Orthogonal Series Density Estimation for Complex Surveys

Shangyuan Ye, Ye Liang and Ibrahim A. Ahmad

Department of Statistics, Oklahoma State University

Abstract

We propose an orthogonal series density estimator for complex surveys, where samples are neither independent nor identically distributed. The proposed estimator is proved to be design-unbiased and asymptotically design-consistent. The asymptotic normality is proved under both design and combined spaces. Two data driven estimators are proposed based on the proposed oracle estimator. We show the efficiency of the proposed estimators in simulation studies. A real survey data example is provided for an illustration.

Keywords: Nonparametric, asymptotic, survey sampling, orthogonal basis, Horvitz-Thompson estimator, mean integrated squared error.

1 Introduction

Nonparametric methods are popular for density estimations. Most work in the area of nonparametric density estimation was for independent and identically distributed samples. However, both assumptions are violated if the samples are from a finite population using a complex sampling design. Bellhouse and Stafford (1999) and Buskirk (1999) proposed kernel density estimators (KDE) by incorporating sampling weights, and their asymptotic properties were studied by Buskirk and Lohr (2005). Kernel methods for clustered samples and stratified samples were studied in Breunig (2001) and Breunig (2008), respectively.

One disadvantage of the KDE is that all samples are needed to evaluate the estimator. However, in some circumstances, there is a practical need to evaluate the estimator without using all samples for confidentiality or storage reasons. For example, many surveys are routinely conducted and sampling data are constantly collected. Data managers want to publish exact estimators without releasing all original data. In Section 6, we provide a real data example from Oklahoma M-SISNet, which is a routinely conducted survey on climate policies and public views. The orthogonal series estimators are useful alternatives to KDEs, without needing to release or store all samples.

The basic idea of the orthogonal series method is that any square integrable function , in our case a density function, can be projected onto an orthogonal basis : , where

| (1) |

is called the th Fourier coefficient. Some of the work using orthogonal series was covered in monographs by Efromovich (1999) and Tarter and Lock (1993), among others. Efromovich (2010) gave a brief introduction of this method. Walter (1994) discussed properties of different bases. Donoho et al. (1996) and Efromovich (1996) studied data driven estimators. Asymptotic properties were studied by Pinsker (1980) and Efromovich and Pinsker (1982).

In this paper, we study orthogonal series density estimators (OSDE) for samples from complex surveys. To the best of our knowledge, no previous work has been done on developing OSDE for finite populations. We propose a Horvitz-Thompson type of OSDE, incorporating sampling weights from the complex survey. We show that the proposed OSDE is design-unbiased and asymptotically design-consistent. We further prove the asymptotic normality of the proposed estimator. We compare the lower bound of minimax mean integrated squared error (MISE) with the I.I.D. case in Efromovich and Pinsker (1982). We propose two data driven estimators and show their efficiency in a simulation study. Finally, we analyze the M-SISNet survey data using the proposed estimation. All proofs to theorems and corollaries are given in the appendix.

2 Notations

Consider a finite population labeled as . A survey variable is associated with each unit in the finite population. A subset of size is selected from according to some fixed-size sampling design . The first and second order inclusion probabilities from the sampling design are and , respectively. The inverse of the first order inclusion probability defines the sampling weight , .

The inference approach used in this paper for complex surveys is the combined design-model-based approach originated in Hartley and Sielken (1975). This approach accounts for two sources of variability. The first one is from the fact that the finite population is a realization from a superpopulation, that is, the units are considered independent random variables with a common distribution function , whose density function is . The second one is from the complex sampling procedure which leads to a sample . Denote design variables that determine the sampling weights. The sampling design is embedded within a probability space . The expectation and variance operator with respect to the sampling design are denoted by and , respectively. The superpopulation , from which the finite population is realized, is embedded within a probability space . The sample and the design variables are -measurable. The expectation and variance operator with respect to the model are denoted by and , respectively. Assume that, given the design variables , the product space, which couples the model and the design spaces, is . The combined expectation and variance operators are denoted by and , where and .

3 Main Results

Consider a sample drawn from a finite population using some fixed-size sampling design . Our goal is to estimate the hypothetical density function of the superpopulation. Equation (1) implies that can be estimated using the Horvitz-Thompson (HT) estimator for the finite population mean

| (2) |

where is the finite population size and is the sampling weight for unit . The HT estimator is a well known design unbiased estimator (Horvitz and Thompson, 1952). The basis can be Fourier, polynomial, spline, wavelet, or others. Properties of different bases are discussed in Efromovich (2010). We consider the cosine basis throughout the paper, which is defined as . Regarding the compact support for the density, we adopt the argument in Wahba (1981):“ it might be preferable to assume the true density has compact support and to scale the data to interior of .” Analogous to Efromovich (1999), we propose an orthogonal series estimator in the form

| (3) |

where is the HT estimator for the Fourier coefficient as in (2) and is a shrinking coefficient. The sequence of determines the smoothness of the estimator. In Section 4, we consider two choices of and the corresponding data driven estimators, for which only a finite number of is needed. Note that . If is known for all units in the finite population, we can write the population estimator for as

where .

The following theorems and a corollary show properties of our proposed estimator under both design and combined spaces. Theorem 1 considers unbiasedness and consistency under the design space.

Theorem 1

Suppose , as , and . Then, the estimator is design-unbiased and asymptotically design-consistent for , i.e.,

An intuitive way to understand the condition as is to consider Hájek (1964)’s condition: under that and . When , , and hence . The condition is satisfied under that , or under Hájek (1964)’s condition. Note that the condition is satisfied for which is practically plausible. We also note that, when the underlying design is a stratified sampling, we restrict our asymptotic framework by assuming that the number of strata is finite and fixed.

The condition can be easily satisfied by choosing a proper sequence of , which is discussed in Section 4. The asymptotic properties here are for the estimator , which we say an ‘oracle’ estimator for that is assumed constant and known. In Section 4, when is estimated, the estimator becomes , which we say a data driven estimator.

The following theorem shows the asymptotic normality of the proposed estimator under the design space.

Theorem 2

We then show the asymptotic normality of the proposed estimator under the combined inference. Define a Sobolev Class of -fold differentiable densities as = , . Note that for any , is -periodic, is absolute differentiable and .

Theorem 3

Suppose that and all assumptions in Theorem 2 hold. Then,

where and .

The following corollary is a direct result of using Theorem 3 and Efromovich and Pinsker (1982). It shows the lower bound of the minimax MISE for the proposed estimator under the Sobolev class.

Corollary 1

Let and be the estimator in Theorem 3. The lower bound of the minimax MISE, under the combined inference approach, is given by:

where and .

Remark that this lower bound is of the same form as the I.I.D. case in Efromovich and Pinsker (1982), but with instead of .

4 Data Driven Estimators

The choice of shrinking coefficients is not unique. To get a proper data driven estimator, we start with the oracle estimator (3), and then obtain by minimizing the MISE for the oracle estimator. Here, we propose two estimators: a truncated estimator and a smoothed truncated estimator, mimicking those in the I.I.D. case.

The truncated estimator, denoted by , is an estimator with for , and for . Alternatively we can write . Then, only the truncation parameter needs to be estimated. Notice that the MISE of this estimator is

Since is fixed and an unbiased estimator for is , a data-driven estimate for can be obtained from

where is the plug-in estimator of . That is, the estimator of the shrinking coefficients can be written as . In practice, the solution is obtained through a numerical search. Efromovich (1999) suggests to set the upper bound for to be for the search. Theoretically, the minimum of the MISE can be approximated in the following corollary.

Corollary 2

Let , . The MISE of is minimized when

and the minimum is approximately

where , , and is a constant.

One possible modification for is to shrink each Fourier coefficient toward zero. We call this estimator the smoothed truncated estimator, denoted by . It is constructed similarly as the truncated estimator, with the first Fourier coefficients shrunk by multiplying the optimal smoothing coefficients , obtained from the proof of Corollary 1. Mathematically, , where is a direct plug-in estimator for .

A potential problem of the nonparametric density estimation is that the estimator may not be a valid density function. A simple modification is to define the -projection of (or ) onto a class of non-negative densities, , where the normalizing constant is to make integrate to . It has been proved that the constant always exists and is unique (Glad et al., 2003).

5 Simulation

We compared our proposed estimators with the series estimator that ignores the finite population and sampling designs, through a Monte Carlo simulation study. We considered estimating density functions for four sampling designs: (1) the simple random sample without replacement (SRSWOR), (2) the Poisson sampling, (3) the unequal probability systematic sampling with random start, and (4) the stratified sampling. Note that the Poisson sampling and the unequal probability systematic sampling both have a random size and hence violates our assumption of fixed size sampling.

-

1.

For the SRSWOR, we considered two superpopulations: the standard normal distribution and a mixture normal distribution .

-

2.

For the Poisson sampling, we considered the same two superpopulations as in (1). We specified the expected sample size for the Poisson sampling to be , with inclusion probabilities .

-

3.

For the unequal probability systematic sampling, we considered the same two superpopulations as in (1). We specified the inclusion probabilities as .

-

4.

For the stratified sampling, we considered two superpopulations: a two-component mixture normal and a three-component mixture normal . We designed two strata for the two-component mixture and three strata for the three-component mixture. A proportional stratified sampling is used.

For all cases, we considered a finite population of size drawn from each of the superpopulations. We repeated drawing the finite population for times. For each of the finite population, we drew samples according to the sampling design, with increasing sample sizes: and . The replication number for each finite population is . The performance of estimators is measured by a Monte Carlo approximation of the MISE:

The results of the simulation study are shown in Table 1. In general, the I.I.D. series estimator, which ignores the sampling design, performs the worst in nearly all cases. It confirms the necessity of incorporating sampling weights into the series estimator for a complex survey. Moreover, the improvement of the proposed estimators is even bigger in the mixture case than the standard normal case. Lastly, the difference between the smoothed truncated estimator and the truncated estimator is quite small.

6 Oklahoma M-SISNet Survey

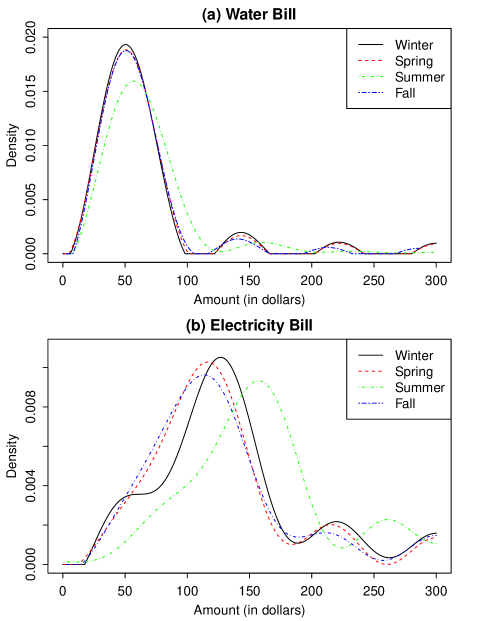

The Oklahoma Weather, Society and Government Survey conducted by Meso-Scale Integrated Sociogeographic Network (M-SISNet) measures Oklahomans’ perceptions of weather in the state, their views on government policies and societal issues and their use of water and energy. The survey is routinely conduced at the end of each season. Until the end of 2016, 12 waves of survey data have been collected. It is desired that estimates can be obtained without constantly pulling out the original data. The sampling design has two separated phases. In Phase I, a simple random sample of size is selected from statewide households. In Phase II, a stratified oversample is selected from five special study areas: Payne County, Oklahoma City County, Kiamichi County, Washita County and Canadian County. In each stratum, the sample size is fixed to be . The second phase can be viewed as a stratified sampling over the entire state with six strata: and , where the sixth stratum contains households not in the five special study areas. This design with oversampling is not a typical fixed-size complex survey. The first-order inclusion probabilities are approximately , for and . Note that for units not in the five areas, this inclusion probability is simply . We presents OSDEs for two continuous variables for illustration: the monthly electricity bill and the monthly water bill. Figure 1 shows OSDEs of the two variables for all seasons in 2015. The upper panel of Figure 1 shows the water bill distribution and the lower panel shows the electricity bill distribution. We clearly see the difference between four seasons for the consumption of water and electricity. For example, the summer electricity bill is much higher than other seasons. Notice that those densities appear to be multimodal, while our simulation studies suggested that our proposed estimators enjoy a remarkable improvement in cases with mixture densities.

7 Conclusion

In this paper, we propose a Horvitz-Thompson type orthogonal series estimator for density estimation under complex survey designs. The estimator is shown to possess certain asymptotic properties and outperforms the ordinary orthogonal series estimator without sampling weights. It is of practical use when an exact nonparametric estimator needs to be released without releasing the original data. In the future, it is worth investigating the orthogonal series estimation under survey designs when auxiliary variables are present or nonresponse occurs.

Acknowledgement

This research is partially supported by National Science Foundation under Grant No. OIA-1301789. We thank an associate editor and a referee for their constructive comments.

Appendix

Proof of Theorem 1

Proof. We first show that is design-unbiased:

It remains to show that is asymptotically design-consistent, that is, the design-variance of approaches zero in the limit. We need the simple fact that

Then, we have

and

where and for every .

Hence, as .

Proof of Theorem 2

Proof. By the definition of and , we have

and

Also, from the proof of Theorem 1, we have

Therefore, by the Lindeberg-Lvy central limit theorem, we have

| (4) |

It remains to show that is consistent for under design, or equivalently,

| (5) |

Condition (5) can be proved by using the facts that is design unbiased and as .

Proof of Theorem 3

Proof. Since is the standard OSDE from an I.I.D. sample which is the finite population, then

| (6) |

The asymptotic distribution of the I.I.D. OSDE under Sobolev class is obtained from Efromovich (1999), Chapter 7. Also,

| (7) | |||||

Next, we calculate the variance of by using Theorem 1:

| (8) | |||||

Then, we evaluate and separately. Based on a standard result in the I.I.D. case, we have

| (9) |

and

| (10) | |||||

Then, plug equations (9) and (10) into (8), we have

| (11) |

Hence, plug (11) into (7) we can get the variance of under the combined inference approach.

Finally, apply Theorem 5.1 in Bleuer and Kratina (1999), Theorem 3 is proved.

Proof of Corollary 1

Proof. The proof is similar to Efromovich and Pinsker (1982). We sketch the steps as follows. We first evaluate the linear minimax MISE for the functions in the Sobolev class defined above. That is, we optimize ’s that minimize . Notice that implying that is an unbiased estimator of . Therefore,

| (12) | |||||

A straightforward calculation yields that

| (13) |

| (14) | |||||

where is of the form (11). Plug (11) into (14), and use the Lagrange multiplier to show that the maximum of (6) is attained at

| (15) |

where is determined by the constraint . Plug equation (15) back to (14), we obtain

Pinsker (1980) shows that for Sobolev ball , the linear minimax risk is asymptotically equal to the minimax risk, that is, . Therefore Corollary 1 is proved.

Proof of Corollary 2

References

- (1)

- Bellhouse and Stafford (1999) Bellhouse, D. and Stafford, J. (1999), ‘Density estimation from complex surveys’, Statistica Sinica 9, 407–424.

- Bleuer and Kratina (1999) Bleuer, S. and Kratina, I. (1999), ‘On the two-phase framework for joint model and design-based inference’, The Annals of Statistics 33, 2789–2810.

- Breunig (2001) Breunig, R. (2001), ‘Density estimation for clustered data’, Econometric Reviews 20, 353–367.

- Breunig (2008) Breunig, R. (2008), ‘Nonparametric density estimation for stratified samples’, Statistics and Probability Letters 78, 2194–2200.

- Buskirk (1999) Buskirk, T. (1999), Using nonparametric methods for density estimation with complex survey data, Technical report, PhD thesis, Department of Mathematics, Arizona State University.

- Buskirk and Lohr (2005) Buskirk, T. and Lohr, S. (2005), ‘Asymptotic properties of kernel density estimation with complex survey data’, Journal of Statistical Planning and Inference 128, 165–190.

- Donoho et al. (1996) Donoho, D., Johnstone, I., Kerkyacharian, G. and Picard, D. (1996), ‘Density estimation by wavelet thresholding’, Annals of Statistics 24, 508–539.

- Efromovich (1996) Efromovich, S. (1996), ‘Adaptive orthogonal series density estimation for small samples’, Computational Statistics and Data Analysis 22, 599–617.

- Efromovich (1999) Efromovich, S. (1999), Nonparametric Curve Estimation: Methods, Theorey and Applications, New York: Springer.

- Efromovich (2010) Efromovich, S. (2010), ‘Orthogonal series density estimation’, WIREs Comp Stat 2, 467–476.

- Efromovich and Pinsker (1982) Efromovich, S. and Pinsker, M. (1982), ‘Estimation of square-integrable probability density of a random variable’, Problems of Information Transmission 18, 19–38.

- Glad et al. (2003) Glad, I., Hjort, N. and Ushakov, N. (2003), ‘Correction of density estimators that are not densities’, Scandinavian Journal of Statistics 30, 415–427.

- Hájek (1964) Hájek, J. (1964), ‘Asymptotic theory of rejective sampling with varying probabilities from a finite population’, The Annals of Mathematical Statistics 35(4), 1491–1523.

- Hartley and Sielken (1975) Hartley, H. and Sielken, R. (1975), ‘A super-population viewpoint for finite population sampling’, Biometrics 31, 411–422.

- Horvitz and Thompson (1952) Horvitz, D. G. and Thompson, D. J. (1952), ‘A generalization of sampling without replacement from a finite universe’, Journal of the American Statistical Association 47(260), 663–685.

- Pinsker (1980) Pinsker, M. (1980), ‘Optimal filtration of square-integrable signals in Gaussian noise’, Problems Inform. Transmission 16, 53–68.

- Tarter and Lock (1993) Tarter, M. and Lock, M. (1993), Model-Free Curve Estimation, New York: Chapman and Hall.

- Wahba (1981) Wahba, G. (1981), ‘Data-based optimal smoothing of orthogonal series density estimates’, The Annals of Statistics 9, 146–156.

- Walter (1994) Walter, G. (1994), Wavelets and other Orthogonal Systems with Applications, London: CRC Press.

| SRSWOR | ||||||

|---|---|---|---|---|---|---|

| Standard Normal | Mixture Normal | |||||

| n | Truncated | Smoothed | I.I.D. | Truncated | Smoothed | I.I.D. |

| 20 | 0.0232 | 0.0220 | 0.0290 | 0.0498 | 0.0480 | 0.0535 |

| 40 | 0.0150 | 0.0140 | 0.0157 | 0.0311 | 0.0318 | 0.0388 |

| 60 | 0.0116 | 0.0109 | 0.0121 | 0.0226 | 0.0234 | 0.0335 |

| 80 | 0.0094 | 0.0089 | 0.0100 | 0.0173 | 0.0180 | 0.0219 |

| 100 | 0.0064 | 0.0067 | 0.0071 | 0.0134 | 0.0139 | 0.0139 |

| Poisson Sampling | ||||||

| Standard Normal | Mixture Normal | |||||

| n | Truncated | Smoothed | I.I.D. | Truncated | Smoothed | I.I.D. |

| 20 | 0.0328 | 0.0317 | 0.0210 | 0.0346 | 0.0343 | 0.0437 |

| 40 | 0.0158 | 0.0153 | 0.0157 | 0.0193 | 0.0194 | 0.0341 |

| 60 | 0.0123 | 0.0117 | 0.0136 | 0.0158 | 0.0159 | 0.0295 |

| 80 | 0.0096 | 0.0091 | 0.0120 | 0.0133 | 0.0135 | 0.0262 |

| 100 | 0.0076 | 0.0071 | 0.0108 | 0.0115 | 0.0117 | 0.0234 |

| Unequal Probability Systematic Sampling | ||||||

| Standard Normal | Mixture Normal | |||||

| n | Truncated | Smoothed | I.I.D. | Truncated | Smoothed | I.I.D. |

| 20 | 0.0277 | 0.0268 | 0.0218 | 0.0311 | 0.0309 | 0.0419 |

| 40 | 0.0152 | 0.0147 | 0.0165 | 0.0183 | 0.0185 | 0.0326 |

| 60 | 0.0125 | 0.0118 | 0.0139 | 0.0140 | 0.0143 | 0.0290 |

| 80 | 0.0089 | 0.0083 | 0.0128 | 0.0129 | 0.0132 | 0.0275 |

| 100 | 0.0058 | 0.0054 | 0.0108 | 0.0125 | 0.0127 | 0.0226 |

| Stratified Sampling | ||||||

| Two Strata | Three Strata | |||||

| n | Truncated | Smoothed | I.I.D. | Truncated | Smoothed | I.I.D. |

| 20 | 0.0415 | 0.0409 | 0.0739 | 0.2847 | 0.2826 | 0.3106 |

| 40 | 0.0231 | 0.0230 | 0.0688 | 0.2731 | 0.2718 | 0.3309 |

| 60 | 0.0181 | 0.0180 | 0.0672 | 0.0426 | 0.0419 | 0.1132 |

| 80 | 0.0142 | 0.0142 | 0.0675 | 0.0412 | 0.0406 | 0.1175 |

| 100 | 0.0128 | 0.0129 | 0.0601 | 0.0381 | 0.0395 | 0.1128 |