A sentiment-based model for the BitCoin: theory, estimation and option pricing

Abstract.

In recent literature it is claimed that BitCoin price behaves more likely to a volatile stock asset than a currency and that changes in its price are influenced by sentiment about the BitCoin system itself; in Kristoufek [10] the author analyses transaction based as well as popularity based potential drivers of the BitCoin price finding positive evidence. Here, we endorse this finding and consider a bivariate model in continuous time to describe the price dynamics of one BitCoin as well as a second factor, affecting the price itself, which represents a sentiment indicator. We prove that the suggested model is arbitrage-free under a mild condition and, based on risk-neutral evaluation, we obtain a closed formula to approximate the price of European style derivatives on the BitCoin. By applying the same approximation technique to the joint likelihood of a discrete sample of the bivariate process, we are also able to fit the model to market data. This is done by using both the Volume and the number of Google searches as possible proxies for the sentiment factor. Further, the performance of the pricing formula is assessed on a sample of market option prices obtained by the website deribit.com.

Keywords: BitCoin, sentiment, stochastic models, equivalent martingale measure, option pricing, likelihood.

1. Introduction

The BitCoin was first introduced as an electronic payment system between peers. It is based on an open source software which generates a peer to peer network. This network includes a high number of computers connected to each other through the Internet and complex mathematical procedures are implemented both to check the truthfulness of the transaction and to generate new BitCoins. Opposite to traditional transactions, which are based on the trust in financial intermediaries, this system relies on the network, on the fixed rules and on cryptography. The open source software was created in 2009 by a computer scientist known under the pseudonym Satoshi Nakamoto, whose identity is still unknown. BitCoin has several attractive properties for consumers: it does not rely on central banks to regulate the money supply and it enables essentially anonymous transactions. BitCoins can be purchased on appropriate websites that allow to change usual currencies in BitCoins. Further, payments can be made in BitCoins for several online services and goods and its use is increasing. Special applications have been designed for smartphones and tablets for transactions in BitCoins and some ATM have appeared all over the world (see Coin ATM radar) to change traditional currencies in BitCoins. At very low expenses it is also possible to send cryptocurrency internationally. However, the downside of BitCoin is that, due to anonymous transactions, it has been labeled as an exchange for organized crime and money laundering. It is worth to mention the recent Wannacry malware which last May has infected the informatic systems of many huge companies as well as thousands of computers around the world. The hackers which have spread this malware asked a ransom of 300 to 600 USD to be payed in BitCoins in order to get each computer rid of the infection.

Besides, BitCoins can be only deposited in a digital wallet which is costly and possibly subject to hacking attacks, thefts and other issues related to cyber-security.

In spite of all the above critics, BitCoin has experienced a rapid growth both in value and in the number of transactions. A number of competitors, so called alt-coins, have also appeared recently without reaching the popularity of BitCoin; the most successful among these is Ethereum.

Economic and financial aspects of BitCoin have been frequently addressed by financial blogs and by financial media but, until recently, researchers in Academia were primarily focused on the underlying technology and on safety and legal issues such as double spending.

From an economic viewpoint, one of the main concerns about BitCoin is whether it should be considered a currency, a commodity or a stock. In Yermack [20], the author performs a detailed qualitative analysis of BitCoin behavior. He remarks that a currency is usually characterized by three properties: a medium of exchange, a unit of account and a store of value. BitCoin is indeed a medium of exchange, though limited in relative volume of transactions and essentially restricted to online markets; however it lacks the other two properties. BitCoin value is rather volatile and traded for different prices in different exchanges, making it unreliable as a unit of account. The conclusion in Yermack [20] is that BitCoin behaves as a high volatility stock and that most transactions on BitCoins are aimed to speculative investments.

In recent years several papers have also appeared in order to analyze which are the main drivers of its price evolution in time; many authors claim that the high volatility in BitCoin prices may depend on sentiment and popularity about the BitCoin market itself; of course sentiment and popularity on BitCoin are not directly observed but several variables may be considered as indicators, from the more traditional volume or number of transactions to the number of Google searches or Wikipedia requests about the topic, in the period under investigation. Main references in this area are Kristoufek [10, 9], Kim et al. [8]. Alternatively, in Bukovina and Martiček [2] a sentiment measure related to the BitCoin system is obtained from the website Sentdex.com. This website collect data on sentiment through an algorithm, based on Natural Language Processing techniques, which is capable of identifying string of words conveying positive, neutral or negative sentiment on a topic (BitCoin in this case). The authors of the paper develop a model in discrete time and show that excessive confidence on the system may boost a Bubble on the BitCoin price.

Motivated by the evidences in the above quoted papers we introduce a bivariate model in continuous time to describe both the dynamics of a BitCoin sentiment indicator and of the corresponding BitCoin price.

From the theoretical viewpoint we give three contributions: the model is proven to be arbitrage-free under proper conditions and its statistical properties are investigated. Then, based on risk-neutral evaluation, a quasi-closed formula is derived for any European style derivative on the BitCoin. It is worth noticing that a market for derivatives on BitCoin has recently raised on appropriate websites such as https://coinut.com and https://deribit.com trading European Calls and Puts as well as Binary option endorsing the idea in Yermack [20] that BitCoins are likely to be used for speculative purposes.

Further, the likelihood for a discrete sample of the model is computed and an approximated closed formula is derived so that maximum likelihood estimates can be obtained for model parameters. Precisely, we suggest a two-step maximum likelihood method, the profile likelihood described in Davison [3], Pawitan [16] to fit the model to market data. From the empirical viewpoint we contribute to the literature by fitting the suggested model to market data considering both the Volume and the number of Google searches as proxies for the sentiment factor. Besides the performance of the pricing formula is assesses on a sample of market option prices obtained by the website https://deribit.com.

The rest of the paper is structured as follows. In Section 2 we describe the model for the BitCoin price dynamics and show that the market is arbitrage-free under a mild condition. In Section 3 we compute the joint distribution of the discretely sampled model as well as a closed form approximation. Then, we propose a statistical estimation procedure based on the corresponding approximated profile likelihood. In Section 4 we prove a quasi-closed formula for European-style derivatives with detailed computations for Plain Vanilla and Binary option prices. Section 5 is devoted to test the possible proxies for the sentiment indicator, such as the number and volume of BitCoin transactions or the internet searches on Google and Wikipedia and to apply the whole estimation procedure to market data obtained from http://blockchain.info. In Section 6 we evaluate model performance for option pricing considering options traded on https://deribit.com for some "test" days. Finally, in Section 7 we give some concluding remarks and draw directions for interesting future investigations. The Appendices collect a brief description of the Levy approximation approach and the proofs of most of the technical results.

2. The BitCoin market model

We fix a probability space endowed with a filtration that satisfies the usual conditions of right-continuity and completeness. On the given probability space, we consider a main market in which heterogeneous agents buy or sell BitCoins and denote by the price process of the cryptocurrency. We assume that the BitCoin price dynamics is described by the following equation:

| (2.1) |

where , represent model parameters; is a standard -Brownian motion on and is a stochastic factor, representing the sentiment index in the BitCoin market, satisfying

| (2.2) |

Here, , , , is a standard -Brownian motion on , which is -independent of , and is a continuous (deterministic) initial function. Note that, the non negative property of the function corresponds to require that the minimum level for sentiment is zero. It is worth noticing that in (2.2) we also consider the effect of the past, since we assume that the sentiment factor affects explicitly the BitCoin price up to a certain preceding time . Assuming that and that factor is observed in the period makes the bivariate model jointly feasible. It is well-known that the solution of (2.2) is available in closed form and that has a lognormal distribution for each , see Black and Scholes [1]. Here, stands for an exogenous factor affecting the instantaneous variance of the BitCoin price changes modulated by . It is worth noticing that the instantaneous variance of the BitCoin price process increases with the delayed process ; this may appear counter-intuitive if is interpreted only as a positive sentiment indicator. However, in our perspective, the factor is mathematically a non-negative variable but does not necessary represent a positive sentiment indicator. Examples are the volume or number of transactions; these are non negative values which increase with both short (fear) and long (enthusiasm) positions in BitCoins. Similarly, the number of internet searches within a fixed time period cannot go negative but internet searches may increase both with enthusiasm and fear about the BitCoin System, or whatever other financial asset we would like to model with the dynamics we suggest here. Hence, an increase in may be actually related to an increase in the uncertainty about the the price . In order to visualize the dynamics implied by the model in equations (2.1) and (2.2), we plot in Figure 1 a possible simulated path of daily observations for the sentiment factor and the corresponding BitCoin prices within one year horizon by letting vary; as expected, market reaction to sentiment is delayed when increases.

Remark 2.1.

The suggested model is motivated by the outcomes in Kristoufek [10, 9], Kim et al. [8], Bukovina and Martiček [2] where the authors relate the BitCoin price dynamics to some sentiment factors and does not take into account special features of the BitCoin market such as the underlying technology or the order mechanism. Besides, BitCoin is treated as a financial stock as suggested in Yermack [20]. Possibly, the model can be applied to any other financial assets whether one believes their price to depend on suitably identified sentiment indicators.

We assume that the reference filtration , describing the information on the BitCoin market, is of the form

where and denote the -algebras generated by and respectively up to time . Note that , for each , with being the -algebra generated by up to time . Since at any time the BitCoin price dynamics is affected by the sentiment index only up to time , to describe the traders information on the digital market, we consider the filtration , defined by

We also remark that all filtrations satisfy the usual conditions of completeness and right continuity (see e.g. Protter [17]). Now, we introduce the integrated information process associated to the sentiment index , defined as follows:

| (2.3) |

Note that, for , we have which is deterministic. In addition, for a finite time horizon , let us define the corresponding variation over the interval , for , as . Obviously, ; moreover, for ,

| (2.4) |

Again, note that for , we get which is deterministic.

The following lemma establishes basic statistical properties for the integrated information process as well as for its variation in case they are not fully deterministic.

Lemma 2.2.

In the market model outlined above we have:

-

(i)

For ,

-

(ii)

For ,

-

(iii)

For ,

In [7] similar outcomes are claimed for without providing a proof; for the sake of clarity, we give a self-contained proof in Appendix B.

The system given by equations (2.1) and (2.2)

is well-defined in as stated in the following theorem, which also provides its explicit solution.

Theorem 2.3.

In the market model outlined above, the followings hold:

-

(i)

the bivariate stochastic delayed differential equation

(2.5) has a continuous, -adapted, unique solution given by

(2.6) (2.7) More precisely, can be computed step by step as follows: for and ,

(2.8) In particular, -a.s. for all . If in addition, , then -a.s. for all .

-

(ii)

Further, for every , the conditional distribution of , given the integrated information , is log-Normal with mean and variance .

-

(iii)

Finally, for every , the random variable has mean and variance ; for every , has mean and variance respectively given by

where and are both provided by Lemma 2.2, point (i).

Proof.

Point (i). Clearly, and , given in (2.6) and (2.7) respectively, are -adapted processes with continuous trajectories. Similarly to Mao and Sabanis [12, Theorem 2.1], we provide existence and uniqueness of a strong solution to the pair of stochastic differential equations in system (2.5) by using forward induction steps of length , without the need of checking any assumptions on the coefficients, e.g. the local Lipschitz condition and the linear growth condition.

First, note that the second equation in the system (2.5) does not depend on , and its solution is well known for all . Clearly, equation (2.7) says that -a.s. for all and that implies that the solution remains strictly greater than over , i.e. , -a.s. for all .

Next, by the first equation in

(2.5) and applying Itô’s formula to , we get

| (2.9) |

or equivalently, in integral form

| (2.10) |

For , (2.10) can be written as

| (2.11) |

that is, (2.8) holds for .

Given that is now known for , we may restrict the first equation in (2.5) on , so that it corresponds to consider (2.9) for . Equivalently, in integral form,

| (2.12) |

This shows that (2.8) holds for . Similar computations for , give the final result.

Point (ii). Set , for and , for , with . Then, by applying the outcomes in Point (i) and the decomposition

for , with , we can write

| (2.13) |

To complete the proof,

it suffices to show that, for each the random variable , conditional on , is Normally distributed with mean and variance . This is straightforward from (2.11) if . Otherwise, we first observe that

since is independent of for every , the distribution of , conditional on , is Normal with mean and variance .

Now, for each , the moment-generating function of , conditioned on the history of the process up to time , is given by

that only depends on its integrated information up to time , that is,

Point (iii). The proof is trivial for . If , (2.13) and Lemma 2.2 together with the null-expectation property of the Itô integral, give

Now, we compute the variance of . Since for each the random variable has mean conditional on , we have

Thus, the proof is complete. ∎

2.1. Existence of a risk-neutral probability measure

Let us fix a finite time horizon and assume the existence of a riskless asset, say the money market account, whose value process is given by

where is a bounded, deterministic function representing the instantaneous risk-free interest rate. To exclude arbitrage opportunities, we need to check that the set of all equivalent martingale measures for the BitCoin price process is non-empty. More precisely, it contains more than a single element, since does not represent the price of any tradeable asset, and therefore the underlying market model is incomplete.

Lemma 2.4.

Let , for each , in (2.2). Then, every equivalent martingale measure for defined on has the following density

| (2.14) |

where is the terminal value of the -martingale given by

| (2.15) |

for a suitable -progressively measurable process .

The proof is postponed to Appendix B. Here denotes the Doleans-Dade exponential of an -semimartingale .

In the rest of the paper, suppose that , for each , in (2.2). Then, Lemma 2.4 ensures that the space of equivalent martingale measures for is described by (2.15). More precisely, it is parameterized by the process which governs the change of drift of the -Brownian motion . Note that the sentiment factor dynamics under in the BitCoin market is given by

The process can be interpreted as the risk perception associated to the future direction or future possible movements of the BitCoin market. One simple example of a candidate equivalent martingale measure is the so-called minimal martingale measure (see e.g. Föllmer and Schweizer [4], Föllmer and Schweizer [5]), denoted by , whose density process , is given by

| (2.16) |

This is the probability measure which corresponds to the choice in (2.15). Intuitively, under the minimal martingale measure, say , the drift of the Brownian motion driving the BitCoin price process is modified to make an -martingale, while the drift of the Brownian motion which is strongly orthogonal to is not affected by the change measure from to . More precisely, under the change of measure from to , we have two independent -Brownian motions and defined respectively by

| (2.17) | ||||

| (2.18) |

Denote by the discounted BitCoin price process defined as , for each . Then, on the probability space , the pair satisfies the following system of stochastic delayed differential equations:

| (2.19) |

By Theorem 2.3, point (i), the explicit expression of the solution to (2.19), which provides the discounted BitCoin price , at any time , is given by

| (2.20) |

with the representation of the sentiment factor still provided by (2.7).

Under our assumptions, the dynamics of the (non-discounted) BitCoin price under the minimal martingale measure is given by

| (2.21) |

where is the risk-free interest rate at time . The above dynamics was assumed in Hull and White [7] to describe price changes for a stock and its instantaneous variance (for which and by definition). However, the authors assumed from the very beginning a risk-neutral framework without defining the dynamics under the physical measure and with no proof of the existence of any equivalent martingale measure.

In Section 4, we derive option pricing formulas via the risk-neutral evaluation procedure based on the minimal martingale measure above defined. As usual, pricing formulas depend on model parameters which have to be estimated on market data. A common approach, when a closed formula for option is available, is the so called calibration of parameters; their value is obtained in order to minimize a proper distance between model an market prices for options. However, this method is particularly of interest when there is a standardized and liquid market for options. Of course, this is not the case for the BitCoin so we will fit the model directly to a time series of BitCoin prices with a more classical statistical procedure based on the approximation of the probability density function of a discrete sample for model described by equations (2.1) and (2.2). To this end we need to know the dynamics of the BitCoin price under the physical measure and derive statistical properties for a discrete sample of the process given in (2.2).

3. Statistical properties of discretely observed quantities and parameter estimation

In this section, we introduce basic statistical properties for a sample of discretely observed prices and suggest a possible closed form approximation for the joint probability density of the discrete sample.

Let us fix a discrete observation step and consider the discrete time process , where . Define the corresponding logarithmic returns process as

| (3.1) |

By (2.13), we get

| (3.2) |

Setting , with , as in the proof of Theorem 2.3, we define

| (3.3) |

so that, (3.2) can be written as

| (3.4) |

where , with being the variation of the integrated information process introduced in (2.3); since is fixed we omit hereafter the dependence on it and, without loss of generality we assume so that . Note that if the quantities are deterministic and the outcomes in what follows still hold if is replaced by the first non deterministic value .

Let us consider a finite time horizon ; under model assumptions the conditional probability distribution of the vector , given the vector , is a multi-variate normal with covariance matrix . Hence, the vector of discretely observed logarithmic returns , conditionally on , is jointly normal with covariance matrix . The application of Bayes’s rule allows to write the unconditional joint probability distribution of , i.e. the density function as

| (3.5) |

with and , .

The probability distribution functions and are not available in closed form; though, several approximations exist among which those introduced in Levy [11] and Milevsky and Posner [14]. Of course any approximation available for such densities can be applied in order to find a closed formula approximating the joint density ; in what follows we adopt the one suggested in Levy [11], see Appendix A for further details. Note that the inverse gamma approach suggested in Milevsky and Posner [14] holds in the limit when tends to infinity, a condition which is not at all consistent with the applications we have in mind; further discussion on the approximating distribution to select is beyond the scope of our paper.

3.1. The approximated likelihood

One of the pillar in statistical inference is the maximum likelihood (in short ML) estimation approach where model parameters are estimated so as to maximize the probability of the the realized sample to be extracted randomly; the likelihood function shares the same mathematical expression of the probability density function but it is computed "ex-post" when a realization of involved random variables is available and assuming the underlying model parameters to be unknown. It is well known that ML estimates are consistent and asymptotically normal and they achieve efficiency, i.e. they have the lowest variance among estimators sharing the same asymptotic properties (see Davison [3]).

By applying the approximation of Levy [11], we prove the following Lemma.

Lemma 3.1.

Let , for each , in (2.2) and . Then, in the market model outlined in Section 2, we have

-

(i)

the distribution of is approximated by a log-normal with mean and variance given by

(3.6) (3.7) -

(ii)

the distribution of given (shortly ), for , is approximated by a log-normal with means and variances given by

(3.8) (3.9)

The proof is postponed to Appendix B. Now, we are in the position to state the following theorem.

Theorem 3.2.

Under the same assumptions of Lemma 3.1, given the realized sample , the log-likelihood function can be approximated by

| (3.10) |

where upper case letters are used for random variables and lowercase for the corresponding realizations.

Proof.

First, recall that the likelihood function of a parameter corresponds to the probability density function where random variables are replaced by they realizations and parameters are unknown. Then, by simply applying the logarithmic function to (3.5) we get

| (3.11) |

Replacing the unknown densities in (3.11) according to Lemma 3.1 gives the desired result.

∎

Maximum likelihood estimates for the model can be obtained by maximizing the log-likelihood approximation in (3.10) i.e.

| (3.12) |

In this case the methodology is referred to as Quasi-Maximum likelihood since the exact expression of the likelihood is not available; under suitable conditions, quasi-maximum likelihood estimates are asymptotically equivalent to the maximum likelihood estimates, see e.g. White [19], Gourieroux et al. [6]. We also performed a simulation study to assess finite sample behavior of the estimates.

It is worth to stress that the above estimation method does not assume the process to be observed, as far as and , are observed (note that is the cumulative of along the time interval ).

3.2. Finite sample behavior of QML estimates

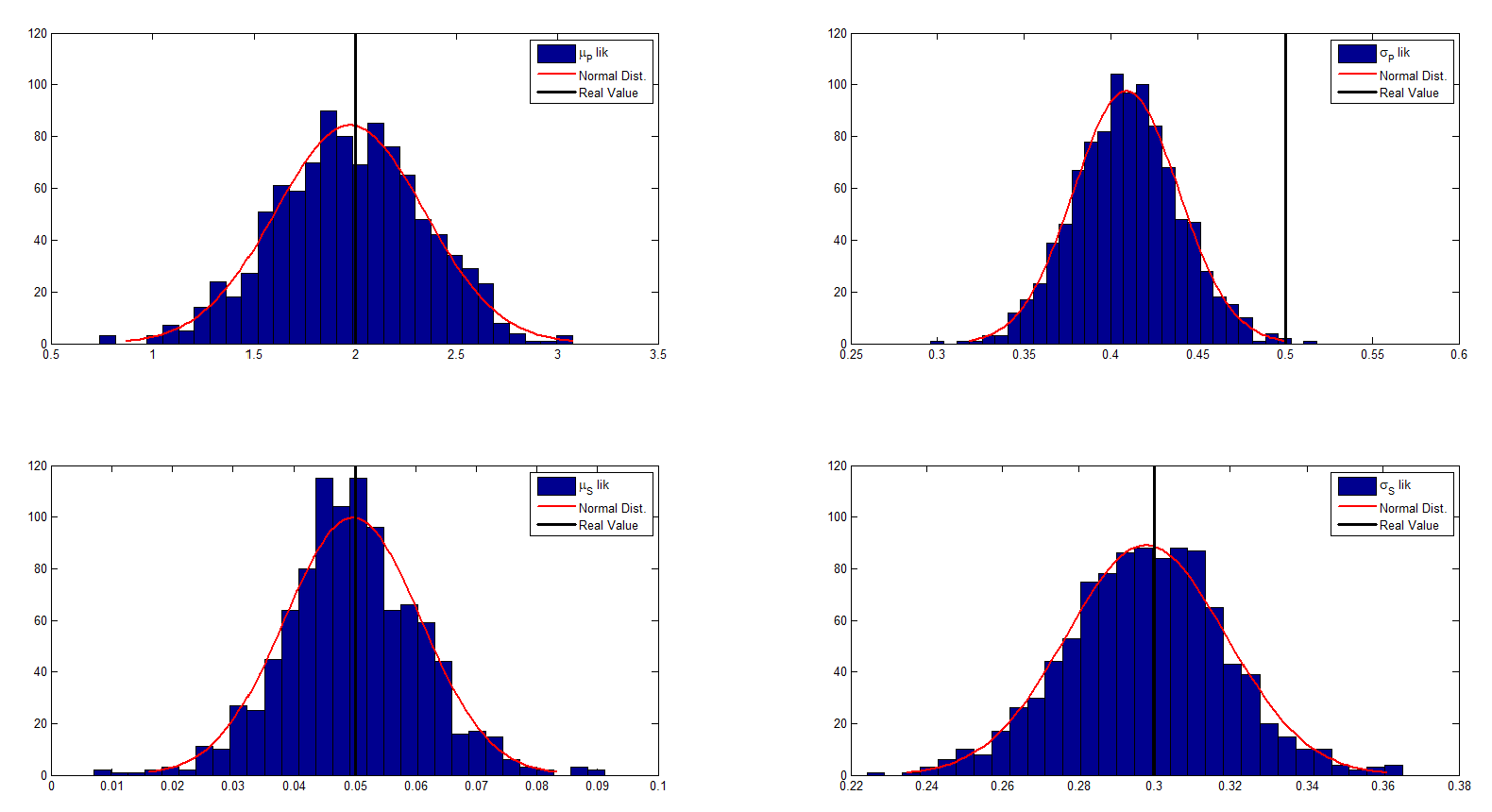

In order to check the goodness of the log-likelihood approximation introduced in Theorem 3.2, we apply the proposed estimation method to simulated data and assume, for the sake of simplicity, . We simulate samples of length for the processes in (2.1) and (2.2) assuming a constant finer observation step ; we extract corresponding samples for at a lower frequency, with observation step . In the numerical exercise we choose , , (daily observations), (weekly observations); parameters values are set as , , . We end with samples of observations for ; for each sample we estimate the parameters by means of the quasi-maximum likelihood as suggested in previous subsection. The results are summed up in Table 1.

| Variable | Theor. value | Fitted value | Std. error | t-value | P() | RMSE |

|---|---|---|---|---|---|---|

| 2.0000 | 1.9759 | 0.3675 | -0.0655 | 0.9478 | 11.6475 | |

| 0.5000 | 0.4089 | 0.0302 | -3.0170 | 0.0026 | 3.0358 | |

| 0.0500 | 0.0497 | 0.0112 | -0.0297 | 0.9763 | 0.3544 | |

| 0.3000 | 0.2978 | 0.0210 | -0.1032 | 0.9178 | 0.6687 |

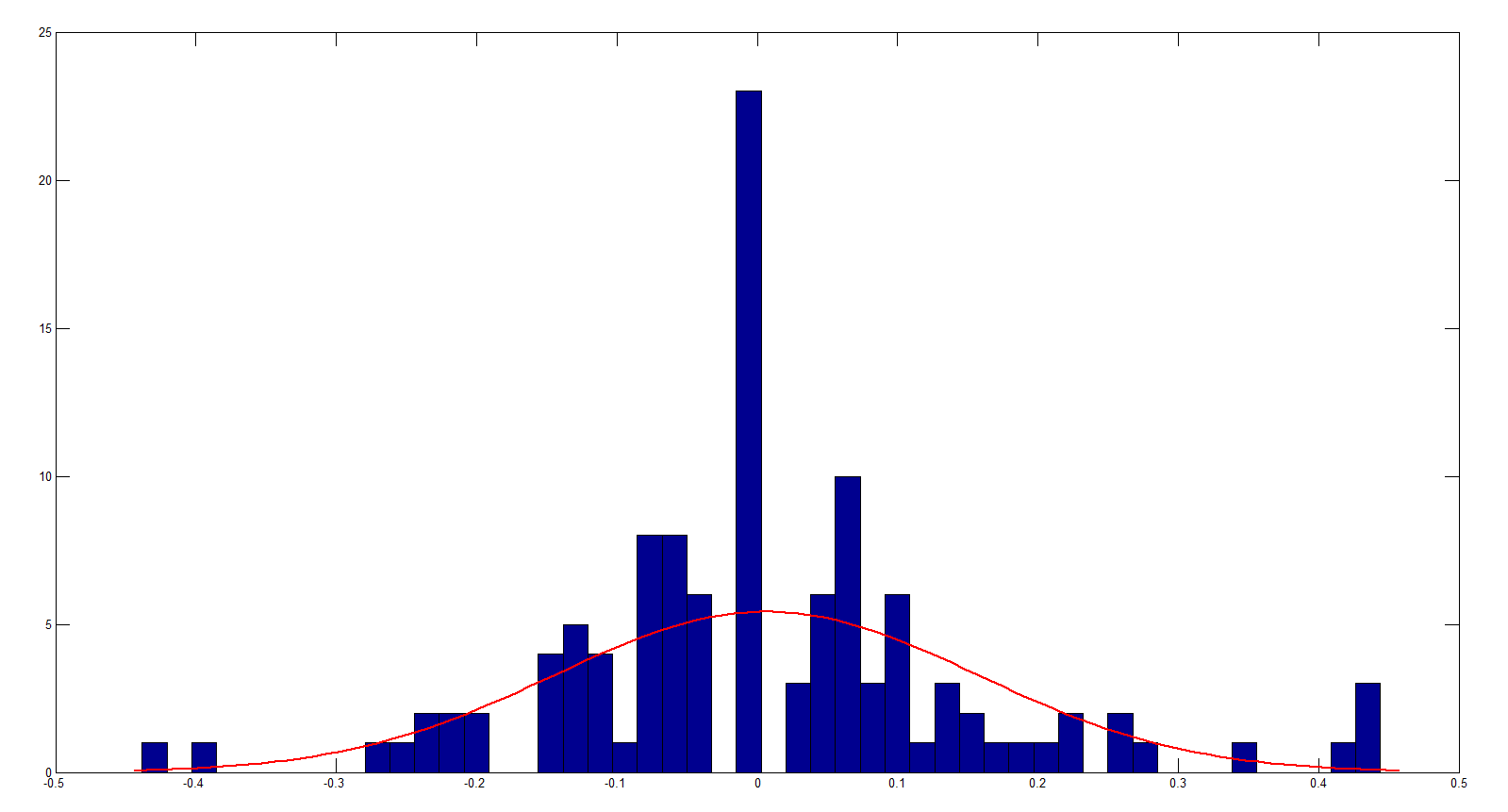

We also performed a -test in order to check for estimation bias. The fitted values of are close in mean to their theoretical value and with a reasonable standard deviation; the -values of the t-test confirm that estimated are not biased. Different conclusions are in order as for parameter which estimations is by no doubt biased. In Figure 2 we plot the histograms of the estimated as well as the fitted normal distribution and the expected mean of the asymptotic distribution. Pictures confirm the biasedness of the estimator for but all other estimates perform well and outcomes may become better by increasing the sample length. The simulation exercise have been repeated by letting the parameters values, the number and the sample length vary obtaining analogous qualitative results.

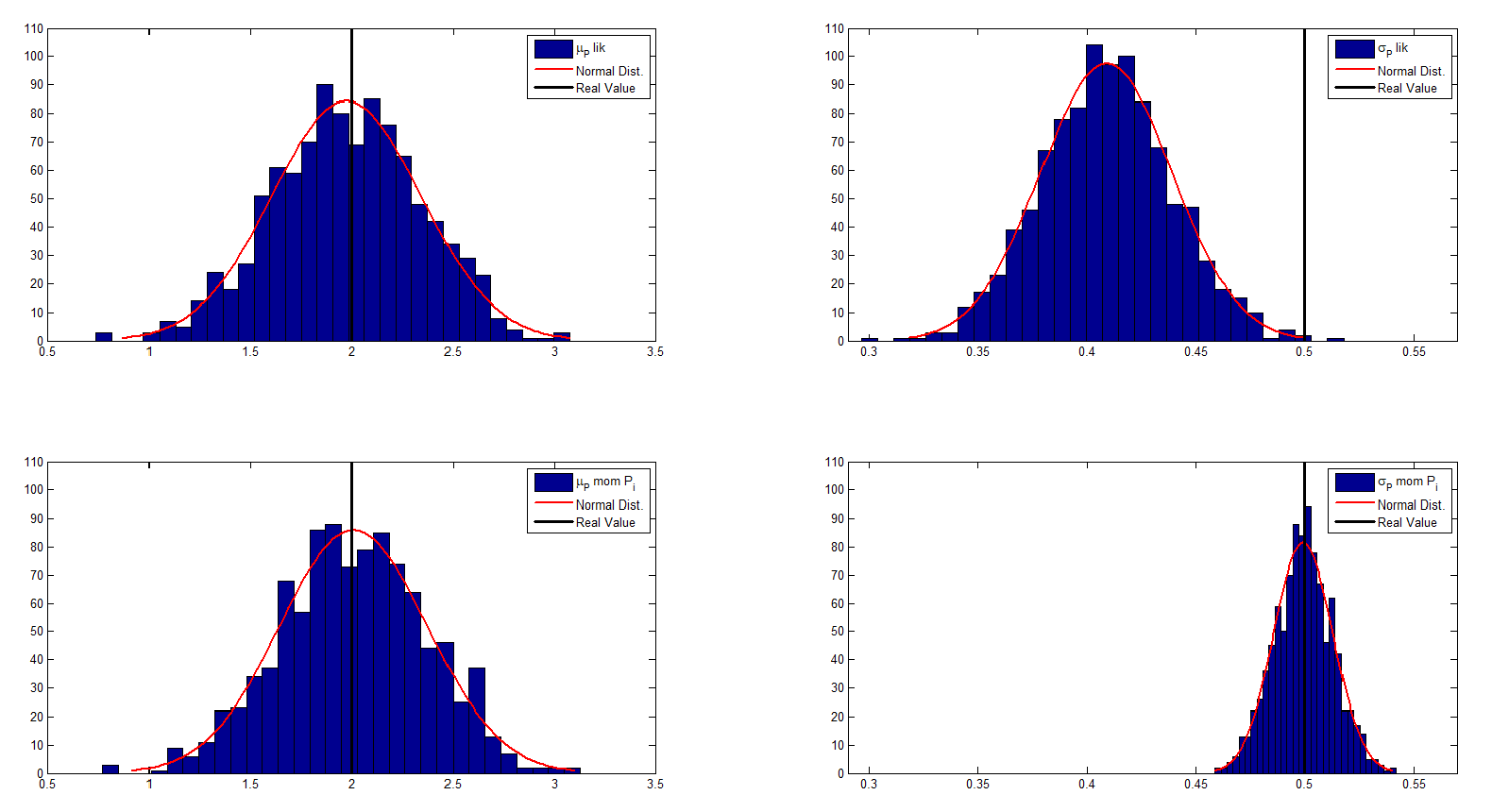

In order to disentangle the contribution of the Levy approximation [11] to the estimation bias, we suggest to apply the method of moments to estimate and considering the whole sample for generated at the finer observation step to compute the sample mean and sample variance of the sentiment realizations. If we then we plug the estimated values in the likelihood (3.10) in order to estimate these two estimates remain unchanged; in fact the likelihood may be maximized separately with respect to and since each of the two addend in the likelihood expression depends on just one of this pairs. The results of this alternative estimation method are reported in Table 2.

| Variable | Theor. value | Fitted value | Std. error | t-value | P() | RMSE |

|---|---|---|---|---|---|---|

| 2.0000 | 2.0104 | 0.3638 | 0.0286 | 0.9772 | 11.5034 | |

| 0.5000 | 0.4995 | 0.0135 | -0.0385 | 0.9693 | 0.4282 |

To visualize the bias of we plot in Figure 3 the histogram of parameter fit with simulated data using the two methods. As we can see using the two step procedure we obtain better estimates of both in terms of expected value and standard deviation. It is evident from Table 2 and Figure 3 the that the estimation of is not biased in this case hence the estimation bias may essentially be attributed to the aggregation of the sentiment over time intervals and to the corresponding approximating distribution. Hence, whether the sentiment factor is observed at a finer step than the price, the above separate estimation is more reliable.

3.3. Estimation of the delay parameter

The delay parameter directly affects the definition of the discrete process . Hence, in order to proceed with its estimation we need to observe the process at a finer observation step with respect to the log-returns. In what follows we set and we adopt a two step estimation procedure known as Profile Likelihood in order to estimate the delay. We briefly describe the Profile Likelihood approach to estimation and its application in our specific case; interested readers are referred to Davison [3], Pawitan [16] for details on the profile likelihood. The basic idea of this approach is to split the parameter vector which has to be estimated, say , in two sub-vectors, one representing the parameter of interest and the other the so called nuisance parameter i.e. ; to estimate and jointly we should maximize at once the likelihood i.e.

| (3.13) |

When this is not feasible and provided the likelihood computed with respect to the nuisance parameter vector is available and it is easy to maximize we can apply a two step procedure by maximizing, in its parametric space,

| (3.14) |

where is the maximum likelihood estimate of for a fixed , then the best estimate for is

| (3.15) |

Classical confidence intervals cannot be defined in this setting; indeed, it is possible to obtain a confidence region for using the likelihood ratio statistics (see Davison [3]), defined as

| (3.16) |

where

| (3.17) |

and is an assigned value for . These results imply that the confidence region for is the set

| (3.18) |

with is the quantile of the distribution.

In our exercise we split in where is the parameter on which we are focusing and is the nuisance parameter vector. The Profile Likelihood approach is feasible in our case since a closed approximating expression for the likelihood with respect to the nuisance parameter is indeed available. The parametric space for is the interval in this case but, for practical purposes, is chosen on a grid i.e. ; the maximization of the likelihood is then performed with respect to for each value in the grid, obtaining for . An estimate for is then obtained as . Finally we get . Of course the estimation error decreases with the mesh of the grid so that it sufficiently spans the parametric set for .

4. Risk neutral evaluation of European-type contingent claims

Let be an -measurable random variable representing the payoff a European-type contingent claim with date of maturity , which can be traded on the underlying market. Here is a a Borel-measurable function such that is integrable under . The function is usually referred to as the contract function. The following result provides a risk-neutral pricing formula under the minimal martingale measure for any -integrable European contingent claim. Since the martingale measure is fixed, the risk-neutral price agrees with the arbitrage free price for those options which can be replicated by investing on the underlying market. Recall that , for each , refers to the variation of the process defined in (2.3), over the interval . Then, denote by the conditional expectation with respect to under the probability measure and so on.

Theorem 4.1.

Let be the payoff a European-type contingent claim with date of maturity . Then, the risk-neutral price at time of is given by

| (4.1) |

where is a Borel-measurable function such that

| (4.2) |

for a suitable function depending on the contract such that is -integrable.

Proof.

For the sake of simplicity suppose that and set , for each . Then, the risk-neutral price at time of a European-type contingent claim with payoff is given by

| (4.3) | ||||

| (4.4) |

where denotes the conditional expectation with respect to under the minimal martingale measure . More generally, (4.4) can be written as

| (4.5) |

for a suitable function depending on the contract function . Since the -Brownian motion driving the factor is not affected by the change of measure from to by the definition of minimal martingale measure, we have that is also an -Brownian motion independent of , see (2.18). Hence, we can apply the same arguments used in point (ii) of the proof of Theorem 2.3, to get that, for each , the random variable conditioned on is Normally distributed with mean and variance . Then, we can write (in law) that , where is a standard Normal random variable and this allows to find a function such that (4.2) holds, which means that the conditional expectation with respect to in (4.5) only depends on and , for every . Consequently, the risk-neutral price can be written as

| (4.6) |

where the last equality holds since is -adapted and is independent of , for each , see e.g. Pascucci [15, Lemma A.108]. More precisely, we have

| (4.7) |

where

| (4.8) |

∎

Remark 4.2.

It is worth to remark that , with , represents the risk-neutral price at time of the contract in a Black & Scholes framework, where the constant volatility parameter is defined by

This is proved explicitly in Corollary 4.4 below for the special case of a plain vanilla European Call option.

Remark 4.3.

A pricing formula analogous to (4.6) is conjectured in Hull and White [7] for a special example of the model suggested here ( and ). As already noticed the authors start from the very beginning under a risk neutral framework. Theorem 4.1 extends their results to the more general case and give a rigorous proof.

4.1. A Black & Scholes-type option pricing formula

Let us consider a European Call option with strike price and maturity and define the function as follows

| (4.9) |

where

| (4.10) |

and , or more explicitly

| (4.11) |

Here, stands for the standard Gaussian cumulative distribution function

Corollary 4.4.

Proof.

As in the proof of Theorem 4.1, let us assume that . Under the minimal martingale measure , the risk-neutral price at time of a European Call option written on the BitCoin with price expiring in and with strike price , is given by

where we have set and . Recall that , for every . Then, the term can be written as

| (4.13) | ||||

| (4.14) | ||||

| (4.15) |

as for each , the random variable has a standard Gaussian law given under the minimal martingale measure . Concerning , consider the auxiliary probability measure on defined as follows:

| (4.16) |

By Girsanov’s Theorem, we get that the process , given by

| (4.17) |

follows a standard -Brownian motion. In addition, using (2.20), we obtain

| (4.18) |

for every . Since is -adapted, by (2.20) and the Bayes formula on the change of probability measure for conditional expectation, for every we get

| (4.19) |

with

In the above computations, analogously to before, we have set , for each . Consequently, we have that conditional on , is a Normally distributed random variable with mean and variance , for each , since is not affected by the change of measure from to . Indeed, by the change of numéraire theorem, we have that the probability measure turns out to be the minimal martingale measure corresponding to the choice of the BitCoin price process as benchmark. Further, by applying again the Bayes formula on the change of probability measure for conditional expectation, we get

| (4.20) |

since the conditional Gaussian distribution of gives

Finally, gathering the two terms (4.20) and (4.19), for every we obtain

| (4.21) |

where the last equality follows again from Pascucci [15, Lemma A.108], since for each , is independent of and is -measurable.

∎

It is worth noticing that the option pricing formula (4.12) only depends on the distribution of which is the same both under measure and . As observed in Remark 4.2, formula (4.12) evaluated in corresponds to the Black & Scholes price at time of a European Call option written on , with strike price and maturity , in a market where the volatility parameter is given by . Then, for every it may be written as:

| (4.22) |

where denotes the density function of , for each (if it exists). The price at time for a plain vanilla European option may also be written as a Black & Scholes style price:

| (4.23) |

where

| (4.24) |

and

| (4.26) |

To compute numerically derivative prices by the above formulas, we should compute the distribution of , which is not an easy task.

Similar formulas can be computed for other European style derivatives as for binary options which, indeed, are quoted in BitCoin markets. For the case of a Cash or Nothing Call, which is essentially a bet of on the exercise event, the risk-neutral pricing formula is given by

| (4.28) | ||||

| (4.29) |

By applying the Levy approximation, see Levy [11], to , the Call option pricing formula becomes

| (4.30) |

which can be computed numerically, once parameters are obtained. Similarly, Binary Options with terminal value when in the money, are priced by computing numerically the following formula:

| (4.31) |

4.2. Numerical exercise

In this subsection we compute European plain vanilla and binary option prices assuming that model parameter are known and considering several strike prices and expiration dates. Besides, we also let the initial sentiment and the delay values change in order to understand their contribution to the option price formation. Assume that model parameters are , the riskless interest rate is and that the BitCoin price at time is (this is the price by October 2016).

In Table 3, Call option prices are reported for months, = 5 days. Rows correspond to different values of while columns to different values for the strike price. As expected, Call option prices are increasing with respect to initial sentiment for the BitCoin and decreasing with respect to strike prices.

| K | 400 | 425 | 450 | 475 | 500 |

|---|---|---|---|---|---|

| 51.24 | 28.35 | 11.46 | 3.09 | 0.54 | |

| 64.12 | 48.05 | 34.94 | 24.69 | 16.97 | |

| 128.68 | 117.75 | 107.77 | 98.66 | 90.35 |

In Table 4, Call option prices are summed up, for , by letting the expiration date and the delay vary. Again as expected, for Plain Vanilla Calls the price increases with time to maturity. Increasing the delay reduces option prices; of course the spread is inversely related to the time to maturity of the option.

| K | 400 | 425 | 450 | 475 | 500 |

|---|---|---|---|---|---|

| =1 month, =1 week | 52.85 | 33.09 | 18.27 | 8.81 | 3.71 |

| =1 month, =2 weeks | 51.58 | 30.62 | 15.18 | 6.13 | 2.00 |

| =3 months, =1 week | 64.12 | 48.05 | 34.94 | 24.69 | 16.97 |

| =3 months, =2 weeks | 62.95 | 46.65 | 33.42 | 23.18 | 15.60 |

In Tables 5 and 6, analogous results are reported for Binary Options with outcome ; Table 5 sums up Binary Cash-or-Nothing prices for , , , , , months, week (5 working days) against several strikes (in colums). Rows correspond to different values for the initial sentiment on BitCoins. As expected, prices are decreasing with respect to strike prices. Here, in the money (ITM) options values are decreasing with respect to while out of the money (OTM) ones are increasing. The difference in ITM and OTM prices is large for low values of , while it is very small for a high level of the initial sentiment factor in BitCoins. This may be justified by the fact that, when the sentiment factor in the BitCoin is strong, all bets are worth, even the OTM ones, since the underlying value is expected to blow up. Binary Call prices decrease with respect to time to maturity for ITM options and increase for OTM options which become more likely to be exercised. The influence of the delay value is tiny, as for vanilla options, being larger for short time to maturities.

| K | 400 | 425 | 450 | 475 | 500 |

|---|---|---|---|---|---|

| 97.17 | 82.77 | 50.31 | 18.87 | 4.24 | |

| 70.07 | 58.38 | 46.58 | 35.66 | 26.27 | |

| 45.70 | 41.77 | 38.14 | 34.79 | 31.72 |

| K | 400 | 425 | 450 | 475 | 500 |

|---|---|---|---|---|---|

| =1 month, =1 week | 86.93 | 69.97 | 48.27 | 28.11 | 13.83 |

| =1 month, =2 weeks | 91.50 | 74.23 | 48.69 | 24.84 | 9.80 |

| =3 months, =1 week | 70.07 | 58.38 | 46.58 | 35.66 | 26.27 |

| =3 months, =2 weeks | 71.21 | 59.10 | 46.77 | 35.36 | 25.62 |

5. Model fitting on real data

This section is devoted to the estimation of the model in (2.1)-(2.2) on real data; the overall procedure is aimed at describing the dynamics of BitCoin price changes over time. In order to fit the model we need data for both the BitCoin price and the sentiment indicator. Several proxies have been suggested for the latter; traditional indicators of market sentiment on a stock asset such as the number and volume of transactions [10] as well as sentiment indicators such as the number of Google searches or Wikipedia requests in the period under investigation [2]. Internet-based proxies are particularly interesting for the BitCoin price formation, being BitCoin itself an internet-based asset. First we investigate which of the suggested proxies is consistent with the dynamics in (2.2) and then we fit the full model to BitCoin prices. Daily data for BitCoin prices, volume and number of transactions are obtained through the website http://blockchain.info which provides a mean price among main exchanges trading on BitCoin and the total exchanged volume. Weekly data for the number of Google searches are downloaded from Google-Trends website (daily data are not available). Daily data for Wikipedia requests are obtained through the website http://tools.wmflabs.org/pageviews.

5.1. Proxies for Sentiment

The univariate process is a Geometric Brownian motion; the corresponding discrete process of logarithmic returns is given by , where , and it is well-known that these are independent an identically distributed with mean and variance . Hence, in order to choose a suitable proxy, based on discrete observations, for the process , we simply perform a stationary test and a normality test on the corresponding realizations of , using respectively the augmented Dickey–Fuller test [18], and the one-sample Kolmogorov-Smirnov test [13]. We consider the number and the volume of transactions as examples of traditional indicators and the number of Google searches and Wikipedia requests as examples of sentiment indicators. The first three series were investigated from 01/01/2012 to 31/03/2017 while Wikipedia requests are considered from 01/07/2015 to 31/03/2017.

The tests are performed on the whole time series and on the sub-samples from 01/01/2015 to 31/03/2017.

| Time series | p-value111 * ; ** ; *** ; ; **** | |||

|---|---|---|---|---|

| Num. trans. | Vol. trans. | Google searches | Wiki requests | |

| All series | 1.0000e-03*** | 1.0000e-03*** | 1.0000e-03*** | - |

| Sub-sample | 1.0000e-03*** | 1.0000e-03*** | 1.0000e-03*** | 1.0000e-03***222Data available only from 01/07/2015. |

| Time series | p-value111 * ; ** ; *** ; ; **** | |||

|---|---|---|---|---|

| Num. trans. | Vol. trans. | Google searches | Wiki requests | |

| All series | 5.1011e-05**** | 4.3576e-07**** | 2.9246e-07**** | - |

| Sub-sample | 0.0035** | 0.2152 | 0.1012 | 1.3575e-11****222Data available only from 01/07/2015. |

Non-stationarity is rejected for all proxies; besides, lognormality is not rejected, for the sub-sample from 01/01/2015 to 31/03/2017, both for the and the number of . In Figure 4 we plot the histograms of the latter two proxies; it is evident that the log-normality fit for the time series is better.

5.2. Estimation Results with QML method

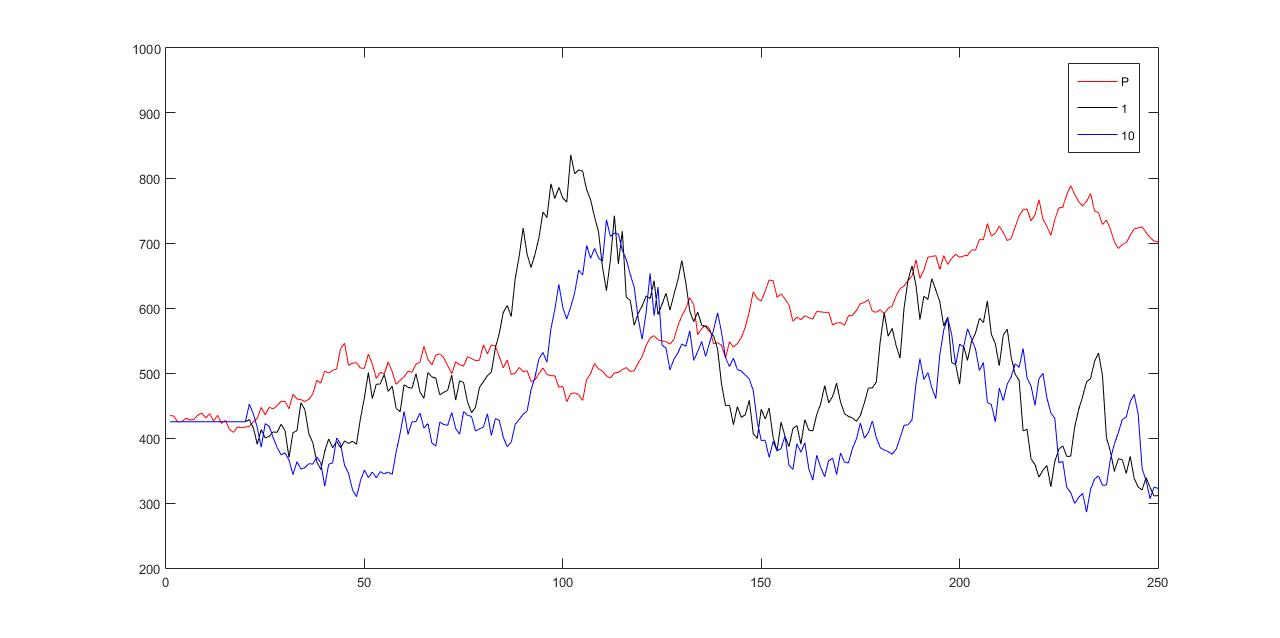

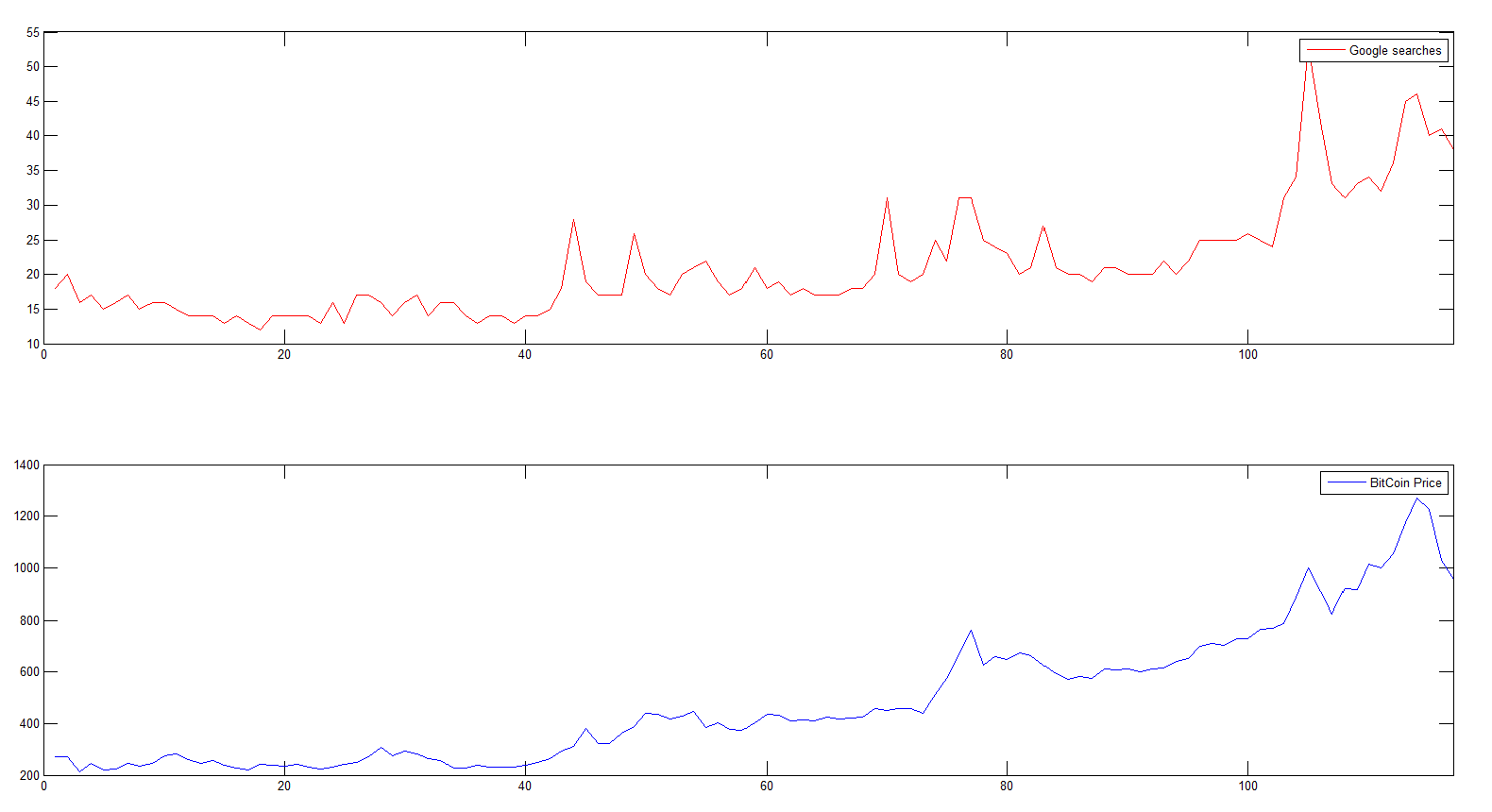

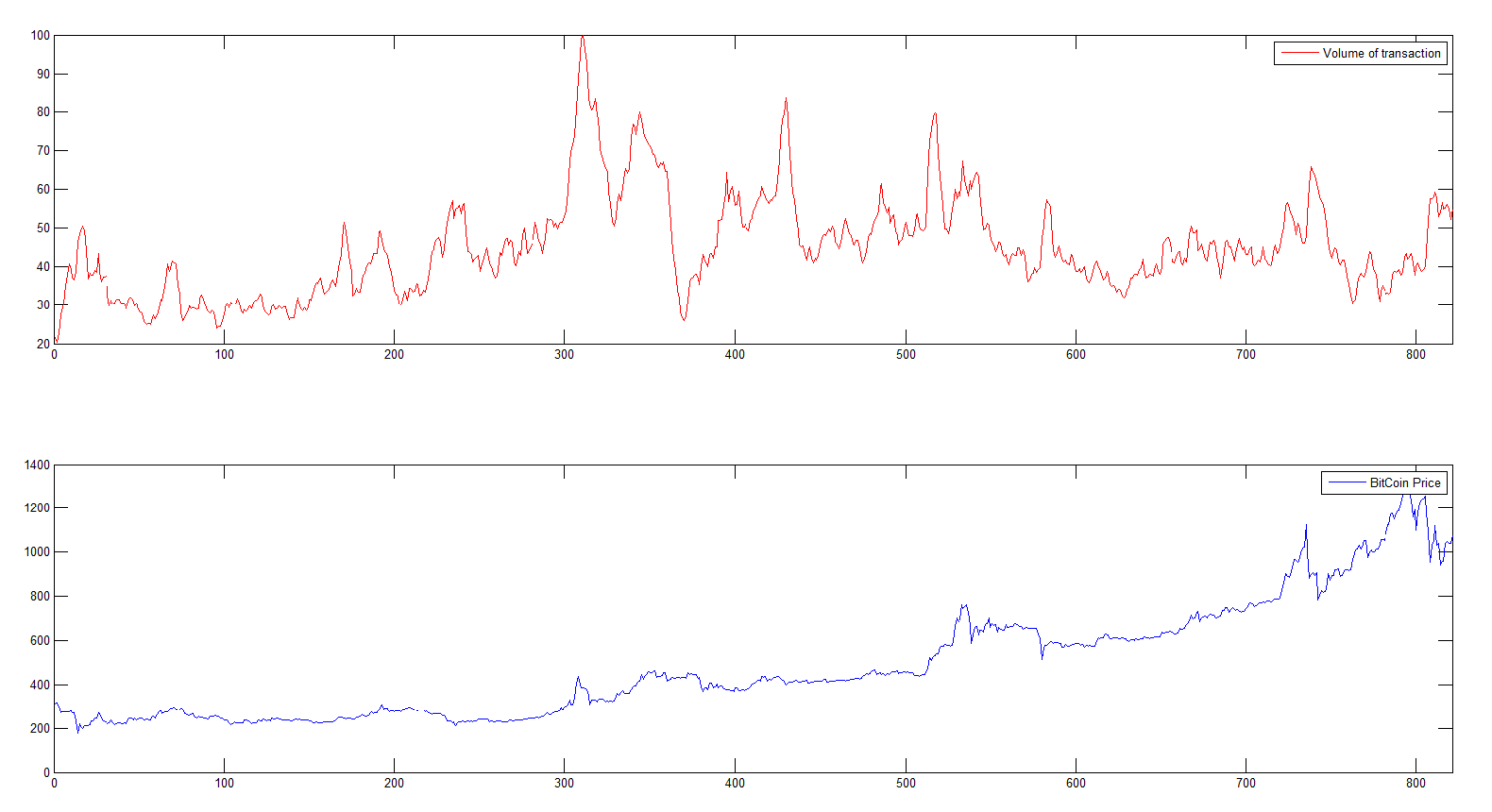

According to the outcomes in Table 8 we consider the daily time series of the volume of transactions and the weekly time series of the Google searches from 01/01/2015 to 31/03/2017 as suitable proxies for process . We fit the model in (2.1) and (2.2) to the BitCoin price and the volume of transaction as well as to the BitCoin prices and number of Google searches by applying the Profile-Quasi-Likelihood (PML) method as describes in Section 5. Google-trends provides a scaled time series for the number of searches so the the maximum value is ; in order to compare outcomes we do the same for the time series. In Figures 5 and 6 we plot the time series of BitCoin price with Google searches (weekly) and the time series of BitCoin price with volume of transactions (daily), respectively.

In what follows we assume that =1 week is the observation step for BitCoin log-returns.

5.2.1. Sentiment maesured by Volume

Given daily observations of the volume of transactions we are able to compute the cumulative weekly sentiment ; for is simply the mean volume during the preceding week i.e.

| (5.1) |

The generalization to is straightforward as soon as we assume for some positive integer ; in which case would be the mean volume of the 7 days preceding time .

By applying the profile quasi maximum likelihood we obtain days and the following estimates of other the parameters:

| Variable | Fitted value | Std. error | t-value | P() |

|---|---|---|---|---|

| 1.0404 | 0.7373 | 1.4110 | 0.1610 | |

| 1.1092 | 0.0725 | 15.2924 | 0.0000 | |

| 0.0153 | 0.0083 | 1.8434 | 0.0679 | |

| 0.0830 | 0.0054 | 15.2403 | 0.0000 |

In order to asses parameters significance the -stat is computed, for each parameter, under the null hypothesis that its value is zero; Table 9 shows that is not statistically significant and that is weakly significant. Finally we evaluate the confidence region for using the (3.18) and days. We find that days belong to the confidence region. Estimates of other parameters are indeed very similar in any of such cases and analogous comments apply.

5.2.2. Sentiment measured by Google Searches

Assume now that Google searches are representative of sentiment about BitCoin. Since we have weekly data we should aggregate both Google searches and BitCoin returns to a coarser observation step; however this would reduce the time series length dramatically and corresponding estimates might be unreliable. Hence we assume that the available observations correspond to the cumulative sentiment time series and we assume it exist a non-negative integer such that i.e. in this case is on a weekly scale and not on a daily scale like in the previous case.

By applying the profile quasi maximum likelihood we obtain week and the following estimates of other parameters:

| Variable | Fitted value | Std. error | t-value | P() |

|---|---|---|---|---|

| 0.9573 | 0.7315 | 1.3087 | 0.1935 | |

| 1.0818 | 0.0714 | 15.1611 | 0.0000 | |

| 0.0181 | 0.0092 | 1.9534 | 0.0535 | |

| 0.0867 | 0.0057 | 15.1774 | 0.0000 |

6. Model performance on market option prices

Recently some online platforms have appeared where it is possible to trade on plain vanilla options on the BitCoin. A relevant platform where bid-ask quotes are publicly available is www.deribit.com; we will consider option prices on this website as "market prices".

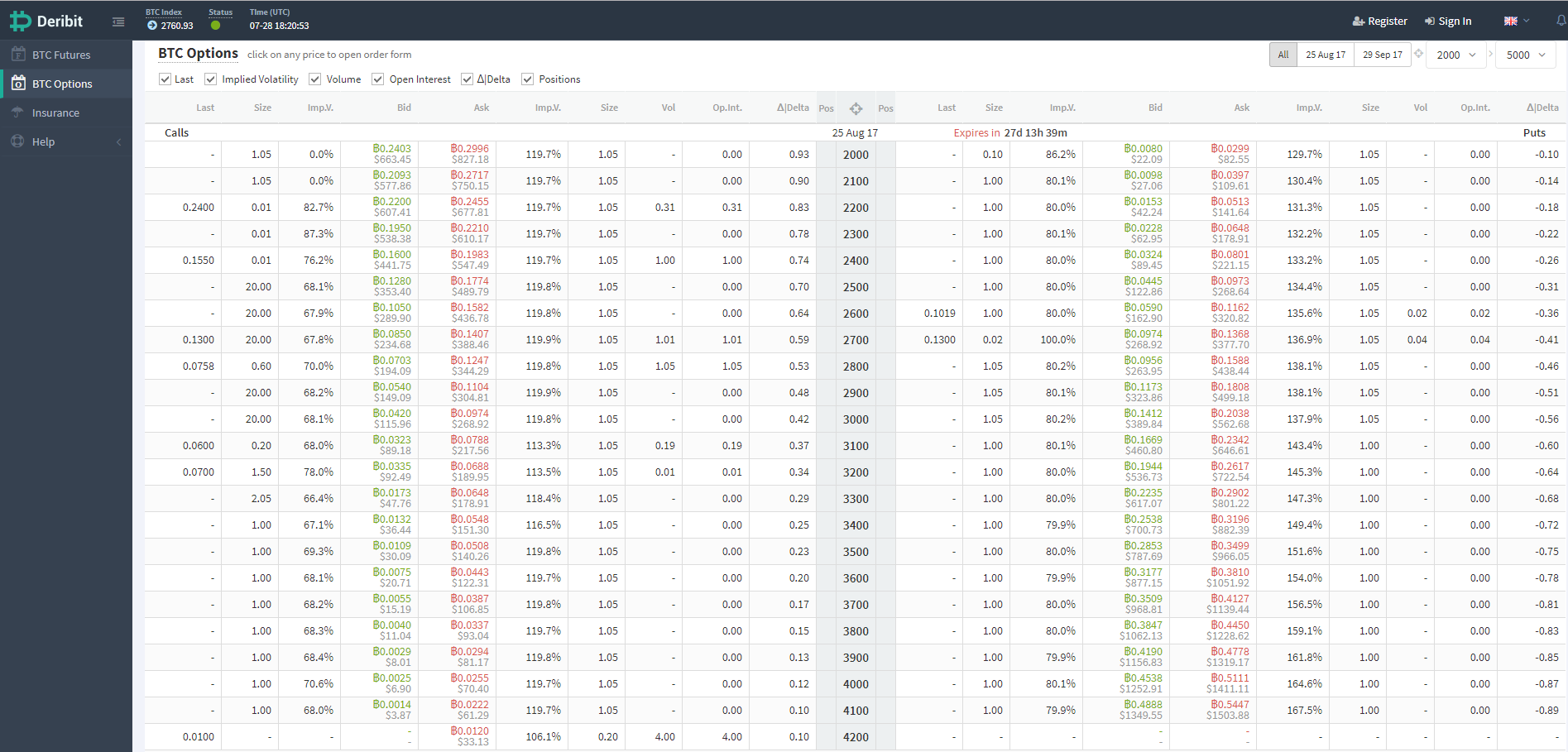

In Figure 7 the screenshot of the website on July 28, 2017; we will consider the mid-value of the Bid-Ask range as a benchmark for assessing model performance discarding options for which there was no transactions. Concerning the price of the underlying BitCoin, it was set as the price of the BitCoin index available from blockchain.info at the same time as the option data download, which also appears in the north-west corner of the screenshot. Every day two different expiration dates are available corresponding to a one month and two months maturity at issue. We are aware of possible synchronicity problems but as a first evaluation of the suggested pricing formula we intentionally neglect this friction. Model prices are then compared with corresponding market prices by computing the Root Mean Squared Error of the model across all the considered sample of options and of suitably chosen sub-samples. The same is done when prices are computed with the benchmark no-sentiment model chosen as Black and Scholes model. Of course the latter is estimated on the same time-series as those considered in Subsection 5.2. Only the volatility estimation matters since we set for both models.

In Tables 11-12 we report market data for July 28, 2017 as well as model option prices in the suggested model and for the Black and Scholes benchmark. On the chosen day available maturities were complete i.e. August 25 and September 29.

| K | Bid | Ask | Model (Vol.) | Model (Google) | BS |

|---|---|---|---|---|---|

| 2200 | 0.2200 | 0.2455 | 0.2125 | 0.2196 | 0.2110 |

| 2300 | 0.1956 | 0.2210 | 0.1820 | 0.1909 | 0.1799 |

| 2400 | 0.1600 | 0.1983 | 0.1538 | 0.1645 | 0.1510 |

| 2500 | 0.1280 | 0.1774 | 0.1281 | 0.1404 | 0.1248 |

| 2600 | 0.1050 | 0.1582 | 0.1052 | 0.1187 | 0.1015 |

| 2700 | 0.0850 | 0.1407 | 0.0867 | 0.0995 | 0.0812 |

| 2800 | 0.0703 | 0.1247 | 0.0696 | 0.0827 | 0.0640 |

| 2900 | 0.0540 | 0.1104 | 0.0482 | 0.0698 | 0.0497 |

| RMSE mean bid/ask | 0.0753 | 0.0395 | 0.0833 | ||

| K | Bid | Ask | Model (Vol.) | Model (Google) | BS |

|---|---|---|---|---|---|

| 2200 | 0.2108 | 0.2764 | 0.2350 | 0.2981 | 0.2297 |

| 2300 | 0.1881 | 0.2547 | 0.2091 | 0.2779 | 0.2029 |

| 2400 | 0.2004 | 0.2343 | 0.1851 | 0.2589 | 0.1781 |

| 2500 | 0.1700 | 0.2154 | 0.1631 | 0.2411 | 0.1555 |

| 2600 | 0.1650 | 0.1950 | 0.1431 | 0.2244 | 0.1349 |

| 2700 | 0.1168 | 0.1710 | 0.1249 | 0.2087 | 0.1164 |

| 2800 | 0.1044 | 0.1630 | 0.1086 | 0.1941 | 0.0999 |

| 2900 | 0.0934 | 0.1490 | 0.0940 | 0.1804 | 0.0853 |

| RMSE mean bid/ask | 0.0723 | 0.1535 | 0.0932 | ||

In Tables 14-16 we sum up the outcomes for the RMSE for All options and for subsamples obtained by considering the same expiration date respectively when sentiment is conveyed by the Volume and by Google searches. The same in Tables 13-15 where the subsample are obtained according to moneyness. Highlighted in the table (in bold) are cases where the plain vanilla Black and Scholes model does better than the model suggested here. Overall our pricing formula does much better than the benchmark in all cases. It is worth noticing that Google Searches tend to overprice long-term options while it is the very best for shorter term options as if this sentiment indicator is driven by enthusiasm giving a sudden impulse to options.

| Options | Num. | RMSE Model | RMSE BS |

|---|---|---|---|

| All | 144 | 0.3089 | 0.4879 |

| Very Shorts | 16 | 0.0898 | 0.0817 |

| 1 Months | 32 | 0.1132 | 0.1448 |

| 2 Months | 32 | 0.1306 | 0.1751 |

| ITM | 54 | 0.1536 | 0.2617 |

| ATM | 36 | 0.1687 | 0.2625 |

| OTM | 54 | 0.2082 | 0.3173 |

| Near | Next | All Day | ||||

|---|---|---|---|---|---|---|

| Date | RMSE Model | RMSE BS | RMSE Model | RMSE BS | RMSE Model | RMSE BS |

| 20/07/2017 | 0.0712 | 0.0648 | 0.0627 | 0.1768 | 0.0949 | 0.1883 |

| 21/07/2017 | 0.0547 | 0.0499 | 0.0172 | 0.1428 | 0.0574 | 0.1512 |

| 22/07/2017 | - | - | 0.0180 | 0.1394 | 0.0180 | 0.1394 |

| 23/07/2017 | - | - | 0.0556 | 0.1475 | 0.0556 | 0.1475 |

| 24/07/2017 | - | - | 0.0773 | 0.1420 | 0.0773 | 0.1420 |

| 25/07/2017 | - | - | 0.1056 | 0.1445 | 0.1056 | 0.1445 |

| 26/07/2017 | - | - | 0.1252 | 0.1519 | 0.1252 | 0.1519 |

| 27/07/2017 | - | - | 0.1306 | 0.1508 | 0.1306 | 0.1508 |

| 28/07/2017 | 0.0753 | 0.0833 | 0.0723 | 0.0932 | 0.1044 | 0.1250 |

| 29/07/2017 | 0.0562 | 0.0717 | 0.0493 | 0.0919 | 0.0748 | 0.1165 |

| 30/07/2017 | 0.0531 | 0.0710 | 0.0705 | 0.0850 | 0.0883 | 0.1107 |

| 31/07/2017 | 0.0343 | 0.0621 | 0.0664 | 0.0795 | 0.0748 | 0.1009 |

| Options | Num. | RMSE Model | RMSE BS |

|---|---|---|---|

| All | 136 | 0.3380 | 0.4854 |

| Very Shorts | 8 | 0.0367 | 0.0648 |

| 1 Months | 32 | 0.0621 | 0.1448 |

| 2 Months | 32 | 0.2408 | 0.1751 |

| ITM | 51 | 0.1912 | 0.2617 |

| ATM | 34 | 0.1613 | 0.2612 |

| OTM | 51 | 0.2273 | 0.3149 |

| Near | Next | All Day | ||||

|---|---|---|---|---|---|---|

| Date | RMSE Model | RMSE BS | RMSE Model | RMSE BS | RMSE Model | RMSE BS |

| 20/07/2017 | 0.0367 | 0.0648 | 0.0578 | 0.1768 | 0.0684 | 0.1883 |

| 21/07/2017 | - | - | 0.0158 | 0.1428 | 0.0158 | 0.1428 |

| 22/07/2017 | - | - | 0.0253 | 0.1394 | 0.0253 | 0.1394 |

| 23/07/2017 | - | - | 0.0891 | 0.1475 | 0.0891 | 0.1475 |

| 24/07/2017 | - | - | 0.0935 | 0.1420 | 0.0935 | 0.1420 |

| 25/07/2017 | - | - | 0.0961 | 0.1445 | 0.0961 | 0.1445 |

| 26/07/2017 | - | - | 0.1018 | 0.1519 | 0.1018 | 0.1519 |

| 27/07/2017 | - | - | 0.1028 | 0.1508 | 0.1028 | 0.1508 |

| 28/07/2017 | 0.0395 | 0.0833 | 0.1535 | 0.0932 | 0.1585 | 0.1250 |

| 29/07/2017 | 0.0275 | 0.0717 | 0.1601 | 0.0919 | 0.1625 | 0.1165 |

| 30/07/2017 | 0.0308 | 0.0710 | 0.0649 | 0.0850 | 0.0718 | 0.1107 |

| 31/07/2017 | 0.0243 | 0.0621 | 0.0677 | 0.0795 | 0.0720 | 0.1009 |

7. Concluding remarks

In this paper we borrow the idea, suggested in recent literature, that BitCoin prices are driven by sentiment on the BitCoin system and underlying technology. Main references in this area are Kristoufek [10, 9], Kim et al. [8], Bukovina and Martiček [2]. In order to account for such behavior we develop a model in continuous time which describes the dynamics of two factors, one representing the sentiment index on the BitCoin system and the other representing the BitCoin price itself, which is directly affected by the first factor; we also take into account a delay between the sentiment index and its delivered effect on the BitCoin price. We investigate statistical properties of the proposed model and we show its arbitrage-free property. Under our model assumption we derived a closed form approximation for the joint density of the discretely observed process and we proposed a statistical estimation for that model. By applying the classical risk-neutral evaluation we are able to derive a quasi-closed formula for European style derivatives on the BitCoin with special attention of Plain Vanilla and Binary options for which a market already exists (e.g. https://deribit.com, https://coinut.com ). Of course sentiment about BitCoin or, more generally, on cryptocurrencies or IT finance is not directly observed but several variables may be considered as indicators. Here, we analyzed the volume and more unconventional sentiment indicators such as the number of Google searches and the number of Wikipedia requests about the topic (as suggested Kristoufek [9], Kim et al. [8]). First of all, we investigated whether these proxies were consistent with the suggested model and we proved that both the volume of transactions and the number of Google searches give a good fit of the dynamics described in the model. Finally we fit the model using real data of BitCoin price with Volume of transactions and Google searches respectively and we provided the estimation results. Several open problems are left for future research. As a first issue would like to address a multivariate extension of the model in order to take into consideration the special feature of BitCoin being traded in different exchanges and related stylized facts and to investigate whether there are arbitrage opportunities between different BitCoin exchanges. Besides we would like to investigate whether the model is suitable to describe bubble effects which have been also evidenced for the BitCoin price dynamics.

Acknowledgments

The first and the second named authors are grateful to Banca d’Italia and Fondazione Cassa di Risparmio di Perugia for the financial support.

References

- Black and Scholes [1973] Fischer Black and Myron Scholes. The pricing of options and corporate liabilities. The Journal of Political Economy, pages 637–654, 1973.

- Bukovina and Martiček [2016] Jaroslav Bukovina and Matúš Martiček. Sentiment and bitcoin volatility. Technical report, Mendel University in Brno, Faculty of Business and Economics, 2016.

- Davison [2003] Anthony Christopher Davison. Statistical models, volume 11. Cambridge University Press, 2003.

- Föllmer and Schweizer [1991] Hans Föllmer and Martin Schweizer. Hedging of contingent claims under incomplete information. In M.H.A Davis and R.J.Elliot, editors, Applied Stochastic Analysis, volume 5, pages 389–414. New York, Gordon and Breach, 1991.

- Föllmer and Schweizer [2010] Hans Föllmer and Martin Schweizer. Minimal martingale measure. In Encyclopedia of Quantitative Finance. Wiley Online Library, 2010.

- Gourieroux et al. [1984] Christian Gourieroux, Alain Monfort, and Alain Trognon. Pseudo maximum likelihood methods: Theory. Econometrica, 52(3):681–700, 1984.

- Hull and White [1987] John Hull and Alan White. The pricing of options on assets with stochastic volatilities. The Journal of Finance, 42(2):281–300, 1987.

- Kim et al. [2015] Young Bin Kim, Sang Hyeok Lee, Shin Jin Kang, Myung Jin Choi, Jung Lee, and Chang Hun Kim. Virtual world currency value fluctuation prediction system based on user sentiment analysis. PLoS ONE, 10(8):e0132944, 2015.

- Kristoufek [2013] Ladislav Kristoufek. BitCoin meets Google Trends and Wikipedia: Quantifying the relationship between phenomena of the Internet era. Scientific Reports, 3, 2013.

- Kristoufek [2015] Ladislav Kristoufek. What are the main drivers of the bitcoin price? Evidence from wavelet coherence analysis. PLoS ONE, 10(4):e0123923, 2015.

- Levy [1992] Edmond Levy. Pricing European average rate currency options. Journal of International Money and Finance, 11(5):474–491, 1992.

- Mao and Sabanis [2013] Xuerong Mao and Sotirios Sabanis. Delay geometric Brownian motion in financial option valuation. Stochastics An International Journal of Probability and Stochastic Processes, 85(2):295–320, 2013.

- Massey Jr [1951] Frank Jones Massey Jr. The Kolmogorov-Smirnov test for goodness of fit. Journal of the American statistical Association, 46(253):68–78, 1951.

- Milevsky and Posner [1998] Moshe Arye Milevsky and Steven E. Posner. Asian options, the sum of lognormals, and the reciprocal gamma distribution. Journal of Financial and Quantitative Analysis, 33(03):409–422, 1998.

- Pascucci [2011] Andrea Pascucci. PDE and Martingale Methods in Option Pricing. Springer Science & Business Media, 2011.

- Pawitan [2001] Yudi Pawitan. In all likelihood: statistical modelling and inference using likelihood. Oxford University Press, 2001.

- Protter [2005] Philip E. Protter. Stochastic differential equations. In Stochastic Integration and Differential Equations, pages 249–361. Springer, 2005.

- Tsay [2005] Ruey S Tsay. Analysis of financial time series, volume 543. John Wiley & Sons, 2005.

- White [1982] Halbert White. Maximum likelihood estimation of misspecified models. Econometrica, pages 1–25, 1982.

- Yermack [2013] David Yermack. Is bitcoin a real currency? An economic appraisal. Technical report, National Bureau of Economic Research, 2013.

Appendix A Levy approximation

In Levy [11] the author proves that the distribution of the mean integrated Brownian motion can be approximated with a log-normal distribution, at least for suitable values of the model parameters ; the parameters of the approximating log-normal distribution are obtained by applying a moment matching technique. Set

| (A.1) |

Of course, the distribution of can also be approximated by a log-normal for . By applying the moment matching technique the parameters of the corresponding log-Normal distribution for are given by

The approximate distribution density function of is thus given by

where denotes the probability distribution function of a log-normal distribution with parameters and , defined as

In the paper the above approximation is applied twice with completely different purposes. In Section 4 it is applied to derive an approximate distribution for the integrated sentiment process starting at i.e. to . Note that hence the derivations of its distribution is trivial once that of is known.

In Section 5, once is assigned, the Levy approximation is applied to derive the distribution of and of given where and, for , .

Appendix B Technical proofs

Proof of Lemma 2.2.

In order to prove the Lemma let us first compute the mean and the variance of given in (A.1) for each .

Fix . Since for each , by applying Fubini’s theorem we get

where, for each , we have

since is a geometric Brownian motion with . Hence

As for the variance of , we have

| (B.1) |

with

| (B.2) | ||||

| (B.3) |

where the last equality again holds thanks to Fubini’s theorem. Moreover, by the independence property of the increments of Brownian motion, for , we get

Further,

Hence

| (B.4) |

and by plugging (B.4) into (B.3), we have

Finally, gathering the results we get

Note that , with , and , with , are fully deterministic and the computation is trivial.

To prove points (i)-(iii), it suffices to observe that

and the computation easily follows once those of are known for .

To prove point (ii), it is worth noticing that given

| (B.5) | ||||

| (B.6) |

where .

To obtain the desired result it suffices to note that, for ,

and apply (B.6). The computation of the mean and variance of the above difference is straightforward given the independence of Brownian increments. ∎

Proof of Lemma 2.4.

Firstly, we prove that formula (2.15) defines a probability measure equivalent to on . This means we need to show that is an -martingale, that is, . Since the -progressively measurable process can be suitably chosen, to prove this relation we can assume , without loss of generality. Set

| (B.7) |

We observe that since , for each , in (2.2), by Theorem 2.3, point (i), we have that , -a.s. for all , so that the process given in (B.7) is well-defined, as well as the random variable . Clearly, is an -progressively measurable process. Moreover, since the trajectories of the process are continuous, then is almost surely bounded on and this implies that -a.s.; on the other hand, the condition , for every , implies that almost every path of is bounded on the compact interval . Set , for . Then, , for every , is -measurable. Since is independent of , for every , the stochastic integral conditioned on has a normal distribution with mean zero and variance . Consequently, the formula for the moment generating function of a normal distribution implies

or equivalently

| (B.8) |

Taking the expectation of both sides of (B.8) immediately yields . Now, set , for each . It remains to verify that the discounted BitCoin price process is an -martingale. By Girsanov’s theorem, under the change of measure from to , we have two independent -Brownian motions and defined respectively by

Under the martingale measure , the discounted BitCoin price process satisfies the following dynamics

which implies that is an -local martingale. Finally, proceeding as above it is easy to check that is a true -martingale.

∎

Proof of Lemma 3.1.

By applying Levy [11] we have (see Appendix A) that the distribution of can be approximated by a log-normal with parameters

| (B.9) |

By applying the outcomes of Lemma 2.2, we have

| (B.10) | ||||

| (B.11) | ||||

| (B.12) |

Hence

| (B.13) | ||||

| (B.14) |

By applying simple computation we get the outcomes for part (i). Moreover,

| (B.15) | ||||

| (B.16) | ||||

| (B.17) | ||||

| (B.18) |

Then

| (B.19) | ||||

| (B.20) | ||||

| (B.21) | ||||

| (B.22) |

Conditioning to

| (B.23) | ||||

| (B.24) |

which gives part (ii).

∎