Optimal hybrid block bootstrap for sample quantiles under weak dependence

Abstract

We establish a general theory of optimality for block bootstrap distribution estimation for sample quantiles under a mild strong mixing assumption. In contrast to existing results, we study the block bootstrap for varying numbers of blocks. This corresponds to a hybrid between the subsampling bootstrap and the moving block bootstrap (MBB), in which the number of blocks is somewhere between 1 and the ratio of sample size to block length. Our main theorem determines the optimal choice of the number of blocks and block length to achieve the best possible convergence rate for the block bootstrap distribution estimator for sample quantiles. As part of our analysis, we also prove an important lemma which gives the convergence rate of the block bootstrap distribution estimator, with implications even for the smooth function model. We propose an intuitive procedure for empirical selection of the optimal number and length of blocks. Relevant examples are presented which illustrate the benefits of optimally choosing the number of blocks.

Keywords and phrases: Hybrid block bootstrap; subsampling; optimality; sample quantile; weak dependence; strong mixing.

1 Introduction

A broad categorization of settings for bootstrap methods might be as follows: (i) smooth functionals of independent data; (ii) nonsmooth functionals of independent data; (iii) smooth functionals of dependent data; and (iv) nonsmooth functionals of dependent data. Setting (i) is the classic setting of the bootstrap, with Hall (1992) being an authoritative reference. In setting (ii), bootstrap methods for approximating distributions of sample quantiles have been studied by Efron (1979); Bickel and Freedman (1981); Singh (1981); Babu (1986); Efron (1982); Ghosh et al. (1984); Hall and Sheather (1988); Hall et al. (1989); Hall and Martin (1991); De Angelis et al. (1993) and Falk and Janas (1992).

In setting (iii), the existing literature is concentrated on block bootstrap methods for smooth functionals with dependent data, beginning with Hall (1985), and Carlstein (1986). Subsequently, the moving block bootstrap (MBB) was proposed by Künsch (1989) and Liu and Singh (1992). Other variants and properties of block bootstrap methods were considered by Paparoditis and Politis (2001); Politis and Romano (1992, 1994) and Politis et al. (1997), to name a few. In setting (iii), various block bootstrap methods and their properties for weakly dependent sequences have been investigated by, for example, Bühlmann (1994); Naik-Nimbalkar and Rajarshi (1994); Hall et al. (1995); Götze and Künsch (1996); Lahiri (1992, 1996, 1999) and Bühlmann and Künsch (1999).

In contrast, there is a less extensive literature about block bootstrap methods in setting (iv), i.e. for nonsmooth functions of dependent data. Sun and Lahiri (2006), Sun (2007) and Sharipov and Wendler (2013) are notable exceptions. Those authors considered block bootstrap approximation for sample quantiles under weak dependence. Sun and Lahiri (2006) established strong consistency of the MBB, assuming only a polynomial (strong) mixing rate, for both distribution and variance estimation of the sample quantiles. Sharipov and Wendler (2013) established similar results for the circular block bootstrap utilizing a different set of conditions to take advantage of empirical process theory for the Bahadur-Ghosh representation of the sample quantile. Sun (2007) is particularly relevant to our work, as discussed further below. All of these earlier results assume that the number of blocks tends to infinity with the sample size.

More recently, Kuffner et al. (2017) established a more general consistency result for a hybrid block bootstrap, for both distribution and variance estimation of sample quantiles. While an exponential mixing rate is assumed, Kuffner et al. (2017) proved weak consistency for any number of blocks, (as ), whereas the existing proofs for the MBB and circular block bootstrap required that , where . Here, is the available sample size, and is the block length. The value of is the number of resampled blocks to be pasted to form the bootstrap data series. The case corresponds to the subsampling bootstrap (Politis and Romano, 1994), and the case is the standard MBB (Künsch, 1989). Therefore, the consistency results in Kuffner et al. (2017) are for a ‘hybrid’ between the MBB and the subsampling bootstrap, and those two extremes are covered by the same theory.

As noted in Kuffner et al. (2017), their theoretical and empirical results suggest that there can be substantial performance improvement, in terms of mean squared errors (MSE) for both the variance and distribution estimators, when choosing some value of , but less than . This suggests the following question: does there exist some optimal choice of the pair which provides the best convergence rate for the bootstrap distribution estimator for sample quantiles under weak dependence? We answer that question in the present paper.

Related to the motivation of the present paper is the paper by Sun (2007). She studied the convergence rate of the moving block bootstrap distribution estimator for sample quantiles with dependent data. A strong mixing condition with exponentially decaying mixing coefficients was assumed. An almost sure convergence result was established, and the best rate of convergence was found to be . We consider a weaker polynomial rate condition, which is also slightly weaker than that assumed in Sun and Lahiri (2006). Moreover, we allow the number of blocks to vary, instead of fixing . Our main theorem establishes the convergence rate of the ‘hybrid’ bootstrap distribution estimator for sample quantiles. It is a hybrid between the MBB () and subsampling () bootstrap. We also apply our theory to the setting of Sun (2007) below.

Another recent development in dependent data bootstrap methodology is the convolved subsampling bootstrap (Tewes et al., 2017). This bootstrap estimator is defined by the -fold self-convolution of a subsampling distribution. In the special case of the sample means problem, this corresponds to our hybrid bootstrap. For the sample quantile problem which is the particular focus here, convolved subsampling bootstrap essentially computes the average of within-block sample quantiles over the resampled blocks. By contrast, our estimator is the sample quantile of a single series formed by joining blocks. Further theoretical comparison of these approaches will be undertaken elsewhere.

Other indirectly-related work includes Lahiri (2005), who studied consistency of jackknife-after-bootstrap variance estimation for bootstrap quantiles, and Gregory et al. (2015), who showed that the Sun and Lahiri (2006) strong consistency results for distribution and variance estimation via the MBB also hold for the smoothed extended tapered block bootstrap (SETBB). We mention that Shao and Politis (2013) employed a fixed subsampling procedure to estimate confidence sets for statistics adhering to the smooth function model, which of course does not include sample quantiles.

Aside from our general optimality results being of foundational and practical value, they also indicate that adaptive selection of the number of blocks could yield considerable improvements in convergence rates for block bootstrap distribution estimators. Moreover, Lemma 5 below is of independent interest, as it gives the convergence rate of the block bootstrap distribution estimator, and has bearing on the regular smooth function model. We have included several relevant empirical examples to illustrate the potential gains of optimal choice of the number of blocks, as opposed to using the prescribed value of for either the subsampling bootstrap or the MBB (). In § 5, we give practical guidance as to how to choose in a given applied problem, by proposing a procedure for this purpose.

2 Problem Setting

Let be the set of all integers. Define to be a doubly-infinite sequence of random variables on the probability space . The elements of the sequence possess a common distribution function , and its corresponding quantile function , defined by

We will study the block bootstrap distribution estimator of a suitably centered and scaled sample quantile. It is assumed throughout that is a strictly stationary process. The sequence denotes a sample of size from .

2.1 The Block Bootstrap

The moving blocks bootstrap (MBB) (Künsch, 1989) splits the original sample into overlapping blocks of size , , together constituting a set . Let be a random sample drawn with replacement from the original blocks, where is the number of blocks that will be pasted together to form a pseudo-time series. For a real number , the notation is defined as the largest integer , and is the smallest integer . That is a random sample from means that the sampled blocks are independently and identically distributed according to a discrete uniform distribution on . The observations in the th resampled block, , are , for . Then the MBB sample is the concatenation of the resampled blocks, written as

Note that this way of constructing the pseudo-time series will reproduce the original dependence structure asymptotically.

The subsampling bootstrap (Politis and Romano, 1994), and specifically the overlapping blocks version relevant to the present setting, first splits the original sample into precisely the same overlapping blocks as the MBB, each of length . However, the subsampling bootstrap draws only a single block. A nice property of this procedure is that the original dependence structure in the sample is exactly retained in the single subsample. By contrast, the pseudo-time series constructed by the MBB only reproduces the original dependence structure asymptotically.

We define dependence for the sequence of random variables in terms of the mixing properties of -algebras generated by subsets of the sequence which are separated by a distance, in units of time, tending to infinity. For any two sub--algebras of , say and , the -mixing coefficient between and is defined to be (Athreya and Lahiri, 2006, Section 16.2.1)

| (1) |

Write for the smallest -algebra of subsets of with respect to which , , are measurable. Let be the smallest -algebra which contains the unions of all of the -algebras as . That is, is a sub--algebra of , and it is the -algebra generated by the random variables as . Similarly, for , let be the -algebra generated by the random variables , as . The -mixing coefficient of the sequence is defined as

where is defined in (1). If the -mixing coefficient decays to zero,

| (2) |

then the process is said to be strongly mixing. The sequence of random variables is said to be weakly dependent if the process is strongly mixing, i.e. if (2) holds.

3 Theoretical Results

Assume that is a sample of a stationary strong mixing process with mixing coefficient satisfying, for some ,

Denote by the distribution function of and the empirical distribution function of .

Define, for , and , to be independent random indices uniformly drawn from the set ,

Define, for ,

Assume that is defined on a neighbourhood of , with

Theorem 1.

Suppose that and . Let be fixed and be any arbitrarily small constant.

-

(i)

If and , then

-

(ii)

If , then

We may deduce from Theorem 1 the following:

- Case (i).

-

and .

The convergence rate of the bootstrap distribution estimator is minimised by setting

which yields, for any ,

(3) Note that as , the optimal orders of and approach , which does not depend on unknown parameters and may be taken as a practical reference for empirical choices of and . With such choices, that is , the bootstrap distribution estimator has the convergence rate , for and any . The latter convergence rate is slightly slower than that specified in (3), a price to pay for the absence of knowledge of .

On the other hand, the MBB sets , based on which the optimal is of order , so that . The convergence rate of the resulting bootstrap distribution estimator is given, for any , by

which is markedly slower than that obtained by setting .

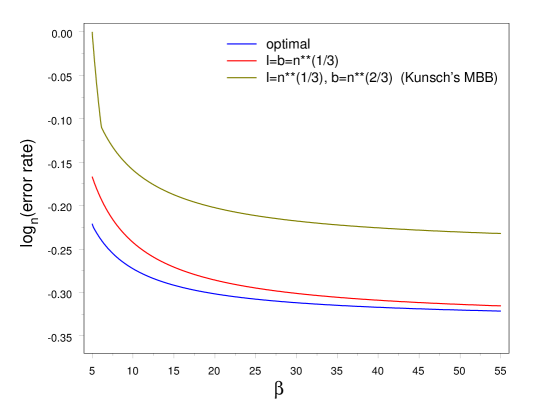

Figure 1 compares the optimal convergence rate with those based on and , respectively.

Figure 1: From Theorem 1, Case (i). Log error rates for the block bootstrap distribution estimator are plotted against for the optimal pairs of . The choice is optimal for , and it is our recommendation when no information about the exact value of is available. Thus the discrepancy between the blue and red curves shows how ignorance about affects the error rate. The MBB choice is optimal for Künsch’s MBB.

- Case (ii).

-

.

The error rate has an order minimised by setting , which yields

for any arbitrarily small . For MBB, the error rate is minimised if is chosen to have order between and , yielding an optimal convergence rate of order for any . If we set , which amounts to the subsampling method, then the fastest error rate has order , attained by setting .

Remark 1.

Case (ii) applies to any strong mixing setting where the mixing coefficients decay faster than any finite polynomial rate. Namely, this includes the exponential rate of Sun (2007), and anything faster. The case that could be replaced by an assumption that the mixing coefficient satisfies as , for some . This is the assumption in Kuffner et al. (2017), which is equivalent to the condition in Sun (2007). Under such an exponential rate condition, the results for Case (ii) would still hold. However, this would unnecessarily exclude any rate that is faster than polynomial but slower than exponential. We emphasize that Sun (2007) proved an almost sure convergence result under this exponential rate condition, using only the MBB choices of .

Remark 2.

Of independent interest is the result of Lemma 5, which gives the convergence rate of the block bootstrap distribution estimator for and has a bearing on the regular smooth function model. Consider the simpler case where . It is easily seen that the convergence rate is minimised at , attained by setting and having order not smaller than , of which MBB is a special case. The subsampling method (), however, has at best a convergence rate of only order , attained by setting .

Remark 3.

Results on distribution estimation for , embodied in Theorem 1, differ substantially from the regular case in that local estimation of over a shrinking neighbourhood of size around incurs an error of order , which favours a small and precludes MBB from yielding an optimal convergence rate.

4 Relevance to Coverage Error

Define

and let be defined by

| (4) |

Our main results in § 3 establish the asymptotic order of and derive the optimal orders of which minimise that order.

5 Practical Procedure for Selecting Optimal

Setting and , the objective is to find the optimal pair of positive constants which minimise the estimation error of , or coverage error under some obvious modification of the procedure. Note from (4) and (8) that

| (5) |

Define, for and a fixed ,

Then the estimation error of has the expansion

| (6) |

We wish to minimise with respect to .

Let be a subsample size satisfying and . Let be constructed analogously to , with the complete sample replaced by the th block of consecutive observations drawn from , for . Then we have, analogous to (5), that

| (7) |

where denotes the version of obtained from the th subsample. Define

Using (8), (5) and (7), we have

It follows that

If we assume, as is typical, that has a leading term of the form for some function independent of , then , and are all minimised at asymptotically the same . Thus, an empirical procedure for choosing , and hence choosing , may be based on the minimisation of .

This procedure constructs the error estimate by considering all subsamples of consecutive points drawn from the original data sample, and is therefore computationally expensive. However, the argument supporting minimization of this quantity actually only requires that the number of subsamples used in the construction should grow with sample size . In practice, therefore, it is reasonable to evaluate the error measure using a smaller set of subsamples: in the numerical illustration given below, 20 subsamples, equally spaced along the data series , are used, allowing rapid evaluation of the error estimate.

6 Examples

To illustrate the benefits of optimally choosing , we consider three very general examples. For concreteness, we consider , and simulate the mean squared errors (MSEs) of hybrid block bootstrap estimators of for particular choices of . The true reference values of are approximated via massive simulation ( replications). For each of the sample sizes , , and , all entries in the included tables and heatmaps are based on replications, with bootstrap samples used within each replication, unless otherwise stated. For , the number of replications and bootstrap samples are each . For convenience, Table 1 provides some reference values of for MBB for the sample sizes we consider. This facilitates comparison with the MBB choice of for a range of values of . In particular, we give values for approximately equal to (not optimal), (thought to be optimal), , and .

Example 1 (ARMA(1,1)).

Suppose that the observations are generated according to an ARMA (1,1) model

with independent, identically distributed . The strong mixing condition is satisfied with an exponential rate (Lahiri, 2003, Example 6.1). An initial is sampled according to the marginal distribution, i.e. , and .

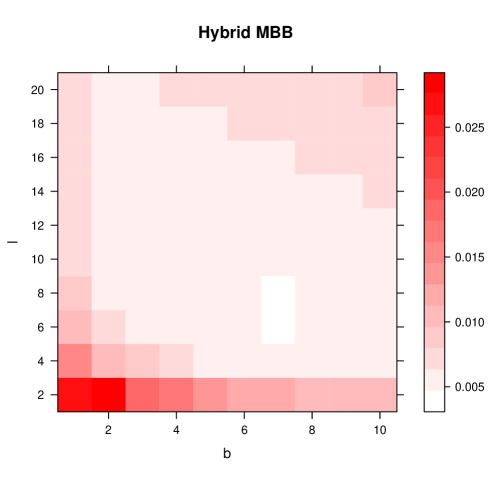

With , we have . We simulate the MSE in estimation of over a range of . The true value being estimated was computed (by massive simulation, as described) as . The heat map in Figure 2 plots MSE for , over a grid of values of . The heat map clearly illustrates the sub-optimality of , the subsampling bootstrap. The minimum MSE is 0.00472, with . By contrast, the minimum MSE for the MBB is 0.00637, with , and the subsampling bootstrap, which fixes , has minimum MSE of 0.00754, with .

We also compute the values of the pair which minimize MSE for other sample sizes, , and . These results are shown in Table 2. Comparing with Table 1, we note that the MSE-minimizing pair for each uses an strictly greater than and a much less than . Additionally, the MSE-minimizing value of is much larger than .

| MSE | ||

|---|---|---|

| (6,8) | 0.00472 | |

| (10,10) | 0.00250 | |

| (10,14) | 0.00154 | |

| (12,18) | 0.00097 |

The theory says that the hybrid MBB has an error rate in estimation of of , so we should expect the MSE to decrease at rate . In fact, a regression of on for the values reported in Table 2 has slope , which is not far off . The heatmap illustrates that the subsampling and MBB choices of are suboptimal.

For the current problem, of estimation of the sampling distribution of the sample quantile, there is therefore clear theoretical and practical advantage in using the hybrid block bootstrap, , over the moving block bootstrap. Remark 2 indicates, by contrast, that we might expect to see little difference, in estimation error terms, between the hybrid block bootstrap procedure and MBB if, instead, we are interested in estimation of . This was verified by considering, for all combinations of , the MSE of the estimator , for , so that , and , for which the quantity being estimated , for sample size . Based on 20,000 replications, with 20,000 bootstrap samples being used in construction of the estimator for each, the minimum MSE achieved by MBB is 0.00084, with . This is very similar to the overall minimum MSE of 0.00082, seen for . The minimum MSE of the subsampling bootstrap, , is 0.00334, substantially larger, when . This same picture was seen for , when, for the same values , the true probability being estimated . Simulation shows that the minimum MSE of MBB is then 0.00108, with , with the same minimum MSE for the hybrid block bootstrap, achieved for . Here the subsampling bootstrap yields an optimal MSE of 0.00227 when . These illustrative figures confirm that the hybrid block bootstrap has little advantage over MBB in error terms for this problem.

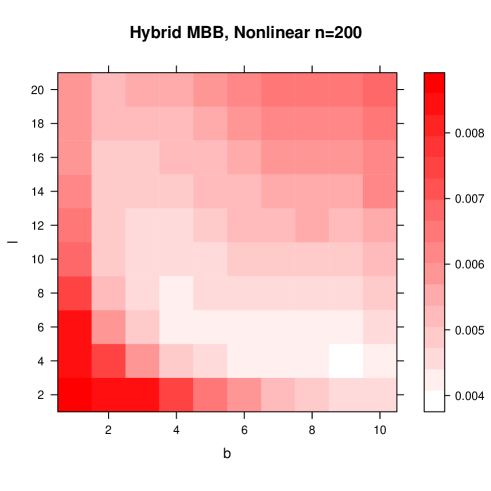

Example 2 (Nonlinear ARMA(2,3)).

Let be a sequence from the ARMA(2,3) process

As noted by Lahiri (2003, Example 6.1), such a sequence is strong mixing with exponentially decaying mixing coefficients. To simulate from this model, we initiate by generating from the marginal distribution, which has , with independent . The nonlinear model we consider is the square transformation of the above ARMA process,

The square transformation above preserves the strong mixing property and also preserves the mixing rate. Therefore, is strong mixing with the same exponential rate as . The interested reader is referred to Fan and Yao (2003, p. 69) or Davis and Mikosch (2009, p. 258). As with the previous example, we consider , and thus satisfies

implying . The simulation approximation to the true value is .

The heatmap of Figure 3 shows again that the subsampling and MBB choices of are suboptimal from the perspective of minimizing MSE.

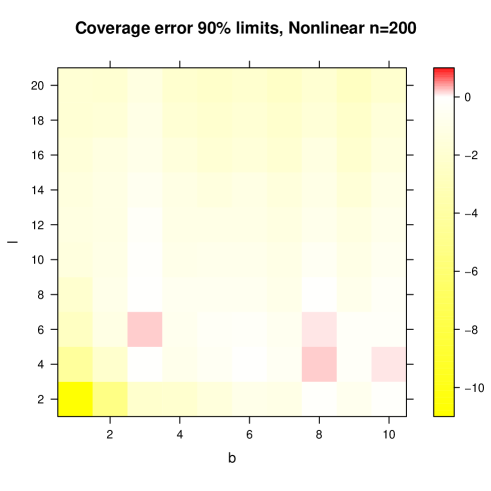

In Figure 4 we display the coverage error of lower percentile confidence intervals, as described in Section 4, of nominal 90% coverage. We observe that there is undercoverage for most choices of , sometimes very substantial, though there is overcoverage in a few cases. Appropriate choice of can yield limits with exactly the required coverage.

As proof of concept of the adaptive procedure for choice of described in Section 5, we consider estimation of , for sample size . We restrict to candidate values , corresponding to adaptive choice of . Table 3 shows the MSE in estimation of over 2500 replications for each combination of . By contrast, the MSE obtained by minimization of for each replication, using 20 subsamples of size in construction of this error quantity, was 0.00189. The adaptive method clearly yields an MSE that is far from optimal in this setting, but outperforms the procedure which fixes to larger values among those being considered.

The adaptive procedure is seen to perform better with increasing sample size. Table 4 provides analagous results for sample size , for which . Using in the minimization of over the same range of , now corresponding to adaptive choice of , and again using just 20 subsamples of length in evaluation of , the MSE of the adaptively chosen estimator over the 2500 replications was observed as 0.00066, much closer to optimal. Further tuning of the adaptive procedure certainly seems worthwhile as a means of providing an effective automatic choice of for the hybrid block bootstrap and will be pursued elsewhere.

| 0.5 | 0.75 | 1.0 | 1.5 | 2.0 | ||

|---|---|---|---|---|---|---|

| 0.5 | 0.00164 | 0.00150 | 0.00158 | 0.00189 | 0.00230 | |

| 0.75 | 0.00143 | 0.00154 | 0.00172 | 0.00220 | 0.00272 | |

| 1.0 | 0.00144 | 0.00166 | 0.00191 | 0.00250 | 0.00300 | |

| 1.5 | 0.00161 | 0.00195 | 0.00232 | 0.00297 | 0.00350 | |

| 2.0 | 0.00179 | 0.00225 | 0.00265 | 0.00335 | 0.00399 |

| 0.5 | 0.75 | 1.0 | 1.5 | 2.0 | ||

|---|---|---|---|---|---|---|

| 0.5 | 0.00062 | 0.00063 | 0.00072 | 0.00089 | 0.00108 | |

| 0.75 | 0.00061 | 0.00131 | 0.00082 | 0.00105 | 0.00126 | |

| 1.0 | 0.00065 | 0.00080 | 0.00094 | 0.00119 | 0.00139 | |

| 1.5 | 0.00076 | 0.00094 | 0.00112 | 0.00138 | 0.00166 | |

| 2.0 | 0.00087 | 0.00106 | 0.00125 | 0.00159 | 0.00182 |

Next we construct a process whose mixing coefficients decay at a polynomial rate, but not an exponential rate. This is accomplished through Theorem 2.1 of Chanda (1974); see also Bandyopadhyay (2006) and §3 of Chen et al. (2016).

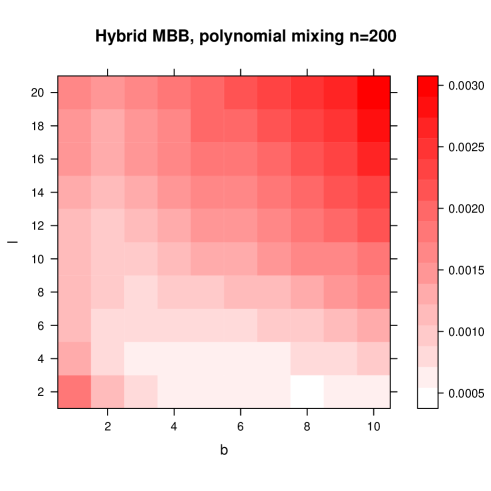

Example 3 (Polynomial Mixing Rate).

Let the sequence be generated according to

where the are independent, identically distributed and . Then is strong mixing with a polynomial rate, and Chanda (1974) may be used to deduce that .

In practice, we cannot simulate from the above process exactly because it is expressed as an infinite series. Therefore, we approximate the process by truncating the series at 100 terms, which means that in reality is approximated by a very high order MA process. For our numerical example, and . As before, we consider , corresponding to . Simulation yields an approximation to the true value . The heatmap for this example shown in Figure 5 is based on 10,000 replications, and 10,000 bootstrap samples for each replication of the experiment.

As with the previous two examples, the heatmap supports our finding of suboptimality of the choices of suggested by the subsampling bootstrap and the MBB.

7 Proofs

In what follows we denote by a generic positive constant independent of . Denote by and the standard normal distribution and density functions, respectively. Standard asymptotic properties (e.g. Lahiri and Sun (2009)) of for dependent data can be invoked to show that, for any ,

| (8) |

where .

We first state a lemma which is a special case of Sun and Lahiri’s (2006) Lemma 5.3.

Lemma 2.

Let be a double array of row-wise stationary strong mixing Bernoulli random variables with and mixing coefficients , for some fixed . Then, for any positive , and any , we have

Define, for any , .

Lemma 3.

Suppose that . Then for any arbitrarily small , the following results hold uniformly over .

-

(i)

for any .

-

(ii)

for some .

-

(iii)

for any .

Proof of Lemma 3:

Define and . Then we have

| (9) |

For each , application of Lemma 2 with , and , for arbitrarily small , yields

It follows by Bonferroni’s inequality that

for sufficiently small , uniformly over . This, in conjunction with (9), implies that , which proves part (i) of Lemma 3.

To prove part (ii), write and note that

| (10) | |||||

Define, for , . It is clear that . Noting that for sufficiently large and sufficiently small ,

we have

We may therefore choose sufficiently close to and some such that and . It follows that for any ,

Consider

Applying part (i), we have, uniformly over , that

and

It is clear that

The bounds on therefore imply that

| (11) |

It follows by part (i) again that

| (12) | |||||

For the proof of part (iii), define and . Then we have

| (13) | |||||

For each , set, for the application of Lemma 2, , and , for arbitrarily small . Noting that , we have, by Lemma 2, that for any ,

It follows by Bonferroni’s inequality that for sufficiently small and for any ,

uniformly over . This, in conjunction with (13), implies that , which proves part (iii) of Lemma 3.

Lemma 4.

Suppose that . Then for any arbitrarily small ,

-

(i)

.

-

(ii)

.

Proof of Lemma 4:

Let be as specified in Lemma 3(ii). Define, for ,

Note that . Using Lemma 3(ii), we have, for some , any and sufficiently large ,

| (14) | |||||

Note that if , then , so that

If for some , then , so that for sufficiently large, we have

The above results suggest that

for sufficiently large. It then follows from (14) that can be made arbitrarily small if we choose and large enough, using the fact that . The same arguments can be applied to the lower tail probability . Thus we have . Lemma 4(i) then follows as can be made arbitrarily small.

To prove part (ii), write

Denote by the ordered sequence of . For any arbitrarily small , is bounded above by

| (15) |

where the supremum in the last probability is taken over . Noting that , we have

for sufficiently small . Thus we may find a positive sequence satisfying

| (16) |

for sufficiently small . Noting that for sufficiently small , following the proof of Lemma 5.4(iv) of Sun and Lahiri (2006) and using (16), the first probability in (15) can be bounded above, for sufficiently large and sufficiently small , by

That the last two probabilities in (15) converge to 0 follows from Lemma 4(i) and Lemma 3(ii), respectively. From the above results we derive that . Similar arguments show also that , which completes the proof of part (ii).

Lemma 5.

For any arbitrarily small and any compact ,

uniformly over .

Proof of Lemma 5:

Denote by the th conditional cumulant of given . It is clear that . It can be shown using somewhat tedious asymptotic expansions that, uniformly over ,

where can be made arbitrarily small if and . Lemma 5 then follows by comparing the Edgeworth expansion of the conditional distribution function of with the distribution function.

Proof of Theorem 1:

8 Conclusion

In the absence of exact, finite-sample results, accurate estimation of quantiles is essential for implementation of statistical inference procedures. As sample quantiles are non-smooth functionals, conventional bootstrap theory for the smooth function model does not apply to estimation of their distribution. In dependent data settings, with some notable exceptions, little is known about the block bootstrap for distribution estimation of sample quantiles. In this paper we have established a general optimality theory for block bootstrap procedures in such settings under strong mixing conditions, and we have shown that a hybrid block bootstrap is optimal, in the sense of having the fastest convergence rate for distribution estimation. In addition, of course, since the hybrid block bootstrap is based on bootstrap samples of smaller size than the data sample, it provides computational advantage over MBB. How one should choose in a given application to capture the good theoretical properties of the hybrid block bootstrap requires further consideration. We have provided discussion of an empirical scheme that seems fruitful for this purpose and which will be further developed and refined elsewhere.

References

- Athreya and Lahiri [2006] Krishna B. Athreya and Soumendra N. Lahiri. Measure Theory and Probability Theory. New York: Springer, 2006.

- Babu [1986] G.J. Babu. A note on bootstrapping the variance of sample quantile. Annals of the Institute of Statistical Mathematics, 38:439–443, 1986.

- Bandyopadhyay [2006] Soutir Bandyopadhyay. A note on strong mixing. Technical report, 2006.

- Bickel and Freedman [1981] P.J. Bickel and D.A. Freedman. Some asymptotic theory for the bootstrap. Annals of Statistics, 9:1196–1217, 1981.

- Bühlmann [1994] Peter Bühlmann. Blockwise bootstrapped empirical process for stationary sequences. Annals of Statistics, 22:995–1012, 1994.

- Bühlmann and Künsch [1999] Peter Bühlmann and Hans R. Künsch. Block length selection in the bootstrap for time series. Computational Statistics and Data Analysis, 31:295–310, 1999.

- Carlstein [1986] E. Carlstein. The use of subseries values for estimating the variance of a general statistic from a stationary sequence. Annals of Statistics, 14:1171–1179, 1986.

- Chanda [1974] K.C. Chanda. Strong mixing properties of linear stochastic processes. Journal of Applied Probability, 11(2):401–408, 1974.

- Chen et al. [2016] Xiaohong Chen, Qi-Man Shao, Wei Biao Wu, and Lihu Xu. Self-normalized Cramér-type moderate deviations under dependence. Annals of Statistics, 44(4):1593–1617, 2016.

- Davis and Mikosch [2009] Richard A. Davis and Thomas Mikosch. Probabilistic properties of stochastic volatility models. In Torben G. Andersen, Richard A. Davis, Jens-Peter Kreiß, and Thomas Mikosch, editors, Handbook of Financial Time Series, pages 255–267. Berlin: Springer, 2009.

- De Angelis et al. [1993] D De Angelis, P Hall, and G. A. Young. A note on coverage error of bootstrap confidence intervals for quantiles. Mathematical Proceedings of the Cambridge Philosophical Society, 114:517–531, 1993.

- Efron [1979] B. Efron. Bootstrap methods: another look at the jackknife. Annals of Statistics, 7:1–26, 1979.

- Efron [1982] B. Efron. The Jackknife, the Bootstrap and Other Resampling Plans. Society for Industrial and Applied Mathematics, Philadelphia., 1982.

- Falk and Janas [1992] M. Falk and J. Janas. Edgeworth expansions for studentized and prepivoted sample quantiles. Statistics and Probability Letters, 14:13–24, 1992.

- Fan and Yao [2003] Jianqing Fan and Qiwei Yao. Nonlinear Time Series: Nonparametric and Parametric Methods. New York: Springer, 2003.

- Ghosh et al. [1984] M. Ghosh, W.C. Parr, K. Singh, and G.J. Babu. A note on bootstrapping the sample median. Annals of Statistics, 12:1130–1135, 1984.

- Götze and Künsch [1996] F. Götze and Hans R. Künsch. Second-order correctness of the blockwise bootstrap for stationary observations. Annals of Statistics, 24:1914–1933, 1996.

- Gregory et al. [2015] Karl B. Gregory, Soumendra N. Lahiri, and Daniel J. Nordman. A smooth block bootstrap for statistical functionals and time series. Journal of Time Series Analysis, 36:442–461, 2015.

- Hall [1985] Peter Hall. Resampling a coverage pattern. Stochastic Processes and their Applications, 20:231–246, 1985.

- Hall [1992] Peter Hall. The Bootstrap and Edgeworth Expansion. New York: Springer, 1992.

- Hall and Martin [1991] Peter Hall and Michael A. Martin. On error incurred using the bootstrap variance estimate when constructing confidence intervals for quantiles. Journal of Multivariate Analysis, 38:70–81, 1991.

- Hall and Sheather [1988] Peter Hall and S.J. Sheather. On the distribution of a studentized quantile. Journal of the Royal Statistical Society Series B, 50:381–391, 1988.

- Hall et al. [1989] Peter Hall, Thomas J. DiCiccio, and Joseph P. Romano. On smoothing and the bootstrap. Annals of Statistics, 17(2):692–704, 1989.

- Hall et al. [1995] Peter Hall, Joel L. Horowitz, and Bing-Yi Jing. On blocking rules for the bootstrap with dependent data. Biometrika, 82(3):561–574, 1995.

- Kuffner et al. [2017] Todd A. Kuffner, Stephen M.S. Lee, and G. Alastair Young. Consistency of block bootstrap for distribution and variance estimation for sample quantiles of weakly dependent sequences. Technical report, 2017.

- Künsch [1989] Hans R. Künsch. The jackknife and the bootstrap for general stationary observations. Annals of Statistics, 17(3):1217–1241, 1989.

- Lahiri [1992] Soumendra N. Lahiri. Edgeworth correction by moving block bootstrap for stationary and nonstationary data. In R. LePage and L. Billard, editors, Exploring the Limits of Bootstrap, pages 263–270. Wiley, 1992.

- Lahiri [1996] Soumendra N. Lahiri. On Edgeworth expansion and moving block bootstrap for studentized m-estimators in multiple linear regression models. Journal of Multivariate Analysis, 56:42–59, 1996.

- Lahiri [1999] Soumendra N. Lahiri. Theoretical comparisons of block bootstrap methods. Annals of Statistics, 27:386–404, 1999.

- Lahiri [2003] Soumendra N. Lahiri. Resampling Methods for Dependent Data. Springer-Verlag, 2003.

- Lahiri [2005] Soumendra N. Lahiri. Consistency of the jackknife-after-bootstrap variance estimator for the bootstrap quantiles of a studentized statistic. Annals of Statistics, 33(5):2475–2506, 2005.

- Lahiri and Sun [2009] Soumendra N. Lahiri and S. Sun. A Berry-Esseen theorem for sample quantiles under weak dependence. Annals of Applied Probability, 19(1):108–126, 2009.

- Liu and Singh [1992] R.Y. Liu and K. Singh. Moving blocks jackknife and bootstrap capture weak convergence. In R. LePage and L. Billard, editors, Exploring the Limits of Bootstrap, pages 225–248. Wiley, 1992.

- Naik-Nimbalkar and Rajarshi [1994] U.V. Naik-Nimbalkar and M.B. Rajarshi. Validity of blockwise bootstrap for empirical processes with stationary observations. Annals of Statistics, 22:980–994, 1994.

- Paparoditis and Politis [2001] E. Paparoditis and D.N. Politis. Tapered block bootstrap. Biometrika, 88:1105–1119, 2001.

- Politis et al. [1997] D. Politis, J.P. Romano, and M. Wolf. Subsampling for heteroskedastic time series. Journal of Econometrics, 81:281–317, 1997.

- Politis and Romano [1992] D.N. Politis and Joseph P. Romano. A circular block resampling procedure for stationary data. In R. LePage and L. Billard, editors, Exploring the Limits of Bootstrap, pages 263–270. Wiley, 1992.

- Politis and Romano [1994] D.N. Politis and J.P. Romano. Large sample confidence regions based on subsamples under minimal assumptions. Annals of Statistics, 22:2031–2050, 1994.

- Shao and Politis [2013] Xiaofeng Shao and Dimitris N. Politis. Fixed subsampling and the block bootstrap: improved confidence sets based on -value calibration. Journal of the Royal Statistical Society Series B, 75(1):161–184, 2013.

- Sharipov and Wendler [2013] Olimjon Sh. Sharipov and Martin Wendler. Normal limits, nonnormal limits, and the bootstrap for quantiles of dependent data. Statistics and Probability Letters, 83:1028–1035, 2013.

- Singh [1981] K. Singh. On asymptotic accuracy of Efron’s bootstrap. Annals of Statistics, 9:1187–1195, 1981.

- Sun [2007] Shuxia Sun. On the accuracy of bootstrapping sample quantiles of strongly mixing sequences. Journal of the Australian Mathematical Society, 82:263–281, 2007.

- Sun and Lahiri [2006] Shuxia Sun and Soumendra N. Lahiri. Bootstrapping the sample quantile of a weakly dependent sequence. Sankhyā, 68(1):130–166, 2006.

- Tewes et al. [2017] Johannes Tewes, Dimitris N. Politis, and Daniel J. Nordman. Convolved subsampling estimation with applications to block bootstrap. arXiv:1706.07237, 2017.