A random walk with catastrophes

Abstract

Random population dynamics with catastrophes (events pertaining to possible elimination of a large portion of the population) has a long history in the mathematical literature. In this paper we study an ergodic model for random population dynamics with linear growth and binomial catastrophes: in a catastrophe, each individual survives with some fixed probability, independently of the rest. Through a coupling construction, we obtain sharp two-sided bounds for the rate of convergence to stationarity which are applied to show that the model exhibits a cutoff phenomenon.

MSC2010: Primary 60J10, 60J80, secondary 92D25, 60K37.

Keywords: population models, catastrophes, persistence, spectral gap, cutoff.

1 Introduction

1.1 Model

Consider a population with the following birth and death rules. Given two parameters and , the population size is a discrete-time Markov chain on the state-space of non-negative integers () with transition function

When there is no risk of ambiguity, we will omit the superscripts and write . In words, conditioned on the history of the process up to time , the population size at time is determined by tossing an independent coin with probability of success. In the case of success, the population increases by , and in the case of a failure, also known as a catastrophe, the population is an independent binomial with parameters and . That is, in a catastrophe, each individual survives with probability independently of the other, and is otherwise killed. Note that is aperiodic and irreducible. As will be shown below, is also geometrically ergodic in total variation.

The model is a version of subcritical branching process (the catastrophes) with linear migration (population increase), and belongs to a larger class of stochastic models with catastrophes extensively studied in the literature. The term “catastrophe” loosely refers to events where a large proportion or the entire population may be wiped out. There are many ways to model catastrophes and several were studied in the literature. We discuss the literature in Section 1.3 below. The particular model we study corresponds to binomial catastrophes of [25, Section 2].

1.2 Motivation

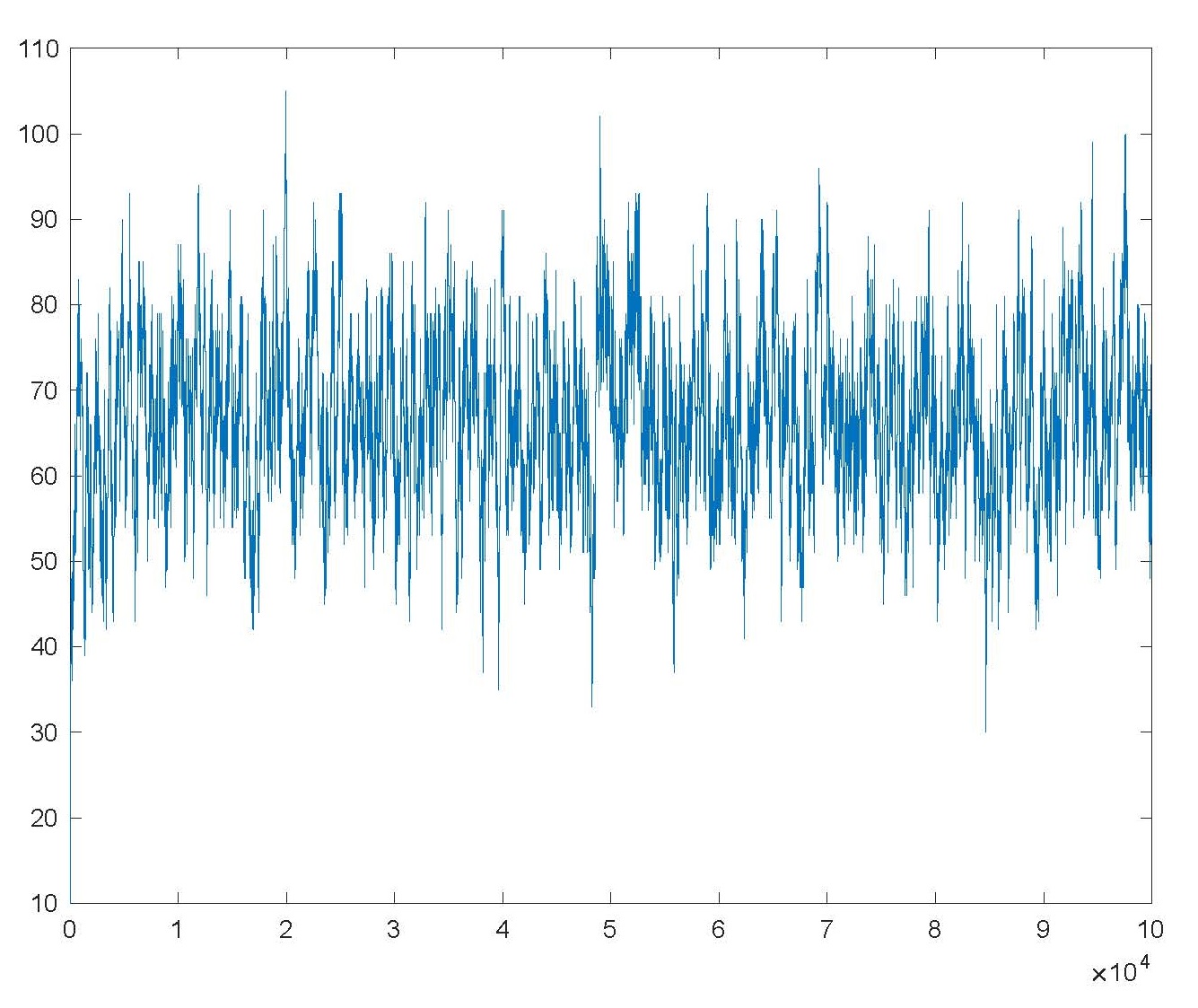

Our original interest in the model came from a curiously strong persistence feature we observed in simulations: repulsion from zero and long fluctuations in a narrow band before first hitting zero. Figure 1 shows a simulation of the model for and , between times and . The initial population size is . The population climbs quickly and fluctuates in a narrow band around an empirical mean close to for a very long time. In Section 2 we show that the process is mean-reverting around the mean of its stationary distribution. Corollary 4.5 shows that already after 1500 steps the total variation distance between the process and its stationary distribution is bounded above by . These, along with the fact that the expectation of the first extinction time is of the order , shown in Section 2, give at least a partial explanation to the simulations.

Additional motivation for our work on the model is in its amenability to coupling methods yielding sharp bounds on the rate of convergence to stationarity. These allow us to prove that the process exhibits the cutoff phenomenon. These results form the bulk of our work.

1.3 Literature

Stochastic models with catastrophes are studied in mathematical literature since mid-1970’s, for a first systematic account and a review of the early literature see [3]. For a motivation and background in biological sciences see, for instance, [9, 10, 19, 23]. Most of the work in the literature concern with either continuous time (generalized) birth and death chains with catastrophes or ODE-based models with a random disturbance. For a recent review and an extensive bibliography see [16]. The persistence feature is discussed for models with catastrophes in, for instance, [6, 23]. We remark that despite the variety of mathematical approaches to modeling population catastrophes, some results seem to be of a universal nature and are exhibited by models of different types. As an example, we mention the logarithmic dependence of the first extinction time on the initial population size which we discuss in Section 5.2.3.

As mentioned above, the model we study is a particular version of binomial catastrophes case in the model introduced by Neuts in [25, Section 2]. A continuous-time analogue of our model was introduced in [3, Section 4]. For recent progress, see [1, 7, 16]. In our model, deaths occur in a branching fashion, and in Section 5.1 we reformulate and discuss the model as a special branching process with immigration in a random environment. The study of branching processes as models of population growth with catastrophes (or disasters) goes back to at least [15], where a branching process without immigration is considered. Due to their tractability, much attention in the literature has been received by models with a deterministic growth between catastrophes, so called semi-stochastic models [5, 10, 11, 20].

1.4 Organization

In Section 2 we give a probabilistic representation of the stationary distribution of the process. The bulk of our contribution is reported in Sections 3 and 4. In Section 3 we introduce a coupling and use it compute sharp bounds on the total variation distance between the distributions of the process starting from two different initial states. In Section 4 we consider a sequence of models whose stationary distribution converges to a Poisson limit. We show that this sequence exhibit a cutoff phenomenon, namely on a certain time scale the total variation distance to the stationary distribution drops from one to zero in a narrow time window. Our study of both topics appear to be original in the context of stochastic models with catastrophes and we are not aware of similar results in the literature for any type of such models. Finally, in Section 5 we estimate the first extinction time and we use a branching representation for several purposes.

Throughout the paper, the notation stands for , and indicates that the random variables and have the same distribution.

2 Stationary distribution

2.1 Representation formula

Given a -valued random variable and , write for the random variable which, conditioned on is binomial with parameters and . We begin with the following lemma whose proof is omitted.

Lemma 2.1.

Suppose that are independent -valued random variables and let be a sequence taking values in . Assume that . For , let be -distributed, with independent, conditional on . Let and . Then has the same distribution as .

For , write for the shifted Geometric distribution with probability mass function equal to . Observe that if , then

| (1) |

The following proposition gives the stationary distribution for . Note that [25, formula (12)] gives the generating function of the stationary distribution for a class of Markov chains. Our model is in that class. The next proposition gives a probabilistic representation of the stationary distribution for our model . An interpretation through branching processes representation is discussed in Section 5.1.

Proposition 2.2.

Let be IID , for . Let be as in Lemma 2.1, and let be its distribution. Then is stationary for .

In the degenerate case , is -distributed. In Section 5.1 we discuss the case when and are both close to one.

Proof of Proposition 2.2.

Before continuing to our next topic we briefly discuss several related observations.

Using Proposition 2.2 and identity (1) we have

Let be the hitting time of , or the first extinction time,

| (3) |

Thus,

In the biological literature, this expected value is often referred to as the persistence time of the model [5, 22, 23]. Using that

| (4) |

we get for that

For example, for and , we get . For and , we get .

2.2 Mean Reversal

It follows from Proposition 2.2 that

| (5) |

Note that the local drift of

| (6) |

has the sign opposite to the deviation from . Thus the random walk always drifts toward its expected value. We also comment that the probability to hit in the next step decays geometrically with the state of the system, that is

These observations suggest that the process will tend to fluctuate about its mean before the first extinction, as can be seen in the simulation, see Figure 1.

3 Coupling and convergence to stationarity

3.1 Construction of the coupling

The key result of this section is a coupling of the probability laws and , obtained from a simple representation of the process.

Let with . Set , and . We continue inductively, assuming were defined and for all . Conditioned on ,

-

•

With probability , independently of the past, , and .

-

•

Otherwise, that is with probability , set

independent of each other and of the past. Moreover, set

It immediately follows that and are both copies of our Markov chain and that

for all . In addition, the process is non-increasing. Write and for the joint distribution and expectation of and . Let be the coupling time of two marginal processes, that is

| (7) |

If , then with probability equal to

Therefore, it immediately follows that under , is stochastically dominated by a sum of independent copies of Geometric random variables with parameter . Hence, , -a.s. and has a geometric tail. Furthermore, for all . Let denote the number of catastrophes up to time . Then . It follows from the construction of the coupling that

| (8) |

Therefore,

| (9) |

where the last inequality is due to Bernoulli’s inequality. Letting

| (10) |

we have that

| (11) |

Therefore

| (12) |

We comment that this bound is asymptotically sharp as . That is

| (13) |

as can be seen by expanding the expression through the binomial theorem and taking expectation.

3.2 Upper bounds on total variation

Recall that the total variation distance between two probability measures and on is defined as

For , let

By Aldous’ coupling inequality [28], . By combining this inequality and (12) we have proved

Proposition 3.1.

Let . Then for ,

Corollary 3.2.

For all

In particular,

Proof.

For any

where the inequality follows from Proposition 3.1. The result follows because of the identity . ∎

3.3 Lower bounds on total variation

The goal of this section is to obtain a lower bound for which is of the same order as the lower bound in Proposition 3.1. We comment that the difficulty in proving such a result stems from the fact that the state space is infinite, because couplings which preserve linear ordering on a finite state space always satisfy this property, see [4] for a proof in continuous-time setting.

We need to introduce some notation. Let

The notation is the law of the Markov chain with initial state , and transition function . We will also refer to the corresponding stationary distribution as .

The main result of this section is the following theorem.

Theorem 3.3.

Let with . Then

Before turning to the proof, we note the following

Corollary 3.4.

Suppose that maximizes . Then

In particular, , thus the spectral gap of the Markov chain is see [18]. The upper bound is Proposition 3.1. As for the lower bound, the ergodicity of the chain shows that for every , each summand in Theorem 3.3 as .

We prove Theorem 3.3 through two lemmas.

Lemma 3.5.

For all

-

1.

.

-

2.

Proof of Lemma 3.5.

The first claim follows immediately from (8) with . We turn to the second claim. Conditioned on , and are independent. Therefore,

Since

This gives

The distribution of conditioned on does not depend on the parameter , and from this we obtain

and the result follows. ∎

Lemma 3.6.

For let Then

Proof of Lemma 3.6.

Clearly,

Since for we have , it follows that the expectations under the summation sign are all zero, and that the last summand is also zero. Therefore,

where the equality follows from Lemma 3.5. The proof of the lemma is complete. ∎

Proof of Theorem 3.3.

We conclude this section with the following generalization of Lemma 3.5.

Theorem 3.7.

converges in distribution to as

Proof.

First,

Let and . Then from (8), we have

For , , and it follows from the binomial formula that

As a result,

Next, repeating the argument in the proof of Lemma 3.5 we obtain

with the last line follows from the binomial theorem and the bounded convergence theorem. Thus,

Putting it all together,

The proof of the theorem is complete. ∎

4 Poisson limit and a cutoff phenomenon

In this section we let and tend to . We will work under the following assumption

Assumption 4.1.

For with and

We will use the superscript to denote the dependence of the total variation distance, probability, expectation, and stationary distribution of the parameters, e.g. the stationary distribution for the process with parameters and will be denoted by .

Theorem 4.2.

Assume 4.1. Then converges weakly to as .

The proof is a routine calculation of moment generating functions, and the proof appears at the end of the section. We note that the actual form of the limit distribution is irrelevant for our next and main result of this section, the cutoff phenomenon, although we do rely on the tightness of to prove the second claim below.

Theorem 4.3.

Let Assumption 4.1 hold. Let be a sequence of a real numbers satisfying . Set

Then, for every

-

1.

-

2.

where

Therefore with a choice of parameters as in Theorem 4.3, the model exhibits a cutoff at with window size , see [21, p. 248].

To prove the theorem we will use the following lemma.

Lemma 4.4.

Proof.

Let . Recall that

- 1.

-

2.

We will use the following Chernoff-Hoeffding bounds for a binomial distribution [12]. If for some and then for any

(14) First, observe that under , is stochastically dominated by the number of births up to time whose distribution is . Let

In what follows, in order to simplify the notation, we will simply write and instead of, respectively, and

By the Chernoff-Hoeffding inequality, for any

Therefore,

(15) On the other hand, under , stochastically dominates which in turn, dominates Notice that

(16) Thus, for large enough, we have

where at the last but one step we used the inequality which is true for any sufficiently small with

∎

In order to obtain easier expressions to work with, we observe that for large enough, independently of , we have

Since and we have that

and so for every and ,

provided is large enough.

This leads to the following corollary. Recall that .

Corollary 4.5.

Under the assumptions of Theorem 4.3,

-

1.

-

2.

For any ,

We are ready to prove Theorem 4.3.

Proof of Theorem 4.3.

We conclude this section with the proof of Theorem 4.2

5 Additional Topics

5.1 Branching process representation

We adopt a scheme of Key [17] for general branching process with immigration in random environment to give a probabilistic interpretation of the particular instance of Neuts’ formula [25]. Using the approach of [1] we compute the generating function of the extinction time in Section 5.2.3.

The process can be thought of as a branching process with immigration in random environment. Branching process have been used to model growth of a population subject to random catastrophes by many authors (see, for instance, a comprehensive literature review in [16]), the idea goes back to at least [15] where a branching process in random environment (without immigration) was considered. In this section we use a branching representation of our process and Key’s [17] representation of its stationary distribution for several purposes. First, it yields Lemma 5.1 below stating that the extinction time has exponential tails, next it provides an illuminating probabilistic representation of the invariant distribution for our process, including the extreme case of rare but nearly total catastrophes (see the discussion after Proposition 5.2 and Theorem 5.3 below).

Let

| (21) |

We refer to the sequence as a random environment. We denote the distribution of the environment by the law of the process conditional on the environment by and the corresponding expectation by

The Markov process can be described using the following branching equation:

| (22) |

where is interpreted as the number of immigrants joining the system at generation and as the number of progeny of -th particle living at generation Under the probability law conditional on the environment are independent Bernoulli variables with parameter which are independent of

In statistical applications, this special type of branching processes with Bernoulli reproduction mechanism is often referred to as a RCINAR(1) random coefficient integer-valued autoregressive process of order one [31]. In this context, (22) is written as

where describes the action of a binomial thinning operator [24, 30].

Stationary distribution of branching processes with immigration in a random environment, in a general (and, in fact, multi-type) setting, was studied in [17]. In particular, it follows from results in [17] that random variable has exponential distribution tails (in order to deduce this, one may replace by 1 in (22) to be able to formally use Theorem 4.2 in [17], and then apply a stochastic dominance argument). We state it formally as

Lemma 5.1.

There exists such that for any

We next consider a branching process obtained from by sampling at the times when catastrophes occur. This auxiliary process has a slightly simpler structure than the underlying process We use it below to obtain an alternative probabilistic representation of the stationary distribution of

Let and

| (23) |

Observe that the sequence is an IID sequence of random variables. Let and

Proposition 5.2.

The Markov chain has a unique stationary distribution whose generating function is given by

Thus, in the language of Proposition 2.2,

Proof.

Considering as an immigration process, can be constructed as a branching process with immigration governed by the following branching identity:

| (24) |

where are IID Bernoulli random variables, independent of the immigration process and such that

The result thus follows from Theorem 4.2 in [17]. ∎

We remark that an auxiliary process similar to our has been used, for instance, in [7, 15] to derive the stationary distribution for different models with catastrophes.

Following the representation of the stationary distribution in [17], one can write

| (25) |

where is the number of descendant alive at time zero of a “demo” immigrant arrived at time Heuristically, in this representation is the population at time zero of a branching process that starts at minus infinity [17]. In between two regeneration times the process goes up number of times. When one observe the original chain in the stationary regime, time-wise the chain is in a random place between two random times This suggests (using the key renewal theorem) that the stationary distribution of the original Markov chain should be the convolution of and an independent variable. The result is formally confirmed in Proposition 5.2. We conclude this section with a brief discussion of the case of “severe but rare” catastrophes. For a biological motivation of this regime see, for instance, [13, 19, 26, 27, 29]. Specifically, a sequence of parameters such that as and for some We will denote the stationary distribution for the -th model, given by Proposition 2.2, by Observe that

| (26) |

With this, it is not hard to verify the following result:

Theorem 5.3.

where is independent of and converges in distribution, as to

Proof.

Recall (26), and set so that

To estimate the right-hand side, one can apply to the inequality which is true for all sufficiently small (and hence, uniformly on for all with large enough). The result follows from the fact

and

where we took in account that is monotone decreasing on Thus converges, as to and the proof of the theorem is complete. ∎

Note that in view of Proposition 5.2, is the limit in distribution of Furthermore, using (25) and a similar representation for the underlying branching process one can by virtue of the renewal theorem interpret as the time of the last catastrophe before time zero and as the distribution of the population right after the last catastrophe in the stationary branching process

5.2 First Extinction Time

5.2.1 Overview

In this section we discuss the following two aspects related to the first extinction time

-

•

Asymptotic behavior of under large initial population.

-

•

Generating function for .

5.2.2 Asymptotic for large population

In this section we discuss the asymptotic behavior of the first extinction time when the process starts from a large population.To do that we will use the coupling construction of Section 3.1. Consider the processes and with initial populations and , respectively. From our coupling we know that for every we have

Let and be the hitting time of by and , respectively:

Then are both nondecreasing.

Let and let be the increasing sequence of times visits . Then clearly,

This is because if and only if and . Now let . Then depends on the past of the coupled system only through the size of the population . Thus its distribution coincides with the distribution of . By ergodicity of , and the fact that a.s. as , it follows that converges weakly to the distribution of , the hitting time of under . We have proved the following:

Proposition 5.4.

converges in distribution to as

It follows from (9) that

Let , and let . Then by the Law of Large Numbers . We have the following two-sided bounds:

| (27) | ||||

Let

If , then it follows from the second inequality in (27) that

while if , it follows from the first inequality in (27) that

Thus in probability. This, and Proposition 5.4 give

Proposition 5.5.

in probability as

5.2.3 Generating function

For let and Note that The process has the following first-step decomposition:

| (28) |

where stands for the indicator of the event namely if and if , and is defined in (21). The generating function can be evaluated using (28) and an analytical method of [1]. In particular, we have

Theorem 5.6.

For let and

Then

| (29) |

The proof of the theorem is similar to the proof of Theorem 3.1, part (ii), in [1]. Namely, an application of (28) leads to a recursive equation for the generating function of a type that has been analyzed in [1]. We comment that through the recurrence relation (5.2.3), we can obtain an explicit formula for for each . The proof below is provided for the sake of completeness.

Proof.

We assume throughout the argument that For simplicity of notation, we will occasionally suppress the dependence of underlying functions on the parameter Using (28), we obtain

Multiplying by and summing over from to yields

where we used the negative binomial formula with Thus

| (30) | |||||

Let

| (31) |

and

For let and for It is easy to verify that

| (32) |

In this notation, (30) can be rewritten as

| (33) |

Note that for Consequently, taking in account (32) and that for all

-

(i)

For any decreases, as to zero, which is the smallest of two fixed points of

-

(ii)

for all

-

(iii)

We have:

and hence is uniformly bounded for

-

(iv)

For and

(34)

Thus, one can iterate (33) to obtain

Plugging in into this formula yields, taking into account that

| (35) |

This yields (29) by virtue of (31) and (32). In fact, after a suitable renaming of variables, equation (35) for is analogous to (3.12) in [1], while our (29) is its solution (3.4) in [1]. ∎

References

- [1] J. R. Artalejo, A. Economou and M. J. Lopez-Herrero (2007). Evaluating growth measures in populations subject to binomial and geometric catastrophes. Math. Biosci. Eng. 4, 573-594.

- [2] P. J. Brockwell (1986). The extinction time of a general birth and death process with catastrophes. J. Appl. Probab. 23, 851-858.

- [3] P. J. Brockwell, J. Gani and S. I. Resnick (1982). Birth, immigration and catastrophe processes. Adv. in Appl. Probab. 14, 709-731.

- [4] K. Burdzy and W. S. Kendall (2000). Efficient Markovian couplings: examples and counterexamples. Ann. Appl. Probab. 10, 362-409.

- [5] B. J. Cairns (2009). Evaluating the expected time to population extinction with semi-stochastic models. Math. Popul. Stud. 16, 199-220.

- [6] B. J. Cairns and P. K. Pollett (2005). Approximating persistence in a general class of population processes. Theoret. Population Biol. 68, 77-90.

- [7] A. Economou (2004). The compound Poisson immigration process subject to binomial catastrophes. J. Appl. Probab. 41, 508-523.

- [8] A. Economou and D. Fakinos (2008). Alternative approaches for the transient analysis of Markov chains with catastrophes. J. Stat. Theory Pract. 2, pp.183-197.

- [9] W. J. Ewens, P. J. Brockwell, J. M. Gani, and S. I. Resnick (1987). Minimum viable population size in the presence of catastrophes. Pp. 59-68 in M. E. Soule, editor. Viable Populations for Conservation. Cambridge University Press, Cambridge, UK.

- [10] F. B. Hanson and H. C. Tuckwell (1978). Persistence times of populations with large random fluctuations. Theoret. Population Biol. 14, 46-61.

- [11] F. B. Hanson and H. C. Tuckwell (1981). Logistic growth with random density independent disasters. Theoret. Population Biol. 19, 1-18.

- [12] W. Hoeffding (1963). Probability inequalities for sums of bounded random variables. J. Amer. Stat. Assoc. 58, 13 30.

- [13] T. E. Huillet (2011). On a Markov chain model for population growth subject to rare catastrophic events. Physica A: Statistical Mechanics and its Applications 390, 4073-4086.

- [14] V. Junior, F. Machado and A. Roldan-Correa (2016). Dispersion as a survival strategy. J. Stat. Phys. 164, 937-951.

- [15] N. Kaplan, A. Sudbury and T. S. Nilsen (1975). A branching process with disasters. J. Appl. Probab. 12, 47-59

- [16] S. Kapodistria, T. Phung-Duc and J. Resing (2016). Linear birth/immigration-death process with binomial catastrophes. Probab. Engrg. Inform. Sci. 30, 79-111.

- [17] E. S. Key (1987). Limiting distributions and regeneration times for multitype branching processes with immigration in a random environment. Ann. Probab. 15, 344-353.

- [18] I. Kontoyiannis and S. P. Meyn (2012). Geometric ergodicity and the spectral gap of non-reversible Markov chains. Probab. Theory Related Fields 154, 327-339.

- [19] R. Lande (1993). Risks of population extinction from demographic and environmental stochasticity and random catastrophes. American Naturalist 142, 911-927.

- [20] M. C. A. Leite, N. P. Petrov and E. Weng (2012). Stationary distributions of semistochastic processes with disturbances at random times and with random severity. Nonlinear Anal. Real World Appl. 13, 497-512.

- [21] D. A. Levin, Y. Peres and E. L. Wilmer (2009). Markov chains and mixing times. American Mathematical Society, Providence, RI.

- [22] S. N. Majumdar and D. Dhar (2001). Persistence in a stationary time series. Phys. Rev. E 64, 046123.

- [23] M. Mangel and C. Tier (1993). Dynamics of metapopulations with demographic stochasticity and environmental catastrophes. Theoret. Population Biol. 44, 1-31.

- [24] E. McKenzie (2003). Discrete variate time series. In: D. N. Shanbhag and C. R. Rao (eds), Handbook of Statistics, Elsevier Science, pp. 573-606.

- [25] M. F. Neuts (1994). An interesting random walk on the non-negative integers. J. Appl. Probab. 31, 48-58.

- [26] R. R. Paine (2000). If a population crashes in prehistory, and there is no paleodemographer there to hear it, does it make a sound? Am. J. Phys. Anthropol. 112, 181-190.

- [27] J. F. Silva, J. Raventos, H. Caswell, and M. C. Trevisan (1991). Population responses to fire in a tropical savanna grass, andropogon semiberbis: a matrix model approach. J. Ecol. 79, 345-355.

- [28] H. Thorisson (2000). Coupling, Stationarity, and Regeneration, Springer, New-York.

- [29] S. Tuljapurkar (1990). Population Dynamics in Variable Environments. Lecture Notes in Biomathematics, Vol. 85, Springer-Verlag.

- [30] C. H. Weiß (2008). Thinning operations for modeling time series of counts - a survey. AStA Adv. Stat. Anal. 92, 319-341.

- [31] H. Zheng, I. V. Basawa and S. Datta (2007). First-order random coefficient integer-valued autoregressive processes, J. Statist. Plann. Inference 173 (2007), 212-229.