A General Class of Multifractional Processes and Stock Price Informativeness

Abstract

We introduce a general class of stochastic processes driven by a multifractional Brownian motion (mBm) and study the estimation problems of their pointwise Hölder exponents (PHE) based on a new localized generalized quadratic variation approach (LGQV). By comparing our suggested approach with the other two existing benchmark estimation approaches (classic GQV and oscillation approach) through a simulation study, we show that our estimator has better performance in the case where the observed process is some unknown bivariate function of time and mBm. Such multifractional processes, whose PHEs are time-varying, can be used to model stock prices under various market conditions, that are both time-dependent and region-dependent. As an application to finance, an empirical study on modeling cross-listed stocks provides new evidence that the equity path’s roughness varies via time and the stock price informativeness properties from global stock markets.

Keywords: Multifractional process pointwise Hölder exponent LGQV estimation stock price informativeness

MSC (2010): 62F10 62F12 62M86

1 Introduction

Being a natural extension of Brownian motion (Bm) and fractional Brownian motion (fBm, see [30]), multifractional Brownian motion (mBm) has nowadays been successfully applied to many fields such as finance, network traffic, biology, geology and signal processing, etc. Unlike Bm and fBm, mBm is a continuous-time Gaussian process whose increment processes are generally not stationary. However, the feature that multifractional process allows its local Hölder regularity to change via time makes the process flexible enough to model a much larger class of empirical data than the fBm does.

In literature, there exist several slightly different ways to define an mBm (see e.g. [8, 33, 3, 38]). In this paper we define an mBm through the so-called harmonizable representation (see [8, 3]): for the time index ,

| (1.1) |

where:

-

is called the pointwise Hölder exponent (PHE) of the . Recall that, for a continuous nowhere differentiable process , its local Hölder regularity can be measured by the PHE. The PHE of is a stochastic process defined by: for each ,

For the mBm , it is shown by the zero-one law (see e.g. [3]) that its PHE is almost surely deterministic.

-

The complex-valued stochastic measure is defined by the Fourier transform of the real-valued Brownian measure . More precisely, for all belonging to the class of squared integrable functions over (i.e. ), we have

where denotes the Fourier transform of :

Multifractional processes, in particular mBm, come into vogue recently and are widely applied to financial modeling under empirical market conditions. For example, the last systemic financial crisis dated from to has strongly questioned the well-posedness of the classic dichotomy between efficient and inefficient markets. It is believed that the real financial markets are a complex system such that Bm and fBm are too reductive to explain it [14]. Unlike fBm, mBm is flexible enough to overcome this inconvenience, mainly because its PHE can vary via time. Through an empirical study by Bianchi et al. [14], it was shown that the real-world stock prices can be modeled based on an mBm. Later, by estimating the PHE of the stock price dynamics, Bianchi et al. [13] find that the PHE fluctuates around (the sole value consistent with the absence of arbitrage), with significant deviations. In , Bertrand et al. [9] introduce sparse modeling for mBm and apply it to NASDAQ time series. Recently, Bianchi et al. [11] have suggested a new way to quantify how far from efficiency a market is at any fixed time . Their dynamical approach, based on estimation of the time-varying PHE of the log-variations of the 3 stock indexes - Dow Jones Industrial Average (DJIA), the Dax (GDAXI) and the Nikkei 225 (N225), allows to detect the periods in which the market itself is efficient, once a confidence interval is fixed. Note that it is more difficult to estimate the mBm’s PHE than the fBm’s, due to the non-stationarity of the mBm’s increment processes. This problem becomes even more challenging when modeling an individual stock price (e.g. stock price of a particular entity) in lieu of averaged equity indexes, because the former one is not necessarily non-arbitrage and its corresponding PHE may be time-dependent and may take arbitrary values between 0 and 1. So far, there is not yet a satisfying model fitting the individual stock price process using multifractional processes. In this paper we aim to provide suitable models to describe these individual stock prices. Our main contribution consists of the following.

-

1.

We introduce a general class of multifractional processes, that can be used to describe the behavior of individual stock returns on equity markets. The proposed model is based on the assumption that the stock return is some unknown function of both time and an mBm at that time (see Section 2).

-

2.

Under the above assumption, we develop a new efficient approach to estimate the above model’s PHE. The estimators from our approach are shown to be consistent (see Section 3).

-

3.

In Section 5, through a simulation study, we compare the performances of three estimation approaches (our new localized generalized quadratic variation approach (LGQV), the classic GQV approach and the oscillation method) on various functions .

-

4.

In the empirical study (Section 6), We apply the general multifractional process to model the individual stocks and use LGQV approach to estimate cross-listed stocks’ PHEs. Then we determine the market factors that drive the individual stock returns’ PHEs. The estimators of the PHEs reveal that the PHEs of individual stock prices are time-varying under various market conditions and their behaviors vary via different market regions. This interesting result enables us to examine the main individual stock’s PHE drivers.

Note that the Matlab codes used in Sections 5 and 6 are provided. We conclude the paper in Section 7 and provide proof of the main result in Sections 8. The supplementary graphs, tables and other detailed technical proofs are given in Appendix see (Section 9).

2 A general class of multifractional processes

Before introducing the general multifractional model that we are interested in, we briefly review the estimation of the multifractional process’ PHE.

In the multifractional process modeling problem, there is an obstacle : the PHE is basically not straightforwardly observed. The issue of estimating the PHE effectively arises. There are so far a number of estimation strategies existing in literature. We refer to [17, 18, 10, 5, 26, 39] and the references therein.

Coeurjolly [17, 18] estimates the PHE of an mBm, starting from an observed discrete sample path of that mBm, using the LGQV approach (see also [16]). Bertrand et al. [10] study the same estimation problem as in [17, 18], using the nonparametric estimation approach - increment ratio (IR) statistic method. This IR estimator has been later improved by Bardet and Surgailis [5] to the so-called pseudo-increment ratio approach, and it is applied to estimate the PHE of a more general multifractional Gaussian process (whose increments are asymptotically a multiple of an fBm) than mBm. There exist other approaches to estimate the PHE of fBm, that can be possibly extended to estimate the PHE of mBm. For example, in chaos theory and time series analysis, the statistical self-affinity is another measurement of the process path roughness. Since this exponent is tightly related to the PHE of self-similar processes (e.g. fBm), the detrended fluctuation analysis (DFA) methods developed by Peng et al. [34, 35] can be used to estimate the PHE of fBm. The time-varying PHE of mBm can be then approximated by applying the DFA piecewisely over time. However, the statistical self-affinity is not equivalent to the PHE of a process, because it does not share all the properties of the Hausdorff dimension [34, 35], while the Hausdorff dimension is equivalent to the PHE when the corresponding process is self-similar. In literature, it has been shown that the wavelet-based method is actually more accurate than the DFA on estimation of the PHE. Muzy et al. [32] have obtained representations of turbulence data and Brownian signals via wavelet decompositions. Bardet et al. [4] have applied the wavelet coefficient methods to estimate the PHE of long-memory processes (e.g. fBm with its PHE being greater than ), where some rate of convergence of the estimators are derived. Wendt et al. [42] have developed the wavelet leader based multifractal analysis for estimating 2D functions (images). Inspired by the above works, Jin et al. [26] have provided a wavelet-based estimator of the time-varying PHE of a class of multifractional processes with a fine convergence rate, when the observations are the wavelet coefficients of some unknown function of a multiple of mBm, i.e. the observed process is of the form , with and being unknown -functions. In both [5] and [26], estimators of PHE with fine convergence rates are constructed and strategies for selecting input parameters are discussed.

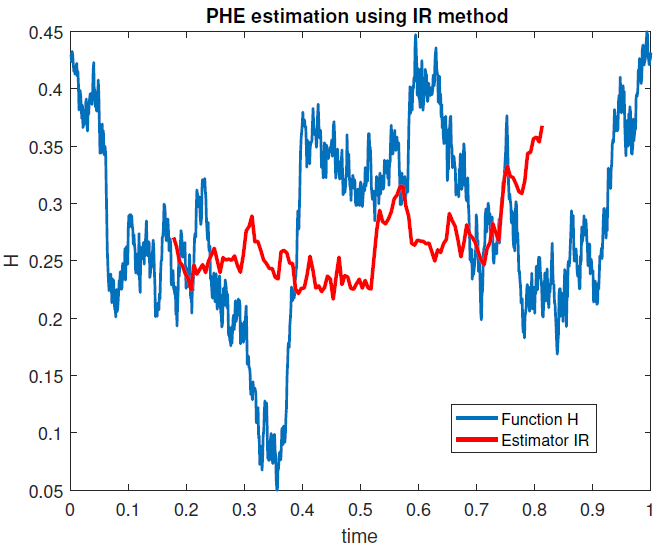

Note that in our paper we also consider a model more general than the one in [26], in that it allows to be a function of both and , i.e. we assume the observed signal is some unknown function of time and mBm : . We apply the LGQV-based approach to estimate the PHE of , when one of its discrete paths is observed. Similar to Jin et al. [26], an estimator with fine convergence rate is constructed and appropriate parameter selection is discussed. In [39, 40] the oscillation estimation method, which could be applied to estimate the PHE of all processes with continuous paths, is discussed. The main advantages of our approaches are: (1) The model is simple and general enough for finance application. (2) Compared to the oscillation estimation method, the LGQV method has higher accuracy and it allows us to select the input parameter from a large range of values. We will provide a fine rate of convergence of our LGQV estimator, which will further help practitioners to determine the best input parameter values. (3) One disadvantage of the increment ratio approaches is that, it is unable to estimate the PHE over the whole time interval . Figure 1 is an example showing that, only part of the path of is estimated by the increment ratio method. However, the algorithm for LGQV-based approach can estimate pointwisely from to . Moreover, it can be easily implemented using various programming languages such as Matlab, R and Python, etc.

Throughout this paper we consider the following model: for ,

| (2.1) |

where

-

is an mBm defined in (1.1). Assume that its PHE belongs to the class of functions (this means that is second-order continuously differentiable over ) and , where and .

-

is supposed to be an unknown deterministic -function. Also we assume that for almost every and there exist two constants such that for almost every .

-

Suppose that a discrete sample path of : is observed for some large enough.

From (2.1) we see that the model is driven only by the time index and the mBm . It is quite general because the function “lives” in a large class of functions , and more importantly, it is supposed to be unknown. Examples of include the mBm, the self-regulating processes based on mBm [7], and those in Section 5.

3 LGQV estimation of the PHE

Observing the discrete sample path of :

where denotes an integer large enough, our goal is to propose a method allowing to estimate the PHE of the hidden mBm at an arbitrary time . To this end, we apply a localized generalized quadratic variations (LGQV) estimation method. Before stating our main results, we need to briefly introduce some notations which will be used throughout the rest of the paper.

-

•

As usual, is an arbitrary but fixed finite sequence having vanishing moments, that is,

(3.1) -

•

For all integer and the generalized increments of , , and that of , , are defined by,

(3.2) where and denote the values of the processes and , at time , that is,

(3.3) -

•

For all integer , we denote by the set of indexes defined by,

(3.4) where is an arbitrary function of , valued in , which satisfies for each integer , and . Note that labels the times in the neighborhood of . As mentioned in [17, 18], the estimation of only relies on the observations of , for being “neighbored to” . Consequently, the estimation accuracy will be in terms of the size of the neighborhood selected for each . Both theoretical and empirical studies tend to show that, the size of the neighborhood shouldn’t be chosen too large nor too small, i.e. there is a trade-off between the estimator’s rate of convergence and bias.

-

•

For all integer we define to be the number of points in :

(3.5) We then quickly observe that

(3.6) where is the integer part function.

The main results are presented in the next section.

4 Estimation of the PHE

In this section we construct a LGQV consistent estimator of , of . Recall that, in statistics theory, an estimator of a parameter is (weakly) consistent if converges to in probability, as . Let be an arbitrary sequence of random variables and be a sequence of non-vanishing real numbers, we use the notations

to denote

Remark that leads to , and the almost sure convergence implies the convergence in probability.

Our first main result below provides a delicate identification of the covariance of the generalized increments of the multifractional process of a particular form . Later we will need this result for estimating the PHE of the more general function of : .

Proposition 4.1

Let be an mBm and , with being a second order stochastic process independent of , and the bivariate function satisfies . For a sequence , assume , then for every , we have,

We quickly point out that, in the above proposition, there is not any inconvenience to regard to be a class deterministic function. It is also worth noting that Proposition 4.1 has its own interests, since it gives an exact estimation of the covariance structure of the generalized increments of , with a fine rate of convergence for its remaining term. To motivate the above facts we briefly compare Proposition 4.1 to Lemma 1 in [17] below:

- 1.

- 2.

- 3.

The proof of Proposition 4.1 is technical and long. It is moved to Section 9: Appendix.

The second main result involves estimation of the PHE of the general process , under a very general condition:

Theorem 4.2

Pick a sequence with its first moments being vanishing. We list the following conditions on .

-

(i)

satisfies:

-

(ii)

satisfies:

For , define

| (4.3) |

and

| (4.4) |

where is the base- logarithm.

(1) If satisfies the condition , we have

(2) If satisfies the conditions -, then

where denotes the convergence almost surely.

Theorem 4.2 is our key result. It provides consistent estimators of the PHE of in a very general setting. Moreover, Theorem 4.2 (1) elaborates the rate of convergence of the estimators. We see that the rate of convergence depends only on the sample size and . The proof of Theorem 4.2 is provided in Section 8.

5 Simulation study: selection of parameters and comparison with benchmark approaches

We conduct simulation studies to compare the performance of our PHE estimator provided in Theorem 4.2 with the other two benchmark methods: the so-called classic GQV (see [6, 3]) and oscillation method (see [6]). Below we briefly introduce the classic GQV and oscillation method.

-

•

The GQV method is applied to estimate the PHE of the so-called generalized mBm [3] and some multifractional signals [6], it is based on the following result (see Theorem 2.2 in [3]):

where . Note that the above convergence holds almost surely if , however, milder condition exists for the convergence in probability to hold. We also remark that although our approach is also based on the classic GQV, it is more complex than the above one, since in our case some constant should be introduced to cancel the unknown factor in (8.30).

- •

The implementation in Matlab codes of the above two approaches can be found in FracLab by INRIA: https://project.inria.fr/fraclab/. We use the code version FracLab 2.2 in the empirical study111https://project.inria.fr/fraclab/download/overview/..

5.1 Parameter selection

To be more convenient, we denote by LGQV (Localized Generalized Quadratic Variation Method) the PHE estimation provided in Theorem 4.2. In this section, we discuss of the best choice of the functional parameter in Theorem 4.2. In LGQV and classic GQV, we set the estimation neighborhood radius to be of the form

In LGQV, to choose some that satisfies the condition in Theorem 4.2, we consider the following condition which is slightly stronger than the condition :

The reason why we don’t choose but a stronger condition is to avoid the system computational error, which often has a strong impact when the parameter is close to an extreme value.

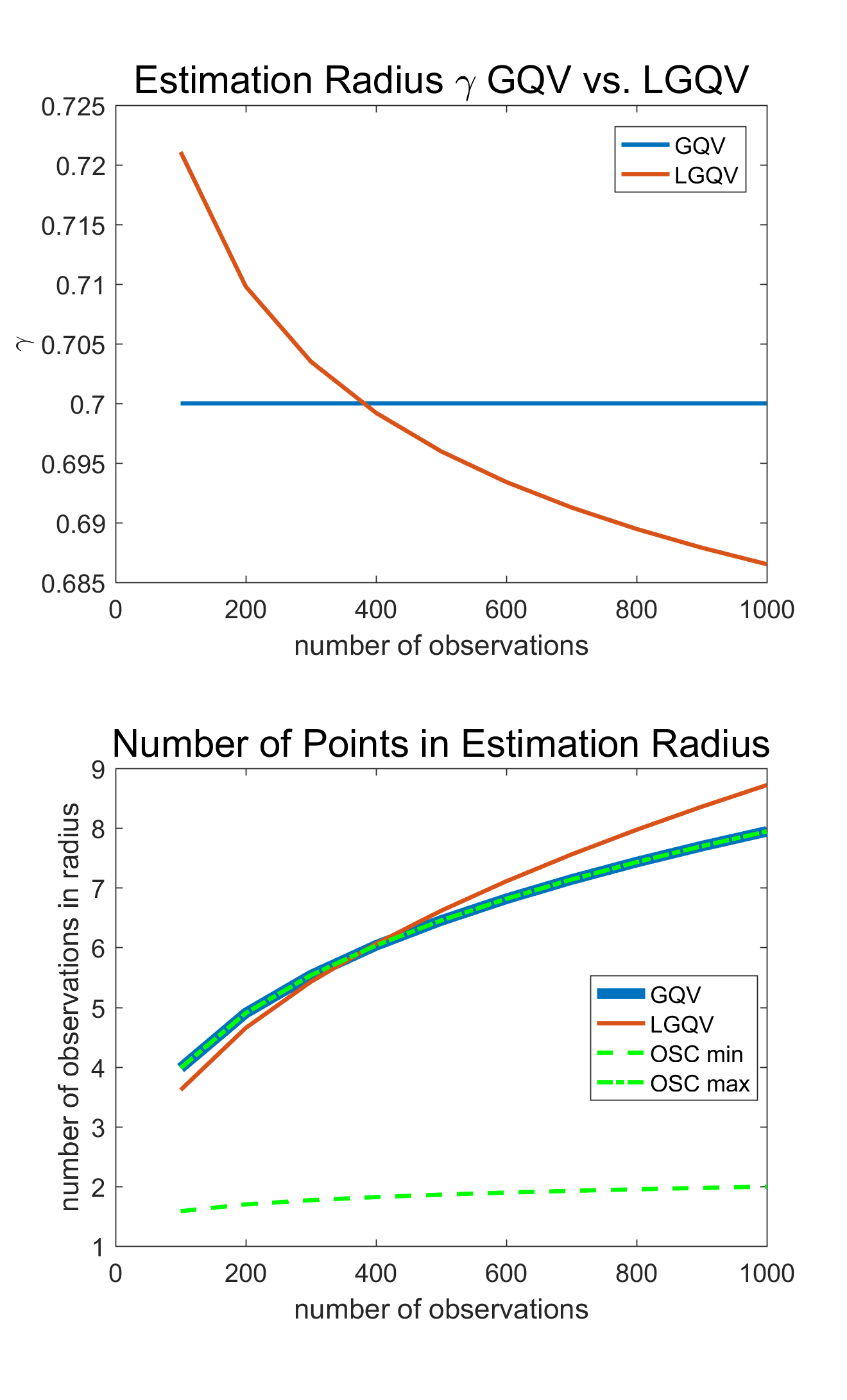

As a benchmark, in the example of the classic GQV in [6], the neighborhood radius parameter is selected to be a constant throughout the simulation study. A noticeable feature of radius selection in LGQV is that decreases as increases, in contrast to the constant selected by the classic GQV method. Moreover by this choice the neighborhood radius of LGQV method is smaller than that of the classic GQV approach once , as illustrated by the graph on the left hand-side of Figure 2.

In the oscillation method, a neighborhood for estimating the PHE at each point is required. By default we set with and in the approach (see [6, 39, 40]).

We have provided the theoretical choice on number of points in estimation neighborhood, which allows fraction number of points. In actual estimation using GQV and LGQV methods, we round the theoretical number of points in neighborhood to its closest integer value. For oscillation method, the lower bound of neighborhood is rounded to ceiling integer value, whereas the upper bound of neighborhood is rounded to floor integer value.

5.2 Experiments design

In this section, we demonstrate simulation experiments that examine and compare estimation accuracy of LGQV estimator with conventional benchmark methods, i.e., the classic GQV with and oscillation methods, in various functional forms of .

The PHE that we choose is , for . We examine the convergence performance of estimators by using the simulated scenarios of , with ranging from 100 to 1000. We utilize Wood-Chan method [43] to generate independent scenarios of mBm. The scenarios of with various forms of , can therefore be generated. We then estimate the PHE straightforwardly starting from these scenarios of .

We then compare the estimation outcome of LGQV with benchmark GQV and oscillation method, using scenarios from different categories of functional forms of . The root-mean-squared error (RMSE) is used to measure and quantify PHE estimation performance. We use independent scenarios to compute each RMSE from the original .

We propose three categories of functional forms of . The first category contains single variate functions of mBm, where is a function. With being smooth enough, the transformed mBm in this category does not behave significantly differently from an mBm itself when the values of are close to 0. Therefore, we expect that LGQV has similar estimation performance to the benchmark methods. The specific functional forms in the first category include:

-

•

,

-

•

.

The second category contains functional forms of both time and mBm, e.g. . This functional type of mBm is where LGQV has advantage over the classic GQV method. It is important to remark that it is more reasonable to use this functional form to model financial time series. Note that the most commonly used form in financial derivative pricing is (where denotes a Bm), on which an Itô formula is often applied. Then our model naturally extends the latter one. We expect that the RMSE of LGQV is smaller in this category than the two benchmark approaches. The functional forms we take in this category include:

-

•

,

-

•

.

The third category of the functional form is , where is a stochastic process independent of (this includes the case for being a deterministic function with continuous non-differentiable path). We would consider the case where with being a smooth function. This is the scenario where both LGQV and classic GQV are not applicable. The PHE estimation of this type of functional form will be of interest for future research. The functional forms we consider in this category include:

-

•

,

-

•

,

where is a Brownian motion independent of the mBm .

We perform simulation study with sample path lengths . For each sample path length , we simulate 100 independent scenarios of each of the above functional type and estimate its PHE using LGQV, the classic GQV and oscillation method, respectively. The averaged RMSE of the PHE estimation is calculated for each method. The speed of convergences of LGQV method with various differencing orders () are illustrated and compared as well.

5.3 Simulation results

Before presenting the simulation results, it is interesting to consider the simplest functional form of mBm: . Theoretically and intuitively, in this case the classic GQV method should have better converging performance than LGQV. The reason is that the latter approach estimates the first and second order terms of the Taylor expansion of , which is not necessary in this particular case. As a result, the LGQV slows down the estimator’s convergence speed. The performances of both approaches when are shown in Table 1 and left-top graph in Figure 8 in Appendix (see Section 9.5). In this special case, it is not surprising that the classic GQV method outperforms LGQV in terms of lower averaged RMSE and estimation standard deviation.

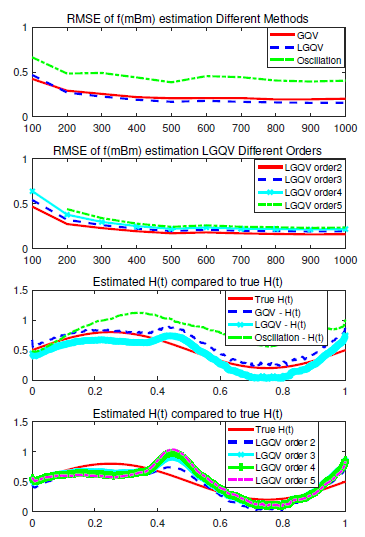

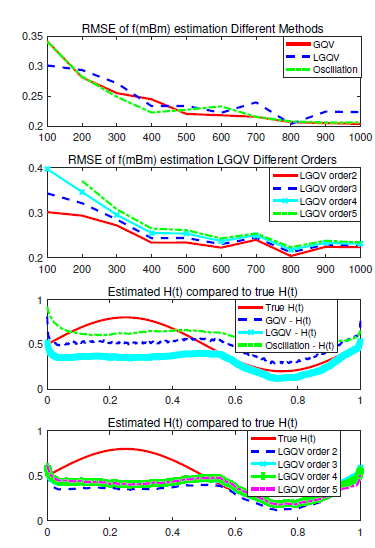

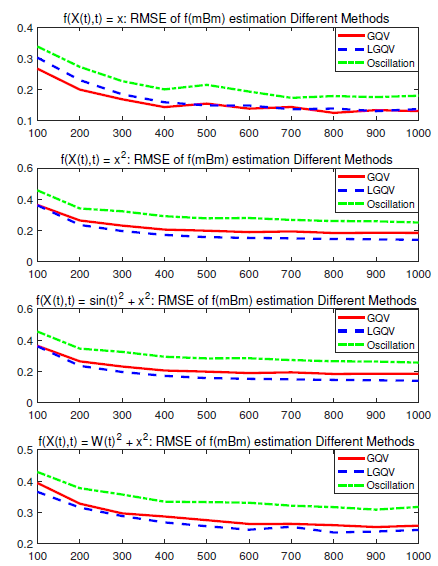

In Figure 3, we illustrate the comparison outcome of the PHE estimation for the first category functional form . From the figure we observe the following:

- (1)

-

From the left-top graph, both the classic GQV and LGQV methods have consistently (averaged) converging tendency towards lower RMSE. The LGQV method outperforms the classic GQV method when . And the averaged RMSE of LGQV method is (), which is lower than that of the classic GQV method when .

- (2)

-

The right-top graph shows that the averaged RMSE grows as the order of differences grows in the LGQV estimates. The differencing order of 2 has the lowest estimation error. The reason is that higher differencing order reduces the number of observed points for each estimation neighborhood, hence it reduces the accuracy of the estimation. High order generalized variations could perform better when the number of observations is relatively large.

- (3)

-

The left bottom graph shows that the oscillation method overestimates .

- (4)

-

In the two bottom graphs we see that the classic GQV and LGQV estimators are definitely better the oscillation estimator. This is because these two approaches are specifically designed for Gaussian processes. But they seem to have a “hump” shape delaying to the peak of true . The classic GQV method has worse delayed overestimation than LGQV method. The higher order the differencing is in LGQV method, the severe the overestimation following a peak on Hölder parameters. In addition, the LGQV method overreacts when the true drops down, but has better performance on tail estimation (around the tail edge in this context). The good performance of the classic GQV comes from the reason that is close to when is near 0, as in the case in our context.

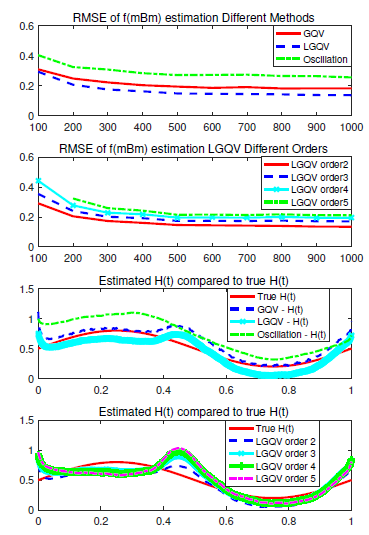

In Figure 4, we illustrate the comparison of PHE estimation results for . The outcome confirms the fact that LGQV consistently outperforms the classic GQV method in terms of lower RMSE, when analyzing the functional form . Quantitatively, the averaged RMSE by LGQV (when ) for this functional form is , which is less than the classic GQV case. Both the classic GQV and LGQV methods outperform the oscillation method, again due to the classic GQV approaches’ specialization on estimating PHE for Gaussian processes. The oscillation estimator of has similar shape to the its target, but it constantly overestimates for each and has PHE estimation exceeding 1, due to the system error.

Figure 5 shows the RMSE comparison of PHE estimation for different methods within the third functional form category, where neither the classic GQV nor LGQV estimation is applicable. The function considered is , where is an independent Brownian motion. The standard deviation of RMSE for LGQV method is higher than the ones for the competing methods. The partial reason for LGQV method not being applicable is that the assumption that for is violated. Another reason that the classic GQV performs better is that the LGQV is more sensitive than the classic GQV and we have selected wider neighborhood radius than the classic GQV does in this simulation study (see Figure 2).

More detailed PHE estimation comparison statistics of each method when with 100 simulations are listed in Table 1. It shows the numerical comparison results for all functional forms considered in this simulation study. The corresponding figures are also given in Figure 8 in Section 9. The conclusion from these examples is consistent with what we have elaborated above.

| Stats. | GQV | LGQV (2) | LGQV (3) | LGQV (4) | LGQV (5) | OSC | |

|---|---|---|---|---|---|---|---|

| avg. | 0.13068 | 0.1369 | 0.1742 | 0.1998 | 0.2187 | 0.1797 | |

| std. | 0.02061 | 0.0224 | 0.0279 | 0.0307 | 0.0324 | 0.0396 | |

| max. | 0.18558 | 0.1871 | 0.235 | 0.2666 | 0.2931 | 0.2759 | |

| min. | 0.07911 | 0.0787 | 0.0968 | 0.1147 | 0.1313 | 0.1076 | |

| avg. | 0.1837 | 0.1394 | 0.1727 | 0.1955 | 0.2119 | 0.2504 | |

| std. | 0.0263 | 0.0224 | 0.0269 | 0.0298 | 0.0321 | 0.077 | |

| max. | 0.252 | 0.1894 | 0.2448 | 0.2755 | 0.2912 | 0.5204 | |

| min. | 0.1213 | 0.081 | 0.0924 | 0.1053 | 0.12 | 0.1147 | |

| avg. | 0.2032 | 0.1592 | 0.1919 | 0.2157 | 0.2337 | 0.4043 | |

| std. | 0.101 | 0.0899 | 0.0919 | 0.0971 | 0.1042 | 0.6456 | |

| max. | 1.1086 | 0.9641 | 1.0001 | 1.0614 | 1.1371 | 6.3053 | |

| min. | 0.122 | 0.0912 | 0.1075 | 0.1165 | 0.1244 | 0.1175 | |

| avg. | 0.1804 | 0.1352 | 0.171 | 0.195 | 0.2119 | 0.2538 | |

| std. | 0.0262 | 0.0214 | 0.0267 | 0.0305 | 0.033 | 0.0449 | |

| max. | 0.2522 | 0.1826 | 0.2257 | 0.2574 | 0.278 | 0.4135 | |

| min. | 0.1249 | 0.0767 | 0.0913 | 0.1034 | 0.1115 | 0.158 | |

| avg. | 0.1838 | 0.1394 | 0.1727 | 0.1955 | 0.2119 | 0.2556 | |

| std. | 0.0263 | 0.0224 | 0.0269 | 0.0298 | 0.0321 | 0.0789 | |

| max. | 0.252 | 0.1894 | 0.2448 | 0.2755 | 0.2912 | 0.5202 | |

| min. | 0.1214 | 0.081 | 0.0924 | 0.1053 | 0.12 | 0.1163 | |

| avg. | 0.2038 | 0.2234 | 0.2278 | 0.2309 | 0.2342 | 0.2064 | |

| std. | 0.0286 | 0.0296 | 0.0329 | 0.0348 | 0.036 | 0.0381 | |

| max. | 0.2817 | 0.2928 | 0.3034 | 0.3126 | 0.3165 | 0.2823 | |

| min. | 0.1423 | 0.1716 | 0.1609 | 0.1544 | 0.1515 | 0.1212 | |

| avg. | 0.2568 | 0.2432 | 0.2455 | 0.2482 | 0.2525 | 0.3169 | |

| std. | 0.0351 | 0.0349 | 0.0378 | 0.0397 | 0.0413 | 0.0543 | |

| max. | 0.3541 | 0.3447 | 0.3595 | 0.365 | 0.3648 | 0.4659 | |

| min. | 0.1752 | 0.1716 | 0.1611 | 0.1495 | 0.1447 | 0.1836 |

We summarize the advantage of LGQV method over the conventional benchmark PHE estimation methods. The converging rate of LGQV method improves significantly, when the underlying process takes functional form of time and mBm. Specifically in our study, the averaged RMSE decreases by in the single variate functional cases and decreases by in the bivariate functional cases. The standard deviation of PHE estimation reduces by and in the two functional form cases, respectively. Therefore, the LGQV method is applicable to a much larger set of multifractional processes in practice: functional form of .

6 An empirical study: application to financial time series

Recently, Keylock [28] has formulated the gradual multifractal reconstruction approach and applied it to stock market returns spanning the 2008 crisis. By comparing the relation between the normalized log-returns and their Hölder exponent for the daily returns of eight financial indexes, Keylock observes that the change for NASDAQ 100 and SP 500 from a non-significant to a strongly significant cross-correlation between the returns and their Hölder exponents from before the 2008 crash to afterwards. However Asian markets don’t exhibit significant cross-correlation to those from elsewhere globally.

Our setting and goal in this section is different from [28]. We apply the functional form to model equity prices and examine the PHE of individual stock series using the proposed LGQV method, from three markets. Then we compare the PHEs of the above three markets. Note that other than equity indexes and stock prices, the current financial literature has also introduced mBm in modeling stochastic volatilities [19] and currency exchange rates [12], etc.

We improve the work of [13] by exploring the functional form of mBm in equity model and extend [19] by providing a practical PHE estimation method using mBm framework. To our best knowledge, this framework is also the first one to provide a financial interpretation of the PHE: we interpret the PHE as a quantitative measure of stock price informativeness on equity market. That is, PHE can be regarded as a new dimension on measuring information content embedded in stock price series. To see this, we provide the motivation on describing equity price informativeness by PHE and establish the connection by showing the shared characteristics of these two concepts.

6.1 PHE and price informativeness

To motivate the interpretation, we summarize three common features of stock market informativeness and the PHE of price series.

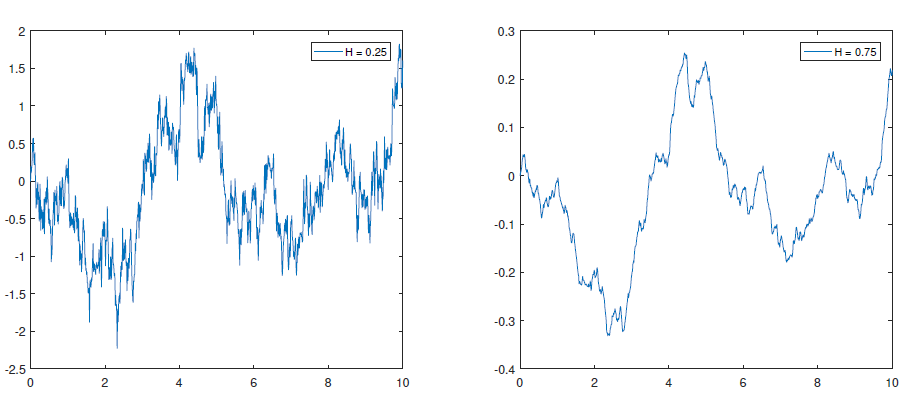

First note that, the more information is contained on the market, the lower is the PHE value of the stock price series, ceteris paribus. Consider the two simulated mBm paths plotted in Figure 6 with different PHEs. With smaller value of its PHE (see the graph on the left-hand side), the mBm path is “rougher” and presents more local fluctuations within certain time interval than that of larger PHE value case (see the graph on the right-hand side). These “zig-zags” in local ranges are analogous to arrivals of information to the market and investors’ digest of the information. More intense arrivals of information generate more local fluctuations, resulting in a lower PHE value.

Secondly, the PHEs of price series and price informativeness of stocks are both time-varying. That is, the quantity of information on the market for the same underlying stock should not be a constant. The time-varying feature of information content orients from business cycle and cyclically financial reporting procedure regulated by SEC. In addition, corporate events, such as merger and acquisition, stock repurchase and executive management change etc., randomly introduce pertinent information to the equity market. The property of multifractionality reflects this time-varying feature of information flows, where our informativeness measure (PHE) allows to be a function of time. Bianchi et al. [13] point out that the equity index has its PHEs close to , but deviations are also observed over the past decades, which supports the non-constant PHE argument under the mBm framework.

Thirdly, corporate characteristics and market conditions influence the information content, as well as the PHE of the underlying stock. More specifically, corporate factors such as business complexity, growth stage, and idiosyncratic features may cause their stocks’ PHEs to be significantly different with each other. For instance, a company with high analyst coverage is expected to have more information on the market and thus lower PHE. Market effects, such as capitalization size, accounting quality and efficiency, would also contribute to changing the PHE values of its stock, from one period to another.

Given the informativeness context, we estimate and compare the PHEs of cross-listed stocks. The empirical study explores the main market factors that impact stock price informativeness.

6.2 Other informativeness measures in literature

Our informativeness measure provides new vision to common believes of information content carriers in the existing literature. Accounting and financial reports are conventionally regarded as the main information sources [24, 15]. Traditional measures of information content in finance literature also include quote revisions [22], internet stock message boards [1] and implied volatility from option markets [21] etc. Besides corporate level effects, different markets and market conditions determine the information content as well. Morck et al. [31] suggest that stock markets in developed economics are more useful as information processor than the stock markets in emerging economics. They argue that better property rights protection in advanced economics explains the fact that stock prices synchronize more closely in emerging markets than in advanced economics. Ivković and Weisbenner [25] show that there is significant asymmetric information between geographical local and nonlocal investors. In addition, empirical study shows that local holdings generates excess return over nonlocal holdings. These findings seem to support the home bias theory [20, 41].

We propose the PHE to be a new quantitative measure of all the above price informativeness on equity markets. As one example, we examine whether this new measure is lieu with the existing stock price informativeness measures in the following two sections.

6.3 Empirical study on real data

This empirical study aims to disentangle the main factors that explain informativeness and informative flow on global equity markets. We focus on a special set of equities: cross-listed stocks. The cross-listed stock refers to as same underlying entity but its stocks are listed on multiple equity markets. The advantage of choosing cross-listings are twofold. Firstly, corporate characteristics keep the same when considering same underlying entity. Secondly, comparing price informativeness measure (PHE) provides evidence on revealing the real information source and answer the question [27]: where does price discovery occur?

We select cross-listed stocks that are listed on the following three equity markets simultaneously for more than 10 years:

- (1)

-

China Mainland (SSE and SZSE, home market).

- (2)

-

Hong Kong (SEHK).

- (3)

-

The U.S. (NYSE) stock markets

The three-market setting enables us to uniquely compare pairwisely the factors that determine informativeness. Empirical results will lead us to the conclusion of the debating question: which factor contributes more on information content, location or market quality?

To be specific, China Mainland’s market locates very close to Hong Kong markets in contrast to the far US market. The term “location” here includes not only geographical exchange location, but also language, time zone, culture and local knowledge etc., which is commonly believed to bring more information to home market investors than foreign market investors. Meanwhile, Hong Kong and the US stock markets are widely believed to be the ones with best market quality, in terms of their easier capital accessibility and sophisticated accounting system, where advanced financial and accounting information drives informativeness significantly.

The China Mainland and Hong Kong markets have location in common but different levels of market quality. Hence the comparison of PHE between cross-listed stock in China Mainland and HK markets reveal the effect of market quality on stock price informativeness. At the meantime, Hong Kong and the US markets have same level of market quality but different locations. Then the comparison of PHE between HK and US markets addresses the effect of home bias on information content.

Table 2 in Appendix presents all cross-listed stocks that satisfy the condition on simultaneously listing on US, HK and China markets for more than 10 years. We exclude the mutual exclusive non-trading days for these three markets, and yield three time series with common trading days for each of the stock. Our empirical data contains 11 stocks and 33 price time series (for three markets in total). The estimation period starts from the earliest available date and ends up to December 30, 2016. Among the samples, the smallest number of observations for each market is , and the largest number of observations is .

We model the equity price series by , an unknown functional form of time and mBm, and estimate each series’ PHE as price informativeness measure. The empirical PHE comparison of the stocks is presented in the next subsection.

| Company Name | T. NYSE | Sector | Date NYSE | Date SHSE | Date SEHK | T. SHSE | T. SEHK |

|---|---|---|---|---|---|---|---|

| Aluminum Corporation Of China | ACH | Primary Production of Aluminum | Dec. 12, 2001 | April 30, 2007 | Dec. 12, 2001 | 601600 | 2600 |

| China Eastern Airlines | CEA | Air Transportation | Feb. 4, 1997 | Nov. 5, 1997 | Feb. 5, 1997 | 600115 | 670 |

| China Unicom | CHU | Radiotelephone Communications | June 21, 2000 | Oct. 9, 2002 | June 22, 2000 | 600050 | 762 |

| Guangshen Railway | GSH | Railroads | May 13, 1996 | Dec. 22, 2006 | May 14, 1996 | 601333 | 525 |

| Huaneng Power International | HNP | Electric Services | Oct. 6, 1994 | Dec. 6, 2001 | Jan. 21, 1998 | 600011 | 902 |

| China Life Insurance | LFC | Life Insurance | Dec. 17, 2003 | Jan. 9, 2007 | Dec. 18, 2003 | 601628 | 2628 |

| PetroChina | PTR | Crude Petroleum & Natural Gas | April 4, 2000 | Nov. 5, 2007 | April 7, 2000 | 601857 | 857 |

| Sinopec Shanghai Petrochemical | SHI | Crude Petroleum & Natural Gas | July 26, 1993 | Nov. 8, 1993 | July 26, 1993 | 600688 | 338 |

| China Petroleum & Chemical | SNP | Petroleum Refining | Oct. 18, 2000 | Aug. 8, 2001 | Oct. 19, 2000 | 600028 | 386 |

| Yanzhou Coal Mining | YZC | Bituminous Coal & Lignite Surface Mining | Mar. 31, 1998 | July 1, 1998 | April 1, 1998 | 600188 | 1171 |

| China Southern Airlines | ZNH | Air Transportation | July 30, 1997 | July 25, 2003 | July 31, 1997 | 600029 | 1055 |

6.4 Empirical results

We separate the whole estimation period (earliest available up to December 30, 2016) into three subintervals: prior, within and post global financial crisis periods. In our study, the subprime crisis time frame is defined as from the beginning of year 2007 up till the end of 2009. The definition of financial crisis in our paper is longer than common definitions. But the information formation, propagation and digestion usually take longer time than the extreme movements observed on the stock market.

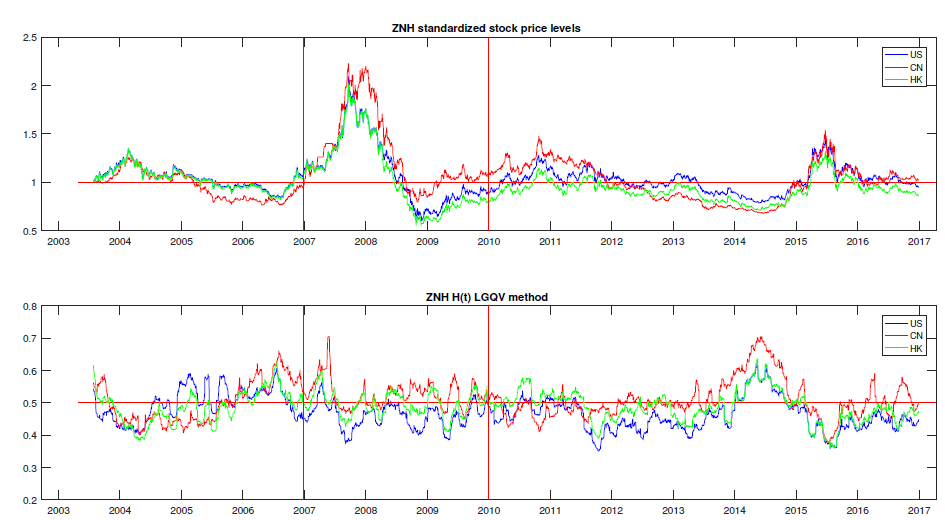

This separation of time periods allows us to analyze the change of PHE over different market performances. The first 100 trading observations are excluded to avoid the price instability in the post-IPO period. To illustrate our empirical findings, the rescaled stock price (initial price to be 1) and corresponding estimated PHE of China Southern Airlines (NYSE ticker: ZNH) are shown in Figure 7.

Observations from bottom graph in Figure 7 prove that the PHE in single stock price series is not constant and may deviate from 0.5. This deviation highly depends on market performance. During the financial crisis period, the PHE is the lowest for all three markets. The US market has the most significant drop on PHE during financial crisis, which is also the orient market of the crisis. The PHE increases when the stock price becomes directional, as in the year 2014. Though the stock prices are highly positively correlated among the global markets, the PHE might be less positively correlated or even negatively correlated, as in the year 2005. This observation provides new evidence to the segmented market hypothesis: there are different driving factors of informativeness and stock prices for the same stock at various markets.

The relationship of PHEs among three markets also changed structurally from prior to post financial crisis periods. There are 8 out of 11 individual stocks in our sample that have prior financial crisis observations, where 4 stocks have lower PHEs in the US market than that of China Mainland and HK markets. The home bias mixes the effect of more sophisticated markets and market participants. However, in post financial crisis time period, 10 of 11 stocks have lower PHE in US market than that in China Mainland markets222We utilize two-sample test in mean to conclude significant difference of averaged PHEs between the two markets. The test significance level in our study is 5%.. In addition, there are 10 stocks whose US PHEs are lower than their HK counterparts. And 8 out of 11 stocks have lower HK market PHE than that of China Mainland market. Home bias seems to lose its dominance on price informativeness or opinion formation. Market sophistication, such as total capitalization, analyst coverage and developed accounting system etc., starts to determine information content on the financial market after the financial crisis. Another plausible explanation of low US market PHEs is that, the trading time (of the same trading day) of US market is running behind that of China Mainland and HK markets. The price informativeness on the Asian markets would increase the informativeness to the US market participants.

For robustness check, we use benchmark approaches to estimate PHE on the same stock price series. More details about the PHE statistics in various markets, time periods and estimation methods are presented in Table 3. The empirical findings on PHE comparison remain the same in the classic GQV and oscillation methods as that in LGQV method. Our conclusion seems to be valid cross various PHE estimation approaches.

| Ticker | Market | Prior | Within | Post | ||||||

|---|---|---|---|---|---|---|---|---|---|---|

| GQV | LGQV | OSC | GQV | LGQV | OSC | GQV | LGQV | OSC | ||

| CN | - | - | - | 0.4898 | 0.4901 | 0.5087 | 0.4848 | 0.4594 | 0.6596 | |

| ACH | HK | - | - | - | 0.5517 | 0.5045 | 0.4689 | 0.4857 | 0.4515 | 0.6204 |

| US | - | - | - | 0.4776 | 0.4637 | 0.4823 | 0.4563 | 0.4255 | 0.6229 | |

| CN | 0.5391 | 0.4663 | 0.5126 | 0.6187 | 0.5402 | 0.3872 | 0.5862 | 0.5056 | 0.5073 | |

| CEA | HK | 0.5218 | 0.4597 | 0.4731 | 0.564 | 0.4901 | 0.3922 | 0.5453 | 0.4845 | 0.476 |

| US | 0.588 | 0.5074 | 0.4887 | 0.4823 | 0.4444 | 0.3968 | 0.5038 | 0.4543 | 0.4992 | |

| CN | 0.5041 | 0.4674 | 0.5581 | 0.4282 | 0.4363 | 0.4131 | 0.5154 | 0.4753 | 0.5158 | |

| CHU | HK | 0.5038 | 0.4416 | 0.4528 | 0.4715 | 0.4107 | 0.371 | 0.4838 | 0.4496 | 0.4361 |

| US | 0.4416 | 0.4214 | 0.4552 | 0.4487 | 0.4033 | 0.3717 | 0.4854 | 0.4508 | 0.4402 | |

| CN | 0.4284 | 0.4149 | 0.4223 | 0.4211 | 0.4101 | 0.4806 | 0.5152 | 0.4643 | 0.5833 | |

| GSH | HK | 0.5009 | 0.3961 | 0.461 | 0.4866 | 0.4298 | 0.4352 | 0.4706 | 0.4408 | 0.4941 |

| US | 0.3197 | 0.3065 | 0.3977 | 0.4292 | 0.4006 | 0.4268 | 0.441 | 0.4183 | 0.493 | |

| CN | 0.5318 | 0.5107 | 0.4682 | 0.5052 | 0.4606 | 0.417 | 0.5043 | 0.4744 | 0.5187 | |

| HNP | HK | 0.4436 | 0.4189 | 0.4697 | 0.5031 | 0.4577 | 0.4035 | 0.5192 | 0.4692 | 0.474 |

| US | 0.4656 | 0.4364 | 0.4686 | 0.4687 | 0.4338 | 0.4005 | 0.4823 | 0.4366 | 0.475 | |

| CN | - | - | - | 0.4645 | 0.4458 | 0.4758 | 0.5034 | 0.4672 | 0.5826 | |

| LFC | HK | - | - | - | 0.4488 | 0.4422 | 0.4228 | 0.5237 | 0.487 | 0.4986 |

| US | - | - | - | 0.3829 | 0.3958 | 0.4393 | 0.4858 | 0.4613 | 0.5301 | |

| CN | - | - | - | 0.4936 | 0.4923 | 0.5446 | 0.5192 | 0.473 | 0.6644 | |

| PTR | HK | - | - | - | 0.493 | 0.4564 | 0.4473 | 0.5591 | 0.5065 | 0.5278 |

| US | - | - | - | 0.4851 | 0.4507 | 0.4498 | 0.5178 | 0.4846 | 0.5271 | |

| CN | 0.544 | 0.4866 | 0.5309 | 0.5657 | 0.4833 | 0.3806 | 0.603 | 0.5019 | 0.4333 | |

| SHI | HK | 0.5533 | 0.4801 | 0.4306 | 0.4939 | 0.44 | 0.3886 | 0.4847 | 0.4209 | 0.428 |

| US | 0.5501 | 0.4881 | 0.4448 | 0.4447 | 0.4106 | 0.3908 | 0.473 | 0.4111 | 0.4517 | |

| CN | 0.523 | 0.4738 | 0.5876 | 0.4926 | 0.4687 | 0.4337 | 0.5278 | 0.4805 | 0.5837 | |

| SNP | HK | 0.5352 | 0.4451 | 0.558 | 0.5027 | 0.4324 | 0.4356 | 0.5148 | 0.4561 | 0.5135 |

| US | 0.5082 | 0.4406 | 0.569 | 0.4549 | 0.4035 | 0.4389 | 0.4882 | 0.433 | 0.5222 | |

| CN | 0.5024 | 0.4543 | 0.4527 | 0.5201 | 0.4585 | 0.3357 | 0.5547 | 0.4935 | 0.4124 | |

| YZC | HK | 0.5534 | 0.454 | 0.4872 | 0.5962 | 0.4962 | 0.3748 | 0.5729 | 0.5105 | 0.4642 |

| US | 0.5566 | 0.4739 | 0.4529 | 0.5436 | 0.4665 | 0.3525 | 0.5087 | 0.4607 | 0.4523 | |

| CN | 0.5444 | 0.4984 | 0.5812 | 0.5731 | 0.5259 | 0.4419 | 0.553 | 0.5102 | 0.5703 | |

| ZNH | HK | 0.5512 | 0.4863 | 0.5519 | 0.5422 | 0.496 | 0.4678 | 0.5413 | 0.486 | 0.5484 |

| US | 0.5564 | 0.4993 | 0.5588 | 0.4853 | 0.4584 | 0.4584 | 0.5108 | 0.4587 | 0.5296 |

7 Conclusion

In this paper, we introduce a general multifractional process of the form , driven by the mBm . We then propose a consistent estimator of PHE of this process. The estimation algorithm is based on identifying the localized quadratic variation statistic. A good convergence condition is found (see Theorem 4.2) and the selection of parameters in the algorithm is discussed.

In the simulation study we show that the proposed LGQV estimator outperforms the other two benchmark approaches in terms of lower PHE estimation RMSE and standard deviation, when the underlying process is an unknown function of time and the mBm .

In the empirical study, we show that the PHE can be interpreted as a quantitative measurement of the stock price informativeness. We use PHE estimated by LGQV to perform an empirical study regarding the impact of market quality and home bias on stock market behaviors. The comparison results indicate that in most recent years, the market quality dominates local knowledge and becomes the main driver of stock price informativeness.

Finally it is worth noting that, there exist other measurements to describe the local regularity of a process, such as the local Hölder exponent and the statistical self-affinity by the DFA methods. These exponents are generally not equivalent and no one could entirely capture the local regularity. A stochastic 2-microlocal analysis [23] is recently developed to provide a finer characterization of the local regularity. This approach particularly describes how the PHEs and the local Hölder exponents evolve subject to (pseudo-)differential operators and multiplication by power functions. Another benefit from the 2-microlocal analysis is that it can be used to derive local behaviour of sample paths from the regularity of the integrand and the integrator. Therefore a more general problem arises: estimation of the local behavior of the stochastic integrals driven by a general class of multifractional processes. We leave this problem for future research.

8 Proof of Theorem 4.2

The proof of Theorem 4.2 mainly relies on the identification of the localized generalized quadratic variation of mBm, and a bivariate Taylor expansion of the function . For identifying the localized generalized quadratic variation of mBm we have the following proposition.

Proposition 8.1

Let be the function defined by: for all ,

| (8.1) |

Then, assuming that satisfies the condition in Theorem 4.2, we have,

In order to prove Proposition 8.1, we need several preliminary results, namely, Lemmas 8.2 - 8.7 as follows.

Lemma 8.2 below is obtained based on the property that the moments of any order of a Gaussian random variable are equivalent. Its proof is quite similar to that of Lemma 6.3.5 in [36], so we omit it.

Lemma 8.2

For each , there is a constant such that for all integer , we have

| (8.2) |

The following lemma (see Lemma 6.3.6 in [36] for its proof) results from a Gaussian vector’s feature.

Lemma 8.3

Let be an arbitrary zero-mean 2-dimensional Gaussian vector such that . Then we have,

Next we state two consequences of Proposition 4.1. The result below can be derived from the proof of (4.2) in Proposition 4.1 (it suffices to take to be a constant ).

Corollary 8.4

Let be the fBm with Hurst parameter . For any integer and any , define the following generalized increment:

| (8.3) |

Then we have,

| (8.4) |

where is the function defined in (8.1).

Another straightforward consequence of Proposition 4.1 is the following statement:

Corollary 8.5

There exist two constants such that for all big enough and all , we have

| (8.5) |

Lemma 8.6 below aims to identify the localized generalized quadratic variation of the mBm in terms of its variances.

Lemma 8.6

Assume that satisfies the condition in Theorem 4.2. Then, we have

The following results in Lemma 8.7 are derived from the mBm’s continuous paths property. More precisely, that property is, the mBm ’s paths behave almost surely as an fBm’s paths with Hurst parameter when takes values in the neighborhood of .

Lemma 8.7

Now we are ready to prove Proposition 8.1.

Proof of Proposition 8.1. First we can decompose into the product of 3 terms:

| (8.9) |

Next we observe from (8.4) in Corollary 8.4 and (3.5) that,

| (8.10) |

and (3.6) entails that,

| (8.11) |

Thus, combining (8.10) with (8.11), we get

| (8.12) |

Finally, Proposition 8.1 results from (8), Lemma 8.6, (8.8) in Lemma 8.7 and (8.12):

In addition to Proposition 8.1, we also need the following Lemmas 8.8 and 8.9 to prove the main result Theorem 4.2.

Lemma 8.8

For any integer , we define

| (8.13) |

and

| (8.14) |

Then,

| (8.15) |

Proof of Lemma 8.8. By definitions (8.13) and (8.14), it is clear that

| (8.16) |

By assumption there exists a random variable with all its moments being finite such that,

| (8.17) |

where is a Gaussian random variable with its moments of any order being finite (see [37, 29]). Using the mean value theorem and the inequality (8.17), we obtain that,

| (8.18) |

where (given in (8.17)), . We now recall an important result on the path behavior of the mBm (see Theorem 1.7 in [8]); namely, there is a positive random variable of finite moments of any order, such that for all ,

| (8.19) |

As a particular case,

It follows from (8), (8.19) and the inequalities: there is a constant such that for all ,

| (8.20) |

that, for all ,

| (8.21) |

where . Finally, (8.13), (8.14), the triangle inequality, (8) and (8), imply that

where is a strictly positive random variable, due to the fact that does not vanish almost surely over and , for , is a non degenerate Gaussian random variable. Lemma 8.8 is thus proved.

Lemma 8.9

Assume that satisfies condition in Theorem 4.2. Then,

| (8.22) |

Proof of Lemma 8.9. In view of (4.3), (3.2) and (3.3), can be expressed as

| (8.23) |

For being in the neighborhood of , the second order Taylor expansion of on , the inequalities (8.17) and (8.19) yield that, for satisfying and , we have

| (8.24) |

where, by (8.19) and (8.20) we know that the remaining term (depending on ) in the above equation satisfies

| (8.25) | |||||

Taking for and in (8), and taking for short, in view of (8.23) and (3.1), we obtain that

| (8.26) |

Using Cauchy-Schwarz inequality and (8.14), we get

| (8.27) |

Putting together (8), (8), (8.25), (8.13), the fact that is an almost surely finite random variable, (3.5), (3.6), Proposition 8.1 and Lemma 8.8, we obtain that, for all ,

| (8.28) | |||||

The following remark is a straightforward consequence of Lemma 8.22, Lemma 8.8 and Proposition 8.1

Remark 8.10

Now we are ready prove Theorem 4.2.

Proof of Theorem 4.2. Let , be the continuous function defined for

all , as:

| (8.31) |

Observe that, in view of (4.4), for all , we have

| (8.32) |

On the other hand observe that (8.10) implies that,

| (8.33) |

Thus combining (8.32), (8.33), (8.10) and the fact that is continuously differentiable on , we obtain that,

This proves the first statement (1) in Theorem 4.2. Next if further satisfies the condition , then similarly starting from (8.30) we get

the statement (2) in Theorem 4.2 is proved.

9 Appendix

9.1 Proof of Proposition 4.1

9.1.1 Proof of ((1))

By using the isometry property of mBm’s harmonizable presentation, the fact that and are independent leads to that the ’s are zero-mean random variables, we then get

Since the PHE of in the neighborhood of behave locally asymptotically like those of fBms with Hurst parameters respectively, we can thus consider a Taylor expansion of around . Fix and define , since belongs to , we take the second order Taylor expansion of the bivariate function on : there exist and such that

| (9.2) |

where we denote, for , ,

and

Thus we rewrite (9.1.1) as

| (9.3) |

where

We note here ’s are notations in short for in (9.1.1). By using (9.1.1), it suffices to make an identification of all the terms ’s in order to estimate the covariance structure of the wavelet coefficients. We consider different cases according to the values of . The key to these identifications is to observe the following:

-

•

First, observe that for , , we have

where for , , with being the binomial coefficient.

-

•

Secondly, for , , , and , a order Taylor expansion of on yields:

where the integral remainder of ’s -th order Taylor expansion (see e.g. [2]) is given as:

-

–

for ,

(9.6) -

–

for ,

and the term is defined to be

(9.8) Here we note that for and ,

-

–

- Case (i)

-

.

- Case (ii)

- Case (iii)

-

Observe that can be expressed as

- Case (iv)

Now denote by

| (9.15) |

It remains to show that for ,

According to (9.15), it suffices to prove for any ,

| (9.16) |

To prove (9.16) holds we only take as an example, since the computations for the other items are similar. Recall that

Remember that, the fact that yields . This implies

The equation ((1)) is proved.

9.1.2 Proof of (4.2)

9.2 Proof of Lemma 8.6

First by using the fact that

and by using Lemma 8.3 (in which we take , and ), we get

| (9.21) |

Then it follows from (9.2) and Proposition 4.1 that there is a constant such that for all ,

| (9.22) |

On the other hand, since , there is a constant such that for any ,

| (9.23) |

Thus, it follows from (3.4) that for all and ,

| (9.24) |

where is finite thanks to the condition (see Theorem 4.2). Also (9.23) and (3.4) imply that

| (9.25) |

where is strictly positive thanks to the condition in Theorem 4.2. It follows from (9.22), (9.24), (3.5), (3.6) that for all ,

| (9.26) |

where the constants , and do not depend on . Thus using Markov’s inequality, (8.2) and (9.2), we obtain that, for any ,

| (9.27) |

On the other hand, there is a constant such that we have for all and all ,

| (9.28) |

Thus, combining (9.28) with (9.25), it follows that there exists a constant such that for all big enough at ,

| (9.29) |

Relations (9.2) and (9.29) imply that, for all big enough,

| (9.30) |

This is equivalent to

Lemma 8.6 has been proved.

9.3 Proof of Corollary 8.4

9.4 Proof of Lemma 8.7

9.4.1 Proof of (8.6)

Let denote the norm of the zero-mean element in the space generated by the mBm . Using the triangle inequality, we obtain

| (9.34) |

where the generalized increments of the fBm , , is defined by

| (9.35) |

First, let us bound . For each , using the harmonizable representations of (see (1.1)) and (see (9.32)), we write

where is the function defined for each and , as,

| (9.37) |

It follows from (9.4.1) and the isometry property of the integral that,

Observe that

| (9.39) |

and

| (9.40) |

Then (9.37), (9.39), (9.40) and the fact that

| (9.41) |

yield that there exists a constant such that for all , and ,

| (9.42) |

where and . Moreover, using for each fixed , a Taylor expansion of order of at , we have, for all ,

| (9.43) |

Combining (9.4.1) with (9.43) we get that

| (9.44) |

where

| (9.45) |

and

| (9.46) |

Let us now give a suitable bound for . Relations (9.45), (3.1) and (9.39) entail that

| (9.47) |

where is the trigonometric polynomial defined for by,

| (9.48) |

and is its derivative. Observe that all the integrals in (9.4.1) are finite since

| (9.49) |

relation (9.49) is in fact a consequence of (3.1). Setting in (9.4.1) and using (9.37), (9.39), (9.41), (9.42) and (9.24), it follows that, for all ,

| (9.50) | |||||

where is a constant non depending on and . Let us now give a suitable bound for . Relation (9.46), the triangle inequality, the inequality for all real numbers and Relation (9.42) imply that,

| (9.51) | |||||

moreover, we have

| (9.52) |

because

is a continuous function on the compact interval . Next, combining (9.51) with (9.52), we obtain that for all big enough and ,

| (9.53) |

where is a constant non depending on and . Next, it follows from (9.44), (9.50) and (9.53) that, for all there is a constant not depending on such that for all ,

| (9.54) |

Now we can use the same process to bound as we did for bounding . It suffices to point out that the term in (in (9.45)) and (in (9.46)) are replaced with in this case. Hence It turns out that there is a constant not depending on such that for ,

| (9.55) |

Next, putting together (9.4.1), (9.54), (9.55) and the inequality , we get (8.6).

9.4.2 Proof of (8.7)

9.4.3 Proof of (8.8)

9.5 Figures for simulation study

In this subsection, we provide more evidences on convergence behavior of the PHE estimation comparison for functional forms, using additional functional forms that are not limited to what we have shown in Figure 4, Figure 4 and Figure 5. The specific functional forms that we present in this section contain:

-

•

;

-

•

;

-

•

;

-

•

;

Figure 8 illustrates the RMSE comparison between PHE estimation using LGQV and using benchmark methods (GQV method and Oscillation method) these four additional functional forms, in supplement to the comparisons in Section 5.

For the case when , the observed mBm returns to itself (no additional functional transformation). We find that classic GQV estimation outperforms the LGQV method for most of the time. However, for the functional of mBm series (from second case to the fourth case above), LGQV outperforms both benchmark methods in terms of its lower RMSE.

References

- [1] Werner Antweiler and Murray Z Frank. Is all that talk just noise? the information content of internet stock message boards. Journal of Finance, 59(3):1259–1294, 2004.

- [2] Tom M Apostol. Calculus. Jon Wiley & Sons, 1967.

- [3] Antoine Ayache and Jacques Lévy-Véhel. On the identification of the pointwise Hölder exponent of the generalized multifractional Brownian motion. Stochastic Processes and their Applications, 111(1):119–156, 2004.

- [4] J M Bardet, G Lang, E Moulines, and P Soulier. Wavelet estimator of long-range dependent processes. Statistical Inference for Stochastic Processes, 3(1–2):85–99, 2000.

- [5] Jean-Marc Bardet and Donatas Surgailis. Nonparametric estimation of the local Hurst function of multifractional Gaussian processes. Stochastic Processes and their Applications, 123(3):1004–1045, 2013.

- [6] Olivier Barrière. Synthèse et estimation de mouvements Browniens multifractionnaires et autres processus à régularité prescrite: définition du processus auto-régulé multifractionnaire et applications. PhD thesis, Ecole Centrale de Nantes, 2007.

- [7] Olivier Barrière, Antoine Echelard, and Jacques Lévy-Véhel. Self-regulating processes. Electronic Journal of Probability, 17(103):1–30, 2012.

- [8] Albert Benassi, Daniel Roux, and Stéphane Jaffard. Elliptic Gaussian random processes. Revista Matemática Iberoamericana, 13(1):19–90, 1997.

- [9] Pierre R Bertrand, Abdelkader Hamdouni, and Samia Khadhraoui. Modelling nasdaq series by sparse multifractional Brownian motion. Methodology and Computing in Applied Probability, 14(1):107–124, 2012.

- [10] Pierre Raphaël Bertrand, Mehdi Fhima, and Arnaud Guillin. Local estimation of the Hurst index of multifractional Brownian motion by increment ratio statistic method. ESAIM: Probability and Statistics, 17:307–327, 2013.

- [11] Sergio Bianchi and Massimiliano Frezza. Fractal stock markets: international evidence of dynamical (in) efficiency. Chaos: An Interdisciplinary Journal of Nonlinear Science, 27(7):071102, 2017.

- [12] Sergio Bianchi, Alexandre Pantanella, and Augusto Pianese. Modeling and simulation of currency exchange rates using multifractional process with random exponent. International Journal of Modeling and Optimization, 2(3):309, 2012.

- [13] Sergio Bianchi, Alexandre Pantanella, and Augusto Pianese. Modeling stock prices by multifractional Brownian motion: an improved estimation of the pointwise regularity. Quantitative Finance, 13(8):1317–1330, 2013.

- [14] Sergio Bianchi and Augusto Pianese. Multifractional properties of stock indices decomposed by filtering their pointwise Hölder regularity. International Journal of Theoretical and Applied Finance, 11(06):567–595, 2008.

- [15] John L Campbell, Hsinchun Chen, Dan S Dhaliwal, Hsin-min Lu, and Logan B Steele. The information content of mandatory risk factor disclosures in corporate filings. Review of Accounting Studies, 19(1):396–455, 2014.

- [16] Grace Chan, Peter Hall, and DS Poskitt. Periodogram-based estimators of fractal properties. Annals of Statistics, pages 1684–1711, 1995.

- [17] Jean-François Coeurjolly. Identification of multifractional Brownian motion. Bernoulli, 11(6):987–1008, 2005.

- [18] Jean-François Coeurjolly. Erratum: Identification of multifractional Brownian motion. Bernoulli, 12(2):381–381, 2006.

- [19] Sylvain Corlay, Joachim Lebovits, and Jacques Lévy-Véhel. Multifractional stochastic volatility models. Mathematical Finance, 24(2):364–402, 2014.

- [20] Joshua D Coval and Tobias J Moskowitz. Home bias at home: Local equity preference in domestic portfolios. Journal of Finance, 54(6):2045–2073, 1999.

- [21] Theodore E Day and Craig M Lewis. Stock market volatility and the information content of stock index options. Journal of Econometrics, 52(1-2):267–287, 1992.

- [22] Joel Hasbrouck. Measuring the information content of stock trades. Journal of Finance, 46(1):179–207, 1991.

- [23] E Herbin and Jacques Lévy-Véhel. Stochastic 2-microlocal analysis. Stochastic Processes and their Applications, 119(7):2277–2311, 2009.

- [24] Allen H Huang, Amy Y Zang, and Rong Zheng. Evidence on the information content of text in analyst reports. Accounting Review, 89(6):2151–2180, 2014.

- [25] Zoran Ivković and Scott Weisbenner. Local does as local is: Information content of the geography of individual investors’ common stock investments. Journal of Finance, 60(1):267–306, 2005.

- [26] Sixian Jin, Qidi Peng, and Henry Schellhorn. Estimation of the pointwise Hölder exponent of hidden multifractional Brownian motion using wavelet coefficients. Statistical Inference for Stochastic Processes, 21(1):113–140, 2018.

- [27] G Andrew Karolyi. The world of cross-listings and cross-listings of the world: challenging conventional wisdom. Review of Finance, 10(1):99–152, 2006.

- [28] C J Keylock. Gradual multifractal reconstruction of time-series: Formulation of the method and an application to the coupling between stock market indices and their hölder exponents. Physica D: Nonlinear Phenomena, 368(1):1–9, 2018.

- [29] Michel Ledoux and Michel Talagrand. Probability in Banach Spaces: isoperimetry and processes. Springer Science & Business Media, 2013.

- [30] B Mandelbrot and J W van Ness. Fractional Brownian motions, fractional noises and applications. SIAM Review, 10(4):422–437, 1968.

- [31] Randall Morck, Bernard Yeung, and Wayne Yu. The information content of stock markets: why do emerging markets have synchronous stock price movements? Journal of Financial Economics, 58(1):215–260, 2000.

- [32] J F Muzy, E Bacry, and A Arneodo. Wavelets and multifractal formalism for singular signals: Application to turbulence data. Physical Review Letters, 67:3515–3518, 1991.

- [33] Romain François Peltier and Jacques Lévy-Véhel. Multifractional Brownian motion: definition and preliminary results. Rapport de Recherche de l’INRIA, INRIA, 2645:239–265, 1995.

- [34] C K Peng, S V Buldyrev, S Havtin, M Simons, H E Stanley, and A L Goldbergerz. Mosaic organization of dna nucleotides. Physical Review E, 49(2):1685–1689, 1994.

- [35] C K Peng, S Havtin, H E Stanley, and A L Goldbergerz. Quantification of scaling exponents and crossover phenomena in nonstationary heartbeat time series. Chaos, 5(1):82–87, 1995.

- [36] Q Peng. Statistical inference for hidden multifractional processes in a setting of stochastic volatility models. PhD thesis, University Lille 1, 2011.

- [37] Mathieu Rosenbaum. Estimation of the volatility persistence in a discretely observed diffusion model. Stochastic Processes and their Applications, 118(8):1434–1462, 2008.

- [38] Stilian A Stoev and Murad S Taqqu. How rich is the class of multifractional Brownian motions? Stochastic Processes and their Applications, 116(2):200–221, 2006.

- [39] Claude Tricot. Curves and fractal dimension. Springer Science & Business Media, 1994.

- [40] Leonardo Trujillo, Pierrick Legrand, Gustavo Olague, and Jacques Lévy-Véhel. Evolving estimators of the pointwise Hölder exponent with genetic programming. Information Sciences, 209:61–79, 2012.

- [41] Stijn Van Nieuwerburgh and Laura Veldkamp. Information immobility and the home bias puzzle. Journal of Finance, 64(3):1187–1215, 2009.

- [42] H Wendt, S G Roux, S Jaffard, and P Abry. Wavelet leaders and bootstrap for multifractal analysis of images. Journal of Signal Processing, 89(6):1100–1114, 2009.

- [43] Andrew T A Wood and Grace Chan. Simulation of stationary Gaussian processes in . Journal of Computational and Graphical Statistics, 3(4):409–432, 1994.