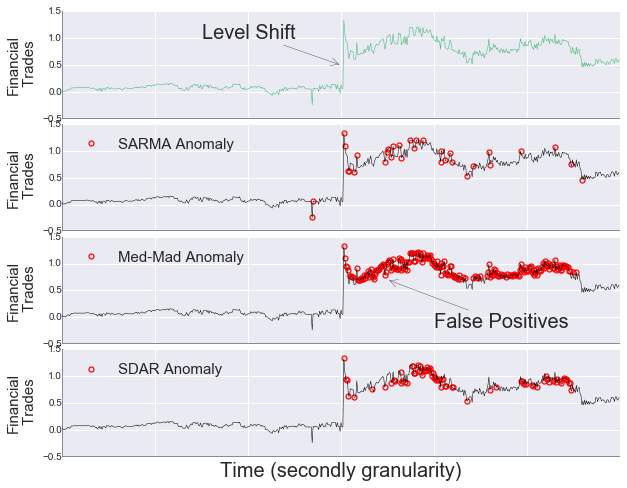

Trend and Level Shifts (LS): Statistical techniques are not robust to trend or level shifts. Consequently, their performance is dependent on the window size, which decides how fast these techniques adapt to a new level. Time series analysis techniques based on state space models (e.g., SARMA, TBATS) can identify level shifts and adapt to the new level without adding false positives. Figure 3(a) illustrates a financial time series, where SARMA and SDAR detect the level shift as an anomaly. med-mad can also detect the level shift but it surfaces many false positives right after the level shift. Pattern techniques mean-adjust the patterns. Hence, in the presence of level shifts, they do not surface false positives as long as the pattern shapes do not change rapidly.

-

❐

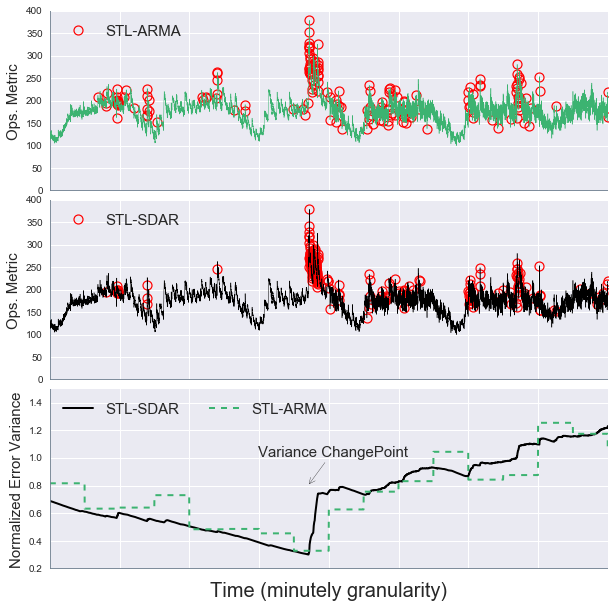

Variance Change (VC): Figure 3(b) shows an operations series with a variance change. Iterative techniques such as STL-SDAR adapt faster to changing variance which allows them to limit the number of false positives. On the other hand, STL-ARMA and SARMA are periodically re-trained and oscillate around the true error variance.

-

❐

Seasonal Drift (SD): Gradually changing seasonal pattern is often observed in iot and ops time series. SARMA adapts to such a drift with default parameters. STL adapts as well if the parameter is set to false – this ensures that seasonality is not averaged out across seasons.

-

❐

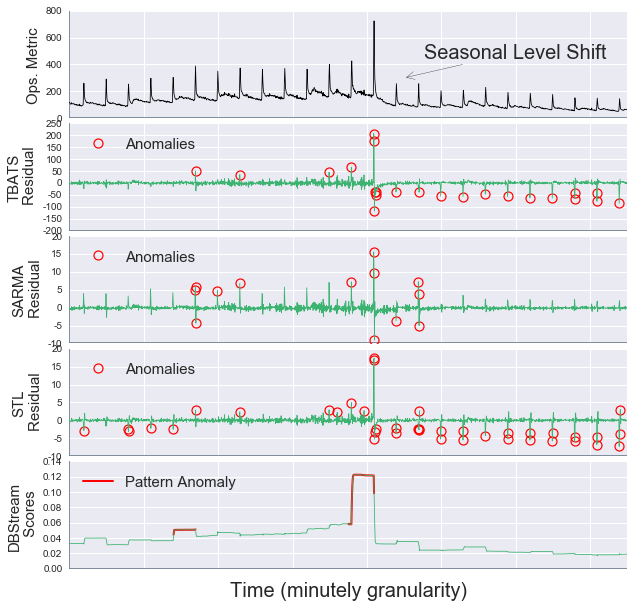

Seasonal Level Shift (SLS): SLS is again exhibited predominantly in iot and ops series as illustrated in Figure 3(c). TBATS does not adapt to SLS or SD as it handles seasonality using Fourier terms and assumes that the amplitudes of seasonality do not change with time. SARMA handles SLS smoothly as it runs a Kalman-Filter on the seasonal lags and hence only detects anomalies when the shift happens. On the other hand, STL is not robust to SLS and may result in false positives as exemplified by Figure 3(c). Pattern Techniques such as DBStream are very robust to SLS and can detect the pattern around the shift without any false positives.

-

❐

Seasonal Jitter (SJ): SJ is an artifact of fine-grain TG and is predominantly exhibited in iot (sec) and health (msec) time series. Statistical and time series analysis techniques do not model this non-stationary behavior. As a consequence, in such cases, only pattern anomaly techniques can be used.

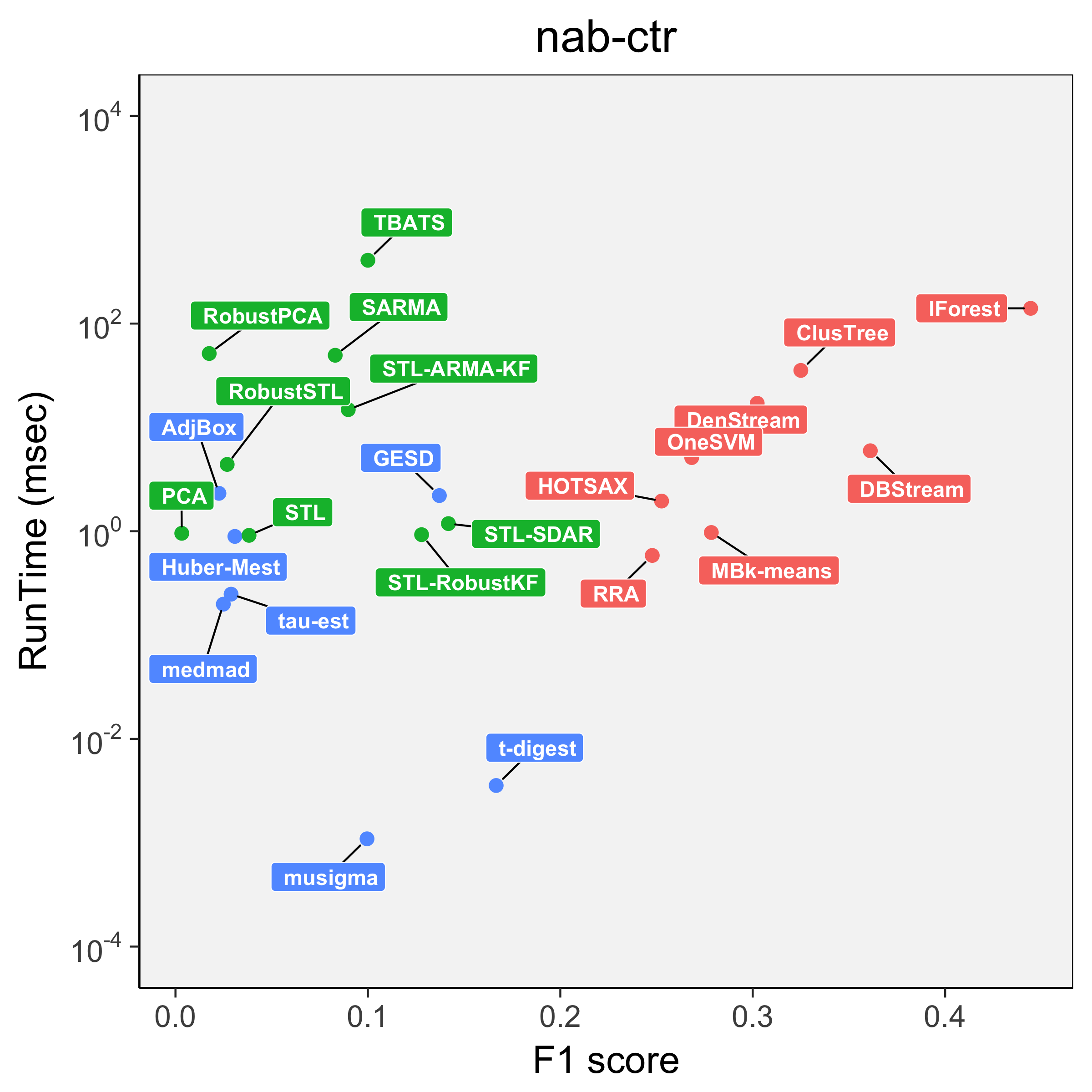

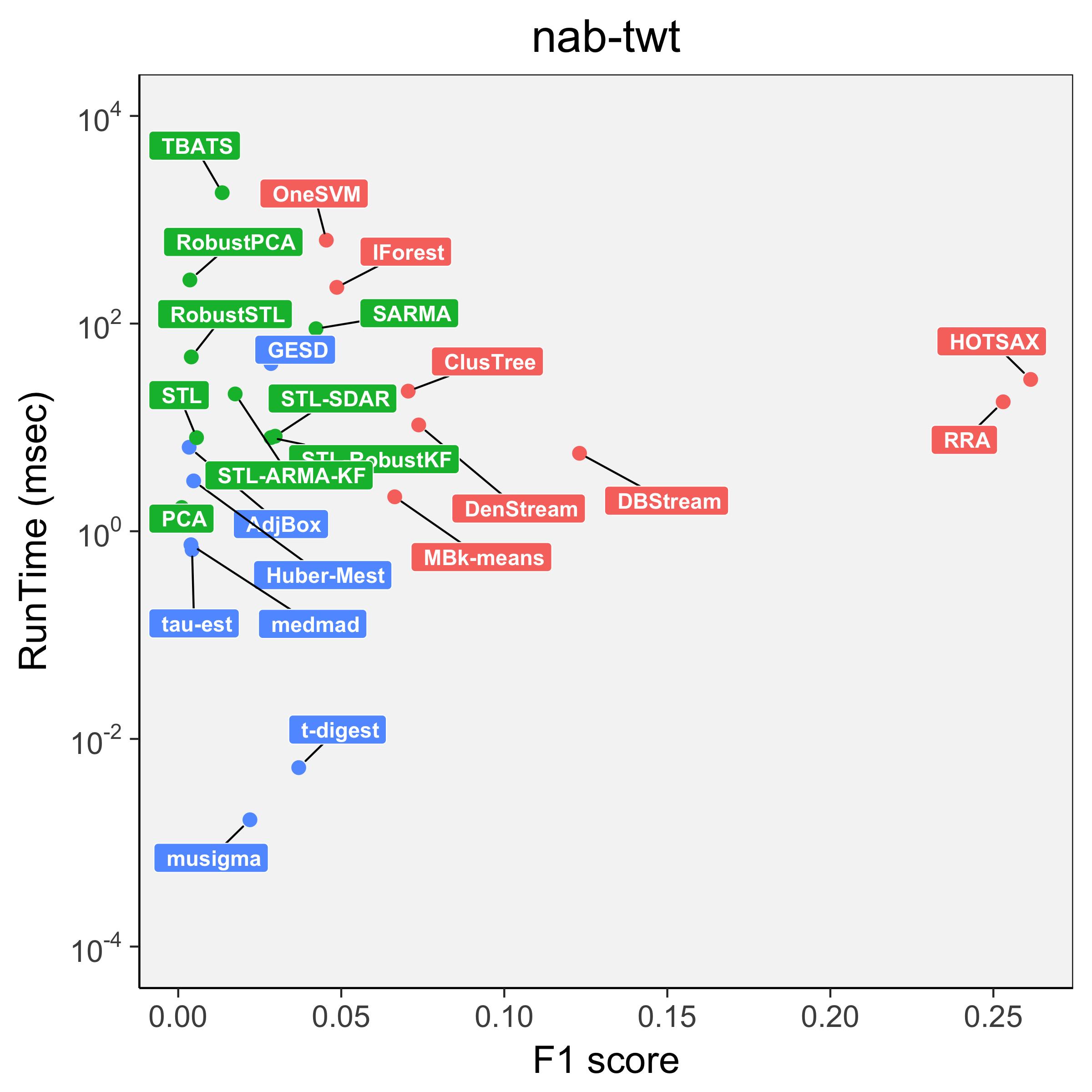

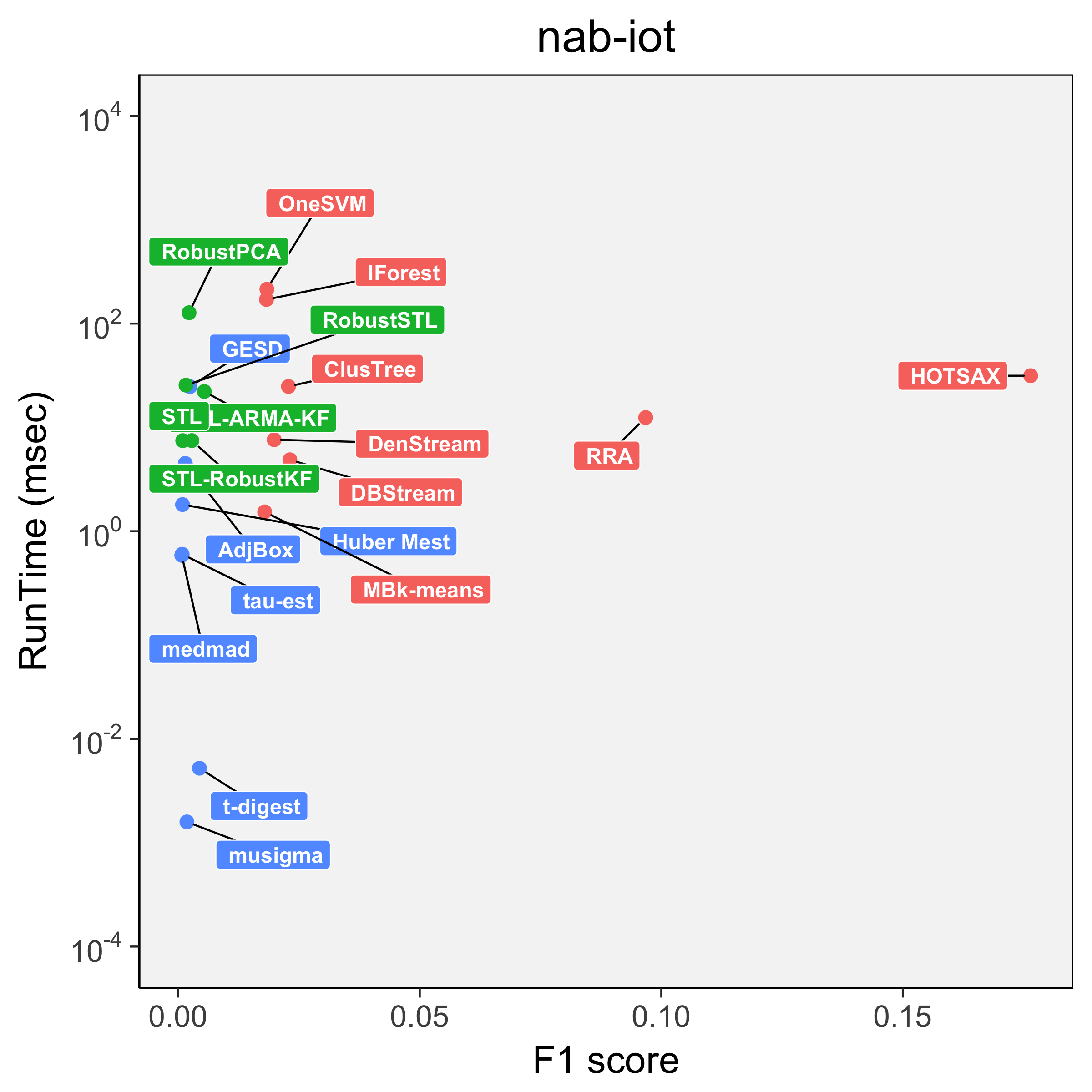

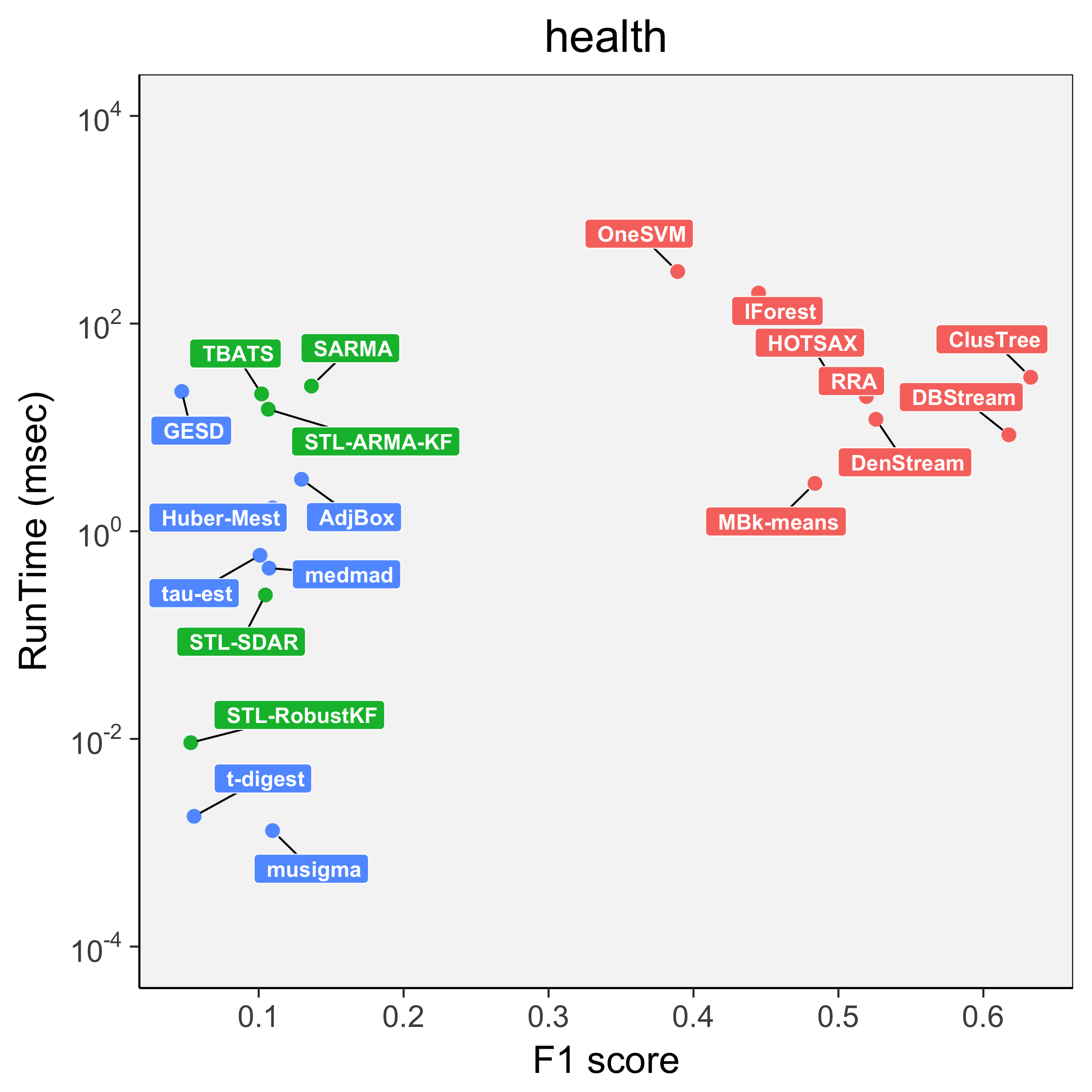

5.2. Runtime Analysis

In this section we present a characterization of the techniques listed in Table 1 with respect to their runtimes. In the figures referenced later in the section, the benchmarks are organized in an increasing order of seasonal period from left to right.

-

❐

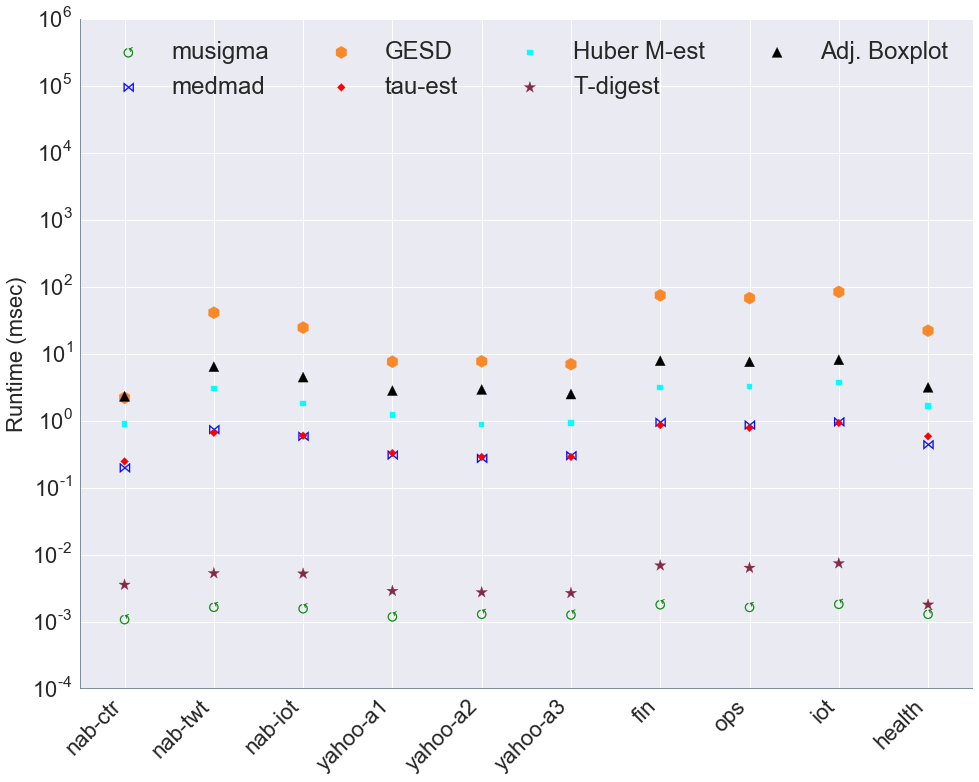

Statistical techniques: From Figure 4(a) we note that mu-sigma and t-digest – recall that these are incremental too – are the fastest(¡10 ) in this category. Robust techniques are at least an order of magnitude slower! This stem from the fact that these techniques solve an optimization problem. Although GESD is the slowest technique in this category, it let’s one set an upper bound on the number of anomalies, which in turn helps control the false alarm rate(CFAR).

-

❐

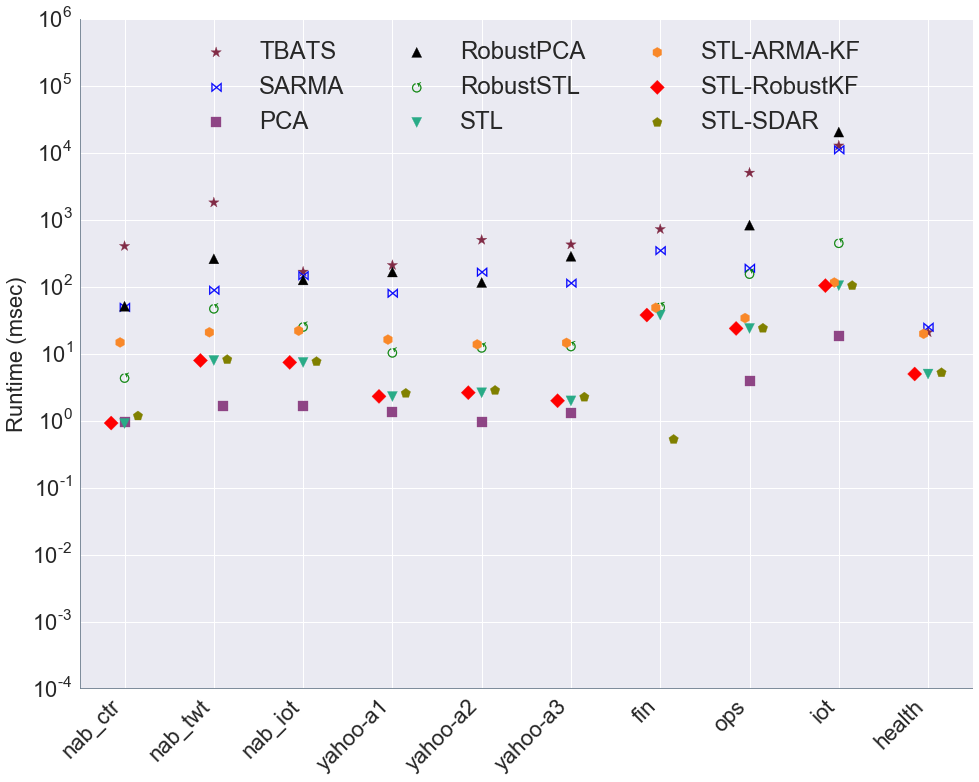

Time series analysis techniques: From Figure 4(b) we note that STL is the fastest technique (1-5 ) in this category. Having said that, the runtime increases considerably as the seasonal period increases (left to right). Robust STL is an order of magnitude slower than STL even when the number of robust iterations is limited to . This can be ascribed to the fact that iterations with the robust weights in STL are significantly slower than the first one.

SARMA and TBATS are significantly slower than most other techniques in this category. This is an artifact of the window length needed to fit these models being proportional to the seasonal period and thus, model parameters need to be estimated on a much larger window. On the other hand, a technique such as STL-ARMA applies ARMA on the residual of STL and therefore does not need to deal with seasonality, which allows for a much smaller training window. Runtimes for TBATS, SARMA and RPCA increase exponentially with an increase in seasonal period. Hence, for secondly time series, these methods become nonviable.

SDAR and RobustKF are fast incremental techniques that can execute in . However, these techniques cannot be applied to seasonal series as is. This limitation can be alleviated by applying STL as a preprocessing step. From Figure 4(b), we note that STL-SDAR and STL-RobustKF are almost as fast as STL. Even though STL-ARMA trains on small training windows, note that it adds significant additional runtime to STL. This impact is not as prominent in the case of the ops and fin data sets - this is due to the fact that STL itself has long runtimes for these data sets. Although we note that PCA is a very fast technique, its accuracy is very low (this is discussed further in the next subsection). This is owing to the PCs being not robust to anomalies. themselves.

-

❐

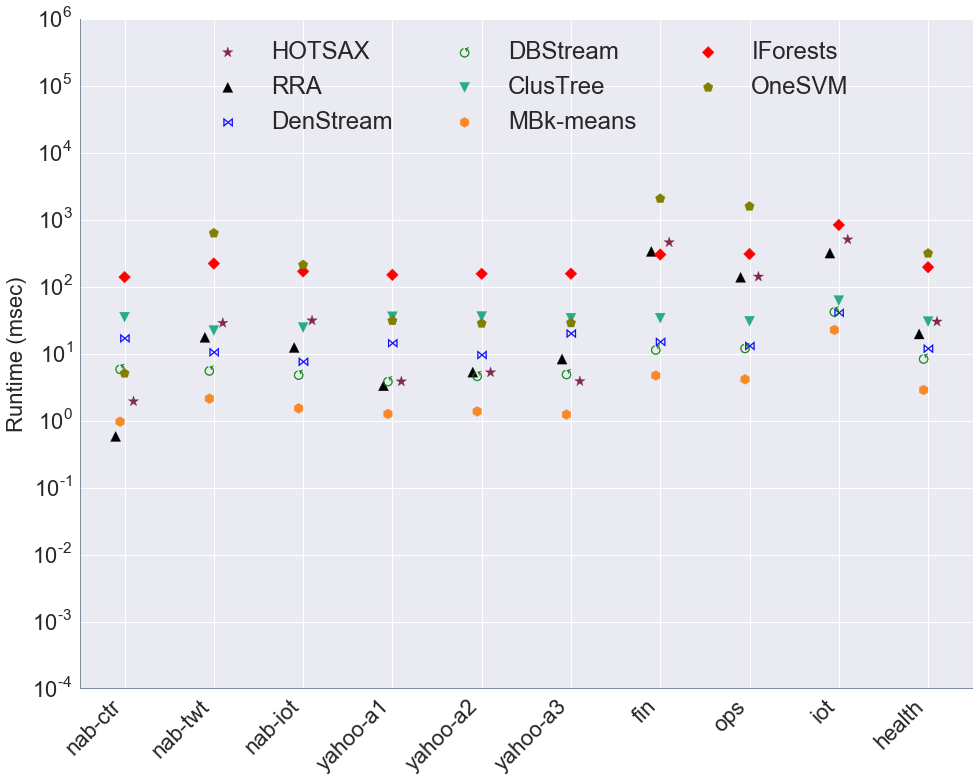

Pattern and machine learning techniques: From Figure 4(c) we note that IForest and OneSVM have the worst runtime performance as they are not incremental and they need to be trained for every new data point. MB-Kmeans is relatively faster even though it performs clustering for every new point. This is because the clustering has fast convergence if the underlying model drift is gradual.

Although the internal data structures HOTSAX and RRA can be generated incrementally, finding the farthest point using these structures accounts for majority of the runtime. Thus, the runtime for HOTSAX, RRA is not dependent on the window size; instead, it is a function of the variance in the data. Data sets such as fin, ops and iot exhibit high variance due to fine grain TG – this impacts the runtime of HOTSAX, RRA. med data set on the other hand has coarse TG and therefore have a low variance in terms of the shapes of patterns and hence, HOTSAX and RRA are significantly faster for them.

DBStream is the fastest micro-clustering technique across all data sets even though it does have an offline clustering component which is executed for every new point. This is because it maintains the shared density between s on-the-fly and then uses DBScan over these s to produce the final clustering. DenStream is slower than DBStream because the distance of a data point to all ’s needs to be computed to calculate the strength of the anomaly. Alternatively, one can tag all s as anomalous which helps to reduce runtime but adversely impacts the FAR. From Figure 4(c) we note that ClusTree is the slowest of all the micro-clustering techniques.

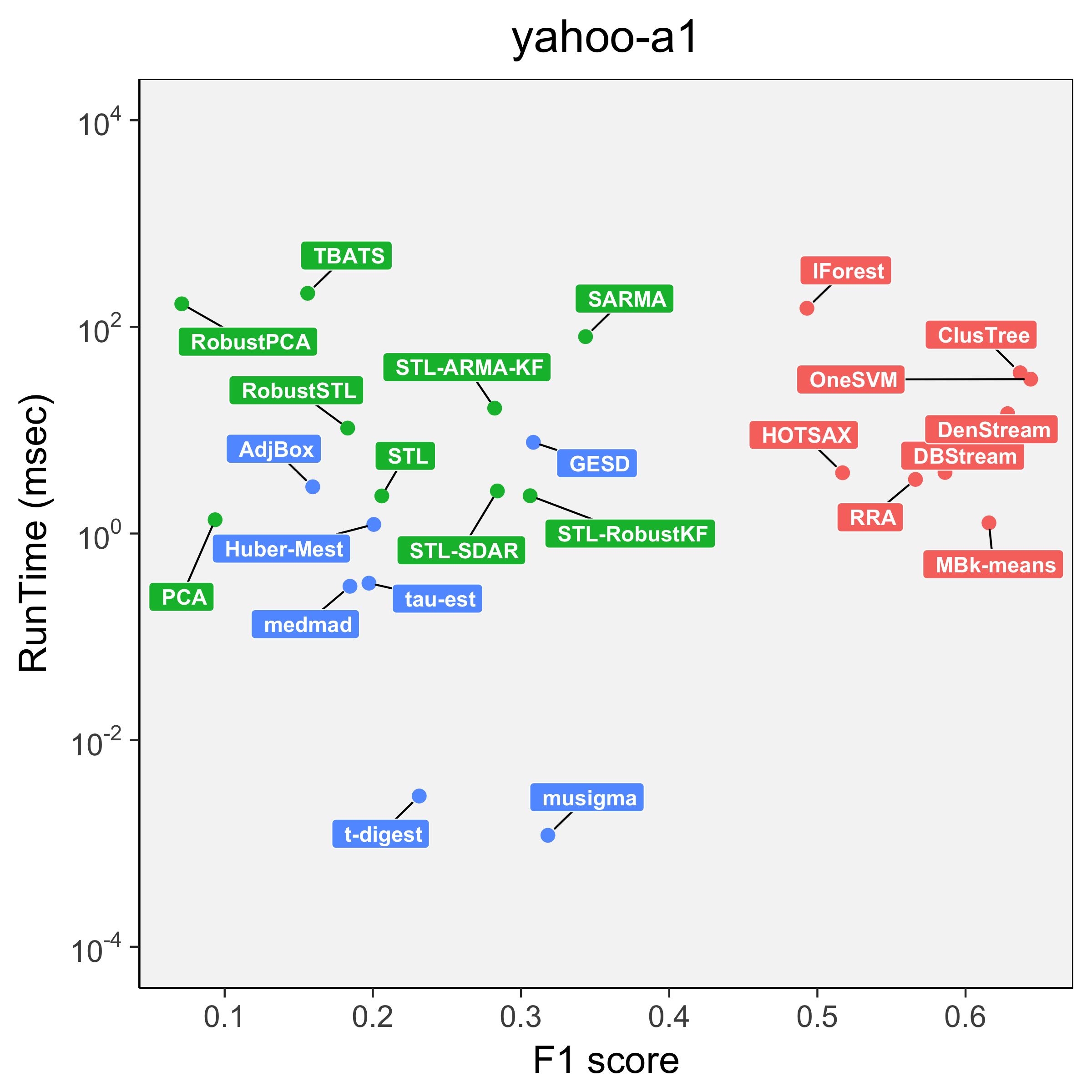

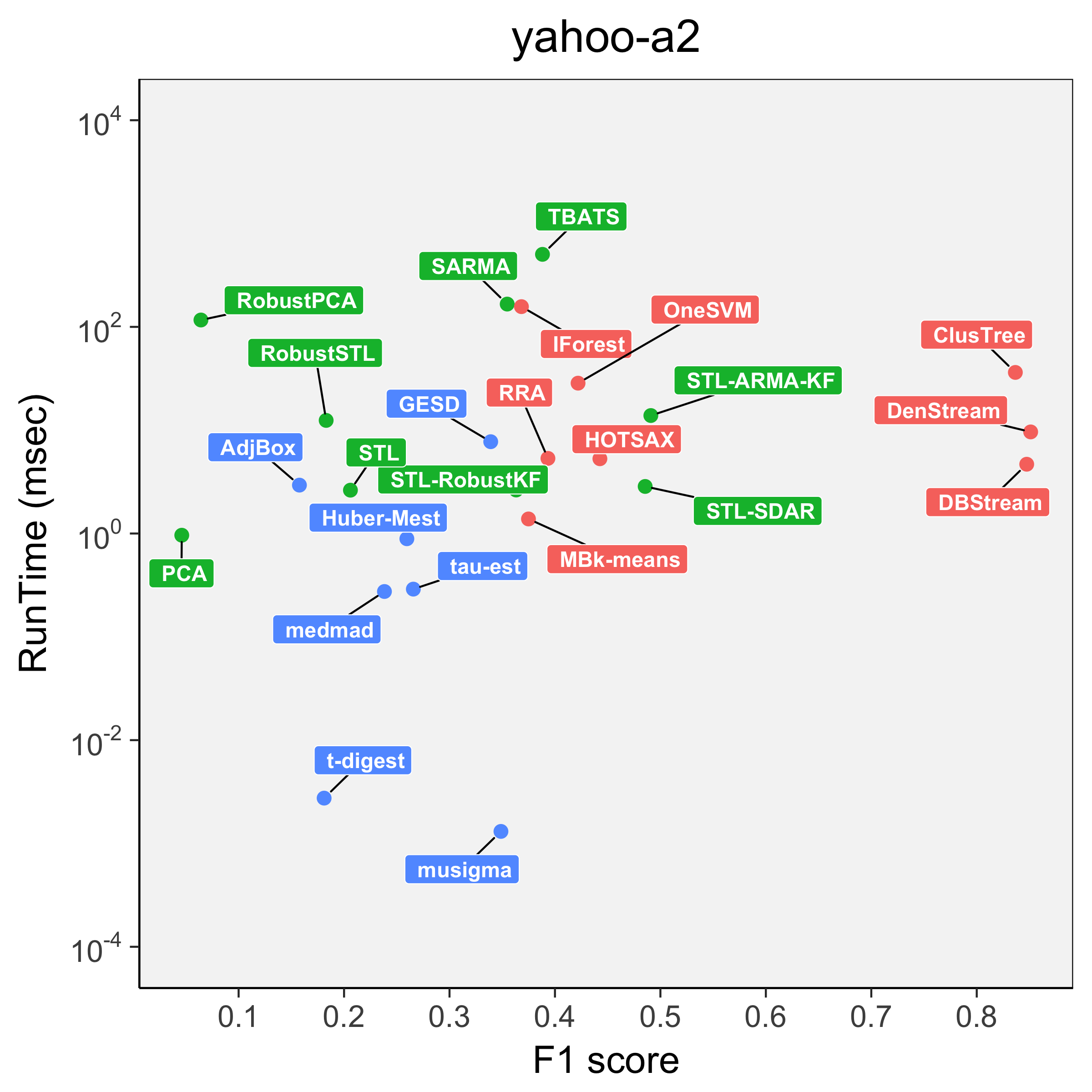

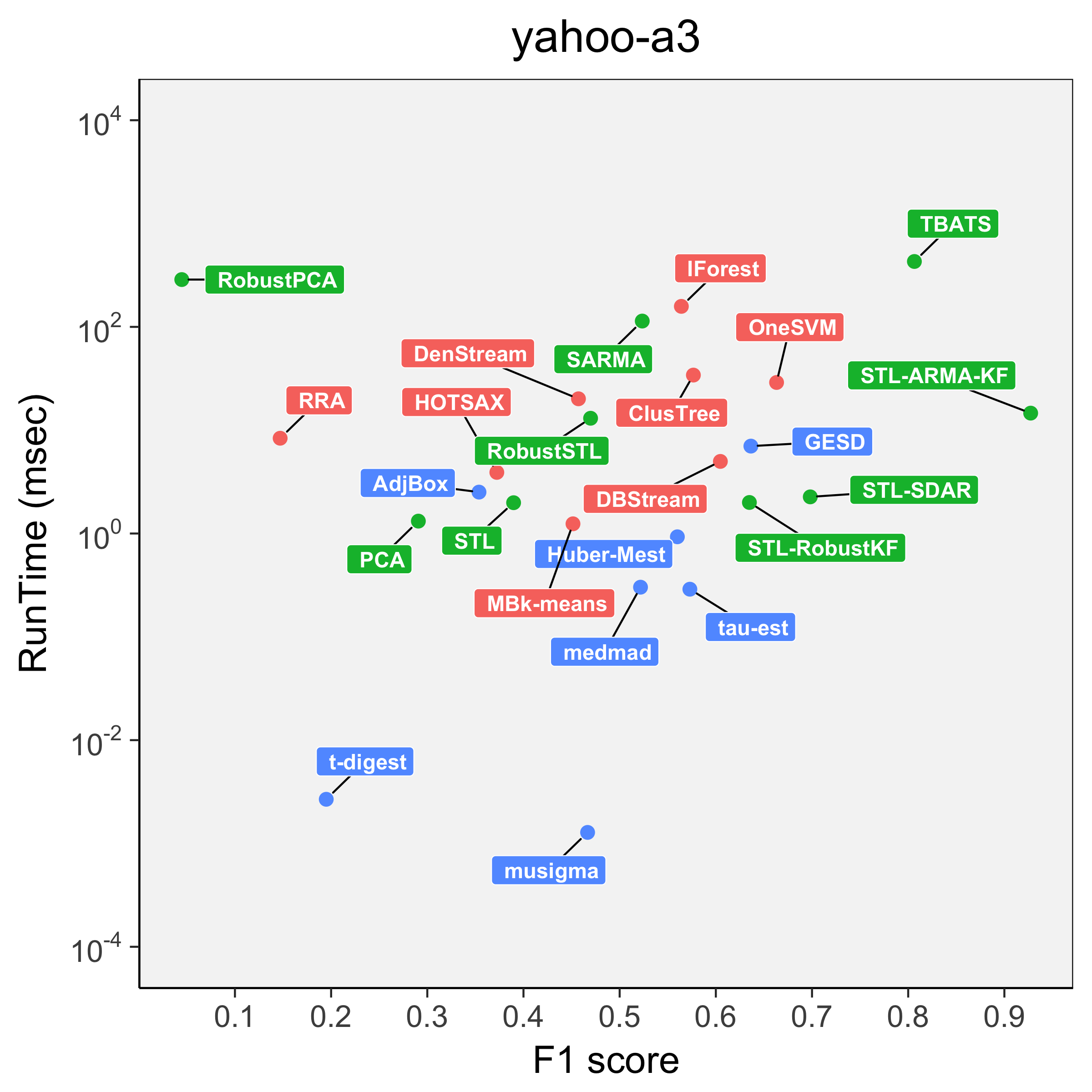

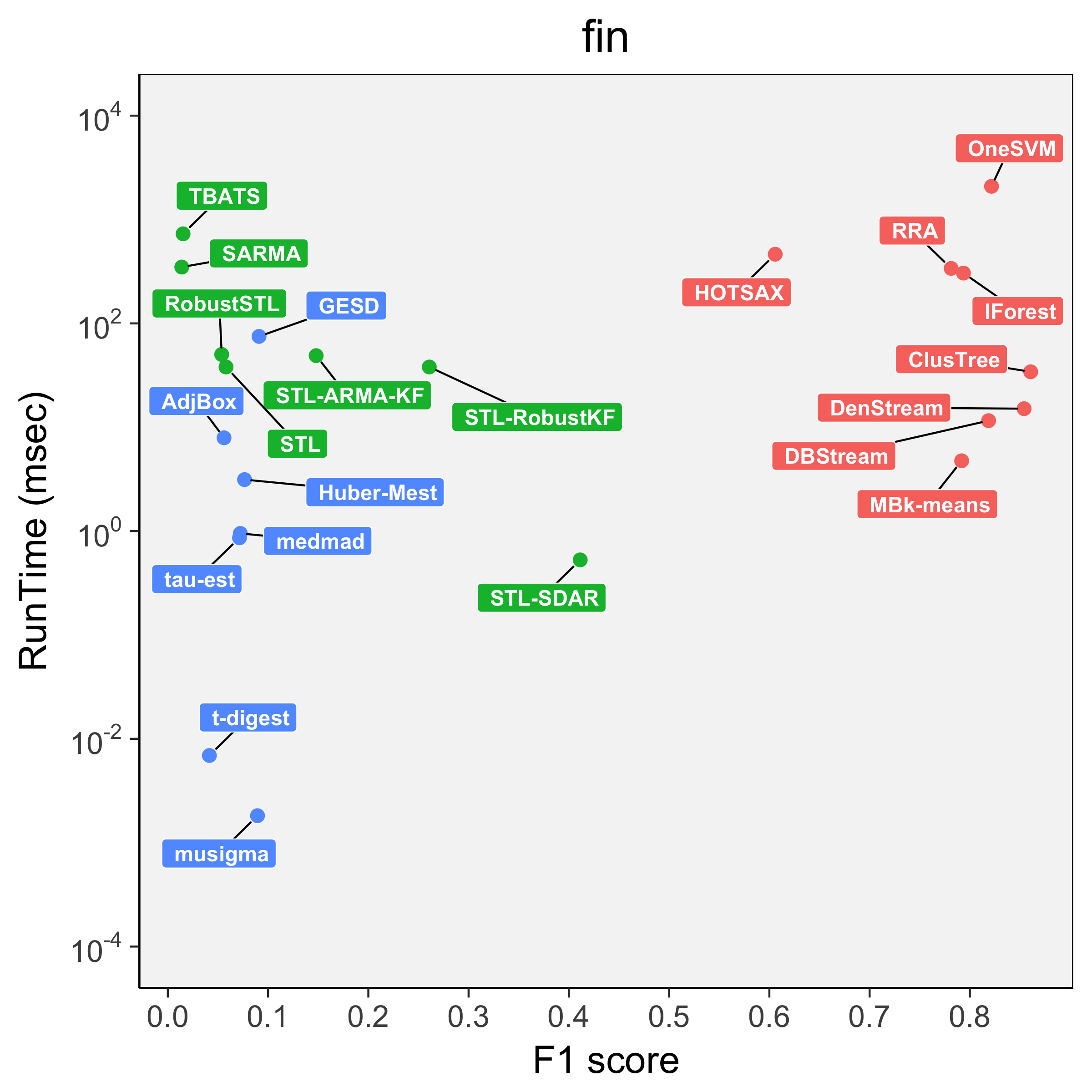

5.3. Accuracy-Speed Tradeoff

Figure 6 charts the landscape of accuracy-speed tradeoff for the techniques listed in Table 1 across all data sets tabulated in Table 2. Table 6 details the Precision, Recall along with the -score. In this rest of this subsection, we present an in-depth analysis of the trade-off from multiple standpoints.

| Datasets | MuSigma | Med-MAD | tau-est | Huber Mest | AdjBox | GESD | t-digest | SARMA | ||||||||||||||||

| Pr | Re | Pr | Re | Pr | Re | Pr | Re | Pr | Re | Pr | Re | Pr | Re | Pr | Re | |||||||||

| yahoo-a1 | 0.268 | 0.392 | 0.318 | 0.108 | 0.623 | 0.185 | 0.118 | 0.61 | 0.197 | 0.121 | 0.592 | 0.201 | 0.092 | 0.579 | 0.159 | 0.303 | 0.314 | 0.308 | 0.221 | 0.242 | 0.231 | 0.284 | 0.434 | 0.344 |

| yahoo-a2 | 0.234 | 0.687 | 0.349 | 0.139 | 0.83 | 0.238 | 0.158 | 0.83 | 0.266 | 0.154 | 0.83 | 0.26 | 0.087 | 0.83 | 0.158 | 0.215 | 0.803 | 0.339 | 0.107 | 0.588 | 0.181 | 0.232 | 0.749 | 0.355 |

| yahoo-a3 | 0.467 | 0.745 | 0.467 | 0.353 | 0.999 | 0.522 | 0.402 | 0.999 | 0.573 | 0.389 | 0.999 | 0.56 | 0.215 | 0.999 | 0.354 | 0.47 | 0.986 | 0.636 | 0.111 | 0.787 | 0.195 | 0.355 | 0.993 | 0.523 |

| nab-ctr | 0.053 | 0.786 | 0.1 | 0.013 | 1 | 0.025 | 0.015 | 1 | 0.029 | 0.016 | 1 | 0.031 | 0.011 | 1 | 0.023 | 0.075 | 0.857 | 0.137 | 0.093 | 0.786 | 0.167 | 0.044 | 0.786 | 0.083 |

| nab-twt | 0.011 | 0.743 | 0.022 | 0.002 | 0.914 | 0.004 | 0.002 | 0.914 | 0.004 | 0.002 | 0.914 | 0.005 | 0.002 | 0.886 | 0.003 | 0.015 | 0.714 | 0.028 | 0.019 | 0.743 | 0.037 | 0.022 | 0.75 | 0.042 |

| nab-iot | 0.001 | 0.167 | 0.002 | 0 | 0.167 | 0.001 | 0 | 0.167 | 0.001 | 0 | 0.167 | 0.001 | 0.001 | 0.333 | 0.001 | 0.001 | 0.167 | 0.002 | 0.002 | 0.333 | 0.004 | 0 | 0 | - |

| fin | 0.073 | 0.114 | 0.089 | 0.044 | 0.203 | 0.072 | 0.045 | 0.17 | 0.071 | 0.049 | 0.177 | 0.076 | 0.033 | 0.196 | 0.056 | 0.073 | 0.12 | 0.091 | 0.037 | 0.047 | 0.041 | 0.007 | 0.144 | 0.014 |

| health | 0.109 | 0.11 | 0.11 | 0.067 | 0.272 | 0.107 | 0.065 | 0.231 | 0.101 | 0.075 | 0.202 | 0.11 | 0.084 | 0.283 | 0.13 | 0.037 | 0.066 | 0.047 | 0.042 | 0.08 | 0.055 | 0.129 | 0.145 | 0.136 |

| TBATS | STL-ARMA-KF | STL | RobustSTL | STL-SDAR | STL-RobustKF | RobustPCA | PCA | |||||||||||||||||

| Pr | Re | Pr | Re | Pr | Re | Pr | Re | Pr | Re | Pr | Re | Pr | Re | Pr | Re | |||||||||

| yahoo-a1 | 0.106 | 0.295 | 0.156 | 0.225 | 0.378 | 0.282 | 0.133 | 0.454 | 0.206 | 0.111 | 0.525 | 0.183 | 0.372 | 0.23 | 0.284 | 0.299 | 0.313 | 0.306 | 0.038 | 0.585 | 0.071 | 0.062 | 0.191 | 0.094 |

| yahoo-a2 | 0.253 | 0.83 | 0.388 | 0.379 | 0.697 | 0.491 | 0.133 | 0.454 | 0.206 | 0.111 | 0.525 | 0.183 | 0.346 | 0.811 | 0.486 | 0.234 | 0.809 | 0.363 | 0.033 | 1 | 0.064 | 0.024 | 0.469 | 0.046 |

| yahoo-a3 | 0.678 | 0.995 | 0.806 | 0.865 | 0.999 | 0.927 | 0.242 | 1 | 0.39 | 0.307 | 0.999 | 0.47 | 0.537 | 0.999 | 0.698 | 0.468 | 0.986 | 0.635 | 0.023 | 0.996 | 0.045 | 0.184 | 0.686 | 0.291 |

| nab-ctr | 0.053 | 0.857 | 0.1 | 0.048 | 0.786 | 0.09 | 0.02 | 0.929 | 0.038 | 0.014 | 1 | 0.027 | 0.079 | 0.714 | 0.142 | 0.07 | 0.786 | 0.128 | 0.009 | 1 | 0.018 | 0.002 | 0.071 | 0.003 |

| nab-twt | 0.007 | 0.8 | 0.013 | 0.009 | 0.8 | 0.017 | 0.003 | 0.943 | 0.006 | 0.002 | 0.857 | 0.004 | 0.015 | 0.686 | 0.03 | 0.015 | 0.714 | 0.028 | 0.002 | 0.935 | 0.004 | 0.001 | 0.226 | 0.001 |

| nab-iot | 0 | 0 | - | 0.003 | 0.167 | 0.005 | 0 | 0.167 | 0.001 | 0.001 | 0.333 | 0.002 | 0 | 0 | - | 0.001 | 0.167 | 0.003 | 0.001 | 1 | 0.002 | 0 | 0 | - |

| fin | 0.008 | 0.151 | 0.015 | 0.109 | 0.231 | 0.148 | 0.034 | 0.191 | 0.058 | 0.032 | 0.182 | 0.054 | 0.443 | 0.383 | 0.411 | 0.221 | 0.319 | 0.261 | - | - | - | - | - | - |

| health | 0.109 | 0.096 | 0.102 | 0.103 | 0.11 | 0.107 | - | - | - | - | - | - | 0.104 | 0.105 | 0.105 | 0.057 | 0.05 | 0.053 | - | - | - | - | - | - |

| HOTSAX | RRA | DenStream | ClusTree | DBStream | IForest | MB-means | OneSVM | |||||||||||||||||

| Pr | Re | Pr | Re | Pr | Re | Pr | Re | Pr | Re | Pr | Re | Pr | Re | Pr | Re | |||||||||

| yahoo-a1 | 0.783 | 0.386 | 0.517 | 0.675 | 0.488 | 0.566 | 0.569 | 0.702 | 0.628 | 0.594 | 0.686 | 0.637 | 0.646 | 0.537 | 0.586 | 0.46 | 0.531 | 0.493 | 0.563 | 0.68 | 0.616 | 0.58 | 0.724 | 0.644 |

| yahoo-a2 | 0.471 | 0.417 | 0.443 | 0.312 | 0.532 | 0.393 | 0.741 | 1 | 0.851 | 0.719 | 1 | 0.837 | 0.759 | 0.959 | 0.847 | 0.226 | 0.989 | 0.368 | 0.231 | 1 | 0.375 | 0.267 | 1 | 0.422 |

| yahoo-a3 | 0.431 | 0.328 | 0.372 | 0.105 | 0.244 | 0.147 | 0.411 | 0.514 | 0.457 | 0.466 | 0.755 | 0.577 | 0.784 | 0.492 | 0.605 | 0.486 | 0.672 | 0.564 | 0.471 | 0.433 | 0.451 | 0.603 | 0.737 | 0.663 |

| nab-ctr | 0.148 | 0.857 | 0.253 | 0.141 | 1 | 0.248 | 0.181 | 0.929 | 0.302 | 0.197 | 0.929 | 0.325 | 0.224 | 0.929 | 0.361 | 0.3 | 0.857 | 0.444 | 0.169 | 0.786 | 0.278 | 0.162 | 0.786 | 0.268 |

| nab-twt | 0.169 | 0.571 | 0.261 | 0.16 | 0.6 | 0.253 | 0.038 | 0.971 | 0.074 | 0.037 | 0.971 | 0.071 | 0.066 | 0.914 | 0.123 | 0.025 | 0.971 | 0.049 | 0.034 | 0.943 | 0.066 | 0.023 | 0.714 | 0.045 |

| nab-iot | 0.107 | 0.5 | 0.176 | 0.054 | 0.5 | 0.097 | 0.01 | 0.5 | 0.02 | 0.012 | 0.5 | 0.023 | 0.012 | 0.333 | 0.023 | 0.009 | 0.667 | 0.018 | 0.009 | 0.667 | 0.018 | 0.009 | 0.667 | 0.018 |

| fin | 0.932 | 0.449 | 0.606 | 0.952 | 0.663 | 0.781 | 0.806 | 0.908 | 0.854 | 0.816 | 0.91 | 0.861 | 0.888 | 0.759 | 0.819 | 0.808 | 0.78 | 0.794 | 0.686 | 0.936 | 0.792 | 0.749 | 0.91 | 0.822 |

| health | 0.949 | 0.335 | 0.495 | 0.788 | 0.387 | 0.519 | 0.775 | 0.398 | 0.526 | 0.827 | 0.512 | 0.633 | 0.9 | 0.47 | 0.618 | 0.858 | 0.3 | 0.445 | 0.79 | 0.349 | 0.484 | 0.679 | 0.273 | 0.389 |

-

❐

Robustness and False Positives: Techniques such as med-mad surface a higher number of anomalies, which improves recall at the expense of precision as evident from Table 6. For best accuracy, we recommend to use robust techniques with CFAR such as GESD. From Table 6 we note that GESD outperforms most other statistical techniques. On the other hand, from Figure 6 we note that GESD has the highest runtime amongst the statistical techniques.

-

❐

Model Building: Estimating model parameters in the presence of anomalies can potentially impact accuracy adversely if the technique is not robust. This is observed from Figure 5 wherein an extreme anomaly biases the model obtained via SARMA thereby inducing false positives in the nab-ctr dataset. STL is susceptible to this as well. In contrast, Robust STL effectively down-weights the anomalies during model parameter estimation. From Figure 5 we also note that pattern mining techniques such as DenStream are more robust to anomalies, as they do not fit a parametric model.

Figure 7. Peformance of t-digest anomaly bursts -

❐

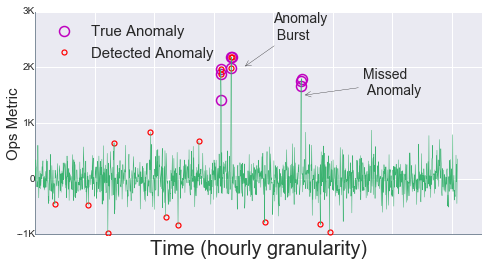

Anomaly Bursts: It is not uncommon to observe bursts of anomalies in production data. In such a scenario, the accuracy of a technique is driven by how soon the technique adapts adapts to the new “normal”. If a burst is long enough, then most techniques do adapt but with different lag. CFAR techniques such as t-digest and GESD fair quite poorly against anomaly bursts. For instance, in the health data set, the anomalies happen in bursts and a CFAR system puts an upper bound on the number of anomalies, thereby missing many of them. Having said that, this can also be advantageous as exemplified by the nab-ctr data set wherein there are a few spaced out anomalies. Table 6 shows that t-digest improves both precision and recall. Figure 7 illustrates an operations time series that highlights why t-digest does not surface anomaly bursts.

Figure 8. HOTSAX similar anomalies -

❐

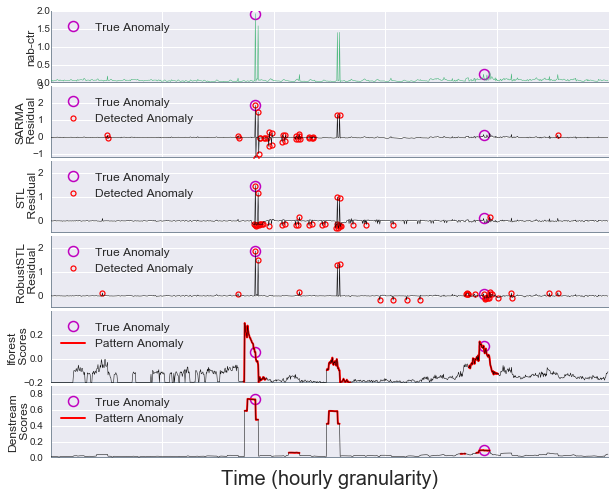

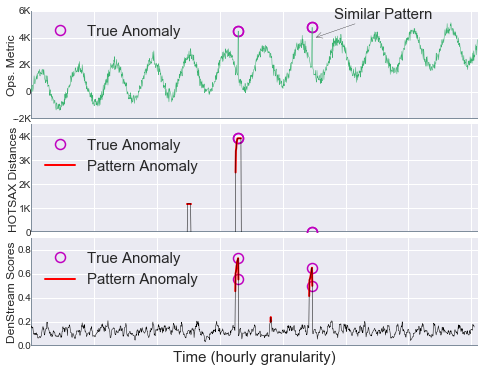

Unique Pattern Anomalies: The performance of HOTSAX and RRA is abysmal on the yahoo-a2 and yahoo-a3 data sets. This is because these synthetic data sets comprise of many similar anomalies. Both HOTSAX and RRA are not robust to the presence of such similar anomalies as the anomaly score is based on the nearest neighbor distance. Figure 8 highlights how similar anomalies may be missed. In contrast, DenStream and DBStream are able to detect self-similar anomalies as they create micro-clusters of similar anomalies.

Figure 9. Anomaly Score Separation -

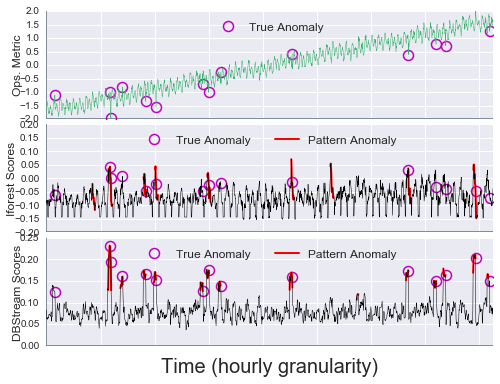

❐

Scale of distance measure: Accuracy of an anomaly detection technique is a function of the distance measure used to differentiate normal vs. anomalous data points. For instance, let us consider IForest and DBStream (refer to Figure 9). The latter creates much better separation between normal and anomalous data points. This can be ascribed to anomaly score in IForest being the depth of the leaf in which the point resides, which is analogous to the log of the distance.

5.4. Model Selection

As mentioned earlier, the analysis presented in this paper should serve as a guide for selection of the “best” anomaly detection technique. In general, model selection is a function of the application domain and latency requirement. Table 7 enlists the various application domains, the attributes exhibited by the datasets in these domains and the “best” algorithms for a given latency requirement (according to the accuracy-speed trade-offs discussed in the previous section).

| Application Domain | DataSets | Attributes | < msec | - msec | > msec |

| Hourly Operations | yahoo-a1, yahoo-a2, yahoo-a3 | LS, VC, SLC, Noisy | STL-SDAR/ STL-RobustKF | DenStream | DenStream |

| Advertising | nab-ctr | No Anomaly Bursts | t-digest | DBStream | IForest |

| Hourly IoT | nab-twt, nab-iot | Unique Anomalies | med-mad | DBStream | HOTSAX |

| Financial | fin | LS, VC | SDAR | DenStream | ClusTree |

| Healthcare | health | SJ, LS | – | DBStream | DBStream/ HOTSAX |

| Minutely Operations | ops | LS, VC, SLS, SLD, Large SP | med-mad | DBStream | DBStream |

For applications with latency requirement ¡ msec, the use of pattern and machine learning based anomaly detection techniques is impractical owing to their high computation requirements. Although techniques geared towards detecting point anomalies can be employed, the “best” technique is highly dependent on the attributes. For instance, STL-SDAR accurately detects anomalies for operations time series that exhibit non-stationarities such as , . On the other hand, in the case of minutely operations time series which typically tend to exhibit long Seasonal Periods (SP), STL becomes expensive, and hence a simpler technique such as med-mad can potentially be used to meet the latency requirement. One can use SDAR for financial time series even if the latency requirements are strict. This stems from the fact that these series (mostly) do not exhibit seasonality, and hence STL is not a bottleneck.

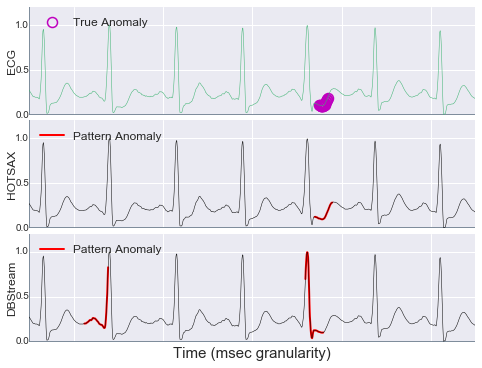

When latency requirement is in the range of - msec, micro-clustering techniques like DBStream and DenStream outperform all others. Although DBStream marginally outperforms DenStream, in the presence of noisy time series DenStream is more effective. It has been shown in prior work (Keogh et al., 2005; Senin et al., 2015) that techniques such as HOTSAX are effective in finding anomalies in ECG data in an offline setting. From Figure 6 we note that the detection runtime is over msec, which is significantly larger than the TG for ECG series. DBStream on the other hand is much faster (-msec) and can detect the same set of anomalies as HOTSAX, refer to Figure 10. Having said that, DBStream does surface more false positives than HOTSAX. A post processing step can help reduce the false positive rate. It should be noted that none of the aforementioned techniques satisfy the ¡ msec latency requirement for the health time series.

Finally, when the latency requirements are ¿msec, a wide range of anomaly techniques can be leveraged. In many cases, DBStream is still the most accurate technique. When an application has very few unique anomalies, HOTSAX usually is the most effective, as is the case with the datasets nab-twt and nab-iot.

6. Conclusion

In this paper, we first presented a classification of over 20 anomaly detection techniques across seven dimensions (refer to Table 1). Next, as a first, using over 25 real-world data sets and real hardware, we presented a detailed evaluation of these techniques with respect to their real-timeliness and performance – as measured by precision, recall and score. We also presented a map of their accuracy-runtime trade-off. Our experiments demonstrate that the state-of-the-art anomaly detection techniques are applicable for data streams with msec or higher granularity, highlighting the need for faster algorithms to support the use cases mentioned earlier in Section 1. Last but not least, given an application domain and latency requirement, based on empirical evaluation, we made recommendations for the “best” technique for anomaly detection.

As future work, we plan to extend our evaluation to other data sets such as live data streams as exemplified by Facebook Live, Twitter Periscope video applications and other live data streams on platforms such as Satori.

References

- (1)

- SPE (2006) 2006. SPEC: Standard Performance Evaluation Corporation. (2006). http://www.spec.org/.

- Lat (2010) 2010. Low Latency 101. (2010). http://www.informatix-sol.com/docs/LowLatency101.pdf.

- AD_(2017) 2017. Anomaly detection in real-time data streams using Heron. (2017). https://www.slideshare.net/arunkejariwal/anomaly-detection-in-realtime-data-streams-using-heron.

- qua (2017) 2017. QuantQuote. (2017). https://quantquote.com/.

- Sat (2017) 2017. Satori: Transforming the world with live data. (2017). https://www.satori.com.

- Agamennoni et al. (2011) G. Agamennoni, J. I. Nieto, and E. M. Nebot. 2011. An outlier-robust Kalman filter. In 2011 IEEE International Conference on Robotics and Automation. 1551–1558.

- Aggarwal (2013) Charu C. Aggarwal. 2013. Outlier analysis. Springer.

- Aggarwal et al. (2003) C. C. Aggarwal, T. J. Watson, R. Ctr, J. Han, J. Wang, and P. S. Yu. 2003. A framework for clustering evolving data streams. (2003).

- Akaike (1969) H. Akaike. 1969. Fitting autoregressive models for prediction. Annals of the Inst. of Stat. Math. 21 (1969), 243–247.

- Akaike (1986) H. Akaike. 1986. Use of Statistical Models for Time Series Analysis. In Proceedings of the International Conference on Acoustics, Speech, and Signal Processing. 3147–3155.

- Al-Aweel IC (1999) Krishnamurthy KB Al-Aweel IC. 1999. Post-Ictal Heart Rate Oscillations in Partial Epilepsy. Neurology 53, 7 (October 1999), 1590–1592.

- Amer et al. (2013) Mennatallah Amer, Markus Goldstein, and Slim Abdennadher. 2013. Enhancing One-class Support Vector Machines for Unsupervised Anomaly Detection. In Proceedings of the ACM SIGKDD Workshop on Outlier Detection and Description. ACM, New York, NY, USA, 8–15.

- Amoualian et al. (2016) Hesam Amoualian, Marianne Clausel, Eric Gaussier, and Massih-Reza Amini. 2016. Streaming-LDA: A Copula-based Approach to Modeling Topic Dependencies in Document Streams. In Proceedings of the 22Nd ACM SIGKDD International Conference on Knowledge Discovery and Data Mining (KDD ’16). ACM, New York, NY, USA, 695–704. https://doi.org/10.1145/2939672.2939781

- Barnett and Lewis (1994) Vic Barnett and Toby Lewis. 1994. Outliers in statistical data. Vol. 3. Wiley New York.

- Beckel et al. (2014) Christian Beckel, Wilhelm Kleiminger, Romano Cicchetti, Thorsten Staake, and Silvia Santini. 2014. The ECO Data Set and the Performance of Non-intrusive Load Monitoring Algorithms. In Proceedings of the 1st ACM Conference on Embedded Systems for Energy-Efficient Buildings. 80–89.

- Bera et al. (2016) A. Bera, S. Kim, and D. Manocha. 2016. Realtime Anomaly Detection Using Trajectory-Level Crowd Behavior Learning. In 2016 IEEE Conference on Computer Vision and Pattern Recognition Workshops (CVPRW). 1289–1296.

- Bhuyan et al. (2012) Monowar Hussain Bhuyan, D. K. Bhattacharyya, and Jugal K. Kalita. 2012. Survey on incremental approaches for network anomaly detection. arXiv preprint arXiv:1211.4493 (2012).

- Box and Jenkins (1990) George Edward Pelham Box and Gwilym Jenkins. 1990. Time Series Analysis, Forecasting and Control. HoldenDay, Incorporated.

- Brys et al. (2003) G. Brys, M. Hubert, and A. Struyf. 2003. A Comparison of Some New Measures of Skewness. Physica-Verlag HD, Heidelberg, 98–113.

- Bu et al. ([n. d.]) Yingyi Bu, Tat-Wing Leung, Ada Wai-Chee Fu, Eamonn Keogh, Jian Pei, and Sam Meshkin. [n. d.]. WAT: Finding Top-K Discords in Time Series Database. 449–454. arXiv:http://epubs.siam.org/doi/pdf/10.1137/1.9781611972771.43 http://epubs.siam.org/doi/abs/10.1137/1.9781611972771.43

- Candès et al. (2011) Emmanuel J. Candès, Xiaodong Li, Yi Ma, and John Wright. 2011. Robust Principal Component Analysis? J. ACM 58, 3, Article 11 (June 2011), 11:1–11:37 pages.

- Cao et al. ([n. d.]) Feng Cao, Martin Estert, Weining Qian, and Aoying Zhou. [n. d.]. Density-Based Clustering over an Evolving Data Stream with Noise. 328–339. https://doi.org/10.1137/1.9781611972764.29 arXiv:http://epubs.siam.org/doi/pdf/10.1137/1.9781611972764.29

- Chakhchoukh et al. (2009) Y. Chakhchoukh, P. Panciatici, and P. Bondon. 2009. Robust estimation of SARIMA models: Application to short-term load forecasting. In 2009 IEEE/SP 15th Workshop on Statistical Signal Processing. 77–80.

- Chandola et al. (2009) Varun Chandola, Arindam Banerjee, and Vipin Kumar. 2009. Anomaly detection: A survey. ACM Computing Surveys (CSUR) 41, 3 (2009), 15.

- Chen (2012) S. Y. Chen. 2012. Kalman Filter for Robot Vision: A Survey. IEEE Transactions on Industrial Electronics 59, 11 (Nov 2012), 4409–4420.

- Chin et al. (2005) Shin C. Chin, Asok Ray, and Venkatesh Rajagopalan. 2005. Symbolic time series analysis for anomaly detection: a comparative evaluation. Signal Processing 85, 9 (2005), 1859–1868.

- Cisco (2016) Cisco. 2016. Cisco Visual Networking Index: Global Mobile Data Traffic Forecast Update, 2016-2021. (Feb. 2016). http://www.cisco.com/c/en/us/solutions/collateral/service-provider/visual-networking-index-vni/mobile-white-paper-c11-520862.html#MeasuringMobileIoT.

- Cleveland et al. (1990) Robert B. Cleveland, William S. Cleveland, Jean E. McRae, and Irma Terpenning. 1990. STL: A Seasonal-Trend Decomposition Procedure Based on Loess (with Discussion). Journal of Official Statistics 6 (1990), 3–73.

- Cleveland (1979) William S. Cleveland. 1979. Robust Locally Weighted Regression and Smoothing Scatterplots. J. Amer. Statist. Assoc. 74, 368 (1979), 829–836.

- Cohen and Strauss (2006) Edith Cohen and Martin J. Strauss. 2006. Maintaining Time-decaying Stream Aggregates. J. Algorithms 59, 1 (April 2006), 19–36.

- de Lacalle (2016) Javier Lopez de Lacalle. 2016. tsoutliers: Detection of Outliers in Time Series. R package version 0.6-5.

- Dunning and Ertl (2015) T. Dunning and O. Ertl. 2015. Computing Extremely Accurate Quantiles using t-Digests. (2015). https://github.com/tdunning/t-digest/.

- Durbin and Koopman (2001) J. Durbin and S.J. Koopman. 2001. Time Series Analysis by State Space Methods. Clarendon Press.

- Ester et al. (1998) Martin Ester, Hans-Peter Kriegel, Jörg Sander, Michael Wimmer, and Xiaowei Xu. 1998. Incremental Clustering for Mining in a Data Warehousing Environment. In Proceedings of the 24rd International Conference on Very Large Data Bases (VLDB ’98). Morgan Kaufmann Publishers Inc., San Francisco, CA, USA, 323–333. http://dl.acm.org/citation.cfm?id=645924.671201

- Feizollah et al. (2014) A. Feizollah, N. B. Anuar, R. Salleh, and F. Amalina. 2014. Comparative study of k-means and mini batch k-means clustering algorithms in android malware detection using network traffic analysis. In 2014 International Symposium on Biometrics and Security Technologies (ISBAST). 193–197. https://doi.org/10.1109/ISBAST.2014.7013120

- Forman and Scholz (2010) George Forman and Martin Scholz. 2010. Apples-to-apples in Cross-validation Studies: Pitfalls in Classifier Performance Measurement. SIGKDD Explor. Newsl. 12, 1 (Nov. 2010), 49–57.

- Fox (1972) Anthony J. Fox. 1972. Outliers in time series. Journal of the Royal Statistical Society. Series B (Methodological) (1972), 350–363.

- Fu et al. (2006) Ada Wai-chee Fu, Oscar Tat-Wing Leung, Eamonn Keogh, and Jessica Lin. 2006. Finding Time Series Discords Based on Haar Transform. In Proceedings of the Second International Conference on Advanced Data Mining and Applications. Springer-Verlag, Berlin, Heidelberg, 31–41.

- G. Grmanova (2016) P. Laurinec G. Grmanova. 2016. Incremental Ensemble Learning for Electricity Load Forecasting. Acta Polytechnica Hungarica 13, 2 (2016).

- Gogoi et al. (2011) Prasanta Gogoi, D. K. Bhattacharyya, Bhogeswar Borah, and Jugal K. Kalita. 2011. A survey of outlier detection methods in network anomaly identification. Comput. J. 54, 4 (2011), 570–588.

- Goldberger et al. (e 13) A. L. Goldberger, L. A. N. Amaral, L. Glass, J. M. Hausdorff, P. Ch. Ivanov, R. G. Mark, J. E. Mietus, G. B. Moody, C.-K. Peng, and H. E. Stanley. 2000 (June 13). PhysioBank, PhysioToolkit, and PhysioNet: Components of a New Research Resource for Complex Physiologic Signals. Circulation 101, 23 (2000 (June 13)), e215–e220.

- Grubbs (1950) Frank E. Grubbs. 1950. Sample Criteria for Testing Outlying Observations. The Annals of Mathematical Statistics 21, 1 (1950), 27–58.

- Grubbs (1969) Frank E. Grubbs. 1969. Procedures for detecting outlying observations in samples. Technometrics 11, 1 (1969), 1–21.

- Guha et al. (2016) Sudipto Guha, Nina Mishra, Gourav Roy, and Okke Schrijvers. 2016. Robust Random Cut Forest Based Anomaly Detection on Streams. In Proceedings of the 33rd International Conference on International Conference on Machine Learning - Volume 48. JMLR.org, 2712–2721.

- Gupta et al. (2014) M. Gupta, J. Gao, C. C. Aggarwal, and J. Han. 2014. Outlier Detection for Temporal Data: A Survey. IEEE Transactions on Knowledge and Data Engineering 26, 9 (Sept 2014), 2250–2267.

- Hafen (2016) Ryan Hafen. 2016. stlplus: Enhanced Seasonal Decomposition of Time Series by Loess. https://CRAN.R-project.org/package=stlplus R package version 0.5.1.

- Hahsler and Bolanos (2016) M. Hahsler and M. Bolanos. 2016. Clustering Data Streams Based on Shared Density between Micro-Clusters. IEEE Transactions on Knowledge and Data Engineering 28, 6 (June 2016), 1449–1461. https://doi.org/10.1109/TKDE.2016.2522412

- Hawkins (1980) Douglas M. Hawkins. 1980. Identification of outliers. Vol. 11. Chapman and Hall London.

- Healey and Picard (2005a) J. A. Healey and R. W. Picard. 2005a. Detecting stress during real-world driving tasks using physiological sensors. IEEE Transactions on Intelligent Transportation Systems 6, 2 (June 2005), 156–166.

- Healey and Picard (2005b) J. A. Healey and R. W. Picard. 2005b. Detecting stress during real-world driving tasks using physiological sensors. IEEE Transactions on Intelligent Transportation Systems 6, 2 (June 2005), 156–166.

- Holt (2004) Charles C. Holt. 2004. Forecasting seasonals and trends by exponentially weighted moving averages. International Journal of Forecasting 20, 1 (2004), 5–10.

- Hotelling (1933a) H. Hotelling. 1933a. Analysis of a Complex of Statistical Variables Into Principal Components. Journal of Educational Psychology 24, 6 (1933), 417–441.

- Hotelling (1933b) H. Hotelling. 1933b. Analysis of a Complex of Statistical Variables Into Principal Components. Journal of Educational Psychology 24, 7 (Oct. 1933), 498–520.

- Huber (1964) Peter J. Huber. 1964. Robust Estimation of a Location Parameter. The Annals of Mathematical Statistics 35, 1 (1964), 73–101.

- Hubert and Vandervieren (2008) M. Hubert and E. Vandervieren. 2008. An adjusted boxplot for skewed distributions. Computational Statistics and Data Analysis 52, 12 (2008), 5186 – 5201.

- Hyndman and Athanasopoulos (2014) R.J. Hyndman and G. Athanasopoulos. 2014. Forecasting: principles and practice:. OTexts.

- Hyndman (2016) Rob J Hyndman. 2016. forecast: Forecasting functions for time series and linear models. http://github.com/robjhyndman/forecast R package version 7.3.

- Jensen et al. (2006) Willis A. Jensen, L. Allison Jones-Farmer, Charles W. Champ, and William H. Woodall. 2006. Effects of parameter estimation on control chart properties: a literature review. Journal of Quality Technology 38, 4 (2006), 349–364.

- Jolliffe (1986) I. T. Jolliffe. 1986. Principal Component Analysis. Springer-Verlag.

- Kaiser and Maravall (2001) Regina Kaiser and Agustín Maravall. 2001. Seasonal outliers in time series. Estadistica 53, 160-161 (2001), 97–142.

- Kalman (1960) Rudolph Emil Kalman. 1960. A New Approach to Linear Filtering and Prediction Problems. Transactions of the ASME-Journal of Basic Engineering 82, Series D (1960), 35–45.

- Kejariwal and Orsini (2016) A. Kejariwal and F. Orsini. 2016. On the Definition of Real-Time: Applications and Systems. In 2016 IEEE Trustcom/BigDataSE/ISPA. 2213–2220.

- Keogh et al. (2005) Eamonn Keogh, Jessica Lin, and Ada Fu. 2005. HOTSAX: Efficiently Finding the Most Unusual Time Series Subsequence. In Proceedings of the Fifth IEEE International Conference on Data Mining. 226–233.

- Kranen et al. (2011) P. Kranen, I. Assent, C. Baldauf, and T. Seidl. 2011. The ClusTree: indexing micro-clusters for anytime stream mining. Knowl Inf Syst 29 (2011).

- Laguna et al. (1997) P. Laguna, R. G. Mark, A. Goldberg, and G. B. Moody. 1997. A database for evaluation of algorithms for measurement of QT and other waveform intervals in the ECG. In Computers in Cardiology 1997. 673–676.

- Laptev et al. (2015) Nikolay Laptev, Saeed Amizadeh, and Ian Flint. 2015. Generic and Scalable Framework for Automated Time-series Anomaly Detection. In Proceedings of the 21th ACM SIGKDD International Conference on Knowledge Discovery and Data Mining. Sydney, NSW, Australia, 1939–1947.

- Lavin and Ahmad (2015) A. Lavin and S. Ahmad. 2015. Evaluating Real-Time Anomaly Detection Algorithms – The Numenta Anomaly Benchmark. In 2015 IEEE 14th International Conference on Machine Learning and Applications (ICMLA). 38–44.

- Lawhern et al. (2007) Vernon Lawhern, Scott Kerick, and Kay A. Robbins. 2007. Minimum Sample Size Requirements For Seasonal Forecasting Models. Foresight: the International Journal of Applied Forecasting (2007).

- Lawhern et al. (2013) Vernon Lawhern, Scott Kerick, and Kay A. Robbins. 2013. Detecting alpha spindle events in EEG time series using adaptive autoregressive models. BMC Neuroscience 14, 1 (2013), 101.

- Leys et al. (2013) Christophe Leys, Christophe Ley, Olivier Klein, Philippe Bernard, and Laurent Licata. 2013. Detecting outliers: Do not use standard deviation around the mean, use absolute deviation around the median. Journal of Experimental Social Psychology (2013).

- Liu et al. (2012) Fei Tony Liu, Kai Ming Ting, and Zhi-Hua Zhou. 2012. Isolation-Based Anomaly Detection. ACM Trans. Knowl. Discov. Data 6, 1, Article 3 (March 2012), 3:1–3:39 pages.

- Livera et al. (2011) Alysha M. De Livera, Rob J. Hyndman, and Ralph D. Snyder. 2011. Forecasting Time Series With Complex Seasonal Patterns Using Exponential Smoothing. J. Amer. Statist. Assoc. 106, 496 (2011), 1513–1527.

- Lowry and Montgomery (1995) Cynthia A. Lowry and Douglas C. Montgomery. 1995. A review of multivariate control charts. IIE transactions 27, 6 (1995), 800–810.

- Lucas and Saccucci (1990) James M. Lucas and Michael S. Saccucci. 1990. Exponentially weighted moving average control schemes: properties and enhancements. Technometrics 32, 1 (1990), 1–12.

- Maechler et al. (2016) Martin Maechler, Peter Rousseeuw, Christophe Croux, Valentin Todorov, Andreas Ruckstuhl, Matias Salibian-Barrera, Tobias Verbeke, Manuel Koller, Eduardo L. T. Conceicao, and Maria Anna di Palma. 2016. robustbase: Basic Robust Statistics. R package version 0.92-7.

- Melillo et al. (2015) Paolo Melillo, Raffaele Izzo, Ada Orrico, Paolo Scala, Marcella Attanasio, Marco Mirra, Nicola De Luca, and Leandro Pecchia. 2015. Automatic Prediction of Cardiovascular and Cerebrovascular Events Using Heart Rate Variability Analysis. PLOS ONE 10, 3 (03 2015), 1–14.

- Mueen et al. (2009) Abdullah Mueen, Eamonn J. Keogh, Qiang Zhu, Sydney Cash, and M. Brandon Westover. 2009. Exact Discovery of Time Series Motifs.. In SDM. SIAM, 473–484.

- Muirhead (1986) Colin R. Muirhead. 1986. Distinguishing outlier types in time series. Journal of the Royal Statistical Society. Series B (Methodological) (1986), 39–47.