Confidence Intervals that Utilize Uncertain Prior Information about Exogeneity in Panel Data

Paul Kabaila∗ and Rheanna Mainzer∗∗

La Trobe University

ABSTRACT

Consider panel data modelled by a linear random intercept model that includes a time-varying covariate. Suppose that we have uncertain prior information that this covariate is exogenous. We present a new confidence interval for the slope parameter that utilizes this uncertain prior information. This interval has minimum coverage probability very close to its nominal coverage. Let the scaled expected length of this new confidence interval be its expected length divided by the expected length of the confidence interval, with the same minimum coverage, constructed using the fixed effects model. This new interval has scaled expected length that (a) is substantially less than 1 when the prior information is correct, (b) has a maximum value that is not too much larger than 1 and (c) is close to 1 when the data strongly contradict the prior information. We illustrate the properties of this new interval using an airfare data set.

* Corresponding author. Department of Mathematics and Statistics, La Trobe University, Victoria 3086, Australia. e-mail: P.Kabaila@latrobe.edu.au

** Department of Mathematics and Statistics, La Trobe University, Victoria 3086, Australia. e-mail: rmmainzer@students.latrobe.edu.au

1 INTRODUCTION

We consider panel data modelled by a linear random intercept model that includes a time-varying covariate. Irrespective of whether or not this covariate is exogenous, valid inference results from the fixed effects model. However, if this covariate is exogenous then valid and more efficient inference results from the random effects model. This greater efficiency motivates the use of this model, whenever it is appropriate, for inference.

The Hausman (1978) pretest is commonly used in practice to decide whether or not subsequent inference will be based on the assumption that the time-varying covariate is exogenous. If the null hypothesis that this covariate is exogenous is accepted then the random effects model is used for subsequent inference; otherwise the fixed effects model is used (see e.g. Hastings, 2004, Papatheodorou and Lei, 2006, Choe, 2008, and Jackowicz, Kowalewski and Kozlowki, 2013.). A somewhat similar approach is to report the inference resulting from both of these models, and to state the preferred model based on the outcome of the Hausman pretest (see e.g. Smith, Smith and Verner, 2006, and Stanca, 2006). This pretest is incorporated in popular software packages such as eViews, R, SAS and Stata.

Guggenberger (2010) and Kabaila, Mainzer and Farchione (2015, 2017) show that the effect of model selection using the Hausman pretest in this way is very damaging to hypothesis tests and confidence intervals for the slope parameter. In particular, the confidence interval constructed using the model selected by the Hausman pretest has minimum coverage probability that is typically far below the nominal coverage. This is an example of a widespread problem with confidence intervals constructed after preliminary data-based model selection (see e.g. Kabaila, 2009, and Leeb and Pötscher, 2005). As in Kabaila et al (2017), throughout the present paper we carry out inference conditional on the observed values of the time-varying covariate. The very important advantages of this conditional inference are described in the introduction to Kabaila et al (2017). These advantages include the fact that this inference is valid irrespective of how the values of the covariate are generated. In the econometric literature, an early recognition of this advantage is provided by Koopmans (1937, pp 29 and 30). In the present paper, the inference of interest is a confidence interval for the slope parameter.

As insightfully pointed out by Leamer (1978, chapter 5), preliminary data-based model selection (such as a Hausman pretest) may be motivated by the desire to utilize uncertain prior information in statistical inference. He goes even further when he states, on p.123, that “The mining of data that is common among non-experimental scientists constitutes prima facie evidence of the existence of prior information”. Leamer uses a Bayesian approach to utilize uncertain prior information in statistical inference. An alternative is to use a frequentist approach to utilize the uncertain prior information. The utilization of uncertain prior information in frequentist inference has a distinguished history. Hodges and Lehmann (1952), Pratt(1961), Stein (1962), Cohen (1972), Bickel (1984), Kempthorne (1983, 1987, 1988), Casella and Hwang (1983, 1987), Goutis and Casella (1991), Tseng and Brown (1997) and Efron (2006) are included in this history, which is briefly reviewed by Kabaila (2009, Sections 8 and 9).

In the present paper we use the frequentist approach and suppose that there is, indeed, uncertain prior information that the covariate is exogenous. If this prior information was certain then we would simply use the random effects model to construct a confidence interval with desired confidence coefficient for the slope parameter. Recall that the confidence coefficient of a confidence interval is defined to be the infimum over the parameter space of the coverage probability of this interval. However, since we assume only uncertain prior information, we seek a confidence interval with the desired confidence coefficient and an expected length that (a) is relatively small when the prior information is correct and (b) is not too large when the prior information happens to be incorrect.

We show how the uncertain prior information that the covariate is exogenous can be utilized to construct a new confidence interval for the slope parameter with the following attractive properties. This confidence interval has a confidence coefficient that is very close to the desired value . Define the scaled expected length of this new confidence interval to be the expected length of this interval divided by the expected length of the confidence interval, with the same minimum coverage, that is constructed using the fixed effects model. This new confidence interval has scaled expected length that (a) is substantially less than 1 when the prior information is correct and (b) has maximum (over the parameter space) that is not too much larger than 1. In addition, the new confidence interval reverts to the confidence interval, with confidence coefficient and constructed using the fixed effects model, when the data strongly contradict the prior information. Unlike the endpoints of the confidence interval constructed using a model chosen by a Hausman pretest, which are discontinuous functions of the data, the endpoints of the new confidence interval are smooth functions of the data.

Consider, as an example, the airfare data set provided by Wooldridge (2013). We are interested in the regression of the response lfare, which is the logarithm of the fare, on the covariate concen, which is the market share of the largest carrier. This is panel data with the response lfare measured for each of city-pair markets over time points. Using an analysis conditional on the observed values of this covariate, Kabaila et al (2017) found that the confidence coefficient of the confidence interval, with nominal coverage 0.95, that results from a Hausman pretest is approximately 0.19, which is much lower than the nominal coverage. This confidence interval also has a scaled expected length that exceeds 1 throughout the parameter space.

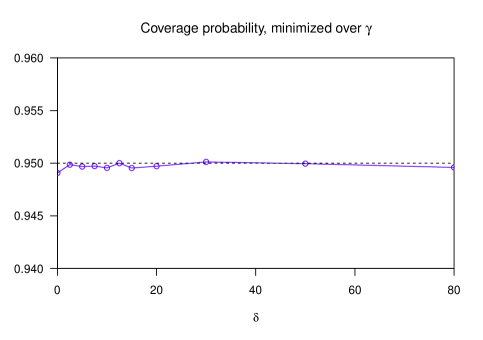

For the linear random intercept model that we consider, the coverage probabilty of the new confidence interval for the slope parameter is a function of two unknown parameters: , which is the ratio (variance of random effect)/(variance of random error), and , a parameter that takes a non-zero value unless the covariate is exogenous. In other words, the covariate is exogenous when . For this airfare data, the new confidence interval, with desired confidence coefficient 0.95, is found to have confidence coefficient that is approximately 0.9493. The coverage probability, minimized over , of this new confidence interval for the airfare data is graphed as a function of in Figure 1.

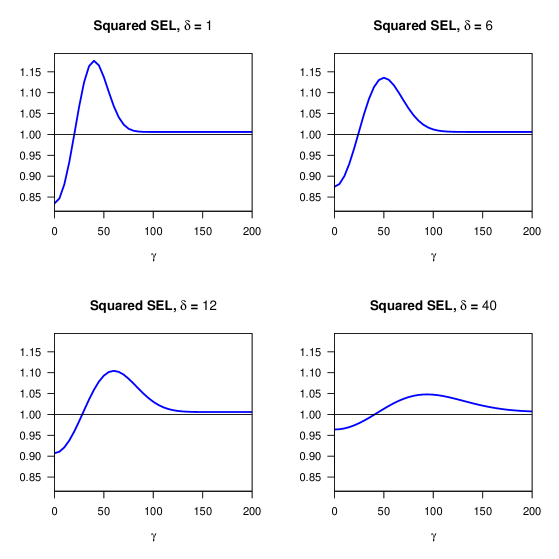

Figure 2 presents graphs of the squared scaled expected length of the new confidence interval for the slope parameter, with desired confidence coefficient 0.95, as a function of , for , for the airfare data. The squared scaled expected length is directly related to the relative sample sizes required for the new confidence interval and the confidence interval, with the same confidence coefficient and constructed using the fixed effects model, to have the same expected length (cf Bickel and Doksum, 1977, p. 137). The graphs of the squared scaled expected lengths were found to be very close to being even functions of and so Figure 2 presents these graphs only for . How far the squared scaled expected length is below 1 when (i.e. when the prior information that the covariate is exogenous is correct) depends on the unknown parameter . The estimate of for the airfare data is 12.774, suggesting that the graph of the squared scaled expected length of the new confidence interval will be similar to the left-hand lower panel of Figure 2.

A description of the simulation methods used to prepare Figures 1 and 2 is provided in Section 3. In the next section we describe the correlated random effects model and the new confidence interval which is obtained using the following two steps. In the first step, we suppose that and the random error variance are known and construct a confidence interval for the slope parameter that utilizes the uncertain prior information that the covariate is exogenous using the method of Kabaila and Giri (2009). This method has since been used in other contexts, including the construction of optimized Stein-type confidence sets for the multivariate normal mean (Abeysekera and Kabaila, 2017). In the second step, we replace these parameter values by estimates. In other words, we use the plug-in principle (Efron, 1998, Section 5).

2 THE CORRELATED RANDOM EFFECTS MODEL AND THE NEW CONFIDENCE INTERVAL

We consider a model for panel data, for which denotes the individual, household or firm etc. () and denotes time (). Let and denote the response variable and the time-varying covariate, respectively, for the ’th individual at the ’th time. Our analysis is conditional on . Suppose that

| (1) |

for and , where . We assume that the ’s and the ’s are independent, with the ’s independent and identically distributed (i.i.d.) and the ’s are i.i.d. . Let . The ’s and the ’s are unobserved. This is the correlated random effects model described, for example, by Wooldridge (2013, p.497). If then the ’s are exogenous. Thus, we call a non-exogeneity parameter. Our aim is to find a confidence interval for the slope parameter with the desired minimum coverage probability and expected length that (a) is relatively small when the prior information is correct and (b) is not too large when the prior information happens to be incorrect.

The new confidence interval is constructed using the following two steps. In the first step we suppose that is known and note that, after the standard transformation described in Appendix A, the model (1) becomes a linear regression model with i.i.d. normal random errors with known variance. The method of Kabaila and Giri (2009) is then adapted to this particular case (as described in Appendix A) to find a confidence interval that has the desired coverage and expected length properties. Of course, this confidence interval is determined by . The second step is to replace the value of used in the construction of this confidence interval by the estimator described in Subsection 2.2.

2.1 First step: confidence interval construction assuming that is known

The details for the first step are as follows. Suppose that is known. Adding and subtracting to the right hand side of (1) gives

| (2) |

where and . Let and denote the GLS estimators of and , respectively, obtained using this model. Note that is the estimator of obtained using the fixed effects model. Now let

where and denote the variances of and , respectively, conditional on . Note that is the test statistic for a Hausman test of the null hypothesis against the alternative hypothesis .

Let and It follows from the proof of Lemma 1 of Kabaila et al (2017) that

We see from this that our assumption that is known is needed to find . The confidence interval for , based on the fixed effects model and with coverage probability , is

where and denotes the cdf.

As shown in Appendix A, after a standard transformation, the model (2) becomes a linear regression model with i.i.d. normal random errors with known variance. Let denote the interval (). Using the method of Kabaila and Giri (2009) as described in Appendix A, we are led to a confidence interval of the form

where is an odd continuous function and is an even continuous function. Obviously, . In addition, we require that and for , where is a (sufficiently large) specified positive number. By construction, reverts to the confidence interval, with confidence coefficient and constructed using the fixed effects model, when i.e. when the data strongly contradict the prior information. We have chosen because extensive numerical experimentation shows this is sufficiently large. Let denote the class of pairs of functions that satisfy these requirements.

Let denote the subset of such that is fully specified by the vectors and as follows. By assumption, and . The values of and for any are found by natural cubic spline interpolation for the given values of and for . We will numerically compute such that has minimum coverage probability and scaled expected length that (a) is substantially less than 1 when the prior information is correct and (b) has maximum (over the parameter space) that is not too much larger than 1.

We now describe the numerical constrained optimization method used to find the pair of functions satisfying these conditions. Let , a scaled version of the non-exogeneity parameter . By Theorem B.1, stated in Appendix B, for any given , the conditional coverage probability is a function of ). We therefore denote this coverage probability by . We define the conditional scaled expected length of as

By Theorem B.1, stated in Appendix B, for any given , this scaled expected length is a function of ). We therefore denote this scaled expected length by .

Suppose for the moment that , satisfying , is given. Numerically compute the pair of functions that minimizes the objective function

| (3) |

subject to the inequality constraint that for all . This numerical constrained optimization is made feasible by the computationally convenient expressions for , which is an even function of , and the objective function (3) given in Appendix A. For the computations, the coverage inequality constraint for all is replaced by for a well chosen finite set of nonnegative values of . Let denote the value of that results from this numerical computation.

For this numerical computation recovers the confidence interval for , based on the fixed effects model and with coverage probability . As decreases from this value, this computation puts increasing weight on achieving a small value of , which results in a smaller value of i.e. an improved confidence interval performance when the prior information that is correct. However, as decreases

increases i.e. the performance of the confidence interval when the prior information happens to be incorrect is degraded. Numerical experimentation revealed that a reasonable tradeoff between this improvement and degradation in performance resulted when was chosen such that the “gain” when the prior information is correct, as measured by

| (4) |

is equal to the maximum possible “loss” when the prior information happens to be incorrect, as measured by

| (5) |

Clearly, the value of chosen in this way is determined by (assuming that is given) and so we denote it by . In other words, the confidence interval constructed assuming that is known is

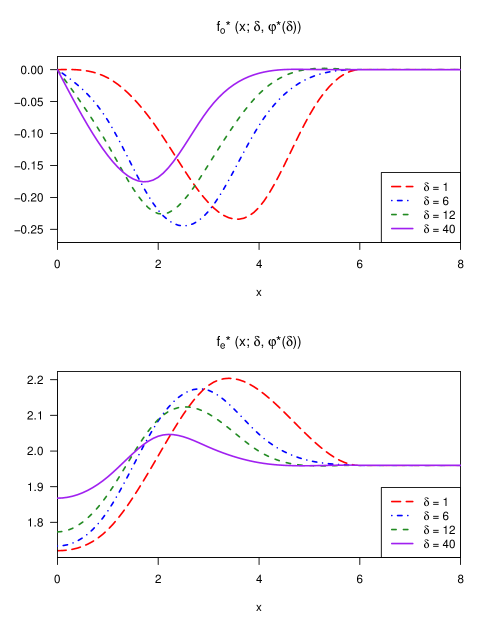

For , Figure 3 presents graphs of the functions (top panel) and (bottom panel) for , for the airfare data. Because is an odd function and is an even function, we present these graphs only for .

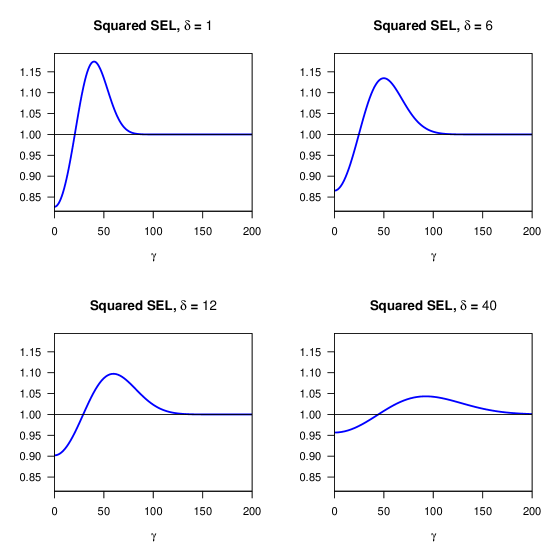

For the airfare data and , the infimum and supremum of the coverage probability of , conditional on , are 0.9500 and 0.9507, respectively. In other words, the coverage probability of this interval, conditional on , is very close to for all . For the airfare data, Figure 4 presents graphs of the squared scaled expected length of as a function of for each and . We can see from this figure that, for each of these values of , the minimum squared scaled expected length is below 1 at (i.e. when the uncertain prior information is correct), the maximum squared scaled expected length is not too much greater than 1, and the squared scaled expected length approaches 1 as increases. This last property is a consequence of the fact that, by construction, reverts to the confidence interval , based on the fixed effects model, when the data strongly contradict the prior information.

2.2 Second step: replace the true parameter value

by an

estimator

We use the same estimator of as Kabaila et al (2017). The motivation for this estimator is provided in Section 2.1 of Kabaila et al (2017). Define and . Let . The estimator of that we use is

Let denote the GLS estimator of based on the model (2). Define . The estimator of that we use is , where

The second step in the construction of the new confidence interval is to replace by the estimator in . In other words, we use the plug-in principle (Efron, 1998, Section 5). The resulting confidence interval is . As proved in Appendix B, the conditional coverage probability and the scaled expected length of this confidence interval are both functions of .

As noted in Subsection 2.1, for assumed known, the infimum over of the coverage probability of , conditional on , is 0.9500 (accurate to four digits after the decimal point) which is very close to . As evidenced by Figure 1, this very desirable property is, to a large extent, inherited by the new confidence interval obtained through the application of the plug-in principle. A comparison of Figures 2 and 4 shows that the squared scaled expected length of is very close to the squared scaled expected length of . To summarize, for the airfare data the plug-in principle works well.

3 SIMULATION METHODS USED TO EVALUATE THE CONDITIONAL COVERAGE AND SCALED EXPECTED LENGTH OF THE NEW CONFIDENCE INTERVAL

In this section we briefly describe the two main ideas employed in the simulation methods that are used to evaluate the conditional coverage and the scaled expected length of the new confidence interval. A detailed description of these simulation methods is given in Appendix C.

The first main idea is as follows. For each given value of , the functions and are found using the method described in Subsection 2.1, with computation time of the order of 1 minute. To make the simulations computationally feasible, we precompute the functions and for a grid of 11 values of , denoted by . For any given and given , the value of is obtained by linear interpolation in from and .

The grid of 11 values of is obtained as follows. Let

| (6) |

where . It can be shown that is the correlation between and . Because and are nonnegative, . To obtain the grid of values of we begin with the grid of values of . We then find by solving for in (). Our grid of values of is, then, . Note that when , is equal to .

The second main idea is as follows. Define and for and . Observe that the ’s and ’s are i.i.d. . It follows from Kabaila et al (2017, Appendix A.3) that the conditional coverage probability and scaled expected length of the new confidence interval can be expressed in terms of the ’s, ’s, , and . We use the ’s and ’s to drive the simulations, thereby removing the need to specify values for either or .

4 ANALYSIS OF THE ROBUSTNESS OF THE NEW CONFIDENCE INTERVAL

The new confidence interval is constructed assuming that the ’s and the ’s are independent, with the ’s i.i.d and the ’s are i.i.d. . As previously, let and , so that the ’s and the ’s are i.i.d. . It follows from Kabaila, Mainzer and Farchione (2017, Appendix A.3) that the conditional coverage probability and scaled expected length of the new confidence interval can be expressed in terms of the ’s, ’s, , and .

In the Supplementary Material we suppose that the ’s and ’s are still independent, but with the ’s identically distributed with a skewed standardized Student’s -distribution and the ’s identically distributed with a, possibly different, skewed standardized Student’s -distribution. For the airfare data, we assess the impact of this change of distributions on the following three properties of the new confidence interval: the minimum conditional coverage probability, the scaled expected length for and the scaled expected length, maximized over . As noted earlier, this confidence interval is constructed assuming that the ’s and ’s are i.i.d. . In other words, we assess the robustness of these properties of the new confidence interval to replacement of the distributions of the ’s and ’s by skewed standardized Student’s -distributions. As shown in the Supplementary Material, these properties are very robust to this replacement.

5 DISCUSSION

Until the present paper, the applied econometrician has been faced with choosing between the following two options. The first of these options is to carry out a Hausman pretest for exogeneity followed by the construction of the confidence interval for the slope parameter, leading to a confidence interval with unacceptably poor coverage properties. The second of these options is to always construct the confidence interval using the fixed effects model i.e. to always avoid using the Hausman pretest. Neither of these options would seem to be particularly attractive to the applied econometrician.

The new confidence interval described in the present paper provides an intermediate between these two options and, in a sense, combines the best features of both. To an excellent approximation, the new confidence interval has the desired minimum coverage probability. The test statistic for the Hausman pretest enters into the expression for the new confidence interval. Furthermore, this confidence interval reduces to the confidence interval obtained using the fixed effects model when the value of the test statistic for the Hausman pretest strongly contradicts the prior information.

We have defined the “gain” of the new confidence interval to be 1 minus its squared scaled expected length, when the prior information is correct (i.e. when the covariate is exogenous). We have also defined the maximum possible “loss” to be the maximum of the squared scaled expected length minus 1, when the prior information happens to be incorrect. For the new confidence interval, we have set the “gain” equal to the maximum possible “loss”. However, if the data strongly contradict the prior information then the “loss” is negligible.

Put another way, the new confidence interval does not dominate the confidence interval, with the same confidence coefficient, obtained using the fixed effects model. Indeed, the fact that the application of the plug-in principle works so well and the admissibility result of Kabaila, Giri and Leeb (2010, Section 4) suggest that it is impossible to find a confidence interval that dominates the confidence interval obtained using the fixed effects model. Overall, the new confidence interval should only be used when there is some reasonable confidence (although not certainty) in the prior information that the covariate is exogenous. Of course, the decision as to whether or not the new confidence interval will be used must be made prior to examination of the vector of observed responses.

The new confidence interval is constructed using the method of Kabaila and Giri (2009), as described in Appendix A. The computation of this confidence interval has previously been carried out using the numerical constrained optimization function fmincon in the MATLAB Optimization Toolbox. The MATLAB programs for the computation of this confidence interval and its conditional coverage and scaled expected length have been translated, with improvements, to R programs, which will be made available in an R package.

Acknowledgement

This work was supported by an Australian Government Research Training Program Scholarship.

REFERENCES

Abeysekera, W. and P. Kabaila (2017) Optimized recentered confidence spheres for the multivariate normal mean. Electronic Journal of Statistics 11, 1798–1826.

Bickel, P.J. (1984) Parametric robustness: small biases can be worthwhile. Annals of Statistics 12, 864–879.

Bickel, P.J. and K.A. Doksum (1977) Mathematical Statistics, Basic Ideas and Selected Topics Holden-Day.

Casella, G. and J.T. Hwang (1983) Empirical Bayes confidence sets for the mean of a multivariate normal distribution. Journal of the American Statistical Association 78, 688–698.

Casella, G. and J.T. Hwang (1987) Employing vague prior information in the construction of confidence sets. Journal of Multivariate Analysis 21, 79–104.

Choe, J. (2008) Income inequality and crime in the United States. Economics Letters 101, 31–33.

Cohen, A. (1972) Improved confidence intervals for the variance of a normal distribution. Journal of the American Statistical Association 67, 382–387.

Efron, B. (1998) R.A. Fisher in the 21st century. Statistical Science 13, 95–112.

Efron, B. (2006) Minimum volume confidence regions for a multivariate normal mean vector. Journal of the Royal Statistical Society, Series B 68, 655–670.

Giri, K. (2008) Confidence Intervals in Regression Utilizing Prior Information. Unpublished PhD thesis.

Goutis, C. and G. Casella (1991) Improved invariant confidence intervals for a normal variance. Annals of Statistics 19, 2015–2031.

Guggenberger, P. (2010) The impact of a Hausman pretest on the size of a hypothesis test: the panel data case. Journal of Econometrics 156, 337–343.

Hastings, J.S. (2004) Vertical relationships and competition in retail gasoline markets: Empirical evidence from contract changes in Southern California. American Economic Review 94, 317–328.

Hausman, J. A. (1978) Specification tests in econometrics. Econometrica 46, 1251–1271.

Hodges, J.L. and E.L. Lehmann (1952) The use of previous experience in reaching statistical decisions. Annals of Mathematical Statistics 23, 396–407.

Jackowicz, K., O. Kowalewski and Ł. Kozłowski (2013) The influence of political factors on commercial banks in Central European countries. Journal of Financial Stability 9, 759–777.

Kabaila, P. (2009) The coverage properties of confidence regions after model selection. International Statistical Review 77, 405–414.

Kabaila, P. and K. Giri (2009) Confidence intervals in regression utilizing prior information. Journal of Statistical Planning and Inference 139, 3419–3429.

Kabaila, P., K. Giri and H. Leeb (2010) Admissibility of the usual confidence interval in linear regression. Electronic Journal of Statistics 4, 300–312.

Kabaila, P. and H. Leeb (2006) On the large-sample minimal coverage probability of confidence intervals after model selection. Journal of the American Statistical Association 101, 619–629.

Kabaila, P., R. Mainzer and D. Farchione (2015) The impact of a Hausman pretest, applied to panel data, on the coverage probability of confidence intervals. Economics Letters 131, 12–15.

Kabaila, P., R. Mainzer and D. Farchione (2017) Conditional assessment of the impact of a Hausman pretest on confidence intervals. Statistica Neerlandica

Kempthorne, P.J. (1983) Minimax-Bayes compromise estimators. In 1983 Business and Economic Statistics Proceedings of the American Statistical Association, pp.568–573, Washington DC.

Kempthorne, P.J. (1987) Numerical specification of discrete least favourable distributions. SIAM Journal of Scientific and Statistical Computing 8, 171–184.

Kempthorne, P.J. (1988) Controlling risks under different loss functions: the compromise decision problem. Annals of Statistics 16, 1594–1608.

Koopmans, T.C. (1937) Linear Regression Analysis of Economic Time Series. Haarlem, Netherlands: Bohn.

Leamer, E. E. (1978) Specification Searches: Ad Hoc Inference with Nonexperimental Data. New York: Wiley.

Leeb, H. and B. Pötscher (2005) Model selection and inference: facts and fiction. Econometric Theory 21, 21–59.

Papatheodorou, A. and Z. Lei (2006) Leisure travel in Europe and airline business models: A study of regional airports in Great Britain. Journal of Air Transport Management 12, 47–52.

Pratt, J.W. (1961) Length of confidence intervals. Journal of the American Statistical Association 56, 549–657.

Smith, N., V. Smith and M. Verner (2006) Do women in top management affect firm performance? A panel study of 2,500 Danish firms. International Journal of Productivity and Performance Management 55, 569–593.

Stanca, L. (2006) The effects of attendance on academic performance: panel data evidence for Introductory Microeconomics. The Journal of Economic Education 37, 251–266.

Stein, C. (1962) Confidence sets for the mean of a multivariate normal distribution. Journal of the Royal Statistical Society, Series B 9, 1135–1151.

Tseng, Y.L. and L.D. Brown (1997) Good exact confidence sets for a multivariate normal mean. Annals of Statistics 5, 2228–2258.

Wooldridge, J. M. (2013), Introductory Econometrics: a Modern Approach, 5th edtion. Ohio: South-Western.

APPENDIX A

Standard transformation of the model (2) when is assumed to be known

The covariance matrix of is , where is an block diagonal matrix with identical block diagonal elements each of which is the matrix , where is a -vector of 1’s. Also, is the block diagonal matrix with identical block diagonal elements, each of which is the matrix . Premultiplying (A.7) by gives

| (A.8) |

where , and . Then . Now assume that is known, so that (A.8) describes a linear regression model with known random error variance . The parameter of interest is and we suppose that we have uncertain prior information that .

Description of the Kabaila and Giri confidence interval for known error variance

Suppose that

| (A.9) |

where is a random -vector of responses, is a known matrix () with linearly independent columns, is an unknown parameter -vector and where is known. Also suppose that the parameter of interest is , where is a specified non-zero -vector. Let , where and are specified and and are linearly independent. Suppose that we have uncertain prior information that . We will construct a confidence interval for that has minimum coverage probability and utilizes this uncertain prior information through the expected length properties described later in this subsection.

Let denote the OLS estimator of , based on the model (A.9). Also let and . Define , and . Note that , and are known. Let and . The scenario described in the last paragraph of the first subsection of this appendix arises from the particular case that , , and are known. For that scenario, , ,

and

We define . It follows that

and .

We consider confidence intervals of the form

where is an odd continuous function and is an even continuous function. In addition, we require that and for all , where is a (sufficiently large) specified positive number. We will numerically compute the functions and such that has minimum coverage probability and the desired expected length properties.

Kabaila and Giri (2009) deal with the more difficult case that is unknown. They provide computationally convenient formulae for the coverage probability and scaled expected length of confidence intervals of similar form to when is unknown. They also provide a computationally convenient formula for the objective function used in the numerical constrained optimization (described below) to find the functions and .

These formulae simplify in the present case that is known. For the sake of brevity, we omit the derivations of the following results. The coverage probability is an even function of which we denote by . A computationally convenient formula for this coverage probability, given by Giri (2008, Subsection 4.3), is

where

and

The standard confidence interval for is

We define the scaled expected length of to be

This scaled expected length is an even function of which we denote by . A computationally convenient formula for this scaled expected length, given by Giri (2008, Subsection 4.3), is

A computationally convenient formula for the objective function

is

We numerically compute the pair of functions that minimizes this objective function subject to the inequality constraint that for all . For these computations, this inequality constraint is replaced by for a well chosen finite set of nonnegative values of . Then is the value of the pair of functions that results from this numerical computation.

APPENDIX B

In this appendix we prove two important theorems on the conditional coverage probability and scaled expected length of the new confidence interval.

THEOREM B.1. For known , the conditional coverage probability and scaled expected length of are, for given , functions of .

Proof. Assume that is known. Let . It is straightforward to show that , the coverage probability of conditional on , is equal to

where

By Theorem 7 of Kabaila et al (2017), conditional on , has a bivariate normal distribution which is determined by . It follows that for any given , the coverage probability of conditional on , is a function of .

The length of is equal to . The length of is equal to . The conditional scaled expected length of is defined to be

By Theorem 7 of Kabaila et al (2017), the distribution of , conditional on , is determined by . It follows that the scaled expected length of is a function of . ∎

THEOREM B.2. The conditional coverage probability and scaled expected length of the new confidence interval are functions of .

Proof. Define and to be the values of and , respectively, when is replaced by . Lemma 1 of Kabaila et al (2017) gives explicit expressions for and . The new confidence interval is

| (A.10) |

The coverage probability of this confidence interval, conditional on , is

Let and . The ’s and ’s are i.i.d. . By Appendix A.3 of Kabaila et al (2017), is a function of the ’s, ’s, and . Also, by this appendix, and are functions of the ’s, ’s, , and . It follows from this that the coverage probability of the new confidence interval, conditional on , is a function of .

Let denote the infimum over of the coverage probability of the new confidence interval (A.10), conditional on . As noted by Kabaila et al (2007, Section 4), for any given , does not depend on any unknown parameters. Now define to be the value of such that . To a very good approximation, . For the airline data this approximation is so accurate that with negligible error we may assume that for this data. The conditional scaled expected length of the new confidence interval (A.10) is defined to be divided by . To an excellent approximation, this is equal to

| (A.11) |

By Appendix A.3 of Kabaila et al (2007), and are both functions of the ’s, ’s, and . Also, by this appendix, is a function of the ’s, ’s, , and . Hence (A.11) is a function of . ∎

APPENDIX C

Estimating the coverage probability of the new confidence interval by simulation

In this section we describe the estimation of the coverage probability of the new confidence interval. Consider independent simulation runs, indexed by . On the ’th simulation run, we do the following. Generate observations of and where the ’s and ’s are i.i.d. . Compute , and , the values of , and for this simulation run, respectively. Find the functions and for this simulation run by the method described in the second and third paragraphs of Section 3. Let and . Define the function

where is an arbitrary event. The simulation based estimator of the coverage probability that we use is

The variance of can be estimated using properties of a binomial proportion.

Estimating the confidence coefficient of the new confidence interval by simulation

In this section we describe the estimation of the confidence coefficient of the new confidence interval. We specify a grid of values and a grid of values. For each of these values we find the coverage probability, minimized over , as follows. Using independent simulation runs, we estimate the coverage probability at each of these values. Store the values that lead to the three smallest estimated coverage probabilities. For each of these three values, estimate the coverage probability again using independent simulation runs, where is substantially larger than . Store the value of which leads to the smallest estimated coverage probability. Once this is done for each , we obtain the and values that minimize the estimated coverage probability over the grid of values of and . Denote these values by and , respectively. To ensure this estimate is not biased downwards, we estimate the coverage probability once more using simulations for true parameter values and , where is substantially larger than . The resulting coverage probability is our estimate of . This search for the minimum coverage probability is similar to that described in Section 3.1 of Kabaila and Leeb (2006).

For the airfare data, the grid of values is and the grid of values is . Note that low values of correspond to large values of , given by (6). We used , and . The resulting estimate of was 0.9493. The standard error of this estimate of the coverage probability at and is .

Estimation of the scaled expected length of the new confidence interval by simulation

We estimate the expected values in the numerator and denominator of the expression for the scaled expected length, given by equation (A.11), by separate sets of independent simulation runs. We begin by describing the estimation of the numerator, . On the ’th simulation run, we do the following. Generate observations of and , where the ’s and ’s are i.i.d. . Compute , and , the values of , and , respectively, for this simulation run. Find the function for this simulation run by the method described in the second and third paragraphs of Section 3. Let . The simulation based estimator of that we use is

We now describe the estimation of the term in the denominator, , of the right-hand side of (A.11). Consider another set of independent simulation runs. On the ’th simulation run we do the following. Generate observations of and . Let denote the value of for this simulation run. The simulation based estimator of that we use is

Overall, the simulation based estimator of the scaled expected length (A.11) is

where is estimated using the simulation method described in the previous subsection.