The Chebyshev method for the implied volatility

Abstract

The implied volatility is a crucial element of any financial toolbox, since it is used for quoting and the hedging of options as well as for model calibration. In contrast to the Black-Scholes formula its inverse, the implied volatility, is not explicitly available and numerical approximation is required. We propose a bivariate interpolation of the implied volatility surface based on Chebyshev polynomials. This yields a closed-form approximation of the implied volatility, which is easy to implement and to maintain. We prove a subexponential error decay. This allows us to obtain an accuracy close to machine precision with polynomials of a low degree. We compare the performance of the method in terms of runtime and accuracy to the most common reference methods. In contrast to existing interpolation methods, the proposed method is able to compute the implied volatility for all relevant option data. In this context, numerical experiments confirm a considerable increase in efficiency, especially for large data sets.

Keywords Black-Scholes implied volatility, real-time evaluation, Chebyshev Polynomials, Polynomial Interpolation, Laplace implied volatility

MSC 2010: 91G60 90-08, 65D05

1 Motivation

Ever since Black and Scholes (1973) and Merton (1973) introduced their option pricing model, the Black-Scholes formula has been omnipresent in the financial industry. The one parameter in the model that can not be observed using market data is the volatility of the underlying asset process. The Black-Scholes call price function is strictly monotone increasing in volatility. Hence, for each observed call price there is a unique volatility such that the resulting model price equals the market price. This is called the implied volatility, one of the most important quantities in finance.

The implied volatility can be seen as a universal language in the daily business of trading, hedging, model calibration and more generally in risk management. Typically, trading desks quote option prices in implied volatilities instead of absolute prices. This allows traders to compare option prices on different underlyings such as equities, indices, currencies or commodities. For high frequency trading in particular, very accurate real-time evaluations of the implied volatility are required for large data sets. As stated in Baumeister (2013) and Salazar Celis (2017) in practice, often millions of option prices have to be inverted in real-time for instance by large data providers. Furthermore, the implied volatility is needed for the most common derivative hedging strategy, the so-called delta-hedging strategy. It is used to infer the sensitivity of the option price with respect to the underlying spot price, the option’s delta. One takes an opposing position to the delta in the underlying asset as a hedge. Since the 1970s a large variety of asset price models that generalize and improve the Black-Scholes model have been introduced. Typically, these models are determined by a number of parameters that are fitted to observed option prices. In the context of this model calibration, the implied volatility enters the objective function. Instead of minimizing (for instance the quadratic) difference of model and market prices, the difference of the corresponding implied volatilities is used. This is a convenient normalization since options from deep in the money to far out of the money are transformed to the same scale. For calibration purposes, the implied volatility needs to be available rapidly—especially in view of routinely processed intraday recalibrations. Depending on the pricing routine employed, the accuracy needs to be medium or high. Moreover, a closed-form of the implied volatility function is advantageous since it allows the implementation of gradient-based optimization routines.

Unfortunately, the solution of this inverse problem is not available in an explicit form and thus a numerical approximation method is required. Since the implied volatility function is a crucial element of any financial toolbox, special care is called for. The method must allow the computation of implied volatilities for options in all of the different markets. Hence options with very low or high volatilities as well as options with moneyness varying from far out of the money to deep in the money have to be included. Therefore the method must cover a large domain of input variables. In order to satisfy the needs of the different applications the method should be highly efficient for a given requirement in terms of accuracy. Even for very large data sets the method must be able to deliver accurate real-time evaluations of the implied volatility. In view of the implied volatility as an ingredient of optimization routines, the approximation should be given in closed-form with accessible derivatives. Finally, the method should be easy to implement and to maintain. There exists a long list of papers dealing with this problem.

The first class of methods to determine the implied volatility are iterative root finders such as

-

•

Newton-Raphson,

-

•

Matlabs implied volatility function blsimpv,

- •

The first approach dates back to Manaster and Koehler (1982) who showed that a Newton-Raphson algorithm can be applied to calculate the implied volatility. The blsimpv function is part of the financial toolbox in Matlab and uses an iterative scheme based on Brent-Dekker. The blsimpv function becomes very slow for larger data-sets and the Newton-Raphson algorithm is highly dependent on the starting value of the iteration. For many standard parameters it often converges fast but for more extreme parameters, the number of iterative steps increases significantly, see Section 7.

To overcome this problem, Jäckel (2006) exploits the limit behaviour of the normalised call price to provide a better initial guess, which reduces the iterative steps in a modified Newton method. In Jäckel (2015) this approach is further improved using rational approximation for the initial guess and Householder’s method for the iteration. This reduces the number of iterative steps even further. One drawback of the method is that it comes with the burden of a relatively complex implementation and therefore a costly maintenance. Already the generation of the initial guess relies on the rational cubic interpolation of Delbourgo and Gregory (1985) and a transformation, which is highly sensitive in terms of the accuracy of the error function and the inverse of the normal distribution.

The second class of methods to compute the implied volatility are non-iterative approximations methods. These methods are popular since they provide

-

•

fast computation of implied volatilities,

-

•

easy implementation and maintenance,

-

•

closed-form expressions,

-

•

a simple interpretation of the formula.

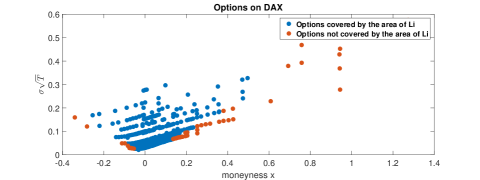

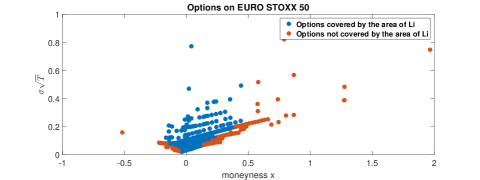

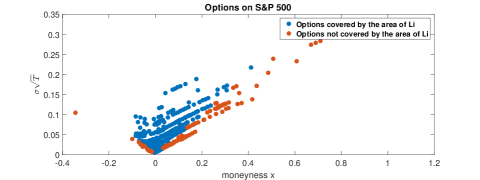

First, analytical approximations for at the money and later near the money options have been developed. Typically, these methods depend on a series expansion of the call price at the money. Prominent examples are the approximation formulas of Brenner and Subrahmanyan (1988), Chance (1996), Corrado and Miller (1996), Chambers and Nawalkha (2001) and Lorig et al. (2014). Typically, these methods suffer from a poor performance for out of the money options. More recently, Li (2008), Pistorius and Stolte (2012) and Salazar Celis (2017) have developed rational approximations of the implied volatility. Unfortunately, the domain for which the latter set up the interpolation is very restrictive and excludes option prices which occur in practice. In particular, options with relatively high or low volatilities cannot be handled. For example Figure 1.1 illustrates the moneyness and implied time-scaled volatilities of options on the DAX index traded on 6/20/2017 (Source Thomson Reuters Eikon). In this example, only of all put options and of the call options are covered. Although the domain was designed for equity options, even in this case the formula cannot be applied to all relevant contracts. Moreover, one needs additional iterative Newton steps to achieve a high accuracy close to machine precision for the methods of Li (2008) and Salazar Celis (2017).

![[Uncaptioned image]](/html/1710.01797/assets/x1.png)

In this paper, we propose polynomial approximation to the implied volatilities surface choosing Chebyshev interpolation. The approximation of the implied volatility thus inherits the appealing properties of Chebyshev interpolation, namely the fact that the approximation is highly efficient, stable and easy to implement. It is sufficient to invert the normalized call price, which reduces the dimensionality of the approximation to a bivariate Chebyshev interpolation. For this we use the algorithm provided in the MATLAB package chebfun (www.chebfun.org) that exploits the low-rank structure of the problem. Hence, the method enables a fast computation of implied volatilities at a high accuracy. In order to cover the whole range of relevant options, one has to investigate the shape of the call price surface further. We observe areas where the call price is almost linear as well as areas where the call price is extremely flat in the volatility. For an optimal treatment of the different areas we introduce a domain splitting. In the flat areas, we exploit the limit behaviour by introducing appropriate transformations. We show that the error of the interpolation decays subexponentially fast and we provide an explicit error bound. It is straightforward to adjust the method to any pre-set accuracy to obtain an optimal efficiency. Furthermore, the implied volatility function is represented by a polynomial and hence very easy to handle. Let us emphasize that this procedure is more general and can be applied to similar problems as well. To illustrate this, we approximate the implied volatility in a market model based on a Laplacian density function instead of a normal distribution introduced by Madan (2016).

The remainder of the article is as follows. In Section 2, we recall the normalized call price and the Chebyshev function on which our approach relies. In Section 3, we introduce a simple, bivariate interpolation of the implied volatility based on a low-rank interpolation in Chebyshev nodes. We highlight the potential of the method and show that we reach a maximal error close to machine precision with a low number of interpolation points. In Section 4, we introduce the bivariate interpolation on a larger domain which includes very low and very high volatilities as well as deep in the money and far out of the money options. In Section 7, we show that the method is both, fast and accurate and compare it to the methods of Newton-Raphson, Li (2008) and Jäckel (2015). We devote the last section to the approximation of the implied volatility in the Laplacian market model.

2 Preliminaries

2.1 The normalized Black-Scholes price

As stated, the implied volatility depends on the parameters ,, , and the option premium . The computational effort to interpolate a function depending on five variables is challenging. Fortunately, we can reduce the dimensionality as stated in Jäckel (2015) amongst others using the normalized call price given as

| (2.1) | |||||

In this context measures the moneyness (the option is out of the money if , at the money if and in the money if ), corresponds to the time-scaled volatility. We have

| (2.2) |

Furthermore, call prices of in the money options can be expressed by those of out of the money options, namely

| (2.3) |

Hence the domain can be reduced to and consequently the call price is normalized to values in . To calculate the implied volatility for a call price it is thus sufficient to solve Equation (2.1) for using the normalized call price .

2.2 Chebyshev Interpolation

The polynomial interpolation of a function on in the Chebyshev points is given by

| (2.4) |

where and indicates that the first and the last summand are halved. If the function has an analytic extension to a Bernstein ellipse , the error decays exponentially, see Theorem 8.2 of Trefethen (2013). In practice, this often yields an approximation close to machine precision with a low interpolation order. Together with a stable implementation being available, see Higham (2004), these are the key advantages of the Chebyshev interpolation that we will exploit.

The univariate Chebyshev interpolation admits a two-dimensional tensor based extension. A function can be approximated by the interpolation

| (2.5) |

with two-dimensional coefficients given by

Again, we obtain an subexponential error decay if the function has an analytic extension to a two-dimensional Bernstein ellipse, see Sauter and Schwab (2010). The tensor approach of (2.5) suffers from the curse of dimension: To decrease the error in the same proportion as in the univariate case, the number of summands and thus the complexity increases quadratically. Therefore more efficient bivariate Chebyshev interpolations have been developed. In particular, the algorithm of Townsend and Trefethen (2013) implemented in chebfun2 reconciles the opposed aims of high accuracy and high efficiency for bivariate functions. It relies on a Gauss elimination with complete pivoting to find an optimal low rank approximation. This leads to

where and are one-dimensional Chebyshev interpolations of degree and . This enables a matrix representation of the resulting interpolation.

3 Introduction of the approximation method

We introduce a direct interpolation of the implied volatility function using Chebyshev nodes. The two-dimensional Chebyshev interpolation requires the function to be defined on the rectangle . For the implied volatility this is not given a priori. The variable can easily be restricted to some interval which can be transformed to by a linear transformation ,

| (3.1) |

The maximal domain of , on the contrary, does depend on as for the upper limit is given by .

The intuitive approach is to choose with for a given moneyness and scale the resulting interval to by a linear transformation. If is not chosen to close to 0, a two-dimensional Chebyshev interpolation on this domain provides promising results.

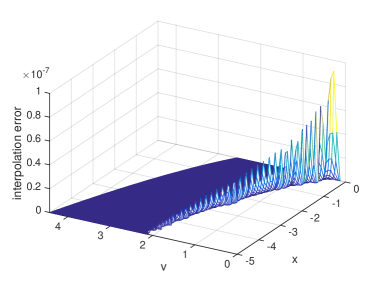

For a first numerical example, we fix , , and . Then we choose a Chebyshev grid and transform the points to the domain by setting and . On these points we compute the implied volatilities using the method of Jäckel (2015) and apply the chebfun2-algorithm.

To determine the interpolation error we define an equidistant grid of points in the interval . For fixed , the interval bounds in are defined as and . For each -value in the fixed equidistant grid, points distributed equidistantly in are determined. This leads to points in the space as reference points for which we compute normalized call prices . For each reference call price we compute the implied volatility using the bivariate Chebyshev method.

Figure 3.1 shows that this approach performs very well. The maximal error lies below a level of for and decreases exponentially fast in .

As in the approximation methods mentioned above, we have pre-fixed a domain that is convenient for the approach. Naturally, the question arises as to which domain is appropriate to cover the relevant option data.

3.1 Investigation of the interpolation domain by market data

To find an appropriate interpolation domain, we investigate option data of the DAX, the EURO STOXX 50, the S&P 500 and the VIX index from Thomson Reuters Eikon. For all options with non-zero trading volume we compute the forward moneyness and the time-scaled volatility . Then we check if the resulting parameters are covered by the domain of Li. Figure 3.2 illustrates the option parameters for all four indices. For all indices we observe that a relevant part of the options is not covered by the domain of Li. We observe moneyness between and as well as time-scaled volatilities up to . In different markets or under different market conditions one can expect to observe even more extreme option parameters. Volatilities become considerably higher during a financial crisis. This motivates us to set up a Chebyshev interpolation of the implied volatility on a significantly larger domain which covers all relevant option data. To do this in the most efficient way we need to enhance the intuitive approach introduced above with a splitting of the domain and tailored scaling functions.

4 Domain splitting and scaling

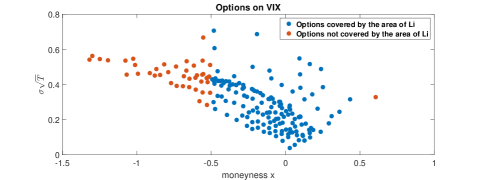

To derive an approximation of the implied volatility on a sufficiently large domain, we further inspect the normalized call price. The implied volatility is not analytic at and . Therefore the maximal possible interval needs to be restricted to with call prices , which excludes these points. This assumption is not restrictive if the chosen is small enough. Extending the domain towards the maximal interval decreases the rate of convergence. To reduce this impact, we exploit the limit behaviour of the call price. Graph 4.1 shows for a fixed moneyness the normalized call price as a function of the volatility. We observe that the call price is flat for very low as well as very high volatilities and almost linear around the point of inflection. This motivates us to split the domain into three parts.

![[Uncaptioned image]](/html/1710.01797/assets/x8.png)

| (4.1) |

with corresponding volatilities . The idea of splitting the domain is based on the method of Jäckel (2015).

For each domain we will tailor a bivariate Chebyshev interpolation. Where call prices are flat its inverse becomes very steep. Hence, a direct polynomial interpolation is not well-suited. Fortunately, by exploiting the asymptotic behaviour of the call price function, we resolve the problem. On each interval, we define a scaling function for which transforms the call price to for each . For the resulting functions , with and for where is the linear scaling of (3.1). For a given call price and moneyness the implied volatility can then be approximated by

4.1 Scaling functions

In the following, we introduce the appropriate scaling functions for each of the areas.

4.1.1 Medium volatilities

First consider the middle part of the function. As discussed, for around the point of inflection, the implied volatility surface is almost linear. Thus, a linear scaling suffices,

Clearly, is analytic and the inverse is given by

4.1.2 Low volatilities

For low volatilities the call price function is very flat, and thus the implied volatility function as its inverse is steep. Therefore, a linear scaling will not provide an appropriate transformation prior to a polynomial interpolation. Instead, we propose a suitable scaling function that reduces the steepness of the inverse such that it becomes almost linear. This will increase the efficiency of the resulting approximation considerably, when compared to a linear scaling. To do this, we explore the limit behaviour of the normalized call price. For we have by equation (2.8) of Jäckel (2006) that

where is the density of the standard normal distribution. By inverting the function , which has the major effect in the limit, we obtain an inverse of the form with constants that are not relevant for us. This leads to the following transformation

The parameter ensures the well-definedness for and the remaining terms are needed to map the interval to . The transformation is analytic with inverse

Using this transformation the function is approximately linear in .

As already mentioned, to guarantee analyticity we restrict the interval to for . Therefore, we define the scaling function for the low volatilities as , where is the linear transformation

The function is analytic in the interval as it is a composition of two analytic functions. The inverse of is given by .

4.1.3 High volatilities

Just as for the low volatilities, the call price function is very flat for high volatilities and thus its inverse becomes steep. As the implied volatility function is not even bounded. As a first step, the volatility is capped by some to guarantee that the slope will not be arbitrarily high. Again, a linear transformation is not the best choice and we propose a different scaling based on the behaviour of the call price. From Jäckel (2006) equation (2.7) we obtain for

A similar transformation as in the case of low volatilities entails improvement. Assume first that and define

with inverse

Exploiting the limit behaviour of the call price, one can show that for large enough . Hence which is linear in .

Now for the transformation is a bijection into a bounded domain which can be normalized to by the linear transform as in the previous case

Thus and depending on the choice of .

4.2 Splitting

The explicit choice of the boundaries depends on the particular application. In the following we want to set the boundaries in such a way that a very large set of parameters is covered and the rate of convergence is about the same for all areas.

Maximal volatility :

We choose as an upper bound for the time scaled volatility . This allows us to include highly volatile markets and long maturities. At the same time the method can achieve accuracies close to machine precision.

Minimal volatility :

We define a lower bound by

For this choice the corresponding prices can be computed with the standard machine precision. It includes very low volatilities. For instance at this choice even allows call options with a time to maturity of one day () and a Black-Scholes volatility of . The rate of convergence can be increased further if is chosen higher.

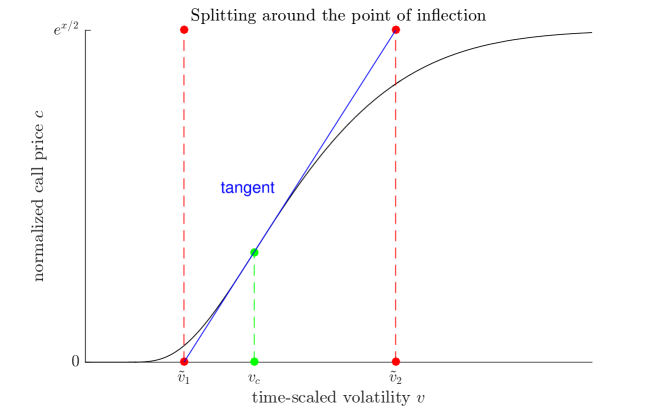

Splitting volatilities and :

We choose and according to the properties of the call price function. The call price function has a unique inflection point for where the slope is maximal. Jäckel (2015) proposes the lower bound as the zeros of the tangent line at this point. The upper bound is set to be the point where the line hits the maximal call price depending on . See Figure 4.2. The tangent line is given as

Thus

However, this choice of boundaries has two serious disadvantages. First, the boundary tends to zero, hence for small values of we obtain . Second, the computation of and requires the evaluation of and for each . For real-time computation on large data sets, this becomes a computational burden. We solve this problem by replacing and with linear approximations. We propose the boundaries

Splitting of the low volatility area

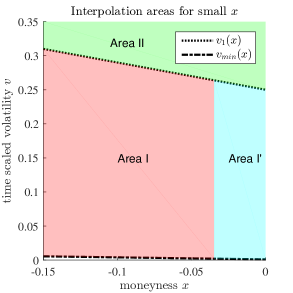

For low volatilities we improve the interpolation by introducing a further splitting in . The behaviour of the function changes at the point of inflection. As shown before, we need to set . Thus at some point the interpolation boundary will cross this change of behaviour. This can be anticipated by a splitting at the point where . For the proposed linear splitting these points are given by and . The first point is outside the domain for , hence we only consider the second point. We divide the area of the low volatilities in an Area I for and an Area I’ for , see Figure 6.1. The empirical results show that this additional splitting further improves the rate of convergence.

5 Error analysis

The following theorem is the theoretical foundation of the high efficiency of the approximation method. Thanks to the analyticity of the Black-Scholes call price and the scaling functions, we gather that the convergence is sub-exponential in the number of nodal points.

Theorem 5.1.

Let be analytically continuable to some open region around and let for each . Then there exist constants such that for and its bivariate Chebshev interpolation

Proof.

According to Lemma 7.3.3 of Sauter and Schwab (2010) we need to show that is analytically continuable and bounded on where and are Bernstein ellipses. Gaß et al. (2015) show that the call price is analytic. For fixed the implied volatility function is holomorphic in since the inverse of a bijective holomorphic function is again holomorphic. Next we need to prove analyticity in . Let . Define . Then the function is implicitly given by the solution of . Furthermore, for each , is holomorphic in some open region with

as . Thus by the complex implicit function theorem (see Theorem 7.6 of Fritzsche and Grauert (2012)) there exits a unique function that is holomorphic in some region around . Thus is holomorphic in where and are open regions of . Thus there exist such that and . The boundedness follows for sufficiently small , as is continuous on . ∎

We can enhance the efficiency even further by exploiting the low-rank structure of the bivariate functions. To do so, in our implementation we use the chebfun2 algorithm based on Townsend and Trefethen (2013).

6 Implementation

As a starting point for the approximation of the implied volatility function, we split the interpolation domain into four different areas. For each area, we approximate the implied volatility by a separate bivariate Chebyshev interpolation of the form where is defined as in (3.1) and for each area we have a different scaling in . For the sake of a lucid presentation, we list the different areas and transformations below.

Area I: For and we have

Area I’: For and we again use transformation .

Area II: For and we have

Area III: For and we have

The call prices and correspond to the volatilities

Moreover, we replace the boundary call prices , and by univariate interpolations to reduce the runtime further. The evaluation of , however, is done directly, since for low volatilities the call price is hard to approximate. For this step we use the implementation of the call price function provided in Jäckel (2015), which is of very high precision.

6.1 Algorithmic structure

Our method allows for an online/offline decomposition:

-

•

offline-phase (preparation):

In each area, we compute the implied volatilities on a grid of Chebyshev points. Then we apply the chebfun2 algorithm with pre-specified accuracy and obtain a low-rank approximation. -

•

online-phase (real-time evaluation):

In the online phase implied volatilities are computed from real-time data, containing a vector of call prices and the corresponding strikes , spot prices , maturities and interest rates .-

–

Normalization: We calculate the normalized call price and the forward moneyness from the data. Option prices with need to be transformed to prices with moneyness by Formula (2.3).

-

–

Splitting: For each pair , we need to find the corresponding area. As the computation of requires the most computational effort, we proceed as follows. First, we compute and check if . Next, we check if and eventually . Only in the latter case, do we compute and check whether .

-

–

Transformation: We compute the transformed call prices and moneyness with the respective transformations.

-

–

Evaluation: We evaluate the bivariate Chebyshev interpolations provided in the offline-phase at the transformed call prices and moneyness to obtain the time-scaled implied volatility.

-

–

The runtime of the online-phase is primarily determined by the splitting and the evalutation-phase. The evaluation of the bivariate interpolations can be done in different ways and can be performed in very few computational steps depending on the required accuracy.

For optimal efficiency in the evaluation step, we consider a bivariate Chebyshev interpolation of a function in the low rank form where and are univariate Chebyshev interpolations of rank and . More precisely,

The Chebyshev polynomials can be computed in different ways, for instance by or by the iterative formula , , . It turns out that for large data sets the iterative evaluation of the Chebyshev polynomials is advantageous compared to the cosine formula as only simple additions and multiplications are involved while the evaluation of and is slightly slower. Therefore we use this approach in our implementation.

After setting up the Chebyshev method for a pre-specified accuracy we obtain a low-rank approximation for each of the four areas. Table 6.1 displays the ranks and the grid sizes of the low rank interpolation operator for the three specified accuracies (low accuracy), (medium accuracy) and (high accuracy). As expected the ranks and grid sizes are higher for a higher accuracy. Moreover, we observe that we need more interpolation nodes in Area I and Area I’ to obtain the same level of accuracy as in Area II and Area III.

| Area | low accuracy | medium accuracy | high accuracy |

|---|---|---|---|

| Area I | , , | , , | , , |

| Area I’ | , , | , , | , , |

| Area II | , , | , , | , , |

| Area III | , , | , , | , , |

7 Numerical Results

We compare our approximation method to

-

•

the Jäckel (2015) method,

-

•

the approximation formula given in Li (2008),

-

•

the approximation formula given in Li (2008) with the proposed polishing of two Newton-Raphson iterations,

-

•

the Newton-Raphson algorithm with the starting point given in Manaster and Koehler (1982). The algorithm terminates if .

In order to do so, we first choose a domain on which all methods can be applied and compare the resulting errors and runtimes (Section 7.1). On the complete domain , we compare the proposed method to the Jäckel (2015) method and the Newton-Raphson algorithm as those are the only ones that can also be applied on this set (Section 7.2). Finally, we include actual market data (Section 7.3). All codes are written in Matlab R2014a and the experiments are run on a computer with Intel Xeon CPU with 3.10 GHz with 20 MB SmartCache.

7.1 Comparison on Domain

The domain on which all methods work is the domain of Li (2008) bounded below by , i.e.

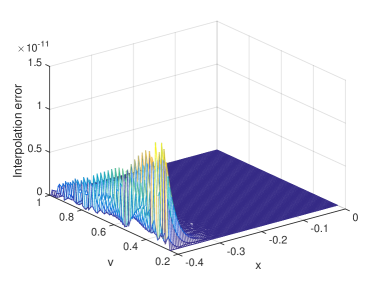

See Figure 7.1 for a comparison of the domain of Li (2008) and the domain of the Chebyshev method. On we compute normalized call prices on a -grid, where the distribution of the points is determined as in the numerical example of Section 3. We compare the runtimes and errors in the time-scaled volatilities and the repricing errors of the methods. Figure 7.2 illustrates the errors of the reference methods. Figure 7.3 displays the errors of the Chebyshev approach for three different pre-specified accuracies.

![[Uncaptioned image]](/html/1710.01797/assets/x12.png)

The Jäckel (2015) method comes with a solution close to machine precision for all input parameters and thus qualifies as our reference method in the offline-phase of the Chebyshev approximation. Also the Newton-Raphson algorithm reaches very high precision. The approximation of Li (2008), however, is not able to reach the same range of precision. As Table 7.1 shows, the mean error of is a factor even higher than Jäckel’s approximation. The proposed modification of Li (2008) with two additional Newton-Raphson steps reduces the error. However, for low volatilities the effect is rather small and the maximal error is still in the region of , see Table 7.1.

Figure 7.3 displays the interpolation error of the Chebyshev method for three different pre-specified accuracies. The error is of the same order for the whole interpolation domain, which shows that a pre-specified accuracy can be reached for all input parameters with the same complexity.

![[Uncaptioned image]](/html/1710.01797/assets/ComparisonDomain1.jpg)

![[Uncaptioned image]](/html/1710.01797/assets/ComparisonDomain1Cheb.jpg)

Table 7.1 shows the maximal and the mean error in terms of the time-scaled volatilities and the normalized call prices as well as the runtime as a proportion of the runtime of the Newton-Raphson method, which takes . For the Chebyshev method, the runtime measures the time of the online phase. When comparing the runtimes, the Li method is the fastest. It comes, however, with the lowest precision of a maximal error in of . For a higher precision in the range of , the Chebyshev method with low accuracy turns out to be faster than the improved Li method. Comparing the mean, the same holds for the Chebyshev method with medium accuracy. For very high precisions the Chebyshev method with high accuracy is faster than the Newton-Raphson approach. Compared to Jäckel’s method, the Chebyshev approach is two times faster but with a maximal error of instead of .

| Method | max | mean | max | mean | runtime |

|---|---|---|---|---|---|

| Jäckel | |||||

| Li | |||||

| Li with 2 steps of Newton-Raphson | |||||

| Newton-Raphson | |||||

| Chebyshev method (low accuracy) | |||||

| Chebyshev method (medium accuracy) | |||||

| Chebyshev method (high accuracy) |

7.2 Comparison on Domain

We compare the Chebyshev method on the large domain to the Newton-Raphson approach and the algorithm of Jäckel. The errors and runtimes on a grid, specified as in Section 7.1, are computed. Figure 7.4 and 7.5 illustrate the resulting errors of the reference methods and the Chebyshev approach. The observations of the error behaviour on the larger domain are consistent with that on the smaller domain , see Figure 7.2 and Figure 7.3.

![[Uncaptioned image]](/html/1710.01797/assets/ComparisonDomain2.jpg)

![[Uncaptioned image]](/html/1710.01797/assets/ComparisonDomain2Cheb.jpg)

Table 7.2 shows the maximal and the mean error as well as the runtimes scaled as in 7.1. Here, the Newton-Raphson method takes .

| Method | max | mean | max | mean | runtime |

|---|---|---|---|---|---|

| Jäckel | |||||

| Newton-Raphson | |||||

| Chebyshev method (low accuracy) | |||||

| Chebyshev method (medium accuracy) | |||||

| Chebyshev method (high accuracy) |

To reach a medium accuracy in the maximal error in the range of , the Chebyshev method is more than six times faster than the Newton-Raphson approach. Moreover, the Chebyshev method is able to reach higher accuracies of and still needs only of the runtime of Newton-Raphson. Jäckel’s method reaches very high precisions and is faster than Newton-Raphson. Compared the Jäckel method, the Chebyshev method allows us to pre-specify accuracies and reduce the runtimes significantly. For example, if accuracies in the region of are sufficient, the Chebyshev method is more than three times faster than Jäckel’s approach.

7.3 Comparison for market data

In Section 3.1 we investigated market data of options and concluded that a significant part of the options is not covered by the domain of Li (2008). This was the motivation to consider a much larger interpolation domain for the Chebyshev method. An empirical investigation confirms that all the options shown in Figure 3.2 lie within our domain.

Next, we compare the Chebyshev method on this market data to the Newton-Raphson approach and the algorithm of Jäckel. The errors and runtimes are computed for options on the S&P 500 index traded on 7/17/2017 (Source Thomson Reuters Eikon). We use the same options as for Figure 3.2. To obtain more reliable results for the runtime comparison we compute the implied volatilities of the options times.

Table 7.3 shows the maximal and the mean error as well as the runtimes scaled as in Section 7.1. Here, the Newton-Raphson method takes .

| Method | max | mean | max | mean | runtime |

|---|---|---|---|---|---|

| Jäckel | |||||

| Newton-Raphson | |||||

| Chebyshev method (low accuracy) | |||||

| Chebyshev method (medium accuracy) | |||||

| Chebyshev method (high accuracy) |

The results are similar to those of Section 7.2. The Chebyshev method is the fastest of the three methods and reaches the target accuracies. The method is about twice as fast as the Newton-Raphson approach for similar accuracies. Again, Jäckel’s method reaches very high precisions but it is significantly slower than the Chebyshev method.

Besides the observed gain in efficiency the Chebyshev method enjoys conceptual advantages. It delivers a closed-form approximation in a simple polynomial structure. The code is easy to implement and maintain. Moreover, the proposed approach can be applied to other problems of similar structure. The following section illustrates this flexibility.

8 Laplace implied volatility

Besides the Black-Scholes implied volatility there are several other models with implied volatilities. To overcome the problems of thin tails in the Black-Scholes model, Madan (2016) proposes the replacement of the density of the normal distribution with a Laplace density. This leads to a model with fatter tails without adding additional parameters. The stock price process in this model is defined by

| (8.1) |

where is distributed according to the time-dependent Laplace density

| (8.2) |

The call price in the model is given by

with

Madan (2016) shows that this model can be used for hedging purposes and outperforms classical delta hedging in the Black-Scholes model. Madan and Wang (2016) considered the application of the model to risk management. For both, hedging and risk management, it is necessary to have a fast and accurate formula for the Laplace implied volatility. To this end, we apply the bivariate Chebyshev method to implied volatilities based on the Laplace density.

As in the previous case, we normalize the call price by setting , and to

| (8.3) |

with

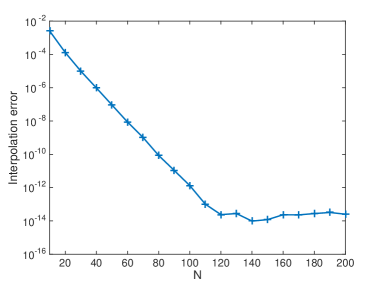

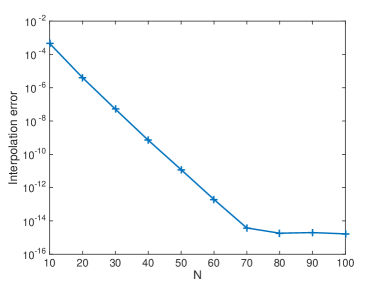

Similar to Section 2.1, we thus have reduced the approximation problem to a bivariate interpolation. For the domain , , we perform a bivariate Chebyshev interpolation of the Laplace implied volatility. At the interpolation nodes a Brent-Dekker algorithm is used to compute the implied volatilities. Figure 8.1 shows the exponential error decay of the interpolation on a -Chebyshev grid. The interpolation is already in the region of for . This shows the high potential of the method in the Laplace model, comparable to the numerical example in Section 3. In order to obtain high efficiency on a larger domain, one can establish a splitting procedure with appropriate scaling functions by exploiting the limit behaviour of the Laplace call price, in the spirit of Section 4.

9 Conclusion

We have introduced a new approximation method to compute the implied volatility. The backbone of the method is a bivariate Chebyshev interpolation. We have set up an interpolation domain, which is able to cover all relevant options based on observed market data. In order to achieve highest efficiency, we have split the domain into different interpolation areas with appropriate scaling functions. A theoretical error analysis shows subexponential convergence and a combination with low-rank techniques allows us to enhance the observed efficiency. Compared to other non-iterative approximation methods, the Chebyshev method is able to cover all relevant option data, including deep in and far out of the money options as well as low and high volatilities, see Figure 3.2 and Figure 7.1. Moreover, numerical experiments show that the Chebyshev method achieves considerably higher accuracies on the common domain . In comparison to the iterative method of Jäckel (2015), the Chebyshev method can reduce the runtimes significantly by pre-specifying the target accuracy. Besides the gain in efficiency, the Chebyshev method exhibits conceptual advantages:

-

•

Closed form bivariate approximation formula: The Chebyshev interpolations in all areas have the polynomial structure

(9.1) where and are the transformations on the respective area. This structure can be further explored to express derivatives in a simple form. For example the first derivative with respect to the call price is given by

We observe that the approximate derivative is again a function of and in polynomial structure. In particular, this avoids the computation of the implied volatility itself.

-

•

Easy Implementation: Once the interpolation operator is set up in an offline phase, the polynomial structure of the approximation formula 9.1 leads to simple code. This facilitates the transfer of the code to other systems and programming languages as part of the maintenance.

-

•

Adaptability: The efficiency of the Chebyshev method can be even further improved by incorporating additional knowledge. If the option data of interest lies in a domain smaller than , one can tailor the method to this domain by modifying the splitting.

The Chebyshev method enjoys high flexibility and the approach can be transferred to similar problems. We have illustrated this by approximating the Laplace implied volatility.

References

- Baumeister (2013) Baumeister, J. (2013). Inverse problems in finance. In Recent Developments in Computational Finance: Foundations, Algorithms and Applications, pp. 81–157. World Scientific.

- Black and Scholes (1973) Black, F. and M. Scholes (1973). The pricing of options and other liabilities. Journal of Political Economy 81, 637–654.

- Brenner and Subrahmanyan (1988) Brenner, M. and M. G. Subrahmanyan (1988). A simple formula to compute the implied standard deviation. Financial Analysts Journal 44(5), 80–83.

- Chambers and Nawalkha (2001) Chambers, D. R. and S. K. Nawalkha (2001). An improved approach to computing implied volatility. Financial Review 36(3), 89–100.

- Chance (1996) Chance, D. M. (1996). A generalized simple formula to compute the implied volatility. Financial Review 31(4), 859–867.

- Corrado and Miller (1996) Corrado, C. J. and T. W. Miller (1996). A note on a simple, accurate formula to compute implied standard deviations. Journal of Banking & Finance 20(3), 595–603.

- Delbourgo and Gregory (1985) Delbourgo, R. and J. A. Gregory (1985). Shape preserving piecewise rational interpolation. SIAM journal on scientific and statistical computing 6(4), 967–976.

- Fritzsche and Grauert (2012) Fritzsche, K. and H. Grauert (2012). From holomorphic functions to complex manifolds, Volume 213. Springer Science & Business Media.

- Gaß et al. (2015) Gaß, M., K. Glau, M. Mahlstedt, and M. Mair (2015). Chebyshev interpolation for parametric option pricing. arXiv preprint arXiv:1505.04648.

- Higham (2004) Higham, N. J. (2004). The numerical stability of barycentric lagrange interpolation. IMA Journal of Numerical Analysis 24(4), 547–556.

- Jäckel (2006) Jäckel, P. (2006). By implication. Wilmott 26, 60–66.

- Jäckel (2015) Jäckel, P. (2015). Let’s be rational. Wilmott 2015(75), 40–53.

- Li (2008) Li, M. (2008). Approximate inversion of the black–scholes formula using rational functions. European Journal of Operational Research 185(2), 743–759.

- Lorig et al. (2014) Lorig, M., S. Pagliarani, and A. Pascucci (2014). A taylor series approach to pricing and implied volatility for local-stochastic volatility models. The Journal of Risk 17(2), 3.

- Madan (2016) Madan, D. B. (2016). Adapted hedging. Annals of Finance 12(3-4), 305–334.

- Madan and Wang (2016) Madan, D. B. and K. Wang (2016). Laplacian risk management. Finance Research Letters.

- Manaster and Koehler (1982) Manaster, S. and G. Koehler (1982). The calculation of implied variances from the black-scholes model: A note. The Journal of Finance 37(1), 227–230.

- Merton (1973) Merton, R. C. (1973). Theory of rational option pricing. The Bell Journal of economics and management science, 141–183.

- Pistorius and Stolte (2012) Pistorius, M. and J. Stolte (2012). Fast computation of vanilla prices in time-changed models and implied volatilities using rational approximations. International Journal of Theoretical and Applied Finance 15(04), 1250031.

- Salazar Celis (2017) Salazar Celis, O. (2017). A parametrized barycentric approximation for inverse problems with application to the Black–Scholes formula. IMA Journal of Numerical Analysis.

- Sauter and Schwab (2010) Sauter, S. and C. Schwab (2010). Boundary Element Methods, Translated and expanded from the 2004 German original, Volume 39. Springer Series Computational Mathematics.

- Townsend and Trefethen (2013) Townsend, A. and L. N. Trefethen (2013). An extension of chebfun to two dimensions. SIAM Journal on Scientific Computing 35(6), C495–C518.

- Trefethen (2013) Trefethen, L. N. (2013). Approximation Theory and Approximation Practice. SIAM books.