HLIBCov: Parallel hierarchical matrix approximation of large covariance matrices and likelihoods with applications in parameter identification

Abstract

We provide more technical details about the HLIBCov package, which is using parallel hierarchical (-) matrices to identify unknown parameters of the covariance function (variance, smoothness, and covariance length). These parameters are estimated by maximizing the joint Gaussian log-likelihood function. The HLIBCov package approximates large dense inhomogeneous covariance matrices with a log-linear computational cost and storage requirement. We explain how to compute the Cholesky factorization, determinant, inverse and quadratic form in the H-matrix format. To demonstrate the numerical performance, we identify three unknown parameters in an example with 2,000,000 locations on a PC-desktop.

Keywords: Computational statistics; parallel hierarchical matrices; large datasets; Matérn covariance; random fields; spatial statistics; HLIB; HLIBCov; HLIBpro; Cholesky; matrix determinant; call C++ from R; parameter identification.

1 Technical details

- Program title:

-

HLIBCov

- Nature of problem:

-

To approximate large covariance matrices. To perform efficient linear algebra with large covariance matrices on a non-tensor grid. To estimate the unknown parameters (variance, smoothness parameter, and covariance length) of a covariance function by maximizing the joint Gaussian log-likelihood function with a log-linear computational cost and storage.

- Software license:

-

HLIBCov (GPL 2.0), HLIBpro (proprietary)

- CiCP scientific software URL:

- Distribution format:

-

*.cc files via github

- Programming language(s):

-

C++

- Computer platform:

-

any

- Operating system:

-

Linux, MacOSX and MS Windows

- Compilers:

-

standard C++ compilers

- RAM:

-

4 GB and more (depending on the matrix size)

- External routines/libraries:

-

HLIBCov requires HLIBpro and GNU Scientific Library (https://www.gnu.org/software/gsl/).

- Running time:

-

with number of CPU cores

- Restrictions:

-

None (similar limitations as HLIBpro)

- Supplementary material and references:

-

www.HLIBpro.com and references therein.

- Additional Comments:

-

HLIBpro is a software library that implements parallel algorithms for hierarchical matrices. It is freely available in binary form for academic purposes. HLIBpro algorithms are designed for one, two, and three - dimensional problems.

2 Introduction

HLIBpro is a very fast and efficient parallel -matrices library. This is an auxiliary technical paper, which contains technical details to our previous paper [31]. In [31] we used the gradient-free optimization method to estimate the unknown parameters of a covariance function using HLIB and HLIBpro.

Parameter estimation and problem settings.

We let be the number of spatial measurements located irregularly across a given geographical region at locations , . We also let , where is a stationary Gaussian random field. Then, we assume that has mean zero and a stationary parametric covariance function , where is a spatial distance and vector denotes unknown parameters. To infer , we maximize the joint Gaussian log-likelihood function,

| (1) |

where , . Let us assume that maximizes (1). When the sample size is large, the evaluation of (1) becomes challenging, due to computational cost of the Cholesky factorization. Hence, scalable and efficient methods that can process larger are needed.

For this, the hierarchical matrices (-matrix) technique is used, which approximates sub-blocks of the dense matrix by a low-rank representation of either a given rank or a given accuracy (see Section 3.2).

Definition 2.1

An -matrix approximation with maximal rank of the exact log-likelihood is defined by :

| (2) |

where is an -matrix approximation of the Cholesky factor with maximal rank in the sub-blocks, , and vector is the solution of the system .

To maximize in (2), we use the Brent-Dekker method [9, 33]. It could be used with or without derivatives.

An additional difficulty is the ill-posedness of the optimization problem. Even a small perturbation in the covariance matrix may result in large perturbations in the log-determinant and the log-likelihood. A possible remedy, which may or may not help, is to take a higher rank .

Features of the -matrix approximation.

Other advantages of applying the -matrix technique are the following:

-

1.

The -matrix class is large, including low-rank and sparse matrix classes;

-

2.

, , , Cholesky decomposition, the Schur complement, and many others can be computed in the -matrix format [16];

-

3.

Since the -matrix technique has been well studied, there are many examples, multiple sequential and parallel implementations and a solid theory already available. Therefore, no specific MPI or OpenMP knowledge is needed;

-

4.

The -matrix cost and accuracy is controlled by ;

-

5.

The -Cholesky factor and the -inverse have moderate ranks.

Structure of the paper.

In Section 3, we introduce the -matrix approximations of Matérn covariance matrices and Gaussian likelihood functions. In Section 4, we estimate the memory storage and computing costs. In Section 5, we describe the software installation details, procedures of the HLIBCov code, and the algorithm for parameter estimation. The estimation of unknown parameters is reported in Section 6. Best practices are listed in Section 7. We end the paper with a conclusion in Section 8. The auxiliary -matrix details are provided in the Appendix B.

3 Methodology and algorithms

3.1 Matérn covariance functions

For any two spatial locations and and the distance , the Matérn class of covariance functions is defined as

| (3) |

where ; is a spatial range parameter; is the smoothness, with larger values of corresponding to smoother random fields; and is the variance. Here, denotes a modified Bessel function of the second kind of order , and denotes the Gamma function. The values and correspond to the exponential and Gaussian covariance functions respectively.

3.2 Introduction to hierarchical matrices

Detailed descriptions of hierarchical matrices [16, 15, 17, 12, 18, 29] and their applications can be found elsewhere [23, 6, 21, 2, 1, 30, 24].

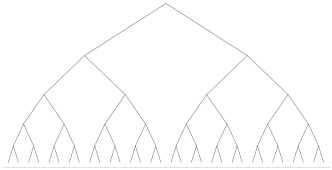

The -matrix technique was originally introduced by Hackbusch (1999) for the approximation of stiffness matrices and their inverses coming from partial differential and integral equations [15, 12, 8]. Briefly, the key idea of the -matrix technique is to divide the initial matrix into sub-blocks in a specific way, identify those sub-blocks which can be approximated by low-rank matrices and compute the corresponding low-rank approximations.

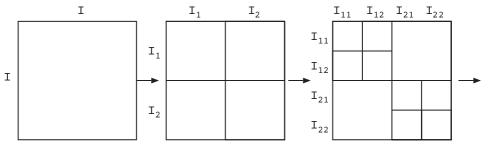

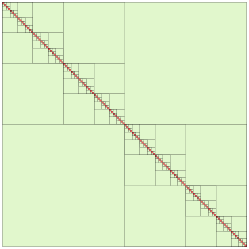

The partitioning of the matrix into sub-blocks starts by recursively dividing the rows and columns into disjoint sub-sets, e.g., splitting the set of all rows into two (equal sized) sub-sets, which are again divided. This yields a cluster tree where each sub-set of rows/columns is called a cluster. By multiplying the cluster trees for the rows and the columns, a hierarchical partitioning of the matrix index set is obtained, the so called block cluster tree or -tree. Within this block cluster tree, low-rank approximable blocks are identified using an admissibility condition. Such admissible blocks are not further refined into sub-blocks, i.e., the corresponding sub-tree is not computed or stored. For all admissible blocks a low-rank approximation of the initial matrix is computed, either with a given rank (fixed-rank strategy) or an accuracy (fixed-accuracy strategy). The result of this computation is called an -matrix. This process is also shown in Figure 1.

Definition 3.1

Let be an index set (representing the rows/columns) and be a cluster tree based in . Furthermore let be a block cluster tree based on and an admissibility condition . Then the set of -matrices with maximal rank is defined as

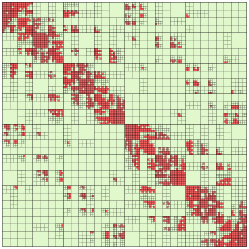

Various partitioning strategies for the rows and columns of the matrix and admissibility conditions have been developed to approximate different types of matrices. Typical admissibility conditions are strong, weak and based on domain decomposition [16], for which examples are shown in Figure 2. The red blocks indicate dense or in-admissible blocks whereas green blocks are identified as admissible. The maximal size of the dense blocks (i.e., how deep the hierarchical subdivision into sub-blocks is) is regulated by the parameter “”, whose value affects the storage size and the runtime of the -matrix arithmetic, e.g., a smaller value leads to less storage but is often in-efficient with respect to CPU performance. Typically values of are in the range to .

For the computation of the low-rank approximation for admissible sub-blocks many different methods are available, e.g., adaptive cross approximation (ACA), hybrid cross approximation (HCA), rank-revealing QR, randomized SVD [11, 3, 5, 8, 7, 22, 19]. For the fixed-rank strategy, the resulting low-rank matrix is of rank at most . In case of the fixed-accuracy strategy with a given , the low-rank approximation of the sub-block is computed such that . The storage size of the resulting -matrix is of order [12].

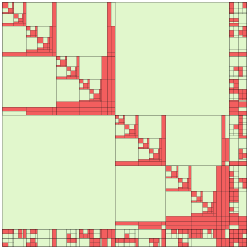

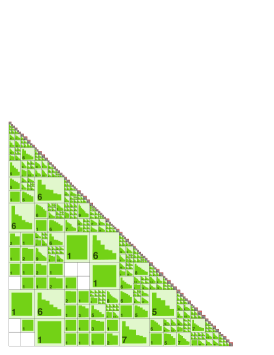

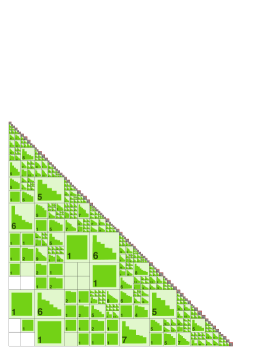

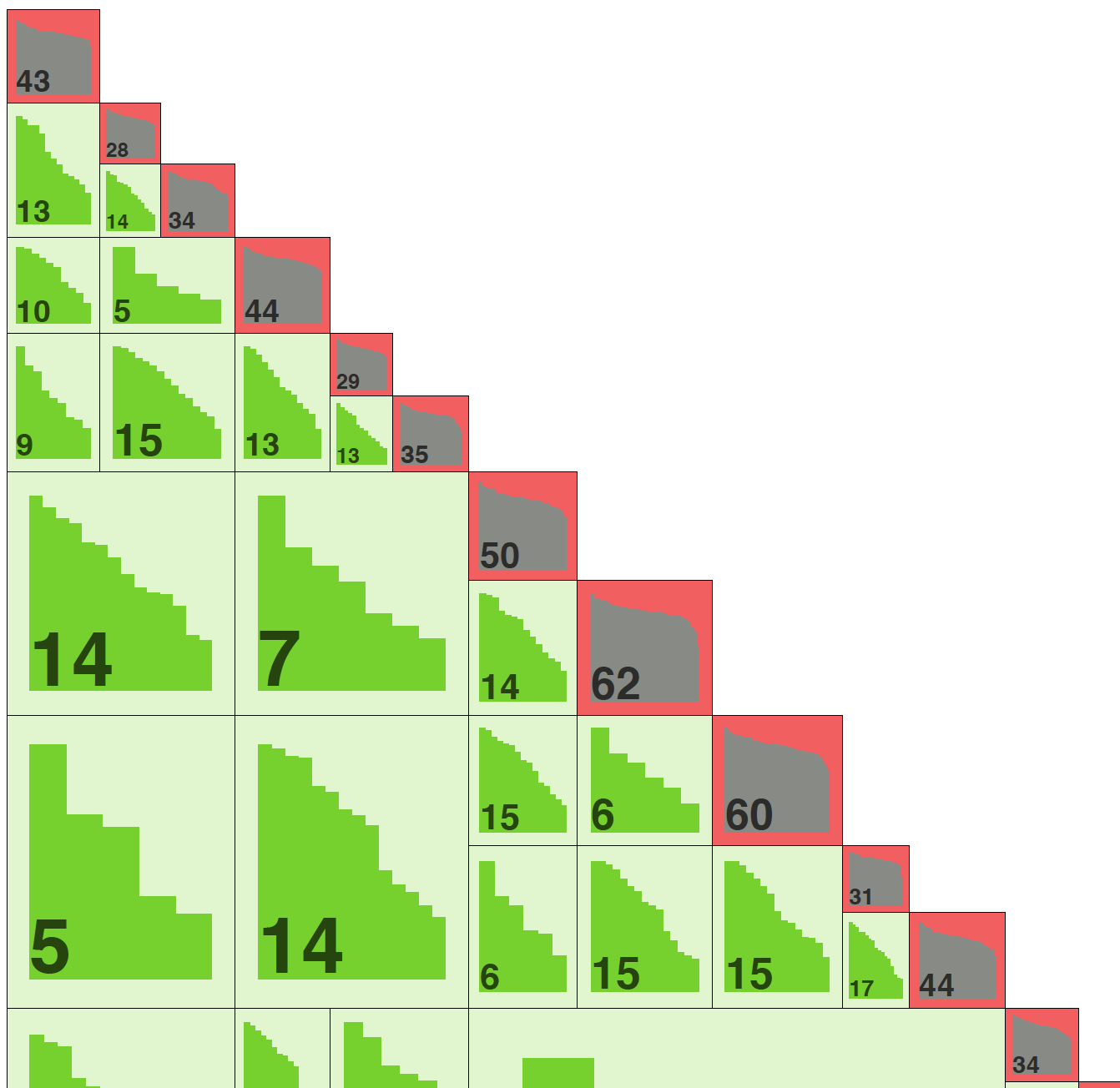

In Figure 3 (left), an example of an -matrix approximation to can be found. There, the local ranks and the decay of singular values in the admissible blocks (green) in logarithmic scale are shown.

In addition to efficient matrix approximation, -matrices also permit full matrix arithmetic, e.g., matrix addition, matrix multiplication, inversion or factorization. However, similar to matrix compression, -matrix arithmetic is approximate to maintain log-linear complexity. The approximation during arithmetic is again either of a fixed-rank or a fixed-accuracy [12]. In this work, we make use of the -Cholesky factorization of (see Figure 3).

For , the predefined rank (or accuracy ) defines the accuracy of the -matrix approximation, for the initial approximation of as well as for the Cholesky factorization for .

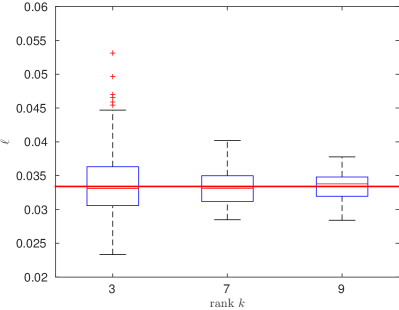

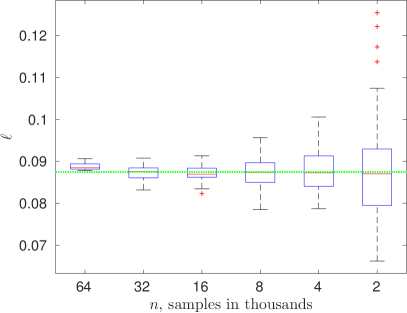

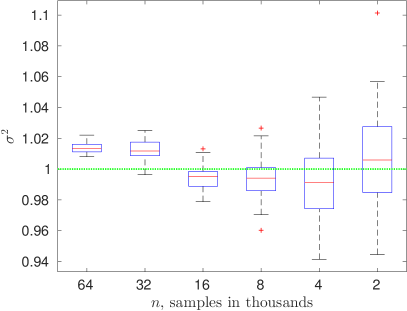

In Fig. 4 (left), the results for computing with a different rank in the -matrix approximation for 100 replicates are shown. On each box, the central red line indicates the median, the small box indicates the 25 percentile, and the top (wide) edge indicates the 75 percentile. The outliers are marked by the red symbol ’+’. The bold long red line denotes the true value of the parameter . With a larger rank and hence, with a better approximation, the variance of decreases.

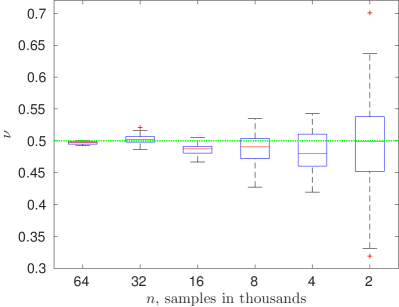

The dependence of on the problem size, e.g., the number of measurements is also tested with the results shown in Figure 4 (right). As the results demonstrate, with a larger number the estimation of the parameter is getting better.

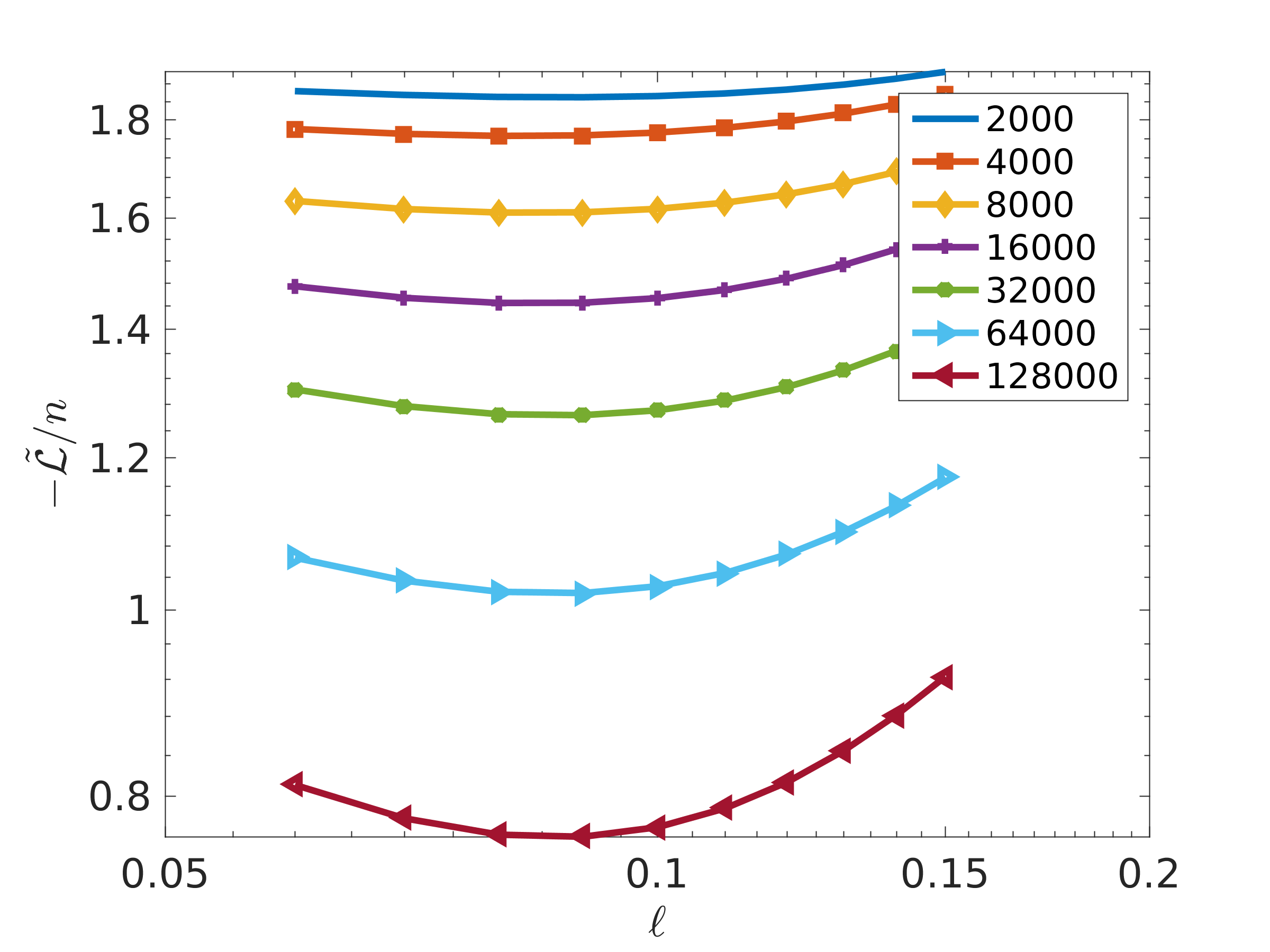

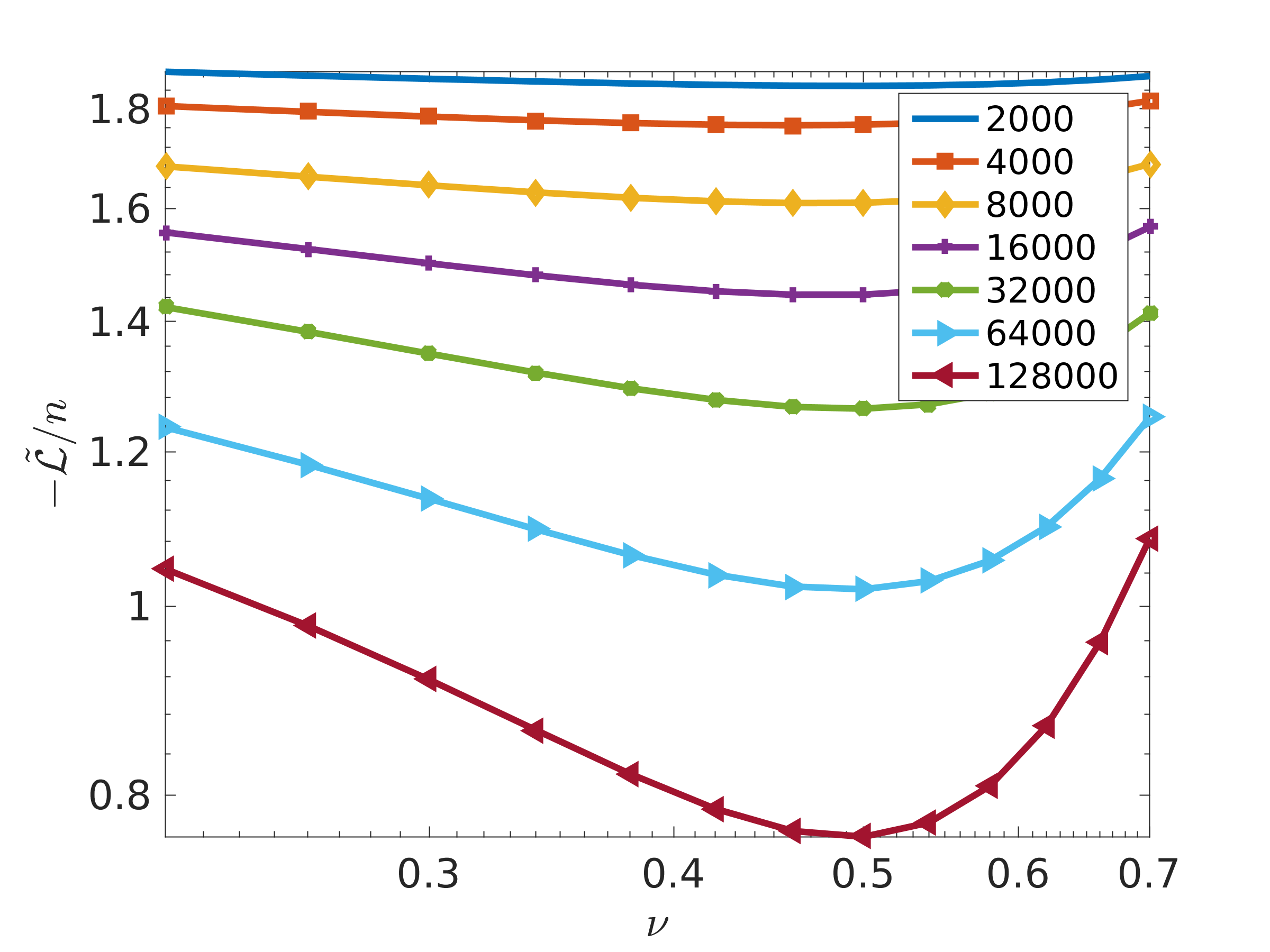

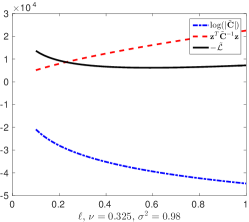

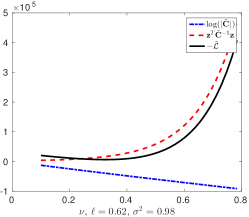

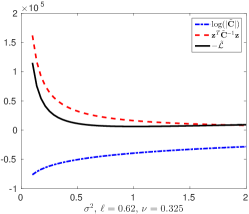

In Fig. 5, we illustrate the dependence of on the parameters (left, with , ), and (right, with and ). Both figures demonstrate the smooth dependance also illustrate the locations of the minima for a different .

3.3 Parallel hierarchical-matrix technique

We used the parallel -matrix library HLIBpro [25, 28, 13, 27], which implements -matrix approximation and arithmetic functions using a task-based approach to make use of todays many-core architectures. For this, the mathematical operation is decomposed into small atomic tasks with corresponding incoming and outgoing data dependencies. This set of tasks and dependencies forms a directed acyclic graph (DAG), which is used for scheduling the tasks to the CPU cores, e.g., if all incoming data dependencies are met, the corresponding task is executed on the next free CPU core available.

The computational complexity of the different -matrix operations is shown in Table 1. Here, denotes the number of vertices, is the number of leaves in the block-cluster tree . The sequential terms in those estimates are typically due to the sequential behaviour of the corresponding algorithm, e.g., strictly following the diagonal during Cholesky factorization, but usually do not show in practical applications since the majority of the computation work is parallelized.

| Operations | Parallel Complexity [26] (Shared Memory) |

|---|---|

| with rank truncation | |

| build | |

| store | |

| -Cholesky | , |

| determinant | , |

4 Memory storage and convergence

The Kullback-Leibler divergence (KLD) is a measure of information loss when a distribution is used to approximate . For the multivariate normal distributions and , it is defined as follows:

In Tables 2 and 3, we show the dependence of KLD and two matrix errors on the -matrix rank for the Matérn covariance function with parameters , , and , computed on the domain . All errors are under control, except for the last column. The ranks are too small to approximate the inverse, and, therefore, the resulting error is large. Relatively often, the -matrix procedure, which computes the -Cholesky factor or the -inverse, produces “NaN” (not a number) and terminates. One possible cause is that some of the diagonal elements can be very close to zero, and their inverse is not defined. This may happen when two locations are very close to each other and, as a result, two columns (rows) are linear dependent. To avoid such cases, the available data should be preprocessed to remove duplicate locations. Very often, the nugget is added to the main diagonal to stabilize numerical calculations (see more in Section 6.2), i.e., . In Tables 2 and 3, the nugget is equal to zero.

| KLD | ||||||

|---|---|---|---|---|---|---|

| 10 | ||||||

| 12 | ||||||

| 15 | ||||||

| 20 | ||||||

| 50 | ||||||

| KLD | ||||||

|---|---|---|---|---|---|---|

| 20 | ||||||

| 30 | ||||||

| 40 | ||||||

| 50 | ||||||

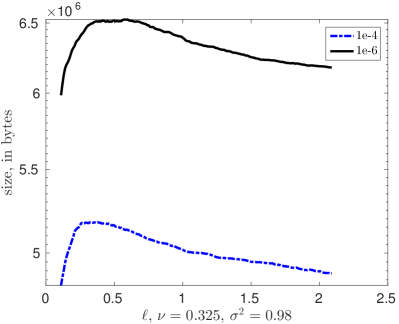

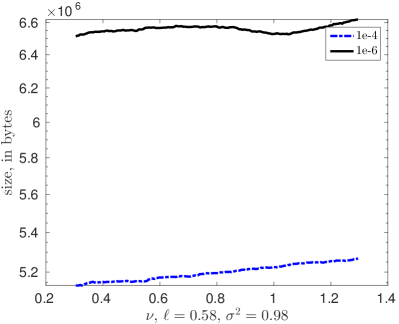

Figure 6 shows that the -matrix storage cost remains almost the same for the different parameters (left) and (right). The computational domain is with .

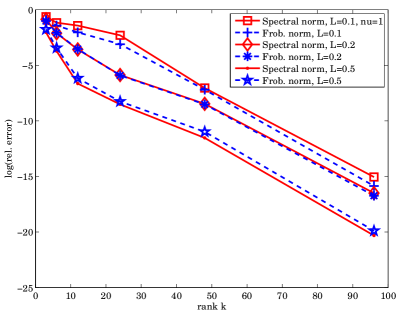

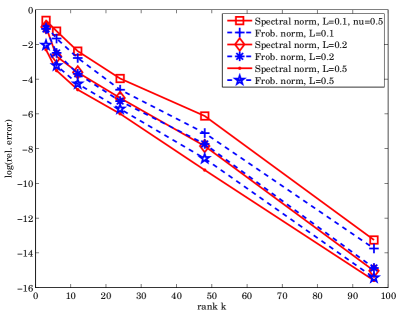

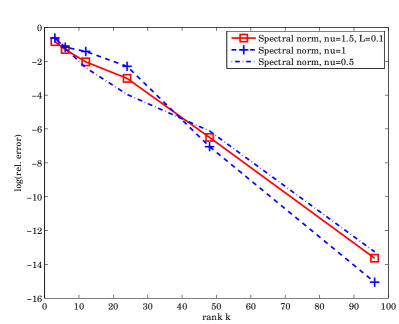

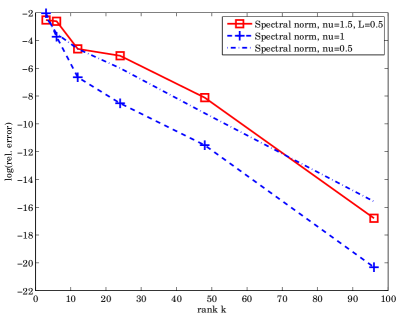

In Figure 7, we plot the convergence of in the Frobenius and spectral norms vs. the rank for different covariance lengths. The smoothness parameter is equal to 1 (left), and 0.5 (right). In Figure 8, we plot vs. the rank for different smoothness parameters. The covariance length is equal to 0.1(left), and 0.5 (right). The computational domain in both cases was a unit square .

5 Software installation

This section contains a summary of the information provided at https://www.hlibpro.com and https://github.com/litvinen/HLIBCov.git . HLIBpro supports both shared and distributed memory architectures, though in this work we only use the shared memory version. For the implementation of the task-parallel approach, Intel’s Threading Building Blocks (TBB) is used. HLIBpro is free for academic purposes, and is distributed in a pre-compiled form (no source code available). Originally, HLIBpro was developed for solving FEM and BEM problems [13, 28]. In this work, we extend the applicability of HLIBpro to dense covariance matrices and log-likelihood functions.

Installation:

HLIBCov uses the functionality of HLIBpro; therefore, HLIBpro must be installed first. All functionality implemented by HLIBCov is based on HLIBpro, i.e., no extra software is needed in addition to the libraries needed by HLIBpro. This also holds for the Matérn kernel, which uses Bessel functions and maximization algorithms, both being provided by the GNU Scientific Library (GSL) and also used by HLIBpro. The reader can easily replace GSL with his own optimization library. The Bessel functions are also available in other packages.

To install HLIBpro on MacOS and Windows, we refer the reader to www.HLIBpro.com for further details.

| Software | Version |

|---|---|

| HLIBCov | 1.0 |

| HLIBpro | 2.6 |

| GSL | 1.16 |

| TBB | 4.3 |

Hardware.

All of the numerical experiments herein are performed on a Dell workstation with two Intel(R) Xeon(R) E5-2680 v2 CPUs (2.80GHz, 10 cores/20 threads) and 128 GB main memory.

Adding HLIBCov to HLIBpro.

The easiest form of compiling HLIBCov is by using the compilation system of HLIBpro. For this, the source code file of HLIBCov is placed in the examples directory of HLIBpro and an entry is added to the file examples/SConscript:

Afterwards, the make process of HLIBpro is run to compile also HLIBCov (see HLIBpro installation instructions at www.hlibpro.com).

Input of HLIBCov.

The input contained in the first line is the total number of locations . Lines contain the coordinates , , and the measurement value. An example is provided below;

HLIBpro requires neither a list of finite elements nor a list of edges. We provide several examples of few input files of different size on the open-access file hosting service GitHub (https://github.com/litvinen/HLIBCov.git). We added two data sets to GitHub: data.tar.gz and moisturedata.zip. Both examples contain multiple data sets of different sizes.

Output of HLIBCov.

The main output is the three identified parameter values . The auxiliary output may include many details: -matrix details (the maximal rank , the maximal accuracy in each sub-block, and the Frobenius and spectral norms of , , , ). Additionally, iterations of the maximization algorithm can also be printed out. The example of an output file provided below contains two iterations: the index, , , , , and the residual TOL of the iterative method:

If the iterative process is converging, then the last row will contain the solution . When computing error boxes, the output file will contain solutions (, , , ), where is the number of replicates:

The name of the output file can be found in the main() procedure in loglikelihood.cc.

6 Numerical experiments

We generate a sample set with parameters and then try to infer these parameters.

6.1 Generation of the synthetic data

To build various data-sets ( replicates) with locations, we generate a large vector with locations, and randomly sample points from it. We note that if the locations are very close to each other, then the covariance matrix may be singular or the Cholesky factorization will be very difficult to compute.

To generate the random data , we compute the -Cholesky factorization of . Then, we evaluate , where is a normal vector with zero mean and unit variance. We generate only once. Next, we run our optimization algorithm and try to identify (recover) the “unknown” parameters . The resulting boxplots for and over replicates are illustrated in Fig. 9. We see that the variance (or uncertainty) decreases with increasing . The green line indicates the true values.

To identify all three parameters simultaneously, we solve a three-dimensional optimization problem. The maximal number of iterations is set to 200, and the residual is . The behavior and accuracy of the boxplots depend on the -matrix rank, the maximum number of iterations to achieve a certain threshold, the threshold (or residual) itself, the initial guess, the step size in each parameter of the maximization algorithm, and the maximization algorithm. All replicates of are sampled from the same generated vector of size .

In Table 5, we present the almost-linear storage cost (columns 3 and 6) and the computing time (columns 2 and 5).

| comp. time | size | kB/dof | comp. time | size | ||

| sec. | MB | sec. | MB | |||

| 32,000 | 3.3 | 162 | 5.1 | 2.4 | 172.7 | |

| 128,000 | 13.3 | 776 | 6.1 | 13.9 | 881.2 | |

| 512,000 | 52.8 | 3420 | 6.7 | 77.6 | 4150 | |

| 2,000,000 | 229 | 14790 | 7.4 | 473 | 18970 | |

The shape of the negative log-likelihood function and its components are illustrated in Fig. 10. This helps us to understand the behavior of the iterative optimization method, and the contributions of the log-determinant and the quadratic functional. We see that the log-likelihood is almost flat, and that it may be necessary to perform many iterations in order to find the minimum.

| 0.001 | 0.005 | 0.01 | 0.02 | 0.03 | 0.05 | 0.07 | 0.1 | |

|---|---|---|---|---|---|---|---|---|

| 44657 | 36157 | 36427 | 40522 | 45398 | 68450 | 70467 | 90649 | |

| 44585 | 36352 | 36113 | 41748 | 47443 | 60286 | 70688 | 90615 | |

| 44529 | 37655 | 36390 | 42020 | 47954 | 60371 | 72785 | 90639 |

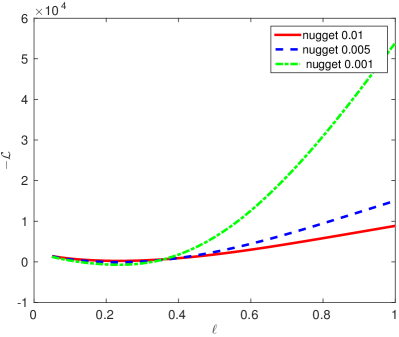

6.2 Adding nugget

When the diagonal values of are very close to zero, -Cholesky becomes unstable producing negative entries on the diagonal during computation. By adding a diagonal matrix with small positive numbers, all the singular values are increased and moved away from zero. However, by adding a nugget, we redefine the original matrix as . Below, we analyze how the loglikelihood function, as well as its maximum are changing by this.

We assume . For a small perturbation matrix [10], it holds that

where is the condition number of , and . Alternatively, by substituting , we obtain

| (4) |

From (4), we see that the relative error on the left-hand side of (4) depends on the norm , i.e., the relative error is inversely proportional to the smallest singular value of . This may explain a possible failing of approximating matrices, where the smallest singular values tend towards zero. The estimates for the -Cholesky and the Schur complement for general sparse positive-definite matrices are given in [4]. The approximation errors are proportional to the , i.e., matrices with a very large condition number may require a very large -matrix rank.

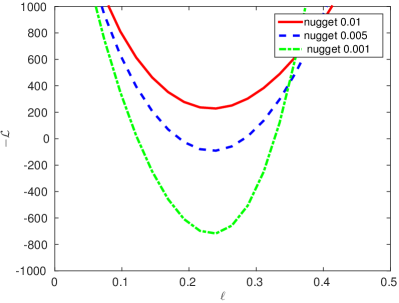

Figure 11 (left) demonstrates three negative log-likelihood functions computed with the nuggets 0.01, 0.005, and 0.001. For this particular example, the behavior of likelihood is preserved, and the minimum does not change (or changes very slightly). Figure 11 (right) is just a zoomed in version of the picture on the left.

7 Best practices (HLIBCov)

In this section, we list our recommendations and warnings.

-

1.

For practical computations, use adaptive-rank arithmetic since it produces smaller matrices and faster runtime.

-

2.

For the input, it is sufficient to define a file by three columns: both location coordinates (, ) and the observed value; no triangles or edges are required.

-

3.

If two locations coincide or are very close to each other, then the matrix will be close to singular or singular. As a result, it will be hard to compute the Cholesky factorization. Our suggested remedy is to improve the quality of the locations by preprocessing the data.

-

4.

By default, the -Cholesky or LU factorizations use a task-based approach employing a DAG (directed acyclic graph). For sequential computations this can be turned off to revert to a slightly faster recursive implementation by setting

HLIB::CFG::Arith::use_dag = false

-

5.

By default, HLIBpro uses all available computing cores. To perform computations on 16 cores, use HLIB::CFG::set_nthreads(16) at the beginning of the program (after command INIT()).

-

6.

Since HLIBpro is working for 1D, 2D and 3D domains, only very minor changes are required to move from 1D locations to 2D or 3D in HLIBCov. Replace dim with dim in

TCoordinate coord(vertices, dim);

then add “ >> z” to

in >> x >> y >> z >> v;

The -matrix data format is a rather complicated data structure (class) in HLIBpro. Therefore, the -matrix objects (or the pointers on them) are neither the input nor the output parameters. Instead, the input parameters for the HLIBpro C++ routines are: a vector (array) of locations and a vector of observations . The triangulation (a list of triangles/edges) is not needed. The output parameters are either scalar values or a vector; for example, the determinant, the trace, a norm, the result of the matrix-vector product, and an approximation error.

8 Conclusion

We extended functionality of the parallel -matrix library HLIBpro to infer unknown parameters for applications in spatial statistics. This new extension allows us to work with large covariance matrices. We approximated the joint multivariate Gaussian likelihood function and found its maxima in the -matrix format. These maxima were used to estimate the unknown parameters ( , , and ) of a covariance model. The new code is parallel, highly efficient, and written in C++ language. With the -matrix technique, we reduced the storage cost and the computing cost (Tables 3, 5) of the log-likelihood function dramatically, from cubic to almost linear. We demonstrated these advantages in a synthetic example, where we were able to identify the true parameters of the covariance model. We were also able to compute the log-likelihood function for locations in just a few minutes on a desktop machine (Table 5). The -matrix technique allowed us to increase the spatial resolution, handle more measurements, consider larger regions, and identify more parameters simultaneously.

Acknowledgments

The research reported in this publication was supported by funding from the Alexander von Humboldt foundation (chair of Mathematics for Uncertainty Quantification at RWTH Aachen) and Extreme Computing Research Center (ECRC) at King Abdullah University of Science and Technology (KAUST).

References

- [1] S. Ambikasaran, D. Foreman-Mackey, L. Greengard, D. W. Hogg, and M. OŃeil. Fast direct methods for Gaussian processes and the analysis of NASA Kepler mission data. arXiv preprint arXiv:1403.6015, 2014.

- [2] S. Ambikasaran, J. Y. Li, P. K. Kitanidis, and E. Darve. Large-scale stochastic linear inversion using hierarchical matrices. Computational Geosciences, 17(6):913–927, 2013.

- [3] M. Bebendorf. Approximation of boundary element matrices. Numerical Mathematics, 86(4):565–589, 2000.

- [4] M. Bebendorf and T. Fischer. On the purely algebraic data-sparse approximation of the inverse and the triangular factors of sparse matrices. Numerical Linear Algebra with Applications, 18(1):105–122, 2011.

- [5] M. Bebendorf and S. Rjasanow. Adaptive low-rank approximation of collocation matrices. Computing, 70(1):1–24, 2003.

- [6] S. Börm and J. Garcke. Approximating Gaussian processes with -matrices. In J. N. Kok, J. Koronacki, R. L. de Mantaras, S. Matwin, D. Mladen, and A. Skowron, editors, Proceedings of 18th European Conference on Machine Learning, Warsaw, Poland, September 17-21, 2007. ECML 2007, volume 4701, pages 42–53, 2007.

- [7] S. Börm and L. Grasedyck. Hybrid cross approximation of integral operators. Numer. Math., 101(2):221–249, 2005.

- [8] S. Börm, L. Grasedyck, and W. Hackbusch. Hierarchical Matrices, volume 21 of Lecture Note. Max-Planck Institute for Mathematics, Leipzig, 2003. www.mis.mpg.de.

- [9] R. P. Brent. Chapter 4: An algorithm with guaranteed convergence for finding a zero of a function, algorithms for minimization without derivatives. Englewood Cliffs, NJ: Prentice-Hall, 1973.

- [10] J. Demmel. The componentwise distance to the nearest singular matrix. SIAM Journal on Matrix Analysis and Applications, 13(1):10–19, 1992.

- [11] S. A. Goreinov, E. E. Tyrtyshnikov, and N. L. Zamarashkin. A theory of pseudoskeleton approximations. Linear Algebra Appl., 261:1–21, 1997.

- [12] L. Grasedyck and W. Hackbusch. Construction and arithmetics of -matrices. Computing, 70(4):295–334, 2003.

- [13] L. Grasedyck, R. Kriemann, and S. LeBorne. Parallel black box H-LU preconditioning for elliptic boundary value problems. Computing and visualization in science, 11(4-6):273–291, 2008.

- [14] P. Guttorp and T. Gneiting. Studies in the history of probability and statistics XLIX: On the Matérn correlation family. Biometrika, 93:989–995, 2006.

- [15] W. Hackbusch. A sparse matrix arithmetic based on -matrices. I. Introduction to -matrices. Computing, 62(2):89–108, 1999.

- [16] W. Hackbusch. Hierarchical matrices: Algorithms and Analysis, volume 49 of Springer Series in Comp. Math. Springer, 2015.

- [17] W. Hackbusch and B. N. Khoromskij. A sparse -matrix arithmetic. II. Application to multi-dimensional problems. Computing, 64(1):21–47, 2000.

- [18] W. Hackbusch, B. N. Khoromskij, and R. Kriemann. Hierarchical matrices based on a weak admissibility criterion. Computing, 73(3):207–243, 2004.

- [19] N. Halko, P. G. Martinsson, and J. A. Tropp. Finding Structure with Randomness: Probabilistic Algorithms for Constructing Approximate Matrix Decompositions. SIAM Review, 53(2):217–288, 2011.

- [20] M. S. Handcock and M. L. Stein. A Bayesian analysis of kriging. Technometrics, 35:403–410, 1993.

- [21] H. Harbrecht, M. Peters, and M. Siebenmorgen. Efficient approximation of random fields for numerical applications. Numerical Linear Algebra with Applications, 22(4):596–617, 2015.

- [22] Y. P. Hong and C.-T. Pan. Rank-revealing qr factorizations and the singular value decomposition. Mathematics of Computation, 58(197):213–232, 1992.

- [23] B. N. Khoromskij and A. Litvinenko. Data sparse computation of the Karhunen-Loève expansion. AIP Conference Proceedings, 1048(1):311, 2008.

- [24] B. N. Khoromskij, A. Litvinenko, and H. G. Matthies. Application of hierarchical matrices for computing the Karhunen–Loève expansion. Computing, 84(1-2):49–67, 2009.

- [25] R. Kriemann. Parallel H-matrix arithmetics on shared memory systems. Computing, 74(3):273–297, 2005.

- [26] R. Kriemann. Parallele Algorithmen für -Matrizen. PhD thesis, University of Kiel, 2005.

- [27] R. Kriemann. HLIBpro user manual. Technical report, Max Planck Institute for Mathematics in the Sciences, 2008.

- [28] R. Kriemann. H-LU factorization on many-core systems. Computing and Visualization in Science, 16(3):105–117, Jun 2013.

- [29] A. Litvinenko. Application of hierarchical matrices for solving multiscale problems. PhD Dissertation, Leipzig University, 2006.

- [30] A. Litvinenko and H. G. Matthies. Sparse data representation of random fields. PAMM, 9(1):587–588, 2009.

- [31] A. Litvinenko, Y. Sun, M. G. Genton, and D. E. Keyes. Likelihood approximation with hierarchical matrices for large spatial datasets. Computational Statistics Data Analysis, 137:115–132, 2019.

- [32] B. Matérn. Spatial Variation, volume 36 of Lecture Notes in Statistics. Springer-Verlag, Berlin; New York, second edition edition, 1986.

- [33] W. H. Press, S. A. Teukolsky, W. T. Vetterling, and B. P. Flannery. Section 9.3. Van Wijngaarden-Dekker-Brent Method. Numerical Recipes: The Art of Scientific Computing, volume 3rd ed. New York: Cambridge University Press., 2007.

Appendix A Admissibility condition

Here we give an example of the admissibility criteria [15, 12, 8]. Let

| (5) |

with singularity at . We will introduce a condition, which divides all sub-blocks into admissible and inadmissible. Admissible blocks will be approximated by low-rank matrices.

Definition A.1

Let be an index set of all degrees of freedom, i.e. . Denote for each index corresponding to a basis function the support .

Let be two clusters (elements of the cluster tree ). Clusters are subsets of , i.e. . We generalise to clusters by setting , i.e., is the minimal subset of that contains the supports of all basis functions with .

Suppose that and are compact and is defined for with . The standard assumption on the kernel function in the -matrix theory is asymptotic smoothness of , i.e, that

holds for constants , and . This estimation is used to control the error from the Taylor expansion

Suppose that is an approximation of in of the separate form (e.g., Taylor or Lagrange polynomials):

| (6) |

where is the rank of separation. We are aiming at an approximation of the form (6) such that exponential convergence

| (7) |

holds.

Let be axis-parallel bounding boxes of the clusters and such that and .

Definition A.2

The standard admissibility condition (Admη), shown in Fig. 2 on the left, for two clusters and is

| (8) |

Another example is

where is some positive number.

Definition A.3

The admissibility condition indicates blocks that allow rank- approximation and those that do not. Admissible blocks are either very small (and computed exactly) or are approximated by rank- matrices. All other (inadmissible) blocks are computed as usual.

In order to get a simpler partitioning (see an example in Fig. 2, right), we define the weak admissibility condition for a pair :

| (9) |

where , are assumed to belong to the same level of .

See more details about derivation of admissibility condition for covariance matrices in [24].

Appendix B Maximum of the log-likelihood function

The C++ code for computing the maximum of the log-likelihood function (loglikelihood.cc):

Below we list the C++ code, which computes the value of the log-likelihood for given parameters (loglikelihood.cc):

Rank- Adaptive Cross Approximation (ACA):

An -matrix contains many sub-blocks, which can be well approximated by low-rank matrices. These low-rank approximations can be computed accurately by truncated singular value decomposition (SVD), but it is very slow. HLIBpro uses the Adaptive Cross Approximation method (ACA) [11] and its improved modifications such as ACA+ and HACA [5, 3, 7].

Remark B.1

Further optimization of the ACA algorithm can be achieved by a recompression using low-rank SVD. If we suppose that a factorization of the matrix , , , is found by ACA and that the actual rank of is , . Then we can apply the low-rank SVD algorithm to compute in time.