Monopoly Pricing in Vertical Markets with Demand Uncertainty

Abstract

Motivation: Pricing decisions are often made when market information is still poor. While modern pricing analytics aid firms to infer the distribution of the stochastic demand that they are facing, data-driven price optimization methods are often impractical or incomplete if not coupled with testable theoretical predictions. In turn, existing theoretical models often reason about the response of optimal prices to changing market characteristics without exploiting all available information about the demand distribution. Academic/practical relevance: Our aim is to develop a theory for the optimization and systematic comparison of prices between different instances of the same market under various forms of knowledge about the corresponding demand distributions. Methodology: We revisit the classic problem of monopoly pricing under demand uncertainty in a vertical market with an upstream supplier and multiple forms of downstream competition between arbitrary symmetric retailers. In all cases, demand uncertainty falls to the supplier who acts first and sets a uniform price before the retailers observe the realized demand and place their orders. Results: Our main methodological contribution is that we express the price elasticity of expected demand in terms of the mean residual demand (MRD) function of the demand distribution. This leads to a closed form characterization of the points of unitary elasticity that maximize the supplier’s profits and the derivation of a mild unimodality condition for the supplier’s objective function that generalizes the widely used increasing generalized failure rate (IGFR) condition. A direct implication is that optimal prices between different markets can be ordered if the markets can be stochastically ordered according to their MRD functions or equivalently, their elasticities. Using the above, we develop a systematic framework to compare optimal prices between different market instances via the rich theory of stochastic orders. This leads to comparative statics that challenge previously established economic insights about the effects of market size, demand transformations and demand variability on monopolistic prices. Managerial implications: Our findings complement data-driven decisions regarding price optimization and provide a systematic framework useful for making theoretical predictions in advance of market movements.

keywords:

Monopoly Pricing , Revenue Maximization , Demand Uncertainty , Pricing Analytics , Comparative Statics , Stochastic Orders , UnimodalityMSC:

[2010] 91A10 , 91A65 , 91B541 Introduction

Making optimal pricing decisions is a crucial driver for firms’ profitability and a well-studied problem in the existing theoretical literature. However, modern markets pose novel opportunities and challenges for firms’ pricing decisions. On the one hand, the sheer amount of historical price/demand data and the wide range of pricing analytics methods allow firms to make more informed decisions. One the other hand, the inherent volatility of contemporary economies frequently renders such data-driven methods impractical. Sellers, often launch new or differentiated products for which demand is unknown or introduce existing products to uncharted emerging markets (Cohen et al., 2016). In other cases, firms act as wholesalers in foreign markets for which they have asymmetrically less information than local retailers or sell their products over competitive digital platforms to highly diversified clienteles (Chen et al., 2018). More generally, firms often need to test the outcome of price changes in advance of anticipated market movements or to constantly adjust their prices in periods of turbulent market conditions.

Common in all these cases is that firms have to make important pricing decisions when market information is still poor (Li and Atkins, 2005). While uncertainties can be mitigated via marketing strategies or contracting schemes between the members of the supply chain, after all efforts, some uncertainty persists and the final point of interaction between wholesalers and retailers or more generally, between sellers and buyers is the selling price (Li and Petruzzi, 2017; Berbeglia et al., 2019).

Whenever possible, pricing analytics on historic price/demand data aid firms to build up knowledge about the (probability) distribution of the uncertain demand. The main challenge lies in leveraging this information to set and adjust prices optimally. However, data-driven approaches that extrapolate past trends to make forward-looking pricing decisions may lead to suboptimal decisions if not coupled with or benchmarked against testable theoretical predictions. In turn, existing theoretical tools to optimize and compare prices across different market instances (instances of the same market that correspond to different demand distributions) are still under development (Xu et al., 2010) or make partial use of the available information, e.g., rely on summary statistics (Lariviere and Porteus, 2001). Moreover, from a managerial perspective, such methods often provide optimality conditions that are not easy to assess in practice or which do not provide intuitive and economic interpretable results (Van den Berg, 2007).

Model

Motivated by the above, we revisit the classic problem of monopoly pricing with demand uncertainty under the informational assumption that the firm knows the probability distribution of the uncertain demand. This distribution may reflect the seller’s informed belief or estimations aggregated from historical data. Our purpose is to link the properties of the demand distribution to economic interpretable conditions and to develop a systematic theoretical framework in which the firm can optimally set and adjust its prices according to changing market characteristics.

To account for the large variety of market structures that modern sellers are facing, we model the monopolistic firm as an upstream supplier who sells its product via a downstream market. The downstream market comprises an arbitrary number of retailers and various forms of market competition between the retailers, such as differentiated Cournot and Bertrand competition, no or full returns and collusions (cf. Table 1).111The two-tier market model is an abstraction to capture the complexity of current markets. If we eliminate the second stage and assume that the supplier sells directly to the consumers, then our results still apply. In all cases, retail demand is linear. In the first stage, the monopolistic firm sets a uniform price and in the second stage, the retailers observe the price and place their orders after the market demand has been realized. We assume that the supplier’s capacity exceeds potential demand and that downstream retailers are symmetric. These assumptions serve the purpose to isolate the study of pricing decisions under uncertainty from various other strategic considerations such as stocking decisions, negotiation power, marketing and production (Xue et al., 2017; Dong et al., 2019).222Under these assumptions, i.e., if the supplier’s capacity exceeds potential demand and if the retailers are symmetric, then the single price scheme is optimal among a wide range of possible pricing mechanisms (Harris and Raviv, 1981; Riley and Zeckhauser, 1983). In addition, the symmetry of the retailers allows the study of purely competitive aspects which is not possible if retailers are heterogeneous Tyagi (1999).

Results

Our main theoretical contribution is that we characterize the seller’s optimal prices as fixed points of the mean residual demand (MRD) function of the stochastic demand level. Informally, if denote the random demand level and the supplier’s price respectively, then any optimal price, , satisfies the equation , where and is a proper scaling constant (that can be normalized to ). The MRD function measures the expected additional demand given that demand has reached or exceeded a threshold .333In reliability applications, this function is known as the mean residual life (MRL), see Shaked and Shanthikumar (2007); Lai and Xie (2006); Belzunce et al. (2013, 2016). This characterization stems from the observation that the price elasticity of expected demand can be expressed in terms of the MRD function as , cf. equation (8). Thus, optimal prices that correspond to points of unitary elasticity are fixed points of the MRD function. If is decreasing (or equivalently, if the price elasticity is increasing), then there exists a unique such optimal price. Both statements are presented in Theorem 3.2.

The above unimodality condition for the otherwise not necessarily concave nor quasi-concave seller’s revenue function, strictly generalizes the well-known increasing generalized failure rate (IGFR) condition (Lariviere and Porteus, 2001; Van den Berg, 2007). Given the inclusiveness of the IGFR conditions, this suggests that Theorem 3.2 applies to essentially most distributions that are commonly used in economic modeling (Paul, 2005; Lariviere, 2006; Banciu and Mirchandani, 2013). The expressions of the price elasticity of expected demand and the seller’s optimal price in terms of well-understood characteristics of the demand distribution (MRD functions) offer a novel perspective to the otherwise standard linear stochastic model.444While our results directly apply to the more general demand function of López and Vives (2019), we stick to the linear model for expositional purposes. Except from the fact that linear markets have been consistently in the spotlight of economic research both due to their tractability and their accurate modeling of real situations, the study of the linear model is also technically motivated by Cohen et al. (2016) who demonstrate that when information about demand is limited, firms may act efficiently as if demand is linear. For practical purposes, this yields a simple and low regret pricing rule and provides a motivation to study linear markets in a systematic way. They provide conditions that are easy to assess in practice and which can be useful to gain intuitive and economic interpretable results (Van den Berg, 2007). In particular, these expressions provide a novel way to derive comparative statics on the response of the optimal price to various market characteristics (expressed as properties of the demand distribution) and to measure market performance.

The key intuition along this line, which is formally established in Lemma 4.2, is that the seller’s optimal price is higher in less elastic markets which are precisely markets that can be ordered in the MRD stochastic order. In other words, if two demand distributions can be ordered in terms of their MRD functions, then the supplier’s optimal price is higher in the market with the dominating MRD function. Thus, the fact that elasticity is a critical factor in setting profitable prices and an important determinant of price changes in response to demand changes is formalized in terms of well-known demand characteristics. As a result, Lemma 4.2 is the key to leverage the theory of stochastic orders as a tool to compare prices in markets with different characteristics, such as market size and demand variability. Stochastic orders take into account various characteristics of the underlying demand distribution going thus, beyond summary statistics such as expectation or standard deviation, which provide a limited amount of information (Shaked and Shanthikumar, 2007).

In the comparative statics analysis, we start with the effect of market size in optimal prices and ask whether larger markets give rise to higher prices. Our first finding is that stochastically larger markets do not necessarily lead to higher wholesale prices (Section 4.2.1). Technically, this follows from the fact that the usual stochastic order does not imply (nor is implied by) the -order (Shaked and Shanthikumar, 2007). Hence, the intuition of Lariviere and Porteus (2001) that “size is not everything” and that prices are driven by different forces is justified by an appropriate theoretical framework. As Lemma 4.2 demonstrates, the correct criterion to order prices is the elasticity of different market instances rather than their size. In Theorem 4.3, we use this to derive a collection of demand transformations that preserve the MRD order (i.e., the elasticity) and hence the order of optimal prices. Returning to the effects of market size, one may still ask whether there exist conditions under which a probabilistic increase in market demand will lead to an increase in optimal prices. This question is addressed in Theorem 4.5, where we show that this is indeed the case whenever the initial demand is increased by a scale factor greater than one or (under some mild additional conditions) whenever an additional demand source is aggregated.

Next, we turn to the effect of demand variability. Does the seller charge higher/lower prices in more variable markets? The answer to this question again depends on the exact notion of variability that will be used. Under mild additional assumptions, Theorem 4.6 gives two variability orders that preserve monotonicity: in both cases the seller charges a lower price in the less variable market. This conclusion remains true under the mean preserving transformation that is used by Li and Atkins (2005); Li and Petruzzi (2017). However, as was the case with market size, the general statement that more variable markets give rise to higher prices does not hold. In Section 4.3.3, we provide an example to show that this generalization fails in the standard case of parametric families of distributions that are compared in terms of their coefficient of variation, cf. Lariviere and Porteus (2001). All results from the comparative statics analysis are summarized in Table 2.

We then turn to measure market performance and efficiency. Our main result in this direction, is a distribution-free (over the class of distributions with decreasing MRD function) upper bound on the probability of a stockout, i.e., of no trade between the supplier and the retailers (Theorem 5.1). As shown in Examples 5.2, 5.3 and 5.4, this bound is tight and cannot be further generalized to distributions with increasing price elasticity of expected demand. In case that trade takes place, we measure market efficiency in terms of the realized profits and their distribution between the supplier and the retailers. Our results are summarized in Theorem 5.5. As intuitively expected (and in line with earlier results, cf. Ai et al. (2012)), the supplier’s profits are always higher if he is informed about the exact demand level and when retail competition is higher. However, there exists a range of intermediate demand realizations for which the supplier captures a larger share of the aggregate profits in the stochastic market.

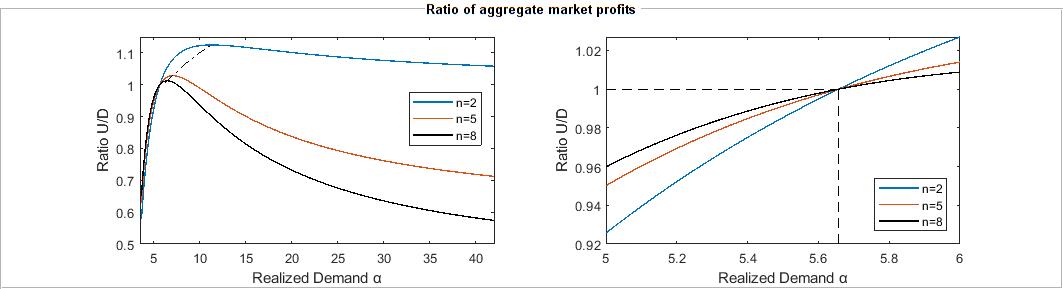

Finally, we compare the aggregate realized profits between the deterministic and stochastic markets. The outcomes depend on the interplay between demand uncertainty and the level of retail competition. More specifically, there exists an interval of demand realizations for which the aggregate profits of the stochastic market are higher than the profits of the deterministic market. The interval reduces to a single point as the number of downstream retailers increases, but is unbounded in the case of retailers. In particular, for , the aggregate profits of the stochastic market remain strictly higher than the profits of the deterministic market for all large enough realized demand levels. However, the performance of the stochastic market in comparison to the deterministic market degrades linearly in the number of competing retailers for demand realizations beyond this interval. This shows that uncertainty on the side of the supplier is more detrimental for the aggregate market profits when the level of retail competition is high, cf. Theorem 5.6.

1.1 Related Literature

The study of price-only contracts under demand uncertainty has been long motivated by Harris and Raviv (1981); Riley and Zeckhauser (1983) who show that committing to a single price is the optimal pricing strategy if the supplier’s capacity exceeds potential demand and retailers are symmetric or if the monopolist is facing a known demand distribution. If the monopolist does not know the distribution of demand a-priori, as we assume in the present paper, then dispersed pricing improves upon the performance of a uniform price Dana (2001). By contrast, Ai et al. (2012) show that wholesale price contracts are optimal even in the case of two competing chains. Compelling arguments for the linear pricing scheme are also provided in Tyagi (1999); Hwang et al. (2018) and references within. Perakis and Roels (2007) and Bernstein and Federgruen (2005) argue that apart from their practical prevalence, price-only contracts are relevant in modeling worst-case scenarios or interaction between sellers and buyers in cases with remaining uncertainty, i.e., after any efforts have been made to reduce the initial uncertainty through more elaborate schemes. This is further supported by Li and Petruzzi (2017) who find that in a vertical market with a single manufacturer and a single retailer that is governed by a wholesale contract between them, less uncertainty may harm either or both members of the supply chain. This is partially the case also in the current model as we show in Section 5.2.1. In particular, we find demand realizations for which the stochastic market outperforms the deterministic market in terms of aggregate profits. However, in our model, the supplier is always better off with reduced uncertainty whereas the retailers may be not.

The vertical market of a single supplier and multiple downstream competing retailers has been widely studied from different perspectives (Padmanabhan and Png, 1997; Tyagi, 1999; Yang and Zhou, 2006; Wu et al., 2012). Our results in Theorems 5.5 and 5.6 are comparable with or mirror earlier findings in this line of literature. However, in the current setting, these findings complement our main results on the characterization of the demand elasticity in terms of the MRD function and the resulting comparative statics rather than being the main focus of our study. Concerning its other assumptions (market structure and timing of demand realization), our model enjoys similarities with the model of De Wolf and Smeers (1997). For extensive surveys of similar demand models, we refer to Huang et al. (2013) and for earlier studies to Yao et al. (2006). Indicatively, the additive demand model with linear deterministic component is used by Petruzzi and Dada (1999) and Ye and Sun (2016).

Regarding the derived unimodality conditions, our findings are most closely related to Lariviere (2006); Van den Berg (2007) who derive the IGFR unimodality condition in the setting of one seller and one buyer. These are special cases of the present setting and, accordingly, the IGFR condition is a restriction of the unimodality condition in terms of the MRD function that we formulate in the current setting. IGFR distributions were first used in economic applications by Singh and Maddala (1976) and were popularized in the context of revenue management by Lariviere and Porteus (2001). Technical aspects of IGFR distributions are studied in Paul (2005); Banciu and Mirchandani (2013). These results are more closely related to a companion paper (Leonardos and Melolidakis, 2020), in which the authors focus on the technical properties of distributions that satisfy the current unimodality condition in terms of the MRD function.555Other closely related papers in the same direction include Leonardos and Melolidakis (2020a, b, 2021), preliminary versions of which appear in Melolidakis et al. (2018); Koki et al. (2018). The MRD function also arises naturally in many revenue management problems with demand uncertainty, see e.g., Mandal et al. (2018); Luo et al. (2016); Colombo and Labrecciosa (2012); Song et al. (2009, 2008) and Petruzzi and Dada (1999) for a non-exhaustive list of related papers. However, to the best of our knowledge, there is no formal link between the elasticity of uncertain demand and the MRD function or the theory of stochastic orders in these papers.

Similarities regarding the technical analysis can also be found between the current model and the literature on the price-setting newsvendor under stochastic demand, see e.g., Chen et al. (2004); Kyparisis and Koulamas (2018); Rubio-Herrero and Baykal-Gürsoy (2018); Kocabıyıkoğlu and Popescu (2011); Kouvelis et al. (2018). However, as the rest of the literature about the newsvendor, these results involve inventory considerations and hence are quite distinct from ours.

More closely related to the current methodology is the study of Xu et al. (2010). This paper is quite distinct from ours since it focus on a restricted set of stochastic orders and in a different newsvendor model that involves both pricing and stocking decisions. Concerning the results, Xu et al. (2010) show that a stochastically larger demand leads to higher selling prices for the additive demand case. We extend these findings by showing that different notions of market size still lead to the same conclusion under certain conditions (Theorems 4.3 and 4.5) and by providing a case under which prices may be actually lower in a stochastically larger market, cf. Section 4.2.1. Within similar contexts, Lariviere and Porteus (2001); Li and Atkins (2005); Krishnan (2010); Chen et al. (2017) show that in general, optimal prices decrease as variability increases. Our current set of results refines these findings by using a wide range of stochastic orders that capture different notions of demand variability. Our findings suggest that increased demand variability may lead to both increased or decreased prices depending on the notion of variability that will be employed (cf. Section 4.3). This demonstrates how various forms of knowledge about the demand distribution can be useful in the study of price movements and provides a theoretical explanation for empirically observed price changes in periods of turbulent market conditions.

1.2 Outline

The rest of the paper is structured as follows. In Sections 2 and 3, we define and analyze our model. Section 4 contains the comparative statics and Section 5 the study of market performance. Section 6 concludes the paper.

2 The Model

We consider a vertical market with a monopolistic upstream supplier or seller, selling a homogeneous product (or resource) to downstream symmetric retailers who compete in a market with retail demand level 666To ease the exposition, we restrict to retailers. As we show in Section 3.3, our results admit a straightforward generalization to arbitrary number of symmetric retailers.. The supplier produces at a constant marginal cost which we normalize to zero. This corresponds to the situation in which the supplier’s capacity exceeds potential demand by the retailers and the supplier’s lone decision variable is his wholesale price, or equivalently his profit margin, .

The supplier acts first (Stackelberg leader) and applies a linear pricing scheme without price differentiation, i.e., he chooses a unique wholesale price, , for all retailers. We consider a market setting in which the supplier is less informed than the retailers about the retail demand level . 777We will refer to throughout as the demand level. However, based on equation (2), is also known as the choke or reservation price. Since, these constants are equivalent up to some transformation in our model, this should cause no confusion. To model this, we assume that after the supplier’s pricing decision but prior to the retailers’ order decisions, a value for is realized from a continuous (not-atomic) cumulative distribution function (cdf) , with finite mean and nonnegative values, i.e., . Equivalently, can be thought of as the supplier’s belief about the demand level and, hence, about the retailers’ willingness-to-pay his price. We write for the tail distribution of and for its probability density function (pdf) whenever it exists. The support of is denoted by , with lower bound and upper bound such that . We don’t make any additional assumption about : in particular, it may or may not be an interval. The case is not excluded888Formally, this case contradicts the assumption that is continuous or non-atomic. It is only allowed to avoid unnecessary notation and should cause no confusion. and corresponds to the situation in which the supplier is completely informed about the retail demand level.

Given the demand realization , the aggregate quantity that the retailers will order from the supplier is a function of the posted wholesale price . Assuming risk neutrality, the supplier aims to maximize his expected profit function , which is equal to

| (1) |

The quantity depends on the form of second stage competition between the retailers. In this paper, we focus on markets with linear demand as in Mills (1959); Petruzzi and Dada (1999); Huang et al. (2013) and Cohen et al. (2016) among others, and allow for a wide range of competition structures between the retailers (Table 1). All these structures give rise – in equilibrium – to the same (up to a scaling constant) functional form for and hence to the same mathematical expression for the supplier’s objective function. More importantly, in all these structures, the second-stage equilibrium between the retailers is unique and hence, is uniquely determined under the assumption that the retailers follow their equilibrium strategies in the game induced by each wholesale price (subgame perfect equilibrium). Specifically, we assume that each retailer faces the inverse demand function

| (2) |

for and . Here, denotes the potential market size (primary demand), the store-level factor and the degree of product differentiation or substitutability between the retailers (Singh and Vives, 1984; Wu et al., 2012). As usual, we assume that . Each retailer’s only cost is the wholesale price that she pays to the supplier. Hence, each retailer aims to maximize her profit function , which is equal to

| (3) |

Given the demand realization , the equilibrium quantities that maximize for are given for various retail market structures in Table 1 as functions of the wholesale price . Here, denotes the positive part, i.e., . The assumption of no uncertainty on the side of retailers about the demand level implies that corresponds both to the quantity that each retailer orders from the supplier and to the quantity that she sells to the market.

| Retail market structure | Retailer ’s equilibrium order |

|---|---|

| Singh and Vives (1984) | |

| Cournot competition – product differentiation | |

| Bertrand competition – product differentiation | |

| Padmanabhan and Png (1997) | |

| Single retailer no/full returns | |

| Competing retailers (orders/price) – no returns | |

| Competing retailers (orders/price) – full returns | |

| Yang and Zhou (2006) | |

| Collusion between retailers – product differentiation |

The standard Cournot and Betrand outcomes arise as special cases of the above. In particular, for , the goods are independent and the monopoly solution for prevails. For , the goods are perfect substitutes with in Bertrand competition (at zero price) and in Cournot competition for . All of the above are assumed to be common knowledge among the participants in the market (the supplier and the retailers).

3 Equilibrium analysis: supplier’s optimal wholesale price

We restrict attention to subgame perfect equlibria of the extensive form, two-stage game.999Technically, these are perfect Bayes-Nash equilibria, since the supplier has a belief about the retailers’ types, i.e., their willingness-to-pay his price, that depends on the value of the stochastic demand parameter . Assuming that at the second stage, the retailers play their unique equilibrium strategies , then, according to (1), the supplier will maximize . For the competition structures of Table 1, has the general form , where is a suitable model-specific constant. Thus, at equilibrium, the supplier’s expected profit maximization problem becomes

| (4) |

From the supplier’s perspective, we are interested in finding conditions such that the maximization problem in (4) admits a unique and finite optimal wholesale price, .

Remark 3.1.

The vertical market structure is not necessary for our analysis to hold. In fact, if we eliminate the downstream market and instead assume that the firm sells directly to a market with inverse linear demand function , then our analysis still applies. This follows from the observation that in this case, the seller’s expected profit maximization problem is

which is the same as the maximization problem in equation (4) after normalizing to .

3.1 Deterministic Market

First, we treat the case in which the supplier knows the primary demand (deterministic market). According to the notation introduced in Section 2, this corresponds to the case . In this case and it is straightforward that . Hence, the complete information two-stage game has a unique subgame perfect Nash equilibrium, under which the supplier sells with optimal price and each retailer orders quantity as determined by Table 1.

3.2 Stochastic Market

The equilibrium behavior of the market in which the supplier does not know the demand level (stochastic market) is less straightforward. Now, and the supplier is interested in finding an that maximizes his expected profit in (4). For an arbitrary demand distribution , may not be concave (nor quasi-concave) and, hence, not unimodal, in which case the solution to the supplier’s optimization problem is not immediate. To obtain a general unimodality condition, we proceed by differentiating the supplier’s revenue function . First, since is nonnegative, we write , for . Since and is non-atomic by assumption, we have that

for any . With this formulation, both the supplier’s revenue function and its first derivative can be expressed in terms of the mean residual demand (MRD) function of . In general, the MRD function, , of a nonnegative random variable with cumulative distribution function (cdf) and finite expectation, , is defined as

| (5) |

and , otherwise, see, e.g., Shaked and Shanthikumar (2007); Lai and Xie (2006) or Belzunce et al. (2016)101010In this literature, the MRD function is known as the mean residual life function due to its origins in reliability applications.. Using this notation, we obtain that and

| (6) |

for . Based on (6), the first order condition (FOC) for the supplier’s revenue function is that or equivalently that . We call the expression

| (7) |

the generalized mean residual demand (GMRD) function, see Leonardos and Melolidakis (2020), due to its connection to the generalized failure rate (GFR) function , defined and studied by Lariviere (1999) and Lariviere and Porteus (2001). Its meaning is straightforward: while the MRD function at point measures the expected additional demand, given the current demand , the GMRD function measures the expected additional demand as a percentage of the given current demand. Similarly to the GFR function, the GMRD function has an appealing interpretation from an economic perspective, since it is related to the price elasticity of expected or mean demand (PEED), (Xu et al., 2010). Specifically,

| (8) |

which implies that corresponds to the inverse of the price elasticity of expected demand (PEED). Hence, in the current setting, demand distributions with decreasing GMRD, (DGMRD property), are precisely distributions that describe markets with increasing PEED, (IPEED property). This observation ties the economic property of IPEED to the distributional property of DGMRD. Accordingly, we will use the terms DGMRD and IPEED interchangeably.

Using (8), the FOC in (6) asserts that the supplier’s payoff is maximized at the point(s) of unitary elasticity. For an economically meaningful analysis, since realistic problems must have a PEED that eventually becomes greater than (Lariviere, 2006), we give particular attention to distributions for which eventually becomes less than , i.e., distributions for which is finite. Observe that for a nonnegative random demand with continuous distribution and finite expectation , and hence .

Based on these considerations, it remains to derive conditions that guarantee the existence and uniqueness of an that satisfies the FOC and to show that this indeed corresponds to a maximum of the supplier’s revenue function as given in (4). This is established in Theorem 3.2 which is the main result of the present Section.

Theorem 3.2 (Equilibrium wholesale prices in the stochastic market).

Consider the supplier’s maximization problem and assume that the nonnegative demand parameter, , follows a continuous (non-atomic) distribution with support within and . Then

-

(a) Necessary condition:

If an optimal price for the supplier exists, then satisfies the fixed point equation

(9) -

(b) Sufficient conditions:

If the generalized mean residual demand (GMRD) function, , of is strictly decreasing and is finite, then at equilibrium, the supplier’s optimal price exists and is the unique solution of (9). In this case, , if , and , otherwise.

Proof.

(a) Since for , the sign of the derivative is determined by the term and any critical point satisfies . Hence, the necessary part of the theorem is obvious from (6) and the continuity of . (b) For the sufficiency part, it remains to check that such a critical point exists and corresponds to a maximum under the assumptions that is strictly decreasing and . Clearly, is continuous and . Hence, starts increasing on . However, the limiting behavior of and hence of as approaches from the left, may vary depending on whether is finite or not. If is finite, i.e., if the support of is bounded, then . Hence, eventually becomes less than 1 and a critical point that corresponds to a maximum exists without any further assumptions. Strict monotonicity of implies that this is unique. If , then an optimal solution may not exist because the limiting behavior of as may vary, see Example 3.4 or Bradley and Gupta (2003). In this case, the condition of finite second moment ensures that . In particular, as shown in Leonardos and Melolidakis (2020), if the GMRD function of a random variable with unbounded support is decreasing, then if and only if is finite. This establishes existence. Uniqueness follows again from strict monotonicity of which precludes intervals of the form that give rise to multiple optimal solutions.

To prove the second claim of the sufficiency part, note that is equivalent to . Then, the DGMRD property implies that for all , hence . In this case, and hence is given explicitly by , which may be compared with the optimal of the complete information case. On the other hand, if , then for all , which implies that must be in . ∎

The economic interpretation of the sufficiency conditions in part (b) of Theorem 3.2 is immediate. By (8), demand distributions with the DGMRD property are precisely distributions that exhibit increasing PEED (IPEED property). In turn, finiteness of the second moment is required to ensure that the expected demand will eventually become elastic, even in the case of unbounded support, see Leonardos and Melolidakis (2020), Theorem 3.2. Thus, part (b) characterizes in terms of their mathematical properties demand distributions that model linear markets with monotone and eventually elastic expected demand. These conditions apply to distributions that may neither be absolutely continuous (do not possess a density) nor have a connected support.

Remark 3.3.

In the statement of Theorem 3.2, strict monotonocity can be relaxed to weak monotonicity without significant loss of generality. This relies on the explicit characterization of distributions with MRD functions that contain linear segments which is given in Proposition 10 of Hall and Wellner (1981). Namely, on some interval if and only if for all . If is unbounded, this implies that has the Pareto distribution on with scale parameter . In this case, , see Example 3.4, which is precluded by the requirement that . Hence, to replace strict by weak monotonicity – but still retain equilibrium uniqueness – it suffices to exclude distributions that contain intervals with in their support, for which for all .

Example 3.4 (Pareto distribution).

The Pareto distribution is the unique distribution with constant GMRD and GFR functions over its support. Let be Pareto distributed with pdf , and parameters and (for we get , which contradicts the basic assumptions of our model). To simplify, let , so that , , and . The mean residual demand of is given by and, hence, is decreasing on and increasing on . However, the GMRD function is decreasing for and is constant thereafter, hence, is DGMRD. Similarly, for the failure (hazard) rate is decreasing, but the generalized failure rate is constant and, hence, is IGFR. The payoff function of the supplier is

which diverges as , for and remains constant for . In particular, for , the second moment of is infinite, i.e., , which shows that for DGMRD distributions, the assumption that the second moment of is finite may not be dropped for part (b) of Theorem 3.2 to hold. On the other hand, for , we get as the unique optimal wholesale price, which is indeed the unique fixed point of .

3.3 General case with identical retailers

To ease the exposition, we restricted our presentation to identical retailers. However, the present analysis applies to arbitrary number of symmetric retailers for all competition-structures that give rise to a unique second-stage equilibrium in which the aggregate ordered quantity depend on via the term as in Table 1. This relies on the fact, that in such markets, the total quantity that is ordered from the supplier depends on only up to a scaling constant. Thus, the approach to the supplier’s expected profit maximization in the first-stage remains the same independently of the number of second-stage retailers. To avoid unnecessary notation, we present the general case for the classic Cournot competition.

Formally, let , with denote the set of symmetric retailers. A strategy profile (retailers’ orders from the supplier) is denoted by with and . Assuming linear inverse demand function , the payoff function of retailer , for , is given by . Under these assumptions, the second stage corresponds to a linear Cournot oligopoly with constant marginal cost, . Hence, each retailer’s equilibrium strategy, , is given by , for . Accordingly, in the first stage, the supplier’s expected revenue function on the equilibrium path is given by . Hence, it is maximized again at if the supplier knows or at if the supplier only knows the distribution of . Based on the above, the number of second-stage retailers affects the supplier’s revenue function only up to a scaling constant and Theorem 3.2 is stated unaltered for any .

4 Comparative Statics

The main implication of the closed form expression of the supplier’s optimal price in terms of the MRD function (equation (9)) is that it facilitates a comparative statics analysis via the rich theory of stochastic orders (Shaked and Shanthikumar, 2007; Lai and Xie, 2006; Belzunce et al., 2016). Since the equilibrium quantity and price are both monotone in the wholesale price , our focus will be on as the demand distribution characteristics vary. To obtain a meaningful comparison between different market instances (i.e., instances of the same market that correspond to different demand distributions), we assume throughout equilibrium uniqueness and hence, unless stated otherwise, we consider only distributions for which Theorem 3.2 applies111111Since the DGMRD property is satisfied by a very broad class of distributions, see Banciu and Mirchandani (2013), Kocabıyıkoğlu and Popescu (2011) and Leonardos and Melolidakis (2020), we do not consider this as a significant restriction. Still, since it is sufficient (together with finitenes of the second moment) but not necessary for the existence of a unique optimal price, the analysis naturally applies to any other distribution that guarantees equilibrium existence and uniqueness.. First, we introduce some additional notation.

Let be two nonnegative random variables – or equivalently demand distributions – with supports between and and and , respectively (cf. definition of and in Section 2) and MRD functions and . We say that is less than in the mean residual demand order, denoted by 121212In reliability applications, the MRD-order is commonly known as the mean residual life (MRL)-order, Shaked and Shanthikumar (2007)., if for all . This order plays a key role in the present model. Specifically, by (8), we have that for any if and only if for any , i.e., if and only if the price elasticity of expected demand in market is less than the price elasticity of expected demand in market for any wholesale price . This motivates the following definition.

Definition 4.1.

We will say that market is less elastic than market , denoted by , if for every . Based on the above, if and only if .

Using this notation, the following Lemma captures the importance of the characterization of the optimal price via the fixed point equation (9).

Lemma 4.2.

Let be two nonnegative, continuous and strictly DGMRD demand distributions with finite second moments. If is less elastic than , then the supplier’s optimal wholesale price is lower in market than in market . In short, if , then .

Proof.

Lemma 4.2 states that the supplier charges a higher price in a less elastic market. Although trivial to prove once Theorem 3.2 has been established, it is the key to the comparative statics analysis in the present model. Indeed, combining the above, the task of comparing the optimal wholesale price for varying demand distribution parameters – such as market size or demand variability – essentially reduces to comparing demand distributions (market instances) in terms of their elasticities or equivalently in terms of their MRD functions. Such conditions can be found in Shaked and Shanthikumar (2007) and Belzunce et al. (2013) and provide the framework for the subsequent analysis.

4.1 Transformations that preserve the MRD-order

Lemma 4.2 provides a natural starting point to study the response of the equilibrium wholesale price, , to changes in the demand distribution. In particular, if a change in the demand distribution preserves the -order, then Lemma 4.2 readily implies that this change will also preserve the order of wholesale prices. Specifically, let denote two different demand distributions, such that . In this case, we know by Lemma 4.2 that . We are interested in determining transformations of that preserve the -order and hence the ordering . Unless otherwise stated, we assume that the random demand is such that it satisfies the sufficiency conditions of Theorem 3.2 and hence that the supplier’s optimal wholesale price exists and is unique.

Theorem 4.3.

Let denote two nonnegative, continuous and strictly DGMRD demand distributions, with finite second moments, such that .

-

(i)

If is a nonnegative, IFR distribution, independent of and , then .

-

(ii)

If is an increasing, convex function, then .

-

(iii)

If for some , then .

Proof.

Part (i) follows from Lemma 2.A.8 of Shaked and Shanthikumar (2007). Since the resulting distributions may not be DGMRD nor DMRD, the setwise notation is necessary. Part (ii) follows from Theorem 2.A.19 (ibid). Equilibrium uniqueness is retained in the transformed markets, , since the DGMRD class of distributions is closed under increasing, convex transformations, see Leonardos and Melolidakis (2020). Finally, part (iii) follows from Theorem 2.A.19. However, the DGMRD class is not closed under mixtures and hence, in this case, the market may have multiple equilibria, which necessitates, as in part (i), the setwise statement for the wholesale equilibrium prices of the market. ∎

Remark 4.4.

Mukherjee and Chatterjee (1990) show that the strict -order – i.e., if the inequality is strict for all – is closed under monotonically non-decreasing transformations and closed in a reversed sense under monotonically non-increasing transformations. The -order is also closed under convolutions, provided that the convoluting distribution has log-concave density (as is the case with many commonly used distributions, Bagnoli and Bergstrom (2005)), Mukherjee and Chatterjee (1992). Finally, if instead of , and are ordered in the stronger hazard rate order, i.e., if for all , denoted by , then part (i) of Theorem 4.3 remains true by Lemma 2.A.10 of Shaked and Shanthikumar (2007), even if is merely DMRD (instead of IFR).

4.2 Market size

Next, we turn to demand transformations that intuitively correspond to larger market instances. Again, to avoid unnecessary technical complications, we will restrict attention to demand distributions which satisfy the sufficiency conditions of Theorem 3.2 (e.g., DMRD or DGMRD distributions).

4.2.1 Stochastically larger markets

Our first finding in this direction is that stochastically larger markets do not necessarily lead to higher wholesale prices. Technically, this follows from the fact that the stochastic order does not imply (nor is implied by) the -order (Shaked and Shanthikumar, 2007). In particular, Lemma 4.2 demonstrates that the correct criterion to order prices is the elasticity rather than the size of different market instances. This provides a theoretical explanation for the intuition of Lariviere and Porteus (2001) that “size is not everything” and that prices are driven by different forces.

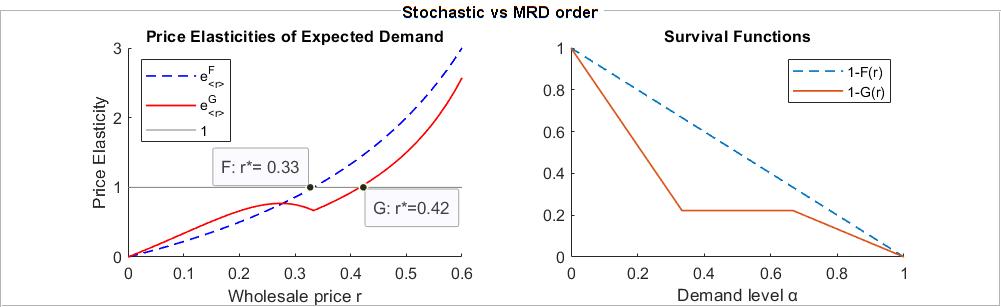

Formally, let denote two market instances. If for all , then is said to be less than in the usual stochastic order, denoted by . It is immediate that implies . The following example, adapted from Shaked and Shanthikumar (1991), shows that wholesale prices can be lower in a stochastically larger market instance. Specifically, let be uniformly distributed on and let have a piecewise linear distribution with and . Then, as shown in Figure 1, (right panel) but (left panel).

4.2.2 Reestimating demand

The above example suggests that the statement larger markets lead to higher prices cannot be obtained in full generality. This brings us to the main part of this section which is to investigate conditions under which an increase in market demand leads to an increase in optimal prices. Formally, let denote the random demand in an instance of the market under consideration. Let denote a positive constant and an additional random source of demand that is independent of . Moreover, let denote the equilibrium wholesale price in the initial market and the equilibrium wholesale prices in the markets with random demand and respectively. How does compare to and ?

While the answer for is rather straightforward, see Theorem 4.5 below, the case of is more complicated. Specifically, since DGMRD random variables are not closed under convolution, see Leonardos and Melolidakis (2020), the random variable may not be DGMRD. This may lead to multiple equilibrium wholesale prices in the market, irrespectively of whether is DGMRD or not. To deal with the possible multiplicity of equilibria, we will write to denote the set of all possible equilibrium wholesale prices. Here, denotes the MRD function of a demand distribution, e.g., . To ease the notation, we will also write , when all elements of the set are less or equal than all elements of the set .

Theorem 4.5 conforms wite prices are always higher in the larger market and under some additional conditions also in the market.

Theorem 4.5.

Let be a nonnegative and continuous demand distribution with finite second moment.

-

(i)

If is DGMRD and is a positive constant, then .

-

(ii)

If is DMRD and is a nonnegative, continuous demand distribution with finite second moment and independent of , then , i.e., for any equilibrium wholesale price of the market.

Proof.

The proof of part (i) follows directly from the preservation property of the -order that is stated in Theorem 2.A.11 of Shaked and Shanthikumar (2007). Specifically, since is the MRD function of , we have that , for all , with the inequality following from the assumption that is DGMRD. Hence, or equivalently , cf. Definition 4.1, which by Lemma 4.2 implies that .

Part (ii) follows from Theorem 2.A.11 of Shaked and Shanthikumar (2007). The proof necessitates that is DMRD and hence requiring that is merely DGMRD is not enough. Since, is DMRD, we know that for all . Together with , this implies that , for all . Hence, , which implies that in this case, is a lower bound to the set of all possible wholesale equilibrium prices in the market. ∎

4.3 Market demand variability

The response of the equilibrium wholesale price to increasing (decreasing) demand variability is even less straightforward. There exist several stochastic orders that compare random variables in terms of their variability and the effects on prices largely depend on the exact order that will be employed. To proceed, we first introduce some additional notation.

4.3.1 Variability or dispersive orders

Let and be two nonnegative distributions with equal means, , and finite second moments. If for all , then is said to be smaller than in the convex order, denoted by . If and denote the right continuous inverses of and for all , then is said to be smaller than in the dispersive order, denoted by . Finally, if for all , then is said to be smaller than in the excess wealth order, denoted by . Shaked and Shanthikumar (2007) show that which in turn implies that .

Does less variability imply a lower (higher) wholesale price?

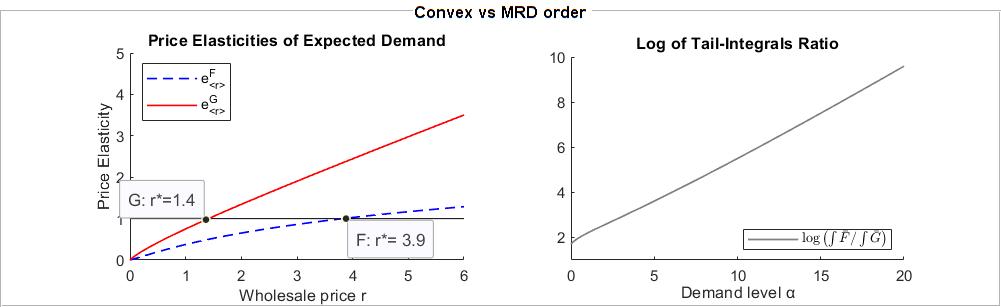

The answer to this question largely depends on the notion of variability that we will employ. Xu et al. (2010) use the more general -order to conclude that under mild additional assumptions, less variability implies higher prices. Concerning the present setting, ordering two demand distributions and in the -order does not in general suffice to conclude that wholesale prices in the and markets are ordered respectively. This is due to the fact that the -order does not imply the -order. An illustration is provided in Figures 2 and 3.

In Figure 2, we consider two demand distributions, , a Lognormal and , a Gamma . For this choice of parameters, and hence are ordered in the -order if and only if the tail-integrals of and are ordered, see Shaked and Shanthikumar (2007) Theorem 3.A.1. The right panel depicts the log of the ratio of these integrals, i.e., which remains throughout positive (and increasing). Hence, . The left panel depicts the price elasticities of expected demand in the and markets. As can be seen, the supplier charges a higher price in the market than in the less variable (according to the -order) market.

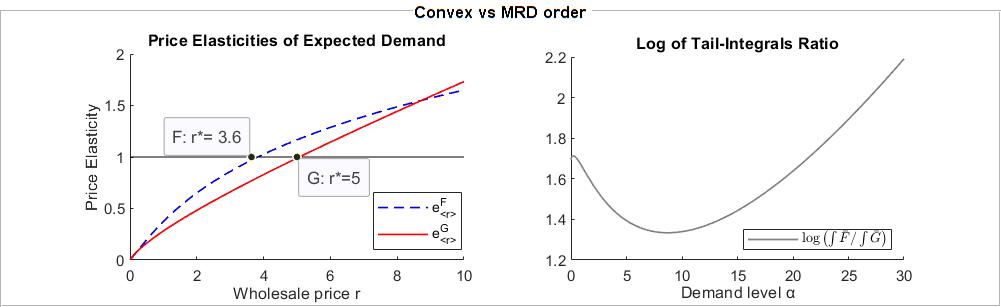

The above conclusion is reversed in the case of Figure 3. In this example, we consider two demand distributions, with , as above, a and , a Gamma . This choice of parameters retains the equality and hence, can be ordered in the -order if and only if the tail-integrals of and can be ordered. Again, the right panel depicts the log of the ratio of these integrals which remains throughout positive (and increasing). Hence, . However, the picture in the left panel is now reversed. As can be seen, the supplier now charges a lower price in the market than in the less variable (according to the -order) market.

More can be said, if we restrict attention to the - and -orders. We will write to denote the lower end of the support of variable for .

Theorem 4.6.

Let be two nonnegative, continuous, strictly DGMRD demand distributions with finite second moment. In addition,

-

(i)

if either or are DMRD and , and if , then .

-

(ii)

if either or are IFR and , then .

Proof.

The first part of Theorem 4.6 follows directly from Theorem 3.C.5 of Shaked and Shanthikumar (2007). Based on its proof, the assumption that at least one of the two random variables is DMRD (and not merely DGMRD) cannot be relaxed. Part (ii) follows directly from Theorem 3.B.20 (b) of Shaked and Shanthikumar (2007) and the fact that the -order implies the -order. As in part (i), the condition that both and are DGMRD does not suffice and we need to assume that at least one is IFR. Recall, that with all inclusions being strict, see e.g., Leonardos and Melolidakis (2020). ∎

The first implication of Theorem 4.6 is that there exist classes of distributions for which less variability implies lower wholesale prices. This is in contrast with the results of Lariviere and Porteus (2001) and Xu et al. (2010) (for the additive demand case) and sheds light on the effects of upstream demand uncertainty. In these models, uncertainty falls to the retailer, and the supplier charges a higher price to capture an increasing share of all supply chain profits as variability reduces. Contrarily, if uncertainty falls to the supplier as in the present model, then the supplier may charge a lower price as variability increases.

The second implication is that these results, albeit general, do not apply to all distributions that are comparable according to some variability order. As illustrated with the examples in Figures 2 and 3 and the convex-order, less variability may lead to both higher or lower wholesale prices. From a managerial perspective, this implies that the effect of demand variability on prices crucially depends on the exact notion of variability that will be employed and may be ambiguous even under the standard setting of linear demand that is studied here.

4.3.2 Mean preserving transformation

To further study the effects of demand variability, we use the mean preserving transformation , where and , see Li and Atkins (2005) and Li and Petruzzi (2017). Indeed, and , i.e., has the same mean and support as but is “less variable” than . Theorem 4.7 shows that and hence, by Lemma 4.2 the supplier always sets a higher price in market than in the “less variable” market . This recovers in a straightforward way the finding of Li and Atkins (2005).

Theorem 4.7.

Let be a nonnegative, continuous, DGMRD demand distribution with finite mean, , and variance, , and let , for . Then, and .

Proof.

It suffices to show that is smaller than in the mrd-order, i.e., that . The conclusion then follows from Theorem 2.A.18 of Shaked and Shanthikumar (2007) and Lemma 4.2. In turn, to show that , it suffices to show that increases in over , cf. Shaked and Shanthikumar (2007) (2.A.3). Since, , this is equivalent to showing that increases in for . Differentiating with respect to and reordering the terms, we obtain that the previous expression increases in for if and only if for . However, this is immediate, since . ∎

4.3.3 Parametric families of distributions

To elaborate on the fact that different variability notions may lead to different responses on wholesale prices, we consider the parametric approach of Lariviere and Porteus (2001). Given a random variable with distribution , let with and for . Lariviere and Porteus (2001) show that in this case, the wholesale price is dictated by the coefficient of variation, . Specifically, if , then , i.e., in their model, a lower , or equivalently a lower relative variability, implies a higher price. This is not true for our model.

To see this, we consider two normal demand distributions and . By Table 2.2 of Belzunce et al. (2016), if and , then and hence, by Lemma 4.2, . However, by choosing and appropriately, we can trivially achieve an arbitrary ordering of their relative variability in terms of their ’s. The reason for this ambiguity is that changing for , not only affects , i.e., the relative variability, but also the central location of the respective demand distribution. In contrast, under the assumption that , the stochastic orders approach of the previous paragraph provides a more clear insight. The results of the comparative statics analysis are summarized in Table 2.

| Demand Transformations | |||

| Assumptions on market demand distributions | Optimal prices | ||

|

|||

| increasing and convex | |||

| , | |||

| Market Size | |||

| Assumptions on market demand distributions | Optimal prices | ||

| DMRD |

|

||

| inconclusive | |||

| Demand Variability | |||

| Assumptions on market demand distributions | Optimal prices | ||

| inconclusive | |||

| and or DMRD | |||

| or IFR | |||

| inconclusive | |||

5 Market Performance

We now turn to the effects of upstream demand uncertainty on the efficiency of the vertical market. As in Section 3.3, we restrict attention to the classic Cournot competition with linear demand and arbitrary number of competing retailers in the second stage. After scaling to , this implies that the equilibrium order quantities are for each and any wholesale price . The supplier’s optimal wholesale price, , is given by Theorem 3.2.

5.1 Probability of no-trade

Markets with incomplete information are usually inefficient in the sense that trades which are profitable for all market participants may actually not take place. In the current model, such inefficiencies appear for values of for which a transaction does not occur in equilibrium under incomplete information although such a transaction would have been beneficial for all parties involved, i.e., supplier, retailers and consumers.

If , then the retailers buy units and there is an immediate stockout. Hence, for a continuous distribution of , the probabilitiy of no-trade in equilibrium under incomplete information is equal to . To study this probability as a measure of market inefficiency, we restrict attention to the family of DMRD distributions, i.e., distributions for which is non-increasing.

Theorem 5.1.

For any demand distribution with the DMRD property, the probability of no-trade at the equilibrium of the stochastic market cannot exceed the bound . This bound is tight over all DMRD distributions.

Proof.

By expressing the distribution function in terms of the MRD function, see Guess and Proschan (1988), we get . Hence, by the DMRD property and the monotonicity of the exponential function, it follows that . Since , we conclude that . If the MRD function is constant, as is the case for the exponential distribution, see Example 5.2, then all inequalities above hold as equalities, which establishes the second claim of the Theorem. ∎

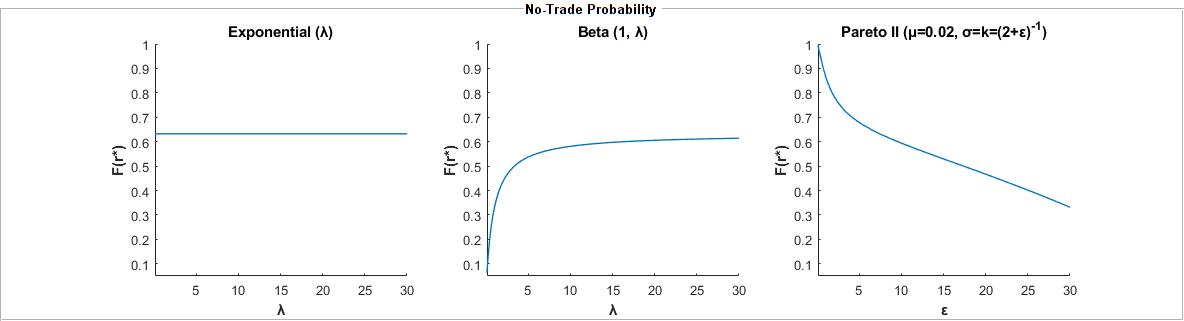

Examples 5.2 and 5.3 highlight the tightness of the no-trade probability bound that is derived in Theorem 5.1. Example 5.4 shows that this bound cannot be extended to the class of DGMRD distributions. The conclusions are summarized in Figure 4.

Example 5.2 (Exponential distribution).

Let , with , and pdf . Since , for , the MRD function is constant over its support and, hence, is both DMRD and IMRD but strictly DGMRD, as , for . By Theorem 3.2, the optimal strategy of the supplier is . The probability of no transaction is equal to , confirming that the bound derived in Theorem 5.1 is tight. Thus, the exponential distribution is the least favorable, over the class of DMRD distributions, in terms of efficiency at equilibrium.

Example 5.3 (Beta distribution).

This example refers to a special case of the Beta distribution, also known as the Kumaraswamy distribution, see Jones (2009). Let with , and pdf . Then, and for . Since the MRD function is decreasing, Theorem 3.2 applies and the optimal price of the supplier is . Hence, as . This shows that the upper bound of in Theorem 5.1 is still tight over distributions with strictly decreasing MRD, i.e., it is not the flatness of the exponential MRD that generated the large inefficiency.

Example 5.4 (Generalized Pareto or Pareto II distribution).

This example shows that the bound of Theorem 5.1 does not extend to the class of DGMRD distributions. Let , with pdf and cdf , with . For the parametrization and , with , the cdf becomes . Moreover, , since for any . Hence, by a standard calculation, , which shows that is DGMRD but not DMRD. In this case, and , which shows that the probability of a stockout may become arbitrarily large for values of close to . The “pathology” of this example relies on the fact that as .

5.2 Division of realized market profits

If the realized value of is larger than , then a transaction between the supplier and the retailers takes place. In this case, we measure market efficiency in terms of the realized market profits. Specifically, we fix a demand distribution (which satisfies the sufficiency conditions of Theorem 3.2) with support (with upper and lower bounds and respectively, as defined in Section 2) and a realized demand level and compare the individual realized profits of the supplier and each retailer between the deterministic and the stochastic markets. For clarity, we summarize all related quantities in Table 3.

| Upstream Demand for the Supplier | ||||||

| Uncertain | Deterministic | |||||

|

||||||

| Realized Profits at Equilibrium | ||||||

| Supplier | ||||||

| Retailer | ||||||

| Aggregate | ||||||

We are interested in addressing the following questions: First, how do the supplier’s (retailers’) realized profits compare between the stochastic and the deterministic market? Second, how does retail competition and demand uncertainty affect the supplier’s (retailers’) share of realized market profits? Third, how does the level or retail competition – number of retailers – affect supplier’s profits in both markets? The answers are summarized in Theorem 5.5 which follows rather immediately from Table 3. To avoid technicalities, we assume throughout that the upper bound of the support is large enough, so that (e.g., ).

Theorem 5.5.

Let denote a demand distribution with support within and , the respective optimal wholesale price in the stochastic market such that , and , with , a realized demand level, for which trading between supplier and retailers takes place in both the stochastic and the deterministic market. Let, also, and denote the supplier’s share of realized profits in the stochastic and deterministic markets respectively. Then,

-

, with equality only for . In particular, for any .

-

decreases in the realized demand level .

-

is independent of the demand level .

-

is higher than for values of , equal for , and lower otherwise.

-

and both increase in the level of retail competition.

Finally, each retailer’s profit in the stochastic market, , is strictly higher than her profit in the deterministic market for all demand levels and less otherwise, with equality for only.

Proof.

By Table 3, we have that: (i) if and only if which holds with strict inequality for all values of , except for for which the quantities are equal. The second part of statement (i) is immediate. For (ii) , and for (iii) . Now, (iv) and (v) directly follow from the previous calculations. Finally, if and only if which holds with strict inequality for all values of and with equality for . ∎

The statements of Theorem 5.5 are rather intuitive and in their largest part, with the exception of part (iv), they conform to earlier findings (Ai et al., 2012). (i) The supplier is always better off if he is informed about the retail demand level. (ii) In the stochastic market, he captures a larger share of the realized market profits for lower values of realized demand (but not lower than the no-trade threshold of ) whereas in the deterministic market (iii) his share of profits is constant with respect to the demand level. (iv) Yet, in the stochastic market, there exists an interval of demand realizations, namely , for which the supplier’s profits (although less than in the deterministic market) represent a larger share of the aggregate market profits. In any case, (v) retail competition benefits the supplier. Finally, in the case that the supplier prices under uncertainty, each retailer makes a larger profit for higher realized demand values which abides to intuition. These observations conform with the existence of conflicting incentives regarding demand-information disclosure between the retailers and the supplier, cf. Li and Petruzzi (2017).

5.2.1 Deterministic and stochastic markets: aggregate profits

We next turn to the comparison of the aggregate market profits between the deterministic and the stochastic market. As before, we fix a demand distribution (which is again assumed to satisfy the sufficiency conditions of Theorem 3.2) with support within and , and evaluate the ratio of the aggregate realized market profits in the stochastic market to the aggregate market profits in the deterministic market. To study market performance under the two scenarios, we need to evaluate the combined effect of demand uncertainty and retail competition. For a realized demand , there is a stockout and the realized aggregated profits are equal to . In this case, the stochastic market performs arbitrarily worse than the deterministic market and the ratio is equal to for any number of competing retailers. Hence, for a non-trivial analysis, we restrict attention to for which trading takes place in both the stochastic and the deterministic markets.

Theorem 5.6.

Let denote a demand distribution with support within and , with large enough, and let denote the respective optimal wholesale price in the stochastic market. Additionally, suppose that , with is a realized demand level for which trading between supplier and retailers takes place in both the stochastic and the deterministic market. Let, also, denote the ratio of the aggregate realized profits in the stochastic market to the aggregate profits in the deterministic market. Then,

-

for if or and for if .

-

is maximized for for , for which it is equal to . Moreover, converges to as for any .

-

increases in the level of competition for demand levels and decreases thereafter.

Again, to avoid unnecessary technicalities in the proof of Theorem 5.6, we assume that is large enough, e.g., .

Proof.

By Table 3, a direct substitution yields that iff

with . For , the result is straightforward, whereas for the result follows from the observation that the roots of the expression in the left part are given by . This establishes (i) and after some trivial algebra, also (ii). To obtain (iii), we compare for arbitrary to for

which yields the statement. ∎

Statement (i) of Theorem 5.6 asserts that there exists an interval of realized demand values, whose upper bound depends on the number of competing retailers, for which the stochastic market outperforms the deterministic market in terms of aggregate profits. The effect of increasing retail competition on the aggregate profits of the stochastic market is twofold. First, the range (interval) of demand values for which the ratio of aggregate profits exceeds reduces to a single point as competition increases (). Second, for larger values of realized demand, the ratio converges to as . This shows that uncertainty on the side of the supplier is less detrimental for the aggregate market profits when the level of retail competition is low. In particular, for , the aggregate profits of the stochastic market remain strictly higher than the profits of the deterministic market for all large enough realized demand levels. As competition increases this remains true only for lower (but still above the no-trade threshold) demand levels. However, for higher demand realizations, the ratio degrades linearly in the number of competing retailers.

The statements of Theorem 5.6 are illustrated in Figure 5. Here but the picture is essentially the same for any choice of demand distribution that satisfies the sufficiency conditions of Theorem 3.2 and for which is large enough, i.e., .

6 Conclusions

In this paper, we revisited the classic problem of optimal pricing by a monopolist who is facing linear stochastic demand. The monopolist may sell directly to the consumers or via a retail market with an arbitrary competition structure. Our main theoretical finding is that the price elasticity of expected demand, and hence also the monopolist’s optimal prices, can be expressed in terms of the mean residual demand (MRD) function of the demand distribution. In economic terms, the MRD function describes the expected additional demand given that current demand has reached or exceeded a certain threshold. This leads to a closed form characterization of the points of unitary elasticity that maximize the monopolist’s profits and the derivation of a mild unimodality condition for the monopolist’s objective function that generalizes the widely used increasing generalized failure rate (IGFR) condition. A direct byproduct is a distribution free and tight bound on the probability of no trade between the supplier and the retailers.

When we compare optimal prices between markets with different demand characteristics, the main implication of the above characterization is that it allows us to exploit various forms of knowledge on the demand distribution via the theory of stochastic orderings. Specifically, if two markets can be ordered in terms of their mean residual demand function, then the seller’s optimal prices can be ordered accordingly. This establishes a link between the price elasticity of expected demand, which is naturally the critical determinant of price movements in response to changes in demand, and some well-understood characteristics of the demand distribution. The stochastic orders approach works under various informational assumptions on the demand distribution and provides a way to systematically exploit the abundance of data that firms possess about historical price/demand.

From a managerial perspective, our study provides a tractable theoretical framework which can be used to reason about price changes in advance of anticipated market movements or to benchmark data-driven predictions that are derived from pricing analytics. Our results suggest that the effects of market size and demand variability on prices critically depend on the notions of size and variability that will be employed. This implies that exact predictions about price movements can only be done in a case by case basis and should only be used with caution. Such tools are particularly useful in industries in which fixing a price often precedes the demand realization such as subscription based businesses or businesses that sell durable goods, tickets or leisure time services. More generally, our findings can be used to explain the diversity of price responses to market characteristics that are observed in practice and provide a diverse toolbox for managers to optimally set and adjust prices under different market conditions.

Acknowledgements

Stefanos Leonardos gratefully acknowledges support by the Alexander S. Onassis Public Benefit Foundation and partial support by NRF 2018 Fellowship NRF-NRFF2018-07.

References

- Ai et al. (2012) X. Ai, J. Chen, and J. Ma. Contracting with demand uncertainty under supply chain competition. Annals of Operations Research, 201(1):17–38, Dec 2012. doi:10.1007/s10479-012-1227-x.

- Bagnoli and Bergstrom (2005) M. Bagnoli and T. Bergstrom. Log-concave probability and its applications. Economic Theory, 26(2):445–469, 2005. doi:10.1007/s00199-004-0514-4.

- Banciu and Mirchandani (2013) M. Banciu and P. Mirchandani. Technical note – new results concerning probability distributions with increasing generalized failure rates. Operations Research, 61(4):925–931, 2013. doi:10.1287/opre.2013.1198.

- Belzunce et al. (2013) F. Belzunce, C. Martínez-Riquelme, and J.M. Ruiz. On sufficient conditions for mean residual life and related orders. Computational Statistics & Data Analysis, 61:199–210, 2013. doi:10.1016/j.csda.2012.12.005.

- Belzunce et al. (2016) F. Belzunce, C. Martinez-Riquelme, and J. Mulero. Chapter 2: Univariate stochastic orders. In F. Belzunce, C. Martínez-Riquelme, and J. Mulero, editors, An Introduction to Stochastic Orders, pages 27 – 113. Academic Press, 2016. doi:10.1016/B978-0-12-803768-3.00002-8.

- Berbeglia et al. (2019) G. Berbeglia, G. Rayaprolu, and A. Vetta. Pricing policies for selling indivisible storable goods to strategic consumers. Annals of Operations Research, 274(1):131–154, Mar 2019. doi:10.1007/s10479-018-2916-x.

- Bernstein and Federgruen (2005) F. Bernstein and A. Federgruen. Decentralized Supply Chains with Competing Retailers Under Demand Uncertainty. Management Science, 51(1):18–29, 2005. doi:10.1287/mnsc.1040.0218.

- Bradley and Gupta (2003) D. Bradley and R. Gupta. Limiting behaviour of the mean residual life. Annals of the Institute of Statistical Mathematics, 55(1):217–226, 2003. doi:10.1007/BF02530495.

- Chen et al. (2004) F. Y. Chen, H. Yan, and L. Yao. A newsvendor pricing game. IEEE Transactions on Systems, Man, and Cybernetics - Part A: Systems and Humans, 34(4):450–456, 2004. doi:10.1109/TSMCA.2004.826290.

- Chen et al. (2017) H. Chen, M. Hu, and G. Perakis. Distribution-Free Pricing. Mimeo, Available at SSRN, 2017.

- Chen et al. (2018) L. Chen, G. Nan, and M. Li. Wholesale Pricing or Agency Pricing on Online Retail Platforms: The Effects of Customer Loyalty. International Journal of Electronic Commerce, 22(4):576–608, 2018. doi:10.1080/10864415.2018.1485086.

- Cohen et al. (2016) M. C. Cohen, G. Perakis, and R. S. Pindyck. Pricing with Limited Knowledge of Demand. In Proceedings of the 2016 ACM Conference on Economics and Computation, EC ’16, page 657, 2016. doi:10.1145/2940716.2940734.

- Colombo and Labrecciosa (2012) L. Colombo and P. Labrecciosa. A note on pricing with risk aversion. European Journal of Operational Research, 216(1):252–254, 2012. ISSN 0377-2217. doi:10.1016/j.ejor.2011.07.027.

- Dana (2001) J.D. Dana. Monopoly price dispersion under demand uncertainty. International Economic Review, 42(3):649–670, 2001. URL http://www.jstor.org/stable/827024.

- De Wolf and Smeers (1997) D. De Wolf and Y. Smeers. A Stochastic Version of a Stackelberg-Nash-Cournot Equilibrium Model. Management Science, 43(2):190–197, 1997. doi:10.1287/mnsc.43.2.190.

- Dong et al. (2019) L. Dong, X. Guo, and D. Turcic. Selling a Product Line Through a Retailer When Demand Is Stochastic: Analysis of Price-Only Contracts. Manufacturing & Service Operations Management, 21(4):742–760, 2019. doi:10.1287/msom.2018.0720.

- Guess and Proschan (1988) F. Guess and F. Proschan. Mean residual life: theory and applications. In P. R. Krishnaiah and C. R. Rao, editors, Quality Control and Reliability, volume 7 of Handbook of Statistics, pages 215–224. Elsevier Amsterdam, 1988. doi:10.1016/S0169-7161(88)07014-2.

- Hall and Wellner (1981) W. Hall and J. Wellner. Mean residual life. In M. Csørgø, D. A. Dawson, J. N. K. Rao, and A. K. Md. E. Saleh, editors, Proceedings of the International Symposium on Statistics and Related Topics, pages 169–184. North Holland Amsterdam, 1981.

- Harris and Raviv (1981) M. Harris and A. Raviv. A Theory of Monopoly Pricing Schemes with Demand Uncertainty. The American Economic Review, 71(3):347–365, 1981. doi:10.2307/1802784.

- Huang et al. (2013) J. Huang, M. Leng, and M. Parlar. Demand functions in decision modeling: A comprehensive survey and research directions. Decision Sciences, 44(3):557–609, 2013. doi:10.1111/deci.12021.

- Hwang et al. (2018) W. Hwang, N. Bakshi, and V. DeMiguel. Wholesale Price Contracts for Reliable Supply. Production and Operations Management, 27(6):1021–1037, 2018. doi:10.1111/poms.12848.

- Jones (2009) C. Jones. Kumaraswamy’s distribution: A beta-type distribution with some tractability advantages. Statistical Methodology, 6:70–81, 2009. doi:10.1016/j.stamet.2008.04.001.

- Kocabıyıkoğlu and Popescu (2011) A. Kocabıyıkoğlu and I. Popescu. An Elasticity Approach to the Newsvendor with Price-Sensitive Demand. Operations Research, 59(2):301–312, 2011. doi:10.1287/opre.1100.0890.

- Koki et al. (2018) C. Koki, S. Leonardos, and C. Melolidakis. Comparative Statics via Stochastic Orderings in a Two-Echelon Market with Upstream Demand Uncertainty, pages 331–343. Springer International Publishing, Cham, 2018. doi:10.1007/978-3-030-00473-6_36.

- Kouvelis et al. (2018) P. Kouvelis, G. Xiao, and N. Yang. On the Properties of Yield Distributions in Random Yield Problems: Conditions, Class of Distributions and Relevant Applications. Production and Operations Management, 27(7):1291–1302, 2018. doi:10.1111/poms.12869.

- Krishnan (2010) H. Krishnan. A note on demand functions with uncertainty. Operations Research Letters, 38(5):436–440, 2010. doi:10.1016/j.orl.2010.06.001.

- Kyparisis and Koulamas (2018) G.J. Kyparisis and C. Koulamas. The price-setting newsvendor with nonlinear salvage revenue and shortage cost. Operations Research Letters, 46(1):64–68, 2018. doi:10.1016/j.orl.2017.11.001.

- Lai and Xie (2006) C.-D. Lai and M. Xie. Stochastic Ageing and Dependence for Reliability. Springer Science + Business Media, Inc., 2006.

- Lariviere (1999) M.A. Lariviere. Supply Chain Contracting and Coordination with Stochastic Demand. In S. Tayur, R. Ganeshan, and M. Magazine, editors, Quantitative Models for Supply Chain Management, pages 233–268. Springer US, Boston, MA, 1999. doi:10.1007/978-1-4615-4949-9_8.

- Lariviere (2006) M.A. Lariviere. A Note on Probability Distributions with Increasing Generalized Failure Rates. Operations Research, 54(3):602–604, 2006. doi:10.1287/opre.1060.0282.

- Lariviere and Porteus (2001) M.A. Lariviere and E. Porteus. Selling to the Newsvendor: An Analysis of Price-Only Contracts. Manufacturing & Service Operations Management, 3(4):293–305, 2001. doi:10.1287/msom.3.4.293.9971.

- Leonardos and Melolidakis (2020) S. Leonardos and C. Melolidakis. A Class of Distributions for Linear Demand Markets. arXiv e-prints, 2020. URL https://arxiv.org/abs/1805.06327.

- Leonardos and Melolidakis (2020a) S. Leonardos and C. Melolidakis. On the Equilibrium Uniqueness in Cournot Competition with Demand Uncertainty. The B.E. Journal of Theoretical Economics, 20(2):20190131, 2020a. doi:10.1515/bejte-2019-0131.

- Leonardos and Melolidakis (2020b) S. Leonardos and C. Melolidakis. Endogenizing the Cost Parameter in Cournot Oligopoly. International Game Theory Review, 22(02):2040004, 2020b. doi:10.1142/S0219198920400046.

- Leonardos and Melolidakis (2021) S. Leonardos and C. Melolidakis. On the Mean Residual Life of Cantor-Type Distributions: Properties and Economic Applications. Austrian Journal of Statistics, 50(4):65–77, 2021. doi:10.17713/ajs.v50i4.1118.