When Is the First Spurious Variable Selected by Sequential Regression Procedures?

Abstract

Applied statisticians use sequential regression procedures to produce a ranking of explanatory variables and, in settings of low correlations between variables and strong true effect sizes, expect that variables at the very top of this ranking are truly relevant to the response. In a regime of certain sparsity levels, however, three examples of sequential procedures—forward stepwise, the lasso, and least angle regression—are shown to include the first spurious variable unexpectedly early. We derive a rigorous, sharp prediction of the rank of the first spurious variable for these three procedures, demonstrating that the first spurious variable occurs earlier and earlier as the regression coefficients become denser. This counterintuitive phenomenon persists for statistically independent Gaussian random designs and an arbitrarily large magnitude of the true effects. We gain a better understanding of the phenomenon by identifying the underlying cause and then leverage the insights to introduce a simple visualization tool termed the “double-ranking diagram” to improve on sequential methods.

As a byproduct of these findings, we obtain the first provable result certifying the exact equivalence between the lasso and least angle regression in the early stages of solution paths beyond orthogonal designs. This equivalence can seamlessly carry over many important model selection results concerning the lasso to least angle regression.

Department of Statistics, University of Pennsylvania, Philadelphia, PA 19104, USA

July 11, 2018

Keywords. Lasso; Least angle regression; Forward stepwise regression; False variable; Familywise error rate.

1 Introduction

Consider observing an -dimensional response vector that is generated by a linear model

where is a design matrix, is a vector of regression coefficients, and is a noise term. To find explanatory variables that are associated with the response , especially in the setting where , three sequential regression procedures are frequently used: forward stepwise regression, the lasso (Tibshirani, 1996), and least angle regression (Efron et al., 2004). These popular methods build a model by sequentially adding or removing variables based upon some criterion. In a very natural way, a sequential method ranks explanatory variables according to when the variables enter the solution path. With this ranking of variables in place, a routine practice for forming the final model is to select all variables ranked earlier than a certain cutoff and discard the rest.

When running a sequential procedure, a practitioner often wishes to understand where along the solution path noise variables (regressors with zero regression coefficients) start to enter the model. In particular, when is the first noise variable selected? A better understanding of this problem is desirable from at least two perspectives. First, the rank of the first noise variable sheds light on the difficulty of consistent model selection, offering guidelines for selecting important variables. More precisely, if the rank is about the same size as the sparsity (the total number of nonzero regression coefficients), we could obtain a model retaining most of the important variables without causing many false selections using a sequential method, whereas a small rank implies that signal variables (regressors with nonzero regression coefficients) and noise variables are interspersed early on in the solution path and, as a result, a false selection must occur long before the power reaches one. Second, the empirical performance of numerous tools for post-selection inference in linear regression is, to a large extent, contingent upon whether the first noise variable occurs early or not (Lockhart et al., 2014; G’Sell et al., 2016; Tibshirani et al., 2016). Insights into the occurrence of the first false variable would be valuable for improving these tools and developing new ones.

However, despite an extensive body of work on these sequential methods, the literature remains relatively silent on questions of the first false variable. Existing results address these questions in a limited setting, mostly characterizing under what conditions all the signal variables precede the first noise variable, that is, perfect support recovery or, put more simply, selecting the exactly correct model. Specifically, this set of results guarantees perfect support recovery using a certain sequential method provided sufficiently strong effect sizes compared to the noise level and a form of local orthogonality of the design matrix. These results can be found for both the lasso (Zhao and Yu, 2006; Bickel et al., 2009; Wainwright, 2009) and forward stepwise (Tropp, 2004; Zhang, 2009; Cai and Wang, 2011).

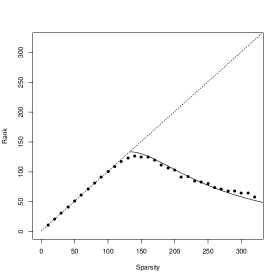

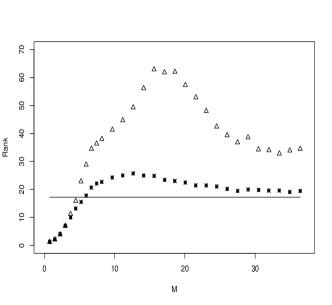

Figure 1 illustrates a simulation study that examines when the first noise variable gets selected by the lasso. The design matrix is of size consisting of independent entries, the noise term is comprised of independent standard normals, and the regression coefficients are set to and for all , with the sparsity varying from to . Note that the true effect sizes can be practically thought of as infinitely strong and the sample correlations between the regressors are small due to the independence. Fig. 1 shows that, in the low sparsity regime, the pairs (sparsity, rank) lie close to the line (precisely, it is the line ). This behavior is equivalent to saying that all the signal variables are selected prior to any false variables, which is in perfect agreement with a copious body of theoretical results available in the literature.

Strikingly, once the sparsity exceeds a certain level (around in the example), a phenomenon that is not explained by existing theory occurs: the average rank of the first noise variable becomes substantially smaller than the sparsity and, more surprisingly, the rank keeps decreasing as the sparsity increases. This phenomenon clearly demonstrates the impossibility of perfect support recovery in this non-extreme sparsity regime using the lasso, even though it is under high signal-to-noise ratios and low correlations. Presumably, as the signal is amplified by setting more components to a large magnitude, one might instinctively anticipate that a sequential method such as the lasso tends to include more signal variables at the beginning and, thus, would imagine that the first noise variable would get selected later and later. Unfortunately, the counterintuitive results as shown in Fig. 1 falsify this belief. We remark that a similar phenomenon is observed earlier in Su et al. (2017), although they did not provide any justification for the observation.

Thus, concrete predictions and explanations are needed to better understand and improve sequential methods in this sparsity regime. In response, we derive an analytical prediction that is asymptotically exact for the first noise variable. The prediction applies to the three methods under our consideration, namely forward stepwise, the lasso, and least angle regression, and potentially to other sequential methods. Denote by the rank of the first noise variable. Informally, the prediction states that, in the setting of strong effect sizes and statistically independent regressors as in Fig. 1, the three sequential procedures in the non-extreme sparsity regime all satisfy

| (1.1) |

The formal statement of this result is given in Theorem 2 in § 2.

The prediction of is additionally presented in Fig. 1, showing excellent agreement between the predicted and observed behaviors. To better appreciate this result, note that the quantity as an approximation to in (1.1) is smaller than once the sparsity exceeds , suggesting the impossibility of perfect support recovery in this regime. This is consistent with the negative result in Corollary 2 of Wainwright (2009). The prediction (1.1), however, implies more. To show this, alternatively write the right-hand side of (1.1) as

The expression above reveals that the predicted decreases as the sparsity increases. Put differently, the first noise variable is bound to occur earlier as the signal vector gets denser, successfully predicting the phenomenon shown in Fig. 1. While problems in selecting the true model by the lasso have been empirically documented in earlier work (Fan and Song, 2010), such sharp and analytical predictions are not available in the literature, perhaps due to technical difficulties.

This result has several implications. First, once the underlying signals go beyond the very sparse regime, using sequential procedures would inevitably lead to a very low power with familywise error rate control, which is the probability of selecting one or more noise variable, no matter how large the effect sizes are. Taking a simple example in which both and are set to be equal and large and for some fixed , the prediction asserts that the first false variable is included after no more than

steps (note that is the leading component for a large ). For a fixed , however, the predicted rank only accounts for a vanishing fraction of the signal variables, which can be gleaned from the fact that . In other words, the three sequential methods being considered yield vanishing power if no noise variable is allowed to be included, even in the noiseless case (). In particular, these negative results are derived under Gaussian designs with independent columns, which have vanishing sample correlations and satisfy some conditions believed to be favorable for model selection, including restricted isometry properties (Candès and Tao, 2005) and restricted eigenvalue conditions (Bickel et al., 2009). Thus, the negative results are likely to carry over to a much broader class of design matrices. In fact, extensive simulations carried out in § 3 demonstrate that problems of the first false variable are only exacerbated in more general settings.

Another implication yielded by this prediction is that the three sequential regression methods seem to behave similarly in ranking variables, at least in the independent random design setting. Compared with forward stepwise, the lasso and least angle regression, along with their infinitesimal version forward stagewise regression (see, for example, Efron et al. (2004)), are long-time considered less greedy because at each step they gradually blend in a new variable instead of adding it discontinuously (Efron et al., 2004). To be more precise, the forward stepwise selects the predictor with the largest absolute correlation with the residual vector and then aggressively takes a large step in the direction of the selected predictor, whereas the others proceed in a more democratic manner along a direction equiangular between the set of selected predictors (the lasso and forward stagewise regression bear certain restrictions on this equiangular approach). This critical distinction between the two strategies is anticipated—or, at least wished—to lead to contrasting model selection performance. Interestingly, this is not the case; these two strategies yield the same behavior of selecting the first noise variables in our setting. As a byproduct, we obtain Theorem 3 for the lasso and least angle regression, which, to the best of our knowledge, is the first mathematically provable result certifying the exact equivalence between early solution paths of these two procedures beyond orthogonal designs.

In the non-extreme sparsity regime, why do these distinct sequential methods select the first false variable so early? Taking a closer look at the derivation of the prediction, we can identify the cause, which is, loosely speaking, due to the greedy nature of these sequential regression methods. Moreover, the equiangular strategy adopted by the lasso and least angle regression fails to alleviate greediness from the perspective of when the first noise variable gets selected. To shed light on this cause, recall that all the three methods at each time include a variable that roughly has the largest absolute inner product with the current residuals. As the regression coefficients get denser, the solution at the beginning of the path is overwhelmingly biased and the residual vector absorbs many of the true effects contributed by the nonzero components of . As a result, some irrelevant variable would exhibit high correlations with the residuals and hence is selected incorrectly and early. That being said, it requires several novel ideas to precisely characterize what we describe here.

With this underlying cause in mind and to improve on sequential methods, we introduce the double-ranking diagram to identify early false variables along solution paths. In slightly more detail, this diagram contrasts the rank of each variable given by a sequential procedure (horizontal axis) with that given by a low-bias estimator (vertical axis) such as the least-squares estimator. In spite of a significant horizontal rank, an early noise variable might be revealed by its possibly less significant vertical rank. Related ideas have appeared in recent variable screening work, for instance, Wang and Leng (2016). We demonstrate the usefulness of this diagram via a mix of theoretical and empirical results.

2 Understanding the Phenomenon

2.1 Predicting the first spurious variable

We consider a sequence of problems indexed by , where , and are all assumed to grow to infinity as in asymptotic statements. The subscript is often omitted when clear from the context. Letters and in various settings denote positive constants that do not depend on the problem index . Below we formalize our working hypothesis concerning the linear model .

Assumption 1.

The design has independent entries and consists of independent errors. We further assume and are independent. The coefficient vector has fixed components equal to some and the rest are all zero. Last, we assume and for arbitrary positive constants , and .

The assumption on is satisfied in some popular examples studied in the literature, for instance, the linear sparsity framework where and converge to some constants (Bayati and Montanari, 2012). Moreover, a number of cases leading to satisfy Assumption 1, for instance, and . Under this assumption, each column of is approximately normalized, having about unit Euclidean norm. This random design is conventionally considered to be easy for model selection since it obeys restricted isometry properties (Candès and Tao, 2005) or restricted eigenvalue conditions (Bickel et al., 2009) with high probability. The nonrandom parameters and both implicitly depend on the index and thus are allowed to vary freely. In particular, the noiseless case is not excluded, in which the signal-to-noise ratio is essentially infinite. For completeness, the number can be replaced by any positive number smaller than 1.

Before presenting our main results Theorems 1 and 2, we give a brief overview of the three methods for ease of reading. In broad outlines, least angle regression increases the coefficients of included variables in their joint least squares direction until an unselected variable has as much inner product with the residuals, which is included in the next step. Least angle regression stops when the residuals are zero or all variables are included. If a nonzero coefficient is removed from the active set whenever it hits zero, this adjustment leads to the lasso, which is better-known as the minimizer of the convex program over for ranging from infinity to zero. Forward stepwise is described in detail in § 8.5 of Weisberg (1980). In our setting, the intercept is not included and normalization is not applied to any columns of . Last, recall that denotes the rank of the first noise variable, and denotes a sequence of random variables converging to zero in probability.

Theorem 1.

Under Assumption 1, the first spurious variable selected by each of forward stepwise, the lasso, and least angle regression satisfies

If the signal magnitude is not sufficiently large compared with , the logarithm of would be much smaller than the upper bound appearing in the display above, meaning that the problems of the first false variables could be worse. Interestingly, this bound is sharp when is sufficiently large compared with , as demonstrated in the theorem below.

Theorem 2.

Under Assumption 1 and in addition provided that , the three sequential methods obey

Provided in the Appendix, the proofs of both theorems involve some techniques that are likely to extend beyond the three sequential methods. The condition concerning the ratio between and can be relaxed to . Setting as in Assumption 1, for example, Theorem 2 follows if is bounded away from . An immediate consequence of this theorem is as follows.

Corollary 2.1.

Under Assumption 1, each of the three methods in the noiseless case () obeys

In addition to predicting the phenomenon observed in Fig. 1, Theorem 2 together with Corollary 2.1 demonstrates that having an even stronger signal magnitude does not affect much as long as it exceeds a certain level.

The theorems presented here differ from results that are found extensively in the literature claiming a high probability of selecting the exactly correct model, mainly due to assuming different sparsity regimes of the regression coefficients . Explicitly, the former assumes whereas the latter often, if not always, assumes a restrictive sparsity regime such as or . In fact, under Assumption 1, it is unrealistic to expect perfect model selection using sequential methods: below a simple corollary of Theorem 1 shows the number of signal variables before the first false variable only accounts for an insignificant fraction of the total number of signal variables.

Corollary 2.2.

Under Assumption 1, each of the three methods satisfies

To better appreciate Corollary 2.2, consider the scenario where and for some positive constants and . Theorem 1 shows that, up to a vanishing fraction, the logarithm of is no larger than . This expression for approximating yields , confirming Corollary 2.2 in this linear sparsity regime. We summarize the finding in the corollary below.

Corollary 2.3.

Under Assumption 1 and additionally provided that and for arbitrary positive constants and , each of the three methods satisfies

This regime of linear sparsity is previously employed in Su et al. (2017), which studies limitations of the lasso for the false discovery rate control. The techniques developed there are not applicable to studying the first noise variable, which is a much finer problem.

2.2 Equivalence between lasso and least angle regression

In contrast to the other two methods, the lasso would drop a selected variable if its coefficient hits zero. This irregularity of the lasso path might lead to ambiguity in interpreting the rank in Theorems 1 and 2. Fortunately, as a byproduct of the above, the theorem below rules out the possibility of such ambiguity.

Theorem 3.

Assume has independent entries. Then, with probability at least , no drop-out occurs before the first

variables along the lasso path are selected, where denotes the least integer greater than or equal to and is some universal constant.

Note that Theorem 3 only requires the normality of , as opposed to additional conditions imposed on , and in Assumption 1. As seen from its proof in the Appendix, the validity of the theorem depends on the design matrix basically only through its restricted isometry property. Thus, this result can seamlessly carry over to other matrix ensembles with an appropriate restricted isometry property constant, such as Bernoulli random matrices (Candès and Tao, 2005).

Under Assumption 1, . Consequently, Theorem 3 together with Theorem 1 ensures that the first noise variable selected by the lasso is not preceded by any drop-out with probability approaching one.

This byproduct provides new insights into the lasso path and is a contribution of independent interest to high-dimensional statistics. The lasso is known to coincide exactly with least angle regression until the first time the lasso drops a selected variable (Efron et al., 2004; Tibshirani and Taylor, 2011). To our knowledge, however, the question of where along the path the lasso and least angle regression differ has not been addressed in prior research, perhaps due to technical difficulties. By confirming the equivalence between these two procedures, Theorem 3 allows us to carry over well-known results on the lasso for model selection to least angle regression.

2.3 Heuristics and insights

In this section we give an informal derivation of Theorems 1 and 2. Although our discussion below lacks rigor, nevertheless, the goal is to gain insights into this counterintuitive phenomenon. For the full proofs, see the Appendix.

We focus on the noiseless case in Assumption 1, which is presumably the most ideal scenario for model selection. Denote by the support of the signals and by an estimate given by any of the three sequential methods somewhere along the solution path. Write for the index off the support having the largest inner product in magnitude with the residual , and for the index on the support having the th largest inner product in magnitude with the residual. By using some technical arguments found in the Appendix, we get

| (2.1) |

Above and henceforth, denotes the transpose of . Recognizing that the sequential methods rank variables essentially according to the correlations with the residual, where in our case correlations are roughly equivalent to inner products since the columns of are approximately normalized, from (2.1) we must have

at the point where the first false variable is just about to enter the model. In the linear sparsity regime , this yields

The exposition above suggests that an early spurious variable is mainly due to a large inner product , which would not be the case if was a low-bias estimator of . However, until a significant proportion of the variables have been selected, a solution provided by a sequential method is overwhelmingly biased. Another way to formalize this point is that the residual still contains a significant amount of true effects, largely contributed by presently unselected variables. This bias acts as if it were noise and, as a consequence, some irrelevant variables happen to correlate highly with the residual vector, leading to false variables selected early. This is not a matter of the signal-to-noise ratio; an increasing signal magnitude would enlarge the bias as well and, hence, noise variables always occur early. Other examples of pseudo noise caused by bias have been observed in previous work (Bayati and Montanari, 2012). To be complete, we remark that this phenomenon does not appear in regimes of extreme sparsity (see, for example, Wainwright (2009)).

3 Illustrations

3.1 Numerical examples

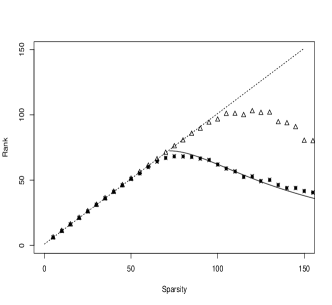

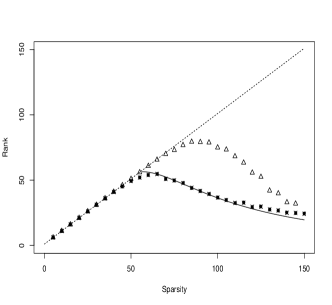

We present simulation experiments to illustrate the first false variable of the three sequential methods, along with the predictions given by Theorems 1 and 2. Specifically, we numerically examine three studies concerning the effect of design matrix shapes, signal magnitudes, and correlations between the columns of on the first spurious variable. Two scenarios are experimented for each study.

Study 1. In the first experiment (square design) the design of size has independent entries, the signals for and for , and each noise component follows independently. In the second experiment (fat design) the design is changed to be size of and has independent Bernoulli entries, which take value with probability half and otherwise , while all the other assumptions remain the same. Results of the two experiments are shown in Figure 2(a) and (b), respectively.

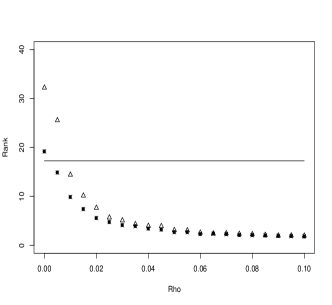

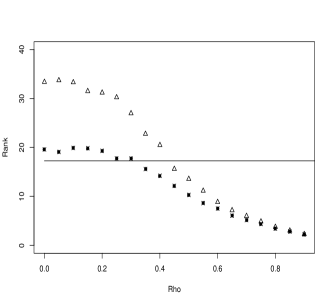

Study 2. In both experiments, the design matrix consists of independent entries and each is independently distributed as . For the first experiment (one mixture), we set for and for . For the second one (two mixtures), we set for for and for . The parameter is varied from to . Note that the two mixtures take the same value when . Results are shown in Fig. 2(c) and (d).

Study 3. This scenario uses obeying for and otherwise. The noise consists of independent standard normals. The design matrix has each row independently drawn from . For the covariance matrix , the first experiment (equi correlation) assumes if and . In the second one (decaying correlation), . Results are shown in Fig. 2(e) and (f).

Both the lasso and least angle regression closely match our predictions. Notably, the two procedures yield exactly the same ranks of the first noise variables, hence supporting Theorem 3. On the other hand, forward stepwise exhibits larger departures from the theoretical predictions, mainly due to the slow convergence to the asymptotics, while as well showing a decreasing rank once the sparsity exceeds a cutoff.

As shown in Fig. 2(a) and (b), the first false variable occurs earlier as decreases while gets larger. In particular, the behaviors of the methods under Bernoulli random designs as in Fig. 2(b) closely resemble that under Gaussian random designs. In Fig. 2(c), the rank of the first false variable increases as the signal magnitude is amplified. While this increasing rank is expected, Fig. 2(d) in contrast illustrates a rather surprising phenomenon: the rank drops after exceeds a certain level. More precisely, given , the lasso selects the first false variable earlier and earlier even though the sparsity is fixed and each signal gets strengthened, and the phenomenon is even more transparent for forward stepwise. Intuitively, this is because the effective sparsity in the case of a moderately large is smaller than the nominal sparsity . To see this, observe that the ratio of the signals of the first 40 components and the next 40 components is , which is noticeably larger than 1. Put another way, the first 40 components act as the main signals and, hence loosely speaking, the effective sparsity is smaller than . In the presence of significant correlations between columns of , Fig. 2(e) and (f) clearly show that the problem of early false variables is further exacerbated.

(a) (b)

(c) (d)

(e) (f)

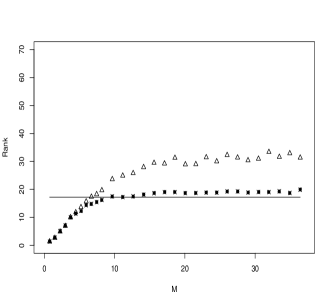

3.2 HIV data

As a real data example, we consider the HIV-1 data introduced by Rhee et al. (2006) to study the genetic basis of HIV-1 resistance to several drugs. Also used in a number of other works (Barber and Candès, 2015; G’Sell et al., 2016; Janson and Su, 2016), this data set in particular contains genotype information of HIV-1-infected individuals across locations after removing duplicate and missing values. The columns of are standardized to have zero mean and unit Euclidean norm. The response is synthetically generated by assigning an effect of to each of uniformly randomly chosen columns of and setting a noise level to 1.

Table 1 reports the results averaged over 500 replicates. The three methods start to have a decreasing rank around , which is much smaller than . In addition, for each level of sparsity, the first spurious variable is included much earlier than the predictions. This gap is not surprising given that the predictions are tailored to independent Gaussian designs while the design from the HIV-1 data has strongly correlated columns. To be more precise, about column pairs of have correlations greater than .

| 10 | 25 | 40 | 55 | 70 | 85 | 100 | |

|---|---|---|---|---|---|---|---|

| Lasso | 10.4 (2.1) | 15.4 (9.6) | 10.3 (9.2) | 6.8 (6.0) | 5.5 (4.6) | 4.4 (3.8) | 3.7 (3.5) |

| Least angle regression | 10.4 (2.1) | 15.4 (9.6) | 10.3 (9.2) | 6.8 (6.0) | 5.5 (4.6) | 4.4 (3.8) | 3.7 (3.5) |

| Forward stepwise | 10.6 (1.9) | 18.8 (10.0) | 18.5 (15.9) | 13.3 (16.0) | 10.0 (11.7) | 7.5 (8.2) | 7.0 (7.6) |

| Gaussian designs | 11.0 | 26.0 | 41.0 | 51.3 | 45.7 | 38.3 | 31.8 |

4 Visualizing Early Noise Predictors

As discussed in § 2.3, the three sequential procedures are marginal correlation-based at the beginning of their solution paths, picking variables essentially according to the correlations with the residuals. In light of this viewpoint, an unbiased or low-bias estimator of the signals might provide sequential methods with complementary information for variable selection. The least-squares estimator, if available, is a natural candidate.

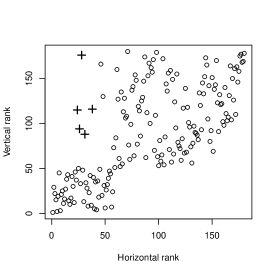

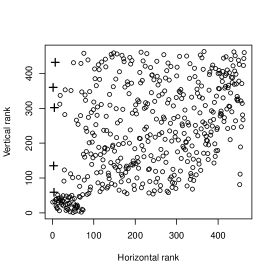

We introduce the double-ranking diagram to bring together the strengths of sequential methods and low-bias estimators such as the least-squares estimator . Figure 3 presents two instances of this diagram: one is in the same setting as Fig. 1 except for a different size and a fixed sparsity , and another is in the same setting as Table 1 with a fixed sparsity . For each variable, the horizontal axis represents its rank by a sequential method, and the vertical axis represents its rank by a low-bias estimator. For example, the horizontal rank of the th variable is given according to the magnitude of : the larger this statistic is, the smaller the rank is. Equivalently, the variables can be ranked using the -values.

The double-ranking diagram can serve as a simple data visualization tool to assist the identification of early false variables for sequential regression methods. Intuitively, an important variable would presumably possess both a small horizontal rank and a small vertical rank, hence appearing in the bottom-left corner of the diagram with a good chance. In light of this intuition, we screen out variables that are selected early by a sequential method but have unusually large vertical ranks, which in the case of least squares amount to small -values or insignificant -values. As seen from Fig. 3, the first five false variables in each instance have much larger vertical ranks compared with their horizontal ranks. In particular, these false variables are placed far away from the signal variables in the diagram. In view of this example, to use this diagram, one can set some threshold for the vertical rank and only select variables that are below the threshold and in addition have significant horizontal ranks. On the other hand, in the low signal-to-noise ratio regime the diagram may not give a clear-cut separation between false and true predictors, and its use requires some caution. The following simple proposition states that the diagram can perfectly separate the first spurious variable from all the true variables using the least-squares estimator under certain conditions.

Proposition 4.1.

Under Assumption 1 and provided that and

for some constant , then in the double-ranking diagram the first noise variable has a greater vertical rank than all the true variables.

The main ingredient behind this tool is a blend of new and old ideas found in the literature. On the one hand, our discussion in § 2.3 demonstrates that, while sequential methods work well in very sparse settings, as the signals get denser, the pseudo noise can accumulate quickly and thus may dwarf some true signals no matter how strong the corresponding coefficients are. On the other hand, the method of least squares favors the case of dense signals since the estimator variances basically stay the same as the sparsity of the signals increases. In particular, variables with sufficiently strong effects can stand out using the least-squares estimator in the presence of highly correlated columns in the design matrix. This property of the least-squares estimator and its variants plays a pivotal role for a number of variable screening procedures (Wasserman and Roeder, 2009; Pokarowski and Mielniczuk, 2015; Wang and Leng, 2016).

5 Discussion

In the regime of non-extreme sparsity, the common intuition that sequential regression procedures find a significant portion of all important variables before the first false variable merits some skepticism. We have developed sharp predictions that disprove this intuition for forward stepwise, the lasso, and least angle regression under independent Gaussian designs, which satisfy certain desirable properties for model selection. Additionally, the predictions hold irrespective of how strong the effect sizes are. Thus, the first noise variable is likely to occur very early in more general settings. Our numerical results are in agreement with this viewpoint.

In light of the above, more caution is required when using these sequential methods, unless the true regression coefficients are very sparse. Useful information for identifying early noise variables can be provided by low-bias methods such as the least-squares estimators. The double-ranking diagram is a simple tool that unifies the strengths of the two groups of methods.

Avenues for further investigation are in order. First, it is of interest to improve the predictions for forward stepwise and extend the predictions to more sequential methods such as backward stepwise and forward-backward stepwise. The simulation studies imply that the lower bound on the sparsity in Assumption 1 could be possibly relaxed to . Second, in the high-dimensional setting where , which low-bias estimator should we choose for the double-ranking diagram to yield the vertical ranking? Candidates worth considering include the lasso with a small penalty, ridge regression with a small penalty, generalized least-squares estimators (see, for example, Wang and Leng (2016)), and some recently proposed ranking procedures such as in Ke and Yang (2017). It is also worth incorporating strategies proposed by Fan et al. (2015) and Fan and Zhou (2016) to investigate spurious discoveries. Last, as seen from Table 1, the rank of the first noise variable has relatively large standard errors. A question of practical relevance is to characterize this large variation.

Acknowledgements

The author is grateful to Jianqing Fan, the editor, associate editor and two referees for their comments that improved the presentation of the paper. This work was supported in part by the National Science Foundation via grant CCF-1763314.

References

- Baraniuk et al. (2008) Richard Baraniuk, Mark Davenport, Ronald DeVore, and Michael Wakin. A simple proof of the restricted isometry property for random matrices. Constructive Approximation, 28(3):253–263, 2008.

- Barber and Candès (2015) Rina Foygel Barber and Emmanuel Candès. Controlling the false discovery rate via knockoffs. The Annals of Statistics, 43(5):2055–2085, 2015.

- Bayati and Montanari (2012) Mohsen Bayati and Andrea Montanari. The LASSO risk for Gaussian matrices. IEEE Transactions on Information Theory, 58(4):1997–2017, 2012.

- Bickel et al. (2009) Peter J Bickel, Ya’acov Ritov, and Alexandre B Tsybakov. Simultaneous analysis of lasso and dantzig selector. The Annals of Statistics, pages 1705–1732, 2009.

- Cai and Wang (2011) T Tony Cai and Lie Wang. Orthogonal matching pursuit for sparse signal recovery with noise. IEEE Transactions on Information Theory, 57(7):4680–4688, 2011.

- Candès and Tao (2005) Emmanuel Candès and Terence Tao. Decoding by linear programming. IEEE Transactions on Information Theory, 51(12):4203–4215, Dec. 2005.

- de Haan and Ferreira (2007) Laurens de Haan and Ana Ferreira. Extreme value theory: An introduction. Springer Science & Business Media, 2007.

- Efron et al. (2004) Bradley Efron, Trevor Hastie, Iain Johnstone, and Robert Tibshirani. Least angle regression. The Annals of Statistics, 32(2):407–499, 2004.

- Fan and Song (2010) Jianqing Fan and Rui Song. Sure independence screening in generalized linear models with NP-dimensionality. The Annals of Statistics, 38(6):3567–3604, 2010.

- Fan and Zhou (2016) Jianqing Fan and Wen-Xin Zhou. Guarding against spurious discoveries in high dimensions. Journal of Machine Learning Research, 17(203):1–34, 2016.

- Fan et al. (2015) Jianqing Fan, Qi-Man Shao, and Wen-Xin Zhou. Are discoveries spurious? Distributions of maximum spurious correlations and their applications. arXiv preprint arXiv:1502.04237, 2015.

- G’Sell et al. (2016) Max Grazier G’Sell, Stefan Wager, Alexandra Chouldechova, and Robert Tibshirani. Sequential selection procedures and false discovery rate control. Journal of the Royal Statistical Society: Series B (Statistical Methodology), 78(2):423–444, 2016.

- Hsu et al. (2012) Daniel Hsu, Sham Kakade, and Tong Zhang. A tail inequality for quadratic forms of subgaussian random vectors. Electronic Communications in Probability, 17, 2012.

- Janson and Su (2016) Lucas Janson and Weijie Su. Familywise error rate control via knockoffs. Electronic Journal of Statistics, 10(1):960–975, 2016.

- Ke and Yang (2017) Zheng Tracy Ke and Fan Yang. Covariate assisted variable ranking. arXiv preprint arXiv:1705.10370, 2017.

- Lockhart et al. (2014) Richard Lockhart, Jonathan Taylor, Ryan J Tibshirani, and Robert Tibshirani. A significance test for the lasso. The Annals of Statistics, 42(2):413, 2014.

- Pokarowski and Mielniczuk (2015) Piotr Pokarowski and Jan Mielniczuk. Combined and greedy penalized least squares for linear model selection. Journal of Machine Learning Research, 16(5), 2015.

- Rhee et al. (2006) Soo-Yon Rhee, Jonathan Taylor, Gauhar Wadhera, Asa Ben-Hur, Douglas L Brutlag, and Robert W Shafer. Genotypic predictors of human immunodeficiency virus type 1 drug resistance. Proceedings of the National Academy of Sciences, 103(46):17355–17360, 2006.

- Su et al. (2017) Weijie J Su, Małgorzata Bogdan, and Emmanuel J Candes. False discoveries occur early on the lasso path. The Annals of Statistics, 45(5):2133–2150, 2017.

- Tibshirani (1996) Robert Tibshirani. Regression shrinkage and selection via the lasso. Journal of the Royal Statistical Society. Series B (Methodological), pages 267–288, 1996.

- Tibshirani et al. (2016) Ryan Tibshirani, Jonathan Taylor, Richard Lockhart, and Robert Tibshirani. Exact post-selection inference for sequential regression procedures. Journal of the American Statistical Association, 111(514):600–620, 2016.

- Tibshirani and Taylor (2011) Ryan J Tibshirani and Jonathan Taylor. The solution path of the generalized lasso. The Annals of Statistics, 39(3):1335–1371, 2011.

- Tropp (2004) Joel A Tropp. Greed is good: Algorithmic results for sparse approximation. IEEE Transactions on Information Theory, 50(10):2231–2242, 2004.

- Vershynin (2012) Roman Vershynin. Introduction to the non-asymptotic analysis of random matrices. In Compressed Sensing, Theory and Applications, 2012.

- Wainwright (2009) Martin J Wainwright. Sharp thresholds for high-dimensional and noisy sparsity recovery using -constrained quadratic programming (Lasso). IEEE transactions on information theory, 55(5):2183–2202, 2009.

- Wang and Leng (2016) Xiangyu Wang and Chenlei Leng. High dimensional ordinary least squares projection for screening variables. Journal of the Royal Statistical Society Series B, 78(3):589–611, 2016.

- Wasserman and Roeder (2009) Larry Wasserman and Kathryn Roeder. High dimensional variable selection. The Annals of Statistics, 37(5A):2178, 2009.

- Weisberg (1980) Sanford Weisberg. Applied linear regression. John Wiley & Sons, 1980.

- Zhang (2009) Tong Zhang. On the consistency of feature selection using greedy least squares regression. Journal of Machine Learning Research, 10(Mar):555–568, 2009.

- Zhao and Yu (2006) Peng Zhao and Bin Yu. On model selection consistency of Lasso. Journal of Machine Learning Research, 7(Nov):2541–2563, 2006.

Appendix A Proofs

The appendix is devoted to proving the main technical results in the paper, namely Theorem 1, Theorem 2, Theorem 3, and Proposition 4.1. Here we collect some notation used in the proofs. Denote by the true support set, that is, . Let be the matrix formed by columns from , and be the matrix derived by removing the th column from . We often use the letter to denote , the signal part in linear regression. Throughout the Appendix, assume in Assumption 1 and adopt the following notation:

| (A.1) |

where denotes the usual norm .

A.1 Theorem 1

We state some preparatory lemmas for the proof of Theorem 1. The proofs of these lemmas are given once the proof of Theorem 1 for all the three sequential procedures is complete.

Lemma A.1.

Lemma A.2.

Let be independent standard normals and be the order statistics. For any (deterministic) sequence such that as , we have

The proof of Lemma A.2 is omitted. Interested readers can find its proof in Chapter 2 of de Haan and Ferreira (2007).

Lemma A.3.

Lemma A.4 (for the lasso case).

Fit on the true support using the lasso and denote by the lasso solution with penalty . Then, under Assumption 1, there exists a constant such that

holds uniformly for all with probability tending to one, where we make the (unusual) convention that .

Above, equals the number of nonzero components of a vector, and is a -dimensional vector which takes on . Next, we proceed to a definition that is the subject of Lemma A.6.

Definition A.5.

Let be the largest positive integer such that

and set to if it does not exist. Let be the largest positive integer such that

and set to if it does not exist.

Lemma A.6.

Let be a constant. Under Assumption 1, all the following statements are true.

-

(a)

Assume . If , then , and

-

(b)

Assume . If and for some constant (which is used to guarantee that ), then we have and

-

(c)

Assume . If , then and

A detailed comment on how and are used in proofs is as follows. Under our Assumption 1, the rank of a variable roughly depends on the absolute value of . The random variable , as seen later in the proof of Theorem 1, is approximately distributed as (note that is defined in (A.1)). Intuitively, taking , the first display of Definition A.5 represents the event that the th true variables along the solution path has an inner product with about equal to that of the first false variable (recognize from Lemma A.2 that the th largest of independent random variables is about and the largest of independent random variables is about ). The notation is introduced because can also take a large magnitude if in the parentheses is about .

Henceforth, is set to and the dependence on the argument is omitted for both and . Due to Lemma A.1, it is without loss of generality to consider and fixed and small.

With these preparatory lemmas in place, we are ready to prove Theorem 1 in the lasso and least angle regression cases. The first part of the proof offers a simple representation of the order statistics of , and this representation serves as useful ingredients in proofs of other results.

Proof of Theorem 1 in the lasso and least angle regression cases.

Without loss of generality, assume that the true support set . Let be a permutation of such that

| (A.2) |

Conditional on and , the exchangeable random variables are jointly normal with means all equal to and an equicorrelated covariance that has on the diagonal and off the diagonal. These can be derived by using properties of the conditional normal distribution: suppose are iid standard normals, then is normally distributed with mean and variance conditional on . Let be normally distributed with mean 0 and variance , and further assume to be independent of the random design and the noise . Then, are independent normals each with conditional mean and conditional variance . Thus, conditional on and , we see that

for independent standard normals . Note that keep the same ordering as in (A.2).

Consider the first time that the full lasso (regressing on ) is just about to include some variable among , where and as in Definition A.5. Call this variable and the penalty at that time . Denote by the event that all the selected variables preceding are true variables. On (the complement of ), there are at most variables selected before the first false variable. Hence, we get

on , where is an arbitrary constant. By Lemma A.6, we get

with probability approaching one. Above, the term is absorbed into . Lemma AA.1 is also used in the inequality following the third equality, with in place of . Since is arbitrary, we get

on .

The rest is devoted to proving . To proceed, we point out an observation on the lasso: the lasso running on the full design is the same as regressing on until the th variable gets selected. In light of this observation, we perform the lasso on the true support . Since is much smaller than the bound given by Theorem 3, we can assume no drop-out has happened until arrives and, hence, least angle regression is the same as the lasso. Because , we get

| (A.3) |

By Lemma A.2, the left-hand side of (A.3) obeys

A little analysis reveals that Assumption 1 implies

Hence, we get

Similarly, the right-hand side of (A.3) obeys

Thus, from (A.3) it follows that

yielding

| (A.4) |

The KKT conditions of the lasso at give

The equality above together with (A.4) and Lemma A.4, which gives , yields

| (A.5) | ||||

Now, we seek a contradiction to get . Since none of has been included at on the event , we get

| (A.6) |

Recognizing the independence between all and , we get

Now we turn to focus on , which is distributed as the maximum absolute values of iid standard normals. Hence, Lemma A.2 gives

Consequently,

By assumption,

Therefore, we get

contradicting (A.6). Thus, .

∎

Next, we aim to prove Theorem 1 in the case of forward stepwise. Below are two preparatory lemmas.

Lemma A.7.

Given , for any subset of cardinality at most , , and , regress on and denote by the least-squares coefficient of in this fit. Then, under Assumption 1, with probability approaching one, we have

uniformly over all , and of cardinality at most .

Lemma A.8.

This lemma is a simple consequence of a well-known concentration inequality of the form

for all . The proof is thus omitted. Now we move to prove Theorem 1 for forward stepwise regression.

Proof of Theorem 1 in the forward stepwise case.

Here, we use the same proof strategy as in the lasso and least angle regression cases. Define and as earlier. To complete the proof, it suffices to show that .

We also assume that forward stepwise is performed on the true support . Denote by the number of variables selected before , that is, is selected in the th step. Take some satisfying for some . It is easy to show that with probability approaching one.

Denote by the set of selected variables before . On the event , the definition of forward stepwise yields

Recall that stands for the complement of . In particular, we have

| (A.7) |

where . Let be residual vector by regressing on . Then,

where ’s are the least-squares coefficients. By Lemma A.7, we get

which makes use of Lemma A.3. Therefore, we get

Together with Lemma A.8, the equality above gives

| (A.8) | ||||

Similarly, we have

| (A.9) |

For the right-hand side of (A.7), we have

| (A.10) |

with probability approaching one. Combining (A.7), (A.8), (A.9), and (A.10) gives

| (A.11) |

on the event .

To complete the proof, we shall show that (A.11) holds with probability tending to zero. On the one hand, from the earlier proof for the case of the lasso, we see that

which makes use of the fact that under our assumptions. On the other hand,

Hence, (A.11) yields

which is a clear contradiction. Hence, .

∎

Proof of Lemma A.1.

Recall the notation . We first list some facts that are constantly used in the proof. First,

This is because is just a random variable with degrees of freedom. Thus, , yielding . Hence, we get

Next we turn to prove that . In fact, we have

| (A.12) |

For , note that

And conditional on , the numerator is normally distributed with mean 0 and variance , implying

Combining the results above, particularly (A.12), gives

Hence, with probability approaching one for an arbitrary constant . ∎

Proof of Lemma A.3.

If , then is independent of . This means conditional on the distribution of is . Thus,

with probability at least . Taking a union bound yields

with probability . Now consider a such that . Note that

| (A.13) |

The first term obeys

for any . Setting to gives

In addition, we have

Recognizing that , we get

| (A.14) |

For the second term of (A.13), note that is distributed as a centered normal random variable with variance conditional on , due to the independence between and . Consequently, holds with probability , from which we get

which makes use of the fact that uniformly for all . Plugging the last display and (A.14) into (A.13) gives

which is smaller than with probability tending to one. ∎

Proof of Lemma A.4.

First, we consider the case where . Since

(we suppress the dependence of on ) and

for all , which makes use of Lemma A.3 (this also follows from (A.17) below). In this case, the proof is simply as follows:

Now we move to the case where . Recognizing that the number of pairs is , we get

under Assumption 1. This result implies

| (A.15) | ||||

for all such that . Let be the index that is the largest. Taking

| (A.16) |

as given for the moment, from (A.15) we get

Summarizing from the two cases, the lemma holds if we take any constant .

Proof of Lemma A.6.

For the first case, by definition we have

and

where we write for . These two inequalities are equivalent to

| (A.18) | ||||

Under Assumption 1, it is easy to check that

Thus, from (A.18) we get

The rest two cases follow from similar reasoning and, thus, their proofs are omitted.

∎

Proof of Lemma A.7.

Here, the least-squares estimate is

which, conditional on , is distributed as

Denote by the event that

where denotes the matrix spectral norm. Note that we have

where the max operator is taken over all triples such that , and . Given , all the eigenvalues of are upper bounded by 2. Since every diagonal element of a square matrix is lower bounded by the minimum eigenvalue of the matrix, all the diagonal elements of are no greater than . As a result,

Hence,

Together with , which follows from the proof of Theorem 3, the last display gives

To see why , recognize that the term on the right-hand side of (A.39) is greater than under Assumption 1. ∎

A.2 Theorem 2

Lemma A.9.

Fit the response on the true support using the lasso and denote by the lasso solution. Under Assumption 1, further assume that with probability tending to one. Then, for an arbitrary constant , with probability approaching one, all the variables enter the model before any of

along the lasso path.

Lemma A.10.

With Lemmas A.9 and A.10 in place, now we give the proof of Theorem 2 where the procedure is the lasso or least angle regression. Note that for large and sufficiently small , we have .

Proof of Theorem 2 in the lasso and least angle regression cases.

The proof starts by making use of Lemma A.10, which concludes

with probability tending to one for any constant . To see this, note that Assumption 1 along ensures and, as a result, we get

given the condition that .

As in the proof of Theorem 1, here it also suffices to only focus on the lasso case. Consider fitting the lasso on . Denote by the last variable among that enters the model and let be the lasso penalty when is just about to enter the lasso path. Note that and . The KKT conditions give

| (A.19) |

Note that

| (A.20) | ||||

From Lemma A.9 we see that, with probability approaching one, by the time of none of the variables has been included in the lasso path. Hence, the lasso model consists of no more than variables at any time before , and it is easy to check that

for all . Consequently, we get

uniformly for all . Thus, Lemma A.4 shows . Hence, taking (A.19) and (A.20) together shows that obeys

| (A.21) |

(Similarly, given a small , Theorem 3 ensures that by that time no drop-out has ever happened and, consequently, the lasso and least angle regression are equivalent in our discussion.) If we can show that

| (A.22) |

for all and all , then the full lasso (on ) selects variables only from before time . Call this event . Thus, on the first selected variables along the lasso path are all signal variables. As for , Lemma A.6 yields

Provided with probability tending to one, we get

Hence, we have

for all constant . Setting gives

as desired.

Establishing (A.22) is the subject of the remaining proof. That is, prove . For , observe that

| (A.23) |

Making use of the independence between and , the first term obeys

with probability approaching one. The second term, , as shown earlier by Lemma A.4, satisfies that

with probability tending to one. Hence, (A.23) yields

where the second last inequality follows from (A.21). Therefore, . ∎

Next, we turn to prove Theorem 2 in the case of forward stepwise regression.

Lemma A.11.

Fit the response on the true support using forward stepwise. Under Assumption 1, further assume that with probability tending to one. Then, for an arbitrary constant , with probability approaching one, all the variables enter the model before any of

by forward stepwise.

Proof of Theorem 2 in the forward stepwise case.

Consider running forward stepwise on the design matrix . Denote by the last variable among that gets selected. Let be the number of variables selected prior to . From Lemma A.11 we see that, with probability approaching to one, by then none of has been selected, that is, . The proof would be completed once we show that by then no noise variables would be selected if we perform forward stepwise on instead of .

Denote by the set of variables selected in the first steps. We would like to show that

| (A.24) |

for all . Denote by the variable selected in the th step. To this end, note that from the proof of Theorem 1 for the forward stepwise case, we see that for any fixed ,

Note that since , we have , and since , we get

An immediate consequence is the following:

which certifies (A.24) provided the arbitrariness of . Therefore, with probability approaching one, we get

Setting completes the proof. Details are the same as the proof for the case of the lasso and least angle regression.

∎

Proof of Lemma A.9.

Consider the first time along the lasso path that a variable among is just about to enter the lasso model and denote by this variable, where . Specifically, writing for the lasso penalty at this point, we know that

and

if for some . For a proof of this lemma by contradiction, assume that has not yet entered the model at for some satisfying . Under this assumption, our discussion below considers the lasso solution at . First of all, the KKT conditions of the lasso give

Consequently,

| (A.25) |

Thus, the proof of the present lemma would be finished if we show that, with probability tending to one, (A.25) cannot be satisfied.

The rest part of the proof is devoted to disproving (A.25). Note that satisfies

which, together with Lemma A.3, implies that

| (A.26) | ||||

Similarly, from we get

| (A.27) |

The quantities appearing on the left- and right-hand sides obey, respectively,

and

Hence, from (A.27) it follows that

yielding

| (A.28) | ||||

Last, combining (A.26) and (A.28) shows that, with probability tending to one, (A.25) cannot be satisfied, as desired.

∎

Proof of Lemma A.10.

Recall that the definition

Observing that , we get

Hence, the present lemma is equivalent to

| (A.29) |

where denotes the usual inter product of vectors. Since

are vectors of unit norm asymptotically, (A.29) boils down to claiming that the angle between the two vectors are asymptotically zero. Recognizing that and are asymptotically orthogonal since they are independent high-dimensional normal vectors, a vanishing angle between and is equivalent to

The display above is a direct consequence of the condition

which is provided in the assumptions. Hence, (A.29) holds. ∎

Proof of Lemma A.11.

Consider the first time a variable among enters the model. Denote by the rank of this variable. As earlier, call this variable . Note that, by definition, . Suppose on the contrary that by the time is selected, at least one variable among , say , has not been included. Denote by this event, on which we must have

| (A.30) |

From the proof of Theorem 1 for the forward stepwise case, we know that

| (A.31) | ||||

Since , we get

| (A.32) |

and from we get

| (A.33) | ||||

which makes use of the fact that . Similarly, we have

| (A.34) |

Plugging (A.32), (A.33), and (A.34) into (A.31) yields

which contradicts (A.30). This implies the event happens with probability vanishing to zero.

∎

A.3 Theorem 3

Proof of Theorem 3.

Write

for some constant to be determined later. A variable might be dropped by the lasso only if its fitted coefficient crosses zero. By using this fact, it suffices to show that the fitted coefficients of the selected variables shall never cross zero in the first selected variables, except for a rare event with probability no more than .

Let be the first time along the lasso path a previously selected variable is just about to drop out of the model. (The proof shall only focus on the event that such exists; otherwise no variable drops out.) Denote by the number of variables selected just before the first dropout and the set of these variables. For the sake of contradiction, assume that .

Pick an that is (slightly) smaller than and at which variables have been included in the model. Observe the following partial KKT condition for the lasso solution:

| (A.35) |

In a componentwise manner, above returns 1 if the corresponding component is positive and if negative. From (A.35) it follows that

Now let us gradually decrease to , moving along the lasso path. If has the same sign as across all coordinates, then in this process of moving down to , we see all positive coefficients of get larger while all negative coefficients become even smaller. This implies that no coefficient will cross zero, a contradiction to the assumption. Therefore, differs from in the sign of at least one coordinate, yielding

| (A.36) |

On the other hand, we have

| (A.37) | ||||

Let be the restricted isometry constant for -sparse vectors, which is defined as the smallest such that

for all -sparse (we use the notation instead of the conventional since the latter has been reserved for denoting the ratio ). It is not hard to see that this definition yields the following more amenable expression

| (A.38) |

where the maximum is taken over all subsets of with cardinality smaller than and denotes . In the case where (if then this theorem is trivially true), a well known result regarding this constant states

| (A.39) |

with probability at least , where is a universal constant (see, e.g., Theorem 5.2 in Baraniuk et al. (2008); note that is random due to its dependence on ).

Now we prove that on the event (A.39), the assumption cannot hold with a suitable of the constant . To this end, we start by observing that (A.38) together with the assumption ensures that all the eigenvalues of are between and . Thus, from (A.37) we get

Substituting (A.36) into the above display, under the assumption that we see that

| (A.40) |

holds on the event (A.39). If we can show that

| (A.41) |

meaning that (A.40) cannot be satisfied, then the assumption that must be violated and, consequently, the first variables are included along the lasso path without any drop-out with probability at least (note that the event (A.39) happens with probability at least ). Indeed, (A.41) is true if we set (note that we have excluded the trivial case )

This concludes the proof. ∎

A.4 Proposition 4.1

Proof of Proposition 4.1.

Note that the least-squares estimator takes the form:

which is, conditional on , distributed as

for all and

for . Above,

Take the following result as given for the moment:

| (A.42) |

with probability approaching one for an arbitrary constant . Then, we can show that

| (A.43) |

To see this, note that

and

with probability approaching one. Hence, (A.43) follows if one can show that

In fact, from (A.42) we have

which is positive by setting sufficiently small. Above, recall that . Hence, (A.43) holds, meaning that all the true variables are vertically ranked higher than any of the false variables. In particular, the first false variable is vertically ranked lower than all of the true variables.

In the remaining part of the proof, our aim is to prove (A.42). Write the singular value decomposition of as

where and are orthogonal matrices, and is diagonal. Then, the left-hand side of (A.42) can be expressed as

where denotes the th canonical basis vector in Euclidean space. Using this fact, we get

where the last step makes use of the exchangeability of given . Therefore, writing , it suffices to prove that

Recognizing that has independent entries, it is known that is independent of and is uniformly distributed on the unit sphere in . In particular, assumes the following representation

where are independent random variables. Using this representation, we get

| (A.44) | ||||

Setting , Assumption 1 ensures that the following inequality must eventually hold:

Plugging the display above into (A.44) gives

Next, denote by

and write for the indicator function of defined as

Then, it is easy to see that

where the last step follows from a Gaussian concentration inequality (see, for example, Hsu et al. (2012)). As a result, it suffices to show that

To this end, first note that from

we get

| (A.45) |

where we use the fact that the smallest singular value of the Wishart matrix is concentrated at with probability tending to one (see, for example, Vershynin (2012)). Second, it is known that

which implies

| (A.46) |

Taking (A.45) and (A.46) together, we get

| (A.47) |

Recognizing that , we get . In addition, . Hence, from (A.47) we have

in probability. In addition, note that

is upper bounded by , which is an integrable function. Hence, by the dominated convergence theorem, we get

as desired. ∎