Market Dynamics. On A Muse Of Cash Flow And Liquidity Deficit.

Abstract

$Id: AMuseOfCashFlowAndLiquidityDeficit.tex,v 1.575 2019/03/28 06:02:45 mal Exp $

A first attempt at obtaining market–directional information from a non–stationary solution of the dynamic equation ‘‘future price tends to the value that maximizes the number of shares traded per unit time’’ Malyshkin and Bakhramov (2015) is presented. We demonstrate that the concept of price impact is poorly applicable to market dynamics. Instead, we consider the execution flow operator with the ‘‘impact from the future’’ term providing information about not–yet–executed trades. The ‘‘impact from the future" on can be directly estimated from the already–executed trades, the directional information on price is then obtained from the experimentally observed fact that the and operators have the same eigenfunctions (the exact result in the dynamic impact approximation ). The condition for ‘‘no information about the future’’ is found and directional prediction quality is discussed. This work makes a substantial contribution toward solving the ultimate market dynamics problem: find evidence of existence (or proof of non–existence) of an automated trading machine which consistently makes positive P&L on a free market as an autonomous agent (aka the existence of the market dynamics equation). The software with a reference implementation of the theory is provided.

I Introduction

Market Dynamics is the central concept of modern economic study. An ultimate form of the study to be an evidence of existence (or a proof of non–existence) of an automated trading machine, consistently making positive P&L (with a given value of risk) trading on a free market as an autonomous agent. In our previous studyMalyshkin (2016); Malyshkin and Bakhramov (2016) we have shown experimentally that supply and demand match each other down to milliseconds time scale, thus their disbalance cannot be a source of market dynamics. Moreover, supply and demand cannot be measured or estimated from the data even after transaction executionMalyshkin (2016). In the modern world all available data is typically represented in a form of recorded transactions, where money, financial instruments, goods, etc. change hands. In each such transaction there are two matched parties (e.g. ‘‘A’’ sold goods to ‘‘B’’ and received dollars for that) what means that in recorded data supply and demand are matched. The disbalance of supply/demand cannot (even in principle!) be measured from a sequence of transactions, as any transaction assume the parties to match. An example of information source, that is not a sequence of transactions, is the Limit Order Book. However, using Limit Order Book as a source of information about Supply and Demand is fruitlessMalyshkin and Bakhramov (2016) since at least 2008–2010 and exchange trading is now little different from dark pool trading. (We tried to consider the Limit Order Book both: as not a sequence of transaction, and as a sequence of add/{cancelexecute} transactions, but without much success; most typical limit order book pattern is: added order spend almost no time in the order book, it either get almost immediately executed or canceled. The ratio observed is that more than 90% of orders being at best price level at some time end up being canceledHautsch and Huang (2011); Malyshkin and Bakhramov (2015). This is due to exchange fee structure, because add/cancel order ‘‘round trip’’ cost (almost) no money and carry little risk for market participants.) This make us to conclude that the disbalance of supply and demand is not a practically applicable concept, because it cannot be measured from recorded transactions.

For practical applications we need a concept that can be estimated from a sequence of transactions. In Malyshkin (2016); Malyshkin and Bakhramov (2015) a concept of execution flow ( a number of shares traded in unit time, a number of dollars paid in unit time, etc.) was introduced and practical approach to its calculation (based on Radon–Nikodym derivatives and their generalization) was developed.

An application of this approach in quasistationary case was demonstrated in Malyshkin (2016), where we have shown that asset price is much more sensitive to execution rate , rather than to trading volume , and dynamic impact (sensitivity to ) was introduced as a practical alternative to regular impactWikipedia (2016a) (sensitivity to )111 Also see later developedMalyshkin (2019) concept of constrained optimization subject to the constraint , considered for a number of operators . This allows us, within the framework of a single formalism of constrained optimization, take into account the driving force of the market , and the reaction, via the operator , of the market participants on it. . In this paper we make one more step forward, demonstrating an application of this approach in a non–stationary case. First, we show that price impact, the central subject of many studies, is poorly applicable to market dynamics. A practical alternative to it is an impact from the future on , that can be estimated from past sample. Then we are trying to obtain directional information on price from a knowledge of future , with the goal to obtain trading strategy with a positive P&L. There is a fundamental philosophical questionBoiko and Malyshkin (27 Feb. 2009) about positive P&L provided by an automated trading machine: Assume one created a ‘‘Real Time Machine’’, but looking only very few moments ahead in the future. How to prove that a given ‘‘Time Machine’’ works? Attach it to an exchange and show the P&L! In this sense any dynamic equation (Newton, Maxwell, Schrödinger) can be considered as some kind of ‘‘Time Machine’’. Moreover, any intelligence can be considered as a ‘‘future prediction system’’ Hawkins and Blakeslee (2007), thus, when applied to the market, the P&L can be considered as an ‘‘intelligence criteria’’ of an automated trading machine. There is a very deep difference between an intelligent agent and statistical approach. For an intelligent agent a single observation is enough to make a prediction. For any statistical approach a large number of observations is required to make any kind of inference. In Malyshkin and Bakhramov (2016) we emphasized the inapplicability of any statistical approach to exchange trading and the importance of the dynamical approach, a practical alternative to a statistical one.

The dynamic equation we introducedMalyshkin and Bakhramov (2015) ‘‘future price tends to the value that maximizes the number of shares traded per unit time’’ in this direct form requires to know ‘‘future’’ prices and flows, and can be easily solved only in quasistationary caseMalyshkin (2016). In a non–stationary case the best result of our previous studyMalyshkin and Bakhramov (2015) was ‘‘maximizing the number of shares traded per unit time on past observations sample’’, but with a limited success. The concept of market dynamics in its ultimate form requires to determine future market movement from past observations sample. In this paper a substantial progress is made toward this goal. In Section VII an estimation (45) of the impact from the future on is made, allowing (from experimentally observedMalyshkin (2016) fact that and operators to have the same eigenfunctions, at least for the states with high ) to obtain price directional answer. This dynamic equation solution is equivalent to some trending model, but have an automatic selection of the relevant time scale, a critically important feature of any automated trading systemMalyshkin and Bakhramov (2015).

In Ref. Malyshkin and Bakhramov (2015), as a first application of the dynamic equation, the concept of liquidity deficit trading was introduced: open a position on low ( is defined in Eq. (41)), close already opened position on high , as the only way to build a strategy, resilient to catastrophic P&L loss. In Ref. Malyshkin and Bakhramov (2015) market directional information was not obtained, thus only volatility trading was available for practical implementation. In this new study we made a substantial progress in dynamic equation application: to obtain market directional information from the dynamic equation.

Computer code with a reference implementation of the theory is presented in the Appendix G.

II Basis Selection

To operate with introduced inMalyshkin and Bakhramov (2015) concepts we need to convert market observable timeserie variables (time, execution price, shares traded) to a set of distribution moments. The three bases, performing time averaging with the exponential weight, are the most convenient for market dynamics study. Laguerre basis:

| (1) | |||||

| (2) | |||||

| (3) | |||||

| (4) | |||||

| (5) | |||||

| (6) | |||||

| (7) |

Shifted Legendre basis:

| (8) | |||||

| (9) | |||||

| (10) | |||||

| (11) | |||||

| (12) | |||||

| (13) | |||||

| (14) |

Price Basis

| (15) | |||||

| (16) | |||||

| (17) | |||||

| (18) | |||||

| (19) |

is a polynomial of –th order (e.g. monomials ), but from numerical stability pointMalyshkin and Bakhramov (2015) for (4) a good choice is the selection , with Laguerre polynomials, and for (11) a good choice is the selection , with Legendre polynomials. This choice make the basis orthogonal in measure: and , what drastically increase the numerical stability of calculations. However, all results are invariant with respect to polynomials selection. The specific choice affects only numerical stability of calculations, thus should be discussed separatelyLaurie and Rolfes (1979); Beckermann (1996); Malyshkin and Bakhramov (2015); Malyshkin (2015a). Proper basis selectionMalyshkin (2015a) allows us to have the numerically stable results even for two–dimensional basis with 100 basis functions in each dimension, i.e. with 10000 basis functions total for 64bit double precision computer arithmetic.

The Eqs. (7), (14) and (19) show how to calculate the moments from a timeserie sample . To simplify working with averages introduce quantum mechanic bra–ket notationWikipedia (2016b) and :

| (20) | |||||

| (21) |

where the integral in (21) is calculated directly from a timeserie according to (7), (14) or (19) depending on basis used. Familiar values can be easily presented with these definitions. Price exponential moving average: put price at time as the , then is required moving average. From all the considerations above one can easily see that bra–ket and notations from quantum mechanic are nothing more, than a ‘‘glorified moving average’’, and think of as taking a moving average with two basis functions product: . Different measures can be defined in a similar way. However the measures (4) and (11) are specialLaurie (14 Nov. 2015), in a sense they allow to calculate the moments from the moments using integration by parts. The following condition also holds:

| (22) |

Infinitesimal time–shift linear operator from (6) and (13), is different from plain differentiation because exponent differentiation in (4) and (11) give an extra term. The selection of basis functions as a function of price in (17) is extremely convenient in the quasistationary caseMalyshkin (2016) but does not possess such a simple infinitesimal time–shift transform.

II.1 as Radon Nikodym Derivative of Lebesgue Measures.

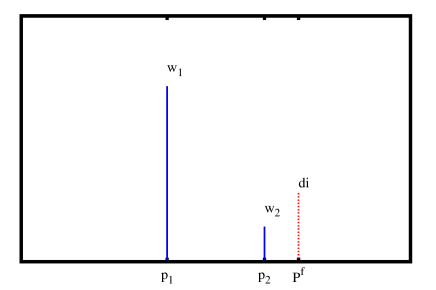

In this subsection we demonstrate price basis convenience for execution flow calculation in the quasistationary case and it’s relation to Radon–Nikodym derivatives, the main technique of our Malyshkin (2016, 2018) papers. The idea is to split price range on a number of intervals, then, for each interval calculate:

-

•

time spent

-

•

volume traded

of timeserie observations when the price is inside the interval, see Fig. 1 for illustration. These calculations give us two Lebesgue measures: and . These measures give time spend and volume traded when the price is inside the range . By itself these two Lebesgue measures are very similar to each other and are nothing more than a ‘‘glorified price–volume distributions’’, both having distribution maximum near price median, see Fig. 3 (top) of Ref. Malyshkin (2016). But when one take a ratio of these two measures, it gives trades execution flow , with singularities near price tipping points, see Fig. 3 (center) of Ref. Malyshkin (2016). The execution rate, the central concept of our theory, can be considered as Radon–Nikodym derivative of two Lebesgue measures and . For numerical calculations the described above histogram–like procedure works well only if discretization scale is properly chosen, what is a non–issue for manual analysis, but can be a real problem for an automated system. From numerical perspective there is a much better way to calculate Radon–Nikodym derivative of two measures, a calculation from distribution moments, see the formula (28) below, the answer in the form of Nevai operatorNevai (1986). Given sufficient number of moments (what may be a problem to calculate numerically, unless a stable basis is chosenMalyshkin and Bakhramov (2015)) the (28) is a superior numerical estimator of Radon–Nikodym derivatives.

III Wavefunction

Introduce a wavefunction to be a linear combination of basis function (here is time–space dimension, typically take some value between 4 and 20).

| (23) |

Then any observable (or calculable) market–related value , corresponding to a probability density can be calculated as:

| (24) | |||||

| (25) |

The (24) is plain ratio of two moving averages, but the weight is not just a regular decaying exponent according to (4) or (11), but exponent, multiplied by the , thus the define how to average a timeserie sample . The (25) is (24) with parentheses expanded according to (23). This way any function is defined by coefficients , and the value of any observable variable, corresponding to this state is a ratio of two quadratic forms (built on coefficients) of dimension , an estimator of stable formMalyshkin (2009). The representation of an observable in a form of two quadratic forms ratio (25) is conceptually different from the representation of an observable in a form of linear superposition of basis functions. In (25) a wavefunction is represented as a linear superposition of basis functions, the define probability density, then is calculated as averaged with this probability densityBobyl et al. (2016). This approach allows do decouple variables determining market dynamics and variables determined by market dynamics, what is critically important for any market dynamics study.

III.1 Interpolation Example

Given the definitions above, let us show some familiar answers. Let be some function, obtain , such as the interpolation , minimize least squares norm: . Taking the derivatives of the norm on obtain the solution:

| (26) |

Here is the inverse to Gramm matrix and the (26) is a regular least squares solution, a polynomial of order, where the coefficients are obtained as the solution of a linear system with Gramm matrix.

A much more interesting case is to obtain probability density , which is localized at given , then calculate , using probability density with interpolated . There are several formsMalyshkin and Bakhramov (2015) of such localized , the simplest one give (28), Nevai operatorNevai (1986):

| (27) | |||||

| (28) |

The (27) is interpolated localized wavefunction (localized at , compare it to interpolation (26)), then this localized at probability density is put to (25) to obtain (28), that is now considered as Radon–Nikodym interpolation of at . In contrast with the least squares answer (26) (which is a linear combination of basis functions), the (28) is a ratio of two quadratic forms of basis functions, a ratio of two polynomials order each in case of polynomial basis. The (28) is used for numerical estimation of , considered as Radon–Nikodym derivative. The (28) answer (basis–invariant answers (26) and (28) take very simple formMalyshkin and Bakhramov (2015); Bobyl et al. (2016) in the basis of eigenfunctions of operator, generated by the ), is typically the most convenient one among other available, because it requires only one measure to be positive. Other answersSimon (2011); Malyshkin and Bakhramov (2015) require both measures to be positive. Radon–Nikodym interpolation (28) has several critically important advantagesMalyshkin and Bakhramov (2015); Malyshkin (2015a, b) compared to the least squares interpolation (26): stability of interpolation, there is no divergence outside of interpolation interval, oscillations near interval edges are very much suppressed, even in multi–dimensional caseMalyshkin (2015a). These advantages come from the very fact, that probability density is interpolated first, then the result is obtained by averaging with this, always positive, interpolated probability.

III.2 Probability States

Considered in subsection III.1 localized wavefunction give a simple example, illustrating the power of the technique. However, much more interesting results can be obtained considering not only localized states such as (27), but arbitrary . This allows us to decouple observable variables and probability state.

As we emphasized inMalyshkin and Bakhramov (2015) system dynamics cannot be obtained from price. The price is secondary and typically fluctuates few percent a day in contrast with the liquidity flow, that fluctuates in orders of magnitude. (This also allows to estimate maximal workable time scale for an automated trading machine: the scale on which execution flow fluctuates at least in an order of magnitude. Minimal time scale is typically determined by available market liquidityMalyshkin and Bakhramov (2016)). The main idea is to obtain the state from the variables, determining the dynamics (e.g. execution flow , execution flow changes , etc.) and then use obtained state to determine the values of interest (e.g. price, price change, or P&L). A critically important feature of this approach is that both: the variables determining the dynamics and the variables determined by the dynamics can be directly calculated from recorded data, what is drastically different from Supply–Demand approach, where the disbalance of it cannot be calculated from recorded transactions data, because in all recorded transactions Supply and Demand are matched.

IV Price Impact

Price impact Moro et al. (2009); Gatheral and Schied (2013); Donier et al. (2014) is typically considered as path–dependent impact of executed shares number on asset price. However the price can be affected by a number of other factors and, moreover, an impact defined in such a way may diverge or even do not exist. In a style of previous section, define price impact as price change in a given state. With the approach we develop in this paper price impact is calculated in two steps. First, find the state of interest (e.g. corresponding to a large or , etc.). Second calculate price change corresponding to the found on the first step. We define price change, corresponding to the , as generalized price impact in the state: . The selection of will be discussed in the next section. In this section we only demonstrate how to calculate price impact for a given . There are two practical answers:

1. The moments can be directly calculated from a sample using (7), (14) or (19) with the replacement of the factor by the factor . After the calculation of moments the can be obtained directly:

| (29) |

The (29) give an answer calculated directly from sample.

2. In some situations the moments are not convenient to use or not available and only sampled moments are available. Then calculate the price , corresponding to the state, and variate using infinitesimal time–shift operator from (6) or (13) depending on the basis used.

| (30) | |||||

| (31) |

The (31) is the first order variation of Rayleigh quotient (30), the second order variation of Rayleigh quotient can be also calculated, see the (180) below with , but note that that terms need to be added to (183) in general case.

The (29) and (31) may or may not give similar answer, because they treat the boundary (time is ‘‘now’’) differently. Substantial difference in between (29) and (31) typically indicates a large contribution of the boundary, and is a signal of possible discrepancy in generalized price impact estimation. But, as we emphasized earlierMalyshkin and Bakhramov (2015), in practical applications other than price, dynamics–related attributes (e.g. P&L or ) should be considered instead.

V Wavefunction States Important For Market Dynamics

Localized state, considered in the subsection III.1, is of interest for interpolation problem only. For dynamic problem other to be considered. There is a number of interesting situations to consider, but consider the two forms of , the most promising for market dynamics and for generalized price impact calculation.

V.1 Corresponding to Maximal

We have already emphasizedMalyshkin (2016) the importance of the states, corresponding to maximal . The problem of maximizing on ‘‘past’’ sampleMalyshkin and Bakhramov (2015) can be reduced to a generalized eigenvalue problem (33).

| (32) | |||||

| (33) | |||||

| (34) |

Generalized eigenvalue problem (33) provide solutions (), each corresponds to the (eigenvalue,eigenfunction) pair . The state , corresponding to the maximal , is a first good candidate for generalized price impact calculation.

V.2 Corresponding to Maximal

The state, corresponding to maximal can be also of interest for market dynamics. In contrast with the , and matrices the matrix cannot be directly calculated from sample. However, in a presence of an infinitesimal time–shift operator (22) this matrix can be calculated by applying integration by parts:

| (35) |

Edge value is unknown in general case. We have tried various values for , but for simplicity of calculation let us put in this section (see the Section VII below for the case ). The means that the trading ‘‘now’’ is expected to stop at this price. Then the matrix can be obtained from (35) and generalized eigenvalue problem can be written in a usual way:

| (36) | |||||

| (37) | |||||

| (38) |

Generalized eigenvalue problem (37) provide solutions (), each corresponds to the (eigenvalue,eigenfunction) pair . The state , corresponding to the maximal , is a second good candidate for generalized price impact calculation.

V.3 Localized at

Localized at (the state ‘‘time is now’’) the wavefunction is of ‘‘interpolatory’’ type and does not provide any valuable information about market dynamics but is useful in some applications. Take (27) and put to obtain the . In Malyshkin (2016); Malyshkin and Bakhramov (2015), just for convenience, we used normalized :

| (39) | |||||

| (40) |

The (39) is plain normalized (27), normalization factor cancels in the numerator and in the denominator of (24) when calculating an observable.

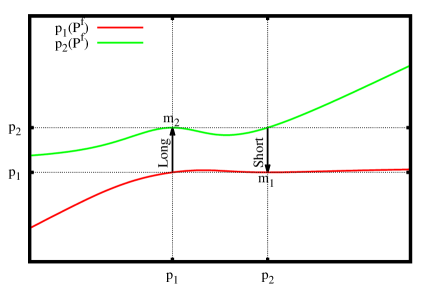

VI Demonstration Of Generalized Price Impact Calculation

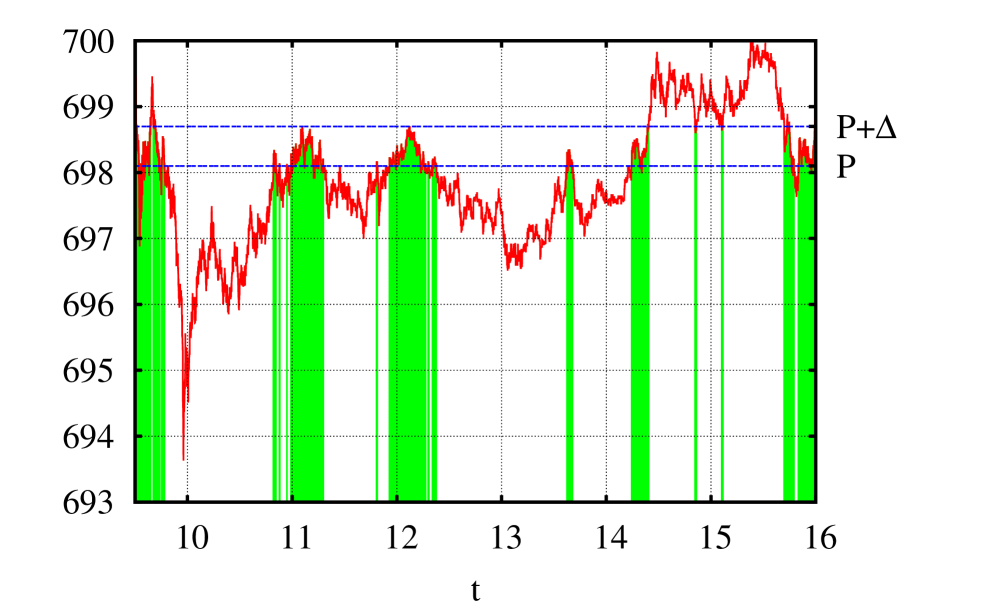

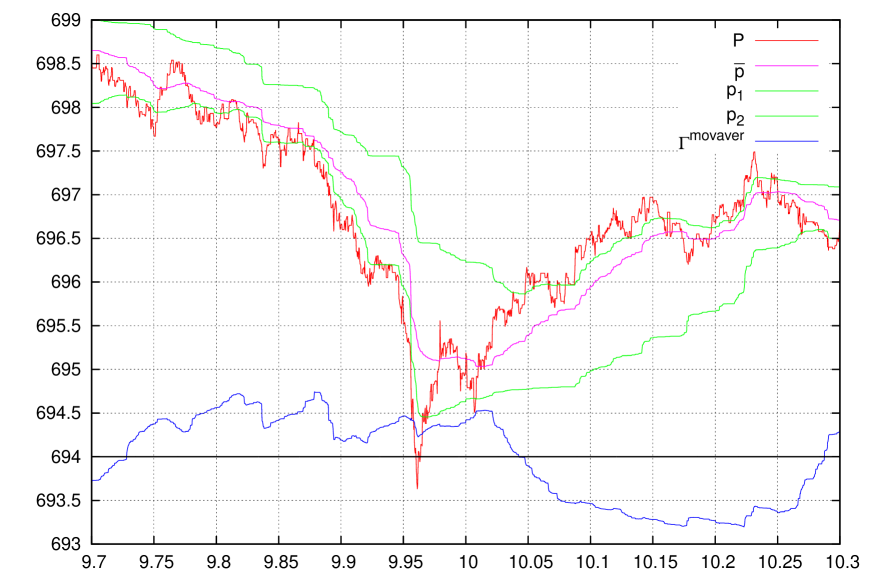

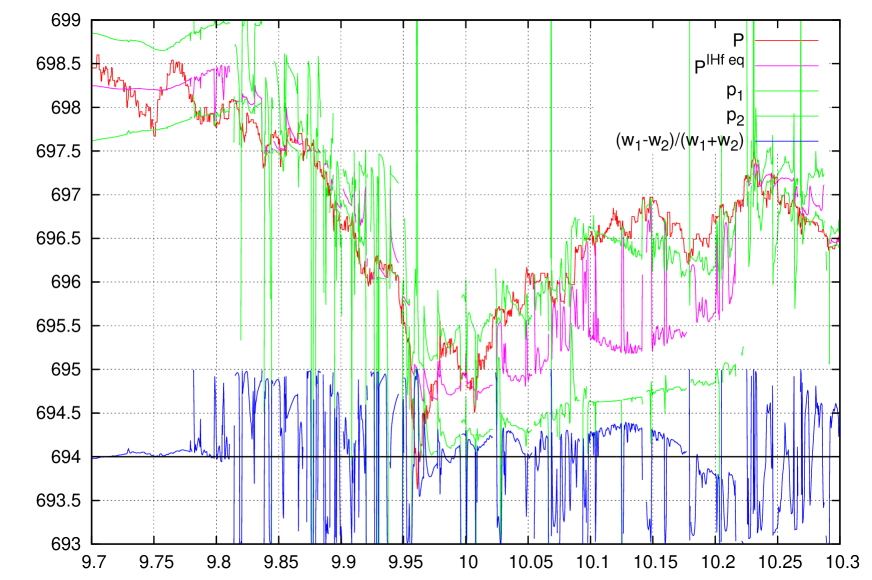

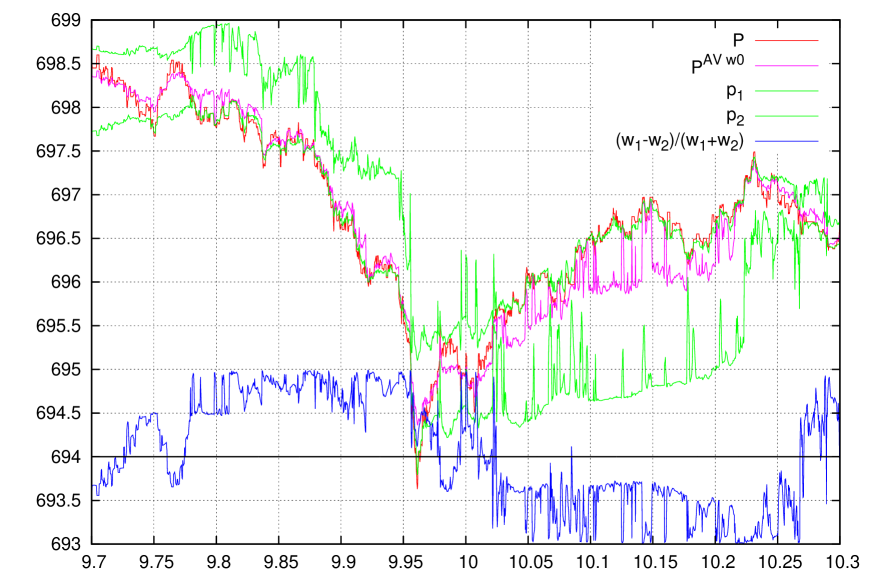

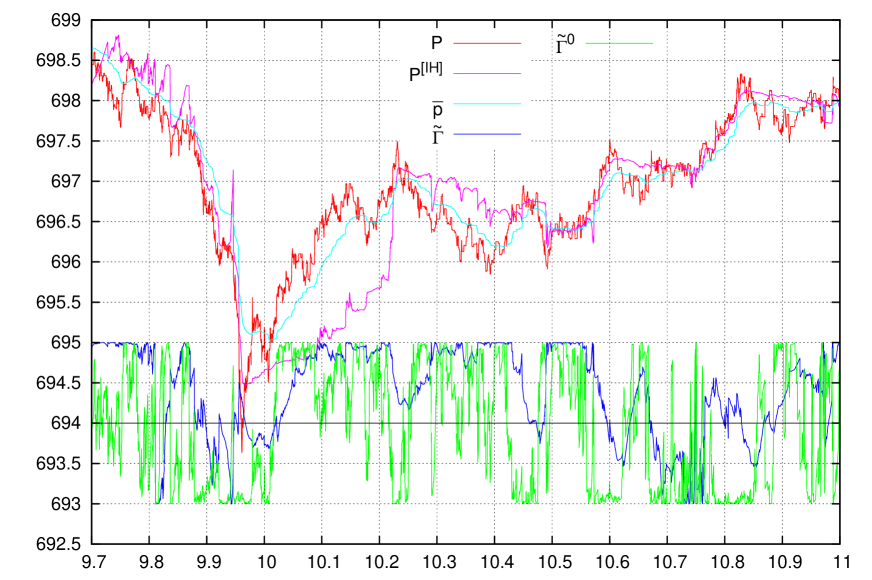

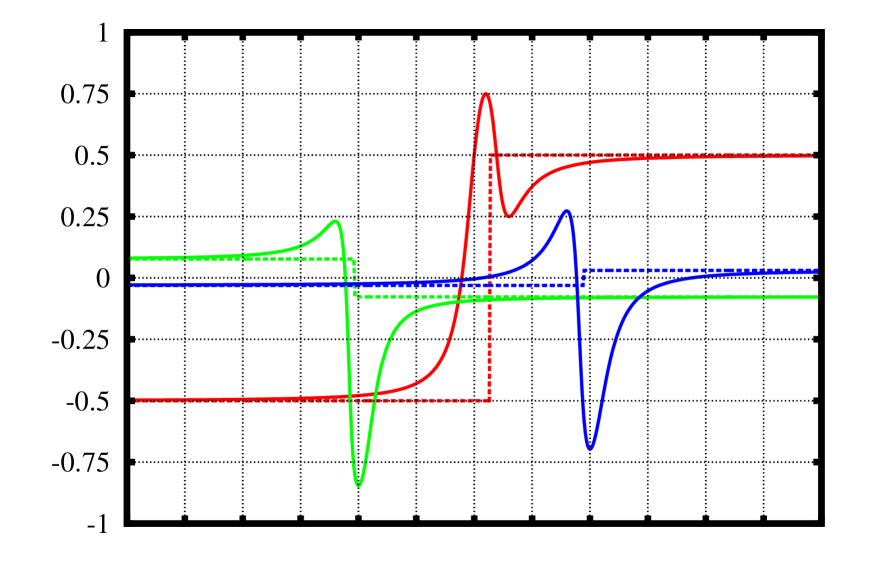

In this section we calculate generalized price impact on states discussed in the previous section. In Fig. 2 price change, corresponding to the state of maximal from (32) subsection V.1 and from (36) subsection V.2 are presented. In these figures

| (41) |

is the ‘‘ now’’, calculated with the from (39), the , max solution of (33), and , the one corresponding to the minimal of (33). The is calculated using (29) and is calculated using (31). From these charts it is clear that:

-

•

Boundary contribution much exceed non–boundary contribution, especially for large ; large typically corresponds to the boundary, i.e. large trading have just started ( state is close to ).

- •

-

•

The is typically much larger in the state, than in the state.

This make us to conclude that:

- 1.

-

2.

The concept of price impact is poorly applicable to market dynamics, because of large contribution of the boundary . Because future () prediction is the goal of any market dynamics study the attributes with large boundary contribution (e.g. ) are poorly applicableMalyshkin and Bakhramov (2015).

- 3.

-

4.

At large the price has a singularity, same as in the quasistationary caseMalyshkin (2016). In this paper we do not use a ‘‘boundary condition ’’ as we did in Malyshkin and Bakhramov (2015), so we always have , see Fig. 2. Bounded to projections

(42) (43) and are good indicators of ‘‘low’’ and ‘‘high’’ value of (also see Eq. (103) below for an alternative criteria). For a decision about ‘‘low’’ or ‘‘high’’ value of an attribute, the estimation of wavefunction projection to the state of interest is a superior approach to any classical one with a norm (i.e. or any other) and a thresholdMalyshkin (2015b).

-

5.

This confirms our approachMalyshkin and Bakhramov (2015) to make a transition from price dynamics to execution flow and P&L dynamics. This to be considered next.

VII Impact From The Future.

While the quasistationary caseMalyshkin (2016) of dynamic equation is easy, in a non–stationary case there are several fundamental questions to be answered before considering any practical application. We start with the ‘‘infinitesimal future’’ problem: knowing the last price value, what information about future price change can be obtained.

VII.1 Open Questions (With Possible Answers)

-

•

What ‘‘practically useful observable’’ can be directly predicted from the dynamic equationMalyshkin and Bakhramov (2015): ‘‘Future price tends to the value that maximizes the number of shares traded per unit time’’? Future value of can be predicted. The (41) gives ‘‘current’’ value of , it is calculated on already executed trades. Future value of (to be calculated on yet unexecuted trades) can be estimated as , the very important fact is that future estimator is calculated on already executed trades! If trading ‘‘now’’ is slow ( from (41) is small), this means that at current price buyers and sellers do not match well and asset price has to move. Asset price is expected to move due to an increase in the ‘‘future’’ , caused by the ‘‘future execution’’. In this sense the more slow the market now is, the more dramatic market move to be expected in the future. The ‘‘past most dramatic ’’, the , can be used as a reasonably good estimator (44) of the ‘‘future dramatic ’’:

(44) (45) (46) Note, that similar ideology is often applied by market practitioners to asset prices or their standard deviations. This is incorrect. Experimental observationsMalyshkin (2016) show: this ideology can be applied only to execution flow , not to the trading volume, asset price standard deviation or any other observable.

-

•

Given the role of the execution flow , what is a criteria of presence (or absense) information about the ‘‘future’’ in the ‘‘past data’’? If current from (41) is close to , this means that we already have a ‘‘very dramatic market’’ and there is no much information about the future of this market. This is the condition of no information about the future:

(47) But the most intriguing task would be to obtain directional information on price. The condition of no directional information about the future:

(48) is more restrictive than (47). If the state ‘‘time is now’’, the from (39), is an eigenfunction of operator (51), then past dynamics of has no information about the future (also note, that if is eigenfunction, then it is eigenfuction either). The (47) is a special case of (48). Imagine extremely high volume was traded at . Then the (33) solution, corresponding to is exactly the , and all other eigenfunctions () have , what immediately give the (47). Another example of (48) condition is the case when execution occurred only ‘‘now’’ () and in the moments of roots, that are the nodes of Gauss–Radau quadrature built on the measure , see Ref. Malyshkin and Bakhramov (2015) and computer code for calculating Gauss-type quadraturesMalyshkin (2014). One more example is, for an arbitrary , to consider , then this give the (48) . There is one more very important situation, when information about the future cannot be obtained: assume we have a trading without execution flow fluctuations, , then operator is degenerated (all eigenvalues are the same: ), what immediately lead to both (47) and (48) being satisfied.

-

•

While the dynamics is more or less understood, how can it be converted to a price dynamics? This is the most difficult problem. The relation between and is the fundamential question of market dynamics. We started this discussion in Malyshkin (2016), and have shown experimentally, that execution flow affect price much stronger (dynamic impact), than traded volume (regular impact). We also noticed there, that and often reach an extremum in the same state, i.e. their operators have the same eigenfunctions. Introduce dynamic impact approximation assuming asset price is affected only by the execution flow , not by the volume traded:

(49) If (49) holds then and have the same tipping points, the behaviour we experimentally observed in Ref.Malyshkin (2016). More generally, if price is only a function of then corresponding and operators to have the same eigenfunctions, the behaviour we observedMalyshkin (2016) for the states with high . We already estimated (44) future value of as and can build operator (51), having contribution ‘‘from the future’’ (45). Then future value of price can be estimated considering the operator (54), on eigenstates already found for operator (52). The price is secondary to the liquidity flow, but their common eigenfunctions allows to use future value of to calculate future value of .

VII.2 Open Questions (Without Answers)

-

•

What is the role of infinitesimal time–shift operator, available in some bases, e.g. (6) and (13)? It is very seductive to use infinitesimal time–shift operator to define a Lagrange functional (combining price volatility and execution rate), build an action (like other dynamic theories do), then try to minimize to build a theory combining both trend following (due to execution flow) and price reverse (due to price volatility)Malyshkin and Bakhramov (2015). Despite all our effort we failed with this plan. Even first order infinitesimal time–shift give the results similar to price impact of Section VI above. Typical for other dynamic theories second order infinitesimal time–shifts give an answer with even larger boundary contribution, thus having little predictive power. This make us to conclude that infinitesimal time–shifts are not very perspective for market dynamics and finite variations to be considered instead.

-

•

What is the role of in the dynamic equation, especially, whether price volatility can be expressed through the term Malyshkin and Bakhramov (2015)? As we already emphaised several times above ‘‘the price is secondary to liquidity flow’’, the spikes are just a consequency of liquidity fluctuations, the charts of Section VI above seems to prove this. But this statement results in ‘‘future price does not depened on past prices’’, what make our theory too provocative, e.g. it predicts that all theories of ‘‘trend following’’ or ‘‘reverse to the mean’’ based only on price trends are invalid.

-

•

What is the role of basis minimal and maximal time scale (how to determine and )? If we assume that the matrix has all the information about , then we can easily calculate the values, that cannot be directly calculated from a sampleMalyshkin and Bakhramov (2015). For example price volatility matrix in the form , that cannot be calculated directly from sample, can be expressed through calculatable directly from sample matrix using :

(50) Numerical experiment have shown this approach is not a very successful one. One can also try to compare the matrix calculated directly and Hermitian part of (50) calculated with and . The determines a ‘‘base’’ time scale, determines the time–scale variation. While this approach is a great advance from ‘‘moving average’’–type of approaches with a single predefined time–scale (corresponds to ), now we automatically select the state out of eigenfunctions with their own time–scales (in practice ), we still do not have a formal way to select proper and .

VII.3 Impact From The Future Operator.

As we stated above maximal (33) eigenvalue, the , can serve as an estimator of future . Then execution flow operator with an impact from the future is:

| (51) |

The term is proportional to the execution flow of not yet executed trades from (45); we now have and . To find future equilibrium wavefunction, according to dynamic equation, eigenvalues problem for operator needs to be solved

| (52) |

the Eq. (52) is the same as the Eq. (33), but with the operator from (51) instead of operator in (33). Eigenvalue selection in (33) was easy, it was the state with the maximal , according to our dynamic equation (32), from where we received the (44). But for (52) the answer is not so trivial. As we demonstrated in Malyshkin (2016), asset price is much more sensitive to execution rate , rather than to trading volume , thus in dynamic impact approximation (49) the contribution of state to future price changes is proportional to the flow of not yet executed trades . For this reason we are going to keep all eigenfunctions of (52) problem. The is operator eigenfunction (52), thus first order variation (53) is equal to zero for arbitrary .

| (53) |

The operator (for practical applications it is more convenient to consider operator instead of ) with an impact from the future is:

| (54) | |||||

| (55) |

The term for is proportional to execution capital flow of not yet executed trades at unknown future price with known future execution rate contribution from (45). ‘‘The last price as estimator (55)’’ is the simplest estimation, meaning the best estimation of future price is current value. In equilibrium the and to have the same eigenfunctions , at least for the states with a high , so the most promissing idea is to consider operator on eigenstates of and .

VII.4 Equilibrium Price in Naïve Dynamic Impact Approximation

In pure dynamic impact approximation formal answer for future equilibrium price can be obtained. This answer is not a very practical, so we would call it Naïve Dynamic Impact Approximation, but it is worth considering to compare it with the answer from our previous workMalyshkin and Bakhramov (2015).

Future equilibrium price enter impact from the future operator (54) from which is calculated as:

| (56) |

Now, assume and are diagonal in the same basis, the solution of (52). Expanding and assuming all off diagonal () matrix elements are zero: , same as we have for in (52). Then the can be estimated only from diagonal elements of :

| (57) |

Then (56) and (57) with (54) give the solution for :

| (58) | |||||

| (59) | |||||

| (60) |

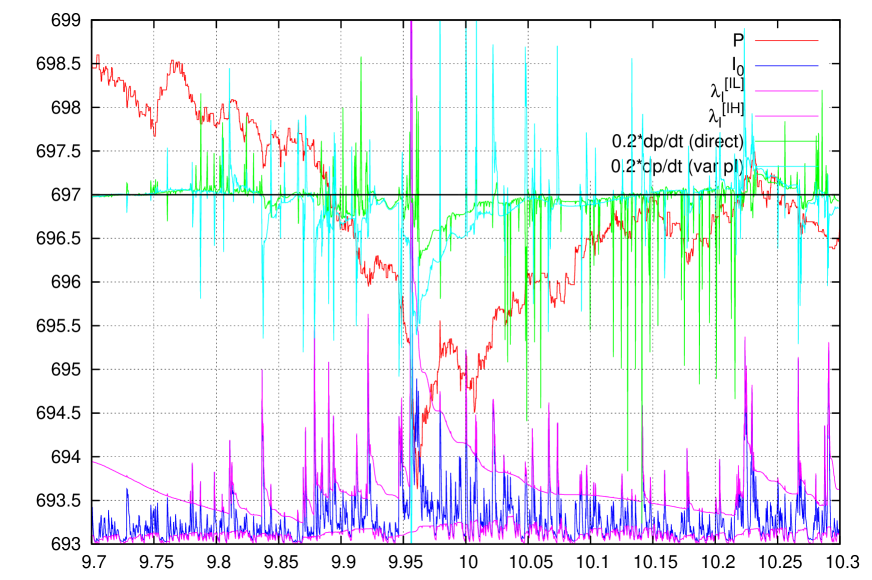

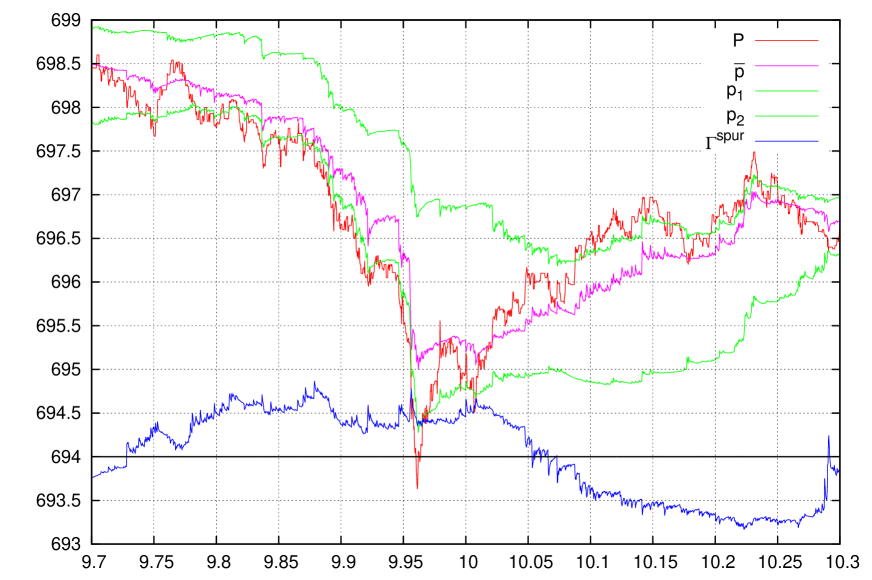

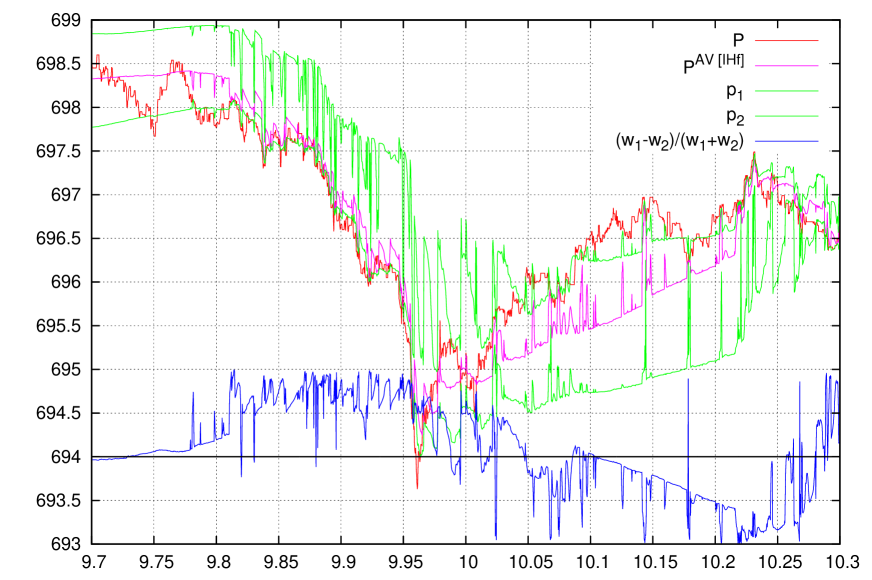

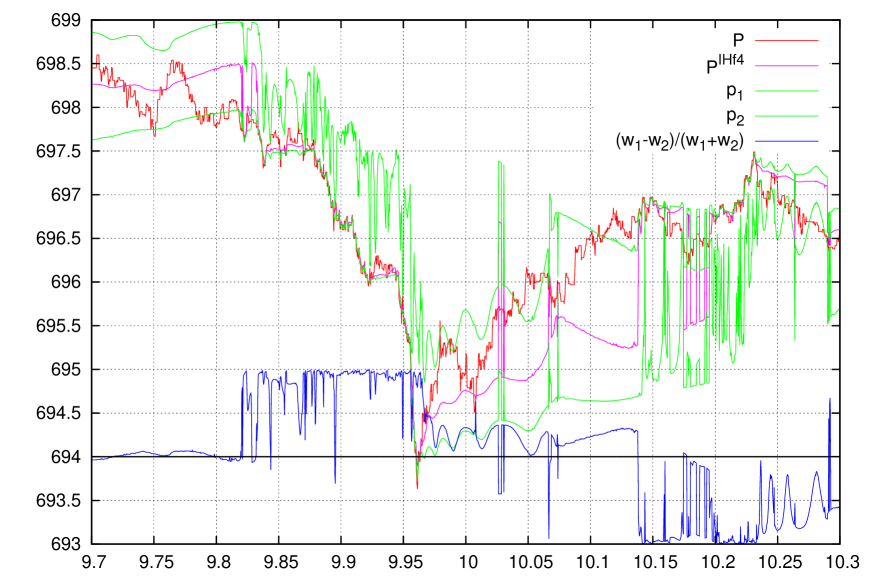

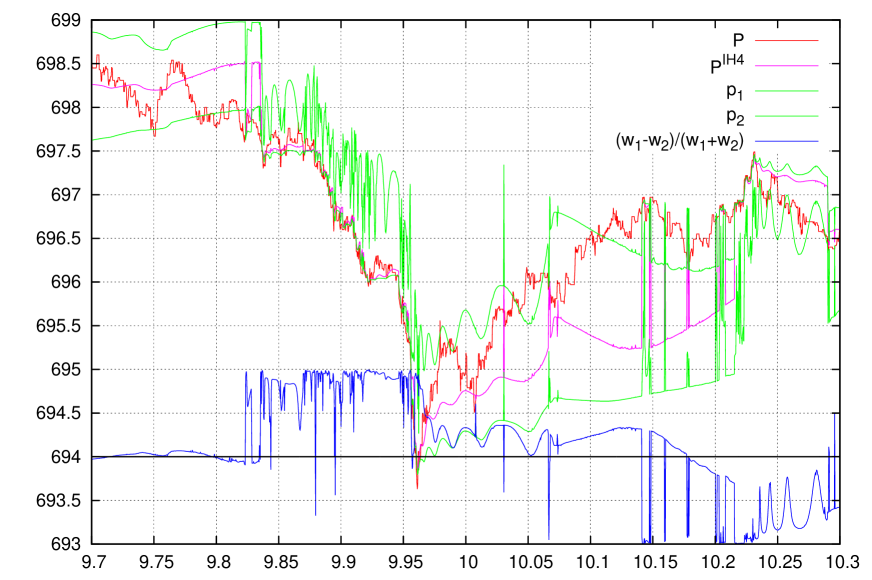

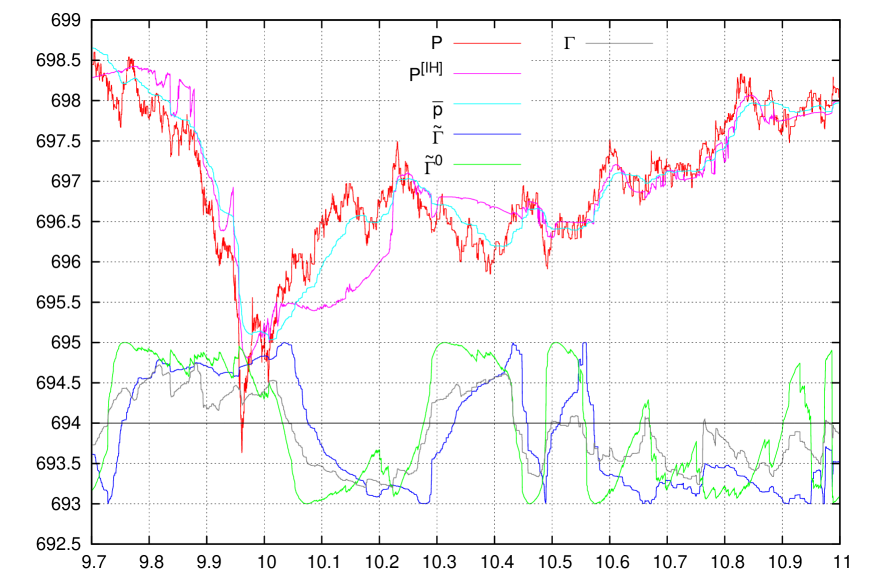

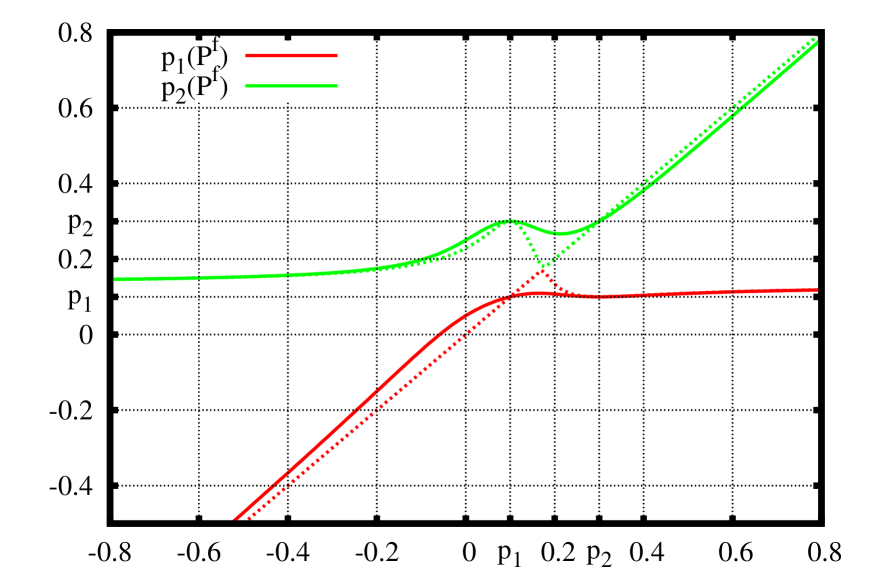

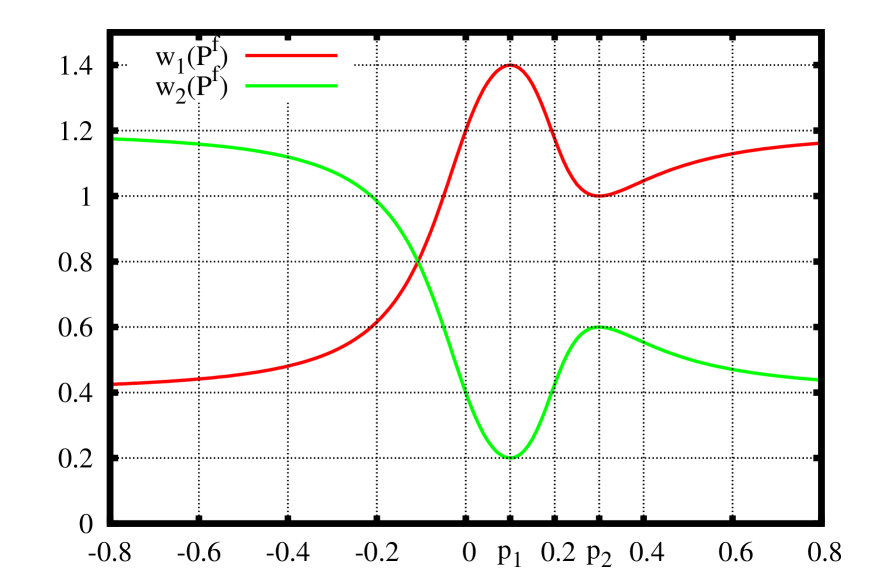

Conceptually (but not practically) the (60) directional answer is a giant step forward from our previous workMalyshkin and Bakhramov (2015), where the best directional estimator was the difference between last price and the price , corresponding to the state of maximal on past sample, the (30) calculated on state (34):

| (61) |

This Ref. Malyshkin and Bakhramov (2015) answer is asset price averaged on past sample with always positive weight ; no explicit information about the future is used in this averaging. The (60) answer is very different: it directly incorporates information about not yet executed trades from the future using and obtained from (44) assumption about . The from (59) formally define the degree of degeneracy, how much directional information can be obtained from the sample, it is zero when is (52) eigenvector, condition (48). Future volatility prediction is easy, for example (42) and (43) projections can be used to estimate whether current (41) is ‘‘low’’ or ‘‘high’’, then use (45). Future directional prediction is much more complicated, the (60) is the simplest (naïve) directional answer that can be obtained. In Fig. 3 the (61), (60), and (59) are presented. The degeneracy typically has a value , but going to at times of high , what correspond to (48) condition. In Malyshkin and Bakhramov (2015) the difference between last price and was used as a directional estimator. If is used instead, the result, as one see from Fig. 3 is very similar (sign does not change), but, as expected, is not close to last price at high . The (60) is asset price averaged on past sample, but, in contrast with (61), with the weight, which is not always positive. This lead to a divergence in (especially at low and/or small ). This divergence typically does not change the sign. Overall the (60) seems to be a marginal improvement over our old answer (61), this is why we call (60) naïve answer. For computer implementation see the \seqsplitPnLdIDSk.Pf_from_pt_true_pi for and \seqsplitPnLdIDSk.deg_from_pt_true_pi for . Computer code structure is described in appendix G.3.

VIII Selection of Time–Scale, Then Determine Price Distribution Asymmetry From Quadrature. Trend–Following vs. Reverse to the Mean

Equilibrium price estimation, let it be (60) of previous section or (61) of our previous workMalyshkin and Bakhramov (2015), and using the difference between and calculated price as directional indicator, typically does not give a satisfactory results, as price is secondary concept to market dynamics. The characteristics, describing the P&L distribution should be considered instead.

Let us start with the simplest problem of price distribution. As we discussed in Section III a measure is defined by a wavefunction , the measure is , then price moments , are:

| (62) |

(similar expression without can be used , but (62) choice is better in applications). The (62) expression selects the time scale based on choice. This way (via ) the (45) information about future can be incorporated. Different choices are considered below. For now assume, that some is chosen and the goal is to estimate price distribution on the measure generated by this . The standard approach is to consider price average, standard deviation and skewness. In the Appendix C of Ref. Malyshkin and Bakhramov (2015) modified skewness estimator was introduced. The moments describe how the price is distributed at times of the support of the measure. The skewness of the distribution is typically used for estimation of future price direction. However, a much better, than a regular skewness, answer can be obtained. The idea is to build two–point Gauss quadrature out of , moments then consider quadrature weights asymmetry (single–point Gauss quadrature require two moments and to calculate and give price average as the node: , the weight ). It is very important, that besides weights, two–point quadrature nodes can be used to determine threshold levels. The two nodes are generalized eigenvalue problem solution:

| (71) | |||||

| (72) | |||||

| (73) | |||||

| (74) |

The quadrature nodes are the eigenvalues (72) (we assume ), and the quadrature weights are expresses via the eigenfunction (73), for numerical calculation see the class \seqsplitcom/polytechnik/utils/Skewness.java. Note that defined in (74) skewness is similar in concept to the ‘‘signed volume’’ (the difference between market–sell matched limit–buy and market–buy matched limit–sell orders). As we emphasized earlierMalyshkin and Bakhramov (2016), regular signed volume concept is not a practical one. Important, that (74) definition allows us to obtain volume difference from trades history only, no matching type knowledge is required. See alternative formulas for (74) in the Appendix C of Ref. Malyshkin and Bakhramov (2015) to obtain (72) and (73) by minimizing over the nodes the expression:

| (75) |

The (75) is the definition of volatility, minimization of which give the nodes (72). Compare it to well known ‘‘minimizing volatility as standard deviation over the ’’:

| (76) |

that gives the (81) expression for the average price (single node Gauss quadrature) and to kurtosis calculation as . For two variables and a , correlating (71) eigenfunction (they are proportional to Lagrange interpolating polynomials) for and quadratures can be introduced, see Appendix B below for calculations.

Two point Gauss quadrature give exact integration answer for integration of a polynomial of degree 3 or less ( point quadrature is exact for a polynomial of degree or less). Familiar average, standard deviation and skewness can be expressed by averaging at with the weight and at with the weight :

| (77) | |||||

| (78) | |||||

| (79) | |||||

| (80) | |||||

| (81) | |||||

| (82) | |||||

| (83) |

The distribution itself can now be considered as two–mode distribution: trading at with the weight and trading at with the weight . This gives huge advantage: an opportunity to implement ‘‘follow the trend’’ type of strategy. For a single–point Gauss quadrature the only node is price average and only strategy available is ‘‘reverse–to-the–average’’ type of strategy (average price as an attractor). For two–point Gauss quadrature one can implement a ‘‘follow the trend’’ type of strategy (average price as a repeller, as the attractors), in a most simplistic way it is: ‘‘Open Short when ; Open Long when ; combine with weights asymmetry’’. The two new price levels: and allow to have a completely new look to trend–following trading: if are moving–average moments, then the and are much better thresholds than often used , because they include the skewness of price distribution, the thresholds are now different for up and down moves, according to the distribution skewness. This approach is much more generic, than this simple demonstration. The key components of it are:

-

•

Find the of interest. Several choices of are considered below. As we emphasized above the most interesting is the one maximizing the operator according to the dynamic equation. However, other choices can be also considered, at least for the purpose of the demonstration of the technique.

-

•

Given obtain the measure to calculate price moments from (62) Then Gauss quadrature nodes and weights to be obtained. This quadrature determines the distribution of price in the state. One can try to obtain some directional information on price from this distribution (e.g. skewness estimation (74)). Note, that when using (54) operators, with an impact from the future term, future price is required to calculate the moments, ‘‘the last price as estimator (55)’’ is a very crude approximation. While future price is unknown, all the calculations above can be reperated using as a parameter, see Appendix D below where the dependendce of on is obtained (161).

-

•

In addition, some other value (e.g. market index, etc.) can be considered and cross–correlation of Appendix B below can be performed.

IX Demonstration of price–distribution estimation from two–point Gauss quadrature built for a measure of interest

Let us demonstrate the technique of building two–point Gauss quadrature out of moments (62) calculated for a number of choices.

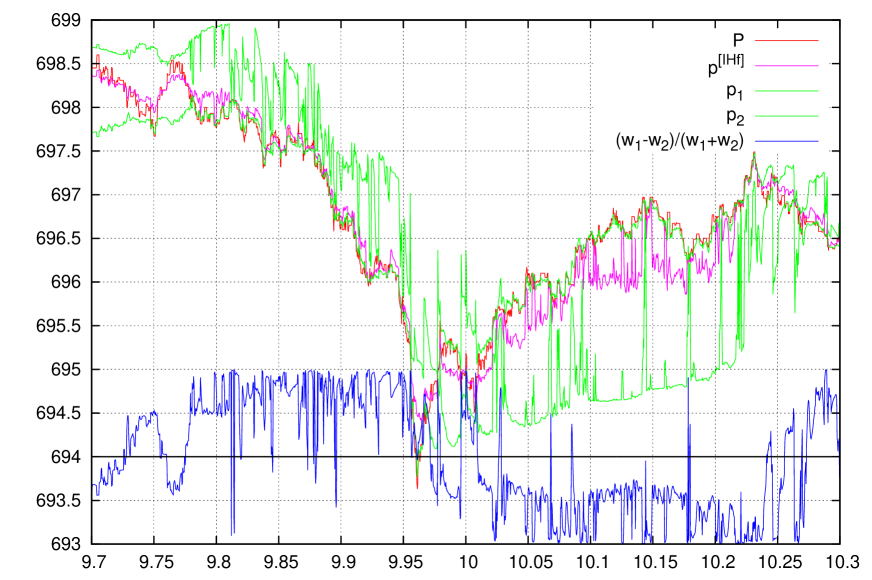

IX.1 Measure: Moving Average and Moving Average –Like

The most simple example is moving average–type of measure (corresponds to , also assume here, that there is no impact from the future: ). Calculate the moments:

| (84) |

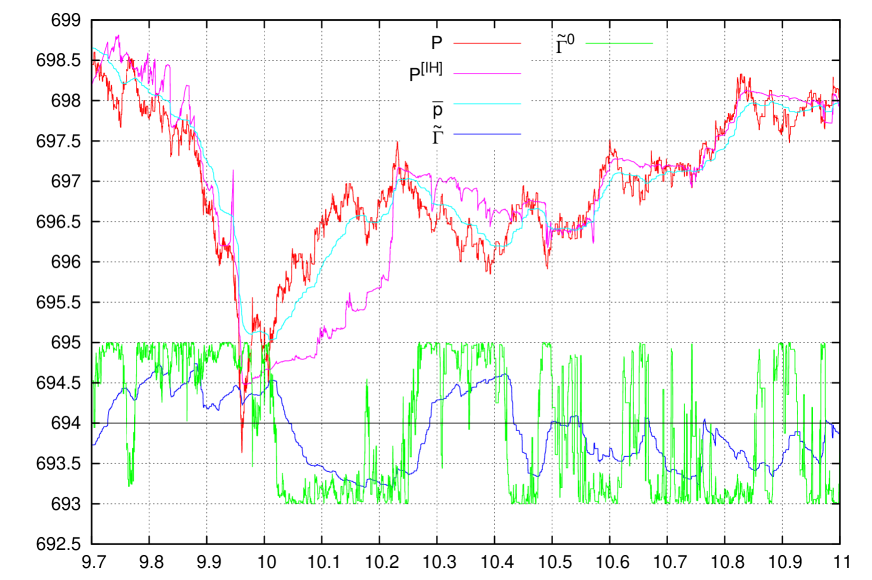

Then is regular exponential moving average. Gauss quadrature nodes and weights are calculated according to (71), and from (74). These values are presented in Fig. 4. Even in this non–practical example (because of fixed time–scale ) we clearly see an asymmetry between and . Median estimator is equal to average only in the case of zero skewness. We also see good skewness correlation with price trend, but, as for any model with a fixed time–scale, there is fixed time delay between price trend change and skewness change. However, the asymmetry between and is a remarkable feature that may be incorporated to a trading model, because three levels now allow to implement a ‘‘follow–the–trend’’ type of strategy.

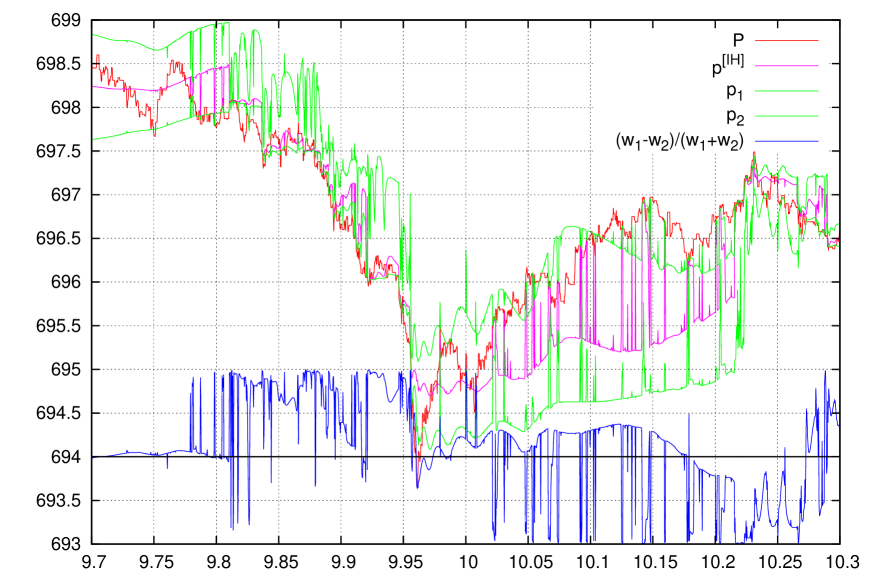

There is a characteristics, that is very similar to exponential moving average, but described by a density–matrix state, it cannot be reduced to a state of some . In its simplistic form the moments are matrix spur:

| (85) |

These are different from (96) in Section IX.5 below in absence of the impact from the future term, . (Note, that (85) is invariant with respect to basis transform, also seeMalyshkin and Bakhramov (2015) Appendix E of the expression in a non–orthogonal basis: ). The result is presented in Fig. 4 bottom. It is very similar to moving average result, as expected. These two kind of ‘‘moving average’’: with (84) ‘‘pure state’’ and (85) ‘‘mixed state’’ moments, demonstrate wavefunction and density–matrix approaches. In this section we specifically chose the situation, when both approaches give very similar result.

IX.2 Measure: The Period of Maximal Future

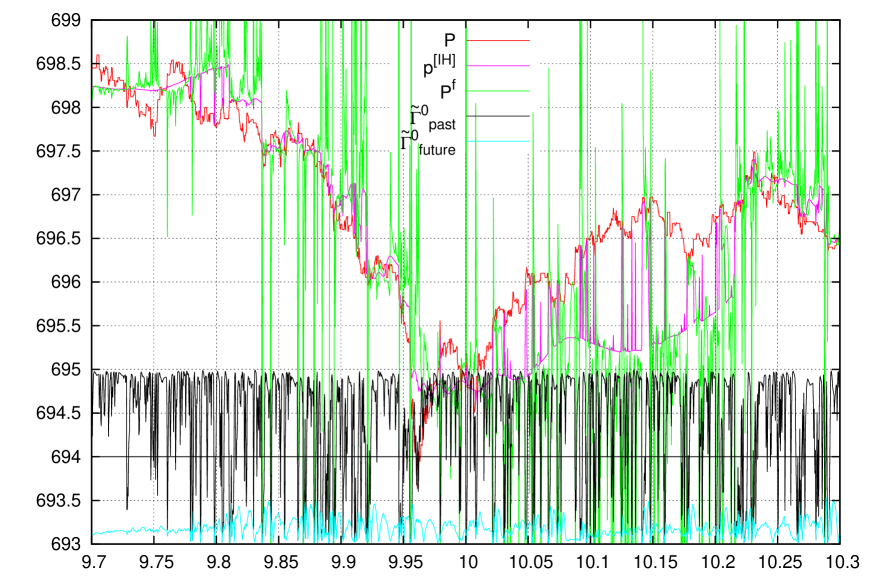

Consider the periods of maximal future . The ‘‘future’’ time scale is determined by the future state , the eigenfunction of (51) operator, the (52) solution, corresponding to maximal eigenvalue . The operators and moments for are:

| (86) |

To practically calculate the — the value of is known (45) and last price can be used as estimator (55). The result is presented in Fig. 5 top.

Then compare the results with the choice for , not having an impact from the future contribution, when the moments

| (87) |

are calculated in the state, the (33) solution (without an impact from the future term estimator is not required). The result is presented in Fig. 5 bottom. One can see the importance of the impact from the future term, however in this simplistic form price skewness has some issues as market directional indicator.

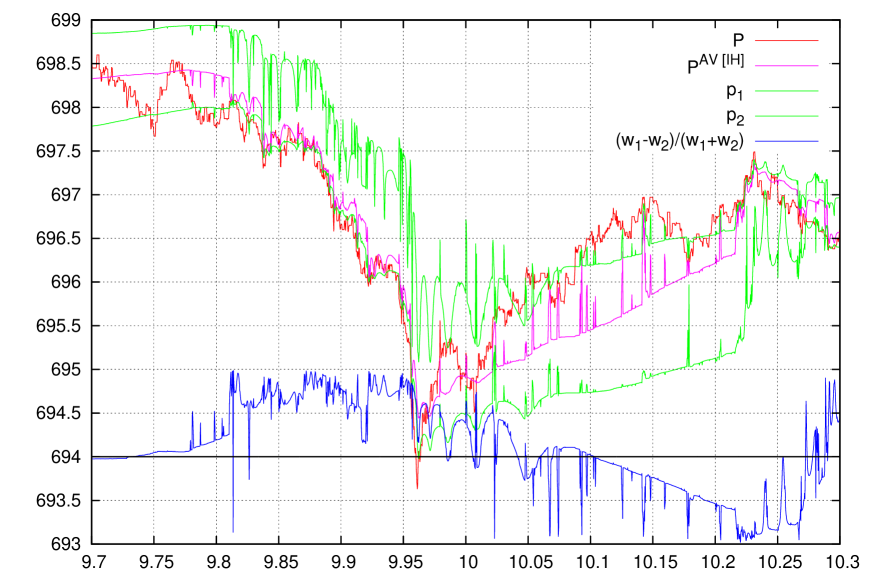

IX.3 Measure: The Period of Maximal Future with equilibrium estimator

While (86) moments from previous section are very promising they have one conceptional weakness: using as estimator (55). Consider operator (54) with an impact from the future. The idea is to modify (55) estimator to obtain some ‘‘equilibrium’’ value of .

As we discussed in Section VII.3 the and the operators to have the same eigenfunctions, thus first order variation should be equal to zero for arbitrary , same as for in (53):

| (88) |

The (53) holds for arbitrary , but for variations (88) only a single parameter is available, thus zero–sensitivity condition can be satisfied only for a single , besides trivial . There are a number of options for variation to consider:

-

•

Zero price impact (31) (zero sensitivity to infinitesimal time–shift).

-

•

Zero sensitivity to transition.

-

•

Zero sensitivity to transition.

among many others.

The estimation, corresponding to (88) equilibrium of (54) operator on state with variation is:

| (89) |

For the most interesting case obtain:

| (90) |

Then for the state with the maximal ():

| (91) |

Obtained have a term added to have zero variation (88). In Fig. 6 corresponding chart is presented. First, what is clearly seen is that Gauss quadrature does not always exist. This is because (90) may not always give a positive standard deviation. However, the formulae for the first moment is actually similar to naïve dynamic impact approximation of Section VII.4 and demonstrate an approach of searching a to variate (88). Despite all our effort we did not achieve much success with this search of , and now think that (88) variation can be a good option only for the first moment, what can give only a equilibrium price (first moment).

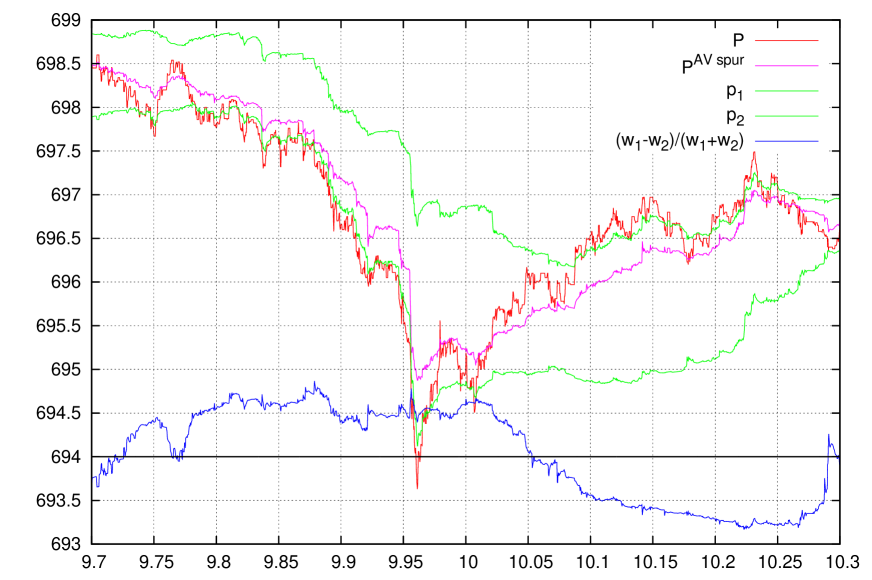

IX.4 Measure: The Period After Maximal Future

The choices (86) and (87) are considering price distribution during the spikes for the future and for the past respectively. It is very interesting to consider the time period after a spike in . Consider and :

| (92a) | ||||

| (92b) | ||||

Here is traded volume, is traded capital, is volume–weighted average price, is time–weighted average price. These values are calculated for the interval between and . Then for a given

| (93) |

Note, that for the measures allowing an integration by parts (i.e. the ones with infinitesimal time–shift operators such as (6) or (13)) the (93) can be interpreted as a transition from an averaging with the weight to an averaging with the weight:

| (94) | |||||

| (95) |

follows from the normalizing. For (4) and (11) measures the (93) can be calculated from the matrix elements using an integration by parts. For these measures Eqs. (93) and (95) are identical.

Consider a , defining the spikes in , the or from the previous section. Then (93) moments give very much a ‘‘moving average with automated time–scale selection’’ measure. These averages are calculated for the period of time: between the spike in and .

The results are presented in Fig. 7. They are worse than that of the previous sections, what probably manifest the importance of the execution flow dynamics over the volume dynamics. This correspond to our earlier work Malyshkin (2016), where an importance of dynamic impact was emphasized experimentally. See also the discussion below in Section XI, where the – and – dynamics are discussed from a different perspective.

IX.5 Measure: Density matrix mixed state of pure states.

As we discussed in Section VII.3 above, in case of the impact from the future presence, proper eigenstate selection is not a trivial question. In the Sections IX.2 and IX.3 the state, corresponding to the maximal , was considered. There are several alternatives. Consider matrix–averages (introduced in the Appendix E of Ref. Malyshkin and Bakhramov (2015), see Ref. Malyshkin (2015b) for quantum mechanics density matrix mixed state relation):

| (96) |

(in this section, when estimating the matrix elements, we assume (55) estimation for simplicity). The (96) answer is very much a moving–average type of answer (84), it is basis–invariant (a unitary transform of basis does not change the result) and can be considered as a density–matrix mixed stateMalyshkin (2015b) with equal contribution of each pure state.

Alternatively, a density–matrix mixed state with contribution of a pure state can be considered:

| (97) |

The (97) result is not basis–invariant and implicitly assume dynamic impact approximation (49) of and operators being simultaneous diagonal in the basis. The (97) is similar to (86), because state with the maximal projection is almost always the state. The results are presented in Fig. 8. They are not much different from the Sections IX.1 and IX.2 of above. This section demonstrate that density matrix approach is a viable option for the market dynamics, but, at this stage of development, does not give much compared to wavefunction pure states.

IX.6 Measure: Combine maximal Future and minimal price volatility

The approach of section IX.2 where corresponding to the maximum of was found on the first stage, then, for the found the corresponding to the minimum of are obtained (75). Consider a ‘‘combined’’ problem (despite it contradicts to the ideology we develop):

| (98) |

The idea is to find a saddle point of (98), the solution that has the maximum over and the minimum over . The results are presented in Fig. 9 (top: for operator with the (55) price estimation, bottom: for operator). They are not very promising. This was one of our many tries to built a functional, like an action in other dynamic theories, to search for a state of maximum and minimum price volatility. As with the other approaches of this type which we have tried, this specific one was also not a very successful. This make us to think that price volatility minimization approach is probably not a very perspective direction.

X Market Directional Information and vs. Probability Correlation

In Section IX we provided a few demonstrations of price skewness estimation technique, consisting in constructing a measure, building the price moments on this measure (either ‘‘pure state’’ (62) or ‘‘mixed state’’ of Section IX.5, depending on the measure used), then a two–node Gauss quadrature is built out of them and price distribution skewness is estimated as weight asymmetry (74). This approach has a built–in asymmetry of and , because the moments are difficult to calculate at best or they are non–exist at worst. It is very attractive to introduce some basis-invariant formulation of skewness concept, obtain and skewness, and then actually try to trade based on the skewnesses obtained. In the Appendix C a concept of probability correlation is introduced, but to trade we only need generalized skewness. Assume we have an observable , for a basis (a polynomial of –th order), and inner product () are defined in a way it can be calculated directly from sample. Important, that now and are not the same variables, in Section VIII for skewness calculation they were both equal to price. Average can be obtained in a regular way:

| (99) | |||||

| (100) |

To build , a similar to (74) skewness–like estimator (like a difference between median and average), we need and estimators of . These can be obtained solving optimization problem:

| (101) |

After parenthesis expansion the problem is reduced to generalized eigenvalue problem (145), the eigenvalues of which are quadratic equation roots. The / estimators of are equal to minimal/maximal eigenvalues and respectively, what allows us to obtain (150) skewness–like222 The (100) is state weight asymmetry expansion over the states corresponding to min/max : . Instead of a different values can be used, e.g. , corresponding to the state “time is now” from (39): , this “skewness”, (103) for , describe asymmetry (compare it with , that describe asymmetry). estimator in (100). If , then we receive exactly the from (74), which requires total 4 moments: to calculate. To calculate it requires total 6 moments: ; (for , there are only 4 independent among them). See the file \seqsplitcom/polytechnik/utils/Skewness.java:getGSkewness for implementation example of numerical calculation of generalized skewness . The most important property of is that it can be readily applied to non–Gaussian variables, e.g. . In our previous studyMalyshkin and Bakhramov (2016) we emphasized the inapplicability of a regular statistical characteristics (e.g. standard deviation) to market dynamics, and, instead, spectral operators should be applied to sampled non–Gaussian dataBobyl et al. (2016, 2018). The (145) generalized eigenvalue problem, finding min/max estimates and from operator spectrum is the simplest application.

X.1 Skewness. A demonstration of skewness estimation for non–Gaussian distribution.

Let us give a simple example of (100) skewness estimation application. Consider execution flow, polynomial basis , and a measure (such as (4), (11), or (17)), that can be calculated directly from sample: (7), (14) or (19). The problem: to estimate skewness. ‘‘Classical’’ approach, that requires , , , and moments to calculate either traditional estimator, or from (74) is not applicable, because second and third moments are infinite (note that first moment has a meaning of the traded volume and zeroth moment is a constant).

However the skewness from (100) can be calculated directly. All six moments: , , , , , are finite, matrices and obtained from these moments, eigenvalues problem (145) solved by solving the quadratic equation ; , obtained, and from (100) calculated.

In Fig. 10 we present the calculation of skewness for two measures: (4) and (17). Blue line: from (100), the asymmetry of ; green line: the asymmetry of , , calculated using (42) and (43) with . Positive skewness correspond to liquidity deficit event (low , slow market), a signal to open a position (but to determine the sing (long/short) of a position to open is a much more problematic task). Negative skewness corresponds to the liquidity excess event (high , fast market), a signal to close already opened position. From these charts one can clearly see that both and can be a good indicator of slow/fast markets, but the skewness is a better indicator as it shows how the ( now) is related to past min/max . Note, that calculated skewness of does not carry market directional price information. Instead, –skewness tells us about when (at negative skewness of ) the position have to be closed to avoid unexpected market move against position held, otherwise just a single such a move can easily kill all the P&L collected. Directional information (whether to open long or short position at positive –skewness), cannot be decided from –skewness, it to be decided from price or P&L dynamics.

X.2 Price Skewness.

In the previous section we have considered skewness, than generate ‘‘position open/position close’’ signals. However the direction (open long or open short) cannot be determined from that. Directional information to be determined from P&L dynamics. Consider the simplest case.

According to the arguments presented in Ref. Malyshkin and Bakhramov (2015) price or price changes cannot be used for directional predictions, and P&L dynamics should be considered insteadMalyshkin and Bakhramov (2016). P&L dynamics includes not only price dynamics, but also trader actions. In Ref. Malyshkin and Bakhramov (2015) (Section ‘‘P&L operator and trading strategy’’) we used probability states trying to analyze P&L dynamics, but here let us start with a very simple problem:

Assume exchange trading take place, and some speculator knows the future for specific time interval (investment horizon) from Oracle Precognition. What trading strategy to be implemented to maximize trading P&L and minimize introduced impact to the markets? The answer is trivial: for the investment horizon calculate price median, then trade at exactly the same time moments when ‘‘natural trading’’ to occur buying an asset when the price is below the median and selling it when the price is above the median, this is equivalent to frontrun the buyers at price below median and to frontrun the sellers at price above median. Why median price as a threshold? Only when price threshold is equal to the median, total position held at the end of investment horizon will be zero. If one use average price as a threshold then, depending on distribution skewness, speculator ends up with long or short position accumulated (to maximize the P&L speculator have to trade all the time) at the end of investment horizon (what means taking market risk because the future is assumed not to be known outside of investment horizon). In the simplest case price skewness, that is proportional to the difference between median price (estimated as midpoint ) and average price can serve as directional price indicator. Consider a simple demonstration:

-

•

Select a measure to define inner product , that can be calculated directly from sample.

-

•

Calculate price skewness out of moments: .

In Fig. 11 we present skewness calculation in two bases: (7) and (19) (top and bottom respectively). For , we have (gray line), (blue line), and (green line) calculated. For basis (and also equal to in Fig. 4 top), so gray line is not presented in this case. The define how close average is to min/max estimated as , and respectively. The do the same for in state. It is of interest to look in Fig. 11 top, where one can see the difference between and (gray and blue lines), that sometimes occur near price tipping points.

X.3 Skewness of future .

In Section X concept (100) was introduced and, for , it can be rigorously defined (along with probability correlation concept) in Appendix C. However a modified concept is convenient in applications. Introduce (the can be either price or execution flow ) :

| (102) | |||||

| (103) |

measure how ( ‘‘now’’) compares with and (min/max eigenvalues of problem), calculated on past observations. For we have , (as we already mentioned this, regarding (42), (43) projections difference), but for this is not the case. For the is plain indicator of how fares with and . The (103) answers the major questions of our dynamic theory: ‘‘whether the we currently observe is low or high’’. The is bounded to interval. value close to means we have liquidity deficit event ( is low), value close to means we have liquidity excess event ( is high). Note, that is a non–Gaussian variable with infinite second moment , so no approach utilizing a standard deviation of can be applied.

Because we do know future operator (51), the can be calculated for it. Now consider operator (54) with unknown , and assume it has the same skewness on the states of operator, then:

| (104) | |||||

| (105) | |||||

| (106) | |||||

The (106) is that, for operator (54), give the same skewness as the one for . This answer is similar to naïve dynamic impact approximation of Section VII.4 (compare (105) with (59), and (106) with (60)). The results are presented in Fig. 12. As for naïve dynamic impact approximation, the from (106) behave similar to from (61), and have numerical instability for low . Future skewness (for ) is negative (the impact from the future (45) make it such). Past skewness (for ) is positive during liquidity deficit and negative during liquidity excess. Trader should open a position during positive and close it during negative , this is the only way to avoid catastrophic P&L hit from an unexpected market move.

XI On A Muse of Cash Flow And Liquidity Deficit Existence

We finally reached the point to decide what information can be obtained from historical (time, execution price, shares traded) market observations deploying introduced inMalyshkin and Bakhramov (2015) the dynamic equation: ‘‘Future price tends to the value that maximizes the number of shares traded per unit time’’. While volatility trading is much easier to implement algorithmicallyMalyshkin and Bakhramov (2015), it is much more difficult to implement practically, on exchange, because it requires building some synthetic assets (such as Straddle Wikipedia (2016c)) using options (or other derivatives). Compared to regular HFT equity trading accounts, HFT derivative trading accounts are much more costly and derivative markets often have insufficient available liquidity for a practical trading strategy implementation. In addition to that trading strategies including derivatives are way more difficult to backtest for the reasons of data availability and insufficient liquidity. In this section we are going to discuss whether a much more ambitions goal, to obtain directional price information (not only volatility!), can be practically achieved with the dynamic equation. Our study show, that there are two pieces of information, required to obtain directional information:

First. Price directional information of the past. A trivial information of this type is ‘‘last price minus moving average’’ currently is in common use. We obtained few more sources of this information, having the benefit of automatic time–scale selection. These are: (price corresponding to max on past sample (61)), skewness of price on max state of operator with an impact from the future (Section IX.2), the skewness of price (or P&L) of Section X, and few other.

Second. Execution flow () directional information. Since Adam SmithWikipedia (2017a) and Karl Marx the volume of the trade is considered to be the key element of goods/money exchange process between buyers and sellers. The concept of Velocity of moneyWikipedia (2017b), velocity of circulation, ( is the velocity of shares, is the velocity of money) while being widely recognized as an important macroeconomic concept, is not in use among both academics and exchange trading practitioners (at best they use the volume, assuming the consumption of shares is limited by the number of shares bought: ‘‘The tailor does not attempt to make his own shoes, but buys them of the shoemaker, page 350’’Smith (1827)). Modern exchange trading currently exists of market participants, that are simultaneously buyers and sellers (modern ‘‘shoemaker’’ not only sells the shoes he made, but also buys shoes to sell them later), and, because of leveraged trading, weakly sensitive to the volume (regular impactWikipedia (2016a)) of the position. As we have shown experimentally, they are much more sensitive to the rate of trading (dynamic impactMalyshkin (2016)). The situation of market separation of – and – trading can be currently observed in Electricity MarketWikipedia (2017c) that is separated on Energy and Power markets on legislative level. Our exchange experiments show that modern exchange trading is actually a Power–like market. The reason why the velocity of money was not actively used for exchange trading is, from our opinion, the absences of mathematical technique to estimate (execution flows are non–Gaussian). Because Radon–Nikodym derivatives can be effectively applied to non–Gaussian processes it is the proper tool for velocity of money analysis. Two indicators of are used in this paper. These are the projections (42) and (43) difference that show whether current is ‘‘low’’ or ‘‘high’’, and the skewness of , the from (100) (or more useful in practice from (103)). The skewness of can be estimated only from Radon–Nikodym approach, because regular skewness estimators are not applicable for the reason of infinite and .

Practical trading to be this: Determine price direction (e.g. from (61)), or the skewness of , Section X.2, with some measure). Then calculate –skewness . Open a position (according to price direction found) when is close to , close already opened position (but do not take opposite position!) when is close to to avoid catastrophic P&L drain in case of unexpected market move against position held. Such a strategy do provide provide a P&L, and, important, is resilient to unexpected market hits. In the next paper I will try to present a demonstration of this strategy computer implementated. Do not expect a big miracle, (even a ‘‘small miracle’’ of paper trading P&L), but avoiding big P&L hits can also be considered as a miracle of some kind.

Acknowledgements.

Vladislav Malyshkin would like to thank Alexei Chekhlov at Systematic Alpha for fruitful discussions on the link between liquidity deficit and execution flows, and Misha Boroditsky at Cantor Fitzgerald for his comments on trading systems’ impact on financial markets.Appendix A Time–Distance Between States

For two states from (34), already separated in –space by the value of eigenvalue , the separation in time space is often required. For this a ‘‘time–distance function’’, between the and states from (34) is required. The is an antisymmetric matrix, showing which state or is later (in time) and which one is earlier.

| (107) |

There are several choices, that can be applied to the task. All of them can be obtained from two–point propagator–like expressions with some antisymmetric

| (108) | |||||

| (109) |

These are the most common choices:

-

•

Probability difference between ‘‘ coming after ’’ and ‘‘ coming before ’’ events. Can be obtained from (109) with . It can be calculated analytically for the measures (4) and (11). See java classes {KkQVMLegendreShifted, KkQVMLaguerre, KkQVMMonomials}.{_getK2,_getEDPsi} from Appendix G for implementation of probability difference function and infinitesimal time shift operator.

-

•

Total volume traded

(110) (111) Corresponds to (109) with . The state with a greater volume can be considered as coming after the state with lower volume.

-

•

Difference in projection to from (39):

(112) Corresponds to (109) with , with and – infinitesimal time shift operators on and . The state with a greater projection to is considered to be the one coming after the state with lower projection. The distance (112) is degenerated: it is equal to 0 for any two for which . Also note, that , i.e. the differ from the on a constant.

-

•

One can variate the (110) with infinitesimal time shift of , applying (6) or (13) operator to receive (after normalization) a time–distance like this:

(113) (114) (115) The (114) is a ‘‘second order distance’’. In contrast with the volume (110), the (114) describe the difference in flows of volume since till ‘‘now’’ per time and the rate .

Appendix B : Value Correlation of Variables.

For two variables and , with some positive measure on them, regular and a new one can be obtained by differentiation (118) and (122):

| (116) | |||||

| (117) | |||||

| (118) | |||||

| (119) | |||||

| (120) | |||||

| (121) | |||||

| (122) | |||||

| (123) |

where and are quadrature nodes obtained from (120) and (121) minimization, exactly as we did in Eq. (75) above. The (122) (and (123) correlation) covariate and , but use higher order moments; for it gives regular relations: , and .

A much more interesting case is to consider the matrix , that covariate –th level of with –th level of ; (here and ). Consider Lagrange interpolating polynomials built on quadrature nodes, (they are proportional to (71) eigenfunctions):

| (124) | |||||

| (125) | |||||

| (126) | |||||

| (127) | |||||

| (128) | |||||

| (129) |

The covariation matrix (129) can be interpreted as a joint distribution matrix of and variables. Corresponding to quadrature nodes Lagrange interpolating polynomials are a useful tool to built such a matrix, because their inner product can be obtained for the measures of interest. The (129) covariance definitions have integrals over time, that can be calculated directly from distribution moments, it can be obtained from observation sample in a way similar to (7) or (14). For the matrix is diagonal: .

matrix components have the dimension of the measure from (128) and can be easily written for two–point Gauss quadratures built on and :

| (130) |

quadrature weights can be expressed through elements sum:

| (131a) | |||||

| (131b) | |||||

From (130) immediately follow that the sum of all four elements of matrix is equal to . To obtain dimensionless ‘‘correlation’’–like matrix the (130) can be divided by from (128), the difference between diagonal and off-diagonal elements of this ‘‘correlation’’–like matrix can be called correlation:

| (132) | |||||

| (133) |

that is different from regular definition by the term describing skewness correlation. The (133) means, that if two distributions have the skewness of the same sign, their ‘‘true’’ correlation is actually higher, than the one, calculated from the lower order moments as . The (133) formula for is obtained directly from joint distribution matrix (130) and has a meaning of values correlation: the element of (129) matrix is the probability that and . The conditions and also holds, same as for from (123). We want to emphasize, that, in applications, the most intriguing feature is not a new formula (133) or (123) for correlation, but an ability to obtain joint distribution matrix (130) from sampled moments of two distributions.

Quadrature nodes and are calculated from the moments (134a) and (134b) respectively applying either formula (72) above or the ones from Appendix C of Ref. Malyshkin and Bakhramov (2015) (or the formulas from Appendix D of this paper with , what give –independent answers). For term in (130) one more moment (cross–moment) from (134c) is required in addition to regular and ():

| (134a) | |||||

| (134b) | |||||

| (134c) | |||||

(to calculate (130) matrix it requires total 8 moment, see the file \seqsplitcom/polytechnik/utils/ValueCorrelation.java for implementation example of numerical calculation of value correlation). The (134) definitions can be be generalized to matrix averages (see Appendix E of Ref.Malyshkin and Bakhramov (2015)), that corresponds to mixed state in quantum mechanics, a generalization from pure states of form.

Appendix C : Probability Correlation of Variables.

Obtained from sampled moments joint distribution estimator (130) of previous appendix is an important step in correlation estimation. However, it still has a number of limitations to be applied to practical data.

-

1.

It requires two quadratures (on and ) to be built, this requires the moments (134) to be calculated from the data. Assume is execution flow of some security, then, for example, is problematic to calculate: it is not possible to calculate it directly from sample and (50) approach does not always give a good result.

-

2.

The cross–moment from (134c) is often problematic to calculate.

-

3.

Some of (134) moments can diverge or even do not exist, their numerical estimation often becomes a kind of numerical regularization exercise.

If we generalize ‘‘correlation concept’’, then the approach to joint distribution matrix estimation can be extended to using the moments calculated in arbitrary basis, not only for the one with basis functions argument as an observable, the case considered in Appendix B. Assume we have two variables and (e.g. execution flow of two securities), some basis for ( can be e.g. time or price; is a polynomial of –th order), inner product (where and ) is defined in some way, such that the inner product can be calculated directly from sample. As we discussed in Bobyl et al. (2016) any observable variable sample can be converted to a matrix, then generalized eigenvalue problems define the spectrum of the observable. For and this would be the equations (similar to Eq. (33) with ):

| (135) | |||||

| (136) |

For generalized eigenvalue problem is reduced to solving quadratic on equation: , same as with Eq. (71):

| (145) | |||||

| (146) |

Found solutions are chosen to have normalized eigenvectors: ; , and ordered eigenvalues . The square of eigenvectors scalar product define matrix , the elements of which are the probabilities of how low/high is correlated to low/high :

| (147) | |||||

| (148) |

The modified correlation is the difference between diagonal and off-diagonal elements of matrix. This is similar to (132) of previous section, but now the matrix is built solely out from moments, that can be defined in arbitrary basis. An important difference between (147) and (129) matrices is that the (129) elements are scalar product of eigenvectors, but (147) elements are squared scalar product of eigenvectors; the elements of both matrices have a meaning of probability, but the probability is defined differently. The (147), as squared scalar product of eigenvectors, is a correlation of probabilities. The is a probability of probability333 In quantum mechanics a scalar product of two wavefunctions can be interpreted as “two wavefunctions correlation”. Taking it squared obtain the probability of probability correlation. If the wavefunctions are of the states having specific value (135) and having specific value (136), then squared scalar product of corresponding eigenvectors can be similarly interpreted as a probability of probability of and . This interpretation also corresponds to (149) normalizing. that has a value and has a value , what is different from the , Eq. (129), that is a probability of and . Instead of (131) we now have:

| (149a) | |||||

| (149b) | |||||

the sum of the elements in any row or column of matrix is equal to . If (typical situation), then, similar to (74) definition, a skewness–like (like a difference between median and average) characteristics of random variable can be introduced:

| (150) | |||||

| (151) | |||||

| (152) | |||||

| (153) |

This skewness definition (150) has a meaning of state expansion weights asymmetry on the states: , corresponding to minimal , and , corresponding to maximal ; . The (148) probability correlation can be also written in a similar ‘‘derivative–like’’ form (152): the difference between in the state of minimal , and in the state of maximal , divided by minimal and maximal difference. For probability correlation classical condition holds, for the (147) matrix is diagonal: . But another classical condition does not hold: , if then eigenvalues problem (136) is degenerated and, without an extra condition on eigenvectors, the value of probability correlation (148) can be arbitrary, depending on specific – eigenvectors choice.

The distinction between ‘‘value’’ and ‘‘probability’’ correlations is an important topic of modern research in both computer science and market dynamics. The problems of Distribution Regression ProblemDietterich et al. (1997); Zhou (2004) (a number of observations of type ‘‘bag of instances to a value’’ are used to build a mapping: probability distribution to value) and Distribution to Distribution Regression Problem (a number of observations of type ‘‘bag of instances to a bag of other instances’’ are used to build a mapping: probability distribution to probability distribution) are the most known generalization of regular Regression Problem (a number of observations of type ‘‘value to a value’’ are used to build a mapping: value to value) have been addressed from a number of points. Our contribution to it is based on an application of Christoffel functionMalyshkin (2015c), and Radon–Nikodym derivativesMalyshkin (2015d). The difficulties in probability estimation using real life data have been emphasizedTaleb et al. (2014), but very different mathematical technique have been used for probability estimation. The (148) answer is, to the best of our knowledge, the first probability correlation answer, that is calculated from the moments of sampled data. To calculate (147) matrix it requires moments: ; total 9 moment, see the file \seqsplitcom/polytechnik/utils/ProbabilityCorrelation.java for implementation example of numerical calculation of probability correlation from (148), also see the file \seqsplitcom/polytechnik/utils/Skewness.java:getGSkewness for calculation from (150). A remarkable feature of these answers is that they use only first order moments on and and higher order moments on . This separation of observable variables and basis functions allows the approach to be applied to and having non–Gaussian distributions, even those with, say, infinite or , a distinguishable feature of Radon–Nikodym approachBobyl et al. (2016).

Appendix D Price distribution estimation with unknown future price as a parameter