ifaamas \acmDOIdoi \acmISBN \acmConference[AAMAS’18]Proc. of the 17th International Conference on Autonomous Agents and Multiagent Systems (AAMAS 2018), M. Dastani, G. Sukthankar, E. Andre, S. Koenig (eds.)July 2018Stockholm, Sweden \acmYear2018 \copyrightyear2018 \acmPrice

1Department of Informatics, University of California, Irvine, Irvine, CA 92617, USA

2 Computer Science Department, Brigham Young University, Provo, UT 84602, USA

3College of Information Engineering, China Jiliang University, Hangzhou 310018, China

Information Design in Crowdfunding under Thresholding Policies

Abstract.

Crowdfunding has emerged as a prominent way for entrepreneurs to secure funding without sophisticated intermediation. In crowdfunding, an entrepreneur often has to decide how to disclose the campaign status in order to collect as many contributions as possible. Such decisions are difficult to make primarily due to incomplete information. We propose information design as a tool to help the entrepreneur to improve revenue by influencing backers’ beliefs. We introduce a heuristic algorithm to dynamically compute information-disclosure policies for the entrepreneur, followed by an empirical evaluation to demonstrate its competitiveness over the widely-adopted immediate-disclosure policy. Our results demonstrate that the immediate-disclosure policy is not optimal when backers follow thresholding policies despite its ease of implementation. With appropriate heuristics, an entrepreneur can benefit from dynamic information disclosure. Our work sheds light on information design in a dynamic setting where agents make decisions using thresholding policies.

Introduction

Crowdfunding reinvents the way that entrepreneurs raise external funding for implementing creative ideas. It has created a rapidly growing market that contributes an annual economic impact of tens of billions of US dollars globally Yu et al. (2017). Unfortunately, not all the crowdfunding campaigns are successful because most campaigns will get funded only if they have reached the fundraising goal within a deadline Short et al. (2017). In fact, less than of the crowdfunding projects reach the targeted goals and receive the funds within the campaign deadlines Short et al. (2017).

Mounting research has begun to investigate the determinants of the success of crowdfunding projects. Although there might be many factors (e.g., project descriptions Marelli and Ordanini (2016), product value Agrawal et al. (2014), geography effect Agrawal et al. (2011), reward details Marelli and Ordanini (2016), entrepreneurs’ reputation Kuppuswamy and Bayus (2015) and the social network effect Agrawal et al. (2014)) that influence a campaign’s success, a recent study indicates that the number of donations made by early backers of a project is often the only difference between that project being funded or not Solomon et al. (2015). A substantial body of both theoretical analyses Agrawal et al. (2014); Mollick (2014); Alaei et al. (2016) and empirical evidence Kuppuswamy and Bayus (2015); Colombo et al. (2015); Marelli and Ordanini (2016); Skirnevskiy et al. (2017) demonstrate that the amount of early contributions has a strong positive effect on the success of crowdfunding campaigns. These prior studies unanimously confirm the crucial role of early contributions in the success of crowdfunding projects.

There are two main reasons why the amount of early contributions matters. First, information about contributions received early in the campaign signals to potential backers the quality of the project, which in turn can trigger social learning behavior Bandura (1989) causing potential backers to also contribute to the campaign Colombo et al. (2015). An empirical study on a sample of 25,058 Kickstarter projects indicates that prospective backers usually make their pledging decisions based on how much of the project goal has already been funded by others Kuppuswamy and Bayus (2015). Second, backers who have made an early contribution are likely to circulate the information of the project to their friends or families, which may attract additional contributions Colombo et al. (2015); Skirnevskiy et al. (2017). Both rationales indicate that it is of interest to entrepreneurs to attract as many contributions from early backers as possible.

In crowdfunding, backers are often reluctant to donate in the early days of a campaign due to high uncertainty Mollick (2014); Alaei et al. (2016); Kuppuswamy and Bayus (2015); Solomon et al. (2015); Colombo et al. (2015). A major source of uncertainty is the probability of success that the campaign will get funded (i.e., Probability of Success, or PoS) Colombo et al. (2015); Kuppuswamy and Bayus (2015). Prospective backers are often uncertain about entrepreneurs’ abilities to collect sufficient contributions to get the project funded. For instance, of the crowdfunding projects in Kickstarter failed to reach the target goals Kickstarter (2017). A backer 111We will use “she” to denote an entrepreneur and “he” a backer/agent. experiences a monetary or non-monetary opportunity cost if the fundraising goal is not achieved (and the project not funded), even if he is refunded upon the failure of the campaign Alaei et al. (2016).

To attract as many early contributions as possible, an entrepreneur must take appropriate measures to coordinate backers’ actions. To do this, the entrepreneur needs to have prior knowledge about the backers’ arrival process, their valuation of the project (if funded), and how they estimate the probability that the campaign will be funded. However, none of this information is perfectly known to the entrepreneur. Thus, it is challenging for the entrepreneur to figure out what actions will make backers, especially early backers, be more willing to contribute.

If conditions permit, the entrepreneur can manipulate backers’ payoffs by offering appealing discounts to early backers that face high uncertainty Ellman and Hurkens (2015); Strausz (2016). The problem of devising allocation and payment schemes falls into the field of mechanism design Nisan and Ronen (1999). While illuminating, it requires additional budgets and thus diminishes the entrepreneur’s revenue Ellman and Hurkens (2015); Strausz (2017). Absent from sophisticated or even unrealistic assumptions of the backers’ private types (e.g., valuation, arrival time, departure time), it is rather difficult or even unfeasible for the entrepreneur to implement effective mechanisms Ellman and Hurkens (2015); Strausz (2017). This is particularly the case in online settings where the entrepreneur has little knowledge about how the backers make their projections of the campaign’s PoS.

Alternatively, the entrepreneur can improve backers’ beliefs of the campaign’s PoS by choosing what information backers see. In particular, the entrepreneur can and is permitted to voluntarily disclose the project status (i.e., how many contributions have been collected up to a given timestamp), a critical factor that influences backers’ beliefs of the campaign’s PoS Kuppuswamy and Bayus (2015); Alaei et al. (2016). The problem of determining which pieces of information are disclosed to whom is called information design Taneva (2015).

Prior work on information design has generally assumed that backers’ strategic behavior was perfectly rational and that games were well-defined (e.g., signaling games) Bergemann and Pesendorfer (2007); Taneva (2015); Bergemann and Wambach (2015); Bergemann and Morris (2016); Alonso and Camara (2016). However, studies on consumer purchasing behavior show that buyers usually follow thresholding policies to decide whether to purchase goods or not Kau and Hill (1972); Kahneman (2003); Zhou et al. (2005). They often buy products when the prices are no more than their reserved values. This is particularly the case when consumers face high degrees of uncertainty and have little knowledge about the environment or the future, as frequently observed in clinical decision making Pauker and Kassirer (1980), crowdsourcing contests Easley and Ghosh (2015), airline ticket sales Zhou et al. (2005), online shopping Lee and Lin (2005), management science Su (2007), societies of autonomous machines Shen et al. (2017) and crowdfunding Mollick (2014); Alaei et al. (2016). Under certain circumstances, thresholding policies are optimal policies and hence represent rational behavior Ohannessian et al. (2014). We thus consider the scenario where backers follow thresholding policies when they decide whether to contribute to a project or not.

In this paper, we study the information design problem in which an entrepreneur voluntarily reveals the project status to backers to influence their beliefs of the project’s probability of success. Our work contributes to the state of the art in the following ways:

-

(1)

We show that excessive information disclosure weakly shrinks the entrepreneur’s revenue. We identify conditions when immediate disclosure is optimal in crowdfunding when agents follow thresholding policies. We demonstrate that immediate disclosure is optimal if the funding goal has been achieved and if the project status increases monotonically by at least one contribution each time.

-

(2)

We introduce a heuristic algorithm called Dynamic Shrinkage with Heuristic Selection (DSHS) to to help the entrepreneur make decisions on information-disclosure policies.

-

(3)

We conducted extensive simulations with real-world dataset to compare the performance of the DSHS algorithm with the widely-adopted information-disclosure policy. Experimental results demonstrate that despite its computational efficiency, the immediate-disclosure policy is not optimal when agents follow thresholding policies. Entrepreneurs can benefit from dynamic information design with appropriate heuristics.

Decision Making in Crowdfunding

After introducing key notations, we formalize backers’ decision model and the entrepreneur’s optimization problem in a crowdfunding campaign.

Preliminaries

We consider discrete time , where is the deadline for the campaign. Before launching the campaign, the entrepreneur must determine a fundraising goal to get funded, a deadline for reaching the goal, the number of rewards , the minimal amount of contributions for a reward , and a detailed description of the project such as motivation, product, milestones, and profiles of the team. All this information is fixed and is disclosed to all the backers. See Figure 1 for the procedure of a typical crowdfunding campaign.

After the campaign starts to accept contributions, backers arrive at the campaign sequentially with at most one each time. This is without loss of generality because batch arrivals can be viewed as a special case where the time interval is minimal Shen et al. (2016); Alaei et al. (2016). Let denote the number of arrivals at time .

At the beginning of time , the entrepreneur discloses the state of the campaign (i.e., project status) to each backer that is in the campaign. Here, where refers to the percentage of funds that have been raised up to time ( not included), with respect to the fundraising goal . For simplicity, let . We denote the entrepreneur’s decision on information disclosure for backer at time by:

| (1) |

Here, . The disclosed project status must reflect the true state of the project at time , which is enforced by the crowdfunding platform. In real-world crowdfunding campaigns, entrepreneurs are allowed to voluntarily disclose truthful project status Solomon et al. (2015); Alaei et al. (2016). In our work, we assume that any information about the project status observed by the backers is directly revealed by the entrepreneur. Future work should address the scenarios when backers have exogenous information due to information contagion Arthur and Lane (1993).

Backers’ Decision Model

It is widely known that backers’ beliefs of PoS are usually correlated with the entrepreneur’s updates of the project status Kuppuswamy and Bayus (2015); Marelli and Ordanini (2016); Alaei et al. (2016); Kuppuswamy and Bayus (2017). However, the exact correlation is privately known to a backer himself only and not observed by the entrepreneur. This makes it difficult to accurately model backers’ decision making process. To tackle this problem, we formalize backers’ decision model using the same pattern as that in the work Ohannessian et al. (2014) by Ohannessian et al., which also assumes that agents use thresholding policies.

Let represent high-value backer ’s estimate of the campaign’s PoS given the report , and be his threshold on to contribute. We denote backer ’s decision on whether to contribute or not at time by , where indicates Not Pledging, and represents Pledging. Backer ’s expected utility is determined as follows:

| (2) |

Here, is backer ’s expected utility if he contributes (i.e., ) when his estimate of PoS is no less than the threshold . Note that , and are all private information known to backer only, while his arrival and pledging behavior are observed by the entrepreneur through the platform. In practice, backer may adapt to the environment and update his threshold accordingly. In this case, his threshold can be treated like the upper bound of all the updated thresholds. Without loss of generality, we assume that each contributing backer pledges the same amount of fund to the project for a reward.

Backer stays at the campaign for at most periods, where is known to backer only. This is without loss of generality because although backers may dynamically enter and exit the system and check the progress, these situations can be viewed as the case that the backers stay in the system for a sufficient period.

Let denote the group of backers who have arrived at the campaign before or at time , have at least one time period to leave and have not yet claimed a contribution. At time , for each backer , his objective function is

| (3) |

where is determined by Equation 2. At time , backer will leave the campaign either if he claims a contribution (i.e., ) or his own deadline is reached.

The Entrepreneur’s Optimization Problem

In crowdfunding, the entrepreneur is interested in attracting as many contributions as possible within the deadline so that her project will get funded. Specifically, her objective is to set the disclosure policy such that the number of contributions is maximized until a given deadline .

Let denote the funds that the entrepreneur has raised up to time ( included) when she uses the disclosure policy . Here, . The entrepreneur’s expected contributions at time is defined as follows:

| (4) |

Due to the deadline constraint, the entrepreneur’s optimization problem (i.e., optimal information design) is formalized as follows:

Definition 1 (Optimal Information Design).

An optimal information design in crowdfunding is to find a disclosure policy , such that is maximized, i.e., .

Due to the dynamic nature of crowdfunding, the design of disclosure policy cannot be based on backers’ later decisions , or use later project status . This constraint is called No Clairvoyance.

Optimal Information Design

After introducing the solution concepts, we show that excessive information weakly shrinks revenue. We further identify conditions under which immediate disclosure is optimal in crowdfunding.

Solution Concepts

In his seminal work Blackwell et al. (1953), Blackwell formulated a partial order that is capable of comparing the quality of two pieces of information (see Theorem 1). According to Blackwell’s theorem, if a piece of information is Blackwell-inferior to , then an agent will always weakly prefer to .

Theorem 1 (Blackwell’s theorem Blackwell et al. (1953)).

Let and represent two pieces of information, the following conditions are equivalent:

-

(1)

When the agent chooses , her expected utility is always at least as big as the expected utility when she chooses , independent of the utility function and the distribution of the input.

-

(2)

is a garbling of .

Blackwell’s theorem implies two types of information: vertical information and horizontal information, which are key solution concepts used in this work. Given two pieces of information, if one is always (weakly) preferred whatever the information receivers’ types are, then they are vertical information (see Definition 2). If the two pieces of information are not comparable without prior knowledge about the receivers’ types, then the information is horizontal (definition omitted since it complements vertical information).

Definition 2 (Vertical Information).

Given two pieces of information and , where , if , , then , where denotes a set of agents and , indicating preferred or indifferent to, is independent of agent ’s private type. If , the information is vertical.

In crowdfunding, backer ’s estimate of the campaign’s PoS (i.e., ) is both time and state-dependent. Both the amount of funding (measured by ) raised, and the time of the project status (denoted by ) are important. We identify three scenarios of vertical information. First, a higher state of project status is always more favorable if the time of the state is the same (e.g., ), which is obvious. Second, the earlier report of project status is always (weakly) preferred if the project status of the two reports are the same (see Proposition 1). Third, the later report of project status is always (weakly) preferred if the revenue increases by more than each time between the timestamps of the two statuses. (see Proposition 2). All the proofs can be found in Appendix A.

Proposition 1.

An earlier report of project status is always weakly preferred if the project status of the two reports are the same. Formally, given project status and , where , , we have : .

Proposition 2.

A later report of project status is always weakly preferred if the revenue increases by more than each time between the period of the two statuses. Given status reports and , where and , we have : .

If the conditions of vertical information cannot be identified, the information is horizontal (see Example 1). Without prior information about backers’ private types (e.g., arrival process, valuation, the estimate of the campaign’s PoS, and the correlation between them), it is not feasible for the entrepreneur to identify optimal information design. However, an effective disclosure policy should capture both the vertical and horizontal component, making the information design problem particularly challenging for the entrepreneur.

Example 1.

Given and , without prior knowledge about backer ’s projection of PoS (i.e., ), it is unclear which project status is more favorable by . This is because .

Excessive Disclosure Shrinks Revenue

Given two project status reports, if their partial order can be identified according to Proposition 1 and 2, then the entrepreneur only needs to disclose the one with higher order. This is because revealing the low-order report does not increase the chance that backers contribute to the campaign (see Lemma 1).

Lemma 1.

If the order of two project status reports can be identified, the low-order report does not increase the change of backers’ contribution. Formally, given project status reports and , if , we have :

| (5) |

where denotes the expectation that backer contributes to the campaign given the information .

If the partial order of the two reports cannot be identified, the entrepreneur should also refrain from disclosing additional information. Depending on how backers estimate the campaign’s PoS, revealing more information than necessary can decrease the revenue. The reason is that excessive information disclosure can decrease backers’ projections of the PoS (See Lemma 2).

Lemma 2.

If the partial order of the two project status reports cannot be identified, excessive information disclosure weakly decrease backers’ projections of PoS. Formally, given project status reports and where , if the partial order of the two cannot be identified by the entrepreneur, then , we have:

| (6) |

In our model of crowdfunding, excessive information disclosure weakly diminishes a backer’s willingness to contribute (see Theorem 2) and thus weakly shrinks the revenue as well as the entrepreneur’s ability to implement optimal information-disclosure policies. To collect as many contributions as possible, the entrepreneur should not disclose more information about the project status than necessary.

Theorem 2.

Excessive information disclosure weakly diminishes the chance that a backer will contribute. Formally, given two project status reports and where , let denote backer ’s decision on pledging if given report either or , and denote his decision on contribution if given . , we have: .

Immediate Disclosure is not Always Optimal

The immediate-disclosure policy (see Definition 3) is widely adopted by entrepreneurs on major crowdfunding platforms (e.g., Kickstarter, Indiegogo) due to its ease of implementation Alaei et al. (2016). It is thus important to investigate if immediate disclosure is optimal.

Definition 3 (Immediate Disclosure).

An immediate-disclosure policy always reveals the current project status to all the backers in the campaign. Formally let denote immediate disclosure, we have .

If the entrepreneur and the backers have identical information, immediate disclosure is optimal Rayo and Segal (2010); Kamenica and Gentzkow (2011); Au (2015). It still holds if the entrepreneur has some unique information provided that such information does not affect the backers’ decisions. Unfortunately, in our model, all information about the campaign (e.g., ) except the project status is known to both the entrepreneur and the backers. Backer ’s estimate of PoS (i.e., ) is influenced by the project status that the entrepreneur reveals. Thus, it is critical for the entrepreneur to identify conditions when immediate disclosure is optimal.

From Proposition 2, we see that to improve backer ’s belief of the campaign’s PoS, the entrepreneur should always disclose the project status that is preferred by all the backers if available. Otherwise, the information design is not optimal. With this intuition in mind, we show that before the campaign reaches the fundraising goal, immediate disclosure is optimal if and only if the project status increases monotonically in time by at least one contribution each time (see Lemma 3). This condition characterizes the relationship between the growth rates of the revenue and the maximum possible arrival rate of the backers. Though the entrepreneur does not have prior knowledge of the backers’ types (e.g., beliefs, thresholds), she can observe the progress of the project and determine if immediate disclosure is optimal given the tracking record of project status.

Lemma 3.

Before the campaign reaches the fundraising goal, immediate disclosure is optimal if and only if the project state increases monotonically in time by at least one contribution each time. Formally, if , then we have:

After successfully reaching the funding objective, it is certain that the campaign will get funded, so immediate disclosure is optimal (see Lemma 4).

Lemma 4.

After the campaign reaches the fundraising goal, Immediate disclosure is optimal. Formally, if , then we have: .

Lemma 3 shows that immediate disclosure is not always optimal during the crowdfunding campaign when backers follow a thresholding policy. According to Definition 1 and Equation 4, in order to compute the optimal solution, the entrepreneur must have a prior knowledge of the sequence of decisions in advance. However, such assumption violates the No Clairvoyance constraint and is not implementable in practice.

Dynamic Information Design

Instead of restricting our attention to optimal information design, we introduce a heuristic algorithm, called Dynamic Shrinkage with Heuristic Selection (DSHS), to help the entrepreneur make decisions on information disclosure.

DSHS treats the two conditions separately: before and after project success (see Algorithm 1) . Before the campaign reaches the fundraising goal, the algorithm determines the disclosure policy according to two processes: dynamic shrinkage (see Algorithm 2) and heuristic selection. After the campaign reaches the fundraising goal (if it happens), the algorithm discloses information immediately.

Dynamic Shrinkage

In the dynamic-shrinkage process, DSHS ranks all the available choices, and removes the least promising choices which are less preferred by the backers according to Propositions 1 and 2. By doing so, the entrepreneur avoids excessive information disclosure that weakly shrinks revenue.

Initially, DSHS includes all the project status disclosures since the last disclosure for backer into a set . That is,

| (7) |

where . It then sorts in the ascending order of . This sorting problem can be easily solved by Quicksort Hoare (1962) with time complexity . Since , the worst-case complexity for the function is .

After the sorting process, DSHS removes the least promising candidates through the function SHRINK (see Algorithm 2). While there are at least two choices available, the SHRINK algorithm removes the project status with later time if the two statuses have the same progress (see line 4, Algorithm 2) according to Proposition 1. This process is equivalent to removing duplicates in a sorted array, which can be solved in time. Given two project statuses, if they satisfy the relation in Proposition 2, then the algorithm removes the project status with the earlier time (see line 7, Algorithm 2) . This step takes time in the worst case. The algorithm does nothing if only one disclosure strategy exists.

Heuristic Selection

After the shrinkage process, if there are still at least two choices available (i.e., ), then the remaining set is horizontal. The entrepreneur has to select some to attract as many contributions as possible. This optimization problem is similar with the renowned restless bandit problem Whittle (1988), which is not solvable due to incomplete information. However, simple heuristics such as random selection, greedy selection, -greedy exploration, and softmax exploration can be used to produce acceptable results. See Appendix B for details of each algorithm.

We further introduce a meta algorithm (See Algorithm 3). The intuition is that the algorithm can improve the quality of decisions by only using the experts that have a satisficing performance for producing the final results Crandall (2014). Besides, we take an ensemble approach to calculate the final selection instead of directly applying the results produced by the selected experts. The benefit is that the algorithm can further reduce potential performance loss due to biases of a single individual expert Shen et al. (2013); Kuncheva and Whitaker (2003).

Before describing the meta algorithm, we first introduce the notations used. Let denote the set of experts, where is one of the four heuristics. We write for expert ’s expected revenue at time and write for expert ’s revenue prospect. Here, is computed by: , where denotes the probability that is selected as the targeted project status by expert at , and is the entrepreneur’s expected increase of revenue given for backer by using expert algorithm . Details of computing for each expert is described in Appendix B. Initially, .

Each time the algorithm selects a subset of experts whose expected revenue is higher than a learned threshold—the minimum learned prospect . This step eliminates the experts that fail to produce better expected revenue than the threshold. The algorithm then performs a majority vote from the results generated by each expert . The selected project status is the one with the most votes. Ties are broken by choosing the result generated by the expert with the highest . This step aims to improve the robustness of selection by reducing the performance loss caused by biases of a single expert.

When a new expert algorithm is selected, the prospect for the expert is updated by . Here, is the number of periods that expert has been used, and is the learning rate ( in our paper). is the entrepreneur’s average revenue gain per time by using expert algorithm in the last periods. It is calculated by: .

DSHS is highly flexible in the sense that it allows the entrepreneur to easily customize both the shrinkage process and the selection process with different methods.

Empirical Evaluation

This section describes the experimental settings and the results.

Experimental Setup

We collected the campaign data from a randomly selected subset of Kickstarter222https://www.kickstarter.com projects using a web crawler. The dataset contains 1,569 projects which satisfy the following conditions: (1) they were all-or-nothing, reward-based campaigns; (2) the campaigns lasted for exactly 1,440 hours (60 days) with both the starting time and the ending time falling between 07/15/2016 and 10/15/2016. Each campaign includes hourly project status, the fundraising goal, the deadline, the minimal amount of contribution, and the number of contributions every hour. The data samples allow us to mimic the operation of real-world crowdfunding projects when the underlying factors and correlations that impact them are yet to be identified Mollick (2014); Alaei et al. (2016).

Most of the projects on Kickstarter offer several tiers of perks for the backers to choose. We only selected the early bird pledges and the regular pledges that would offer a product to the backers to compensate backers’ financial support. We adjusted the funding goal for each project accordingly. The early bird pledges were proportioned to the regular pledges. For instance, an early bird pledge with value is equivalent to regular pledge with value .

Due to Kickstarter’s API constraints, we were unable to track the number of backers who visited the campaign per hour. We simulated backers’ arrivals using Poisson Ross et al. (1996) distribution for each project. The arrival process was independently and identically distributed with a mean across time, where . The mean of was 0.1 (consistent with the empirical arrival rates of backers in crowdfunding projects Marwell (2015)).

We used the anticipating random walk Alaei et al. (2016) model for simulating backers’ projections of PoS because it is tailored for computing backers’ estimates of PoS in crowdfunding. For each project, the backers’ valuation of a reward was Gaussian Ross et al. (1996) distributed with a mean equivalent to the value of the reward and a randomly selected standard deviation ranging 0.05 of the mean to 0.5 of the mean.

We performed six groups of experiments: immediate disclosure (immediate), and DSHS with five heuristics (random, greedy, -greedy, softmax, and meta) . Each group was run 30 times with the same 2.9GHz quad-core machine.

Results

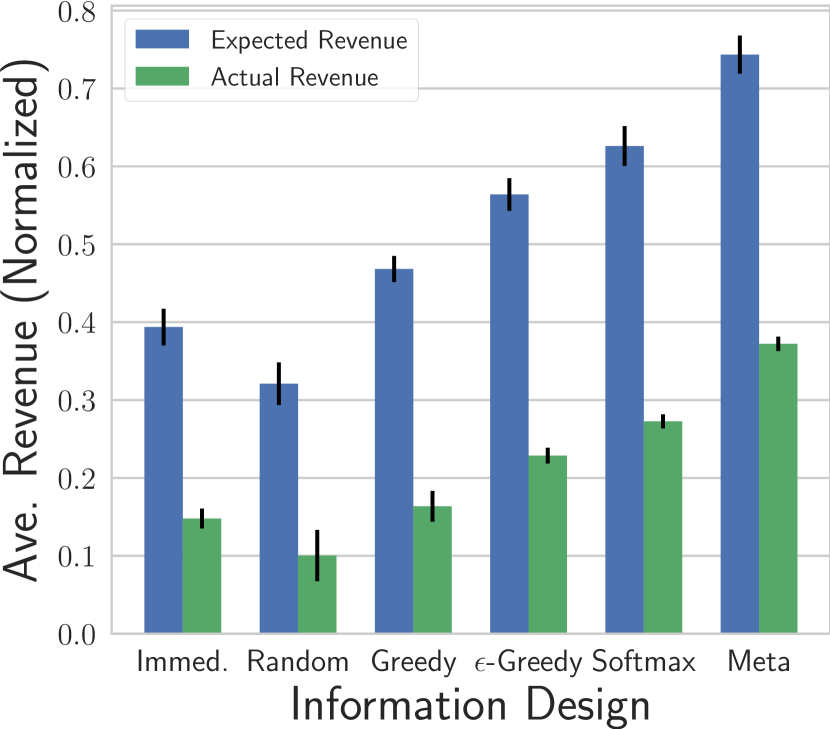

Figure 2(a) shows the average revenue (normalized by the highest revenue achieved in all experiments) obtained in the end by each group. The actual revenue excluded the projects that failed (), while the expected revenue included all the projects regardless of whether they succeeded to meet the funding goal or not. Not surprisingly, the expected revenue of each group was significantly higher than their respective actual revenue. This is because the majority of the campaigns failed due to not having met the funding goal within the deadline (see Figure 2(c)). Among the six groups, the meta group scored the best for both the expected revenue (mean = 0.7435, std = 0.0244) and the actual revenue (mean = 0.3722, std = 0.0092), followed by the softmax group, and the -greedy group. The greedy group and the immediate group performed better than the immediate group in the expected revenue, but not in the actual revenue due to a lower success rate. The random group received the lowest scores in terms of both the expected revenue (mean = 0.3210, std = 0.0273) and the actual revenue (mean = 0.1004, std = 0.0329).

At the beginning, the immediate, the meta, the greedy, and -greedy groups performed better than the other two (see Figure 2(b)). As time progressed, the meta and the -greedy groups continued to lead the way until the later left behind the former at around . The -greedy group kept the second until at time that it was surpassed by the softmax group. One explanation is that the -greedy algorithm initially encouraged exploration to a higher degree than the softmax algorithm. However, it acted more greedily than the softmax exploration over time, which was not favorable since better choices were rarely explored. The meta group used a set of refined policies to produce more robust decisions than the others. The random group performed the worst possibly because the random algorithm completely ignored the history of backers’ responses.

The meta algorithm took the most computation time (mean = 0.2300 std = 0.0290 ), while the random method required the least time (mean = 0.1037, std = 0.0034) (see Figure 2(d)). Immediate disclosure required no additional time.

In summary, although the meta group required the most computation time, it performed consistently the best among all the groups in terms of both actual and expected revenue. This echoes our previous findings that immediate disclosure is not always optimal in crowdfunding.

Conclusion

In this paper, we present the very first study on information design where a sender interacts with multiple receivers that follow thresholding policies. Our work demonstrates that excessive information disclosure weakly shrinks the revenue in crowdfunding when backers use cutoff policies. It further shows that the widely-adopted immediate-disclosure policy is not optimal. We also present how the entrepreneur can benefit from dynamic information disclosure with appropriate heuristics. To further evaluate the performance of the heuristic algorithm, user studies and real-world deployment are needed.

Although our analysis is in the context of crowdfunding and the DSHS algorithm is intended to help the entrepreneur make decisions on information disclosure in crowdfunding, extensions to other domains (e.g., transportation systems, smart grids, and online shopping) where agents typically use thresholding policies can be straightforward. For instance, online shopping marketplace can employ DSHS variants to dynamically reveal the number of products available or the number of products sold to attract potential buyers to buy the products. Further research is required to assess the variants’ performance in these domains.

This work was supported by National Science Foundation through grant no. CCF-1526593. Yan was supported by National Science Foundation of China under grant no. 61602431. The authors wish to thank the anonymous reviewers for their helpful comments and suggestions.

Appendix A Proofs

Proof of Proposition 1

By condition, . That means the revenue does not increase between time to time . Since , we have , which means less time is left to achieve the fundraising goal . Thus, the campaign’s PoS decreases or stays the same, regardless of backers’ arrivals from time to . That is, . By Equation 2, the utility of all the subsequently arriving backers weakly decreases, i.e, . By Definition 2, we have for all , and for all .

Proof of Proposition 2

By assumption , we have that the number of arrivals from time to is: . Since , we have that at least backers have contributed from time to . Without loss of generality, one can assume that each time from to , at least one backer arrives at the campaign and makes a contribution. In other words, the revenue of the campaign grows faster than or equal to the arrival of backers between and . Thus, the campaign’s PoS increases or stays the same. That is, . By Equation 2, the utility of all the subsequently arriving backers weakly increases, i.e., . By Definition 2, we have .

Proof of Lemma 1

By condition, we have . By relation of preferences and utilityChambers and

Echenique (2016), . According to backers’ utility function (Equation 2), . Depending on the order of the backer ’s threshold , his belief when given report and the belief given report , there are the following three cases.

-

: in this case, backer will not contribute to the campaign given either or . That is, .

-

: given report , backer will contribute to the campaign and leave the system. An additional signal about the project status cannot improve his possibility of pledging, i.e, .

-

: under this condition, backer will contribute to the campaign and leave the system given either of the two reports. That is, .

Thus, .

Proof of Lemma 2

We prove it by contradiction. Assume, to the contrary, that , . Depending on the order of backer ’s threshold , , and , we have the following three cases:

Thus, .

Proof of Theorem 2

If the information is vertical, by Lemma 1, we have . If the information is horizontal, by Lemma 2, . By Equation 2, there are three cases:

-

: in this case, backer will contribute for both conditions, .

-

: in this case, backer will not contribute for both conditions, .

-

: in this case, backer will not contribute if given , i.e., . If given either or , backer will either contribute or not contribute, i.e., .

Therefore, .

Proof of Lemma 3

If the right side holds for all , then : . According to Proposition 2, , where . That is, immediate disclosure is always preferred by all the backers in the campaign.

We prove it by contradiction. Assume, to the contrary, that such that is optimal for some . Without loss of generality, we let , where . Since , where , we have . Therefore, , which indicates that . According to Proposition 1, , which contradicts the supposition that is optimal.

Proof of Lemma 4

We prove it by contradiction. Assume, to the contrary, that: is not optimal for some . This indicates that at time , the entrepreneur could possibly profit by delaying information disclosure. Without loss of generality, we assume that is the disclosure strategy used in the optimal disclosure policy for backer , where . Depending on the relation between and , there are two cases (since ) : (i) ; (ii) .

-

: at time , the project has already succeeded, which means there is no uncertainty for backer since the campaign’s PoS is 1. Therefore, delaying disclosure does not increase backer ’s estimate on PoS, which contradicts the proposition that is not optimal.

-

: at time , backer ’s estimate , while . That is, (), which contradicts the proposition that is not optimal.

Appendix B Expert Algorithms

Random Selection

The random algorithm picks the project status at random from with equal probability. The expected increase of revenue is computed by averaging the revenue received when the entrepreneur disclosed the project status .

Greedy Selection

The greedy selection algorithm chooses the project status based on the empirical responses that the entrepreneur has received from the backers, using a one-step-look-ahead approach.

At time , given the disclosure strategy , the entrepreneur establishes a historical belief of the expected increase in the revenue, where , and :

| (8) |

where denotes the times that has been revealed to backers up to time . is backer ’s action given disclosure strategy . , and are the revenue growth rates up to time and , respectively. Note that if or .

The historical belief represents the entrepreneur’s estimate of the average revenue she receives by revealing project status to the backers, with discounting of the revenue growth rates. It is a rough estimate of revenue increase that brings.

At time , the entrepreneur’s temporal belief of the expected increase in the revenue given the disclosure decision , is determined as follows:

| (9) |

where denotes the set of backers in the campaign at time and is backer ’s action at time . If or , then . The temporal belief captures the latest decisions of the backers that will most probably stay in the campaign at time .

The entrepreneur estimates the belief of the expected increase of revenue, given for backer , with the following equation:

| (10) |

where is the learning rate (we use ).

The greedy algorithm then selects the project status by using the following equation:

| (11) |

The probability for selects the project status is 1 and 0 for others.

-Greedy Exploration

In -greedy exploration, with probability the algorithm selects a random choice . Otherwise, with probability it selects the greedy choice determined in Equation 11.

| (12) |

where is the times that has been reveled to backers up to time , , and is a constant. Note that if .

Softmax Exploration

Softmax selects the choice using a Boltzmann distribution Ross

et al. (1996). At time , the algorithm selects choice with the probability:

,

where is the temperature parameter.

Here, , when , and is determined by:

.

The softmax exploration selects each choice with a probability that is proportional to the average .

References

- (1)

- Agrawal et al. (2014) Ajay Agrawal, Christian Catalini, and Avi Goldfarb. 2014. Some simple economics of crowdfunding. Innovation Policy and the Economy 14, 1 (2014), 63–97.

- Agrawal et al. (2011) Ajay K Agrawal, Christian Catalini, and Avi Goldfarb. 2011. The geography of crowdfunding. Technical Report. National bureau of economic research.

- Alaei et al. (2016) Saeed Alaei, Azarakhsh Malekian, and Mohamed Mostagir. 2016. A Dynamic Model of Crowdfunding. In Proceedings of the 2016 ACM Conference on Economics and Computation. ACM, 363–363.

- Alonso and Camara (2016) Ricardo Alonso and Odilon Camara. 2016. Bayesian persuasion with heterogeneous priors. Journal of Economic Theory 165 (2016), 672–706.

- Arthur and Lane (1993) W Brian Arthur and David A Lane. 1993. Information contagion. Structural Change and Economic Dynamics 4, 1 (1993), 81–104.

- Au (2015) Pak Hung Au. 2015. Dynamic information disclosure. The RAND Journal of Economics 46, 4 (2015), 791–823.

- Bandura (1989) Albert Bandura. 1989. Human agency in social cognitive theory. American psychologist 44, 9 (1989), 1175.

- Bergemann and Morris (2016) Dirk Bergemann and Stephen Morris. 2016. Bayes correlated equilibrium and the comparison of information structures in games. Theoretical Economics 11, 2 (2016), 487–522.

- Bergemann and Pesendorfer (2007) Dirk Bergemann and Martin Pesendorfer. 2007. Information structures in optimal auctions. Journal of Economic Theory 137, 1 (2007), 580–609.

- Bergemann and Wambach (2015) Dirk Bergemann and Achim Wambach. 2015. Sequential information disclosure in auctions. Journal of Economic Theory 159 (2015), 1074–1095.

- Blackwell et al. (1953) David Blackwell et al. 1953. Equivalent comparisons of experiments. The Annals of Mathematical Statistics 24, 2 (1953), 265–272.

- Chambers and Echenique (2016) Christopher P Chambers and Federico Echenique. 2016. Revealed preference theory. Vol. 56. Cambridge University Press.

- Colombo et al. (2015) Massimo G Colombo, Chiara Franzoni, and Cristina Rossi-Lamastra. 2015. Internal social capital and the attraction of early contributions in crowdfunding. Entrepreneurship Theory and Practice 39, 1 (2015), 75–100.

- Crandall (2014) Jacob W Crandall. 2014. Towards minimizing disappointment in repeated games. Journal of Artificial Intelligence Research 49 (2014), 111–142.

- Easley and Ghosh (2015) David Easley and Arpita Ghosh. 2015. Behavioral mechanism design: Optimal crowdsourcing contracts and prospect theory. In Proceedings of the Sixteenth ACM Conference on Economics and Computation. ACM, 679–696.

- Ellman and Hurkens (2015) Matthew Ellman and Sjaak Hurkens. 2015. Optimal crowdfunding design. Available at SSRN 2709617 (2015).

- Hoare (1962) Charles AR Hoare. 1962. Quicksort. Comput. J. 5, 1 (1962), 10–16.

- Kahneman (2003) Daniel Kahneman. 2003. A perspective on judgment and choice: mapping bounded rationality. American Psychologist 58, 9 (2003), 697.

- Kamenica and Gentzkow (2011) Emir Kamenica and Matthew Gentzkow. 2011. Bayesian persuasion. The American Economic Review 101, 6 (2011), 2590–2615.

- Kau and Hill (1972) Paul Kau and Lowell Hill. 1972. A threshold model of purchasing decisions. Journal of Marketing Research (1972), 264–270.

- Kickstarter (2017) Kickstarter. 2017. Kickstarter Stats. https://www.kickstarter.com/help/stats. (2017). Online; accessed November 10th, 2017.

- Kuncheva and Whitaker (2003) Ludmila I Kuncheva and Christopher J Whitaker. 2003. Measures of diversity in classifier ensembles and their relationship with the ensemble accuracy. Machine learning 51, 2 (2003), 181–207.

- Kuppuswamy and Bayus (2015) Venkat Kuppuswamy and Barry L Bayus. 2015. Crowdfunding creative ideas: The dynamics of project backers in Kickstarter. (2015).

- Kuppuswamy and Bayus (2017) Venkat Kuppuswamy and Barry L Bayus. 2017. Does my contribution to your crowdfunding project matter? Journal of Business Venturing 32, 1 (2017), 72–89.

- Lee and Lin (2005) Gwo-Guang Lee and Hsiu-Fen Lin. 2005. Customer perceptions of e-service quality in online shopping. International Journal of Retail & Distribution Management 33, 2 (2005), 161–176.

- Marelli and Ordanini (2016) Alessandro Marelli and Andrea Ordanini. 2016. What Makes Crowdfunding Projects Successful Before and During the Campaign? In Crowdfunding in europe. Springer, 175–192.

- Marwell (2015) Nathan Marwell. 2015. Competing Fundraising Models in Crowdfunding Markets. Available at SSRN 2777020 (2015).

- Mollick (2014) Ethan Mollick. 2014. The dynamics of crowdfunding: An exploratory study. Journal of Business Venturing 29, 1 (2014), 1–16.

- Nisan and Ronen (1999) Noam Nisan and Amir Ronen. 1999. Algorithmic mechanism design. In Proceedings of the thirty-first annual ACM symposium on Theory of computing. ACM, 129–140.

- Ohannessian et al. (2014) Mesrob I Ohannessian, Mardavij Roozbehani, Donatello Materassi, and Munther A Dahleh. 2014. Dynamic estimation of the price-response of deadline-constrained electric loads under threshold policies. In American Control Conference (ACC), 2014. IEEE, 2798–2803.

- Pauker and Kassirer (1980) Stephen G Pauker and Jerome P Kassirer. 1980. The threshold approach to clinical decision making. New England Journal of Medicine 302, 20 (1980), 1109–1117.

- Rayo and Segal (2010) Luis Rayo and Ilya Segal. 2010. Optimal information disclosure. Journal of Political Economy 118, 5 (2010), 949–987.

- Ross et al. (1996) Sheldon M Ross et al. 1996. Stochastic processes. Vol. 2. John Wiley & Sons New York.

- Shen et al. (2017) Wen Shen, Alanoud Al Khemeiri, Abdulla Almehrzi, Wael Al Enezi, Iyad Rahwan, and Jacob W Crandall. 2017. Regulating Highly Automated Robot Ecologies: Insights from Three User Studies. In Proceedings of the 5th International Conference on Human Agent Interaction. ACM, 111–120.

- Shen et al. (2013) Wen Shen, Vahan Babushkin, Zeyar Aung, and Wei Lee Woon. 2013. An ensemble model for day-ahead electricity demand time series forecasting. In Proceedings of the fourth international conference on Future energy systems. ACM, 51–62.

- Shen et al. (2016) Wen Shen, Cristina V. Lopes, and Jacob W. Crandall. 2016. An Online Mechanism for Ridesharing in Autonomous Mobility-on-Demand Systems. In Proceedings of the Twenty-fifth International Joint Conference on Artificial Intelligence (IJCAI-16). 475–481.

- Short et al. (2017) Jeremy C Short, David J Ketchen, Aaron F McKenny, Thomas H Allison, and R Duane Ireland. 2017. Research on Crowdfunding: Reviewing the (Very Recent) Past and Celebrating the Present. Entrepreneurship Theory and Practice 41, 2 (2017), 149–160.

- Skirnevskiy et al. (2017) Vitaly Skirnevskiy, David Bendig, and Malte Brettel. 2017. The influence of internal social capital on serial creators’ success in crowdfunding. Entrepreneurship Theory and Practice 41, 2 (2017), 209–236.

- Solomon et al. (2015) Jacob Solomon, Wenjuan Ma, and Rick Wash. 2015. Don’t wait!: How timing affects coordination of crowdfunding donations. In Proceedings of the 18th ACM Conference on CSCW. ACM, 547–556.

- Strausz (2016) Roland Strausz. 2016. A Theory of Crowdfunding-a mechanism design approach with demand uncertainty and moral hazard. CEPR Discussion Paper No. DP11222 (2016).

- Strausz (2017) Roland Strausz. 2017. A Theory of Crowdfunding: A Mechanism Design Approach with Demand Uncertainty and Moral Hazard. American Economic Review 107, 6 (2017), 1430–76.

- Su (2007) Xuanming Su. 2007. Intertemporal pricing with strategic customer behavior. Management Science 53, 5 (2007), 726–741.

- Taneva (2015) Ina A Taneva. 2015. Information design. University of Edinburgh (2015).

- Whittle (1988) Peter Whittle. 1988. Restless bandits: Activity allocation in a changing world. Journal of applied probability (1988), 287–298.

- Yu et al. (2017) Sandy Yu, Scott Johnson, Chiayu Lai, Antonio Cricelli, and Lee Fleming. 2017. Crowdfunding and regional entrepreneurial investment: an application of the CrowdBerkeley database. Research Policy 46, 10 (2017), 1723–1737.

- Zhou et al. (2005) Yong-Pin Zhou, Ming Fan, and Minho Cho. 2005. On the threshold purchasing behavior of customers facing dynamically priced perishable products. University of Washington (2005).