Regularized Estimation and Testing

for High-Dimensional Multi-Block Vector-Autoregressive Models

Abstract

Dynamical systems comprising of multiple components that can be partitioned into distinct blocks originate in many scientific areas. A pertinent example is the interactions between financial assets and selected macroeconomic indicators, which has been studied at aggregate level –e.g. a stock index and an employment index– extensively in the macroeconomics literature. A key shortcoming of this approach is that it ignores potential influences from other related components (e.g. Gross Domestic Product) that may exert influence on the system’s dynamics and structure and thus produces incorrect results. To mitigate this issue, we consider a multi-block linear dynamical system with Granger-causal ordering between blocks, wherein the blocks’ temporal dynamics are described by vector autoregressive processes and are influenced by blocks higher in the system hierarchy. We derive the maximum likelihood estimator for the posited model for Gaussian data in the high-dimensional setting based on appropriate regularization schemes for the parameters of the block components. To optimize the underlying non-convex likelihood function, we develop an iterative algorithm with convergence guarantees. We establish theoretical properties of the maximum likelihood estimates, leveraging the decomposability of the regularizers and a careful analysis of the iterates. Finally, we develop testing procedures for the null hypothesis of whether a block “Granger-causes” another block of variables. The performance of the model and the testing procedures are evaluated on synthetic data, and illustrated on a data set involving log-returns of the US S&P100 component stocks and key macroeconomic variables for the 2001–16 period.

1 Introduction.

The study of linear dynamical systems has a long history in control theory (Kumar and Varaiya, 1986) and economics (Hansen and Sargent, 2013) due to their analytical tractability and ease to estimate their parameters. Such systems in their so-called reduced form give rise to Vector Autoregressive (VAR) models (Lütkepohl, 2005) that have been widely used in macroeconomic modeling for policy analysis (Sims, 1980; Sims et al., 1982; Sims, 1992), in financial econometrics (Gourieroux and Jasiak, 2001), and more recently in functional genomics (Shojaie et al., 2012), financial systemic risk analysis (Billio et al., 2012) and neuroscience (Seth, 2013).

In many applications, the components of the system under consideration can be naturally partitioned into interacting blocks. For example, Cushman and Zha (1997) studied the impact of monetary policy in a small open economy, where the economy under consideration is modeled as one block, while variables in other (foreign) economies as the other. Both blocks have their own autoregressive structure, and the inter-dependence between blocks is unidirectional: the foreign block influences the small open economy, but not the other way around, thus effectively introducing a linear ordering amongst blocks. Another example comes from the connection between the stock market and employment macroeconomic variables (Fitoussi et al., 2000; Phelps, 1999; Farmer, 2015) that focuses on the impact through a wealth effect mechanism of the former on the latter. Once again, the underlying hypothesis of interest is that the stock market influences employment, but not the other way around. In another application domain, molecular biologists conduct time course experiments on cell lines or animal models and collect data across multiple molecular compartments (transcripotmics, proteomics, metabolomics, lipidomics) in order to delineate mechanisms for disease onset and progression or to study basic biological processes. In this case, the interactions amongst the blocks (molecular compartments) are clearly delineated (transciptomic compartment influencing the proteomic and metabolomic ones), thus leading again to a linear ordering of the blocks (see Richardson et al., 2016).

The proposed model also encompasses the popular in marketing, regional science and growth theory VAR-X model, provided that the temporal evolution of the exogenous block of variables “X” exhibits autoregressive dynamics. For example, Nijs et al. (2001) examine the sensitivity of over 500 product prices to various marketing promotion strategies (the exogenous block), while Pauwels and Weiss (2008) examine changes in subscription rates, search engine referrals and marketing efforts of customers when switched from a free account to a fee-based structure, the latter together with customer characteristics representing the exogenous block. Pesaran et al. (2004) examine regional inter-dependencies, building a model where country specific macroeconomic indicators evolve according to a VAR model and they are influenced exogenously by key macroeconomic variables from neighboring countries/regions. Finally, Abeysinghe (2001) studies the impact of the price of oil on Gross Domestic Product growth rates for a number of countries, while controlling for other exogenous variables such as the country’s consumption and investment expenditures along with its trade balance.

The proposed model gives rise to a network structure that in its most general form corresponds to a multi-partite graph, depicted in Figure 1 for 3 blocks, that exhibits a directed acyclic structure between the constituent blocks, and can also exhibit additional dependence between the nodes in each block. Selected properties of such multi-block structures, known as chain graphs (Drton and Perlman, 2008), have been studied in the literature. Further, their maximum likelihood estimation for independent and identically distributed Gaussian data under a high-dimensional sparse regime is thoroughly investigated in Lin et al. (2016), where a provably convergent estimation procedure is introduced and its theoretical properties are established.

Given the wide range of applications of multi-block VAR models, which in addition encompass the widely used VAR-X model, the key contributions of the current paper are fourfold: (i) formulating the model as a recursive dynamical system and examining its stability properties; (ii) developing a provably convergent algorithm for obtaining the regularized maximum likelihood estimates (MLE) of the model parameters under high-dimensional scaling; (iii) establishing theoretical properties of the ML estimates; and (iv) devising a testing procedure for the parameters that connect the constituent blocks of the model: if the null hypothesis is not rejected, then one is dealing with a set of independently evolving VAR models, otherwise with the posited multi-block VAR model. Finally, the model, estimation and testing procedures are illustrated on an important problem in macroeconomics, as gleaned by the background of the problem and discussion of the results provided in Section 6.

For the multi-block VAR model, we assume that the time series within each block are generated by a Gaussian VAR process. Further, the transition matrices within and across blocks can be either sparse or low rank. The posited regularized Gaussian likelihood function is not jointly convex in all the model parameters, which poses a number of technical challenges that are compounded by the presence of temporal dependence. These are successfully addressed and resolved in Section 3, where we provide a numerically convergent algorithm and establish the theoretical properties of the resulting ML estimates, that constitutes a key contribution in the study of multi-block VAR models.

The remainder of this paper is organized as follows. In Section 2, we introduce the model setup and the corresponding estimation procedure. In Section 3, we provide consistency properties of the obtained ML estimates under a high-dimensional scaling. In Section 4, we introduce the proposed testing framework, both for low-rank and sparse interaction matrices between the blocks. Section 5 contains selected numerical results that assess the performance of the estimation and testing procedures. Finally, an application to financial and macroeconomic data that was previously discussed as motivation for the model under consideration is presented in Section 6.

Notation. Throughout this paper, we use and respectively to denote the matrix induced -norm and infinity norm of , that is, , , and use and respectively to denote the element-wise -norm and infinity norm: , . Moreover, we use , and to denote the nuclear, Frobenius and operator norms of , respectively. For two matrices and of commensurate dimensions, denote their inner product by . Finally, we write if there exists some absolute constant that is independent of the model parameters such that .

2 Problem Formulation.

To convey the main ideas and the key technical contributions, we consider a recursive linear dynamical system comprising of two blocks of variables, whose structure is given by:

| (1) |

where are the variables in groups 1 and 2, respectively. The temporal intra-block dependence is captured by transition matrices and , while the inter-block dependence by . Noise processes and , respectively, capture additional contemporaneous intra-block dependence of and , after conditioning on their respective past values. Further, we assume that and follow mean zero Gaussian distributions with covariance matrices given by and , i.e.,

With the above model setup, the parameters of interest are transition matrices , and , as well as the covariances . In high-dimensional settings, different combinations of structural assumptions can be imposed on these transition matrices to enable their estimation from limited time series data. In particular, the intra-block transition matrices and are sparse, while the inter-block matrix can be either sparse or low rank. Note that the block of variables acts as an exogenous effect to the evolution of the block (e.g., Cushman and Zha, 1997; Nicolson et al., 2016). Further, we assume and are sparse.

Remark 1.

The triangular (recursive) structure of the system enables a certain degree of separability between and . In the posited model, is a stand-alone process, and the time series in block is “Granger-caused”’ by that in block , but not vice versa. The second equation in (1), as mentioned in the introductory section, also corresponds to the so-called “VAR-X” model in the econometrics literature (e.g., Sims, 1980; Bianchi et al., 2010; Pesaran, 2015), that extends the standard VAR model to include influences from lagged values of exogenous variables. Consider the joint process , it corresponds to a model whose transition matrix has a block triangular form:

| (2) |

The model in (2) can also be viewed from a Structural Equations Modeling viewpoint involving time series data, and also has a Moving Average representation corresponding to a structural VAR representation with Granger causal ordering (Lütkepohl, 2005). As mentioned in the introductory section, the focus of this paper is model parameter estimation under high-dimensional scaling, rather than their cause and effect relationship. For a comprehensive discourse of causality issues for VAR models, we refer the reader to Granger (1969); Lütkepohl (2005), and references therein.

Next, we introduce the notion of stability and spectrum with respect to the system.

System Stability.

To ensure that the joint process is stable (Lütkepohl, 2005), we require the spectral radius, denoted by , of the transition matrix to be smaller than 1, which is guaranteed by requiring that and , since

implying that the set of eigenvalues of is the union of the sets of eigenvalues of and , hence

The latter relation implies that the stability of such a recursive system imposes spectrum constraints only on the diagonal blocks that govern the intra-block evolution, whereas the off-diagonal block that governs the inter-block interaction is left unrestricted.

Spectrum of the joint process.

Throughout, we assume that the spectral density of exists, which then possesses a special structure as a result of the block triangular transition matrix . Formally, we define the spectral density of as

where . For two (generic) processes and , define their cross-covariance as and . In general, . The cross-spectra are defined as:

For the model given in (2), by writing out the dynamics of , the cross-spectra between and are given by

| (3) |

Similarly, we have

| (4) |

Combining (3) and (4), and after some algebra, the spectrum of the joint process is given by

| (5) |

where is a matrix with all entries being 1, and

Equation (5) implies that the spectrum of the joint process can be decomposed into the sum of two parts: the first, is a function of , while the second part involves the embedded idiosyncratic error process of , which only affects the right-bottom block of the spectrum. Note that since is a process, its matrix-valued characteristic polynomial is given by

and its spectral density also takes the following form (c.f. Hannan, 1970; Anderson, 1978):

with

and being the conjugate transpose. One can easily reach the same conclusion as in (5) by multiplying each term, followed by some algebraic manipulations.

2.1 Estimation.

Next, we outline the algorithm for obtaining the ML estimates of the transition matrices and and inverse covariance matrices and from time series data. We allow for a potential high-dimensional setting, where the ambient dimensions and of the model exceed the total number of observations .

Given centered times series data and , we use and respectively, to denote the “response” matrix from time to , that is:

and use and without the superscript to denote the “design” matrix from time to :

We use and to denote the error matrices. To obtain estimates for the parameters of interest, we formulate optimization problems using a penalized log-likelihood function, with regularization terms corresponding to the imposed structural assumptions on the model parameters–sparsity and/or low-rankness. To solve the optimization problems, we employ block-coordinate descent algorithms, akin to those described in Lin et al. (2016), to obtain the solution.

As previously mentioned, is not “Granger-caused” by and hence it is a stand-alone process; this enables us to separately estimate the parameters governing the process ( and ) from those of the process (, , and ).

Estimation of and .

Conditional on the initial observation , the likelihood of is given by:

where the second equality follows from the Markov property of the process. The log-likelihood function is given by:

Letting , then the penalized maximum likelihood estimator can be written as

| (6) |

Algorithm 1 describes the key steps for obtaining and .

| (7) |

Specifically, for fixed , each row of is cyclically updated by:

where

Here is the estimate from the previous iteration, and for notation convenience we drop the index for the outer iteration and use to denote the index for the inner iteration, for each round of cyclic update of the rows.

Estimation of , and .

Similarly, to obtain estimates of , and , we formulate the optimization problem as follows:

| (8) |

where the regularizer if is assumed to be sparse, and if is assumed to be low rank. Algorithm 2 outlines the procedure for obtaining estimates , and . Note that and need to be treated as a “joint block” in the outer update and convergence of the “joint block” is required before moving on to updating .

In many real applications, is low rank and is sparse, while in other settings both are sparse. In the first case, “Granger-causes” and the information can be compressed to a lower dimensional space spanned by a relative small number of bases compared to the dimension of the blocks, and is autoregressive through a subset of its components. Next, we give details for updating and under this model specification.

For fixed , with being low rank and sparse, the updated and satisfies

To obtain the solution to the above optimization problem, and need to be updated alternately, and within the update of each block, an iterative algorithm is required. Here we drop the superscript that denotes the outer iterations, and use as the inner iteration index for the alternate update between and , and use as the index for the within block iterative update.

-

–

Update for fixed : instead of directly updating , update with

(9) where is the singular value thresholding operator with thresholding level ,

and

Denote the convergent solution by , and .

-

–

Update for fixed : each row of is cyclically updated by

where

and are entries of coming from the previous outer iteration.

Although based on the outlined procedure, a number of iterative steps are required to obtain the final estimate, we have empirically observed that the number of iterations between the and blocks is usually rather small. Specifically, based on large number of simulation settings (selected ones presented in Section 5), for fixed , the alternate update for and usually converges within 20 iterations, while the update involving and takes less than 10 iterations.

In case, is sparse, it can be updated by Lasso regression as outlined in Algorithm 2 (details omitted).

Remark 2.

In the low dimensional setting where the Gram matrix is invertible, the update of when can be obtained by a one-shot SVD and singular value thresholding; that is, we first obtain the generalized least squares estimator, then threshold the singular values at a certain level. On the other hand, in the high dimensional setting, an iterative algorithm is required. Note that the singular value thresholding algorithm corresponds to a proximal gradient algorithm, and thus a number of acceleration schemes are available (see Nesterov, 1983, 1988, 2005, 2007), whose theoretical properties have been thoroughly investigated in Tseng (2008). We recommend using the acceleration scheme proposed by Beck and Teboulle (2009), in which the “momentum” is carried over to the next iteration, as an extension of Nesterov (1983) to composite functions. Instead of updating with (9), an “accelerated” update within the SVT step is given by:

Note that the objective function in (6) is not jointly convex in both parameters, but biconvex. Similarly in (8), the objective function is biconvex in . Consequently, convergence to a stationary point is guaranteed, as long as estimates from all iterations lie within a ball around the true value of the parameters, with the radius of the ball upper bounded by a universal constant that only depends on model dimensions and sample size (Lin et al., 2016, Theorem 4.1). This condition is satisfied upon the establishment of consistency properties of the estimates.

To establish consistency properties of the estimates requires the existence of good initial values for the model parameters , and , respectively, in the sense that they are sufficiently close to the true parameters. For the parameters, the results in Basu and Michailidis (2015) guarantee that for random realizations of , with sufficiently large sample size, the errors of and are bounded with high probability, which provides us with good initialization values. Yet, additional handling of the bounds is required to ensure that estimates from subsequent iterations are also uniformly close to the true value (see Section 3.2 Theorems 1). A similar property for and subsequent iterations is established in Section 3.2 Theorems 2 (see also Theorem 4 in Appendix A).

3 Theoretical Properties.

In this section, we investigate the theoretical properties of the penalized maximum likelihood estimation procedure proposed in Section 2, with an emphasis on the error bounds for the obtained estimates. We focus on the model specification in which the inter-block transition matrix is low rank, which is of interest in many applied settings. Specifically, we consider the consistency properties of and that are solutions to the following two optimization problems:

| (10) |

and

| (11) |

The case of a sparse can be handled similarly to that of and/or with minor modifications (details shown in Appendix E).

3.1 A road map for establishing the consistency results.

Next, we outline the main steps followed in establishing the theoretical properties for the model parameters. Throughout, we denote with a superscript “” the true value of the corresponding parameters.

The following key concepts, widely used in high-dimensional regularized estimation problems, are needed in subsequent developments.

Definition 1 (Restricted Strong Convexity (RSC)).

For some generic operator , it satisfies the RSC condition with respect to norm with curvature and tolerance if

Note that the choice of the norm is context specific. For example, in sparse regression problems, corresponds to the element-wise norm of the matrix (or the usual vector norm for the vectorized version). The RSC condition becomes equivalent to the restricted eigenvalue (RE) condition (see Loh and Wainwright, 2012; Basu and Michailidis, 2015, and references therein). This is the case for the problem of estimating transition matrix . For estimating and , define to be the weighted regularizer , and the associated norm in this setting is defined as

Definition 2 (Diagonal dominance).

A matrix is strictly diagonally dominant if

Definition 3 (Incoherence condition (Ravikumar et al., 2011)).

A matrix satisfies the incoherence condition if:

where denotes the Hessian of the log-determinant barrier restricted to the true edge set of denoted by , and is similarly defined.

The above two conditions are associated with the inverse covariance matrices and . Specifically, the diagonal dominance condition is required for and as we build the consistency properties for and with the penalized maximum likelihood formulation. The incoherence condition is primarily required for establishing the consistency of and .

We additionally introduce the upper and lower extremes of the spectrum, defined as

Analogously, the upper extreme for the cross-spectrum is given by:

with being the conjugate transpose of . With this definition,

Next, consider the solution to (10) that is obtained by the alternate update of and . If is held fixed, then solves (12), and we denote the solution by and its corresponding vectorized version as :

| (12) |

where

| (13) |

Using a similar notation, if is held fixed, then solves (14):

| (14) |

where

| (15) |

For fixed realizations of and , by Basu and Michailidis (2015), the error bound of relies on (1) satisfying the RSC condition defined above; and (2) the tuning parameter is chosen in accordance with a deviation bound condition associated with . By Ravikumar et al. (2011), the error bound of relies on how well concentrates around , that is, . Specifically, for (13) and (15), with and plugged in respectively, for random realizations of and , these conditions hold with high probability. In the actual implementation of the algorithm, however, quantities in (13) and (15) are substituted by estimates so that at iteration , and solve

where

As a consequence, to establish the finite-sample bounds of and given in (10), we need to satisfy the RSC condition, a bound on and a bound on for all . Toward this end, we prove that for random realizations of and , with high probability, the RSC condition for and the universal bounds for and hold for all iterations , albeit the quantities of interest rely on estimates from the previous or current iterations. Consistency results of and then readily follow.

Next, consider the solution to (11) that alternately updates and . As the regularization term involves both the nuclear norm penalty and the norm penalty, additional handling of the norms is required which leverages the idea of decomposable regularizers (Agarwal et al., 2012). Specifically, if and are respectively held fixed, then

where . If we let , and define the operator induced jointly by and as

| (16) |

then and are equivalently given by

| (17) |

where . Then, for fixed realizations of , and , with an extension of Agarwal et al. (2012) the error bound of relies on (1) the operator satisfying the RSC condition; and (2) tuning parameters and are respectively chosen in accordance with the deviation bound conditions associated with

| (18) |

The error bound of again relies on . In an analogous way, for the actual alternate update,

and the error bound of defined in (11) depends on the properties of , and for all . Specifically, when and (in (16) and (18), resp.) are substituted by estimated quantities, we prove that the RSC condition and bounds hold with high probability for random realizations of , and , for all iterations , which then establishes the consistency properties of and .

3.2 Consistency results for the Maximum Likelihood estimators.

Theorems 1 and 2 below give the error bounds for the estimators in (10) and (11) obtained through Algorithms 1 and 2, using random realizations coming from the stable VAR system defined in (1). As previously mentioned, to establish error bounds for both the transition matrices and the inverse covariance matrix obtained from alternating updates, we need to take into account that the quantities associated with the RSC condition and the deviation bound condition are based on estimated quantities obtained from the previous iteration. On the other hand, the sources of randomness contained in the observed data are fixed, hence errors from observed data stop accumulating once all sources of randomness are considered after a few iterations, which govern both the leading term of the error bounds and the probability for the bounds to hold.

Specifically, using the same notation as defined in Section 3.1, we obtain the error bounds of the estimated transition matrices and inverse covariance matrices iteratively, building upon that for all iterations :

-

(1)

or the operator satisfies the RSC condition;

-

(2)

deviation bounds hold for , , and ;

-

(3)

a good concentration given by and .

We keep track of how the bounds change in each iteration until convergence, by properly controlling the norms and track the rate of the error bound that depends on and , and reach the conclusion that the error bounds hold uniformly for all iterations, for the estimates of both the transition matrices and and the inverse covariance matrices and .

Theorem 1.

Consider the stable Gaussian VAR process defined in (1) in which is assumed to be -sparse. Further, assume the following:

-

C.1

The incoherence condition holds for .

-

C.2

is diagonally dominant.

-

C.3

The maximum node degree of satisfies .

Then, for random realizations of and , and the sequence returned by Algorithm 1 outlined in Section 2.1, there exist constants such that for sample size , with probability at least

the following hold for all for some that are functions of the upper and lower extremes of the spectrum and do not depend on or :

-

(i)

satisfies the RSC condition;

-

(ii)

;

-

(iii)

.

As a consequence, the following bounds hold uniformly for all iterations :

It should be noted that the above result establishes the consistency for the ML estimates of the model presented in Basu and Michailidis (2015).

Theorem 2.

Consider the stable Gaussian VAR system defined in (1) in which is assumed to be low rank with rank and is assumed to be -sparse. Further, assume the following

-

C.1

The incoherence condition holds for .

-

C.2

is diagonally dominant.

-

C.3

The maximum node degree of satisfies .

Then, for random realizations of , and , and the sequence returned by Algorithm 2 outlined in Section 2.1, there exist constants and such that for sample size , with probability at least

the following hold for all for that are functions of the upper and lower extremes of the spectrum and of the upper extreme of the cross-spectrum and do not depend on or :

-

(i)

satisfies the RSC condition;

-

(ii)

and ;

-

(iii)

.

As a consequence, the following bounds hold uniformly for all iterations :

Remark 3.

It is worth pointing out that the initializers and are slightly different from those obtained in successive iterations, as they come from the penalized least square formulation where the inverse covariance matrices are temporarily assumed diagonal. Consistency results for these initializers under deterministic realizations are established in Theorems 3 and 4 (see Appendix A), and the corresponding conditions are later verified for random realizations in Lemmas 1 to 4 (see Appendix B). These theorems and lemmas serve as the stepping stone toward the proofs of Theorems 1 and 2.

Further, the constants reflect both the temporal dependence among and blocks, as well as the cross-sectional dependence within and across the two blocks.

3.3 The effect of temporal and cross-dependence on the established bounds.

We conclude this section with a discussion on the error bounds of the estimators that provides additional insight into the impact of temporal and cross dependence within and between the blocks; specifically, how the exact bounds depend on the underlying processes through their spectra when explicitly taking into consideration the triangular structure of the joint transition matrix.

First, we introduce additional notations needed in subsequent technical developments. The definition of the spectral densities and the cross-spectrum are the same as previously defined in Section 2 and their upper and extremes are defined in Section 3.1. For defined in (1), let denote the characteristic matrix-valued polynomial of and denote its conjugate. We further define its upper and lower extremes by:

The same set of quantities for the joint process are analogously defined, that is,

Using the result in Theorem 2 as an example, we show how the error bound depends on the underlying processes . Specifically, we note that the bounds for can be equivalently written as

which holds for all and some constant that does not depend on or . Specifically, by Theorem 4, Lemmas 3 and 4,

This indicates that the exact error bound depends on and . Next, we provide bounds on these quantities. The joint process as we have noted in (2), is a process with characteristic polynomial and spectral density . The bounds for and are given by Basu and Michailidis (2015, Proposition 2.1), that is,

| (19) |

Consider the bound for . First, we note that is a sub-process of the joint error process , where . Then, by Lemma 8,

where the second inequality follows from Basu and Michailidis (2015, Proof of Proposition 2.4).

What are left to be bounded are and . By Proposition 2.2 in Basu and Michailidis (2015), these two quantities are bounded by:

| (20) |

and

where with being a diagonal matrix consisting of the eigenvalues of . Since , it follows that

and therefore

| (21) |

Remark 4.

The impact of the system’s lower-triangular structure on the established bounds. Consider the bounds in (20) and (21). An upper bound of depends on and , whereas a lower bound of involves only the spectral radius of . Combined with (19), this suggests that the lower extreme of the spectral density is associated with the average of the maximum weighted in-degree and out-degree of the system, whereas the upper extreme is associated with the stability condition: the less the system is intra- and inter-connected, the tighter the bound for the lower extreme will be; similarly, the more stable (exhibits smaller temporal dependence) the system is, the tighter the bound for the upper extreme will be. Finally, we note that an upper bound for is given by

The presence of and depicts the role of the inter-connectedness between and on the lower extreme of the spectrum, which is associated with the overall curvature of the joint process.

The impact of the system’s lower-triangular structure on the system capacity. With being a lower-triangular matrix, we only require and to ensure the stability of the system. This enables the system to have “larger capacity” (can accommodate more cross-dependence within each block), since the two sparse components and can exhibit larger average weighted in- and out-degrees compared with a system where does not possess such triangular structure. In the case where is a complete matrix, one deals with a -dimensional VAR system and is required to ensure its stability. As a consequence, the average weighted in- and out-degree requirements for each time series become more restrictive.

4 Testing Group Granger-Causality.

In this section, we develop a procedure for testing the hypothesis . Note that without the presence of , the blocks and in the model become decoupled and can be treated as two separate VAR models, whereas with a nonzero , the group of variables in is collectively “Granger-caused” by those in . Moreover, since we are testing whether or not the entire block of is zero, we do not need to rely on the exact distribution of its individual entries, but rather on the properly measured correlation between the responses and the covariates. To facilitate presentation of the testing procedure, we illustrate the proposed framework via a simpler model setting with and testing whether ; subsequently, we translate the results to the actual setting of interest, namely, whether or not in the model .

The testing procedure focuses on the following sequence of tests for the rank of :

| (22) |

Note that the hypothesis of interest, corresponds to the special case with . To test for it, we develop a procedure associated with canonical correlations, which leverages ideas present in the literature (see Anderson, 1999).

As mentioned above, we consider a simpler setting similar to that in Anderson (1999, 2002), given by

where , and is independent of . At the population level, let

The population canonical correlations between and are the roots of

i.e., the nonnegative solutions to

| (23) |

with being the unknown. By the results in Anderson (1999, 2002), the number of positive solutions to (23) is equal to the rank of , and indicates the “degree of dependency” between processes and . This suggests that if , we would expect to be small, where the ’s solve the eigen-equation

and and are the sample counterparts corresponding to and , respectively.

With this background, we switch to our model setting given by

| (24) |

where is assumed to be independent of and , encodes the canonical correlation between and , conditional on . We use the same notation as in Section 3; that is, let , , and , with omitted whenever . At the population level, under the Gaussian assumption,

which suggests that conditionally,

where

| (25) |

Then, we have that jointly

so the partial covariance matrix between and conditional on is given by

| (26) |

The population canonical correlations between and conditional on are the non-negative roots of

and the number of positive solutions corresponds to the rank of ; see Anderson (1951) for a discussion in which the author is interested in estimating and testing linear restrictions on regression coefficients. Therefore, to test , it is appropriate to examine the behavior of , where ’s are ordered non-increasing solutions to

| (27) |

and , and are the empirical surrogates for the population quantities and . For subsequent developments, we make the very mild assumption that and so that is invertible.

Proposition 1 gives the tail behavior of the eigenvalues and Corollary 1 gives the testing procedure for block “Granger-causality” as a direct consequence.

Proposition 1.

Consider the model setup given in (24), where . Further, assume all positive eigenvalues of the following eigen-equation are of algebraic multiplicity one:

| (28) |

where and are given in (25) and (26). The test statistic for testing

is given by

where ’s are ordered decreasing solutions to the eigen-equation where

and . Moreover, the limiting behavior of is given by

Remark 5.

We provide a short comment on the assumption that the positive solutions to (28) have algebraic multiplicity one in Proposition 1. This assumption is imposed on the eigen-equation associated with population quantities, to exclude the case where a positive root has algebraic multiplicity greater than one and its geometric multiplicity does not match the algebraic one, and hence we would fail to obtain mutually independent canonical variates and the rank- structure becomes degenerate. With the imposed assumption which is common in the canonical correlation analysis literature (e.g. Anderson, 2002; Bach and Jordan, 2005), such a scenario is automatically excluded. Specifically, this condition is not stringent, as for ’s that are solutions to the eigen-equation associated with sample quantities, the distinctiveness amongst roots is satisfied with probability 1 (see Hsu, 1941b, Proof of Lemma 3).

Corollary 1 (Testing group Granger-causality).

Under the model setup in (24), the test statistic for testing is given by

with being the ordered decreasing solutions of

Asymptotically, . To conduct a level test, we reject the null hypothesis if

where is the upper quantile of the distribution with degrees of freedom.

Remark 6.

Corollary 1 is a special case of Proposition 1 with the null hypothesis being , which corresponds to the Granger-causality test. Under this particular setting, we are able to take the inverse with respect to , yet maintain the same asymptotic distribution due to the fact that under the null hypothesis . This enables us to perform the test even with .

The above testing procedure takes advantage of the fact that when , the canonical correlations among the partial regression residuals after removing the effect of are very close to zero. However, the test may not be as powerful under a sparse alternative, i.e., is sparse. In Appendix D, we present a testing procedure that specifically takes into consideration the fact that the alternative hypothesis is sparse, and the corresponding performance evaluation is shown in Section 5.3 under this setting.

5 Performance Evaluation.

Next, we present the results of numerical studies to evaluate the performance of the developed ML estimates (Section 2.1) of the model parameters, as well as that of the testing procedure (Section 4).

5.1 Simulation results for the estimation procedure.

A number of factors may potentially influence the performance of the estimation procedure; in particular, the model dimension and , the sample size , the rank of and the sparsity level of and , as well as the spectral radius of and . Hence, we consider several settings where these parameters vary.

For all settings, the data and are generated according to the model

For the sparse components, each entry in and is nonzero with probability and respectively, and the nonzero entries are generated from , then scaled down so that the spectral radii and satisfy the stability condition. For the low rank component, each entry in is generated from , followed by singular value thresholding, so that conforms with the model setup. For the contemporaneous dependence encoded by and , both matrices are generated according to an Erdös-Rényi random graph, with sparsity being 0.05 and condition number being 3.

Table 1 depicts the values of model parameters under different model settings. Specifically, we consider three major settings in which the size of the system, the rank of the cross-dependence component, and the stability of the system vary. The sample size is fixed at unless otherwise specified. Additional settings examined (not reported due to space considerations) are consistent with the main conclusions presented next.

| model parameters | ||||||

| model dimension | A.1 | 50 | 20 | 5 | 0.5 | 0.5 |

| A.2 | 100 | 50 | 5 | 0.5 | 0.5 | |

| A.3 | 200 | 50 | 5 | 0.5 | 0.5 | |

| A.4 | 50 | 100 | 5 | 0.5 | 0.5 | |

| rank | B.1 | 100 | 50 | 10 | 0.5 | 0.5 |

| B.2 | 100 | 50 | 20 | 0.5 | 0.5 | |

| spectral radius | C.1 | 50 | 20 | 5 | 0.8 | 0.5 |

| C.2 | 50 | 20 | 5 | 0.5 | 0.8 | |

| C.3 | 50 | 20 | 5 | 0.8 | 0.8 | |

We use sensitivity (SEN), specificity (SPC) and relative error in Frobenius norm (Error) as criteria to evaluate the performance of the estimates of transition matrices , and . Tuning parameters are chosen based on BIC. Since the exact contemporaneous dependence is not of primary concern, we omit the numerical results for and .

Table 2 illustrates the performance for each of the parameters under different simulation settings considered. The results are based on an average of 100 replications and their standard deviations are given in parentheses.

| performance of | performance of | performance of | ||||||

|---|---|---|---|---|---|---|---|---|

| SEN | SPC | Error | Error | SEN | SPC | Error | ||

| A.1 | 0.98(0.014) | 0.99(0.004) | 0.34(0.032) | 5.2(0.42) | 0.11(0.008) | 1.00(0.000) | 0.97(0.008) | 0.15(0.074) |

| A.2 | 0.97(0.014) | 0.99(0.001) | 0.38(0.015) | 5.2(0.42) | 0.31(0.011) | 0.97(0.008) | 0.97(0.004) | 0.28(0.033) |

| A.3 | 0.99(0.005) | 0.96(0.002) | 0.87(0.011) | 5.8(0.92) | 0.54(0.022) | 0.98(0.000) | 0.92(0.009) | 0.28(0.028) |

| A.4 | 0.96(0.0261) | 0.99(0.002) | 0.36(0.034) | 5.2(0.42) | 0.32(0.012) | 0.95(0.009) | 0.98(0.001) | 0.37(0.010) |

| B.1 | 0.97(0.008) | 0.99(0.001) | 0.37(0.017) | 11.4(1.17) | 0.15(0.008) | 1.00(0.000) | 0.99(0.001) | 0.09(0.021) |

| B.2 | 0.98(0.008) | 0.99(0.001) | 0.38(0.016) | 21.2(0.91) | 0.12(0.006) | 1.00(0.000) | 0.99(0.001) | 0.08(0.018) |

| C.1 | 1.00(0.000) | 0.97(0.005) | 0.25(0.015) | 5.6(0.52) | 0.23(0.006) | 1.00(0.000) | 0.92(0.021) | 0.11(0.072) |

| C.2 | 0.99(0.007) | 0.95(0.004) | 0.45(0.022) | 5.0(0.00) | 0.31(0.014) | 1.00(0.000) | 0.92(0.019) | 0.04(0.011) |

| C.3 | 1.00(0.000) | 0.96(0.004) | 0.18(0.013) | 6.7(1.16) | 0.19(0.011) | 1.00(0.000) | 0.87(0.029) | 0.14(0.067) |

| C.3’ | 1.00(0.000) | 0.99(0.002) | 0.13(0.016) | 5.2(0.42) | 0.23(0.005) | 1.00(0.000) | 0.90(0.021) | 0.06(0.023) |

Overall, the results are highly satisfactory and all the parameters are estimated with a high degree of accuracy. Further, all estimates were obtained in less than 20 iterations, thus indicating that the estimation procedure is numerically stable. As expected, when the the spectral radii of and increase thus leading to less stable and processes, a larger sample size is required for the estimation procedure to match the performance of the setting with same parameters but smaller and . This is illustrated in row C.3’ of Table 2, where the sample size is increased to , which outperforms the results in row C.3 in which and broadly matches that of row A.1.

Next, we investigate the robustness of the algorithm in settings where the marginal distributions of and deviate from the Gaussian assumption posited and may be more heavy-tailed. Specifically, we consider the following two distributions that have been studied in Qiu et al. (2015):

-

•

-distribution: the idiosyncratic error processes and are generated from multivariate -distributions with degree of freedom 3, and covariance matrices and , respectively.

-

•

elliptical distribution: and are generated from an elliptical distribution (e.g. Rémillard et al., 2012) with a log-normal generating variate and covariance matrices and – both are block-diagonal with and respectively on the diagonals.

For both scenarios, transition matrices, and are generated analogously to those in the Gaussian setting. We present the results for and under model settings A.2, B.1, C.1 and C.2 (see Table 1).

| performance of | performance of | performance of | |||||||

|---|---|---|---|---|---|---|---|---|---|

| SEN | SPC | Error | Error | SEN | SPC | Error | |||

| A.2 | t(df=3) | 0.99(0.005) | 0.95(0.013) | 0.60(0.062) | 6.00(1.45) | 0.24(0.019) | 0.96(0.013) | 0.96(0.005) | 0.27(0.038) |

| elliptical | 0.97(0.014) | 0.99(0.001) | 0.36(0.016) | 5.1(0.30) | 0.34(0.009) | 1.00(0.000) | 0.85(0.026) | 0.15(0.033) | |

| B.1 | t(df=3) | 0.98(0.008) | 0.95(0.014) | 0.61(0.083) | 10.4(0.49) | 0.34(0.026) | 0.99(0.015) | 0.95(0.004) | 0.25(0.091) |

| elliptical | 0.95(0.015) | 0.99(0.001) | 0.37(0.024) | 10.1(0.22) | 0.40(0.013) | 1.00(0.000) | 0.90(0.013) | 0.09(0.001) | |

| C.1 | t(df=3) | 0.99(0.001) | 0.92(0.011) | 0.22(0.03) | 6.0(1.13) | 0.09(0.014 | 1.00(0.000) | 0.93(0.016) | 0.10(0.068) |

| elliptical | 1.00(0.000) | 0.90(0.006 | 0.32(0.013) | 5.2(0.44) | 0.13(0.007) | 1.00(0.000) | 0.92(0.020) | 0.07(0.041) | |

| C.2 | t(df=3) | 0.99 (0.002) | 0.95(0.023) | 0.37(0.056) | 5.1(0.22) | 0.22(0.017) | 1.00(0.000) | 0.89(0.017) | 0.10(0.029) |

| elliptical | 0.88(0.029) | 0.97(0.001) | 0.43(0.032) | 5.1(0.14) | 0.40(0.020) | 1.00(0.000) | 0.86(0.026) | 0.10(0.046) | |

Based on Table 3, the performance of the estimates under these heavy-tailed settings is comparable in terms of sensitivity and specificity for and , as well as for rank selection for to those under Gaussian settings. However, the estimation error exhibits some deterioration which is more pronounced for the -distribution case. In summary, the estimation procedure proves to be very robust for support recovery and rank estimation even in the presence of more heavy-tailed noise terms.

Lastly, we examine performance with respect to one-step-ahead forecasting. Recall that VAR models are widely used for forecasting purposes in many application areas (Lütkepohl, 2005). The performance metric is given by the relative error as measured by the norm of the out-of-sample points and , where the predicted values are given by and , respectively. It is worth noting that both and are mean-zero processes. However, since the transition matrix of is subject to the spectral radius constraints to ensure the stability of the corresponding process, the magnitude of the realized value ’s is small; whereas for , since no constraints are imposed on the coefficient matrix that encodes the inter-dependence, ’s has the capacity of having relative large values in magnitude. Consequently, the relative error of is significantly larger than that of , partially due to the small total magnitude of the denominator.

The results show that an increase in the spectral radius (keeping the other structural parameters fixed) leads to a decrease of the relative error, since future observations become more strongly correlated over time. On the other hand, an increase in dimension leads to a deterioration in forecasting, since the available sample size impacts the quality of the parameter estimates. Finally, an increase in the rank of the matrix is beneficial for forecasting, since it plays a stronger role in the system’s temporal evolution.

| baseline | A.1 | 0.89(0.066) | 0.23(0.075) |

|---|---|---|---|

| spectral radius | C.1 | 0.62(0.100) | 0.10(0.035) |

| C.2 | 0.93(0.062) | 0.17(0.059) | |

| C.3 | 0.68(0.096) | 0.10(0.045) | |

| rank | B.1 | 0.92(0.044) | 0.14(0.038) |

| B.2 | 0.94(0.042) | 0.14(0.025) | |

| dimension | A.2 | 0.87(0.051) | 0.24(0.073) |

| A.3 | 0.96(0.040) | 0.44(0.139) | |

| A.4 | 0.89(0.059) | 0.274(0.068) |

5.2 A comparison between the two-step and the ML estimates.

We briefly compare the ML estimates to the ones obtained through the following two-step procedure:

-

–

Step 1: estimate transition matrices through penalized least squares:

-

–

Step 2: estimate the inverse covariance matrices applying the graphical Lasso algorithm (Friedman et al., 2008) to the residuals calculated based on the Step 1 estimates.

Note that the two-step estimates coincide with our ML estimates at iteration 0, and they yield the same error rate in terms of the relative scale of and . We compare the two sets of estimates under setting A.1 with being low rank and setting A.2 with being sparse, whose entries are nonzero with probability .

In Table 7, we present the performance evaluation of the two-step estimates and the ML estimates under setting A.1. Additionally in Tables 7 and 7, we track the value of the objective function, the relative error (in ) and the cardinality (or rank) of the estimates along iterations, with iteration 0 corresponding to the two-step estimates. A similar set of results is shown in Tables 10 to 10 for setting A.2, but with a sparse . All other model parameters are identically generated according to the procedure described in Section 5.1.

As the results show, the ML estimates clearly outperform their two-step counterparts, in terms of the relative error in Frobenius norm. On the other hand, both sets of estimates exhibit similar performance in terms of sensitivity and specificity and rank specification. More specifically, when estimating , the ML estimate decreases the false positive rate (higher SPC). Under setting A.1, while estimating and , both estimates correctly identify the rank of , and the ML estimate provides a more accurate estimate in terms of the magnitude of , at the expense of incorrectly including a few more entries in its support set; under setting A.2 with a sparse , improvements in both the relative error of and are observed. In particular, due to the descent nature of the algorithm, we observe a sharp drop in the value of the objective function at iteration 1, as well as the most pronounced change in the estimates.

| performance of | performance of | performance of | ||||||

|---|---|---|---|---|---|---|---|---|

| SEN | SPC | Error | Error | SEN | SPC | Error | ||

| two-step estimates | 0.97 | 0.95 | 0.52 | 0.27 | 5 | 1.00 | 0.98 | 0.12 |

| ML estimates | 0.97 | 0.97 | 0.36 | 0.24 | 5 | 1.00 | 0.95 | 0.05 |

| iteration | 0 | 1 | 2 | 3 | 4 | 5 |

|---|---|---|---|---|---|---|

| Rel.Error | 0.521 | 0.408 | 0.376 | 0.360 | 0.359 | 0.359 |

| Cardinality | 227 | 169 | 160 | 155 | 155 | 155 |

| Value of Obj | 128.14 | 41.74 | 37.94 | 37.85 | 37.70 | 37.70 |

| iteration | 0 | 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 | 9 | 10 |

|---|---|---|---|---|---|---|---|---|---|---|---|

| Rel.Error of | 0.274 | 0.235 | 0.236 | 0.237 | 0.237 | 0.237 | 0.237 | 0.237 | 0.237 | 0.237 | 0.237 |

| Rank of | 5 | 5 | 5 | 5 | 5 | 5 | 5 | 5 | 5 | 5 | 5 |

| Rel.Error of | 0.119 | 0.050 | 0.049 | 0.049 | 0.048 | 0.048 | 0.048 | 0.047 | 0.047 | 0.047 | 0.047 |

| Cardinality of | 30 | 34 | 38 | 41 | 39 | 39 | 39 | 39 | 39 | 39 | 39 |

| Value of Obj | 160.41 | 134.26 | 131.90 | 131.48 | 131.38 | 131.17 | 131.01 | 130.96 | 130.96 | 130.85 | 130.8 |

| performance of | performance of | performance of | |||||||

|---|---|---|---|---|---|---|---|---|---|

| SEN | SPC | Error | SEN | SPC | Error | SEN | SPC | Error | |

| two-step estimates | 0.97 | 0.95 | 0.44 | 0.96 | 0.98 | 0.45 | 1 | 0.99 | 0.35 |

| ML estimates | 0.97 | 0.98 | 0.35 | 0.99 | 0.95 | 0.34 | 1 | 0.98 | 0.30 |

| iteration | 0 | 1 | 2 | 3 | 4 |

|---|---|---|---|---|---|

| Rel.Error | 0.438 | 0.346 | 0.351 | 0.351 | 0.351 |

| Cardinality | 479 | 350 | 325 | 324 | 324 |

| Value of Obj | 156.58 | 48.25 | 38.16 | 36.97 | 36.93 |

| iteration | 0 | 1 | 2 | 3 | 4 |

|---|---|---|---|---|---|

| Rel.Error of | 0.454 | 0.340 | 0.337 | 0.337 | 0.337 |

| Cardinality of | 301 | 325 | 323 | 323 | 323 |

| Rel.Error of | 0.35 | 0.304 | 0.302 | 0.302 | 0.301 |

| Cardinality of | 63 | 70 | 74 | 74 | 74 |

| Value of Obj | 143.942 | 59.63 | 41.46 | 41.87 | 41.87 |

5.3 Simulation results for the block Granger-causality test.

Next, we illustrate the empirical performance of the testing procedure introduced in Section 4, together with the alternative one (in Appendix D) when is sparse, with the null hypothesis being and the alternative being , either low rank or sparse. Specifically, when the alternative hypothesis is true and has a low-rank structure, we use the general testing procedure proposed in Section 4, whereas when the alternative is true and sparse, we use the testing procedure presented in Appendix D. We focus on evaluating the type I error (empirical false rejection rate) when , as well as the power of the test when has nonzero entries.

For both testing procedures, the transition matrix is generated with each entry being nonzero with probability , and the nonzeros are generated from , then further scaled down so that . For transition matrix , each entry is nonzero with probability , and the nonzeros are generated from , then further scaled down so that or , depending on the simulation setting. Finally, we only consider the case where and have diagonal covariance matrices.

We use sub-sampling as in Politis and Romano (1994) and Politis et al. (1999) with the number of subsamples set to 3,000; an alternative would have been a block bootstrap procedure (e.g. Hall, 1985; Carlstein, 1986; Kunsch, 1989). Note that the length of the subsamples varies across simulation settings in order to gain insight on how sample size impacts the type I error or the power of the test.

Low-rank testing.

To evaluate the type I error control and the power of the test, we primarily consider the case where , with the data alternatively generated based on . We test the hypothesis and tabulate the empirical proportion of falsely rejecting when (type I error) and the probability that we reject when (power). In addition, we also show how the testing procedure performs when the underlying has rank . In particular, when , the type I error of the test corresponds to the empirical proportion of rejections of the null hypothesis , while the power of the test to the empirical proportion of rejections of the null hypothesis set to . The latter resembles the sequential test in Johansen (1988).

Empirically, we expect that when , the value of the proposed test statistic mostly falls below the cut-off value (upper quantile), while when , the value of the proposed test statistic mostly falls beyond the critical value with being the sample size, hence leading to a detection. Table 11 gives the type I error of the test when setting , and the power of the test using the upper 0.01 quantile of the reference distribution as the cut-off, for different combinations of model dimensions and sample size.

| type I error () | power () | |||||

| sample size | cut-off | |||||

| 0.028 | 0.123 | 0.227 | 1 | |||

| 0.015 | 0.073 | 0.137 | 1 | |||

| 0.011 | 0.059 | 0.118 | 1 | |||

| 0.070 | 0.228 | 0.355 | 1 | |||

| 0.026 | 0.125 | 0.226 | 1 | |||

| 0.013 | 0.094 | 0.163 | 1 | |||

| 0.484 | 0.751 | 0.857 | 1 | |||

| 0.089 | 0.246 | 0.375 | 1 | |||

| 0.020 | 0.088 | 0.164 | 1 | |||

| 0.997 | 0.999 | 1 | 1 | |||

| 0.608 | 0.828 | 0.908 | 1 | |||

| 0.166 | 0.374 | 0.511 | 1 | |||

| 0.533 | 0.789 | 0.880 | 1 | |||

| 0.130 | 0.306 | 0.452 | 1 | |||

| 0.045 | 0.145 | 0.252 | 1 | |||

| 0.083 | 0.250 | 0.382 | 1 | |||

| 0.039 | 0.133 | 0.234 | 1 | |||

| 0.019 | 0.096 | 0.174 | 1 | |||

| type I error | power | |||||

| cut-off | ||||||

| 0.092 | 0.274 | 0.400 | 1 | |||

| 0.034 | 0.140 | 0.236 | 1 | |||

| 0.022 | 0.096 | 0.178 | 1 | |||

| 0.454 | 0.722 | 0.829 | 1 | |||

| 0.126 | 0.313 | 0.452 | 1 | |||

| 0.062 | 0.184 | 0.284 | 1 | |||

Based on the results shown in Table 11, it can be concluded that the proposed low-rank testing procedure accurately detects the presence of “Granger causality” across the two blocks, when the data have been generated based on a truly multi-layer VAR system. Further, when , the type I error is close to the nominal level for sufficiently large sample sizes, but deteriorates for increased model dimensions. In particular, relatively large values of and larger spectral radius negatively impact the empirical false rejection proportion, which deviates from the desired control level of the type I error. In the case where , the testing procedure provides satisfactory type I error control for larger sample sizes and excellent power.

Sparse testing.

Since the rejection rule of the HC-statistic is based on empirical process theory (Shorack and Wellner, 2009) and its dependence on is not explicit, we focus on illustrating how the empirical proportion of false rejections (type I error) varies with the sample size , the model dimensions and the spectral radius of . To show the power of the test, each entry in is nonzero with probability such that with , to ensure the overall sparsity of satisfies the sparsity requirement posited in Proposition 2. The magnitude is set such that the signal-to-noise ratio is 1.2. Note that the actual number of parameters is , while the total number of subsamples used is 3000 with the length of subsamples varying according to different simulation settings to demonstrate the dependence of type I error and power on sample sizes.

| type I error () | power () | ||||||||

| 200 | 500 | 1000 | 2000 | 200 | 500 | 1000 | 2000 | ||

| 0.244 | 0.097 | 0.074 | 0.055 | 1 | 1 | 1 | 1 | ||

| 0.393 | 0.131 | 0.108 | 0.074 | 1 | 1 | 1 | 1 | ||

| 0.996 | 0.351 | 0.153 | 0.093 | 1 | 1 | 1 | 1 | ||

| 1.000 | 0.963 | 0.270 | 0.115 | 1 | 1 | 1 | 1 | ||

| 0.402 | 0.158 | 0.112 | 0.075 | 0.829 | 0.996 | 1 | 1 | ||

| 0.999 | 0.430 | 0.166 | 0.111 | 1 | 1 | 1 | 1 | ||

Based on the results shown in Table 12, when , the proposed testing procedure can effectively detect the absence of block “Granger causality”, provided that the sample size is moderately large compared to the total number of parameters being tested. However, if the model dimension is large, whereas the sample size is small, the test procedure becomes problematic and fails to provide legitimate type I error control, as desired. When is nonzero, empirically the test is always able detect its presence, as long as the effective signal-to-noise ratio is beyond the detection threshold.

6 Real Data Analysis Illustration.

We employ the developed framework and associated testing procedures to address one of the motivating applications. Specifically, we analyze the temporal dynamics of the log-returns of stocks with large market capitalization and key macroeconomic variables, as well as their cross-dependence. Specifically, using the notation in (1), we assume that the block consists of the stock log-returns, while the macroeconomic variables form the block. With this specification, we assume that the macroeconomic variables are “Granger-caused” by the stock market, but not vice versa. Note that our framework allows us to pose and test a more general question than previous work in the economics literature considered. For example, Farmer (2015) building on previous work by Fitoussi et al. (2000); Phelps (1999) tests only the relationship between the employment index and the composite stock index, using a bivariate VAR model. On the other hand, our framework enables us to consider the components of the S&P 100 index and the “medium” list of macroeconomic variables considered in the work of Stock and Watson (2005).

Next, we provide a brief description of the data used. The stock data consist of monthly observations of 71 stocks corresponding to a stable set of historical components comprising the S&P 100 index for the 2001-2016 period. The macroeconomic variables are chosen from the “medium” list in Stock and Watson (2005); that is, the 3 core economic indicators (Fed Funds Rate, Consumer Price Index and Gross Domestic Product Growth Rate), plus 17 additional variables with aggregate information (e.g., exchange rate, employment, housing, etc.). However, in our study, we exclude variables that exhibit a significant change after the financial crisis of 2008 (e.g. total reserves/reserves of depository institutions). We process the macroeconomic variables to ensure stationarity following the recommendations in Stock and Watson (2005). As a general guideline, for real quantitative variables (e.g., GDP, money supply M2), we use the relative first difference, which corresponds to their growth rate, while for rate-related variables (e.g., Federal Funds Rate, unemployment rate), we use their first differences directly. The complete lists of stocks and macroeconomic variables used in this study are given in Appendix G.

We start the analysis by using the VAR model for the stock log-returns to study their evolution over the 2001-2016 period. Analogously to the strategy employed by Billio et al. (2012), we consider 36-month long rolling-windows for fitting the model , for a total of 143 estimates of the transition matrix . VAR models involving more than 1 lag were also fitted to the data, but did not indicate temporal dependence beyond lag 1.

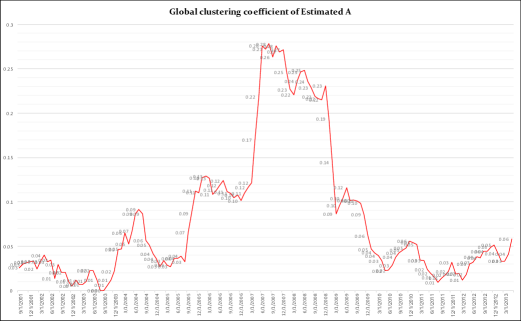

To obtain the final estimates across all 143 subsamples, we employ stability selection (Meinshausen and Bühlmann, 2010), with the threshold set at 0.6 for including an edge in .111The threshold is set at a relatively low level to compensate for the relative small rolling window size. Figure 2 depicts the global clustering coefficient (Luce and Perry, 1949) of the skeleton of the estimated over all 143 rolling windows, with the time stamps on the horizontal axis specifying the starting time of the corresponding window.

The results clearly indicate strong connectivity in lead-lag stock relationships during the financial crisis period March 2007-June 2009. It is of interest that the data exhibit such sharp changes at time points that correspond to well documented events in the literature; namely, March 2007 when several subprime lenders declared bankruptcy, put themselves up for sale or reported significant losses and June 2009 that the National Bureau of Economic Research declared as the end point of the crisis. Similar patterns were broadly observed in Billio et al. (2012); Brunetti et al. (2015), albeit for a different set of stocks and using a different statistical methodology. Specifically, Billio et al. (2012) considered financial sector stocks (banks, brokerages, insurance companies), while Brunetti et al. (2015) considered European banking stocks, and both studies used bivariate VAR models to obtain the results, thus ignoring the influence of all other components on the pairwise Granger causal relationship estimated and hence producing potentially biased estimates of connectivity.

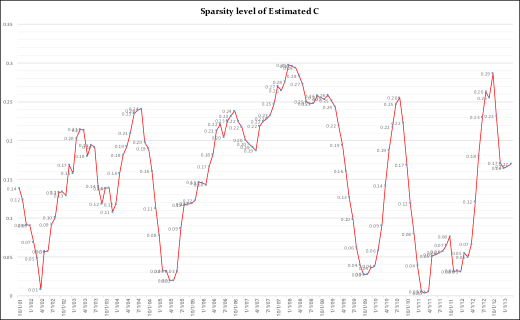

Next, we present the analysis based on the VAR-X component of our model, given by with the stock log-returns corresponding to the block and the (stationary) macroeconomic variables to the block. As before, we fit the data within each rolling window, with the tuning parameters based on a search over a lattice (with , equal-spaced) using the BIC. It should be noted that for the majority of the rolling windows, the rank of is 1 (data not shown). The sparsity level of the estimated over the 143 rolling windows is depicted in Figure 3.

The connectivity patterns in show more complex and nuanced patterns than for stocks. Several local peaks depicted correspond to the following events: (i) March-April 2003, when the Federal Reserve cut the Effective Federal Funds Rate aggressively driving it down to 1%, the lowest level in 45 years up to that point, (ii) January-March 2008, a significant decline in the major US stock indexes, coupled with the freezing up of the market for auctioning rate securities with investors declining to bid, (iii) January-April 2009, characterizes the unfolding of the European debt crisis with a rescue package put together for Greece and significant downgrades of Spanish and Portuguese sovereign debt by rating agencies and (iv) July 2010, that correspond to the enactment of the Dodd-Frank Wall Street Reform and Consumer Protection Act and the acceleration of quantitative easing by the Federal Reserve Board.

Based on the previous findings, we partition the time frame spanning 2001-2016 into the following periods: pre- (2001/07–2007/03), during- (2007/01–2009/12) and post-crisis (2010/01-2016/06) one. We estimate the model parameters using the data within the entire sub-period(s).

The estimation procedure of the transition matrix for different periods is identical to that described above using subsamples over rolling-windows. For the pre- and post- crisis periods, since we have 76 and 77 samples respectively, the stability selection threshold is set at 0.75, whereas for the during-crisis period, at 0.6 to compensate for the small sample size (36). Table 13 shows the average R-square for all 71 stocks, as well as its standard deviation, which is calculated based on in-sample fit; i.e.,the proportion of variation explained by using the model to fit the data. The overall sparsity level and the spectral radius of the estimated transition matrices are also presented. The results are consistent with the previous finding of increased connectivity during the crisis. Further, for all periods the estimate of the spectral radius is fairly large, indicating strong temporal dependence of the log-returns.

| 2001/07–2007/03 | 2007/01–2009/12 | 2010/01–2016/06 | |

|---|---|---|---|

| Averaged R sq | 0.31 | 0.72 | 0.28 |

| Sd of R sq | 0.103 | 0.105 | 0.094 |

| Sparsity level of | 0.17 | 0.23 | 0.19 |

| Spectral radius of | 0.67 | 0.90 | 0.75 |

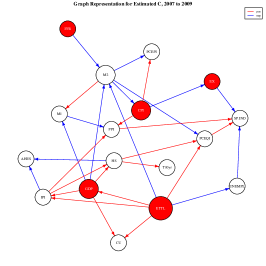

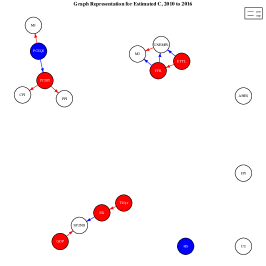

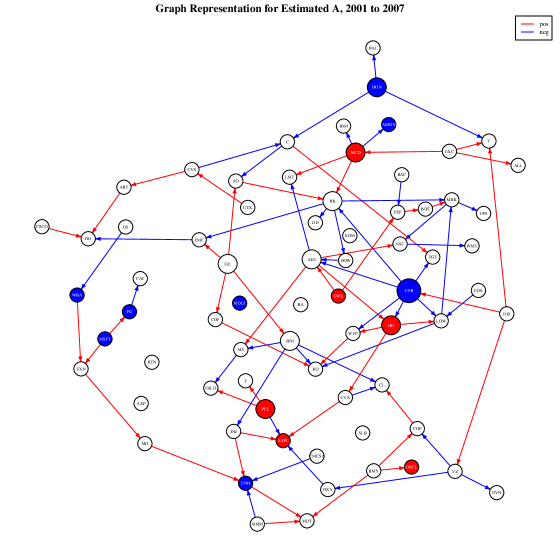

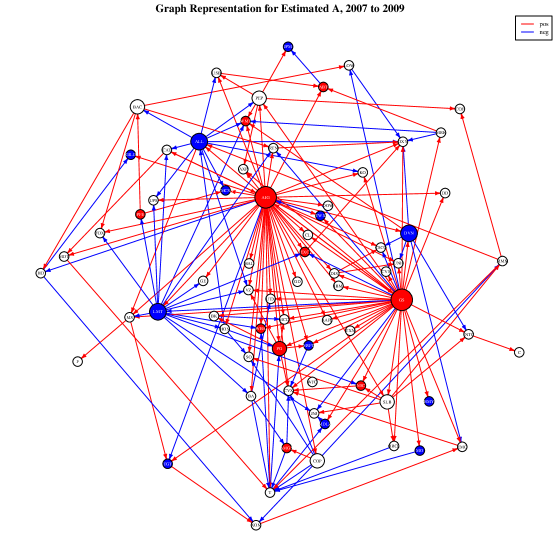

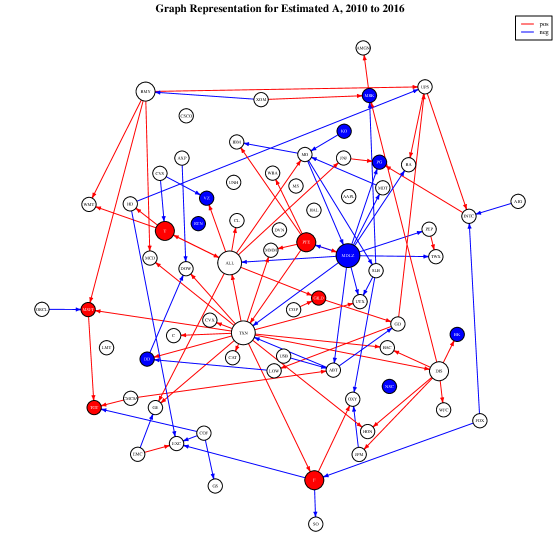

Figures 7 to 9 depict the estimated transition matrices for different periods, as a network, with edges thresholded based on their magnitude for ease of presentation. The node or edge coloring red/blue indicates the sign positive/negative of the corresponding entry in the transition matrix. Further, node size is proportional to the out-degree, thus indicating which stocks influence other stocks in the next time period. The most striking feature is the outsize influence exerted by the insurance company AIG and the investment bank Goldman Sachs, whose role during the financial crisis has been well documented (Financial Crisis Inquiry Commission, 2011). On the other hand, the pre- and post-crisis periods are characterized by more sparse and balanced networks, in terms of in- and out-degree magnitude.

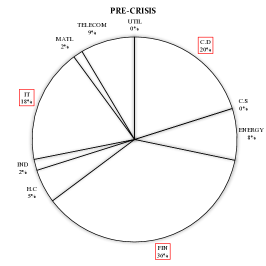

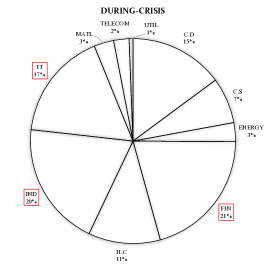

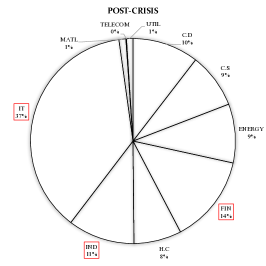

Next, we focus on the key motivation for developing the proposed modeling framework, namely the inter-dependence of stocks and macroeconomic variables over the specified three sub-periods. The -value for testing the hypothesis of lack of block “Granger causality” , together with the spectral radius and the sparsity level for the estimated transition matrices are listed in Table 14. Specifically, for all three periods, the rank of estimated is 1, indicating that the stock market as captured by its leading stocks, “Granger-causes” the temporal evolution of the macroeconomic variables. The fact that the rank of is 1, indicates that the inter-block influence can be captured as a single portfolio acting in unison. To investigate the relative importance of each sector in the portfolio, we group the stocks by sectors. The proportion of each sector (up to normalization) is obtained by summing up the loadings (first right singular vector of the estimated ) of the stocks within this sector, weighted by their market capitalization. Further, the estimated transition matrices ’s are depicted in network form, in Figures 4 to 6. It is worth noting that the temporal correlation of the macroeconomic variables significantly increased during the crisis.

Note that the proportion of various sectors in the portfolio is highly consistent with their role in stock market. For example, before crisis the financial sector had a large market capitalization (roughly 20%), while it shrunk (to roughly 12%) after the crisis. Also, the Information Technology (IT) and Financial (FIN) sectors are the ones exhibiting highest volatility (high beta) relative to the market, while the Utilities is the one with low volatility (low beta) , a well established stylized fact in the literature for the time period under consideration.

Next, we discuss some key relationships emerging from the model. We start with total employment (ETTL), whose dynamics are only influenced by its own past values as seen by the lack of an incoming arrow in Figure 5. Further, an examination of the left singular vector (see Table 15) of strongly indicates the impact of the stock market on total employment. This finding is consistent with the analysis in Farmer (2015), which argues that the crash of the stock market provides a plausible explanation for the great recession. However, the analysis in Farmer (2015) is based on bivariate VAR models involving only employment and the stock index. Therefore, there is a possibility that the stock market is reacting to some other information captured by other macroeconomic variables, such as GDP, capital spending, inflation, interest rates, etc. However, our high-dimensional VAR model simultaneously analyzes a key set of macroeconomic variables and also accounts for the influence of the largest stocks in the market. Hence, it automatically overcomes the criticism leveraged by Sims (1992) about misinterpretations of findings from small scale VAR models due to the omission of important variables, and further echoed in the discussion in Bernanke et al. (2005).

Another interesting finding is the strong influence of the stock market on GDP in the pre- and post-crisis period, consistent with the popular view of being a leading indicator for GDP growth. Further, capital utilization is positively impacted during the crisis period by GDP growth and total employment—which are both falling and hence reducing capital utilization—and further accentuated by the impact of the stock market—also falling—thus reinforcing the lack of available capital goods and resources.

In summary, the brief analysis presented above provides interesting insights into the interaction of the stock market with the real economy, identifies a number of interesting developments during the crisis period and reaffirms a number of findings studied in the literature, while ensuring that a much larger information set is utilized (a larger number of variables included) than in previous analysis. Therefore, high-dimensional multi-block VAR models are useful for analyzing complex temporal relationships and provide insights into their dynamics.

| 2001/07–2007/03 | 2007/01–2009/12 | 2010/01–2016/16 | |

|---|---|---|---|

| -value for testing | 0.075 | 0.009 | 0.044 |

| Sparsity level of | 0.06 | 0.25 | 0.06 |

| Spectral radius of | 0.35 | 0.76 | 0.40 |

| Pre-Crisis | During-Crisis | Post-Crisis | |

|---|---|---|---|

| FFR | -0.24 | -0.26 | -0.23 |

| T10yr | -0.09 | 0.14 | 0.16 |

| UNEMPL | -0.07 | 0.01 | -0.07 |

| IPI | -0.43 | 0.34 | 0.26 |

| ETTL | 0.33 | 0.24 | 0.13 |

| M1 | 0.23 | -0.12 | -0.47 |

| AHES | -0.01 | 0.30 | 0.17 |

| CU | -0.49 | 0.32 | 0.27 |

| M2 | 0.10 | -0.04 | -0.32 |

| HS | 0.51 | -0.02 | -0.02 |

| EX | -0.18 | 0.41 | 0.06 |

| PCEQI | -0.07 | -0.18 | 0.41 |

| GDP | 0.10 | -0.02 | 0.05 |

| PCEPI | 0.00 | 0.14 | -0.01 |

| PPI | -0.15 | 0.00 | 0.06 |

| CPI | 0.01 | 0.15 | -0.31 |

| SP.IND | -0.06 | -0.53 | 0.38 |

Remark 7.

We also applied our multi-block model with the first block corresponding to the macro-economic variables and the second block the stocks variables (results not shown). The key question is whether there is also “Granger causality” from the broader economy to the stock market. The results are inconclusive due to sample size issues that do not allow us to properly test for the key hypothesis whether or not. Specifically, the length of the sub-periods is short compared to the dimensionality required for the test procedure. A similar issue arises, which is related to the detection boundary for the sparse testing procedure during the crisis period. Further, for a sparse , an examination of its entries shows that Employment Total did not impact the stock market, which is in line with the conclusion reached at the aggregate level by Farmer (2015). On the other hand, GDP negatively impacts stock log-returns, which may act as a leading indicator for suppressed investment and business growth and hence future stock returns.

7 Discussion.

We briefly discuss generalizations of the model to the case of more than two blocks, as mentioned in the introductory section. For the sake of concreteness, consider a triangular recursive linear dynamical system given by:

| (29) |

where denotes the variables in group , encodes the dependency of on the past values of variables in group , and encodes the dependency on its own past values. Further, is the innovation process that is neither temporally, nor cross-sectionally correlated, i.e.,

with capturing the conditional contemporaneous dependency of variables within group . The model in (29) can also be viewed from a multi-layered time-varying network perspective: nodes in each layer are “Granger-caused” by nodes from its previous layers, and are also dependent on its own past values. As previously mentioned, in various real applications, it is of interest to obtain estimates of the transition matrices, and/or test if “Granger-causality” is present between interacting blocks; i.e., to test for some .

The triangular structure of the system decouples the estimation of the transition matrices from each equation, and hence a straightforward extension of the estimation procedure presented in Section 2.1 becomes applicable. Specifically, to obtain estimates of the transition matrices ’s for fixed and , and the inverse covariance , the optimization problem is formulated as follows:

| (30) |

where the exact expression for the adapts to the structural assumption imposed on the corresponding transition matrix (sparse/low-rank). Solving (30) again requires an iterative algorithm involving the alternate update between transition matrices and the inverse covariance matrices. Further, for updating the values of the transition matrices, a cyclic block-coordinate updating procedure is used.

Consistency results can be established analogously to those provided in Section 3, under the posited conditions of restricted strong convexity (RSC) and a deviation bound. With a larger number of interacting blocks of variables, lower bounds for the lower extremes of the spectra involve all corresponding transition matrices. The error rates that can be obtained are as follows: (i) if equation only involves sparse transition matrices, then the finite-sample bounds of the transition matrices in this layer in Frobenius norm are of the order , while (ii) if some of the transition matrices are assumed low rank, then the corresponding finite sample bounds are of the order .

Another generalization that can be handled algorithmically with the same estimation procedure discussed above is the presence of -lags in the specification of the linear dynamical system. Based on the consistency results developed in this work, together with the theoretical findings for VAR() models presented in Basu and Michailidis (2015), we expect all the established theoretical properties of the transition matrices estimates to go through under appropriate RSC and deviation bound conditions.

Appendix A Additional Theorems and Proofs for Theorems.

In this section, we introduce two additional theorems that respectively establish the consistency properties for the initializers and , for fixed realizations of the processes and . Specifically, and are solutions to the following optimization problems:

| (31) | ||||

| (32) |

Note that they also correspond to estimators of the setting where there is no contemporaneous dependence among the idiosyncratic error processes. If we additionally introduce operators and defined as

then (31) and (32) can be equivalently written as

where .

Theorem 3 (Error bounds for ).

Suppose the operator satisfies the RSC condition with norm , curvature and tolerance , so that

Then, with regularization parameter satisfying , the solution to (31) satisfies the following bounds:

Theorem 4 (Error bound for ).

Let be the support set of and denote its cardinality. Let be the rank of . Assume that satisfies the RSC condition with norm

curvature and tolerance such that

Then, with regularization parameters and satisfying

the solution to (32) satisfies the following bounds:

In the rest of this subsection, we first prove Theorem 3 and 4, then prove Theorem 1 and 2, whose statements are given in Section 3.2.

Proof of Theorem 3.

For the ease of notation, in this proof, we use to refer to whenever there is no ambiguity. Let and denote the residual matrix and its vectorized version by and , respectively. By the optimality of and the feasibility of , the following basic inequality holds:

which is equivalent to:

| (33) |

where . By Hölder’s inequality and the triangle inequality, an upper bound for the right-hand-side of (33) is given by

| (34) |

Now with the specified choice of , by Lemma 1, i.e., , hence . By choosing , (34) is further upper bounded by

| (35) |

Combined with the RSC condition and the upper bound given in (35), we have

which implies

It is easy to see that these bounds also hold for and , respectively. ∎

Next, to prove Theorem 4, we introduce the following two sets of subspaces and associated with some generic matrix , in which the nuclear norm and the -norm are decomposable, respectively (see Negahban et al., 2012). Specifically, let the singular value decomposition of be with and being orthogonal matrices. Let , and we use and to denote the first columns of and associated with the singular values of . Further, define

| (36) |

Then, for an arbitrary (generic) matrix , its restriction on the subspace and , denoted by and respectively, are given by:

where and is defined and partitioned as

Note that by Lemma 3, . Moreover, when is restricted to the subspace induced by itself (and we write for short for this specific case), the following decomposition for the nuclear norm holds:

Let be the set of indexes in which is nonzero. Analogously, we define