∎

Guanajuato, Mexico

jluis.garmendia@cimat.mx 33institutetext: Kazutoshi Yamazaki 44institutetext: Kansai University

Osaka, Japan

kyamazak@kansai-u.ac.jp 55institutetext: Xiang Yu (Corresponding author) 66institutetext: The Hong Kong Polytechnic University

Kowloon, Hong Kong

xiang.yu@polyu.edu.hk

On the Bail-Out Optimal Dividend Problem

Abstract

This paper studies the optimal dividend problem with capital injection under the constraint that the cumulative dividend strategy is absolutely continuous. We consider an open problem of the general spectrally negative case and derive the optimal solution explicitly using the fluctuation identities of the refracted-reflected Lévy process. The optimal strategy as well as the value function are concisely written in terms of the scale function. Numerical results are also provided to confirm the analytical conclusions.

Keywords:

stochastic control scale functions refracted-reflected Lévy processes bail-out dividend problemMSC:

60G51 93E20 49J401 Introduction

In the bail-out model of de Finetti’s optimal dividend problem, one wants to maximize the total expected dividends minus the costs of capital injection under the constraint that the surplus must be kept non-negative uniformly in time. Typically, a spectrally negative Lévy process (a Lévy process with only downward jumps) is used to model the underlying surplus process of an insurance company that increases because of premiums and decreases by insurance payments. Avram et al. 1. showed that it is optimal to reflect from below at zero and also from above at a suitably chosen threshold.

We investigate an extension with the absolutely continuous constraint on dividend strategies. To be precise, the cumulative dividend process must be absolutely continuous with respect to the Lebesgue measure with its density bounded by a given constant. This problem (without bail-out) has been previously considered by 2. and 3. in the diffusive case, and 4. for the case of Crámer-Lundberg processes with exponential jumps. In the classical setting, the set of admissible strategies is too general and counterintuitive in the context of insurance. Consequently, there have been several attempts to restrict the solution to more realistic strategies. The absolutely continuous condition is one way of achieving this goal without losing analytical tractability.

Regarding the version with both bail-out and the absolutely continuous condition, the dual case (the spectrally positive Lévy case) has recently been solved by 5. . In this paper, we further consider the spectrally negative case for the underlying process. This can also be seen as the bail-out version of 6. , where they incorporated the absolutely continuous constraint, however, without capital injections.

Our ultimate aim is to verify the conjecture on the optimality of a refraction-reflection strategy that reflects the surplus from below at zero in the classical sense and refracts the process (decreases the drift) at a suitably chosen threshold. The resulting controlled surplus process becomes the so-called refracted-reflected Lévy process recently studied in 7. . Indeed, many interesting probabilistic properties of the refracted-reflected Lévy process have been developed in 7. . However, as an important application to the optimal dividend problem with capital injection, it is still an open problem whether the optimal control for the spectrally negative case fits this type of refraction-reflection. This paper fills the gap and provides the closed-form choice of the threshold.

As is commonly used in the related literature, we adopt the scale function and the fluctuation identities so as to follow efficiently the “guess-and-verify” procedure described below.

-

(1)

By focusing on the set of refraction-reflection strategies, we select a judicious candidate strategy via the smooth fit principle. In particular, we choose the threshold value such that the corresponding net present value (NPV) becomes continuously (resp. twice continuously) differentiable at the threshold for the case of bounded (resp. unbounded) variation.

-

(2)

The optimality of the selected strategy is then confirmed by verifying the variational inequalities that require the computation of the generators and certain slope conditions of the value functions.

In general, in the optimal dividend problem and its extensions, the verification of optimality is significantly more challenging for the spectrally negative case than the dual case. The difficulty typically lies in the required proof of the properties of the candidate value function above the barrier/threshold that separates the waiting and controlling regions. Intuitively speaking, this is difficult because, with negative jumps, the surplus can jump below from the controlling region to the waiting region as well as directly to the reflection region below the zero boundary, where the forms of the value function change. It is demonstrated in the literature that the optimality can fail by the choice of the Lévy measure (see, e.g., 6. assumes the completely monotone Lévy density). However, in the dual model, it is usually not necessary to assume any property on the Lévy measure (see 8. ; 9. ; 10. ; 11. ).

Mathematically speaking, in our problem, the major challenge is to show the slope condition above the selected threshold such that the slope is bounded uniformly by . Nonetheless, we show that the optimality holds for a general spectrally negative Lévy case. To this end, we use our observation that the slope of the candidate value function coincides with the Laplace transform of the ruin time of the refracted Lévy process of 12. , which is monotone in the starting value. Other required computations such as generators and the slopes below the threshold can be performed efficiently by taking advantage of the analytical properties of the scale function.

The rest of the paper is organized as follows. In Section 2, we review the spectrally negative Lévy process and give the precise formulation of the bail-out optimal dividend control problem with the absolutely continuous condition. Section 3 defines the refraction-reflection strategy and formulates the corresponding NPV of dividends minus capital injection using the scale function. Section 4 provides the conjectured candidate threshold and Section 5 proves the optimality of the selected strategy. Some numerical examples are presented in Section 6. At last, we give our conclusions in Section 7.

2 Preliminaries

2.1 Spectrally Negative Lévy Processes

In this paper, we consider a spectrally negative Lévy process . For , we denote the law of when it starts at by and refer to it as instead of for convenience. and are the associated expectation operators.

Its Laplace exponent is defined by for with the Lévy-Khintchine formula

where , , and is a measure on called the Lévy measure of that satisfies .

It is well-known that has paths of bounded variation if and only if and is finite. In this case, , where and is a driftless subordinator. Note that necessarily , as we have ruled out the case that has monotone paths. Its Laplace exponent is given by for .

2.2 Bail-Out Optimal Dividend with the Absolutely Continuous Condition

A strategy is a pair of nondecreasing, right-continuous, and adapted processes (with respect to the filtration generated by ) starting at zero, where is the cumulative amount of dividends and is that of the injected capital. With , and, , , it is required that a.s. uniformly in . In addition, with fixed, is required to be absolutely continuous with respect to the Lebesgue measure of the form , , with restricted to take values in uniformly in time. As for , it is assumed that , a.s.

Assuming that is the cost per unit injected capital and is the discount factor, the expected NPV of dividends minus the costs of capital injection under a strategy becomes

The corresponding stochastic control problem is defined by

| (1) |

where is the set of all admissible strategies that satisfy the constraints described above.

Throughout the paper, to exclude the trivial case, we consider the next assumption.

Assumption 1

We assume that .

Moreover, as being commonly imposed in the literature (see 6. ), the next assumption is made so that the process does not have monotone paths.

Assumption 2

For the case of bounded variation, let .

3 Refraction-Reflection Strategies

Our objective is to show the optimality of the refraction-reflection strategy , with a suitable refraction level . Namely, dividends are paid at the maximal rate whenever the surplus process is above the pre-specified threshold while it is pushed upward by capital injection whenever it attempts to downcross zero. The resulting surplus process

becomes the standard refracted-reflected Lévy process of 7. .

In terms of the optimal control theory, we recognize that the candidate dividend strategy is of the bang-bang type, i.e., dividends should either be paid out at the maximum rate or at the rate . On the other hand, the capital injection strategy, which is the reflection control, fits into the singular control framework. To wit, we can explicitly write the described cumulative dividend control as , and for the case of bounded variation we can write the candidate capital injection . Here, we define , , for any càdlàg process . For a formal construction of this process, we refer the reader to 7. .

Clearly, each aforementioned refraction-reflection strategy is admissible for any . We denote the corresponding expected NPV by

| (2) |

In order to express (2), we apply the fluctuation identities. Following the same notations as in 12. , we call and the scale functions of and , respectively. These are the mappings from to that take the value zero on the negative half-line, while on the positive half-line, they are strictly increasing functions that are defined by their Laplace transforms

| (3) | ||||

| (4) |

Here , , is the Laplace exponent for and

We also define, for ,

Noting that for , we have

| (5) |

Analogously, we define , and for . From computations in 7. , we already know

| (6) | ||||

| (7) |

Remark 1

Lemma 1

For , and , we have

Proof

4 Selection of the Candidate Threshold

We shall choose the candidate threshold so that the corresponding expected NPV can be smooth at . Lemma 1 and integration by parts imply that

By differentiating this, we have

| (9) |

which is continuous for .

For the case of bounded variation, where (see Remark 1(ii)), it is straightforward to see that is continuously differentiable at if and only if .

For the case of unbounded variation, where , by differentiating (4), we have, for , that

which is continuous for and hence .

These observations, together with the smoothness of the scale function on as in Remark 1, are summarized as follows.

Lemma 2

Suppose that there exists such that . Then, is continuously (resp. twice continuously) differentiable on when is of bounded (resp. unbounded) variation.

Remark 4 (Continuity/smoothness at zero)

(i) By Lemma 1, we have that is continuous at zero for .

(ii) If , (10) gives for the case of unbounded variation.

Let us define our candidate threshold by

| (13) |

with the convention that .

Lemma 3

We have if and only if is of bounded variation and

| (14) |

Proof

To continue, we can further show that .

Lemma 4

(i) Define . Then, for ,

| (15) |

where and is the refracted Lévy process of 12. , which is the unique strong solution to the stochastic differential equation

, for .

(ii)

We have .

Proof

(i) We have, by (12), that

| (16) | ||||

On the other hand, by integration by parts,

| (17) | ||||

Therefore, due to (16) and (17), we obtain the first equality of (4). The second equality of (4) holds by Theorem 5 (ii) of 12. .

(ii) For , because is strictly increasing on , we get

Using the fact that and hence that is dominated from below by the down-crossing time of , we have the convergence as . This and (4) imply that . Hence, by the positivity of , must be negative for a sufficiently large . Consequently, it follows that . ∎

5 Verification of Optimality

In this section, we provide a rigorous verification argument for the choice of defined in such that the value function of the stochastic control problem can be achieved.

With the selected barrier , by Lemma 1, our value function becomes

| (18) | ||||

Here, for the case , because , by (12) and (4), we derive that

| (19) |

For the case , is already given in Remark 2.

Our goal is to prove the main result of this paper given below.

Theorem 5.1

The strategy is optimal and the value function of the stochastic control problem is given by .

Let be the infinitesimal generator associated with the process applied to a (resp. ) function for the case where is of bounded (resp. unbounded) variation, i.e., for ,

Further, let be that of . We have .

To show the optimality, it suffices to verify variational inequalities. The proof of the next lemma is omitted as it is essentially the same as the spectrally positive case in Lemma 4.2 of 5. . Here we slightly relax the assumption on the smoothness at zero, which can be achieved by applying the Meyer-Itô formula as in Theorem 4.71 of 15. . We refer to 1. ; 6. ; 16. ; 17. for other stochastic control problems and verification lemmas with spectrally one-sided Lévy processes.

Lemma 5 (Verification lemma)

Suppose such that is sufficiently smooth on , continuous on , and, for the case of unbounded variation, continuously differentiable at zero. In addition, we assume that

| (20) | ||||

Then, for all , and hence, is an optimal strategy.

We shall first compute the generator parts.

Lemma 6

Fix .

(i) If , we have for .

(ii) We have for .

Proof

(i) For , Theorem 2.1 in 8. leads to

Lemma 7

For the threshold defined by , we have for , and for .

Proof

Step (i): Suppose . By (4) and (19), we have

| (21) |

where the second equality holds by the second equality of (19), and the last equality holds by Theorem 5 (ii) in 12. . Thanks to (5), we deduce that and is non-increasing for . This and implied by Remark 3 complete the proof.

Proof (of Theorem 5.1)

Remark 6

Regardless of the negative jumps of , our conclusion interestingly indicates that our conjectured threshold strategy is still the optimal strategy. However, as the term appears in the value function, the negative jumps clearly have direct impacts on the optimal solution.

Another important impact of the jumps can be seen in the bounded variation case, where the optimal threshold can be , which implies that it is optimal to always pay dividends. This outcome does not occur in the classical Brownian motion model.

6 Numerical Examples

We conclude this paper with a sequence of numerical experiments on the underlying process modeled by the spectrally negative Lévy process with phase-type jumps of the form that , for . Here, is a standard Brownian motion, is a Poisson process with arrival rate , and is an i.i.d. sequence of phase-type random variables that approximate the Weibull distribution with shape parameter and scale parameter (see 16. for the parameters of the phase-type distribution and also 20. for the accuracy of approximation). The processes , , and are assumed to be mutually independent. We refer the reader to 14. and 20. for the forms of the corresponding scale functions. We consider Case 1 (unbounded variation) with and and Case 2 (bounded variation) with and . For other parameters, let us set , , and unless stated otherwise.

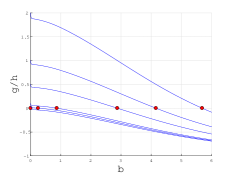

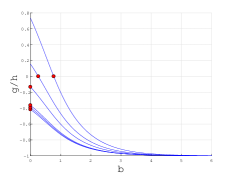

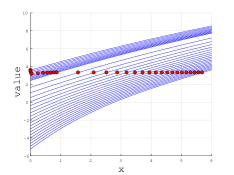

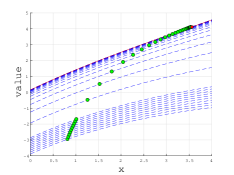

Recall that the optimal threshold is given by (13). In Figure 1, we plot the function (recall that is uniformly positive) for various values of for Cases 1 and 2. For the case (and hence ), we have . Otherwise, is monotonically decreasing and becomes the value at which (and ) vanish. As observed in Lemma 3, for Case 1 (unbounded variation), for any value of while in Case 2 (bounded variation case), if is sufficiently close to . In order to confirm the optimality of the selected threshold strategy , we plot, as shown in Figure 2 (for ), the value function together with for . For Case 1, we have ; while for Case 2, we have . It is illustrated in the figure that satisfactorily dominates uniformly in .

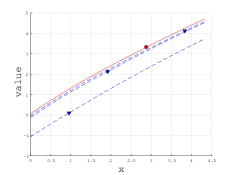

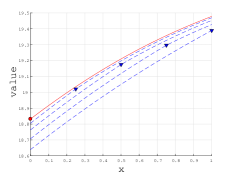

In Figure 3, we present the sensitivity of the optimal solutions with respect to parameters and focusing on Case 1. On the left panel, we plot for ranging from to . The graph indicates that the value function decreases in uniformly in and that the optimal threshold increases as increases. On the right panel, we show for varying from to along with results in the case without the absolutely continuous assumption as in 1. . It is observed that the value function converges increasingly to that in 1. . The convergence of to the optimal barrier in 1. is also confirmed.

7 Conclusions

We solved the dividend problem with capital injection under the constraint that the cumulative dividend strategy is absolutely continuous. In particular, we proved that the solution is a refraction-reflection strategy that reflects the surplus from below at zero and decreases the drift at a suitable threshold.

It is noted that the methods and results in this current paper can potentially be applied in other related stochastic control problems driven by one dimensional spectrally one-sided Lévy processes. In inventory/cash management control problems as in 21. , it is of interest to pursue the optimality of refraction-reflection strategies under suitable absolutely continuous assumptions. Using the results in 7. , smooth fit and verification are expected to be carried out in an efficient way as in this current paper.

|

|

| Case 1 | Case 2 |

|

|

| Case 1 | Case 2 |

|

|

| sensitivity w.r.t. | sensitivity w.r.t. |

Acknowledgements.

J. L. Pérez is supported by CONACYT, project no. 241195. K. Yamazaki is in part supported by MEXT KAKENHI grant no. 17K05377. X. Yu is supported by Hong Kong Early Career Scheme under grant no. 25302116.References

- (1) Avram, F., Palmowski, Z. and Pistorius, M.R.: On the optimal dividend problem for a spectrally negative Lévy process. Ann. Appl.Probab. 17, 156-180, (2007).

- (2) Asmussen, S., and Taksar, M.: Controlled diffusion models for optimal dividend pay-out. Insur. Math. Econ. 20(1), 1-15, (1997).

- (3) Boguslavaskaya, E.: Optimization problems in financial mathematics: Explicit solutions for diffusion models., Ph.D. Thesis, University of Amsterdam, (2006).

- (4) Gerber, H. U. and Shiu, E. S. W.: On optimal dividend strategies in the compound Poisson model. N. Am. Actuar. J. 10(2), 76-93, (2006).

- (5) Pérez, J. L., Yamazaki, K.: Refraction-reflection strategies in the dual model. Astin Bull. 47(1), 199-238, (2017).

- (6) Kyprianou, A.E., Loeffen, R., and Pérez, J.L.: Optimal control with absolutely continuous strategies for spectrally negative Lévy processes. J. Appl. Probab. 49(1), 150-166, (2012).

- (7) Pérez, J. L., Yamazaki, K.: On the refracted-reflected spectrally negative Lévy processes. Stochastic Process. Appl. 128(1), 306-331, (2018).

- (8) Bayraktar, E., Kyprianou, A. E., Yamazaki, K.: Optimal dividends in the dual model under transaction costs. Insur. Math. Econ. 54, 133-143, (2014).

- (9) Li, Y., Li, Z., and Zeng, Y.: Equilibrium dividend strategy with non-exponential discounting in a dual model. J. Optim. Theory Appl. 168(2), 699-722, (2016).

- (10) Marciniak, E., and Palmowski, Z.: On the optimal dividend problem in the dual model with surplus-dependent premiums. J. Optim. Theory Appl. 168(2), 723-742, (2016).

- (11) Zhao, Y., Wang, R., Yao, D., and Chen, P.: Optimal dividends and capital injections in the dual model with a random time horizon. J. Optim. Theory Appl. 167(1), 272-295, (2015).

- (12) Kyprianou, A.E., Loeffen, R.: Refracted Lévy processes. Ann. Inst. H. Poincaré. 46(1), 24-44, (2010).

- (13) Chan, T., Kyprianou, A.E., and Savov, M.: Smoothness of scale functions for spectrally negative Lévy processes. Probab. Theory Relat. Fields 150, 691-708, (2011).

- (14) Kuznetsov, A., Kyprianou, A.E., and Rivero, V.: The theory of scale functions for spectrally negative Lévy processes. Lévy Matters II: Recent Progress in Theory and Applications: Fractional Lévy Fields and Scale Functions, Springer Berlin Heidelberg. 97-186, (2013).

- (15) Protter, P.E.: Stochastic integration and differential equations. Second edition. Version 2.1. Springer-Verlag, Berlin, (2005).

- (16) Avanzi, B., Pérez, J. L., Wong, B., and Yamazaki, K.: On optimal joint reflective and refractive dividend strategies in spectrally positive Lévy models. Insur. Math. Econ. available online, (2016).

- (17) Jiaqin, W., Yang, H., and Wang, R.: Classical and impulse control for the optimization of dividend and proportional reinsurance policies with regime switching. J. Optim. Theory Appl. 147(2), 358-377, (2010).

- (18) Egami, M. and Yamazaki, K.: Precautionary measures for credit risk management in jump models. Stochastics. 111-143, 1-22, (2013).

- (19) Kyprianou, A.E.: Introductory lectures on fluctuations of Lévy processes with applications. Springer, Berlin, (2006).

- (20) Egami, M. and Yamazaki, K.: Phase-type fitting of scale functions for spectrally negative Lévy processes. J. Comput. Appl. Math. 264, 1-22, (2014).

- (21) Bensoussan, A., Liu, R.H. and Sethi, S.P.: Optimality of an (s,S) policy with compound Poisson and diffusion demands: A quasi-variational inequalities approach. SIAM J. Control. Optim. 44(5), 1650-1676, (2005).