A Modified Lévy jump diffusion model Based on Market Sentiment Memory for Online Jump Prediction

Abstract

In this paper, we propose a modified Lévy jump diffusion model with market sentiment memory for stock prices, where the market sentiment comes from data mining implementation using Tweets on Twitter. We take the market sentiment process, which has memory, as the signal of Lévy jumps in the stock price. An online learning and optimization algorithm with the Unscented Kalman filter (UKF) is then proposed to learn the memory and to predict possible price jumps. Experiments show that the algorithm provides a relatively good performance in identifying asset return trends.

Introduction

Stock price is considered as one of the most attractive index that people like to predict (?; ?). An important model for the stock price that has been built in the academia is Lévy process (?; ?; ?), which is a class of stochastic processes essentially show three features: a linear drift, a Brownian motion and a compound Poisson process. This model gains some success but it is pure random regarding the fluctuation.

With the external information of market and macroeconomics, a purely random compound Poisson process does not accurately reflect the fluctuation of the financial asset in a constantly changing financial environment. The necessity of developing a model that incorporates external signal from the market is critical in improving accuracy in financial derivative pricing. One of the incentive for accurate pricing is to avoid financial crisis. In 2007-2008, part of the financial crisis was caused by unforeseen drop in option prices. Researchers have tried to develop distributions other than a normal distribution for pricing noise (?), but not many have incorporated external signal for online learning and prediction.

Instead of trying to develop a model which takes accurate noise into consideration, we aim to develop in this paper a modified Lévy jump diffusion model with market sentiment memory to follow volatility clustering of financial assets, and a UKF algorithm to predict possible price jumps online. We intend to address the jump-diffusion effect in the financial market with big-data and machine learning technology to exploit market sentiment from Twitter. Different from previous approaches in financial asset pricing, the model involves non-Markovian processes with exponentially decaying memory, which can then be transformed into Markovian processes with higher dimension.

The main results of this paper include:

Incorporating market sentiment memory which has memory in financial asset pricing and developing a modified Lévy jump-diffusion model. We take the market sentiment memory as the signal of Lévy jumps in the pricing model (see Equations (16) and (17)).

Developing an unscented Kalman filter algorithm that actively learns market sentiment memory and accurately predicts asset trend accordingly (see Section Market Sentiment Memory UKF Optimization Algorithm).

Capturing majority of big asset price movements (asset price jumps) from market sentiment with relatively high accuracy. We found that outbreak of market sentiment indeed can predict majority of price jumps (see, for example, Figures 2 (a) and (c)).

Review of Current Work

Much academic effort to model the stock market has been devoted to produce a better mathematical model based on Levy process and geometric Brownian model as foundations. Geman in 2002 used Levy process modeled with normal inverse Gaussian model, generalized hyperbolic distributions, variance gamma model and CGMY process, which reduces the complexity of underlying Levy measure, and produced meaningful statistical estimation of stock prices (?). Cheridito in 2001 proposed fractional geometric Browniam motion model in order to gain a better estimate of stock price (?).

Other academic efforts have been put in the field of sentiment analysis and prediction based on market data and public views. Sul et al. in 2014 collected posts about firms in S&P 500 and analyzed their cumulative emotional valence and compared the return of firms with positive sentiment with other companies in S&P 500 and found significant correlation (?). Bollen et al. in 2011 also produced similar result that Tweet sentiment and stock price are strongly correlated in short term (?). Zhang and Skiena in 2010 used stock and media data to develop a automatic trading agent that was able to long and short stock based on sentiment analysis on media (Twitter and news platforms) data and getting a return as well as a high Sharpe ratio (?). Apart from pure sentiment analysis and trading strategies, Vincent and Armstrong in 2010 introduced prediction mechanisms also based on Twitter data to alert investors of breaking-point event, such as an upcoming recession (?).

In this paper, we propose a modified Lévy jump diffusion model where we replace the standard compound Poisson component with a process determined by an exponentially decaying market sentiment memory, while the latter is extracted by UKF. UKF is able to take into account the non-linear transformation between market sentiment and asset return compared with the linear Kalman filter in (?), where Duan et al. proposed using linear Kalman filter to model exponential term structures in financial and economic systems.

Background and preliminaries

In this section, we give a brief introduction to the Lévy jump-diffusion model for the price movement of assets and unscented Kalman filter. These are the building blocks for our modified Lévy jump-diffusion model with market sentiment memory and its algorithm.

Lévy Jump-Diffusion Model

In many theories such as Black-Scholes Model, the price movement of financial assets are modeled by the stochastic differential equation (SDE) driven by Brownian motion ((?, Chap. 10))

where is a standard Brownian motion. The solution of this SDE is known to be the geometric Brownian motion

is called the drift factor of the geometric Brownian motion and represents the log annual return of the financial asset. represents the volatility of daily return of the asset. An interesting fact is that does not affect option pricing in the Black-Scholes model (?; ?). However, if equals the interest rate , this geometric Brownian motion becomes risk-neutral and gives the Black-Scholes formula for the no-arbitrage cost of a call option directly (?, Chap. 7).

One of the drawbacks of the geometric Brownian motion is that the possibility of discontinuous price jumps is not allowed (?; ?). The Lévy Jump-Diffusion Model is one that tries to resolve this issue ((?, Chap. 8), (?)):

| (1) |

where i.i.d. are the jump parameters. i.i.d. are the Poisson parameters that control the occurance of the jump. and are constant parameters and are assumed to be mutually independent. The log return for day is given by:

| (2) |

The Lévy jump-diffusion model consists of three components. The first part, is the expected logarithmic return of the financial asset. The second component, is the white noise of the price or logarithmic return that is unpredictable. The third component, , is a compound Poisson distribution that provides a jump signal and a jump magnitude. The standard Lévy jump diffusion model intends to include the fat tails that have been generally observed in asset returns in addition to the Gaussian structure that is commonly assumed. The downside of Lévy jump diffusion model is that, although the model works well in a long-term structure, it fails to recognize market specific information that can be extracted from public opinion if used to predict short-term asset return.

Unscented Kalman Filter

In this section, we give a brief introduction to UKF ((?; ?)), which is used to give an accurate estimate of the state of nonlinear discrete dynamic system. Suppose that the state of a system evolves according to

| (3) |

where represents the state of the system at time , is the external input and is a noise with mean zero and covariance . is the known model of dynamics for . A measurement is then made to :

| (4) |

where is the measurement noise with mean zero and covariance , independent of . is the known measurement function.

Suppose that is the belief of the state at time and the covariance matrix of is . The general process of Kalman filter is given as follows:

-

•

Predict: Using the belief , , we obtain a predict (prior belief) of the state . Denote the covariance matrix of (current prior belief in process covariance matrix).

-

•

Update: Using the prediction , we have the predicted measurement . When we have the observation , we update the belief of the state at as

is the Kalman gain matrix computed as follows: first of all, we compute the approximation of the covariance matrix of the residue as , and the covariance matrix between and as . Then, the Kalman gain matrix is given as

The intuition is that this is the ration between belief in state and belief in measurement. The covariance matrix of is then computed as

In the case and are nonlinear, it is usually hard to compute the mean and covariance of and . The unscented transform computes these statistics as following: (i) generates () (deterministic) sigma points using , and , with certain weights and . (ii) Evolve these sigma points under , and obtain data . Then, the statistics are approximated using these data. The UKF makes use of the unscented transform to approximate , , and to second order accuracy. Hence, the cycle of UKF can be summarized as following:

1. Predict the next state from the posterior belief in the last step: (UKF.predict())

| (5) |

Here, is the algorithm to generate sigma points from the posterior belief . The standard algorithm is Van der Merwe’s scaled sigma point algorithm (?), which, with a small number of sampling with corresponding weights and , gives a good performance in belief state representation. See (?) for the formulas of and .

2. Update from prior belief to posterior belief according to current noisy measurement. (UKF.update())

| (6) |

Refer to (?) for the details of implementation of a UKF. An important aspect of UKF that can be utilized in estimating jump-diffusion process is its Gaussian belief. We can regard each Gaussian component in the compound Poisson distribution in jump-diffusion as a state belief of UKF and apply to UKF to obtain a stable transition function with current sentiment data as input.

Market sentiment

VaderSentiment

We aim to extract information from Twitter for both idiosyncratic sentiment information and market sentiment information. Before we present the implementation of data mining and analytics, we introduce VaderSentiment (?). For a given sentence , VaderSentiment produces,

| (7) |

where , and are respective signals calculated and is an overall evaluation of the quantitative sentiment of the sentence. Each of these signals are bounded within . Since we would like to extract instability of the sentiment analysis, we take vader’s neutral as the noise and the confidence level is defined by the value of . For each input sentence , we extract:

| (8) |

For a single day , we have,

| (9) |

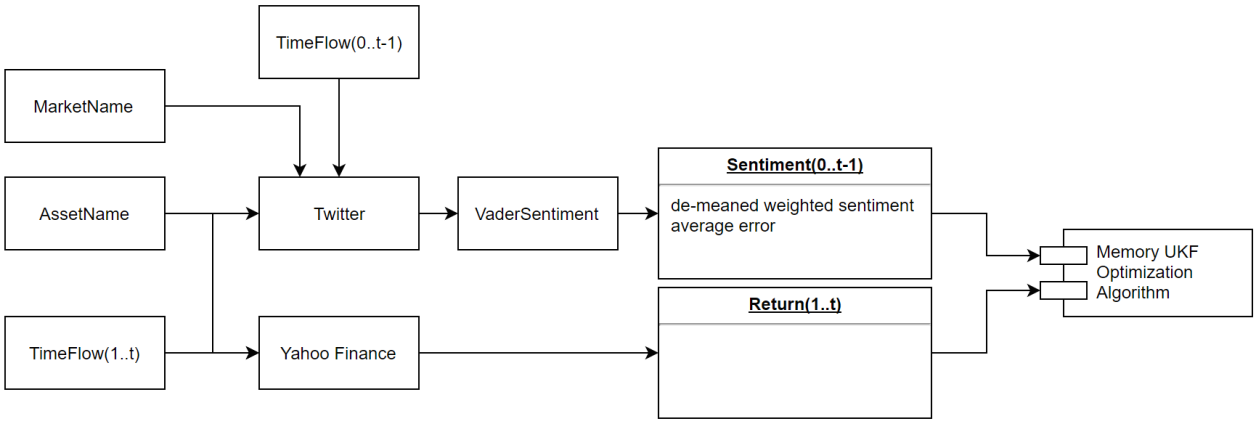

See Figure 1. At day t, from Twitter, we extract daily tweets from two pairs of keyword inputs, asset name (e.g. MSFT for Microsoft) and its trading market (e.g. NASDAQ) for idiosyncratic comments and trading sector (e.g. tech for Microsoft) and its trading market for market-related comments. For each day, we calculate idiosyncratic sentiment , macroeconomic sentiment , and the corresponding and from day t’s Tweets using (9). We then feed them into UKF sentiment memory optimization algorithm (which will be introduced in Section Model and Algorithm ) to learn the exponentially decaying memory model and then predict.

Market Sentiment Memory

We now consider adding the memory process of a random variable into the model:

| (10) |

where and are memory kernels and the second term represents the white noise. In this work, we assume throughout that the effect of white noise is negligible so that .

In general, the kernel could be completely monotone. By the Bernstein theorem, any completely monotone function is the superposition of exponentials (?). For approximation, we can consider finite of them:

| (11) |

The advantage of these exponential kernels is that we can decompose as

so that each satisfies the following SDE driven by :

| (12) |

In this way, the non-Markovian memory process is embedded into Markovian processes with higher dimension.

In this work, for simplicity, we just assume (i.e. the memory kernel is a single exponential mode) and consider the memories (denoted as ) of two individual sentiment inputs, idiosyncratic sentiment () and macroeconomic sentiment () so that the two sentiment processes are given by the discretized SDE (12):

| (13) |

where is called unit decay factor, and is called the inclusion factor. We define the market sentiment memory process as a linear combination of two components and with

| (14) |

For algorithmic development purpose, we impose

| (15) |

to limit the search space. Note that (15) is not a constraint because we later we care only. Enforcing only selects a scaling for .

Model and Algorithm

In this section we present a modified Lévy jump model for the asset. A UKF is then used to predict jump magnitude on the next day using computed market sentiment.

Modified Lévy Jump Diffusion Model

Recall the logarithmic return in Lévy jump diffusion (2). As we state in Section VaderSentiment, we would like to incorporate external information from social media to extract market sentiment, which contributes to asset return movements. Here we define the modified Lévy jump diffusion model,

| (16) |

where is the jump amplitude random variable. is a constant to take off the drift trend in (equivalent to in the Lévy jump diffusion model) and we compute in advance using history data.

We assume that the jump magnitude is determined by the total memory effect of market sentiment, or the market sentiment process in (14). In particular, we assume:

| (17) |

which indicates that a current jump magnitude is determined by the sentiment memory. An implication of this setting is that market sentiment value from an individual day is a kind of volatile velocity to the return of an asset. We assume that evolves with momentum so that it satisfies the order 1 autocorrelation model (AR(1)):

| (18) |

with being a constant for the innovation and being a discrete white noise.

Market Sentiment Memory UKF Optimization Algorithm

In this section, we introduce a UKF optimization algorithm. In the algorithm, the drift is determined in advance, which is the daily return in the long history, we set in (18), and preset ’s in Equation (14) for each iteration. The algorithm is used to find the optimal , and defined in Equation (13) and (18) with in-sample data .

State of the system is represented as

and the input vector is

The dynamics of the system (see (3)) is given by:

| (19) |

with being the parameters.

We define true return on day and

as the measurements of and :

| (20) |

Motivated by the fact that are random, we assume the measurement noise variance is a combination of that for and :

where and are confidence level of sentiment values computed by the second equation in (9). The randomness in and provides noise for the evolution and .

We introduce here Jenson’s alpha and beta market risk to set and in (14). Beta market risk is defined as (?):

| (21) |

where is the market log return. Jenson’s alpha is:

| (22) |

where is individual return and is risk free rate (, are all computable from current data). Using Jenson’s risk, we set

| (23) |

for computing .

We define the objective function in the optimization.

| (24) |

In the formula,

represents the set of jumps 1.96 standard deviations away from the process mean, or 1.96 volatility from the drift factor. indicates positive jumps and indicates negative jumps. What we aim to achieve here is that jumps identified by UKF overlaps the most with the actual jumps that happens. The major goal of UKF Optimization is essentially trying to identify a trend in the asset return time series.

With the settings above, we present the UKF optimization algorithm for searching optimal , and , with restriction that and .

where is the objective function of UKF-Optimization algorithm defined in (24). means if is bigger than the old , we update to the new parameter and keep the old values otherwise.

We first use with in-sample data to find the optimal , and for the maximum coverage on the actual jumps. After the optimal parameters are obtained, we use UKF predict the Stoke price using Model (16) online.

The UKF is generally used for state transition learning where the transition rules and noises are relatively stable. One reason is that during a near-stationary process, state belief is generally strengthened such that state transition converges. The Kalman gain factor, due to a strong belief in state, with very small covariance, quickly approaches 0. Consequently, UKF has learned pattern of state transition and is only mildly adjusted by input. In our case, the economic process has different trends in different time windows while the UKF is hardly used to model a non-stationary process. A critical idea of learning the non-stationary economic model using UKF in our model is that, we would not want to model observations from the market as a sensor with fixed volatility. The volatility clustering effect of asset returns can greatly impact the training result. Here we model the volatility clustering effect with sentiment error term. The significance of this algorithm is that with a small modification, UKF can be used to learn multiple exponentially decaying sentiment memory with guaranteed process covariance convergence performance even given a chaotic non-linear system(?) with a quadratic time complexity over the standard UKF by searching the coefficient space with some acceptable coefficient error. Note that the output of UKF is not a strictly exponentially decaying memory due to its non-pre-deterministic Kalman gain parameter.

Experiment

We now present the experimental results for Facebook (FB), Microsoft (MSFT) and Twitter (TWTR).

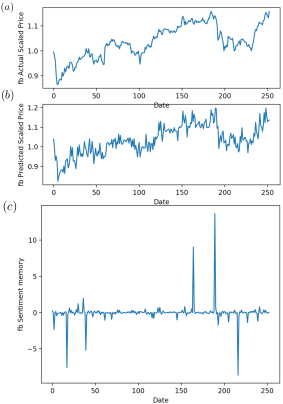

Figure 2 (a) and 2 (b) represent the actual return and the UKF return prediction based the modified Lévy jump diffusion model for FB during the time period from 2016-02-03 to 2017-02-02 (note that there are only trading days in a year). The parameters are trained by the UKF optimization algorithm using date from 2013-02-02 to 2016-02-02. The jump prediction precision is . The in-sample prediction precision for time period 2013-02-02 to 2016-02-02 is . Figure 2 (c) shows (we have offset in the memory plot because we use to do the prediction for day ) .

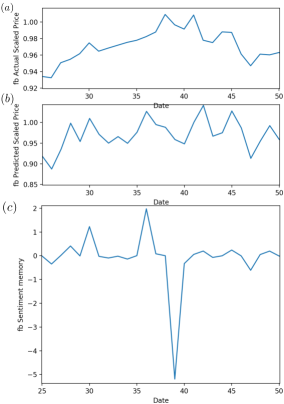

The spikes in indicate outbreaks of market sentiment. To see how these spikes affect the jump prediction, we zoom in the plots for FB from Day to Day in Figure 3. There are evident spikes in for . For and , the real stock price curve has abnormal jumps, and our prediction of jumps based on the setiment memory has accurately predicted them. There is big outbreak of sentiment for , and we can see that the real stock price goes down on Day and . This indicates that the jumps in stock price curve are strongly correlated to market sentiment memory process and our model is able to predict a significant amount of abnormal jumps.

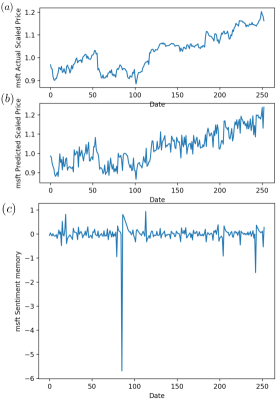

Figure 4 (a) and 4 (b) represent the actual return and the UKF return prediction for MSFT during the time period from 2016-02-02 to 2017-02-02, with training data from 2010-02-02 to 2016-02-02. The jump prediction precision is . The in-sample prediction precision for time period 2010-02-02 to 2016-02-02 is . Figure 4 (c) shows the market sentiment memory process (Eq. (14)) .

Figure 5 (a) and 5 (b) represent the actual return and the UKF return prediction for TWTR during the time period from 2016-02-03 to 2017-02-02, with the training data from 2014-02-02 to 2016-02-02. The jump prediction precision is . The in-sample prediction precision for time period 2014-02-02 to 2016-02-02 is . Figure 5 (c) shows the memory process .

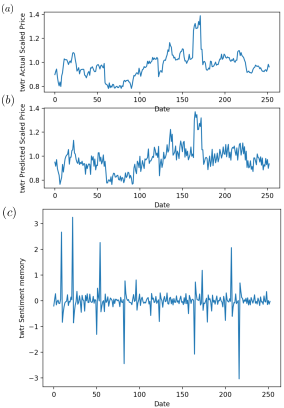

There are a few significant observations we can draw from the results.

1. Using UKF generally captures the movement trend of the underlying asset, with little guidance with daily returns. More specifically, during periods where sentiment memory kernel value peaks, the stock asset’s return has very strong correspondence. However, when there is very minor value in market sentiment kernel, the asset return prediction follows the previous trading day’s return, triggering some inaccuracy.

2. Movements in UKF return prediction are in general greater in magnitude than actual returns. This could be caused by high volatility of sentiment values.

3. From the sentiment memory graphs (Figures 4- 5 (c)), we can observe a strong indication of clustering, which is an evidence of a decaying memory, analogous to GARCH model (?) which measures volatility clustering. This can also be confirmed by trained parameters from UKF-optimization algorithm:

MSFT: .

FB: .

TWTR: .

Discussion

In this paper, we propose a modified Lévy jump diffusion model with market sentiment memory for stock prices. An online learning and optimization algorithm with UKF is used to predict possible price jumps. The result from the experiments instantiate our theory in market sentiment memory and its impact on asset returns. Our work has significance in both economics and computer science.

Regarding economics, our experiments have shown the existence of predictability in return by sentiment, which indicates market inefficiency in digesting public sentiment. The impact of market sentiment memory on asset returns can dramatically change the pricing models for options and financial derivatives because currently most of these products rely on the Markovian assumption about financial assets. To incorporate market sentiment memory into the pricing models, one possible way is to multiplying previous jumps occurring in asset’s return history with decaying factors and then add the models, since jumps are strong indicators of market sentiment outbreak. Another possible way is to include a time series of market sentiment with explicit values into asset pricing models. Clearly, our model adopts the second strategy.

Regarding computer science, our work indicates that Kalman filter techniques (especially UKF) allow online learning for non-observable variables. The market sentiment memory can not be measured directly and it is an indirect variable, however, unlike other machine learning techniques, UKF allows online learning of such indirect variables in an iterative manner.

References

- [Bollen, Mao, and Zeng 2011] Bollen, J.; Mao, H.; and Zeng, X. 2011. Twitter mood predicts the stock market. Journal of Computational Science 2(1):1–8.

- [Bollerslev 1986] Bollerslev, T. 1986. Generalized autoregressive conditional heteroskedasticity. Journal of econometrics 31(3):307–327.

- [Borland 2002] Borland, L. 2002. Option pricing formulas based on a non-gaussian stock price model. Physical review letters 89(9):098701.

- [Cheridito 2001] Cheridito, P. 2001. Regularizing fractional brownian motion with a view towards stock price modelling. Dissertation at Swiss Federal Institute of technology Zurich.

- [Cont and Tankov 2003] Cont, R., and Tankov, P. 2003. Financial modelling with jump processes, volume 2. CRC press.

- [Duan and Simonato 1999] Duan, J.-C., and Simonato, J.-G. 1999. Estimating and testing exponential-affine term structure models by kalman filter. Review of Quantitative Finance and Accounting 13(2):111–135.

- [Feng, Fan, and Chi 2007] Feng, J.; Fan, H.; and Chi, K. T. 2007. Convergence analysis of the unscented kalman filter for filtering noisy chaotic signals. In Circuits and Systems, 2007. ISCAS 2007. IEEE International Symposium on, 1681–1684. IEEE.

- [Geman 2002] Geman, H. 2002. Pure jump levy process for asset price modelling. Journal of Banking and Finance.

- [Hutto and Gilbert 2014] Hutto, C. J., and Gilbert, E. 2014. Vader: A parsimonious rule-based model for sentiment analysis of social media text. In Eighth International AAAI Conference on Weblogs and Social Media.

- [Jensen 1968] Jensen, M. C. 1968. The performance of mutual funds in the period 1945–1964. The Journal of finance 23(2):389–416.

- [Julier and Uhlmann 1997] Julier, S. J., and Uhlmann, J. K. 1997. New extension of the kalman filter to nonlinear systems. In AeroSense’97, 182–193. International Society for Optics and Photonics.

- [Ornthanalai 2014] Ornthanalai, C. 2014. Levy jump risk: Evidence from options and returns. Journal of Financial Economics 112(1):69–90.

- [Papapantoleon 2000] Papapantoleon, A. 2000. An introduction to levy processes with applications in finance. Mathematics Subject Classification.

- [Ross 2011] Ross, S. M. 2011. An elementary introduction to mathematical finance. Cambridge University Press.

- [Steele 2012] Steele, J. M. 2012. Stochastic calculus and financial applications, volume 45. Springer Science & Business Media.

- [Sul, Dennis, and Yuan 2014] Sul, H. K.; Dennis, A. R.; and Yuan, L. I. 2014. Trading on twitter: The financial information content of emotion in social media. In System Science (HICSS), 47th Hawaii International Conference.

- [Van Der Merwe 2004] Van Der Merwe, R. 2004. Sigma-point Kalman filters for probabilistic inference in dynamic state-space models. Ph.D. Dissertation, Oregon Health & Science University.

- [Vincent and Armstrong 2010] Vincent, A., and Armstrong, M. 2010. Predicting break-points in trading strategies with twitter. SSRN.

- [Wan and Van Der Merwe 2000] Wan, E. A., and Van Der Merwe, R. 2000. The unscented kalman filter for nonlinear estimation. In Adaptive Systems for Signal Processing, Communications, and Control Symposium 2000. AS-SPCC. The IEEE 2000, 153–158. Ieee.

- [Widder 1941] Widder, D. 1941. The Laplace Transform. Princeton University Press.

- [Zhang and Skiena 2010] Zhang, W., and Skiena, S. 2010. Trading strategies to exploit blog and news sentiment. Association for the Advancement of Artificial Intelligence (AAAI).