Bayesian Dynamic Tensor Regression††thanks: We are grateful to Federico Bassetti, Sylvia Frühwirth-Schnatter, Christian Gouriéroux, Søren Johansen, Siem Jan Koopman, Gary Koop, André Lucas, Alain Monfort, Peter Phillips, Christian Robert, Mike West, for their comments and suggestions. Also, we thank the seminar participants at: CREST, University of Southampton, Vrije University of Amsterdam, London School of Economics, Maastricht University, Polytechnic University of Milan. Moreover, we thank the conference and workshop participants at: “ICEEE 2019” in Lecce, 2019, “CFENetwork 2018” in Pisa, 2018, “29th EC2 conference” in Rome, 2018, “12th RCEA Annual meeting” in Rimini, 2018, “8th MAF” in Madrid, 2018, “CFENetwork 2017” in London, 2017, “ICEEE 2017” in Messina, 2017, “3rd Vienna Workshop on High-dimensional Time Series in Macroeconomics and Finance” in Wien, 2017, “BISP10” in Milan, 2017, “ESOBE” in Venice, 2016, “CFENetwork” in Seville, 2016, and the “SIS Intermediate Meeting” of the Italian Statistical Society in Florence, 2016. This research used the SCSCF multiprocessor cluster system and is part of the project Venice Center for Risk Analytics (VERA) at Ca’ Foscari University of Venice.

Abstract

Tensor-valued data are becoming increasingly available in economics and this calls for suitable econometric tools. We propose a new dynamic linear model for tensor-valued response variables and covariates that encompasses some well-known econometric models as special cases. Our contribution is manifold. First, we define a tensor autoregressive process (ART), study its properties and derive the associated impulse response function. Second, we exploit the PARAFAC low-rank decomposition for providing a parsimonious parametrization and to incorporate sparsity effects. We also contribute to inference methods for tensors by developing a Bayesian framework which allows for including extra-sample information and for introducing shrinking effects. We apply the ART model to time-varying multilayer networks of international trade and capital stock and study the propagation of shocks across countries, over time and between layers.

Keywords: Tensor calculus; multidimensional autoregression; Bayesian statistics; sparsity; dynamic networks; international trade

1 Introduction

The increasing availability of long time series of complex-structured data, such as multidimensional tables ([8], [21]), multidimensional panel data ([11], [9], [24], [59]), multilayer networks ([3], [57]), EEG ([50]), neuroimaging ([68]) has put forward some limitations of the existing multivariate econometric models. Tensors, i.e. multidimensional arrays, are the natural class where this kind of complex data belongs.

A naïve approach to model tensors relies on reshaping them into lower-dimensional objects (e.g., vectors and matrices) which can then be easily handled using standard multivariate statistical tools. However, mathematical representations of tensor-valued data in terms of vectors have non-negligible drawbacks, such as the difficulty of accounting for the intrinsic structure of the data (e.g., cells of a matrix representing a geographical map or pairwise relations, contiguous pixels in an image). Neglecting this information in the modelling might lead to inefficient estimation and misleading results. Tensor-valued data entries are highly likely to depend on contiguous cells (within and between modes) and collapsing the data into a vector destroys this information. Thus, statistical approaches based on vectorization are unsuited for modelling tensor-valued data.

Tensors have been recently introduced in statistics and machine learning (e.g., [38], [48]) and provide a fundamental background for efficient algorithms in Big Data handling (e.g., [23]). However, a compelling statistical approach extending results for scalar random variables to multidimensional random objects beyond dimension 2 (i.e., matrix-valued random variables, see [37]) is lacking and constitutes a promising field of research.

The development of novel statistical methods able to deal directly with tensor-valued data (i.e., without relying on vectorization) is currently an open field of research in statistics and econometrics, where such kind of data is becoming increasingly available. The main purpose of this article is to contribute to this growing literature by proposing an extension of standard multivariate econometric regression models to tensor-valued response and covariates.

Matrix-valued statistical models have been widely employed in time series econometrics over the past decades, especially for state space representations ([39]), dynamic linear models ([21], [63]), Gaussian graphical models ([20]), stochastic volatility ([61], [35], [34]), classification of longitudinal datasets ([62]), models for network data ([29], [70], [71]) and factor models ([22]).

[27] proposed a bilinear multiplicative matrix regression model, which in vector form becomes a VAR() with restrictions on the covariance matrix. The main shortcoming in using bilinear models is the difficulty in introducing sparsity. Imposing zero restrictions on a subset of the reduced form coefficients implies zero restrictions on the structural coefficients.

Recent papers dealing with tensor-valued data include [68] and [64], who proposed a generalized linear model to predict a scalar real or binary outcome by exploiting the tensor-valued covariate. Instead, [66], [67] and [43] followed a Bayesian nonparametric approach for regressing a scalar on tensor-valued covariate. Another stream of the literature considers regression models with tensor-valued response and covariates. In this framework, [50] proposed a model for cross-sectional data where response and covariates are tensors, and performed sparse estimation by means of the envelope method and iterative maximum likelihood. [41] exploited a multidimensional analogue of the matrix SVD (the Tucker decomposition) to define a parsimonious tensor-on-tensor regression.

We propose a new dynamic linear regression model for tensor-valued response and covariates. We show that our framework admits as special cases Bayesian VAR models ([60]), Bayesian panel VAR models ([16]) and Multivariate Autoregressive Index models (i.e. MAI, see [19]), as well as univariate and matrix regression models. Furthermore, we exploit a suitable tensor decomposition for providing a parsimonious parametrization, thus making inference feasible in high-dimensional models. One of the areas where these models can find application is network econometrics.

Most statistical models for network data are static ([26]), whereas dynamic models maybe more adequate for many applications (e.g., banking) where data on network evolution are becoming available. Few attempts have been made to model time-varying networks (e.g., [42], [47], [4]), and most of the contributions have focused on providing a representation and a description of temporally evolving graphs. We provide an original study of time-varying economic and financial networks and show that our model can be successfully used to carry out impulse response analysis in this multidimensional setting.

The remainder of this paper is organized as follows. Section 2 provides an introduction to tensor algebra and presents the new modelling framework. Section 3 discusses parametrization strategies and a Bayesian inference procedure. Section 4 provides an empirical application and section 5 gives some concluding remarks. Further details and results are provided in the supplementary material.

2 A Dynamic Tensor Model

In this section, we present a dynamic tensor regression model and discuss some of its properties and special cases. We review some notions of multilinear algebra which will be used in this paper, and refer the reader to Appendix A and the supplement for further details.

2.1 Tensor Calculus and Decompositions

The use of tensors is well established in physics and mechanics (e.g., see [7] and [2]), but few contributions have been made beyond these disciplines. For a general introduction to the algebraic properties of tensor spaces, see [38]. Noteworthy introductions to operations on tensors and tensor decompositions are [49] and [45], respectively.

A -order real-valued tensor is a -dimensional array with entries with and . The order is the number of dimensions (also called modes). Vectors and matrices are examples of 1- and 2-order tensors, respectively. In the rest of the paper we will use lower-case letters for scalars, lower-case bold letters for vectors, capital letters for matrices and calligraphic capital letters for tensors. We use the symbol “” to indicate selection of all elements of a given mode of a tensor. The mode- fiber is the vector obtained by fixing all but the -th index of the tensor, i.e. the equivalent of rows and columns in a matrix. Tensor slices and their generalizations, are obtained by keeping fixed all but two or more dimensions of the tensor.

It can be shown that the set of -order tensors endowed with the standard addition and scalar multiplication , with , is a vector space. We now introduce some operators on the set of real tensors, starting with the contracted product, which generalizes the matrix product to tensors. The contracted product between and with , is denoted by and yields a -order tensor , with entries

When is a vector, the contracted product is also called mode- product. We define with a sequence of contracted products between the -order tensor and the -order tensor . Entry-wise, it is defined as

Note that the contracted product is not commutative. The outer product between a -order tensor and a -order tensor is a -order tensor with entries .

Tensor decompositions allow to represent a tensor as a function of lower dimensional variables, such as matrices of vectors, linked by suitable multidimensional operations. In this paper, we use the low-rank parallel factor (PARAFAC) decomposition, which allows to represent a -order tensor in terms of a collection of vectors (called marginals). A -order tensor is of rank 1 when it is the outer product of vectors. Let be the rank of the tensor , that is minimum number of rank-1 tensors whose linear combination yields . The PARAFAC() decomposition is rank- decomposition which represents a -order tensor as a finite sum of rank- tensors defined by the outer products of vectors (called marginals)

| (1) |

The mode- matricization (or unfolding), denoted by , is the operation of transforming a -dimensional array into a matrix. It consists in re-arranging the mode- fibers of the tensor to be the columns of the matrix , which has size with . The mode- matricization of maps the element of to the element of , where . For some numerical examples, see [45] and Appendix A. The mode- unfolding is of interest for providing a visual representation of a tensor: for example, when be a 3-order tensor, its mode- matricization is a matrix obtained by horizontally stacking the mode- slices of the tensor. The vectorization operator stacks all the elements in direct lexicographic order, forming a vector of length . Other orderings are possible, as long as it is consistent across the calculations. The mode- matricization can also be used to vectorize a tensor , by exploiting the relationship , where stacks vertically into a vector the columns of the matrix . Many product operations have been defined for tensors (e.g., see [49]), but here we constrain ourselves to the operators used in this work. For the ease of notation, we will use the multiple-index summation for indicating the sum over all the corresponding indices.

Remark 2.1.

Consider a -order tensor with a PARAFAC(R) decomposition (with marginals ), a -order tensor and a vector . Then

where .

2.2 A General Dynamic Tensor Model

Let be a -dimensional tensor of endogenous variables, a -dimensional tensor of covariates, and and sets of -tuples of integers. We define the autoregressive tensor model of order , ART(), as the system of equations

| (2) |

, with given initial conditions , where and is the -th entry of . The general model in eq. (2) allows for measuring the effect of all the cells of and of the lagged values of on each endogenous variable.

We give two equivalent compact representations of the multilinear system (2). The first one is used for studying the stability property of the process and is obtained through the contracted product that provides a natural setting for multilinear forms, decompositions and inversions. From (2) one gets the tensor equation

| (3) |

where is a shorthand notation for the contracted product , is a -order tensor of the same size as , , , are -order tensors of size and is a -order tensor of size . The error term follows a -order tensor normal distribution ([54]) with probability density function

| (4) |

where and , and are -order tensors of size . Each covariance matrix , , accounts for the dependence along the corresponding mode of .

The second representation of the ART() in eq. (2) is used for developing inference. Let be the -dimensional commutation tensor such that , where is the tensor obtained by flipping the modes of . Define the -dimensional tensor and the -dimensional tensor , with . We obtain and the compact representation

| (5) |

Let be the space of -dimensional tensors endowed with the contracted product . We define the identity tensor to be the neutral element of , that is the tensor whose entries are if for all and otherwise. The inverse of a tensor is the tensor satisfying . A complex number and a nonzero tensor are called eigenvalue and eigenvector of the tensor if they satisfy the multilinear equation . We define the spectral radius of to be the largest modulus of the eigenvalues of . We define a stochastic process to be weakly stationary if the first and second moment of its finite dimensional distributions are finite and constant in . Finally, note that it is always possible to rewrite an ART() process as a ART(1) process on an augmented state space, by stacking the endogenous tensors along the first mode. Thus, without loss of generality, we focus on the case . We use the definition of inverse tensor, spectral radius and the convergence of power series of tensors to prove the following result.

Lemma 2.1.

Every -dimensional ART() process can be rewritten as a -dimensional ART(1) process .

Proposition 2.1 (Stationarity).

If and the process is weakly stationary, then the ART process in eq. (3), with , is weakly stationary and admits the representation

2.3 Parametrization

The unrestricted model in eq. (5) cannot be estimated, as the number of parameters greatly outmatches the available data. We address this issue by assuming a PARAFAC() decomposition for the tensor coefficients, which makes the estimation feasible by reducing the dimension of the parameter space. The models in eqq. (5)-(3) are equivalent but the assuming a PARAFAC decomposition for the coefficient tensors leads to different degrees of parsimony, as shown in the following remark.

Remark 2.2 (Alternative parametrization via contracted product).

The two models (5) and (3) combined with the PARAFAC decomposition for the tensor coefficients allow for different degree of parsimony. To show this, without loss of generality, focus on the coefficient tensor (similar argument holds for , and ). By assuming a PARAFAC() decomposition for in (3) and for in (5), we get, respectively

The length of the vectors and coincide for each . However, has length while have length , respectively. Therefore, the number of free parameters in the coefficient tensor is , while it is for . This highlights the greater parsimony granted by the use of the PARAFAC() decomposition in model (3) as compared to model (5).

Remark 2.3 (Vectorization).

There is a relation between the -dimensional ART() and a -dimensional VAR() model. The vector form of (5) is

| (6) |

where the constraint on the covariance matrix stems from the one-to-one relation between the tensor normal distribution for and the distribution of its vectorization ([54]) given by if and only if . The restriction on the covariance structure for the vectorized tensor provides a parsimonious parametrization of the multivariate normal distribution, while allowing both within and between mode dependence. Alternative parametrizations for the covariance lead to generalizations of standard models. For example, assuming an additive covariance structure results in the tensor ANOVA. This is an active field for further research.

Example 2.1.

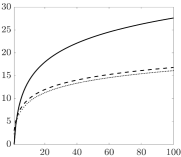

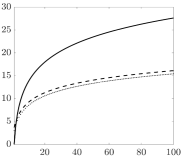

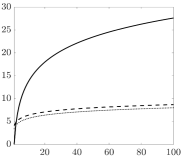

For the sake of exposition, consider the model in eq. (5), where , the response is a 3-order tensor and the covariates include only a constant coefficient tensor . Define by the number of parameters of the noise distribution. The total number of parameters to estimate in the unrestricted case is , with in this example. Instead, in a ART model defined via the mode- product in eq. (5), assuming a PARAFAC() decomposition on the total number of parameters is . Finally, in the ART model defined by the contracted product in eq. (3) with a PARAFAC() decomposition on the number of parameters is . A comparison of the different parsimony granted by the PARAFAC decomposition in all models is illustrated in Fig. 1.

| (a) vectorized | (b) contracted product as (5) | (c) contracted product as (3) |

|---|---|---|

|

|

|

The structure of the PARAFAC decomposition poses an identification problem for the marginals , which may arise from three sources:

-

(i)

scale identification, since for any collection such that ;

-

(ii)

permutation identification, since for any permutation of the indices the outer product of the original vectors is equal to that of the permuted ones;

-

(iii)

orthogonal transformation identification, since for any orthonormal matrix .

Note that in our framework these issues do not hamper the inference, since our object of interest is the coefficient tensor , which is exactly identified. The marginals have no interpretation, as the PARAFAC decomposition is assumed on the coefficient tensor for the sake of providing a parsimonious parametrization.

2.4 Important Special Cases

The model in eq. (5) is a generalization of several well-known econometric models, as shown in the following remarks. See the supplement for the proofs of these results.

Remark 2.4 (Univariate).

Remark 2.5 (SUR).

Remark 2.6 (VARX and Panel VAR).

Consider the setup of Remark 2.5. If , then weoobtain a VARX(1) model, with restricted covariance matrix. Another vector of regressors may enter the regression (8) pre-multiplied (along mode-) by a tensor . Therefore, model (5) encompasses as a particular case also the panel VAR models of [16], [18], [17], provided that we make the same restriction on .

Remark 2.7 (VECM).

The model in eq. (5) generalises the Vector Error Correction Model (VECM) widely used in multivariate time series analysis (see [31], [58]). Consider a -dimensional VAR(1) model

Defining and , where and are matrices of rank , we obtain the associated VECM

| (9) |

This is used for studying the cointegration relations among the components of . Since , we can interpret the VECM model in eq. (9) as a particular case of the model in eq. (5) where the coefficient is the matrix . Furthermore by writing we can interpret this relation as a rank-R PARAFAC decomposition of . Following this analogy, the PARAFAC rank corresponds to the cointegration rank, are the mean-reverting coefficients and are the cointegrating vectors. See the supplement for details. This interpretation opens the way to reparametrization of based on tensor SVD representations, and to the application of regularization methods in the spirit of [10]. This is beyond the scope of the paper, thus we leave it for further research.

Remark 2.8 (MAI of [19]).

The multivariate autoregressive index model (MAI) of [19] is another special case of model (5). A MAI is a VAR model with a low rank decomposition imposed on the coefficient matrix, as follows

where is a vector, whereas are and matrices, respectively. In [19], the authors assumed . This corresponds to our parametrization using and defining and , which leads us to .

Remark 2.9 (Tensor autoregressive model (ART)).

By removing all the covariates from eq. (5) except the lags of the dependent variable, we obtain a tensor autoregressive model of order (or ART())

| (10) |

2.5 Impulse Response Analysis

In this section we derive two impulse response functions (IRF) for ART models, the block Cholesky IRF and the block generalised IRF, exploiting the relationship between ART and VAR models. Without loss of generality, we focus on the ART() model in eq. (10), with and , and introduce the following notation. Let and be the tensor response and noise term in vector form, respectively, where is the covariance of the model in vector form and . Partition in blocks as

| (11) |

where is , is and is . Then, denoting by the Schur complement of , the LDU decomposition of is

Hence can be block-diagonalised

| (12) |

From the Cholesky decomposition of one obtains a block Cholesky decomposition

where are the Cholesky factors of and , respectively. Assume the vectorised ART process admits an infinite MA representation, with and , then using the previous results we get:

| (13) |

where are the block-orthogonalised shocks and is the block-diagonal matrix in eq. (12). Denote with the matrix that selects columns from a pre-multiplying matrix, i.e. is a matrix containing columns of . Denote with a -dimensional vector of shocks. Using the property of the multivariate Normal distribution, and recalling that the top-left block of size of is , we extend the generalised IRF of [46] and [56] by defining the block generalised IRF

| (14) |

where is the natural filtration associated to the stochastic process. Starting from eq. (13) we derive the block Cholesky IRF (OIRF) as

| (15) |

Define with the -th column of the -dimensional identity matrix. The impact of a shock to the -th variable on all variables is given below in eq. (16), whereas the impact of a shock to the -th variable on the -th variable is given in eq. (17).

| (16) | |||||||

| (17) |

Finally, denoting , we have the compact notation

3 Bayesian Inference

In this section, without loss of generality, we present the inference procedure for a special case of the model in eq. (5), given by

| (18) |

Here is a -order tensor response of size , and is thus a -order coefficient tensor of size , with . This is a -order tensor autoregressive model of lag-order , or ART(), coinciding with eq. (10) for and . The noise term has as tensor normal distribution, with zero mean and covariance matrices of sizes , and , respectively, accounting for the covariance along each of the three dimensions of . The specification of a tensor model with a tensor normal noise instead of a vector model (like a Gaussian VAR) has the advantage of being more parsimonious. By vectorising (18), we get the equivalent VAR

| (19) |

whose covariance has a Knocker structure, which contains parameters (as opposed to of an unrestricted VAR) and allows for heteroskedasticity.

The choice the Bayesian approach for inference is motivated by the fact that the large number of parameters may lead to an overfitting problem, especially when the samples size is rather small. This issue can be addressed by the indirect inclusion of parameter restrictions through a suitable specification of the corresponding prior distributions. In the unrestricted model (18) it would be necessary to define a prior distribution on the -order tensor . The literature on tensor-valued distributions is limited to the elliptical family (e.g., [54]), which includes the tensor normal and tensor . Both distributions do not easily allow for the specification of restrictions on a subset of the entries of the tensor, hampering the use of standard regularization prior distributions (such as shrinkage priors).

The PARAFAC() decomposition of the coefficient tensor provides a way to circumvent this issue. This decomposition allows to represent a tensor through a collection of vectors (the marginals), for which many flexible shrinkage prior distributions are available. Indirectly, this introduces a priori sparsity on the coefficient tensor.

3.1 Prior Specification

The choice of the prior distribution on the PARAFAC marginals is crucial for recovering the sparsity pattern of the coefficient tensor and for the efficiency of the inference. Global-local prior distributions are based on scale mixtures of normal distributions, where the different components of the covariance matrix govern the amount of prior shrinkage. Compared to spike-and-slab distributions (e.g., [52], [33], [44]) which become infeasible as the parameter space grows, global-local priors have better scalability properties in high-dimensional settings. They do not provide automatic variable selection, which can nonetheless be obtained by post-estimation thresholding ([55]).

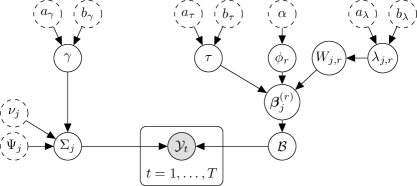

Motivated by these arguments, we define a global-local shrinkage prior for the marginals of the coefficient tensor following the hierarchical prior specification of [36] (see also [13], [69]). For each , we define a prior distributions as a scale mixture of normals centred in zero, with three components for the covariance. The global parameter governs the overall variance, the middle parameter defines the common shrinkage for the marginals in -th component of the PARAFAC, and the local parameter drives the shrinkage of each entry of each marginal. Summarizing, for , ( in eq. (18)) and , the hierarchical prior structure111We use the shape-rate formulation for the gamma distribution. for each vector of the PARAFAC() decomposition in eq. (1) is

| (20) | ||||

where is the vector of ones of length and we assume and . The conditional prior distribution of a generic entry of is the law of a sum of product Normals222A product Normal is the distribution of the product of independent centred Normal random variables.: it is symmetric around zero, with fatter tails than both a standard Gaussian or a standard Laplace distribution (see the supplement for further details). Note that a product Normal prior promotes sparsity due to the peak at zero. The following result characterises the conditional prior distribution of an entry of the coefficient tensor induced by the hierarchical prior in eq. (20). See the supplement for the proof.

Lemma 3.1.

Let , where , and let , , and . Under the prior specification in (20), the generic entry of the coefficient tensor has the conditional prior distribution

where denotes convolution and

with a Meijer G-function and

The use of Meijer G- and Fox H-functions is not new in econometrics (e.g., [1]), and they have been recently used for defining prior distributions in Bayesian statistics ([6], [5]).

From eq. (4), we have that the covariance matrices enter the likelihood in a multiplicative way, therefore separate identification of their scales requires further restrictions. [63] and [28] adopt independent hyper-inverse Wishart prior distributions ([25]) for each , then impose the identification restriction for . The hard constraint (where is the identity matrix of size ), for all but one , implicitly imposes that the dependence structure within different modes is the same, but there is no dependence between modes. We follow [40], who suggests to introduce dependence between the Inverse Wishart prior distribution of each via a hyper-parameter affecting their prior scale. To account for marginal dependence, we add a level of hierarchy, thus obtaining

| (21) |

Define and , and let denote the collection of all parameters. The directed acyclic graph (DAG) of the prior structure is given in Fig. 2.

Note that our prior specification is flexible enough to include Minnesota-type restrictions or hierarchical structures as in [16].

3.2 Posterior Computation

Define , , and , with . The likelihood function of model (18) is

| (22) |

where . Since the posterior distribution is not tractable in closed form, we adopt an MCMC procedure based on Gibbs sampling. The technical details of the derivation of the posterior distributions are given in Appendix B. We articulate the sampler in three main blocks:

-

(I)

sample the global and middle variance hyper-parameters of the marginals, from

(23) (24) where , then set . For improving the mixing, we sample with a Hamiltonian Monte Carlo (HMC) step ([53]).

-

(II)

sample the hyper-parameters of the local variance component of the marginals and the marginals themselves, from

(25) (26) (27) -

(III)

sample the covariance matrices and the latent scale, respectively, from

(28) (29)

4 Application to Multilayer Dynamic Networks

We apply the proposed methodology to study jointly the dynamics of international trade and credit networks. The international trade network has been previously studied by several authors (e.g., [32], [30]), but to the best of our knowledge, this is the first attempt to model the dynamics of two networks jointly. The bilateral trade data come from the COMTRADE database, whereas the data on bilateral outstanding capital come from the Bank of International Settlements database. Our sample of yearly observations for 10 countries runs from 2003 to 2016. At at each time , the -order tensor has size and represents a -layer node-aligned network (or multiplex) with vertices (countries), where each edge is given by a bilateral trade flow or financial stock. See the supplement for data description

We estimate the tensor autoregressive model in eq. (18), using the prior structure described in section 3, running the Gibbs sampler for iterations after burn-in iterations. We retain every second draw for posterior inference.

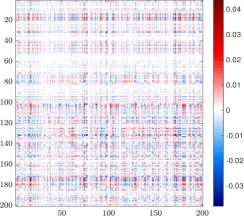

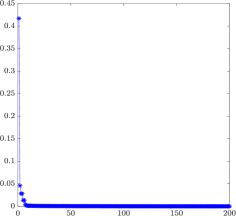

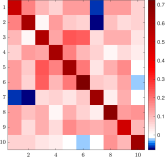

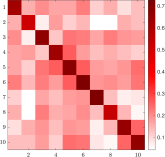

The mode- matricization of the estimated coefficient tensor, , is shown in the left panel of Fig. 3. The -th entry of the matrix reports the impact of the edge on edge (in vectorised form333For example, and corresponds to the coefficient of entry on .). The first rows/columns correspond to the edges in the first layer. Hence, two rows of the matricized coefficient tensor are similar when two edges are affected by all the edges of the (lagged) network in a similar way, whereas two similar columns identify the situation where two edges impact the (next period) network in a similar way. The overall distribution of the estimated entries of is symmetric around zero and leptokurtic, as a consequence of the shrinkage to zero of the estimated coefficients. The right panel of Fig. 3 shows the log-spectrum of . As all eigenvalues of have modulus smaller than one, we conclude that the estimated ART() model is stationary444It can be shown that the stationarity of the mode- matricised coefficient tensor implies stationarity of the ART() process.. Fig. 4 shows the estimated covariance matrices. In all cases, the highest values correspond to individual variances, while the estimated covariances are lower in magnitude and heterogeneous. We also find evidence of heterogeneity in the dependence structure, since , which captures the covariance between rows (i.e., exporting and creditor countries), differs from , which describes the covariance between columns (i.e., importing and debtor countries). With few exceptions, estimated covariances are positive.

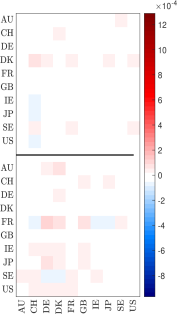

After estimating the ART() model (18), we may investigate shock propagation across the network computing generalised and orthogonalised impulse response functions presented in equations (14) and (15), respectively. Impulse responses allow us to analyze the propagation of shocks both across the network, within and across layers, and over time. For illustration, we study the responses to a shock in all edges of country, by applying block Cholesky factorisation to , in such a way that the shocked country contemporaneously affects all others and not vice-versa.555To save space, we do not report generalised IRFs, which are very similar to the ones presented. Thus, the matrices and in eq. (11) reflect contemporaneous correlations across transactions of the shock-originating country and with transactions of all other countries, respectively. For expositional convenience, we report only statistically significant responses.

In the first analysis we consider a negative shock to US trade imports666That is, we allocate the shock across import originating countries to match import shares as in the last period of the sample.. The results of the block Cholesky IRF at horizon are given in Fig. 5. We report the impact on the whole network (panel (a)) and, for illustrative purposes, the impact on Germany’s transactions. The main findings follows.

Global effect on the network. The negative shock to US imports has an effect on both layers (trade and financial) of the network. There is evidence of heterogeneous responses across countries and country-specific transactions. On average, trade flows exhibit a slight expansion in response to the shock. Switzerland is the most positively affected, both in terms of exports and imports, and trade imports of the US show (on average) a reverted positive response one period after the shock. This reflects an oscillating impulse response. The overall average effect on the financial layer is negative, similar in magnitude to the effect on the trade layer. More specifically, we observe that Denmark’s and Sweden’s exports to Switzerland, Germany and France show a contraction, whereas the effect on US’, Japan’s and Ireland’s exports to these countries is positive. We may interpret these effects as substitution effects: The decreasing share of Denmark’s and Sweden’s exports to Switzerland, Germany and France is offset by an increase of US, Japanese and Irish exports. In conclusion, the dynamic model can be used for predicting possible trade creation and diversion effects (e.g., see [14]).

Local effect on Germany. In panel (b) of Fig. 5 we report the response of Germany’s transactions to the negative shock in US imports. The effects on imports are mixed: while Germany’s imports from most other EU countries increase, imports from Sweden and Denmark decrease. Likewise, Germany’s exports show heterogeneous responses, whereby exports to Switzerland react strongest (positively). The shock of US imports does not have a significant impact on Germany’s outstanding credit against most countries (except Switzerland and Japan). On the other hand, the reactions of Germany’s outstanding debt reflect those on trade imports.

Local effect on other countries. We observe that the most affected trade transactions are those of Denmark, Japan, Ireland, Sweden and US (as exporters) vis-á-vis Switzerland and France (as importers). The financial layer mirrors these effects with opposite sign, while the magnitudes are comparable. Outstanding credit of Ireland and Japan to Switzerland, Germany and France decrease at horizon . By contrast, Denmark’s outstanding credit to these countries increases. Note that outstanding debt of US vis-á-vis almost all countries decreases after the shock. Overall, responses to a shock on US imports at horizon are heterogeneous in sign but rather low in magnitude, whereas at horizon (plot not reported) the propagation of the shock has vanished. We interpret this as a sign of fast (and monotone) decay of the IRF.

| (a) Network IRF at | |

|

Financial (layer 2) Trade (layer 1) |

|

| (b) IRF for Germany’s edges at | |||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

|

Financial (layer 2) Trade (layer 1) |

|

||||||||||||

| (a) Network IRF at | |

|

Financial (layer 2) Trade (layer 1) |

|

| (b) IRF for Germany’s edges at | |||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

|

Financial (layer 2) Trade (layer 1) |

|

||||||||||||

| (c) Network IRF at | |

|

Financial (layer 2) Trade (layer 1) |

|

| (d) IRF for Germany’s edges at | |||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

|

Financial (layer 2) Trade (layer 1) |

|

||||||||||||

| (a) Network IRF at | |

|

Financial (layer 2) Trade (layer 1) |

|

| (b) IRF for Germany’s edges at | |||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

|

Financial (layer 2) Trade (layer 1) |

|

||||||||||||

| (c) Network IRF at | |

|

Financial (layer 2) Trade (layer 1) |

|

| (d) IRF for Germany’s edges at | |||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

|

Financial (layer 2) Trade (layer 1) |

|

||||||||||||

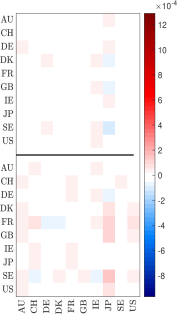

Fig. 6 shows the block Cholesky IRF at horizon , resulting from a negative shock to GB’s outstanding debt777Again, the shock is allocated across countries to reflect country-specific shares of the last period in the sample.. The main findings follow.

Global effect on the network. We observe heterogeneous effects across countries. Effects on the trade layer at horizon are equally heterogeneous, but smaller in magnitude compared with the financial layer.

Local effect on Germany. Compared with other countries, the shock has smaller effects on Germany’s trade. The negative shock to GB’s outstanding debt has a negative impact on Germany’s exports and imports to all countries but Ireland and Sweden for exports and Denmark for imports. Germany’s outstanding credit increases vis-á-vis Denmark, GB, Japan and US. Germany’s outstanding debt increases against all countries but Denmark and Sweden, in particular against France, Japan and Ireland. At horizon responses are not reverted, but nearly all effects turn insignificant, providing evidence of monotone and fast decay of the IRFs.

Local effect on other countries. On the trade layer at horizon , we observe a positive response in Denmark’s exports and on average a negative response of Switzerland’s, Ireland’s and Japan’s exports. France and Sweden are the most affected countries on the financial layer: The increase in outstanding credit of France towards Germany, Denmark and GB is counterbalanced by a reduction in Sweden’s outstanding credit towards the same countries. We observe reverse effects concerning France’s and Sweden’s outstanding credit towards Switzerland and Ireland. Finally, Ireland’s outstanding credit reacts positively towards most other countries.

Compared with responses to the shock to US imports, the persistence of a negative shock to GB’s outstanding debt is slightly stronger, see impulse responses at horizon in Fig. 6. The decay is monotonic. However, the speed of decay is heterogeneous across countries. For some countries, there are small effects at horizon 2, while for others the effects are completely wiped already. Overall, we do not find evidence of a relation between the size of a country in terms of exports or outstanding credit and the persistence in the impulse response. At the most, persistence seems determined by the origin of the shock, the effects of a financial shock being more persistent than those of a trade shock.

Finally, in Fig. 7 we plot the block Cholesky IRF, respectively, at horizon , resulting from a negative shock to GB’s outstanding debt coupled with a positive shock to GB’s outstanding credit. The main findings follow.

Global effect on the network. The results remarkably differ from the previous ones (see Fig. 6). The responses to this simultaneous shock in GB’s outstanding debt and credit are larger, in particular in the trade layer. However, already at horizon responses are nearly fully decayed. The results in Fig. 6 and Fig. 7 suggest that an increase in GB’s outstanding credit has an overall positive effect on trade, stimulating export/import activities of most other countries.

Local effect on Germany. One period after the shock, we observe an overall positive effect on German exports, the exception being towards GB, Ireland and Sweden. Imports react mostly positively. Imports from US and Ireland react most, while those from Denmark react negatively. The responses of Germany’s outstanding debt vis-á-vis most countries but Denmark and Sweden are negative, especially against France. At horizon Germany’s responses have nearly faded away, suggesting a rapid monotone decay of the shock’s effect.

Local effect on other countries. In particular, the reactions of Switzerland’s imports and outstanding debt are strikingly different from the previous case, compare with Fig. 6. Imports from US and Ireland, and to a lesser extent from France and Austria, are strongly boosted, while those from Denmark and Sweden decrease strongly. Moreover, we note that Japan’s outstanding debt increases significantly against most countries. We interpret this as a signal for Japan’s attractiveness for foreign capital. Compared with the previous exercise, France’s financial responses are now mostly insignificant, or of opposite sign. Finally, the reactions of GB’s exports and outstanding credit are heterogeneous, the latter ones being larger in absolute magnitude.

5 Conclusions

We defined a new statistical framework for dynamic tensor regression. It is a generalisation of many models frequently used in time series analysis, such as VAR, panel VAR, SUR and matrix regression models. The PARAFAC decomposition of the tensor of regression coefficients allows to reduce the dimension of the parameter space but also permits to choose flexible multivariate prior distributions, instead of multidimensional ones. Overall, this allows to encompass sparsity beliefs and to design efficient algorithm for posterior inference.

The proposed methodology has been used for analysing the temporal evolution of the international trade and financial network, and the investigation has been complemented with an impulse response analysis. We have found evidence of (i) wide heterogeneity in the sign and magnitude of the estimated coefficients; (ii) stationarity of the network process. The impulse response analysis has highlighted the role of network topology in shock propagation across countries and over time. Irrespective of its origin, any shock is found to propagate between layers, but financial shocks are more persistent than those on international trade. Moreover, we we do not find evidence of a relation between the size of a country, expressed by the total trade or capital exports, and the persistence its response to a shock. Finally, we have found evidence of substitution effects in response to the shocks, meaning that pairs of countries experience opposite effects from a shock to another country. In conclusion, our dynamic model can be used for predicting possible trade creation and diversion effects.

Supplementary Material

Supplementary material including background results on tensors, the derivation of the posterior, simulation experiments and the description of the data is available online888https://matteoiacopini.github.io/docs/BiCaIaKa_Supplement.pdf.

References

- [1] Karim M Abadir and Paolo Paruolo. Two mixed normal densities from cointegration analysis. Econometrica, pages 671–680, 1997.

- [2] Ralph Abraham, Jerrold E Marsden, and Tudor Ratiu. Manifolds, tensor analysis, and applications. Springer Science & Business Media, 2012.

- [3] Iñaki Aldasoro and Iván Alves. Multiplex interbank networks and systemic importance: an application to European data. Journal of Financial Stability, 35:17–37, 2018.

- [4] Osvaldo Anacleto and Catriona Queen. Dynamic chain graph models for time series network data. Bayesian Analysis, 12(2):491–509, 2017.

- [5] JAA Andrade and PN Rathie. Exact posterior computation in non-conjugate gaussian location-scale parameters models. Communications in Nonlinear Science and Numerical Simulation, 53:111–129, 2017.

- [6] JAA Andrade and Pushpa Narayan Rathie. On exact posterior distributions using h-functions. Journal of Computational and Applied Mathematics, 290:459–475, 2015.

- [7] Rutherford Aris. Vectors, tensors and the basic equations of fluid mechanics. Courier Corporation, 2012.

- [8] Laszlo Balazsi, Laszlo Matyas, and Tom Wansbeek. The estimation of multidimensional fixed effects panel data models. Econometric Reviews, pages 1–23, 2015.

- [9] Badi H Baltagi, Georges Bresson, and Jean-Michel Etienne. Hedonic housing prices in paris: An unbalanced spatial lag pseudo-panel model with nested random effects. Journal of Applied Econometrics, 30(3):509–528, 2015.

- [10] Nalan Baştürk, Lennart Hoogerheide, and Herman K van Dijk. Bayesian analysis of boundary and near-boundary evidence in econometric models with reduced rank. Bayesian Analysis, 12(3):879–917, 2017.

- [11] Patrick Bayer, Robert McMillan, Alvin Murphy, and Christopher Timmins. A dynamic model of demand for houses and neighborhoods. Econometrica, 84(3):893–942, 2016.

- [12] Ratikanta Behera, Ashish Kumar Nandi, and Jajati Keshari Sahoo. Further results on the drazin inverse of even order tensors. arXiv preprint arXiv:1904.10783, 2019.

- [13] Anirban Bhattacharya, Debdeep Pati, Natesh S. Pillai, and David B. Dunson. Dirichlet-Laplace priors for optimal shrinkage. Journal of the American Statistical Association, 110(512):1479–1490, 2015.

- [14] Jacob A Bikker. The gravity model in international trade: advances and applications, chapter An extended gravity model with substitution applied to international trade, pages 135–164. Cambridge University Press, 2010.

- [15] Michael Brazell, Na Li, Carmeliza Navasca, and Christino Tamon. Solving multilinear systems via tensor inversion. SIAM Journal on Matrix Analysis and Applications, 34(2):542–570, 2013.

- [16] Fabio Canova and Matteo Ciccarelli. Forecasting and turning point predictions in a Bayesian panel VAR model. Journal of Econometrics, 120(2):327–359, 2004.

- [17] Fabio Canova and Matteo Ciccarelli. Estimating multicountry VAR models. International Economic Review, 50(3):929–959, 2009.

- [18] Fabio Canova, Matteo Ciccarelli, and Eva Ortega. Similarities and convergence in G-7 cycles. Journal of Monetary Economics, 54(3):850–878, 2007.

- [19] Andrea Carriero, George Kapetanios, and Massimiliano Marcellino. Structural analysis with multivariate autoregressive index models. Journal of Econometrics, 192(2):332 – 348, 2016.

- [20] Carlos M. Carvalho, Hélène Massam, and Mike West. Simulation of hyper-inverse Wishart distributions in graphical models. Biometrika, 94(3):647–659, 2007.

- [21] Carlos M Carvalho and Mike West. Dynamic matrix-variate graphical models. Bayesian Analysis, 2(1):69–97, 2007.

- [22] Elynn Y Chen, Ruey S Tsay, and Rong Chen. Constrained factor models for high-dimensional matrix-variate time series. Journal of the American Statistical Association, ((forthcoming)), 2019.

- [23] Andrzej Cichocki. Era of Big data processing: a new approach via tensor networks and tensor decompositions. In Proceedings of the International Workshop on Smart Info-Media Systems in Asia (SISA2013), 2014.

- [24] Peter Davis. Estimating multi-way error components models with unbalanced data structures. Journal of Econometrics, 106(1):67–95, 2002.

- [25] A Philip Dawid and Steffen L Lauritzen. Hyper Markov laws in the statistical analysis of decomposable graphical models. The Annals of Statistics, 21(3):1272–1317, 1993.

- [26] Aureo De Paula. Econometrics of network models. In Advances in Economics and Econometrics: Theory and Applications, Eleventh World Congress, pages 268–323. Cambridge University Press Cambridge, 2017.

- [27] Shanshan Ding and R Dennis Cook. Matrix-variate regressions and envelope models. Journal of the Royal Statistical Society: Series B (Statistical Methodology), 80(2):387–408, 2018.

- [28] Adrian Dobra. Handbook of Spatial Epidemiology, chapter Graphical Modeling of Spatial Health Data. Chapman & Hall /CRC, first edition, 2015.

- [29] Daniele Durante and David B Dunson. Nonparametric Bayesian dynamic modelling of relational data. Biometrika, 101(4):883–898, 2014.

- [30] Jonathan Eaton and Samuel Kortum. Technology, geography, and trade. Econometrica, 70(5):1741–1779, 2002.

- [31] Robert F Engle and Clive WJ Granger. Co-integration and error correction: representation, estimation, and testing. Econometrica, pages 251–276, 1987.

- [32] Ana Cecilia Fieler. Nonhomotheticity and bilateral trade: Evidence and a quantitative explanation. Econometrica, 79(4):1069–1101, 2011.

- [33] Edward I George and Robert E McCulloch. Approaches for Bayesian variable selection. Statistica Sinica, 7:339–373, 1997.

- [34] Vasyl Golosnoy, Bastian Gribisch, and Roman Liesenfeld. The conditional autoregressive wishart model for multivariate stock market volatility. Journal of Econometrics, 167(1):211–223, 2012.

- [35] Christian Gouriéroux, Joann Jasiak, and Razvan Sufana. The wishart autoregressive process of multivariate stochastic volatility. Journal of Econometrics, 150(2):167–181, 2009.

- [36] Rajarshi Guhaniyogi, Shaan Qamar, and David B Dunson. Bayesian tensor regression. Journal of Machine Learning Research, 18(79):1–31, 2017.

- [37] Arjun K Gupta and Daya K Nagar. Matrix variate distributions. CRC Press, 1999.

- [38] Wolfgang Hackbusch. Tensor spaces and numerical tensor calculus. Springer Science & Business Media, 2012.

- [39] Jeff Harrison and Mike West. Bayesian forecasting & dynamic models. Springer, 1999.

- [40] Peter D Hoff. Separable covariance arrays via the Tucker product, with applications to multivariate relational data. Bayesian Analysis, 6(2):179–196, 2011.

- [41] Peter D Hoff. Multilinear tensor regression for longitudinal relational data. The Annals of Applied Statistics, 9(3):1169–1193, 2015.

- [42] Petter Holme and Jari Saramäki. Temporal networks. Physics Reports, 519(3):97–125, 2012.

- [43] Masaaki Imaizumi and Kohei Hayashi. Doubly decomposing nonparametric tensor regression. In International Conference on Machine Learning, pages 727–736, 2016.

- [44] Hemant Ishwaran and J Sunil Rao. Spike and slab variable selection: frequentist and Bayesian strategies. The Annals of Statistics, 33(2):730–773, 2005.

- [45] Tamara G. Kolda and Brett W. Bader. Tensor decompositions and applications. SIAM Review, 51(3):455–500, 2009.

- [46] Gary Koop, M Hashem Pesaran, and Simon M Potter. Impulse response analysis in nonlinear multivariate models. Journal of Econometrics, 74(1):119–147, 1996.

- [47] Vassilis Kostakos. Temporal graphs. Physica A: Statistical Mechanics and its Applications, 388(6):1007–1023, 2009.

- [48] Pieter M Kroonenberg. Applied multiway data analysis. John Wiley & Sons, 2008.

- [49] Namgil Lee and Andrzej Cichocki. Fundamental tensor operations for large-scale data analysis in tensor train formats. Multidimensional Systems and Signal Processing, 29(3):921–960, 2018.

- [50] Lexin Li and Xin Zhang. Parsimonious tensor response regression. Journal of the American Statistical Association, 112(519):1131–1146, 2017.

- [51] Helmut Lütkepohl. New introduction to multiple time series analysis. Springer Science & Business Media, 2005.

- [52] Toby J Mitchell and John J Beauchamp. Bayesian variable selection in linear regression. Journal of the American Statistical Association, 83(404):1023–1032, 1988.

- [53] Radford M Neal. MCMC using Hamiltonian dynamics. In Steve Brooks, Andrew Gelman, Jones L Galin, and Xiao-Li Meng, editors, Handbook of Markov Chain Monte Carlo, chapter 5. Chapman & Hall /CRC, 2011.

- [54] Martin Ohlson, M Rauf Ahmad, and Dietrich Von Rosen. The multilinear normal distribution: introduction and some basic properties. Journal of Multivariate Analysis, 113:37–47, 2013.

- [55] Trevor Park and George Casella. The Bayesian lasso. Journal of the American Statistical Association, 103(482):681–686, 2008.

- [56] H Hashem Pesaran and Yongcheol Shin. Generalized impulse response analysis in linear multivariate models. Economics Letters, 58(1):17–29, 1998.

- [57] Sebastian Poledna, José Luis Molina-Borboa, Serafín Martínez-Jaramillo, Marco Van Der Leij, and Stefan Thurner. The multi-layer network nature of systemic risk and its implications for the costs of financial crises. Journal of Financial Stability, 20:70–81, 2015.

- [58] Peter Schotman and Herman K Van Dijk. A Bayesian analysis of the unit root in real exchange rates. Journal of Econometrics, 49(1-2):195–238, 1991.

- [59] Yongcheol Shin, Laura Serlenga, and George Kapetanios. Estimation and inference for multi-dimensional heterogeneous panel datasets with hierarchical multi-factor error structure. Journal of Econometrics, (forthcoming), 2019.

- [60] Christopher A Sims and Tao Zha. Bayesian methods for dynamic multivariate models. International Economic Review, 39(4):949–968, 1998.

- [61] Harald Uhlig. Bayesian vector autoregressions with stochastic volatility. Econometrica, 65:59–73, 1997.

- [62] Cinzia Viroli. Finite mixtures of matrix normal distributions for classifying three-way data. Statistics and Computing, 21(4):511–522, 2011.

- [63] Hao Wang and Mike West. Bayesian analysis of matrix normal graphical models. Biometrika, 96(4):821–834, 2009.

- [64] Tan Xu, Zhang Yin, Tang Siliang, Shao Jian, Wu Fei, and Zhuang Yueting. Logistic tensor regression for classification, volume 7751, chapter Intelligent science and intelligent data engineering, pages 573–581. Springer, 2013.

- [65] Arnold Zellner. An efficient method of estimating seemingly unrelated regressions and tests for aggregation bias. Journal of the American Statistical Association, 57(298):348–368, 1962.

- [66] Qibin Zhao, Liqing Zhang, and Andrzej Cichocki. A tensor-variate Gaussian process for classification of multidimensional structured data. In Twenty-seventh AAAI conference on artificial intelligence, 2013.

- [67] Qibin Zhao, Guoxu Zhou, Liqing Zhang, and Andrzej Cichocki. Tensor-variate Gaussian processes regression and its application to video surveillance. In Acoustics, Speech and Signal Processing (ICASSP), 2014 IEEE International Conference on, pages 1265–1269. IEEE, 2014.

- [68] Hua Zhou, Lexin Li, and Hongtu Zhu. Tensor regression with applications in neuroimaging data analysis. Journal of the American Statistical Association, 108(502):540–552, 2013.

- [69] Jing Zhou, Anirban Bhattacharya, Amy H. Herring, and David B. Dunson. Bayesian factorizations of big sparse tensors. Journal of the American Statistical Association, 110(512):1562–1576, 2015.

- [70] Xuening Zhu, Rui Pan, Guodong Li, Yuewen Liu, and Hansheng Wang. Network vector autoregression. The Annals of Statistics, 45(3):1096–1123, 2017.

- [71] Xuening Zhu, Weining Wang, Hansheng Wang, and Wolfgang Karl Härdle. Network quantile autoregression. Journal of Econometrics, (forthcoming), 2019.

Appendix A Background Material on Tensor Calculus

This appendix provides the main tools used in the paper. See the supplement for further results and details. A -order tensor is an element of the tensor product of vector spaces. Since there exists a isomorphism between two vector spaces of dimensions and , it is possible to define a one-to-one map between their elements, that is, between a -order tensor and a -order tensor.

Definition A.1 (Tensor reshaping).

Let and be vector subspaces and be a -order real tensor of dimensions . Let be a canonical basis of and let be the projection defined as

with . Let be a partition of . The tensor reshaping of is defined as . The mapping is an isomorphism between and .

The matricization is a particular case of reshaping a -order tensor into a -order tensor, by choosing a mapping between the tensor modes and the rows and columns of the resulting matrix, then permuting the tensor and reshaping it, accordingly.

Definition A.2 (Matricization).

Let be a -order tensor with dimensions . Let the ordered sets and be a partition of . The matricized tensor is defined by

Indices of are mapped to the rows and the columns, respectively, and

The inner product between two -dimensional tensors is defined as

The PARAFAC() decomposition (e.g., see [45]), is rank- decomposition which represents a tensor as a finite sum of rank- tensors obtained as the outer products of vectors (called marginals)

Lemma A.1 (Contracted product – some properties).

Let and . Let be a partition of , where , . It holds:

-

(i)

if and , , then .

-

(ii)

if and for , then

-

(iii)

let and . If and , , then

-

(iv)

let , then , where are - and -dimensional tensors, respectively, given by , and .

Proof.

Case (i). By definition of contracted product and tensor scalar product

Case (ii). Define and . By definition of contracted product and tensor scalar product

Note that the one-to-one correspondence established by the mapping between and corresponds to that of the vectorization of a -dimensional tensor. It also corresponds to the mapping established by the tensor reshaping of a -order tensor with dimensions into a -order tensor with dimensions . Let , then

where . Following the same approach, and defining , we obtain the second part of the result.

Case (iii). We follow the same strategy adopted in case b). Let , and , such that is a partition of . Let be defined as in case b). Then

Case (iv). Let and be two multi-indexes. By the definition of outer and contracted product we get . Therefore, with a slight abuse of notation, we use and write , when the meaning of the products is clear form the context. ∎

Lemma A.2 (Kronecker - matricization).

Let be a matrix, for , and let be the -dimensional tensor obtained as the outer product of the matrices . Let be a partition of , where and . Then .

Proof.

Use the pair of indices for the entries of the matrix , . By definition of outer product . By definition of matricization, . Moreover with and . By definition of the Kronecker product, the entry of is , where and . Since and and the associated elements of and are the same, the result follows. ∎

Lemma A.3 (Outer product and vectorization).

Let be vectors such that has length , for . Then, for each , it holds

Proof.

The result follows from the definitions of vectorisation operator and outer product. For , the result follows directly from

For consider, without loss of generality, (an analogous proof holds for ). Then, from the definitions of outer product and Kronecker product we have

∎

Proof of Proposition 2.1.

Denote with the lag operator, s.t. , by properties of the contracted product in Lemma A.1, case (iv), we get . We apply to both sides the operator , take , and get

From [12], if and is finite a.s., then and the operator applied to a sequence s.t. a.s. converges to the inverse operator . By the properties of the contracted product we get

From the assumption , we know that , which is finite. Consider the auto-covariance at lag . From Lemma A.1, we have . Using the infinite moving average representation for , we get

where we used the assumption of independence of , for any , and the fact that . Using and linearity of expectation and of the contracted product we get

where . From the assumption it follows that the above series converges to a finite limit, which is independent from , thus proving that the process is weakly stationary. ∎

Proof of Proposition 2.2.

From Theorem 3.2, Corollary 3.3 of [15], we know that is a group (called tensor group) and that the matricization operator is an isomorphism between and the linear group of square matrices of size . Therefore, there exists a one-to-one relationship between the two eigenvalue problems and , where . In particular, and . Consequently, and the result follows for from the fact that is a sufficient condition for the VAR(1) stationarity Proposition 2.1 of [51]. Since any VAR() and ART() processes can be rewritten as VAR(1) and ART(1), respectively, on an augmented state space, the result follows for any . ∎

Proof of Lemma 2.1.

Consider a ART() process with and . We define the -dimensional tensors and as and , for , respectively. Define the -dimensional tensor as , for , , for and elsewhere. Using this notation, we can rewrite the -dimensional ART() process as the -dimensional ART(1) process . ∎

Appendix B Computational Details

This appendix shows the derivation of the results. See the supplement for details.

B.1 Full conditional distribution of

Define and note that, since , it holds . The posterior full conditional distribution of , integrating out , is

where the integrand is the kernel of the GiG for in eq. (23). Then, by renormalizing, .

B.2 Full conditional distribution of

B.3 Full conditional distribution of

The full conditional distribution of , integrating out , is

which is the kernel of the Gamma in eq. (26).

B.4 Full conditional distribution of

B.5 Full conditional distributions of PARAFAC marginals

Define with and , we obtain

| (B.5) |

Consider the case . By exploiting eq. (B.2) we get

| (B.6) |

Consider the case . From eq. (B.3) we get

| (B.7) |

Consider the case , by exploiting eq. (B.4) we get

| (B.8) |

Finally, in the case . From eq. (B.5) we get

| (B.9) |

B.5.1 Full conditional distribution of

B.5.2 Full conditional distribution of

B.5.3 Full conditional distribution of

B.5.4 Full conditional distribution of

B.6 Full conditional distribution of

Define , , and . The posterior full conditional distribution of is

which is the kernel of the Inverse Wishart in eq. (28).

B.7 Full conditional distribution of

Define , and . The posterior full conditional distribution of is

which is the kernel of the Inverse Wishart in eq. (28).

B.8 Full conditional distribution of

Define , , and . The posterior full conditional distribution of is

which is the kernel of the Inverse Wishart in eq. (28).