A family of transformed copulas with singular component

Abstract

In this paper, we present a family of bivariate copulas by transforming a given copula function with two increasing functions, named as transformed copula. One distinctive characteristic of the transformed copula is its singular component along the main diagonal. Conditions guaranteeing the transformed function to be a copula function are provided, and several classes of the transformed copulas are given. The singular component along the main diagonal of the transformed copula is verified, and the tail dependence coefficients of the transformed copulas are obtained.

Finally, some properties of the transformed copula are discussed, such as the totally positive of order 2 and the concordance order.

Keywords: Transformed copula; Singular component; Tail dependence.

1 Introduction

A copula is a joint distribution function with all uniform [0, 1] marginal distributions. Copula functions have been received a great deal of attentions due to Sklar’s Theorem, providing a description of every joint distribution function about a random vector by its marginal distribution functions and its copula function. For more detailed introduction about copula theory, we refer to Joe (1997) and Nelsen (2006). Nowadays, copula functions play an important role for modeling the dependence structure in insurance, finance, risk management and econometrics (Denuit et al., 2005; McNeil et al., 2005).

As a distribution function, a copula can be written as the sum of an absolutely continuous component and a singular component (see, e.g., Ash, 2000, Theorem 2.2.6). Many popular copula functions, such as the Gaussian copula, the student’s copula and the Farlie-Gumbel-Morgenstern (FGM) copula, do not have singular component. However, the increasing importance and widespread applications of copulas have required to model the dependence structure by using copula functions with singular component. In the credit risk modelling, for modeling the dependence structure between the default times of the two credit entities, the copula function serves to describe the event that two entities default simultaneously, please refer to Sun et al. (2010), Mai and Scherer (2014) and Bo and Capponi (2015). In the engineering applications, for modeling the lifetimes of two components in the same system which is influenced by exogenous shocks, the corresponding lifetimes take the same value if a shock hits two components simultaneously (Navarro and Spizzichino, 2010; Navarro et al., 2013). The copula functions with the singular component along the main diagonal should be employed to model the dependence structure in the above applications.

Construction of copula functions with singular component is important for practical applications. The Marshall-Olkin copula is originated from exogenous shock models (Marshall and Olkin, 1967) having singular component. Durante et al. (2007) presented a generalization of the Archimedean family of bivariate copulas with a singular component along the main diagonal. Mai et al. (2016) provided a family of the copula functions interrelated with the set of exchangeable exogenous shock models, and the copula functions have singular components along the main diagonal. Xie et al. (2017) introduced a new family of the multivariate copula functions defined by two generators, which is a generalization of the multivariate Archimedean copula family with a singular component along the main diagonal.

In this paper, we consider a transformed function of a given copula with two functions and as the following:

| (1) |

where and . Our motivation is to construct new families of copulas by applying both the functions and the copula . Conditions on the functions and the copula are provided to guarantee that the transformation is a copula function, and the copula function is named as the transformed (TF) copula and as the base copula. We will show that the TF copula has the following properties:

(1). Singularization. If the base copula is absolutely continuous, the TF copula may have a singular component along the main diagonal to take into account the event that two entities default simultaneously.

(2). Modification of the tail dependence. The tail dependence of the base copula can be changed by choosing two different functions and .

(3). Preservation of some orders and properties. The TF copula preserves the common concordance order and the totally positive of order 2 (TP2) property of the base copula under some conditions.

(4). Inclusion of many known copula families. The family of TF copulas includes many known bivariate copulas, such as the copula functions presented in Durante et al. (2007), Mai et al. (2016) and Xie et al. (2017). The TF copula family can be regarded as a generalization of the above copula functions.

The rest of the paper is organized as follows. In Section 2, we provide sufficient conditions guaranteeing that is a copula function, and the existence of a singular component of the TF copula is verified. Several classes of TF copulas are also provided in Section 2. In Section 3, we discuss the tail dependence of the copula function , and the tail dependence relationship between the copula and the TF copula is provided. In Section 4, some properties of the TF copula, such as the TP2 and the concordance order, are discussed. Conclusions are drawn in Section 5. Some proofs are put in Appendix.

2 The family of transformed copulas

In this section, we first give some notations that will be useful for introducing the function defined by (1). The sufficient conditions are provided such that is a copula function, and a singular component of the TF copula is verified. Finally, several classes of TF copulas are provided.

2.1 Preliminaries

As a multivariate distribution, the copula function has all uniform [0,1] marginal distributions. In the two-dimensional case, there are three important copula functions, the product copula , the Fréchet upper bound and the Fréchet lower bound . It is known that for each bivariate copula ,

For details on copulas, please refer to Nelsen (2006).

Next we introduce the notion of supermigrative copula presented in Durante and Ricci (2012). A bivariate copula is called supermigrative if it is exchangeable and satisfies that

| (2) |

for all and with . If the inequality in (2) is strict whenever , is called strictly supermigrative.

The supermigrative was introduced firstly in the study of the bivariate ageing by Bassan and Spizzichino (2005). Supermigrative copulas are important for constructing stochastic models for the bivariate ageing (Durante and Ricci, 2012). Some common copulas are supermigrative. For instance, the product copula and the Fréchet upper bound are supermigrative. The Cuadras-Augé bivariate copula ( Cuadras and Augé, 1981)

| (3) |

with parameter is supermigrative. Furthermore, some popular copulas are also supermigrative under certain conditions. An Archimedean copula with generator is defined as

| (4) |

where the generator is a continuous and strictly decreasing convex function satisfying . The Archimedean copula is supermigrative if and only if the inverse function of is log-convex and . A bivariate FGM copula

| (5) |

is supermigrative if and only if the parameter . A bivariate Gaussian copula with correlation index parameter is supermigrative if and only if .

Let be a continuous and strictly increasing function with . When , the function is a distortion function (see, e.g., Yaari, 1987), which is widely used in risk management. The pseudo-inverse of is defined by

It is easy to see that the function is increasing in [0,1] and strictly increasing in . Specially, if , then the pseudo-inverse function coincides with the inverse function, that is, .

From the definition of the pseudo-inverse , we can see that for all ,

| (6) |

and

| (7) |

Finally, we introduce some notations. Denote

and

Notice that .

2.2 Definition of the TF copula

Given a base copula and a pair of functions , the transformed function is defined by (1). From the definition of , we can see that the copula and the two functions and are three essential elements of the function . In the next, we will prove that under some assumptions, the function is a copula function.

First we give some preliminary lemmas.

Lemma 2.1.

(Marshall and Olkin, 1979, Proposition 4.B.2) Let , where is an interval of . If is convex and increasing, then, for each , , , such that

and , we have

Lemma 2.2.

(Stewart, 2003, Page 290) Let . If is a concave function, then is convex in [0,1].

In the following, we will provide sufficient conditions on the functions , and the copula such that the function of type (1) is a bivariate copula.

Theorem 2.1.

Let be an arbitrary bivariate copula. Assume that and is a concave function. If the inequality

| (8) |

holds for all , then the function of type (1) is a bivariate copula. Specially, if is supermigrative and is increasing in [0,1], then is a copula function.

Proof.

(1). First we prove that when (8) holds, is a copula function.

For each ,

and

Similarly, for each ,

Now, it suffices to prove that is 2-increasing, i.e., for every subset in the unit square,

| (9) |

where

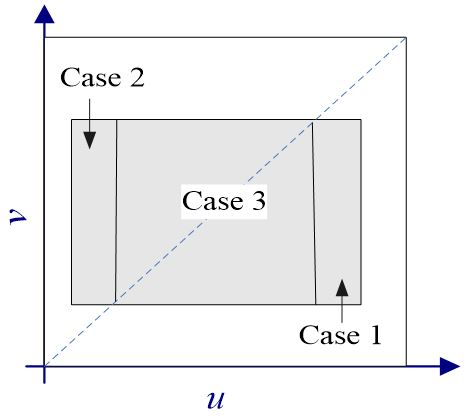

In order to show (9), we will focus on the following three special cases which are illustrated in Figure 1:

-

•

Case 1: is a rectangle contained in the triangular region entirely.

-

•

Case 2: is a rectangle contained in the triangular region entirely.

-

•

Case 3: The diagonal of lies on the diagonal of the unit square.

Note that each rectangle in can be decomposed as the union of at most three non-intersect sub-rectangles of the above cases. Furthermore, is the sum of the values . Hence, we can verify that is 2-increasing if is 2-increasing in the above three cases.

In the next, we only need to prove that is 2-increasing in the above three cases. Since is exchangeable, then the arguments of the first two cases are similar. We only prove that is 2-increasing in Case 1 and Case 3.

-

•

Case 1. Since and are increasing in [0,1], then and for . In this case,

Since the copula function is increasing in every variable, then follows. Furthermore, using the fact that is a bivariate copula and consequently is 2-increasing, we have that . Now, noting that is concave in [0,1], from Lemma 2.2, we know that is convex in [0,1]. Then applying Lemma 2.1 to the function , we can get (9).

- •

(2). Now we assume that is a supermigrative copula and is increasing in [0,1]. In order to prove that is a bivariate copula, we only need to show that under the assumptions, holds for all , .

Since and is increasing in [0,1], then for all , , thus follows. Then for all , ,

where the first inequality holds because is increasing in [0,1] and is increasing in every variable, the second inequality follows from (2), and the last equation holds because is exchangeable by its supermigrative property. Thus (8) holds and is a copula function. ∎

Remark 2.1.

One advantage of the TF copula is that the copula family includes many known bivariate copulas. Letting the base copula is exchangeable and , then the TF copula coincides with the copula given by

| (11) |

Please see Genest and Rivest (2001), Klement et al. (2005), Morillas (2005), Alvoni et al. (2009) and Durante et al. (2010) for the detailed discussion on the copula . The Archimedean copula with multiplicative generator is also a special case of (11) with .

The Cuadras-Augé copula is a special TF copula where the base copula is the product copula and . In particular, let the base copula be the product copula , then the TF-product copula is simplified as

| (12) |

Note that the function coincides with the generalization of Archimedean copula introduced by Durante et al. (2007).

Remark 2.2.

When for all , using , for , we have

Given a bivariate copula , we denote

and let be the family of all functions such that is a copula. From Theorem 2.1, we know that if and is concave, then . In the following, some properties of and the relationships between and are presented, which will allow us to find more generators from such that is a copula.

Proposition 2.1.

Let be a bivariate copula. The following statements hold:

(1). If and , then . Furthermore, if is concave in [0,1], then .

(2). If and , then . Furthermore, if is concave in [0,1], then .

(3). If and , then . Furthermore, if is concave in [0,1], then .

Proof.

(1). From the assumption that , we know that is a strictly increasing function in [0,1] satisfying . Then for and . Since , then for all , , it holds that

Thus . Furthermore, if is concave in [0,1], then the assumptions of Theorem 2.1 are satisfied such that .

(2). From the assumptions that and , we easily know that is a continuous and strictly increasing function in [0,1] satisfying such that . From the assumptions, we also know that for all , and .

Then for all , , it holds that

Hence . Furthermore, when is concave in [0,1], the assumptions of Theorem 2.1 are satisfied, thus .

(3). It can be proved similarly as in (2). ∎

2.3 A singular component of the TF copula

In this section, it is verified that the TF copula may have a singular component even if the base copula is absolutely continuous. It is interesting to note that, if is absolutely continuous, then the TF copula has both singular and absolutely continuous components under some conditions. A singular component of the TF copula can be identified as in the following theorem.

Theorem 2.2.

Let be a copula function with second order continuous derivatives, , and be differentiable in [0,1] and be a concave function. Denote

and

where and . Let .

(1). If , then the singular set of contains .

(2). If and , then the singular component of the copula is concentrated on the main diagonal . Moreover, for the random variables and with the joint distribution , we have

| (13) |

where and are the singular component and the absolutely continuous component of respectively, i.e.,

| (14) |

Proof.

(1). From the definitions of the copula and the pseudo-inverse , we have that for all , . Hence we only need to focus on the set .

Fix . If , then . Since , from Eq.(7), we get

From the assumptions that the copula function has second order continuous derivatives and is differentiable, then differentiating the above equation with respect to yields

Similarly, for ,

Note that in . Hence,

| (15) |

Notice also that . Therefore, for a fixed ,

and from (15) we know that the equality holds only if .

Summarizing the above facts, we know that if , then has jump discontinuity in . Hence, in view of Theorem 1.1 of Joe (1997), we conclude that the singular set of the copula contains .

(2). If , then . From (1) we get

From the assumptions that and , are differentiable in [0,1], we know that is differentiable and strictly increasing in [0,1]. Also, since the copula function has second order continuous derivatives, then we easily know that is absolutely continuous in .

Note that is concentrated on the main diagonal. Thus, if , then from the above analysis, we conclude that is absolutely continuous in and its singular component is concentrated on the main diagonal.

Remark 2.3.

In Theorem 2.2, the condition is dependent on the base copula . Note that the condition can be simplified if the base copula is exchangeable. Suppose that is exchangeable and , where is also exchangeable and satisfies that in . Then when is strictly increasing in [0,1], we can prove that and contains a singular component along the main diagonal. The proof will be given in Appendix.

As an example, choosing an Archimedean copula with additive generator as the base copula, then and if the function is strictly increasing in , the copula contains a singular component along the main diagonal. Furthermore, letting the base copula being the product copula and , the condition can be simplified as that is strictly increasing in .

2.4 Some classes of TF copulas

Besides including many important families of bivariate copulas, the TF copula of type (1) is of importance since such transformation allows us to construct new families of copulas with singular components along the main diagonal.

In the following, we consider TF copulas by choosing the FGM copula, the Cuadras-Augé copula and the Archimedean copula as the base copula respectively. It is well-known that the FGM copula is absolutely continuous and it has a polynomial form, thus we choose the FGM copula as the first example. For comparison purpose, in the second example we choose the Cuadras-Augé copula as the base copula, because it has a singular component along the main diagonal. Since the Archimedean copula is an important family of copulas in many areas, we take the Archimedean copula as the third example.

Example 2.1.

(TF-FGM copula) The FGM copula of type (5) is supermigrative when . If and is a concave function such that is increasing in [0,1], then from Theorem 2.1, we know that

| (16) |

is a bivariate copula.

Let and , where . In this case, , is a concave function and is increasing in [0,1]. Then (16) can be written as

| (17) |

Setting , in (17), then

Define , . Since for all and , then is an increasing function in [0,1]. Furthermore, it is easy to see that and . Thus we can get that for all . From Theorem 2.2, we know that the TF-FGM copula contains a singular component along the main diagonal. Also, from the double integral in (14) for the TF-FGM copula, we get

and

Hence, we have

and consequently

Furthermore,

where and are the uniform [0,1] random variables following the joint distribution function (17) with and .

In the following example, we choose the Cuadras-Augé copula as the base copula. It is known that the Cuadras-Augé copula also has a singular component along the main diagonal.

Example 2.2.

(TF-Cuadras-Augé copula) Recall that the Cuadras-Augé copula of type (3) is supermigrative. Let and , , where . In this case, , is a concave function and is increasing in [0,1]. Thus

| (18) |

is a copula function. Setting in (18), we have

and consequently

For having the copula (18) with and having the Cuadras-Augé copula , we have

and

Then

Hence, the value of for the copula of type (18) with is larger than for the Cuadras-Augé copula. It shows that the transformation (1) enlarges the singular component along the main diagonal of the Cuadras-Augé copula.

In the next example, we choose the Archimedean copula as the base copula.

Example 2.3.

(TF-Archimedean copula) Let the base copula be an Archimedean copula of type (4) with generator and . Then

From Lemma 3.7 in Morillas (2005), we can know that . Then can be simplified as

| (19) |

From Theorem 2.1, we know that when is concave and the function is decreasing in [0,1], then the function of type (19) is a copula.

2.5 Numerical illustration

For understanding the singular component of the TF copula , in the following we will give the scatter plots for some TF-Archimedean copulas.

Letting the base copula be an Archimedean copula with generator , then the TF-Archimedean copula has simple form (19). The Clayton copula, the Gumbel copula and the Frank copula are three important classes of copulas in the Archimedean family and their generators can be expressed as , and respectively. We choose three base copulas, which are the Clayton copula with parameter , the Gumbel copula with parameter and the Frank copula with parameter for numerical illustrations.

In order to get a comparison result, we choose four pairs of functions : (a) ; (b) ; (c) ; (d) . It is easy to verify that for every Archimedean generator mentioned above, is concave and is decreasing in all the four cases described above. Then the assumption (8) holds such that is a bivariate copula in each case. Note that for every TF-Archimedean copula described above, and in case (a) and case (b). Then, all the three classes of TF-Archimedean copulas contain a singular component along the main diagonal in case (a) and case (b). Since in case (c), we know that the TF copula coincides with the copula of type (11) in this case. In case (d), . Since the Archimedean copula is exchangeable, then such that in case (c) and case (d). Thus, all the three classes of TF-Archimedean copulas are absolutely continuous and should not contain a singular component along the main diagonal in both case (c) and case (d).

We generate 10,000 samples of the TF-Calyton copula, the TF-Gumbel copula and the TF-Frank copula and illustrate them in Figures 2-4, respectively. We also calculate the values of Kendall’s as well as Spearman’s and the results are shown below.

(). The base copula is a Clayton copula with parameter : (a) =0.6226, =0.7712; (b) =0.5220, =0.6848; (c) =0.3313, =0.4756; (d) =0.5023, =0.6839.

(). The base copula is a Gumbel copula with parameter : (a) =0.8734, =0.9608; (b) =0.8017, =0.9273; (c) =0.6677, =0.8499; (d) =0.6575, =0.8399.

(). The base copula is a Frank copula with parameter : (a) =0.5768, =0.7359; (b) =0.4828, =0.6469; (c) =0.3297, =0.4787; (d) =0.3859, =0.5548.

From the scatter plots presented in Figures 2-4, we find that there are straight lines in both case (a) and case (b) of all the three pictures, which are the singular components along the main diagonal of the corresponding copulas. It can also be seen that all cases (c) and (d) of the three base copulas do not contain a singular component. By Theorem 2.2, these results are conceivable since equals for (a),(b) and for (c),(d). For every TF-Archimedean copula described above, it is also observable that the values of Kendall’s as well as Spearman’s in case (a) and case (b) are greater than those in (c) and (d) when the base copula is the same. Thus the rank correlations are enhanced when the copula is transformed by (1).

3 Tail dependence coefficient of the TF copula

Copulas with different tail dependence are usually required for modelling the extreme events (McNeil et al., 2005; Salvadori et al., 2007). Tail dependence coefficient was proposed for studying the tail dependence of copula functions (Nelsen, 2006; McNeil et al., 2005). For a copula function , its upper and lower tail dependence coefficients and , respectively, are defined by

| (20) |

| (21) |

given that the above limits exist. The upper and lower tail dependence coefficients and have been shown to be of importance in the study of the tail dependence (Nelsen, 2006). We say that has upper tail dependence if , otherwise we say that has no upper tail dependence; similarly for .

In the following proposition, we give the tail dependence relationship between the base copula and its TF copula .

Proposition 3.1.

Let be a bivariate copula, and be a concave function.

(a). Suppose that exists and it is finite, and for some ,

(1). If , then

| (22) |

(2). If and , then

| (23) |

(b). Suppose that exists and it is finite, and for some ,

(1). If , then

| (24) |

(2). If and , then .

Proof.

(a). Since is a continuous and strictly increasing function satisfying , then for . Thus, we have

| (25) | |||||

given that the above limit exists. In order to derive , we need to calculate and

respectively if the limits exist.

We first calculate the limit . From (20) and the assumptions that exists and it is finite, we know that

| (26) |

thus

| (27) |

follows. On the other hand, from the assumption that , we know . Since the functions and are continuous in [0,1] with , we have . Thus we get

| (28) |

Combining (27) and (28) we conclude that

| (29) |

In the following, we will calculate the limit

under two different conditions.

(1). We first consider the case , i.e., . In this case, we will apply Sandwich Theorem to calculate the limit . Since is increasing in every variable and for all , we get

| (30) |

such that

| (31) |

Now, we calculate the limit of the left side in the inequality (31). Since , from (26) we have

Based on the above result and the assumption that , we derive

Then, letting and applying Sandwich Theorem to the inequality (31), we get . Substituting this result and (29) into (25), we can obtain (22).

(2). Now we consider the case , . For a copula function , we define

| (32) |

Note that

| (33) |

Combining (26) and (32), we have

Thus

| (34) |

follows.

Next we calculate the limit . Note that

| (35) | |||||

where the second equality follows from the definition of given in (32). Then, in order to get the limit (35), we need to calculate , and respectively if the limits exist.

From the assumptions, we know that . Since and , from (34) we get

| (36) |

In the next, we apply Sandwich Theorem to calculate the limit . From the assumption , the inequality (8) holds. Then, from Remark 2.2, we know that for all . Thus, from (33) it is easy to verify that

Also, notice that for all . Then, for we have

| (37) |

From (36), we know that when , the limit of the right side in the inequality (37) equals 0. Thus from (37) we get . Substituting the above results into (35), we obtain

| (38) |

Then substituting (38) into (25), we can get (23).

(b). If on for a small , it is easy to see that .

From the assumption , we can get and .

Thus from (21), we have

Then holds in case (1) and case (2).

Next we assume that for all . Then we have

| (39) |

Next we calculate and

respectively.

We first calculate the limit . From the assumption , we know that . Since , we have . Thus we get

| (40) |

In the next, we also apply Sandwich Theorem to calculate the limit . Dividing each part of the inequality (30) by , we get

| (41) |

Note that from the assumption , we know that in the case . From (21) we have

| (42) |

(1). We first consider the case . Note that the limit of the left side in the inequality (41) is given in (42) and is . From (42) and the assumption that , we also derive

Thus, letting and applying Sandwich Theorem to the inequality (41), we get

Substituting this result and (40) into (39), we can derive the formula (24).

(2). The result in the case , can be calculated similarly and we omit the proof.

The proposition is proved. ∎

Example 3.1.

(Tail dependence coefficient of the TF-FGM copula) Consider the TF-FGM copula defined by (16) with . Note that the FGM copula has no tail dependence, i.e., .

(a). Assume that and , , where . It is easy to see that functions and satisfy the assumptions of Theorem 2.1, Proposition 3.1(a-2) and Proposition 3.1(b-2). In this case, the upper tail dependence coefficient of the TF-FGM copula defined in (16) equals to .

Remark 3.1.

(1) Eqs (22)-(24) show the influence of the transformation on the tail dependence coefficient of the base copula . We can see that the TF copula can have upper tail dependence even though the base copula has no upper tail dependence.

(2) In Proposition 3.1(b), the results on the lower tail dependence coefficients of TF copulas, are only given in the case or the case , . In such cases, the lower tail dependence coefficient is related to only. For the other cases, the result is complicated. For instance, choosing the FGM copula of type (5) as the base copula and letting , , , it is easy to see that the assumptions of Theorem 2.1 are satisfied and thus is a copula. Also, notice that for all and . By direct calculation, we get the lower tail dependence coefficient which is related to .

Next we discuss the special case . The TF-product copula has been given in (12) and it has multiplicative generators. In the following, we discuss its tail dependence coefficient.

Let be a continuous and strictly decreasing function such that , be a continuous and non-increasing function satisfying that and is increasing in [0,1]. Furthermore, let be concave. Setting and , we have , is concave and is increasing in [0,1]. Then, we get an additive form of the TF-product copula with additive generators and presented as

| (43) |

Since the product copula has no tail dependence, applying Proposition 3.1 we can get the tail dependence coefficient of the TF-product copula.

Corollary 3.1.

Let be a copula of type (43) generated by the pair .

(1). If for some ,

then .

(2). If for some ,

then .

4 Properties of TF copulas

This section aims at investigating some properties of the TF copula , including the totally positive of order 2 (TP2) and the concordance order. More precisely, we study how the properties are preserved under the transformation defined by (1).

4.1 The TP2 property

Following the definition of Lehmann (1966), given intervals and in , a function is said to be TP2 if, for all , , , such that , ,

For the TP2 property of the copula, please see Nelsen (2006). The TP2 has been widely studied and used, such as in the multivariate analysis, the reliability theory and the statistical decision procedure. See for example, Lai and Balakrishnan (2009), Olkin and Liu (2003) and the references therein.

In this subsection, we study how the TP2 property of the basic copula can be transformed to its TF copula. In other words, starting with a base copula satisfying the property of TP2, we would like to investigate the conditions on the functions and such that the TF copula of type (1) also satisfies the TP2 property. Preliminarily, we need the following lemma.

Lemma 4.1.

(Durante et al., 2010, Lemma 3.1) Let the function be increasing in every variable. If satisfies the TP2 property, then it is 2-increasing.

Then we have the following proposition.

Proposition 4.1.

Let be a TP2 copula and . If is log-convex, then is also a TP2 copula.

Proof.

In order to verify that is TP2, we firstly prove that is 2-increasing. Suppose that the rectangle is a subset of the unit square. Define

Then Note that each rectangle can be decomposed as the union of at most three non-intersect sub-rectangles described in Figure 1. Furthermore, is the sum of the values . Thus, we can verify that is 2-increasing if is 2-increasing in the three cases described in Figure 1. We only prove that is 2-increasing in Case 3, i.e., , and , since the other two cases can be proved in a similar way.

In Case 3, , , . Since , are increasing in [0,1] and is increasing in every variable, it follows that

| (44) |

From the assumption that is TP2, we have . Since , then the inequality (8) holds such that . Combining the above inequalities, we know and applying the function to this inequality, we get

| (45) |

Also, from the assumption that is log-convex, we know is convex in . Therefore, from inequalities (44) and (45) and applying Lemma 2.1 to the function , we obtain

| (46) |

This shows that is 2-increasing. From the inequality (46), we also get

for arbitrary rectangle contained in the unit square. Hence, is a TP2 function.

Corollary 4.1.

Let and be a TP2 copula.

(1). If is supermigrative, is increasing in [0,1] and is log-convex, then is a TP2 copula.

(2). Let for . If the assumption (8) holds, then is a TP2 copula.

Proof.

From the definition (2) of the supermigrative copula, using Theorem 2.1 and Proposition 4.1, we get the first part of the corollary.

Note that every power function , , has the properties that is also a power function and is log-convex. Then, we get the second part of the corollary. ∎

These results allow us to construct the TP2 multiple parameters’ copula family from a known TP2 copula. In the following, we give two examples discussed in the previous sections.

Example 4.1.

Example 4.2.

Let the base copula be a member of the Cuadras-Augé family. Then is TP2 for all . Assume that and for all , where . Then, the TF copula of type (18) also defines a family of TP2 copulas.

4.2 Concordance order

We first give the definition of the concordance order between two copulas. Given two copulas and , if for any , then is said to more concordant than , denoted by (see Joe, 1997, for more details). In the following proposition, we discuss the concordance order of TF copulas.

Proposition 4.2.

(1). Let and be two bivariate copulas, and be concave in [0,1]. If , then . Conversely, if , then on | , .

(2). Let be a bivariate copula, and be concave in [0,1]. Then if and only if for all .

(3). Let be a bivariate copula, and , be concave in [0,1]. Then if and only if for all , where .

Proof.

We only prove (3). The proofs of (1) and (2) are similar.

From the definition of given in (1), we can know that if and only if

| (47) |

Let and . From the assumption , we know for all , . Then, from Remark 2.2, we have , , such that . Hence, the inequality (47) is equivalent to that for all . Furthermore, if , then . Therefore, if and only if

| (48) |

We start by proving the necessity. Assume that . Then (48) follows. Applying to the both sides of (48) and noting that is non-decreasing in [0,1] as well as for all , it yields that

for all .

Next we prove the sufficiency. If and satisfy , , then applying to the both sides of this inequality and noting that is non-decreasing in and , it yields that (48) holds, i.e., .

This completes the proof. ∎

5 Conclusions

In this paper, we presented a family of bivariate copulas by transforming a given copula function with two increasing functions, named as transformed copula. Conditions guaranteeing that the transformed function is a copula function are provided, and several classes of transformed copulas are given. A singular component along the main diagonal of the transformed copula is verified, and the tail dependence coefficients of the transformed copulas are obtained. The transformed copula preserve some orders and properties of the base copula , such as the TP2 property and the concordance order.

Acknowledgement

Xie’s research was supported by the National Natural Science Foundation of China (Grants No. 11561047). Yang’s research was supported by the National Natural Science Foundation of China (Grants No. 11671021, Grants No. 11271033).

Appendix A Proof of Remark 2.3

When is exchangeable, . Also, if is exchangeable, then . Furthermore, if is strictly increasing in , we know that for all .

Summarizing the above results, we conclude that for all ,

i.e., . From Theorem 2.2, we know that contains a singular components along the main diagonal.

References

- Alvoni et al. (2009) Alvoni, E., Papini, P.L., and Spizzichino, F. (2009). On a class of transformations of copulas and quasi-copulas. Fuzzy Sets and Systems, 160:334-343.

- Ash (2000) Ash, R.B., (2000). Probability and measure theory, 2nd edition. Harcourt/Academic Press, Burlington, Massachusetts.

- Bassan and Spizzichino (2005) Bassan, B., and Spizzichino, F. (2005). Relations among univariate aging, bivariate aging and dependence for exchangeable lifetimes. Journal of Multivariate Analysis, 93:313-339.

- Bo and Capponi (2015) Bo, L., and Capponi, A. (2015). Counterparty risk for CDS: default clustering effects. Journal of Banking and Finance, 52:29-42.

- Cuadras and Auge (1981) Cuadras, C.M., and Augé, J. (1981). A continuous general multivariate distribution and its properties. Communications in Statistics: Theory and Methods, 10:339-353.

- Denuit et al. (2005) Denuit M., Dhaene J., Goovaerts M., and Kaas R. (2005). Actuarial Theory for Dependent Risks: Measures, Orders and Models. John Wiley and Sons Ltd, Chichester.

- Durante et al. (2010) Durante, F., Foschi, R., and Sarkoci, P. (2010). Distorted copulas: constructions and tail dependence. Communications in Statistics: Theory and Methods, 39:2288-2301.

- Durante et al. (2007) Durante F., Quesada-Molina J.J., and Sempi C. (2007). A generalization of the Archimedean class of bivariate copulas. Annals of the Institute of Statistical Mathematics, 59:487-498.

- Durante and Ricci (2012) Durante, F, and Ricci, R.G. (2012). Supermigrative copulas and positive dependence. ASTA Advances in Statistical Analysis, 96:327-342.

- Genest and Rivest (2001) Genest, C., and Rivest, L.P. (2001). On the multivariate probability integral transformation. Statistics and Probability Letters, 53:391-399.

- Joe (1997) Joe, H. (1997). Multivariate Models and Dependence Concepts. Chapman & Hall, Boca Raton.

- Klement et al. (2005) Klement, E.P., Mesiar, R., and Pap, E. (2005). Transformations of copulas. Kybernetika, 41:425-434.

- Lai and Balakrishnan (2009) Lai, C.D., and Balakrishnan, N. (2009). Continuous Bivariate Distributions. Springer, New York.

- Lehmann (1966) Lehmann, E.L. (1966). Some concepts of dependence. Annals of Mathematical Statistics, 37(5):1137-1153.

- Mai and Scherer (2014) Mai, J. F., and Scherer, M. (2014). Simulating from the Copula that generates the maximal probability for a joint default under given (inhomogeneous) marginals. Topics in Statistical Simulation. Springer, New York, 333-341.

- Mai et al. (2016) Mai, J. F., Schenk, S., and Scherer, M. (2016). Exchangeable exogenous shock models. Bernoulli, 22:1278-1299.

- Marshall and Olkin (1967) Marshall, A. W., and Olkin, I. (1967). A multivariate exponential distribution. Journal of the American Statistical Association, 62:30-44.

- Marshall and Olkin (1979) Marshall, A. W., and Olkin, I. (1979). Inequalities: theory of majorization and its application, volume 143 of Mathematics in Science and Engineering. Academic Press Inc., New York.

- McNeil et al. (2005) McNeil A.J., Frey R., and Embrechts P. (2005). Quantitative Risk Management. Princeton University Press,Princeton.

- Morillas (2005) Morillas, P. M. (2005). A method to obtain new copulas from a given one. Metrika, 61:169-184.

- Navarro et al. (2013) Navarro, J., Águila, Y.D., Sordo, M.A., and Suárez-Llorens, A. (2013). Stochastic ordering properties for systems with dependent identically distributed components. Applied Stochastic Models in Business and Industry, 29:264-278.

- Navarro and Spizzichino (2010) Navarro, J., and Spizzichino, F. (2010). Comparisons of series and parallel systems with components sharing the same copula. Applied Stochastic Models in Business and Industry, 26:775-791.

- Nelsen (2006) Nelsen, R. B. (2006). An introduction to copulas, 2nd edition. Springer Series in Statistics. Springer, New York.

- Olkin and Liu (2003) Olkin, I., and Liu, R. (2003). A bivariate beta distribution. Statistics and Probability Letters, 62(4):407-412.

- Salvadori et al. (2007) Salvadori, G., De Michele, C., Kottegoda, N.T., and Rosso, R. (2007). Extremes in Nature. An Approach Using Copulas, volume 56 of Water Science and Technology Library. Springer, New York.

- Stewart (2003) Stewart, J. (2003). Calculus: early transcendentals, 6th edition. Thomson Learing, Inc., California.

- Sun et al. (2010) Sun, Y., Mendoza-Arriaga, R., and Linetsky, V. (2010). Marshall-Olkin, distributions, subordinators, efficient simulation, and applications to credit risk. Social Science Electronic Publishing, 58(1):61-3.

- Xie et al. (2017) Xie, J. H., Lin, F., and Yang, J. P. (2017). On a generalization of Archimedean copula family. Statistics and Probability Letters, 125:121-129.

- Yaari (1987) Yaari, M.E. (1987). The dual theory of choice under risk. Econometrica, 55(1):95-115.