Risk assessment using suprema data††thanks: This work was supported by the LABEX MILYON (ANR-10-LABX-0070) of Universit de Lyon, within the program "Investissements d’Avenir"(ANR-11-IDEX-0007) opera operated by the French National Research Agency (ANR).

Abstract

This paper proposes a stochastic approach to model temperature dynamic and study related risk measures. The dynamic of temperatures can be modelled by a mean-reverting process such as an Ornstein-Uhlenbeck one. In this study, we estimate the parameters of this process thanks to daily observed suprema of temperatures, which are the only data gathered by some weather stations. The expression

of the cumulative distribution function of the supremum is obtained thanks to the law of the hitting time. The parameters are estimated by a least square method quantiles based on this function. Theoretical results, including mixing property and consistency of model parameters estimation, are provided. The parameters estimation is assessed on simulated data and performed on real ones. Numerical illustrations are given for both data. This estimation will allow us to estimate risk measures, such as the probability of heat wave and the mean duration of an heat wave.

Keywords. Ornstein-Uhlenbeck process, supremum law, parameters estimation, heat wave risk assessment.

1 Introduction

Forecasting and assessing the risk of heat waves is a crucial public policy stake. It requires measure tools in order to evaluate the probability of heat waves and their severity. For example, the paper [SÖK+10] is interested in assessing the likelihood of occurrence of the heat wave of 2003. For that purpose, they model annual maximum temperatures thanks to mean monthly data. However, the

available information depends on meteorological stations. Daily extremes (maximum and / or minimum) might be the only available data. Since temperature does not deviate from its mean level, a mean-reverting process such as an Ornstein-Uhlenbeck (OU) process is commonly used to model temperature process (see [Dis98a], [Dis98b] for example). The authors of [DQ00] and [ADS02] propose to use an ARMA version of the OU process while [BSZ02] propose a fractional Brownian motion (to take into account the long range dependence) instead of the classical Brownian motion in the OU process. In [CIM06], the OU process is the basic model used to model the local temperature (of air, of ocean water).

The main purpose of this paper is to estimate the parameters of this OU process. Estimation of OU parameters has been done using observations of the process (see [Fra03]) or more recently using hitting time data in [MI08] for the neuronal activity. However, weather stations do not record either of these data. That’s why we propose an estimation based on daily observed suprema of temperatures. Once the parameter estimation is done,

risk measures related to heat waves may be obtained from Monte Carlo simulations of the dynamic of temperatures with the estimated parameters. For example, we would like to estimate the

probability of heat waves, namely the probability for outdoor air temperature to exceed a threshold (26.67∘C during 3 days, see [Gri68]) or two thresholds (one

during night and one during day, see [LPL+04]). Other interesting measures would be the corresponding expected area over the threshold or the mean time over the threshold.

Recently, lots of results on the first passage time

of the process have been obtained. In [APP05], different expressions for the density function of the first hitting time to a fixed level by an OU process are given. Since hitting time and suprema are related, the cumulative distribution function (cdf) of the supremum is obtained.

Unlike classical quantile estimation (such as done in [CHBS05] or [Pek14]), we do not use the cdf inverse and propose though a new approach to estimate the parameters. Thanks

to the cdf, we perform a least square method to estimate the OU parameters.

The paper is organized as follows. In the next section, the estimation problem is presented. Section 3 is concerned with the theoretical tools. Finally, Section 4 is devoted to the numerical illustrations of the estimation and the related risk measures thanks to the only available data : the daily suprema of temperatures.

2 Estimation Problem

Since temperature does not deviate from its mean level, a mean-reverting process such as an OU process is commonly used to model temperature process (see [Dis98a], [Dis98b] for example). Here, we use a stationary OU process. The temperature variations process is given by :

where , and is a standard Brownian motion. Suppose that and are independent. We recall that the measure is the stationary measure. This modelling is reasonable, as, in the applications, we consider observations only from a sub-period of annual observations (e.g. from summer). Let us note . We say that is a stationary OU with parameter .

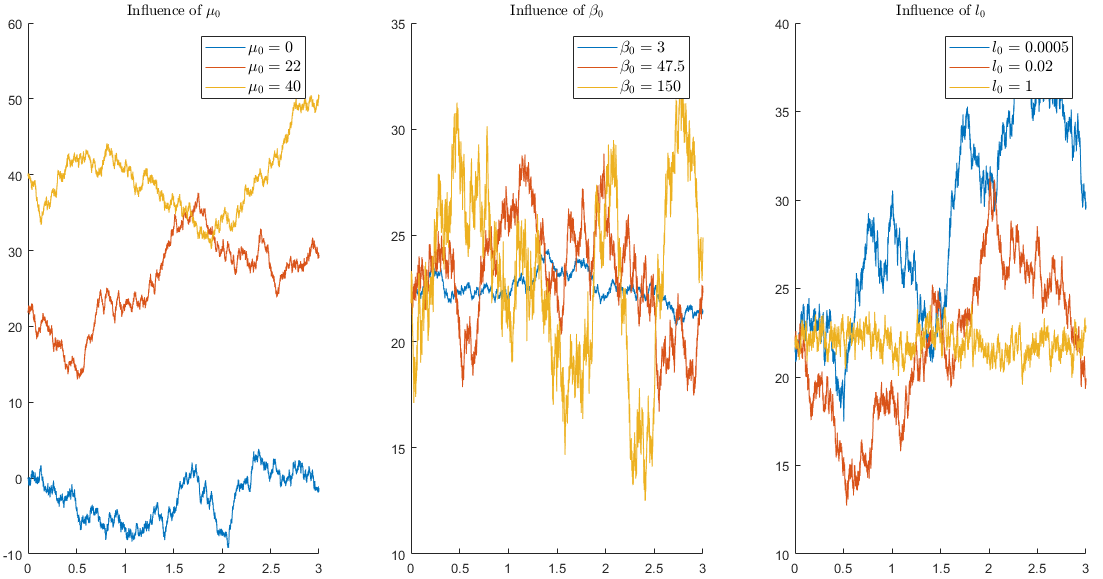

The parameter is the mean of the stationary process. The parameter is the volatility of the process. It indicates the degree of variation. For the temperature, it reveals a tendency to change quickly and unpredictably. If , the process is purely deterministic and well-known then. Finally, the parameter shows the "speed" of mean-reversion. The parameter is sometimes called the relaxation parameter. If , the process is just a Brownian motion, standard if . The influence of these parameters is shown on Figure 5 in Appendix 6.

Let us note for , and .

Assume that we observe the suprema on a period with a partition of constant step . We then have suprema for on disjoint intervals. Let us remark here that in our problem of daily observations we will take .

Classical estimation methods are not well suited for the parameter estimation from the supremum observations. Indeed, the likelihood maximization requires the probability density function of the supremum and in order to use quantile methods, one needs to know the supremum’s cdf inverse. These two functions can only be obtained by numerical approximations that are more time consuming than numerical methods to get the cdf itself.

This is why we propose to use the cdf of the supremum, denoted , whose expression is given in Proposition 3.1.

Let and , be real numbers. Let us denote the empirical distribution function on the sample , . We recall that, for .

A way to estimate is to use a least square method by minimizing the sum of squares of the differences between theoretical and empirical cdf. Then, we want to minimize the following function :

where is the parameter of the OU process, and are real numbers (to be chosen later).

Thus, is estimated by

| (1) |

Remark 2.1.

The problem is stated here with suprema but the same reasoning may be applied to the infima (or both infima and suprema) to deduce the estimation.

3 Theoretical Tools

In this section, we present some useful results to estimate the parameters.

3.1 Cdf of the supremum

To minimize the function , we need to compute the cdf of the supremum. As the cdf of the supremum is directly linked with the one of the hitting time, we can find thanks to [APP05].

Proposition 3.1.

For and , the cdf of the supremum of the stationary OU process with parameter is given by

where is a 3-dimensional Bessel bridge over the interval between 0 and and is the cdf of the standard normal distribution.

We first need the following lemma.

Lemma 3.2.

For , and , the cdf of the conditional supremum of the OU process with parameter starting at is given by

where is a 3-dimensional Bessel bridge over the interval between 0 and .

For , .

Using the hitting time density for an OU process (see [APP05]), we can deduce this result on the conditional cdf.

Proof.

Let be given and fixed.

Let set and (which is thus a standard Brownian motion). Then the dynamic of is

For , we introduce the first passage time .

Since , we have :

We conclude using the density of given (in [APP05]) by :

where is a 3-dimensional Bessel bridge over the interval between 0 and . Then, we have

with a 3-dimensional Bessel bridge over the interval between 0 and . ∎

Remark 3.3.

Similarly, we can obtain the cdf of the conditional infimum of . For , , and , we have

with a 3-dimensional Bessel bridge over the interval between 0 and .

For , .

Proof of Proposition 3.1.

Integrating with respect to the law of , we can express the cdf of the supremum of the OU process with parameter .

∎

Remark 3.4.

Note that the cdf is decreasing with respect to . Numerically, the cdf seems to be decreasing with respect to and .

3.2 Mixing property

In order to get statistical properties of estimators, some mixing properties are usually required. Indeed, statistics beyond independence have received a deep attention from the 90’s. Mixing is used instead of independence and results such as Laws of Large Numbers or Central Limit Theorems may still hold. There is a very large literature on that subject and we refer to [Bil65, Dou94, Rio93] and the references therein for definitions and main results.

Roughly speaking, mixing properties of a process quantify the convergence to as goes to infinity of

for and in an appropriate class of measurable functions and . The following proposition means that is exponentially -mixing.

Proposition 3.5 (Mixing property).

Let us consider an OU with parameter . For any , for any function , such that , are square-integrable with respect to the law of , and for any , we have

3.3 Consistency of the estimation

Following the idea of the proof of Theorem II.5.1 in [ABC92], we may prove the consistency of our estimation of the parameter provided that the , are chosen such that the function

is injective and that the parameter belong to a compact subset of .

Proposition 3.6.

Consider an OU process with parameters . Assume that the parameters belong to a compact subset of . For any , let be given by (1). Then, any a.s. limit point of satisfies .

Proof.

We adapt the lines of the proof of Theorem II.5.1 in [ABC92] and use the ergodic theorem for mixing sequences (see [Bil65] e.g.).

We denote

Since is a compact set, the sequence has limit points. Let be any limit point of . Since no confusion can be made, and in order to simplify notations, we use instead of for this proof. For , let we write

| (2) |

The ergodic theorem for mixing sequences implies that goes to a.e. as goes to infinity for . Now,

Let be a subsequence such that goes to , using (2), we have

and a.e. We deduce that

which gives the announced result. ∎

Remark 3.7.

Of course, if the application is injective, then Proposition 3.6 implies that and thus goes to a.s. as goes to infinity. From some numerical tests, it seems that the injectivity is satisfied.

4 Numerical Applications

In this section, we want to estimate the parameters, first on some simulated data, and then on real ones. First of all, we need to implement the cdf of the supremum of the OU process with 3 parameters.

We want to make an estimation on real data with daily suprema observations. This is why without any precision, will be equal to for numerical applications in the rest of the paper.

4.1 Cdf Numerical Computation

We describe here the used method for the numerical computation. Contrary to what is written in [APP05], the process is the unique solution of the following SDE ([DB08])

Since the process starts from 0 here, the Euler scheme cannot be applied for this SDE. Recall that the process with and and the process defined by with and have same distributions (Exercise XI.3.7 of [RY13]). Therehence, we can use the Euler scheme on the switched Bessel bridge which verifies the SDE ([RY13])

Finally, the integrals are computed by considering the corresponding Riemann sum and the expectation by a Monte-Carlo method with simulations.

The code is written in C++ and the evaluation of the function is very long. Consequently, we had to make a parallel code. Yet, the function "rand" in C++ is not thread safe. Thus, we propose to use the Mersenne Twister generator for the simulation of the random numbers. With the parallelisation, the time for one evaluation of the function to be minimized has been divided approximately by 5 but is still long (around 52 secs for , , with a 40 cores machine). The duration is not a problem since the optimisation needs to be done once and for all.

4.2 Bounding parameters

The problem (1) is solved by an algorithm which performs a Nelder-Mead method. More precisely, we use optim procedure on the software R. Initial values for the parameters to be optimized over are required. To set those initial values, we propose to bound each parameter. For each of them, we give here a lower and an upper bound.

As well as we observe the maxima, suppose we also have the minima : (still for a partition of of constant step ). Then, the available quantities for bounding the parameters are the minima mean, denoted ; the maxima mean, denoted ; the smallest observed temperature, denoted and the largest one, denoted .

Let us recall the OU process is assumed to be stationary, then we have, for all ,

The expectation gives us natural bounds for the parameter :

Moreover, we have As for all , , one may say that it is natural to upper bound the variance by

It then gives us a lower-bound for .

For the upper-bound, we use Theorem 2.7 of [LS01]. For all , we have

Hence

It remains to find the domain of . First of all, .

Since , a classical estimator of (see [LBM84]) is .

Then,

Finally, where

4.3 Parameters estimation on simulated data

We are going to test our method on simulated data. To choose realistic parameters, we use some temperatures data. The mean temperature leads us to take . Using the difference between the maximal (respectively minimal) temperature and the mean temperature, we take . The hourly correlation allows us to set (see e.g. [Gri68] and [BSZ02]). Then, .

We made several tests to make a compromise between the algorithm complexity and the precision of the estimation (with RMSE) which lead us to take here. Then, we take the empirical quantiles on the sample for and respectively so that there are uniformly distributed on the interval . The values are settled and fixed for the whole estimation procedure.

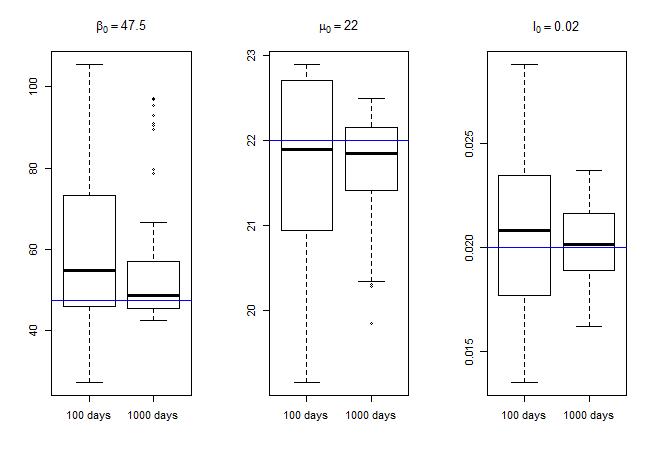

50 samples are simulated over days for each, with an Euler Scheme (time scale days), with . The algorithm is launched on R twice on those 50 samples, once with the truncated samples over 100 days and one with the whole samples. The parameters found minimizing and are presented in the following boxplots:

As we expected, the estimations are better on a larger sample. The relative RMSE for , and are respectively equal 0.4955, 0.04759 and 0.2194 for the small samples (100 days) and 0.4205, 0.03453 and 0.08928 for the larger samples (1000 days). The median parameters are satisfying. However, the parameters and seem biased. It appears that tends to be overestimated and on the contrary underestimated. Moreover, we observe a big variation in the estimators of . It is confirmed by the relative RMSE (see above). Better results are obtained if is fixed and performing a 2D-estimation, as in [MI08]. Indeed, the relatives RMSE for and are then respectively equal to 0.0107 and 0.0929. It is consistent with the results in [MBS95] where is assumed to be known.

4.4 Real data

4.4.1 Parameters estimation

In [KTa02], daily temperature dataset in Paris through the ECA&D project is provided (Data and metadata available at http://www.ecad.eu). This dataset is one of the longest in temperature measurement since it begins in 1900 but it records only maximum, minimum and mean daily temperature. In our application, we study daily summer temperature. In that way, we select maximal and minimal temperatures from 15th of june to the 14th of august ( days) each year between 1950 and 1984 included, representing years of records and days. These years are selected in order to avoid climate change influence so we can consider the dataset as maximum observations of a stationary process (see [GIE]). This is our train sample. We will keep the years after 1985 for the test sample.

When we apply the estimation procedure presented in Section 2, we find . In order to assess the quality of this estimation, we propose to compare some theoretical quantities with empirical ones. That is done in the next section.

4.4.2 Estimation validation

To verify the estimation, we propose two models validation indicators: : comparison of quantiles and prediction. The first validation indicator is just to check the quantile-quantile matching over our train sample. The second one is a validation using prediction and then does not use the train sample.

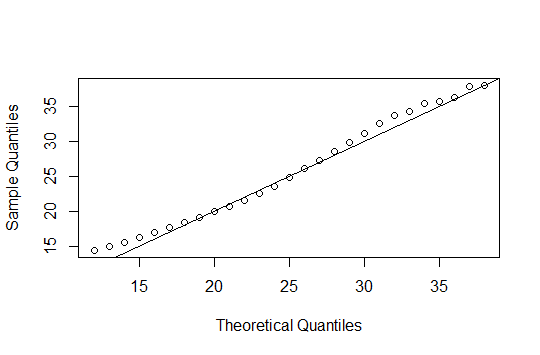

The first thing to check is the match of quantiles. To this aim, we draw a quantile-quantile plot (see Figure 2). The plotted points fall near the line which indicates that the quantiles of the theoretical and data distributions agree.

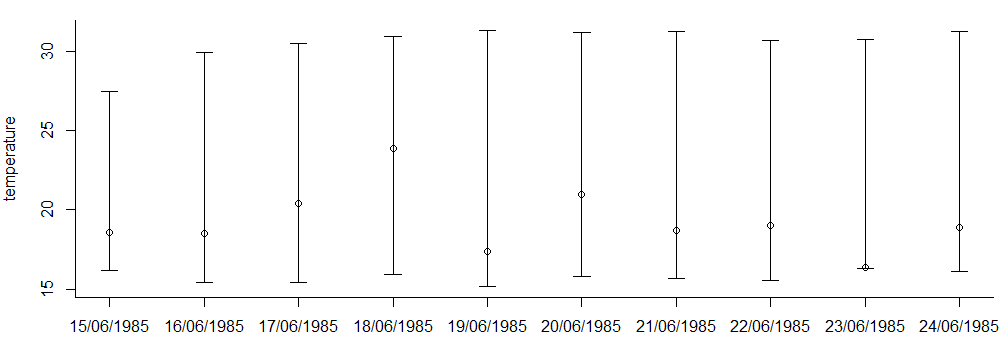

We also want to assess the estimation quality by a prediction method. The estimation ends on the 14/08/1984. We take the mean temperature of the 14/06/1985 as an initial point to simulate processes (time scale days) on 10 days with the estimated parameters. Then, we make a confidence interval by Monte Carlo simulations (1000 simulations) for the maxima over each of those days and compare it with the real values (between 15/06/1985 and 24/06/1985, in the test sample).

We observe that the real values (the dots) are all in the confidence interval which confirms the pertinence of our model. We also made this test with 30 days and the results were also very good.

4.5 Risk measures

4.5.1 Definitions

Let us recall the goal of our study. We want to estimate some risk measures related to heat waves. Let us note that one may estimate any risk measure of his choice. Indeed, once the minimisation is performed, we can use a Monte-Carlo method simulating independent processes with estimated parameters.

There is two classical definition for a heat wave. The first one (see [LPL+04]) is a sequence of consecutive days ( days) for which the maximum daily temperature is larger than a high-level threshold () and the minimum daily temperature is greater than a low level one (). Those temperatures thresholds (, ) depend on the geographical zone. The second definition (see [Gri68]) is a sequence of consecutive days ( days) for which the minimum daily temperature is greater than a level ().

As we have daily observations, to simplify the expression, we take and is then the supremum on the first day for example.

We define the two random variables

and

for .

Then, we can express the probability of heat wave (for the first definition):

Another interesting measure is the duration of an heat wave. Let us note, when there exists

and

Then, the mean duration of an heat wave is

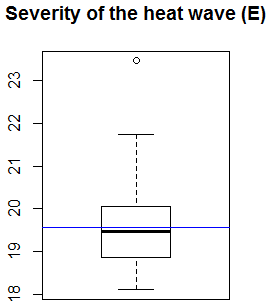

Using the second definition, we can also measure the severity of a heat wave with the area over the threshold for the first days. Let be the first moment of a heat wave. This area is :

As the process is assumed to be stationary, this quantity does not depend on .

4.5.2 Simulated data

Since our goal is to estimate risk measures, we would like to see how they are impacted by the estimation of the parameters. We propose here to look at the last one, , which uses the process itself.

4.5.3 Real data

We use the markers of M t o France for Paris (see [LPL+04]), we take , C and C. As we want to estimate the measures for a summer, we take days. Those measures are calculated with the estimated parameters on the real data, namely .

For the probability of heat wave, the Monte-Carlo method is performed with the simulation of years of days and we obtain a probability of for a summer. There were 2 heat waves between 1985 to 2011 then a proportion of . This highlights the deviation of the temperatures in the last decades, due to climate change ([GIE]).

With simulations for the Monte-Carlo, we obtain a mean duration for an heat wave of 3.2 days. The 2 heat waves had lasted respectively 3 and 10 days.

5 Conclusion and and future research directions

In this paper, a new method to estimate the parameters of an OU process is proposed. Indeed, the proposed method includes a least square estimation based on the suprema observations. To this aim, the cdf of the suprema of an OU is given and theoretical results, including consistency of model parameter estimation, are established.

The numerical applications on real and simulated data prove the goodness of the estimation and its relevance. Risk measures such as the probability of heat wave or the duration of one have been studied and compared with the reality. The proposed model is also able to predict temperatures for a few days.

Some directions for further investigations are summarized as follows. For example, in continuity with this work, obtaining explicit expressions of risk measures may be interesting in the model. To this aim, one may know the joint law of the supremum and the process. Moreover, another interesting estimation for the parameters of the process might be done using Maximum Simulated Likelihood Estimation (see [JL11]).

6 Appendix

References

- [ABC92] A. Antoniadis, J. Berruyer, and R. Carmona. Régression non linéaire et applications. Collection "Economie et statistiques avancées.": Série Ecole nationale de la statistique et de l’administration économique et Centre d’études des programmes économiques. Economica, 1992.

- [ADS02] P. Alaton, B. Djehiche, and D. Stillberger. On modelling and pricing weather derivatives. Applied Mathematics in Finance, (9):1–20, 2002.

- [APP05] L. Alili, P. Patie, and J. L. Pedersen. Representations of first hitting time density of an Ornstein-Uhlenbeck process. Stochastic Models, 21(4):967–980, 2005.

- [Bil65] P. Billingsley. Ergodic Theory and Information. Wiley series in probability and mathematical statistics. Wiley, 1965.

- [BSZ02] D. Brody, J. Syroka, and M. Zervos. Dynamical pricing of weather derivatives. Quantitative Finance, 2(3):189–198, 2002.

- [CHBS05] E. Castillo, A. Hadi, N. Balakrishnan, and J. Sarabia. Extreme Value and Related Models With Applications in Engineering and Science. 01 2005.

- [CIM06] S. Chaumont, P. Imkeller, and M. Müller. Equilibrium trading of climate and weather risk and numerical simulation in a markovian framework. Stochastic Environmental Research and Risk Assessment, 20(3):184–205, 2006.

- [DB08] A. N. Downes and K. Borovkov. First Passage Densities and Boundary Crossing Probabilities for Diffusion Processes. Methodology and Computing in Applied Probability, 10(4):621–644, 2008.

- [Dis98a] B. Dischel. At least: a model for weather risk, weather risk special report. Energy and Power Risk Management, (March):30–32, 1998.

- [Dis98b] B. Dischel. Black-Scholes won’t do it, weather risk special report. Energy and Power Risk Management, (October):8–9, 1998.

- [Dou94] P. Doukhan. Mixing. In Mixing, pages 15–23. Springer, 1994.

- [DQ00] F. Dornier and M. Queruel. Caution to the wind, Weather risk special report. Energy Power Risk Management, pages 30–32, 2000.

- [Fra03] J. C. G. Franco. Maximum likelihood estimation of mean reverting processes. Real Options Practice, 2003.

- [GIE] IPCC, 2014: Climate Change 2014: Synthesis report. Contribution of Working Groups I, II and III to the Fifth Assessment Report of the Intergovernmental Panel on Climate Change [Core Writing Team, R.K. Pachauri and L.A. Meyer (eds.)]. IPCC, Geneva, Switzerland, 151 pp.

- [GM16] E. Gobet and G. Matulewicz. Parameter estimation of Ornstein-Uhlenbeck process generating a stochastic graph. Statistical Inference for Stochastic Processes, pages 1–25, 2016.

- [Gri68] I. Gringorten. Estimating finite-time maxima and minima of a stationary Gaussian Ornstein-Uhlenbeck process by Monte Carlo simulation. Journal of the American Statistical Association, 63(324):1517–1521, 1968.

- [JL11] I. Jeliazkov and A. Lloro. Maximum Simulated Likelihood Estimation: Techniques and Applications in Economics, pages 85–100. Springer Berlin Heidelberg, Berlin, Heidelberg, 2011.

- [KTa02] A. M. G. Klein Tank and al. Daily dataset of 20th-century surface air temperature and precipitation series for the European Climate Assessment. Int. J. of Climatol., (22):1441–1453, 2002.

- [LBM84] A. Le Breton and M. Musiela. A study of a one-dimensional bilinear differential model for stochastic processes (STMA V26 2481). Probability and Mathematical Statistics, 4:91–107, 1984.

- [LPL+04] K. Laaidi, M. Pascal, M. Ledrans, A. Le Tertre, S. Medina, C. Casério, J.-C. Cohen, J. Manach, P. Beaudeau, and P. Empereur Bissonnet. Le système français d’alerte canicule et santé 2004 (sacs 2004) un dispositif intégré au plan national canicule. Bulletin épidémiologique hebdomadaire, pages 134–136, 2004.

- [LS01] W. V. Li and Q.-M. Shao. Gaussian processes: Inequalities, small ball probabilities and applications. Stochastic Processes : Theory and Methods . Handbook of Statistics, (19):533–597, 2001.

- [MBS95] B. Martin Bibby and M. Sørensen. Martingale estimation functions for discretely observed diffusion processes. Bernoulli, 1(1-2):17–39, 03 1995.

- [MI08] P. Mullowney and S. Iyengar. Parameter estimation for a leaky integrate-and-fire neuronal model from ISI data. Journal of Computational Neuroscience, 24(2):179–194, 2008.

- [Pek14] D. Pekasiewicz. Application of quantile methods to estimation of Cauchy distribution parameters. Statistics in Transition, 15(1):133–144, 2014.

- [Rio93] E. Rio. Covariance inequalities for strongly mixing processes. Annales de l’IHP, 29(4):587–597, 1993.

- [RY13] D. Revuz and M. Yor. Continuous martingales and Brownian motion, volume 293. Springer Science & Business Media, 2013.

- [SÖK+10] B. Siliverstovs, R. Ötsch, C. Kemfert, C. Jaeger, A. Haas, and H. Kremers. Climate change and modelling of extreme temperatures in switzerland. Stochastic environmental research and risk assessment, 24(2):311–326, 2010.