ON THE TIME OF FIRST LEVEL CROSSING AND INVERSE GAUSSIAN DISTRIBUTION

Vsevolod K. MalinovskiiCentral Economics and Mathematics Institute (CEMI) of Russian Academy of Science,

117418, Nakhimovskiy prosp., 47, Moscow, Russia

malinov@orc.ru, malinov@mi.ras.ruhttp://www.actlab.ru

Abstract.

We propose a new approximation for the distribution of the time of the first

level crossing by the random process , where ,

, is compound renewal process and . It is competitive with respect to

existing approximations, particularly in the region around the critical point

which separates processes with positive and negative drifts. This

approximation is tightly related to inverse Gaussian distributions.

Key words and phrases:

Time of first level crossing, Compound renewal processes, Inverse

Gaussian distributions.

1. Introduction and main result

The inverse Gaussian distribution has probability density function (p.d.f.)

(1.1)

where , , and are positive. Parameter is

called shape parameter, and is called mean parameter.

In the study of this distribution, paramount is finding explicit expression

(1.2)

for cumulative distribution function (c.d.f.) corresponding to p.d.f.

(1.1); by and we denote

c.d.f. and p.d.f. of a standard normal distribution.

By and we denote p.d.f. of positive random variable

, and of positive random variables ,

, all distributed identically. The random variable is the

time between starting time zero and time of the first renewal, and the random

variables are inter-renewal times. By we denote p.d.f. of

positive random variables , , all

distributed identically. The random variables are called jump sizes,

and the jumps occur only in the moments of renewals. Throughout the entire

presentation, p.d.f. and are assumed bounded from above

by a finite constant. Having assumed that , i.i.d.

, , i.i.d. ,

, are all mutually independent, we are within renewal model, where

the distribution of the first interval may be different from the

distribution of the other interclaim intervals, i.e., from the distribution of

.

Compound renewal process with time is

or , if (or ), where

, or , if

. The random variable

(1.3)

or , as for all , is the time of the

first level crossing by the process .

It is easily seen that for

(1.4)

This distribution of appears in many branches of applied probability,

including risk and queueing theories, and was considered by many authors. For

it, there are many closed-form formulas and approximations, derived by

different techniques. The goal of this paper is to get the approximation that

involves inverse Gaussian distribution, and seems new. Remarkable is that it is

derived under a set of conditions similar to those usually imposed in the

common local central limit theorem.

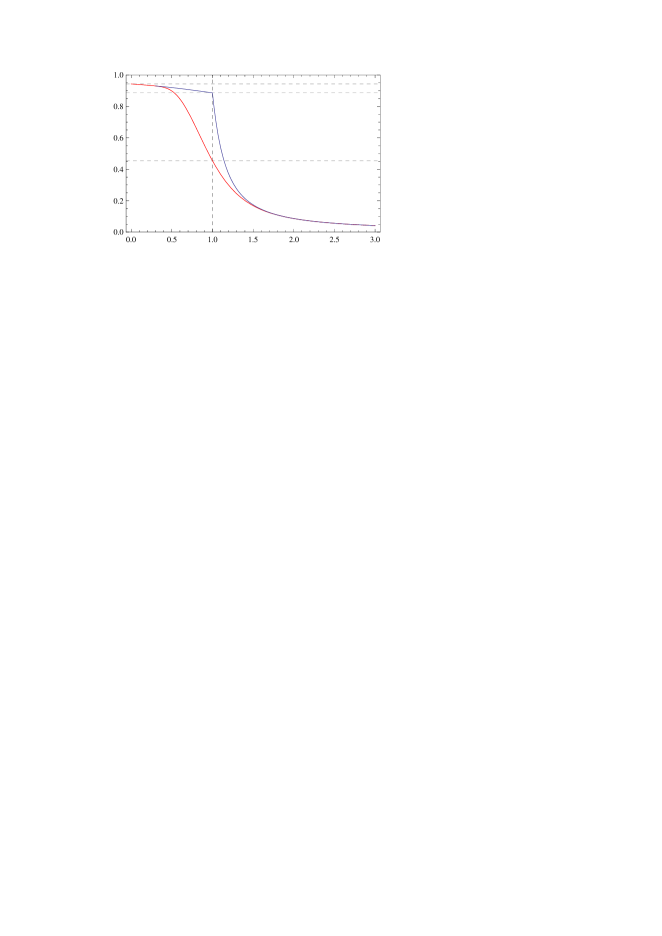

Figure 1. Graphs (-axis is ) of the functions

and , as , , ,

. Horizontal lines are ,

, and , where

.

In the above model, let p.d.f. and be bounded from above

by a finite constant, , , . Then for

, for fixed we have

(1.5)

as .

As soon as the distribution of is specified, the similar results for

are straightforward from Theorem 1.1. In

particular, for exponential with parameter

If is exponential with parameter , we have

2. Closed-form expression using convolutions

The following result is a modification of a result in \citeNP[Borovkov Dickson

2008].

Theorem 2.1.

For , we have

(2.1)

and

(2.2)

Corollary 2.1(Theorem 1 in \citeNP[Borovkov Dickson 2008]).

The main idea of this proof is to change jumps direction from “toward the

boundary” to “away from the boundary” and then use Kendall’s identity. We

set and write

(2.4)

where is the crossing time of the lower level by the

process (here ), which is a skip-free in the negative

direction111Recall that this means that this process has no negative

jumps and its increments are stationary independent. Lévy process.

The Kendall’s identity writes as (see \citeNP[Borovkov Dickson 2008]):

where

According to (2.4), we have . We observe that holds always and

write

In the sequel, let , , , etc., be “sufficiently large”

positive constants, and , , , etc., be

“sufficiently small” positive constants. All of them do not depend on

summation and integration variables, such as , , , etc., and possibly

are different in different equations.

Bearing in mind that , and , are

mutually independent, the second equality in (3.1) holds true since

The proof of Theorem 1.1 consists of several steps. The first and

the third steps are elimination of the terms that have little impact in

(3.1); it may be called preparation of (3.1) for

further analysis. The former is elimination of those terms that correspond to

small , i.e., to such that the event has a small

probability, provided that is large. The latter is elimination of the

terms containing , i.e., defect of the random walk ,

, as it nearly crosses the high level . In the first

step, we use the bounds for large deviations of sums of i.i.d. random

variables, like in \citeNP[Nagaev 1965]. In the third step, we apply the

Taylor formula to the normal p.d.f.

The second step yields the main term of approximation and the corresponding

remainder term in a raw form. That is made by means of applying standard

non-uniform Berry-Esseen bounds in local CLT formulated in

Section 4.1 to the product of and in

(3.1). The fourth step consists in investigation of the asymptotic

behavior of core components in the remainder terms which appear all over the

proof. The fifth step is the simplification of the main term of approximation,

up to the terms of required order of magnitude. It relies on a standard

estimation technique developed on the fourth step.

To get the approximation (3.2), to the product

we applied Theorem 4.2,

which is the Berry-Esseen bounds in two-dimensional local CLT. Instead,

we could apply the Berry-Esseen bounds in one-dimensional local CLT to each of

these factors, separately. We preferred to use Theorem 4.2 to get

the remainder term in a form better suited

for the further analysis.

3.3. Step 3: bringing the approximation to a convenient form

We do this in several steps. Major objective is simplification of the main term

and verification that the remainder term

is of required order of smallness.

Written in terms of elementary functions and considered as functions of ,

the expressions (3.6) and (3.7) are liable to such

standard calculus manipulations as, e.g., use of Taylor’s formula.

We divide as above the region of integration with respect to in

(3.7) in two parts, and , where

, . On the latter, we use Chebyshev’s

inequality . On the former, bearing

in mind that , we put

and use Taylor’s formula

where .

The proof reduces to checking that for all

(3.14)

and

(3.15)

as . The proof of (3.14) and (3.15) by

means of core asymptotic analysis of the expressions of the first kind, is

deferred until Step 4.

as . The proof of (3.16) with

written down in (3.12),

carried out by means of core asymptotic analysis of the expressions of the

first kind, is deferred until Step 4.

3.4. Step 4: core asymptotic analysis

Before we formulate and prove the main results of this section, we examine in

more detail and defined in

(3.9). From the definition, it follows straightforwardly that

(3.17)

(3.18)

and that for555Since we are concerned with uniform bounds, we are ready

to stretch out the range in (3.6) and

(3.7) up to .

In Lemmas 4.2–4.4, we proved a

number of identities for ,

defined in (4.2). In particular, they hold for

and

. Let us establish two more identities for

and .

Lemma 3.1.

The following identities hold true:

(3.19)

and

(3.20)

Proof.

From (3.18) and (3.17), we have two expressions for

:

(3.21)

To get (3.19), we equate the right-hand sides of both equations

(3.21) and do straightforward algebraic transformations. To have

(3.20), we transform the right-hand side of the second equation

(3.21), bearing in mind that and

consequently that .

∎

Asymptotic analysis of the expressions of the first kind

By the expressions of the first kind we call those arising in the analysis of

the remainder term in the approximation (3.2). Their integrands

contain rational functions modified by a square root. The first expression of

this type (cf. (3.12) and (3.16)) is

Let us put for brevity and , ,

, i.e., for

, , , we have

and , i.e.,

.

It is easily seen that

(3.23)

where

The essence of (3.23) is the following. For such that

, we simplify the denominator by

switching to . The latter has no singularity since

. For such that , we keep in the denominator and

use the inequality between the arithmetic mean and the geometric mean. Both

these estimates are such that the integrals in and

may be evaluated explicitly.

Examining , the explicit expression for the integral

is

found in Lemma 4.5. Using it, the asymptotic behavior of

, as , is checked as required in

Section 4.6.

Examining and bearing in mind that for

, we split the integrand and make the change of

variables as follows:

The explicit expressions for two latter integrals are found in Lemma 4.7.

Using this result, the asymptotic behavior of , as , is checked as required

in Section 4.7. The proof is complete.

∎

Let us put for brevity and , ,

, i.e., for777If we put in these expressions,

they will be equal to , , introduced in the proof of

Lemma 3.2 for . , , , we have

and, completing the square and making the change of variables, rewrite it as

(3.26)

Case

In this case, . The second summand in brackets in the integrand in

(3.26) is positive since in this case

; it is easily seen from the second equality

(3.24). Moreover, for the difference

increases, as increases, and exceeds

for . The integrand in (3.26) has no singularities in

the region of integration since

We use the estimate , where

The explicit expression for the integral in is found in

Lemma 4.7. Using it, the asymptotic behavior of ,

as , is checked as required in Section 4.8. The

proof is complete.

which can be verified by direct calculations, the range of summation

in may we

written as ,

the range of summation in may we

written as , and the range of

summation in may

we written as .

The explicit expressions for the integrals in and

are similar to that one for the integral in . Using it, the

asymptotic behavior of and , as , is

checked as required in Section 4.9.

The explicit expression for the integral in is similar to that one for the integral

in . Using it, the asymptotic behavior of , as , is checked

as required in Section 4.10. The proof is complete.

∎

This proof is a modification of the proof of Lemma 3.3 for

, alike the proof of Lemma 3.2 for was a

modification of that proof for . It uses essentially the same techniques

and is left to the reader.

∎

Processing of

Just as we did in the analysis of , rewrite as

Lemma 3.4.

We have ,

as .

Proof.

This proof goes along the same lines as the proof of Lemma 3.3 and

is left to the reader.

∎

Asymptotic analysis of the expressions of the second kind

By the expressions of the second kind we call those arising when we simplify

the main term of approximation (3.2). Their integrands contain

exponential, inherited from CLT, and rational functions. The first expression

of this type (cf. (3.8)) is

Other expressions of this type are (cf. (3.10) and

(3.11))

Applying the identities of Lemma 3.1 and making the change of

variables in the integral with respect to , we

rewrite it as

(3.28)

Lemma 3.5.

We have ,

as .

As before, we prove first this lemma in the case and then in the case

. In both cases, we use notation set in respective parts of the

proof of Lemma 3.2.

Recall (see (3.24)) that for ,

for , that999Therefore, the integrand in

(3.29) does not contain singularities within the range of

integration. The unique point of singularity of the first factor lies to the

left of since . The second factor is positive

everywhere. for all , and for

, for , and

consider , i.e.,

(3.29)

It is easily seen that

(3.30)

where101010While using (3.23) was essential, using of

(3.30) is largely for convenience: it emphasizes that is

small for , and the factor

is unessential.

The asymptotic behavior of , as , is checked as

required in Section 4.14. The asymptotic behavior of

, as , is checked as required in

Section 4.15. The proof is complete.

∎

As before (see (3.24)), we put and ,

, . Rewrite (3.28) as

and, completing the square and making the change of variables, as

Since the exponential factor is easier to work, this expression is suitable for

its asymptotic analysis without its simplifying111111Recall that dealing

with the analogue formula for (see (3.26)), due to

technical complexities, we had to switch to certain upper bounds for

..

Case

In this case, . Recall that it yields and

use the arguments outlined in the respective part of the proof of

Lemma 3.2, for . The asymptotic behavior of the integral

is examined by means of a direct extension, as it was done in

Section 4.8, of Lemma 4.11. Using it, the

asymptotic behavior of , as , is easily checked as

required along the lines traced in Sections 4.8,

4.14 and 4.15. The proof is complete.

Case

In this case, when , used should be the arguments outlined in the

respective part of the proof of Lemma 3.2, for , with the

difference that integrals are analyzed along the lines traced in

Sections 4.14 and 4.15. The proof is complete.

∎

3.5. Step 5: further simplification of the main term of approximation

In Step 3 of the proof, the main term of approximation

(see (3.6)) was simplified up to

(see (3.8)). Let us further

simplify up to the terms of allowed order of

smallness. We use for it core asymptotic analysis developed in Step 4. It is

noteworthy that in the rest of the proof this analysis is applied only to the

expressions of the second kind.

as . It is done by means of core asymptotic analysis of the

expressions of the second kind described in Step 4. In particular, for this

purpose we have to prove that

as . It is done by means of core asymptotic analysis of the

expressions of the second kind described in Step 4. This standard check is left

to the reader.

By means of standard core asymptotic analysis of the expressions of the second

kind described in Step 4, we prove that

as , where

which yields the required approximation. The proof of Theorem 1.1 is

complete.

4. Main technicalities and auxiliary results

In this section, we gather main auxiliary results used in Section

3.

4.1. Non-uniform Berry-Esseen bounds in local CLT

Let the random vectors , , assuming values in be

i.i.d. with c.d.f. , with zero mean and with identity covariance matrix .

Put , , , , .

The Berry-Esseen bounds in one-dimensional, as , central limit theorem

(CLT) are well known. The following theorem follows from Theorem 11 in Ch. 7,

§ 2 of \citeNP[Petrov 1975] proved for non-identically distributed random

variables , .

Theorem 4.1(\citeNP[Petrov 1975]).

Let , , and

for any fixed

. Then for all sufficiently large a bounded p.d.f.

exists and

The non-uniform Berry-Esseen bounds in integral rather than local

one-dimensional CLT may be found in \citeNP[Petrov 1995] (see, e.g., Theorems

15 and 14 in Ch. 5, § 6 in \citeNP[Petrov 1995]).

A detailed study of normal approximations and asymptotic expansions in the CLT

in , as , is conducted in \citeNP[Bhattacharya Rao 1976] (see

particularly Theorem 19.2 in \citeNP[Bhattacharya Rao 1976]. The non-uniform

Berry-Esseen bounds in , , that is used in

Section 3 as auxiliary result, is Theorem 4 in § 3 of

\citeNP[Dubinskaite 1982] with and . We first formulate the

following conditions.

Condition (): there exists such that

and

, where is a sequence of positive numbers such that

, as , and .

Condition (): ,

.

Theorem 4.2(\citeNP[Dubinskaite 1982]).

To have

(4.1)

it is necessary and sufficient that conditions , , and

be satisfied.

Remark 4.1.

It is known that the estimate (4.1) is optimal in terms of

dependence on , i.e., the power in (4.1) can not be

replaced by a greater one.

4.2. Large deviations for sums of i.i.d. r.v.

The following theorem is Corollary 2 in \citeNP[Nagaev 1965] (see also

\citeNP[Nagaev 1979]).

Lemma 4.1.

Let , , be i.i.d. random variables such that

and . If with , then for

where , and is an absolute constant depending

only on .

4.3. Fundamental identities

For , , ,

and , we use notation

(4.2)

Lemma 4.2.

We have the identity

Proof.

Getting of this identity is based on algebraic manipulations with the left-hand

side, aimed at completing the square. Its proof may be done as well by means of

a straightforward check.

∎

Lemma 4.3.

We have the identity

Proof.

We have

Indeed, since

the first summand is

The second summand is

The proof is complete.

∎

Lemma 4.4.

We have the identities

and

Proof.

Bearing in mind that , we have

Rewrite it

as required. The proof is complete.

∎

Remark 4.2.

The identities of Lemmas 4.2–4.4 in a more general

form were proved and used first in \citeNP[Malinovskii 1993].

4.4. Sums related to zeta-functions and polygamma functions

For real and for integer , fairly easy is the upper bound

. Much more

accurate are the following equalities well known in the theory of Riemann

zeta-function and its generalizations.

Sums related to Riemann zeta-function

By Riemann zeta-function with , we call

It is known that

where , and for

The former equality is explicit as Corollary 2 in Ch. 1, § 4 of

\citeNP[Karatsuba Voronin 1992], the latter is shown in the proof of Lemma 3

in Ch. 1, § 4 of \citeNP[Karatsuba Voronin 1992].

Sums related to Hurwitz zeta-function

By Hurwitz zeta-function with and , we call

For and for any

, a convergent Newton series representation is known:

It is easily seen that , and we have

(4.3)

Sums related to polygamma functions

By polygamma function, we call

. By polygamma function of

order , we call . It is

known that for

where are Stirling’s numbers with . It is known that

for . Consequently, we

have, e.g.,

Using polygamma functions, we can get the explicit expressions and exact asymptotics of a

number of series of this type. In particular, for we have

and

4.5. Integrals of rational functions

The following integrals of rational functions modified by a square root (cf.

3.158 in \citeNP[Gradshtein 1980]) can be found in explicit form. We leave to

the reader the details of these calculations.

Lemma 4.5.

For , , we have

Lemma 4.6.

For , , , we have

and for , , , we have

To shorten notation in the following two lemmas, we put ,

.

Lemma 4.7.

For , we have

and for , we have

Lemma 4.8.

For , , we have

4.6. The asymptotic behavior of

Let us verify that for ,

,

with

Put the above , , and in the integral evaluated in

Lemma 4.5. It is checked by direct calculations that

where

We have , where

To investigate the asymptotic behavior of , ,

, as , note that the fractions under the summation

sign, as well as the argument of the logarithmic function in ,

are rational functions of modified by a square root. Extracting the highest

power of from both nominators and denominators of these fractions, we have

Since for the ratio is bounded by a constant, and even

monotone decreases to zero, as growth to infinity, the expressions

underlined by a brace and do not exceed a

constant for all , as growth to infinity. The proof is completed

by summation, as it was done in Section 4:

, , and

, as .

4.7. The asymptotic behavior of

Let us verify that for ,

,

with

Put the above , , and in the integrals evaluated in

Lemma 4.7. For the first of them, it is checked by direct

calculations that

(4.4)

For the second of them, it is checked by direct calculations that

(4.5)

where

and

Using the standard technique of investigating the asymptotic behavior of the

summands in

described in Section 4.6, we

have first131313Note that in sums with the

ratio tends to zero, as . , as

, since

and similarly

as . The proof is complete.

4.8. The asymptotic behavior of

Let us verify that

where

(4.6)

i.e., for ,

,

with ,

, defined in (3.24) with

,

,

.

Put these , , and into the integral evaluated in

Lemma 4.5. It is checked by direct calculations that141414It

is noteworthy that since (see (3.25)).:

Recall (see (3.27)) that

. The difference

between , and lies only in the

range of summation: for it is

, and for

it is . The same way as in

analyzing , for , , set in (4.6), we turn

to the integral evaluated in Lemma 4.5, and the rest of the proof

consist in examining the asymptotic behavior, as , of the sums

similar to those in Section 4.8, e.g., of

Leaving this checking to the reader, we point the main difference: in this case

and vanishes for . But both cases, for

, since

, and for

, since

, we have

4.10. The asymptotic behavior of

The investigation of the asymptotic behavior of

where , , and are defined in (4.6), is quite analogous to

investigation of the asymptotic behavior of . We leave it to the

reader.

4.11. The asymptotic behavior of

We have to verify that

for151515In the first sum (with ) we have , while in the second sum (with ) we have . , ,

with

.

Put the above , , and in the first integral (wherein )

evaluated in Lemma 4.6. It is checked by direct calculations that

where

Put the above , , and in the second integral (wherein )

evaluated in Lemma 4.6. It is checked by direct calculations that

where

We have

,

where

and

The proof is complete.

4.12. The asymptotic behavior of

We have to verify that

for161616In the sum with we have .

, ,

with

.

By making the change of variables, rewrite the integral in as

and recall that it is evaluated in explicit form in Lemma 4.8. Put

the above , , and into thus modified . It is checked

by direct calculations that

and so on, so that , , as required.

The proof is complete.

4.13. Asymptotics for integrals of rational and exponential functions

The following integrals of rational and exponential functions can be evaluated

in explicit form in terms of and

, where

is Dawson function. Recall that for

(4.7)

and

(4.8)

so that , as

.

Lemma 4.9.

For , we have

Proof.

Bearing in mind (4.7) and (4.8), for we

have171717Note that .

Both Lemmas 4.9 and 4.10 are proved by means of very

precise calculations which yield exactly the main terms of approximations,

rather than investigate the asymptotic behavior. Investigation of mere the

asymptotic behavior can be done much simpler (see, e.g., \citeNP[De Bruijn

1958]). Indeed, the function is concentrated in a

narrow region around the origin. For the remaining factor in the integrand,

note that in this region . Routine estimation completes the proof. Using these considerations, it

is easy to check the following lemma.

Lemma 4.11.

For , we have

We merely note that the integrand in Lemma 4.11 is positive and has

no singularities within the range of integration . Indeed, the

point of singularity of lies outside the range of

integration since .

for with . The same way

as in Section 4.14, we have

as , as required.

References

[1]

[Bhattacharya and Ranga Rao (1976)]Bhattacharya, R.N., and Ranga Rao, R. (1976)

Normal Approximation and Asymptotic Expansions. Wiley & Sons, New York,

etc.

[Borovkov and Dickson (2008)]Borovkov, K., and Dickson, D.C.M. (2008) On the ruin

time distribution for a Sparre Andersen process with exponential claim sizes,

Insurance: Mathematics and Economics, Vol. 42, 1104–1108.

[Dubinskaite (1982)]Dubinskaite, J. (1982) Limit theorems in . I,

Lith. Math. J., Vol. 22, No. 2, 129–140, doi:10.1007/BF00969611.

[Gradshtein and Ryzhik (1980)]Gradshtein, I.S., and Ryzhik, I.M. (1980) Table of

Integrals, Series, and Products. Academic Press, New York.

[Kendall (1957)]Kendall, D.G. (1957) Some problems in the theory of dams,

Journal of the Royal Statist. Soc., Ser. B, Vol. 19, 207–212.

[Malinovskii (1993)]Malinovskii, V.K. (1993) Limit theorems for stopped

random sequences. I: rates of convergence and asymptotic expansions, Theory Probab. Appl.,

Vol. 38, 673–693.

[Nagaev (1965)]Nagaev, S.V. (1965) Some limit theorems for large

deviations, Theory Probab. Appl., Vol. 10, 214–235.

[Nagaev (1979)]Nagaev, S.V. (1979) Large deviations of sums of

independent random variables, Annals of Probability, Vol. 7, 754–789.

[Petrov (1975)]Petrov, V.V. (1975) Sums of Independent Random

Variables. Springer, Berlin, etc.

[Petrov (1995)]Petrov, V.V. (1995) Limit Theorems of Probability

Theory. Sequences of Independent Random Variables. Clarendon Press, Oxford

Studies in Probability.

[Karatsuba and Voronin (1992)]Karatsuba, A.A., and Voronin, S.M. (1992) The

Riemann Zeta-Function. Walter de Gruyter.