Estimation of Graphical Models using the Norm

Abstract

Gaussian graphical models are recently used in economics to obtain networks of dependence among agents. A widely-used estimator is the Graphical Lasso (GLASSO), which amounts to a maximum likelihood estimation regularized using the matrix norm on the precision matrix . The norm is a lasso penalty that controls for sparsity, or the number of zeros in . We propose a new estimator called Structured Graphical Lasso (SGLASSO) that uses the mixed norm. The use of the penalty controls for the structure of the sparsity in . We show that when the network size is fixed, SGLASSO is asymptotically equivalent to an infeasible GLASSO problem which prioritizes the sparsity-recovery of high-degree nodes. Monte Carlo simulation shows that SGLASSO outperforms GLASSO in terms of estimating the overall precision matrix and in terms of estimating the structure of the graphical model. In an empirical illustration using a classic firms’ investment dataset, we obtain a network of firms’ dependence that exhibits the core-periphery structure, with General Motors, General Electric and U.S. Steel forming the core group of firms.

JEL classification: C55, C10.

keywords:

Gaussian graphical models; Glasso; Inverse covariance matrices; Lasso; Precision matrices; Sparsity.1 Introduction

The Gaussian graphical model is a graph summarizing the conditional independence relationships among a group of random variables. Suppose that is distributed with . If the -th entry of the precision matrix is zero, i.e., , then it is known that and are independent conditional on all other , (e.g., Chapter 9 of Hastie et al. (2015)). The Gaussian graphical model is then obtained by identifying the zeros of the precision matrix, and letting nodes and be linked if and only if the -th entry of is non-zero.

In our empirical illustration, the variables represent the annual investment or the residuals of investment equations of the number of firms: . If two firms and are not linked in this graphical model, it means that the investment decisions of firms and are independent of each other, conditional on all other firms , . Hence the investment decisions of firms and do not directly affect each other. On the other hand, if two firms and are linked in the graphical model, then the investments of firms and have direct effects on each other, without the mediation of other firms. In recent applications in economics, for instance, Giudici and Spelta (2016) uses graphical modeling to obtain the network of international financial flows.

It is well known that the inverse of the standard sample covariance estimator, performs poorly particularly in recovering the underlying graphical structure. The reason is that the sample precision matrix produces a dense matrix without any zeros, and hence the resulting graphical model is always a complete network where all nodes are linked to all other nodes.

A widely-used technique to estimate graphical models is called Graphical Lasso (GLASSO), which aims to estimate the precision matrix while imposing a sparsity constraint on . For an overview of this topic, see Hastie et al. (2015); Cai et al. (2016); Fan et al. (2016). In this paper, we propose an estimation method for graphical models, which works by estimating the precision matrix, , taking into account the structure of sparsity in .

The standard GLASSO approach estimates the precision matrices while controlling for the sparsity of , i.e. the number of zeros in . However it does not consider when these zeros could be distributed in a certain pattern or structure in . For instance, in many economic applications it is reasonable to think that in the graphical model, some nodes have very few links, while some hub-like nodes have many links to other nodes. Such settings are common in economic applications: for instance, we commonly observe the so-called small-world properties in social and economic networks (Jackson (2008)).

The main feature of our estimation method is to use the -norm penalty, which corresponds to the second moment of the weighted degree of nodes, i.e. , for . Notice that Lasso uses the -norm penalty, which is proportional to the first moment of the weighted degree distribution. We derive the asymptotic distribution of the new estimator, called Structured Graphical Lasso (SGLASSO) when the sample size and the dimension of , , is fixed.

The main theoretical finding is that when the network size is fixed, SGLASSO is asymptotically equivalent to an infeasible GLASSO problem which penalizes an entry of proportionally according to the influence of the entry, where the influence of an -th entry is defined as the sum of the true weighted degrees of nodes and in the graphical model. Specifically, SGLASSO is asymptotically equivalent to a modified GLASSO where the element-by-element penalty factor for the -th entry of is proportional to , where is the true weighted degree of node . Note that is unknown to us, and hence it is infeasible to be implemented as a GLASSO estimator.

By means of Monte Carlo simulations, we demonstrate that SGLASSO performs better than GLASSO in finite samples. In terms of estimating the overall precision matrix, SGLASSO achieves lower Kullback-Leibler and Frobenius losses. Moreover, in terms of recovering the structure of the graphical model, we also show that SGLASSO outperforms GLASSO.

Overall, we should use the norm in cases where we are more interested in the relationships among influential nodes. For instance, in a financial network that exhibits a core-periphery structure, we are more interested in the relationships between the major core banks, and less interested in the relationships between the minor peripheral banks. Knowing how shocks cascades and propagates among influential banks is key to understanding financial contagion (Elliott et al. (2014)).

However if we were to remain completely agnostic about the empirical context, there are still reasons for using the norm. Here, the virtue of the norm is that it allows us to express lasso penalties that scale automatically according to degree influences (this insight is due to our main theoretical result). In practice, when we use the norm in conjunction with the norm, we are allowing for lasso penalties that have a constant factor and an increasing factor over the nodes’ degrees. This can only improve fit. The analogy is that the norm is a linear first-order lasso penalty, and the norm is a quadratic lasso penalty. Moreover, our simulation shows that using just the norm can achieve significant improvements over the norm. This suggests that it is important to allow for lasso penalties that scale according to nodes’ degrees, and not restricted to a constant lasso penalty.

The paper is organized as follows. Section 2 introduces the model, the -norm penalty, and a motivating example. Section 3 presents the theoretical results. Section 4 provides a brief summary of the Monte Carlo simulation results. The full simulation results are available in the Supplemental Information. Section 5 contains an empirical illustration. The Appendix contains technical proofs and derivations.

1.1 Related literature

This paper is related to literature of estimating high-dimensional inverse covariance matrices. In addition to the aforementioned surveys, one can refer to Banerjee et al. (2008); Friedman et al. (2008); Yuan and Lin (2007); Rothman et al. (2008); Ravikumar et al. (2011).

A different class of procedure frames the estimation of graphical models as nodewise or pairwise regressions, where the Lasso or Dantzig selector can then be used to achieve variable selection and high-dimensional regularization. The relevant papers belonging to this class are Cai et al. (2011, 2016); Meinshausen and Bühlmann (2006); Peng et al. (2012); Ren et al. (2015). For ultra high-dimensional Gaussian graphical models, a recent approach is the Innovated Scalable Efficient Estimation proposed by Fan and Lv (2016).

Lam and Fan (2009) study a general class of estimators that nests the GLASSO. In particular, they consider , where is a penalty function that depends on a regularization parameter . The SGLASSO estimator does not belong to this class because our penalty term is not additively separable in the entries of . Hence, SGLASSO cannot be analyzed using the framework proposed in Lam and Fan (2009).111It is possible to incorporate other penalty functions into our estimator. Consider: , where denotes the matrix (of the same dimension as ) such that . For instance, we can then let to be the Smoothly Clipped Absolute Deviation (SCAD) penalty function (Fan and Li (2001)).

Another type of mixed norm that is widely used in the high-dimensional linear regression setting is the -norm, also known as the Group Lasso (Friedman et al. (2010); Yuan and Lin (2006)), which is useful when parameters are naturally partitioned into disjoint groups, and we would like to achieve sparsity with respect to whole groups. In contrast, our proposed -norm is distinct from the -norm, and has not been studied in the context of covariance estimation.

2 Setup

Let be a -dimensional vector distributed according to a multivariate distribution with mean zero and covariance matrix . Our goal is to obtain the graphical model corresponding to , which is defined as follows.

The (Gaussian) graphical model of is an undirected graph . The set of nodes (or vertices) of this graph is . Each node corresponds to a random variable . The set of links (or edges) is such that if and only if conditional on all . That is, the graphical model is defined such that there is no link between nodes and in the graph if and only if and are independent conditional on all other nodes besides and . As such the graphical model summarizes the pairwise conditional independence relationships among . The existence of a link in amounts to conditional dependence between the two nodes given all other ones.

Estimation of graphical models is based on the following known fact: if is Gaussian, then the non-zeros in its precision matrix (or inverse covariance matrix) corresponds exactly to links in the graphical model (see Hastie et al. (2015); Whittaker (2009)). That is, there is a link between nodes and if and only if the -th entry of is non-zero. Similarly the lack of a link between a pair of nodes and is equivalent to the -th entry of being zero.

Now suppose we observe i.i.d samples from . We now introduce the GLASSO estimator, as well as our proposed SGLASSO estimator, that allows us to recover the graphical model from the samples. The output of these estimators is a sparse precision matrix . From , the estimated graphical model is then constructed by including a link between nodes and if and only if .

For a matrix , define the mixed norm as follows:

The following norm in equation (2.1) will play a crucial role in our estimator:

| (2.1) |

Our Structured-GLASSO (SGLASSO) estimator is defined in equation (2.2) below, where is the sample covariance matrix calculated from the sample .

| (2.2) |

In comparison, the GLASSO estimator (Banerjee et al. (2008); Friedman et al. (2008); Yuan and Lin (2007); Fan et al. (2015)) is defined in equation (2.3). While SGLASSO uses the mixed norm as a penalty to the likelihood, GLASSO in equation (2.3) uses the norm, which is the familiar lasso penalty (sum of the absolute values of the entries of ).

| (2.3) |

Another definition of the GLASSO is one where only is penalized, where denotes the matrix where its’ diagonal entries are set to zero. While Yuan and Lin (2007); Rothman et al. (2008) use equation (2.3), other authors such as Banerjee et al. (2008); Friedman et al. (2008) use the latter. For various expositional reasons, we will penalize instead of . However in the Monte Carlo simulation, we will also compare with the variant of GLASSO where the diagonals are not penalized.

Although we are comparing SGLASSO with GLASSO in this paper, we could also combine them together. That is, , and use cross-validation procedures to tune the parameters and .

We do not require that the data-generating process be Gaussian.222When the DGP is non-Gaussian, the graphical model estimated using GLASSO or SGLASSO is still useful – it corresponds to the structure of pairwise conditional correlations (partialling out other variables). Therefore our estimator can be seen as maximizing a Gaussian quasi-likelihood subject to regularization. When there is no penalty (), then defined in both (2.2) and (2.3) correspond to the Quasi Maximum Likelihood estimator of the inverse covariance matrix, which is given by the inverse of the empirical sample covariance matrix. As we mentioned in the introduction, it is well-known that the unpenalized sample estimator behaves poorly, and it is unsuitable for graphical modeling when zeros of the estimates are important.

2.1 Motivating Example

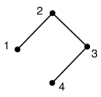

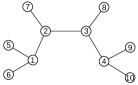

We illustrate the difference between the and the conventional lasso norms. Define and as the precision matrices given by equations (2.4) and (2.5) below.

| (2.4) |

| (2.5) |

The precision matrices and give rise respectively to the graphical models in Figure 2 and Figure 2 below, where links in the graphs represent non-zero entries in the precision matrices.

Both the standard Lasso and Frobenius norms do not distinguish between and , while our proposed -norm does. The reason is clear: both and have the same number of zeros. They have the same sparsity but the structure of this sparsity is very different. For the lasso norm, we have: . Similarly, for the Frobenius norm, we have .

Now on the other hand, the -norm can distinguish between these two structures. The norm evaluated at for the star graph is . While the norm evaluated at for the AR(1) graph is .

3 Theoretical properties

In this section we derive the limiting distribution of SGLASSO when the number of samples goes to infinity while is fixed (following Yuan and Lin (2007)). The main finding of this section is that SGLASSO is asymptotically equivalent to an infeasible GLASSO problem which prioritizes the sparsity-recovery of high-degree nodes. More precisely, we show that SGLASSO is asymptotically equivalent to a modified GLASSO estimator where each row of is penalized proportionally according to its true degree. The true degree of row (or node) is defined by . The term “degree” should be understood as “weighted degree” henceforth.

This asymptotic equivalence result has two implications. First, SGLASSO inherits the sparsity-discovery property of GLASSO where zeros in the precision matrix are estimated precisely to be zero (due to the non-differentiability of the penalty function at zeros). Therefore SGLASSO estimates are also sparse. Secondly, SGLASSO differs from GLASSO in that it prioritizes recovering the zero-pattern of high-degree nodes. Nodes with higher weighted degrees can be viewed as being more influential and important, and we might be more interested in uncovering the relationships among influential agents.

To derive the limiting distributions of our SGLASSO estimator, we assume a high level assumption on the weak limit of the sample covariance matrix.

Assumption 3.1

We assume that

where the notation is the half-vectorization operator that takes only the lower-triangular part of a symmetric matrix.

This high level condition holds when have higher moments and the serial dependence is weak. When , then , where is such that .

Now let be a matrix whose entry is , the true weighted degree of node . Define

| (3.6) |

to be a variant of the GLASSO estimator. Here, the operator is the element-wise multiplication. The SGLASSO estimator is defined as: .

Theorem 3.1

Suppose that as , . Then,

In addition, suppose that Assumption 3.1 holds. Then,

where

| (3.7) |

as . Here is the true covariance matrix of , and .

Compared to the limit in Theorem 3.1, the GLASSO estimator has the following limiting distribution (Yuan and Lin (2007))333Yuan and Lin (2007) consider the GLASSO estimator where the diagonals are not penalized, so that in their paper.:

where

| (3.8) |

where .

Comparing equations (3.7) and (3.8), we see that the SGLASSO obtains the same limiting distribution as that of a modified GLASSO with element-wise LASSO penalty given by . Since is constructed using the true, unknown values of , SGLASSO cannot be simply implemented as GLASSO.

Moreover from Proposition 3.1 below, we can further say that SGLASSO is asymptotically equivalent to a variant of GLASSO where the penalty term is . That is, each entry is given the penalty factor equals to the sum of the (true) weighted degrees of nodes and .

Proposition 3.1

Let be a matrix whose entry is . It is true that .

All proofs are relegated to the Appendix. In the Supporting Information, we plot and illustrate the asymptotic distribution in Theorem 3.1. We show that with a higher probability, SGLASSO correctly estimates a non-link (a zero entry) belonging to a high-degree node.

The distribution of can be simulated after replacing the unknown components and with their consistent estimates, and this can be used in inference procedures on .

A noticeable feature, however, is that the limit distribution in Theorem 3.1 is discontinuous with respect to true DGP. This is because is discontinuous as a function of at . This implies that the inference based on this limit would only be valid pointwise, not uniformly in .444See Belloni et al. (2014) and Van de Geer et al. (2014). We thank one of the referees who pointed this out.

4 Simulation Results

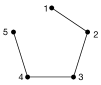

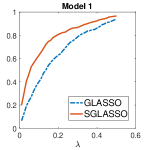

We compare our estimator against GLASSO by considering 3 different graphical models here. In the Supplemental Information, we consider 8 other models. The first two models are depicted in Figure 3. The last model is the graphical model calibrated to the empirical application as depicted in Figure 5. From a given graphical model, we generate the true precision matrix such that if and only if there is a link between nodes and , otherwise we set . We set .

For each model, we draw 1,000 independent datasets from . That is, each dataset comprises of , where is randomly drawn from . For the sample size, we consider and .

Both estimators involve choosing the tuning parameters. We use a 2-folds cross-validation procedure to tune . Specifically, we use the Kullback-Leibler (KL) loss averaged over the two-folds to evaluate predictive accuracies. Equation (3.18) gives the KL loss between the estimated from the training set versus the estimated from the validation set:

| (4.9) |

We report the simulation result in Table 1. In the table, the (a) columns corresponds to SGLASSO whereas the (b) columns refer to GLASSO. In Columns 1(a) and 1(b), we report the optimal as determined by cross-validations, averaged across the 1,000 replications. In Columns 2(a) and 2(b), we report the Kullback-Leibler loss averaged across 1,000 replications.555The KL loss between and is given by In Columns 3(a) and 3(b), we report the average Frobenius loss between and .

In the last two columns of Table 1, we report the score, which measures the accuracy of graph recovery. The Kullback-Leibler loss and the Frobenius norms may not fully capture how accurately the zeros are recovered. We introduce an additional metric: , where precision is the ratio of true positives (TP) to all predicted positives (TP + FP), recall is the ratio of true positives to all actual positives (TP + FN). Alternatively, the score can be written as . The score measures the quality of a binary classifier by equally balancing both the precision and the recall of a classifier. The larger the score is, the better the classifier is. The score is commonly used in machine learning to evaluate binary classifiers. For instance, the Yelp competition uses the score as a metric to rank competing models.666https://www.kaggle.com/c/yelp-restaurant-photo-classification The score is favored over the metric especially in our current setting where the graphical models are sparse. This is because a model that naively predicts all negatives will obtain a high Accuracy score just because there are many actual negatives, and the TN term dominates the Accuracy score.

Model Optimal KL Frobenius score (a) (b) (a) (b) (a) (b) (a) (b) SGLASSO GLASSO SGLASSO GLASSO SGLASSO GLASSO SGLASSO GLASSO (1) 0.181 0.342 0.430 0.483 0.896 0.948 0.439 0.367 \rowfont (0.118) (0.133) (0.207) (0.215) (0.223) (0.214) (0.248) (0.259) (10) 0.207 0.399 0.946 1.096 1.353 1.456 0.336 0.272 \rowfont (0.094) (0.109) (0.278) (0.527) (0.183) (0.414) (0.143) (0.162) (11) 20 0.198 0.389 1.201 1.390 1.569 1.701 0.403 0.341 \rowfont (0.097) (0.117) (0.312) (0.723) (0.186) (0.522) (0.143) (0.164) (1) 0.088 0.179 0.246 0.265 0.710 0.736 0.564 0.541 \rowfont (0.054) (0.076) (0.084) (0.091) (0.129) (0.134) (0.225) (0.248) (10) 0.109 0.230 0.593 0.651 1.137 1.190 0.466 0.437 \rowfont (0.040) (0.052) (0.115) (0.128) (0.113) (0.117) (0.136) (0.159) (11) 50 0.091 0.206 0.747 0.807 1.312 1.370 0.563 0.541 \rowfont (0.041) (0.053) (0.153) (0.167) (0.128) (0.133) (0.120) (0.137)

The conclusion from Table 1 is that SGLASSO achieves significantly lower Kullback-Leibler and Frobenius losses. Moreover in in terms of graph accuracy, SGLASSO also outperforms GLASSO, as indicated by the scores.

To abstract away from the effects of cross-validations, we consider the lowest Kullback-Leibler losses that can be achieved by our estimator versus the GLASSO. Specifically, we vary and at each , we compute the KL and Frobenius losses between the true and . We see from Table 7 that the superior performance of SGLASSO over GLASSO exists after taking away the randomness due to cross-validations. The lowest possible KL losses achievable by our estimator appears to be smaller, than the corresponding KL losses for the GLASSO.

| Model | Minimum | Minimum | Percentage | |||||

|---|---|---|---|---|---|---|---|---|

| KL | Frobenius | Dominance | ||||||

| (a) | (b) | (a) | (b) | |||||

| SGLASSO | GLASSO | SGLASSO | GLASSO | |||||

| (1) | 20 | 0.340 | 0.376 | 0.779 | 0.821 | 0.99 | ||

| (0.106) | (0.120) | (0.096) | (0.116) | |||||

| (10) | 20 | 0.824 | 0.887 | 1.234 | 1.279 | 0.99 | ||

| (0.162) | (0.176) | (0.085) | (0.101) | |||||

| (11) | 20 | 1.041 | 1.102 | 1.415 | 1.466 | 0.95 | ||

| (0.191) | (0.205) | (0.087) | (0.101) | |||||

| (1) | 50 | 0.199 | 0.211 | 0.606 | 0.634 | 0.92 | ||

| (0.063) | (0.065) | (0.095) | (0.098) | |||||

| (10) | 50 | 0.509 | 0.533 | 1.021 | 1.035 | 0.96 | ||

| (0.087) | (0.095) | (0.072) | (0.082) | |||||

| (11) | 50 | 0.652 | 0.675 | 1.203 | 1.204 | 0.86 | ||

| (0.104) | (0.114) | (0.067) | (0.082) | |||||

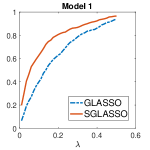

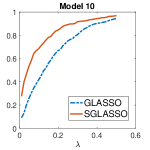

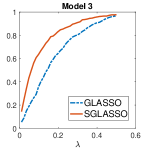

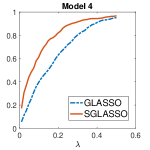

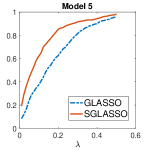

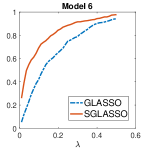

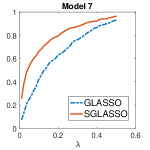

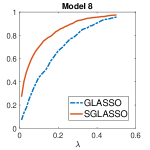

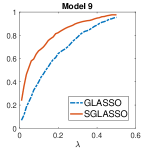

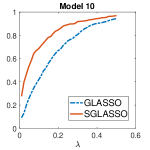

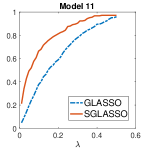

Theorem 3.1 says that the SGLASSO prioritizes recovering the sparsity between nodes that have higher degrees. We now show some numerical evidence that lends support to this. For each model, we examined the pair of nodes such that is largest and , where is the true weighted degree of node . For instance, for model 1, the such that would correspond to the pairs of nodes and . For simplicity, if there are multiple pairs of nodes that maximize , we will pick the pair of nodes that comes first when the adjacency matrix is vectorized.

In each of the model (set ), we calculate the fraction of times that GLASSO and SGLASSO correctly recover for the largest . We plot this result in Figure 11, which shows that at any given , the probability of correctly recovering for high-degree nodes is greater when SGLASSO is used, compared to GLASSO.

4.1 Computational details

Computing the SGLASSO estimator is a convex optimization problem. More precisely, the problem consists of minimizing a smooth convex term given by , and a non-differentiable convex term corresponding to . Since the objective can be formulated as minimizing the sum of a differentiable convex function and a non-differentiable convex function, we can use the proximal gradient method (Beck and Teboulle (2009)) to compute SGLASSO.

In this paper, we use CVX, a Matlab package for specifying and solving convex programs (Grant et al. (2008)). CVX supports convex objective functions that are non-smooth (Grant and Boyd (2008)). CVX also allows us to easily enforce symmetry and positive-definiteness of the matrix minimand, which is needed here. The code is readily available from the authors upon request.

5 Empirical illustration

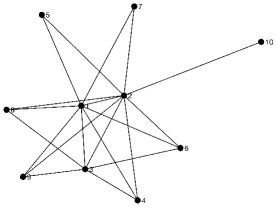

For a real-world empirical illustration, we use the classic Grunfeld investment data (see Greene (2012) or Baltagi (2008)). The goal is to estimate the network dependence structure of firms’ investment decision.777The data can be downloaded freely from Greene (2012)’s companion website.

The data consist of time series of yearly observations on firms. The three variables are real gross investment of firm in year , , .

The investment decision for firm is modeled as follows: , where . The zeros and non-zeros in correspond to the dependence structure of firms’ investment decisions (the object of interest here).

For each firm , we first estimate the linear equation: . This is also the first step in the estimation of Seemingly Unrelated Regressions. Secondly, we use our proposed SGLASSO to estimate the precision matrix of the first-step residuals , , . The tuning parameter is determined using a two-fold cross-validation procedure. The result is shown in Figure 5. (We also estimated the graphical model corresponding to the observed investment variable , the result is similar)

The recovered graphical model exhibits a clear core-periphery structure. There are two groups of firms: a group of core firms and a group of periphery firms. The core firms are linked to each other, as well as linked to the periphery firms. The periphery firms however, are not linked to each other, but are only linked to the core firms. Therefore every node is linked directly to a core firm. The core firms here are firms 1, 2 and 3, which are respectively General Motors, U.S. Steel and General Electric. Using the GLASSO estimator, we recover an identical graphical model – the finding is robust to different choices of penalty functions.

Finally we cannot recover this core-periphery structure using the sample estimator (without regularization). To show this, we estimate the sample precision matrix of the residual estimates from the first step. The graphical model corresponding to this sample precision matrix is the complete graph, where every node is linked to all other nodes – the sample precision matrix is dense and do not contain any zeros.

6 Concluding remarks and policy implications

Graphical model is a potentially useful tool for economists. Using graphical models, we can obtain the network of dependence among random variables. We introduce Structured Graphical Lasso (SGLASSO) as an estimator of graphical models. Using a classic firms’ investment dataset, we find that the dependence structure of firms’ investment decision exhibits a core-periphery network. This has some relevant policy implications – small shocks to those core firms will affect the entire network, creating large aggregate fluctuations as in Acemoglu et al. (2012). Indeed per our finding, one of the core firms is General Motors, whose Chapter 11 restructuring posed a systemic risk to the U.S. economy in 2009.

Acknowledgements

We thank Victor Chernozhukov and two referees for helpful comments and suggestions. The first draft of the paper was written while Moon and Chiong were Associate Director and a postdoctoral fellow of USC Dornsife INET, respectively. Moon acknowledges that this work was supported by the Ministry of Education of the Republic of Korea and the National Research Foundation of Korea (NRF-2017S1A5A2A01023679).

Appendix

Appendix A Proofs

We will use the following important result that concerns the asymptotics of the minimizer of a convex random function (Geyer (1994); Hjort and Pollard (2011); Kato (2009); Pollard (1991)).

Lemma 1.1

Let be a random convex function, that is, is a random variable for each . Moreover, let be the unique minimizer of with respect to . Suppose that converges in distribution to some random convex function for each . Now if is the unique minimizer of , then the random variable converges in distribution to the random variable

A.1 Proof of Theorem 3.1

To prove Theorem 3.1, define the following convex random functions by re-parameterization :

| (1.10) |

and

| (1.11) |

This function is random because of its dependence on the sample covariance matrix, . By definition, our SGLASSO estimator satisfies the following.

By Lemma 1.1, the limit distribution of follows if we show

| (1.12) |

as and as , where the random limit function is defined in equation (3.7).

Following the argument in the proof of Theorem 1 of Yuan and Lin (2007), we have that:

| (1.13) | |||||

| (1.14) | |||||

Moreover, we know that when is large enough,

where . Therefore we can show that the difference of the penalty terms can be written as

| (1.15) |

We can rewrite the second term of equation (1.15) as follows:

where is the true weighted degree of node defined as .

Combining equations (1.10), (1.13), (1.14) and (1.15), we can write as

In the limit as , we then have:

Similarly, in the limit as , we have:

Therefore, we have the first result of the theorem.

A.2 Proof of Proposition 3.1

Proof A.2.

Since is symmetric, we have

| (1.16) | ||||

| (1.17) |

Appendix B Illustrating the asymptotic distribution

We consider the following true precision matrix, . It is an AR(1) model with . The corresponding graph representing is depicted in Figure 6.

In Figure 7 here, we illustrate the asymptotic distribution for both GLASSO and SGLASSO, setting in Theorem 3.1 (see the main text). Each circle in the plot represents a draw from the distribution over as given by Theorem 3.1. Note that the precision matrix is such that . For GLASSO, we have , while for SGLASSO, . Therefore, SGLASSO does a better job at estimating , where a non-link involves a node of relatively higher degree.

In Figure 8, we show the asymptotic distribution of without any penalty or regularization, which corresponds to the Maximum-Likelihood estimator of the inverse covariance matrix. Comparing the two figures, we see that both and norms are able to estimate entries of to be zero exactly, while MLE without regularization fails to recover any sparsity structure.

Appendix C Simulation results

In addition to the 3 graphical models considered in the main text, we explore 8 other models here. The first 10 different graphical models are as depicted in Figures 9 and 10. The last model is the graphical model calibrated to the empirical application. The models in Figure 9 has 5 nodes (), and the models in Figure 10 has 10 nodes (). From a given graphical model, we generate the true precision matrix such that if and only if there is a link between nodes and , otherwise we set . We set .

For each model, we draw 1,000 independent datasets from . That is, each dataset comprises of , where is randomly drawn from . Here, our sample size is when and when . For each of the 100 dataset, we use our estimator, as well as the GLASSO, to estimate the underlying inverse covariance matrix.

Both estimators involve choosing the tuning parameters. We use a 2-folds cross-validation procedure to tune . Specifically, we use the Kullback-Leibler (KL) loss averaged over the two-folds to evaluate predictive accuracies. Equation (3.18) gives the KL loss between the estimated from the training set versus the estimated from the validation set.

| (3.18) |

We report the simulation result in Table 4 for and Table 5 for . In the table, the (a) columns corresponds to SGLASSO whereas the (b) columns refer to GLASSO. In Columns 1(a) and 1(b), we report the optimal as determined by cross-validations, averaged across the 1,000 replications. In Columns 2(a) and 2(b), we report the Kullback-Leibler loss averaged across 1,000 replications. The KL loss between and is given by . In Columns 3(a) and 3(b), we report the average Frobenius loss between and .

In the last two columns of Tables 4 and 5, we report the accuracy of graph recovery using SGLASSO and GLASSO. The Kullback-Leibler loss and the Frobenius norms may not fully capture how accurately the zeros are recovered. We introduce an additional metric: score is , where precision is the ratio of true positives (TP) to all predicted positives (TP + FP), recall is the ratio of true positives to all actual positives (TP + FN). The notations are further explained in the confusion matrix in Table 3. Alternatively, the score can be written as .

| Predicted value is 1 | Predicted value is 0 | |

|---|---|---|

| Actual value is 1 | True positive (TP) | False negative (FN) |

| Actual value is 0 | False positive (FP) | True negative (TN) |

Hence, the score measures the quality of a binary classifier by equally balancing both the precision and the recall of a classifier. The larger the score is, the better the classifier is. The score is commonly used in machine learning to evaluate binary classifiers. For instance, the Yelp competition uses the score as a metric to rank competing models.888https://www.kaggle.com/c/yelp-restaurant-photo-classification The score is favored over the metric especially in our current setting where the graphical models are sparse. This is because a model that naively predicts all negatives will obtain a high Accuracy score just because there are many actual negatives, and the TN term dominates the Accuracy score.

The conclusion from Tables 4 and 5 is that SGLASSO achieves significantly lower KL and Frobenius losses across all models. Moreover in in terms of graph accuracy, SGLASSO also outperforms GLASSO, as indicated by the scores. We also observe that as we increase to , the optimal tuning parameter decreases, the KL and Frobenius losses also decrease, while the score increases. This makes sense because the likelihood becomes more informative as the sample size increases, and therefore the need for regularization decreases.

C.1 Minimum Kullback-Leibler losses

To abstract away from the effects of cross-validations, we consider the lowest Kullback-Leibler losses that can be achieved by our estimator versus the GLASSO. Specifically, we vary and at each , we compute the KL and Frobenius losses between the true and . We see from Table 7 that the superior performance of SGLASSO over GLASSO exists after taking away the randomness due to cross-validations. The lowest possible KL losses achievable by our estimator appears to be smaller, than the corresponding KL losses for the GLASSO.

C.1.1 Recovering high-degree sparsities

Theorem 3.1 says that the SGLASSO prioritizes recovering the sparsity between nodes that have higher degrees. We now show some numerical evidence that lends support to this. For each model, we examined the pair of nodes such that is largest and , where is the true weighted degree of node . For instance, for model 1, the such that would correspond to the pairs of nodes and . For simplicity, if there are multiple pairs of nodes that maximize , we will pick the pair of nodes that comes first when the adjacency matrix is vectorized.

In each of the model (set ), we calculate the fraction of times that GLASSO and SGLASSO correctly recover for the largest . We plot this result in Figure 11, which shows that at any given , the probability of correctly recovering for high-degree nodes is greater when SGLASSO is used, compared to GLASSO.

Model Optimal KL Frobenius score (a) (b) (a) (b) (a) (b) (a) (b) SGLASSO GLASSO SGLASSO GLASSO SGLASSO GLASSO SGLASSO GLASSO (1) 0.181 0.342 0.430 0.483 0.896 0.948 0.439 0.367 \rowfont (0.118) (0.133) (0.207) (0.215) (0.223) (0.214) (0.248) (0.259) (2) 0.180 0.341 0.419 0.469 0.858 0.906 0.400 0.349 \rowfont (0.118) (0.136) (0.205) (0.215) (0.232) (0.226) (0.254) (0.276) (3) 0.183 0.345 0.438 0.492 0.904 0.956 0.415 0.353 \rowfont (0.119) (0.138) (0.210) (0.206) (0.216) (0.204) (0.240) (0.262) (4) 0.181 0.341 0.422 0.471 0.859 0.905 0.396 0.325 \rowfont (0.119) (0.137) (0.223) (0.208) (0.234) (0.210) (0.253) (0.274) (5) 0.188 0.348 0.453 0.504 0.985 1.032 0.436 0.349 \rowfont (0.121) (0.138) (0.195) (0.204) (0.189) (0.181) (0.262) (0.270) (6) 0.203 0.397 0.913 1.050 1.248 1.340 0.332 0.296 \rowfont (0.095) (0.106) (0.270) (0.446) (0.172) (0.312) (0.153) (0.172) (7) 0.206 0.398 0.909 1.067 1.264 1.377 0.314 0.274 \rowfont (0.094) (0.110) (0.289) (0.579) (0.204) (0.507) (0.141) (0.163) (8) 0.210 0.402 0.939 1.089 1.327 1.431 0.308 0.261 \rowfont (0.098) (0.110) (0.287) (0.555) (0.192) (0.431) (0.145) (0.160) (9) 0.208 0.400 0.936 1.089 1.291 1.397 0.317 0.260 \rowfont (0.098) (0.109) (0.297) (0.624) (0.202) (0.470) (0.149) (0.161) (10) 0.207 0.399 0.946 1.096 1.353 1.456 0.336 0.272 \rowfont (0.094) (0.109) (0.278) (0.527) (0.183) (0.414) (0.143) (0.162) (11) 0.198 0.389 1.201 1.390 1.569 1.701 0.403 0.341 \rowfont (0.097) (0.117) (0.312) (0.723) (0.186) (0.522) (0.143) (0.164)

Model Optimal KL Frobenius score (a) (b) (a) (b) (a) (b) (a) (b) SGLASSO GLASSO SGLASSO GLASSO SGLASSO GLASSO SGLASSO GLASSO (1) 0.088 0.179 0.246 0.265 0.710 0.736 0.564 0.541 \rowfont (0.054) (0.076) (0.084) (0.091) (0.129) (0.134) (0.225) (0.248) (2) 0.090 0.183 0.232 0.252 0.663 0.692 0.548 0.517 \rowfont (0.052) (0.075) (0.083) (0.090) (0.127) (0.130) (0.233) (0.248) (3) 0.090 0.181 0.249 0.269 0.715 0.744 0.565 0.530 \rowfont (0.053) (0.077) (0.083) (0.091) (0.124) (0.131) (0.215) (0.239) (4) 0.090 0.183 0.234 0.256 0.666 0.696 0.540 0.504 \rowfont (0.053) (0.076) (0.086) (0.095) (0.127) (0.135) (0.222) (0.250) (5) 0.089 0.181 0.268 0.290 0.800 0.831 0.568 0.521 \rowfont (0.054) (0.079) (0.081) (0.092) (0.125) (0.138) (0.228) (0.252) (6) 0.106 0.228 0.557 0.615 1.024 1.076 0.485 0.479 \rowfont (0.038) (0.050) (0.118) (0.132) (0.109) (0.116) (0.135) (0.160) (7) 0.109 0.230 0.551 0.607 1.030 1.084 0.453 0.437 \rowfont (0.040) (0.048) (0.109) (0.119) (0.109) (0.111) (0.145) (0.156) (8) 0.110 0.231 0.583 0.642 1.105 1.160 0.457 0.419 \rowfont (0.040) (0.050) (0.114) (0.129) (0.112) (0.117) (0.128) (0.147) (9) 0.109 0.230 0.577 0.635 1.061 1.117 0.460 0.438 \rowfont (0.040) (0.050) (0.106) (0.118) (0.111) (0.114) (0.137) (0.158) (10) 0.109 0.230 0.593 0.651 1.137 1.190 0.466 0.437 \rowfont (0.040) (0.052) (0.115) (0.128) (0.113) (0.117) (0.136) (0.159) (11) 0.091 0.206 0.747 0.807 1.312 1.370 0.563 0.541 \rowfont (0.041) (0.053) (0.153) (0.167) (0.128) (0.133) (0.120) (0.137)

| Model | Minimum | Minimum | Percentage | ||||

|---|---|---|---|---|---|---|---|

| KL | Frobenius | Dominance | |||||

| (a) | (b) | (a) | (b) | ||||

| SGLASSO | GLASSO | SGLASSO | GLASSO | ||||

| (1) | 0.340 | 0.376 | 0.779 | 0.821 | 0.99 | ||

| (0.106) | (0.120) | (0.096) | (0.116) | ||||

| (2) | 0.324 | 0.361 | 0.734 | 0.780 | 0.99 | ||

| (0.107) | (0.120) | (0.102) | (0.121) | ||||

| (3) | 0.341 | 0.378 | 0.778 | 0.821 | 0.98 | ||

| (0.105) | (0.119) | (0.095) | (0.115) | ||||

| (4) | 0.326 | 0.362 | 0.734 | 0.779 | 0.99 | ||

| (0.106) | (0.120) | (0.102) | (0.121) | ||||

| (5) | 0.362 | 0.399 | 0.873 | 0.908 | 0.98 | ||

| (0.104) | (0.118) | (0.081) | (0.099) | ||||

| (6) | 0.789 | 0.846 | 1.134 | 1.177 | 0.99 | ||

| (0.162) | (0.172) | (0.092) | (0.103) | ||||

| (7) | 0.771 | 0.831 | 1.136 | 1.182 | 1.00 | ||

| (0.159) | (0.168) | (0.091) | (0.102) | ||||

| (8) | 0.805 | 0.865 | 1.199 | 1.242 | 1.00 | ||

| (0.158) | (0.168) | (0.087) | (0.097) | ||||

| (9) | 0.800 | 0.860 | 1.166 | 1.211 | 1.00 | ||

| (0.161) | (0.172) | (0.091) | (0.100) | ||||

| (10) | 0.824 | 0.887 | 1.234 | 1.279 | 0.99 | ||

| (0.162) | (0.176) | (0.085) | (0.101) | ||||

| (11) | 1.041 | 1.102 | 1.415 | 1.466 | 0.95 | ||

| (0.191) | (0.205) | (0.087) | (0.101) | ||||

| Model | Minimum | Minimum | Percentage | ||||

|---|---|---|---|---|---|---|---|

| KL | Frobenius | Dominance | |||||

| (a) | (b) | (a) | (b) | ||||

| SGLASSO | GLASSO | SGLASSO | GLASSO | ||||

| (1) | 0.199 | 0.211 | 0.606 | 0.634 | 0.92 | ||

| (0.063) | (0.065) | (0.095) | (0.098) | ||||

| (2) | 0.185 | 0.198 | 0.575 | 0.596 | 0.87 | ||

| (0.059) | (0.066) | (0.088) | (0.102) | ||||

| (3) | 0.198 | 0.210 | 0.606 | 0.632 | 0.93 | ||

| (0.062) | (0.064) | (0.093) | (0.096) | ||||

| (4) | 0.184 | 0.197 | 0.575 | 0.596 | 0.85 | ||

| (0.058) | (0.064) | (0.086) | (0.100) | ||||

| (5) | 0.218 | 0.231 | 0.679 | 0.697 | 0.94 | ||

| (0.063) | (0.069) | (0.086) | (0.098) | ||||

| (6) | 0.468 | 0.488 | 0.916 | 0.931 | 0.90 | ||

| (0.091) | (0.100) | (0.078) | (0.090) | ||||

| (7) | 0.465 | 0.491 | 0.917 | 0.940 | 0.99 | ||

| (0.091) | (0.098) | (0.081) | (0.089) | ||||

| (8) | 0.497 | 0.522 | 0.987 | 1.005 | 0.96 | ||

| (0.085) | (0.093) | (0.073) | (0.083) | ||||

| (9) | 0.485 | 0.512 | 0.940 | 0.964 | 0.99 | ||

| (0.091) | (0.097) | (0.080) | (0.085) | ||||

| (10) | 0.509 | 0.533 | 1.021 | 1.035 | 0.96 | ||

| (0.087) | (0.095) | (0.072) | (0.082) | ||||

| (11) | 0.652 | 0.675 | 1.203 | 1.204 | 0.86 | ||

| (0.104) | (0.114) | (0.067) | (0.082) | ||||

References

- Acemoglu et al. (2012) Acemoglu, D., V. M. Carvalho, A. Ozdaglar, and A. Tahbaz-Salehi (2012). The network origins of aggregate fluctuations. Econometrica 80(5), 1977–2016.

- Baltagi (2008) Baltagi, B. (2008). Econometric analysis of panel data. John Wiley & Sons.

- Banerjee et al. (2008) Banerjee, O., L. El Ghaoui, and A. d’Aspremont (2008). Model selection through sparse maximum likelihood estimation for multivariate gaussian or binary data. The Journal of Machine Learning Research 9, 485–516.

- Beck and Teboulle (2009) Beck, A. and M. Teboulle (2009). A fast iterative shrinkage-thresholding algorithm for linear inverse problems. SIAM journal on imaging sciences 2(1), 183–202.

- Belloni et al. (2014) Belloni, A., V. Chernozhukov, and C. Hansen (2014). Inference on treatment effects after selection among high-dimensional controls. The Review of Economic Studies 81(2), 608–650.

- Cai et al. (2011) Cai, T., W. Liu, and X. Luo (2011). A constrained ??1 minimization approach to sparse precision matrix estimation. Journal of the American Statistical Association 106(494), 594–607.

- Cai et al. (2016) Cai, T. T., W. Liu, H. H. Zhou, et al. (2016). Estimating sparse precision matrix: Optimal rates of convergence and adaptive estimation. The Annals of Statistics 44(2), 455–488.

- Elliott et al. (2014) Elliott, M., B. Golub, and M. O. Jackson (2014). Financial networks and contagion. The American economic review 104(10), 3115–3153.

- Fan and Li (2001) Fan, J. and R. Li (2001). Variable selection via nonconcave penalized likelihood and its oracle properties. Journal of the American statistical Association 96(456), 1348–1360.

- Fan et al. (2015) Fan, J., Y. Liao, and H. Liu (2015). An overview on the estimation of large covariance and precision matrices. arXiv preprint arXiv:1504.02995.

- Fan et al. (2016) Fan, J., Y. Liao, and H. Liu (2016). An overview of the estimation of large covariance and precision matrices. The Econometrics Journal 19(1), C1–C32.

- Fan and Lv (2016) Fan, Y. and J. Lv (2016). Innovated scalable efficient estimation in ultra-large gaussian graphical models. arXiv preprint arXiv:1605.03313.

- Friedman et al. (2008) Friedman, J., T. Hastie, and R. Tibshirani (2008). Sparse inverse covariance estimation with the graphical lasso. Biostatistics 9(3), 432–441.

- Friedman et al. (2010) Friedman, J., T. Hastie, and R. Tibshirani (2010). A note on the group lasso and a sparse group lasso. arXiv preprint arXiv:1001.0736.

- Geyer (1994) Geyer, C. J. (1994). On the asymptotics of constrained m-estimation. The Annals of Statistics, 1993–2010.

- Giudici and Spelta (2016) Giudici, P. and A. Spelta (2016). Graphical network models for international financial flows. Journal of Business & Economic Statistics 34(1), 128–138.

- Grant et al. (2008) Grant, M., S. Boyd, and Y. Ye (2008). Cvx: Matlab software for disciplined convex programming.

- Grant and Boyd (2008) Grant, M. C. and S. P. Boyd (2008). Graph implementations for nonsmooth convex programs. In Recent advances in learning and control, pp. 95–110. Springer.

- Greene (2012) Greene, W. H. (2012). Econometric analysis (7th ed.). Prentice hall.

- Hastie et al. (2015) Hastie, T., R. Tibshirani, and M. Wainwright (2015). Statistical learning with sparsity. CRC press.

- Hjort and Pollard (2011) Hjort, N. L. and D. Pollard (2011). Asymptotics for minimisers of convex processes. arXiv preprint arXiv:1107.3806.

- Jackson (2008) Jackson, M. O. (2008). Social and economic networks. Princeton University Press.

- Kato (2009) Kato, K. (2009). Asymptotics for argmin processes: Convexity arguments. Journal of Multivariate Analysis 100(8), 1816–1829.

- Lam and Fan (2009) Lam, C. and J. Fan (2009). Sparsistency and rates of convergence in large covariance matrix estimation. Annals of statistics 37(6B), 4254.

- Meinshausen and Bühlmann (2006) Meinshausen, N. and P. Bühlmann (2006). High-dimensional graphs and variable selection with the lasso. The annals of statistics, 1436–1462.

- Peng et al. (2012) Peng, J., P. Wang, N. Zhou, and J. Zhu (2012). Partial correlation estimation by joint sparse regression models. Journal of the American Statistical Association.

- Pollard (1991) Pollard, D. (1991). Asymptotics for least absolute deviation regression estimators. Econometric Theory 7(02), 186–199.

- Ravikumar et al. (2011) Ravikumar, P., M. J. Wainwright, G. Raskutti, B. Yu, et al. (2011). High-dimensional covariance estimation by minimizing ??-penalized log-determinant divergence. Electronic Journal of Statistics 5, 935–980.

- Ren et al. (2015) Ren, Z., T. Sun, C.-H. Zhang, H. H. Zhou, et al. (2015). Asymptotic normality and optimalities in estimation of large gaussian graphical models. The Annals of Statistics 43(3), 991–1026.

- Rothman et al. (2008) Rothman, A. J., P. J. Bickel, E. Levina, and J. Zhu (2008). Sparse permutation invariant covariance estimation. Electronic Journal of Statistics 2, 494–515.

- Van de Geer et al. (2014) Van de Geer, S., P. Bühlmann, Y. Ritov, R. Dezeure, et al. (2014). On asymptotically optimal confidence regions and tests for high-dimensional models. The Annals of Statistics 42(3), 1166–1202.

- Whittaker (2009) Whittaker, J. (2009). Graphical Models in Applied Multivariate Statistics. London: Wiley Publishing.

- Yuan and Lin (2006) Yuan, M. and Y. Lin (2006). Model selection and estimation in regression with grouped variables. Journal of the Royal Statistical Society: Series B (Statistical Methodology) 68(1), 49–67.

- Yuan and Lin (2007) Yuan, M. and Y. Lin (2007). Model selection and estimation in the gaussian graphical model. Biometrika 94(1), 19–35.