Multi-scale analysis of lead-lag relationships in high-frequency financial markets

Abstract

We propose a novel estimation procedure for scale-by-scale lead-lag relationships of financial assets observed at high-frequency in a non-synchronous manner. The proposed estimation procedure does not require any interpolation processing of original datasets and is applicable to those with highest time resolution available. Consistency of the proposed estimators is shown under the continuous-time framework that has been developed in our previous work [21]. An empirical application to a quote dataset of the NASDAQ-100 assets identifies two types of lead-lag relationships at different time scales.

Keywords: Brownian motion; Cross-covariance estimation; Daubechies’ wavelet filter; Non-synchronous data; Stochastic volatility; Wavelet.

1 Introduction

A financial market accommodates a diversified groups of participants. They have different sources of money, different time horizons and different risk attitudes, with different quality and quantity of information. In Müller et al. [32] it is argued that such differences are engraved in price formation at each of distinct time scales. They can cause a multi-scale structure embedded in the financial market.

This paper intends to study such a multi-scale structure of financial markets that can exist in a very short time period. In particular, we are to investigate lead-lag relationships between financial assets by the use of high-frequency data. Identification of lead-lag relationships among assets is fundamentally important both for theoretical and practical perspectives; the existence of such relationships may mean the inefficiency of financial markets for theorists but it may also provide opportunities for market participants to earn “excess” profits. So that so, it is quite natural that lead-lag analysis has been conducted in the finance literature for a long time. Since 90’s as high-frequency data has become more and more accessible, lead-lag relationships with high-frequency data have been studied by such authors as [6, 10, 36, 28]. In the meantime, multi-scale analysis with high-frequency financial data has been carried out; e.g., [31, 19, 4, 37, 14]. However, main interest of most of these articles is the estimation of volatilities of assets. There is little work that conducts multi-scale analysis of lead-lag relationships in the high-frequency domain; one exception is Hafner [16] which has examined multi-scale structures of the lead-lag relationships between the returns, durations and volumes of high-frequency transaction data of the IBM stock.

To our understanding, the main focus of those studies conducting multi-scale analysis is empirical application per se, not to develop a new estimation methodology. Their adopted approaches are theoretically based on “classical” discrete time series that appear to be more suitable for daily or lower frequency data with longer time horizons. On one hand, analysis of high-frequency financial data shall focus on a short time horizon, that is, one day or shorter. So, it is unclear whether one can reasonably apply such a “classical” method to high-frequency financial data without reservation. On the other hand, continuous-time modeling provides a convenient and powerful framework to analyze high-frequency data observed in a short horizon (cf. Aït-Sahalia and Jacod [1]).

With these in mind, in [21] the authors have developed a continuous-time framework that is designed specifically for multi-scale analysis of lead-lag relationships in high-frequency data. There, they introduce two Brownian motions and with a scale-by-scale correlation structure. More precisely, they have shown that, for any and (), there exists a bivariate Gaussian process () with stationary increments such that

-

(I)

both and are two-sided Brownian motions,

-

(II)

the cross-spectral density of is given by

(1) where for every .

The frequency band corresponds to the time scale between and in the time domain. Also, note that, if () is a two-sided bivariate Brownian motion with correlation , for the process () has the cross-spectral density (). Therefore, we can consider that and have a lead-lag relationship with the time-lag in the time scale between and . Hence, under this model we can understand the multi-scale structure of the lead-lag relationships by estimating the parameters from observation data.

The main contribution of this paper is to develop a novel estimation procedure for the parameters based on non-synchronous observations of (volatility-modulated versions of) and . In the above mentioned [21] the authors proposed another estimation procedure, which required data interpolation in accordance with a regular grid with size equated to the finest time resolution at which the fastest market participants (will) act. When analyzing a dataset with sub mili-second time precision, one typically wishes to let this finest resolution coarser than the actual time precision (see Section 6 for instance). If so, such an intermediary data interpolation step can inevitably discard a large amount of data. Even in such a situation the newly proposed procedure in this paper is free from any interpolation processing of the original data and able to efficiently use them. Besides, a theoretical consideration along with numerical experiments suggests that the new estimators can potentially have better performance than the interpolation-based estimator when the sampling times are non-synchronous to a reasonable degree. An empirical application with a NASDAQ-100 dataset identifies two types of lead-lag relationships at different time scales. At the best of our knowledge, this observation is new in the empirical literature, indicating potential usefulness of the new estimation methodology.

The rest of the paper is organized as follows. In Section 2 we present the theoretical setting considered in this paper in details. Our new estimation procedure is described in Section 3. We develop an asymptotic theory associated with the proposed estimators in Section 4. In Section 5 we assess finite sample performance of the proposed estimators by Monte Carlo experiments, and in Section 6 we apply our procedure to empirical datasets. Section 7 concludes the paper. All the proofs are collected in Section 8.

2 Setting

We let the finest time resolution correspond to for some . We suppose is comparable to the observation frequency of data. We will develop an asymptotic theory in the high-frequency setting, i.e., when tends to infinity, or the time resolution shrinks to zero, while the length of the whole observation interval stays fixed.

As mentioned in the Introduction, our theoretical framework is based on a bivariate Gaussian process () with stationary increments satisfying properties (I)–(II). Since we are mainly interested in the lead-lag relationships at scales close to the finest time resolution, it is convenient to “relabel” indices of the parameters and in (1) so that the finest resolution corresponds to the level while we consider the asymptotic theory such that tends to infinity. For this reason, as in [21] we replace property (II) with the following one: The cross-spectral density of is given by

| (2) |

We also assume that for every with some .

Now, for each , we consider the log price process of the -th asset given by

| (3) |

where is a càdlàg process adapted to the filtration such that the process is, respectively, a one-dimensional -Brownian motion. We observe the process on the interval at the sampling times . The sampling times and are random variables which are independent of and implicitly depend on such that

as , where we set and for each .

Remark 1.

Our model is generally not a semimartingale, so it is generally not free of arbitrage in the absence of market frictions due to the well-known fundamental theorem of asset pricing (see e.g. [11]). However, if we take account of market frictions such as discrete trading or transaction costs, we can show that our model has no arbitrage; see [22] for details.

3 Construction of the estimators

Our aim is to estimate the parameters for each based on discrete observation data and . We begin by introducing some notation. For each , we associate the observation times with the collection of intervals . We will systematically employ the notation (resp. ) for an element of (resp. ).

For an interval , we set , , . In addition, we set for a a stochastic process , and for a real number .

Now we explain how to construct our estimators. To explain the idea behind the construction, we focus on the case of for . The parameter is the unique maximizer of the scale-by-scale cross-covariance function between and , which is defined by

where for and denotes the Littlewood-Paley wavelet:

(see Sections 2.2–2.3 of [21] for details). Motivated by this fact, we first construct a sensible covariance estimator for , and then construct the lead-lag estimator for as a maximizer of as in [26]. The idea behind the construction of the estimator is as follows. Let be the inverse Fourier transform of . Then we have

by the convolution theorem. This suggests us to consider the following estimator for :

where is an estimator for and is an approximation of (it turns out that the factor corresponding to is unnecessary because does not tend to 0 in our asymptotic setting), both of which are explicitly defined in the following. Since may be regarded as the “cross-covariance function between and ”, we adopt the following estimator introduced in Hoffmann et al. [26] as :

where we set for two intervals and . This can be regarded as the empirical cross-covariance estimator between the returns of and at the lag computed by Hayashi and Yoshida [23]’s method to handle the non-synchronous sampling times. In the meantime, the Fourier inversion formula yields

so the transfer function of is . In particular, well approximates if the transfer function of well approximates . We construct such a sequence from Daubechies’ wavelet filter as follows. We refer to Section 4.8 of [35] for details about Daubechies’ wavelets (see also Appendix A). Let be Daubechies’ wavelet filter of (even) length whose power transfer function is given by

The associated scaling filter111We use the notation that denotes the wavelet filter and denotes the scaling filter following [35]. Note that the reverse notation is often used in the literature. is defined via the quadrature mirror relationship as , , hence its power transfer function satisfies . Then, for every we construct the associated level wavelet filter recursively by for and for , where and for . Now we define the sequence by

These quantities are identical to the autocorrelation wavelets from Nason et al. [33] (see Definition 3 from [33]). The transfer function of is given by

(see Eq.(28) from [33]). In particular, well approximates as (see (A.3)) and thus may be used an approximation of . Finally, for every we define the estimator for as a solution of the following equation:

Here, we maximize the function regarding over the finite grid

with some positive integer as in [26].

Remark 2.

Given the length of Daubechies’ wavelet filter, we still have several options of such as the external phase wavelet and the least asymmetric wavelet (cf. Section 4.8 of [35]). However, all of them have the same power transfer function by definition, so only depends on the length of Daubechies’ wavelet filters.

4 Asymptotic theory

For a function , we denote by the Fourier transform of :

We impose the following conditions to derive our asymptotic results.

Assumption 1.

There is a constant such that almost surely has -Hölder continuous sample paths for every .

Assumption 2.

(i) as for any .

(ii) There are constants , , and an absolutely continuous real-valued function on such that

as for any sequence of real numbers satisfying for every , where ,

and . Moreover, for almost all and .

The simplest situation where Assumption 2 is satisfied is the equidistant and synchronous sampling case such that for every with some . In this case one can easily see that

for any . Hence, Assumption 2 is satisfied with being the quantity in the right side of the above equation. Another example is Lo and MacKinlay [30]’s sampling scheme as described by the following proposition:

Proposition 1.

Let . Suppose that, for each , the observation times are randomly chosen from using Bernoulli trials with success probability (). Then, Assumption 2 is satisfied with

| (4) |

Now we state asymptotic results. The first result concerns the asymptotic behavior of the estimators and can be considered as a counterpart of Propositions 3–4 in [26]:

Theorem 1.

The next theorem concerns consistency of the estimators and can be considered as a counterpart of Theorem 1 in [26]:

Theorem 2.

Theorem 2 shows that the proposed estimators enjoy a similar asymptotic property to that of the lead-lag estimator by [26]. Remarkably, our estimators achieve the same convergence rate as Hoffmann et al. [26]’s one, so we have no cost to separate multiple lead-lag relationships in our setting.

Remark 3.

The convergence rate given in our result is better than the one in [21, Theorem 2], where the latter presents convergence rates of different estimators for . This improvement is not due to our new construction of estimators but due to gain from a special property of Daubechies’ wavelets (presented in Corollary A.1), which is ignored in [21].

Remark 4.

Our estimators are expected to perform better than [21]’s one for non-synchronous data. To see this, let us consider the Lo-MacKinlay sampling scheme considered in Proposition 1 with . Then, converges in probability to as , where is give by (4). Meanwhile, the counterpart of in [21] converges in probability to as , where

See Theorem 1 in [21] (note that is essentially constructed from observations on ). A straightforward computation shows

which is always non-negative and strictly positive when and . Therefore, we may expect that our cross-covariance estimators could identify peaks of true correlograms better when observations are non-synchronous. In the next section we give numerical evidence to support this argument.

5 Simulation study

In this section we assess the finite sample accuracy of the proposed estimators by a Monte Carlo study. We set , with .

We simulate model (3) with the following two scenarios of the volatility processes:

- Scenario 1

-

Constant volatilities. for .

- Scenario 2

-

Stochastic volatilities with a leverage effect. The Heston model is adopted to generate the volatility process for each : The process is the solution of the following stochastic differential equation:

where is a standard Wiener process and the initial value is randomly drawn from the stationary distribution of the process in each iteration, i.e. . We assume that the processes , and are mutually independent. The parameters , , and are chosen as in [7]: , , and .

The parameters for the spectral density (2) are chosen as in Table 1. Simulation of the paths of the process is performed in the same way as in [21]. Namely, we simulate the bivariate stationary Gaussian sequence () by the multivariate circulant embedding method of [5] with the following approximation222Note that there are typos in the first and second displayed equations in page 1221 of [21]: The -th summands on their right hand sides should have been multiplied by .:

This simulation scheme has been implemented in the R package yuima as the function simBmllag since version 1.10.2. The R package yuima also contains the function wllag to implement our scale-by-scale lead-lag time estimators .

| 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 | 9–15 | |

| \hdashline | 0.3 | 0.5 | 0.7 | 0.5 | 0.5 | 0.5 | 0.5 | 0.5 | 0 |

| 0 |

We use the Lo-MacKinlay sampling scheme with presented in Section 4 to generate the sampling times and . We fix as and vary as . Recall that is the probability of occurrence of observation missing for the -th asset . The larger value takes the less frequently is observed, making the degree of non-synchronicity higher. We use as the length of Daubechies’ wavelet filter and set For comparison we also compute the estimators for proposed in [21], each of which is defined as a maximizer of the corresponding so-called wavelet cross-covariance estimator based on data synchronized by interpolation (we refer to it as “WCCF”). Here, the computation of the wavelet cross-covariance estimators requires the specification of Daubechies’ wavelet and we use the least asymmetric wavelet with length 20. We run 1,000 Monte Carlo iterations with each of three experimental conditions in each scenario. Table 2 reports the sample median and the median absolute deviation (MAD) of the estimates for each experiment in Scenario 1. We see from Table 2 that both estimators accurately estimate the true values in the case of at the levels . It is theoretically natural that the accuracy of the estimators declines as increases because the contrast function , gets flatter as increases. In the cases of and , the WCCF estimators are apparently biased at the levels , while the estimators still keep the good precision. Hence our new estimators can handle high-frequency data with rather a high degree of non-synchronicity, which is theoretically expected from the argument in Remark 3. Table 3 shows simulation results in Scenario 2. As the table reveals, the presence of a time variation and a leverage effect in the volatilities does not affect the performance of the proposed estimators, which is aligned with the obtained asymptotic theory.

| True | ||||||||

|---|---|---|---|---|---|---|---|---|

| WCCF | ||||||||

| WCCF | ||||||||

| WCCF | ||||||||

This table reports the median and the median absolute deviation (in parentheses) of the estimates in Scenario 1 (divided by ).

| True | ||||||||

|---|---|---|---|---|---|---|---|---|

| WCCF | ||||||||

| WCCF | ||||||||

| WCCF | ||||||||

This table reports the median and the median absolute deviation (in parentheses) of the estimates in Scenario 2 (divided by ).

6 Empirical application

In this section we apply the proposed method to actual high-frequency data in the U.S. stock market. We investigate the lead-lag relationships between quote updates of a single asset traded concurrently at multiple exchanges.333This is closely related to the issue of identifying the particular exchange at which price discovery of the assets actually takes place. Such an issue is one of the fundamental problems in financial econometrics and has been widely studied in the literature; see e.g. [18, 38, 17, 34, 20]. The exchanges chosen for the current analysis are the NASDAQ and BATS. We focus on the component stocks of NASDAQ-100 in 2015, containing totally 108 assets. The source is the Daily TAQ database, whose time precision is one micro-second. The sample period is the whole month of August 2015, consisting of 21 trading days. We use quote data recorded between 9:45 and 15:45. Namely, we discard the first and last 15 minutes from the market opening time to avoid abnormal behavior frequently observed at the start and end of trading sessions. To construct log-price processes from quote data, we compute logarithms of micro-prices (cf. Eq.(2.2) in [13]).

As argued in [3, 20], the Daily TAQ database provides two kinds of timestamps for each record. The one denotes the time when a quote update is recorded by an exchange matching-engine, while the other denotes the time when it is processed by a securities information processor (SIP). Henceforth we refer to the former as the participant timestamp and to the latter as the SIP timestamp, following [3]. In the present analysis we focus mainly on the SIP timestamp because it is assigned by the single SIP managed by the NASDAQ (“NASDAQ SIP”) and thus cause no clock synchronization issue. Nevertheless, we will later consider a geographical effect on lead-lag times. For this purpose we will need to take account of reporting latencies between the NASDAQ SIP and each exchange, requiring us to handle the participant timestamp. Since each exchange is obligated to synchronize their clocks to UTC to within , we set our finest time resolution as .444It will also be reasonable to suppose that market participants react at time scales in or slower because it takes at least around to transmit information among the exchanges considered here; see Table 2 in [39]. Then we take

as the search grid. We use as the length of Daubechies’ wavelet filter.

For comparison we also compute the following two estimators for lead-lag times.

-

•

Hoffmann-Rosenbaum-Yoshida (HRY) estimator [26]: This estimator is defined as a maximizer of over the grid :

-

•

Dobrev-Schaumburg (DS) estimator [12]: This estimator is constructed as follows. For each and each , we set if and otherwise. Then we define

for each . Now, the DS estimator is defined as a maximizer of over the grid :

6.1 Results

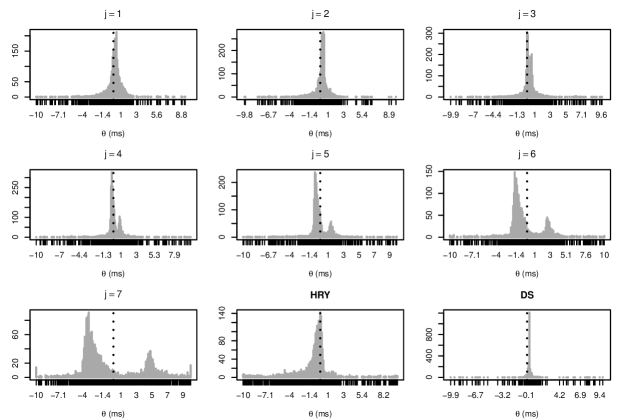

Figure 1 shows the histograms of the lead-lag time estimates of , () and for the 108 assets, evaluated every trading day. Here, the horizontal axis is expressed in mili-seconds and the positive values imply that the NASDAQ leads the BATS and vice versa. We see that the estimates of at the levels have sharp peaks at small positive values, while those at the levels have two peaks located at positive and negative values, respectively. The estimates of have a peak around 0 but are negatively skewed. The estimates of have a very sharp peak at a small positive value, suggesting the presence of consistent leadership of the NASDAQ against the BATS in trading activity.

These observations suggest that the estimates of at the finer levels (corresponding to the time scales between 0.1ms and 0.8ms) might be related to those of , while the negative estimates of at the coarser levels (corresponding to the time scales between 0.8ms and 12.8ms) might have some links with those of . To confirm the first claim, we compute summary statistics for the estimates of for and in the left panel of Table 4. As the table reveals, the estimates of are concentrated at and the other estimates are mostly distributed around this lead-lag time. Now, following [12], we argue that the value comes from a geographical reason. First, we note that our analysis is based on timestamps placed by the NASDAQ SIP and they contain reporting latencies when quote updates are transmitted from each exchange: See [3, 20] for more details. In particular, Table A.1 in [3] suggests that SIP quote updates for the BATS would primitively lag those for the NASDAQ with lead-lag times around 0.2ms due to the difference between their reporting latencies. To check this, we re-evaluate for and using the participant timestamp instead of the SIP timestamp. The results are reported in the right panel of Table 4. The table shows that the estimates of are concentrated at , supporting the above discussion. We speculate that the value is originated from the transit time between the matching engines of the NASDAQ and BATS exchanges: The former’s are located in Carteret, NJ, while the latter’s are located at the Equinix data center in Secaucus, NJ. The fastest transit time between Carteret and Secaucus is estimated as around 0.1ms; see Table 2 in [39].

Now we turn to the second claim. Panel A of Table 5 shows summary statistics for the negative and positive estimates of for as well as the whole estimates of . Here, the row “Spearman” in the table indicates Spearman’s rank correlation coefficients with the estimates of . These values of Spearman’s rank correlation coefficients suggest that the negative estimates of for would have some relationships with those of . This becomes more pronounced if we focus on estimates based on larger sample sizes: Panel B of Table 5 shows the above summary statistics computed for the estimates based on samples with more than 50,000 quote updates.

In summary, we infer from the above analysis the following lead-lag relationships between the NASDAQ and BATS exchanges for the NASDAQ-100 assets: On one hand, the lead-lag time estimates of capture cross-market trading activity by the fastest traders and their values come from the geographical distance between the data centers of the two exchanges. At this finest time scales, the NASDAQ exchange typically leads the BATS exchange. On the other hand, the lead-lag time estimates of basically capture trading activity by relatively slower traders acting at time scales in mili-seconds. At this relatively coarser time scales, the BATS primally leads the NASDAQ, although there are non-negligible cases that the BATS lags the NASDAQ. Our new estimators successfully separate these two types of lead-lag relationships at different time scales up to some extent. At the best of our knowledge, this empirical observation is new in the literature, which has been drawn for the first time by our proposed estimation methodology for multiple lead-lag times.

This figure shows the histograms of the daily lead-lag time estimates (), and of quote updates between the NASDAQ and BATS exchanges, computed for all the component stocks of the NASDAQ-100 in August, 2015. The price processes are constructed by computing the micro prices. The horizontal axis is expressed in mili-seconds. The dash line denotes 0ms. A positive lead-lag time estimate implies that the NASDAQ leads the BATS and vice versa.

| SIP timestamp | Participant timestamp | |||||||

|---|---|---|---|---|---|---|---|---|

| DS | DS | |||||||

| 1st Quartile | -0.20 | 0.00 | 0.00 | 0.20 | -0.10 | -0.20 | -0.20 | -0.10 |

| Median | 0.20 | 0.30 | 0.20 | 0.30 | 0.10 | 0.10 | 0.00 | 0.10 |

| 3rd Quartile | 0.60 | 0.50 | 0.60 | 0.30 | 0.20 | 0.30 | 0.40 | 0.10 |

| Mode | 0.40 | 0.40 | 0.00 | 0.30 | 0.10 | 0.30 | -0.10 | 0.10 |

This table reports the quartiles and modes of the daily lead-lag time estimates () and (DS) of quote updates between the NASDAQ and BATS exchanges, computed for all the component stocks of the NASDAQ-100 in August, 2015. The values are expressed in mili-seconds. A positive lead-lag time estimate implies that the NASDAQ leads the BATS and vice versa. The left panel is for the estimates based on the SIP timestamp. The right panel is for the estimates based on the participant timestamp.

| Panel A: All the estimates | |||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|

| Negative values | Positive values | ||||||||||

| HRY | |||||||||||

| 1st Quartile | -0.40 | -0.70 | -1.60 | -3.50 | 0.30 | 0.60 | 1.80 | 4.10 | -1.30 | ||

| Median | -0.30 | -0.60 | -1.30 | -3.00 | 0.80 | 1.30 | 2.60 | 4.70 | -0.40 | ||

| 3rd Quartile | -0.20 | -0.40 | -0.90 | -2.20 | 1.00 | 1.70 | 3.20 | 5.60 | 0.10 | ||

| Mode | -0.20 | -0.70 | -1.60 | -3.20 | 0.10 | 1.40 | 2.60 | 4.80 | 0.00 | ||

| Spearman | 0.22 | 0.45 | 0.52 | 0.51 | -0.13 | -0.10 | -0.09 | -0.00 | 1.00 | ||

| # of samples | 1188 | 1543 | 1634 | 1560 | 897 | 634 | 618 | 700 | 2268 | ||

| Panel B: Estimates based on more than 50,000 quote updates in the NASDAQ | |||||||||||

| Negative values | Positive values | ||||||||||

| HRY | |||||||||||

| 1st Quartile | -0.30 | -0.70 | -1.60 | -3.40 | 0.10 | 0.20 | 2.40 | 4.40 | -1.00 | ||

| Median | -0.20 | -0.50 | -1.30 | -2.90 | 0.40 | 1.30 | 2.70 | 4.80 | -0.40 | ||

| 3rd Quartile | -0.10 | -0.30 | -0.80 | -2.10 | 0.90 | 1.60 | 3.10 | 5.73 | 0.00 | ||

| Mode | -0.20 | -0.60 | -1.40 | -3.20 | 0.10 | 0.10 | 2.50 | 4.80 | 0.00 | ||

| Spearman | 0.44 | 0.69 | 0.73 | 0.75 | -0.35 | -0.36 | -0.04 | 0.05 | 1.00 | ||

| # of samples | 667 | 913 | 990 | 977 | 415 | 251 | 220 | 244 | 1223 | ||

This table reports several summary statistics of the negative and positive estimates of () as well as the whole estimates of (HRY) for quote updates between the NASDAQ and BATS exchanges, computed for all the component stocks of the NASDAQ-100 in August, 2015. A positive lead-lag time estimate implies that the NASDAQ leads BATS and vice versa. The values for the quartiles and mode are expressed in mili-seconds. The row “Spearman” reports Spearman’s rank correlation coefficients with the estimates of . The row “# of estimates” reports the number of lead-lag time estimates for which the summary statistics are evaluated. The values in Panel A are evaluated with all the estimates. The values in Panel B are based on the estimates for samples with more than 50,000 quote updates in the NASDAQ exchange.

7 Conclusion

In this paper we have proposed a new estimation method for multi-scale analysis of lead-lag relationships between two assets based on their high-frequency observation data when they are non-synchronously observed. The key idea was our novel construction of estimators for scale-by-scale cross-covariance functions, where we apply a wavelet transform to the empirical cross-covariance function rather than the raw observation data. We have also developed an associated asymptotic theory to obtain consistency of the proposed estimators in the modeling framework proposed in our previous work [21]. Compared with the estimation method proposed in [21], which essentially adopts the same method as the traditional one in the wavelet literature, the newly proposed method is more appropriate in applications to irregularly-spaced high-frequency financial data as it can handle the whole data more effectively. The simulation study has indeed shown that the proposed estimators can perform far better for non-synchronously observed data than the previous one, as intended. The empirical results have demonstrated that the new method can provide a deep insight into lead-lag relationships in the financial markets in the high-frequency domain. In particular, we identify two types of lead-lag relationships at finer and (relatively) coarser time scales, respectively.

8 Proofs

8.1 Proof of Proposition 1

We begin by proving some lemmas. Let us set for and . We denote by (resp. ) the conditional probability (resp. conditional expectation) given .

Lemma 1.

Let and set . Suppose that for all . Then, under the assumptions of Proposition 1, there is a constant depending only on such that

for any , any and any such that .

-

Proof.

Fix and satisfying arbitrarily. Set

Then we have

First we consider . We can rewrite it as

Conditionally on , follows the geometric distribution with success probability truncated from above by . More precisely, we have

Therefore, we obtain

Consequently, there is a constant depending only on such that

Here, we use the inequality holding for all .

Next we consider . We can rewrite it as

Now, an analogous argument to the above yields

where is a constant depending only on . Hence we have

Finally, we have

Therefore, a simple computation yields the desired result. ∎

-

Proof of Proposition 1.

First, similarly to the proof of Eq.(36) form [8], we can prove

(5) for any . In particular, Assumption 2(i) holds true.

Next, take a constant arbitrarily. We prove with this that there are constants such that Assumption 2(ii) holds true. For simplicity of exposition, we assume for all (this assumption can be easily removed).

Set

One can easily check

as for any . Therefore, it suffices to show that there are constants such that

(6) as . For the proof we adopt an analogous strategy to the proof of Proposition 6 in [8]. Let be a number such that and set . Let be the event on which the interval contains at least one point from and one point from for every . We have

(7) In the following we denote by the conditional expectation given an event .

For and , we set

Then, we decompose as

First we consider . Using the inequality holding for , we have

Therefore, noting that for every , we obtain

(8) as uniformly in and . Moreover, Lemma 1, (5) and (8) imply that

uniformly in and . Since ’s are i.i.d. variables whose distributions are the geometric distribution with success probability , the Wald identity yields

uniformly in and . Consequently, we obtain

uniformly in and for any .

Next we consider . By construction is independent conditionally to . Therefore, the Burkholder-Davis-Gundy inequality, (5) and (7)–(8) yield

uniformly in and for any . Moreover, (7)–(5) imply that uniformly in and for any . Consequently, we obtain uniformly in and for any . An analogous argument yields uniformly in and for any .

8.2 Proof of Theorem 1

First we remark that a standard localization procedure presented e.g. at the beginning of Section 7.3 of [21] allows us to assume that there is a constant such that

| (9) |

for any throughout the proof.

Next we introduce some notation. For each and , we set

and

and

and

where denotes the conditional expectation given and .

For a random variable and , we set . Also, we denote by the Orlicz norm of based on the function with respect to the conditional probability given :

Throughout this subsection, we write for two real numbers if for some constant depending only on .

Lemma 2.

-

Proof.

By symmetry it is enough to consider the case of .

First we apply the so-called reduction procedures used in [24, 25] to every realization of and (see also the proof of Lemma 2 from [8]). We define a new partition as follows: if and only if either and it has non-empty intersection with two distinct intervals from or there is such that is the union of all intervals from included in . We also define a new partition as follows: if and only if either and has non-empty intersection with two distinct intervals from or there is such that is the union of all intervals from such that is included in . Due to bilinearity both and are invariant under this procedure. is also unchanged by this application because of its definition. Moreover, by construction we have

Consequently, for the proof we may replace by . This allows us to assume that

(10) throughout the proof without loss of generality.

We turn to the main body of the proof. We decompose the target quantity as

Let us consider . For every , the Minkovski and Schwarz inequalities yield

Therefore, Proposition 4.2 in [2] and (9) imply that

Thus we obtain by (10). Hence, we conclude by Proposition 2.7.1 in [41]. By symmetry we also have . This completes the proof. ∎

Lemma 3.

For any and ,

-

Proof.

Since has the cross-spectral density , we have

where denotes convolution. Thus, Parseval’s identity yields

Since and only if , we obtain the desired result. ∎

Lemma 4.

-

Proof.

Again, by symmetry it suffices to consider the case of . Moreover, as in the proof of Lemma 2, we may assume (10) without loss of generality.

Set and

where . Then we have . Therefore, by Lemma 13 in [21] there is a universal constant such that

Let be the -conditional covariance matrix of and set . Then we have , where denotes the Frobenius norm of matrices. Hence the proof is completed once we show that

(11) for some universal constant . By Theorem 5.6.9 in [27] and (10), we have . Therefore, inequalities (ii)–(iii) in Appendix II of [9] yield

By Lemma 3 and using the Schwarz inequality twice, we obtain

Hence we have

This completes the proof of (11). ∎

Lemma 5.

Under the assumptions of Theorem 1, we have for any , and .

-

Proof.

Similarly to the above proofs, we may assume and that (10) holds true without loss of generality. Then we have

This completes the proof. ∎

Lemma 6.

-

Proof.

We decompose the target quantity as

We have

Hence, we obtain by Lemmas 2 and 4–5

So Lemma 2.2.2 in [40] yields

Now, we have by (A.2) and Corollary A.2

(12) as . Hence we conclude by assumption.

Next, Lemma 4 yields

so we obtain by Lemma 2.2.2 in [40]

Since for some and by assumption, we conclude from (12).

- Proof of Theorem 1.

(a) From Lemma 6 it is enough to prove

as . The above equation follows once we show the following statements: If () satisfy for every , then

as . To prove this statement, we decompose as

Since by (A.1) ( denotes the essential supremum of ), it suffices to prove as for any fixed due to the dominated convergence theorem. When , this follows from (A.3) and the bounded convergence theorem. In the meantime, using integration by parts, we obtain

Hence we obtain as by Corollary A.1 and assumption.

8.3 Proof of Theorem 2

Appendix A Appendix: Fundamental properties of Daubechies’ wavelet filter

This appendix collects a few key properties of Daubechies’ wavelet filter used in the proofs of our main results. First, since for all by Eq.(69d) in [35], we have

| (A.1) |

Next, for every , the filter has unit energy: (cf. Section 4.6 of [35]). Hence, the Schwarz inequality yields

| (A.2) |

Third, well approximates as in the sense that

| (A.3) |

by Theorem 1 in [29]. Here, note that Lai [29] defines Daubechies’ wavelet filter of length as a filter whose power transfer function is given by .

Finally, we prove an important property of the derivatives of and as well as its consequences.

Lemma A.1.

For any even positive integer ,

| (A.4) |

- Proof.

Corollary A.1.

For any and even positive integer ,

- Proof.

Corollary A.2.

For any , even positive integer and ,

Acknowledgments

Takaki Hayashi’s research was partly supported by JSPS KAKENHI Grant Numbers JP16K03601, JP17H01100. Yuta Koike’s research was partly supported by JST CREST Grant Number JPMJCR14D7 and JSPS KAKENHI Grant Number JP16K17105, JP18H00836, JP19K13668.

References

- Aït-Sahalia and Jacod [2014] Aït-Sahalia, Y. and Jacod, J. (2014). High-frequency financial econometrics. Princeton University Press.

- Barlow and Yor [1982] Barlow, M. T. and Yor, M. (1982). Semi-martingale inequalities via the Garsia-Rodemich-Rumsey lemma and application to local times. J. Funct. Anal. 49, 198–229.

- Bartlett and McCrary [2019] Bartlett, R. P. and McCrary, J. (2019). How rigged are stock markets? Evidence from microsecond timestamps. Journal of Financial Markets 45, 37–60.

- Barunik and Vacha [2015] Barunik, J. and Vacha, L. (2015). Realized wavelet-based estimation of integrated variance and jumps in the presence of noise. Quant. Finance 15, 1347–1364.

- Chan and Wood [1999] Chan, G. and Wood, A. T. A. (1999). Simulation of stationary Gaussian vector fields. Statist. Comput. 9, 265–268.

- Chan [1992] Chan, K. (1992). A further analysis of the lead–lag relationship between the cash market and stock index futures market. Review of Financial Studies 5, 123–152.

- Christensen et al. [2017] Christensen, K., Podolskij, M., Thamrongrat, N. and Veliyev, B. (2017). Inference from high-frequency data: A subsampling approach. J. Econometrics 197, 245–272.

- Dalalyan and Yoshida [2011] Dalalyan, A. and Yoshida, N. (2011). Second-order asymptotic expansion for a non-synchronous covariation estimator. Ann. Inst. Henri Poincaré Probab. Stat. 47, 748–789.

- Davies [1973] Davies, R. B. (1973). Asymptotic inference in stationary Gaussian time-series. Adv. in Appl. Probab. 5, 469–497.

- de Jong and Nijman [1997] de Jong, F. and Nijman, T. (1997). High frequency analysis of lead-lag relationships between financial markets. Journal of Empirical Finance 4, 259–277.

- Delbaen and Schachermayer [1994] Delbaen, F. and Schachermayer, W. (1994). A general version of the fundamental theorem of asset pricing. Math. Ann. 300, 463–520.

- Dobrev and Schaumburg [2016] Dobrev, D. and Schaumburg, E. (2016). High-frequency cross-market trading: Model free measurement and applications. Working paper.

- Gatheral and Oomen [2010] Gatheral, J. and Oomen, R. C. (2010). Zero-intelligence realized variance estimation. Finance Stoch. 14, 249–283.

- Gençay et al. [2010] Gençay, R., Gradojevic, N., Selçuk, F. and Whitcher, B. (2010). Asymmetry of information flow between volatilities across time scales. Quant. Finance 10, 895–915.

- Gradshteyn and Ryzhik [2007] Gradshteyn, I. and Ryzhik, I. (2007). Table of integrals, series, and products. Elsevier Inc., seventh edn.

- Hafner [2012] Hafner, C. M. (2012). Cross-correlating wavelet coefficients with applications to high-frequency financial time series. J. Appl. Stat. 39, 1363–1379.

- Harris et al. [2002] Harris, F. H. d., McInish, T. H. and Wood, R. A. (2002). Security price adjustment across exchanges: an investigation of common factor components for Dow stocks. Journal of Financial Markets 5, 277–308.

- Hasbrouck [1995] Hasbrouck, J. (1995). One security, many markets: Determining the contributions to price discovery. Journal of Finance 50, 1175–1199.

- Hasbrouck [2018] Hasbrouck, J. (2018). High frequency quoting: Short-term volatility in bids and offers. Journal of Financial and Quantitative Analysis 53, 613–641.

- Hasbrouck [2019] Hasbrouck, J. (2019). Price discovery in high resolution. Journal of Financial Econometrics (forthcoming) .

- Hayashi and Koike [2018] Hayashi, T. and Koike, Y. (2018). Wavelet-based methods for high-frequency lead-lag analysis. SIAM J. Financial Math. 9, 1208–1248.

- Hayashi and Koike [2019] Hayashi, T. and Koike, Y. (2019). No arbitrage and lead-lag relationships. Statist. Probab. Lett. 154, 108530.

- Hayashi and Yoshida [2005] Hayashi, T. and Yoshida, N. (2005). On covariance estimation of non-synchronously observed diffusion processes. Bernoulli 11, 359–379.

- Hayashi and Yoshida [2008] Hayashi, T. and Yoshida, N. (2008). Asymptotic normality of a covariance estimator for nonsynchronously observed diffusion processes. Ann. Inst. Statist. Math. 60, 357–396.

- Hayashi and Yoshida [2011] Hayashi, T. and Yoshida, N. (2011). Nonsynchronous covariation process and limit theorems. Stochastic Process. Appl. 121, 2416–2454.

- Hoffmann et al. [2013] Hoffmann, M., Rosenbaum, M. and Yoshida, N. (2013). Estimation of the lead-lag parameter from non-synchronous data. Bernoulli 19, 426–461.

- Horn and Johnson [2013] Horn, R. A. and Johnson, C. R. (2013). Matrix analysis. Cambridge University Press, 2nd edn.

- Huth and Abergel [2014] Huth, N. and Abergel, F. (2014). High frequency lead/lag relationships — empirical facts. Journal of Empirical Finance 26, 41–58.

- Lai [1995] Lai, M.-J. (1995). On the digital filter associated with Daubechies’ wavelets. IEEE Trans. Signal Process. 43, 2203–2205.

- Lo and MacKinlay [1990] Lo, A. W. and MacKinlay, A. C. (1990). An econometric analysis of nonsynchronous trading. J. Econometrics 45, 181–211.

- Müller et al. [1997] Müller, U. A., Dacorogna, M. M., Davé, R. D., Olsen, R. B., Pictet, O. V. and von Weizsäcker, J. E. (1997). Volatilities of different time resolutions — analyzing the dynamics of market components. Journal of Empirical Finance 4, 213–239.

- Müller et al. [1993] Müller, U. A., Dacorogna, M. M., Davé, R. D., Pictet, O. V., Olsen, R. B. and Ward, J. R. (1993). Fractals and intrinsic time — a challenge to econometricians. Tech. Rep. UAM.1993-08-16, Olsen and Associates.

- Nason et al. [2000] Nason, G. P., von Sachs, R. and Kroisandt, G. (2000). Wavelet processes and adaptive estimation of the evolutionary wavelet spectrum. J. R. Stat. Soc. Ser. B Stat. Methodol. 62, 271–292.

- Ozturk et al. [2017] Ozturk, S. R., van der Wel, M. and van Dijk, D. (2017). Intraday price discovery in fragmented markets. Journal of Financial Markets 32, 28–48.

- Percival and Walden [2000] Percival, D. B. and Walden, A. T. (2000). Wavelet methods for time series analysis. Cambridge University Press.

- Renò [2003] Renò, R. (2003). A closer look at the Epps effect. Int. J. Theor. Appl. Finance 6, 87–102.

- Subbotin [2008] Subbotin, A. (2008). A multi-horizon scale for volatility. Unpublished paper.

- Subrahmanyam [1997] Subrahmanyam, A. (1997). Multi-market trading and the informativeness of stock trades: An empirical intraday analysis. Journal of Economics and Business 49, 515–531.

- Tivnan et al. [2020] Tivnan, B. F., Dewhurst, D. R., Van Oort, C. M., Ring, J. H., Gray, T. J., Tivnan, B. F., Koehler, M. T. K., McMahon, M. T., Slater, D. M., Veneman, J. G. and Danforth, C. M. (2020). Fragmentation and inefficiencies in US equity markets: Evidence from the Dow 30. PLoS ONE 15, e0226968.

- van der Vaart and Wellner [1996] van der Vaart, A. W. and Wellner, J. A. (1996). Weak convergence and empirical processes. Springer.

- Vershynin [2018] Vershynin, R. (2018). High-dimensional probability. Cambridge University Press.