Line —– \newarrowDashdashdash \newarrowCorresponds <—> \newarrowMapsto |—> \newarrowInto C—> \newarrowEmbed >—> \newarrowOnto —->> \newarrowTeXonto —–>> \newarrowNto –+-> \newarrowDashto dashdash>

Lazy stochastic principal component analysis

Abstract

Stochastic principal component analysis (SPCA) has become a popular dimensionality reduction strategy for large, high-dimensional datasets. We derive a simplified algorithm, called Lazy SPCA, which has reduced computational complexity and is better suited for large-scale distributed computation. We prove that SPCA and Lazy SPCA find the same approximations to the principal subspace, and that the pairwise distances between samples in the lower-dimensional space is invariant to whether SPCA is executed lazily or not. Empirical studies find downstream predictive performance to be identical for both methods, and superior to random projections, across a range of predictive models (linear regression, logistic lasso, and random forests). In our largest experiment with 4.6 million samples, Lazy SPCA reduced 43.7 hours of computation to 9.9 hours. Overall, Lazy SPCA relies exclusively on matrix multiplications, besides an operation on a small square matrix whose size depends only on the target dimensionality.

I Stochastic Dimensionality Reduction

Stochastic dimensionality reduction (DR) exploits randomization to scale up traditional techniques to large, high-dimensional datasets. Stochastic DR may be applied as a preprocessing step before feeding the data into a computationally expensive classifier, e.g. a neural network [1], or it may be directly embedded within algorithms to improve scalability [2].

I-A Random Projection (RP)

Given a dataset of samples in dimensions, we perform a random projection (RP) to dimensions via

| (1) |

where is a matrix of random numbers and is a scalar for norm preservation that depends upon the random projection method used.111Where possible, vectors in are denoted by and vectors in are denoted by .,222Note that a random projection is technically not actually a projection (an endomorphism that satisfies ). Random projection is a computationally cheap technique that approximately preserves pairwise distances between samples with high probability (with error depending on and ).

There are many methods for constructing the random matrix . A theoretically convenient Gaussian RP takes each as an i.i.d draw from a normal distribution, for example . Very sparse random projections [3] save storage and computation by taking each as an i.i.d draw from with probabilities for appropriate choice of . Other variants with similar concentration of measure properties include the subsampled randomized Hadamard transformation (also known as a fast Johnson-Lindentrauss transform) [4] and feature hashing [5].

I-B Stochastic Principal Component Analysis (SPCA)

| Approximation to dataset , with general form ( is a pseudo-inverse for ) | |

| Approximation to , formed via random projection | |

| Matrix implementation of with and without orthonormal basis for | |

| Matrix of approximate right singular vectors formed by SPCA and Lazy SPCA, respectively | |

| Principal subspace (spanned by dominant principal component directions) | |

| Approximation to , given by span of columns of either or | |

| Dimensionality reduction maps for SPCA and Lazy SPCA, respectively | |

| th element of the standard basis, identity on set S, taking the span, preimage of under |

Principal component analysis (PCA) is a classical linear dimensionality reduction strategy. Given dataset , one finds a -dimensional subspace (the principal subspace) on which projection of the data has the largest possible variance. Stochastic principal component analysis (SPCA) [6] works similarly, but it uses randomization to find an approximation .333For common symbols and terms, see Table I. SPCA has a greater computational cost than RP, but because PCA satisfies well-known optimality criteria, one might expect to better approximate , thereby producing a “better” dimensionality reduction than RP. As a result, SPCA has become widely used, implemented in popular libraries by MATLAB [7], scikitlearn [8], Apache Mahout [9], Facebook [10], and others.444The same algorithm may be called stochastic/randomized PCA or stochastic/randomized SVD. See the last paragraph in this section.

SPCA begins by solving the approximate (low-rank) matrix decomposition (AMD) problem [11], [12]: Given a matrix , a target rank and a number ,555Typically , where p is a small oversampling parameter. we seek to construct a matrix with orthonormal columns such that

| (2) |

Most commonly, the matrix is found by using the RP in (1) to produce a matrix whose columns lie within (and in fact approximate well [11]), and then orthonormalizing , e.g. via QR decomposition. The resulting matrix approximation is provably good; for example, Theorem 1.1 of [11] states that when a Gaussian RP is used in (1), the approximation satisfies

| (3) |

where is the st largest singular value of .

Thus, the approximation is computationally useful because, on one hand, it lies within a small polynomial factor of the minimum possible error for a rank- approximation, and on the other hand, it can be expressed as the product of two factors, and , which are substantially smaller than . Then, factorizing yields an approximate factorization of . In particular, we can take the SVD of the small factor to obtain:

| (4) |

SPCA implementations [6], [8] use the columns of in (4) as approximate principal component directions for . Technically, the right singular vectors of are its principal components only if is centered. However, centering may pose problems for large, sparse datasets , and the SPCA procedure in (4) will project samples into the same subspace of regardless of whether X is centered. Moreover, right singular vectors still approximate principal components by adhering to the theory of “uncentered” principal components [13]. Thus, in the context of this paper, we will refer to approximate right singular vectors as approximate principal components.

I-C Lazy stochastic principal component analysis (Lazy SPCA)

In Proposition 1, we will show that the quality of the low-rank approximation depends only upon the subspace formed by the collection . Thus, we may generalize the construction of so that there is no need for orthonormalizing vectors when approximating . That is, we generalize in (2) to what we call a lazily approximated (low-rank) matrix decomposition (Lazy AMD).

| (5) |

where the columns of are not necessarily orthonormal, is a pseudo-inverse for , and and will be given in (7) and (11).

Lazy SPCA cheaply obtains a good dimensionality reduction by exploiting Lazy AMD followed by a “premature truncation” trick (see Section II-C). Despite the simplification, LSPCA projects samples to the same subspace of (Proposition 2) and outputs identical pairwise distances between samples in the new space (Proposition 3), yielding equivalent performance in downstream predictions (Experiments 1 and 2). This is true even though Lazy SPCA has reduced computational complexity (Proposition 4), substantially reducing run time for many large-scale applications (Experiment 1). Moreover, the algorithm can now be expressed entirely in terms of easily distributed matrix multiplications, with the exception of a single eigendecomposition of a relatively small matrix.

II THEORY

II-A Overview

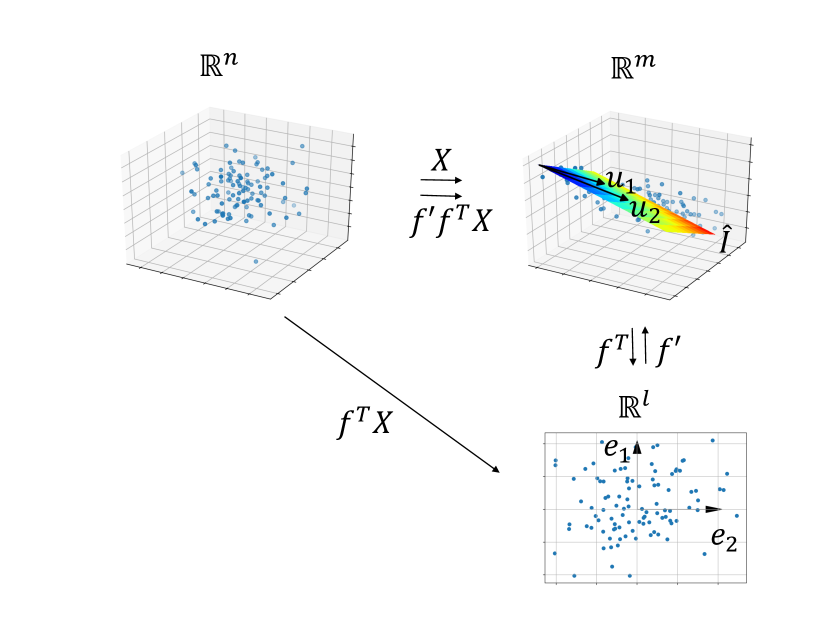

The overview of our argument is described here and reflected in Figure 1.

-

1.

We view dataset as a linear map from to with image . Using a random projection, we can construct a good approximation by taking to be the span of the columns of , where is a random projection matrix [11], [14]. We use to construct a low-rank approximation , which maps to subspace instead of to . The approximation has error bounds given in (3).

-

2.

The approximation error depends only on the subspace , and not on the basis for that subspace. To see this, we will express using constructions666Here, is a pseudo-inverse for ; the notation generalizes the special case where where has orthonormal columns. in (6) and (8) and show:

- (a)

-

(b)

So back in , where samples naturally live, points which get mapped to by will be unchanged by the approximation, and points which get mapped to will get mapped to 0 [see (16), (LABEL:null_piece_in_Rn)].

Thus, the quality of the low-rank approximation to does not depend on representing with an orthonormal basis (see Proposition 1), even though this procedure is commonly done (e.g., [6], [11], [8], [9]).

-

3.

The approximate principal subspace for is the span of the right singular vectors of , and this can be obtained by simply taking the right singular vectors of . (See Proposition 2).

II-B Lazily approximated low-rank matrix decompositions (Lazy AMD)

II-B1 Construction of ,

Consider the Lazy AMD introduced in (5). We construct and via subspaces that approximate . Suppose we choose a linearly independent but not necessarily orthonormal collection such that is a subspace of . Define

| (6) |

So has matrix form

| (7) |

Lemma 1.

The map above maps bijectively to .

Proof.

Since , it follows that . So for any there exists such that . Write where and . Then . So maps surjectively onto . It follows that and maps injectively to . ∎

Thus, there exist such that . If we define

| (8) |

then

| (9) | ||||

| (10) |

So is a pseudo-inverse for . Note has matrix form

| (11) |

II-B2 Effect of the approximation to on points in

Using , we have

| (12) | ||||

| (13) |

Thus, we describe the operator in terms of its action on two complementary subspaces

| (14) |

and

| (15) |

Back in the domain of the linear map , the operator can again be described in terms of its action on two complementary subspaces:

| (16) | ||||

This will be used in Proposition 1.

Note that in the case , the restriction of the function in (15) is over a set that contains only the vector, and so we obtain an exact approximation

| (18) |

Otherwise we have an inexact approximation because, via (LABEL:null_piece_in_Rn), we have

| (19) |

II-B3 Theoretical results

Proposition 1 states that AMD and Lazy AMD construct identical approximators .

Proposition 1.

(Lazy AMD) Let be a linearly independent collection such that . Let be an orthonormalization of that collection. Let be the matrix whose column is , be the matrix whose column is , and be the matrix defined as in (11). Then

| (20) |

Thus, we may now generalize Theorem 1.1 of [6] and (3) to a more general class of approximators without incurring additional error.777Corollary 1, unlike the original theorem, assumes that is full rank. In actuality, the entire framework holds even when the collection is linearly dependent, as we show in a future paper. For now, we show that, in any case is full rank with probability 1.

Lemma 2.

Let and be as in Corollary 1. Then is full rank with probability 1.

Proof.

Recall that . Assume the first vectors have been chosen and they are linearly independent. Then the subspace has measure 0 in . So .

∎

Corollary 1.

Let be a real non-trivial matrix and be a Gaussian random projection matrix where . Suppose is full rank and has been constructed as in (11). Then for any ,

| (21) |

where denotes expectation and denotes the singular value of .

II-C Lazy SPCA

II-C1 Procedures

SPCA constructs to approximate where the are orthonormal. Thus the low-rank matrix approximation described in Section II-B is given by . Using this, one obtains an approximate SVD.888We use a tilde to reflect a temporary computational byproduct, and we use superscripts and to refer to factors relevant to SPCA and Lazy SPCA, respectively.

| (22) |

Using Lazy AMD, we construct to approximate without orthonormalizing the . By Proposition 1, we obtain an equally good approximation . From this approximation we can obtain the same approximate SVD as before, but with an alternate pathway:

| (23) |

By the uniqueness of SVD for , the approximate SVDs in the final lines of (22) and (23) are identical. However, as we show in Propositions 2 and 3, we may use , an intermediate product of pathway (23), instead of , to perform dimensional reduction. We call this idea premature truncation. This saves a computation (either a QR in (22) or SVD in (23)) that is expensive and can be cumbersome for distributed computation.999Also note that, for the purposes of dimensionality reduction, we never need to explicitly form the matrix .

II-C2 Projecting samples to

We define the dimensionality reduction maps

| (24) |

where is the the mapping formed by SPCA using in (22) and is the mapping formed by Lazy SPCA using in (23). Here we show that both and project samples into the same subspace of .101010The term “project” is used loosely here. More precisely, since , we can consider these maps as projecting samples onto and then identifying with by using the approximate dominant principal component directions as a basis for .,111111Note, that the two methods will not, in general, find the same basis for .

Proposition 2.

The approximate right singular vectors of given by either the columns of (for SPCA) or (for Lazy SPCA) form an orthonormal basis for in .

II-C3 Pairwise distances after dimensionality reduction

Here we show that, while dimensionality reduction will often shrink pairwise distances between samples, the resulting distances will be invariant to whether SPCA is executed lazily or not.

Let be a matrix whose columns are a collection of orthonormal vectors in and consider the linear map

Lemma 3.

(norm before and after transformation by orthonormal ) Suppose is orthonormal. If then , else .

Proof.

If then . Else write for some and nonzero . Then . ∎

Corollary 2.

(distance before and after transformation by orthonormal ) Suppose is orthonormal. If then , else .

Proof.

This follows from the fact and Lemma 3. ∎

Proposition 3.

Suppose and are the dimensionality reduction maps for SPCA and Lazy SPCA, as described in (24). Then for all ,

II-C4 Computational complexity

Here we show that Lazy SPCA reduces the complexity of SPCA.

Proposition 4.

SPCA has computational complexity . Lazy SPCA is .

III ALGORITHMS

| Data Dataset (for streaming versions, split into horizontal slices, denoted ); target dimensionality ; |

| random projection matrix where . |

| Result Dimension reduction map |

| Straightforward implementations |

| Algorithm 1: SPCA [6] 1. Construct 2. Orthonormalize via 3. Form , as in (22). 4. Decompose† . Algorithm 2: Lazy SPCA 1. Construct . 2. Form , as in (23). 3. Decompose† . |

| Streaming implementations |

| Algorithm 3: Streaming SPCA [15] 1. Initialize ; ; and . 2. for do (a) Construct . (b) Update , as in (22). (c) Update R via . end for 3. Update , as in (22). 4. Decompose† . Algorithm 4: Streaming Lazy SPCA 1. Initialize and . 2. for do (a) Construct . (b) Update , as in (23). end for 3. Decompose† . |

We provide straightforward (i.e., in core) implementations of SPCA and Lazy SPCA in Algorithms 1 and 2. However, stochastic dimensionality reduction is typically performed when exceeds the size of a computer’s core memory.121212Otherwise, if fits into memory, traditional (deterministic) SVD would be easily applied. Thus, we also provide streaming implementations in Algorithms 3 and 4. Overall, Lazy SPCA is both faster and less cumbersome for large datasets (as all operations can be rendered as matrix multiplications, besides finding the eigensolution of a small matrix.)

IV Experiment 1

In Experiment 1, we demonstrate the techniques on a large dataset from the context of automatic malware classification.

IV-A Data and Method

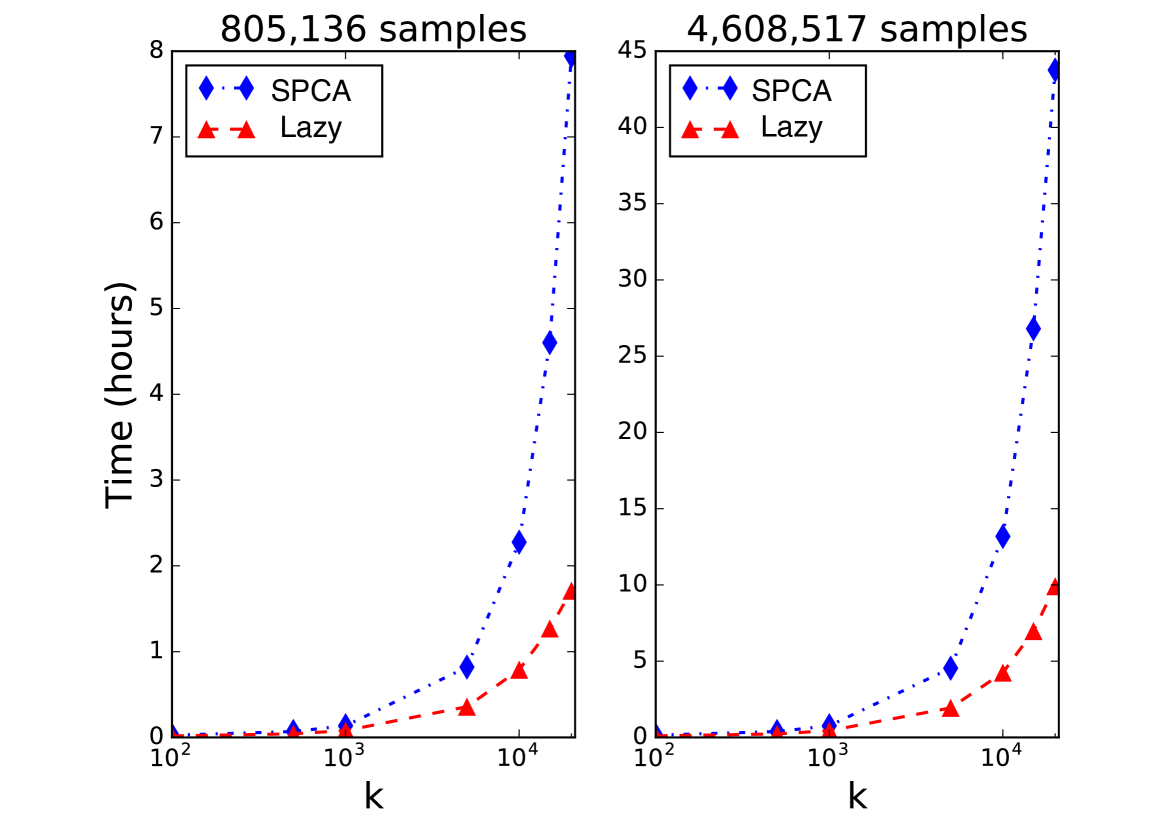

This dataset [15] consists of 4,608,517 portable executable files and determined to be either malicious or clean. Each file is represented as 98,450 features, mostly binary, with mean density 0.0244.

We applied three dimensionality reduction methods to this dataset: RP, SPCA and Lazy SPCA. Across methods, we employed fixed very sparse random projections with density set to , the aggressive value in [3]. The target dimensionality was set to 100, 500, 1000, 5000, 10000 and 20000. For simplicity, we avoid oversampling and set .

The dataset was divided up into horizontal slices that were represented as (Float32, Int64) Sparse CSC matrices. The most expensive steps (dense-by-sparse matrix multiplication and QR decomposition) were implemented using the Intel Math Kernel Library (mkl). All computations were performed in Julia v0.3.8 on a single Amazon EC2 r3.8 instance with 16 physical cores (32 hyperthreaded cores) and 244 GB of RAM.131313Note that although the exact timings depend on implementation, the qualitative properties of the results depend on the computational complexity of the algorithms.

A -penalized logistic regression (or “logistic lasso") classifier was trained on 80% of the samples, randomly selected without replacement.141414The model complexity parameter was fixed at 1 (rather than optimized) to place equal weight on the likelihood term and the penalty term. The classifier was tested on the remaining 20%.

IV-B Results

| Dimensionality Reduction | |||

| Target Dim. () | RP | SPCA | Lazy SPCA |

| 100 | 89.63 | 94.86 | 94.84 |

| 500 | 94.41 | 97.24 | 97.24 |

| 1,000 | 96.40 | 97.98 | 97.98 |

| 5,000 | 98.38 | 98.74 | 98.74 |

| 10,000 | 98.73 | 98.92 | 98.92 |

| 15,000 | 98.84 | 98.99 | 98.99 |

| 20,000 | 98.94 | 99.03 | 99.03 |

In the left table of Figure 2, we see that SPCA and Lazy SPCA yield identical downstream predictive performance. Moreover, both outperform RP for all , although the superiority decreases as increases. In the right plots of Figure 2, we see that Lazy SPCA is faster than SPCA across all . This superiority increases as increases, as expected by Proposition 4. In the largest data analysis, it took 9.9 versus 43.7 hours to obtain an equivalently useful dimensionality reduction.

V Experiment 2

In Experiment 2, we demonstrate the techniques on a smaller yet publicly available dataset, with publicly available code.151515See https://github.com/CylanceSPEAR/lazy-stochastic-principal-component-analysis.

V-A Data and Methods

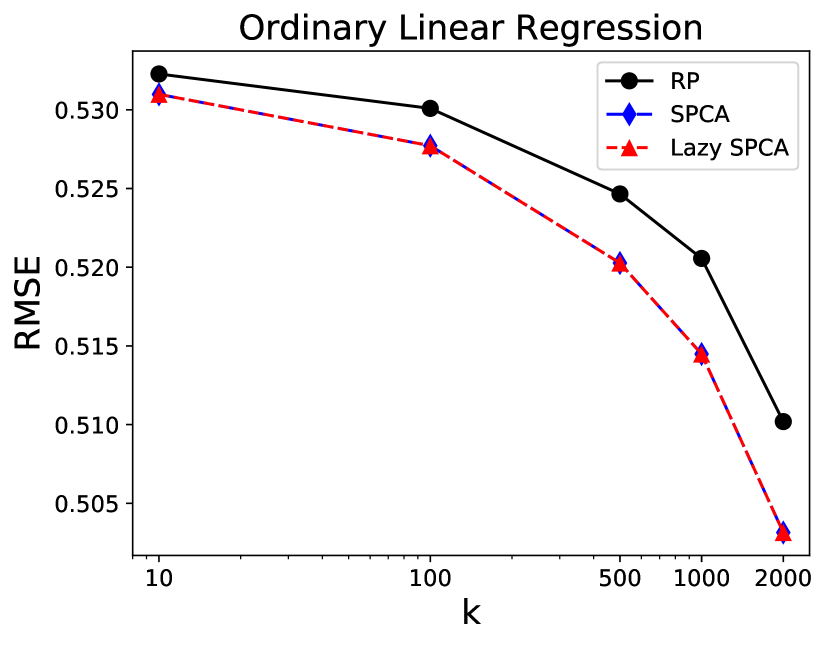

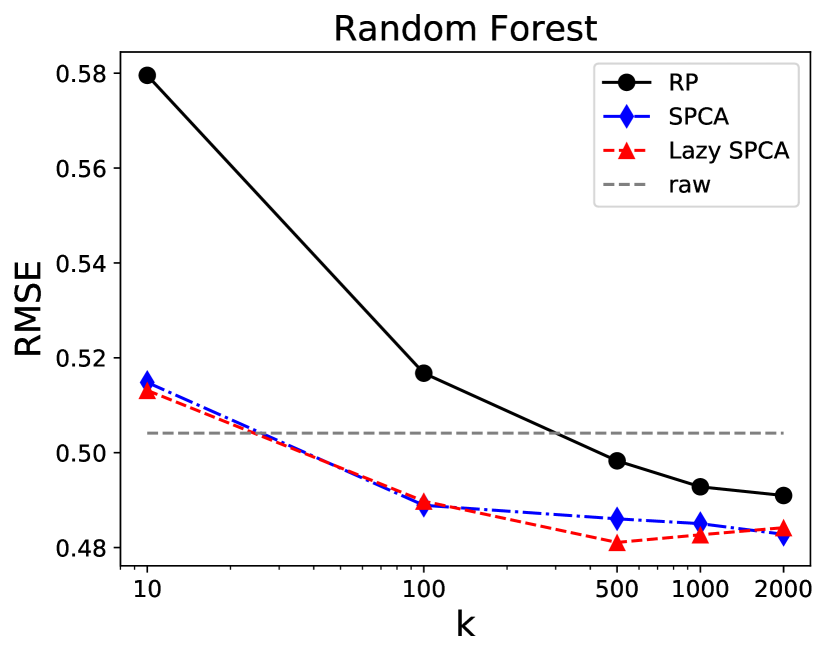

We evaluated our dimensionality reduction methods on the Home Depot Product Search Relevance dataset from the Kaggle competition of the same name. The goal is to predict the ratings of the relevance of a customer search term to a product.161616For example, one rater might consider a search for ”AA battery” to be highly relevant to a pack of size AA batteries (relevance = 3), mildly relevant to a cordless drill battery (relevance = 2.2), and not relevant to a snow shovel (relevance = 1.3). For this study, we generated features by using the co-occurrence TF-IDF of product title and search terms. The resulting dataset of samples (search term-product pairs) and features has a density of . Dimensionality reduction was performed as in Experiment 1, except that the RP matrix was constructed using the conservative density [10]. Distances between approximate principal subspaces were measured by the chordal distance on the Grassmann manifold, , where the columns of form an orthonormal basis for the th subspace.

V-B Results

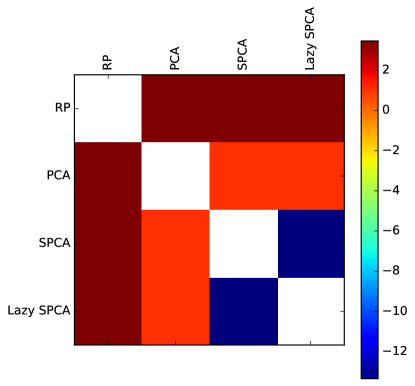

In Figure 3, we see that SPCA and Lazy SPCA result in identical downstream predictive accuracy across a range of target dimensionalities , and that both outperform RP. To help explain this, Figure 4 shows that, as expected by Proposition 2, SPCA and Lazy SPCA project samples onto the same -dimensional approximate principal subspace (which is closer to the true principal subspace than the subspace found by RP).

VI Conclusion

We develop a framework for simplifying stochastic principal component analysis when used as a tool for dimensionality reduction. Compared to SPCA, Lazy SPCA is both faster and better suited for distributed computation. At the same time, it projects samples to the same subspace, yields identical pairwise distances between samples, and results in identical empirical performance in downstream classification.

Acknowledgments

We thank John Hendershott Brock for helpful comments.

References

- [1] Dahl, G. E., Stokes, J. W., Deng, L., & Yu, D. (2013, May). Large-scale malware classification using random projections and neural networks. In Acoustics, Speech and Signal Processing (ICASSP), 2013 IEEE International Conference on (pp. 3422-3426). IEEE.

- [2] Wojnowicz, M., Cruz, B., Zhao, X., Wallace, B., Wolff, M., Luan, J., & Crable, C. (2016). “Influence sketching”: Finding influential samples in large-scale regressions. In Big Data (Big Data), 2016 IEEE International Conference on (pp. 3601-3612). IEEE.

- [3] Li, P., Hastie, T. J., & Church, K. W. (2006, August). Very sparse random projections. In Proceedings of the 12th ACM SIGKDD international conference on Knowledge discovery and data mining (pp. 287-296). ACM.

- [4] Ailon, N., & Chazelle, B. (2009). The fast Johnson-Lindenstrauss transform and approximate nearest neighbors. SIAM Journal on Computing, 39(1), 302-322.

- [5] Weinberger, K., Dasgupta, A., Langford, J., Smola, A., & Attenberg, J. (2009, June). Feature hashing for large scale multitask learning. In Proceedings of the 26th Annual International Conference on Machine Learning (pp. 1113-1120). ACM.

- [6] Halko, N., Martinsson, P. G., Shkolnisky, Y., & Tygert, M. (2011). An algorithm for the principal component analysis of large data sets. SIAM Journal on Scientific computing, 33(5), 2580-2594.

- [7] Liutkus, A. (2014). Randomized SVD. MATLAB Central File Exchange.

- [8] Pedregosa, F. et al. (2011). Scikit-learn: Machine learning in Python. JMLR, 12:2825-2830.

- [9] Lyubimov, D., & Palumbo, A. (2016). Apache Mahout: Beyond MapReduce. CreateSpace Independent Publishing Platform.

- [10] Tulloch, A. (2014). Fast randomized singular value decomposition. http://research.facebook.com/blog/294071574113354/fast-randomized-svd/

- [11] Halko, N., Martinsson, P. G., & Tropp, J. A. (2011). Finding structure with randomness: Probabilistic algorithms for constructing approximate matrix decompositions. SIAM review, 53(2), 217-288.

- [12] Kishore Kumar, N., & Schneider, J. (2016). Literature survey on low-rank approximation of matrices. Linear and Multilinear Algebra, 1-33.

- [13] Jolliffe, I. T., & Cadima, J. (2016). Principal component analysis: a review and recent developments. Phil. Trans. R. Soc. A, 374(2065), 20150202.

- [14] Mahoney, M. W. (2011). Randomized algorithms for matrices and data. Foundations and Trends in Machine Learning, 3(2), 123-224.

- [15] Wojnowicz, M., Zhang, D., Chisholm, G., Zhao, X., & Wolff, M. (2016). Projecting “better than randomly”: How to reduce the dimensionality of very large datasets in a way that outperforms random projections. In Data Science and Advanced Analytics (DSAA), 2016 IEEE International Conference on (pp. 184-193). IEEE.