Hurst estimation of scale invariant processes with drift and stationary increments

Abstract

The characteristic feature of the discrete scale invariant (DSI) processes is the invariance of their finite dimensional distributions by dilation for certain scaling factor.

DSI process with piecewise linear

drift and stationary increments inside prescribed scale intervals is introduced and studied.

To identify the structure of the process, first we determine the scale intervals, their linear drifts and eliminate them.

Then a new method for the estimation of the Hurst

parameter of such DSI processes is presented and applied to some period of the Dow Jones indices.

This method is based on fixed number equally spaced samples inside successive scale intervals. We also present some efficient

method for estimating Hurst parameter of self-similar processes with stationary increments. We compare the performance of this method with the celebrated FA, DFA and DMA on the simulated data of fractional Brownian motion.

Mathematics Subject Classification MSC 2010: 62L12; 60G22; 60G18.

keywords: Discrete scale invariance; Hurst estimation; Fractional Brownian motion; Scale parameter.

1 Introduction

Scale invariance or self-similarity has been discovered, analyzed and exploited in many frameworks, such as natural images [23], fluctuations of stock market [11], [12] and traffic modeling in broadband networks [1], [21]. These processes are invariant in distribution under suitable scaling of time and space. Discrete scale invariant (DSI) processes are invariant by dilation for certain preferred scaling factors or the observable obeys scale invariance for specific choices of scale [8], [24], [28]. In practice, the main object is detecting the scale invariant property and estimating the Hurst index and scale parameter of such processes [5]. Estimation methods depend on several factors, e.g, the estimation technique, sample size, time scale, level shifts, correlation and data structure. Among all estimation methods for scale invariant and long-memory processes, the rescaled adjusted range or statistic and semi-variogram are frequently used, see Beran [7]. Balasis et al. used the statistic in [3] and the wavelet spectral analysis in [4] to estimate the Hurst exponents for self-similar time series originated from space physics applications. Recently, Wang [27] presented a moving average method to estimate the Hurst exponent. Vidacs and Virtamo obtained maximum likelihood estimator of the Hurst parameter based on some geometric sampling of the fractional Brownian motion (fBm) traffic [25]. Some estimation methods of Hurst index are based on variance-time, see [9], [10]. In the econophysics, there are some celebrated methods for the estimation of Hurst parameters called fluctuation analysis (FA) [17], detrended fluctuation analysis (DFA) [18] and detrending moving average (DMA) which is described in [2].

Regression analysis is a form of predictive modeling technique which allows to detect the trend of time series. We apply some piece-wise linear regression to detect drift to the DSI processes.

Especially we determine such piece-wise linear drift by applying regression lines to the plots of the corresponding scale intervals of DSI processes.

In real data scale invariant behavior often occures with some linear drift. To dtermine the structure of such processes one need to eliminate the drift first, and then estimate the Hurst parameter.

Brownian motion with drift is an example of scale invariant processes with drift which has lots of applications in mathematical finance and stock price modelings l [22].

Usually the DSI behavior of the processes are characterized by detecting some regular behavior of the process inside successive scale intervals which can be identified by fitting homologous parabolas.

In this paper we present some flexible sampling scheme which provide some fixed number equally spaced sample points in each scale interval.

This sampling scheme provide a bases for our estimation method of Hurst parameter.

Then a DSI process with drift is introduced where by evaluating successive scale intervals, the evaluation and elimination of the linear piece-wise drift is studied.

Then a new innovative method for the estimation of Hurst parameter of DSI processes, having stationary increments inside scale intervals, is developed.

Finally we present some heuristic estimator of the Hurst parameter of self-similar processes with stationary increments (Hsssi).

The performance of this estimator are examined by using simulated data.

We show that our method is more efficient than the FA, DFA and DMA methods.

We compare our method using simulated samples of fractional Brownian motion (fBm) with drift and different Hurst parameters and show that the mean square error (MSE) of our method is much less than the compared methods.

The paper is structured as follows. In section 2, we present our flexible discrete sampling scheme and provide intuition on some basic notions of the scale invariance and DSI processes in discrete parameter space.

Section 3 is devoted to introducing DSI processes with drift, piece-wise linear drift and its elimination. We also present our estimation methods for scale and Hurst parameter of DSI processes while the increments are stationary inside scale intervals, and apply

our estimation methods to some part of Dow Jones indices in section 3.

A heuristic method for estimating the Hurst parameter of self-similar process with stationary increments is developed and its performance is compared with the celebrated methods FA, DFA and DMA for simulated data of fBm in section 4.

Conclusions are presented in section 5.

2 Method of Flexible Discrete Sampling

For our estimation method some appropriate sampling scheme is required. Current authors [14] considered geometric sampling at points , of DSI processes with scale , where is determined by , and is some predefined number of observations in the scale interval , .

Here we present some basic definitions and flexible sampling for DSI processes, see [15].

A process is called discrete time self similar (or scale invariant) process with parameter space ,

where is any subset of countable distinct points of positive real numbers, if for any , where denotes equality of finite dimensional distributions.

The process is called discrete time DSI process with scale and parameter space , if for any , the above equation holds in distribution. So

sampling of at points , , we have a discrete time scale invariant process with parameter space .

A random process is called self-similar ( scale invariant) in the wide sense with Hurst index and parameter space , if for all and all , where we have that , and . If these properties hold for some then the process is called wide sense DSI with parameter space , see [14].

Following Modarresi and Rezakhah [15] we consider discrete flexible sampling of DSI process with scale by

choosing arbitrary sample points of in the first scale interval as

as and sampling in the scale interval , , at points , . So by recalling sample points with our sample space are being .

3 DSI processes with drift

For the real data, DSI behavior often occurs in short periods. The Dst time series [5] and stock market indices [6], [15], [16] and [19] are some examples of such situations. The change of drift is another feature that specially occurs by the changes in growth of stock markets. So their simultaneous effect can not be ignored. There are many examples in modeling the behavior of stock prices by Brownian motion with drift [13]. Besides the regression modeling approaches, Brownian motion with linear drift has drawn much attention in prognostics [26]. Here we present the definition of Brownian motion with linear drift.

Definition 3.1

The process is a Brownian motion with drift coefficient and variance parameter if , the process has stationary and independent increments and is normally distributed with mean and variance . Equivalently is Brownian motion with drift, where the standard Brownian motion is self-similar.

Now we present the definition of DSI processes with piece-wise linear drift, which we apply in subsection 3.3 to model some part of the Dow Jones indices .

Definition 3.2

A process is DSI process with drift if it satisfies the relation , where is a DSI process and is a drift function. We call the process , DSI with piece-wise linear drift if the drift consist of different line in successive scale intervals of the DSI process as , where and are real numbers and is the -th scale interval for .

Following the idea of the Brownian motion with drift, described in [22], and simple Brownian motion as a DSI process, described in [14], we present an example, which we call simple Brownian motion with drift as a flexible pattern for modeling more comprehensive processes with DSI behavior.

Example: Following Modarresi et al. [16] we call a process a simple Brownian motion with drift , the Hurst index and scale if

where is the standard Brownian motion, an indicator function. The expected value of the process is

Also for , the covariance function of the process is determined as

This by the fact that . One can easily verify that is a DSI process. As in the real world the DSI behavior just appears locally in different processes, one need to detect the DSI period first.

The rest of this section can be described as follows. In this section we introduce DSI processes with drift and give an example which has Markov property. In subsection 3.1 we study the detection and elimination of the piece-wise linear drift to the DSI processes. In subsection 3.2 we introduce some innovative method for estimating the Hurst parameters of DSI processes with stationary increments. In subsection 3.3 we apply our estimation method for estimating the Hurst parameter of real data as some part Dow Jones indices.

3.1 Elimination of the drift

We consider the DSI process with piece-wise linear drift as in some duration of time, say , where is a DSI process and the drift is assumed to be

piece-wise linear function of time as where is some partition of this duration.

For decomposition of as above and detecting the DSI behavior of one need to estimate such piece-wise linear drift and eliminate it from the main process first. For this, we need to detect the corresponding scale intervals of the main process by fitting some parabola as has been applied in [6] and [15]. Then we fit separate regression lines to the samples of successive scale intervals of main process . These regression lines are considered as piece-wise linear drift to the process .

Then we eliminate the drift by subtracting from to obtain the DSI process . Eliminating this drift Then one can estimate the Hurst parameter of the corresponding DSI process by the following method.

Using detected scale intervals of for the corresponding DSI process , we consider some fixed number of equally spaced samples in each scale interval,

say . By this and the assumption that the process have stationary increment property inside each scale interval, we conclude that the increments arises by this sampling method inside each scale interval are identically distributed.

Now we consider the following procedure for the estimation of the parameters of the DSI process .

3.2 Estimation procedure

Let be a DSI process with stationary increment property inside each scale interval. This cause the increments of equally spaced samples inside each scale interval to be identically distributed. Our

estimation method is presented by the following steps.

1- The time interval that we study the DSI process is considered as .

2- Following the methods of Bartolozzi et al. [6] and Modarresi et al. [15] and [16], we evaluate scale intervals by fitting appropriate parabola to the samples of the period .

So the scale of the process can be estimated by

where is the number of the scale intervals.

3- We consider equally spaced sample points in each scale interval so that the sample points of -th scale interval are determined as , where , and . So is the number of observations in each scale interval. Thus our parameter space is and is a DSI process with parameter space .

4- Now we consider as the increment process, where ,

and ,

where , the sample variance of increments in the -th scale interval, .

5- By the scale invariant property of the process we have that for , so , where . Estimating by , one can evaluate the estimation of the Hurst parameter by .

Denoting , we have estimate for as , and the final estimation of is evaluated as the mean of these .

This estimation method of the Hurst parameter is based on the first order of the increments. We also consider the second order difference of the increments inside scale intervals and evaluate the sample variance

of corresponding to -th scale interval by

and , .

Also we have that

, where .

Estimating by , one can estimate the Hurst parameter by

.

Denoting , , we have the final estimation of as mean of these .

3.3 Real data analysis

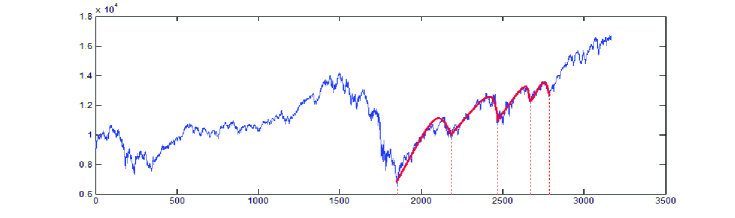

As an example of DSI process with drift we consider daily indices of Dow Jones from 25/10/2001 till 28/5/2014 and try to estimate the relevant parameters. As these indices are no available on Saturdays, Sundays and holidays, the available indices for this duration are 3168 days, which are plotted in Figure 1 (left). For the duration of the study 6/3/2009 till 14/11/2012 corresponding to the sample points we have evaluated a drift line as . So the existence of the drift is clear by the fitted drift line which is shown in Figure 1. The DSI samples which has been evaluated by differencing the data set from this drift line is plotted in the bottom panel of the Figure 1 (right) which shows the DSI behavior. The fitted red lines reveals the scale intervals of DSI variation with drift for the period 6/3/2009 till 14/11/2012. The end points of these scale intervals are . The scale parameter is estimated as mean of the ratio of length of successive scale intervals, so the time dependent scale parameters are estimated as and their mean as .

|

|

|

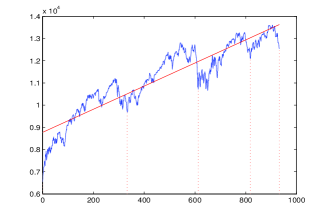

Now we consider some fixed number of equally spaced samples in each two consecutive interval. Then we estimate their corresponding Hurst parameter as the logarithm of the ratio of sample variance of increments in such successive scale intervals.

This is done after eliminating the drifts by different drift lines which have been fitted to the samples of scale intervals separately. The slop of successive drift lines from the left are and share index unit per day, respectively.

Therefore where is the sample variance of increments inside -th scale interval after eliminating the corresponding drift. Dividing this value by we estimate the time dependent Hurst parameters for the variation of -th scale interval with respect to the previous one. A new method for the time dependent Hurst parameter estimation which is more accurate estimation was studied [19].

This evaluation leads to the estimation of time dependent Hurst parameters as with mean .

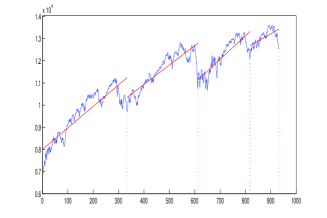

We should remind that considering such drift lines has two advantages. First it causes to model the mean changes of the process by such regression lines and the second advantage is that it reveals the true DSI behavior of the process after eliminating such drifts. For more clarification we represents here the estimated Hurst parameters without fitting such drift lines as

and for the Hurst parameters of second, third and fourth scale intervals with respect to the previous scale intervals. Also when we fit just one drift line to the whole duration of DSI behavior and eliminating such drift from the data the corresponding Hurst parameters are estimated as and . Comparing the variations of these estimates with the ones that were estimated by eliminating different drifts for successive scale intervals, reveals that those estimates are more close to each other and are more promising since all estimates are in the range . Also the bottom panel of Figure 1 (right) shows such drift provides much better estimation of share indices.

4 Comparison of Estimation methods for Hurst parameter of HSSSI process

In this section we develop the method presented in [20] for the estimation of Hurst parameter of the scale invariant processes with stationary increments. We consider the case that the scale invariant processes could have linear drift. Let be equally spaced samples of such a process. For this, first we eliminate the drift. We estimate this drift by the regression line by evaluating and . Then we eliminate the drift from the process as . Now we are to estimate the Hurst parameter from this new process . Following the method of sampling of Rezakhah et al. [20], we consider sub-samples at points as the -th sub-sample for some fixed . Choosing depends on the sample size we take . We consider }. For every we consider two kind of sampled process and , where , and evaluate first and second order sample variances for

| (4.1) |

where and correspondingly. One can easily verify that for . So , where and . Thus and are corresponding sample variances and estimates of and respectively. So for different values of we evaluate by the relation.

| (4.2) |

and estimate as the mean of such different ’s by

| (4.3) |

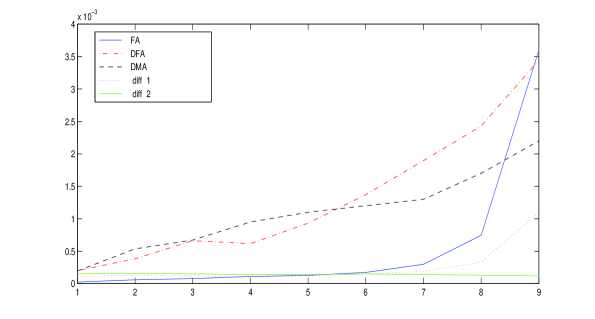

Now we compare the performance of the introduced method for estimation of Hurst parameter with FA, DFA and DMA methods. First we simulate 10000 samples from fBm with different Hurst parameters as . Then we estimate the Hurst parameters by different methods, FA, DFA, DMA and our two methods first difference (diff 1) and second difference (diff 2) ones with 500 repetitions. The MSE of the methods are plotted in Figure 2. As it is shown in the figure, the diff 2 method always have much better performance than the previous methods. The diff 1 method is the best for the Hurst parameters between and , but for Hurst between and the diff 2 method is the best.

5 Conclusions

In this paper some heuristic method for the estimation of scale and Hurst parameter of discrete scale invariant processes with piece-wise linear drift. As many DSI processes are accompanied by some piece-wise linear drift, the method of this paper in estimating and eliminating of such piecewise drifts, motivates further research in this way and provide a platform to extend the applications of DSI processes. So one would expect to have a better understanding of the processes involving DSI behavior. As an example, for the presented part of Dow Jones indices it is shown that the DSI behavior is accompany with piece-wise linear drift. We also presented new method to improve estimation of the Hurst parameter of DSI processes. Comparing the presented method for the estimation of the Hurst parameter of Hsssi processes with the celebrated methods FA, DFA and DMA shows its superior by producing less mean squared errors. This paper could initiate further research and application in compare to the existing methods by applying our method in estimating and eliminating different piece-wise drifts. Our method has the privilege to present a better estimation of the Hurst parameter of DSI processes by eliminating such additional structure for the variations.

References

- [1] P. Abry, P. Goncalves, J.L. Vehel (2010) Scale invariance in computer network traffic, Scaling Fractals and Wavelets, 413-436.

- [2] E. Alessio, A. Carbone, G. Castelli, V. Frappietro (2002) Second-order moving average and scaling of stochastic time series, Eur. Phys. J. B 27, 197.

- [3] G. Balasis, I.A. Daglis, A. Anastasiadis, K. Eftaxias (2011) Detection of dynamical complexity changes in Dst time series using entropy concepts and rescaled range analysis, in ”The dynamic magnetosphere”, IAGA Special Sopron Book Series, Springer, Vol. 3, 211-220.

- [4] G. Balasis, I.A. Daglis, C. Papadimitriou, M. Kalimeri, A. Anastasiadis, K. Eftaxias (2009) Investigating dynamical complexity in the magnestosphere using various entropy measures, J. Geophys. Res., 114, A00D06.

- [5] G. Balasis, C. Papadimitriou, I.A. Daglis, A. Anastasiadis, L. Athanasopoulou, K. Eftaxias (2011) Signatures of discrete scale invariance in Dst time series, Geophys. Res. Lett., 38, L13103/1-6, doi:10.1029/2011GL048019.

- [6] M. Bartolozzi, S. Drozdz, D.B. Leieber, J. Speth, A.W. Thomas (2005) Self-similar log-periodic structures in Western stock markets from 2000, International Journal of Modern Physics C, Vol.16, No.9, pp. 1347-1361.

- [7] J. Beran (1994) Satistics for long memory processes, Chapman and Hall, NewYork.

- [8] P. Borgnat, P.O. Amblard, P. Flandrin (2005) Scale invariances and Lamperti transformations for stochastic processes, J. Phys. A: Math. Gen., Vol.38, No.10, 2081-2101.

- [9] A. Chronopoulouc, C. Tudor, F.G. Viens (2010) Self-similarity parameter estimation and reproduction property for non-Gaussian Hermite processes, Communications in Stochastic Analysis, Vol. 5, No. 1, 161-185.

- [10] J.F. Coeurjolly (2001) Estimating the parameters of a fractional Brownian motion by discrete variations of its sample paths, Statistical Inference for Stochastic Processes, 4, 199-227.

- [11] R. Cont, M. Potters, J.P. Bouchaud (1997) Scaling in stock market data: stable laws and beyond, Scalin Invariance and Beyond, 75-85.

- [12] J.A. Feigenbaum, P.G.O. Freund (1996) Discrete scale invariance in stock markets before crashes, Int. J. Mod. Phys.B, Vol.10, Issue.27, 3737-3745.

- [13] J. Hull (2009) Options, Futures, and other Derivatives, 10 ed., Pearson/Prentice Hall.

- [14] N. Modarresi, S. Rezakhah (2010), Spectral analysis of Multi-dimensional selfsimilar Markov processes, Journal of Physics A: Mathematical and Theoretical, Vol.43, No.12, 125004, 14pp.

- [15] N. Modarresi, S. Rezakhah (2013) A new structure for analyzing discrete scale invariant processes: Covariance and Spectra, Journal of Statistical Physics, Vol.152(6), 15pp.

- [16] N. Modarresi, S. Rezakhah (2016) Characterization of Discrete Scale Invariant Markov Sequences, Communications in Statistics: Theory and Methods, 45, 18, 5263-5278 .

- [17] C.K. Peng, S.V. Buldyrev, A.L. Goldberger, S. Havlin, F. Sciortino, M. Simons, H.E. Stanley (1992) Long range correlations in nucleotide sequences, Nature 356, 168.

- [18] C.K. Peng, S.V. Buldyrev, S. Havlin, M. Simons, H.E. Stanley, A.L. Goldberger (1994) Moaic organization of DNA nucleotides, Phys. Rev. E 49, 1685.

- [19] S. Rezakhah, Y. Maleki (2016) Discretization of continuous time discrete scale invariant processes: estimation and spectra, Journal of Statistical Physics, Vol.164(2), pp. 438-448.

- [20] S. Rezakhah, A. Philippe and N. Modarresi (2017) Innovative methods for modeling of scale invariant processes. Communication in Statisctics: Theory and Methods, Accepted.

- [21] R. Rao, S. Lee (2000) Self-similar network traffic characterization through linear scale invariant system models, IEEE Int. Con. On Personal Wireless Communications. Conference Proceedings.

- [22] S.M. Ross (2014) Variations on Brownian Motion, Introduction to Probability Models, 11th ed., Amsterdam: Elsevier, 612-614.

- [23] D.L. Ruderman (1997) Origins of scaling in natural images, Vision Research, 37, 3385-3398.

- [24] D. Sornette (1998) Discrete scale invariance and complex dimensions, Physics Reports, 297, 239-270.

- [25] A. Vidacs, J. Virtamo (1999) ML estimation of the parameters of fBm traffic with geometrical sampling, IFIP TC6, Int. Conf. on Broadband communications 99, Hong-Kong.

- [26] W. Wang, M. Carr, W. Xu, K. Kobbacy (2011) A model for residual life prediction based on Brownian motion with an adaptive drift, Microelectron. Reliab., 51, 285-293.

- [27] N. Wang, Y. Li, H. Zhang (2010) Hurst exponent estimation based on moving average method, Advances in Wireless Networks and Information Systems, Vol.72, 137-142.

- [28] W.-X. Zhou, D. Sornette (2009) Numerical investigations of descrete scale invariance in fractals and multifractal measures, Physica A. Stat. Mech. App., Vol.388, No. 13, 2623-2639.