Evaluation of the rate of convergence in the PIA

Abstract.

Folklore says that Howard’s Policy Improvement Algorithm converges extraordinarily fast, even for controlled diffusion settings.

In a previous paper, we proved that approximations of the solution of a particular parabolic partial differential equation obtained via the policy improvement algorithm show a quadratic local convergence.

In this paper, we show that we obtain the same rate of convergence of the algorithm in a more general setup. This provides some explanation as to why the algorithm converges fast.

We provide an example by solving a semilinear elliptic partial differential equation numerically by applying the algorithm and check how the approximations converge to the analytic solution.

Key words and phrases:

Policy improvement algorithm; Stochastic control; Elliptic partial differential equations; Semilinear partial differential equations1. Introduction

In [13], we introduced a new model for pricing derivatives products when we have a position concentration in the over-the-counter market. The model requires us to solve a nonlinear partial differential equation (PDE) and this may prevent traders from using it in practice due to possible difficulties in implementing a solution in their pricing models. To overcome this difficulty, we used the policy improvement algorithm (PIA) to enable us to approximate the nonlinear PDE by a series of linear ones parameterized by a control. The solutions of the linear PDEs converge to that of the original semilinear PDE as we iteratively solve the linear PDEs under the algorithm. Since their stochastic volatility pricing models can solve linear PDEs (as in Heston’s model), the traders can now implement the new model. We further showed that the PIA approximated solutions show quadratic local convergence (QLC) to the analytic solution. This provides an explanation of why the convergence happens so fast.

The natural question to ask is how general this QLC is in the PIA framework. In this paper, we consider a general infinite time horizon problem and calculate the rate of convergence of the PIA-derived approximations to that of the corresponding semilinear elliptic PDE. We give three conditions which enable us to show the QLC. These assumptions are indeed satisfied by the problem considered in [13]. We describe in Remark 2 how some of these assumptions can be relaxed.

The rest of the paper is organized as follows: Section 2 briefly explains the setup. In Section 3, we state the main theorem about Quadratic Local Convergence of the approximated solutions to the semilinear PDE. We give a numerical example in Section 4 and give some concluding questions in Section 5.

2. Setup

We briefly explain our setup.

Let be a filtered probability space. We assume that is a simply connected, convex, and bounded subset of that has boundary. We define

| (2.1) |

for any continuous process .

For a control and starting point , we wish to define the controlled process by

| (2.2) |

where and are measurable mappings, is an -dimensional Wiener process and takes values in .

For any define , the set of admissible control at , as

| (2.3) | ||||

A measurable function is a Markov policy if for every and there exists a process that is unique in law and satisfies the following:

| (2.4) | ||||

We define the payoff function for any admissible as

| (2.5) | ||||

where is some positive constant and and . We assume that is with respect to and is continuous. The problem is to find the value function defined as

| (2.6) |

For any Markov policy that is Lipschitz continuous on , define by

| (2.7) |

where is the Hessian of .

From [8], satisfies the PDE

| (2.8) |

Starting from a Markov policy , the PIA defines successive controls by the recursion

| (2.9) |

Note finally that, we assume that such that the differential operator is uniformly elliptic, i.e.,

| (2.10) |

3. Main Results

We make the following assumptions in this section.

Assumption 1.

is in the form of for some constant matrix and dimensional vector .

Assumption 2.

is independent of .

Assumption 3.

is strictly and uniformly concave in , i.e. such that for all , where represents the Hessian of with respect to .

With these assumptions, we show the following:

Theorem 3.1.

| (3.1) |

Remark 1.

Remark 2.

Suppose that , the action space (the value space for ) is not . We may replace it by its image under , provided we simultaneously replace by given by

since we wish to maximise . Suppose that this image is . By allowing relaxed controls (see for example [1]) we can replace this by , the closure of the convex hull of . This will simultaneously replace by , the smallest concave majorant of . If is strictly uniformly concave and is an affine set in then we recover Assumptions 1 and 3.

As we shall see, the proof of Theorem 3.1 relies heavily on Taylor’s theorem and the disappearance of at its maximum. So, if is a compact subset of then we hit a problem when the maximizer lies on the boundary of .

We should still be able to obtain good approximations to with QLC by extending the action space to and extending to in such a way that in , always takes its maximum, in the interior of and .

Remark 3.

We considered the elliptic case, but the parabolic case follows exactly in the same fashion. We have the following theorem:

Theorem 3.2.

This is a generalization of Proposition 5.3 in [13].

The proof of Theorem 3.1 is deferred to the Appendix.

4. Numerical Example

We apply the PIA in solving numerically a semilinear elliptic PDE.

We take to be with its corners smoothed in a fashion (this is needed to apply the boundary estimate in Theorem 3.1). The SDEs we consider are

| (4.1) |

where and are 1-dimensional Wiener processes and .

Thus

| (4.2) |

We take to be

| (4.3) |

We define as in (2.5) with on .

Then, satisfies the elliptic PDE:

| (4.4) | ||||

where is determined by

| (4.5) |

Note that if converges, the limit function satisfies a semilinear elliptic PDE

| (4.6) | ||||

The variables we use are in Table 1.

| parameter | value |

|---|---|

| 0.03 | |

| 2.0 | |

| 0.2 | |

| 2.0 | |

| 0.50 | |

| 2.0 | |

| 0.50 | |

| ToleranceLevel1 | 0.00001 |

| ToleranceLevel2 | 0.001 |

| discretization nodes | 100 |

We use the explicit finite difference method (FDM) to see the convergence starting at with the boundary condition . We discretize (4.4) and obtain

| (4.7) | ||||

where and represent coordinates of the mesh points, and are corresponding values at the mesh points, and and are corresponding mesh size. We therefore can write (4.7) in the form

| (4.8) | ||||

We use the Gauss-Seidel method [14] together with the PIA to solve (4.6). The procedure is as follows:

The method converges if the diagonal terms of the matrix are greater than the sum of the absolute values of the off-diagonal terms (Theorem 4.4.5, [2]). That is, on (4.8), the method converges if

| (4.11) |

With small enough, the condition of the cited theorem is satisfied with the parameters we have chosen.

To compare the calculation load, we also numerically solved the corresponding linear PDE

| (4.12) |

Table 2 shows the numerical results in both linear and semilinear cases. For the linear case (4.12), we used Gauss-Seidel method with the tolerance level equal to ToleranceLevel1 in Table 1. We see that the linear and semilinear cases have similar order in terms of the number of calculations to approximate to the specified tolerance level.

| Problem Type | Method | # of calculations |

|---|---|---|

| Linear | FDM (Gauss-Seidel) | 24,541,704 |

| Semilinear | PIA & Gauss-Seidel | 34,372,107 |

Table 3 shows the result in more detail.

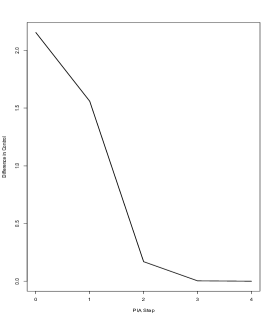

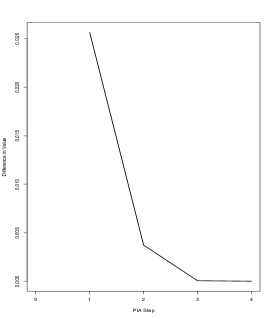

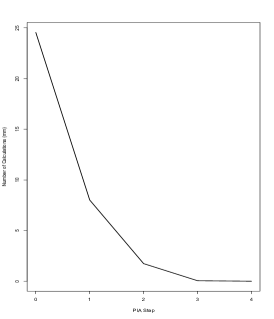

| PIA | Max Difference in | Max Difference in | # of | Calculation |

|---|---|---|---|---|

| steps | calculations | time | ||

| 0 | 2.15455038 | 24,541,704 | 0:16 | |

| 1 | 1.55932909 | 0.02563695 | 8,017,218 | 0:05 |

| 2 | 0.16986263 | 0.00372773 | 1,744,578 | 0:01 |

| 3 | 0.00400477 | 0.00006031 | 58,806 | 0:00 |

| 4 | 0.00066038 | 0.00000995 | 9,801 | 0:00 |

Table 3 shows that the first step in the PIA already decreases the number of calculation to get the convergence in the Gauss-Seidel method. The data is plotted in Figure 1.

Remark 4.

We did try applying the FDM directly to the differential equation (4.6), but could not get the convergence.

5. Conclusions

We have shown that the PIA has the QLC property in a fairly general framework. The natural questions to ask are

-

1.

Can we show QLC under weaker conditions?

and

-

2.

Can we show some convergence rate outside the “local quadratic region” (see Remark 1)?

References

- [1] D. Andersson and B. Djehiche, A maximum principle for relaxed stochastic control of linear SDEs with application to bond portfolio optimization, Math. Meth. of OR, 72 (2010), pp. 273-310.

- [2] E. K. Blum, Numerical Analysis and Computation Theory and Practice, Addison-Wesley Publishing Company, Reading, MA, 1972.

- [3] L. C. Evans, Partial Differential Equations, AMS, Providence, RI, 2010.

- [4] W. Forst and D. Hoffmann, Optimization - Theory and Practice, Springer, New York, NY, 2010.

- [5] A. Friedman, Partial Differential Equations of Parabolic Type, Princeton-Hall, Inc., Englewood Cliffs, NJ, 1964.

- [6] D. Gilbarg and N. S. Trudinger, Elliptic Partial Differential Equations of Second Order, Springer, Berlin, 2001.

- [7] S. D. Jacka and A. Mijatović, On the policy improvement algorithm in continuous time, Stochastics, 89-1 (2017), pp. 348-359.

- [8] S. D. Jacka, A. Mijatović, and D. Širaj, Policy improvement algorithm for controlled multidimensional diffusion processes, forthcoming.

- [9] S. D. Jacka, A. Mijatović, and D. Širaj, Policy improvement algorithm for continuous finite horizon problem, forthcoming.

- [10] C. T. Kelley, Iterative Methods for Linear and Nonlinear Equations, SIAM, Philadelphia, PA, 1995.

- [11] C. T. Kelley, Solving Nonlinear Equations with Newton’s Method, SIAM, Philadelphia, PA, 2003.

- [12] O. A. Ladyzhenskaya and N. N. Ural’tseva, Linear and Quasilinear Elliptic Equations, Academic Press, New York, NY, 1968.

- [13] J. Maeda and S. D. Jacka, A market driver volatility model via policy improvement algorithm, arXiv: 1612.00780.

- [14] J. M. Ortega and W. C. Rheinboldt, Iterative Solution of Nonlinear Equations in Several Variables, Academic Press, New York, NY, 1970.

- [15] G. D. Smith, Numerical Solution of Partial Differential Equations: Finite Difference Methods, Clarendon Press, Oxford, 1985.

- [16] D. Tavella and C. Randall, Pricing Financial Instruments: The Finite Difference Method, John Wiley & Sons, Inc., New York, NY, 2000.

Appendix

A. Proof of Theorem 3.1

satisfies

| (A.1) |

and since Assumption 2 is that does not depend on , is determined by the iteration:

| (A.2) | ||||

From Assumption 1, we can write

| (A.3) |

It then follows from (A.2) that

| (A.4) |

Subtracting (A.4) with from the same equation with , and setting , we obtain

| (A.5) |

Using the Mean Value Theorem, we can then write (A.5) as

| (A.6) |

for some .

It follows from Assumption 3 that is negative definite, hence invertible, so we can rewrite (A.6) as

| (A.7) |

Comparing (A.1) for and ,

| (A.8) |

and subtracting, we get

| (A.9) | ||||

We define as

| (A.10) |

then we obtain, from Taylor’s theorem,

| (A.11) | ||||

| (A.12) |

and then we can rewrite (A.9) as

| (A.13) |

We have the same Dirichlet condition on the boundary of the domain for each , therefore on . From Schauder’s estimate on second order linear elliptic partial differential equations [6, pg. 108], we conclude that

| (A.14) |

where the constant depends only on the domain , the ellipticity constant , and the bounds on the coefficients of the elliptic differential operator.